Embed Size (px)

Citation preview

BRINKER INTERNATIONAL

Financial Analysis Draft 3

Josh Moore, Brad Bolte, James Hall, Tanner Swaringen, Tim Meyer

4/1/2014

Page | 1

Table of Contents

Liquidity Ratios ...................................................................................................................................................... 3

Introduction ....................................................................................................................................................... 3

Current Ratio ..................................................................................................................................................... 3

Quick Ratio ......................................................................................................................................................... 4

Inventory Turnover ........................................................................................................................................ 5

Inventory Days ................................................................................................................................................. 7

Accounts Receivable Turnover .................................................................................................................. 8

Accounts Receivable Days ........................................................................................................................... 9

Cash to Cash Cycle ...................................................................................................................................... 10

Working Capital Turnover ......................................................................................................................... 11

Conclusion ........................................................................................................................................................ 12

Profitability Ratios ............................................................................................................................................. 12

Introduction .................................................................................................................................................... 12

Sales Growth ................................................................................................................................................... 12

Gross Profit Margin ...................................................................................................................................... 13

Operating Profit Margin ............................................................................................................................. 14

Net Profit Margin ........................................................................................................................................... 16

Asset Turnover............................................................................................................................................... 17

Return on Assets (“ROA”) ........................................................................................................................ 18

Return on Equity (“ROE”) ......................................................................................................................... 19

Conclusion ........................................................................................................................................................ 20

Capital Structure Ratios .................................................................................................................................. 20

Introduction .................................................................................................................................................... 20

Debt to Equity ................................................................................................................................................ 21

Times Interest Earned ................................................................................................................................ 22

Altman’s Z-Score ........................................................................................................................................... 23

Conclusion .................................................................................................................................................... 25

Growth Rates....................................................................................................................................................... 25

Introduction .................................................................................................................................................... 25

Internal Growth Rate .................................................................................................................................. 25

Sustainable Growth Rate .......................................................................................................................... 26

Page | 2

Industry-Specific Ratios ................................................................................................................................. 27

Introduction .................................................................................................................................................... 27

Company-Owned Locations ..................................................................................................................... 28

Financial Analysis Conclusion ...................................................................................................................... 29

Financial Forecasting ....................................................................................................................................... 29

Income Statement ....................................................................................................................................... 30

.............................................................................................................................................................................. 32

.............................................................................................................................................................................. 33

Dividends Forecasting ................................................................................................................................ 34

Balance Sheet................................................................................................................................................. 34

Statement of Cash Flows .......................................................................................................................... 40

.............................................................................................................................................................................. 41

Restated Financial Statements ............................................................................................................... 42

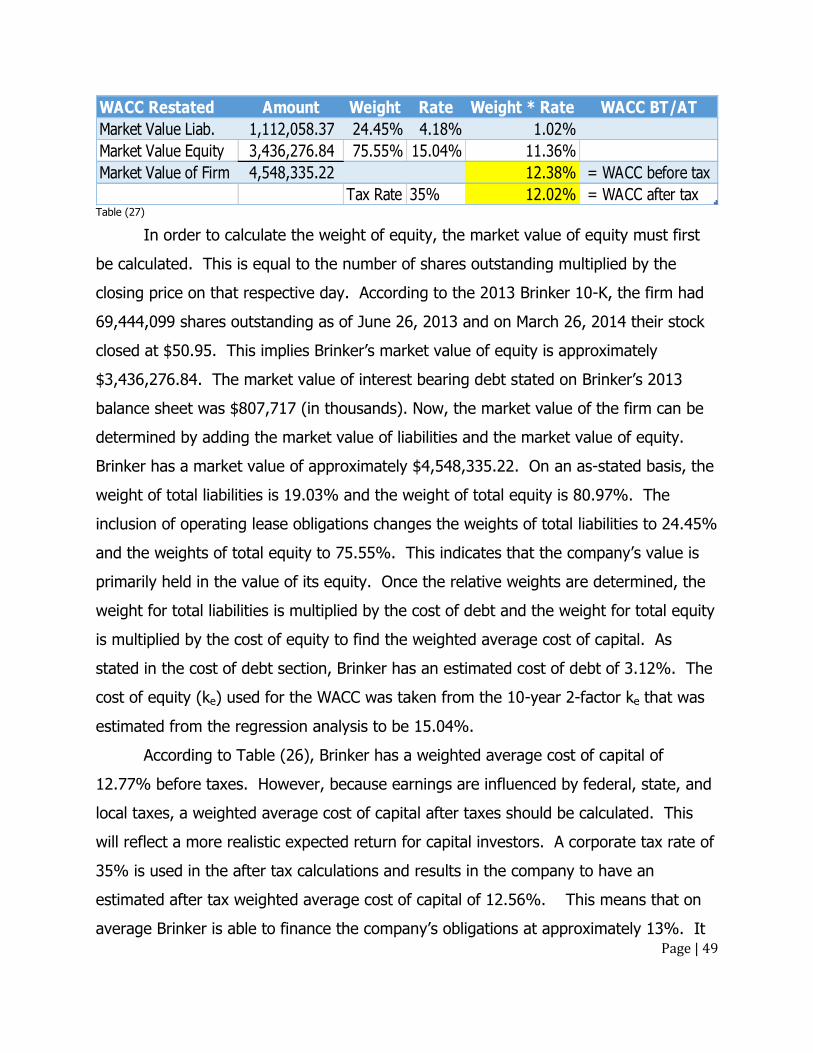

Cost of Capital Estimation ............................................................................................................................. 42

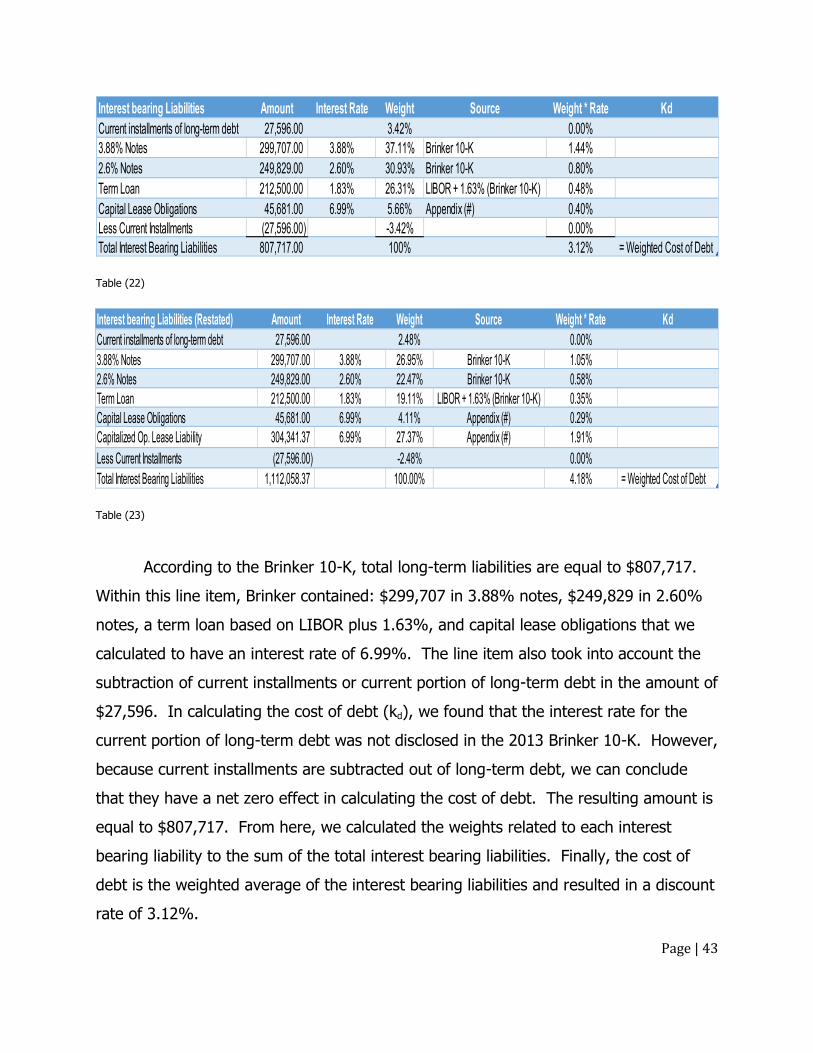

Cost of Debt .................................................................................................................................................... 42

Cost of Equity ................................................................................................................................................. 44

Backdoor Cost of Equity ............................................................................................................................ 47

Weighted Average Cost of Capital (WACC) ...................................................................................... 48

Appendix ................................................................................................................................................................ 53

Appendix (1) ........................................................................................................................................................ 53

Page | 3

Liquidity Ratios

Introduction Liquidity is the ability or quality of an asset that makes it easily convertible to

cash. In general, liquidity represents more safety to companies and investors alike

because it is easier for the holder of the asset to collect the cash value associated with

the asset. On a company balance sheet, marketable securities and accounts payable are

two examples of relatively liquid assets. In this analysis of liquidity ratios, we will looks

at the current and quick ratios, inventory turnover, inventory days, accounts receivable

turnover, accounts receivable days, cash to cash cycle, and working capital turnover.

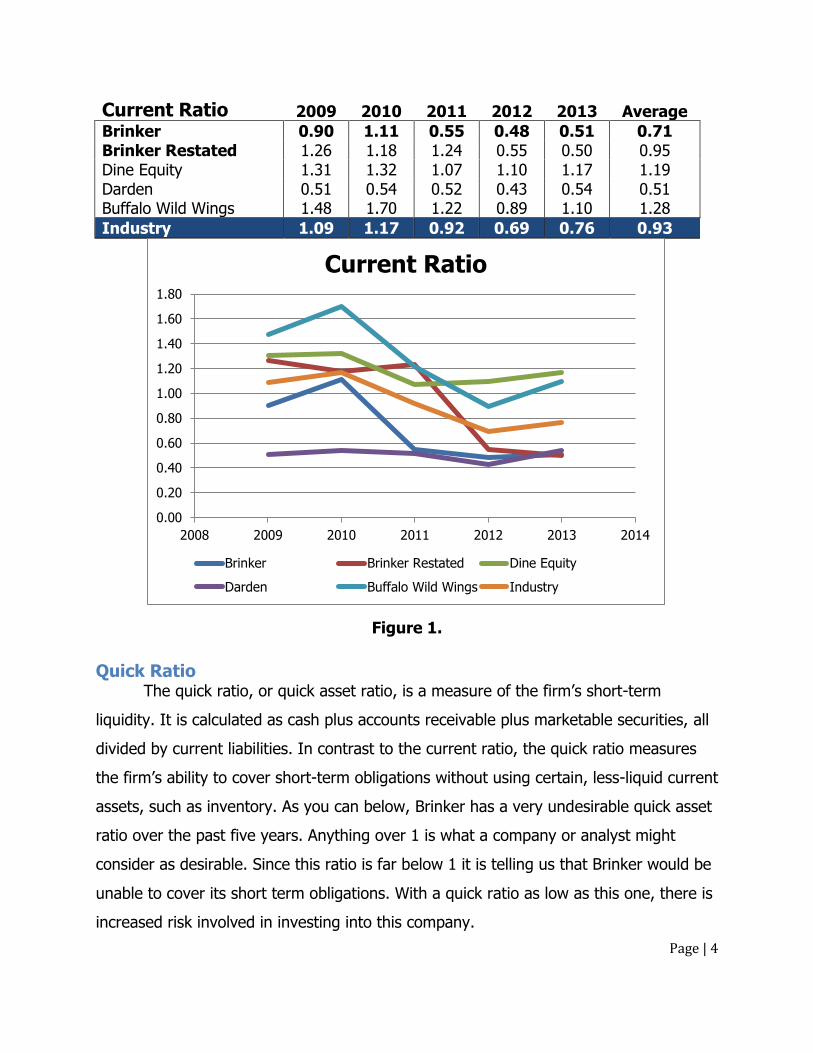

Current Ratio The current ratio, also known as the liquidity or cash asset ratio, is defined and

calculated as the current assets divided by current liabilities. It is used to measure the

firm’s ability to pay current liabilities with current assets. A higher number is generally

better. As evidenced below, Brinker’s yearly current ratio was higher than the average

of its peers until 2011, but it has since slumped below the mean. We believe this is due

primarily to the firm selling its On The Border segment in 2010. The segment’s efficient

financials helped bolster the holding company’s current ratio as a whole.

Page | 4

Current Ratio 2009 2010 2011 2012 2013 Average

Brinker 0.90 1.11 0.55 0.48 0.51 0.71 Brinker Restated 1.26 1.18 1.24 0.55 0.50 0.95 Dine Equity 1.31 1.32 1.07 1.10 1.17 1.19 Darden 0.51 0.54 0.52 0.43 0.54 0.51 Buffalo Wild Wings 1.48 1.70 1.22 0.89 1.10 1.28

Industry 1.09 1.17 0.92 0.69 0.76 0.93

Figure 1.

Quick Ratio The quick ratio, or quick asset ratio, is a measure of the firm’s short-term

liquidity. It is calculated as cash plus accounts receivable plus marketable securities, all

divided by current liabilities. In contrast to the current ratio, the quick ratio measures

the firm’s ability to cover short-term obligations without using certain, less-liquid current

assets, such as inventory. As you can below, Brinker has a very undesirable quick asset

ratio over the past five years. Anything over 1 is what a company or analyst might

consider as desirable. Since this ratio is far below 1 it is telling us that Brinker would be

unable to cover its short term obligations. With a quick ratio as low as this one, there is

increased risk involved in investing into this company.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2008 2009 2010 2011 2012 2013 2014

Current Ratio

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 5

Quick Ratio 2009 2010 2011 2012 2013 Average

Brinker 0.35 0.87 0.31 0.27 0.25 0.41 Brinker Restated 0.12 0.10 0.11 0.11 0.10 0.11 Dine Equity 0.72 0.76 0.68 0.72 0.88 0.75 Darden 0.06 0.24 0.11 0.08 0.12 0.12 Buffalo Wild Wings 0.83 0.93 0.64 0.36 0.52 0.66

Industry 0.42 0.58 0.37 0.31 0.37 0.41

Figure 2.

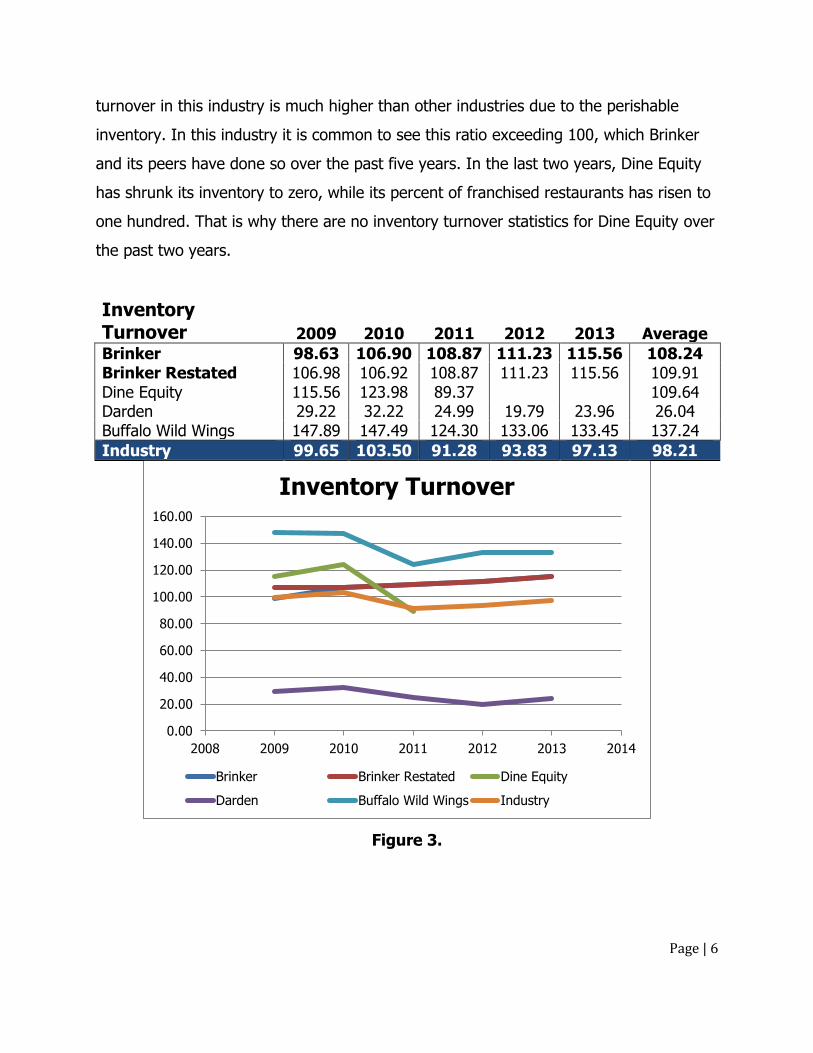

Inventory Turnover Inventory turnover represents the number of times each company’s inventory

currently on hand is sold during a specified period. In general, a higher number is

better, because the ratio is calculated as cost of goods sold divided by inventory. A

higher number is better because it implies a higher amount of sales, whereas a lower

number implies excess inventories. It should be noted that companies in this industry

have higher than average inventory turnover levels because their food is perishable,

and they move their inventory much faster than other companies in industries such as

retail or technology. Brinker has been slightly increasing its inventory turnover each

year for the past five years. When comparing Brinker to its peers it is maintaining a

relatively consistent pattern matching its peers. As stated previously, the inventory

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

2008 2009 2010 2011 2012 2013 2014

Quick Ratio

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 6

turnover in this industry is much higher than other industries due to the perishable

inventory. In this industry it is common to see this ratio exceeding 100, which Brinker

and its peers have done so over the past five years. In the last two years, Dine Equity

has shrunk its inventory to zero, while its percent of franchised restaurants has risen to

one hundred. That is why there are no inventory turnover statistics for Dine Equity over

the past two years.

