Embed Size (px)

Citation preview

FINANCIAL EXAMINERS HANDBOOK (E) TECHNICAL GROUP Conference Call

Wednesday, September 27, 2017 2:00 p.m. ET/ 1:00 p.m. CT

ROLL CALL

Susan Bernard, Chair California Omar Akel/Renee Hanshaw Nevada Richard Ford Alabama Colin Wilkins New Hampshire William Arfanis Connecticut Steve Kerner New Jersey N. Kevin Brown District of Columbia Tracy Snow Ohio Cindy Andersen Illinois Joel Sander Oklahoma Grace Kelly Minnesota Missy Greiner Pennsylvania Leslie Nehring/Levi Nwasoria Missouri Patrick McNaughton Washington Justin Schrader Nebraska John Litweiler Wisconsin NAIC Support Staff: Bailey Henning

AGENDA

1. Receive Comments on Exposure Draft and Consider Adoption—Susan Bernard (CA)• Exposure Drafts Attachment One

o Guidance Related to Communication Between Analyst and Examiner Pages 5 - 12 o Handbook Technical Group Amendment Procedures Page 13 o Guidance Related to Examination Repository Updates Pages 15 - 59 o Guidance Related to Referral from PBR Review (E) Working Group Pages 61 - 103 o Guidance Related to Referral from Receivership Model Law (E) Working Group Pages 105 - 108

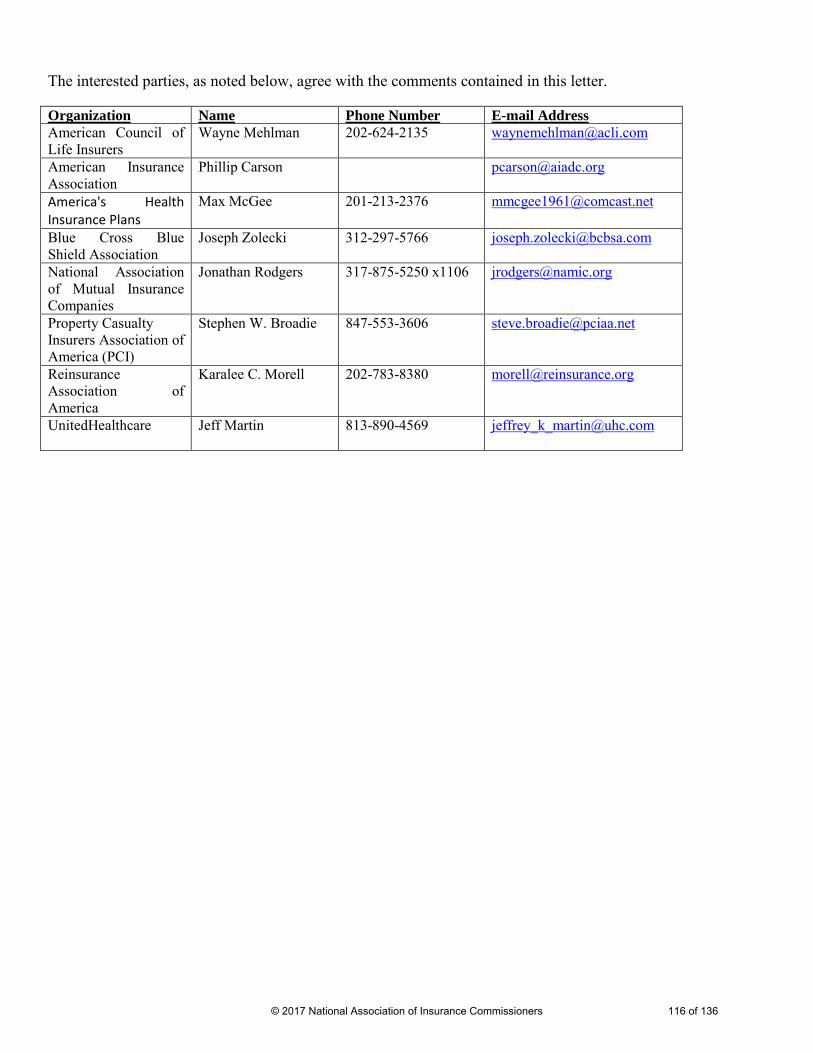

• Comment Letters Attachment Two o American Academy of Actuaries Pages 111 - 113 o Fontaine Consulting, LLC Page 114 o Joint Interested Parties Pages 115 - 116

2. Consider Exposure of Handbook Guidance Related to Referral from Financial Analysis (E)Working Group—Susan Bernard (CA)

Attachment Three

• Financial Analysis (E) Working Group Referral Page 119 • Section 1-3: Run-off Examinations Pages 120 – 121 • Section 2-1: Redomestication Pages 122 - 123

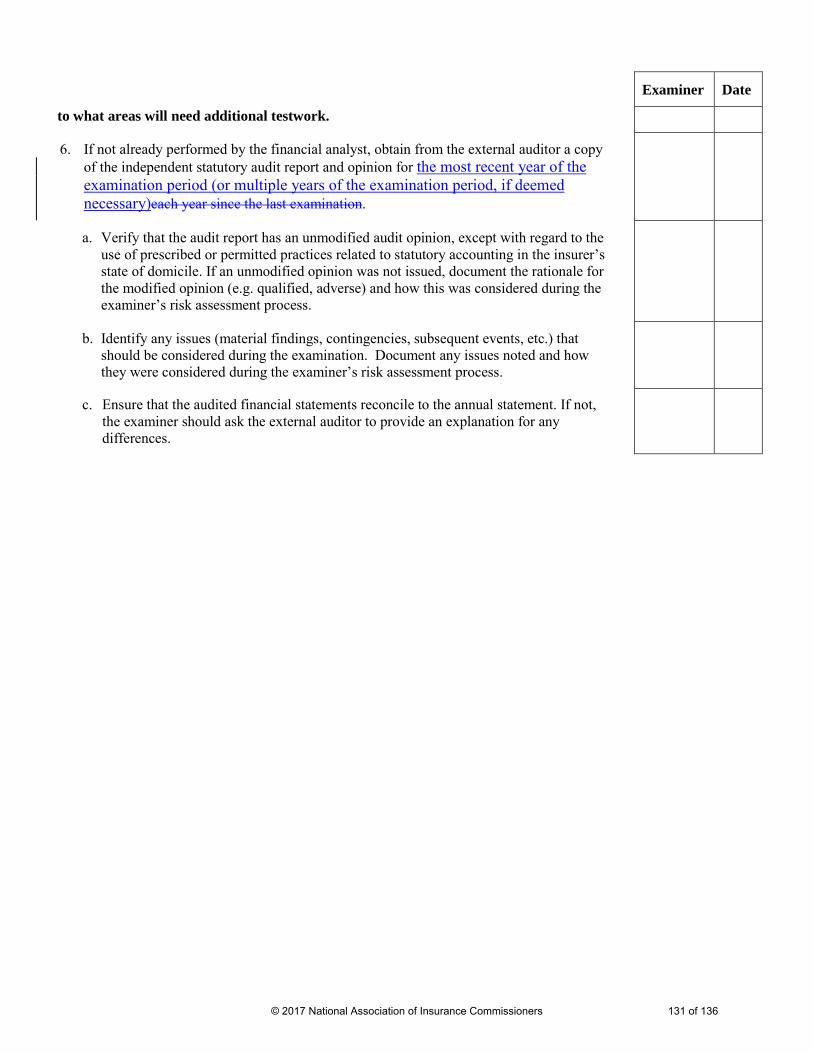

3. Consider Exposure of Handbook Guidance Related to Clean-Up—Susan Bernard (CA) Attachment Four • Section 1-1: Review & Reliance on Another State’s Workpapers (Coordination Plan) Pages 127 - 128 • Exhibit E Pages 129 - 131

4. Review 2017 Project Listing—Susan Bernard (CA) Attachment Five Pages 135 - 136

5. Any Other Matters Brought Before the Technical Group—Susan Bernard (CA)

6. Adjournment

© 2017 National Association of Insurance Commissioners 1 of 136

This page was intentionally kept blank.

© 2017 National Association of Insurance Commissioners 2 of 136

Attachment OneExposure Drafts:

• Communication Between Examiner and Analyst• Handbook Technical Group Amendment

Procedures• Examination Repository Updates• Revisions related to referral from PBR Review

(E) Working Group• Revisions related to referral from Receivership

& Insolvency (E) Task Force

© 2017 National Association of Insurance Commissioners 3 of 136

This page was intentionally kept blank.

© 2017 National Association of Insurance Commissioners 4 of 136

--

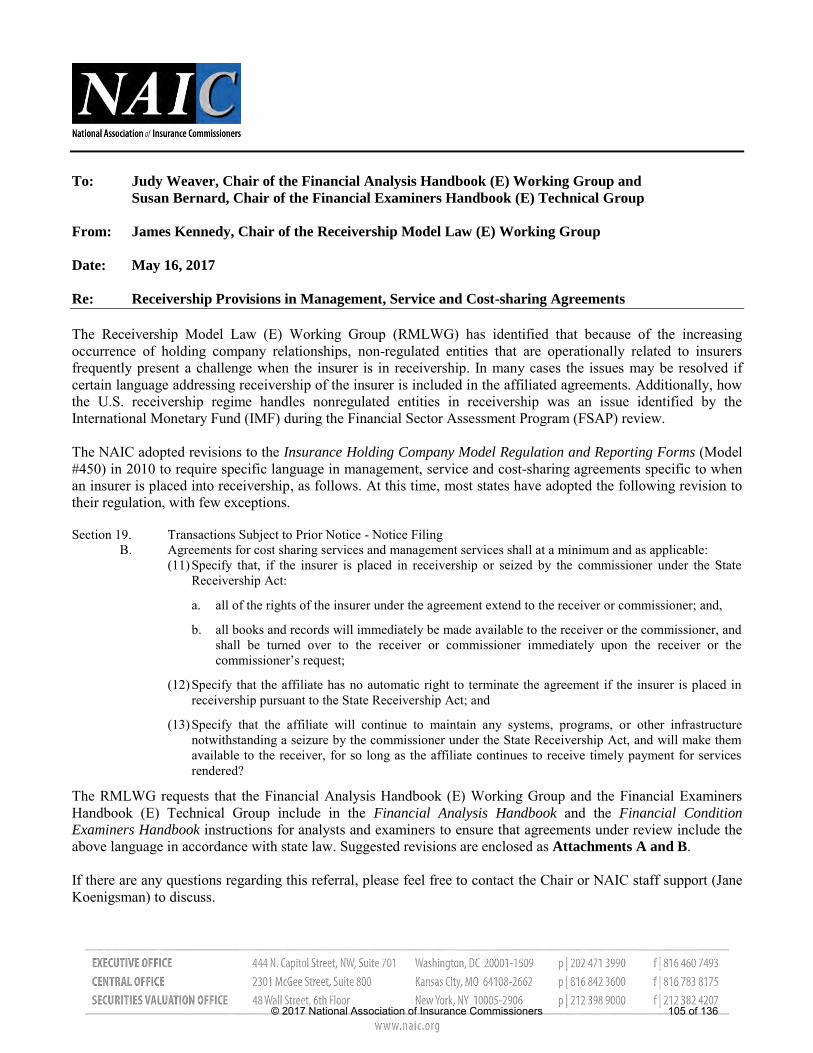

To: Commissioner Todd E. Kiser, Chair, Financial Regulation Standards and Accreditation (F) Committee From: Judy Weaver, Chair, Financial Analysis Handbook (E) Working Group Date: July 10, 2017 Re: Revisions to Accreditation Review Team Guidelines for Risk-Focused Analysis

On the Financial Analysis Handbook (E) Working Group’s July 10, 2017 conference call, the Working Group finalized proposed revisions to Accreditation Review Team Guidelines to incorporate enhancements to the financial analysis process, including the Financial Analysis Handbook (Handbook), for the risk-focused assessment of insurers during annual and quarterly analysis. The Working Group adopted the risk-focused framework on its January 23, 2017 conference call. The changes to the Handbook for risk-focused analysis will be applicable beginning with the annual 2017 analysis. The revisions to the Accreditation Review Team Guidelines, included in Attachment A, are intended to align the standards and guidelines with the new analysis process.

Within the revisions is included a change to the process-oriented guidelines for communication of relevant information to/from financial analysis staff (b.3.). The Financial Examiners Handbook (E) Technical Group reviewed the revisions on their June 29 conference call and drafted coordinating revisions to examination guidelines necessary for consistency, which will be referred separately.

Please contact Financial Analysis Handbook (E) Working Group staff Jane Koenigsman ([email protected]) if you have any questions or would like additional information.

© 2017 National Association of Insurance Commissioners 5 of 136

Part B1: Financial Analysis

--------------------------------------------DETAIL ELIMINATED TO CONSERVE SPACE----------------------------

b. Communication of Relevant Information to/from Financial Analysis Staff

Standard: The department should ensure that all relevant information and data obtained that may assist in the financial analysis process is provided to the financial analysis staff. The department should ensure that findings of the financial analysis staff are communicated to the appropriate person(s) within the department.

Results-Oriented Guidelines: 1. Analysts should effectively communicate and coordinate with various areas within the department,

including management, the financial examination staff and other non-financial areas, as applicable.Evidence of this communication should be clearly documented in the analysis files. When assessingcompliance with this guideline, consideration should be given to the following: The analyst’s utilization of pertinent information that is obtained from management and/or other

areas of the department Sharing by the analyst of any pertinent information obtained as a result of the financial analysis

with management and/or other areas of the department The analyst’s communication and collaboration with the financial examination staff before,

during and at the conclusion of a financial examination The analyst’s utilization and incorporation of pertinent information from the financial

examination in conducting ongoing analysis procedures.

