Embed Size (px)

Citation preview

Finance

Chapter 13Capital structure & leverage

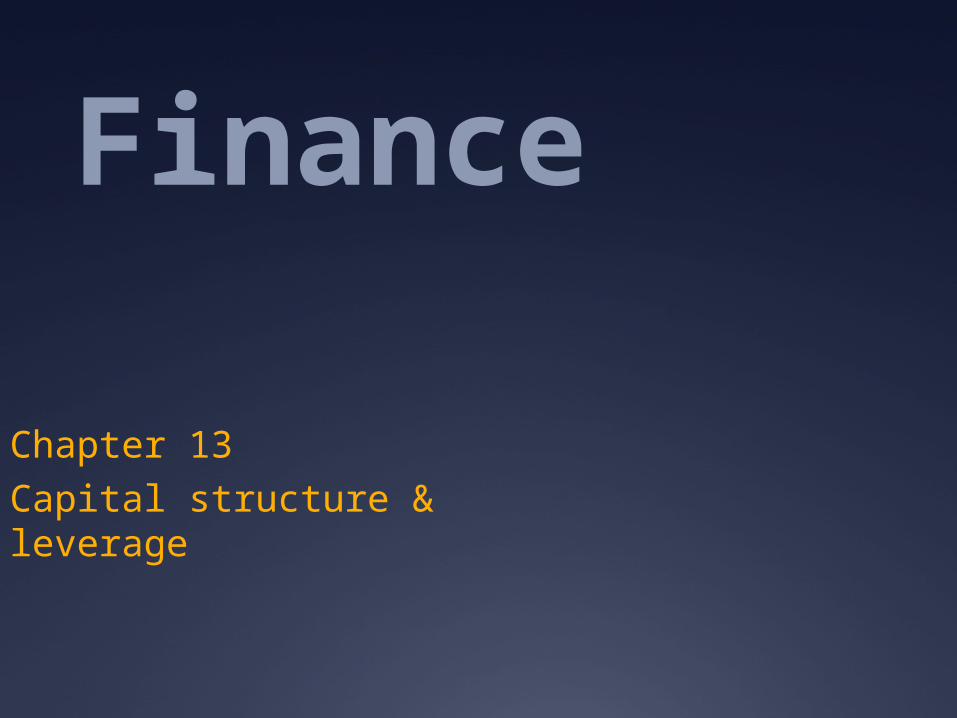

Financing assets

What is the best way for a firm to finance its asset?

What is the effect of financial leverage on stock prices, earnings per share, & the cost of capital

Leverage = the use of borrowed money to increase production volume, and thus sales and earnings. It is measured as the ratio of total debt to total assets; greater the amount of debt, greater the financial leverage. BusinessDictionary.com

