Embed Size (px)

Citation preview

1.1 Problem statement

Analysis of financial statements of Hindustan Unilever Limited

1.2 Research objective

To study and analyze the financial performance of HUL for the year 2011-12 & 2012-13

To analyze the growth and profitability of HUL for the year 2011-12 and 2012-13

To determine the credibility of HUL and suggest appropriate measure to enhance it

1.3 Hypothesis

H0: Financial performance of HUL was not up to the mark for the year 2011-12 & 2012-13

H1: Financial performance of HUL was up to the mark for the year 2011-12 & 2012-13

H0: HUL has no significant growth in recent years

H1: HUL has significant growth in recent years

1.4 Limitations

The study is based on annual reports published by the firm. The study is quantitative in nature. The study is limited to Horizontal analysis, and ratio analysis.

2. Introduction

2.1 Financial statement

Meaning

Financial statements mean the statements showing the financial affairs of an enterprise. It refers to that statement which reflects collection of fund from various sources, cost of using such funds, investment of such funds in various assets, return accrued from such resources and similar bits of information.

Objectives The objectives of financial statements are to: Provide information needs of various present and prospective

stakeholders about the net results of the business activities at regular intervals.

Make the affairs of the company transparent to the parties external to the day-to-day activities of the enterprise.

Safeguard the interests of the stakeholders who do not have access to the day-to-day affairs of the company.

Keep the management under pressure so that the scope of manipulation can be minimized as they are to measure and report the financial results of the business adhering to certain rules and regulations promulgated by the regulatory authorities.

Enhance credibility of the enterprise and increase its market acceptability.

What is Financial Statement Analysis?Financial Statement Analysis (FSA) is a tool for business analysis. Business analysis is the evaluation of a company’s prospects and risks for the purpose of making business decisions. Different stakeholders analyze business for different purpose. An investor and an analyst analyze a business for valuation of equity and debt. A creditor analyses a business to assess the credit risk. The trade union analyses business for compensation negotiations. A buyer analyses the business of a prospective supplier for the purpose of vendor rating. There are myriad of reasons for analyzing business. The objective is to make informed decisions.

Business analysis involves evaluation of the business environment and strategy of the company, and analysis of financial statements. Analysts take an integrated approach to financial statement analysis. Information provided in financial statements are analyzed in the context of changes, particularly

structural changes in the business environment and changes in the industry structure during the period covered financial statements. Changes in business environment include changes in technology, changes in the level of competition in the market place due to changes in government policy or otherwise, changes in the overall economic environment and changes in the demography. Integrated approach in business analysis is essential because financial statement analysis, in isolation, does not provide insights required to forecast future performance and financial position of the company.Financial analysis consists of the following broad areas:

Profitability analysisProfitability analysis measures the income of the company relative to its revenue and investment. It focuses on margin and returns on investment, and also identifies and measures the impact of various factors that determine the profitability.

Risk analysis Risk analysis measures the company’s ability to meet its commitments. Risk analysis includes liquidity analysis and solvency analysis. Liquidity of a company refers to the ability of the company to meet its short-term commitments. Solvency refers to the company to meet its long term commitments. Therefore, liquidity analysis evaluates the adequacy of liquid assets relative to short-term liabilities. Solvency analysis evaluates the capital structure of the company.

Activity analysisActivity analysis, which is a part of profitability analysis, evaluates revenue and output generated by company’s assets; it measures the productivity of assets.

2.2 Parties interested in financial statement analysis Investors and analysts

Equity investors and analysts use financial statement analysis to forecast cash flow that the company is expected to generate in future. The forecasted cash flow forms the basis for the valuation of business and the valuation of equity. Discounted cash flow methods require estimation of free cash flow and determination of the appropriate discount rate. Free cash flow is the cash flow available for distribution to investors. Security analysts compare the intrinsic value of equity of share calculated using discounted cash flow method with market price to identify over-valued and under-valued shares.

Mergers, acquisition and divestitures

Restructuring of business involves mergers, acquisitions and divestitures. In restructuring, whole or a part of an undertaking change hands. Both the parties use financial statement analysis to estimate the intrinsic value of business from their own perspective and based on their own assumptions. Intrinsic value forms the benchmark in negotiating price with the counter party.Merchant bankers use financial statement analysis to identify target companies for their clients.

ManagersManagers pursue the core objective function of maximization of value of the firm. They use financial statement analysis to evaluate alternative strategies and to compare actual results of strategic decisions with expected results. Managers use financial statement analysis to value business from investors’ perspective. Therefore, goal of financial statement analysis by managers is similar to the goal of financial statement analysis by equity analysts.

Financial management Managers use financial statement analysis to evaluate the financial management decisions (e.g. capital structure decisions and dividend decisions) on future profitability and risks. Managers also use financial statement analysis to estimate the intrinsic value of equity shares to determine the timing for issuing equity shares and timing for buying back shares. Managers buy back shares when shares are under-priced, that is, when shares are traded in the capital market at a price below the intrinsic value. Similarly, managers issue new shares when shares are over-priced or are traded at a price close to the intrinsic value.

External auditorsAn external auditor expresses her opinion on the true and fairness of information provided in financial statement analysis to evaluate the reasonableness of the financial statements as a whole.

Directors and top managementDirectors and top management of a company that is engaged in different businesses or that has customers or assets in different geographic locations, use financial statement analysis to evaluate the performance of different businesses and geographical segments.

Employees and trade unionsEmployees use financial statement analysis to evaluate the sustainability and growth of the company. This helps them to plan their career. A trade union uses financial statement analysis to understand the profitability and the financial position of the company. This understanding is essential to formulate strategy in collective bargaining negotiations.

CustomersCustomers use financial statement analysis to evaluate the sustainability and growth of the company and its financial strength. This is important to assess the ability of the company to supply goods and services over a long period of time. Customers also use financial statements to estimate the profitability of products that the customers procedures from the company. Although such an estimate is, at best, rough, it helps the customer to negotiate price with the company.

Regulators and governmentRegulators and government uses financial statement analysis for different purposes. For example, the income tax department uses financial statement analysis to evaluate the accuracy of the tax return. Government and regulators frame policies for different industries taking into account, among other things, the attractiveness of the industry and the financial position of representative firms operating in the industry. Financial statement provides insights into the attractiveness of the industry and financial position of representative firms

2.3 METHODS OF ANALYSIS Financial statement analysis should focus primarily on isolating information useful for making a particular decision. The information required can take many forms but usually involves comparisons, such as comparing changes in the same item for the same company over a number of years, comparing key relationships within the same year, or comparing the operations of several different companies in the same industry.

Horizontal AnalysisHorizontal analysis, also called trend analysis, refers to studying the behavior of individual financial statement items over several accounting periods. These periods may be several quarters within the same fiscal year or they may be several different years. The analysis of a given item may focus on trends in the absolute dollar amount of the item or trends in percentages.

Absolute AmountsThe absolute amounts of particular financial statement items have many uses. Various national economic statistics, such as gross domestic product and the amount spent to replace productive capacity are derived by combining absolute amounts reported by businesses. Financial statement users with expertise in particular industries might evaluate amounts reported for research and development costs to judge whether a company is spending

excessively or conservatively. Users are particularly concerned with how amounts change over time. For example, a user might compare a pharmaceutical company’s revenue before and after the patent expired on one of its drugs.Comparing only absolute amounts has drawbacks, however, because materiality levels differ from company to company or even from year to year for a given company. The materiality of information refers to its relative importance. An item is considered material if knowledge of it would influence the decision of a reasonably informed user. Generally accepted accounting principles permit companies to account for immaterial items in the most convenient way, regardless of technical accounting rules. For example, companies may expense, rather than capitalize and depreciate, relatively inexpensive long-term assets like pencil sharpeners or waste baskets even if the assets have useful lives of many years. The concept of materiality, which has both quantitative and qualitative aspects, underlies all accounting principles.It is difficult to judge the materiality of an absolute financial statement amount without considering the size of the company reporting it.

Percentage AnalysisPercentage analysis involves computing the percentage relationship between two amounts. In horizontal percentage analysis, a financial statement item is expressed as a percentage of the previous balance for the same item.Percentage analysis sidesteps the materiality problems of comparing different size companies by measuring changes in percentages rather than absolute amounts. Each change is converted to a percentage of the base year.

Whether basing their analyses on absolute amounts, percentages, or ratios, users must avoid drawing overly simplistic conclusions about the reasons for the results. Numerical relationships flag conditions requiring further study. Recall that a change that appears favorable on the surface may not necessarily be a good sign. Users must evaluate the underlying reasons for the change.

Vertical AnalysisVertical analysis uses percentages to compare individual components of financial statements to a key statement figure. Horizontal analysis compares

items over many time periods; vertical analysis compares many items within the same time period.