Process-Oriented Guidelines: 1. The analysis process should include a formal periodic method that allows for pertinent information

from other areas (e.g. legal, rates and forms, actuarial, etc.) that could impact the financial analysisprocess to be shared with the financial analysis staff Although no one method is required, thefollowing are examples that may demonstrate compliance: quarterly department heads meetings,department managers’ meetings, information requests to other areas, etc.

2. Financial solvency information identified as a result of the financial analysis, particularly adversefindings or significant unresolved issues, should be communicated to, management and otherdepartment staff, as necessary.

3. Results of ongoing analysis procedures should be shared with the financial examiners to assist inexamination planning. At the beginning of each examination, the analyst should communicate areasof concern and specific issues to address during the examination. To assist in communication, theanalyst should provide a current copy of the Insurer Profile Summary as well as any other supportingdocumentation necessary to communicate concerns and suggested procedures.

1. Results of ongoing analysis procedures should be shared with the financial examiners to assist inexamination planning through a coordination meeting. An email exchange alone, between analyst and examiner is not considered sufficient communication in planning an examination. During the planning process of each examination, the analyst should meet (in person or via conference call) with the examiner to communicate areas of concern and specific issues to address during the examination. To assist in communication, the analyst should provide a current copy of the Insurer

© 2017 National Association of Insurance Commissioners 6 of 136

Profile Summary as well as other supporting analyst work papers and other documentation already on file at the department to communicate current or prospective concerns or observations and suggested procedures.

1.2.The financial analyst should participate in a collaborative follow-up meeting or conference call at the end of the examination to discuss the following: Examination results and/or findings Insurer’s prioritization level Ongoing supervisory plan and the completed Summary Review Memorandum Re-aAssessment of branded risks as contained in the Insurer Profile Summary

5. The analyst should follow-up with the insurer to address concerns/issues identified as a result ofexamination activities, which may include examination report findings, management lettercomments or prospective risks.

--------------------------------------------DETAIL ELIMINATED TO CONSERVE SPACE----------------------------

© 2017 National Association of Insurance Commissioners 7 of 136

Part B2: Financial Examinations

------------------------------------------------DETAIL ELIMINATED TO CONSERVE SPACE---------------------------------------------

b. Communication of Relevant Information to/from Examination Staff

Standard: The department should ensure that all relevant information and data obtained that may assist in the financial examination process is provided to the financial examination staff. The department should ensure that findings of the financial examination staff are communicated to the appropriate person(s).

Results-Oriented Guidelines: 1. Examiners should effectively communicate and coordinate with various areas within the department.

Such communication should consist of both: 1) communication of information held by other areas ofthe department to the examiners as appropriate to enhance the quality of the examination; and 2)communication of key examination findings to other areas of the department as appropriate toenhance the work performed by those other areas. Evidence of this communication should be clearlydocumented in the examination files. When assessing compliance with this guideline, considerationshould be given to the following: The examiner’s utilization of pertinent information that is obtained from management and/or

other areas of the department. Sharing by the examiner of any pertinent information obtained as a result of the financial

examination with management and/or other areas of the department. The examiner’s communication and collaboration with the financial analysis staff before, during

and at the conclusion of a financial examination. The examiner’s utilization and incorporation of pertinent information from the financial analysis

in planning and conducting examination procedures.

Process-Oriented Guidelines: 1. The examination process should include a formal method that allows for pertinent information from

other areas (e.g., legal, rates and forms, actuarial, etc.) within the department that could impact thefinancial examination to be shared with the examination staff. Although no one method is required,the following are examples that may demonstrate compliance: regularly scheduled department headmeetings, department managers’ meetings, information requests to other areas of the department,etc.).

2. The examiner-in-charge (EIC) should provide a status report to the chief examiner (or designee) atleast monthly and include information as required by the NAIC Financial Condition ExaminersHandbook (Examiners Handbook).

3. Financial solvency information identified as a result of the financial examination, particularlyadverse findings or significant unresolved issues, should be communicated by the examination teamto the chief examiner, financial analyst, management and other department staff, as necessary

4. At the beginningDuring the planning process of each examination, the examiner should meet (inperson or via conference call) with the assigned financial analyst (and/or analyst supervisor) toobtain input from the financial analyst regarding areas of concern and specific issues to addressduring the examination. An email exchange alone is not considered sufficient communication in

© 2017 National Association of Insurance Commissioners 8 of 136

planning an examination. To assist in gathering this information, the examiner should obtain a current IPS from the financial analyst, as well as any other supporting analyst workpapers and other documentation already on file at the department to communicate current or prospective necessary to understand the financial analyst’s concerns or observations and suggested procedures.

5. Results of examination activities should be shared with the financial analyst to assist in conductingongoing analysis procedures. At the conclusion of an examination, the examiner should hold acollaborative follow-up meeting or conference call with the financial analyst to discuss thefollowing: Examination results and/or findings. Insurer’s prioritization level. Ongoing supervisory plan and the completed SRM. Assessment of branded risks contained in the IPS.

6. The examiner should recommend follow-up for the financial analyst to perform in addressingconcerns/issues identified as a result of examination activities. In so doing, the examiner shouldcommunicate examination report recommendations, management letter comments and/orprospective risks. Information to be provided as a result of each full-scope examination shouldinclude the report of examination, management letter (if used) and SRM (or substantially similardocument).

© 2017 National Association of Insurance Commissioners 9 of 136

EXHIBIT A EXAMINATION PLANNING PROCEDURES CHECKLIST

COMPANY NAME __________________________________________________________________________

PERIOD OF EXAMINATION _________________________________________________________________

The following checklist details the components of Phase 1 and Phase 2, as well as other information that should be considered during the planning process. Narrative guidance is provided within Section 2 of this Handbook to aid examiners in understanding the risk-focused surveillance process.

Pre-planning Procedures Examiner Date

1. At least six months prior to the as-of date, notify the company and itsexternal auditors, with company personnel’s assistance, that anexamination will take place and that the auditor workpapers will berequested when the exam begins.

2. If the examination is to be performed on a company that is part of aholding company group, send an informal notification at least sixmonths prior to the as-of date to other states that have domestics in thegroup.

3. Call the examination in the Financial Exam Electronic TrackingSystem (FEETS) at least 90 days prior to the exam start date.

a. If the examination is to be performed on a company that is partof a holding company group, document your attempts tocoordinate the exam with the Lead State and other domesticstate(s) within your group. Utilize Exhibit Z – ExaminationCoordination to assist with this process.

4. Send preliminary information requests to the company with sufficientlead-time to allow information to be provided prior to the start ofexamination fieldwork. Exhibit B – Examination PlanningQuestionnaire and Exhibit C, Part One – Information TechnologyPlanning Questionnaire can be utilized to assist in developing pre-planning requests. Note: The examiner is encouraged, with input fromthe financial analyst when possible, to customize Exhibit B to theinsurer being examined prior to submitting the information request.

Phase 1 – Understand the Company and Identify Key Functional Activities to be Reviewed

Part 1: Understanding the Company

Step 1. Gather Necessary Planning Information

Meet with the Financial Analyst

1. Meet (in person or via conference call) with the assigned financialanalyst (and/or analyst supervisor) to gain an understanding of

© 2017 National Association of Insurance Commissioners 10 of 136

company information available to the department. In addition, discuss risks and concerns highlighted in the Insurer Profile Summary as well as the company’s financial condition and operating results since the last examination. Ascertain the reasons for unusual trends, abnormal ratios and transactions that are not easily discernible. Document a summary of significant risks identified by the analyst for further review on the examination. Note: An email exchange, in and of itself, is not deemed sufficient to achieve the expectation of a planning meeting with the assigned analyst.

a. If deemed necessary, obtain supporting documentationfrom the most recent annual financial statement analysis toaid in the identification of significant risks and facilitateongoing discussion with the analyst.

--------------------------------------------DETAIL ELIMINATED TO CONSERVE SPACE--------------------------------------

© 2017 National Association of Insurance Commissioners 11 of 136

EXHIBIT B EXAMINATION PLANNING QUESTIONNAIRE

The Examination Planning Questionnaire contains procedures and questions that are designed to assist the examiner in gathering necessary planning information and obtaining an understanding of the insurer’s organization. The examiner or company personnel should complete this questionnaire as early in exam planning as practical. If company personnel complete this exhibit, identification of who completed each request, as well as supporting documentation, should be provided to the examination team and the responses to this questionnaire should be critically evaluated by the examiner. If information requested through the questionnaire has already been provided to the department, the company’s response should so state and reference when and how the information was provided. The substance of the information collected during the completion of this questionnaire should be incorporated into the Examination Planning Memorandum. The questionnaire responses should be considered when identifying the inherent risks of the insurer. They should also impact the planned examination approach, and the nature, timing and extent of examination procedures performed.

Examiners may consider requesting the completion of Section K: Liquidity during intervals outside of the full-scope examination period (e.g., annually). The majority of questions in this section are intended for all insurers; however, questions 9, 10 and 11 in this section apply to life insurers only. Therefore, the questionnaire should be customized before it is provided to the insurer. If the examiner has prior knowledge or reason to believe the company may be facing significant liquidity risks, the additional liquidity tables included at Attachment 1 may also be requested to prompt the company to provide greater detail regarding potential liquidity risks (typically most applicable to life insurers). Alternatively, if the examiner is not already aware of significant liquidity risks, it may be appropriate to first review the company’s responses to the liquidity questions before determining whether the additional detail provided by the tables should be gathered.

Customization of Questionnaire Prior to Distribution This questionnaire should be customized to the insurer being examined to allow the examiner or company personnel completing the questionnaire to focus only on the applicable questions. The questions that remain should be completely addressed, providing additional support if necessary. It is possible that the financial analyst has performed work in these areas as part of the analysis procedures; therefore, prior to completion of the questionnaire, the exam team should communicate with the analyst to determine whether the information has already been obtained in order to reduce duplication of work and duplicative information requests to the insurer.

To assist the exam team in identifying information that may already be provided to the department, requests that may be collected through the financial analysis process have been denoted with an asterisk (*) for ease in identification and potential removal from the questionnaire.

Instructions for Completing Exhibit Please provide the most current version of the following items to the examination team within the specified timeline. If a requested item has already been provided to the department, please note the date and to whom it was provided.

COMPLETED BY

SUPPORTING DOCUMENTATION

I. OWNERSHIP AND MANAGEMENT INFLUENCES

A. Concentration of Ownership

1. Provide documentation explaining:

a. The concentration of ownership.*

--------------------------------------------DETAIL ELIMINATED TO CONSERVE SPACE--------------------------------------

© 2017 National Association of Insurance Commissioners 12 of 136

PROCEDURES OF THE FINANCIAL EXAMINERS HANDBOOK (E) TECHNICAL GROUP IN CONNECTION WITH PROPOSED AMENDMENTS

TO THE FINANCIAL CONDITION EXAMINERS HANDBOOK

The following establishes procedures of the Financial Examiners Handbook (E) Technical Group (Technical Group) for proposed changes, amendments and/or modifications to the Financial Condition Examiners Handbook.

1. The Technical Group may consider relevant proposals to change the NAIC Financial ConditionExaminers Handbook (Handbook) at any conference call, interim or national meeting (“themeeting”) throughout the year as scheduled by the Technical Group.

2. If a proposal for suggested changes, amendments and/or modifications is submitted to, or filedwith, NAIC staff support it may be considered at the next regularly scheduled meeting of theTechnical Group.

3. The Technical Group publishes a formal submission form and instructions that can be used tosubmit proposals and is available on the Group’s webpage. However, proposals may also besubmitted in an alternate format provided that they are stated in a concise and complete format. Inaddition, if another NAIC committee, task force or Technical group is known to have consideredthis proposal, that committee, task force or Technical group should provide any relevantinformation.

4. Any proposal that would change the Handbook will be effective following the NAIC Fall/WinterNational Meeting (i.e. of the preceding year) in which it was adopted (e.g., a change proposed tobe effective January 1, 2018 must be adopted no later than the 2017 Fall/Winer National Meeting).

5. Upon receipt of a proposal, the Technical Group will review the proposal at the next scheduledmeeting and determine whether to consider the proposal for public comment. The publiccomment period shall be thirty days unless extended by the Technical Group. The Technical Groupwill consider comments received on each proposal at its next meeting and take action. Proposalsunder consideration may be deferred by the Technical Group until the following scheduledmeeting. The Technical Group may form an ad hoc group to study the proposal, if needed. TheTechnical Group may also refer proposals to other NAIC committees for technical expertise orreview. If a proposal has been referred to another NAIC committee, the proposal will come off theTechnical Group’s agenda until a response has been received.

6. NAIC staff support will prepare an agenda inclusive of all proposed changes. The agenda andrelevant materials shall be sent via e-mail to each member of the Technical Group, interestedregulators and interested parties and posted to the Technical Group’s webpage approximately 5-10business days prior to the next regularly scheduled meeting during which the proposal would beconsidered.

7. In rare instances, or where emergency action may be required, suggested changes and amendmentscan be considered as an exception to the above stated process and timeline based on a two-thirdsmajority consent of the Technical Group members present.

8. NAIC staff support will publish the Handbook on or about February 28, each year. NAIC staffwill post to the NAIC Publications Web site any material subsequent corrections to thesepublications.

© 2017 National Association of Insurance Commissioners 13 of 136

This page was intentionally kept blank.