Inventory Turnover 2009 2010 2011 2012 2013 Average

Brinker 98.63 106.90 108.87 111.23 115.56 108.24 Brinker Restated 106.98 106.92 108.87 111.23 115.56 109.91 Dine Equity 115.56 123.98 89.37 109.64 Darden 29.22 32.22 24.99 19.79 23.96 26.04 Buffalo Wild Wings 147.89 147.49 124.30 133.06 133.45 137.24

Industry 99.65 103.50 91.28 93.83 97.13 98.21

Figure 3.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

2008 2009 2010 2011 2012 2013 2014

Inventory Turnover

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 7

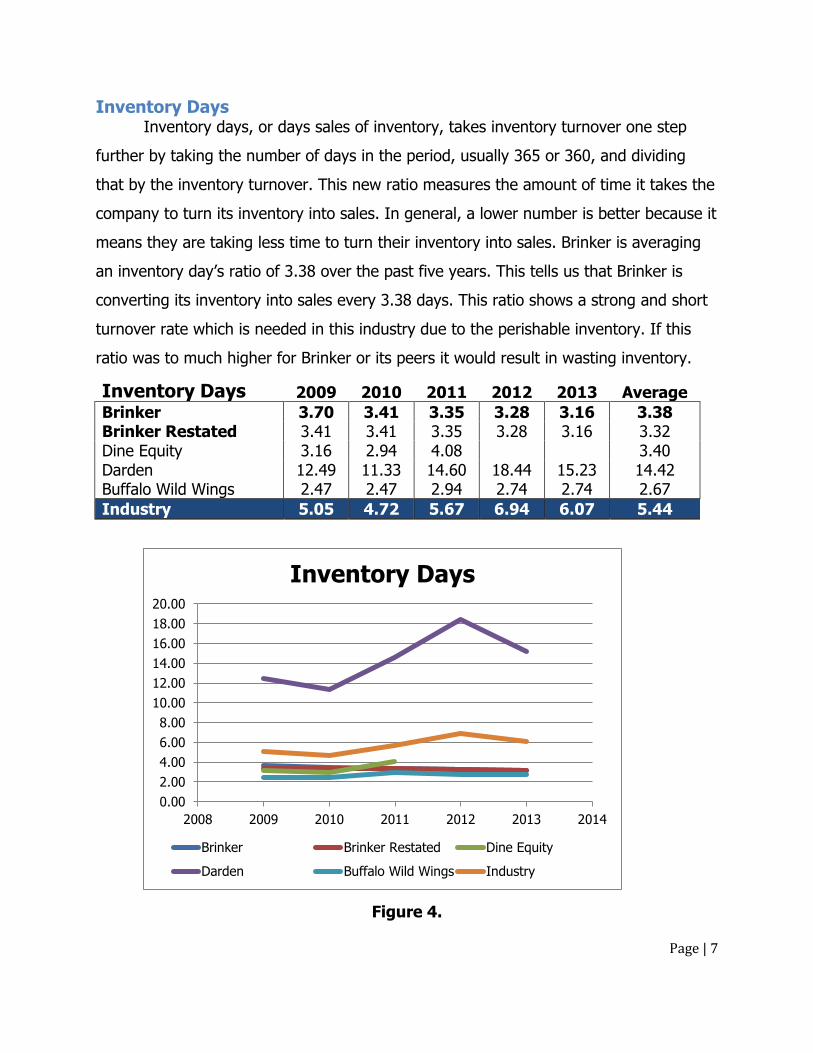

Inventory Days Inventory days, or days sales of inventory, takes inventory turnover one step

further by taking the number of days in the period, usually 365 or 360, and dividing

that by the inventory turnover. This new ratio measures the amount of time it takes the

company to turn its inventory into sales. In general, a lower number is better because it

means they are taking less time to turn their inventory into sales. Brinker is averaging

an inventory day’s ratio of 3.38 over the past five years. This tells us that Brinker is

converting its inventory into sales every 3.38 days. This ratio shows a strong and short

turnover rate which is needed in this industry due to the perishable inventory. If this

ratio was to much higher for Brinker or its peers it would result in wasting inventory.

Inventory Days 2009 2010 2011 2012 2013 Average

Brinker 3.70 3.41 3.35 3.28 3.16 3.38 Brinker Restated 3.41 3.41 3.35 3.28 3.16 3.32 Dine Equity 3.16 2.94 4.08 3.40 Darden 12.49 11.33 14.60 18.44 15.23 14.42 Buffalo Wild Wings 2.47 2.47 2.94 2.74 2.74 2.67

Industry 5.05 4.72 5.67 6.94 6.07 5.44

Figure 4.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2008 2009 2010 2011 2012 2013 2014

Inventory Days

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 8

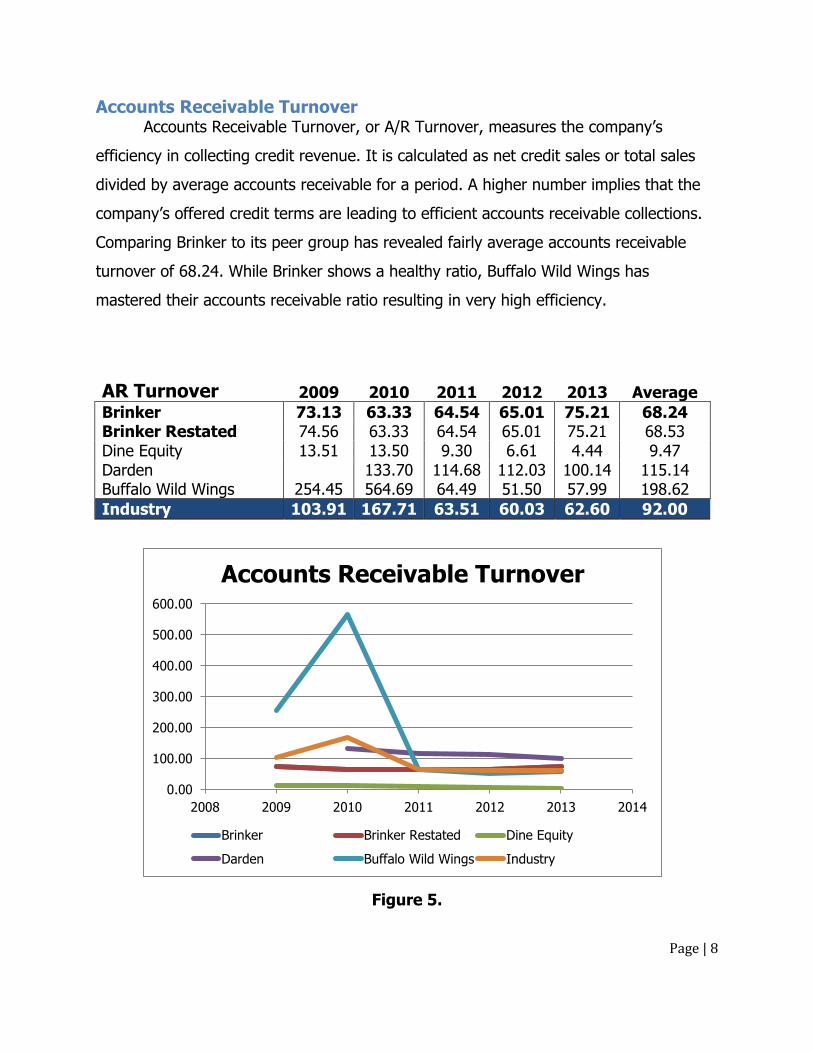

Accounts Receivable Turnover Accounts Receivable Turnover, or A/R Turnover, measures the company’s

efficiency in collecting credit revenue. It is calculated as net credit sales or total sales

divided by average accounts receivable for a period. A higher number implies that the

company’s offered credit terms are leading to efficient accounts receivable collections.

Comparing Brinker to its peer group has revealed fairly average accounts receivable

turnover of 68.24. While Brinker shows a healthy ratio, Buffalo Wild Wings has

mastered their accounts receivable ratio resulting in very high efficiency.

AR Turnover 2009 2010 2011 2012 2013 Average

Brinker 73.13 63.33 64.54 65.01 75.21 68.24 Brinker Restated 74.56 63.33 64.54 65.01 75.21 68.53 Dine Equity 13.51 13.50 9.30 6.61 4.44 9.47 Darden 133.70 114.68 112.03 100.14 115.14 Buffalo Wild Wings 254.45 564.69 64.49 51.50 57.99 198.62

Industry 103.91 167.71 63.51 60.03 62.60 92.00

Figure 5.

0.00

100.00

200.00

300.00

400.00

500.00

600.00

2008 2009 2010 2011 2012 2013 2014

Accounts Receivable Turnover

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 9

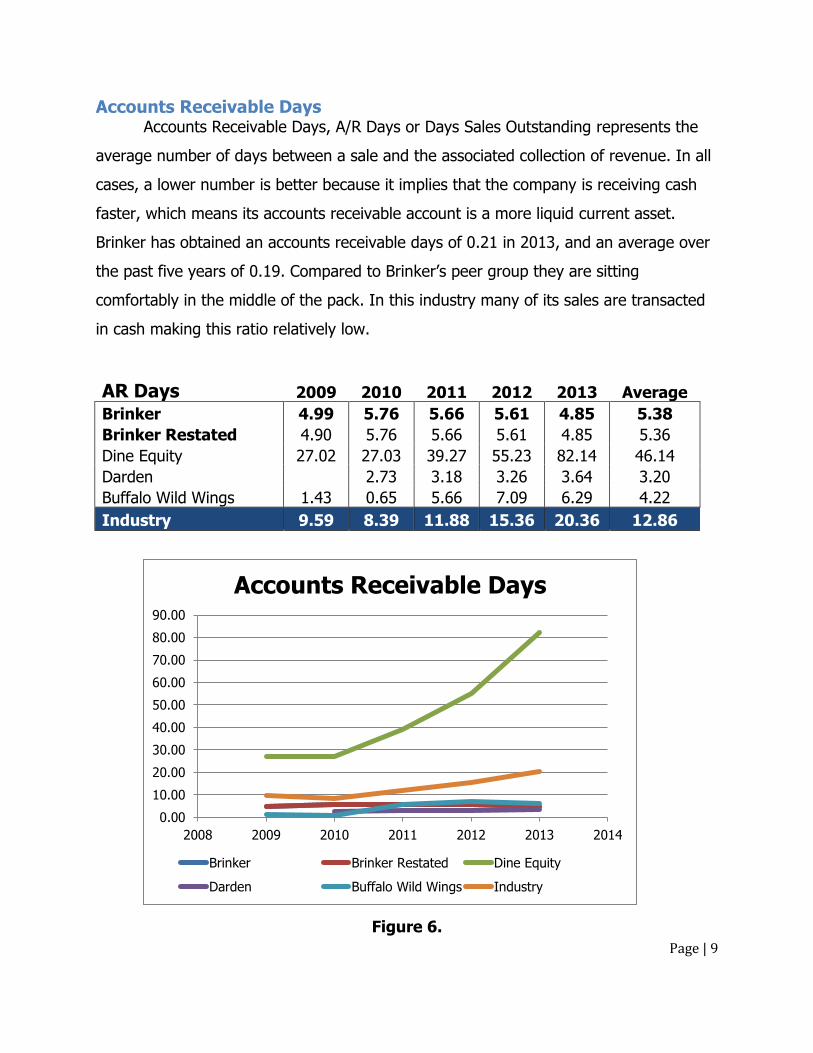

Accounts Receivable Days Accounts Receivable Days, A/R Days or Days Sales Outstanding represents the

average number of days between a sale and the associated collection of revenue. In all

cases, a lower number is better because it implies that the company is receiving cash

faster, which means its accounts receivable account is a more liquid current asset.

Brinker has obtained an accounts receivable days of 0.21 in 2013, and an average over

the past five years of 0.19. Compared to Brinker’s peer group they are sitting

comfortably in the middle of the pack. In this industry many of its sales are transacted

in cash making this ratio relatively low.

AR Days 2009 2010 2011 2012 2013 Average

Brinker 4.99 5.76 5.66 5.61 4.85 5.38

Brinker Restated 4.90 5.76 5.66 5.61 4.85 5.36

Dine Equity 27.02 27.03 39.27 55.23 82.14 46.14

Darden 2.73 3.18 3.26 3.64 3.20

Buffalo Wild Wings 1.43 0.65 5.66 7.09 6.29 4.22

Industry 9.59 8.39 11.88 15.36 20.36 12.86

Figure 6.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2008 2009 2010 2011 2012 2013 2014

Accounts Receivable Days

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 10

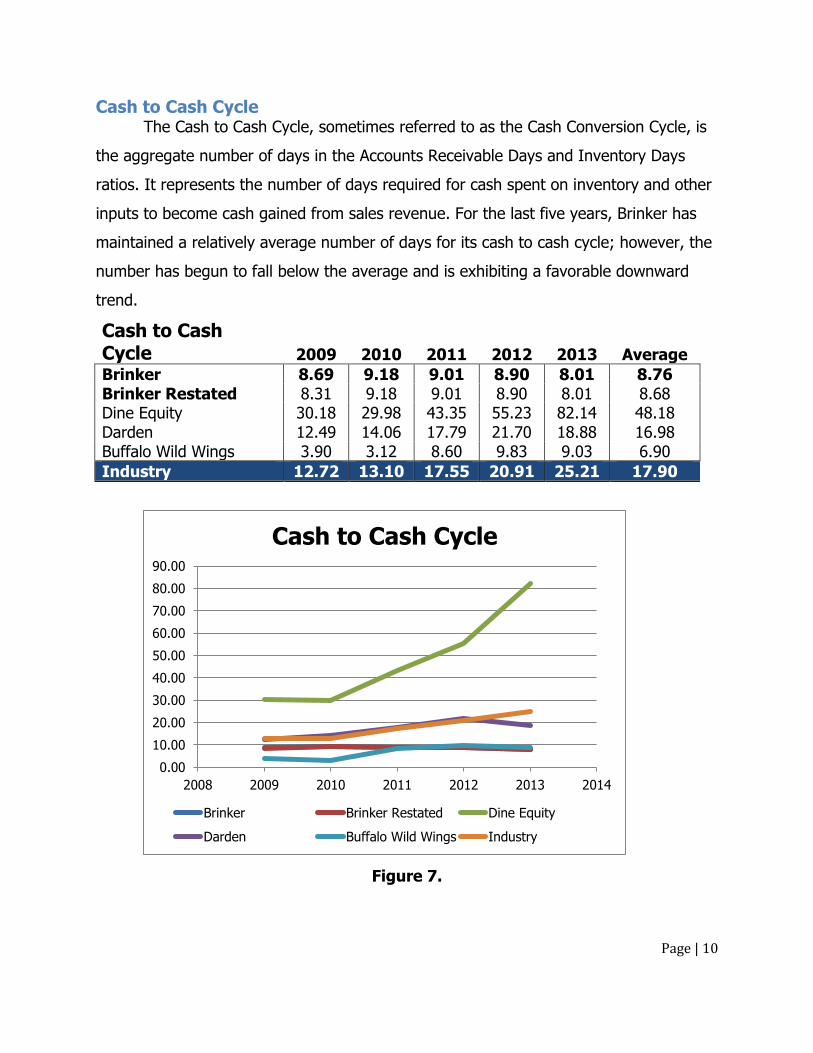

Cash to Cash Cycle The Cash to Cash Cycle, sometimes referred to as the Cash Conversion Cycle, is

the aggregate number of days in the Accounts Receivable Days and Inventory Days

ratios. It represents the number of days required for cash spent on inventory and other

inputs to become cash gained from sales revenue. For the last five years, Brinker has

maintained a relatively average number of days for its cash to cash cycle; however, the

number has begun to fall below the average and is exhibiting a favorable downward

trend.

