Embed Size (px)

Citation preview

2004

LIBERIA

NIGERIA

CHAD SUDAN

CAM

EROO

N

CENTRAL AFRICANREPUBLIC

ETHIOPIA

KENYAUGANDA

RWANDABURUNDIC

ON

GO

GABON

ANGOLA

TANZANIA

MOZA

MBI

QUE

DEM. REP.OF CONGO

EQUATORIAL GUINEA

MALAW I

GUINEA

SIERRA LEONE

GH

ANA

TOGO

BENI

N

THE AFRICAN PROGRAMME FOR ONCHCERCIASIS CONTROL (APOC) THE AFRICAN PROGRAMME FOR ONCHCERCIASIS CONTROL (APOC)

MANAGEMENT OF APOC FUNDSMANAGEMENT OF APOC FUNDSBY THE BY THE NOTFsNOTFs ::

Financial and Administrative ProceduresFinancial and Administrative Procedures

2004

LIBERIA

NIGERIA

CHAD SUDAN

CAM

EROO

N

CENTRAL AFRICANREPUBLIC

ETHIOPIA

KENYAUGANDA

RWANDABURUNDIC

ON

GO

GABON

ANGOLA

TANZANIA

MOZA

MBI

QUE

DEM. REP.OF CONGO

EQUATORIAL GUINEA

MALAW I

GUINEA

SIERRA LEONE

GH

ANA

TOGO

BENI

N

LIBERIA

NIGERIA

CHAD SUDAN

CAM

EROO

N

CENTRAL AFRICANREPUBLIC

ETHIOPIA

KENYAUGANDA

RWANDABURUNDIC

ON

GO

GABON

ANGOLA

TANZANIA

MOZA

MBI

QUE

DEM. REP.OF CONGO

EQUATORIAL GUINEA

MALAW IMALAW I

GUINEA

SIERRA LEONE

GUINEA

SIERRA LEONE

GH

ANA

TOGO

BENI

N

GH

ANA

TOGO

BENI

N

THE AFRICAN PROGRAMME FOR ONCHCERCIASIS CONTROL (APOC) THE AFRICAN PROGRAMME FOR ONCHCERCIASIS CONTROL (APOC)

MANAGEMENT OF APOC FUNDSMANAGEMENT OF APOC FUNDSBY THE BY THE NOTFsNOTFs ::

Financial and Administrative ProceduresFinancial and Administrative Procedures

2

MANAGEMENT OF APOC FUNDS BY THE NOTFS :

FINANCIAL AND ADMINISTRATIVE PROCEDURES

ACKNOWLEDGEMENTS

The Management of The African Programme for Onchocerciasis Control (WHO/APOC) based in Ouagadougou, Burkina Faso gratefully acknowledges the Financial and Technical support provided by the Onchocerciasis Coordination Unit of the World Bank toward the completion of this manual. The Management also acknowledges the World Health Organization (WHO) who’s Imprest System of Accounting has been adopted in sections of this manual; and the input of the WHO/APOC Staff for their invaluable contribution and commitment to proper financial accountability and reporting.

3

In accordance with the provisions of the Memorandum for the African Programme for Onchocerciasis Control (APOC) signed by the Governments of the Participating Countries, the Donor Community as well as all partnering institutions, and within the specific framework of the institutional and administrative arrangements described in the different “Letters of Agreement”, the following procedures shall, henceforth, govern the financial and administrative management of funds made available to the National Onchocerciasis Task Forces (NOTFs) enabling them to successfully carry out their operational objectives . The “Letters of Agreement” for APOC projects should be made available to all Stakeholders. As the Project Accounting Officers/Administrative Assistants are responsible for tracking the approved budget included in the “Letter of Agreement”, a copy must always be provided to them to ensure timely preparation and submission of returns to the Management of APOC.

4

PREFACE

This manual is designed for use as a reference guide on administrative and financial procedures for all the African Programme for Onchocerciasis Control (APOC) projects, and for training courses on the World Health Organization (WHO/APOC) Imprest System of Accounting. The manual, based on material progressively developed over the past several years by the World Health Organisation, is adapted to respond to specific needs of the African Programme for Onchocerciasis Control. This manual aims to present broad coverage of the WHO Imprest System of Accounting by describing the required techniques to be used by all APOC project accountants. The specific process to be followed to fulfil the accounting requirement of submitting the returns may vary from country to country and may also differ among APOC projects within a country due to the specificity of the Projects concerned The manual is designed to provide only the core material for the WHO Imprest System of Accounting and should be supplemented with specific instructions relating to the particular administrative and financial set-up of the country projects. The Management of APOC programme based in Ouagadougou, Burkina Faso will be the main source of additional materials and instructions where necessary. This includes specific guidelines on the use of this manual by the OCP Special Intervention Zones and other establishments such as Non-Governmental Development Organizations. The manual is divided into four Sections.

• Section 1 provides an introduction to the Financial and Administrative set up of APOC and the Letter of Agreement. This section also presents key definitions that will be found when using the Imprest System of Accounting.

• Section 2 focuses on the Accounting Guidelines developed for all APOC funded projects.

This section presents the mechanism to be used in the management of funds by projects and mechanisms for monitoring transactions.

• Section 3 provides the administrative guidelines and audit requirements that examine

expenditure per budget line item and addresses the question of how to spend more wisely. It examines expenditure planning and the formulation of each budget line item including the utilisation of capital equipment.

• Section 4 provides details on how to perform monthly closures to ensure timely submission

of returns to APOC management.

• Section 5 provides an overview of the financial reporting requirements for APOC projects.

5

TABLE OF CONTENTS

SECTION 1

INTRODUCTION............................................................................................................................ 6 Basic information on the APOC Administrative and Financial Structure ............................ 6 Basic information on the Imprest Accounting System.......................................................... 7 Key definitions found in the Imprest Accounting System .................................................... 7

THE LETTER OF AGREEMENT ................................................................................................ 10 Purpose.................................................................................................................................. 10 Period covered....................................................................................................................... 10 Financial Agreements and Amounts ..................................................................................... 10 Reporting Requirements........................................................................................................ 11 Sample Letter of Agreement .................................................................................................. 12 Common Misinterpretations of the Letter of Agreement....................................................... 15

SECTION 2

ACCOUNTING GUIDELINES...................................................................................................... 16 THE IMPREST ACCOUNTING DOCUMENTS AND FORMS

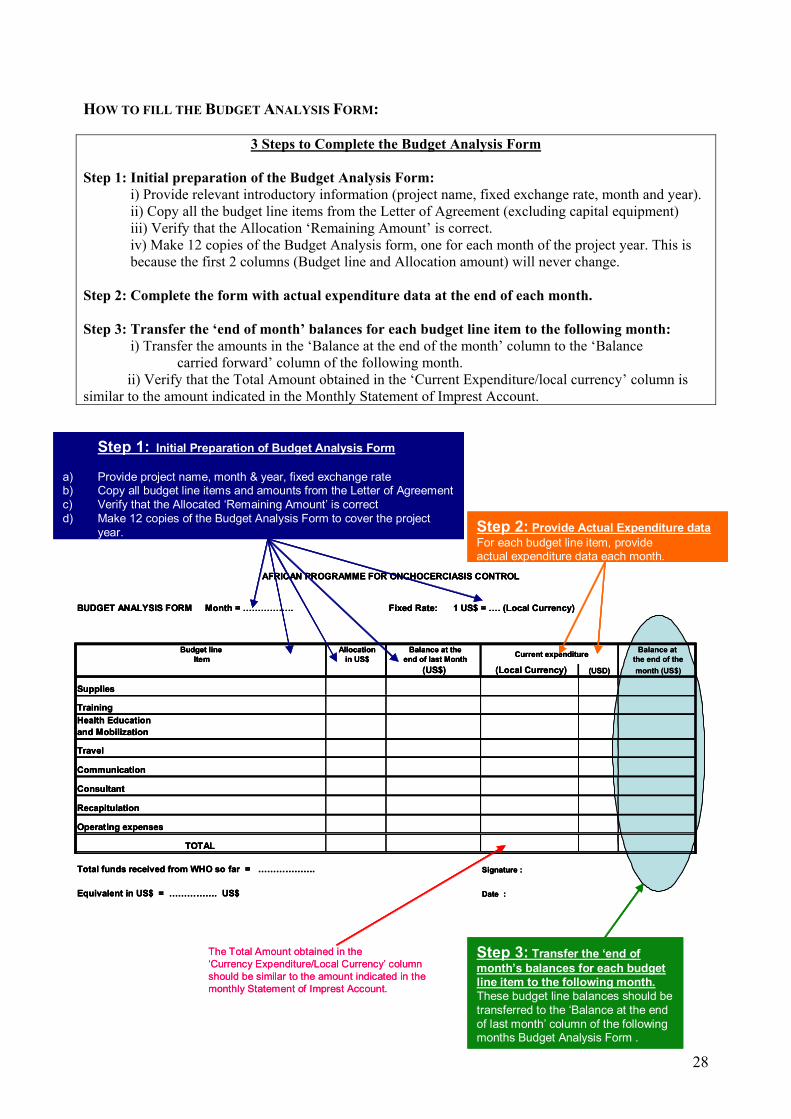

Imprest Voucher.................................................................................................................... 16 Cash book.............................................................................................................................. 18 Monthly Statement of Imprest Account ................................................................................ 23 Budget Analysis Form........................................................................................................... 27

SECTION 3

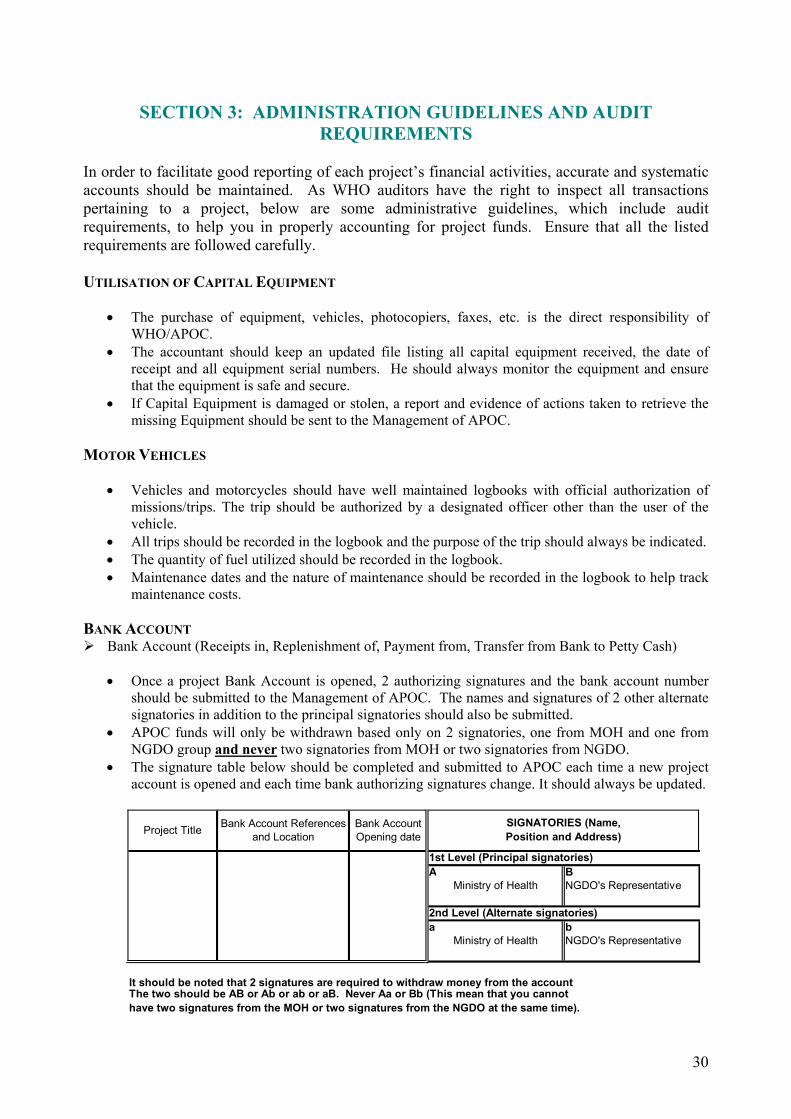

ADMINISTRATION GUIDELINES AND AUDIT REQUIREMENTS .................................... 30

Utilisation of Capital Equipment .......................................................................................... 30 Motor Vehicles...................................................................................................................... 30 Bank Account ....................................................................................................................... 30 Petty Cash ............................................................................................................................ 31 Operating expenses .............................................................................................................. 31 Per diems............................................................................................................................... 31 Travel and Training............................................................................................................... 31 Supplies and stationery ......................................................................................................... 32 Telephone.............................................................................................................................. 32

