Embed Size (px)

Citation preview

(h^^

FINANCIAL ACCOUNTING FOR PETROLEUM RETAINED PRODUCTION

PAYMENTS BY THE WORKING-INTEREST PURCHASER

by

JERRY LANE PITTMAN, B.B.A.

A THESIS

IN

ACCOUNTING

Submitted to the Graduate Faculty of Texas Technological College

in Partial Fulfillment of the Requirements for

the Degree of

MASTER OF SCIENCE IN ACCOUNTING

Approved

August, 1969

ire

- n !r

Cr

ACKNOWLEDGMENTS

I am deeply indebted to my friend cind

professor. Dr. Kenneth L. FoX/ who directed

this thesis. Without his continued support

and guidance, completion of this thesis would

have been impossible.

ii

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

LIST OF TABLES V

LIST OP FIGURES vi

I. THE NATURE OF PRODUCTION PAYI-IENTS—

AN INTRODUCTORY DISCUSSION 1

II. FEDERAL INCOME TAX INFLUENCES 8

Introduction 8

Illustrative Case Study 9

A* s Tax Consequences 11

B's Tax Consequences 15

C*s Tax Consequences 18

Influence of Proposed Legislation . . . 21

Suinmary 22

III. FINANCIAL REPORTING UNDER THE

EQUITABLE-LIEN METHOD 25

Introduction 25

Oilola Case Study 26

Annual Report Excerpts 36

Surtunary' 38

IV. FINANCIAL REPORTING UNDER THE NET

AND ECONOMIC-INTEREST METHODS 40

Introduction 40

Oilola Case Study 42

Annual Report Excerpts 55

Summary 58 iii

iv

V. COMPARISON AND CRITIQUE OF THE THREE DIVERSE METHODS 60

Introduction 60

General Critiques and Comparison . . . . 61

Specific Critique and

Recommendation 68

Sumnary 73

VI. SUMMARY - . 75

BIBLIOGRAPHY 79

LIST OF TABLES

Table Page

1. Oilola Production Payment

Application 12

2. Computation of A's Taxable Income 14

3. Computation of B's Taxable Income 18

4. Computation of C's Taxable Income 20

5. Purchaser B's Income Statement Under the Equitable-Lien Method 30

6. Excerpts of Purchaser B's Balance Sheet Under the Equitable-Lien Method 33

7. Purchaser B's Income Statement Under the Net Method 47

8. purchaser B's Income Statement Under the Economic-Interest Method 48

9. Excerpts of Purchaser B's Balance Sheet Under Net and Economic-Interest Methods 52

10. Per Share Analysis of Earnings and Book Values for the Oilola Case 62

LIST OP FIGURES

Figure Page

1. Earnings Per Share for the Three Methods 64

vi

CHAPTER I

THE NATURE OF PRODUCTION PAYMENTS—

AN INTRODUCTORY DISCUSSION

In the past fifty years increasing importance has

been placed on the financing arrangement utilized by the

oil and gas industry called the production payment. This

production payment is a means to borrow money or to trade

oil and gas properties with minimal initial cash outlay

by the purchaser yet sufficient consideration to effect

the transfer of property. As described by Breeding and

Burton in their Income Taxation of Oil and Gas Production,

a production payment, more commonly known as an oil pay

ment or gas payment, is an interest in oil and gas in the

ground that entitles its owner to a specified fraction of

production for a limited time or until a specified sum of

money or a specified number of units of oil and gas has

been produced and received.

There are two types of production payments currently

used by the oil and gas industry—the carved-out and the

retained production payment. The carved-out production

payment is used at the time the holder of a working interest

Clark W. Breeding and A. Gordon Burton, Income Taxation of Oil and Gas Production (Englewood Cliffs, New Jersey: Prentice-Hall, Inc., 1961), p. 205.

2

may sell or "carve-out" an overriding royalty of a short

duration (more commonly called a production payment) to

be paid back as production ensues. Once payout status

has been reached, the working interest that was carved out

reverts to the original holder.

The retained production payment, on the other hand,

is used to effect a transfer or sale of property permanently

to the purchaser. The owner of the working interest of a

producing property sells his interest in the property for

a relatively small initial cash payment plus a designated

amount payable, retained out of future oil and gas pro

duction, if and when, produced from the property.

The carved-out production payment is simply a loan

with a temporary pledge of oil or gas reserves attached

as security. While the carved-out payment has not been

subjected to the controversy that the retained payment has,

the retained production payment has been given the most

diverse treatment for accounting purposes and is, by far,

the most popular type of production payment. For such

reason this thesis deals solely with the retained pro

duction payment and its ramifications on accounting treat

ment and thought. To further limit this thesis the author

restricts his discussions to producing properties only and

to the accounting treatment as recorded by the purchaser

of the working interest.

Before getting to the essence of the current

accounting controversy, it is necessary to identify the

parties in the retained production payment and to intro

duce their functions applicable thereto. In the retained

production payment transactions, B, an oil and gas operator,

desires to buy a certain hydrocarbon lease or leases owned

by A. B will only advance a nominal portion of the sales

price for the initial cash consideration, and A will assign

the working interest in the property to B, subject to a

sizable retained production payment expressed in terms of

a fixed principal plus interest on the remaining balance

of the purchase price. The production payment will be paid

out of a certain percentage of first production until the

principal plus interest thereon has been licjuidated.

Arthur Andersen & Co. stated this procedure quite well.

The retained production payment is payable only out of the proceeds from the sale of a specified portion of the minerals, if, as/ and when produced; and B bears the cost of lifting all of the oil and gas produced/ including that applied to liquidation of the retained production payment.2

At the same time/ A sells the production payment to C/ an

investor/ banker/ or separate corporation/ for payment of

the production payment/ generally on a discounted basis

2 Arthur Andersen & Co., Accounting and Reporting

Problems of the Accounting Profession (Chicago, 111.: Arthur Andersen & Co., 1962), p. 113.

4

plus interest. The parties. A, B, and C, constitute what

is commonly known as the ABC arrangement by Federal income

tax authorities.

party B is not directly nor indirectly liable for

payment of the production payment since he has not acquired

and will not acquire the portion of the property retained

for the payment out of oil; he is, therefore, not liable

for the amounts of the lien on the total properties. B is

only liable, effectively, to operate the property. Any

liability attaches between Parties A and C since A has

borrowed the principal from C with a guaranty that it will

be repaid by A, only if the leases prove to be worthless

before liquidation of the payment occurs.

The existing problem in accounting, for the retained

production payment, is that it provides the working interest

(purchaser B) a fraction of production during the payout

period and a significantly larger fraction of production

after payout status is reached. This situation results in

an extreme variation in operating results for B between the

payout period and the period after payout. The cash income

to the working interest, B, may be so small during payout

that out-of-pocket production expenses are not covered,

purchaser B possibly will make an accounting in his financial

3 A. W. Walker, JT., "Oil Payments," Texas Law Review,

XX (January, 1942), 268-270.

statements for only his net investment (the initial small

cash outlay) in the property and the applicable propor

tional income; or he may present in his statements the

total value of the entire invested property subject to a

liability against the property which he did not assume and

the total gross income produced from the leases. Thus, a

problem has evolved due to the lack of uniformity and

comparability among companies in reference to appropriate

accounting treatment of the retained production payment.

Stanley Porter, partner with Arthur Young & Co./ commented

that.

The evolution of accounting thought on this problem, from both the financial and tax accounting viewpoints, constitutes one of the most fascinating stories in the history of accounting. Nor has this story ended, for the problem remains challenging and unresolved, today. 4

Three different methods have been used by the

petroleum industry accounting for the retained production

payment by the purchaser of a working interest—the

ecjuitable-lien method, the net method, and the economic-

interest method. Chapter III discusses the equitable-lien

method, while Chapter IV discusses the net and economic-

interest methods.

^Stanley P. Porter, Petroleum Accounting Practices (New York, N.Y.: McGraw-Hill Book Comtpany/ 1965)/ p. 189,

In Chapter II an examination is made of oil and

gas Federal income tax law and cases involving the purchaser

of a working interest. A major emphasis in Chapter II is

to present how Federal income tax laws influence the

accounting treatment of the retained production payment.

A discussion of the retained production payment without

defining or setting forth these tax laws would constitute

a wholly inadequate discourse. Chapter II also makes an

investigation into the future outlook of the ABC transaction

in relation to the Internal Revenue Service and possible

future Congressional legislation.

Chapter III describes the equitable-lien theory of

accounting for the purchaser's working interest. The

equitable-lien method presents the arrangement as though

the purchaser B had acquired the entire interest that was

owned by the seller A, with the production payment consti

tuting a liability in the nature of an equitable lien to

be satisfied only from the proceeds of the sale of oil or

gas if, and when, produced.

Chapter IV presents the net and the economic-

interest methods. The two methods are closely related to

each other since they are derivaties of income tax law.