© 2017 National Association of Insurance Commissioners 14 of 136

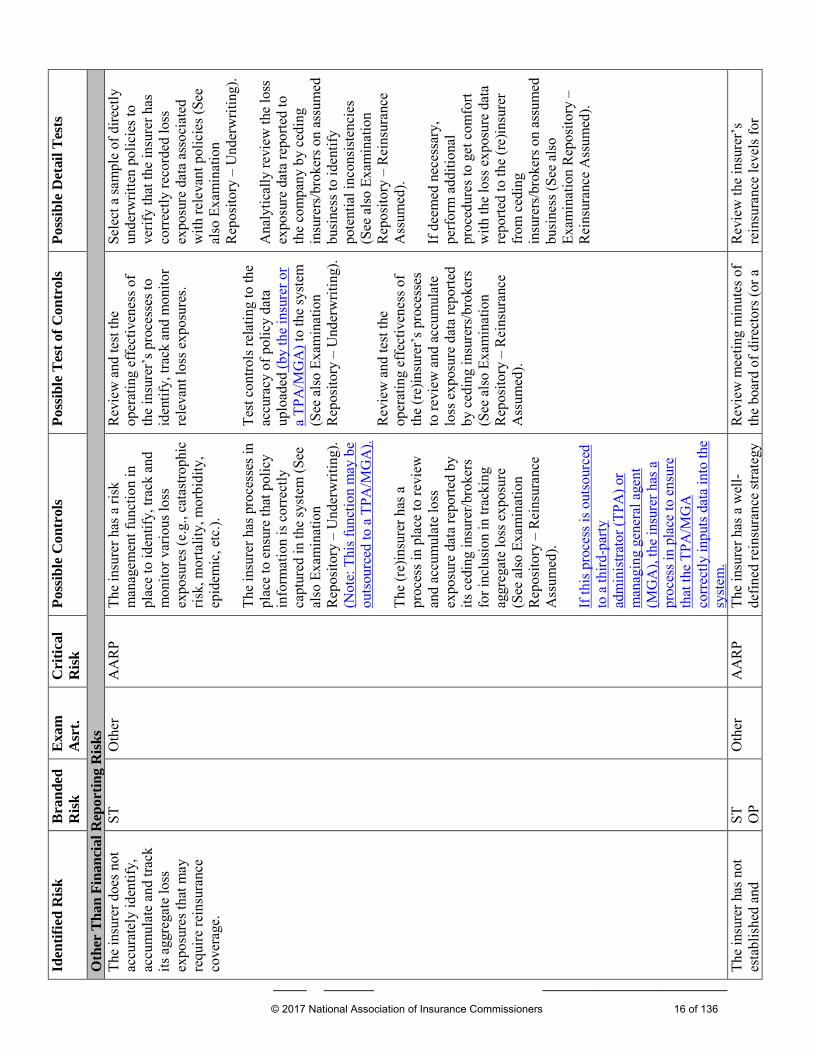

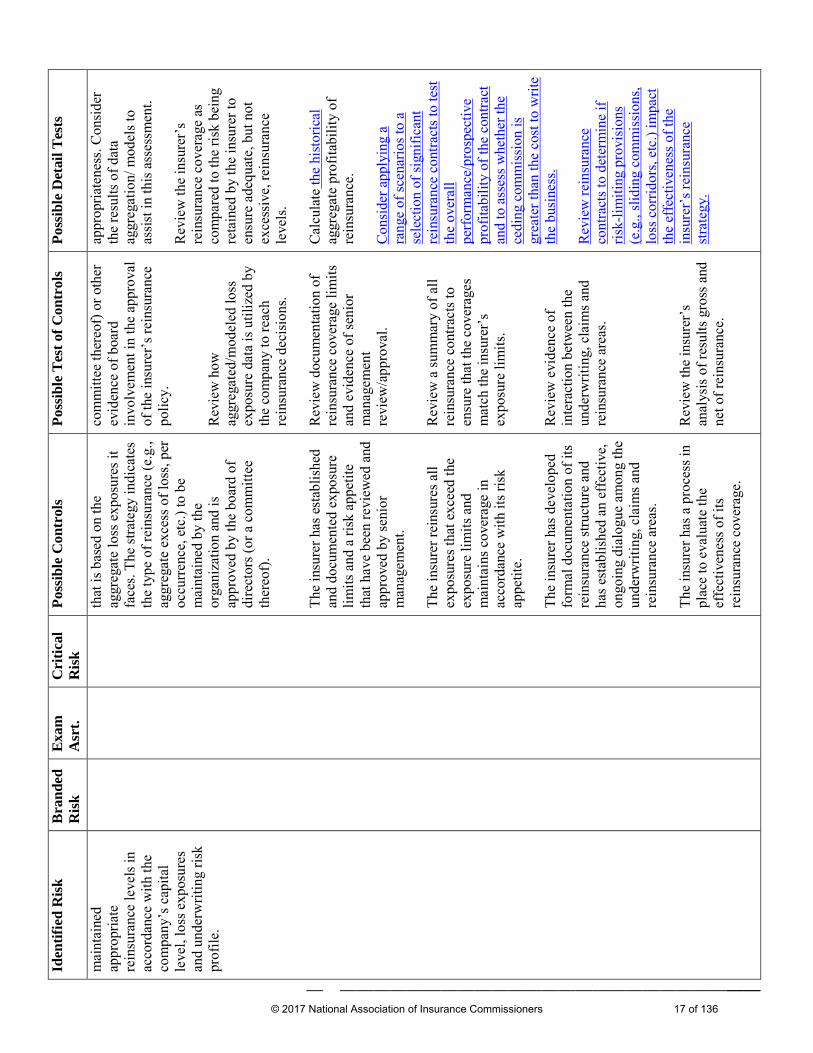

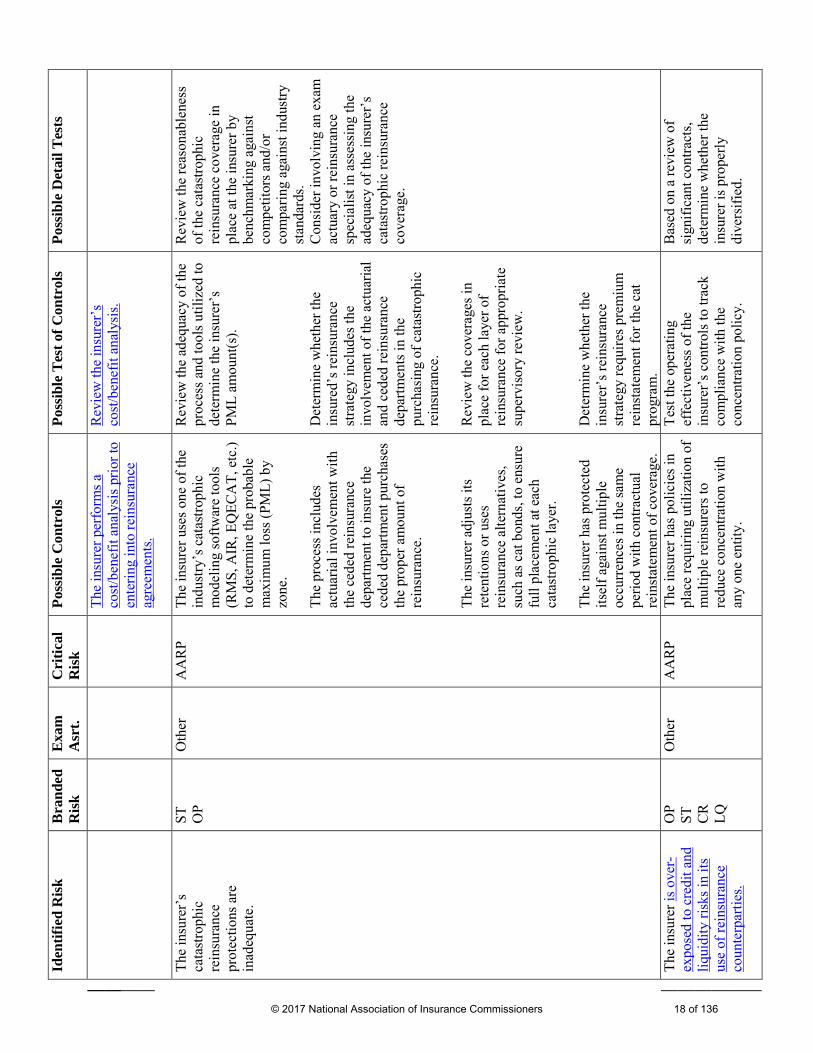

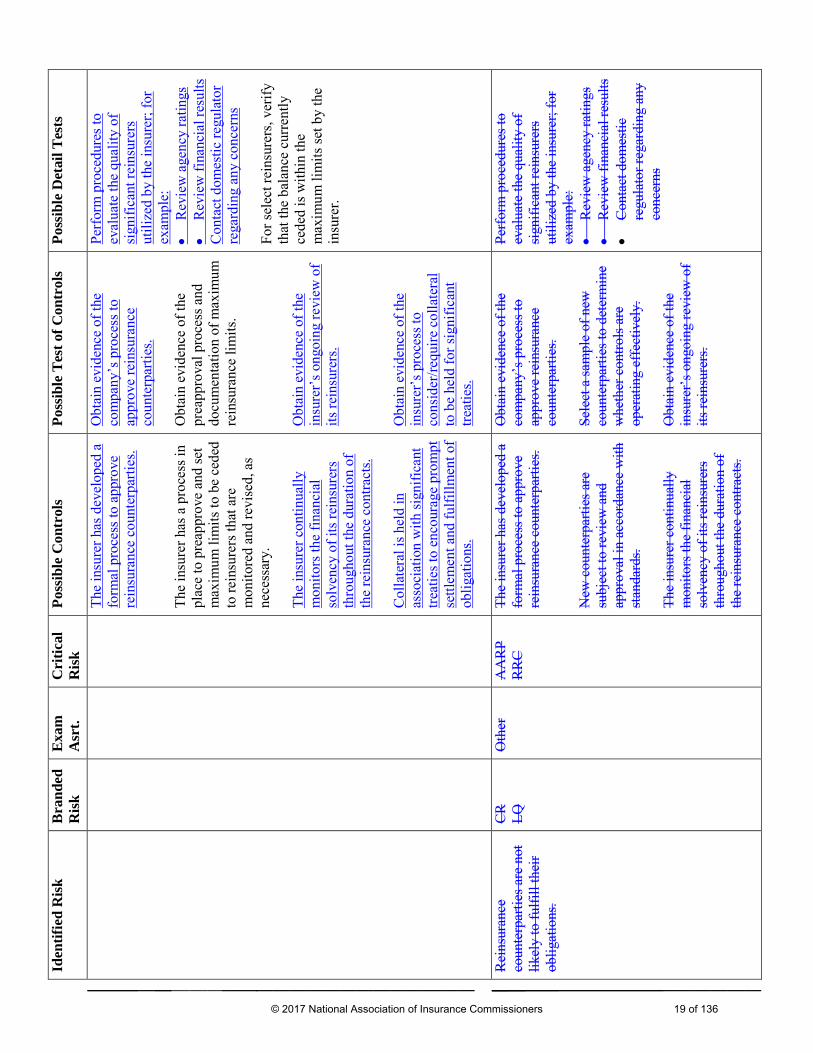

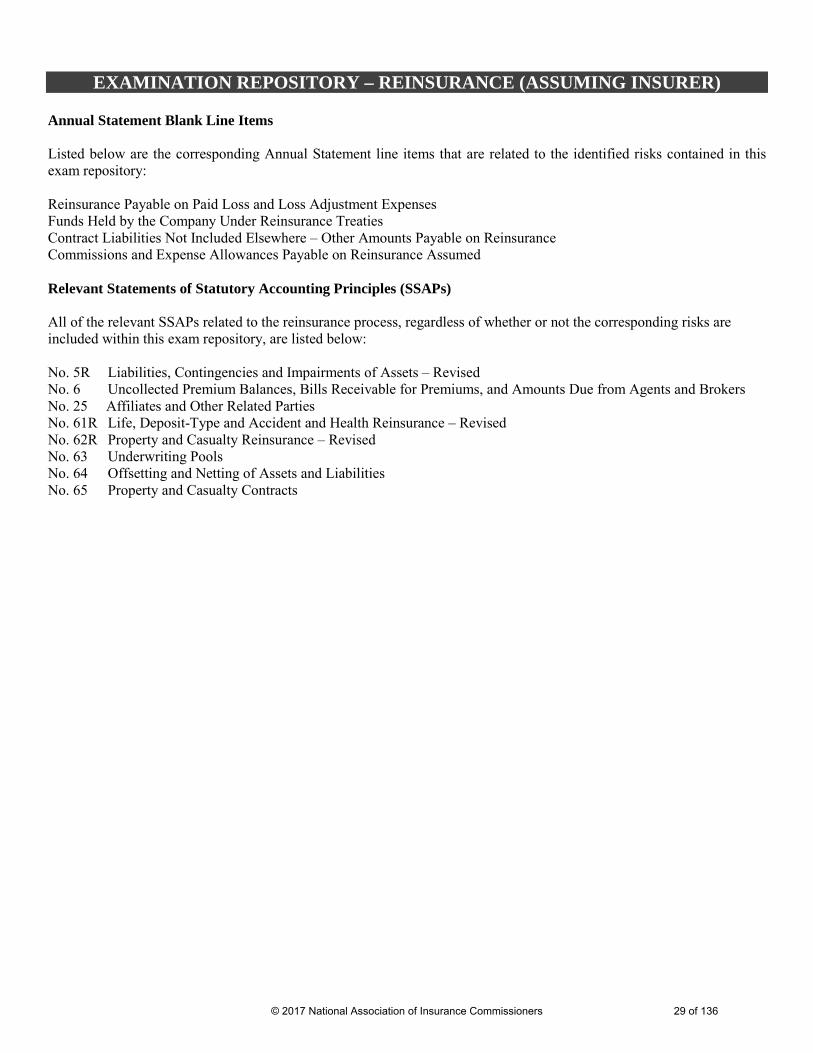

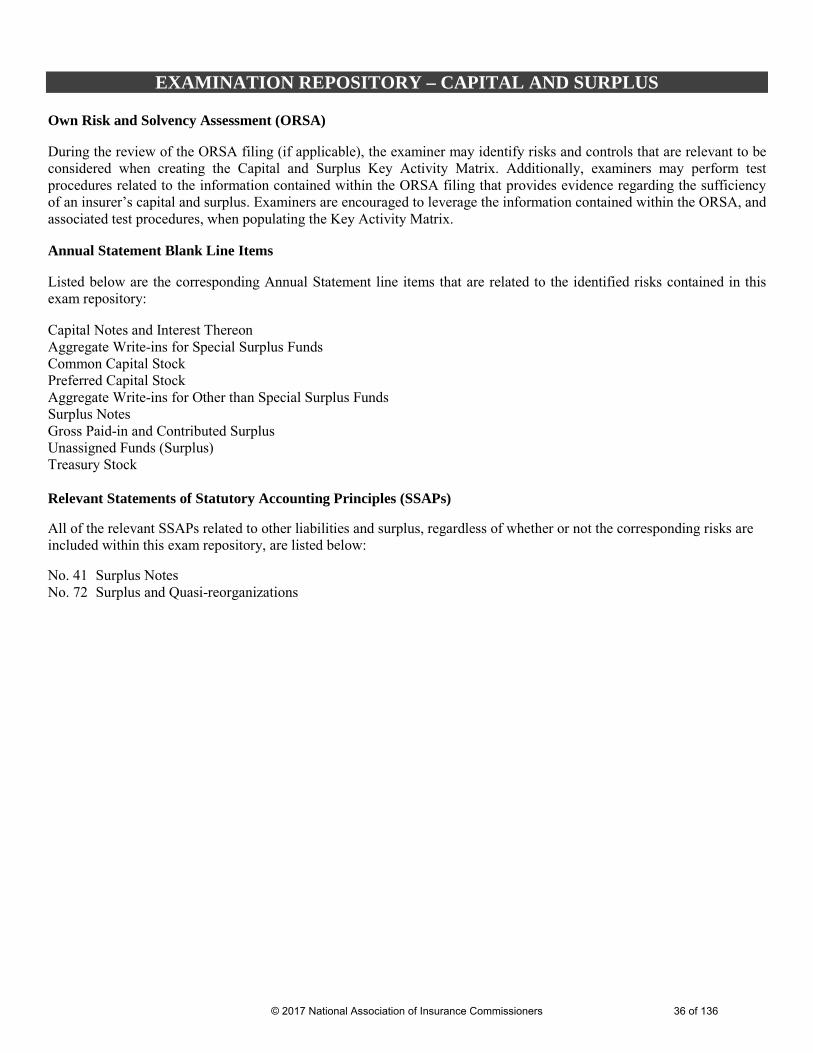

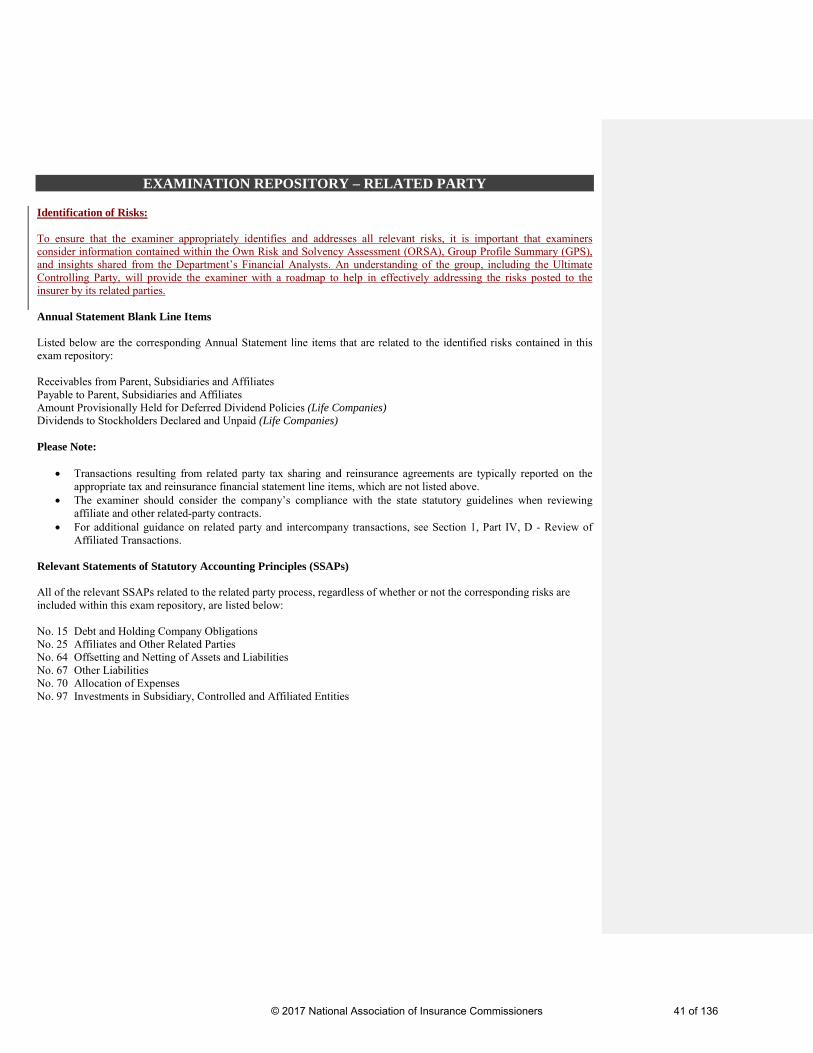

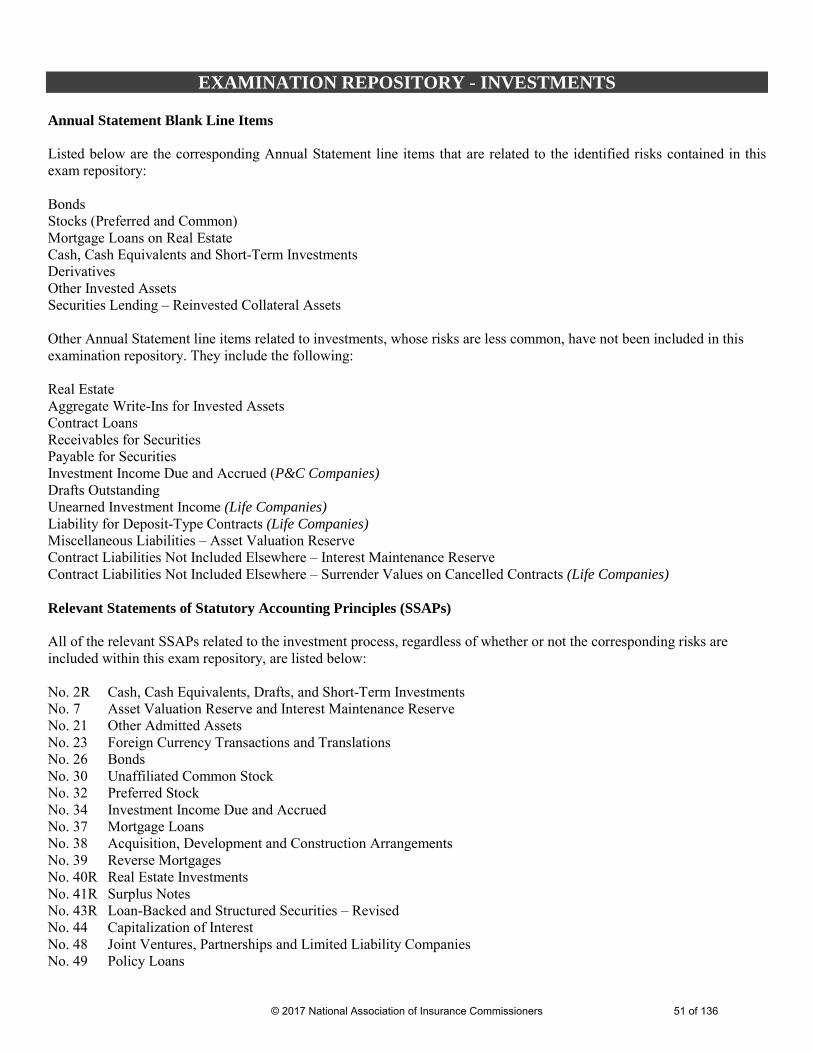

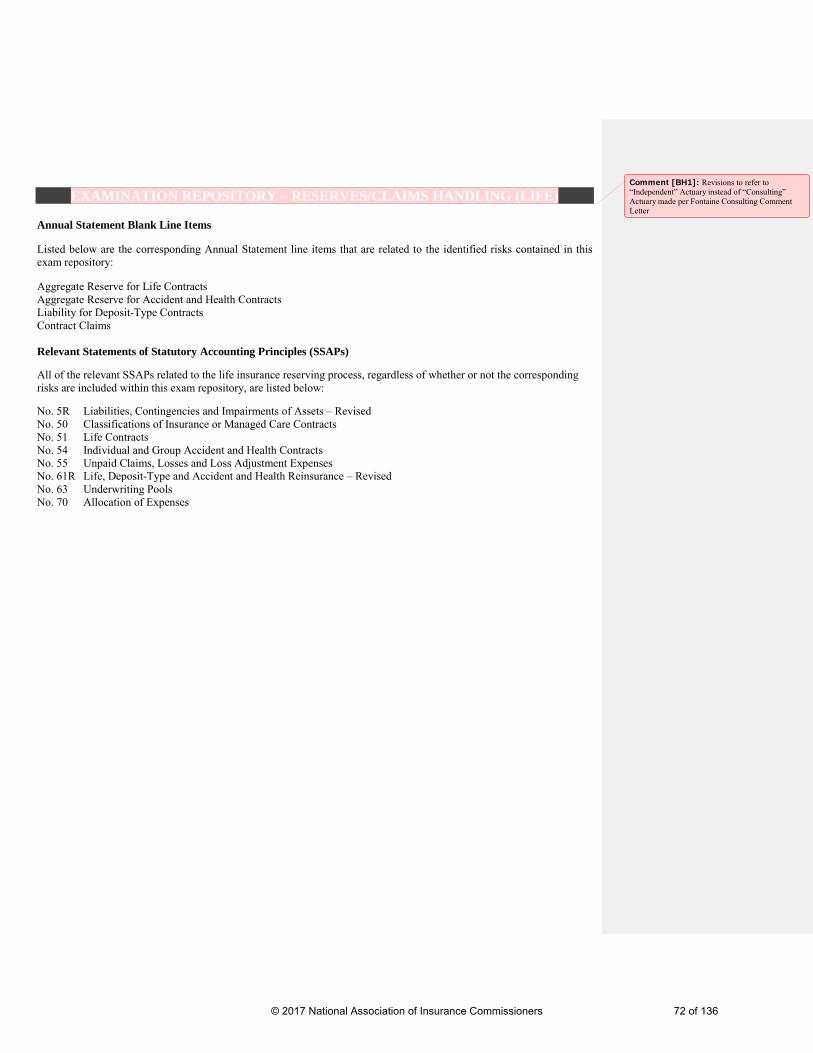

EXAMINATION REPOSITORY – REINSURANCE (CEDING INSURER)

Annual Statement Blank Line Items

Listed below are the corresponding Annual Statement line items that are related to the identified risks contained in this exam repository:

Amounts Recoverable from Reinsurers Funds Held by or Deposited with Reinsured Companies Other Amounts Receivable Under Reinsurance Contracts Ceded Reinsurance Premiums Payable (Net of Ceding Commissions) Funds Held by Company Under Reinsurance Treaties (P&C Companies) Funds Held Under Reinsurance Treaties with Unauthorized Reinsurers (Life Companies) Provision for Reinsurance Contract Liabilities Not Included Elsewhere – Other Amounts Payable on Reinsurance Miscellaneous Liabilities – Reinsurance in Unauthorized Companies (Life Companies) Funds Held Under Coinsurance (Life Companies)

Relevant Statements of Statutory Accounting Principles (SSAPs)

All of the relevant SSAPs related to the reinsurance process, regardless of whether or not the corresponding risks are included within this exam repository, are listed below:

No. 5R Liabilities, Contingencies and Impairments of Assets – Revised No. 25 Affiliates and Other Related Parties No. 61R Life, Deposit-Type and Accident and Health Reinsurance – Revised (Health/Life Companies) No. 62R Property and Casualty Reinsurance – Revised (P&C Companies) No. 63 Underwriting Pools (Health/Life Companies) No. 64 Offsetting and Netting of Assets and Liabilities No. 65 Property and Casualty Contracts (P&C Companies)

© 2017 National Association of Insurance Commissioners 15 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

Oth

er T

han

Fina

ncia

l Rep

ortin

g R

isks

Th

e in

sure

r doe

s not

ac

cura

tely

iden

tify,

ac

cum

ulat

e an

d tra

ck

its a

ggre

gate

loss

ex

posu

res t

hat m

ay

requ

ire re

insu

ranc

e co

vera

ge.

ST

Oth

er

AA

RP

The

insu

rer h

as a

risk

m

anag

emen

t fun

ctio

n in

pl

ace

to id

entif

y, tr

ack

and

mon

itor v

ario

us lo

ss

expo

sure

s (e.

g., c

atas

troph

ic

risk,

mor

talit

y, m

orbi

dity

, ep

idem

ic, e

tc.).

The

insu

rer h

as p

roce

sses

in

plac

e to

ens

ure

that

pol

icy

info

rmat

ion

is c

orre

ctly

ca

ptur

ed in

the

syst

em (S

ee

also

Exa

min

atio

n R

epos

itory

– U

nder

writ

ing)

. (N

ote:

Thi

s fun

ctio

n m

ay b

e ou

tsou

rced

to a

TPA

/MG

A).

The

(re)

insu

rer h

as a

pr

oces

s in

plac

e to

revi

ew

and

accu

mul

ate

loss

ex

posu

re d

ata

repo

rted

by

its c

edin

g in

sure

r/bro

kers

fo

r inc

lusi

on in

trac

king

ag

greg

ate

loss

exp

osur

e (S

ee a

lso

Exam

inat

ion

Rep

osito

ry –

Rei

nsur

ance

A

ssum

ed).