SECTION 4

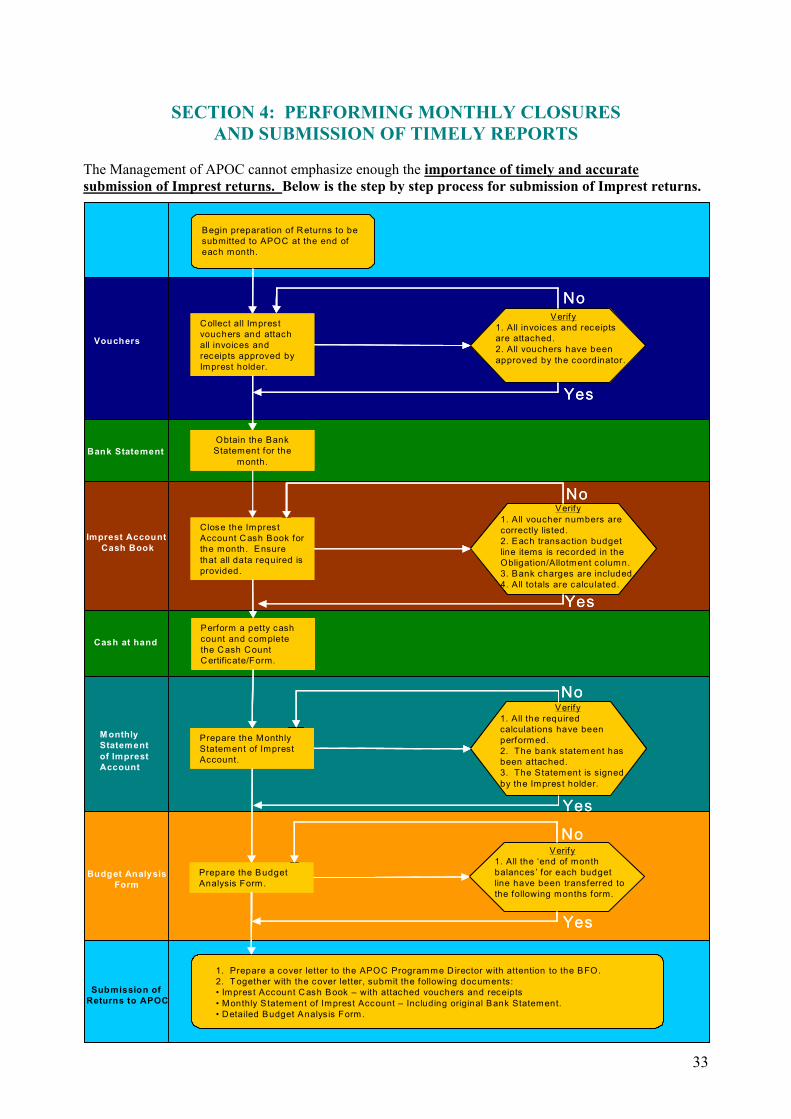

PERFORMING MONTHLY CLOSURES AND SUBMISSION OF TIMELY REPORTS ... 33

Preparing the Imprest Account Cash Book Verification of Petty cash Reconciliation of the Bank Account Preparing the Monthly Statement of Imprest Account Preparing the Budget Analysis Form Submission of Returns to APOC

SECTION 5

FINANCIAL REPORTING REQUIREMENTS FOR APOC PROJECTS............................... 35

6

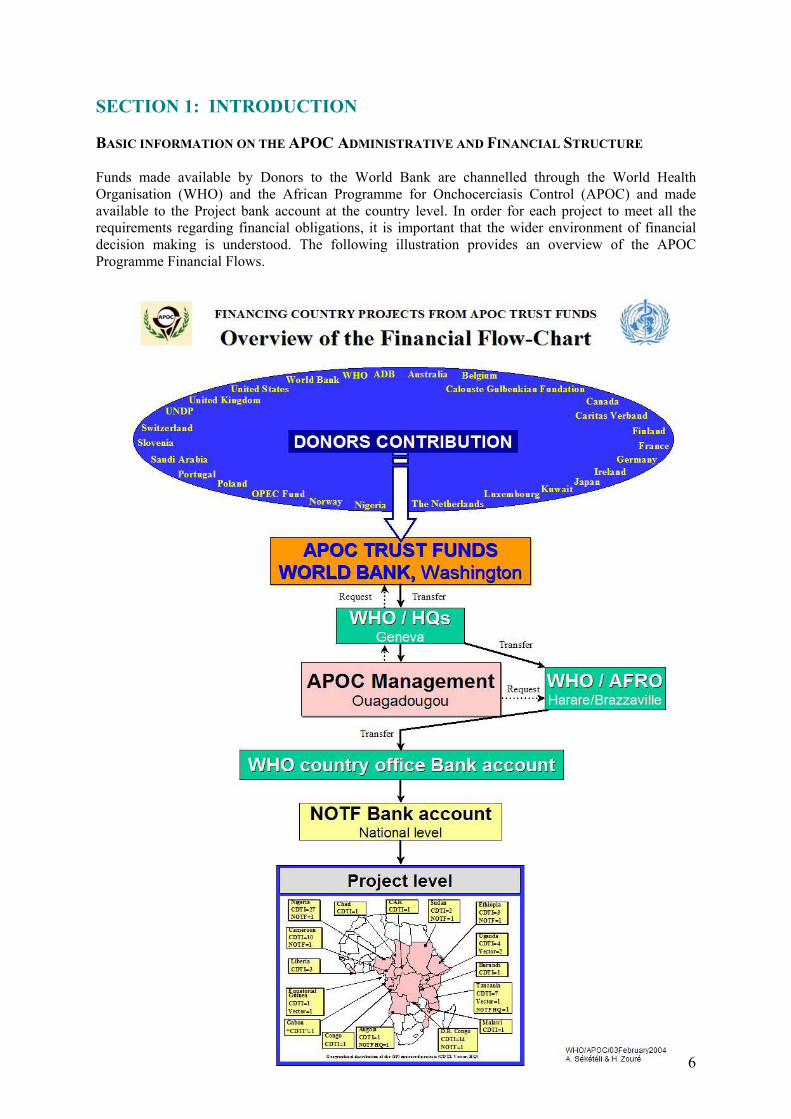

SECTION 1: INTRODUCTION BASIC INFORMATION ON THE APOC ADMINISTRATIVE AND FINANCIAL STRUCTURE Funds made available by Donors to the World Bank are channelled through the World Health Organisation (WHO) and the African Programme for Onchocerciasis Control (APOC) and made available to the Project bank account at the country level. In order for each project to meet all the requirements regarding financial obligations, it is important that the wider environment of financial decision making is understood. The following illustration provides an overview of the APOC Programme Financial Flows.

7

Governing the financial and administrative management of funds made available to the National Onchocerciasis Task Forces (NOTFs) is the Letter of Agreement (LOA) signed between WHO/APOC and the NOTF/MOH of the APOC participating country. The LOA spells out the institutional and administrative arrangements the NOTF needs to carry out to ensure that the projects operational objectives are met successfully.

BASIC INFORMATION ON THE IMPREST ACCOUNTING SYSTEM Imprest is the advance given by WHO/APOC to the NOTF for expenses to be made during a given period (generally quarterly or semi-annually). All expenses made by using the imprest account should be justified monthly through the use of accounting documents. The WHO Imprest Accounting System was developed in accordance with WHO imprest accounting procedures, as outlined in the WHO Manual, “Finance and Accounts: Imprest Accounts.” The WHO Imprest Accounting System is designed to perform all accounting tasks ranging from recording daily accounting transactions (Page 16 of this manual) to performing monthly closures (Page 32 of this manual). KEY DEFINITIONS AND PRINCIPLE RULES FOUND IN THE WHO IMPREST ACCOUNTING SYSTEM In order to harmonize the administrative and accounting practices, the following terms are mainly used in WHO/APOC documents in relation to the Imprest Accounting System. 1. Bank Account In the execution of field operations, funds are made available to the NOTFs on the basis of the estimated expenditures contained in the budget and annexed to the Letters of Agreement. These funds represent WHO/APOC assets and are covered by the legal provisions of the WHO. Principle rules and requirements for the Bank Account: a) The bank account at the country level should be operated jointly by two signatories whose specimen signatures should be deposited at the Project’s bank. The imprest is to be operated by cheque or through the petty cash. b) All debits and credits should be followed-up and cleared promptly. c) The account name notation should be as follows:

• NOTF/ WHO-APOC • Name of Country

d) A monthly bank statement is required and must be reconciled with the monthly statement of the imprest account. 2. Petty Cash

Petty Cash is the cash on hand or in the safe which is made available from the bank account to the project and is used to pay for small expenditures related to operating costs. The National Coordinator is accountable for the money in the Petty Cash. These funds are also covered by the legal provisions of WHO.

8

Principle rules and requirements for Petty Cash: a) The maximum amount allowable in the petty cash should be the local currency equivalent of USD 200. If the petty cash amount is more than USD 200 in local currency at the monthly closures, detailed justification must be provided explaining the amount recorded in the cash count certificate and the amount of advances provided to decentralized implementers of activities yet to be accounted for. b) Unauthorized expenditures should not be paid from the Petty Cash. This includes advances paid for per diem without proper authorization or justification. c) All large advances or payments to contractors should be made by cheque from the Bank Account and not through petty cash. It is not advisable to have a lot of cash in the safe except when paying per diem to participants of a meeting or paying top-ups at the end of each month. If not, the justification should be the amount of advances provided to decentralized implementers. d) A Cash Count Form/Certificate (see point 2.1) should be filled at the end of every month, and after approval, signed by the national coordinator. This form should be made available to the auditors or any supervisor if required. 2.1 The Cash-Count Form/Certificate (CCC) a) The cash count certificate is used to confirm the current amount available in petty cash at the end of each month. It is a list used to take stock of the available petty cash each month. b) The petty cash amount indicated on the cash count certificate must be shown in terms of bank notes and coins available. It is not advisable to keep your personal cash in the project safe, therefore ensure that the cash count conducted is for project petty cash only. c) The cash count certificate should always be cosigned by the coordinator and the accountant at the end of every month and it should reconcile with the amount indicated in the petty cash column of the cash book. 3. Imprest Account As described earlier, the advance given by WHO/APOC to the NOTF for expenses to be made during a given period is called imprest. WHO/APOC approves and effects the replenishment of the imprest account. Additional definitions, principles, rules and requirements 3.1 The Imprest Holder a) The National Coordinator is normally the Imprest Holder and is the person accountable to WHO/APOC and to his Government for the funds made available to the NOTFs by WHO/APOC.

9

3.2 The Imprest Voucher The imprest voucher is a document accompanying all payments made and it describes each transaction in detail. a) Please noted that an Imprest Voucher should be used for each transaction (that is for each invoice or group of invoices settled). b) It is strictly forbidden to group invoices not related to the same transaction and/or the same budget line item together attached to one Imprest Voucher. c) All invoices attached to an Imprest voucher should relate to a transaction in only one currency. 3.3 The Imprest Account Cash Book This is the accounting book prepared by WHO known as “WHO 412 FIN (ACT)” showing the details of all the expenditures in chronological order. a) Records are made in the Imprest Account Cash Book on the basis of the individual Imprest Vouchers. 3.4 The Monthly Statement of the Imprest Account This statement shows the different balances obtained in the Imprest Account Cash Book and the status of the bank account as shown on the monthly bank statement. a) To fill the Monthly Statement of Imprest Account, one should have finished completing the Imprest account cash book and should have it in front of him.