Under the net method no liability is recognized; only the

initial cash consideration for the residual interest

acquired is capitalized; depletion is based on such cash

contribution; and the purchaser excludes from his income

that portion of the oil or gas sales proceeds applied to

reduce the production payment which the purchaser did not

assume. The purchaser, under the net method, includes in

his own expenses the total lifting costs for producing the

oil or gas. The economic-interest theory, also presented

in Chapter T7, requires that the proceeds from production

of the retained production payment be excluded from the

purchaser's gross income. The estimated total lifting

costs applicable to the production payment are capitalized

€Uid amortized over the production attributable to the

purchaser's interest.

Chapter V consolidates all three of these accounting

methods for comparative purposes. The diversity and lack

of comparability among the three methods under identical

assumptions are clearly displayed in this chapter. Each

method is critiqued for fair reporting and accounting

requirements, and a recommendation is made to solve this

accounting dilemma.

In the last chapter. Chapter VI, a summary of all

chapters of this thesis is made.

CHAPTER II

FEDERAL INCOME TAX INFLUENCES

Introduction

Tax authorities have termed the retained production

payment, more popularly known as the ABC transaction, as a

child of our tax law which allows the purchaser of an oil

property, subject to a retained oil payment, to exclude

from his income the revenue used to satisfy the oil payment

plus applicable interest. This "child" is partially the

reason for the widespread diversity in uniformity and

comparability as pointed out previously in Chapter I,

This chapter discusses these tax laws and their

influences on accounting treatment. Tax and Supreme Court

cases are surveyed, and an illustrative case applied to

the ABC arrangement is introduced to present the tax con

sequences of the parties involved. Furthermore, proposed

legislation in Congress which will materially affect the

production payment is investigated together with its

possible influence on accounting thought.

A. G. Schlossstein, Jr., "Financial Accounting for Oil payment Transactions," The Texas Certified Public Accountant, XXXI, No, 6 (1959), 13,

8

Illustrative Case Study

Party A wishes to sell his Oilola lease properties

for $16,000,000. Under conventional selling arrangements

Party B would purchase the Oilola leases by either paying

total cash or by borrowing the sum of $16,000,000. B,

thereby, would differentiate the initial cash outlay between

lease and well equipment of $2,500,000 (the fair market

value) and leasehold cost of $13,500,000 (the balance).

For tax purposes B could only recover these investment

costs through depreciation and depletion charges against

oil income as produced or through abandonment losses if 2

the leases proved to be worthless. Percentage depletion

would be allowed to B rather than cost depletion only if

it should be larger.

Since the $16,000,000 is such a large cash outlay

for B, and since the total is recoverable fully only if

four of the total ten million reserve barrels are produced

(see assumption below), this conventional method is not

too appealing to him, B, still desiring to purchase the

property, looks for a better financing arrangement—one

in which the initial cash payment is not as crippling to

him financially. Thus, the ABC production payment arrange

ment has been devised.

2 Kenneth G. Miller, Oil and Gas Federal Income

Taxation (New York, N,Y,: Commerce Clearing House, Inc, 1967)/ p, 185.

10 I

For explanatory purposes the ABC sale of oil and

gas is set forth below in a hypothetical case study

(hereinafter called the Oilola Case). The Oilola Case is

utilized in this chapter to explore current tax laws and

cases which serve for the appropriate tax treatment of the

transaction. The Oilola Case is carried throughout

Chapters III/ IV, and V to illustrate financial accounting

for the retained production payment. Listed below is a

summary of the major assumptions and other information

inherent in understanding the Oilola Case.

Oilola Case Major Assumptions 1. Party A: the seller or assignor 2. Party B: the purchaser of the working

interest 3. Party C: the payment lender or corporation 4. Initial cash payment: $4,000,000 5. Retained production payment: $12,000,000 6. Interest on unliquidated payment balance: S^o 7. Principal and interest payable out of 75%

of production 8. Total reserves: 10,000,000 barrels of oil 9. Barrel production per year: 2,000/000/

constant 10. Sales price per barrel: $3.00/ constant 11. Lifting costs per barrel: $.40, constant 12. Fair market value of lease and well

equipment: $2,500,000

13. Royalties and production taxes: disregarded

Party A will sell his working interest leases for

an initial cash consideration of $4,000,000 and retain an

oil payment of $12,000/000 plus interest of 5i^ to be paid

solely out of 75% of oil production if/ and when, produced.

A will then assign the retained production payment to a

third party/ C, for $12,000,000 plus interest.

11

As can easily be seen, a major advantage to B is

the relatively small amount of cash needed.to acquire the

properties coupled with the favorable contingency since

the production payment is not a direct or an indirect 3

liability. Another advantage to B is that income taxes

are saved since/ as explained later in this chapter,

gross income applied to the production payment is excluded

from B's taxable income under current tax regulations.

Application of the production payment for the

Oilola leases is illustrated in Table 1, This table presents

the requirement in barrels (75% of total yearly production)

necessary to liquidate the $12,000,000 production payment

plus the 5 1% interest on the outstanding principal amounts.

Note that the production payment is fully liquidated during

the third year, and observe that the fourth and fifth year

are free from the encumbrance; that is, all barrels pro

duced belong to B, the working-interest party.

A' s Tax Conseguences

A, the seller of the property/ realizes a capital

gain on the sale of the lease provided the tax holding

period requirement has been met. The production payment

must be assigned to C at the same time as, or subsequent

C. Aubrey Smith and Horace R. Brock, Accounting for Oil and Gas Producers (Englewood Cliffs, N.J.: Prentice-Hall/ 1959), p. 132,

12

o H

u H

O

H O

to

!3 rH rH

a a (1)

&

o •H

o

0 M

rH 0)

u

4J w

^ 0) JX^ M in 0)

c: H

•H U

•H U 0*

(0

o

Cn-P c: -H i u

tn 0) M 0)

0 -M IS

c: 0 •H

+j o TJ 0 M CU

c: H

4J c Q) U

lA

fd 04

rH fd

O EH

fd

o o o V o vO vO

<y>

o o o H o Tl-00

V

CO

<o-

••t

o o o «« o o in

V

-^

</>

o o o o o in

o o o s o o in ^

H

O O O

O O O

N

CM

o o 00

V

CO Tl* ^

o o (N

V

rH in

o % "^

o o o V o o ID

V

^

o o o o o in

o o o V o o in

V

rH

O

o o O O O

K

CN

o o CM «> vO CM CM

O O 00 ««

CO

o rH *.

"^

O O O ^

in CO CO •»

^

o o o If) in in

o o o V in ^ ^

K

rH

O O

o O O O

N

CM

1 1

1 1

1 1

O

o o o o o % CM

1 1

'

o o o o o o »» CM

1 1

1 1

1 1

o o o o o o H CM

1 1

o o o o o o *» CN

o o o

V

in t^ CO

rH </>

O

o o

V

o o O

K

CM rH </>

O

o o K in CO en

*, en rH •co-

o o o in in in ^

in

o o o N in -* ;f «.

^

o o o o o o > o rH

o o o o o in

U U fd A U 0) ft o o

• en </>

X m

rH 0) u u fd

o o o o o in

s rH

CN CO LO

13

to, the assignment of the working interest to B for A to

be entitled to capital gain treatment on the entire con

sideration. To determine gain or loss on sale, A must

allocate his original cost basis between the interest sold

and the interest retained in the proportion of their

respective fair market values, and A must compute the gain

or loss on the difference between the cash received and

the basis of the interest sold. A then sells the retained

oil payment to another party/ C, and derives gain or loss 4

from such sale. According to Ernest L. Minyard,

If A assigns the reproduction payment interest to C prior to the assignment of the working interest to B, the proceeds from assignment of the production payment will be treated as an anticipatory assignment of income from the property and will be subject to taxation as ordinary depletable income. In other words, such proceeds would be added to proceeds from regular oil and gas sales from the property ^ prior to sale and would be taxed accordingly.

Oilola Case Application

In applying the above principles of income tax

regulations and cases to the illustrative case study.

^Commissioner v, Fleming, 82 F, 2d, 324 (C,A, 5th, 1936).

^Ernest L, Minyard, "How To Determine the Tax Saving that Makes an ABC Deal Worthwhile," The Journal of Taxation, XXIII (May, 1960), 291.

14

A's income on the sale of the Oilola leases would be

computed as shown in Table 2.

TABLE 2

COMPUTATION OF A'S TAXABLE INCOME

Fair Market Value

Total Properties

Properties Sold

Cash received Production payment

Less: Fair market value of lease and well ec[uipment

Value of leasehold rights

$ 4,000/000 12,000,000 $16,000,000

2,500,000 $13,500,000

$4,000,000

$4,000,000

2,500,000 $1,500,000

$13:500:000 $1-000'000 (1) = nilrlll =

Basis attributable to leasehold rights sold

A's Taxable Income Cash proceeds Less: Lease and well equipment Leasehold costs Selling and legal expenses

Taxable gain to A

$ 1,800,000* 111,111 18,889

$4,000,000

1,930,000

$2,070,000

*A's adjusted tax basis, prior to sale.