Cash to Cash Cycle 2009 2010 2011 2012 2013 Average

Brinker 8.69 9.18 9.01 8.90 8.01 8.76 Brinker Restated 8.31 9.18 9.01 8.90 8.01 8.68 Dine Equity 30.18 29.98 43.35 55.23 82.14 48.18 Darden 12.49 14.06 17.79 21.70 18.88 16.98 Buffalo Wild Wings 3.90 3.12 8.60 9.83 9.03 6.90

Industry 12.72 13.10 17.55 20.91 25.21 17.90

Figure 7.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2008 2009 2010 2011 2012 2013 2014

Cash to Cash Cycle

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 11

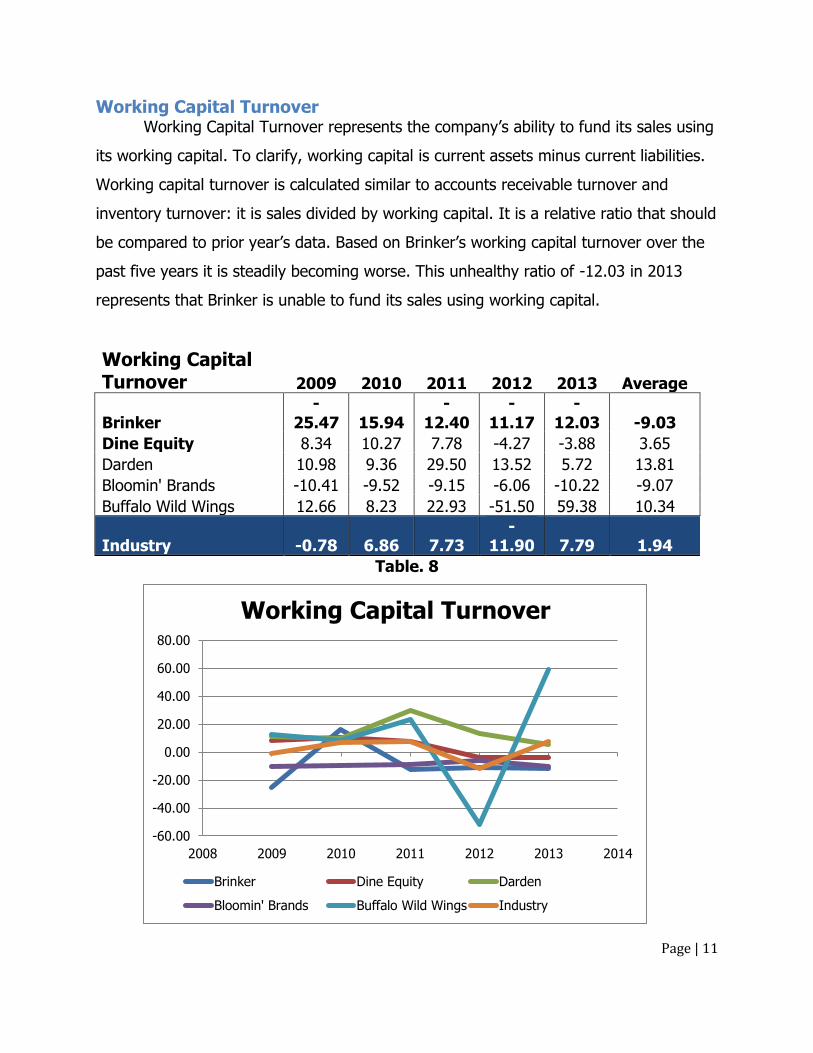

Working Capital Turnover Working Capital Turnover represents the company’s ability to fund its sales using

its working capital. To clarify, working capital is current assets minus current liabilities.

Working capital turnover is calculated similar to accounts receivable turnover and

inventory turnover: it is sales divided by working capital. It is a relative ratio that should

be compared to prior year’s data. Based on Brinker’s working capital turnover over the

past five years it is steadily becoming worse. This unhealthy ratio of -12.03 in 2013

represents that Brinker is unable to fund its sales using working capital.

Working Capital Turnover 2009 2010 2011 2012 2013 Average

Brinker -

25.47 15.94 -

12.40 -

11.17 -

12.03 -9.03

Dine Equity 8.34 10.27 7.78 -4.27 -3.88 3.65

Darden 10.98 9.36 29.50 13.52 5.72 13.81

Bloomin' Brands -10.41 -9.52 -9.15 -6.06 -10.22 -9.07

Buffalo Wild Wings 12.66 8.23 22.93 -51.50 59.38 10.34

Industry -0.78 6.86 7.73 -

11.90 7.79 1.94

Table. 8

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

2008 2009 2010 2011 2012 2013 2014

Working Capital Turnover

Brinker Dine Equity Darden

Bloomin' Brands Buffalo Wild Wings Industry

Page | 12

Figure 8.

Conclusion After rigorous analysis of Brinker’s liquidity ratios many of their ratios are

undesirable, representing an increased amount of risk involved in investing in this

company. Given these low liquidity ratios, representing Brinker we can come to the

conclusion that the margin for safety if significantly lower than the industry average.

We will discuss Brinker’s likelihood of going bankrupt with the Altman’s Z-score later in

this ration analysis section.

Profitability Ratios

Introduction Profitability ratios assess the extent to which a company’s revenues exceed

various measures of their cost. As a rule of thumb the higher this ratio is compared to

its competitors the better shape the company is in. Profitability ratios are the most

commonly analyzed ratios when an investor is doing a financial analysis. These ratios by

themselves may not make sense at certain times. It is important to have a good overall

understanding of the industry from where these ratios are being taken in order to

complete the entire story that this analysis will provide.

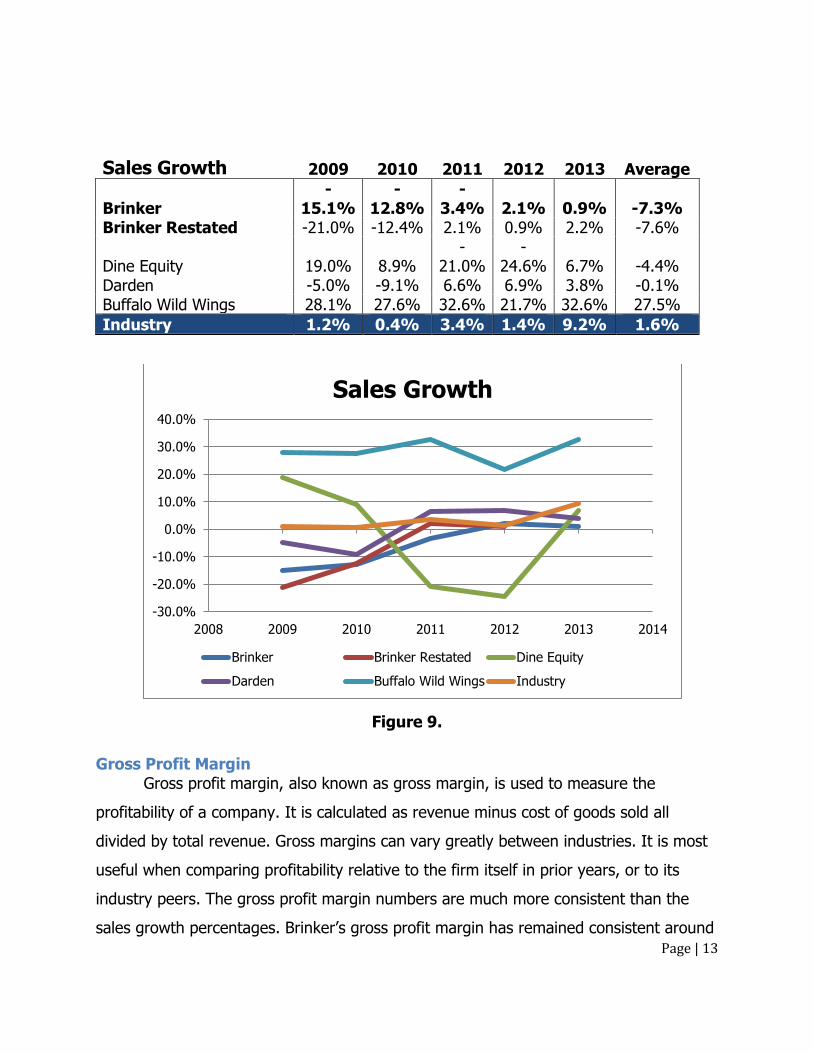

Sales Growth Sales Growth is the percentage change of sales from one year to the next. A

higher number is considered to be the most desirable figure for this ratio. While it does

not factor in the associated cost of revenue, it can be a useful statistic in measuring the

firms’ growth or accumulation of the market share compared to its peer. Brinker’s sales

decreased from 2009 to 2011, but have since displayed an upward trend. The sales

numbers are very volatile within this peer group, but Brinker’s numbers are generally

lower than the average.

Page | 13

Sales Growth 2009 2010 2011 2012 2013 Average

Brinker -

15.1% -

12.8% -

3.4% 2.1% 0.9% -7.3% Brinker Restated -21.0% -12.4% 2.1% 0.9% 2.2% -7.6%

Dine Equity 19.0% 8.9% -

21.0% -

24.6% 6.7% -4.4% Darden -5.0% -9.1% 6.6% 6.9% 3.8% -0.1% Buffalo Wild Wings 28.1% 27.6% 32.6% 21.7% 32.6% 27.5%

Industry 1.2% 0.4% 3.4% 1.4% 9.2% 1.6%

Figure 9.

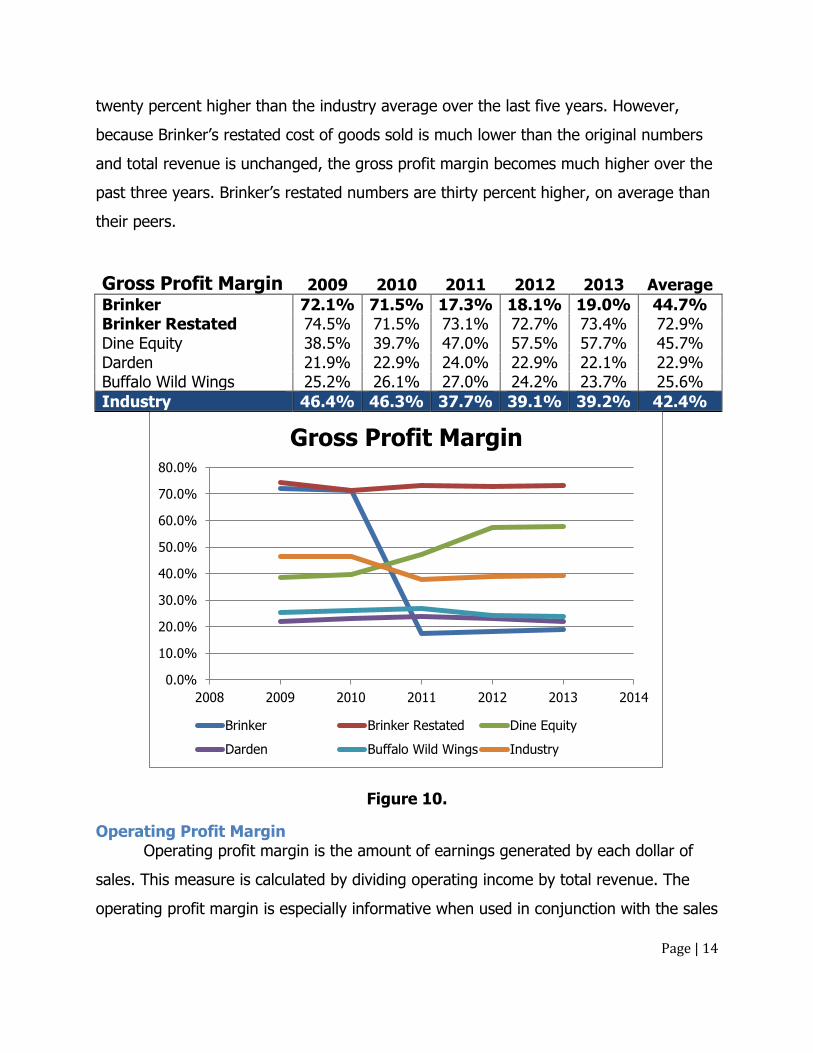

Gross Profit Margin Gross profit margin, also known as gross margin, is used to measure the

profitability of a company. It is calculated as revenue minus cost of goods sold all

divided by total revenue. Gross margins can vary greatly between industries. It is most

useful when comparing profitability relative to the firm itself in prior years, or to its

industry peers. The gross profit margin numbers are much more consistent than the

sales growth percentages. Brinker’s gross profit margin has remained consistent around

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2008 2009 2010 2011 2012 2013 2014

Sales Growth

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 14

twenty percent higher than the industry average over the last five years. However,

because Brinker’s restated cost of goods sold is much lower than the original numbers

and total revenue is unchanged, the gross profit margin becomes much higher over the

past three years. Brinker’s restated numbers are thirty percent higher, on average than

their peers.

Gross Profit Margin 2009 2010 2011 2012 2013 Average

Brinker 72.1% 71.5% 17.3% 18.1% 19.0% 44.7% Brinker Restated 74.5% 71.5% 73.1% 72.7% 73.4% 72.9% Dine Equity 38.5% 39.7% 47.0% 57.5% 57.7% 45.7% Darden 21.9% 22.9% 24.0% 22.9% 22.1% 22.9% Buffalo Wild Wings 25.2% 26.1% 27.0% 24.2% 23.7% 25.6%

Industry 46.4% 46.3% 37.7% 39.1% 39.2% 42.4%

Figure 10.

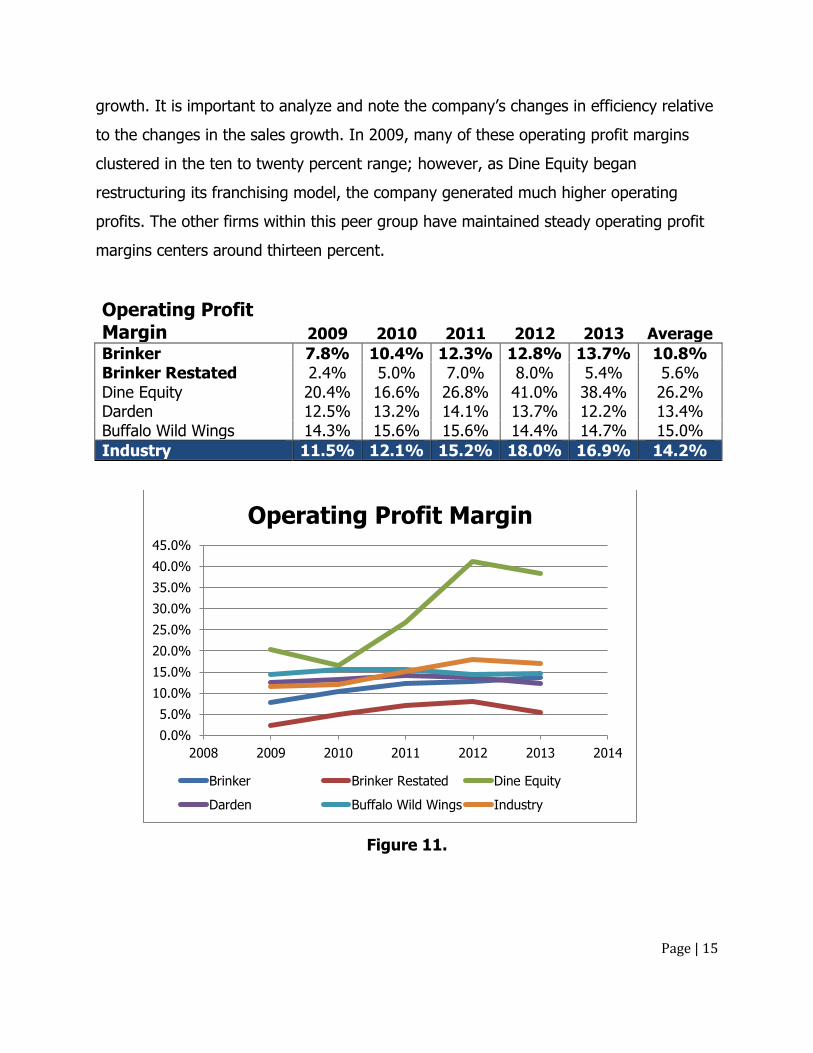

Operating Profit Margin Operating profit margin is the amount of earnings generated by each dollar of

sales. This measure is calculated by dividing operating income by total revenue. The

operating profit margin is especially informative when used in conjunction with the sales

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2008 2009 2010 2011 2012 2013 2014

Gross Profit Margin

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 15

growth. It is important to analyze and note the company’s changes in efficiency relative

to the changes in the sales growth. In 2009, many of these operating profit margins

clustered in the ten to twenty percent range; however, as Dine Equity began

restructuring its franchising model, the company generated much higher operating

profits. The other firms within this peer group have maintained steady operating profit

margins centers around thirteen percent.

Operating Profit Margin 2009 2010 2011 2012 2013 Average

Brinker 7.8% 10.4% 12.3% 12.8% 13.7% 10.8% Brinker Restated 2.4% 5.0% 7.0% 8.0% 5.4% 5.6% Dine Equity 20.4% 16.6% 26.8% 41.0% 38.4% 26.2% Darden 12.5% 13.2% 14.1% 13.7% 12.2% 13.4% Buffalo Wild Wings 14.3% 15.6% 15.6% 14.4% 14.7% 15.0%

Industry 11.5% 12.1% 15.2% 18.0% 16.9% 14.2%

Figure 11.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2008 2009 2010 2011 2012 2013 2014

Operating Profit Margin

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 16

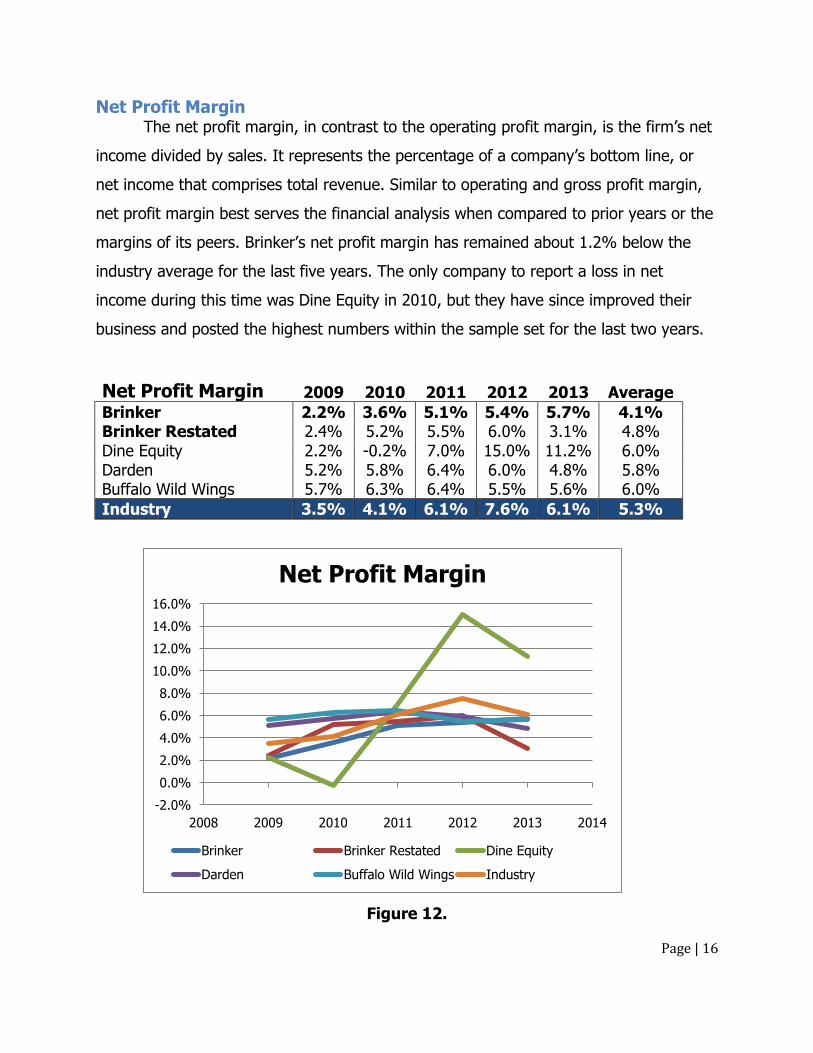

Net Profit Margin The net profit margin, in contrast to the operating profit margin, is the firm’s net

income divided by sales. It represents the percentage of a company’s bottom line, or

net income that comprises total revenue. Similar to operating and gross profit margin,

net profit margin best serves the financial analysis when compared to prior years or the

margins of its peers. Brinker’s net profit margin has remained about 1.2% below the

industry average for the last five years. The only company to report a loss in net

income during this time was Dine Equity in 2010, but they have since improved their

business and posted the highest numbers within the sample set for the last two years.

