Embed Size (px)

DESCRIPTION

Financial Fundamentals. AM 570 Overview of Fund Accounting, Revenue Sources and Use Restrictions. Welcome. Janet A. Parker, Associate Vice President – Financial Affairs - PowerPoint PPT Presentation

Citation preview

Financial Fundamentals

AM 570 Overview of Fund Accounting, Revenue Sources and

Use Restrictions

Welcome

Janet A. Parker, Associate Vice President – Financial AffairsOversight for – Controller’s Office: Accounting,

Payroll, Disbursements & Travel, Grants & Contracts Financial

Services

Financial Services & Capital Assets Budget Planning & Development Management Reporting & DEFINE

Welcome

Janet A. Parker, Associate Vice President – Financial AffairsHigher Education

Experience – 3 Yrs Colorado State University 10 Yrs University of Alaska,

Anchorage 1 Yr University of So California,

Information Sciences Institute 9 Yrs Cal State Univ, Long Beach

4 Yrs UTSA

Course Objectives• Fund Accounting Principles• Revenue Sources• Fund Use Restrictions• Chart of Accounts• Reporting Expenses• How Higher Education is Funded• UTSA Budgeting

Fund Accounting Principles

• Why fund accounting?– Universities have unique obligations for

accounting and financial reporting according to the sources of funds received and their subsequent net uses than just reporting net income to investors.

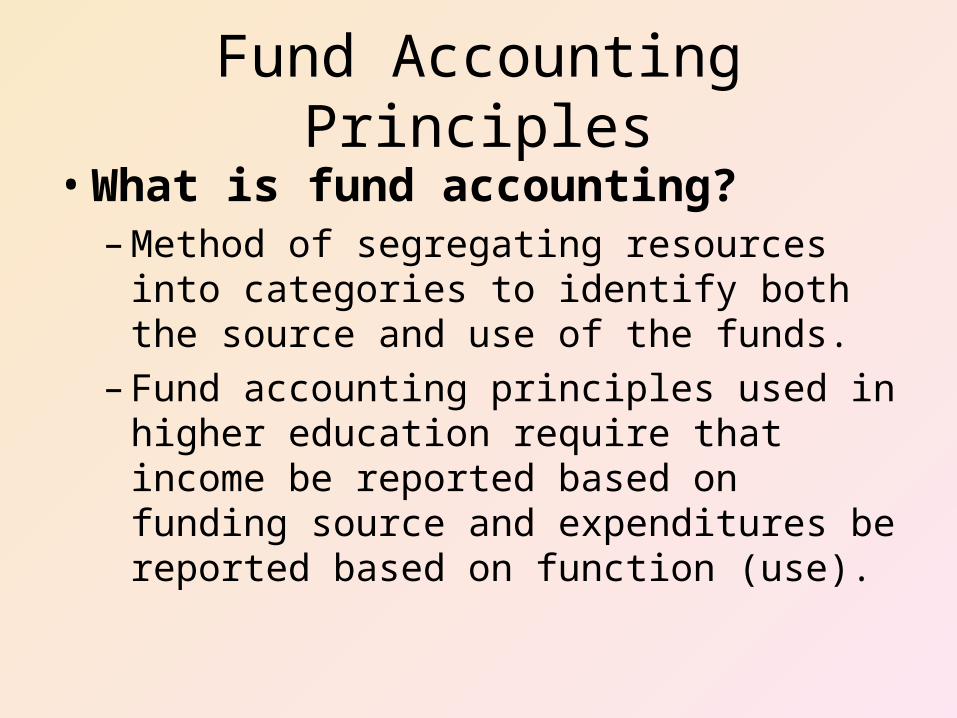

Fund Accounting Principles

• What is fund accounting?–Method of segregating resources into

categories to identify both the source and use of the funds.

– Fund accounting principles used in higher education require that income be reported based on funding source and expenditures be reported based on function (use).

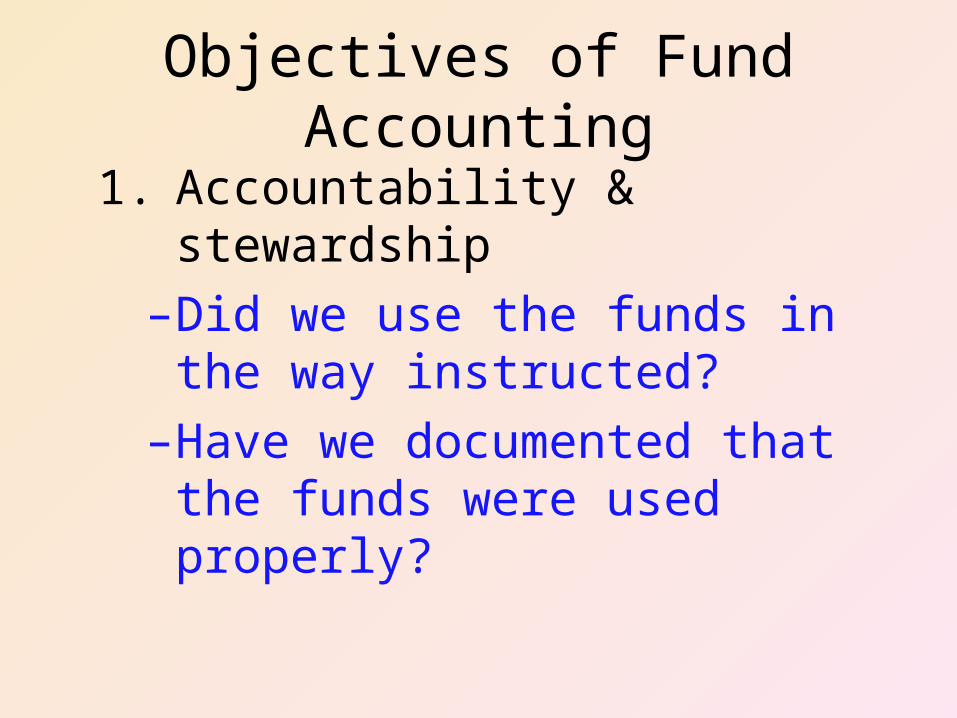

Objectives of Fund Accounting

1. Accountability & stewardship–Did we use the funds in the way

instructed?–Have we documented that the funds

were used properly?

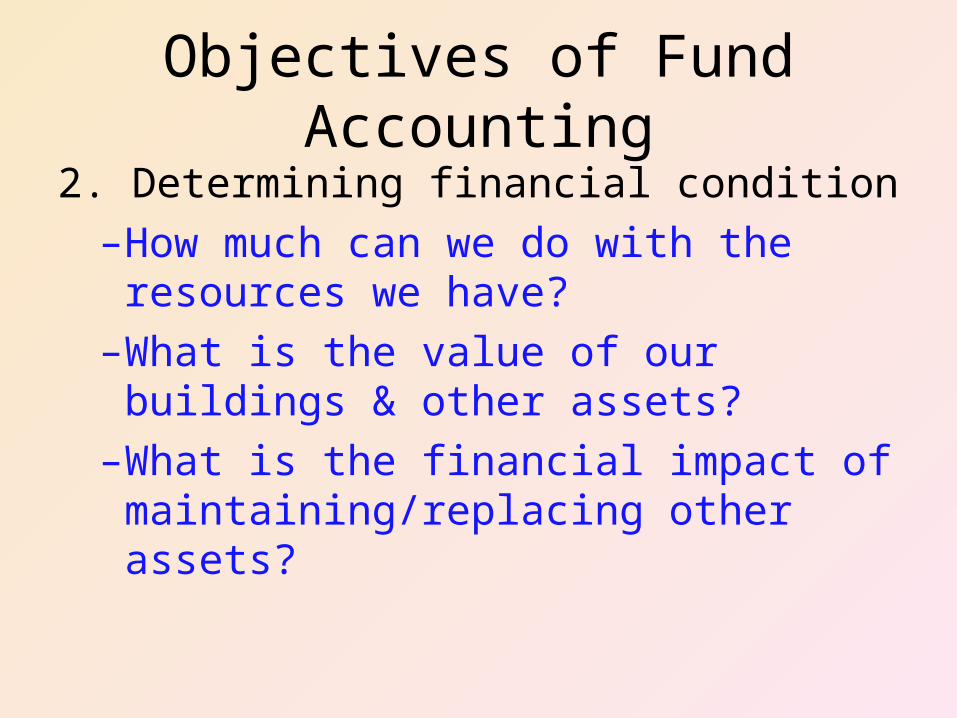

Objectives of Fund Accounting

2. Determining financial condition–How much can we do with the

resources we have?–What is the value of our buildings &

other assets?–What is the financial impact of

maintaining/replacing other assets?

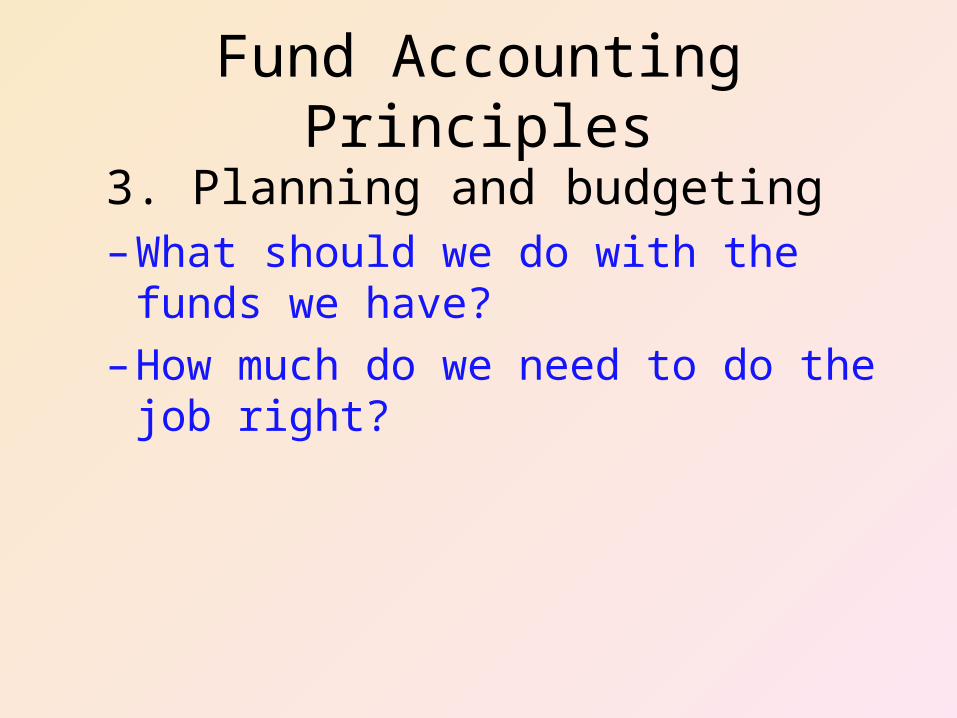

Fund Accounting Principles

3. Planning and budgeting–What should we do with the funds we

have?–How much do we need to do the job right?

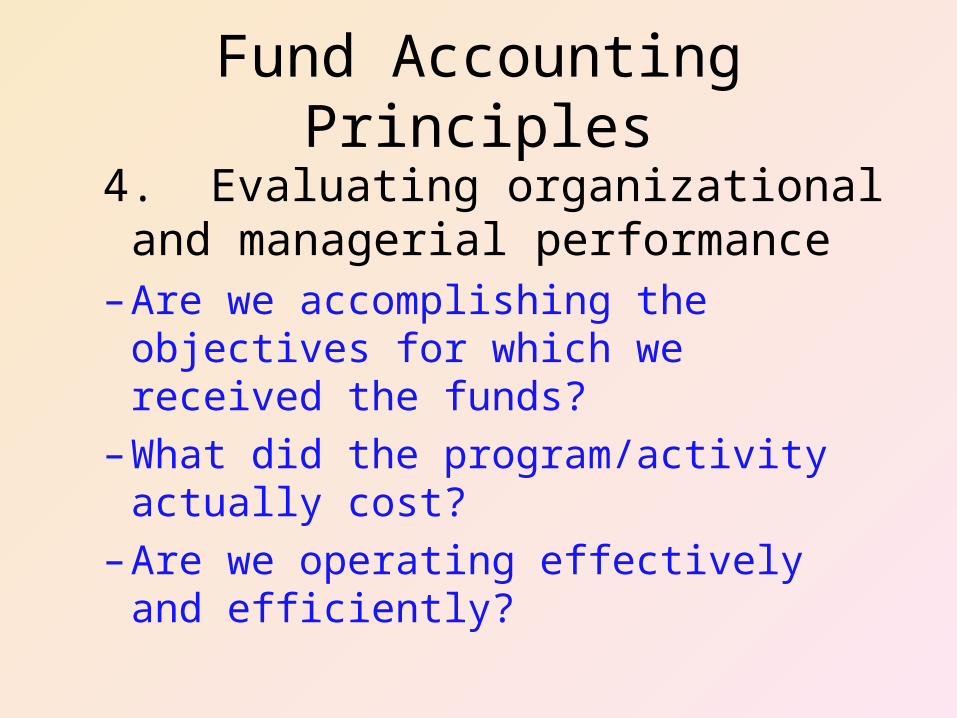

Fund Accounting Principles

4. Evaluating organizational and managerial performance–Are we accomplishing the objectives for

which we received the funds?–What did the program/activity actually

cost?–Are we operating effectively and efficiently?

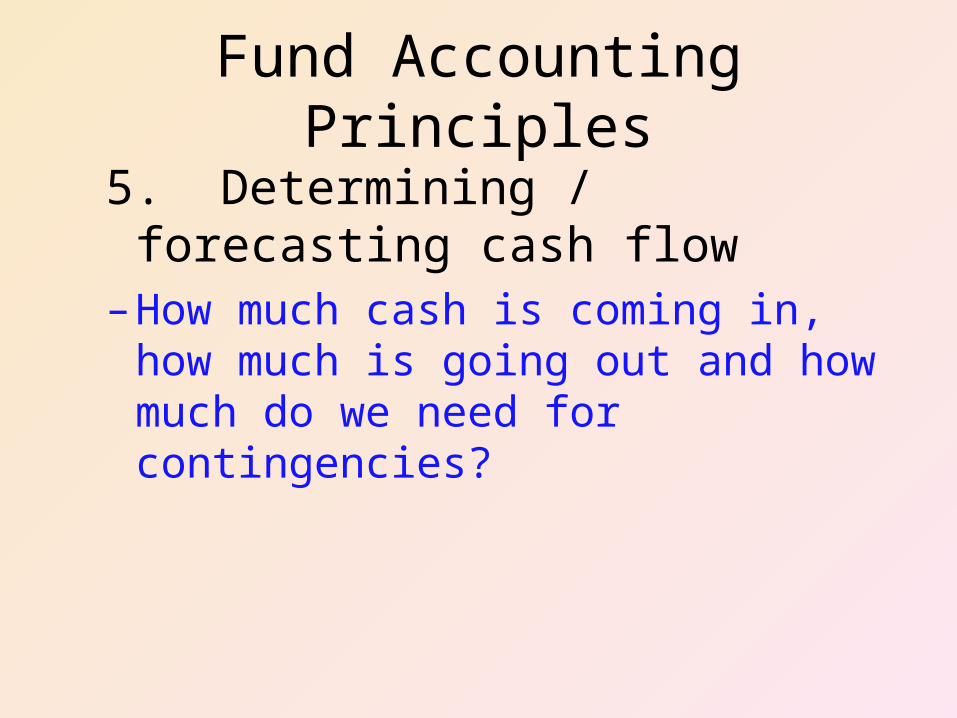

Fund Accounting Principles

5. Determining / forecasting cash flow–How much cash is coming in, how much is

going out and how much do we need for contingencies?

