Embed Size (px)

Citation preview

Finance & Investment ClubTechnology Sector

Fall 2012

Circuit Boards & EMS

2

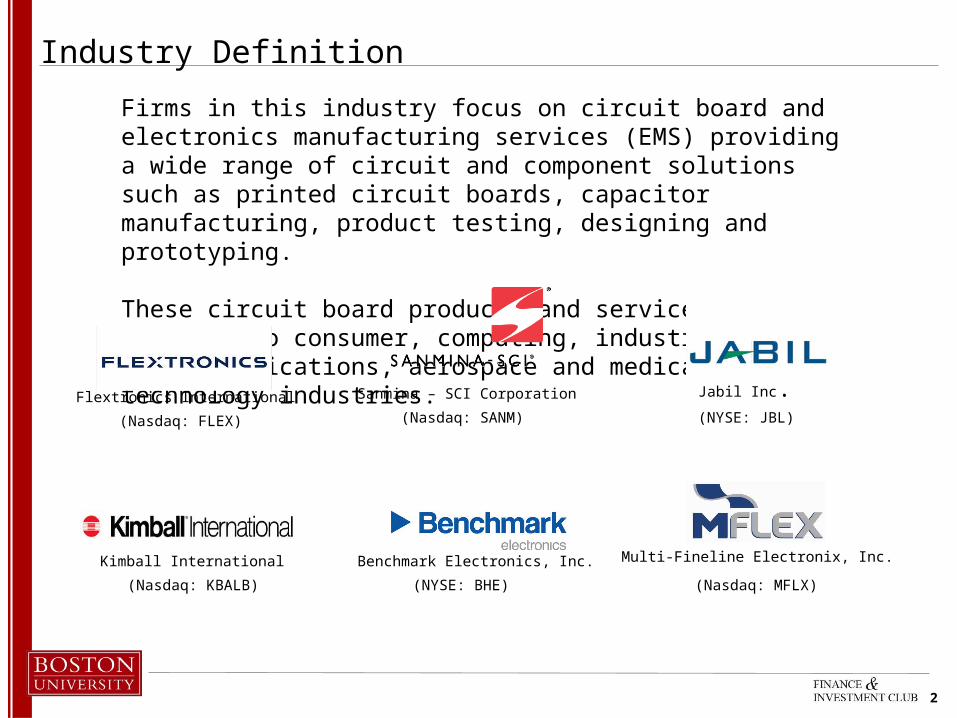

Industry Definition

Firms in this industry focus on circuit board and electronics manufacturing services (EMS) providing a wide range of circuit and component solutions such as printed circuit boards, capacitor manufacturing, product testing, designing and prototyping.

These circuit board products and services are tailored to consumer, computing, industrials, telecommunications, aerospace and medical technology industries.

(Nasdaq: FLEX)

Flextronics International Sanmina – SCI Corporation

(Nasdaq: SANM) (NYSE: JBL)

(Nasdaq: KBALB) (NYSE: BHE) (Nasdaq: MFLX)

Jabil Inc.

Kimball International Benchmark Electronics, Inc. Multi-Fineline Electronix, Inc.

3

Revenue Generation and Product Life Cycle

Sources: Company 10K information, company investor presentations

GLOBAL SUPPLY CHAIN MANAGEMENT

OEM

Product Development

Production Volumemanufacturing

Final systemassembly

OEM END MARKETS

Personal Computing

Aerospace and Defense

Medical

THE CUSTOMER

WHERE THE CIRCUIT BOARDS ARE GOING

HOW THE PRODUCT IS DESIGNED

VER

TIC

ALL

Y IN

TEG

RAT

ED M

AU

FAC

TUR

ING Printed Circuit Boards

Cable assemblies

Optical modules

Enclosure design

•OEM = Original Equipment Manufacturer,Ex: Apple, Inc.