10

THE LETTER OF AGREEMENT

The Letter of Agreement is the legal document signed between the Ministry of Health/the National Onchocerciasis Task Force (NOTF) and the World Health Organisation/African Programme for Onchocerciasis Control (APOC) for the purpose of developing the partnership toward the control of the onchocerciasis in the country. PURPOSE a) The objective of this document is:

(i) to define and clarify the financial procedures that the benefiting project should follow in order to justify the expenses incurred each month;

(ii) to define the administrative procedures which govern the release of funds from the trust funds to the projects;

(iii) to highlight the legal limitations of the project. b) The Letter of Agreement clearly specifies the financial arrangements (including actual budget and amount to be transferred to the project for field activities, capital equipment, and overhead) as well as other expenses to be paid by each of the partners. c) The Letter of Agreement also defines the work to be performed, the obligations of each of the partners including financial input, staff required during execution and the period covered by the Agreement. d) Audit arrangements are also an integral part of the Agreement. Note: The plan of work and the time line as defined in the approved Project proposal may be modified by mutual agreement of the parties taking into account the operating experience and needs of the Programme by use of “Implementation letters” issued by WHO/APOC. PERIOD COVERED The Letter of Agreement is a legal document that defines the period it covers. In the case of the APOC project, it always covers a period of 12 months. FINANCIAL AGREEMENTS AND AMOUNTS a) The amount to be paid by WHO/APOC to the Institution is transferred in 2 or 3 installments. Each installment is called "Imprest" which is the advance given by WHO/APOC to the NOTFs for the different expenses to be made by the project implementers during a period. All expenses shall be justified on a monthly basis by a set of accounting documents. (see Page 16 on Imprest Accounting Guidelines). b) Based on the signed Letters of Agreement, a total amount of cash is provided by APOC from the “Trust Fund” to the NOTFs for expenses to be made during the period covered by the LOA. This amount is called the total amount of expenditure estimated by the agreement. The Total Financial Obligation Important Note: The amount of expenditure called the “Total Financial Obligation” should be considered an estimate of the amount to be used for the payment of project activities during the (12-

11

month) period covered by the Letter of Agreement. The “Total Financial Obligation” is an estimate and not a full grant. c) Any unliquidated balance at the end of the 12 month period should be returned to APOC/WHO at the end of each project period. d) From the Total Financial Obligation: • WHO/APOC retains a portion used for the purchase of Capital Equipment because of best prices

obtained in the international markets by WHO. • The NOTFs are not concerned with the management of the Capital Equipment portion of the total

financial obligation. However, the NOTFs should request and obtain all items approved under Capital Equipment as soon as the Letters of Agreement are signed by both parties.

• Equipment that is not approved in the Budget attached to the LOA should not be purchased form

the Imprest (with APOC funds) without approval from the Management of APOC. • The amount referred to in the Letters of Agreement as "Remaining amounts paid to the

Institution" is the portion of the Total Financial Obligation made available to the NOTFs for field activities.

• These “Remaining amounts paid to the Institution” needs to be used strictly during the period

covered by the Letter of Agreement. REPORTING REQUIREMENTS A request for further funding/installment to a Project should be made when 80% of the previous advances have been spent. The following reports should be submitted to APOC before the Project account can be replenished: i) The regular transmission at the end of each month of a copy of the bank statement, reconciled

with a list of all cheques drawn on the account. ii) A statement reconciling expenditure already made to the various budget lines. iii) A semi-annual report indicating the activities carried out and the amount spent against each

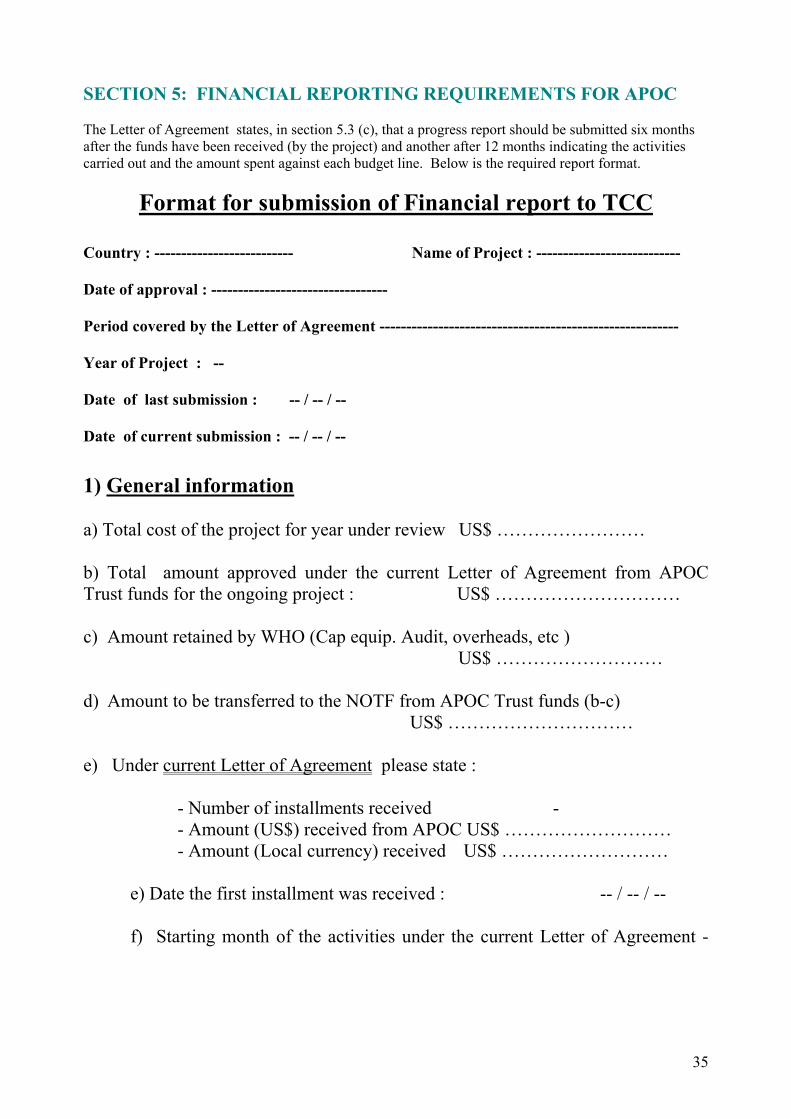

budget line (to be submitted 6 months after the first instalment has been received). The form to be completed for the semi-annual financial report is hereby attached on page 35.

iv) An annual report after 12 months indicating the activities carried out and the amount spent against each budget line.

As stated in the Letters of Agreement, any unliquidated balance from the "Remaining amount ... paid to the Institution" shall be paid back to WHO/APOC at the end of the period covered by the Letters of Agreement or it could be used to reduce the instalments to be made in the subsequent year.

FOLLOWING IS A SAMPLE LETTER OF AGREEMENT

12

SAMPLE LETTER OF AGREEMENT

SAMPLE LETTER OF AGREEMENT

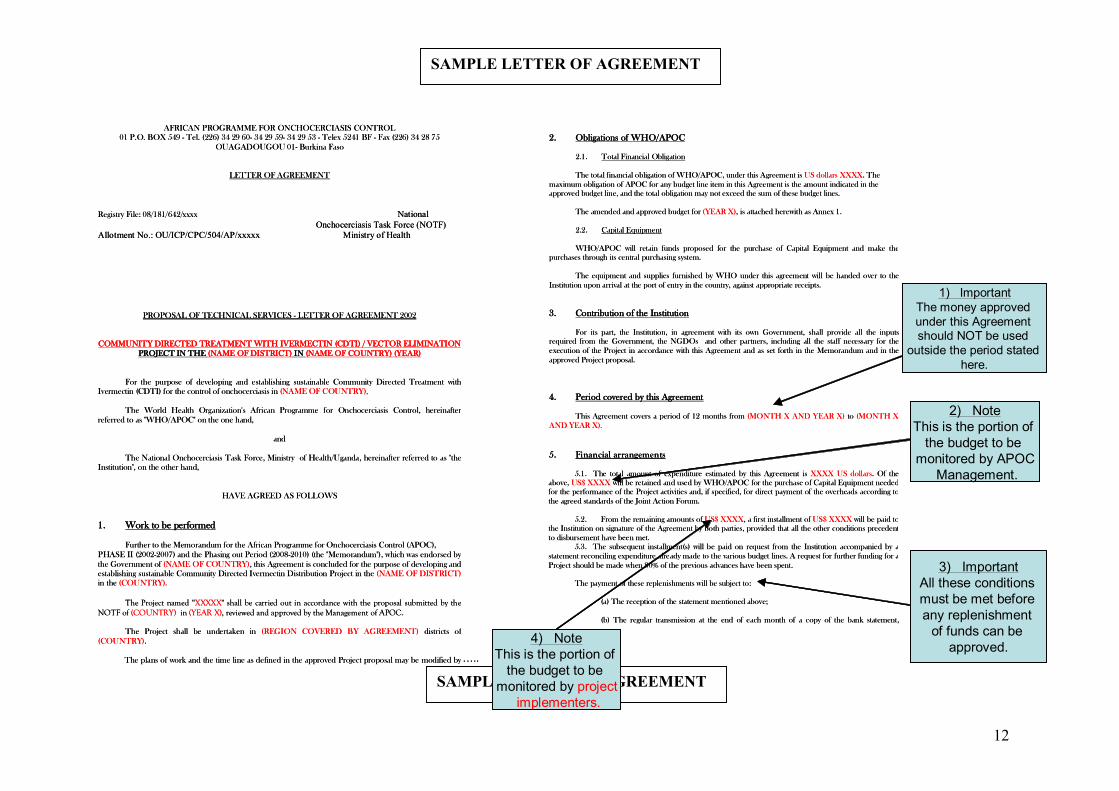

2. Obligations of WHO/APOC

2.1. Total Financial Obligation

The total financial obligation of WHO/APOC, under this Agreement is US dollars XXXX. The maximum obligation of APOC for any budget line item in this Agreement is the amount indicated in the approved budget line, and the total obligation may not exceed the sum of these budget lines.

The amended and approved budget for (YEAR X), is attached herewith as Annex 1.

2.2. Capital Equipment

WHO/APOC will retain funds proposed for the purchase of Capital Equipment and make thepurchases through its central purchasing system.

The equipment and supplies furnished by WHO under this agreement will be handed over to the

Institution upon arrival at the port of entry in the country, against appropriate receipts.

3. Contribution of the Institution

For its part, the Institution, in agreement with its own Government, shall provide all the inputsrequired from the Government, the NGDOs and other partners, including all the staff necessary for theexecution of the Project in accordance with this Agreement and as set forth in the Memorandum and in theapproved Project proposal. 4. Period covered by this Agreement

This Agreement covers a period of 12 months from (MONTH X AND YEAR X) to (MONTH XAND YEAR X). 5. Financial arrangements

5.1. The total amount of expenditure estimated by this Agreement is XXXX US dollars. Of theabove, US$ XXXX will be retained and used by WHO/APOC for the purchase of Capital Equipment neededfor the performance of the Project activities and, if specified, for direct payment of the overheads according tothe agreed standards of the Joint Action Forum.

5.2. From the remaining amounts of US$ XXXX, a first installment of US$ XXXX will be paid tothe Institution on signature of the Agreement by both parties, provided that all the other conditions precedentto disbursement have been met.

5.3. The subsequent installment(s) will be paid on request from the Institution accompanied by astatement reconciling expenditure already made to the various budget lines. A request for further funding for aProject should be made when 80% of the previous advances have been spent.

The payment of these replenishments will be subject to:

(a) The reception of the statement mentioned above;

(b) The regular transmission at the end of each month of a copy of the bank statement,

1) ImportantThe money approved under this Agreement should NOT be used

outside the period stated here.

2) NoteThis is the portion of

the budget to be monitored by APOC

Management.

3) ImportantAll these conditions must be met before any replenishment

of funds can be approved.

AFRICAN PROGRAMME FOR ONCHOCERCIASIS CONTROL 01 P.O. BOX 549 - Tel. (226) 34 29 60- 34 29 59- 34 29 53 - Telex 5241 BF - Fax (226) 34 28 75 OUAGADOUGOU 01- Burkina Faso LETTER OF AGREEMENT Registry File: 08/181/642/xxxx National

Onchocerciasis Task Force (NOTF) Allotment No.: OU/ICP/CPC/504/AP/xxxxx Ministry of Health

PROPOSAL OF TECHNICAL SERVICES - LETTER OF AGREEMENT 2002 COMMUNITY DIRECTED TREATMENT WITH IVERMECTIN (CDTI) / VECTOR ELIMINATION

PROJECT IN THE (NAME OF DISTRICT) IN (NAME OF COUNTRY) (YEAR)

For the purpose of developing and establishing sustainable Community Directed Treatment withIvermectin (CDTI) for the control of onchocerciasis in (NAME OF COUNTRY),

The World Health Organization's African Programme for Onchocerciasis Control, hereinafterreferred to as "WHO/APOC" on the one hand, and

The National Onchocerciasis Task Force, Ministry of Health/Uganda, hereinafter referred to as "theInstitution", on the other hand, HAVE AGREED AS FOLLOWS 1. Work to be performed

Further to the Memorandum for the African Programme for Onchocerciasis Control (APOC), PHASE II (2002-2007) and the Phasing out Period (2008-2010) (the "Memorandum"), which was endorsed bythe Government of (NAME OF COUNTRY), this Agreement is concluded for the purpose of developing andestablishing sustainable Community Directed Ivermectin Distribution Project in the (NAME OF DISTRICT)in the (COUNTRY).