Vertical Analysis of the Income StatementVertical analysis of an income statement (also called a common size income statement) involves converting each income statement component to a percentage of sales. Although vertical analysis suggests examining only one period, it is useful to compare common size income statements for several years. This analysis discloses that cost of goods sold increased significantly as a percentage of sales. Operating expenses and income taxes, however, decreased in relation to sales. Each of these observations indicates a need for more analysis regarding possible trends for future profits.

Vertical Analysis of the Balance SheetVertical analysis of the balance sheet involves converting each balance sheet component to a percentage of total assets.

Ratio AnalysisRatio analysis involves studying various relationships between different items reported in a set of financial statements. For example, net earnings (net income) reported on the income statement may be compared to total assets reported on the balance sheet. Analysts calculate many different ratios for a wide variety of purposes.

Objectives of Ratio AnalysisAs suggested earlier, various users approach financial statement analysis with many different objectives. Creditors are interested in whether a company will be able to repay its debts on time. Both creditors and stockholders are concerned with how the company is financed, whether through debt, equity, or earnings. Stockholders and potential investors analyze past earnings performance and dividend policy for clues to the future value of their investments. In addition to using internally generated data to analyze operations, company managers find much information prepared for external purposes useful for examining past operations and planning future policies. Although many of these objectives are interrelated, it is convenient to group ratios into categories such as measures of debt-paying ability and measures of profitability.Auditors use ratio analysis as an analytical tool to assess whether financial statements provide true and fair view and to determine the scope of audit. They use ratios to identify break in the pattern of interrelationship among

different economic variables recognized in financial statements. This helps to identify anything abnormal or anything that deviates from the expected and the known.Top management use ratios to evaluate divisional performance. It measures divisional performance by comparing actual ratios with target ratios.Interpretation of ratios Calculation of ratios is easy, but interpretation requires skill and care. A ratio by itself does not provide any insight. For example, an analyst cannot say whether current ratio of 2 is good or bad unless he understand the context and compare it with a benchmark ratio. Suppose the benchmark ratio is 1.33. Comparing with the benchmark ratio of 1.33, a creditor may conclude that the company, whose current ratio is 2, has sound liquidity position and should be able to honor its short-term financial commitments. An in equity may conclude that the company is unable to manage working capital, which is defined as the difference between current assets and current liabilities, efficiently.

Classification of Accounting RatioThe definition of many ratios is not standardized and may vary from analyst to analyst. Therefore, analyst should define each ratio clearly to avoid misinterpretation. Similarly, there is no standard classification of ratios. In this section, ratios are classified based on common classifications.

Profitability analysisa. Return on investment (ROI): ROI measures the overall profitability

of the company.b. Operating performance: analysts’ measures operating performance

in terms of profit margin from operating activities. Activity analysisa. Short term activity ratios: analysts use short term activity ratios to

measures the effectiveness of utilization of current assets.b. Long term activity ratio: analysts use long term activity ratios to

measure the effectiveness of utilization of non-current assets. Credit (risk) analysisa. Liquidity ratios: analysts use liquidity ratios to evaluate the ability of

the company to meet short term obligations.b. Capital structure and solvency ratios: analysts use capital

structure and solvency ratios to assess the ability of the company to meet long term obligations.

Return on InvestmentReturn on investment measures the overall profitability of the company in terms of financial rewards to the suppliers of equity and debt capital. Following are the different concepts of return on investment:

Return on assets (ROA) Return on capital employed (ROCE) Return on equity (ROE)

Return on assets (ROA)

The return on assets (ROA) percentage shows how profitable a company's assets are in generating revenue.

ROA can be computed as:

Return on capital employed (ROCE)Return on capital employed is an accounting ratio used in finance, valuation, and accounting.

ROCE can be computed as:

Where,EBIT stands for Earnings before interest and tax.In the denominator we have net assets or capital employed instead of total assets (which is the case of Return on Assets). Capital Employed has many definitions. In general it is the capital investment necessary for a business to function. It is commonly represented as total assets less current liabilities (or fixed assets plus working capital).

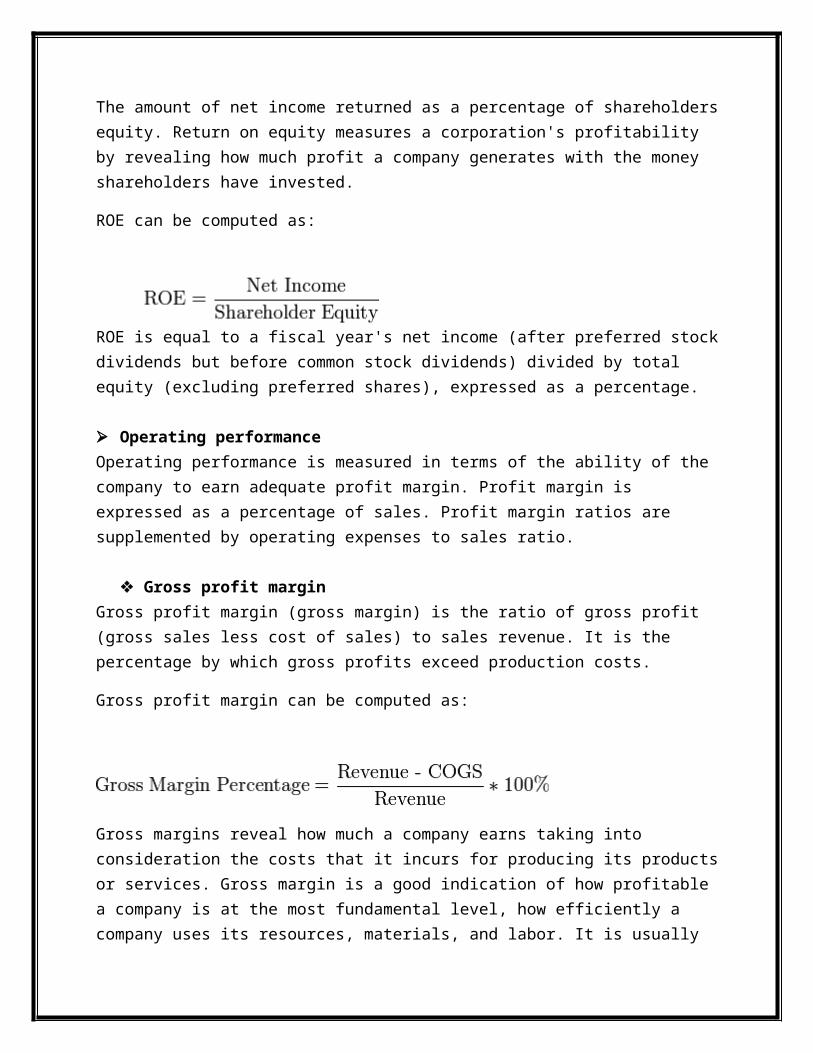

Return on equity (ROE) The amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation's profitability by revealing how much profit a company generates with the money shareholders have invested.

ROE can be computed as:

ROE is equal to a fiscal year's net income (after preferred stock dividends but before common stock dividends) divided by total equity (excluding preferred shares), expressed as a percentage.

Operating performance Operating performance is measured in terms of the ability of the company to earn adequate profit margin. Profit margin is expressed as a percentage of sales. Profit margin ratios are supplemented by operating expenses to sales ratio.

Gross profit marginGross profit margin (gross margin) is the ratio of gross profit (gross sales less cost of sales) to sales revenue. It is the percentage by which gross profits exceed production costs.

Gross profit margin can be computed as:

Gross margins reveal how much a company earns taking into consideration the costs that it incurs for producing its products or services. Gross margin is

a good indication of how profitable a company is at the most fundamental level, how efficiently a company uses its resources, materials, and labor. It is usually expressed as a percentage, and indicates the profitability of a business before overhead costs; it is a measure of how well a company controls its costs.

Operating profit margin

In business, operating margin — also known as operating income margin, operating profit margin and return on sales (ROS) — is the ratio of operating income ("operating profit" in the UK) divided by net sales, usually presented in percent.

Operating profit margin can be computed as:

These financial metrics measure levels and rates of profitability. How does a company decide whether it is successful or not? Probably the most common way is to look at the net profits of the business. Companies are collections of projects and markets, individual areas can be judged on how successful they are at adding to the corporate net profit. Not all projects are of equal size, however, and one way to adjust for size is to divide the profit by sales revenue. The resulting ratio is return on sales (ROS), the percentage of sales revenue that gets 'returned' to the company as net profits after all the related costs of the activity are deducted.