A, therefore, will report a capital gain of

$2,070,000 and will allocate a tax basis of $888,889

($1,000,000 less $111,111) to the production payment retained

15

by him. A then sells the retained oil payment to C for

$12,000,000 and will recognize a capital gain or loss,

if applicable, on such assignment.

B's Tax Conseguences

The ABC financing arrangement, under current tax

regulations, has direct tax benefits for B, the purchaser

of the oil and gas leases. B's tax benefits have evolved

primarily from one well-known Supreme Court Case entitled

Thomas v. Perkins established in 1937. The Supreme Court

held that a production payment constituted an economic

Interest in the oil and gas in place. Due to this economic

interest factor, the oil and gas income received by C, in

liquidation of his production payment, is considered to

be taxable and depletable income to him as though that

share of the hydrocarbon was produced and sold by him.

Therefore, the only taxable income to be reported by B

during the payout period of the payment is the remaining

working interest not retained, thus constituting the major

tax benefit attributable to B.

In an ABC transaction the production payment must

qualify as a depletable economic interest requiring the

liquidation of the payment to be paid solely out of oil

^Thomas v. Perkins, 301 U,S. 655 (1937),

16

or gas produced.*^ if the production payment is, or might

be, liquidated in any part from proceeds not derived from

a sale of the oil or gas produced from the property, it

is not a depletable economic interest in the property, in

such cases B will be taxed on income liquidating the pro-

duction payment.

B must allocate the initial cash outlay between

lease and well equipment and leasehold cost for income

tax purposes. Lease and well equipment is a depreciable

asset while leasehold cost is a depletable asset. Such

allocation of the initial cash outlay is determined by the

ratio of the asset's respective fair market values, if

known. Tax allocation of these two assets by B frequently

differs from the tax allocation previously recorded by A, 9

the seller.

All operating costs for the producing leases are

fully deductable by B for tax purposes provided that, at

the time of acquisition of lease, it is anticipated that

the income accruing to B during payout of the production

payment will be adeq[uate to pay these operating expenditures

7 Anderson v, Helvering, 310 U.S, 404 (1940). g Minyard, The Journal of Taxation, XXIII, p. 291. 9 Arthur Andersen & Co,, Oil and Gas Federal Income

Tax Manual (Chicago, 111,: Arthur Andersen & Co,, 1966)/ p. 248.

17

If it is predicted that the operating costs will be in

excess of B's gross income while the retained production

payment is being liquidated/ this excess must be capitalized

as additional leasehold cost each year as costs are

incurred.10

Oilola Case Application

Application of the above principles of income tax

regulations to the Oilola Case would recjuire B to record

$2/500/000 of the initial cash paid ($4/000,000) as lease

and well equipment with the balance of $1,500/000 allocated

to leasehold cost. B will depreciate his lease and well

equipment over the remaining productive life of the Oilola

leases and will deplete his leasehold cost under maximum

allowable laws also during the productive life of the

leases.

B has no direct or indirect tax consequences until

production of the oil begins, computation of B's taxable

income from his 25% working interest of the Oilola leases

during the first year of production is illustrated in

Table 3, assuming 2,000,000 barrels or 20% of total reserve

barrels of oil are produced by the leases.

Lifting costs are deducted in full as incurred

for the entire property. Depreciation is based on the

Breeding and Burton, p. 501,

18

TABLE 3

COMPUTATION OF B'S TAXABLE INCOME

Revenue

Oil sales (2,000,000 barrels x

25% working interest x $3.00) $1,500,000

Expenses

Lifting costs (2,000,000 x $.40) $800,000

Depreciation (500,000 x $.45) 225,000

Depletion (20% x $1,500,000) 300,000 1,325/000

Taxable income to B $ 175,000

unit-of-production method by dividing the total leasehold

cost by B's total working-interest reserve ($2/500/000 *

5/555/000 = $.45). The per barrel provision is then

amortized over B's working-interest barrels. Cost depletion

is used in computing B's taxable income or loss because

of his high leasehold costs and because percentage depletion

would be less than cost, considering the applicable 50%

limitation of taxable income before the depletion provision.

C ' s Tax Consecfuences

C, an investor or corporation, will record the

production payment as a receivable asset and will reduce

this asset each year by the 75% working-interest revenue

applicable to the principal.received from B's Oilola lease

19

and will recognize income as the contra, c will also

record the interest on the unliquidated production payment

as income to him. Therefore, the entire amount received

by C, as consideration for the assignment of the production

payment, will be ordinary income to him in the year of

production, and it will be subject to an allowance for

depletion which is generally computed on the sum-of-the-

dollars method.

Oilola Case Application

In applying these tax principles to the Oilola

Production Payment, C will receive $4,500,000 in the first

year of production of which $3,840,000 will be applied to

the principal and $660,000 will be interest income, as

noted in Table 1. The total amount is ordinary income

subject to depletion. Depletion computed by C will, of

course, be the maximum under tax laws. Table 4 illustrates

C's tax position under current income tax regulations.

As can be noted in Table 4, C's taxable income of

$450,000 is essentially the 5J$% interest received on the

production payment. All of the principal and part of the

interest has been eliminated by the maximum allowable

depletion taken.

Commissioner v, P, G. Lake, Inc., 356 U,S, 260 (1958); and Arthur Andersen & Co., Oil and Gas « , , , p. 173.

20

TABLE 4

COMPUTATION OF C'S TAXABLE INCOME

Revenue

Oil sales (2,000,000 barrels x 75% working interest x $3.00)

Composed of: Principal $3,840,000 Interest 660,000 $4,500,000

Expenses

Depletion 4,050,000*

Taxable income to C $ 450,000

*Sura-of-dollars method: 12

Receipts for year ^ principal Total Expected Receipts ^

°^ lit:33°:000 $12,000,000 = $4,050,000

Frequently, C will borrow part or all of the

principal from another party, D, at a slightly lower percent

interest of/ for example, 5%. This procedure gives C a

^ interest spread (5 1% less 5%) as his ultimate tax

profit.

^^Ibid. 13 Arthur Andersen & Co., Oil and Gas . . . /

p. 174.

21

Influence of Proposed Legislation

An interview with Mr. E. L. Wehner/ partner in

charge of Arthur Andersen & Co.'s Houston office, disclosed

proposed legislation before The United States House of

Representatives' Ways and Means Committee which will

affect materially the ABC transaction and the respective

14 parties involved. As support for this interview, a

copy of the proposal prepared by the Treasury Department

has been secured by this author.

The Treasury Department's proposal, in effect,

would treat production payments as non-recourse loan trans

actions. As a result, the owner of the oil and gas lease

subject to the production payment would take into account

income and expenses with respect to the production payment

in the same taxable year. When an oil and gas property,

subject to a production payment, is transferred, it is

proposed that the transferee of the mineral property be

treated as if he had accjuired the lease subject to a

mortgage. The income derived from the property used to

satisfy the production payment would be taxable to the

owner of the property and would be subject to the allowance

for depletion. In the case of a working interest burdened

by a retained production payment, the production costs

14 E. L. Wehner/ private interview, June, 1969.

22

attributable to oil or gas applied to satisfy the pro

duction payment would be deductible in the year incurred. ^

Oilola Case Application

The proposed tax reforms would materially affect

Parties B and C in the Oilola Case, but would have no

effect on Party A. A will treat the gain on the sale of

his interest as a capital gain in the same manner as shown

in Table 2. B, however, will include the production pay

ment revenue in his gross income, subject to depletion,

during the payout period and will deduct as current expenses

the lifting costs incurred with respect to the oil used to

satisfy the production payment. C will treat the

$12,000,000 production payment as a nontaxable return of

capital and will record the interest as ordinary income.

Summary

The ABC transaction is, without a doubt, a "child"

of our Federal tax law. To discuss the transaction without

defining or setting forth these tax laws (both current and

proposed) would constitute a wholly inadequate discourse.

For that matter, it is extremely difficult to discuss any

Treasury Department, "Summary of The President's Tax Reform Proposals for The Revenue Act of 1969," Washington, D.C, April, 1969, (Xeroxed,)

23

major topic dealing with oil or gas accounting without

including income tax aspects and influences.

Current tax laws surrounding the purchaser of a

working interest subject to a retained production payment

have established the foundation for two of the three

variations in financial accounting treatment—the net

method and the economic-interest method. The net method

follows tax laws with few exceptions. Purchaser B

excludes from his income the proceeds from production

applicable to the retained production payment and includes

in his expenses all costs required to produce the total

hydrocarbon from the lease. The economic-interest method

follows income tcix laws and the net method with primarily

one major exception; that iS/ estimated lifting costS/

applicable to the production payment are capitalized and

amortized over the production attributable to B's interest.

The net cind economic-interest methods will be discussed

in Chapter IV.

The ecjuitable-lien method of financial accounting

treatment, however, does not follow current income tax

laws with respect to income to be recognized by B, This

method treats the ABC transaction as though B accjuires the

entire interest that was owned by A, the seller, with the

production payment assigned to B, The payment constitutes a

liability in the nature of an ecjuitable lien to be satisfied

24

only from the proceeds of the sale of oil and gas if,

and when, produced. The equitable-lien method of financial

accounting is supported by the proposed tax law changes

being considered currently by the House Ways and Means

Conmittee. . Foundations and possible consequences of the

equitable-lien method are discussed in chapter III.