If th

is p

roce

ss is

out

sour

ced

to a

third

-par

ty

adm

inis

trato

r (TP

A) o

r m

anag

ing

gene

ral a

gent

(M

GA

), th

e in

sure

r has

a

proc

ess i

n pl

ace

to e

nsur

e th

at th

e TP

A/M

GA

co

rrec

tly in

puts

dat

a in

to th

e sy

stem

.

Rev

iew

and

test

the

oper

atin

g ef

fect

iven

ess o

f th

e in

sure

r’s p

roce

sses

to

iden

tify,

trac

k an

d m

onito

r re

leva

nt lo

ss e

xpos

ures

.

Test

con

trols

rela

ting

to th

e ac

cura

cy o

f pol

icy

data

up

load

ed (b

y th

e in

sure

r or

a TP

A/M

GA

) to

the

syst

em

(See

als

o Ex

amin

atio

n R

epos

itory

– U

nder

writ

ing)

.

Rev

iew

and

test

the

oper

atin

g ef

fect

iven

ess o

f th

e (r

e)in

sure

r’s p

roce

sses

to

revi

ew a

nd a

ccum

ulat

e lo

ss e

xpos

ure

data

repo

rted

by c

edin

g in

sure

rs/b

roke

rs

(See

als

o Ex

amin

atio

n R

epos

itory

– R

eins

uran

ce

Ass

umed

).

Sele

ct a

sam

ple

of d

irect

ly

unde

rwrit

ten

polic

ies t

o ve

rify

that

the

insu

rer h

as

corr

ectly

reco

rded

loss

ex

posu

re d

ata

asso

ciat

ed

with

rele

vant

pol

icie

s (Se

e al

so E

xam

inat

ion

Rep

osito

ry –

Und

erw

ritin

g).

Ana

lytic

ally

revi

ew th

e lo

ss

expo

sure

dat

a re

porte

d to

th

e co

mpa

ny b

y ce

ding

in

sure

rs/b

roke

rs o

n as

sum

ed

busi

ness

to id

entif

y po

tent

ial i

ncon

sist

enci

es

(See

als

o Ex

amin

atio

n R

epos

itory

– R

eins

uran

ce

Ass

umed

).

If de

emed

nec

essa

ry,

perf

orm

add

ition

al

proc

edur

es to

get

com

fort

with

the

loss

exp

osur

e da

ta

repo

rted

to th

e (r

e)in

sure

r fr

om c

edin

g in

sure

rs/b

roke

rs o

n as

sum

ed

busi

ness

(See

als

o Ex

amin

atio

n R

epos

itory

–

Rei

nsur

ance

Ass

umed

).

The

insu

rer h

as n

ot

esta

blis

hed

and

ST

OP

Oth

er

AA

RP

The

insu

rer h

as a

wel

l-de

fined

rein

sura

nce

stra

tegy

R

evie

w m

eetin

g m

inut

es o

f th

e bo

ard

of d

irect

ors (

or a

R

evie

w th

e in

sure

r’s

rein

sura

nce

leve

ls fo

r

© 2017 National Association of Insurance Commissioners 16 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

mai

ntai

ned

appr

opria

te

rein

sura

nce

leve

ls in

ac

cord

ance

with

the

com

pany

’s c

apita

l le

vel,

loss

exp

osur

es

and

unde

rwrit

ing

risk

prof

ile.

that

is b

ased

on

the

aggr

egat

e lo

ss e

xpos

ures

it

face

s. Th

e st

rate

gy in

dica

tes

the

type

of r

eins

uran

ce (e

.g.,

aggr

egat

e ex

cess

of l

oss,

per

occu

rren

ce, e

tc.)

to b

e m

aint

aine

d by

the

orga

niza

tion

and

is

appr

oved

by

the

boar

d of

di

rect

ors (

or a

com

mitt

ee

ther

eof)

.

The

insu

rer h

as e

stab

lishe

d an

d do

cum

ente

d ex

posu

re

limits

and

a ri

sk a

ppet

ite

that

hav

e be

en re

view

ed a

nd

appr

oved

by

seni

or

man

agem

ent.

The

insu

rer r

eins

ures

all

expo

sure

s tha

t exc

eed

the

expo

sure

lim

its a

nd

mai

ntai

ns c

over

age

in

acco

rdan

ce w

ith it

s ris

k ap

petit

e.

The

insu

rer h

as d

evel

oped

fo

rmal

doc

umen

tatio

n of

its

rein

sura

nce

stru

ctur

e an

d ha

s est

ablis

hed

an e

ffec

tive,

on

goin

g di

alog

ue a

mon

g th

e un

derw

ritin

g, c

laim

s and

re

insu

ranc

e ar

eas.

The

insu

rer h

as a

pro

cess

in

plac

e to

eva

luat

e th

e ef

fect

iven

ess o

f its

re

insu

ranc

e co

vera

ge.

com

mitt

ee th

ereo

f) o

r oth

er

evid

ence

of b

oard

in

volv

emen

t in

the

appr

oval

of

the

insu

rer’

s rei

nsur

ance

po

licy.

Rev

iew

how

ag

greg

ated

/mod

eled

loss

ex

posu

re d

ata

is u

tiliz

ed b

y th

e co

mpa

ny to

reac

h re

insu

ranc

e de

cisi

ons.

Rev

iew

doc

umen

tatio

n of

re

insu

ranc

e co

vera

ge li

mits

an

d ev

iden

ce o

f sen

ior

man

agem

ent

revi

ew/a

ppro

val.

Rev

iew

a su

mm

ary

of a

ll re

insu

ranc

e co

ntra

cts t

o en

sure

that

the

cove

rage

s m

atch

the

insu

rer’

s ex

posu

re li

mits

.

Rev

iew

ev i

denc

e of

in

tera

ctio

n be

twee

n th

e un

derw

ritin

g, c

laim

s and

re

insu

ranc

e ar

eas.

Rev

iew

the

insu

rer’

s an

alys

is o

f res

ults

gro

ss a

nd

net o

f rei

nsur

ance

.

appr

opria

tene

ss. C

onsi

der

the

resu

lts o

f dat

a ag

greg

atio

n/ m

odel

s to

assi

st in

this

ass

essm

ent.

Rev

iew

t he

insu

rer’

s re

insu

ranc

e co

vera

ge a

s co

mpa

red

to th

e ris

k be

ing

reta

ined

by

the

insu

rer t

o en

sure

ade

quat

e, b

ut n

ot

exce

ssiv

e, re

insu

ranc

e le

vels

.

Cal

cula

te th

e hi

stor

ical

ag

greg

ate

prof

itabi

lity

of

rein

sura

nce.

Con

side

r app

lyin

g a

rang

e of

scen

ario

s to

a se

lect

ion

of si

gnifi

cant

re

insu

ranc

e co

ntra

cts t

o te

st

the

over

all

perf

orm

ance

/pro

spec

tive

prof

itabi

lity

of th

e co

ntra

ct

and

to a

sses

s whe

ther

the

cedi

ng c

omm

issi

on is

gr

eate

r tha

n th

e co

st to

writ

e th

e bu

sine

ss.

Rev

iew

rein

sura

nce

cont

ract

s to

dete

rmin

e if

risk-

limiti

ng p

rovi

sion

s (e

.g.,

slid

ing

com

mis

sion

s, lo

ss c

orrid

ors,

etc.

) im

pact

th

e ef

fect

iven

ess o

f the

in

sure

r’s r

eins

uran

ce

stra

tegy

.

© 2017 National Association of Insurance Commissioners 17 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

The

insu

rer p

erfo

rms a

co

st/b

enef

it an

alys

is p

rior t

o en

terin

g in

to re

insu

ranc

e ag

reem

ents

.

Rev

iew

the

insu

rer’

s co

st/b

enef

it an

alys

is.

The

insu

rer’

s ca

tast

roph

ic

rein

sura

nce

prot

ectio

ns a

re

inad

equa

te.

ST

OP

Oth

er

AA

RP

The

insu

rer u

ses o

ne o

f the

in

dust

ry’s

cat

astro

phic

m

odel

ing

softw

are

tool

s (R

MS,

AIR

, EQ

ECA

T, e

tc.)

to d

eter

min

e th

e pr

obab

le

max

imum

loss

(PM

L) b

y zo

ne.

The

proc

ess i

nclu

des

actu

aria

l inv

olve

men

t with

th

e ce

ded

rein

sura

nce

depa

rtmen

t to

insu

re th

e ce

ded

depa

rtmen

t pur

chas

es

the

prop

er a

mou

nt o

f re

insu

ranc

e.

The

insu

rer a

djus

ts it

s re

tent

ions

or u

ses

rein

sura

nce

alte

rnat

ives

, su

ch a

s cat

bon

ds, t

o en

sure

fu

ll pl

acem

ent a

t eac

h ca

tast

roph

ic la

yer.

The

insu

rer h

as p

rote

cted

its

elf a

gain

st m

ultip

le

occu

rren

ces i

n th

e sa

me

perio

d w

ith c

ontra

ctua

l re

inst

atem

ent o

f cov

erag

e.

Rev

iew

the

adeq

uacy

of t

he

proc

ess a

nd to

ols u

tiliz

ed to

de

term

ine

the

insu

rer’

s PM

L am

ount

(s).

Det

erm

ine

whe

ther

the

insu

red’

s rei

nsur

ance

st

rate

gy in

clud

es th

e in

volv

emen

t of t

he a

ctua

rial

and

cede

d re

insu

ranc

e de

partm

ents

in th

e pu

rcha

sing

of c

atas

troph

ic

rein

sura

nce.

Rev

iew

the

cove

rage

s in

plac

e fo

r eac

h la

yer o

f re

insu

ranc

e fo

r app

ropr

iate

su

perv

isor

y re

view

.

Det

erm

ine

whe

ther

the

insu

rer’

s rei

nsur

ance

st

rate

gy re

quire

s pre

miu

m

rein

stat

emen

t for

the

cat

prog

ram

.

Rev

iew

the

reas

onab

lene

ss

of th

e ca

tast

roph

ic

rein

sura

nce

cove

rage

in

plac

e at

the

insu

rer b

y be

nchm

arki

ng a

gain

st

com

petit

ors a

nd/o

r co

mpa

ring

agai

nst i

ndus

try

stan

dard

s. C

onsi

der i

nvol

ving

an

exam

ac

tuar

y or

rein

sura

nce

spec

ialis

t in

asse

ssin

g th

e ad

equa

cy o

f the

insu

rer’

s ca

tast

roph

ic re

insu

ranc

e co

vera

ge.

The

insu

rer i

s ove

r-ex

pose

d to

cre

dit a

nd

liqui

dity

risk

s in

its

use

of re

insu

ranc

e co

unte

rpar

ties.

OP

ST

CR

LQ

Oth

er

AA

RP

The

insu

rer h

as p

olic

ies i

n pl

ace

requ

iring

util

izat

ion

of

mul

tiple

rein

sure

rs to

re

duce

con

cent

ratio

n w

ith

any

one

entit

y.

Test

the

oper

atin

g ef

fect

iven

ess o

f the

in

sure

r’s c

ontro

ls to

trac

k co

mpl

ianc

e w

ith th

e co

ncen

tratio

n po

licy.

Bas

ed o

n a

revi

ew o

f si

gnifi

cant

con

tract

s, de

term

ine

whe

ther

the

insu

rer i

s pro

perly

di

vers

ified

.

© 2017 National Association of Insurance Commissioners 18 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

The

insu

rer h

as d

evel

oped

a

form

al p

roce

ss to

app

rove

re

insu

ranc

e co

unte

rpar

ties.

The

insu

rer h

as a

pro

cess

in

plac

e to

pre

appr

ove

and

set

max

imum

lim

its to

be

cede

d to

rein

sure

rs th

at a

re

mon

itore

d an

d re

vise

d, a

s ne

cess

ary.

The

insu

rer c

ontin

ually

m

onito

rs th

e fin

anci

al

solv

ency

of i

ts re

insu

rers

th

roug

hout

the

dura

tion

of

the

rein

sura

nce

cont

ract

s.

Col

late

ral i

s hel

d in

as

soci

atio

n w

ith si

gnifi

cant

tre

atie

s to

enco

urag

e pr

ompt

se

ttlem

ent a

nd fu

lfillm

ent o

f ob

ligat

ions

.

Obt

ain

evid

ence

of t

he

com

pany

’s p

roce

ss to

ap

prov

e re

insu

ranc

e co

unte

rpar

ties.

Obt

ain

evid

ence

of t

he

prea

ppro

val p

roce

ss a

nd

docu

men

tatio

n of

max

imum

re

insu

ranc

e lim

its.

Obt

ain

evid

ence

of t

he

insu

rer’

s ong

oing

revi

ew o

f its

rein

sure

rs.

Obt

ain

evid

ence

of t

he

insu

rer’

s pro

cess

to

cons

ider

/requ

ire c

olla

tera

l to

be

held

for s

igni

fican

t tre

atie

s.

Perf

orm

pro

cedu

res t

o ev

alua

te th

e qu

ality

of

sign

ifica

nt re

insu

rers

ut

ilize

d by

the

insu

rer;

for

exam

ple:

•

Rev

iew

age

ncy

ratin

gs•

Rev

iew

fina

ncia

l res

ults

Con

tact

dom

estic

regu

lato

r re

gard

ing

any

conc

erns

For s

elec

t rei

nsur

ers,

verif

y th

at th

e ba

lanc

e cu

rren

tly

cede

d is

with

in th

e m

axim

um li

mits

set b

y th

e in

sure

r.

Rei

nsur

ance

co

unte

rpar

ties a

re n

ot

likel

y to

fulfi

ll th

eir

oblig

atio

ns.