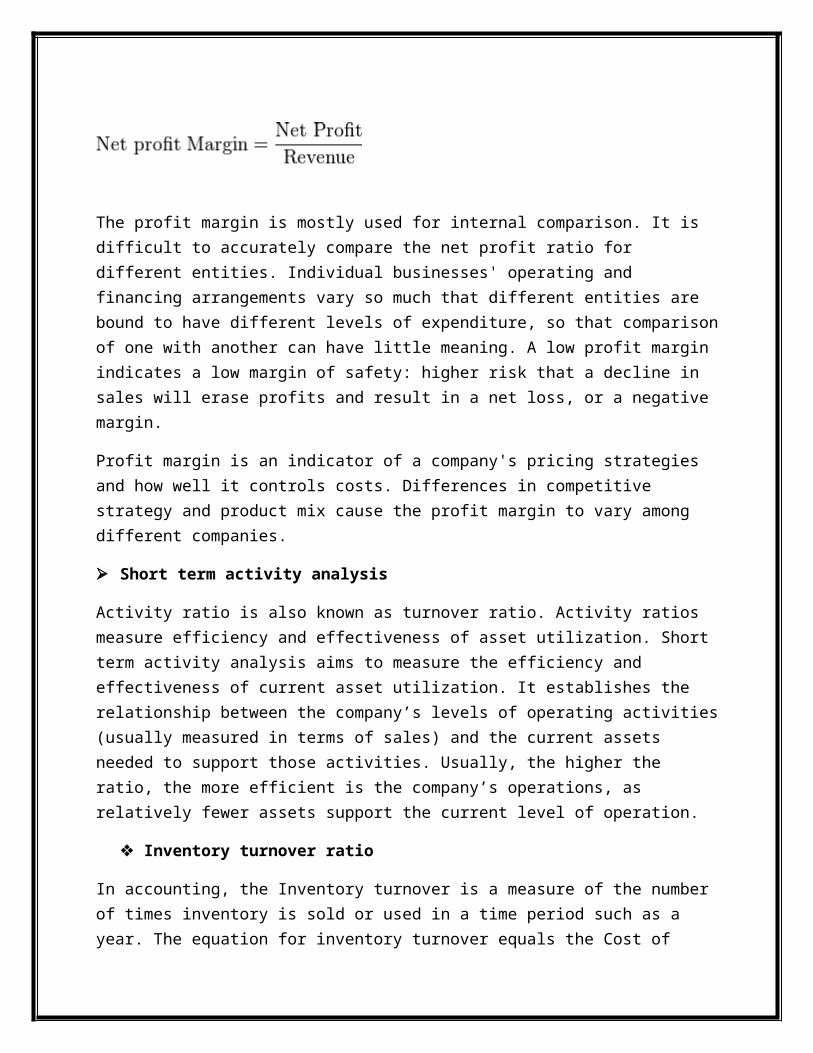

Net profit margin

Profit margin, net margin, net profit margin or net profit ratio all refer to a measure of profitability. It is calculated by finding the net profit as a percentage of the revenue.

Net profit margin can be computed as:

The profit margin is mostly used for internal comparison. It is difficult to accurately compare the net profit ratio for different entities. Individual businesses' operating and financing arrangements vary so much that different entities are bound to have different levels of expenditure, so that comparison of one with another can have little meaning. A low profit margin indicates a low margin of safety: higher risk that a decline in sales will erase profits and result in a net loss, or a negative margin.

Profit margin is an indicator of a company's pricing strategies and how well it controls costs. Differences in competitive strategy and product mix cause the profit margin to vary among different companies.

Short term activity analysis

Activity ratio is also known as turnover ratio. Activity ratios measure efficiency and effectiveness of asset utilization. Short term activity analysis aims to measure the efficiency and effectiveness of current asset utilization. It establishes the relationship between the company’s levels of operating activities (usually measured in terms of sales) and the current assets needed to support those activities. Usually, the higher the ratio, the more efficient is the company’s operations, as relatively fewer assets support the current level of operation.

Inventory turnover ratio

In accounting, the Inventory turnover is a measure of the number of times inventory is sold or used in a time period such as a year. The equation for inventory turnover equals the Cost of goods sold divided by the average inventory. Inventory turnover is also known as inventory turns, stock turn, stock turns, turns, and stock turnover.

The formula for inventory turnover:

Alternatively, it can be also calculated as:

Inventory Turnover = Sales

Average Inventory

Where,

The average days to sell the inventory are calculated as follows:

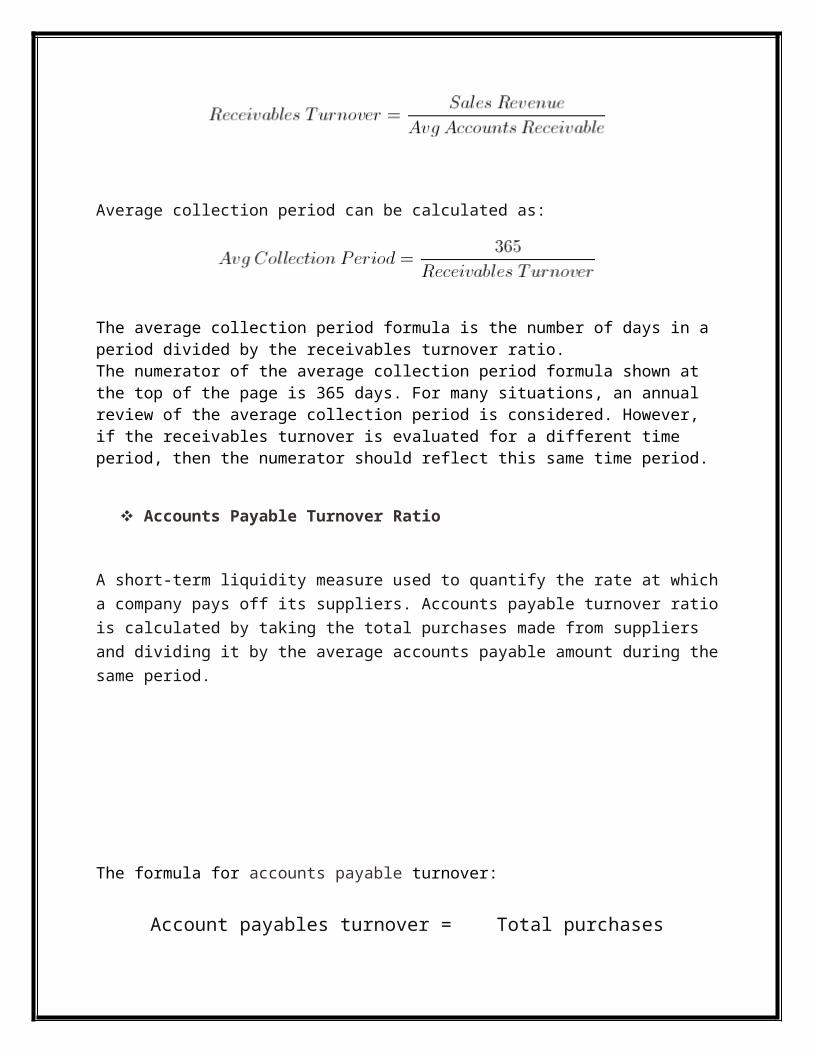

Receivables Turnover Ratio

An accounting measure used to quantify a firm's effectiveness in extending

credit as well as collecting debts. The receivables turnover ratio is an activity

ratio, measuring how efficiently a firm uses its assets.

The formula for receivables turnover:

Average collection period can be calculated as:

The average collection period formula is the number of days in a period divided by the receivables turnover ratio.The numerator of the average collection period formula shown at the top of the page is 365 days. For many situations, an annual review of the average collection period is considered. However, if the receivables turnover is evaluated for a different time period, then the numerator should reflect this same time period.

Accounts Payable Turnover Ratio

A short-term liquidity measure used to quantify the rate at which a company

pays off its suppliers. Accounts payable turnover ratio is calculated by taking

the total purchases made from suppliers and dividing it by the average

accounts payable amount during the same period.

The formula for accounts payable turnover:

Account payables turnover = Total purchases Average account payables

Average number of days payable outstanding can be calculated as:

Average number of days payable outstanding =

365

Accounts Payable Turnover

Working Capital Turnover

A measurement comparing the depletion of working capital to the generation

of sales over a given period. This provides some useful information as to how

effectively a company is using its working capital to generate sales.

The formula for working capital turnover:

Working capital turnover = Sales

Net working capital

The working capital turnover ratio measures how efficiently a business uses its working capital to produce sales. A higher ratio indicates greater efficiency. In general, a high ratio can help your company’s operations run more smoothly and limit the need for additional funding.

Long term activity ratio

Companies invest in fixed assets to create expected growth in sales. Fixed assets are long lived tangible assets that are used in production and administration. Long term activity ratios measure the quality of investment (in fixed assets) decisions. Long term activity ratios include the summary ratio which measures the efficiency in managing total assets.