CHAPTER III

FINANCIAL REPORTING UNDER THE

EQUITABLE-LIEN METHOD

Introduction

The equitable-lien concept of accounting for retained

production payments treats the transaction as though B, the

purchaser of the working-interest, acquired from A, the

seller, the entire or total property. This method, effec

tively, is contrary to the current legal view of the

"economic-interest" theory of law established previously in

Chapter II. The production payment is treated as a liability

of B in the nature of an ecjuitable lien to be satisfied only

from the proceeds of the sale of oil and gas as, and when,

produced. According to Arthur Andersen & Co., this method

regards the retained production payment as a method of

financing. Accordingly, the purchaser looks through the

legal form of the transaction and regards the substance

of the transaction as the acquisition of the entire property

subject to an unassumed lien thereagainst.

In substance, the equitable-lien method can be

inferred as being a lease which gives rise to property

^Arthur Andersen & Co., Accounting and Reporting . , p. 115.

25

26

rights since the purchaser of the working interest considers

himself the "owner" of the entire property. To the extent

that the leases acquired give rise to property rights for

the purchaser, then those rights and related liabilities

should be measured and incorporated in the balance sheet.

This chapter presents the equitable-lien method

of financial accounting and reporting by illustration of

the Oilola Case study and by examination of petroleum

company annual reports. These annual reports ser-ve this

chapter as support for the equitable-lien's use in practice.

Oilola Case Study

Assumptions

The Oilola Case study was introduced in chapter II

as the illustrative case for presentation purposes of this

thesis. For the sake of clarity and understanding in this

chapter, details of and assumptions to the case study are

reproduced in the following paragraphs.

A, the owner of the Oilola leases desires to sell

his leases to B, an oil operator, for $16,000,000. A,

utilizing the ABC tax arrangement for the transaction,

requires B to pay $4,000,000 in cash and retains an oil

John H. Myers, "Reporting of Leases In Financial Statements," Accounting Research Study No, 4 (New York, N.Y.: American Institute of Certified Public Accountants, 1962), p. 4.

27

production payment of $12,000,000 payable out of 75% of

future production. Upon completion of the transfer, A will

assign the production payment to C, a banker or separate

corporation, for immediate access of the principal cash.

Listed below is a summary of the major assumptions and

other information inherent in understanding the Oilola Case.

Oilola Case Major Assumptions 1. Party A 2. Party B 3. Party C

the seller or assignor the purchaser of the working interest the payment lender or corporation

4. Initial cash payment: $4,000,000 5. Retained production payment: $12,000,000 6. Interest on unliquidated payment balance: 5 ^ 7. Principal and interest payable out of 75%

of production 8. Total reserves: 10,000,000 barrels of oil 9. Barrel production per year: 2,000,000,

constant 10. Sales price per barrel: $3.00, constant 11. Lifting costs per barrel: $.40, constant 12. Fair market value of lease and well

equipment: $2,500,000

13. Royalties and production taxes: disregarded

Assume, additionally, that B is a recently formed corpora

tion with 40,000 shares of $100 par value capital stock

and no other assets or accounts than those recjuired for

the purchase transaction.

Purchase Transaction

The acquisition of the Oilola leases by B is

generally accounted for by recording the cash paid plus

the production payment's principal as productive assets

with the principal as a liability at the date of such

purchase, shown in the following entry:

J*!'*"''"

Lease and well equipment

Leasehold cost Production payment payable

Cash

Debit

2,500,000 13,500,000

28

Credit

12,000,000 4/000,000

Observe that the fair market value ($2,500/000) is used

for the recording value of lease and well equipment in

accord with income tax purposes. The leasehold cost is

the difference between the total sales price and the lease

and well fair market value ($16,000,000 less $2,500,000),

a treatment contrary to income tax regulations. Occasionally,

only the initial cash payment is charged to the leasehold

account at the date of accjuisition, and the additional

payments in liquidation of the production payment are

debited to the property account as they are subsecjuently

made. Let it be assumed, however, for the purpose of this

thesis, that the initial cash paid, net of the fair market

value of equipment, plus the production payment are

capitalized as leasehold cost as shown in the above entry.

The production payment payable account is more

frequently treated as a contra to the leasehold cost account

on the asset side of the balance sheet, in lieu of a debt

Leo C, Haynes, "Accounting for Leasehold Costs in the Petroleum Industry," The Journal of Accountancy (April, 1942), p, 336.

29 4

on the liability side. The theory behind this treatment

is founded on the fact that the payment is a contingent

liability to be paid only if the applicable hydrocarbon is

produced. As the production payment is liquidated, the

book value of the leasehold cost increases.

Income Statement Presentation

B's equitable-lien income statement for the five

productive years of the Oilola leases is shown in Table 5.

Oil sales revenue in Table 5 is the total gross production

from the leases. Gross income for the entire lease is

used under the equitable-lien method because B has acquired

A's entire interest subject to the lien on production.

This procedxire is contrary to the income tax accoiinting

discussed in chapter II where only oil sales applicable to

B's working interest are included in his gross income in

determination of taxable income.

According to Table 1, the first three years include

both the amounts applied to the liquidation of the produc

tion payment (75%) and the amounts applicable to B's

working interest (25%) or 2,000,000 barrels times $3.00

per barrel. Payout of the payment occurs at the end of

the third year, thereby boosting B's cash position

^Porter, p, 498.

in

W •J

fd

O

in

u fd 0)

fO

CM

O O O

s o o o o en

o o o

s o o o

s VO

O o o o o o vD

O o o o o o

s

o o o o o o VO

o o o o o o

«. VO

Q)

Q) > (U

dJ rH fd n H -H O

o o o o o o o o o o o o

*• N S K

O O O LO C O O ro o in in ro -^ CM ro H

rH

000

33

5,

$2

1,

o o o o o o o o o

«. «. s o o o o o o 00 in r^

CM

o o o o o o o o o

% •> •• o o o o o o 0 0 LO t ^

CM CO-

o o o o o o o o O O O CM

O O O VO O O O CN 00 in r^ CM

CM </>

VO CN CM

•c/M

o o o o o o o o O O O CO

•» ^ % V

O O O 00 O O O ' ^ CO in r "*

CM </>

o o o o o o o o o o o o o o o o O O O VO 00 IT) r- vo

CM </>

o VO VO

w

CO +J M O

o

•H

^H •ri

o -H

fd

o u

o -H +J (U

4J w 0) M 0) P^O^-^J

0) (U d Q n H

o o o

•» LO VO VO

^ CO

</>

•K ro ro

* ro ' ^

</H

30

o o o

N

o o o

«« "^ <0-

o o o

V

o o o

N

CM </>

o o • o in

<M

o o o •>

o o o

^ </>

o o o

V

o o o

V

CM •CO-

o o • o in

<M

o o 00

*. CO

r r-

% H V>

lO ro

• ^ ->*

</>j

o o CO

•« CO " * ^t

V

- ^ •CO-

o o CN

s.

H in LO

«. rH <o-

00 r • CO ro

<M

O O

o

o v}< CO

V

H •CO-

o lO

• CO ro

•co]

0) B o o i^

-H

-M 0)

(D

(U u 0

u 0)

m \j\ (U d u

• H fd

U w fd w

in u fd (D

>1

p> •H IH U O IH (U cn fd M (U

> •rl +> O 0)

in

w

31

substantially for the fourth and fifth years. The income

statement, which, of course, continues to report total

property gross income after payout, does not indicate the

change in B's cash flow. More comments concerning proper

disclosure under these circumstances are discussed later

in this chapter.

Lease operating expenses and other lifting costs

are deducted in full from gross income as incurred, thereby

fairly matching costs given up with the applicable income

reported.

Lease and well equipment is depreciated over the

leases' productive life of five years on the unit-of-

production basis. Computation of depreciation per barrel

is determined by dividing the cost by the total reserves

($2,500,000 * 10,000,000 = $.25).

The leasehold cost is depleted over the productive

life of the leases also on the unit-of-production basis.

Computation of depletion per barrel is determined by

dividing the cost by the total reserves ($13,500,000 *

10,000,000 = $1.35).

Under the ecjuitable-lien method the oil production

applied to interest expense on the unlicjuidated principal

is deducted in the income statement along with operating

expenditures. Since the total interest on the unlic[uidated

payment is not capitalized with the leasehold cost and

32

since gross income includes the application of the payment's

principal and interest, this expenditure must be deducted

on the income statement.

Balance Sheet Presentation

The only significant items on B's balance sheet

under the equitable-lien method are the leasehold cost

section with its applicable amortization and the equity

section. Table 6 presents these two items as though they

were extracted from B's balance sheet.