Net Profit Margin 2009 2010 2011 2012 2013 Average

Brinker 2.2% 3.6% 5.1% 5.4% 5.7% 4.1% Brinker Restated 2.4% 5.2% 5.5% 6.0% 3.1% 4.8% Dine Equity 2.2% -0.2% 7.0% 15.0% 11.2% 6.0% Darden 5.2% 5.8% 6.4% 6.0% 4.8% 5.8% Buffalo Wild Wings 5.7% 6.3% 6.4% 5.5% 5.6% 6.0%

Industry 3.5% 4.1% 6.1% 7.6% 6.1% 5.3%

Figure 12.

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2008 2009 2010 2011 2012 2013 2014

Net Profit Margin

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 17

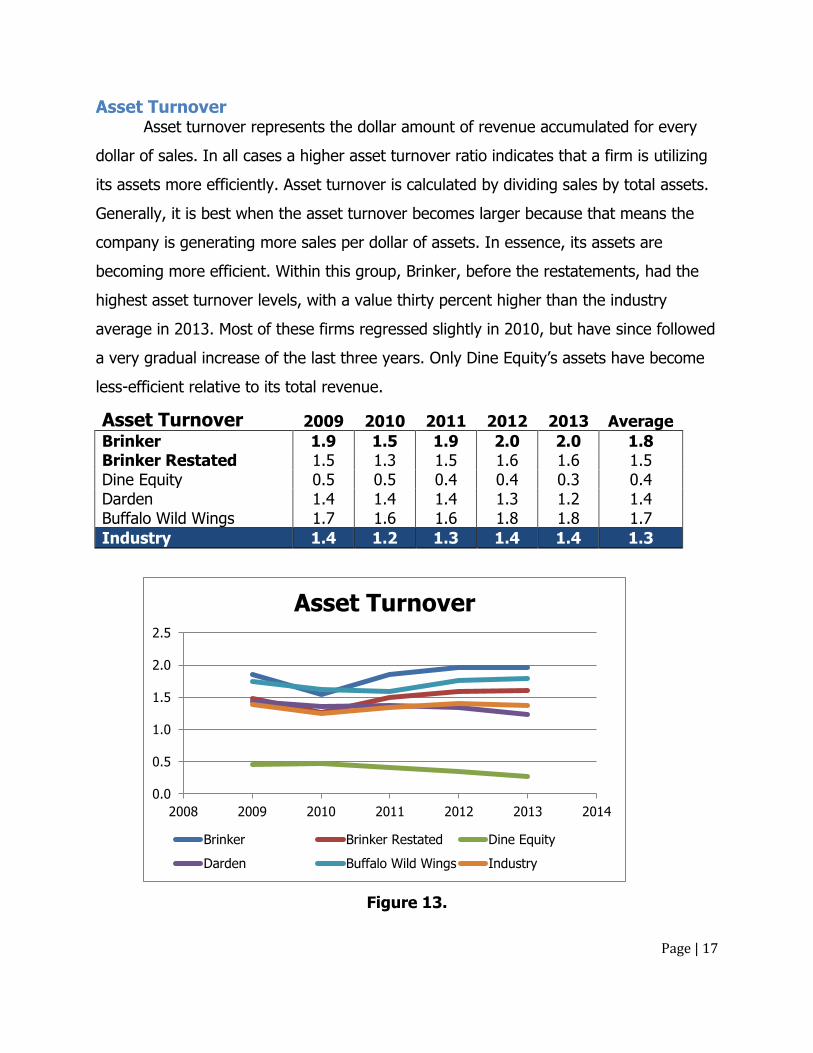

Asset Turnover Asset turnover represents the dollar amount of revenue accumulated for every

dollar of sales. In all cases a higher asset turnover ratio indicates that a firm is utilizing

its assets more efficiently. Asset turnover is calculated by dividing sales by total assets.

Generally, it is best when the asset turnover becomes larger because that means the

company is generating more sales per dollar of assets. In essence, its assets are

becoming more efficient. Within this group, Brinker, before the restatements, had the

highest asset turnover levels, with a value thirty percent higher than the industry

average in 2013. Most of these firms regressed slightly in 2010, but have since followed

a very gradual increase of the last three years. Only Dine Equity’s assets have become

less-efficient relative to its total revenue.

Asset Turnover 2009 2010 2011 2012 2013 Average

Brinker 1.9 1.5 1.9 2.0 2.0 1.8 Brinker Restated 1.5 1.3 1.5 1.6 1.6 1.5 Dine Equity 0.5 0.5 0.4 0.4 0.3 0.4 Darden 1.4 1.4 1.4 1.3 1.2 1.4 Buffalo Wild Wings 1.7 1.6 1.6 1.8 1.8 1.7

Industry 1.4 1.2 1.3 1.4 1.4 1.3

Figure 13.

0.0

0.5

1.0

1.5

2.0

2.5

2008 2009 2010 2011 2012 2013 2014

Asset Turnover

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 18

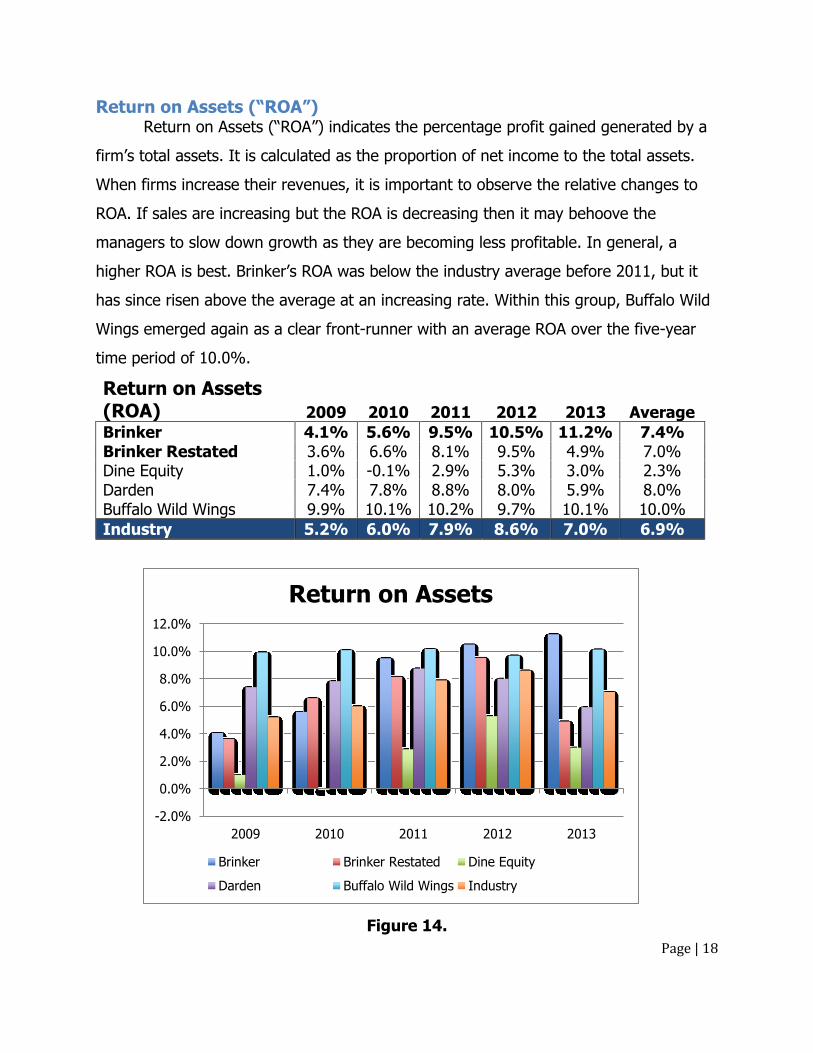

Return on Assets (“ROA”) Return on Assets (“ROA”) indicates the percentage profit gained generated by a

firm’s total assets. It is calculated as the proportion of net income to the total assets.

When firms increase their revenues, it is important to observe the relative changes to

ROA. If sales are increasing but the ROA is decreasing then it may behoove the

managers to slow down growth as they are becoming less profitable. In general, a

higher ROA is best. Brinker’s ROA was below the industry average before 2011, but it

has since risen above the average at an increasing rate. Within this group, Buffalo Wild

Wings emerged again as a clear front-runner with an average ROA over the five-year

time period of 10.0%.

Return on Assets (ROA) 2009 2010 2011 2012 2013 Average

Brinker 4.1% 5.6% 9.5% 10.5% 11.2% 7.4% Brinker Restated 3.6% 6.6% 8.1% 9.5% 4.9% 7.0% Dine Equity 1.0% -0.1% 2.9% 5.3% 3.0% 2.3% Darden 7.4% 7.8% 8.8% 8.0% 5.9% 8.0% Buffalo Wild Wings 9.9% 10.1% 10.2% 9.7% 10.1% 10.0%

Industry 5.2% 6.0% 7.9% 8.6% 7.0% 6.9%

Figure 14.

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2009 2010 2011 2012 2013

Return on Assets

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 19

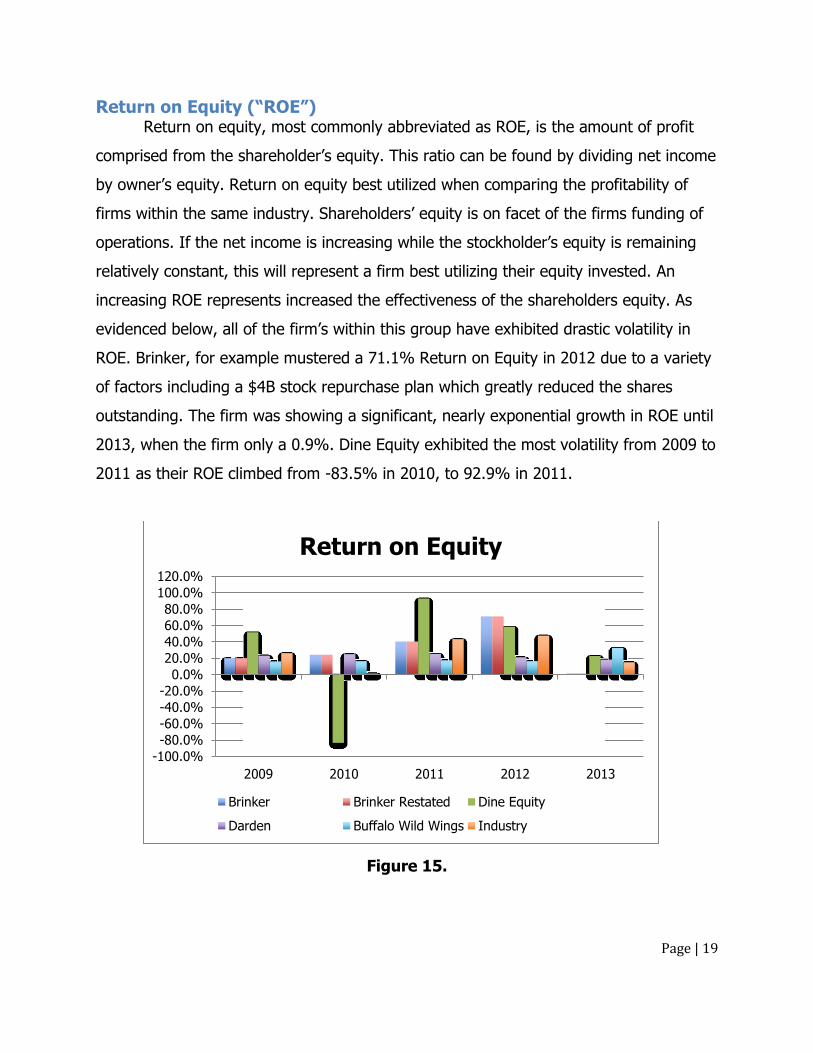

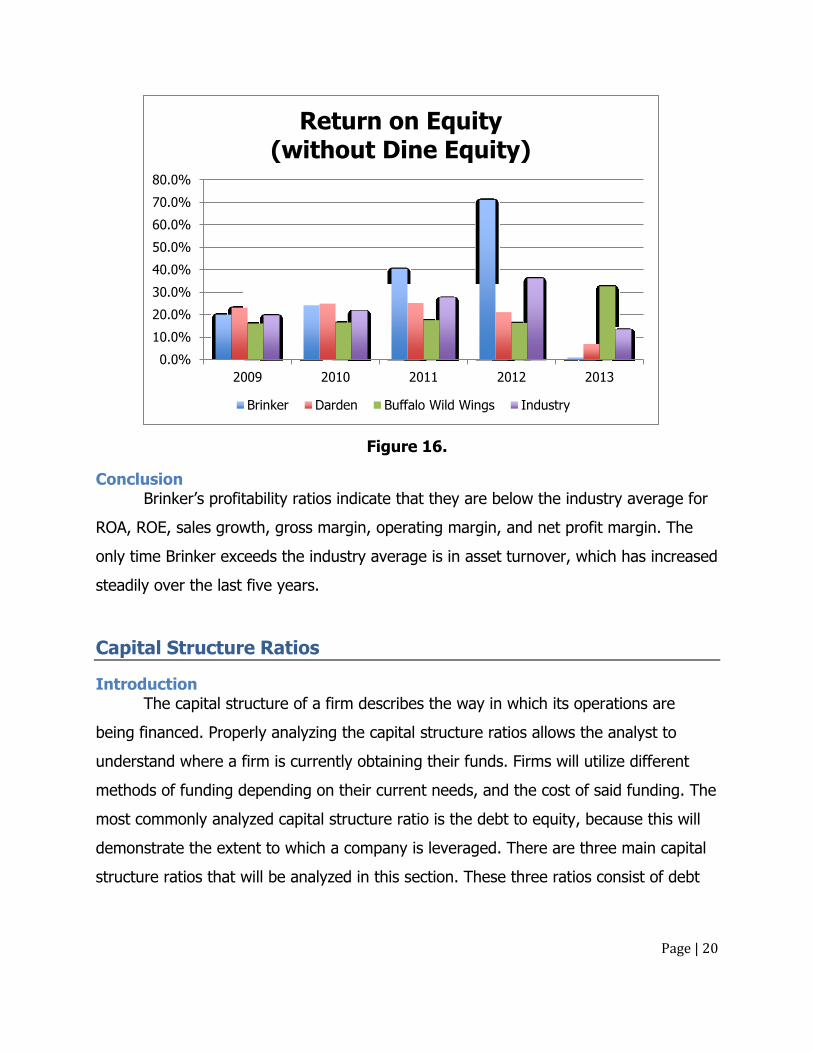

Return on Equity (“ROE”) Return on equity, most commonly abbreviated as ROE, is the amount of profit

comprised from the shareholder’s equity. This ratio can be found by dividing net income

by owner’s equity. Return on equity best utilized when comparing the profitability of

firms within the same industry. Shareholders’ equity is on facet of the firms funding of

operations. If the net income is increasing while the stockholder’s equity is remaining

relatively constant, this will represent a firm best utilizing their equity invested. An

increasing ROE represents increased the effectiveness of the shareholders equity. As

evidenced below, all of the firm’s within this group have exhibited drastic volatility in

ROE. Brinker, for example mustered a 71.1% Return on Equity in 2012 due to a variety

of factors including a $4B stock repurchase plan which greatly reduced the shares

outstanding. The firm was showing a significant, nearly exponential growth in ROE until

2013, when the firm only a 0.9%. Dine Equity exhibited the most volatility from 2009 to

2011 as their ROE climbed from -83.5% in 2010, to 92.9% in 2011.

Figure 15.

-100.0%

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2009 2010 2011 2012 2013

Return on Equity

Brinker Brinker Restated Dine Equity

Darden Buffalo Wild Wings Industry

Page | 20

Figure 16.

Conclusion Brinker’s profitability ratios indicate that they are below the industry average for

ROA, ROE, sales growth, gross margin, operating margin, and net profit margin. The

only time Brinker exceeds the industry average is in asset turnover, which has increased

steadily over the last five years.

Capital Structure Ratios

Introduction The capital structure of a firm describes the way in which its operations are

being financed. Properly analyzing the capital structure ratios allows the analyst to

understand where a firm is currently obtaining their funds. Firms will utilize different

methods of funding depending on their current needs, and the cost of said funding. The

most commonly analyzed capital structure ratio is the debt to equity, because this will

demonstrate the extent to which a company is leveraged. There are three main capital

structure ratios that will be analyzed in this section. These three ratios consist of debt

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2009 2010 2011 2012 2013

Return on Equity (without Dine Equity)

Brinker Darden Buffalo Wild Wings Industry

Page | 21

to equity, times interest earned, and the Altman’s Z-score, which will be discussed in

further detail below.