Fixed-asset turnover ratio

Fixed-asset turnover is the ratio of sales (on the profit and loss account) to the value of fixed assets (on the balance sheet). It indicates how well the business is using its fixed assets to generate sales.

Generally speaking, the higher the ratio, the better, because a high ratio indicates the business has less money tied up in fixed assets for each unit of currency of sales revenue. A declining ratio may indicate that the business is over-invested in plant, equipment, or other fixed assets.

Asset turnover ratio

Asset turnover is a financial ratio that measures the efficiency of a company's use of its assets in generating sales revenue or sales income to the company.

Companies with low profit margins tend to have high asset turnover, while those with high profit margins have low asset turnover. Companies in the retail industry tend to have a very high turnover ratio due mainly to cutthroat and competitive pricing.

"Sales" is the value of "Net Sales" or "Sales" from the company's income statement

"Average Total Assets" is the average of the values of "Total assets" from the company's balance sheet in the beginning and the end of the fiscal period. It is calculated by adding up the assets at the beginning of the period and the assets at the end of the period, then dividing that number by two.

Liquidity ratios

Liquidity refers to the ability of a company to meet short term obligations when they are due for payment. Ratios that are used to measure liquidity are also known as working capital ratios, because they use current assets in the numerator and current liabilities in denominator.

Current ratio

The current ratio is a financial ratio that measures whether or not a firm has enough resources to pay its debts over the next 12 months. It compares a firm's current assets to its current liabilities. It is expressed as follows:

The current ratio is an indication of a firm's market liquidity and ability to meet creditor's demands. Acceptable current ratios vary from industry to industry and are generally between 1.5 and 3 for healthy businesses. If a company's current ratio is in this range, then it generally indicates good short-term financial strength. If current liabilities exceed current assets (the current ratio is below 1), then the company may have problems meeting its short-term obligations. If the current ratio is too high, then the company may not be efficiently using its current assets or its short-term financing facilities. This may also indicate problems in working capital management.

Quick ratio or acid test ratio

In finance, the Acid-test or quick ratio or liquid ratio measures the ability of a company to use its near cash or quick assets to extinguish or retire its current liabilities immediately. Quick assets include those current assets that presumably can be quickly converted to cash at close to their book values. A company with a Quick Ratio of less than 1 cannot currently fully pay back its current liabilities.

Notice that very often "Acid test" refers to Cash ratio, instead of Quick ratio:

Cash Ratio

The ratio of a company's total cash and cash equivalents to its current

liabilities. The cash ratio is most commonly used as a measure of company

liquidity. It can therefore determine if, and how quickly, the company can

repay its short-term debt. A strong cash ratio is useful to creditors when

deciding how much debt, if any, they would be willing to extend to the asking

party. Cash ratio is calculated using the following formula:

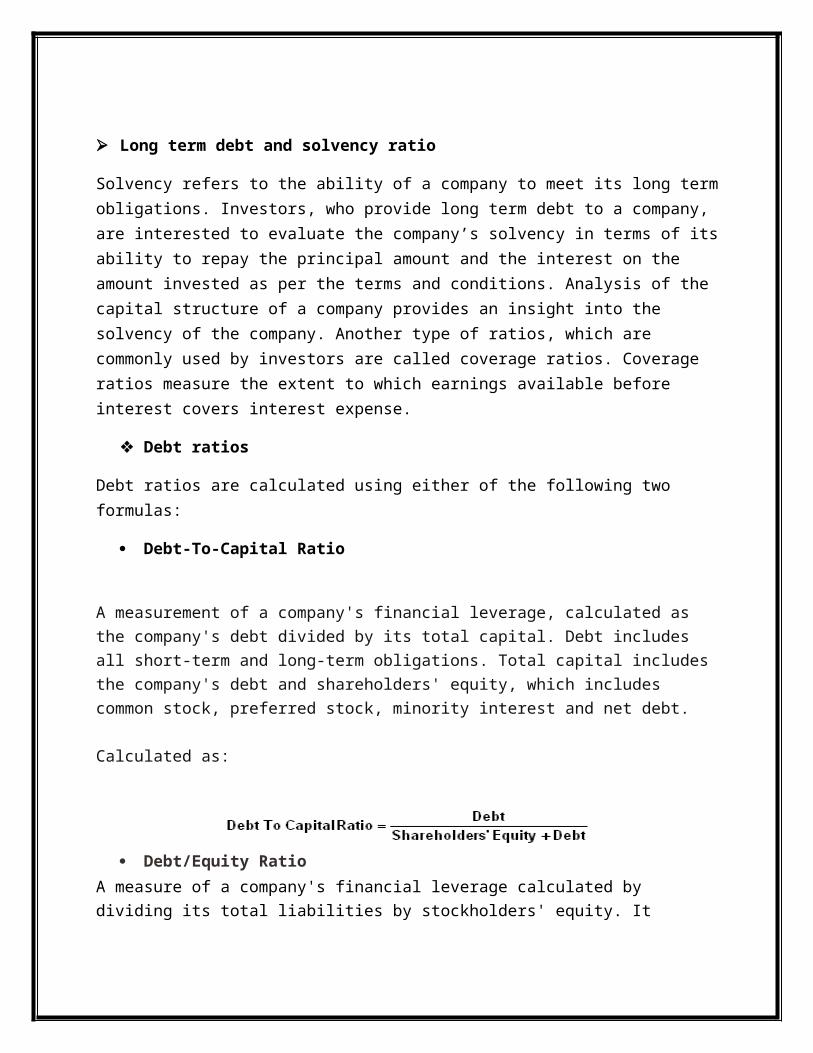

Long term debt and solvency ratio

Solvency refers to the ability of a company to meet its long term obligations. Investors, who provide long term debt to a company, are interested to evaluate the company’s solvency in terms of its ability to repay the principal amount and the interest on the amount invested as per the terms and conditions. Analysis of the capital structure of a company provides an insight into the solvency of the company. Another type of ratios, which are

Cash Ratio =Cash + Cash Equivalents

Current Liabilities

commonly used by investors are called coverage ratios. Coverage ratios measure the extent to which earnings available before interest covers interest expense.

Debt ratios

Debt ratios are calculated using either of the following two formulas:

Debt-To-Capital Ratio

A measurement of a company's financial leverage, calculated as the

company's debt divided by its total capital. Debt includes all short-term and

long-term obligations. Total capital includes the company's debt and

shareholders' equity, which includes common stock, preferred stock,

minority interest and net debt.

Calculated as:

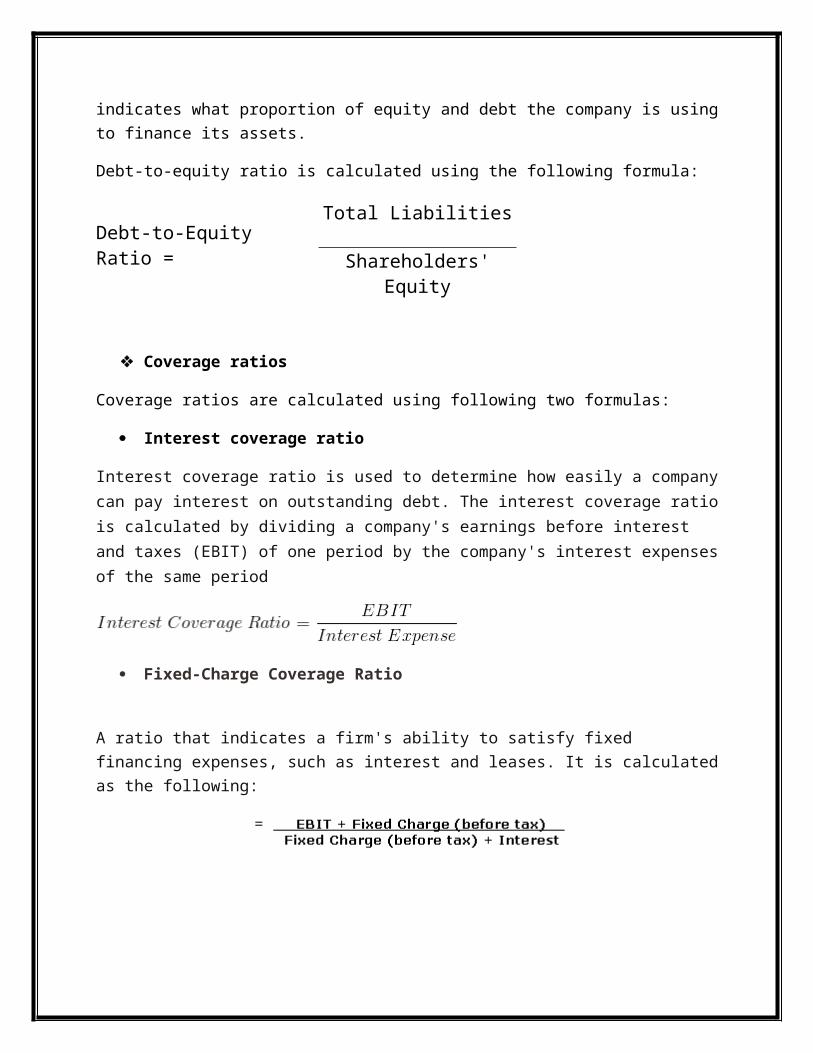

Debt/Equity Ratio

A measure of a company's financial leverage calculated by dividing its total

liabilities by stockholders' equity. It indicates what proportion of equity and

debt the company is using to finance its assets.