The cash allocated to leasehold cost, as shown in

Table 6, is capitalized together with the production pay

ment principal, and the unlicjuidated principal is deducted

as a contra to the gross leasehold. As B produces the oil

subject to the production payment, he makes the entry

below to record the payment to the holder (see application

of production payment in Table 1 for determination of

amounts) . These proceeds paid to the holder are treated

partly as a reduction of the contingent liability account

operating to increase B's ecjuity in the leasehold account 6

and partly as a discount or interest expense.

^Smith and Brock, p. 350.

Sorter, p. 189.

33

3

»n

14 rtJ V

0

c u

n

CN

o o o o o p

* i o o o o in o « ^ rH <N

r H </>•

§ o % O 1

O 1 in

% m H '•A-

O

o o H

o o i n % c*>

H « / » •

o o o ^ o

o in ^ n

f - i

1 1

</v

o o o o o o ^ V

o o O O 1.-) o

« ^ r^ CN

i H

V>

O o o

s

O 1 O 1 in

s

(*) H to-

o o o %

o o m ^

n H vy

O o o o o 00

o H

o o o ^

o o r ^

CN

fA.

o o o o o o o o o o «n o f-i CN

rH

o o o ^ O 1

O 1 i n

^ n H

</>

O o o ^ o

o in ^ n

H v>

O o o * O

o r H

% CO

o o o

* i

o o t l "

^ i n

vy

o o o o o o

,500,

,000,

-H CN -H

C/J-

O O O O O 03

,500,

.108, 200

,391, 000

400,

in

200

991,

o o o o o o ^ ^ o o

o o in o N «k

rH a rH

</>

o o o o o o

H «.

o o O VO i n r-l

*. -CO GO rH V >

O o o ^ o

vT m ^ i n

'/>

o o o

•k

o o r-

K

CN

O o o

V

o '!l< vO

h .

n

</>J

O

o O s

o o o *. in

</>•

o o o o o o

^ Ik

in o ^0 o vO o

^ «k

o n </>

o o o

•b

in U3 ' 0

«k

CO

</>

o o o ^

in -0 vO « ro

r-l <A

m VO

• H ^ n

v>

o o o o o o in

o o o o o o in o o o '0 o 'f CN

VJ1 </>

n t

H

CM

VH

o o o o o o N

in

<o-

o o o o CN 0 0

^ -. rA CO (j\ r^ 00 r-

^ s CN r-{

v>

o o o

^ in <.o vO ^ 1"

</y

O O o

•. in VO VO

^ CT>

V>

ro vO

• H •* CN

vy

000

000,

^ m oy

O o

o o

340,

551,

•. ^ i-i rH

t o -

200

891,

•» C l

w

200

891,

•-r-vy

.28

197

</>

o o o

o o o

•-in

CO-

o o o

1 o 1 'J-

ro <> r-l

</>

O o o o • *

fO

^ rH

</:

O o o

• o • < *

ro ^ vO

</>

o in

• 00 in r-i

<^-»

.a u •) r: • 1 rj

0 T - •' ;J 0 , i : 0 r j

-3 r-f

a c r^ 0 ,0 H ..! 4J 'J t ;

0 -H :J -."r- l r j J O^ 0 •• C^ 'H

- • ; ' ' • ^

4

•-0 UJ 0 t O

r H lO 0-. H 0 ii

•ri

u cu •d llJ 4J (3

• a .H :3 0 " r-l

r H

' J

• • •J) •r)

••J • J

M 0

' H

0) c

u o Ii rl f j -p •« 0 0 rH

r-i Pi r-i 'U ITJ ' 0

• • '.1 '-1 0

K )

-M 0) :

,. i n

Q) rH

W ,Q

> -P - r t

Di .:! 14 Ef

•H - - ' r ;- c: n rj M lU

,'' . ' I \V

0 r-J tn 11 -t' J C 0 ;T H U

T^ !.' c; ' 6 ! -1 O >H -H . -; r j c; rH 0

_(; /'. o c W

4' -H :.-! .P .H rj .J y P) ,'J PT K .1 0 r J '--1

<U

13 rC U3

W <u Oi

0) ^

rH rO >

M 0 0 M

34

Debit Credit

Interest expense 660,000 Production payment payable

(leasehold cost) 3,840,000 ^^^^ 4,500,000

Net income and retained earnings are substantially

high under the equitable-lien theory on a per year analysis

and on a cumulative years' analysis since revenue is

reported at gross including both production payment

application and remaining working interest income. The

application of the production payment of $4,500,000 out of

$6,000,000 gross income in the first year's production /

presents an interpretative problem for financial reporting.

As to the solution to this matter, Stanley Porter commented,

"It is apparent that, in those instances where the gross

method" (equitable-lien) "of accounting is followed, it

is necessary to supplement the basic financial statements

of cash flow or working capital provided if they are to be 7

meaningful to the ordinary reader." The cash flow or

working capital analysis serves to reconcile the reported

income with the production payment applications until

payout status is reached.

" Ibid., p. 517.

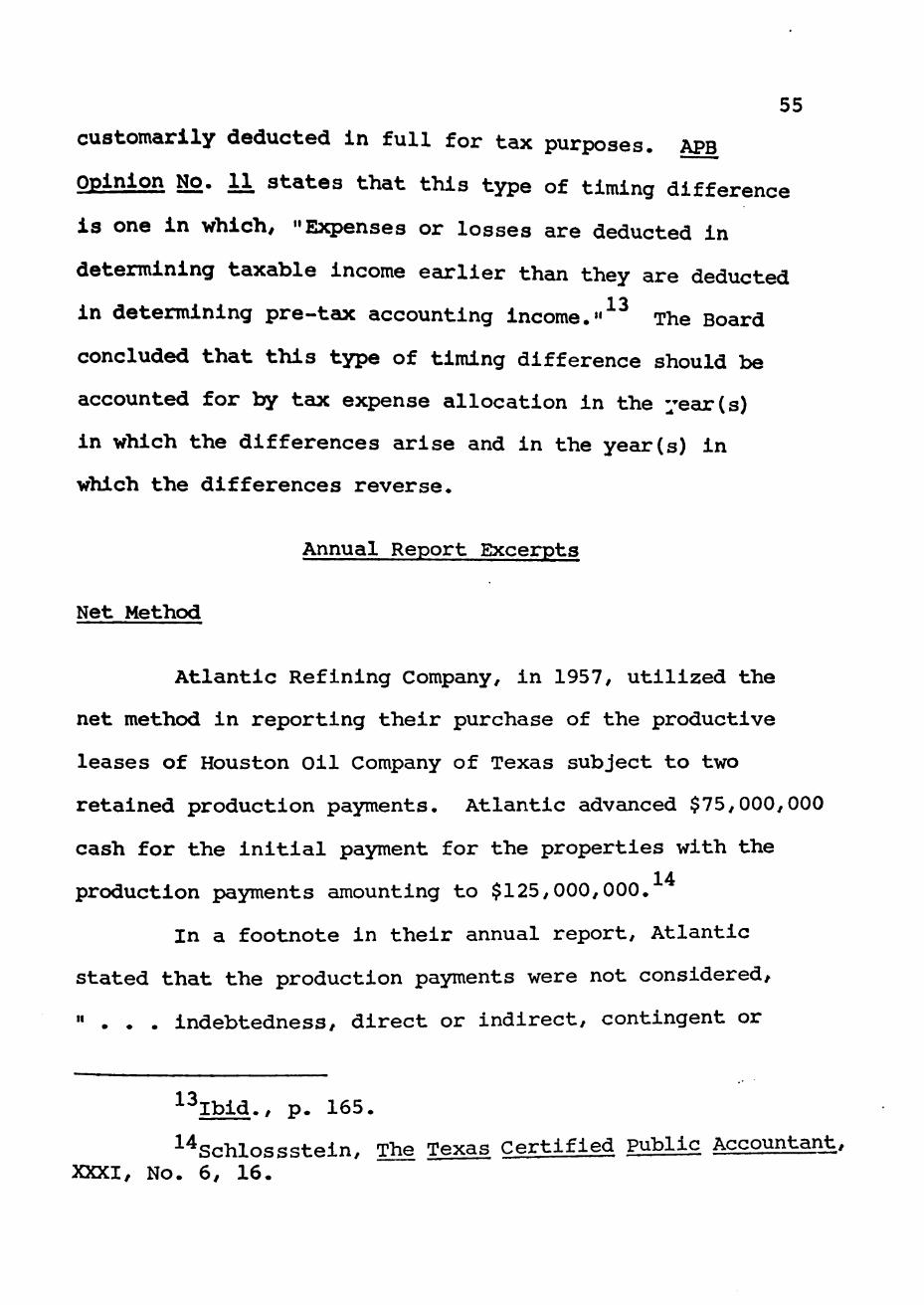

35 Income Tax Allocation

income tax allocation under the equitable-lien

method Imposes, primarily, two problem areas determining

tax expenses in the statement of income and the amount of

Income tax for the Federal return. These areas are gross

income and depletion expense.

The gross income problem is centered around the

"total-property concept," characteristic of the equitable-

lien method of accounting, versus the "separate-property

concept," characteristic of Federal income tax regulations.