•PCB manufacturers follow a horizontal supplychain structure based on contracts won from OEMsto physically build the circuit boards and electroniccomponent hardware for the OEM product

•PCB manufacturers build out products that OEMsuse in a variety of end markets as shown on theright-hand diagram

HOW THE PRODUCT IS BUILT

Consumer

Telecom

Industrials

4

FLEX

JBL

SANM

BHE

KBALB

MFLX

Industry Summary

51%

12%

29%

2%4% 1%

Market Share by 2011(ttm) Revenue

Total 2011 Sector Revenue – 45,113.6M IBISWorld Industry Data

Technology 75941.4B 100%

Computer Based Systems 10149.5B 13%

Integrated Circuits 161.0B 0.21%

Circuit Boards and EMS 17.4B 0.03%

Industry Breakdown by Market Cap ($B)

5

Industry Information

Revenue ($m) 47,038

Establishments 3,490

Exports ($m) 15,780

Domestic Demand ($m) 68,101

Revenue ($m) 44,055

Establishments 3,124

Exports ($m) 16,321

Domestic Demand ($m) 69,328

Key Metrics – 2007-2011 averages 2012-2016 forecasted averages

Product Segmentationby Revenue

Source: IBISWorld industry data

Printed Circuits

Other electronic com-ponents

Bare printed circuit boards

Electronic connectors

48%

31%

11%

10%Type Profit

Margin %*

PrintedCircuit

70%

Other Components 5%

BarePrinted

20%

Connectors 5%

*estimates based on FLEX sales

6

Presentation Overview

Circuit Boards & Electronics Manufacturing Service Sub-Sector

TREND 2TREND 1 TREND 3 TREND 4

Decreasing prices of electronic components

Demand in Aerospace

Increased electronic demand and usage in China

Key Industry Drivers/Trends

PRINTED CIRCUIT BOARD & EMS INDUSTRY RATING:

NEUTRAL

Percentage of Households with at least 1 computer

7

Trend 1 – Growth in the Personal Computing Market

Percentage of Households with at least 1 computer

Decreasing prices of electronic components

Demand in Aerospace

Increased electronic demand and usage in China

8

Increasing Household Personal Computer Ownership

0

10

20

30

40

50

60

70

80

90

100

71.373.9 75.677.333096480927979.105923430271280.919391651402982.774432827458584.67286.613068058638988.5986342419038

Year

Perc

enta

ge O

wne

rshi

p

• U.S household computer ownership is growing at a CAGR of 2.20%

Percentage of Total Households with at least one computer

2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

Sources: U.S Bureau of Labor Statistics, Leichtman Research Group Broadband Access and Services survey 2012

• Rising consumer ownership positively affects PCB demand which boosts industryrevenues

Use a Computer at Home

Internet at Home Broadband at Home

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Under $30,000$30,000-$50,000Over $50,000

Perc

enta

ge o

f Usa

ge

Broadband and Computer Service Usage in Households, 2012

• 97% of U.S households making over$50,000/year use at least one computer

• 84% for households making between $30,000 and $50,000 – market expansion leading to increased opportunity for PCB usage

• Increasing PC ownership represents a stable avenue for firms in the industry to service this growing demand

9

Innovation in the Personal Computer Market

• By 2016 tablets and like devicesare poised to assume 54.9% of allportable PC devices

• Growth of tablet computermarket

• 2011 total U.S tablet market: 28.1 million units

• 2016 forecasted U.S tablet market: 45.3 million units

• Apple, Inc is poised to be tablet market leader, a directOEM customer of firms in the PCB industry

Sources: iGR-Inc Market Research; Forrester Market Research; International Data Corporation, June 2012 Press Release

0

10

20

30

40

50

60

70

80

90

10.326

50.7

67.776.1 82.1

U.S Tablet Users

Year

U.S

Tab

let U

sers

(in

mill

ions

)

2010 2011 2012 2013e 2014e 2015e

Number of Tablet PC users in the U.S

CAGR: 37.2%

• 37% growth rate of U.S tablet user marketpresents a large growth avenue for PCB manufacturers

0

100

200

300

400

500

600

98.9 100.8 104.3 107.6 110.1 112.4

110.1 123.6 140.7 162.6 187 213.756.1 5757.2

5655.6

53.899.4 101.1

111.4124.7

138148.7

Portable PCs in Mature Markets

Desktops in Mature Markets

Portable PCs in Emerging Markets

Desktop PCs in Emerging Markets

Year

Tota

l Shi

pmen

ts (i

n m

illio

ns)