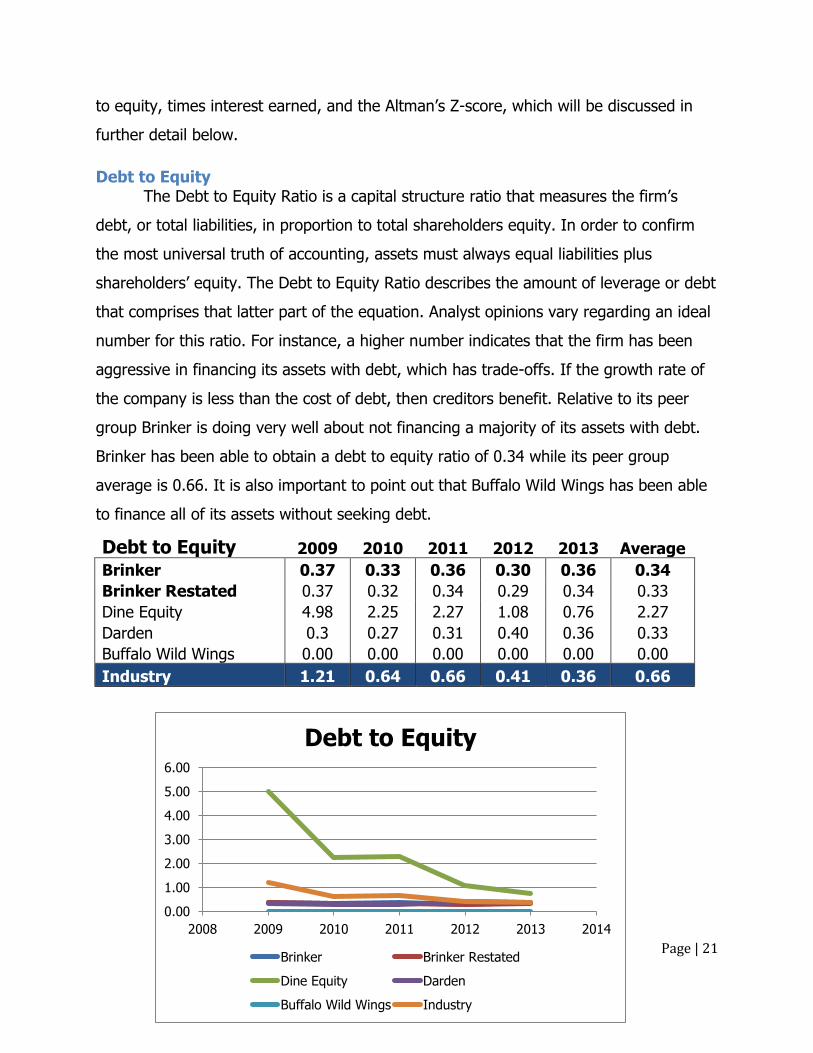

Debt to Equity The Debt to Equity Ratio is a capital structure ratio that measures the firm’s

debt, or total liabilities, in proportion to total shareholders equity. In order to confirm

the most universal truth of accounting, assets must always equal liabilities plus

shareholders’ equity. The Debt to Equity Ratio describes the amount of leverage or debt

that comprises that latter part of the equation. Analyst opinions vary regarding an ideal

number for this ratio. For instance, a higher number indicates that the firm has been

aggressive in financing its assets with debt, which has trade-offs. If the growth rate of

the company is less than the cost of debt, then creditors benefit. Relative to its peer

group Brinker is doing very well about not financing a majority of its assets with debt.

Brinker has been able to obtain a debt to equity ratio of 0.34 while its peer group

average is 0.66. It is also important to point out that Buffalo Wild Wings has been able

to finance all of its assets without seeking debt.

Debt to Equity 2009 2010 2011 2012 2013 Average

Brinker 0.37 0.33 0.36 0.30 0.36 0.34

Brinker Restated 0.37 0.32 0.34 0.29 0.34 0.33

Dine Equity 4.98 2.25 2.27 1.08 0.76 2.27

Darden 0.3 0.27 0.31 0.40 0.36 0.33

Buffalo Wild Wings 0.00 0.00 0.00 0.00 0.00 0.00

Industry 1.21 0.64 0.66 0.41 0.36 0.66

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2008 2009 2010 2011 2012 2013 2014

Debt to Equity

Brinker Brinker Restated

Dine Equity Darden

Buffalo Wild Wings Industry

Page | 22

Figure 17.

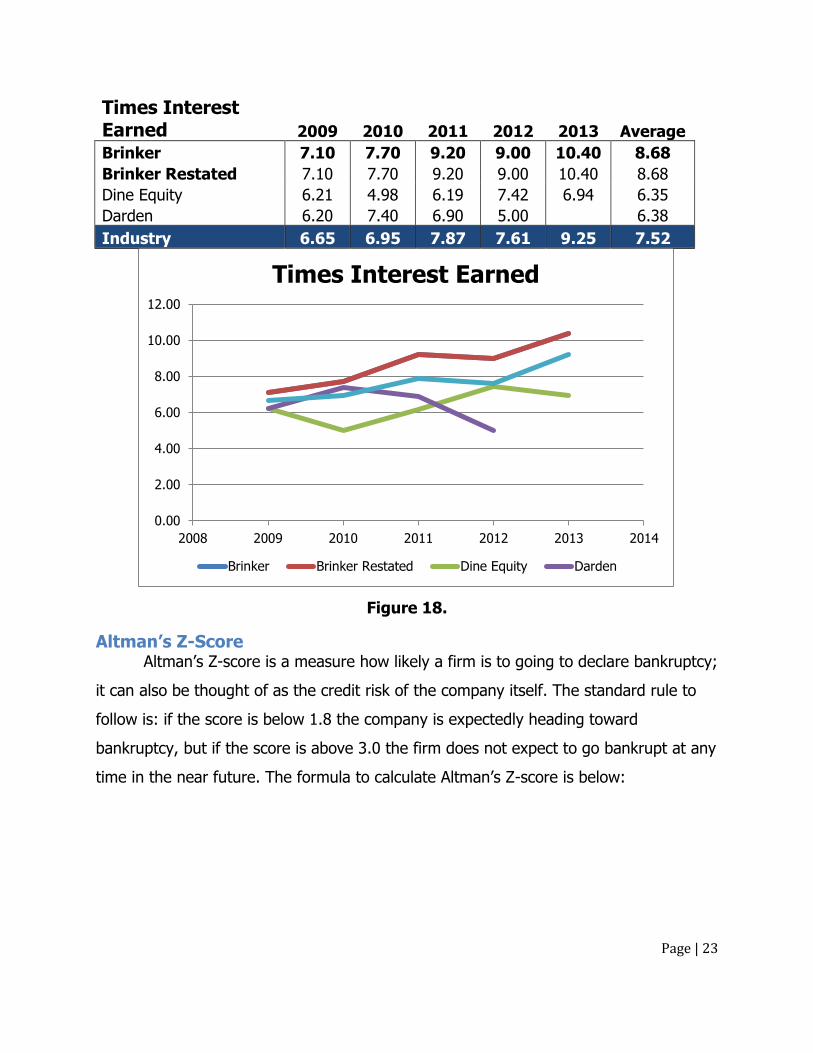

Times Interest Earned Times interest earned is useful when analyzing the proportion of interest that

comprises operating income. It is the number of times a company can pay its interest

expenses out of the earnings before interest and taxes account. Anything below one is

considered to be undesirable and risky to potential investors. This ratio is attained by

dividing earnings before interest and taxed by total interest payable. Over the past

three years, all of the firms in this group, except Darden, have exhibited a strong

upward trend in times interest earned. Their total revenues are beginning to cover a

larger amount of the interest owed on outstanding debt. Because Buffalo Wild Wings is

debt-free, it does not need to pay interest on any debt. Thus, the times interest earned

ratio is undefined.

Page | 23

Times Interest Earned 2009 2010 2011 2012 2013 Average

Brinker 7.10 7.70 9.20 9.00 10.40 8.68

Brinker Restated 7.10 7.70 9.20 9.00 10.40 8.68

Dine Equity 6.21 4.98 6.19 7.42 6.94 6.35

Darden 6.20 7.40 6.90 5.00 6.38

Industry 6.65 6.95 7.87 7.61 9.25 7.52

Figure 18.

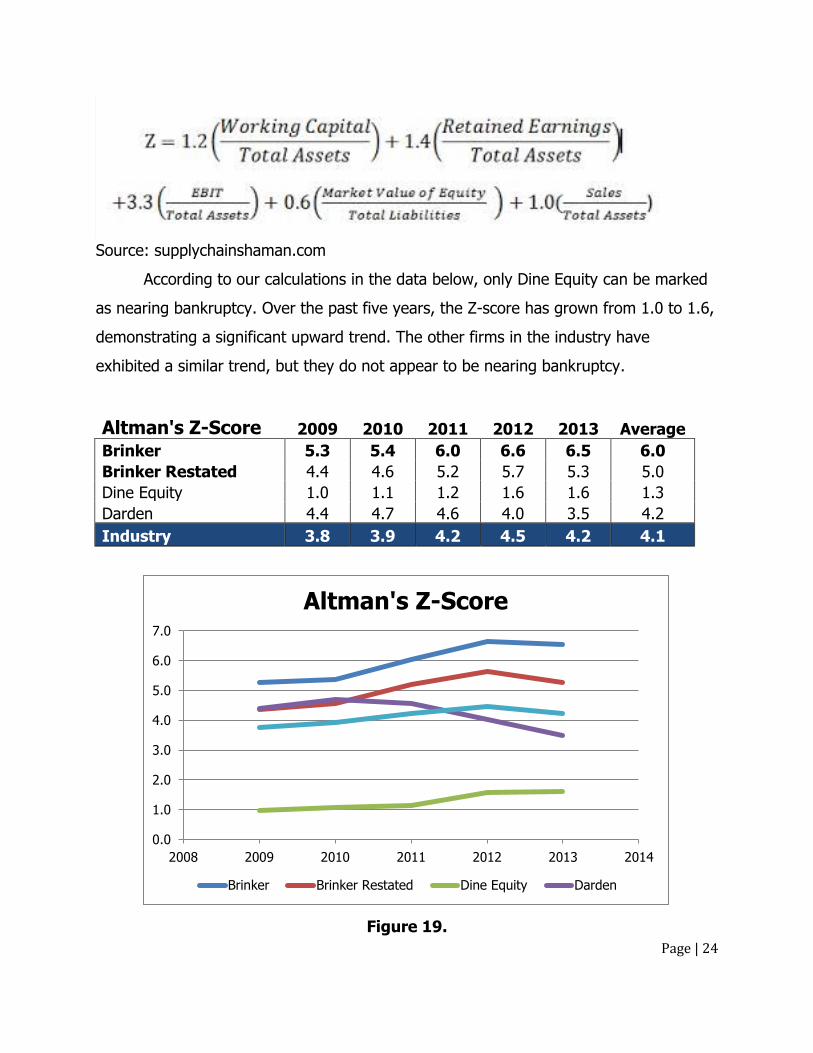

Altman’s Z-Score Altman’s Z-score is a measure how likely a firm is to going to declare bankruptcy;

it can also be thought of as the credit risk of the company itself. The standard rule to

follow is: if the score is below 1.8 the company is expectedly heading toward

bankruptcy, but if the score is above 3.0 the firm does not expect to go bankrupt at any

time in the near future. The formula to calculate Altman’s Z-score is below:

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2008 2009 2010 2011 2012 2013 2014

Times Interest Earned

Brinker Brinker Restated Dine Equity Darden

Page | 24

Source: supplychainshaman.com

According to our calculations in the data below, only Dine Equity can be marked

as nearing bankruptcy. Over the past five years, the Z-score has grown from 1.0 to 1.6,

demonstrating a significant upward trend. The other firms in the industry have

exhibited a similar trend, but they do not appear to be nearing bankruptcy.

Altman's Z-Score 2009 2010 2011 2012 2013 Average

Brinker 5.3 5.4 6.0 6.6 6.5 6.0

Brinker Restated 4.4 4.6 5.2 5.7 5.3 5.0

Dine Equity 1.0 1.1 1.2 1.6 1.6 1.3

Darden 4.4 4.7 4.6 4.0 3.5 4.2

Industry 3.8 3.9 4.2 4.5 4.2 4.1

Figure 19.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2008 2009 2010 2011 2012 2013 2014

Altman's Z-Score

Brinker Brinker Restated Dine Equity Darden

Page | 25

Conclusion

As evidenced by the debt to equity ratio, the percentage of invested capital

allocated to debt is generally lower in this industry, with the exception of Dine Equity,

whom has seven times the amount of debt as they do equity, which may be negative

affects their bankruptcy risk in the Altman’s Z-score. For the most part, Brinker’s capital

structure numbers are on par with many of the statistics of the casual dining sector as a

whole, despite the volatility within this small peer group.

Growth Rates

Introduction In this section, there are two relevant growth rates to be analyzed: internal

growth rate and sustainable growth rate. The sustainable growth rate measures the

level of growth attainable while receiving no outside additional funding. The internal

growth rate is used to assess the ability to which a firm can grow by keeping its capital

structure constant.

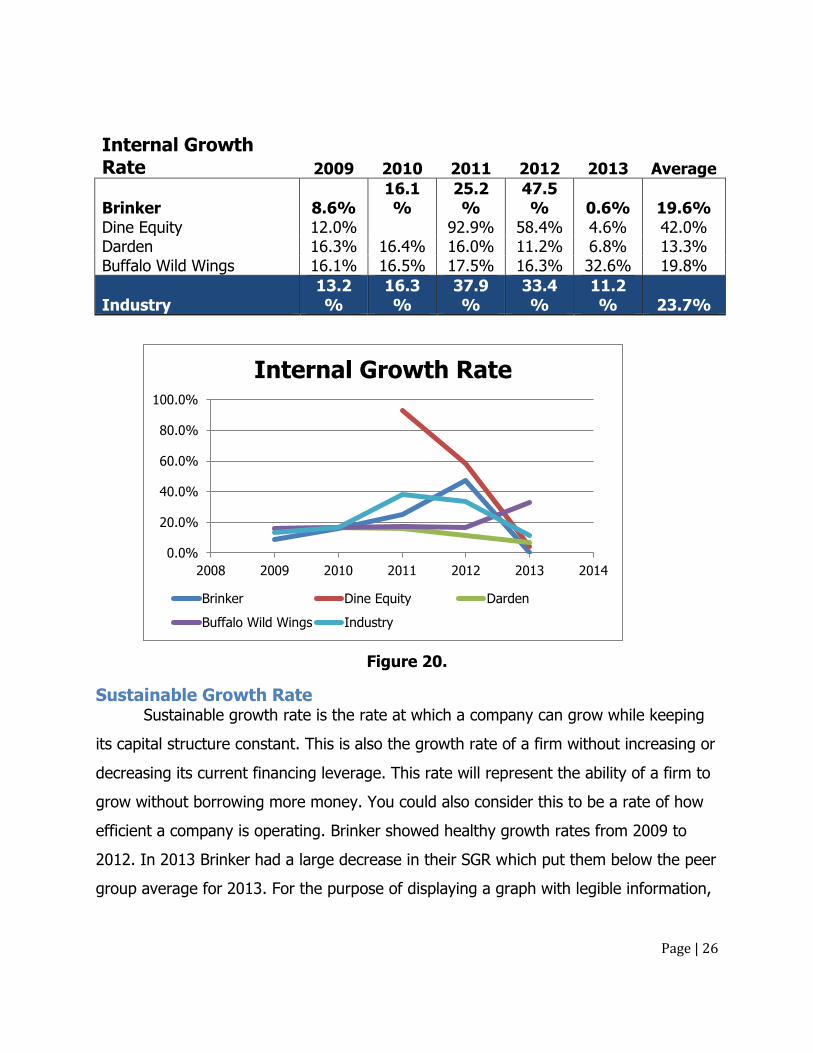

Internal Growth Rate Internal growth rate is the level of a firm’s growth rate without obtaining

financing from outside sources. This ratio is very important for smaller firms and startup

firms. If a firm is able to obtain a healthy internal growth rate is represents the ability of

a company to grow with only its available assets. After analyzing Brinker’s IGR over the

past five years, there has not been a noticeable trend associated with this information.

Brinker’s five year average is consistent with its peer group average, which shows it is

similar to the rest of its competitors.

Page | 26

Internal Growth Rate 2009 2010 2011 2012 2013 Average

Brinker 8.6% 16.1%

25.2%

47.5% 0.6% 19.6%

Dine Equity 12.0% 92.9% 58.4% 4.6% 42.0% Darden 16.3% 16.4% 16.0% 11.2% 6.8% 13.3% Buffalo Wild Wings 16.1% 16.5% 17.5% 16.3% 32.6% 19.8%

Industry 13.2%

16.3%

37.9%

33.4%

11.2% 23.7%

Figure 20.