Debt-to-equity ratio is calculated using the following formula:

Debt-to-Equity Ratio =Total Liabilities

Shareholders' Equity

Coverage ratios

Coverage ratios are calculated using following two formulas:

Interest coverage ratio

Interest coverage ratio is used to determine how easily a company can pay interest on outstanding debt. The interest coverage ratio is calculated by

dividing a company's earnings before interest and taxes (EBIT) of one period by the company's interest expenses of the same period

Fixed-Charge Coverage Ratio

A ratio that indicates a firm's ability to satisfy fixed financing expenses, such

as interest and leases. It is calculated as the following:

Market evaluation analysis

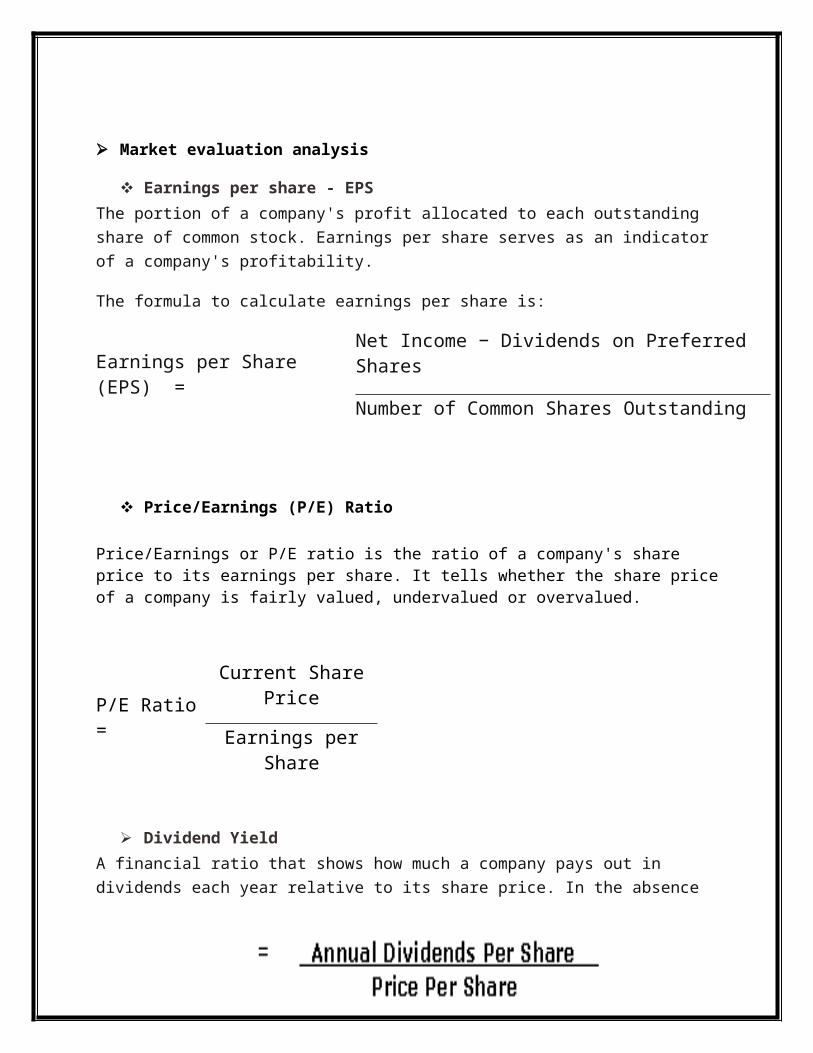

Earnings per share - EPS

The portion of a company's profit allocated to each outstanding share of

common stock. Earnings per share serves as an indicator of a company's

profitability.

The formula to calculate earnings per share is:

Earnings per Share (EPS) =

Net Income − Dividends on Preferred Shares

Number of Common Shares Outstanding

Price/Earnings (P/E) Ratio

Price/Earnings or P/E ratio is the ratio of a company's share price to its earnings per share. It tells whether the share price of a company is fairly valued, undervalued or overvalued.

P/E Ratio =

Current Share Price

Earnings per Share

Dividend Yield

A financial ratio that shows how much a company pays out in dividends each

year relative to its share price. In the absence of any capital gains, the

dividend yield is the return on investment for a stock. Dividend yield is

calculated as follows:

Dividend yield

Price to book value ratio

This ratio is computed with a view to revealing how the market evaluates the performances of the assets under the firm’s ownership and control. By means of this ratio financial analysts and investors want to determine whether the assets under present management are underperforming or overperforming.

This ratio is calculated as:

Price-to-book value ratio = Market price per share

Book value per share

If the ratio is greater than 1, it is inferred that the firm’s assets performed more than what market perceived about it. If it is less than 1, it is assumed that the assets are underperformed.

Earning yield

Investors are interested in the rate of earnings on their invested shares in terms of market price as it reveals markets’ expectations about the firm’s future earning capacity. Earning yield indicated by the following ratio:

Earning yield = Earning per share

Market price per share

2.4 Cash flow statement analysis

Introduction

As per AS-3, cash flow statement is to be drawn with the objective of providing users of financial statements “a basis to assess the ability of the enterprise to generate cash and cash equivalents and the needs of the enterprise to utilize those cash flows… and the timing and certainty of their generation”. It is also provided that this statement should classify cash flows during the period into three categories: cash flow from operating, investing and financing activities.

Such classification by itself is not sufficient to indicate cash generating capacity of an enterprise and how this capacity is utilized. This statement should be analyzed according to the needs of user groups. Various ratios have been suggested for analysis.

Objectives of analyzing cash flow statement

Cash flow statement is analyzed according to the needs of the decision-makers. As the needs vary from one decision-maker to another, not a single measure can serve all the purposes. But there is something in common, which most of the decision-makers interested in this statement want to analyze. Here are some major objectives of analyzing this statement are stated as follows:

To determine the cash generating capacity of the enterprise as a whole

To determine the main drivers of cash generation

To know the adequacy of cash flow from operating activities to meet long-term commitments

To know the sufficiency of the cash flow to pay dividends

Cash flow ratios and their classifications

A few ratios based on cash flow statements and other financial statements and their significances are as follows:

Liquidity analysis ratios

Cash flow (liquidity) ratio

Cash flow ratio measures the short term solvency of a business. It is computed as follows:

Cash flow ratio = Operating cash flow

Current liabilities

The higher the ratio, the higher the debt paying capacity of the business. Traditionally, current ratio is used to measure short-term solvency of a business. But cash flow ratio is considered a better substitute for current ratio.

Credit management analysis ratio

Cash collection ratio

Cash collection ratio indicates the speed of collecting dues from the customers. This ratio is derived as follows:

Cash collection ratio = Annual cash collection from customers × 100

Annual credit sales

This ratio reveals the percentage of annual credit sales realized in cash. The higher the percentage, the higher the cash collection efficiency. This ratio should be considered along with cash payment rate for measuring overall cash management efficiency. Collection from customers is the primary source of cash generation.

Cash payment ratio

Cash payment ratio indicates rate of cash outflow for obtaining cost of goods sold (excluding non-cash expenses like depreciation). This ratio is calculated as follows:

Cash payment ratio = Cash outflow to suppliers of goods and services

for producing cost of goods sold × 100

Cost of goods sold - Depreciation

Ratios for analyzing cash generating capacity by margin ratios

Cash flow margin

Cash flow margin ratio is computed to show the relationship between cash generated from operations and sales. The ratio is calculated as follows:

Cash flow margin = Cash flow from operating activities

Net sales

This measure indicates the ability of the enterprise to convert its sales into cash. The higher the ratio, the greater is the cash generating capacity of the business.

Cash gross margin

Cash gross margin ratio indicates the primary source of cash generation. Here are the two basic factors of cash inflows and outflows, i.e. cash from customers and cash payment for expenses are considered at a time. This ratio is calculated as follows:

Cash gross margin = Cash flow from customers – cash outflows to suppliers

Cash flow from customers

Cash flow ratio to analyze rate of return on assets

Cash return on assets

Cash return on assets measures the cash generating capacity of the assets of an enterprise. This ratio is defined as follows:

Cash return on assets = Cash flow from operating activities

Total assets

This ratio reveals the relation between generated cash and the funds invested in total assets. The higher the ratio, it is expected; the higher is the managerial efficiency in effective use of assets and transforming those uses in cash flows.