2011 2012e 2013e 2014e 2015e 2016e

PC Shipments by Market and Product Type

• Large prospects for portable PC (including tablets) growth in both mature markets (U.S, Western Europe)and emerging markets (Asia, South America)

-Portable PC Mature Market CAGR (‘11-’16): 6.2%-Portable PC Emerging Market CAGR (‘11-’16): 10.5%

• Innovations in the PC market representlarger growth and act to stabilize sinkingtraditional desktop sales

10

Trend 2 – Decreasing Prices of Electronic Components

Decreasing prices of electronic components

Demand in Aerospace

Increased electronic demand and usage in China

Percentage of Households with at least 1 computer

11

Decreasing Input Prices for PCB Components

0

10

20

30

40

50

60

70

80

Year

Pric

e in

$

2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

• Inputs for PCBs are decreasing at aCAGR of 3.23%

• Creation of more powerful componentchips with less expensive silicon

• Application of Moore’s law: on average, transistor count on circuit board doubles every two years. Better transistors influences better PCBs at lower costs to the firms in the industry

Prices for PCB Components

Demonstration of Moore’s Law in Intel Corp. chips

1,000

10,000

100,000

1,000,000

10,000,000

100,000,000

1,000,000,000

Transistors

Num

ber o

f Tra

nsis

tors

54x

3000x

1971 1982 1997 2005

• Recently IBM has developed chiptwo times faster than existing technologiesproving that Moore’s Law is not at an end

Sources: IBISWorld Industry Data; Intel Corporation press releases; CBS Zdnet Industry Research

- 3.23%

2x

236800x

• Consistency in PCB firm COGS marginsinput prices are not causing any rise

• Continuation of Moore’s law indirectlycontinues the decrease of PCB inputprices.

• Better inputs, cheaper prices. Cost margins stabilize. PCB firms benefit.

12

Trend 3 – Demand In Governmental Aerospace and Defense

Decreasing prices of electronic components

Demand in Aerospace

Increased electronic demand and usage in China

Percentage of Households with at least 1 computer

13

Demand in Domestic Aerospace and Defense

0

20

40

60

80

100

120

140

Total Aircraft

Missles

Space

Related Products

Year

Aer

ospa

ce S

ales

in B

illio

ns o

f Dol

lars

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012e

U.S Aerospace Sales in Current Dollars• U.S aerospace and defense saleshave consistently risen since the start ofthe 21st century

CAGRs (2001-2011):

• Total Aircraft Sales: 2.72%

• Missles Sales: 8.53%

• Space Defense Sales: 4.20%

• Related Products Sales: 1.56%

Sources: Aerospace Industries Association (AIA) data in cooperation with NASA, U.S Departments of Commerce and Defense

Forecasted Sales ($B)2012e 2013e 2014e 2015e

Total Aircraft Sales

Missile Sales

Space Defense Sales

Related Products Sales

116.75 119.61 122.54 125.54

25.12 27.05 29.13 31.36

45.14 46.84 48.61 50.45

30.63 31.06 31.50 31.94

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

ShipmentsOrders

Year

Ship

men

ts in

Mill

ions

of D

olla

rs

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S Aerospace Shipments vs. Orders

• Firms in this industry can expect consistentrevenue growth through a 3.36% YoY CAGRfor total aerospace and defense industry sales.

14

Increased Demand in Foreign Aerospace Markets

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

U.S. Foreign Military Sales Agreements and Direct Commercial Sales Authorizations• U.S foreign military sales agreements

has increased by a steady CAGR of 6.72%

0

50

100

150

200

250

300

47 55 52 53 62 67 52 6789 107 123

154168.408351287479184.164758333552201.395346209159220.238040338022

11 11 12 12 13 139

1818

2930

2425.4509394997266

26.98959672578128.6212747245779

30.3515971425119

Foreign Military Sales Agreements

Direct Commercial Sales Authorizations

2011 2012e 2013e 2014e

CAGR 6.72

%• Factors driving future industry revenues :• Saudi Arabian purchases of F-15sand other upgrades worth $30 Billion

• Japan selects F-35 for nextGen fighter, deal worth $8 Billion

• UAE buys THAAD missiles worth $3.5 Billion

Sources: PWC Aerospace and Defense Review 2011-2012, Deloitte 2012 A&D Industry Review and Outlook

• The aerospace and defense industry contributes2.23% to U.S GDP and 7.0% of total exports, in whicha growing Chinese military imports 14.9% of U.S exports,the largest share.