CR

LQ

O

ther

A

AR

P R

RC

Th

e in

sure

r has

dev

elop

ed a

fo

rmal

pro

cess

to a

ppro

ve

rein

sura

nce

coun

terp

artie

s.

New

cou

nter

parti

es a

re

subj

ect t

o re

view

and

ap

prov

al in

acc

orda

nce

with

st

anda

rds.

The

insu

rer c

ontin

ually

m

onito

rs th

e fin

anci

al

solv

ency

of i

ts re

insu

rers

th

roug

hout

the

dura

tion

of

the

rein

sura

nce

cont

ract

s.

Obt

ain

evid

ence

of t

he

com

pany

’s p

roce

ss to

ap

prov

e re

insu

ranc

e co

unte

rpar

ties.

Sele

ct a

sam

ple

of n

ew

coun

terp

artie

s to

dete

rmin

e w

heth

er c

ontro

ls a

re

oper

atin

g ef

fect

ivel

y.

Obt

ain

evid

ence

of t

he

insu

rer’

s ong

oing

revi

ew o

f its

rein

sure

rs.

Perf

orm

pro

cedu

res t

o ev

alua

te th

e qu

ality

of

sign

ifica

nt re

insu

rers

ut

ilize

d by

the

insu

rer;

for

exam

ple:

•

Rev

iew

age

ncy

ratin

gs•

Rev

iew

fina

ncia

l res

ults

•C

onta

ct d

omes

ticre

gula

tor r

egar

ding

any

conc

erns

© 2017 National Association of Insurance Commissioners 19 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

Col

late

ral i

s hel

d in

as

soci

atio

n w

ith si

gnifi

cant

tre

atie

s to

enco

urag

e pr

ompt

se

ttlem

ent a

nd fu

lfillm

ent o

f ob

ligat

ions

.

Obt

ain

evid

ence

of t

he

insu

rer’

s pro

cess

to

cons

ider

/requ

ire c

olla

tera

l to

be

held

for s

igni

fican

t tre

atie

s. Sm

alle

r, le

ss c

ompl

ex

or n

ew in

sure

rs a

re

unab

le to

neg

otia

te

equi

tabl

e re

insu

ranc

e co

ntra

ct te

rms f

rom

la

rger

or m

ore

expe

rienc

ed

rein

sure

rs.

OP

ST

LQ

Oth

er

AA

RP

The

insu

rer e

ngag

es

licen

sed

rein

sura

nce

inte

rmed

iarie

s to

nego

tiate

fa

ir an

d ac

cura

te

rein

sura

nce

cont

ract

s on

its

beha

lf.

Rev

iew

the

wor

k pe

rfor

med

by

the

insu

rer t

o de

term

ine

whe

ther

the

inte

rmed

iary

is

licen

sed.

Rev

iew

the

cred

entia

ls,

back

grou

nd a

nd e

xper

ienc

e of

thos

e ne

gotia

ting

the

cont

ract

s to

ensu

re th

at th

ey

are

licen

sed

to re

pres

ent t

he

insu

rer i

n co

ntra

ct

nego

tiatio

ns.

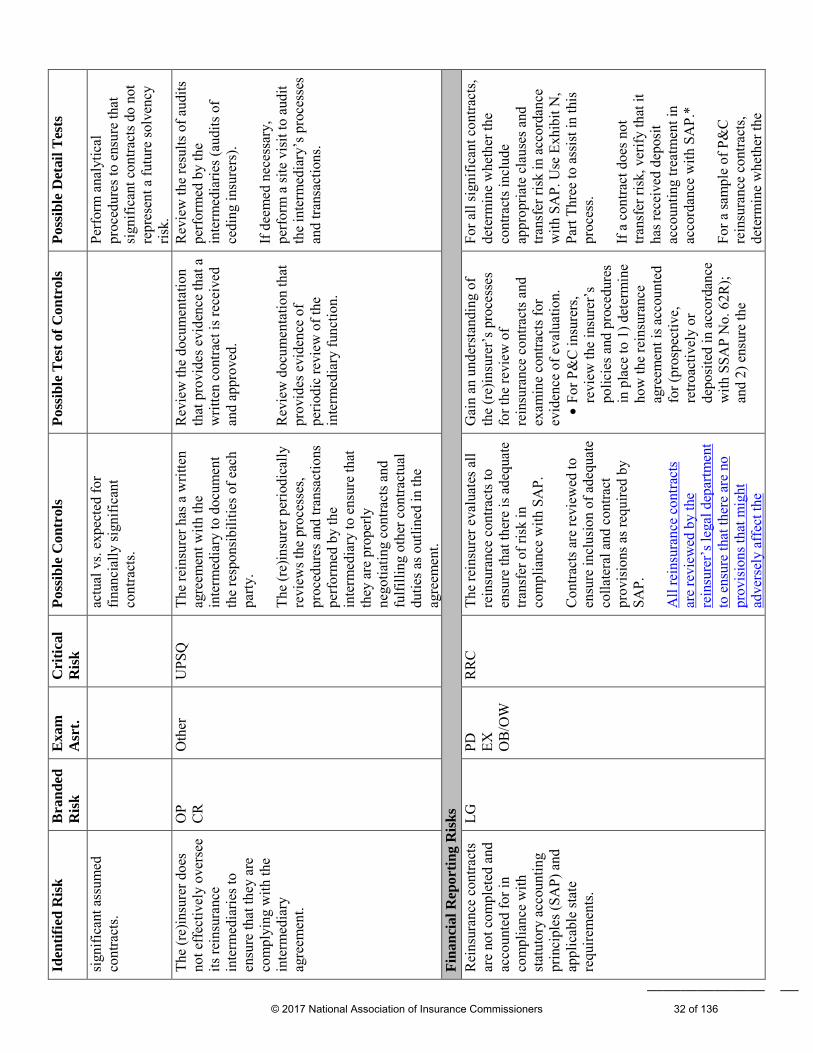

Fina

ncia

l Rep

ortin

g R

isks

R

eins

uran

ce c

ontra

cts

with

aff

iliat

es h

ave

not b

een

filed

in

acco

rdan

ce w

ith

appl

icab

le st

ate

stat

utes

and

do

not

incl

ude

equi

tabl

e co

ntra

ct p

rovi

sion

s.

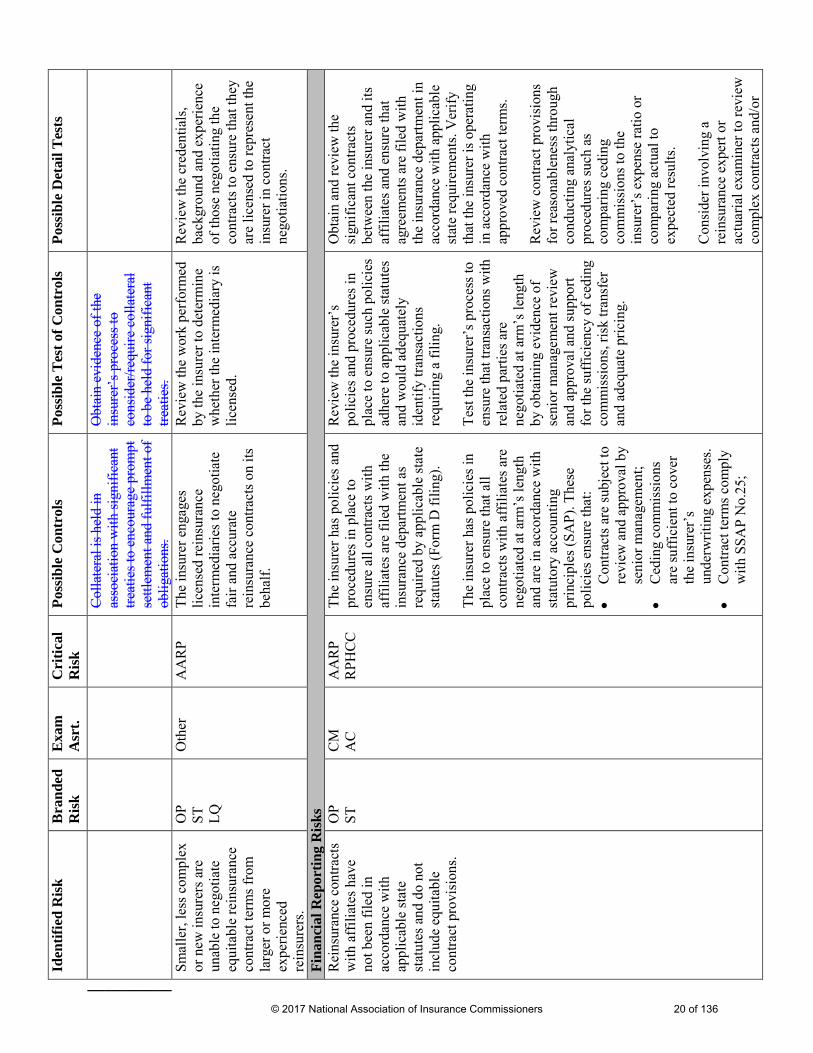

OP

ST

CM

A

C

AA

RP

RPH

CC

Th

e in

sure

r has

pol

icie

s and

pr

oced

ures

in p

lace

to

ensu

re a

ll co

ntra

cts w

ith

affil

iate

s are

file

d w

ith th

e in

sura

nce

depa

rtmen

t as

requ

ired

by a

pplic

able

stat

e st

atut

es (F

orm

D fi

ling)

.

The

insu

rer h

as p

olic

ies i

n pl

ace

to e

nsur

e th

at a

ll co

ntra

cts w

ith a

ffili

ates

are

ne

gotia

ted

at a

rm’s

leng

th

and

are

in a

ccor

danc

e w

ith

stat

utor

y ac

coun

ting

prin

cipl

es (S

AP)

. The

se

polic

ies e

nsur

e th

at:

•C

ontra

cts a

re su

bjec

t to

revi

ew a

nd a

ppro

val b

yse

nior

man

agem

ent;

•C

edin

g co

mm

issi

ons

are

suff

icie

nt to

cov

erth

e in

sure

r’s

unde

rwrit

ing

expe

nses

.•

Con

tract

term

s com

ply

with

SSA

P N

o.25

;

Rev

iew

the

insu

rer’

s po

licie

s and

pro

cedu

res i

n pl

ace

to e

nsur

e su

ch p

olic

ies

adhe

re to

app

licab

le st

atut

es

and

wou

ld a

dequ

atel

y id

entif

y tra

nsac

tions

re

quiri

ng a

filin

g.

Test

the

insu

rer’

s pro

cess

to

ensu

re th

at tr

ansa

ctio

ns w

ith

rela

ted

parti

es a

re

nego

tiate

d at

arm

’s le

ngth

by

obt

aini

ng e

vide

nce

of

seni

or m

anag

emen

t rev

iew

an

d ap

prov

al a

nd su

ppor

t fo

r the

suff

icie

ncy

of c

edin

g co

mm

issi

ons,

risk

trans

fer

and

adeq

uate

pric

ing.

Obt

ain

and

revi

ew th

e si

gnifi

cant

con

tract

s be

twee

n th

e in

sure

r and

its

affil

iate

s and

ens

ure

that

ag

reem

ents

are

file

d w

ith

the

insu

ranc

e de

partm

ent i

n ac

cord

ance

with

app

licab

le

stat

e re

quire

men

ts. V

erify

th

at th

e in

sure

r is o

pera

ting

in a

ccor

danc

e w

ith

appr

oved

con

tract

term

s.

Rev

iew

co n

tract

pro

visi

ons

for r

easo

nabl

enes

s thr

ough

co

nduc

ting

anal

ytic

al

proc

edur

es su

ch a

s co

mpa

ring

cedi

ng

com

mis

sion

s to

the

insu

rer’

s exp

ense

ratio

or

com

parin

g ac

tual

to

expe

cted

resu

lts.

Con

side

r inv

olvi

ng a

re

insu

ranc

e ex

pert

or

actu

aria

l exa

min

er to

revi

ew

com

plex

con

tract

s and

/or

© 2017 National Association of Insurance Commissioners 20 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

•R

eins

uran

ce is

not

bein

g us

ed to

tran

sfer

capi

tal t

o af

filia

tes;

and

•A

ctua

rial r

evie

w is

perf

orm

ed p

rior t

oco

ntra

ct e

xecu

tion

toen

sure

that

pol

icie

s are

enfo

rced

.

The

insu

rer h

as p

olic

ies i

n pl

ace

to e

nsur

e m

ultip

le

cede

nt c

ontra

cts h

ave

fair

and

equi

tabl

e al

loca

tion

term

s and

are

subj

ect t

o re

view

and

app

rova

l by

all

impa

cted

div

isio

ns (e

.g.,

acco

untin

g, a

ctua

rial,

etc.

).