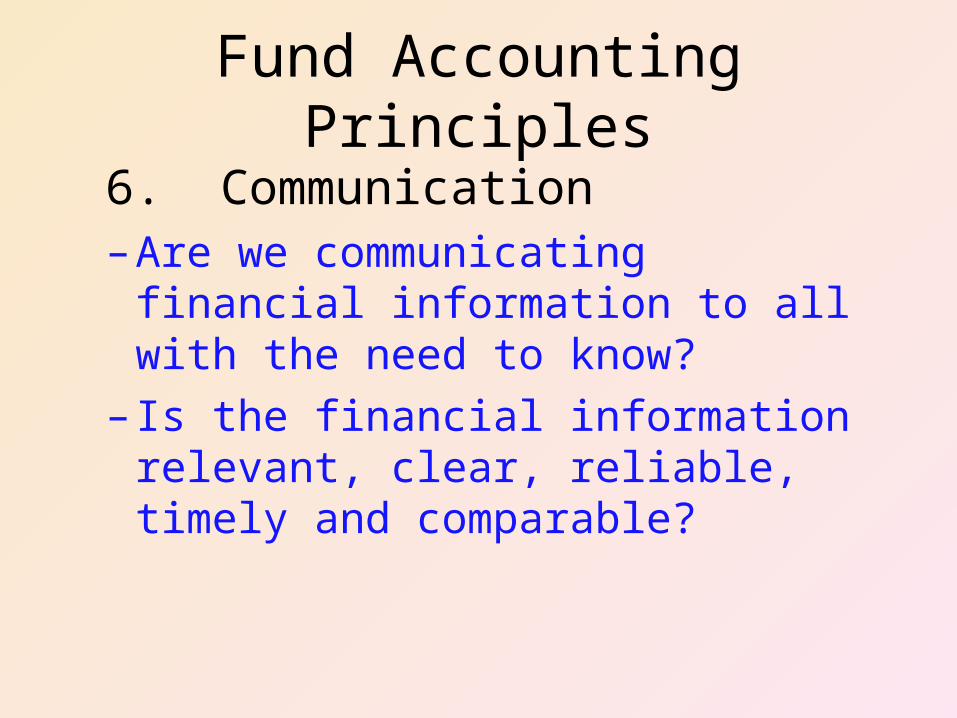

Fund Accounting Principles

6. Communication–Are we communicating financial

information to all with the need to know?– Is the financial information relevant, clear,

reliable, timely and comparable?

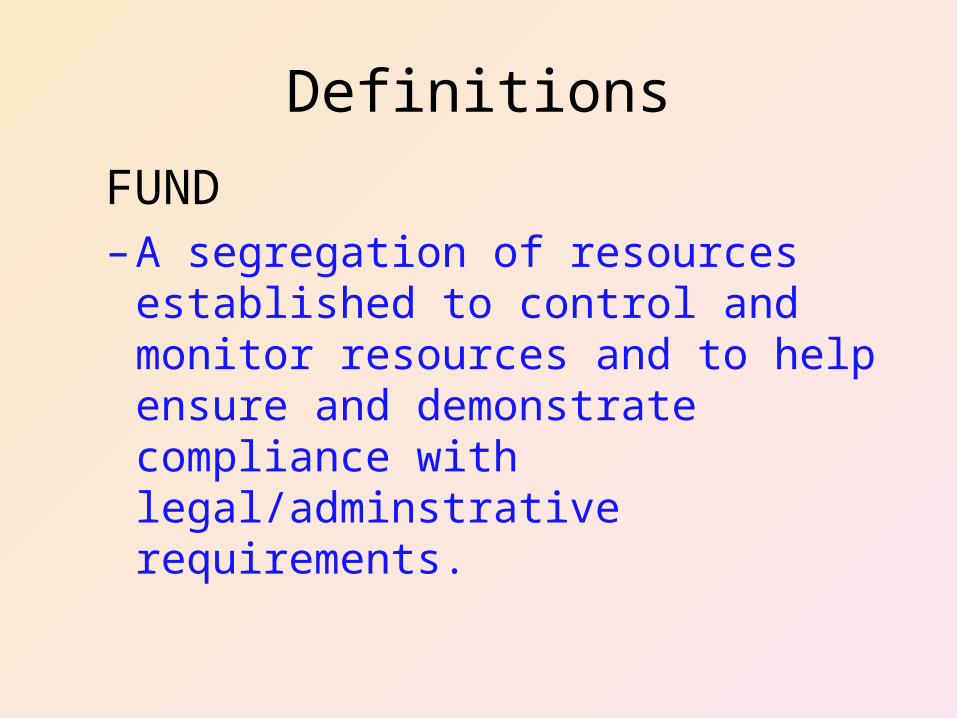

Definitions

FUND–A segregation of resources established to

control and monitor resources and to help ensure and demonstrate compliance with legal/adminstrative requirements.

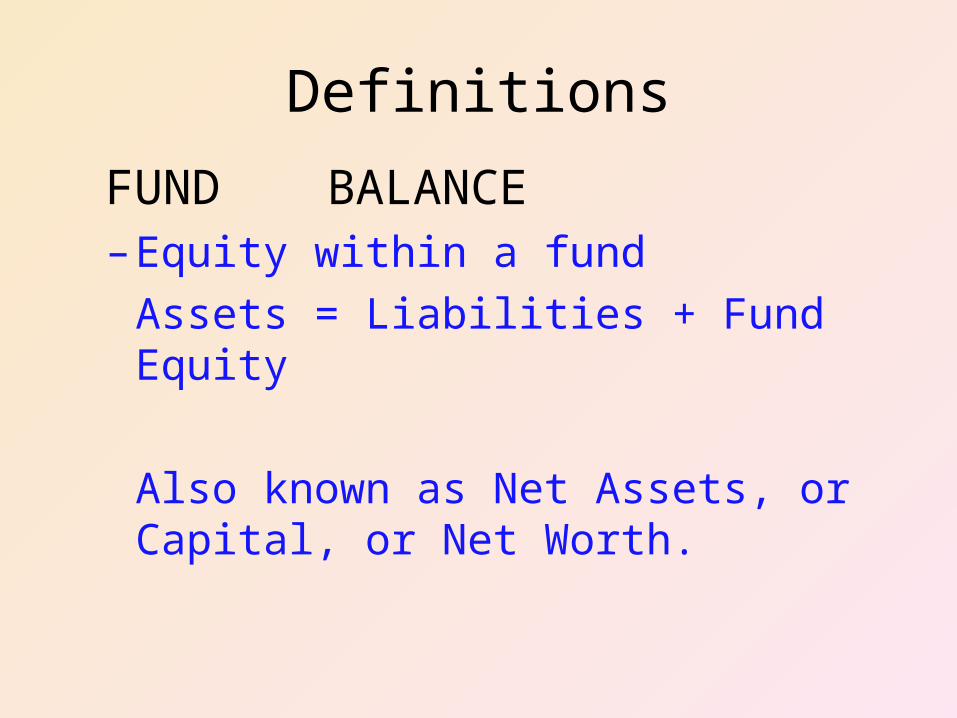

Definitions

FUND BALANCE– Equity within a fund

Assets = Liabilities + Fund Equity

Also known as Net Assets, or Capital, or Net Worth.

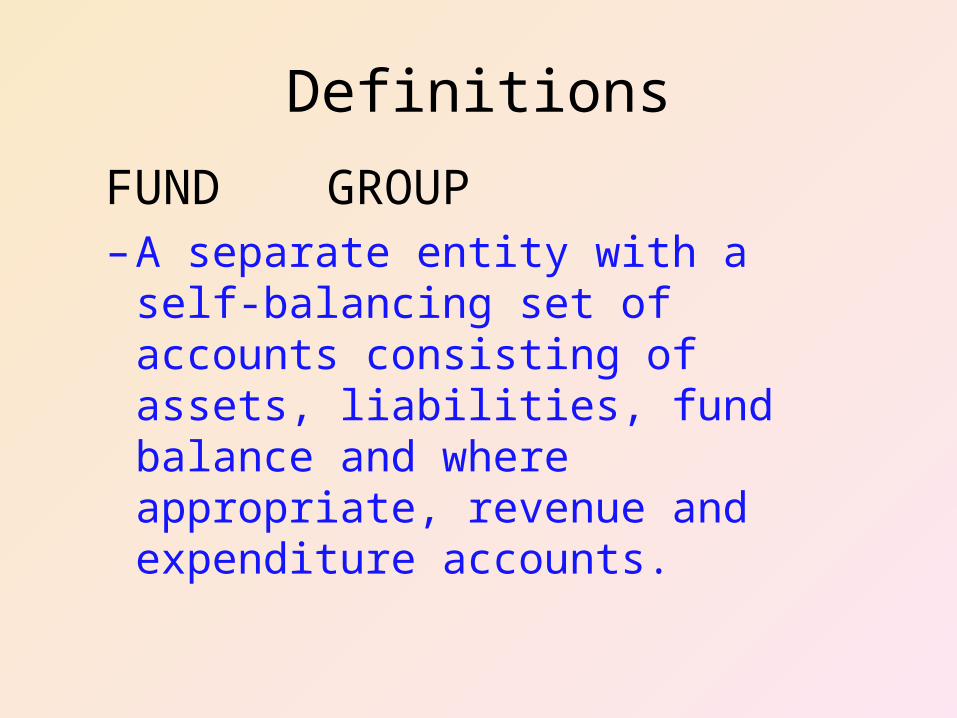

Definitions

FUND GROUP–A separate entity with a self-balancing set

of accounts consisting of assets, liabilities, fund balance and where appropriate, revenue and expenditure accounts.

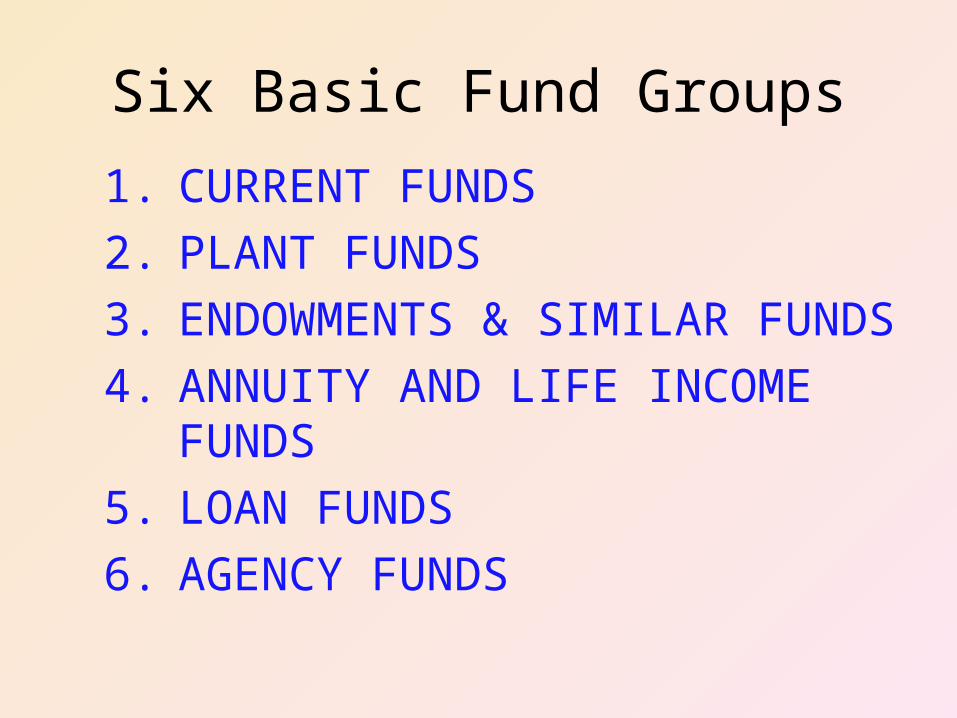

Six Basic Fund Groups

1. CURRENT FUNDS2. PLANT FUNDS3. ENDOWMENTS & SIMILAR FUNDS4. ANNUITY AND LIFE INCOME FUNDS5. LOAN FUNDS6. AGENCY FUNDS

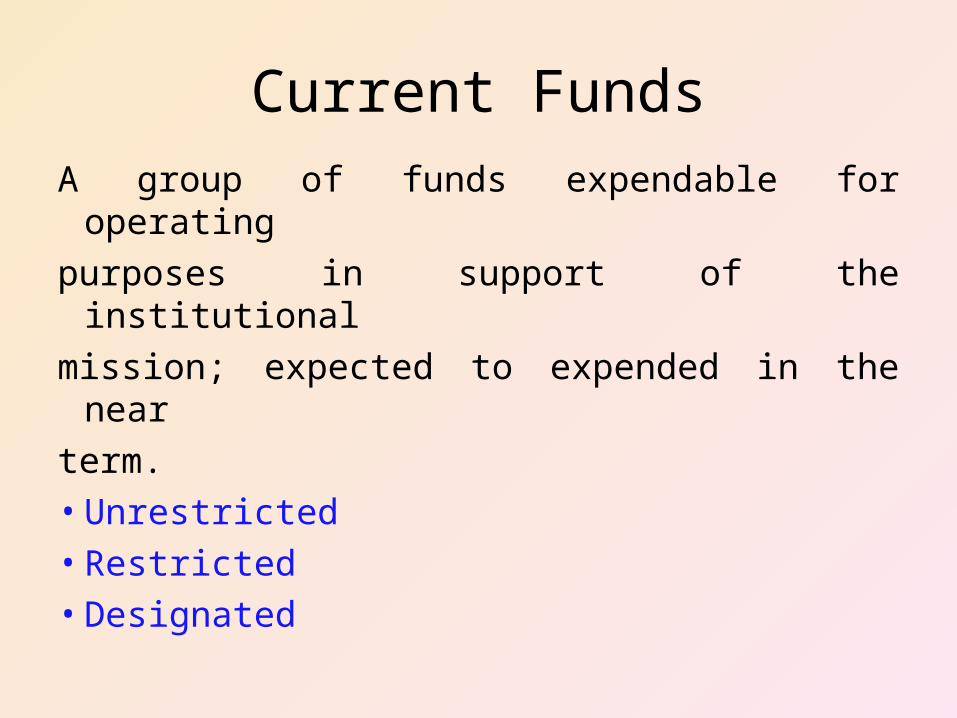

Current Funds

A group of funds expendable for operating purposes in support of the institutionalmission; expected to expended in the near term.• Unrestricted• Restricted• Designated

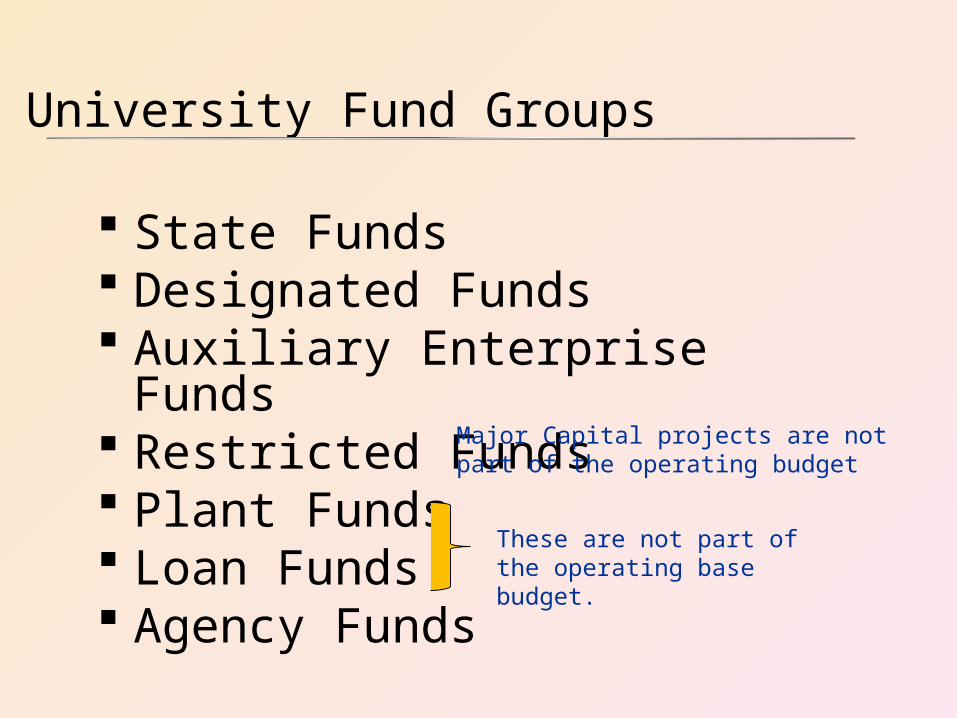

University Fund Groups

State Funds Designated Funds Auxiliary Enterprise Funds Restricted Funds Plant Funds Loan Funds Agency Funds

These are not part of the operating base budget.