The Project named “XXXXX" shall be carried out in accordance with the proposal submitted by theNOTF of (COUNTRY) in (YEAR X), reviewed and approved by the Management of APOC.

The Project shall be undertaken in (REGION COVERED BY AGREEMENT) districts of

(COUNTRY). The plans of work and the time line as defined in the approved Project proposal may be modified by

4) NoteThis is the portion of

the budget to be monitored by project

implementers.

…..

2. Obligations of WHO/APOC

2.1. Total Financial Obligation

The total financial obligation of WHO/APOC, under this Agreement is US dollars XXXX. The maximum obligation of APOC for any budget line item in this Agreement is the amount indicated in the approved budget line, and the total obligation may not exceed the sum of these budget lines.

The amended and approved budget for (YEAR X), is attached herewith as Annex 1.

2.2. Capital Equipment

WHO/APOC will retain funds proposed for the purchase of Capital Equipment and make thepurchases through its central purchasing system.

The equipment and supplies furnished by WHO under this agreement will be handed over to the

Institution upon arrival at the port of entry in the country, against appropriate receipts.

3. Contribution of the Institution

For its part, the Institution, in agreement with its own Government, shall provide all the inputsrequired from the Government, the NGDOs and other partners, including all the staff necessary for theexecution of the Project in accordance with this Agreement and as set forth in the Memorandum and in theapproved Project proposal. 4. Period covered by this Agreement

This Agreement covers a period of 12 months from (MONTH X AND YEAR X) to (MONTH XAND YEAR X). 5. Financial arrangements

5.1. The total amount of expenditure estimated by this Agreement is XXXX US dollars. Of theabove, US$ XXXX will be retained and used by WHO/APOC for the purchase of Capital Equipment neededfor the performance of the Project activities and, if specified, for direct payment of the overheads according tothe agreed standards of the Joint Action Forum.

5.2. From the remaining amounts of US$ XXXX, a first installment of US$ XXXX will be paid tothe Institution on signature of the Agreement by both parties, provided that all the other conditions precedentto disbursement have been met.

5.3. The subsequent installment(s) will be paid on request from the Institution accompanied by astatement reconciling expenditure already made to the various budget lines. A request for further funding for aProject should be made when 80% of the previous advances have been spent.

The payment of these replenishments will be subject to:

(a) The reception of the statement mentioned above;

(b) The regular transmission at the end of each month of a copy of the bank statement,

1) ImportantThe money approved under this Agreement should NOT be used

outside the period stated here.

2) NoteThis is the portion of

the budget to be monitored by APOC

Management.

3) ImportantAll these conditions must be met before any replenishment

of funds can be approved.

AFRICAN PROGRAMME FOR ONCHOCERCIASIS CONTROL 01 P.O. BOX 549 - Tel. (226) 34 29 60- 34 29 59- 34 29 53 - Telex 5241 BF - Fax (226) 34 28 75 OUAGADOUGOU 01- Burkina Faso LETTER OF AGREEMENT Registry File: 08/181/642/xxxx National

Onchocerciasis Task Force (NOTF) Allotment No.: OU/ICP/CPC/504/AP/xxxxx Ministry of Health

PROPOSAL OF TECHNICAL SERVICES - LETTER OF AGREEMENT 2002 COMMUNITY DIRECTED TREATMENT WITH IVERMECTIN (CDTI) / VECTOR ELIMINATION

PROJECT IN THE (NAME OF DISTRICT) IN (NAME OF COUNTRY) (YEAR)

For the purpose of developing and establishing sustainable Community Directed Treatment withIvermectin (CDTI) for the control of onchocerciasis in (NAME OF COUNTRY),

The World Health Organization's African Programme for Onchocerciasis Control, hereinafterreferred to as "WHO/APOC" on the one hand, and

The National Onchocerciasis Task Force, Ministry of Health/Uganda, hereinafter referred to as "theInstitution", on the other hand, HAVE AGREED AS FOLLOWS 1. Work to be performed

Further to the Memorandum for the African Programme for Onchocerciasis Control (APOC), PHASE II (2002-2007) and the Phasing out Period (2008-2010) (the "Memorandum"), which was endorsed bythe Government of (NAME OF COUNTRY), this Agreement is concluded for the purpose of developing andestablishing sustainable Community Directed Ivermectin Distribution Project in the (NAME OF DISTRICT)in the (COUNTRY).

The Project named “XXXXX" shall be carried out in accordance with the proposal submitted by theNOTF of (COUNTRY) in (YEAR X), reviewed and approved by the Management of APOC.

The Project shall be undertaken in (REGION COVERED BY AGREEMENT) districts of

(COUNTRY). The plans of work and the time line as defined in the approved Project proposal may be modified by

4) NoteThis is the portion of

the budget to be monitored by project

implementers.

…..

13

SAMPLE LETTER OF AGREEMENT

The Programme Director Attention: Budget and Finance Officer

WHO/APOC 01 BP 549

Ouagadougou 01 Burk ina Faso

(c) An annual report after 12 months indicating the activities carried out and the amount spent against each budget line. This report will be formally reviewed as a basis for extension of this Agreement for a further period or the signing of a s ubsequent Agreement for further funding. The report should be forwarded to the following address:

The Programme Director

WHO/APOC 01 BP 549

Ouagadougou 01 Burkina Faso

5.4. The installments shall be paid to the Institution, through the special Nationa l Onchocerciasis Task Force Bank Account, opened exclusively for WHO/APOC funds to be used on the project.

5.5. Any unliquidated balance at the end of the period covered by the current Agreement shall be paid back to WHO/APOC by the Institution or if spe cifically agreed, deducted later on from the amount of the sum WHO/APOC will pay in the framework of any possible subsequent Agreement.

6. Legal arrangements

It is understood that the work under this Agreement will be performed under the technical supervision of WHO/APOC but does not create any employer/employee relationship between WHO/APOC and the Institution. The Institution shall in that respect be solely responsible for the manner in which the work will be carried out.

WHO/APOC shall not be respo nsible for any loss, accident, damage or injury suffered by the Institution or any person claiming under it, arising during or as a result of the execution of this work or in any manner whatsoever.

Any dispute relating to the interpretation or execution o f this Agreement shall, unless amicably settled, be subject to conciliation. In the event of failure of the latter, the dispute shall be settled by arbitration. The arbitration shall be conducted in accordance with the modalities to be agreed upon by the p arties or, in the absence of agreement, with the Uncitral Arbitration Rules. The parties shall accept the arbitral award as final.

If your Institution accepts this proposal, we should be grateful if you would see to the signing of all the four copies of t his Agreement by two persons authorized to sign on behalf of the Institution responsible for the execution of the work and return three copies to us.

Signatories WHO/APOC

Signatories Institution

1.

1.

Name ................................ ..............................

Budget and Finan ce Officer/APOC Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

2.

Dr A.Sékétéli

2.

Name ................................ ..............................

Programme Director Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

Please read section to understand the limits of this agreement

The Programme Director Attention: Budget and Finance Officer

WHO/APOC 01 BP 549

Ouagadougou 01 Burk ina Faso

(c) An annual report after 12 months indicating the activities carried out and the amount spent against each budget line. This report will be formally reviewed as a basis for extension of this Agreement for a further period or the signing of a s ubsequent Agreement for further funding. The report should be forwarded to the following address:

The Programme Director

WHO/APOC 01 BP 549

Ouagadougou 01 Burkina Faso

5.4. The installments shall be paid to the Institution, through the special Nationa l Onchocerciasis Task Force Bank Account, opened exclusively for WHO/APOC funds to be used on the project.

5.5. Any unliquidated balance at the end of the period covered by the current Agreement shall be paid back to WHO/APOC by the Institution or if spe cifically agreed, deducted later on from the amount of the sum WHO/APOC will pay in the framework of any possible subsequent Agreement.

6. Legal arrangements

It is understood that the work under this Agreement will be performed under the technical supervision of WHO/APOC but does not create any employer/employee relationship between WHO/APOC and the Institution. The Institution shall in that respect be solely responsible for the manner in which the work will be carried out.

WHO/APOC shall not be respo nsible for any loss, accident, damage or injury suffered by the Institution or any person claiming under it, arising during or as a result of the execution of this work or in any manner whatsoever.

Any dispute relating to the interpretation or execution o f this Agreement shall, unless amicably settled, be subject to conciliation. In the event of failure of the latter, the dispute shall be settled by arbitration. The arbitration shall be conducted in accordance with the modalities to be agreed upon by the p arties or, in the absence of agreement, with the Uncitral Arbitration Rules. The parties shall accept the arbitral award as final.

If your Institution accepts this proposal, we should be grateful if you would see to the signing of all the four copies of t his Agreement by two persons authorized to sign on behalf of the Institution responsible for the execution of the work and return three copies to us.

Signatories WHO/APOC

Signatories Institution

1.

1.

Name ................................ ..............................

Budget and Finan ce Officer/APOC Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

2.

Dr A.Sékétéli

2.

Name ................................ ..............................

Programme Director Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

The Programme Director Attention: Budget and Finance Officer

WHO/APOC 01 BP 549

Ouagadougou 01 Burk ina Faso

(c) An annual report after 12 months indicating the activities carried out and the amount spent against each budget line. This report will be formally reviewed as a basis for extension of this Agreement for a further period or the signing of a s ubsequent Agreement for further funding. The report should be forwarded to the following address:

The Programme Director

WHO/APOC 01 BP 549

Ouagadougou 01 Burkina Faso

5.4. The installments shall be paid to the Institution, through the special Nationa l Onchocerciasis Task Force Bank Account, opened exclusively for WHO/APOC funds to be used on the project.

5.5. Any unliquidated balance at the end of the period covered by the current Agreement shall be paid back to WHO/APOC by the Institution or if spe cifically agreed, deducted later on from the amount of the sum WHO/APOC will pay in the framework of any possible subsequent Agreement.

6. Legal arrangements

It is understood that the work under this Agreement will be performed under the technical supervision of WHO/APOC but does not create any employer/employee relationship between WHO/APOC and the Institution. The Institution shall in that respect be solely responsible for the manner in which the work will be carried out.

WHO/APOC shall not be respo nsible for any loss, accident, damage or injury suffered by the Institution or any person claiming under it, arising during or as a result of the execution of this work or in any manner whatsoever.

Any dispute relating to the interpretation or execution o f this Agreement shall, unless amicably settled, be subject to conciliation. In the event of failure of the latter, the dispute shall be settled by arbitration. The arbitration shall be conducted in accordance with the modalities to be agreed upon by the p arties or, in the absence of agreement, with the Uncitral Arbitration Rules. The parties shall accept the arbitral award as final.

If your Institution accepts this proposal, we should be grateful if you would see to the signing of all the four copies of t his Agreement by two persons authorized to sign on behalf of the Institution responsible for the execution of the work and return three copies to us.

Signatories WHO/APOC

Signatories Institution

1.

1.

Name ................................ ..............................

ce Officer/APOC Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

2.

Dr A.Sékétéli

2.

Name ................................ ..............................

Programme Director Title ................................ ................................ .

................................ ................................ ........