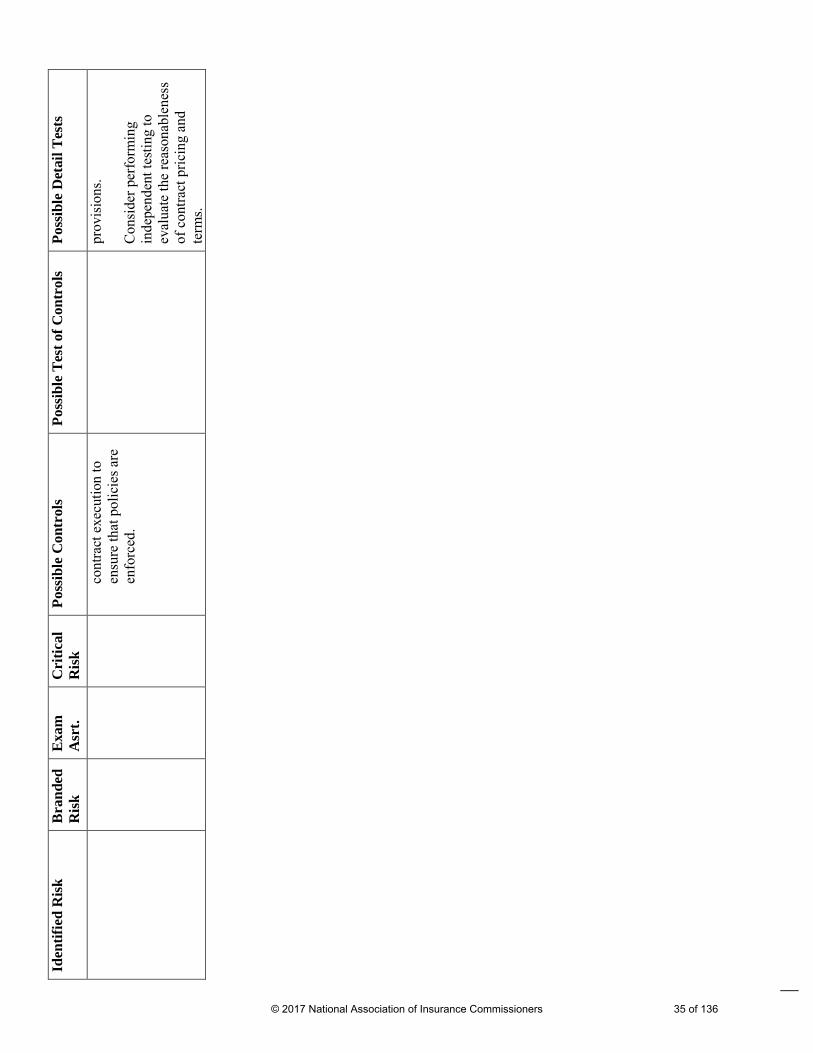

Eval

uate

pro

cedu

res i

n pl

ace

to e

nsur

e m

ultip

le

cede

nt a

rran

gem

ents

hav

e al

loca

tion

term

s in

plac

e (in

clud

ing

cost

allo

catio

n ag

reem

ents

whe

n ap

prop

riate

), an

d th

at su

ch

term

s are

fair

and

equi

tabl

e an

d ap

plic

able

to u

nder

lyin

g re

insu

ranc

e ag

reem

ent.

thos

e w

ith q

uest

iona

ble

prov

isio

ns.

Con

side

r per

form

ing

inde

pend

ent t

estin

g to

ev

alua

te th

e re

ason

able

ness

of

con

tract

pric

ing

and

term

s.

Rev

iew

sign

ifica

nt m

ultip

le

cede

nt a

gree

men

ts to

ens

ure

allo

catio

n te

rms a

nd

agre

emen

ts a

re c

lear

ly

docu

men

ted

and

equi

tabl

e.

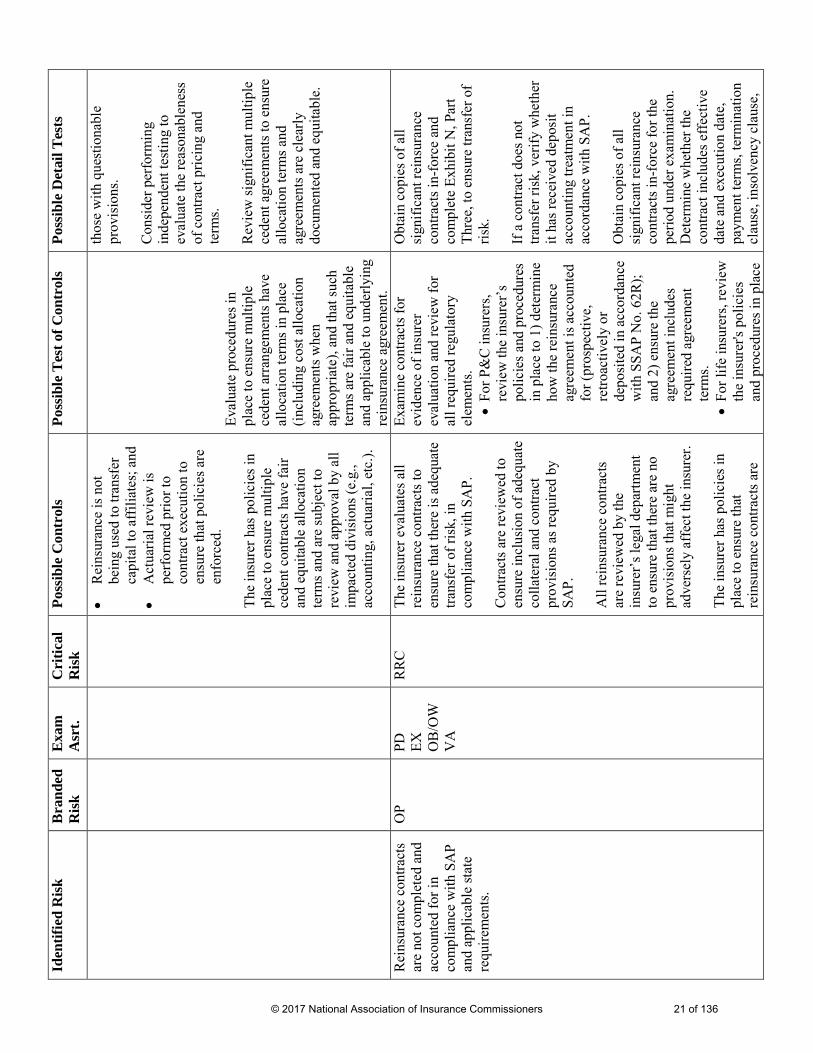

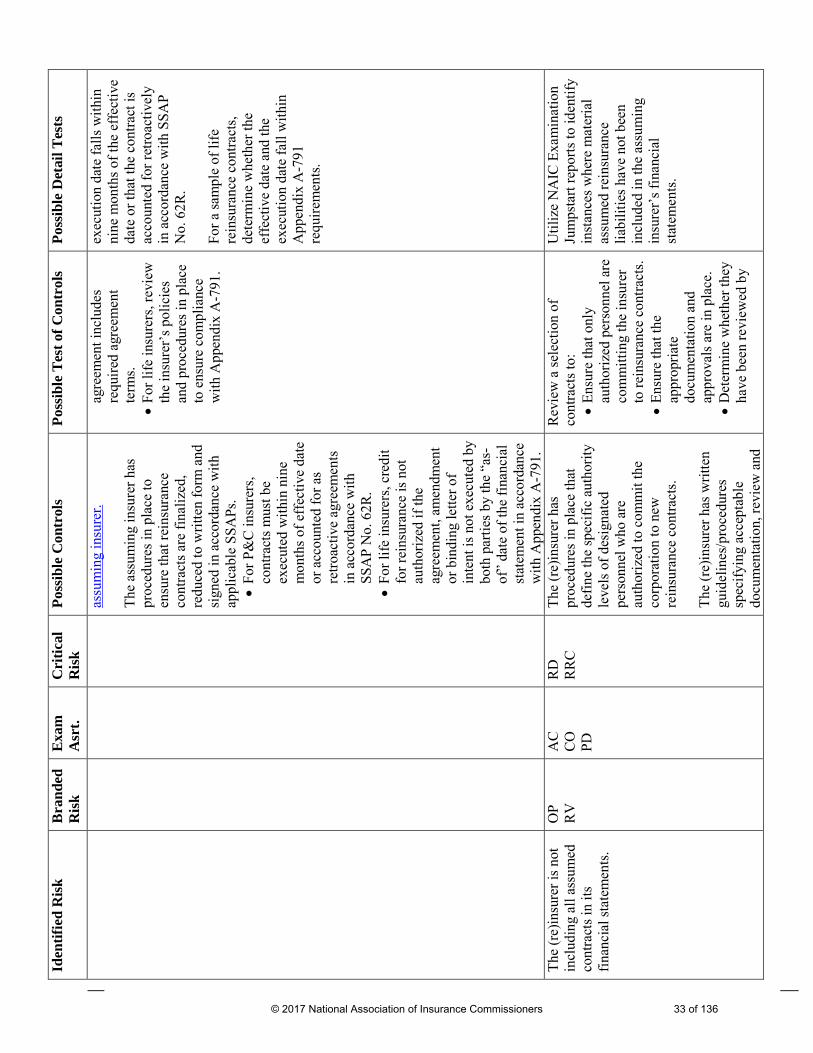

Rei

nsur

ance

con

tract

s ar

e no

t com

plet

ed a

nd

acco

unte

d fo

r in

com

plia

nce

with

SA

P an

d ap

plic

able

stat

e re

quire

men

ts.

OP

PD

EX

OB

/OW

V

A

RR

C

The

insu

rer e

valu

ates

all

rein

sura

nce

cont

ract

s to

ensu

re th

at th

ere

is a

dequ

ate

trans

fer o

f ris

k, in

co

mpl

ianc

e w

ith S

AP.

Con

tract

s are

revi

ewed

to

ensu

re in

clus

ion

of a

dequ

ate

colla

tera

l and

con

tract

pr

ovis

ions

as r

equi

red

by

SAP.

All

rein

sura

nce

cont

ract

s ar

e re

view

ed b

y th

e in

sure

r’s l

egal

dep

artm

ent

to e

nsur

e th

at th

ere

are

no

prov

isio

ns th

at m

ight

ad

vers

ely

affe

ct th

e in

sure

r.

The

insu

rer h

as p

olic

ies i

n pl

ace

to e

nsur

e th

at

rein

sura

nce

cont

ract

s are

Exam

ine

cont

ract

s for

ev

iden

ce o

f ins

urer

ev

alua

tion

and

revi

ew fo

r al

l req

uire

d re

gula

tory

el

emen

ts.

•Fo

r P&

C in

sure

rs,

revi

ew th

e in

sure

r’s

polic

ies a

nd p

roce

dure

sin

pla

ce to

1) d

eter

min

eho

w th

e re

insu

ranc

eag

reem

ent i

s acc

ount

edfo

r (pr

ospe

ctiv

e,re

troac

tivel

y or

depo

site

d in

acc

orda

nce

with

SSA

P N

o. 6

2R);

and

2) e

nsur

e th

eag

reem

ent i

nclu

des

requ

ired

agre

emen

tte

rms.

•Fo

r life

insu

rers

, rev

iew

the

insu

rer's

pol

icie

san

d pr

oced

ures

in p

lace

Obt

ain

copi

es o

f all

sign

ifica

nt re

insu

ranc

e co

ntra

cts i

n-fo

rce

and

com

plet

e Ex

hibi

t N, P

art

Thre

e, to

ens

ure

trans

fer o

f ris

k.

If a

cont

ract

doe

s not

tra

nsfe

r ris

k, v

erify

whe

ther

it

has r

ecei

ved

depo

sit

acco

untin

g tre

atm

ent i

n ac

cord

ance

with

SA

P.

Obt

ain

copi

es o

f all

sign

ifica

nt re

insu

ranc

e co

ntra

cts i

n-fo

rce

for t

he

perio

d un

der e

xam

inat

ion.

D

eter

min

e w

heth

er th

e co

ntra

ct in

clud

es e

ffec

tive

date

and

exe

cutio

n da

te,

paym

ent t

erm

s, te

rmin

atio

n cl

ause

, ins

olve

ncy

clau

se,

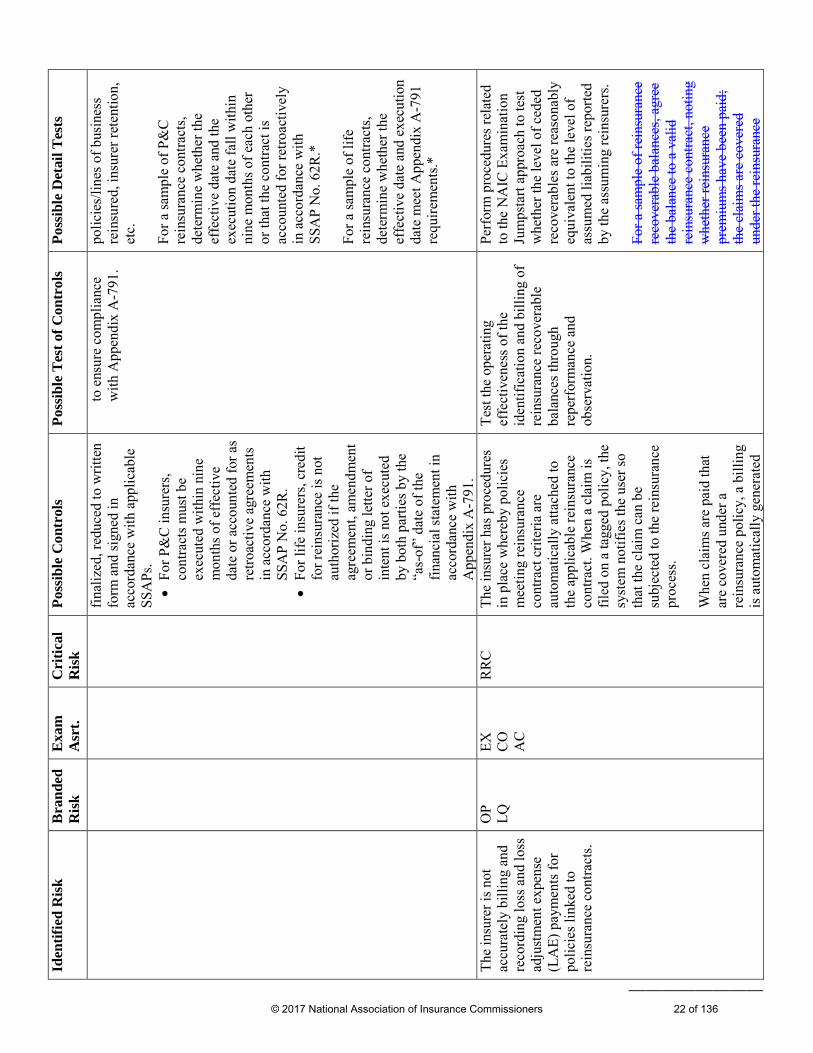

© 2017 National Association of Insurance Commissioners 21 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

final

ized

, red

uced

to w

ritte

n fo

rm a

nd si

gned

in

acco

rdan

ce w

ith a

pplic

able

SS

APs

. •

For P

&C

insu

rers

,co

ntra

cts m

ust b

eex

ecut

ed w

ithin

nin

em

onth

s of e

ffec

tive

date

or a

ccou

nted

for a

sre

troac

tive

agre

emen

tsin

acc

orda

nce

with

SSA

P N

o. 6

2R.