Major Capital projects are not part of the operating budget

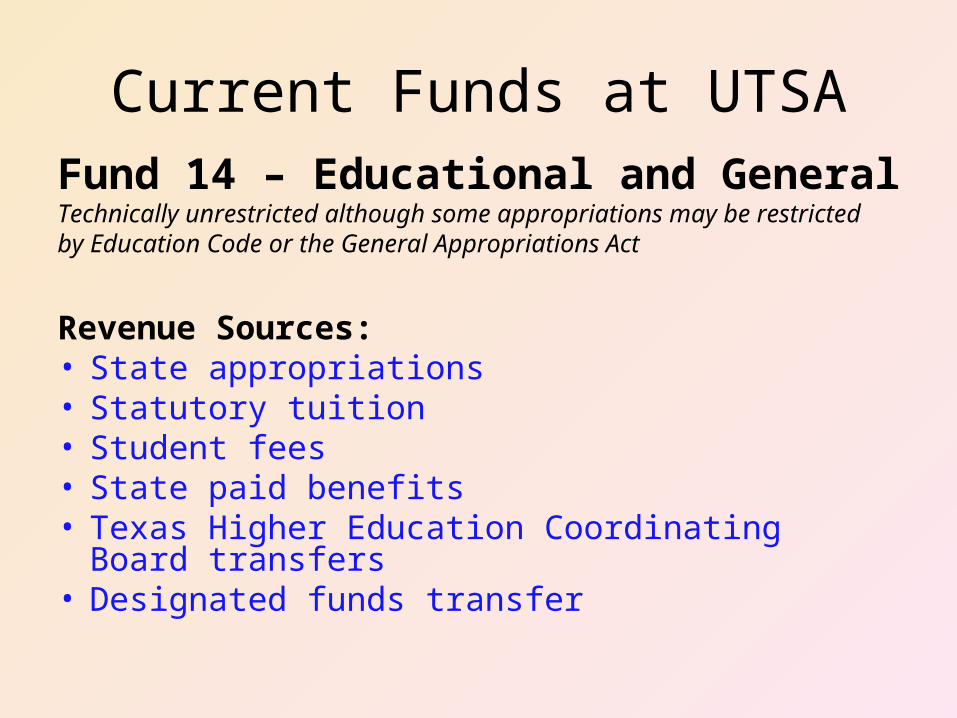

Current Funds at UTSAFund 14 – Educational and General Technically unrestricted although some appropriations may be restricted by Education Code or the General Appropriations Act

Revenue Sources:• State appropriations• Statutory tuition• Student fees• State paid benefits• Texas Higher Education Coordinating Board transfers• Designated funds transfer

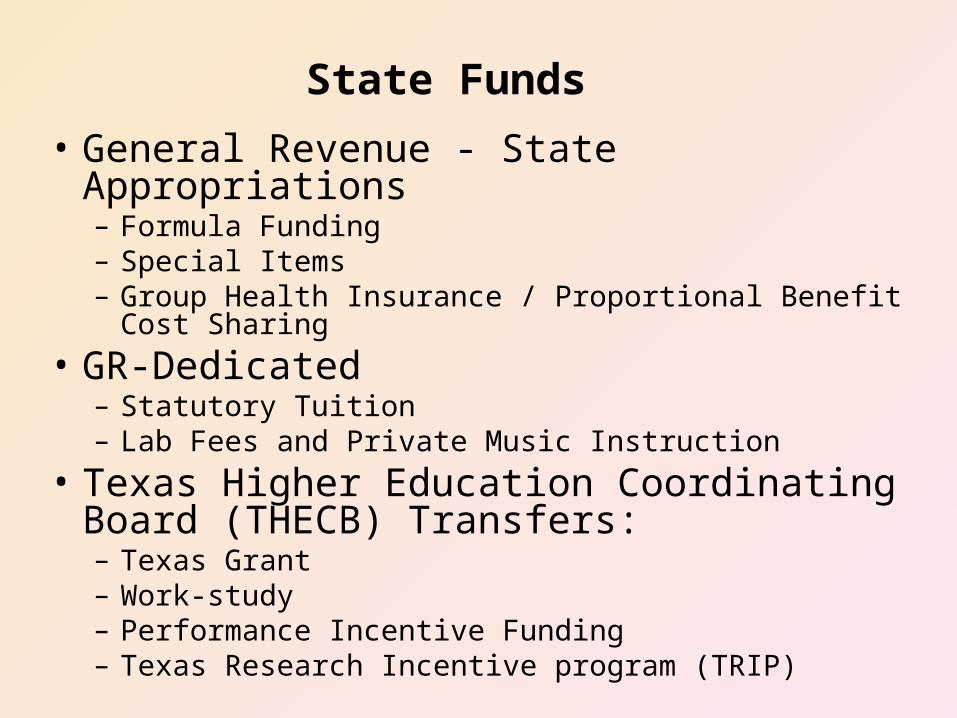

State Funds

• General Revenue - State Appropriations– Formula Funding– Special Items– Group Health Insurance / Proportional Benefit Cost Sharing

• GR-Dedicated– Statutory Tuition– Lab Fees and Private Music Instruction

• Texas Higher Education Coordinating Board (THECB) Transfers: – Texas Grant– Work-study – Performance Incentive Funding– Texas Research Incentive program (TRIP)

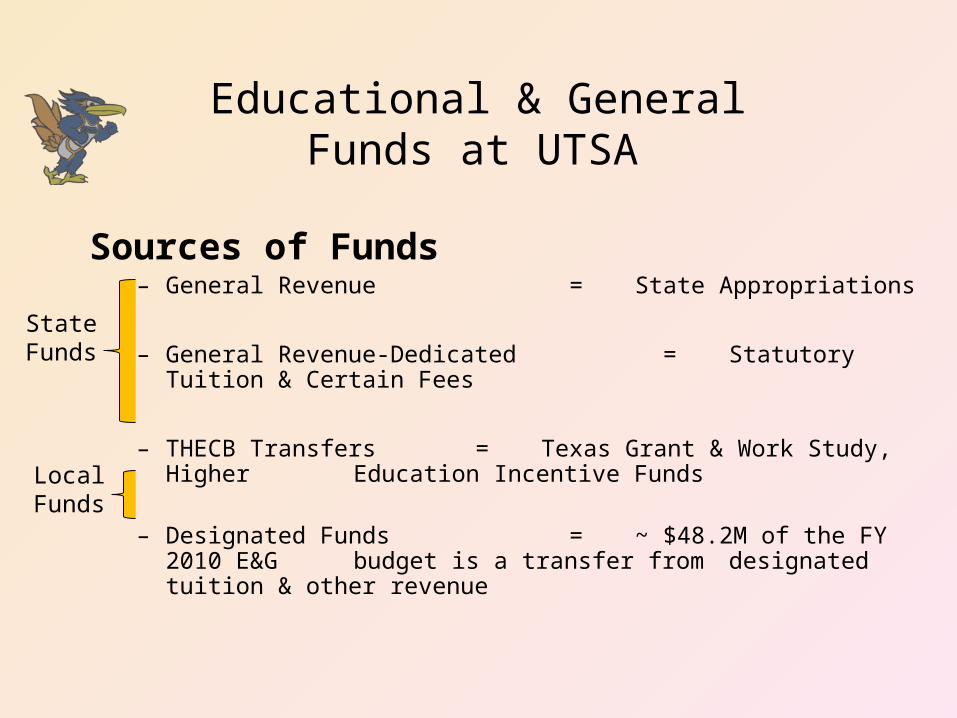

Educational & General Funds at UTSA

Sources of Funds

– General Revenue = State Appropriations

– General Revenue-Dedicated = Statutory Tuition & Certain Fees

– THECB Transfers = Texas Grant & Work Study, Higher Education Incentive Funds

– Designated Funds = ~ $48.2M of the FY 2010 E&G

budget is a transfer from designated tuition & other revenue

State Funds

Local Funds

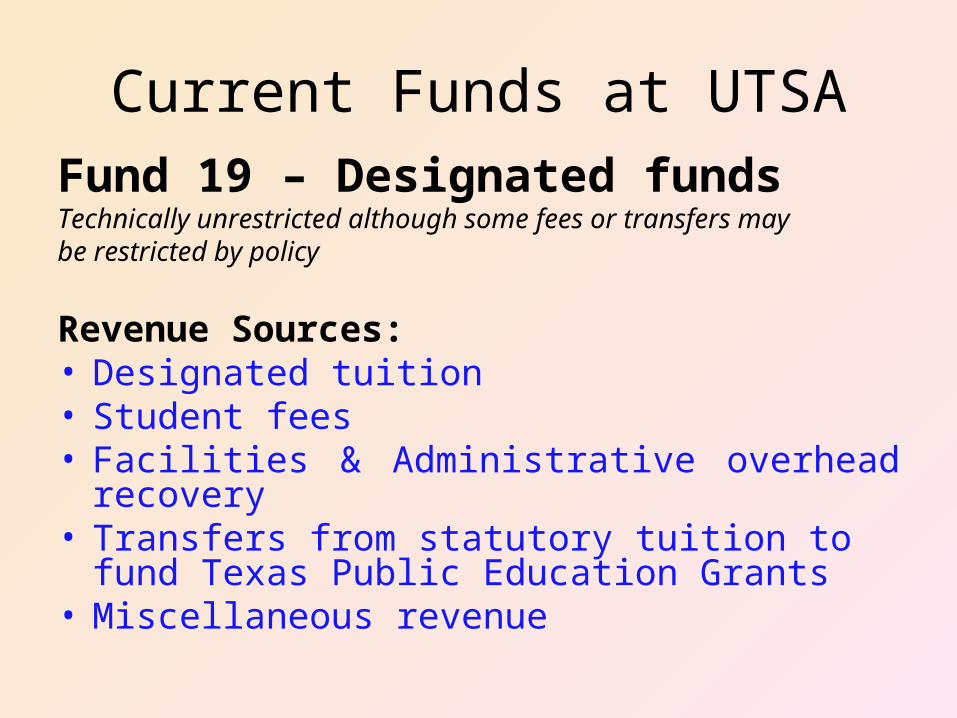

Current Funds at UTSAFund 19 – Designated fundsTechnically unrestricted although some fees or transfers may be restricted by policy

Revenue Sources:• Designated tuition• Student fees• Facilities & Administrative overhead recovery• Transfers from statutory tuition to fund Texas Public

Education Grants• Miscellaneous revenue

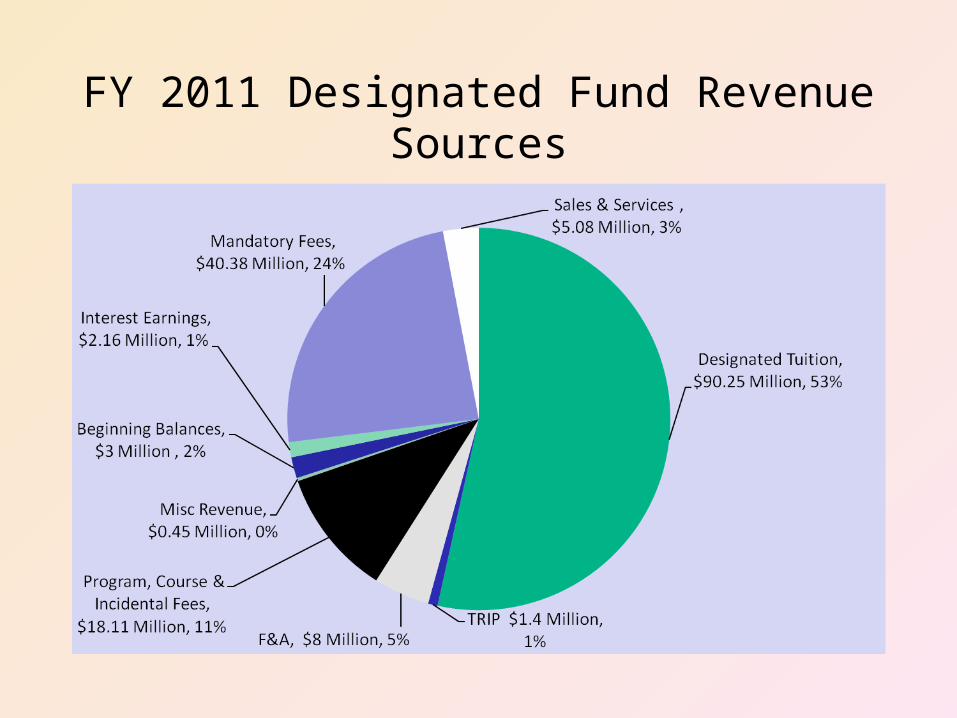

FY 2011 Designated Fund Revenue Sources

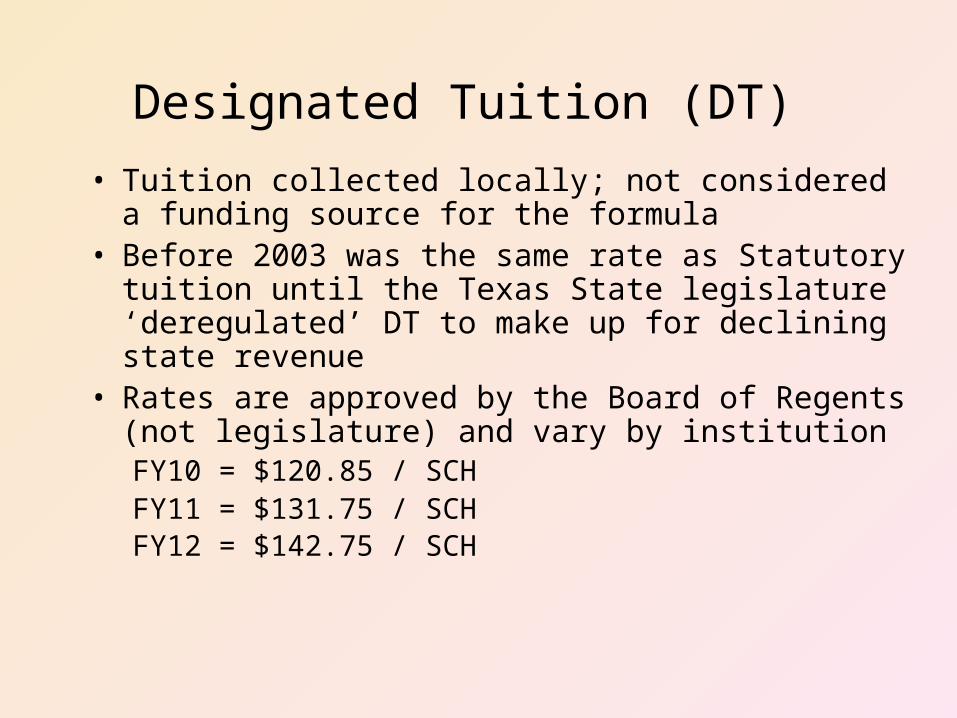

Designated Tuition (DT)