China UK

France

Russia

Japan

Saudi A

rabia

German

yInd

ia Italy

Brazil

South

Korea

Austral

ia

Canad

aIsr

ael

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000119400

59598 5866845245 41284

3353823972

14036

Expenditures

• Increasing fighter aircraft and space projects willfurther increase aerospace revenue and demand growth in China

• Demand growth in both domestic and foreignmarkets is steady and will directly lead to greater PCB industry future revenues.

Global Military Expenditures by Country in 2010 ($M)

15

Trend 4 – Electronic Demand in China

Decreasing prices of electronic components

Demand in Aerospace

Increased electronic demand and usage in China

Percentage of Households with at least 1 computer

16

Increasing Electronics Demand and Usage in China

• PCB firms have increased their net sales in China by 5.41% from 2009 to 2011

• PCB firms are investing in expansive operational facilities in China

-Flextronics (FLEX) owns 41% of itsnet PPE in China in 2012. The next largestshare is Mexico at 15%

-Asia/Pacific region PC shipments climbed2% to 30.3 million units in Q1 2012 fromQ1 2011

Source: Gartner Market Research; Bloomberg Businessweek; International Data Corporation, June 2012 Press Release

FLEX SANM BHE MFLX0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

32%22%

35%

68%

33% 29% 36% 87%

38%

27%

38%

94%

200920102011

Year

Sale

s as

% o

f tot

al re

venu

es

Net Sales by Region as a Percentage of Total Revenues

• China’s electronics market is set for 70%expansion to 2.14 trillion yuan (343 billion USD)By 2015

Portable Electronics Growth in Emerging Asian Markets

0

50

100

150

200

250

Portable PCDesktop PC

2011 2012e 2013e 2014e 2015e 2016e

• China GDP expected to grow 7.9% in 2013

• Growth prospects in China for consumerelectronics can be volatile but present agrowing trend for PCB firms who are Increasing foreign manufacturing presence.

17

Industry under Porter’s Five Forces Model

SUPPLIERS

INDUSTRY RIVALRY CUSTOMERS

NEW ENTRANTS

SUBSTITUTES

Entry Barriers

Exit Barriers

Forward Integration Backward Integration

LOW

HIGH

• Largest 4 companies represent 20% of market revenue

• Smaller companies rely on contract manufacturing

• Large amount of competition between smaller companies

• Increased manufacturing capabilities and foreign operations

• Intellectual capital barriers• Economies of scale

• Close relationships with direct OEM customers

MEDIUM

MEDIUM

LOW

• PCB industry under constant pressure to innovate new products

• Alternative designs and fluid uses are being rapidly introduced

18

Industry Risks and Sensitivities

Risk of New Breakthrough Technologies– Companies involved in printed circuit board and EMS manufacturing are constantly at risk of having their

core products rendered obsolete by newer, smaller, thinner, faster circuit components.– The company that can innovate the fastest can gain patent protection and a distinct technological

advantage over other firms in the industry.

Risk of Input Shortages– Natural disasters in Asian countries can drastically limit electronic and circuit component supply, thus

dramatically increasing input prices.

Risk of Foreign Currency Exchange Rate Fluctuation– Because industry operations happen in many foreign markets, currency exchange rates directly affect

industry costs. An increasing Trade Weighted Index also poses a currency valuation threat to the industry.

Risk of Large Scale Product Defection– PCB defections can cause the loss of customer bases including original equipment manufacturers and

create reputational issues that are extremely difficult to recover from.