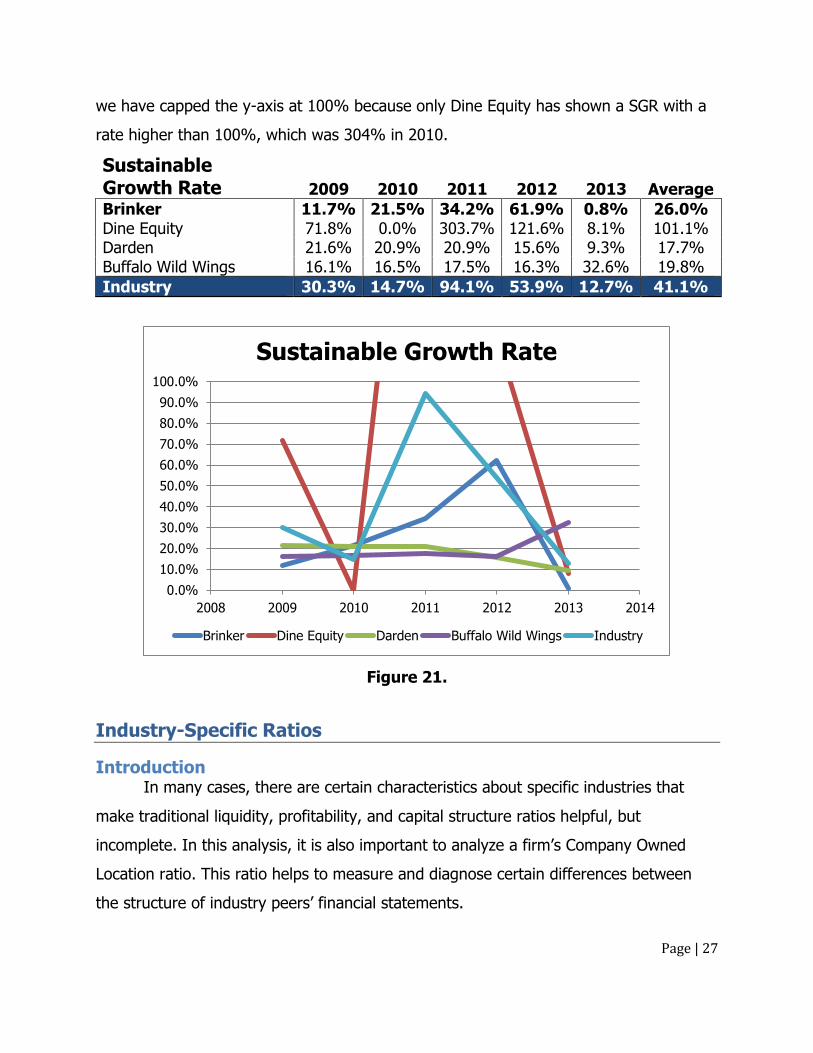

Sustainable Growth Rate Sustainable growth rate is the rate at which a company can grow while keeping

its capital structure constant. This is also the growth rate of a firm without increasing or

decreasing its current financing leverage. This rate will represent the ability of a firm to

grow without borrowing more money. You could also consider this to be a rate of how

efficient a company is operating. Brinker showed healthy growth rates from 2009 to

2012. In 2013 Brinker had a large decrease in their SGR which put them below the peer

group average for 2013. For the purpose of displaying a graph with legible information,

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2008 2009 2010 2011 2012 2013 2014

Internal Growth Rate

Brinker Dine Equity Darden

Buffalo Wild Wings Industry

Page | 27

we have capped the y-axis at 100% because only Dine Equity has shown a SGR with a

rate higher than 100%, which was 304% in 2010.

Sustainable Growth Rate 2009 2010 2011 2012 2013 Average

Brinker 11.7% 21.5% 34.2% 61.9% 0.8% 26.0% Dine Equity 71.8% 0.0% 303.7% 121.6% 8.1% 101.1% Darden 21.6% 20.9% 20.9% 15.6% 9.3% 17.7% Buffalo Wild Wings 16.1% 16.5% 17.5% 16.3% 32.6% 19.8%

Industry 30.3% 14.7% 94.1% 53.9% 12.7% 41.1%

Figure 21.

Industry-Specific Ratios

Introduction In many cases, there are certain characteristics about specific industries that

make traditional liquidity, profitability, and capital structure ratios helpful, but

incomplete. In this analysis, it is also important to analyze a firm’s Company Owned

Location ratio. This ratio helps to measure and diagnose certain differences between

the structure of industry peers’ financial statements.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2008 2009 2010 2011 2012 2013 2014

Sustainable Growth Rate

Brinker Dine Equity Darden Buffalo Wild Wings Industry

Page | 28

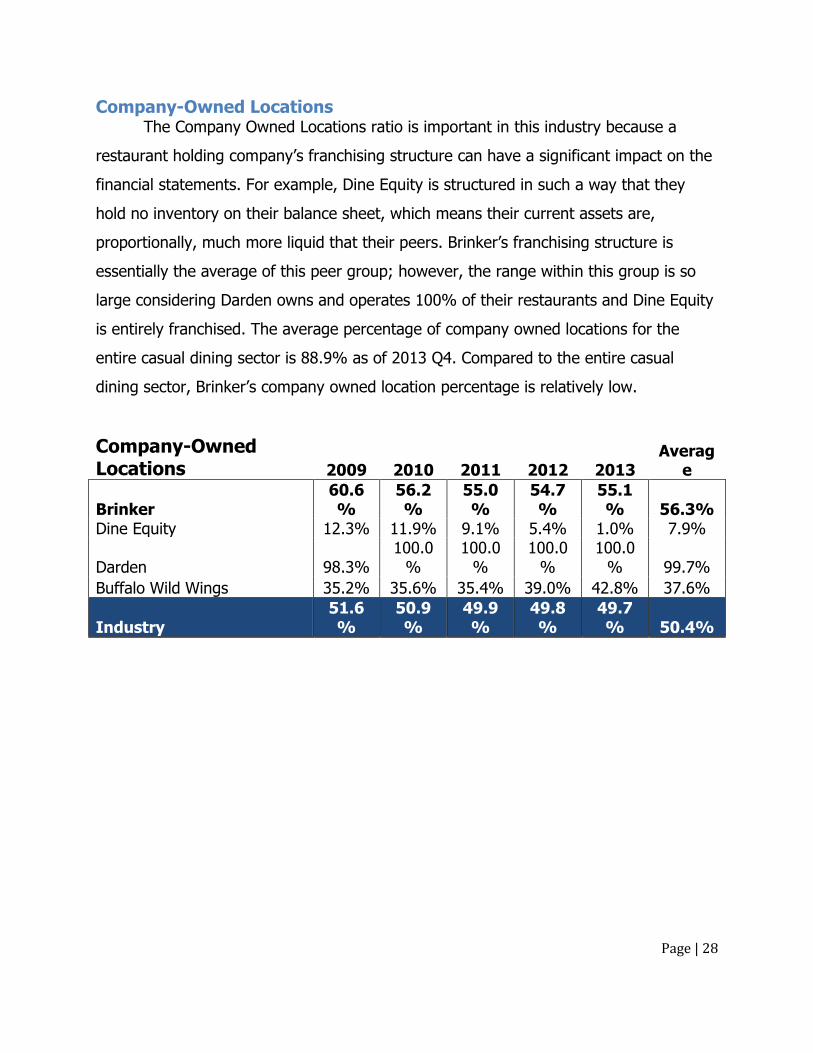

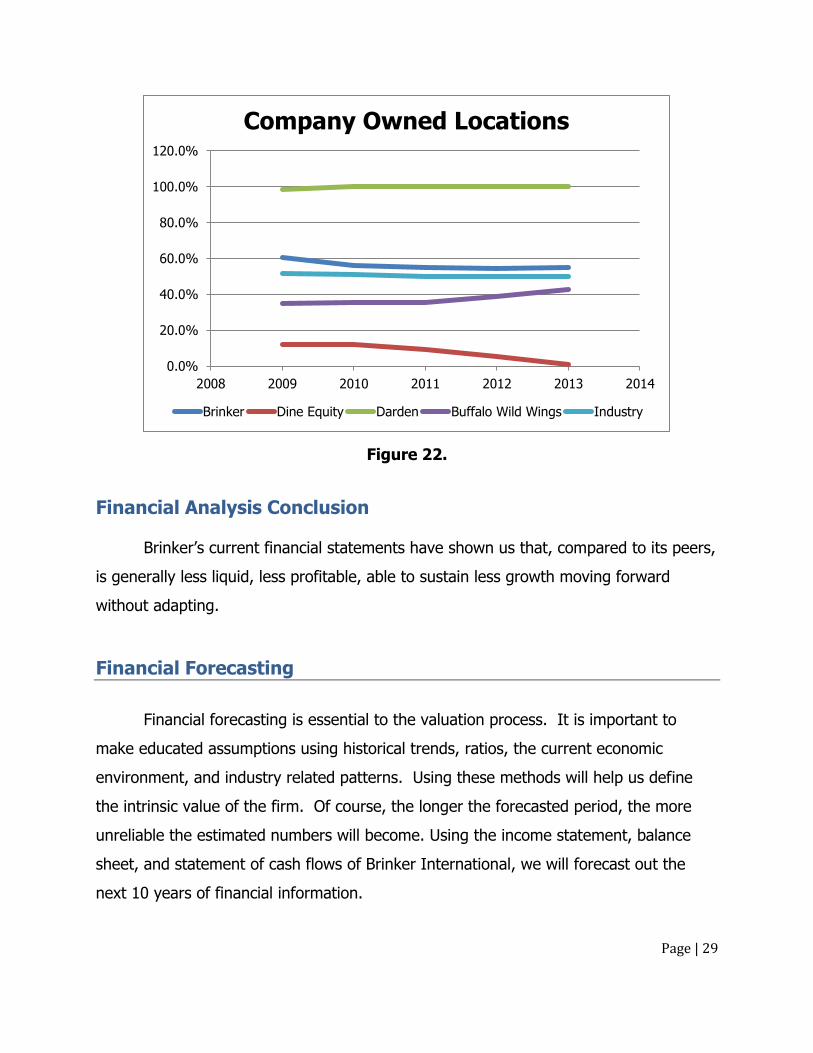

Company-Owned Locations The Company Owned Locations ratio is important in this industry because a

restaurant holding company’s franchising structure can have a significant impact on the

financial statements. For example, Dine Equity is structured in such a way that they

hold no inventory on their balance sheet, which means their current assets are,

proportionally, much more liquid that their peers. Brinker’s franchising structure is

essentially the average of this peer group; however, the range within this group is so

large considering Darden owns and operates 100% of their restaurants and Dine Equity

is entirely franchised. The average percentage of company owned locations for the

entire casual dining sector is 88.9% as of 2013 Q4. Compared to the entire casual

dining sector, Brinker’s company owned location percentage is relatively low.

Company-Owned Locations 2009 2010 2011 2012 2013

Average

Brinker 60.6%

56.2%

55.0%

54.7%

55.1% 56.3%

Dine Equity 12.3% 11.9% 9.1% 5.4% 1.0% 7.9%

Darden 98.3% 100.0

% 100.0

% 100.0

% 100.0

% 99.7%

Buffalo Wild Wings 35.2% 35.6% 35.4% 39.0% 42.8% 37.6%

Industry 51.6%

50.9%

49.9%

49.8%

49.7% 50.4%

Page | 29

Figure 22.

Financial Analysis Conclusion

Brinker’s current financial statements have shown us that, compared to its peers,

is generally less liquid, less profitable, able to sustain less growth moving forward

without adapting.

Financial Forecasting

Financial forecasting is essential to the valuation process. It is important to

make educated assumptions using historical trends, ratios, the current economic

environment, and industry related patterns. Using these methods will help us define

the intrinsic value of the firm. Of course, the longer the forecasted period, the more

unreliable the estimated numbers will become. Using the income statement, balance

sheet, and statement of cash flows of Brinker International, we will forecast out the

next 10 years of financial information.

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2008 2009 2010 2011 2012 2013 2014

Company Owned Locations

Brinker Dine Equity Darden Buffalo Wild Wings Industry

Page | 30

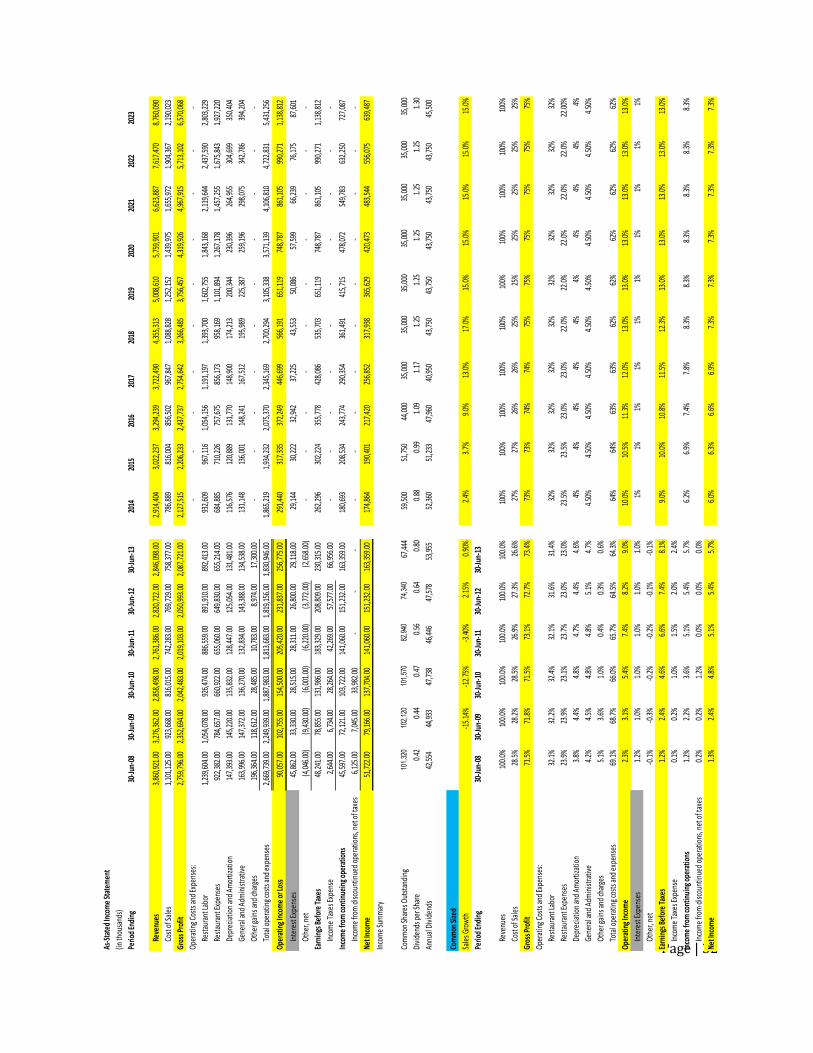

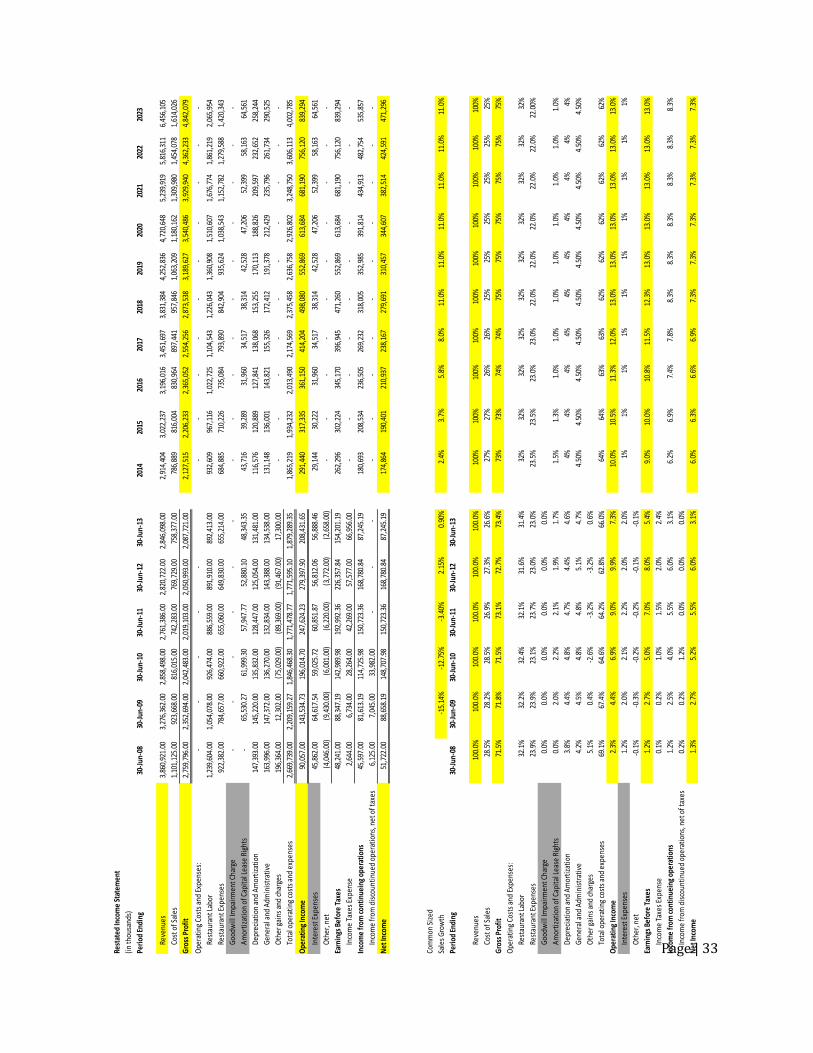

Income Statement The first financial statement to be forecasted is the income statement. The

income statement is important to forecast with logical assumptions because the

numbers used in the balance sheet and statement of cash flows are pulled directly from

it. The most important factor in forecasting the income statement is the sales growth

figure. Future revenues are used in multiple ratios, including liquidity and profitability.

As always, the current economic conditions must also me taken into consideration.