Analysis from the investor’s point of view

Cash flow per share

This measure indicates how much cash flow in per common share outstanding. This measure is usually considered better than earning per share measure. This is calculated as follows:

Cash flow per share = Operating cash flow - Preference dividend

Number of common shares outstanding

3. Industry profile

3.1 FMCG Industry

Introduction

Fast Moving Consumer Goods

Products which have a quick turnover, and relatively low cost are known as Fast Moving Consumer Goods (FMCG). FMCG products are those that get replaced within a year. Examples of FMCG generally include a wide range of frequently purchased consumer products such as toiletries, soap, cosmetics, tooth cleaning products, shaving products and detergents,

as well as other non-durables such as glassware, bulbs, batteries, paper products, and plastic goods. FMCG may also include pharmaceuticals, consumer electronics, packaged food products, soft drinks, tissue paper, and chocolate bars.

The FMCG Industry

The Indian FMCG sector is the fourth largest sector in the economy with a total market size in excess of US$ 13.1 billion. It has a strong MNC presence and is characterized by a well-established distribution network, intense competition between the organized and unorganized segments and low operational cost. Availability of key raw materials, cheaper labor costs and presence across the entire value chain gives India a competitive advantage.

The FMCG market is set to treble from US$ 11.6 billion in 2003 to US$ 33.4 billion in 2015. Penetration level as well as per capita consumption in most product categories like jams, toothpaste, skin care, hair wash etc. in India is low indicating the untapped market potential. Burgeoning Indian population, particularly the middle class and the rural segments, presents an opportunity to makers of branded products to convert consumers to branded products.

Growth is also likely to come from consumer 'upgrading' in the matured product categories. With 200 million people expected to shift to processed and packaged food by 2010, India needs around US$ 28 billion of investment in the food-processing industry.

Automatic investment approval (including foreign technology agreements within specified norms), up to 100 per cent foreign equity or 100 per cent for NRI and Overseas Corporate Bodies (OCBs) investment, is allowed for most of the food processing sector.

FMCG industry provides a wide range of consumables and accordingly the amount of money circulated against FMCG products is also very high. The competition among FMCG manufacturers is also growing and as a result of this, investment in FMCG industry is also increasing, specifically in India, where FMCG industry is regarded as the fourth largest sector with total market size of US$13.1 billion. FMCG Sector in India is estimated to grow 60% by 2010.

Common FMCG products

Some common FMCG product categories include food and dairy products, glassware, paper products, pharmaceuticals, consumer electronics, packaged food products, plastic goods, printing and stationery, household products, photography, drinks etc. and some of the examples of FMCG products are coffee, tea, dry cells, greeting cards, gifts, detergents, tobacco and cigarettes, watches, soaps etc.

Market potentiality of FMCG industry

Some of the merits of FMCG industry, which made this industry as a potential one, are low operational cost, strong distribution networks, presence of renowned FMCG companies. Population growth is another factor which is responsible behind the success of this industry.

Leading FMCG companies

Some of the well-known FMCG companies are Sara Lee, Nestlé, Reckitt Benckiser, Unilever, Procter & Gamble, Coca-Cola, Carlsberg, Kleenex, General Mills, Pepsi and Mars etc.

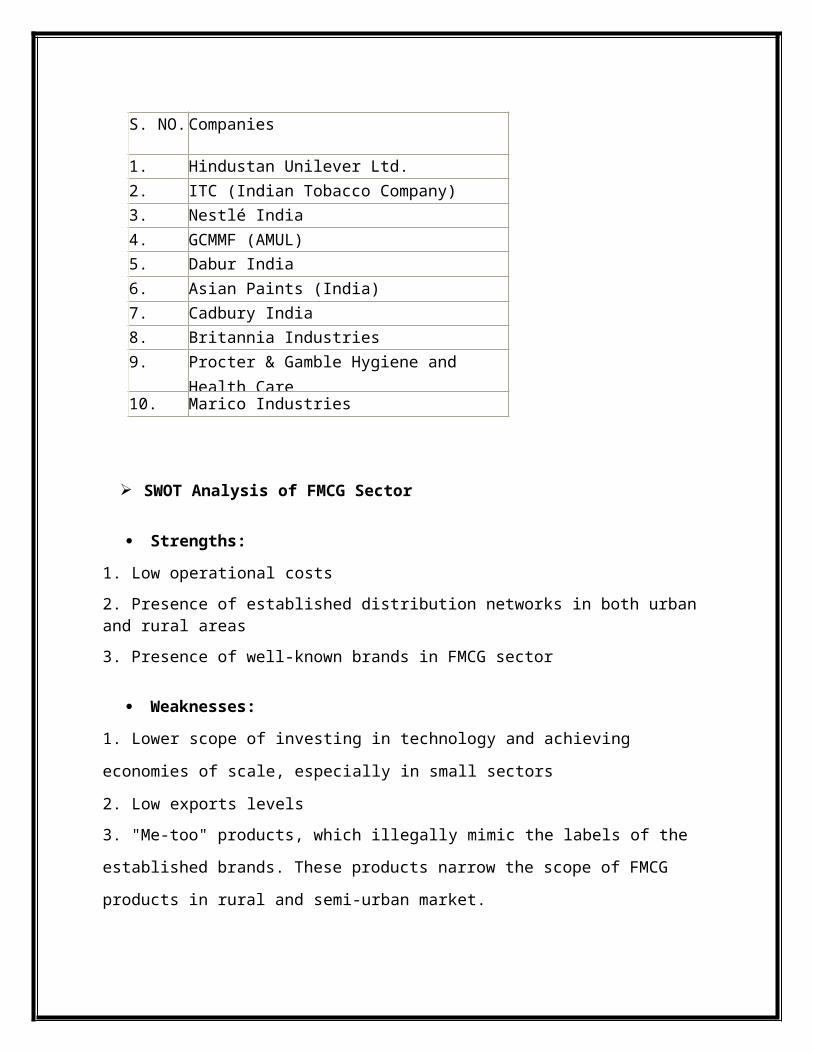

The top 10 companies in FMCG sectorS. NO. Companies

1. Hindustan Unilever Ltd.

2. ITC (Indian Tobacco Company)

3. Nestlé India

4. GCMMF (AMUL)

5. Dabur India

6. Asian Paints (India)

7. Cadbury India

8. Britannia Industries

9. Procter & Gamble Hygiene and Health Care

10. Marico Industries

SWOT Analysis of FMCG Sector

Strengths:

1. Low operational costs

2. Presence of established distribution networks in both urban and rural areas

3. Presence of well-known brands in FMCG sector

Weaknesses:

1. Lower scope of investing in technology and achieving economies of

scale, especially in small sectors

2. Low exports levels

3. "Me-too" products, which illegally mimic the labels of the established

brands. These products narrow the scope of FMCG products in rural and

semi-urban market.

Opportunities:

1. Untapped rural market

2. Rising income levels i.e. increase in purchasing power of consumers

3. Large domestic market- a population of over one billion.

4. Export potential

5. High consumer goods spending

Threats:

1. Removal of import restrictions resulting in replacing of domestic brands

2. Slowdown in rural demand

3. Tax and regulatory structure

4. Company profile

4.1 Hindustan Unilever Limited

Introduction

Hindustan Unilever Limited (HUL) is India's largest Fast Moving Consumer Goods Company with a heritage of over 80 years in India and touches the lives of two out of three Indians.

HUL works to create a better future every day and helps people feel good, look good and get more out of life with brands and services that are good for them and good for others.

With over 35 brands spanning 20 distinct categories such as soaps, detergents, shampoos, skin care, toothpastes, deodorants, cosmetics, tea, coffee, packaged foods, ice cream, and water purifiers, the Company is a part of the everyday life of millions of consumers across India. Its portfolio includes leading household brands such as Lux, Lifebuoy, Surf Excel, Rin, Wheel, Fair & Lovely, Pond’s, Vaseline, Lakmé, Dove, Clinic Plus, Sunsilk, Pepsodent, Closeup, Axe, Brooke Bond, Bru, Knorr, Kissan, Kwality Wall’s and Pureit.

The Company has over 16,000 employees and has an annual turnover of around Rs.25,206 crores (financial year 2012 - 2013). HUL is a subsidiary of Unilever, one of the world’s leading suppliers of fast moving consumer goods with strong local roots in more than 100 countries across the globe with annual sales of €51 billion in 2012. Unilever has 67.25% shareholding in HUL.

History

In the summer of 1888, visitors to the Kolkata harbour noticed crates full of Sunlight soap bars, embossed with the words "Made in England by Lever Brothers". With it, began an era of marketing branded Fast Moving Consumer Goods (FMCG).