Signature

Signature

Date

Date

Please read section to understand the limits of this agreement

14

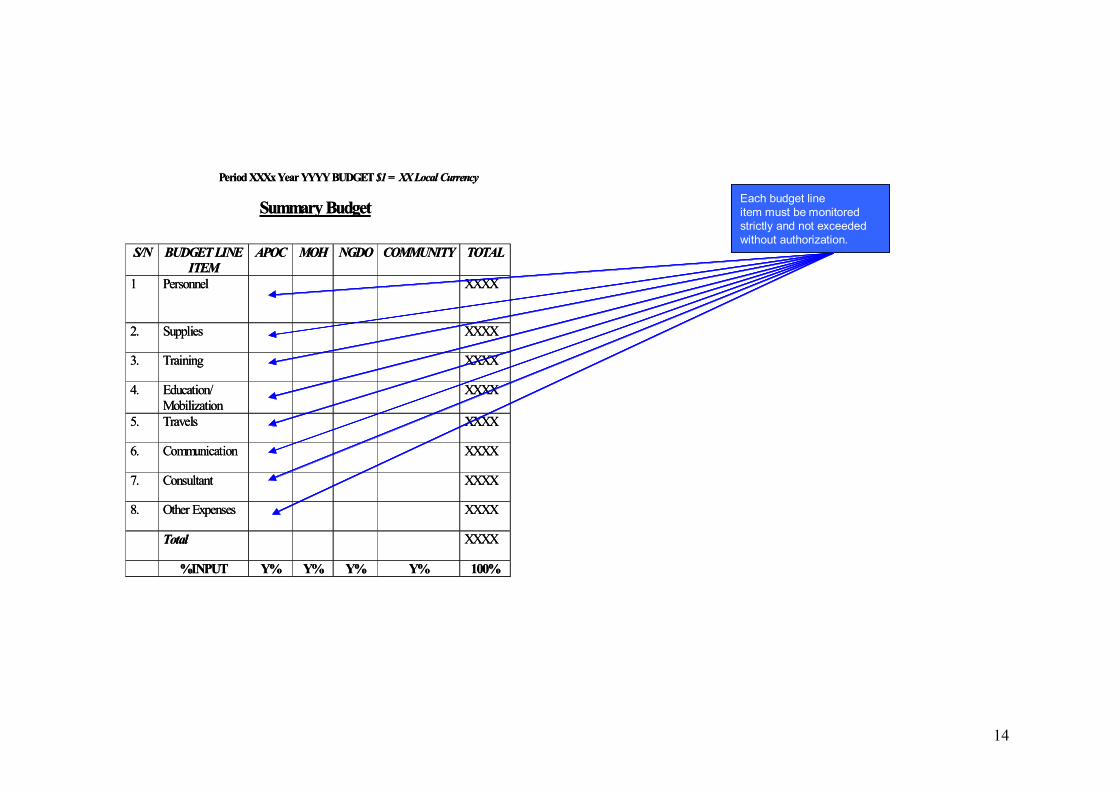

Period XXXx Year YYYY BUDGET $1 = XX Local Currency

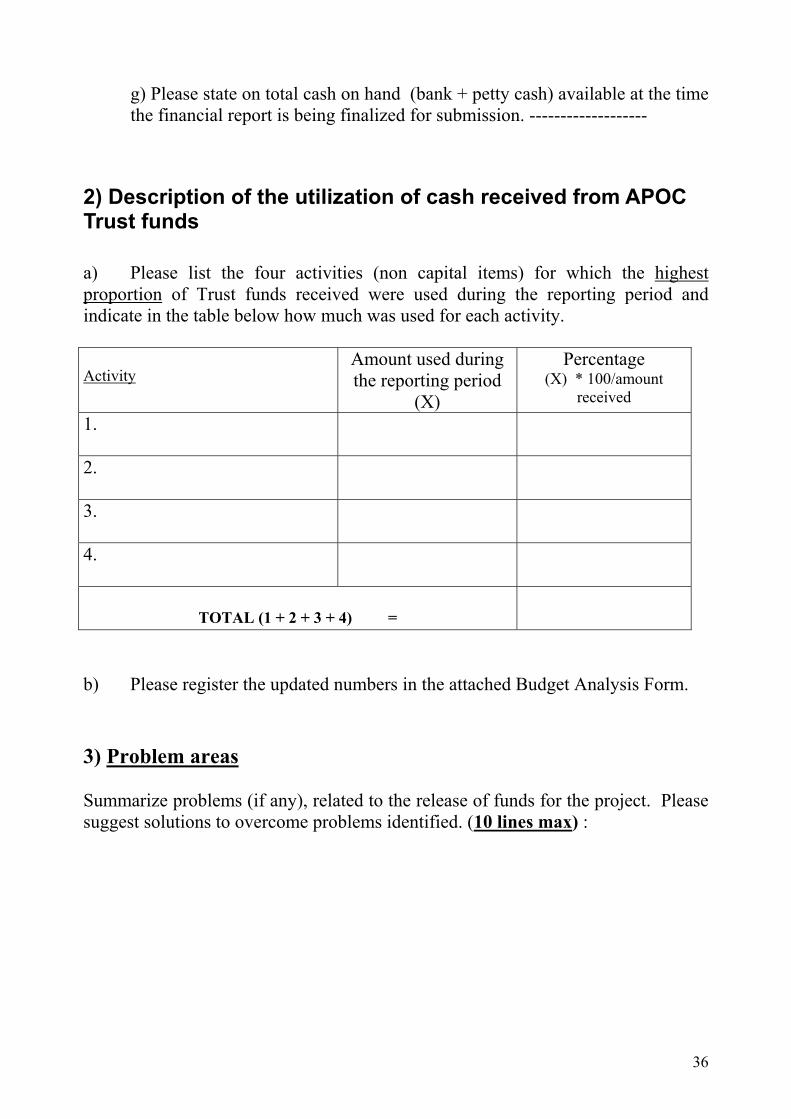

Summary Budget S/N BUDGET LINE

ITEM APOC MOH NGDO COMMUNITY TOTAL

1 Personnel XXXX

2. Supplies XXXX

3. Training XXXX

4. Education/ Mobilization

XXXX

5. Travels XXXX

6. Communication XXXX

7. Consultant XXXX

8. Other Expenses XXXX

Total XXXX

%INPUT Y% Y% Y% Y% 100%

Each budget line item must be monitored strictly and not exceeded without authorization.

Period XXXx Year YYYY BUDGET $1 = XX Local Currency

Summary Budget S/N BUDGET LINE

ITEM APOC MOH NGDO COMMUNITY TOTAL

1 Personnel XXXX

2. Supplies XXXX

3. Training XXXX

4. Education/ Mobilization

XXXX

5. Travels XXXX

6. Communication XXXX

7. Consultant XXXX

8. Other Expenses XXXX

Total XXXX

%INPUT Y% Y% Y% Y% 100%

Each budget line item must be monitored strictly and not exceeded without authorization.

15

COMMON MISINTERPRETATIONS OF THE LETTER OF AGREEMENT The project period The project period stated in the Letter of Agreement should be observed strictly. All transactions charged to a particular budget should stop once the project period comes to an end. Understanding the approved budget amount (Total financial obligation) and financial arrangements The approved budget amount that will be due to the project during the project period is clearly stated in the Letter of Agreement. This amount is to be tracked during the specific project period.

16

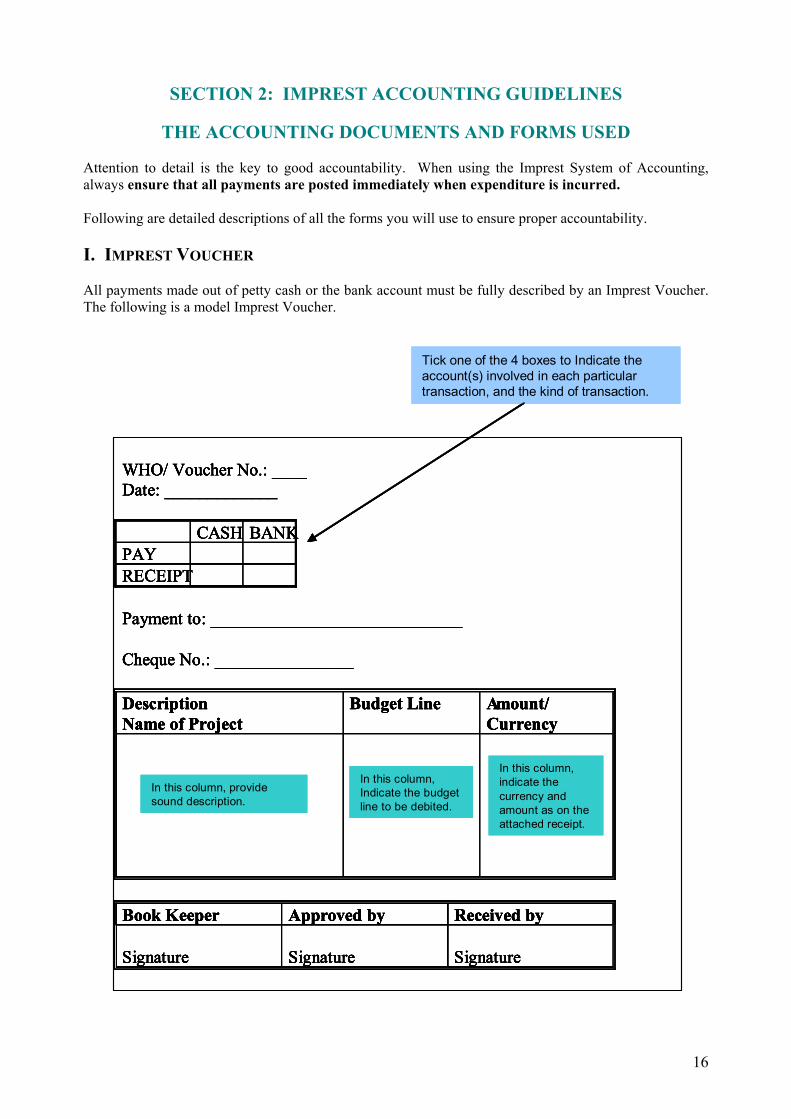

SECTION 2: IMPREST ACCOUNTING GUIDELINES

THE ACCOUNTING DOCUMENTS AND FORMS USED Attention to detail is the key to good accountability. When using the Imprest System of Accounting, always ensure that all payments are posted immediately when expenditure is incurred. Following are detailed descriptions of all the forms you will use to ensure proper accountability. I. IMPREST VOUCHER All payments made out of petty cash or the bank account must be fully described by an Imprest Voucher. The following is a model Imprest Voucher.

Tick one of the 4 boxes to Indicate the account(s) involved in each particular transaction, and the kind of transaction.

WHO/ Voucher No.: ____Date: _____________

CASH BANKPAYRECEIPT

Payment to: _____________________________

Cheque No.: ________________

DescriptionName of Project

Budget Line Amount/Currency

Book Keeper Approved by Received by

Signature Signature Signature

In this column, provide sound description.

In this column, Indicate the budget line to be debited.

In this column, indicate the currency and amount as on the attached receipt.

Tick one of the 4 boxes to Indicate the account(s) involved in each particular transaction, and the kind of transaction.

WHO/ Voucher No.: ____Date: _____________

CASH BANKPAYRECEIPT

Payment to: _____________________________

Cheque No.: ________________

DescriptionName of Project

Budget Line Amount/Currency

Book Keeper Approved by Received by

Signature Signature Signature

Tick one of the 4 boxes to Indicate the account(s) involved in each particular transaction, and the kind of transaction.

WHO/ Voucher No.: ____Date: _____________

CASH BANKPAYRECEIPT

Payment to: _____________________________

Cheque No.: ________________

DescriptionName of Project

Budget Line Amount/Currency

Book Keeper Approved by Received by

Signature Signature Signature

WHO/ Voucher No.: ____Date: _____________

CASH BANKPAYRECEIPT

Payment to: _____________________________

Cheque No.: ________________

DescriptionName of Project

Budget Line Amount/Currency

Book Keeper Approved by Received by

Signature Signature Signature

WHO/ Voucher No.: ____Date: _____________

CASH BANKPAYRECEIPT

Payment to: _____________________________

Cheque No.: ________________

DescriptionName of Project

Budget Line Amount/Currency

Book Keeper Approved by Received by

Signature Signature Signature

In this column, provide sound description.

In this column, Indicate the budget line to be debited.

In this column, indicate the currency and amount as on the attached receipt.

17

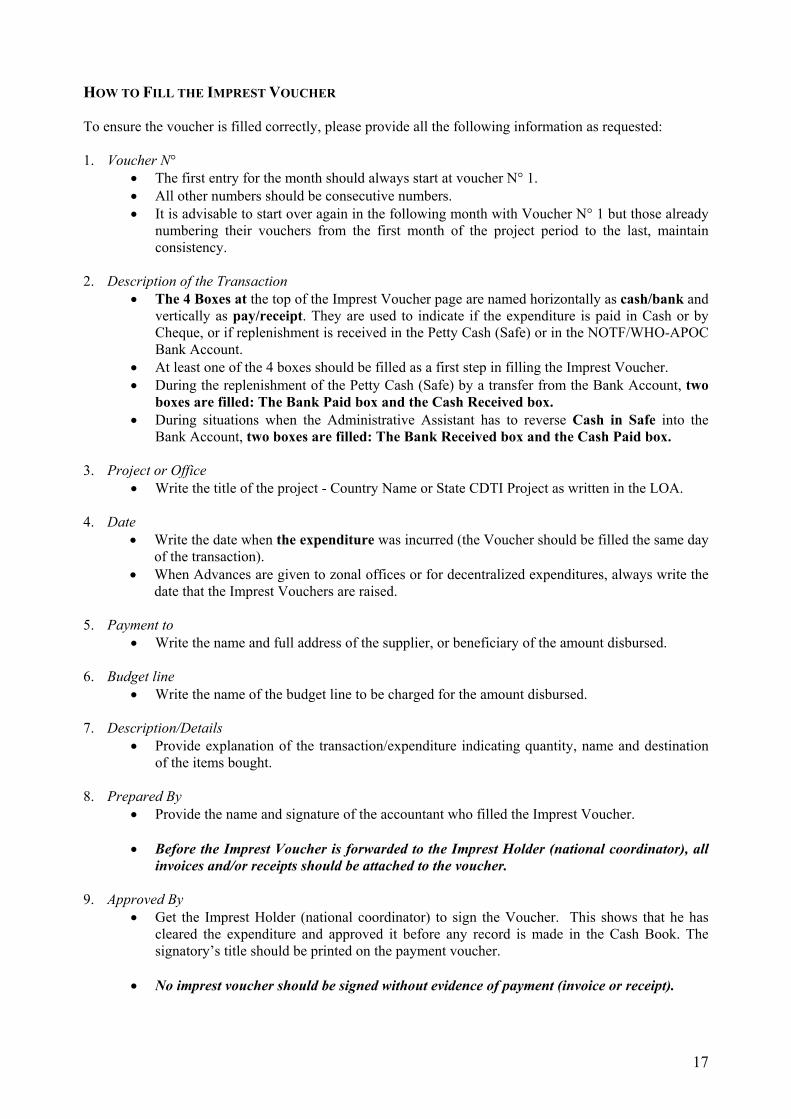

HOW TO FILL THE IMPREST VOUCHER To ensure the voucher is filled correctly, please provide all the following information as requested: 1. Voucher N°

• The first entry for the month should always start at voucher N° 1. • All other numbers should be consecutive numbers. • It is advisable to start over again in the following month with Voucher N° 1 but those already

numbering their vouchers from the first month of the project period to the last, maintain consistency.