In the Oilola Case Purchaser B accounts for total property

gross income for financial purposes ($6,000,000)7 whereas,

under income tax laws, B must account for his separate

property gross income ($1,500,000).

The depletion expense problem is also founded on

the total property concept of the equitable-lien method.

Capitalization of $13,500,000 of leasehold costs for

equitable-lien purposes, as opposed to $1,500,000 for

income tax purposes, creates substantial differences in

the two methods' depletion expense.

These two differences are considered to be permanent

differences according to APB Opinion No. _11 since they

" . . . arise from statutory provisions under which

specified revenues are exempt from taxation and specified

expenses are not allowable as deductions in determining

36 8

taxable income." Only a footnote informing the statement

reader of the nature and amounts, if material, of these

permanent differences would be required for fair financial

disclosure.

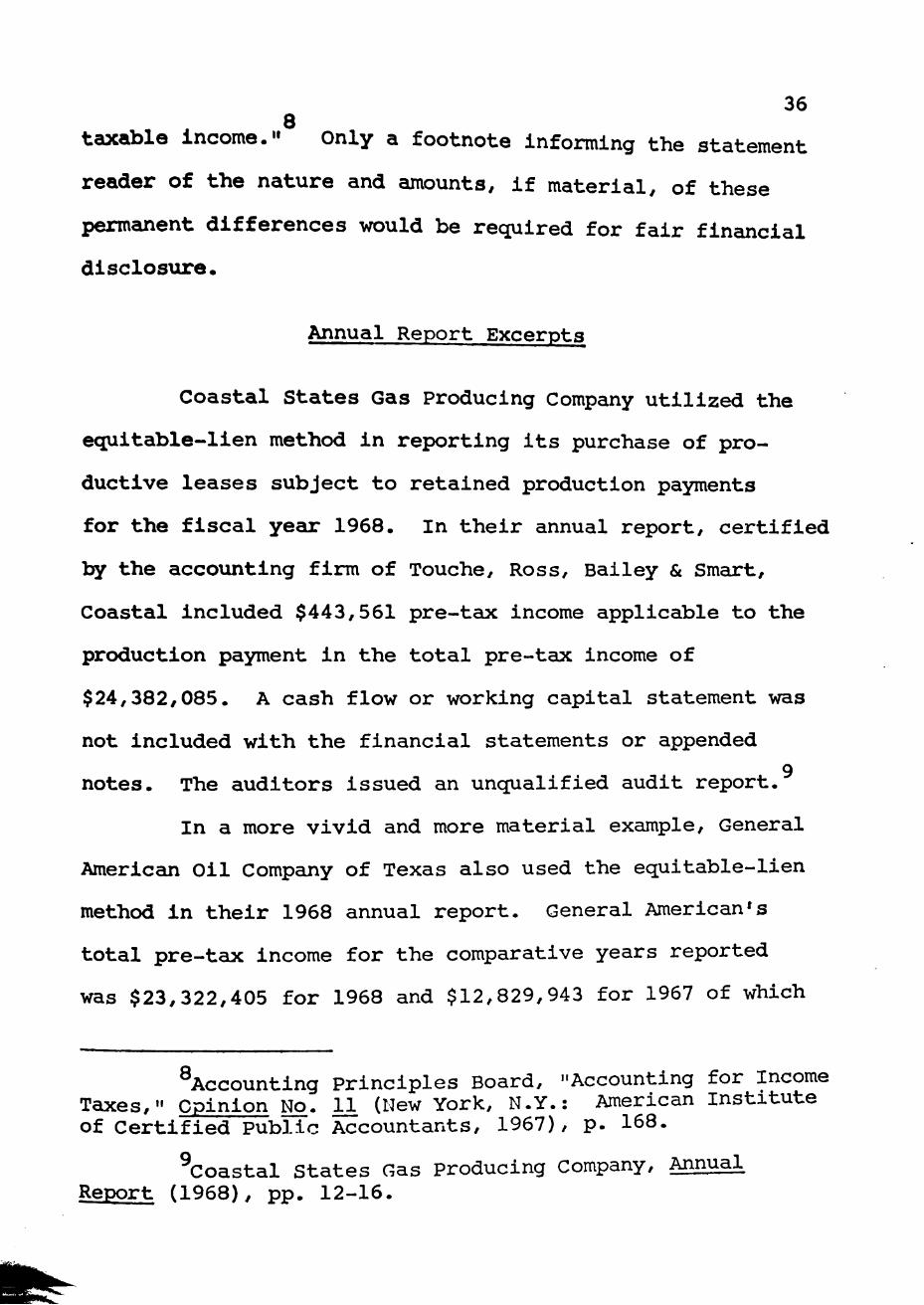

Annual Report Excerpts

Coastal States Gas Producing Company utilized the

equitable-lien method in reporting its purchase of pro

ductive leases subject to retained production payments

for the fiscal year 1968. In their annual report, certified

by the accounting firm of Touche, Ross, Bailey & Smart,

Coastal included $443,561 pre-tax income applicable to the

production payment in the total pre-tax income of

$24,382,085. A cash flow or working capital statement was

not included with the financial statements or appended 9

notes. The auditors issued an unqualified audit report.

In a more vivid and more material example. General

American Oil Company of Texas also used the equitable-lien

method in their 1968 annual report. General American's

total pre-tax income for the comparative years reported

was $23,322,405 for 1968 and $12,829,943 for 1967 of which

^Accounting Principles Board, "Accounting for Income Taxes," Opinion No. U (New York, N.Y.: American Institute of Certified Public Accountants, 1967), p. 168.

^Coastal States Gas Producing Company, Annual Report (1968), pp. 12-16.

37

$14,448,770 in 1968 and $11,028,504 in 1967 amounted to

income applied to liquidation of the retained production

payment's principal and interest.

The Company's balance sheet for both years included

in the gross cost of producing properties approximately

$170,000,000 applicable to leases subject to the produc

tion payment. In a footnote to the financial statements,

disclosure was made of such amounts together with a state

ment that since no direct liability attached to these

payments, the unpaid balances were shown as a deduction

from the property accounts.

General American included a statement of source

and application of funds with its financial statements

which presented the amounts applied to liquidation of the

retained payments; and the Company disclosed, in the foot

note, the accounting method employed and the retained

amounts involved—gross income from crude oil and gas sales,

taxes and interest expense, and net proceeds. General

American also provided another footnote on income taxes

stating that the recognized production payment amounts

were excluded in determination of the income tax liability

for financial reporting purposes. Ernst and Ernst,

^^General American Oil Company of Texas, Annual Report (1968), pp. 15-21.

^^Ibid.

38

General American's auditors, issued an unqualified audit 1 o

report for the reported year.

Summary

The equitable-lien method treats the retained

production payment as an acquisition by the working-interest

party of the entire leases subject to an unassumed lien.

This view looks through the legal concept (Federal income

tax law) which requires separate reporting of income as

between the purchaser and the holder of the production

payment for their appropriate interests. The production

payment principal and initial cash paid are capitalized in

full as property accounts. The unpaid payment is pre

sented as a liability, either contra to the property or

as a debt on the right side of a balance sheet.

Net income, total and per share, includes all

amounts of income and expense applicable to the total

property, even though a certain percent of gross income,

retained by the payment holder, is paid to him during

payout status of the production payment.

Fair and informative disclosure under the equitable-

lien concept has required practitioners to include either

in the footnotes or in the funds statement sufficient

information for the reader to ascertain the accounting

•"•^Ibid.

39

and reporting nature of retained payments and amounts «

involved, if material. A footnote, regarding income tax

expense allocation has also been regarded as necessary

for informative disclosure.

CHAPTER IV

FINANCIAL REPORTING UNDER THE NET

AND ECONOMIC-INTEREST METHODS

Introduction

Current tax laws and legal framework of the ABC

transaction have established two related methods of

financial reporting and accounting for retained production

payments—the net and the economic-interest methods.

The net method follows Federal income-tax reporting

with one minor exception. The purchaser of the working-

interest, B, under this method, records his initial cash

outlay as property,* he includes in his gross income only

that which is applicable to his working interest, and he

deducts all costs and expenses incurred in operation of

the total properties. The primary exception between this

financial method and income tax reporting lies in the area

of cost depletion for book purposes versus percentage

depletion for tax purposes.

The economic-interest method follows Federal income

tax reporting and the net method with one major exception.

Similar to the net method of financial reporting, this

method requires the purchaser to include in his gross

income only that which is attributable to his working

40

41

interest, not that retained by the production payment

holder; and it requires the purchaser to record his initial

cash outlay as property. The major exception to the

economic-interest method, when compared to Federal income

tax reporting, is that lifting costs applicable to the

retained production percentage are capitalized as additional

leasehold cost for the payout period of the production

payment and are amortized over the productive life of the

property. This procedure, of course, creates a difference

between cost depletion expense for book purposes and

percentage or cost depletion, whichever is applicable,

for income tax purposes.

Basic reasoning that supports the accounting

treatment of these two related methods is that retainment

of the oil payment has resulted in the creation of two

complete and separate properties. This concept is the

legal view established by the Thomas v. Perkins Supreme

Court case. The purchaser is considered to be the owner

of a future or residual interest, and the production

payment holder is considered to be the owner of a right

to substantially all the oil produced from the property 2

until his interest has been liquidated.