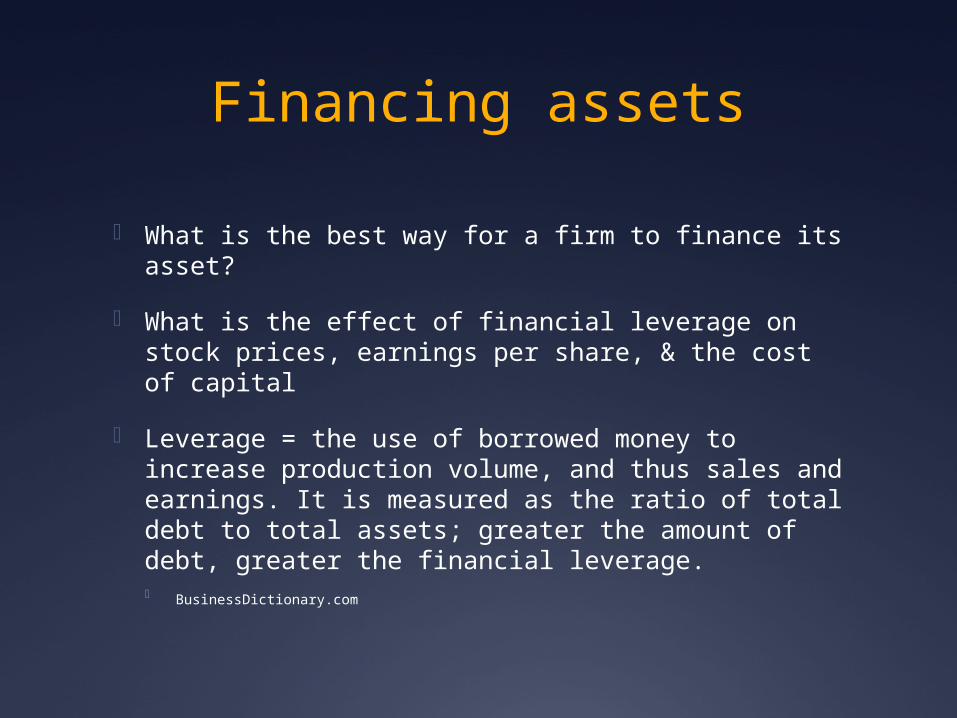

Target capital structure

Target capital structure = the mix of debt, preferred stock, and common equity the firm plans to use to raise capital If debt level is below target, expansion capital

should be raised using debt If debt level is above target, expansion capital

should be raised using equity

Capital structure Influences

Business risk

Tax position

Need for financial flexibility

Managerial conservatism or aggressiveness

Business risk

Business risk = the risk inherent in the firm’s operations if it uses no debt. The lower a firm’s business risk, the higher its optimal debt ratio. A firm has little risk if:

The demand for its products is stable (Demand variability)

Firms selling products in stable markets—no significant changes in prices (Sales price variability)

The prices for inputs and products remain relatively constant It can adjust its costs freely if costs increase

A high percentage of its costs are variable and will therefore decrease as sales decrease (operating leverage A firm with high fixed costs is more exposed if sales decline

Business risk

In high tech industries (drugs, computers) if they are able to produce new products in a timely and cost-efficient manner

The firm’s dependence on foreign sales is minimized reducing exposure to currency rate fluctuations and political instability

Operating leverage

Operating leverage = the extent to which fixed costs are used in a form’s operations. A high degree of operating leverage, ceteris paribus, implies that a relatively small change in sales results in a large change in ROE. (pg. 483, figure 13.3)

Operating break even is the output quantity at which EBIT=0 (ROE = 0)

Financial risk

Financial risk is the additional risk placed on stockholders as a result of the decision to finance with debt

Financial risk = an increase in stockholders’ risk, above and beyond the firm’s basic business risk, resulting from the use of financial leverage

Financial leverage = the extent to which fixed income securities (debt & preferred stock) are used in a firm’s capital structure