Lifebuoy soap advertisement - cartoon boy rowing a lifebuoy soap boat soon after followed Lifebuoy in 1895 and other famous brands like Pears, Lux and Vim. Vanaspati was launched in 1918 and the famous Dalda brand came to the market in 1937.

In 1931, Unilever set up its first Indian subsidiary, Hindustan Vanaspati Manufacturing Company, followed by Lever Brothers India Limited (1933) and United Traders Limited (1935). These three companies merged to form HUL in November 1956; HUL offered 10% of its equity to the Indian public, being the first among the foreign subsidiaries to do so. Unilever now holds 67.25% equity in the company. The rest of the shareholding is distributed among about three lakh individual shareholders and financial institutions.

The erstwhile Brooke Bond's presence in India dates back to 1900. By 1903, the company had launched Red Label tea in the country. In 1912, Brooke Bond & Co. India Limited was formed. Brooke Bond joined the Unilever fold in 1984 through an international acquisition. The erstwhile Lipton's links with

India were forged in 1898. Unilever acquired Lipton in 1972 and in 1977 Lipton Tea (India) Limited was incorporated.

Pond's (India) Limited had been present in India since 1947. It joined the Unilever fold through an international acquisition of Chesebrough Pond's USA in 1986.

Since the very early years, HUL has vigorously responded to the stimulus of economic growth. The growth process has been accompanied by judicious diversification, always in line with Indian opinions and aspirations.

The liberalization of the Indian economy, started in 1991, clearly marked an inflexion in HUL's and the Group's growth curve. Removal of the regulatory framework allowed the company to explore every single product and opportunity segment, without any constraints on production capacity.

Simultaneously, deregulation permitted alliances, acquisitions and mergers. In one of the most visible and talked about events of India's corporate history, the erstwhile Tata Oil Mills Company (TOMCO) merged with HUL, effective from April 1, 1993. In 1996, HUL and yet another Tata company, Lakme Limited, formed a 50:50 joint venture, Lakme Unilever Limited, to market Lakme's market-leading cosmetics and other appropriate products of both the companies. Subsequently in 1998, Lakme Limited sold its brands to HUL and divested its 50% stake in the joint venture to the company.

HUL formed a 50:50 joint venture with the US-based Kimberly Clark Corporation in 1994, Kimberly-Clark Lever Ltd, which markets Huggies Diapers and Kotex Sanitary Pads. HUL has also set up a subsidiary in Nepal, Unilever Nepal Limited (UNL), and its factory represents the largest manufacturing investment in the Himalayan kingdom. The UNL factory manufactures HUL's products like Soaps, Detergents and Personal Products both for the domestic market and exports to India.

The 1990s also witnessed a string of crucial mergers, acquisitions and alliances on the Foods and Beverages front. In 1992, the erstwhile Brooke Bond acquired Kothari General Foods, with significant interests in Instant Coffee. In 1993, it acquired the Kissan business from the UB Group and the Dollops Icecream business from Cadbury India.

As a measure of backward integration, Tea Estates and Doom Dooma, two plantation companies of Unilever, were merged with Brooke Bond. Then in 1994, Brooke Bond India and Lipton India merged to form Brooke Bond Lipton India Limited (BBLIL), enabling greater focus and ensuring synergy in

the traditional Beverages business. 1994 witnessed BBLIL launching the Wall's range of Frozen Desserts. By the end of the year, the company entered into a strategic alliance with the Kwality Icecream Group families and in 1995 the Milkfood 100% Icecream marketing and distribution rights too were acquired.

Finally, BBLIL merged with HUL, with effect from January 1, 1996. The internal restructuring culminated in the merger of Pond's (India) Limited (PIL) with HUL in 1998. The two companies had significant overlaps in Personal Products, Speciality Chemicals and Exports businesses, besides a common distribution system since 1993 for Personal Products. The two also had a common management pool and a technology base. The amalgamation was done to ensure for the Group, benefits from scale economies both in domestic and export markets and enable it to fund investments required for aggressively building new categories.

In January 2000, in a historic step, the government decided to award 74 per cent equity in Modern Foods to HUL, thereby beginning the divestment of government equity in public sector undertakings (PSU) to private sector partners. HUL's entry into Bread is a strategic extension of the company's wheat business. In 2002, HUL acquired the government's remaining stake in Modern Foods.

In 2003, HUL acquired the Cooked Shrimp and Pasteurised Crabmeat business of the Amalgam Group of Companies, a leader in value added Marine Products exports.

HUL launched a slew of new business initiatives in the early part of 2000’s. Project Shakti was started in 2001. It is a rural initiative that targets small villages populated by less than 5000 individuals. It is a unique win-win initiative that catalyzes rural affluence even as it benefits business. Currently, there are over 45,000 Shakti entrepreneurs covering over 100,000 villages across 15 states and reaching to over 3 million homes.

In 2002, HUL made its foray into Ayurvedic health & beauty centre category with the Ayush product range and Ayush Therapy Centres. Hindustan Unilever Network, Direct to home business was launched in 2003 and this was followed by the launch of ‘Pureit’ water purifier in 2004.

In 2007, the Company name was formally changed to Hindustan Unilever Limited after receiving the approval of shareholders during the 74th AGM on

18 May 2007. Brooke Bond and Surf Excel breached the the Rs 1,000 crore sales mark the same year followed by Wheel which crossed the Rs.2, 000 crore sales milestone in 2008.

On 17th October 2008, HUL completed 75 years of corporate existence in India.

In January 2010, the HUL head office shifted from the landmark Lever House, at Backbay Reclamation, Mumbai to the new campus in Andheri (E), Mumbai.

On 15th November, 2010, the Unilever Sustainable Living Plan was officially launched in India at New Delhi.

In March, 2012 HUL’s state of the art Learning Centre was inaugurated at the Hindustan Unilever campus at Andheri, Mumbai.

Company structure

Hindustan Unilever Limited is India's largest Fast Moving Consumer Goods (FMCG) company. It is present in Home & Personal Care and Foods & Beverages categories. HUL has over 16,500 employees, including over 1500 managers

The fundamental principle determining the organization structure is to infuse speed and flexibility in decision-making and implementation, with empowered managers across the company’s nationwide operations.

Board of Directors

The Board of Directors of the Company represents an optimum mix of professionalism, knowledge and experience. The total strength of the Board of Directors of the Company is eight Directors, comprising Non-Executive Chairman, three Executive Directors and four Non-Executive Independent Directors.

Management Committee

The day-to-day management of affairs of the Company is vested with the Management Committee which is subjected to the overall superintendence and control of the Board.

Product Portfolio Home and Personal Care

Personal Wash

Lux Lifebuoy Liril Hamam Breeze Dove Pears Rexona

Laundry

Surf Excel Rin Wheel

Hair Care

Sunsilk Clinic Plus

Skin Care

Fair & Lovely

Pond’s Vaseline Aviance

Oral Care

Pepsodent Close Up

Deodorants

Axe Rexona

Color Cosmetics

Lakme

Food

Tea

Brooke Bond Lipton

Coffee

Bru

Foods

Kissan Annapurna Knoor

Ice Cream

Kwality Wall’s

Hindustan Unilever Limited (HUL) is India's largest Fast Moving Consumer Goods Company, touching the lives of two out of three Indians with over 20 distinct categories in Home & Personal Care Products and Foods & Beverages. They endow the company with a scale of combined volumes of about 4 million tones and sales of nearly Rs.13718 crores. HUL is also one of the country's largest exporters; it has been recognized as a Golden Super Star Trading House by the Government of India.

The mission that inspires HUL's over 15,000 employees, including over 1,300 managers, is to "add vitality to life." HUL meets every day needs for nutrition, hygiene, and personal care with brands that help people feel good, look good and get more out of life. It is a mission HUL shares with its parent company, Unilever, which holds 52.10% of the equity. The rest of the shareholding is distributed among 360,675 individual shareholders and financial institutions.

HUL's brands - like Lifebuoy, Lux, Surf Excel, Rin, Wheel, Fair & Lovely, Pond's, Sunsilk, Clinic, Pepsodent, Close-up, Lakme, Brooke Bond, Kissan, Knorr-Annapurna, Kwality Wall's – are household names across the country and span many categories - soaps, detergents, personal products, tea, coffee, branded staples, ice cream and culinary products. They are manufactured over 37 factories across India. The operations involve over 2,000 suppliers and associates. HUL's distribution network comprises of about 2, 500 redistribution stockiest, covering 6.3 million retail outlets reaching the entire urban population, and about 250 million rural consumers.