• Tuition collected locally; not considered a funding source for the formula

• Before 2003 was the same rate as Statutory tuition until the Texas State legislature ‘deregulated’ DT to make up for declining state revenue

• Rates are approved by the Board of Regents (not legislature) and vary by institutionFY10 = $120.85 / SCH FY11 = $131.75 / SCH FY12 = $142.75 / SCH

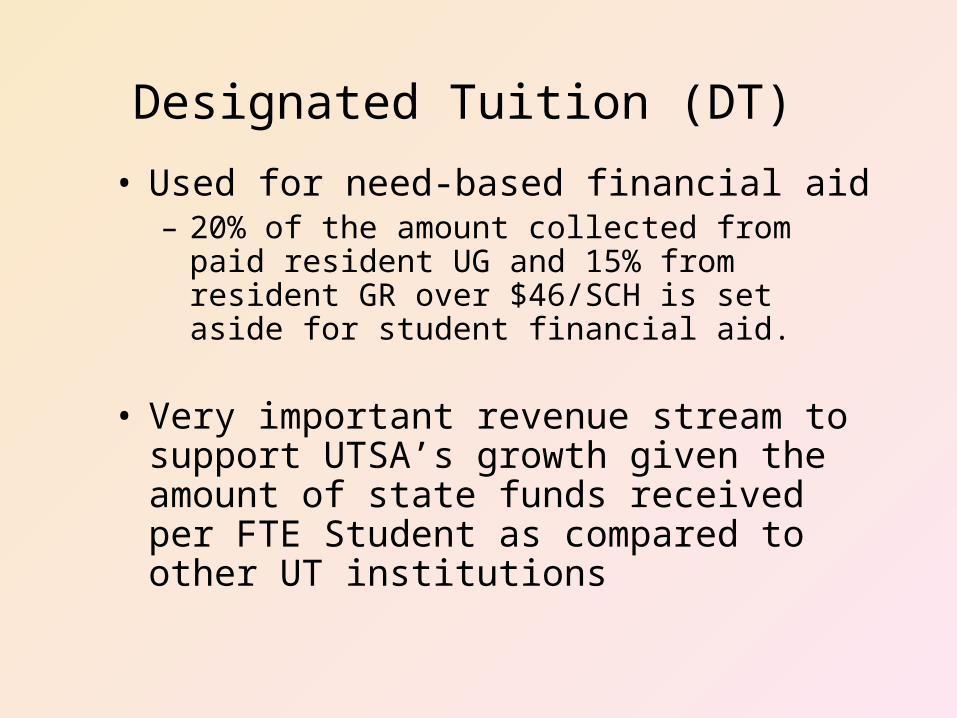

Designated Tuition (DT)

• Used for need-based financial aid– 20% of the amount collected from paid resident UG

and 15% from resident GR over $46/SCH is set aside for student financial aid.

• Very important revenue stream to support UTSA’s growth given the amount of state funds received per FTE Student as compared to other UT institutions

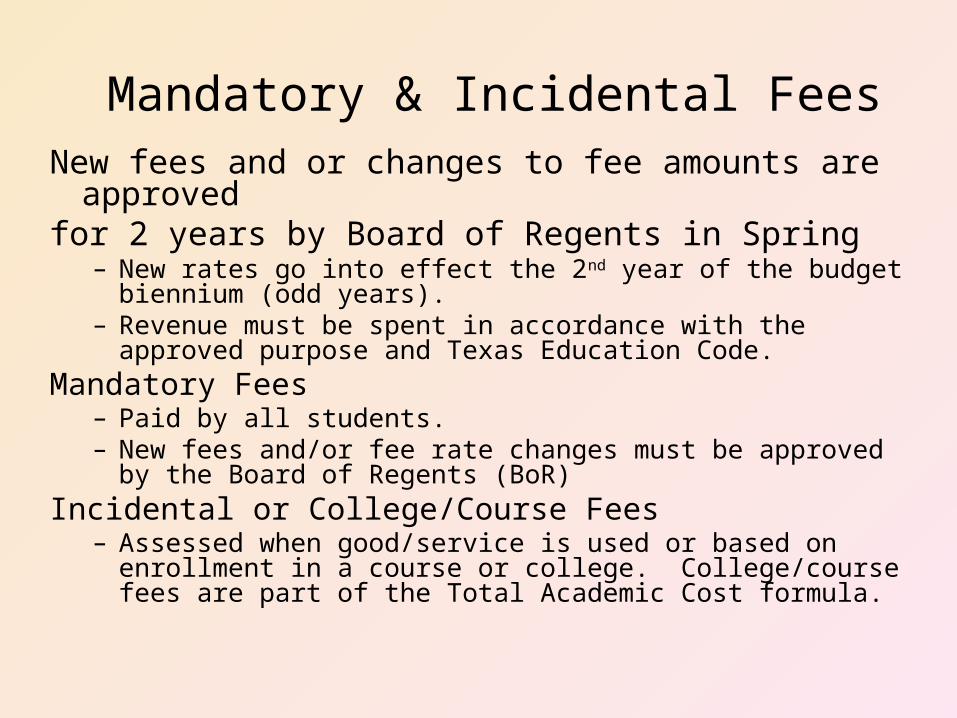

Mandatory & Incidental FeesNew fees and or changes to fee amounts are approved for 2 years by Board of Regents in Spring

– New rates go into effect the 2nd year of the budget biennium (odd years).

– Revenue must be spent in accordance with the approved purpose and Texas Education Code.

Mandatory Fees – Paid by all students. – New fees and/or fee rate changes must be approved by the

Board of Regents (BoR)Incidental or College/Course Fees

– Assessed when good/service is used or based on enrollment in a course or college. College/course fees are part of the Total Academic Cost formula.

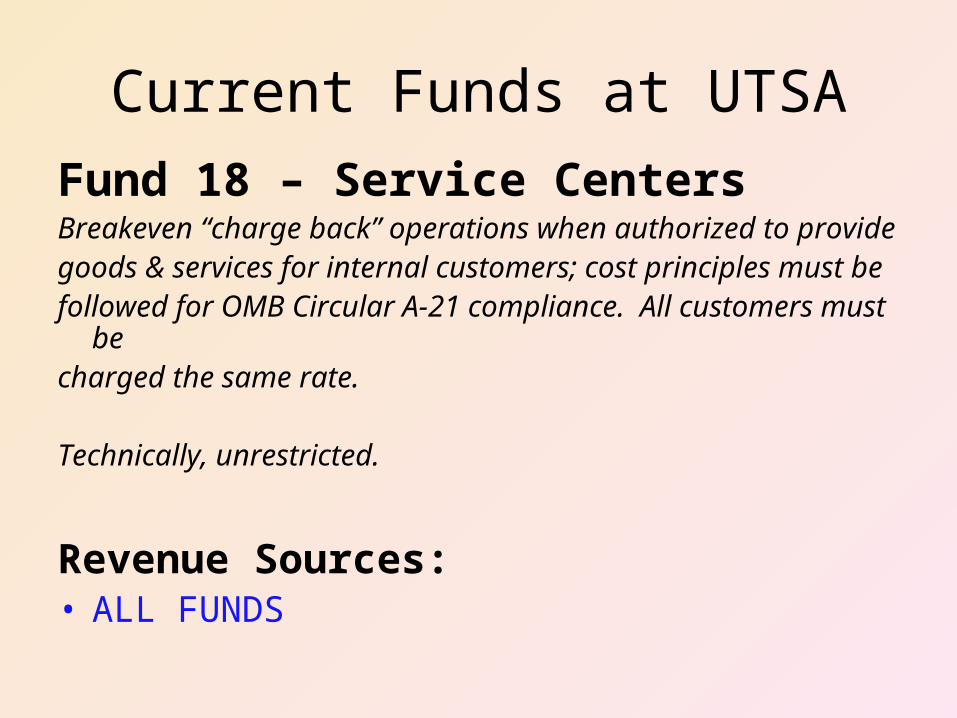

Current Funds at UTSAFund 18 – Service CentersBreakeven “charge back” operations when authorized to provide goods & services for internal customers; cost principles must be followed for OMB Circular A-21 compliance. All customers must be charged the same rate.

Technically, unrestricted.

Revenue Sources:• ALL FUNDS

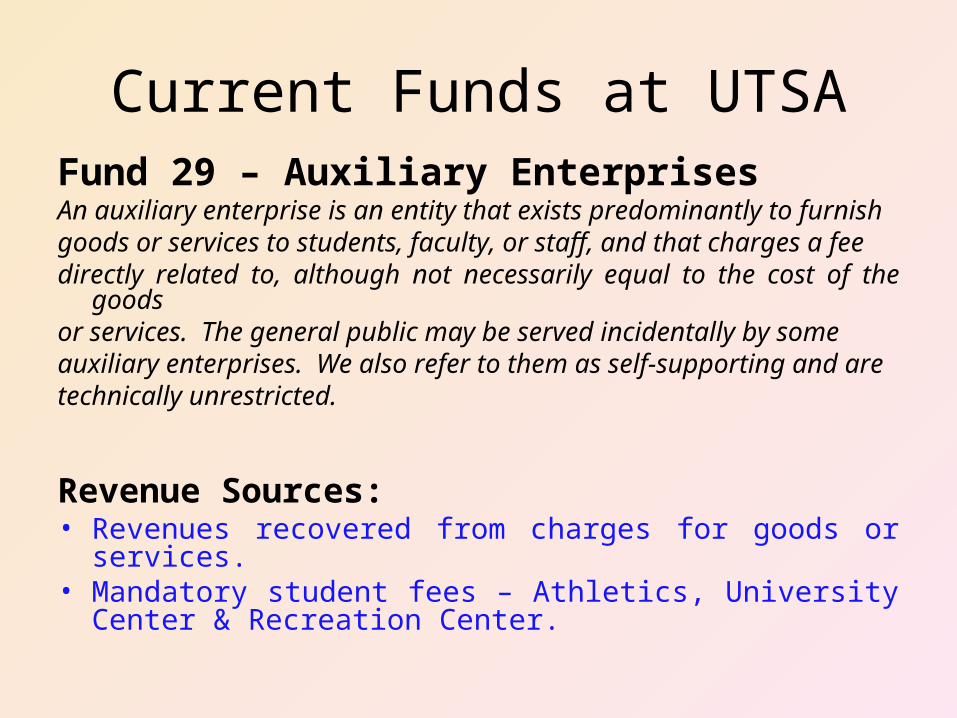

Current Funds at UTSAFund 29 – Auxiliary EnterprisesAn auxiliary enterprise is an entity that exists predominantly to furnish goods or services to students, faculty, or staff, and that charges a fee directly related to, although not necessarily equal to the cost of the goods or services. The general public may be served incidentally by some auxiliary enterprises. We also refer to them as self-supporting and are technically unrestricted.

Revenue Sources:• Revenues recovered from charges for goods or services.• Mandatory student fees – Athletics, University Center &

Recreation Center.

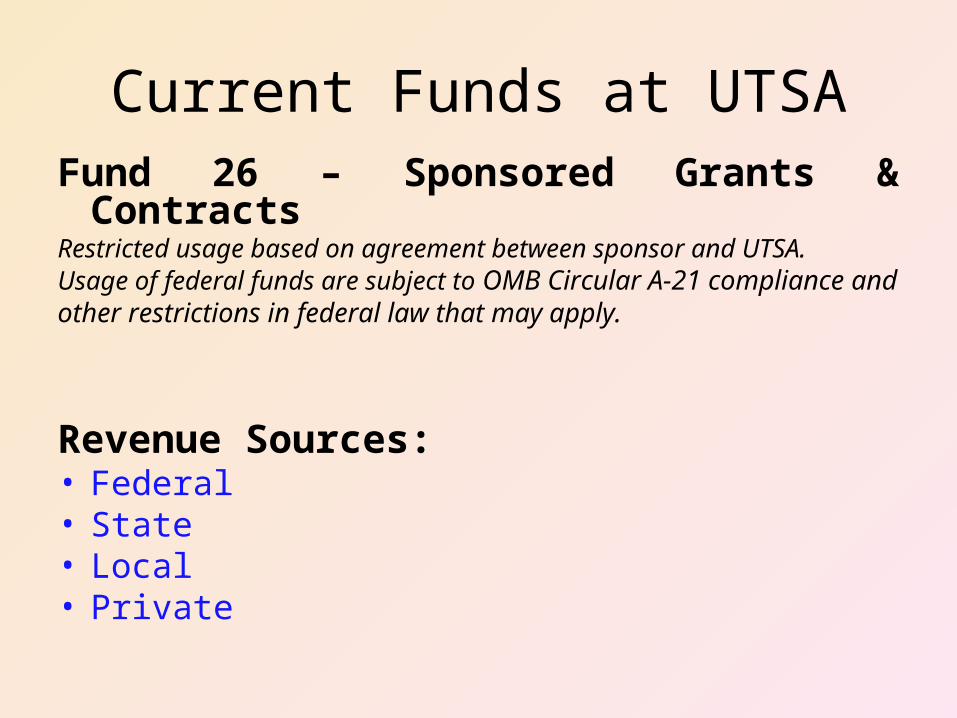

Current Funds at UTSAFund 26 – Sponsored Grants & ContractsRestricted usage based on agreement between sponsor and UTSA. Usage of federal funds are subject to OMB Circular A-21 compliance andother restrictions in federal law that may apply.

Revenue Sources:• Federal • State • Local • Private

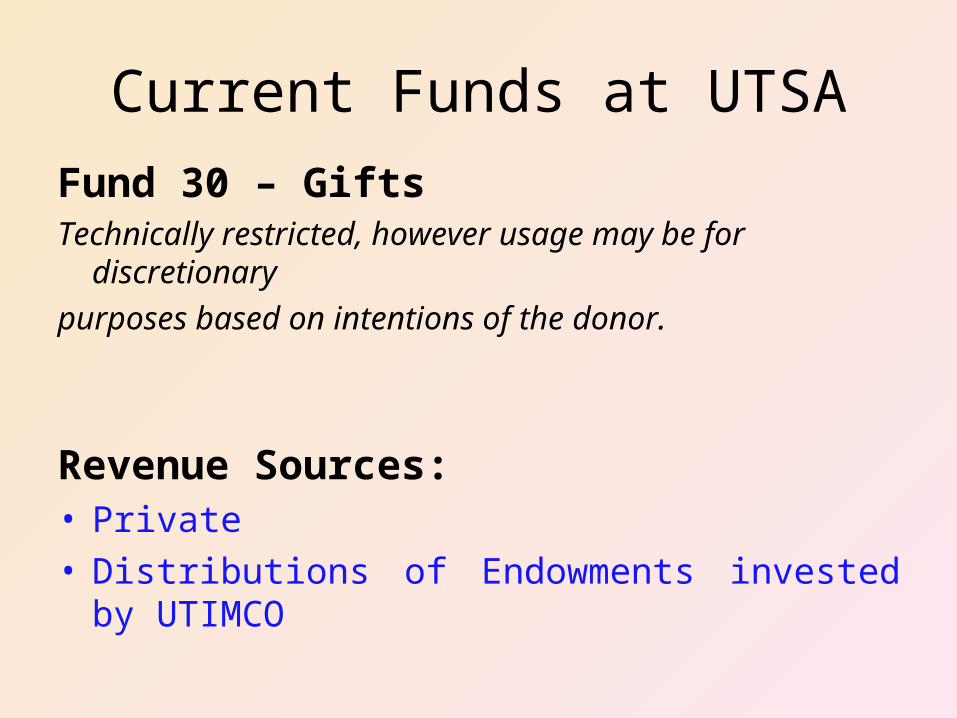

Current Funds at UTSAFund 30 – GiftsTechnically restricted, however usage may be for discretionarypurposes based on intentions of the donor.