2. Description of the Transaction

• The 4 Boxes at the top of the Imprest Voucher page are named horizontally as cash/bank and vertically as pay/receipt. They are used to indicate if the expenditure is paid in Cash or by Cheque, or if replenishment is received in the Petty Cash (Safe) or in the NOTF/WHO-APOC Bank Account.

• At least one of the 4 boxes should be filled as a first step in filling the Imprest Voucher. • During the replenishment of the Petty Cash (Safe) by a transfer from the Bank Account, two

boxes are filled: The Bank Paid box and the Cash Received box. • During situations when the Administrative Assistant has to reverse Cash in Safe into the

Bank Account, two boxes are filled: The Bank Received box and the Cash Paid box. 3. Project or Office

• Write the title of the project - Country Name or State CDTI Project as written in the LOA. 4. Date

• Write the date when the expenditure was incurred (the Voucher should be filled the same day of the transaction).

• When Advances are given to zonal offices or for decentralized expenditures, always write the date that the Imprest Vouchers are raised.

5. Payment to

• Write the name and full address of the supplier, or beneficiary of the amount disbursed. 6. Budget line

• Write the name of the budget line to be charged for the amount disbursed. 7. Description/Details

• Provide explanation of the transaction/expenditure indicating quantity, name and destination of the items bought.

8. Prepared By

• Provide the name and signature of the accountant who filled the Imprest Voucher.

• Before the Imprest Voucher is forwarded to the Imprest Holder (national coordinator), all invoices and/or receipts should be attached to the voucher.

9. Approved By

• Get the Imprest Holder (national coordinator) to sign the Voucher. This shows that he has cleared the expenditure and approved it before any record is made in the Cash Book. The signatory’s title should be printed on the payment voucher.

• No imprest voucher should be signed without evidence of payment (invoice or receipt).

18

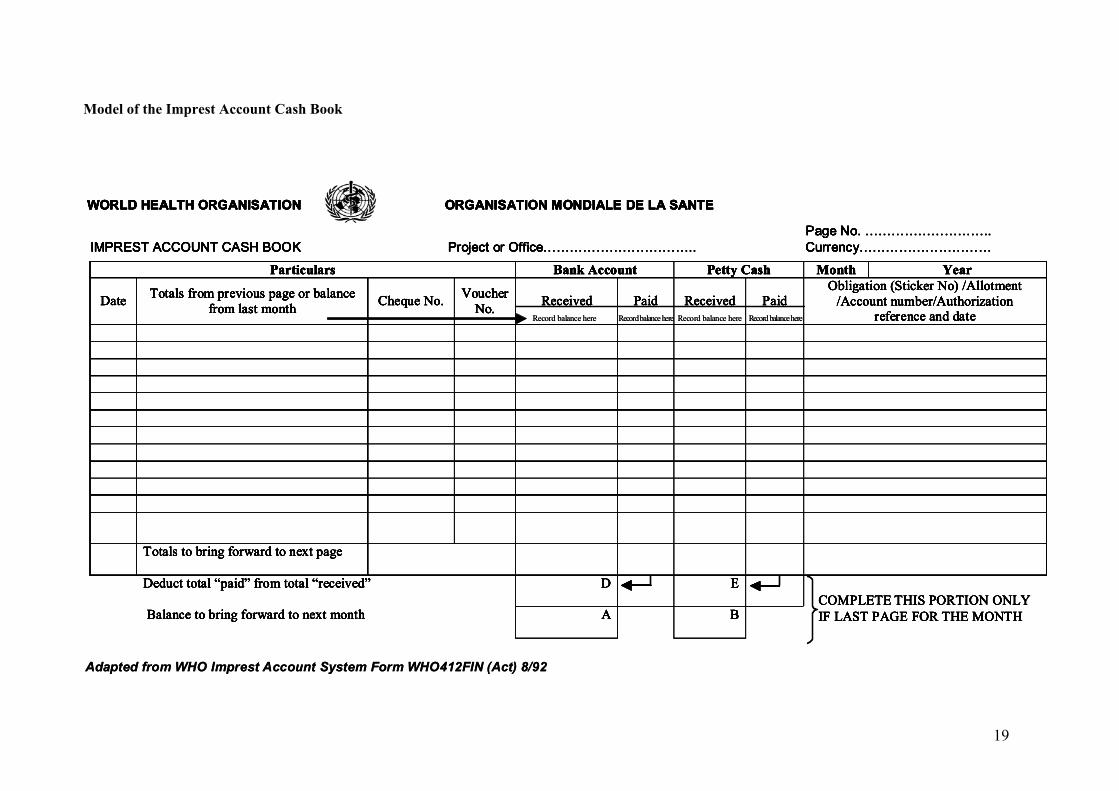

II. THE IMPREST ACCOUNT CASH BOOK The “Cash Book” is a book in which record is kept of all financial transactions (cash receipts and disbursements). It is a very important accounting document that captures all transactions made each day. After the Imprest Vouchers are approved by the Imprest Holder, entries into the cashbook should be made daily and solely by the designated Accountant/Administrative Assistant. The same numbers recorded on the voucher are the same numbers recorded in the Cash Book by the Accountant/Administrative Assistant. As a principle, all expenditures should be recorded promptly in the Imprest Account Cash Book. Following is a model of the Imprest Account Cash Book.

19

Model of the Imprest Account Cash Book

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Adapted from WHO Imprest Account System Form WHO412FIN (Act) 8/92

Record balance here Record balance here Record balance here Record balance here

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A B

COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Adapted from WHO Imprest Account System Form WHO412FIN (Act) 8/92

Record balance here Record balance here Record balance here Record balance here

20

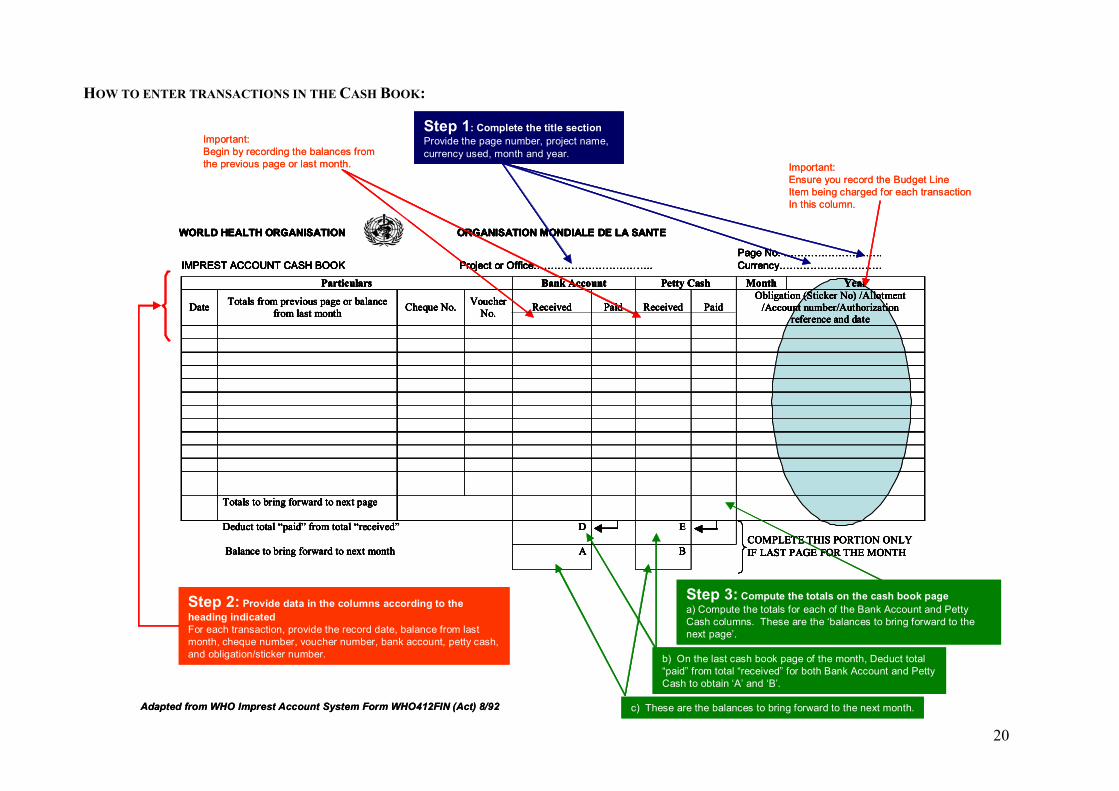

HOW TO ENTER TRANSACTIONS IN THE CASH BOOK:

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Step 1: Complete the title sectionProvide the page number, project name, currency used, month and year.

Step 2: Provide data in the columns according to the heading indicatedFor each transaction, provide the record date, balance from lastmonth, cheque number, voucher number, bank account, petty cash, and obligation/sticker number. b) On the last cash book page of the month, Deduct total

“paid” from total “received” for both Bank Account and Petty Cash to obtain ‘A’ and ‘B’.

c) These are the balances to bring forward to the next month.

Step 3: Compute the totals on the cash book pagea) Compute the totals for each of the Bank Account and Petty Cash columns. These are the ‘balances to bring forward to the next page’.

Important:Ensure you record the Budget LineItem being charged for each transactionIn this column.

Important:Begin by recording the balances from the previous page or last month.

Adapted from WHO Imprest Account System Form WHO412FIN (Act) 8/92

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Particulars Bank Account Petty Cash Month Year

Date Totals from previous page or balance from last month Cheque No. Voucher

No. Received Paid Received Paid Obligation (Sticker No) /Allotment

/Account number/Authorization reference and date

Totals to bring forward to next page

Deduct total “paid” from total “received” D E

Balance to bring forward to next month A

B COMPLETE THIS PORTION ONLY IF LAST PAGE FOR THE MONTH

Page No. ………………………..IMPREST ACCOUNT CASH BOOK Project or Office…………………………….. Currency…………………………

WORLD HEALTH ORGANISATION ORGANISATION MONDIALE DE LA SANTE

Step 1: Complete the title sectionProvide the page number, project name, currency used, month and year.

Step 2: Provide data in the columns according to the heading indicatedFor each transaction, provide the record date, balance from lastmonth, cheque number, voucher number, bank account, petty cash, and obligation/sticker number. b) On the last cash book page of the month, Deduct total

“paid” from total “received” for both Bank Account and Petty Cash to obtain ‘A’ and ‘B’.

c) These are the balances to bring forward to the next month.

Step 3: Compute the totals on the cash book pagea) Compute the totals for each of the Bank Account and Petty Cash columns. These are the ‘balances to bring forward to the next page’.

Important:Ensure you record the Budget LineItem being charged for each transactionIn this column.

Important:Begin by recording the balances from the previous page or last month.

Adapted from WHO Imprest Account System Form WHO412FIN (Act) 8/92

21

HOW TO ENTER TRANSACTIONS IN THE CASH BOOK:

3 Steps to Fill the Cash Book

Step 1: Complete the title section (page number, project name, currency used, month and year). Step 2: Provide data in the columns indicated (record date, balance from last month, cheque number, voucher number, bank account, petty cash, and obligation/sticker number). Step 3: Calculate the totals (Balance to bring forward to next page and the balance to bring forward to the next month).