HUL has traditionally been a company, which incorporates latest technology in all its operations. The Hindustan Unilever Research Centre (HURC) was set up in 1958, and now has facilities in Mumbai and Bangalore. HURC and the Global Technology Centers in India have over 200 highly qualified scientists and technologists, many with post-doctoral experience acquired in the U.S and Europe. HUL believes that an organization’s worth is also in the service it renders to the community. HUL is focusing on health & hygiene education, women empowerment, and water It is also involved in education and rehabilitation of special or underprivileged children, care for the destitute and HIV-positive, and rural development. HUL has also responded in case of national calamities / adversities and contributes through various welfare measures, most recent being the village built by HUL in earthquake affected

Gujarat, and relief & rehabilitation after the Tsunami caused devastation in South India.

In 2007, Hindustan Unilever was rated as the most respected company in India for the past 25 years by Business world, one of India’s leading business magazines. The rating was based on a compilation of the magazine’s annual survey of India’s Most Reputed Companies over the past

25 years. HUL is the market leader in Indian consumer products with presence in over 20 consumer categories such as soaps, tea, detergents and shampoos amongst others with over 700 million Indian consumers using its products. It has over 35 brands. Sixteen of HUL’s brands featured in the ACNielsen Brand Equity list of 100 Most Trusted Brands Annual Survey (2008). According to Brand Equity, HUL has the largest number of brands in the Most Trusted Brands List. It’s a company that has consistently had the largest number of brands in the Top 50 and in the Top 10 (with 4 brands).

Hindustan Unilever's distribution covers over 1 million retails outlets across India directly and its products are available in over 6.3 million outlets in India, i.e., nearly 80% of the retail outlets in India. It has 39 factories in the country. Two out of three Indians use the company’s products and HUL products have the largest consumer reach being available in over 80 per cent of consumer homes across India.

SWOT Analysis of Hindustan Unilever Limited

Strengths:

Strong company image

Strong brand portfolio

Success of the slogan

Quantity & variety

Effective & attractive packaging

High quality man power

Solid base of the company

Innovative aspects

Corporate behavior

Health & personal care products

Help people getting more out of life

Weaknesses:

High prices of products

Substitute products

Policy of spending for the social responsibility

Lack of control in the market

Dual leadership

Decrease in revenues

Reduced spending for research & development

Opportunities:

Changing life style of people

New markets

Increase the volume of production Focus on R&D Low income consumers

Threats:

Competitors (P&G,)

Political effects

Legislative effect

Environmental effect

Economic crises

Obstacle faced

Change in life style of people

Financial highlights of HUL

Consolidated Profit and Loss Statement Rs.Crores

Year ended31st march

2012

Year ended31st march

2013Revenue from operations 23,436.33 27,003.99

Other income 259.62 532.03

Total 23,695.95 27,536.02

Operating expenses (13,704.24) 15,525.48

Other expenses (6,250.18) 7,298.91

Profit before depreciation and taxes 3,741.53 4,711.63

Depreciation and amortization (233.54) 251.32

Profit before taxation and extraordinary items 3,507.99 4,460.31Extraordinary items 113.69 605.72

Profit before tax 3,621.68 5,066.03

Taxation for the year-current tax-deferred taxTax adjustment of previous year(net)

(832.21)2.608.07

(1241.20)1.39

15.93Profit before minority interests 2,800.14 3839.37

Minority interests (9.48) (10.39)

Net profit 2790.66 3828.98

*figures shown in brackets are deductions

Horizontal (Comparative) analysis of profit and loss statement

Rs.CroresYear ended31st march2011

Year ended31st march2012

AbsoluteChange

(%) change

Revenue from operations 23,436.33

Other income 259.62

Total 23,695.95

Operating expenses (13,704.24)

Other expenses (6,250.18)

Profit before depreciation and taxes

3,741.53

Depreciation and amortization (233.54)

Profit before taxation and extraordinary items 3,507.99Extraordinary items 113.69

Profit before tax 3,621.68

Taxation for the year-current tax-deferred taxTax adjustment of previous year(net)

(832.21)2.608.07

Profit before minority interests 2,800.14

Minority interests (9.48)

Net profit 2790.66

Interpretation:

5. Data analysis and Interpretation

5.2 Horizontal (Comparative) analysis of profit and loss statement

Rs.CroresYear ended31st march2012

Year ended31st march 2013

AbsoluteChange

(%) change

Revenue from operations 23,436.33

27,003.99 3,567.66 15.22

Other income 259.62 532.03 272.41 104.93

Total 23,695.95

27,536.02 3,840.07 16.21

Operating expenses (13,704.24)

(15,525.48)

1,821.24 13.28

Other expenses (6,250.18)

(7,298.91) 1,048.73 16.78

Profit before depreciation and taxes

3,741.53 4,711.63 970.10 25.92

Depreciation and amortization (233.54) (251.32) 17.78 7.61

Profit before taxation and extraordinary items 3,507.99 4,460.31 952.32 27.15Extraordinary items 113.69 605.72 492.03 432.78

Profit before tax 3,621.68 5,066.03 1,444.35 39.88

Taxation for the year-current tax-deferred taxTax adjustment of previous year(net)

(832.21)2.608.07

(1241.20)(1.39)15.93

408.99(-)3.99

7.86

49.15(-)153.46

97.39Profit before minority interests 2,800.14 3839.37 1,039.23 37.11

Minority interests (9.48) (10.39) 0.91 9.60

Net profit 2790.66 3828.98 1038.32 37.56

Interpretation:

From the comparative analysis of profit and loss statement it is observed that almost all elements of the statement are showing positive change. The

above analysis shows that operating revenue has grown by 15.22% from the previous year. Operating expenses has grown by 13.28% and Depreciation and amortization expenses by 7.61%. Therefore, overall net profit has grown by 37.56%.

Horizontal (Comparative) analysis of Balance SheetRs.Crores

As at31st

March, 2011

As at31st

March,2012

Absolutechange

(%) change

Equity and Liabilities Shareholder’s fund

Share Capital 216.15Reserves and Surplus 3,464.93

Minority interest 18.30 Non-current liabilities

Long term borrowings -Other long term liabilities 331.67Long term provisions 674.30

Current liabilitiesShort term borrowings -Trade payable 4,843.87Other current liabilities 564.36Short term provisions 1,293.67

Total 11,407.25

Assets Non-current assets

Fixed assets Tangible assets 2,232.91 Intangible assets 29.95 Capital work-in-progress 217.32 Intangible asset under

development 10.32Non-current investment 70.25Deferred tax assets(net) 209.91Long term loans and advances 385.91Other non-current assets -

Current assetsMarketable investment 2,251.91Inventories 2,667.37Trade receivables 856.74Cash and bank balances 1,996.43Short term loans and advances 441.02Other current assets 37.21Total 11,407.2

5

5.4 Horizontal (Comparative) analysis of Balance SheetRs.Crores

As at31st

March, 2012

As at31st

March,2013

Absolutechange

(%) change

Equity and Liabilities Shareholder’s fund

Share Capital 216.15 216.25 0.10 0.05Reserves and Surplus 3,464.93 2,648.52 (-)816.41 (-)23.56

Minority interest 18.30 20.86 2.56 13.98

Non-current liabilitiesLong term borrowings - 8.44 8.44 -

Other long term liabilities 331.67 482.12 150.45 45.36Long term provisions 674.30 710.13 35.83 5.31

Current liabilitiesShort term borrowings - 16.30 16.30 -

Trade payable 4,843.87 5,341.74 497.87 10.28Other current liabilities 564.36 659.11 94.75 16.79Short term provisions 1,293.67 1,988.37 694.70 53.70

Total 11,407.25

12,091.84

684.59 6.00

Assets Non-current assets

Fixed assets Tangible assets 2,232.91 2,395.32 162.41 7.27 Intangible assets 29.95 36.11 6.16 20.56 Capital work-in-progress 217.32 212.10 5.22 2.40 Intangible asset under

development 10.32 10.32 - -Non-current investment 70.25 395.32 325.07 462.73Deferred tax assets(net) 209.91 208.52 (-)1.39 (-)0.66Long term loans and advances 385.91 421.64 35.73 9.25Other non-current assets - 296.85 296.85 -

Current assetsMarketable investment 2,251.91 1,857.02 (-)394.89 (-)17.53Inventories 2,667.37 2,705.97 38.6 1.45Trade receivables 856.74 996.53 139.79 16.32Cash and bank balances 1,996.43 1,900.71 95.72 4.79Short term loans and advances 441.02 581.98 140.96 31.96Other current assets 37.21 73.45 36.24 97.39

Total 11,407.25

12,091.84

684.59 6.00

Interpretation:

Balance sheet analysis also shows the positive figures except certain elements. Share capital has grown by 0.05%, however, Reserves and surplus are showing decline in their amount by 23.56%. Tangible assets have grown by 7.27%. Non-current investment has grown by 462.73%.