There are four main risks affecting firms in the Printed Circuit Board Industry:

19

Key Financials

Company Market Cap (B)

% of 52 week high

Closing Price

P/E Ratio (ttm) EPS (ttm) EV/

EBITDA Debt/Equity Debt/EBITDA LTM ROE LTM ROA

FLEX 3.71 25.23% 5.60 7.63 0.73 4.20x 85.44 2.02x 23.05% 3.05%

SANM 0.693 32.35% 8.49 3.93 2.16 4.37x 93.11 3.32x 20.79% 3.26%

JBL 3.53 37.34% 17.17 9.18 1.87 4.05x 79.55 1.77x 19.85% 5.23%

KBALB 0.464 7.85% 12.21 27.88 0.44 6.95x 0.07 .005x 19.85% 2.93%

BHE 0.837 19.93% 15.11 20.96 0.72 6.26x 0.97 .126x 3.81% 2.96%

MFLX 0.404 42.73% 17.01 13.94 1.22 4.09x N/A* N/A* 6.87% 2.91%

High 3.71 42.73% 17.17 27.88 2.16 6.95x 93.11 3.32x 23.05% 5.23%

Low 0.404 7.85% 5.60 3.93 0.44 4.05x 0.07 .005x 3.81% 2.91%

Median 0.765 28.79% 13.66 11.56 0.975 4.29x 79.55 1.77x 19.85% 3.01%

Mean 1.61 27.57% 12.60 13.92 1.19 4.99x 51.83 1.45x 15.70% 3.39%

*Multi-Fineline Electronix (MFLX) has no outstanding debt and was left out of debt averaging as a result

20

Industry Conclusion

PRINTED CIRCUIT BOARD & EMS INDUSTRY RATING:

NEUTRAL

1. Industry Recap• International electronic usage and demand will continue to benefit and increase industry growth• Aerospace expenditures in major nations requires increasing circuit technology and addedmanufacturing jobs for firms in the industry• Chinese electronic growth is boosting revenues for firms with operational capabilities in China

3. Continued Risk Factors• PCB Industry faces high revenue volatility through stagnating technological innovation and input shortages

Decreasing revenue growth but continued international relevance give the industry a neutral rating

2. Industry Outlook• Volatile revenue growth that is currently in decline but is forecasted to improve

• Industry life cycle that is falling out of maturity

• Major macroeconomic risks such as international trade imbalances and foreign currency risks threaten industry growth

21

Backup Slides

22

Backup Slide 1 - PCB Supply Chain

Printed Circuit Board& EMS Industry

Key Drivers

Percentage of households with at leastone computer or tablet

Trade weighted index comparisons

Demand in Aerospace

Demand in foreign markets

Supply Industries Demand Industries

Glass Product Manufacturing

Laminated Plastics Manufacturing

Wire & cable manufacturing

Computer Manufacturing

Semiconductor and Electronic Parts

Related Industries

Semiconductor and Circuit Manufacturing

Solar Panel Manufacturing

Source: IBISWorld Industry Research

23

Backup Slide 2 – U.S vs. China Historical GDP (in USD, not inflation adjusted)

Source: Google Public Data

24

Backup Slide 3 – Technically Speaking, What is a PCB? PCB’s are used to support and connect electronic components using conductive pathways or signal tracks

etched from copper sheets laminated onto non-conductive substrate Because of advancing manufacturing technologies, PCBs are now one of the easiest commercially-made

electronic devices Inputs: Laminates, copper-clad laminates, resign impregnated B-stage cloth, copper foils Methods: -Silk Screen printing: uses etch-resistant ink to remove unwanted copper during the manufacturing process.

Mostly used to make hybrid circuits -Photoengraving: uses computer software to remove the photoresist coating on the PCB and removing the

unwanted copper in the process -PCB milling: uses a milling process to remove the copper

Source: Wikipedia

25

Backup Slide 4 – Further PC and Desktop Sales Data

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Sales at current prices DesktopsSales at current prices Laptops

• Desktop sales CAGR: -3.70%

• Laptop sales CAGR: 3.43%

2007 2008 2009 2010 2011 2012 2013e 2014e 2015e 2016e 2017e

Year

Sale

s (in

mill

ions

of d

olla

rs)

Source: Mintel Market Research based on CEA & BEA data