Step by Step Explanation 1. Complete the title bar section

• write down the name of the project or office using this imprest account (Country name or State CDTI Project),

• write down the page number (1, 2, 3, etc.) and the currency used (USD, CHF, currency of the country of assignment, etc). Also, in few African countries, two currencies are used –for those cases, two cash books are used.

• Write in the month and year in the space provided. 2. Input entries into the columns provided as follows

a) Date – Record the date money was received or disbursed. Since cash book entries are made daily, the dates recorded here should be the same one of entry in the cash book. b) Balance from last month/Totals from last page – This first entry should show the totals from the previous page or the “balances carried forward”. Each of the rows that follow describe each transaction in that month (e.g. ‘salary paid to Mr. ---‘or ‘electricity bill’). c) Cheque No. – Record the serial number of the cheque used by the imprest holder to make a payment. Make sure that the cheque numbers are consecutive. All cheque numbers missing should be justified. d) Voucher No. – Record the voucher number attached to each transaction to enter. The voucher numbers should be sequential. e) Bank Account – There are two columns, for amounts received and for amounts paid.

• In the received column - record any money credited to the bank account (replenishment transfers by WHO/APOC, cheques deposited, or transfers from petty cash) during that calendar month.

• In the paid column - record any disbursements for the month (generally expenditures paid by cheque or replenishment of safe through a cheque).

At the end of the month, record bank charges noted after the bank statement has been issued.

f) Petty Cash – Has two columns similar to the Bank Account. Record any cash received to replenish the petty cash in the received column and record all the expenditures made in the cash in the paid column. g) Obligation (sticker number)/Allotment etc. – This is a very important column. Each

expenditure is charged to a budget line item on the projects budget. In this column record the budget line item associated with the recorded transaction.

o For non expenditure transactions (those that do not constitute an outflow of project resources from Bank or Petty cash) leave the line in this column blank.

22

o Incoming funds: In some cases, incoming funds may be used to reduce the amount already charged to a specific budget line item. Record the budget line item in brackets. For example: when payment is made for the month’s telephone charges, the obligation/sticker number in the cash book will read “Communication” as this is a charge to the communication budget line item. If upon reviewing the bill it is discovered that staff members made personal call not related to the programme activities, they may be asked to pay back to the programme the amount already paid for their personal calls. This incoming fund (paid by the staff back to the project) will them be recorded in brackets as “ (communication) ” because it represents a credit to the ‘communication’ budget line item and is being used to reduce the amount already paid out of the communication budget line item. This also applies when reversing any cash book entries.

3. Calculate the totals to be brought forward

• Totals to bring forward to next page – just add up all the amounts in the bank account and petty cash columns

• Totals to bring forward to next month (lettered ‘A’ and ‘B’) – To obtain ‘A’ in the bank account column; subtract all the amounts ‘paid’ from all the amounts ‘received’. To obtain ‘B’ in the petty cash column; subtract all the amounts ‘paid’ from all the amounts ‘received’.

NOTE: How to record advances made from Bank Account and Petty Cash in the Cash Book Only actual expenditures with supporting justification are recorded in the cash book. Therefore, an advance made out of the bank account is recorded in the cash book as a replenishment of the petty cash as it is justified by the bank statement. An advance made out of the petty cash is not recorded in the cash book. Actual expenditures associated with the advance are recorded provided they have supporting justification. • Advances made out of the bank account;

o should be recorded as a replenishment of the petty cash, o When actual expenditures are made out of the advanced money and are justified with receipts, the

accountant should then record the amount as an expense made from the petty cash. o If the advanced amount was not spent in full, the remainder is simply deposited in the petty cash

with no further record. • Advances made out of the petty cash

o No record is made in the cash book by the accountant at the time of the advance as it is not a justified actual expense. However, every time an advance is made, a separate record should be kept to monitor the amount of advance made and the amount paid back and associated justification of the spent money.

o The separate record you keep to monitor the advance made from petty cash should have attached to it the document approving the advance.

o The money spent with justification is then recorded in the cash book like any other expenditure. The balance from the advance is deposited in the petty cash with no further record. If the amount is very large, it is deposited in the bank account as transfer from petty cash to the bank.

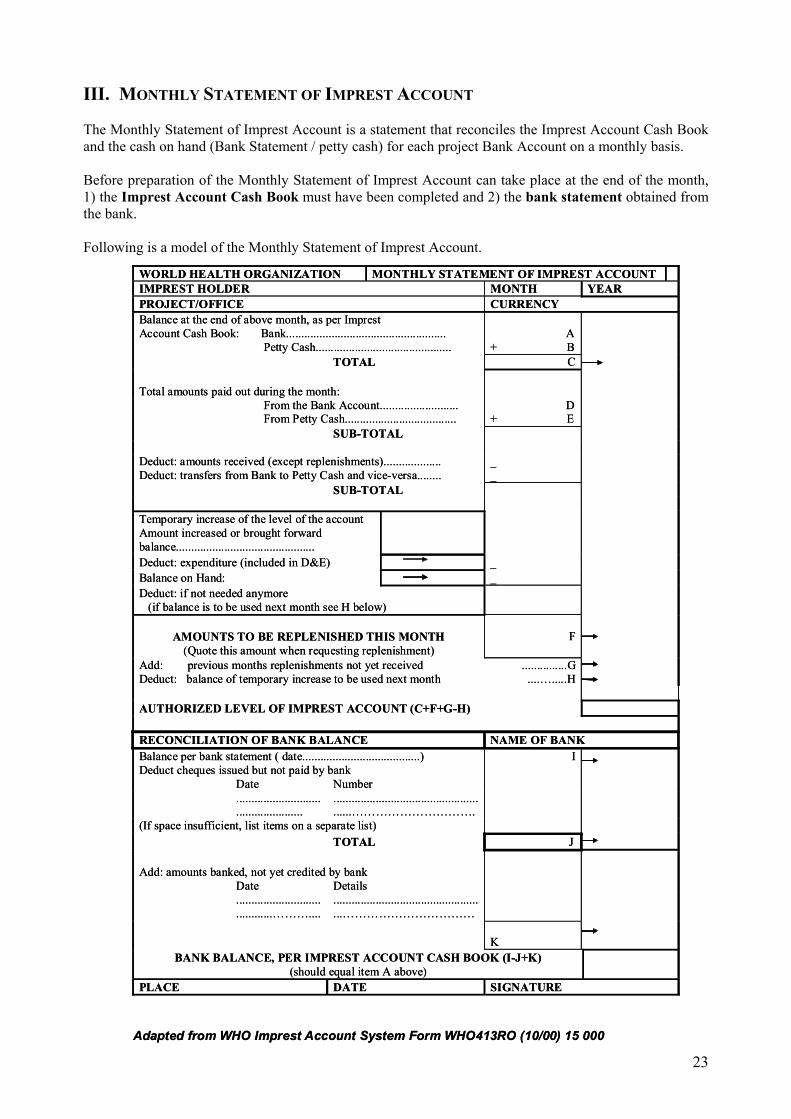

23

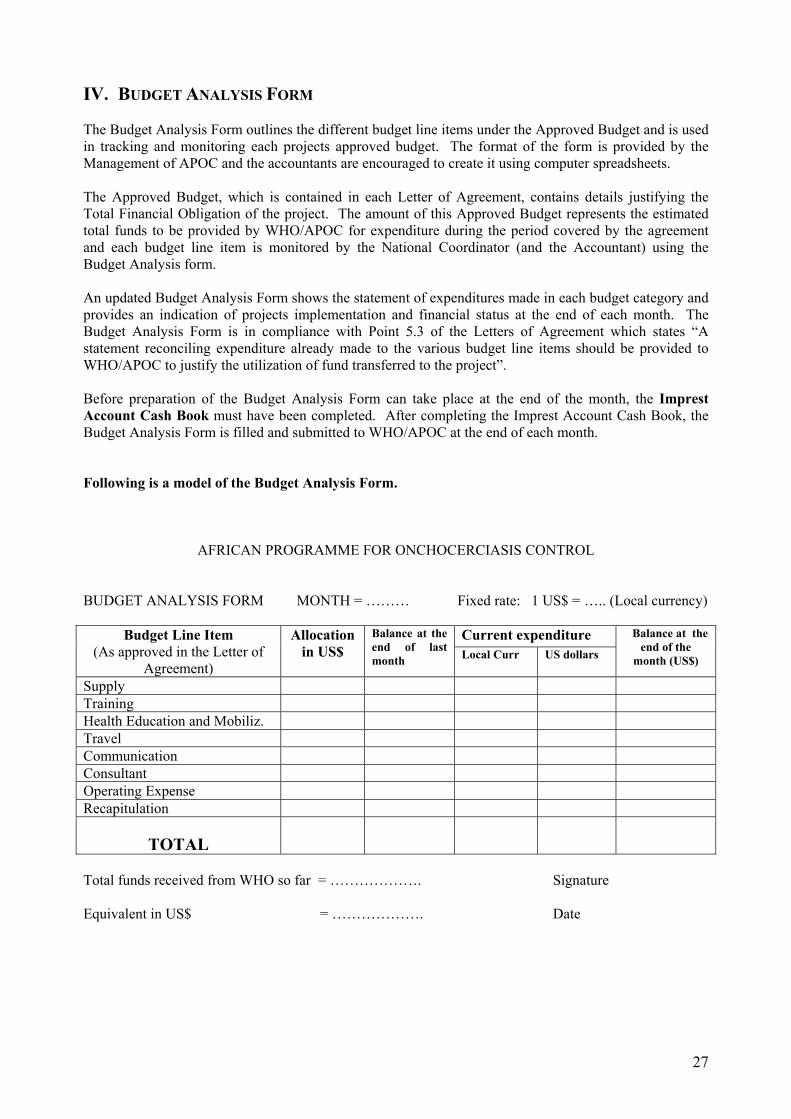

III. MONTHLY STATEMENT OF IMPREST ACCOUNT The Monthly Statement of Imprest Account is a statement that reconciles the Imprest Account Cash Book and the cash on hand (Bank Statement / petty cash) for each project Bank Account on a monthly basis. Before preparation of the Monthly Statement of Imprest Account can take place at the end of the month, 1) the Imprest Account Cash Book must have been completed and 2) the bank statement obtained from the bank. Following is a model of the Monthly Statement of Imprest Account.

WORLD HEALTH ORGANIZATION MONTHLY STATEMENT OF IMPREST ACCOUNT IMPREST HOLDER MONTH YEAR PROJECT/OFFICE CURRENCY Balance at the end of above month, as per Imprest Account Cash Book: Bank.....................................................

A

Petty Cash............................................. + B TOTAL C Total amounts paid out during the month:

From the Bank Account.......................... D From Petty Cash..................................... + E SUB-TOTAL Deduct: amounts received (except replenishments)................... _ Deduct: transfers from Bank to Petty Cash and vice-versa........ _ SUB-TOTAL Temporary increase of the level of the account Amount increased or brought forward balance..............................................

Deduct: expenditure (included in D&E) _ Balance on Hand: _ Deduct: if not needed anymore (if balance is to be used next month see H below)

AMOUNTS TO BE REPLENISHED THIS MONTH

(Quote this amount when requesting replenishment)

F

Add: previous months replenishments not yet received ...............G Deduct: balance of temporary increase to be used next month ....….....H AUTHORIZED LEVEL OF IMPREST ACCOUNT (C+F+G-H) RECONCILIATION OF BANK BALANCE NAME OF BANK Balance per bank statement ( date.......................................) I Deduct cheques issued but not paid by bank Date Number ............................

...................... ......................................................………………………….

(If space insufficient, list items on a separate list) TOTAL J Add: amounts banked, not yet credited by bank Date Details ............................

............……….... ...................................................……………………………

K

BANK BALANCE, PER IMPREST ACCOUNT CASH BOOK (I-J+K) (should equal item A above)

PLACE DATE SIGNATURE

Adapted from WHO Imprest Account System Form WHO413RO (10/00) 15 000

WORLD HEALTH ORGANIZATION MONTHLY STATEMENT OF IMPREST ACCOUNT IMPREST HOLDER MONTH YEAR PROJECT/OFFICE CURRENCY Balance at the end of above month, as per Imprest Account Cash Book: Bank.....................................................

A

Petty Cash............................................. + B TOTAL C Total amounts paid out during the month:

From the Bank Account.......................... D From Petty Cash..................................... + E SUB-TOTAL Deduct: amounts received (except replenishments)................... _ Deduct: transfers from Bank to Petty Cash and vice-versa........ _ SUB-TOTAL Temporary increase of the level of the account Amount increased or brought forward balance..............................................