Revenue Sources:• Private • Distributions of Endowments invested by UTIMCO

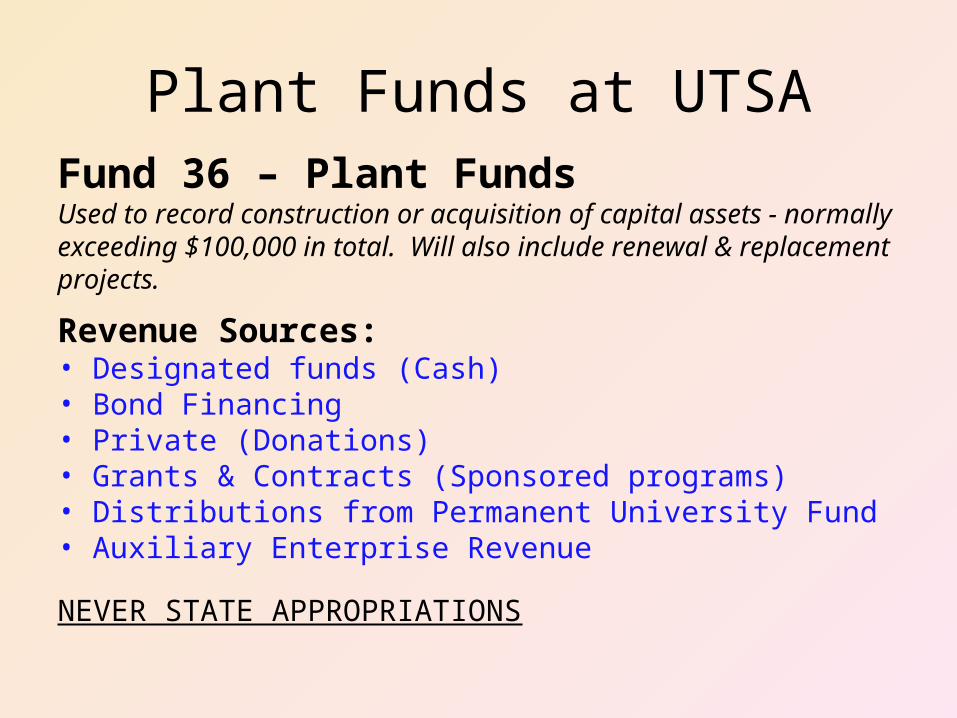

Plant Funds at UTSAFund 36 – Plant FundsUsed to record construction or acquisition of capital assets - normally exceeding $100,000 in total. Will also include renewal & replacement projects.

Revenue Sources:• Designated funds (Cash)• Bond Financing• Private (Donations)• Grants & Contracts (Sponsored programs)• Distributions from Permanent University Fund• Auxiliary Enterprise Revenue

NEVER STATE APPROPRIATIONS

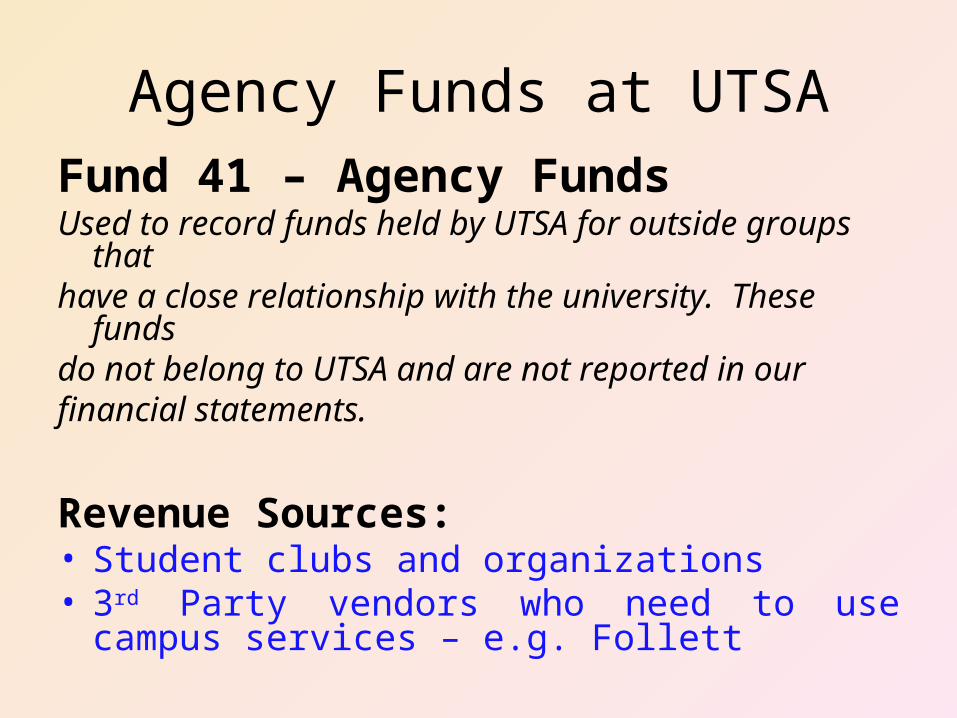

Agency Funds at UTSAFund 41 – Agency FundsUsed to record funds held by UTSA for outside groups that have a close relationship with the university. These funds do not belong to UTSA and are not reported in our financial statements.

Revenue Sources:• Student clubs and organizations• 3rd Party vendors who need to use campus services –

e.g. Follett

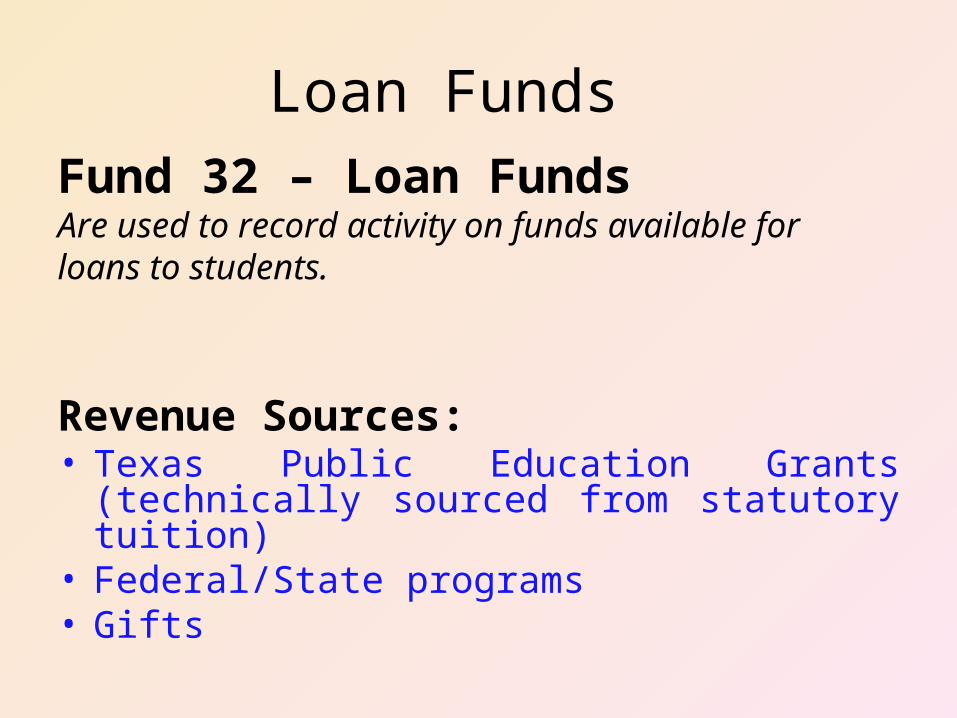

Loan Funds Fund 32 – Loan FundsAre used to record activity on funds available for loans to students.

Revenue Sources:• Texas Public Education Grants (technically sourced

from statutory tuition)• Federal/State programs• Gifts

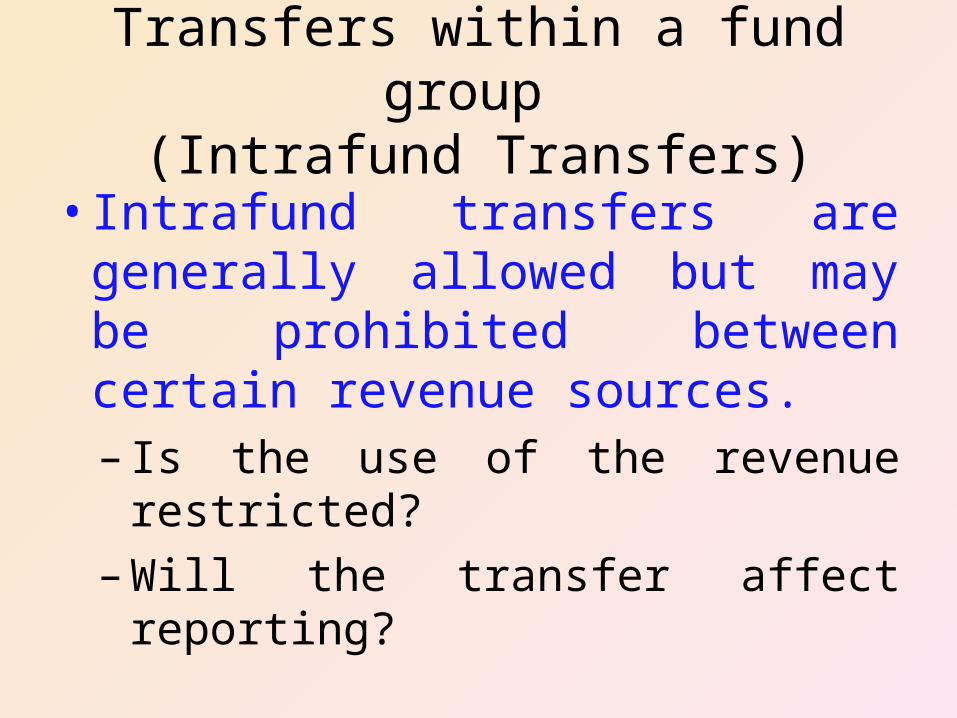

Transfers within a fund group (Intrafund Transfers)

• Intrafund transfers are generally allowed but may be prohibited between certain revenue sources.–Is the use of the revenue restricted?–Will the transfer affect reporting?

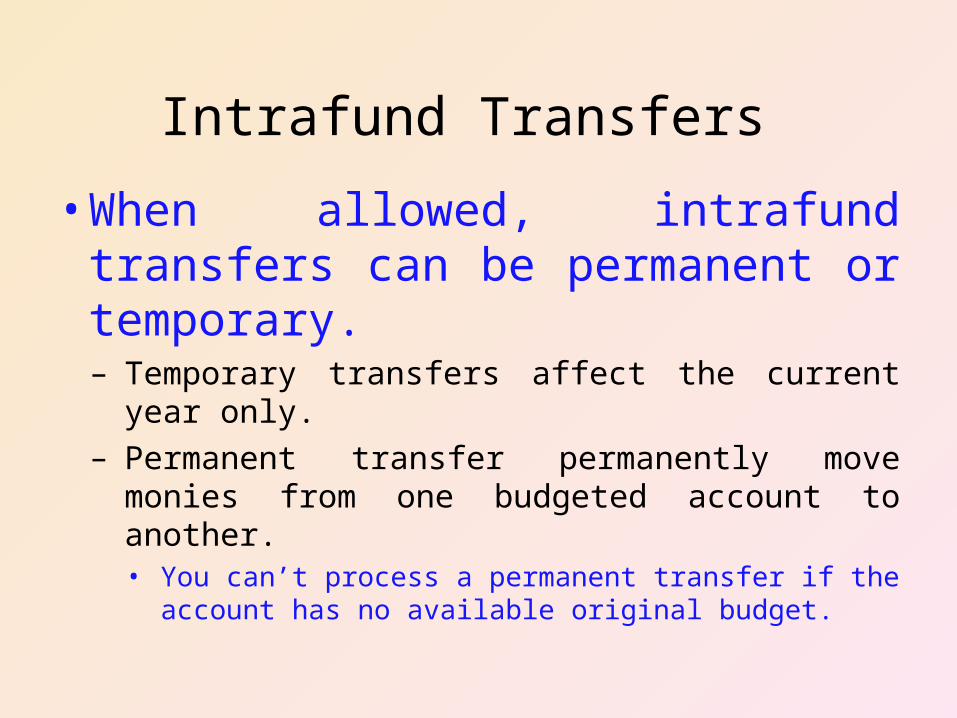

Intrafund Transfers

• When allowed, intrafund transfers can be permanent or temporary.– Temporary transfers affect the current year only.– Permanent transfer permanently move monies

from one budgeted account to another. • You can’t process a permanent transfer if the account

has no available original budget.

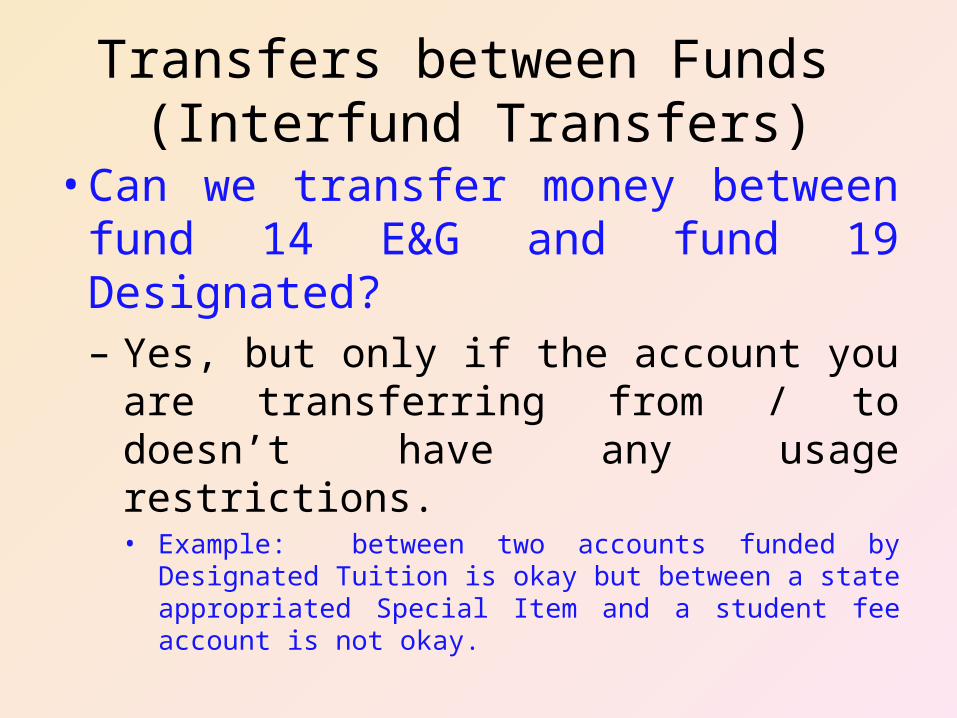

Transfers between Funds (Interfund Transfers)

• Can we transfer money between fund 14 E&G and fund 19 Designated?–Yes, but only if the account you are

transferring from / to doesn’t have any usage restrictions.• Example: between two accounts funded by Designated

Tuition is okay but between a state appropriated Special Item and a student fee account is not okay.