Since we are slowly coming out of the housing recession, the sales growth rate has

been adjusted to take this into account. Brinker International has been showing an

increasing trend in sales over the past 5 years. We have continued this trend, but on a

cautious basis, since the average consumer still seems hesitant about the economic

future. We started with a sales growth of 2.4% in 2014 and continued the upward

trend to a max of 17% in 2018 and finally settling down to 15% in 2019 and on.

After the sales growth is projected, a common sized income statement can be

created. A common size income statement reports line items as a percentage of

revenues. Using this method, trends and patterns are easier to see and easier to

forecast. We have continued Brinker International’s upward trend and have forecasted

their gross profit margin to rise steadily from 73% in 2014 to a maintenance amount of

75% in 2018 and on. This gives us a cost of goods sold of 27% in 2014 and a final

number of 25% in 2018 and thereafter. We have also noticed a trend of Brinker

lowering their restaurant expenses. We have continued this trend by forecasting these

expenses as 23.5% in 2014 and slowly decreasing to 21.5% in 2019 and thereafter.

Following the trend of lower expenses and increasing sales growth, we have naturally

forecasted the operating income, earnings before taxes, and the net income, to

continue this favorable trend. We started with an operating income of 10% in 2014

and gradually increased it to 13% in 2018 and thereafter. The earnings before taxes

number was forecasted at 9% in 2014 and reached a max of 13% in 2019 and

remaining at that rate. And finally we show net income increasing from 6% in 2014 to

7.3% in 2018 and maintaining at that rate. Again, with a long forecast period of 10

Page | 31

years, unexpected factors could affect our projections. Using these forecasted income

statement numbers, we can now forecast the balance sheet, statement of cash flows,

and look at dividends.

Page | 32

As-S

tate

d In

com

e St

atem

ent

(in th

ousa

nds)

Perio

d En

ding

30-Ju

n-08

30-Ju

n-09

30-Ju

n-10

30-Ju

n-11

30-Ju

n-12

30-Ju

n-13

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Reve

nues

3,86

0,92

1.00

3,

276,

362.

00

2,85

8,49

8.00

2,

761,

386.

00

2,82

0,72

2.00

2,

846,

098.

00

2,91

4,40

4

3,02

2,23

7

3,29

4,23

9

3,

722,

490

4,35

5,31

3

5,00

8,61

0

5,

759,

901

6,

623,

887

7,

617,

470

8,76

0,09

0

Cost

of S

ales

1,10

1,12

5.00

92

3,66

8.00

816,

015.

00

74

2,28

3.00

769,

729.

00

75

8,37

7.00

786,

889

816,

004

856,

502

96

7,84

7

1,08

8,82

8

1,25

2,15

2

1,

439,

975

1,

655,

972

1,

904,

367

2,19

0,02

3

Gros

s Pro

fit2,

759,

796.

00

2,35

2,69

4.00

2,

042,

483.

00

2,01

9,10

3.00

2,

050,

993.

00

2,08

7,72

1.00

2,

127,

515

2,

206,

233

2,

437,

737

2,75

4,64

2

3,

266,

485

3,

756,

457

4,31

9,92

6

4,96

7,91

5

5,71

3,10

2

6,

570,

068

Oper

atin

g Cos

ts an

d Ex

pens

es:

-

-

-

-

-

-

-

-

-

-

Rest

aura

nt La

bor

1,23

9,60

4.00

1,

054,

078.

00

926,

474.

00

88

6,55

9.00

891,

910.

00

89

2,41

3.00

932,

609

967,

116

1,05

4,15

6

1,

191,

197

1,39

3,70

0

1,60

2,75

5

1,

843,

168

2,

119,

644

2,

437,

590

2,80

3,22

9

Rest

aura

nt Ex

pens

es92

2,38

2.00

784,

657.

00

66

0,92

2.00

655,

060.

00

64

9,83

0.00

655,

214.

00

68

4,88

5

71

0,22

6

75

7,67

5

856,

173

95

8,16

9

1,

101,

894

1,26

7,17

8

1,45

7,25

5

1,67

5,84

3

1,

927,

220

Depr

ecia

tion

and

Amor

tizat

ion

147,

393.

00

14

5,22

0.00

135,

832.

00

12

8,44

7.00

125,

054.

00

13

1,48

1.00

116,

576

120,

889

131,

770

14

8,90

0

174,

213

200,

344

23

0,39

6

26

4,95

5

30

4,69

9

350,

404

Gene

ral a

nd A

dmin

istra

tive

163,

996.

00

14

7,37

2.00

136,

270.

00

13

2,83

4.00

143,

388.

00

13

4,53

8.00

131,

148

136,

001

148,

241

16

7,51

2

195,

989

225,

387

25

9,19

6

29

8,07

5

34

2,78

6

394,

204

Othe

r gai

ns an

d ch

arge

s19

6,36

4.00

118,

612.

00

28

,485

.00

10,7

83.0

0

8,

974.

00

17,3

00.0

0

-

-

-

-

-

-

-

-

-

-

Tota

l ope

ratin

g cos

ts an

d ex

pens

es2,

669,

739.

00

2,24

9,93

9.00

1,

887,

983.

00

1,81

3,68

3.00

1,

819,

156.

00

1,83

0,94

6.00

1,

865,

219

1,

934,

232

2,

075,

370

2,34

5,16

9

2,

700,

294

3,

105,

338

3,57

1,13

9

4,10

6,81

0

4,72

2,83

1

5,

431,

256

Oper

atin

g Inc

ome

or Lo

ss90

,057

.00

102,

755.

00

15

4,50

0.00

205,

420.

00

23

1,83

7.00

256,

775.

00

29

1,44

0

31

7,33

5

37

2,24

9

446,

699

56

6,19

1

65

1,11

9

748,

787

861,

105

990,

271

1,

138,

812

Inte

rest

Expe

nses

45,8

62.0

0

33

,330

.00

28,5

15.0

0

28

,311

.00

26,8

00.0

0

29

,118

.00

29,1

44

30,2

22

32,9

42

37,2

25

43

,553

50

,086

57,5

99

66

,239

76

,175

87,6

01

Othe

r, ne

t(4

,046

.00)

(9,4

30.0

0)

(6

,001

.00)

(6,2

20.0

0)

(3

,772

.00)

(2,6

58.0

0)

-

-

-

-

-

-

-

-

-

-

Earn

ings

Bef

ore

Taxe

s48

,241

.00

78,8

55.0

0

13

1,98

6.00

183,

329.

00

20

8,80

9.00

230,

315.

00

26

2,29

6

30

2,22

4

35

5,77

8

428,

086

53

5,70

3

65

1,11

9

748,

787

861,

105

990,

271

1,

138,

812

Inco

me

Taxe

s Exp

ense

2,64

4.00

6,

734.

00

28,2

64.0

0

42

,269

.00

57,5

77.0

0

66

,956

.00

-

-

-

-

-

-

-

-

-

-

Inco

me

from

cont

inue

ing o

pera

tions

45,5

97.0

0

72

,121

.00

103,

722.

00

14

1,06

0.00

151,

232.

00

16

3,35

9.00

180,

693

208,

534

243,

774

29

0,35

4

361,

491

415,

715

47

8,07

2

54

9,78

3

63

2,25

0

727,

087

Inco

me

from

disc

ount

inue

d op

erat

ions

, net

of t

axes

6,12

5.00

7,

045.

00

33,9

82.0

0

-

-

-

-

-

-

-

-

-

-

-

-

-

Net I

ncom

e51

,722

.00

79,1

66.0

0

13

7,70

4.00

141,

060.

00

15

1,23

2.00

163,

359.

00

17

4,86

4

19

0,40

1

21

7,42

0

256,

852

31

7,93

8

36

5,62

9

420,

473

483,

544

556,

075

63

9,48

7

Inco

me

Sum

mar

y

Com

mon

Shar

es O

utst

andi

ng

101,

320

10

2,12

0

101,

570

8

2,94

0

74,

340

67,4

4459

,500

51

,750

44

,000

35,0

0035

,000

35,0

0035

,000

35,0

0035

,000

35,0

00

Divi

dend

s per

Shar

e0.

420.

440.

470.

560.

640.

800.

880.

991.

091.

171.

251.

251.

251.

251.

251.

30

Annu

al D

ivid

ends

42,5

54

44

,933

47,7

38

46

,446

47,5

78

53

,955

52,3

60

51,2

33

47,9

60

40,9

50

43

,750

43

,750

43,7

50

43

,750

43

,750

45,5

00

Com

mon

Size

d

Sale

s Gro

wth

-15.

14%

-12.

75%

-3.4

0%2.

15%

0.90

%2.

4%3.

7%9.

0%13

.0%

17.0

%15

.0%

15.0

%15

.0%

15.0

%15

.0%

Perio

d En

ding

30-Ju

n-08

30-Ju

n-09

30-Ju

n-10

30-Ju

n-11

30-Ju

n-12

30-Ju

n-13

Reve

nues

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

Cost

of S

ales

28.5

%28

.2%

28.5

%26

.9%

27.3

%26

.6%

27%

27%

26%

26%

25%

25%

25%

25%

25%

25%

Gros

s Pro

fit71

.5%

71.8

%71

.5%

73.1

%72

.7%

73.4

%73

%73

%74

%74

%75

%75

%75

%75

%75

%75

%

Oper

atin

g Cos

ts an

d Ex

pens

es:

Rest

aura

nt La

bor

32.1

%32

.2%

32.4

%32

.1%

31.6

%31

.4%

32%

32%

32%

32%

32%

32%

32%

32%

32%

32%

Rest

aura

nt Ex

pens

es23

.9%

23.9

%23

.1%

23.7

%23

.0%

23.0

%23

.5%

23.5

%23

.0%

23.0

%22

.0%

22.0

%22

.0%

22.0

%22

.0%

22.0

0%

Depr

ecia

tion

and

Amor

tizat

ion

3.8%

4.4%

4.8%

4.7%

4.4%

4.6%

4%4%

4%4%

4%4%

4%4%

4%4%

Gene

ral a

nd A

dmin

istra

tive

4.2%

4.5%

4.8%

4.8%

5.1%

4.7%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

Othe

r gai

ns an

d ch

arge

s5.

1%3.

6%1.

0%0.

4%0.

3%0.

6%

Tota

l ope

ratin

g cos

ts an

d ex

pens

es69

.1%

68.7

%66

.0%

65.7

%64

.5%

64.3

%64

%64

%63

%63

%62

%62

%62

%62

%62

%62

%

Oper

atin

g Inc

ome

2.3%

3.1%

5.4%

7.4%

8.2%

9.0%

10.0

%10

.5%

11.3

%12

.0%

13.0

%13

.0%

13.0

%13

.0%

13.0

%13

.0%

Inte

rest

Expe

nses

1.2%

1.0%

1.0%

1.0%

1.0%

1.0%

1%1%

1%1%

1%1%

1%1%

1%1%

Othe

r, ne

t-0

.1%

-0.3

%-0

.2%

-0.2

%-0

.1%

-0.1

%

Earn

ings

Bef

ore

Taxe

s1.

2%2.

4%4.

6%6.

6%7.

4%8.

1%9.

0%10

.0%

10.8

%11

.5%

12.3

%13

.0%

13.0

%13

.0%

13.0

%13

.0%

Inco

me

Taxe

s Exp

ense

0.1%

0.2%

1.0%

1.5%

2.0%

2.4%

Inco

me

from

cont

inui

ng o

pera

tions

1.2%

2.2%

3.6%

5.1%

5.4%

5.7%

6.2%

6.9%

7.4%

7.8%

8.3%

8.3%

8.3%

8.3%

8.3%

8.3%

Inco

me

from

disc

ount

inue

d op

erat

ions

, net

of t

axes

0.2%

0.2%

1.2%

0.0%

0.0%

0.0%

Net I

ncom

e1.

3%2.

4%4.

8%5.

1%5.

4%5.

7%6.

0%6.

3%6.

6%6.

9%7.

3%7.

3%7.

3%7.

3%7.

3%7.

3%

Page | 33

Rest

ated

Inco

me

Stat

emen

t

(in

thou

sand

s)

Peri

od E

ndin

g30

-Jun

-08

30-J

un-0

930

-Jun

-10

30-J

un-1

130

-Jun

-12

30-J

un-1

320

1420

1520

1620

1720

1820

1920

2020

2120

2220

23

Reve

nues

3,86

0,92

1.00

3,

276,

362.

00

2,

858,

498.

00

2,76

1,38

6.00

2,

820,

722.

00

2,84

6,09

8.00

2,

914,

404

3,

022,

237

3,19

6,01

6

3,45

1,69

7

3,83

1,38

4

4,

252,

836

4,

720,

648

5,

239,

919

5,81

6,31

1

6,45

6,10

5

Cost

of S

ales

1,10

1,12

5.00

92

3,66

8.00

81

6,01

5.00

742,

283.

00

76

9,72

9.00

758,

377.

00

78

6,88

9

81

6,00

4

830,

964

897,

441

957,

846

1,

063,

209

1,

180,

162

1,

309,

980

1,45

4,07

8

1,61

4,02

6

Gro

ss P

rofi

t2,

759,

796.

00

2,35

2,69

4.00

2,04

2,48

3.00

2,

019,

103.

00

2,05

0,99

3.00

2,

087,

721.

00

2,12

7,51

5

2,20

6,23

3

2,

365,

052

2,

554,

256

2,

873,

538

3,18

9,62

7

3,54

0,48

6

3,92

9,94

0

4,

362,

233

4,

842,

079

Ope

rati

ng C

osts

and

Exp

ense

s:-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Rest

aura

nt L

abor

1,23

9,60

4.00

1,

054,

078.

00

92

6,47

4.00

886,

559.

00

89

1,91

0.00

892,

413.

00

93

2,60

9

96

7,11

6

1,02

2,72

5

1,10

4,54

3

1,22

6,04

3

1,

360,

908

1,

510,

607

1,

676,

774

1,86

1,21

9

2,06

5,95

4

Rest

aura

nt E

xpen

ses

922,

382.

00

78

4,65

7.00

66

0,92

2.00

655,

060.

00

64

9,83

0.00

655,

214.

00

68

4,88

5

71

0,22

6

735,

084

793,

890

842,

904

93

5,62

4

1,03

8,54

3

1,15

2,78

2

1,

279,

588

1,

420,

343

Goo

dwill

Impa

irm

ent C

harg

e-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Am

orti

zati

on o

f Cap

ital

Lea

se R

ight

s-

65

,530

.27

61,9

99.3

0

57,9

47.7

7

52,8

80.1

0

48,3

43.3

5

43,7

16

39,2

89

31

,960

34

,517

38

,314

42,5

28

47,2

06

52,3

99

58

,163

64

,561

Dep

reci

atio

n an

d A

mor

tiza

tion

147,

393.

00

14

5,22

0.00

13

5,83

2.00

128,

447.

00

12

5,05

4.00

131,

481.

00

11

6,57

6

12

0,88

9

127,

841

138,

068

153,

255

17

0,11

3

188,

826

20

9,59

7

232,

652

258,

244

Gen

eral

and

Adm

inis

trat

ive

163,

996.

00

14

7,37

2.00

13

6,27

0.00

132,

834.

00

14

3,38

8.00

134,

538.

00

13

1,14

8

13

6,00

1

143,

821

155,

326

172,

412

19

1,37

8

212,

429

23

5,79

6

261,

734

290,

525

Oth

er g

ains

and

cha

rges

196,

364.

00

12

,302

.00

(75,

029.

00)

(89,

369.

00)

(91,

467.

00)

17,3

00.0

0

-

-

-

-

-

-

-

-

-

-

Tota

l ope

rati

ng c

osts

and

exp

ense

s2,

669,

739.

00

2,20

9,15

9.27

1,84

6,46

8.30

1,

771,

478.

77

1,77

1,59

5.10

1,

879,

289.

35

1,86

5,21

9

1,93

4,23

2

2,

013,

490

2,

174,

569

2,

375,

458

2,63

6,75

8

2,92

6,80

2

3,24

8,75

0

3,

606,

113

4,

002,

785

Ope

rati

ng In

com

e90

,057

.00

14

3,53

4.73

19

6,01

4.70

247,

624.

23

27

9,39

7.90

208,

431.

65

29

1,44

0

31

7,33

5

361,

150

414,

204

498,

080

55

2,86

9

613,

684

68

1,19

0

756,

120

839,

294

Inte

rest

Exp

ense

s45

,862

.00

64

,617

.54

59,0

25.7

2

60,8

51.8

7

56,8

12.0

6

56,8

88.4

6

29,1

44

30,2

22

31

,960

34

,517

38

,314

42,5

28

47,2

06

52,3

99

58

,163

64

,561

Oth

er, n

et(4

,046

.00)

(9

,430

.00)

(6,0

01.0

0)

(6,2

20.0

0)

(3,7

72.0

0)

(2,6

58.0

0)

-

-

-

-

-

-

-

-

-

-

Earn

ings

Bef

ore

Taxe

s48

,241

.00

88

,347

.19

142,

989.

98

19

2,99

2.36

226,

357.

84

15

4,20

1.19

262,

296

302,

224

34

5,17

0

39

6,94

5

47

1,26

0

552,

869

61

3,68

4

681,

190

75

6,12

0

83

9,29

4

Inco

me

Taxe

s Ex

pens

e2,

644.

00

6,

734.

00

28

,264

.00

42

,269

.00

57

,577

.00

66

,956

.00

-

-

-

-

-

-

-

-

-

-

Inco

me

from

con

tinu

eing

ope

rati

ons

45,5

97.0

0

81,6

13.1

9

11

4,72

5.98

150,

723.

36

16

8,78

0.84

87,2

45.1

9

180,

693

208,

534

23

6,50

5

26

9,23

2

31

8,00

5

352,

985

39

1,81

4

434,

913

48

2,75

4

53

5,85

7

Inco

me

from

dis

coun

tinu

ed o

pera

tion

s, n

et o

f tax

es6,

125.