Deduct: expenditure (included in D&E) _ Balance on Hand: _ Deduct: if not needed anymore (if balance is to be used next month see H below)

AMOUNTS TO BE REPLENISHED THIS MONTH

(Quote this amount when requesting replenishment)

F

Add: previous months replenishments not yet received ...............G Deduct: balance of temporary increase to be used next month ....….....H AUTHORIZED LEVEL OF IMPREST ACCOUNT (C+F+G-H) RECONCILIATION OF BANK BALANCE NAME OF BANK Balance per bank statement ( date.......................................) I Deduct cheques issued but not paid by bank Date Number ............................

...................... ......................................................………………………….

(If space insufficient, list items on a separate list) TOTAL J Add: amounts banked, not yet credited by bank Date Details ............................

............……….... ...................................................……………………………

K

BANK BALANCE, PER IMPREST ACCOUNT CASH BOOK (I-J+K) (should equal item A above)

PLACE DATE SIGNATURE

Adapted from WHO Imprest Account System Form WHO413RO (10/00) 15 000

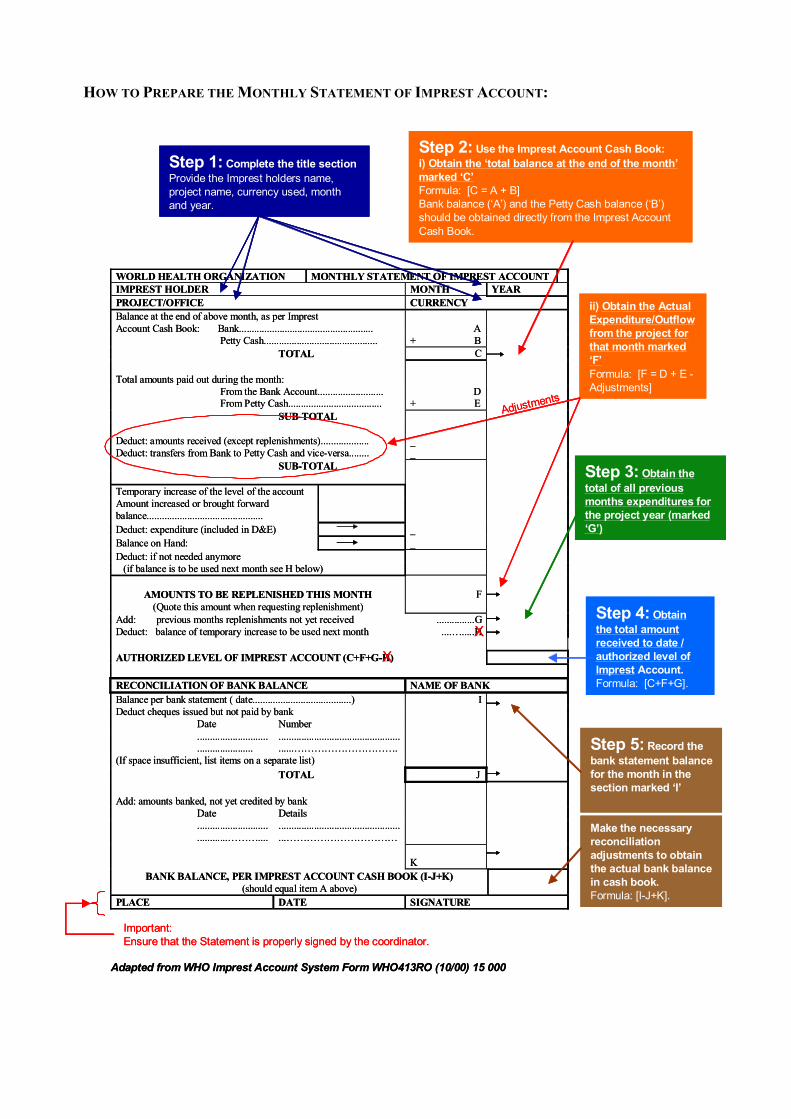

HOW TO PREPARE THE MONTHLY STATEMENT OF IMPREST ACCOUNT:

WORLD HEALTH ORGANIZATION MONTHLY STATEMENT OF IMPREST ACCOUNT IMPREST HOLDER MONTH YEAR PROJECT/OFFICE CURRENCY Balance at the end of above month, as per Imprest Account Cash Book: Bank.....................................................

A

Petty Cash............................................. + B TOTAL C Total amounts paid out during the month:

From the Bank Account.......................... D From Petty Cash..................................... + E SUB-TOTAL Deduct: amounts received (except replenishments)................... _ Deduct: transfers from Bank to Petty Cash and vice-versa........ _ SUB-TOTAL Temporary increase of the level of the account Amount increased or brought forward balance..............................................

Deduct: expenditure (included in D&E) _ Balance on Hand: _ Deduct: if not needed anymore (if balance is to be used next month see H below)

AMOUNTS TO BE REPLENISHED THIS MONTH

(Quote this amount when requesting replenishment)

F

Add: previous months replenishments not yet received ...............G Deduct: balance of temporary increase to be used next month ....….....H AUTHORIZED LEVEL OF IMPREST ACCOUNT (C+F+G-H) RECONCILIATION OF BANK BALANCE NAME OF BANK Balance per bank statement ( date.......................................) I Deduct cheques issued but not paid by bank Date Number ............................

...................... ......................................................………………………….

(If space insufficient, list items on a separate list) TOTAL J Add: amounts banked, not yet credited by bank Date Details ............................

............……….... ...................................................……………………………

K

BANK BALANCE, PER IMPREST ACCOUNT CASH BOOK (I-J+K) (should equal item A above)

PLACE DATE SIGNATURE

Step 1: Complete the title sectionProvide the Imprest holders name, project name, currency used, month and year.

Step 2: Use the Imprest Account Cash Book:i) Obtain the ‘total balance at the end of the month’ marked ‘C’Formula: [C = A + B] Bank balance (‘A’) and the Petty Cash balance (‘B’) should be obtained directly from the Imprest Account Cash Book.

ii) Obtain the Actual Expenditure/Outflow from the project for that month marked ‘F’Formula: [F = D + E -Adjustments]

Step 3: Obtain thetotal of all previous months expenditures for the project year (marked ‘G’)

Step 4: Obtain the total amount received to date / authorized level of Imprest Account. Formula: [C+F+G].

Step 5: Record the bank statement balance for the month in the section marked ‘I’

Make the necessary reconciliation adjustments to obtain the actual bank balance in cash book. Formula: [I-J+K].

Important:Ensure that the Statement is properly signed by the coordinator.

X

X

Adjustments

Adapted from WHO Imprest Account System Form WHO413RO (10/00) 15 000

WORLD HEALTH ORGANIZATION MONTHLY STATEMENT OF IMPREST ACCOUNT IMPREST HOLDER MONTH YEAR PROJECT/OFFICE CURRENCY Balance at the end of above month, as per Imprest Account Cash Book: Bank.....................................................

A

Petty Cash............................................. + B TOTAL C Total amounts paid out during the month:

From the Bank Account.......................... D From Petty Cash..................................... + E SUB-TOTAL Deduct: amounts received (except replenishments)................... _ Deduct: transfers from Bank to Petty Cash and vice-versa........ _ SUB-TOTAL Temporary increase of the level of the account Amount increased or brought forward balance..............................................

Deduct: expenditure (included in D&E) _ Balance on Hand: _ Deduct: if not needed anymore (if balance is to be used next month see H below)

AMOUNTS TO BE REPLENISHED THIS MONTH

(Quote this amount when requesting replenishment)

F

Add: previous months replenishments not yet received ...............G Deduct: balance of temporary increase to be used next month ....….....H AUTHORIZED LEVEL OF IMPREST ACCOUNT (C+F+G-H) RECONCILIATION OF BANK BALANCE NAME OF BANK Balance per bank statement ( date.......................................) I Deduct cheques issued but not paid by bank Date Number ............................

...................... ......................................................………………………….

(If space insufficient, list items on a separate list) TOTAL J Add: amounts banked, not yet credited by bank Date Details ............................

............……….... ...................................................……………………………

K

BANK BALANCE, PER IMPREST ACCOUNT CASH BOOK (I-J+K) (should equal item A above)

PLACE DATE SIGNATURE

Step 1: Complete the title sectionProvide the Imprest holders name, project name, currency used, month and year.

Step 2: Use the Imprest Account Cash Book:i) Obtain the ‘total balance at the end of the month’ marked ‘C’Formula: [C = A + B] Bank balance (‘A’) and the Petty Cash balance (‘B’) should be obtained directly from the Imprest Account Cash Book.

ii) Obtain the Actual Expenditure/Outflow from the project for that month marked ‘F’Formula: [F = D + E -Adjustments]

Step 3: Obtain thetotal of all previous months expenditures for the project year (marked ‘G’)

Step 4: Obtain the total amount received to date / authorized level of Imprest Account. Formula: [C+F+G].

Step 5: Record the bank statement balance for the month in the section marked ‘I’

Make the necessary reconciliation adjustments to obtain the actual bank balance in cash book. Formula: [I-J+K].

Important:Ensure that the Statement is properly signed by the coordinator.

X

X

Adjustments

Adapted from WHO Imprest Account System Form WHO413RO (10/00) 15 000

25

5 Steps to Fill the Monthly Statement of Imprest Account

To begin, start by carefully reviewing and understanding the structure of this statement. Step 1: Complete the title section (record imprest holders name, project name, currency used, month and year). Step 2: Use the Imprest Account Cash Book to provide:

i) The ‘total balance at the end of the month’(marked ‘C’ on the Monthly Statement of Imprest Account) – you will need the months Bank balance (‘A’) and the Petty Cash balance (‘B’) both obtained directly from the Imprest Account Cash Book.

Formula: [C = A + B]

ii) The Actual Expenditure/Outflow from the project for that month (marked ‘F’ on the Monthly Statement of Imprest Account).

Formula: [F = D + E - Adjustments] Step 3: Obtain the total of all previous months expenditures (marked ‘G’) - this is the total of all expenditures from the first month of the project for the year under consideration. Step 4: Using the data above, obtain the total amount received to date from APOC / authorized level of Imprest Account. Formula: [C+F+G]. Step 5: Record the Balance per bank statement in the reconciliation of Bank Balance section marked ‘I’ and make the necessary reconciliation adjustments. Formula: [I-J+K]. Step by Step Explanation 1. Complete the title section

• Record the Imprest holders name, project name, currency used, month and year. 2. Use the Imprest Account Cash Book to provide:

i) The ‘total balance at the end of the month’(marked ‘C’ on the Monthly Statement of Imprest Account) – this total balance is the sum of the months Bank balance (‘A’) and the Petty Cash balance (‘B’) both obtained directly from the Imprest Account Cash Book in the columns labeled ‘A’ and ‘B’. ii) The actual Expenditure/Outflows from the project for that month (marked ‘F’ on the Monthly Statement of Imprest Account) is obtained by first computing ‘D’ and ‘E’ and making the necessary adjustments as follows: • Provide the ‘total amounts paid out during the month’ as per the Imprest Account Cash

Book – this balance is the sum of the months Bank account receipts (‘D’) and the Petty Cash receipts (‘E’) obtained directly from the Imprest Account Cash Book in the columns labeled ‘D’ and ‘E’.

• Make adjustments to the amounts paid out of the Bank Account and Petty Cash - this is done by deducting all other amounts received (except replenishment) and deducting all transfers made from bank to petty cash and vice versa. By so doing you will have obtained the Actual Expenditure/Outflows from the project for that month.

3. Obtain the total of all previous months’ expenditures

• This amount is the total of all expenditures from the first month of the project for the year under consideration.

4. Obtain the total amount received from APOC to date / authorized level of Imprest Account

26

• This is the total obtained by adding the ‘total balance at the end of the month’ (‘C’) plus amount of total expenditure for the month (‘F’) and the total of all previous months’ expenditures (‘G’).

Note: Please ignore the section on Temporary Increases of the level of the Account. This section will be explained to those projects requiring it on a need-to-know basis. 5. Record the Balance per bank statement in the reconciliation of Bank Balance section (marked ‘I’). From this balance,

i) Deduct all cheques issued by the project and not cleared by the bank (marked ‘J’), ii) Add all amounts banked and not yet credited in the bank (i.e. not yet reflected in the bank statement (marked ‘K’). iii) Obtain the Bank balance per Imprest Account Cash Book. Formula: [I-J+K].

6. Attach the Bank Statement for the month to the Monthly Statement of Imprest Account.

27