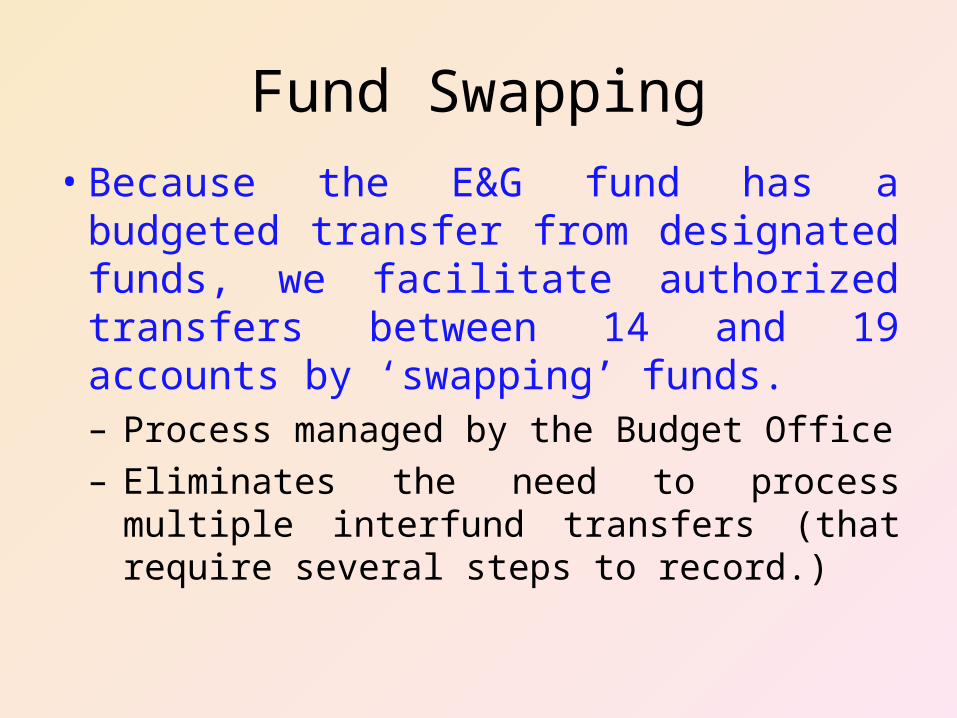

Fund Swapping

• Because the E&G fund has a budgeted transfer from designated funds, we facilitate authorized transfers between 14 and 19 accounts by ‘swapping’ funds. –Process managed by the Budget Office– Eliminates the need to process multiple

interfund transfers (that require several steps to record.)

Interfund Transfers

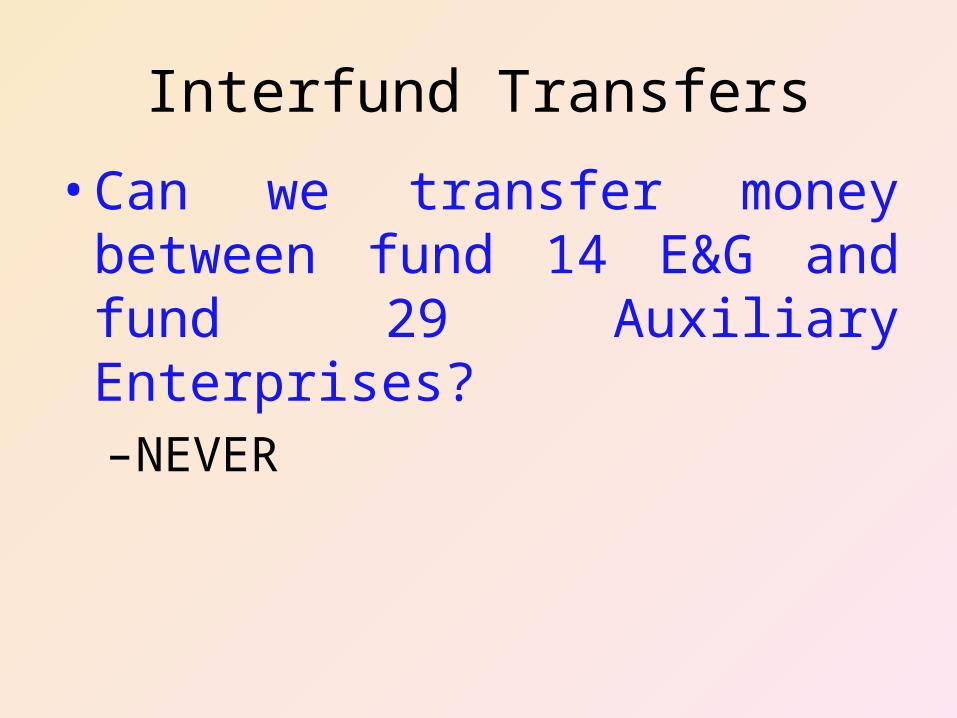

• Can we transfer money between fund 14 E&G and fund 29 Auxiliary Enterprises?–NEVER

Interfund Transfers

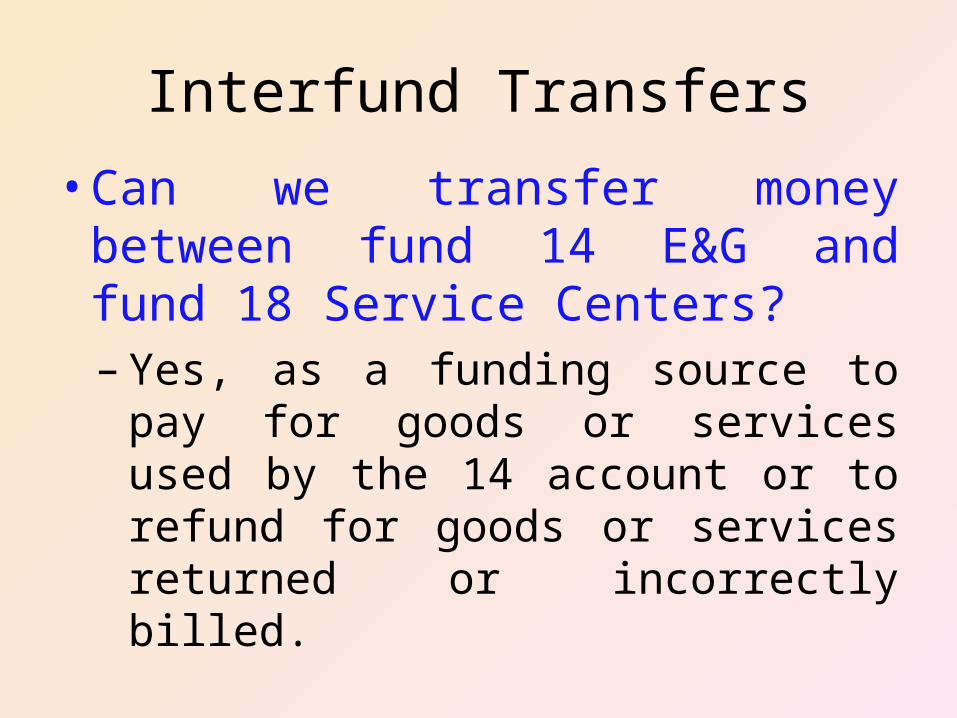

• Can we transfer money between fund 14 E&G and fund 18 Service Centers?–Yes, as a funding source to pay for

goods or services used by the 14 account or to refund for goods or services returned or incorrectly billed.

Interfund Transfers

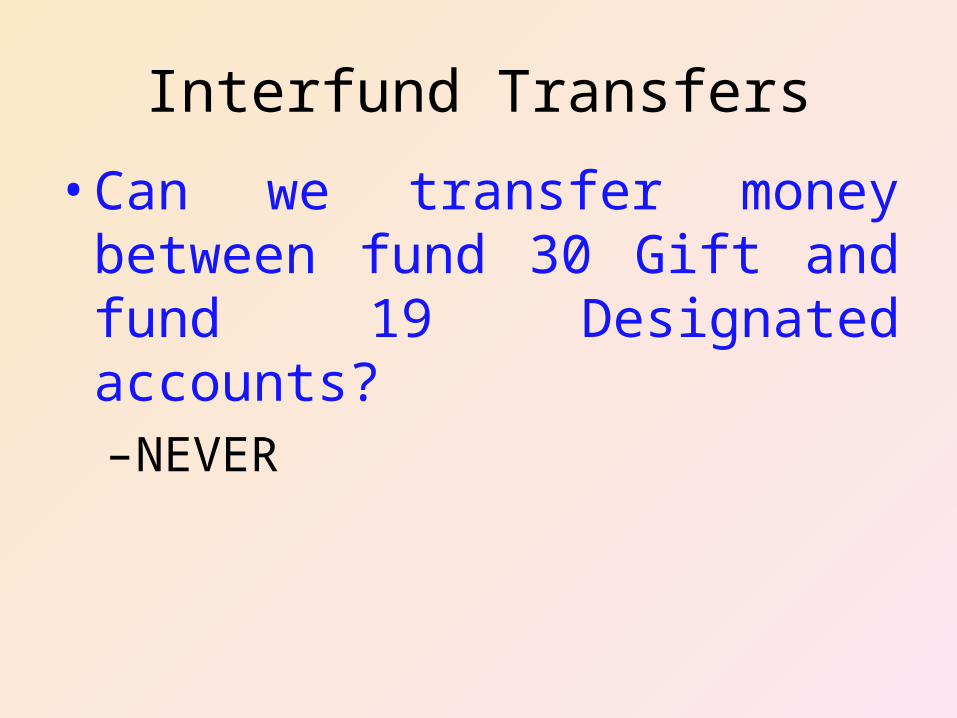

• Can we transfer money between fund 30 Gift and fund 19 Designated accounts?–NEVER

Interfund Transfers

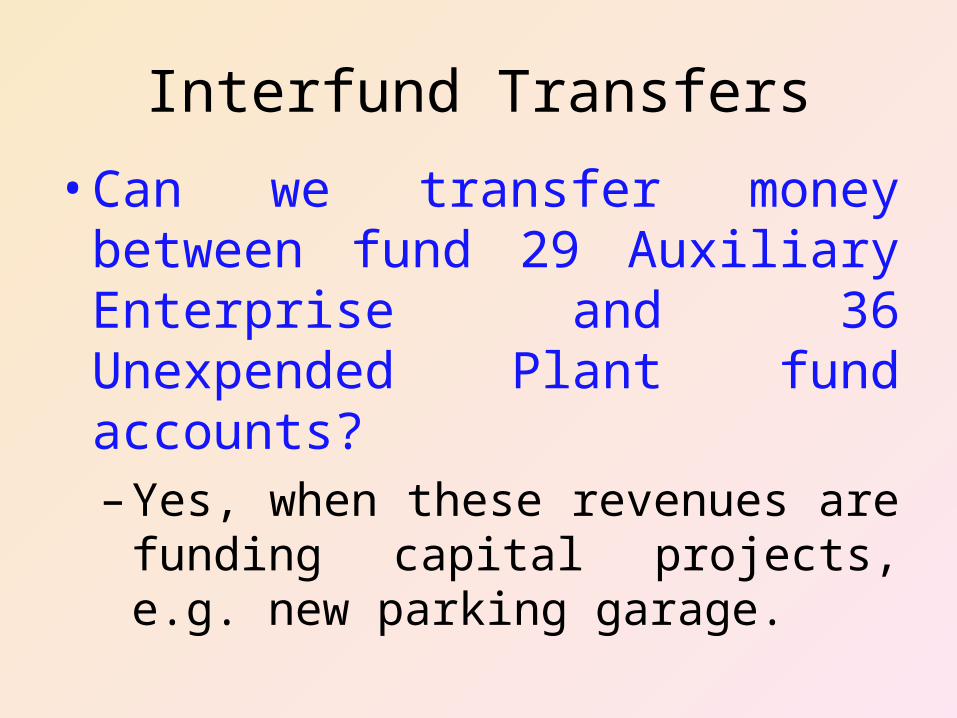

• Can we transfer money between fund 29 Auxiliary Enterprise and 36 Unexpended Plant fund accounts?–Yes, when these revenues are funding

capital projects, e.g. new parking garage.

Interfund Transfers

• Can interfund transfers be permanent?

Questions about fund accounting, revenue sources or related subjects?

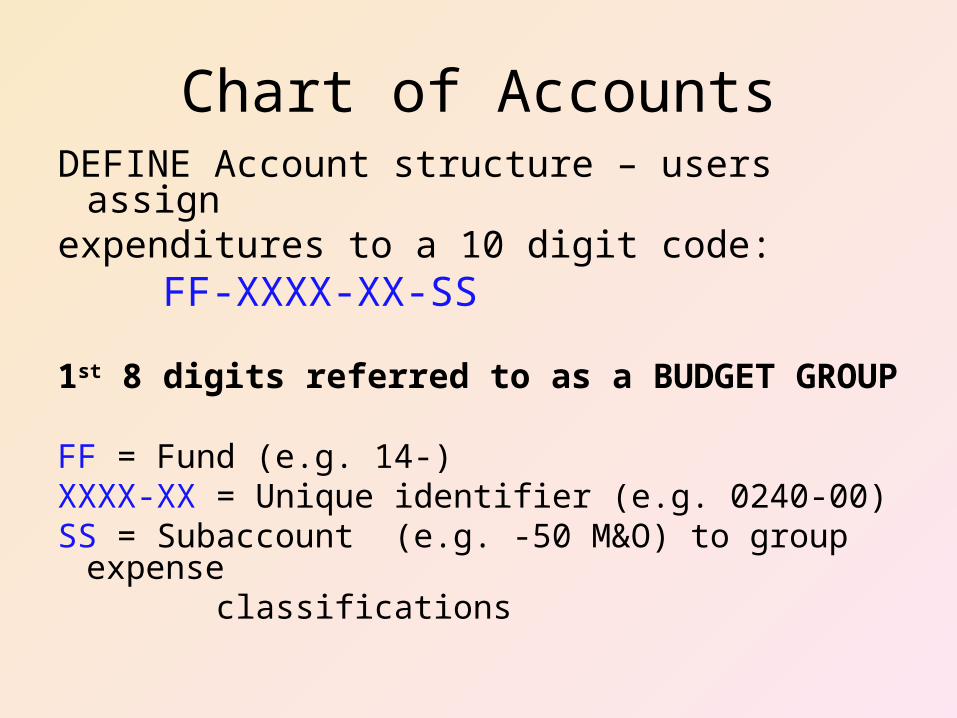

Chart of AccountsDEFINE Account structure – users assign expenditures to a 10 digit code: FF-XXXX-XX-SS

1st 8 digits referred to as a BUDGET GROUP

FF = Fund (e.g. 14-)XXXX-XX = Unique identifier (e.g. 0240-00)SS = Subaccount (e.g. -50 M&O) to group expense classifications

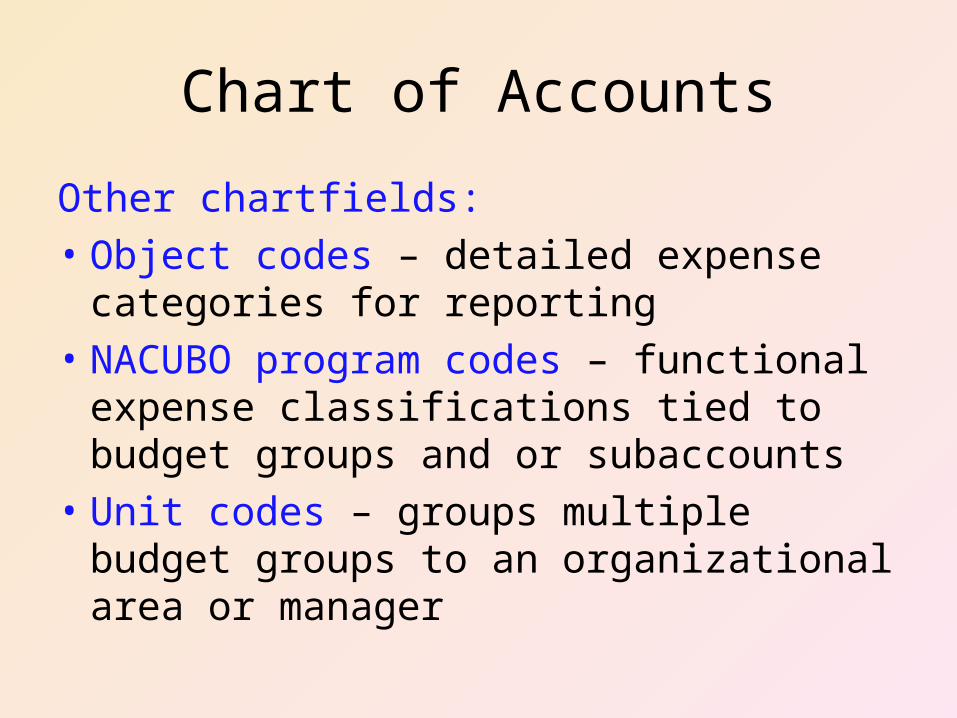

Chart of Accounts

Other chartfields:• Object codes – detailed expense categories

for reporting• NACUBO program codes – functional

expense classifications tied to budget groups and or subaccounts

• Unit codes – groups multiple budget groups to an organizational area or manager

Reporting Expenses – Functional Expense Classifications

• A functional expense classification is a method of grouping expenses according to the purpose for which the costs are incurred.– The classifications tell why an expense was

incurred rather than what was purchased. Reporting expenses this way helps stakeholders understand the various mission-related activities and their relative importance.