00

7,

045.

00

33

,982

.00

-

-

-

-

-

-

-

-

-

-

-

-

-

Net

Inco

me

51,7

22.0

0

88,6

58.1

9

14

8,70

7.98

150,

723.

36

16

8,78

0.84

87,2

45.1

9

174,

864

190,

401

21

0,93

7

23

8,16

7

27

9,69

1

310,

457

34

4,60

7

382,

514

42

4,59

1

47

1,29

6

Com

mon

Siz

ed

Sale

s G

row

th-1

5.14

%-1

2.75

%-3

.40%

2.15

%0.

90%

2.4%

3.7%

5.8%

8.0%

11.0

%11

.0%

11.0

%11

.0%

11.0

%11

.0%

Peri

od E

ndin

g30

-Jun

-08

30-J

un-0

930

-Jun

-10

30-J

un-1

130

-Jun

-12

30-J

un-1

3

Reve

nues

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

Cost

of S

ales

28.5

%28

.2%

28.5

%26

.9%

27.3

%26

.6%

27%

27%

26%

26%

25%

25%

25%

25%

25%

25%

Gro

ss P

rofi

t71

.5%

71.8

%71

.5%

73.1

%72

.7%

73.4

%73

%73

%74

%74

%75

%75

%75

%75

%75

%75

%

Ope

rati

ng C

osts

and

Exp

ense

s:

Rest

aura

nt L

abor

32.1

%32

.2%

32.4

%32

.1%

31.6

%31

.4%

32%

32%

32%

32%

32%

32%

32%

32%

32%

32%

Rest

aura

nt E

xpen

ses

23.9

%23

.9%

23.1

%23

.7%

23.0

%23

.0%

23.5

%23

.5%

23.0

%23

.0%

22.0

%22

.0%

22.0

%22

.0%

22.0

%22

.00%

Goo

dwill

Impa

irm

ent C

harg

e0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%

Am

orti

zati

on o

f Cap

ital

Lea

se R

ight

s0.

0%2.

0%2.

2%2.

1%1.

9%1.

7%1.

5%1.

3%1.

0%1.

0%1.

0%1.

0%1.

0%1.

0%1.

0%1.

0%

Dep

reci

atio

n an

d A

mor

tiza

tion

3.8%

4.4%

4.8%

4.7%

4.4%

4.6%

4%4%

4%4%

4%4%

4%4%

4%4%

Gen

eral

and

Adm

inis

trat

ive

4.2%

4.5%

4.8%

4.8%

5.1%

4.7%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

4.50

%4.

50%

Oth

er g

ains

and

cha

rges

5.1%

0.4%

-2.6

%-3

.2%

-3.2

%0.

6%

Tota

l ope

rati

ng c

osts

and

exp

ense

s69

.1%

67.4

%64

.6%

64.2

%62

.8%

66.0

%64

%64

%63

%63

%62

%62

%62

%62

%62

%62

%

Ope

rati

ng In

com

e2.

3%4.

4%6.

9%9.

0%9.

9%7.

3%10

.0%

10.5

%11

.3%

12.0

%13

.0%

13.0

%13

.0%

13.0

%13

.0%

13.0

%

Inte

rest

Exp

ense

s1.

2%2.

0%2.

1%2.

2%2.

0%2.

0%1%

1%1%

1%1%

1%1%

1%1%

1%

Oth

er, n

et-0

.1%

-0.3

%-0

.2%

-0.2

%-0

.1%

-0.1

%

Earn

ings

Bef

ore

Taxe

s1.

2%2.

7%5.

0%7.

0%8.

0%5.

4%9.

0%10

.0%

10.8

%11

.5%

12.3

%13

.0%

13.0

%13

.0%

13.0

%13

.0%

Inco

me

Taxe

s Ex

pens

e0.

1%0.

2%1.

0%1.

5%2.

0%2.

4%

Inco

me

from

con

tinu

eing

ope

rati

ons

1.2%

2.5%

4.0%

5.5%

6.0%

3.1%

6.2%

6.9%

7.4%

7.8%

8.3%

8.3%

8.3%

8.3%

8.3%

8.3%

Inco

me

from

dis

coun

tinu

ed o

pera

tion

s, n

et o

f tax

es0.

2%0.

2%1.

2%0.

0%0.

0%0.

0%

Net

Inco

me

1.3%

2.7%

5.2%

5.5%

6.0%

3.1%

6.0%

6.3%

6.6%

6.9%

7.3%

7.3%

7.3%

7.3%

7.3%

7.3%

Page | 34

Dividends Forecasting

The valuation of a firm is heavily dependent on future expectations of dividend

growth and value. Brinker International announced plans to spend $4 billion on a share

repurchase plan in 2012. As a result, the dividends paid out have been steadily

increasing while share outstanding have been decreasing. We have forecasted this

trend to continue starting with a dividend of $0.88 per share in 2014 and reaching a

max of $1.25 per share in 2018.

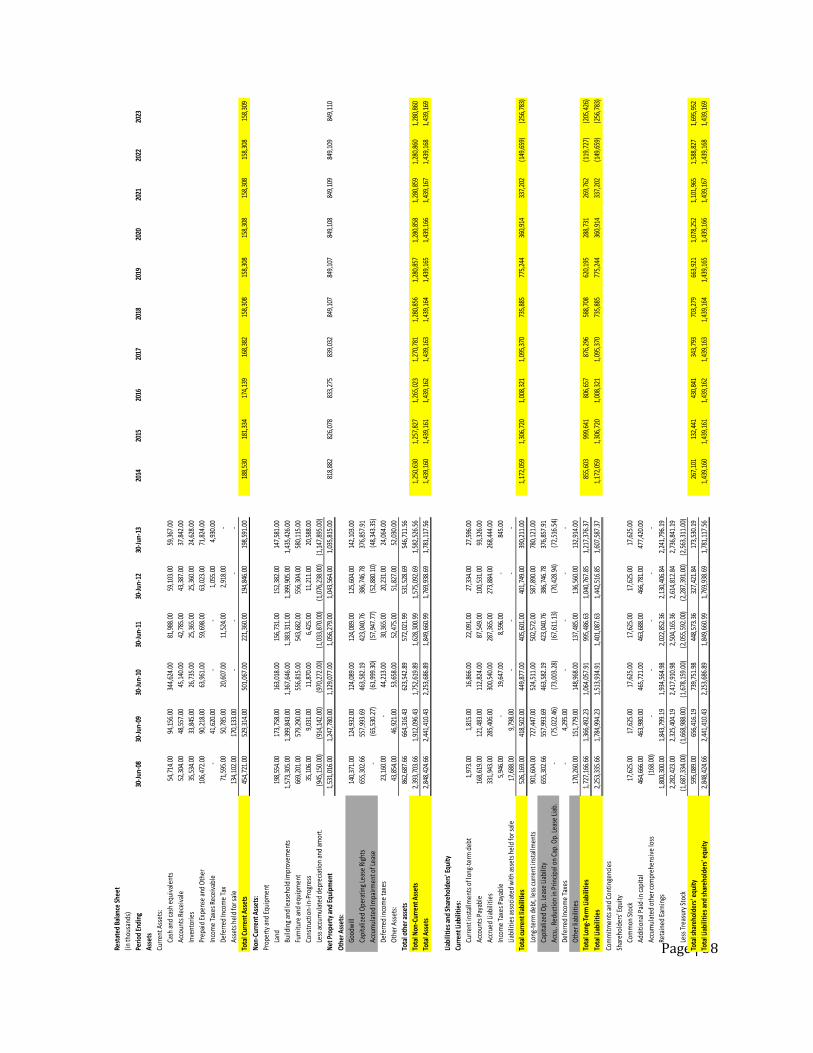

Balance Sheet

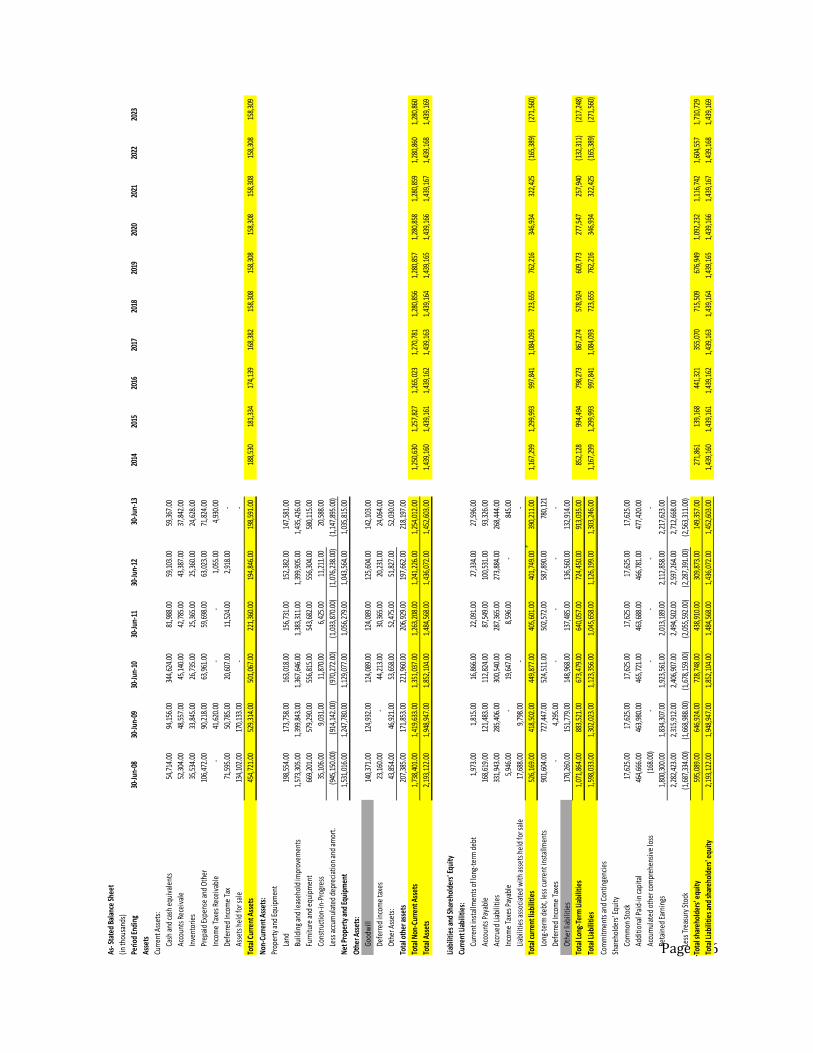

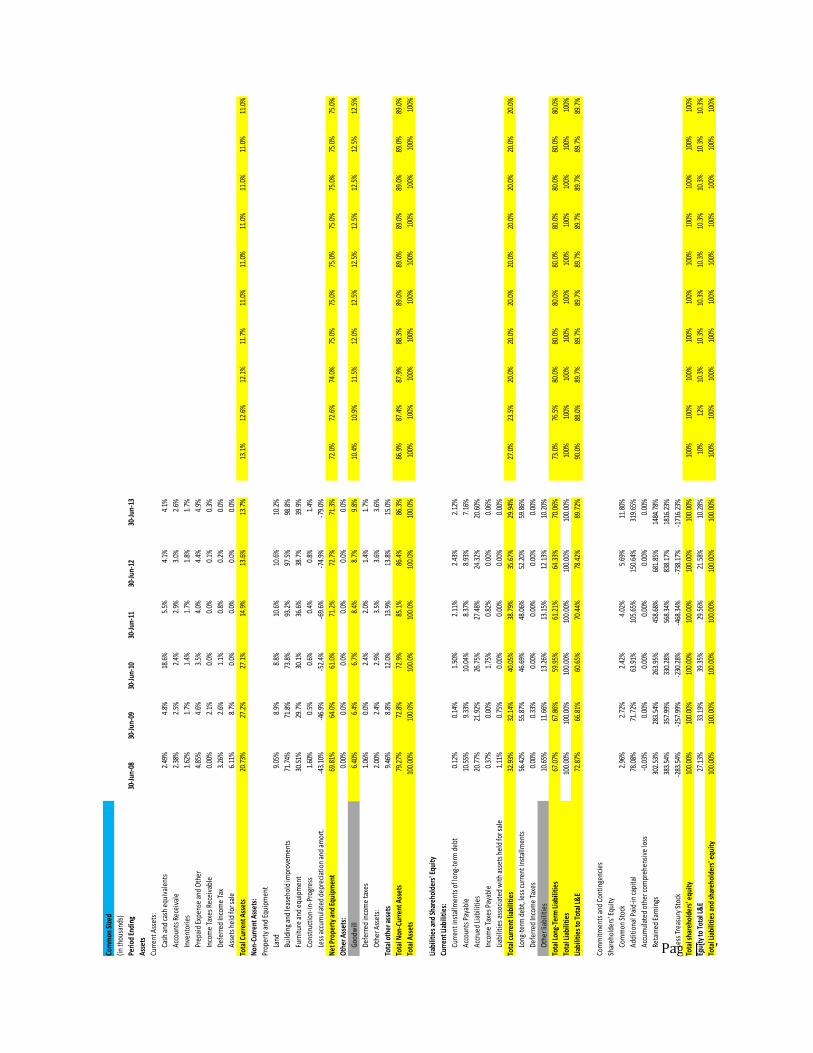

After forecasting the income statement, the next step is to forecast the balance

sheet. There are many ratios and methods used to do this, but we find the asset

turnover ratio is the best at tying the income statement to the balance sheet. Just like

the favorable trend in sales, we have found an increasing trend in the asset turnover

ratio from 1.6 in 2008 to 2.0 in 2013. Using this trend, we have forecasted the asset

turnover ratio in 2014 to be 2.1. With this ratio, we then backed into the total assets

figure. The total assets figure is the basis for forecasting the balance sheet. With the

use of Liquidity ratios we also forecasted the current assets and current liabilities. Now

that we have the total assets figure, the next step was to create a common size balance

sheet to help indentify patterns and trends.

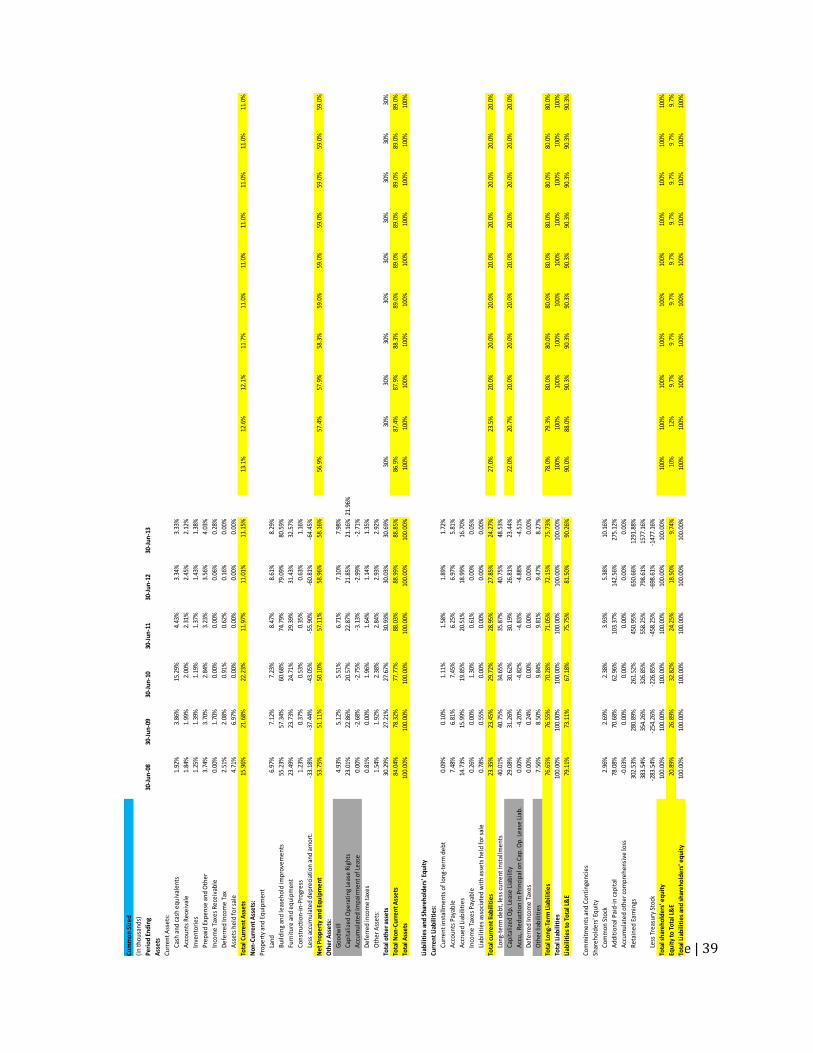

Using the common size balance sheet we found a trend of decreasing current

assets and an increase in long term assets. We forecasted the current assets in 2014 at

13.1% of total assets and slowly decreased it to 11% in 2018 where it remained

constant. The long term assets were forecasted at 86.9% in 2014 and slowly increased

to 89% in 2018 and stayed constant as well. This same trend was found in the current

and long term liabilities of Brinker. Again, we continued this trend in our forecasts. We

started with 27% in current liabilities in 2014 and decreased it to 20% in 2016 where it

stayed constant. The long term liabilities increased from 73% in 2014 to 80% in 2016.

Page | 35

The trends we are finding in Brinker match the trends of the casual dining industry, as

well as, the slowly improving economy.

Page | 36

As- S

tate

d Ba

lanc

e Sh

eet

(in th

ousa

nds)

Perio

d En

ding

30

-Jun

-08

30-J

un-0

930

-Jun

-10

30-J

un-1

130

-Jun

-12

30-J

un-1

320

1420

1520

1620

1720

1820

1920

2020

2120

2220

23

Asse