^Thomas v. Perkins, 301 U.S. 655 (1937); and A. W. Walker Jt., Texas Law Review, XX, No. 3, 268-270.

^Ibid.

42

This chapter discusses these accounting and

reporting aspects of the two related methods. Like

Chapter III, emphasis on presentation in this chapter is

placed on the Oilola Case study and on appropriate petroleum

company annual reports. These annual reports serve this

chapter, like Chapter III, as support for the methods'

use in practice.

Oilola Case Study

The Oilola Case study, previously introduced in

Chapters II and III, is the illustrative case for presen

tation purposes of this thesis. For the sake of clarity

and understcinding in this chapter, details and assimiption

to the case study are reproduced in the following

paragraphs.

A, the owner of the Oilola leases, desires to

sell his leases to B, an oil operator, for $16,000,000.

A, utilizing the ABC tax arrangement for the transaction,

requires B to pay $4,000,000 in cash and retains an oil

production payment of $12,000,000 payable out of 75% of

future production. Upon completion of the transfer A will

assign the production payment to C, a banker or separate

corporation, for immediate access of the principal cash.

Listed below is a summary of the major assumptions and

other information inherent in understanding the Oilola

Case.

43

Oilola Case Ma lor Assumptions 1. Party A: the seller or assignor 2. Party B: the purchaser of the working

interest 3. Party C: the payment lender or corporation 4. Initial cash payment: $4,000,000 5. Retained production payment: $12,000,000 6. Interest on unliquidated payment balance: 5^. 7. Principal and interest payable out of 75%

of production 8. Total reserves: 10,000,000 barrels of oil 9. Barrel production per year: 2,000,000,

constfioit 10. Sales price per barrel: $3.00, constant 11. Lifting costs per barrel: $.40, constant 12. Fair market value of lease and well

equipment: $2,500,000

13. Royalties and production taxes: disregarded

Assume, additionally, that B is a recently formed corpor

ation with 40,000 shares of $100 par value capital stock

and no other assets or accounts than those required for

the purchase transaction.

Purchase Transaction

The net method records the acquisition of the

productive leases on the basis of fair market values. The

initial cash payment of $4,000,000 by B is allocated to

lease and well equipment ($2,500,000, the fair market

value) and leasehold cost ($1,500,000, the balance). This

proportioning is in full compliance with Federal income

tax reporting discussed in Chapter 11.^ The entry below

^Arthur Andersen & Co., Oil and Gas . . • / p. 248.

44

reflects the accounting mechanics of the purchase trans

action under the net method.

Debit Credit

Lease and well equipment 2,500,000

Leasehold cost 1,500,000 Cash 4,000,000

Similar to the net method, the economic-interest

accounting requires the fair market value to be used in

allocating a value to the lease and well equipment account.

The leasehold cost account, however, includes not only

the balance between the equipment' s fair market value and

the initial cash outlay, but also the capitalized lifting

costs to the extent of the interest retained by the pro

duction payment. Determination of these lifting costs is

made by estimation both of the lifting cost per barrel

and of the barrel reserves needed to liquidate the pro

duction payment. These estimations, based on engineering

and costs analyses, are usually realistic and have general 4

acceptance among accountants in the petroleum industry.

The Oilola Case purchase transaction under

economic-interest accounting would be recorded as shown

on the following page.

^porter, p. 499.

45

Debit Credit

Lease and well equipment 2,500,000

Leasehold cost 3,278,000 Cash 4,000,000 Accrued lifting costs 1,778,000

The capitalized lifting costs in the above entry are

computed by multiplying the barrel reserves applicable

to the retained interest (see Table 1) times the lifting

cost per barrel (4,445,000 x $.40 = $1,778,000). These

costs are credited to an accrued liability account since

they are an estimate of future amounts payable which are

attributable to C's share of future production. The

accrued account, sometimes termed a reserve or a deferred

liability, is amortized only by payments of these lifting

costs when incurred or by revised engineering or cost 5

estimations.

Occasionally, lifting costs are capitalized each

year as incurred, thereby eliminating the need for a

reserve for lifting costs. Under this procedure the

leasehold cost account increases annually, requiring

separate computations of per-barrel depletion cost for

each year during payout. Results of annual lifting cost

capitalization are lower per-barrel amounts in earlier

^Robert M. Pitcher, Practical Accounting for O U Producers (Tulsa, Okla.: Robert M. Pitcher, 1957), p. 116.

46

years and higher amounts in later years. For illustration

purposes, however, this thesis utilizes the reserve or

accrual method of capitalizing lifting cost.^

In both the net and the economic-interest methods,

a memorandum entry of the production payment principal

($12,000,000) is made, but no actual recording or reflec

tion is made on B's books or financial statements, except,

perhaps, in footnote form. This procedure characterizes

the separate property concept, discussed previously.

Income Statement Presentation

B's income statements, under the net and the

economic-interest methods, for Oilola's five productive

years, are presented in Tables 7 and 8, respectively.

Reference should be made, at this point, that payout of

the production payment occurs at the end of the third

year, converting B's percentage of gross income from

25% to 100%. At the bottom of these tables, a reproduc

tion from Table 1 is made of barrels attributable to

B and C's interests in regard to pre-payout and post-

payout status of the production payment.

Oil sales revenue in Tables 7 and 8 represent

solely B's working interest for each year, computed by

^porter, p. 501.

47

u>

u flj

cn

CN

o o o

K

in vO VO

S

vO r-i </

o o o o o o

% vO </y

o o o

^ o o o

% vO i/y

o o o

^ in '0 vD

o o o

H

o o o

% •^ «/>•

o o o

^ o o CO

vy

o o o

^ o o 00

</>

o o o

• < k

o o 00

o o o

^ o o in

^ CN

o o o

« o o <

o o o

^ o o (T\

O O O

•• o in r j

w

o o o o o tn

o o o o o in

o o

VJ-

o o o ^ o

o 00

o o o

N

in CN CN

o>

o o o

% o o O)

o o o

< k

in CJ Cl

O o o

^ o o in

*. r-i

o o o s

o •5 c^

^ 00

«/i

o o o

« in vO VO

CO

iA

* * ro n

• ro ^

CO

O o o

s o •<t in

o o o

^ o -* CN

s

CN «•

o o o

^ o VO

r-ro </>

o o

• - t a>

</2

o o o CD ^ in

o o o s

o •'J' CN

^ CN v>

o o o

•. o vO r

^ ro V,

o o

• r}-<T>

</H

O O O

V

o in rH

o o o

o o Cl

r-i V>

o o o

*. in vO ' t

to

ro ' 0

• r-i H

</H

o o o ^

in ro r-i

O o o

-o ' 0

1,1

o>

o o o

. o •^ ro

to

o in

• CO

<o

o o o «

in i n r-i

o o o

^ o >0 T

'T

to

o o o

o 'J* ro

to

o in

• CO

col

0 r-4

c (0 > Q) cn

•-•1 f O t />

rH - ^ -rl o

•M • C • • 71 ^ O rH rH 0 ,1 rl ,Q A O ,0 -IJ ,0 C Xi

•rl in ••) r-rj .« -|J CN 0 • J

•/. I J '.•> 51 to- r^ to-

o-.H o -J

e O 'D O h C 0 •H 'M

•J

•p /:!

"J P<

t/i Di a) c: u

•ri rJ Crc:

,:)

o o o in 'f

o o o in

o o o o o in

o o o o o in

o o o

s

in in in

•• in

o o o

^ o o o

^ o r-i

o o o o o o ^ CM

o o o ^ o

o o

H

CN

o o o V

m in in

o o o

*. o o o

< k

CN

o o o

• o o in

o o o

^ o o o

*. OJ

0 H

d

'.n r i 0 u U rJ m

T - ;

M M 4J <

A5 o .y a rl

o

lO .;J O

pq

0

n) -P

•H

•P 4J (0

0) H 0) U • ^^ ID

C (0 O

CO

Q) ,C ui -P

rSrS 0) M M O d in

-PrH G 0)

O U 6 (0 (0 ,Q

O (d -H 4J -P O (U -P

rH

OJ O M

•d rd 0) c ra (0 m 0)

•Q > -H

O rl rl U -P -P o •rH O O 0 (U

v cn (d cue u <U -H

rO -P

(d 0)

0)

> -H

CT r-l 0

rH 0) -H (0 rH -P W -H O

rH ^ "H -rl

O rH

EH

O

o VH iH W fM •)£ ->:

-)c •»:

it

48

CO

H

3 o

in

U n

tn

CM

o o o in VO VO

VO i-H

v>

</H

O O o

o in r-l

o o o % CN

CM

r

O O o «

§ i n

CN

to

</J-

</>

v>

CM

o o o

s o o o ^ VO

V)

o o o % o

o o ^ VO

v>

o o o ^ i n

VO VO

o o o ^ o

o 00

v>

o o o o o CO

</>

o o o ^ CM

CM CM

o o o ^ o

o 0^

o o o ^ o

o o\

o o o

K

o in CM

o o o ^ o

o i n

o o o ^ o

o CM

o o o ^ i n

CM CM

o o o •. o

o C«J

o o o % in

CM a

000

00 r-CM

^ ro

000

0

00

,

^ CO

v>

000

in VO VO

^ CO

vy

* *

ro

ro

</>

o o o ^

o o 00 ^ t-i

o o o

«•

o 00 03 ^ CM

</>

o o o ^

o CM r-i

K

ro </>

o o

t

00 t^

v>

o o o ^

o CO rH

^ rH

o o o *.

o CO CO

^ CM </>

o o o

V

o CM rH

^ fO to^

o o •

CO r-

<JH

o o o ^ CO

CN ro

o o o o o CO

CO-

o o o ^ in

vD CO

o^

ro vD •

r l CM

to-

O o o ^

in cr> CM

o o o «,

o CN r~-

to

o o o

K

o 00 t^

v>

o m

• 0^ rH

toH

o o O ^

in CT> CM

o o o o CN r

CO-

o o o •.

o 00 r-

v>

o in •

c rH

co]

* rH A

. < 0 o

rH O * rJ • 0 :i c. o > 0 c

OJ ro c/>

rH ^ ' r l O

Ui ^^ — 4J • c: • 10 r 1 0 r-l 0 , 0 .H ,D 0 , 0 -P .0 r.

* t;' CJ -r-l L'l -r-1 : - | t ; • ; v ••.- 4' y r{ . 0 - J l" ' ; ' Vi- '. 1 '^" rH ::[••' - - Or-' 0 . O H -J o 0 .A n n y.\

C - - ' l

v>

to 0)

0 -P B O 0 V u c o -H "-I

o 4 ' .O o

u 0

C 11 • r l rJ

I : CO

* •K * 0) U 73 '0 0 U Oi

ri o u u (d cn

o o o

in

O O O

in

o o o o o in

o o o C) o in

o o o

^ in in in

« in

o o o

^ o o o

H

o H

o o o ^

o o o

^ CN

o o o

« o o o

^ CM

o o o ^ o

o o

H

CM

o o o % o

o o

« b

CN

o o o % in

in in

o o o

^ o o o V

CM

o o o o o in

o o o

• k .

o o in

o o o

^ o o o *> CN

H

(0 -P 0

rQ O J^ ^

r-i (0

o

o

10 4J

A -rl U -P (d

CQ rH 0) U

u 10 tn

•^ \i lO

C (1) o >, 13 o 0) >

p.) <4H

A

U to

tn c o

•ri 4J Id •P 7i ft e. o u

H H < *

u 0

v*-(

<D cn to u 0)

rH A ro

r' •A • P CH

o S iw O

•X -K • > : *

•5c

49

multiplying his yearly working-interest barrels times

$3.00 per barrel. When payout status of the production

payment is reached, B's gross income is increased sub-

stantially^ reflecting the conversion from separate

properties into total properties.

Lease and well equipment is depreciated in the

same manner under the net and the economic-interest

methods (also in full accord with Federal income tax law).

Computation of the per-barrel provision is based on the

unit-of-production method by dividing the total leasehold

cost by B's total working-interest reserve ($2,500,000 ^

5,555,000 = $.45). Observe that B's working-interest

reserve is used as the denominator in this computation in

lieu of the total-barrel reserve of the property, a method

utilized by the equitable-lien method (Chapter III).

Under the net method lifting costs in full are

deducted from revenue as the expense is incurred each

year (2,000,000 barrels x $.40 per barrel). Leasehold

cost of $1,500,000 is amortized as depletion expense by

the unit-of-production method, utilizing B's working-

interest reserve in the same manner depreciation expense

is computed for both methods ($1,500,000 t- 5,555,000 =

$.27).

The economic-interest method, however, has an

interrelationship between lifting cost and depletion

50

expense. Estimated lifting costs attributable to C's

working interest during payout are capitalized as additional

leasehold cost at the date of acquisition. This capitalized

lifting cost is added to the allocated amount from the

initial cash payment, as demonstrated in the purchase

transaction. The total leasehold cost of $3,278,000 is

then amortized as depletion expense by the unit-of-

production method, also using B's working-interest barrels

($3,278,000 • 5,555,000 = $.59).

Interest expense which is incurred on the un

liquidated payment principal before payout status has

been reached is not deducted on the income statements

following net or economic-interest accounting methods.

Reasoning supporting this treatment follows the separate

property concept. Since the production payment is con

sidered to be a separate economic interest (under these

related methods) and since the gross income applicable

thereto is excluded from B's gross income for the two

methods' statement purposes, this expenditure must be 7

deducted on the income statement.

Balance Sheet Presentation

Leasehold cost and stockholder equity accounts

are presented as though they were extracted from B's

" Ibid., p. 189

>.0t*^

51

balance sheet in Table 9 for both the net and the economic-

interest methods. These two accounts are considered the

most significant items on B's balance sheet for comparative

purposes.

Observe, in Table 9, the significant variances

between leasehold cost for the net method and the leasehold

cost for the economic-interest method. The amount for the

net method runs about half that of the same amount for the

economic-interest method until the Oilola leases have

been fully depleted of all reserves (end of fifth year),

at which time the two accounts are equal. This difference,

of course, is the result of the capitalized lifting costs

under the economic-interest method.

B does not account for the production payment in

his balance sheet as a direct or an indirect liability

since he has not acquired and will not acquire the portion

of the property retained for the payment out of oil; he

is, therefore, not liable for the amounts of the lien on

the total properties. B is only liable, effectively, to

operate the property. Any liability, as previously stated

in Chapter II, attaches between parties A and C since A

has borrowed the principal from C with a guaranty that it

will be repaid by A, only if the leases prove to be 8

worthless before liquidation of the payment occurs.

^A. W. walker, Jr., Texas Law Review, XX, No. 3, 268-270.

HHBBkrr-

52

3

g

O

(1<

o Vi H

m

0)

o ro

CM

O O O

O O m r-i

vy

o o o o o in

r-i

to-

o o o o o in

vy

o o o CD o in

to-

o o o o o m

to-

o o o o o in

000

000,

». i n

c/v

o o o o o o

S S

in o O vO

% «. t m

«/>

000

565,

00

V5

000

665,

%

S13

.63

341

<A\

000

960, 00

0

- ;

000

000,

N

in

t/>

o o o o o o

145,

760,

^ ^ r-i ro

to-

000

905,

^ %"

t o 000

905,

V

a\ to-

.63

247

<yH

o O o

*. o CM 1 "

o o o

V

o CO o

^ rH <fy

o o o

^ o o o

K

i n tO-

o o o o o o ^ ^ O LT

00 ' 0 vO • ^

t >

o o o

^ i n <-rH

V

r-i • W l

o o o

^ i n ^ r-i

^ \D to-

ro VD

• ro i n r-l

COH

o o o

o r-CN

o o O

H

o ro CN

r-i t/>

o o o

V

o o o i n <A

o o o o o o CD O r . vj-ro ro

tO-

O O O

^ o CO vD

<A

o o o

«. o CO

i n to-

o o

• CM • *

rH

tOH

o o o

^

^1

''y ^

i n 1. n j n -oi r-l' ro

1 ~l 'A 'o!

O O O

^ O o o U I '7>

o o o

^ 1 o 1 • ^ '

ro

' y>

O o o

<. o '^ f 1

to-

o o o

^ o •> '' ro

^ i n to-

o m

• ro CM r-i

t / v l

o o o o o in

to-

o o o o o in

to-

o o o o o in

rH to-

o o o o o m

</>

o o o o o in

<n-

o o o

^ CO r r*

V

H

O o o

H

CO t ^ CM

^ fO

</>

o o o •.

a, t--CM

H

ro

1 1

VH

O O O

« CO

r-r-

« r-l

o o o

« CO r>-CN

^ ro

v>

O o o

V

CO Ov o

^ C l

o o o ^

o CO r-l

« r-i

</H

o o o *.

CO r-r-

^ r-t

o o o ^

00 i~-CM

V

ro CO-

O O O

«> 00 r-i CTi

o O o

H

o vO 0 0

^ C l coj

o o o

«w

00 > r-

V

H

o o o

V

00 t ^ CN

^ ro vy

o o o

^ o 0> i n

o o o

• I .

00 00 VO

K

CN vy\

a o o

s.

CO t~~ r-

K

r-i

a o o

N

00 t ^ CN

% ro vy

O o o

% i n CTi CN

o o o

• h

ro 00 <T<

.. CN vy]

o o o

H

o o o in

vy

o o o

c> o o

in

to-

o o o o o o *.

un to-

o o o o o o in vy

o o o O o o in to-

o o o o o o « K

in o Tl ' CM

in H ^ «.

in ro

to-

o o o

in 'O <o

% 00

vy

O o o

in to VO

• k

ro r-i vy

ro VO

• H •«t (*)

vy

o o o o o o ^ *. in o