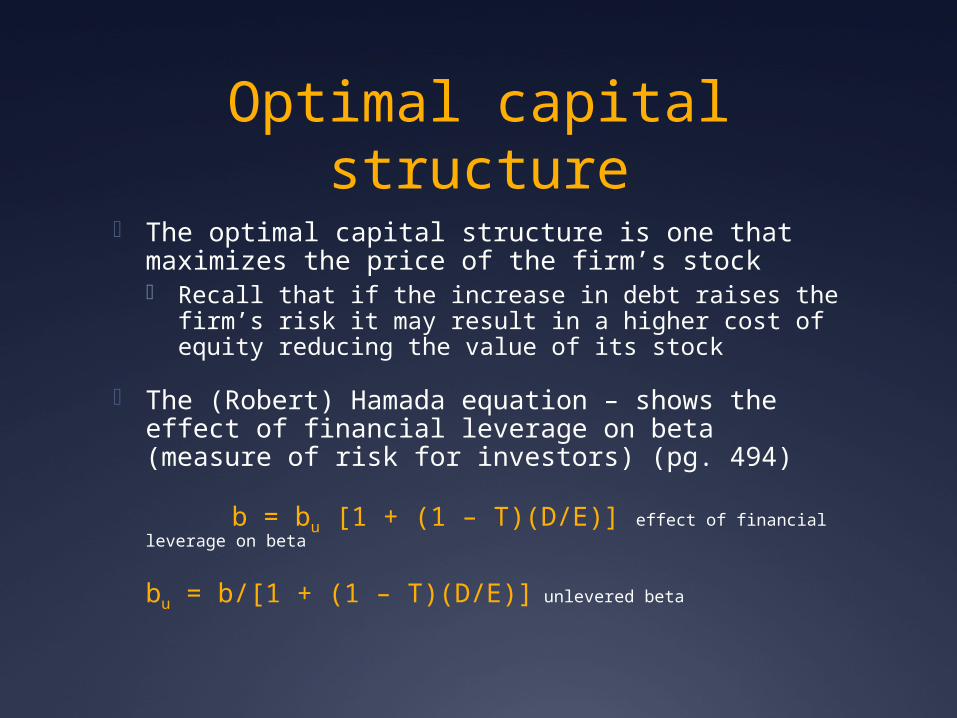

Optimal capital structure

The optimal capital structure is one that maximizes the price of the firm’s stock Recall that if the increase in debt raises the

firm’s risk it may result in a higher cost of equity reducing the value of its stock

The (Robert) Hamada equation – shows the effect of financial leverage on beta (measure of risk for investors) (pg. 494)

b = bu [1 + (1 – T)(D/E)] effect of financial leverage on beta

bu = b/[1 + (1 – T)(D/E)] unlevered beta

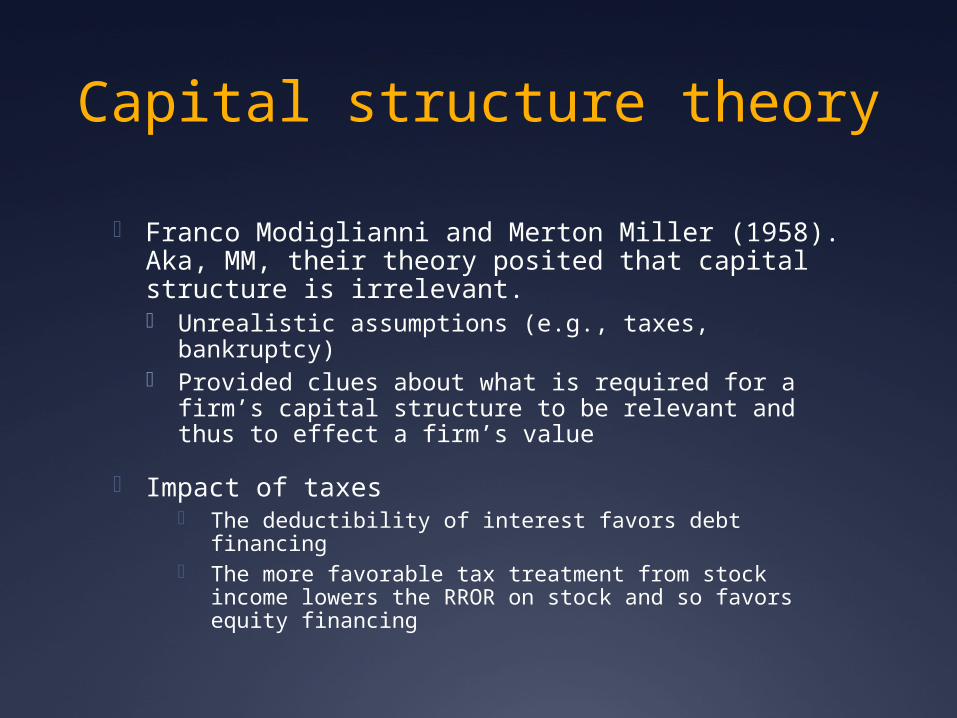

Capital structure theory

Franco Modiglianni and Merton Miller (1958). Aka, MM, their theory posited that capital structure is irrelevant. Unrealistic assumptions (e.g., taxes, bankruptcy) Provided clues about what is required for a firm’s