Reporting Expenses – Functional Expense Classifications

• Primary functional expense classifications - InstructionResearchPublic ServiceAcademic SupportStudent ServicesInstitutional SupportScholarships and FellowshipsAuxiliary EnterprisesOperations & Maintenance of Plant

Reporting Expenses – Natural Expense Classifications

• A natural expense classification is a method of grouping expenses according to the type of costs that are incurred. – The classifications tell what was purchased rather

than why an expense was incurred.

Reporting Expenses – Natural Expense Classifications

• Included are:– Salaries & Wages (can be further broken into

categories of employee types)– Employee Benefits– Utilities– Supplies– Travel– Scholarships and fellowships– Services

Fund Accounting & Financial Reporting

UT System requires regular monthly & annual financial reports • Annual Financial Report:

– Balance Sheet– Statement of Revenues, Expenses & Changes in Net Assets– Statement of Cash Flows– Miscellaneous Supporting Schedules

Annual Sources & Uses Analysis of Financial Condition

Fund Accounting & Financial Reporting

UTSA’s FY 2009 AFRhttp://www.utsa.edu/financialaffairs/controller/docsDF/annualRpt09.pdf

Other Key UT Financial Reports:http://www.utsystem.edu/cont/internal_reports.htm

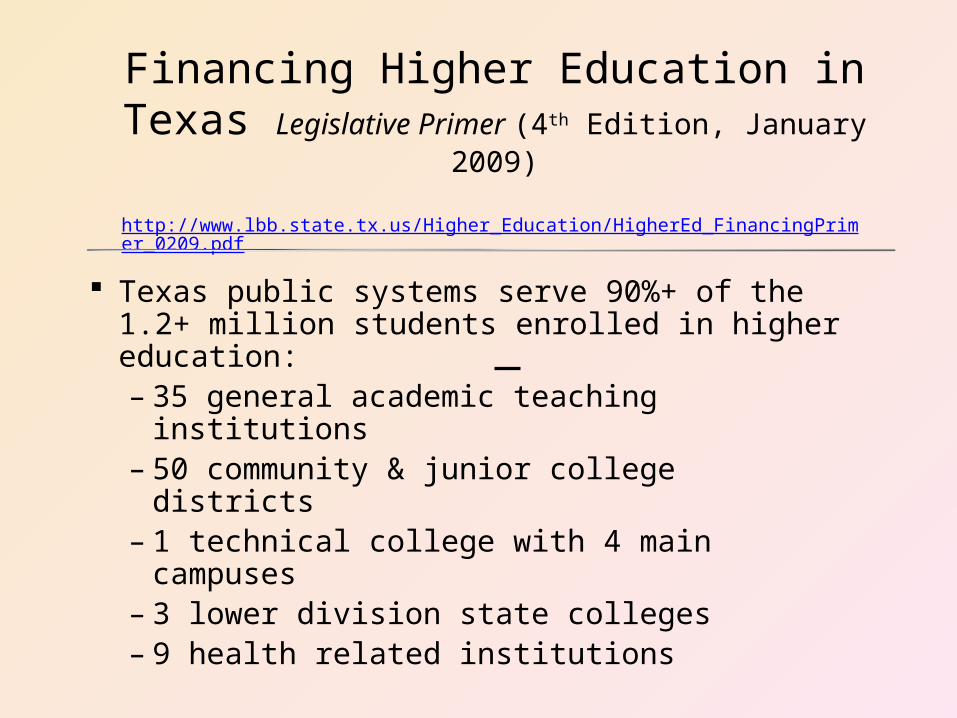

Financing Higher Education in Texas Legislative Primer (4th Edition, January 2009)

http://www.lbb.state.tx.us/Higher_Education/HigherEd_FinancingPrimer_0209.pdf

Texas public systems serve 90%+ of the 1.2+ million students enrolled in higher education: – 35 general academic teaching institutions – 50 community & junior college districts– 1 technical college with 4 main campuses– 3 lower division state colleges– 9 health related institutions

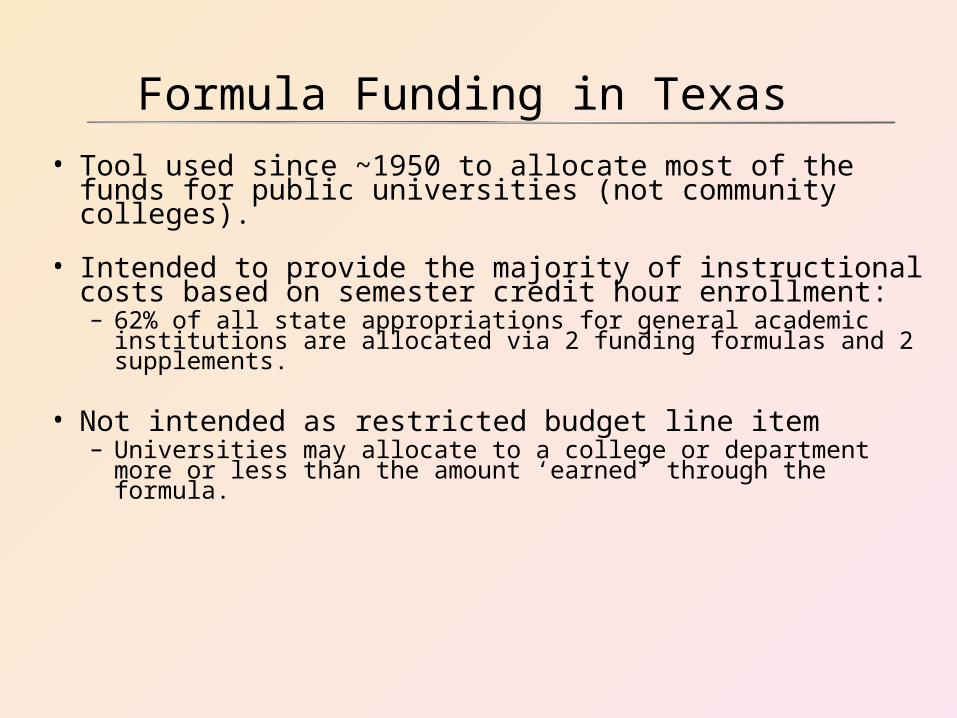

Formula Funding in Texas• Tool used since ~1950 to allocate most of the funds for

public universities (not community colleges).

• Intended to provide the majority of instructional costs based on semester credit hour enrollment: – 62% of all state appropriations for general academic institutions

are allocated via 2 funding formulas and 2 supplements.

• Not intended as restricted budget line item– Universities may allocate to a college or department more or less

than the amount ‘earned’ through the formula.

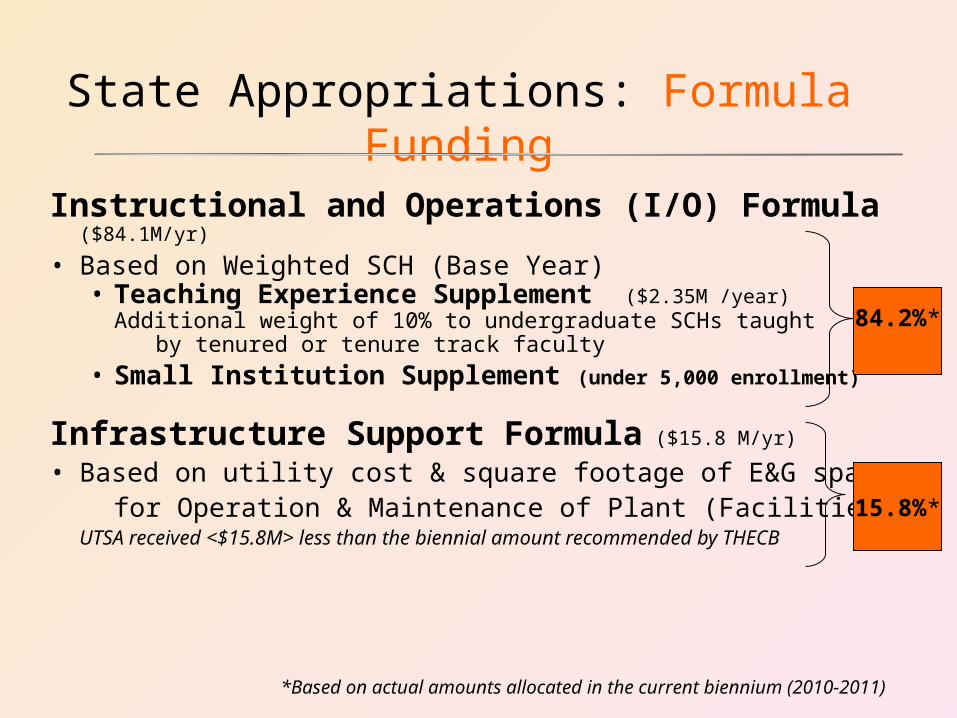

State Appropriations: Formula Funding

Instructional and Operations (I/O) Formula ($84.1M/yr)

• Based on Weighted SCH (Base Year)• Teaching Experience Supplement ($2.35M /year)

Additional weight of 10% to undergraduate SCHs taught by tenured or tenure track faculty• Small Institution Supplement (under 5,000 enrollment)

Infrastructure Support Formula ($15.8 M/yr)

• Based on utility cost & square footage of E&G space for Operation & Maintenance of Plant (Facilities)

UTSA received <$15.8M> less than the biennial amount recommended by THECB

84.2%*

15.8%*

*Based on actual amounts allocated in the current biennium (2010-2011)

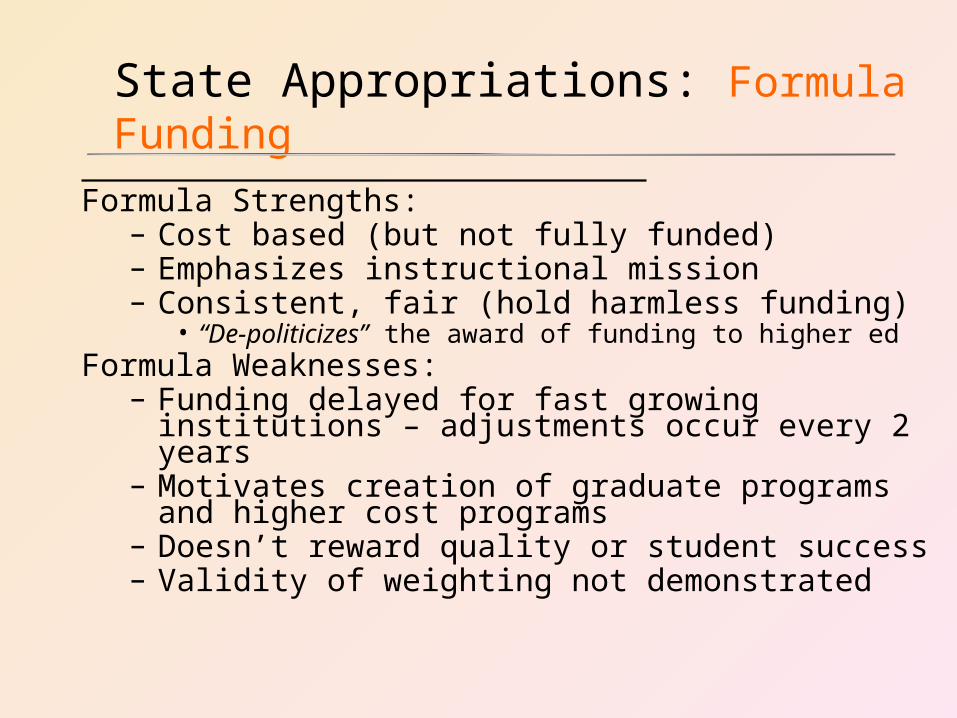

State Appropriations: Formula Funding Formula Strengths: – Cost based (but not fully funded)– Emphasizes instructional mission– Consistent, fair (hold harmless funding)

• “De-politicizes” the award of funding to higher edFormula Weaknesses: – Funding delayed for fast growing institutions – adjustments

occur every 2 years– Motivates creation of graduate programs and higher cost

programs– Doesn’t reward quality or student success – Validity of weighting not demonstrated

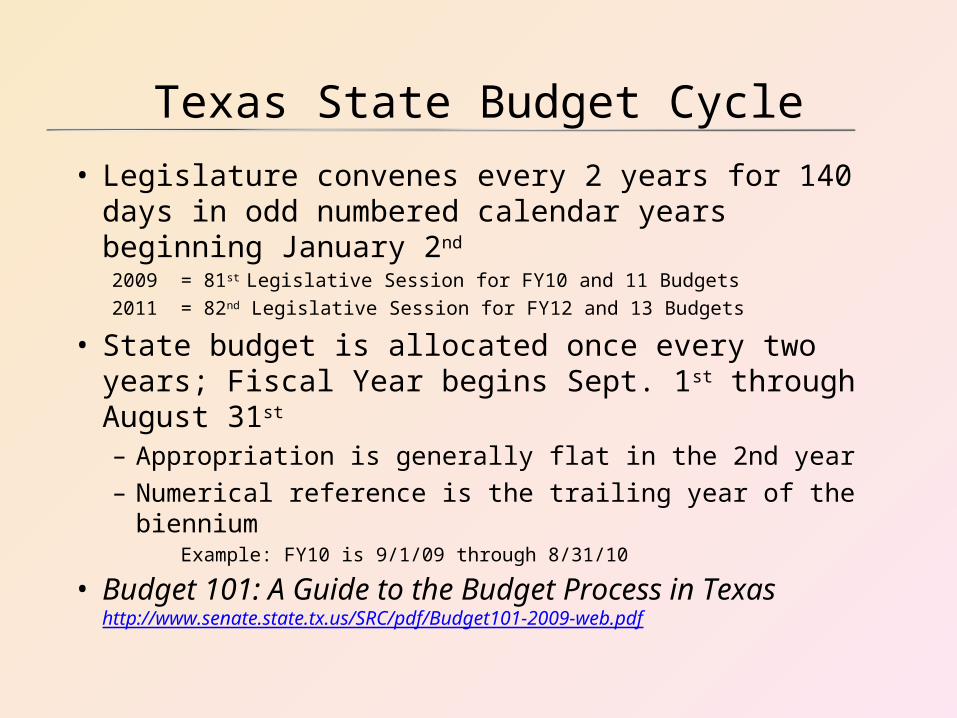

Texas State Budget Cycle

• Legislature convenes every 2 years for 140 days in odd numbered calendar years beginning January 2nd

2009 = 81st Legislative Session for FY10 and 11 Budgets2011 = 82nd Legislative Session for FY12 and 13 Budgets