•Fo

r life

insu

rers

, cre

dit

for r

eins

uran

ce is

not

auth

oriz

ed if

the

agre

emen

t, am

endm

ent

or b

indi

ng le

tter o

fin

tent

is n

ot e

xecu

ted

by b

oth

parti

es b

y th

e“a

s-of

” da

te o

f the

finan

cial

stat

emen

t in

acco

rdan

ce w

ithA

ppen

dix

A-7

91.

to e

nsur

e co

mpl

ianc

e w

ith A

ppen

dix

A-7

91.

polic

ies/

lines

of b

usin

ess

rein

sure

d, in

sure

r ret

entio

n,

etc.

For a

sam

ple

of P

&C

re

insu

ranc

e co

ntra

cts,

dete

rmin

e w

heth

er th

e ef

fect

ive

date

and

the

exec

utio

n da

te fa

ll w

ithin

ni

ne m

onth

s of e

ach

othe

r or

that

the

cont

ract

is

acco

unte

d fo

r ret

roac

tivel

y in

acc

orda

nce

with

SS

AP

No.

62R

.*

For a

sam

p le

of li

fe

rein

sura

nce

cont

ract

s, de

term

ine

whe

ther

the

effe

ctiv

e da

te a

nd e

xecu

tion

date

mee

t App

endi

x A

-791

re

quire

men

ts.*

The

insu

rer i

s not

ac

cura

tely

bill

ing

and

reco

rdin

g lo

ss a

nd lo

ss

adju

stm

ent e

xpen

se

(LA

E) p

aym

ents

for

polic

ies l

inke

d to

re

insu

ranc

e co

ntra

cts.

OP

LQ

EX

CO

A

C

RR

C

The

insu

rer h

as p

roce

dure

s in

pla

ce w

here

by p

olic

ies

mee

ting

rein

sura

nce

cont

ract

crit

eria

are

au

tom

atic

ally

atta

ched

to

the

appl

icab

le re

insu

ranc

e co

ntra

ct. W

hen

a cl

aim

is

filed

on

a ta

gged

pol

icy,

the

syst

em n

otifi

es th

e us

er so

th

at th

e cl

aim

can

be

subj

ecte

d to

the

rein

sura

nce

proc

ess.

Whe

n cl

aim

s are

pai

d th

at

are

cove

red

unde

r a

rein

sura

nce

polic

y, a

bill

ing

is a

utom

atic

ally

gen

erat

ed

Test

the

oper

atin

g ef

fect

iven

ess o

f the

id

entif

icat

ion

and

billi

ng o

f re

insu

ranc

e re

cove

rabl

e ba

lanc

es th

roug

h re

perf

orm

ance

and

ob

serv

atio

n.

Perf

orm

pro

cedu

res r

elat

ed

to th

e N

AIC

Exa

min

atio

n Ju

mps

tart

appr

oach

to te

st

whe

ther

the

leve

l of c

eded

re

cove

rabl

es a

re re

ason

ably

eq

uiva

lent

to th

e le

vel o

f as

sum

ed li

abili

ties r

epor

ted

by th

e as

sum

ing

rein

sure

rs.

For a

sam

ple

of re

insu

ranc

e re

cove

rabl

e ba

lanc

es, a

gree

th

e ba

lanc

e to

a v

alid

re

insu

ranc

e co

ntra

ct, n

otin

g w

heth

er re

insu

ranc

e pr

emiu

ms h

ave

been

pai

d;

the

clai

ms a

re c

over

ed

unde

r the

rein

sura

nce

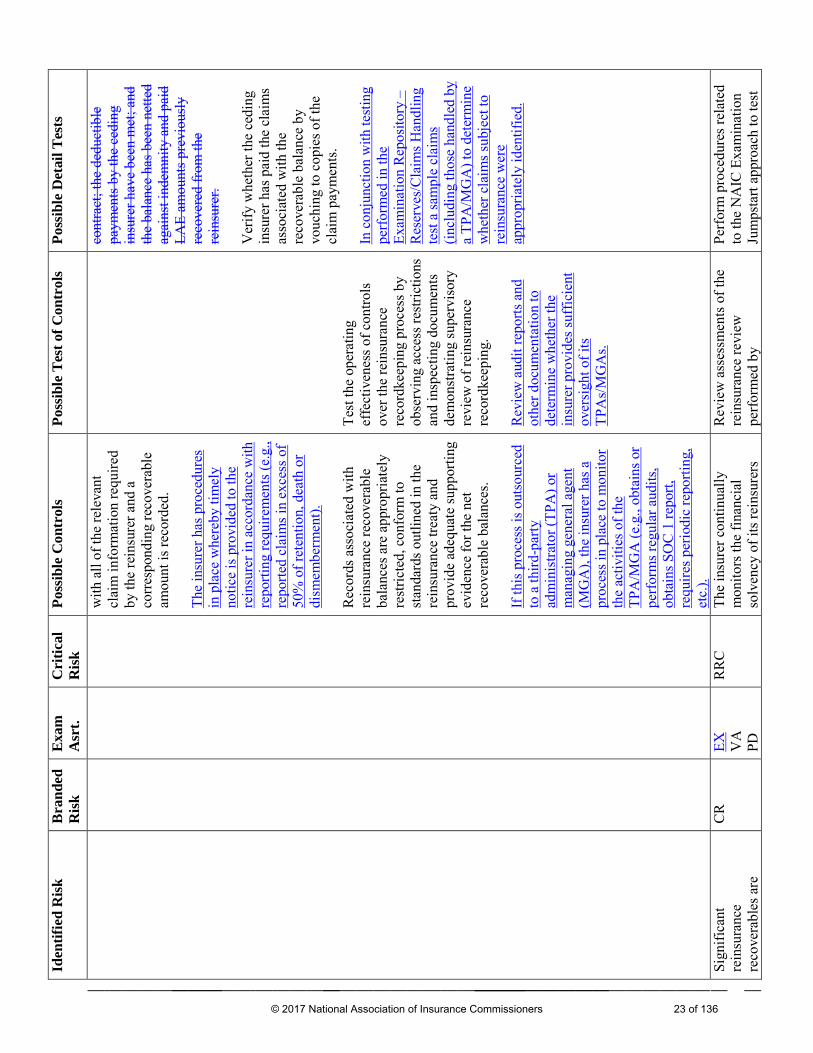

© 2017 National Association of Insurance Commissioners 22 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

with

all

of th

e re

leva

nt

clai

m in

form

atio

n re

quire

d by

the

rein

sure

r and

a

corr

espo

ndin

g re

cove

rabl

e am

ount

is re

cord

ed.

The

insu

rer h

as p

roce

dure

s in

pla

ce w

here

by ti

mel

y no

tice

is p

rovi

ded

to th

e re

insu

rer i

n ac

cord

ance

with

re

porti

ng re

quire

men

ts (e

.g.,

repo

rted

clai

ms i

n ex

cess

of

50%

of r

eten

tion,

dea

th o

r di

smem

berm

ent).

Rec

ords

ass

ocia

ted

with

re

insu

ranc

e re

cove

rabl

e ba

lanc

es a

re a

ppro

pria

tely

re

stric

ted,

con

form

to

stan

dard

s out

lined

in th

e re

insu

ranc

e tre

aty

and

prov

ide

adeq

uate

supp

ortin

g ev

iden

ce fo

r the

net

re

cove

rabl

e ba

lanc

es.

If th

is p

roce

ss is

out

sour

ced

to a

third

-par

ty

adm

inis

trato

r (TP

A) o

r m

anag

ing

gene

ral a

gent

(M

GA

), th

e in

sure

r has

a

proc

ess i

n pl

ace

to m

onito

r th

e ac

tiviti

es o

f the

TP

A/M

GA

(e.g

., ob

tain

s or

perf

orm

s reg

ular

aud

its,

obta

ins S

OC

1 re

port,

re

quire

s per

iodi

c re

porti

ng,

etc.

).

Test

the

oper

atin

g ef

fect

iven

ess o

f con

trols

ov

er th

e re

insu

ranc

e re

cord

keep

ing

proc

ess b

y ob

serv

ing

acce

ss re

stric

tions

an

d in

spec

ting

docu

men

ts

dem

onst

ratin

g su

perv

isor

y re

view

of r

eins

uran

ce

reco

rdke

epin

g.

Rev

iew

aud

it re

ports

and

ot

her d

ocum

enta

tion

to

dete

rmin

e w

heth

er th

e in

sure

r pro

vide

s suf

ficie

nt

over

sigh

t of i

ts

TPA

s/M

GA

s.

cont

ract

; the

ded

uctib

le

paym

ents

by

the

cedi

ng

insu

rer h

ave

been

met

; and

th

e ba

lanc

e ha

s bee

n ne

tted

agai

nst i

ndem

nity

and

pai

d LA

E am

ount

s pre

viou

sly

reco

vere

d fr

om th

e re

insu

rer.

Ver

ify w

heth

er th

e ce

ding

in

sure

r has

pai

d th

e cl

aim

s as

soci

ated

with

the

reco

vera

ble

bala

nce

by

vouc

hing

to c

opie

s of t

he

clai

m p

aym

ents

.

In c

onju

nctio

n w

ith te

stin

g pe

rfor

med

in th

e Ex

amin

atio

n R

epos

itory

–

Res

erve

s/C

laim

s Han

dlin

g te

st a

sam

ple

clai

ms

(incl

udin

g th

ose

hand

led

by

a TP

A/M

GA

) to

dete

rmin

e w

heth

er c

laim

s sub

ject

to

rein

sura

nce

wer

e ap

prop

riate

ly id

entif

ied.

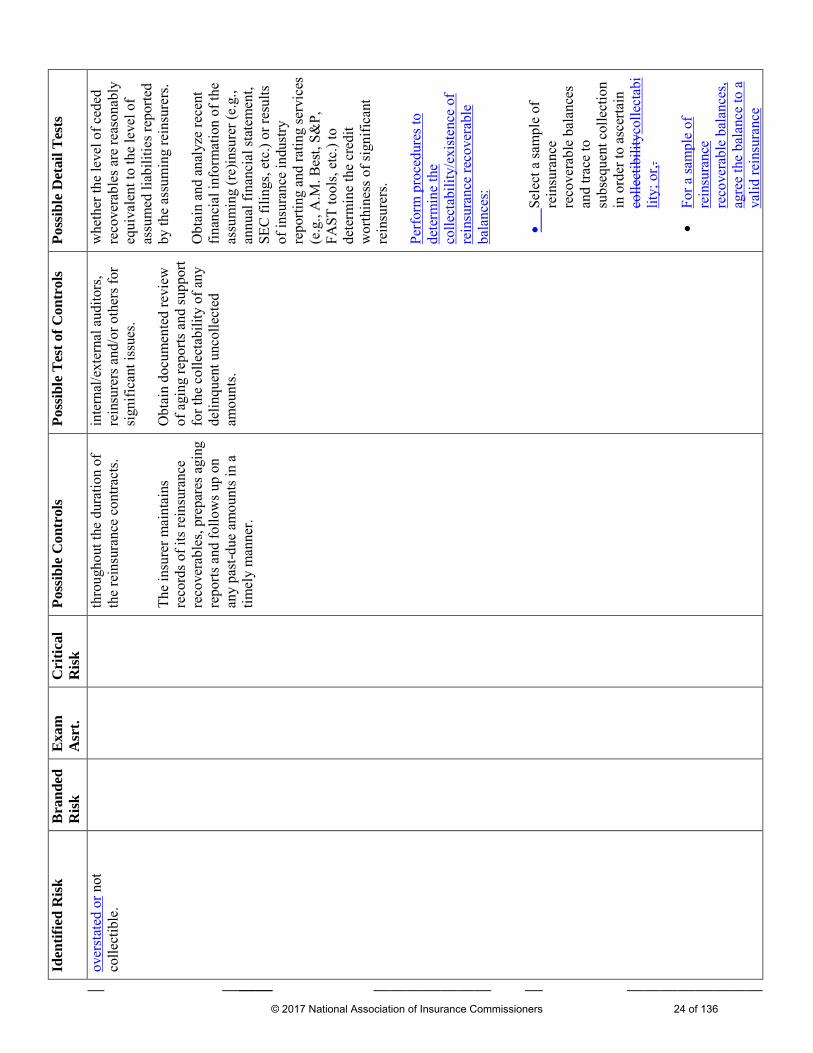

Sign

ifica

nt

rein

sura

nce

reco

vera

bles

are

CR

EX

V

A

PD

RR

C

The

insu

rer c

ontin

ually

m

onito

rs th

e fin

anci

al

solv

ency

of i

ts re

insu

rers

Rev

iew

ass

essm

ents

of t

he

rein

sura

nce

revi

ew

perf

orm

ed b

y

Perf

orm

pro

cedu

res r

elat

ed

to th

e N

AIC

Exa

min

atio

n Ju

mps

tart

appr

oach

to te

st

© 2017 National Association of Insurance Commissioners 23 of 136

Iden

tifie

d R

isk

Bra

nded

R

isk

Exa

m

Asr

t. C

ritic

al

Ris

k Po

ssib

le C

ontr

ols

Poss

ible

Tes

t of C

ontr

ols

Poss

ible

Det

ail T

ests

over

stat

ed o

r not

co

llect

ible

. th

roug

hout

the

dura

tion

of

the