capital structure to be relevant and thus to effect a firm’s value

Impact of taxes The deductibility of interest favors debt financing The more favorable tax treatment from stock

income lowers the RROR on stock and so favors equity financing

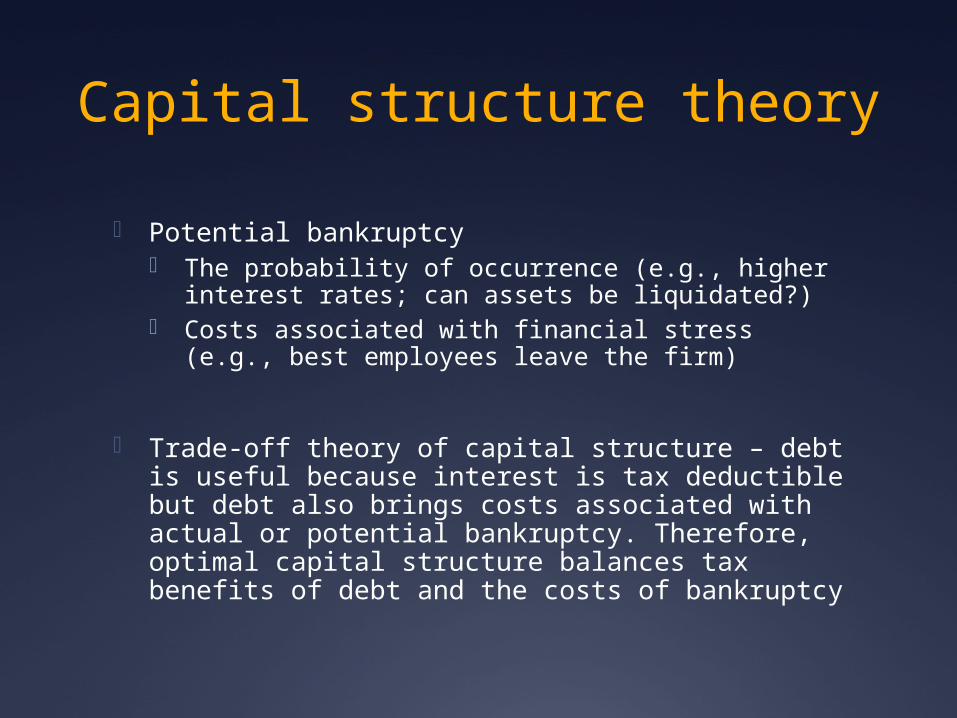

Capital structure theory

Potential bankruptcy The probability of occurrence (e.g., higher interest

rates; can assets be liquidated?) Costs associated with financial stress (e.g., best

employees leave the firm)

Trade-off theory of capital structure – debt is useful because interest is tax deductible but debt also brings costs associated with actual or potential bankruptcy. Therefore, optimal capital structure balances tax benefits of debt and the costs of bankruptcy

Signals

An alternative theory of capital structures relates to the signals given to investors by a firm’s decision to use debt vs. stock to raise new capital based on:

Symmetric information – managers and investors have similar access to information about the firm’s prospects

Asymmetric information – managers have better information about the firm’s prospects (pg. 506)

Stock = negative signal

Debt = neutral – positive signal

Reserve borrowing capacity – managers use less debt in normal times to avoid issuing stock in volatile times

Debt and management constraint

Owners may desire a high amount of debt to constrain managers since this raises the threat of bankruptcy. This results in managers being more careful with shareholders’ money. Many corporate take-overs and LBO’s were

aimed at improving efficiency by reducing the free cash flow available to managers

Capital structure practice

In practice, financial executives generally treat the optimal capital structure as a range (e.g., 40-50%) rather than a precise number

Capital structure checklist

Sales stability

Asset structure

Operating leverage

Growth rate

Profitability

Taxes

control

Management attitudes

Lender & rating agency attitudes

Market conditions

Firm’s internal conditions

Financial flexibility

Capital structure goal

Maintain financial flexibility

Maintain adequate reserve borrowing capacity