• State budget is allocated once every two years; Fiscal Year begins Sept. 1st through August 31st – Appropriation is generally flat in the 2nd year– Numerical reference is the trailing year of the biennium Example: FY10 is 9/1/09 through 8/31/10

• Budget 101: A Guide to the Budget Process in Texas http://www.senate.state.tx.us/SRC/pdf/Budget101-2009-web.pdf

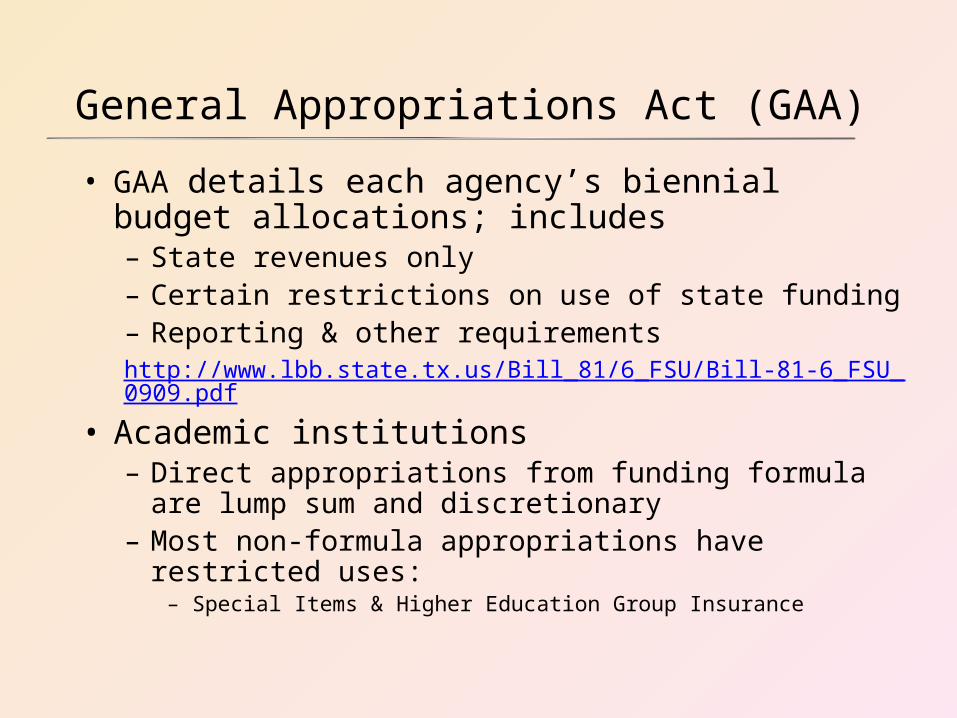

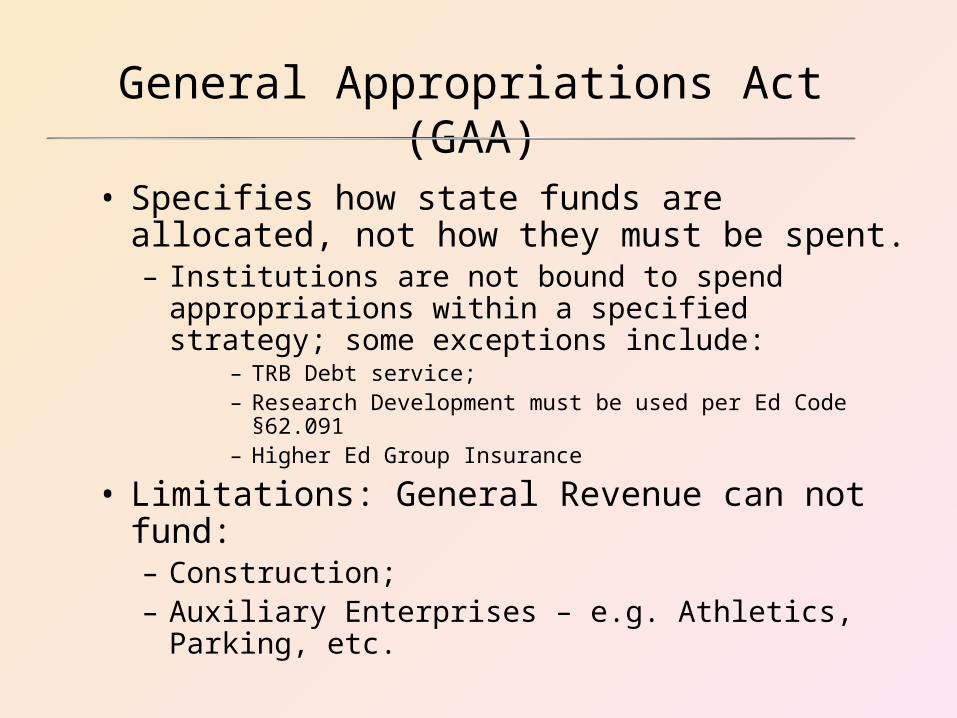

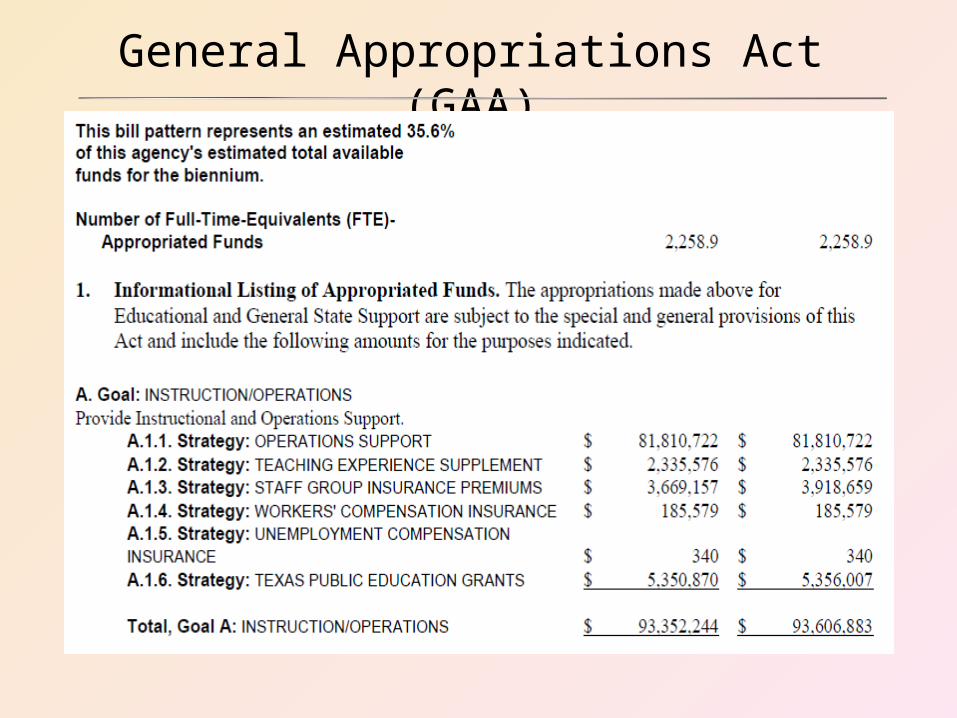

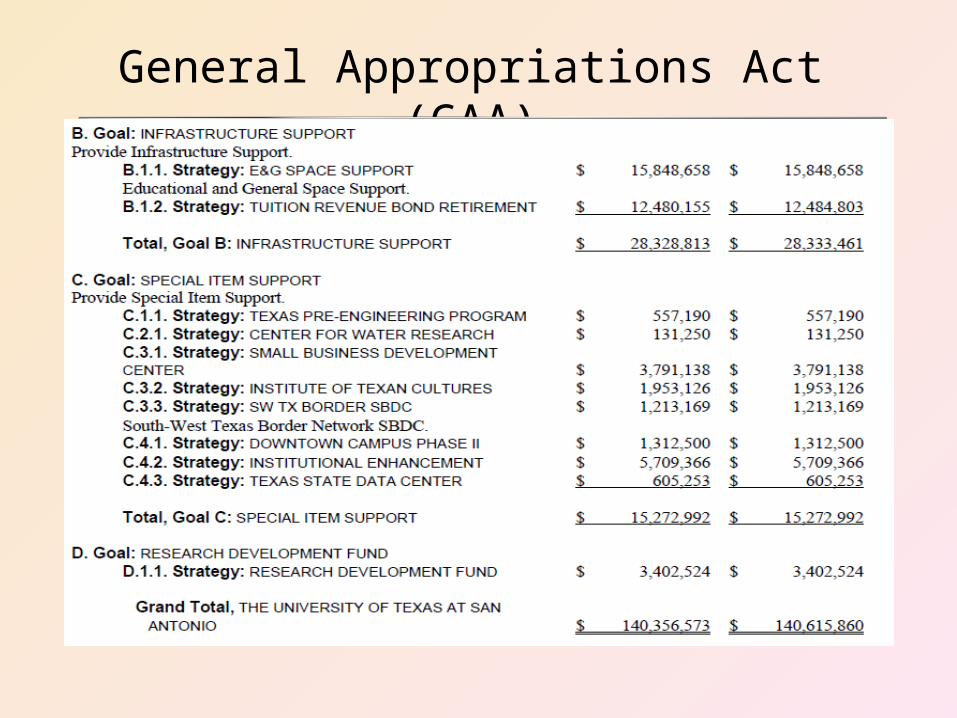

General Appropriations Act (GAA)

• GAA details each agency’s biennial budget allocations; includes– State revenues only– Certain restrictions on use of state funding– Reporting & other requirementshttp://www.lbb.state.tx.us/Bill_81/6_FSU/Bill-81-6_FSU_0909.pdf

• Academic institutions – Direct appropriations from funding formula are lump sum

and discretionary– Most non-formula appropriations have restricted uses:

– Special Items & Higher Education Group Insurance

General Appropriations Act (GAA)

• Specifies how state funds are allocated, not how they must be spent.– Institutions are not bound to spend appropriations

within a specified strategy; some exceptions include:– TRB Debt service;– Research Development must be used per Ed Code §62.091– Higher Ed Group Insurance

• Limitations: General Revenue can not fund:– Construction;– Auxiliary Enterprises – e.g. Athletics, Parking, etc.

General Appropriations Act (GAA)

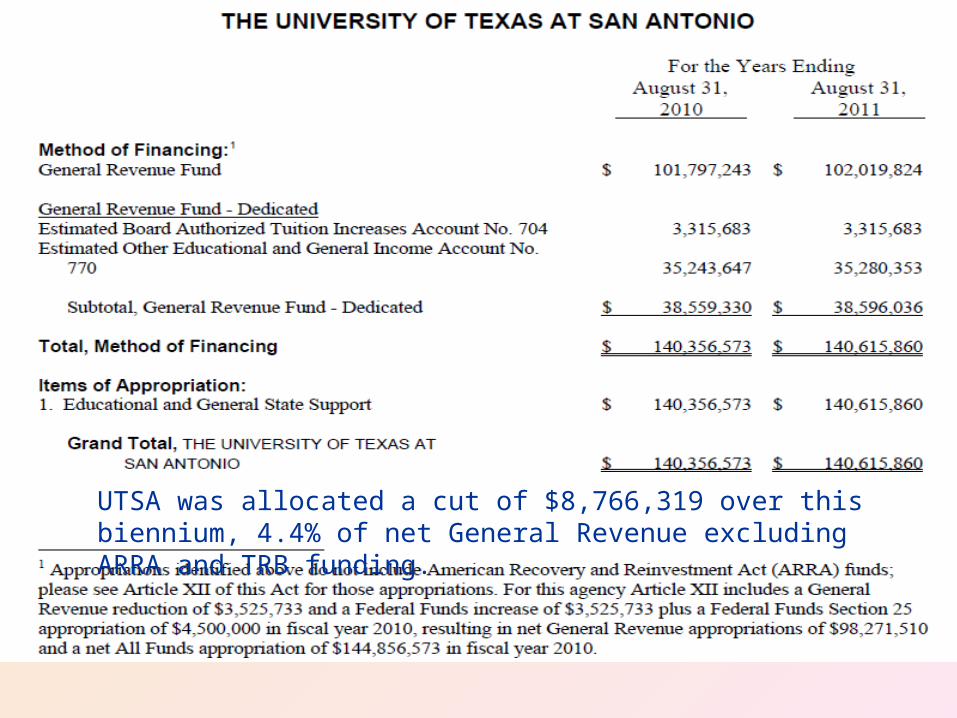

UTSA was allocated a cut of $8,766,319 over this biennium, 4.4% of net General Revenue excluding ARRA and TRB funding.

General Appropriations Act (GAA)

General Appropriations Act (GAA)

Legislative Appropriations Request (LAR)• Budget Request prepared by each agency during the

Summer (of an “even” year) prior to legislative session • “Performance” budget tied to goals, objectives, strategies

and measures• Does not include formula funding for higher education• Joint Budget Hearings

– Result in draft budget bill (General Appropriations Act) filed in both houses of the legislature

• Comptroller’s Biennial Revenue Estimate – Revenue sources, projections, economic outlook, detailed accounting of state treasury

Legislature can not appropriate an amount

greater than anticipated revenue!

University Budget Process

• University Strategic Resource Planning Council (USRPC) Recommends Budget Changes

• Council on Management & Operations (CMO) Endorses & President Approves

• Draft Budget Document Prepared• UT System Budget Hearings• Board of Regents Approvalhttp://www.utsa.edu/financialaffairs/budget/

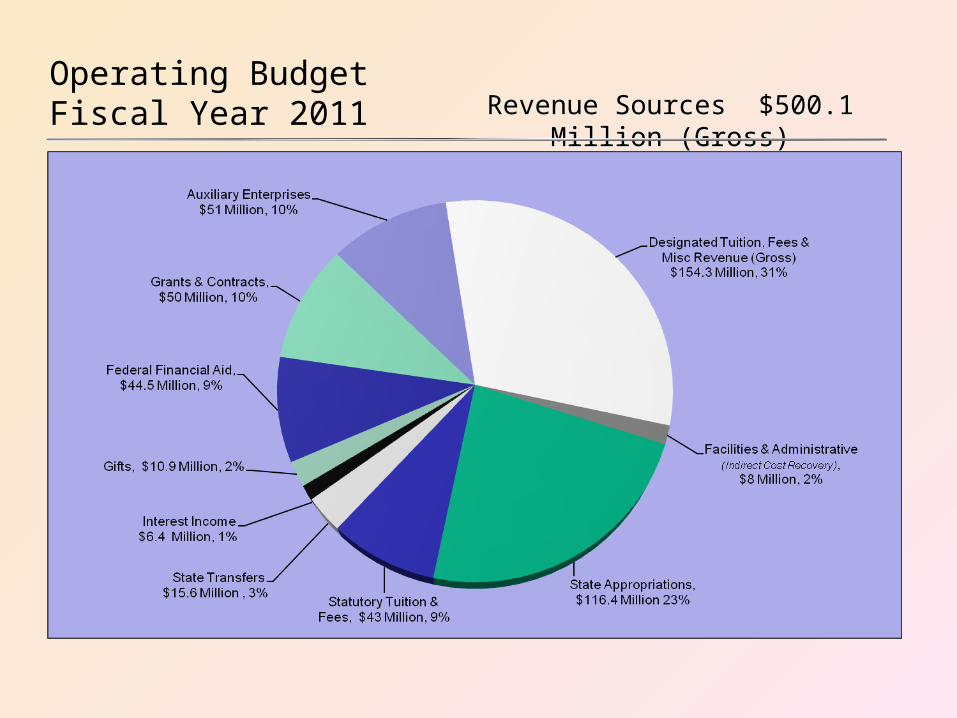

Operating BudgetFiscal Year 2011

Revenue Sources $500.1 Million (Gross)Revenue Sources $500.1 Million (Gross)

THE END!

Questions and Answers?