Embed Size (px)

Citation preview

Financial Highlights and Strategic OpportunitiesRick Carucci

CFO, YUM! Brands Inc.

This announcement contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements include those identified by such words as may, will, expect, project, anticipate, believe, plan and other similar terminology. These “forward-looking”statements reflect management’s current expectations regarding future events and operating andfinancial performance and are based on currently available data. However, actual results are subject to future events and uncertainties, which could cause actual results to differ from those projected in this announcement. Factors that can cause actual results to differ materially include changes in global and local business, economic and political conditions in the countries and territories where Yum! Brands operates, including the effects of war and terrorist activities; changes in currency exchange and interest rates; changes in commodity, labor and other operating costs; changes in competition in the food industry, consumer preferences, spending patterns and demographic trends; the impact that any widespread illness or general health concern may have on our business and the economy of the countries in which we operate; the effectiveness of our operating initiatives and advertising and promotional efforts; new-product and concept development by Yum! Brands and other food-industry competitors; the success of our refranchising strategy; the ongoing business viability of our franchise and license operators; our ability to secure alternative distribution to our restaurants at competitive rates and to ensure adequate supplies of restaurant products and equipment in our stores; publicity that may impact our business and/or industry; severe weather conditions; effects and outcomes of legal claims involving the company; changes in effective tax rates; our actuarially determined casualty loss estimates; changes in legislation and governmental regulations; and changes in accounting policies and practices. Further information about factors that could affect Yum! Brands’ financial and other results are included in the company’s Forms 10-Q and 10-K, filed with the Securities and Exchange Commission.

Information herein is as of 4/21/05

3

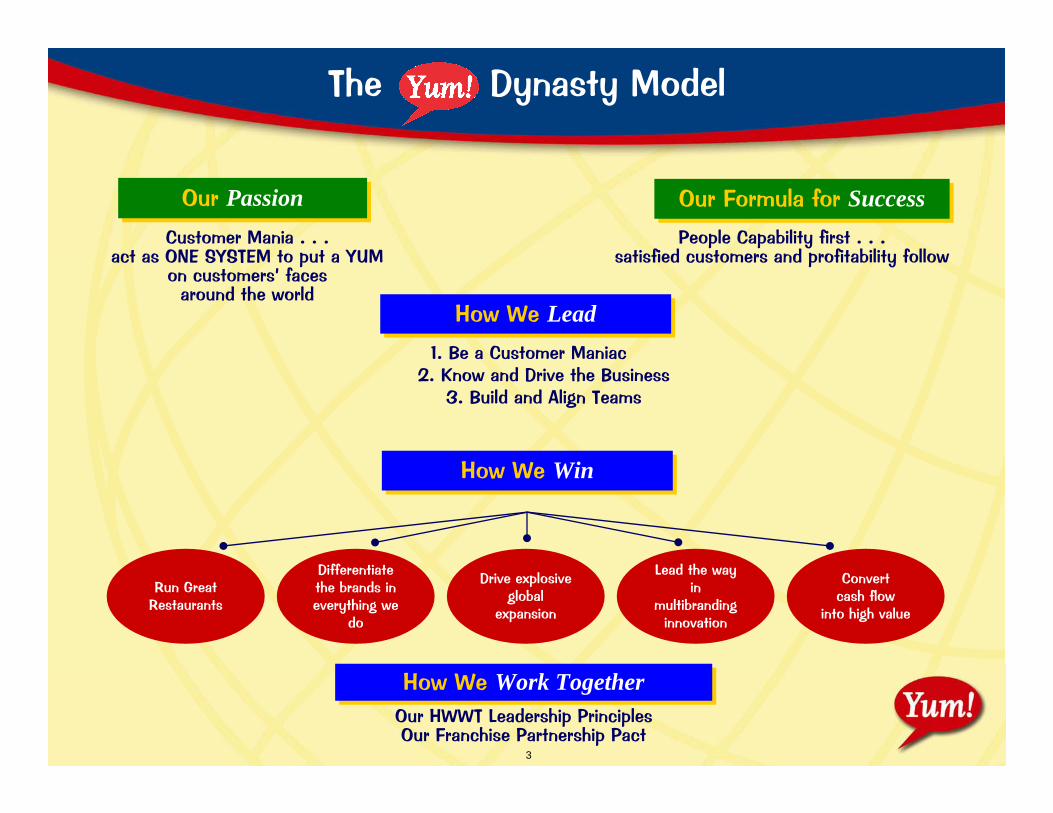

People Capability first . . .satisfied customers and profitability follow

Our PassionOur PassionCustomer Mania . . .

act as ONE SYSTEM to put a YUM on customers’ faces

around the world

How We WinHow We Win

How We Work TogetherHow We Work TogetherOur HWWT Leadership PrinciplesOur Franchise Partnership Pact

How We LeadHow We Lead1. Be a Customer Maniac

2. Know and Drive the Business3. Build and Align Teams

The Dynasty Model

Run Great Restaurants

Drive explosive global

expansion

Lead the wayin

multibrandinginnovation

Convert cash flow

into high value

Differentiatethe brands in everything we

do

Our Formula for SuccessOur Formula for Success

4

YUM! — Track Record of Performance

2002 +13%2002 +13%

2003 +13%2003 +13%

2004 +15%2004 +15%

Shareholder Commitment . . . Shareholder Commitment . . . At Least +10% Annual EPS GrowthAt Least +10% Annual EPS Growth

5

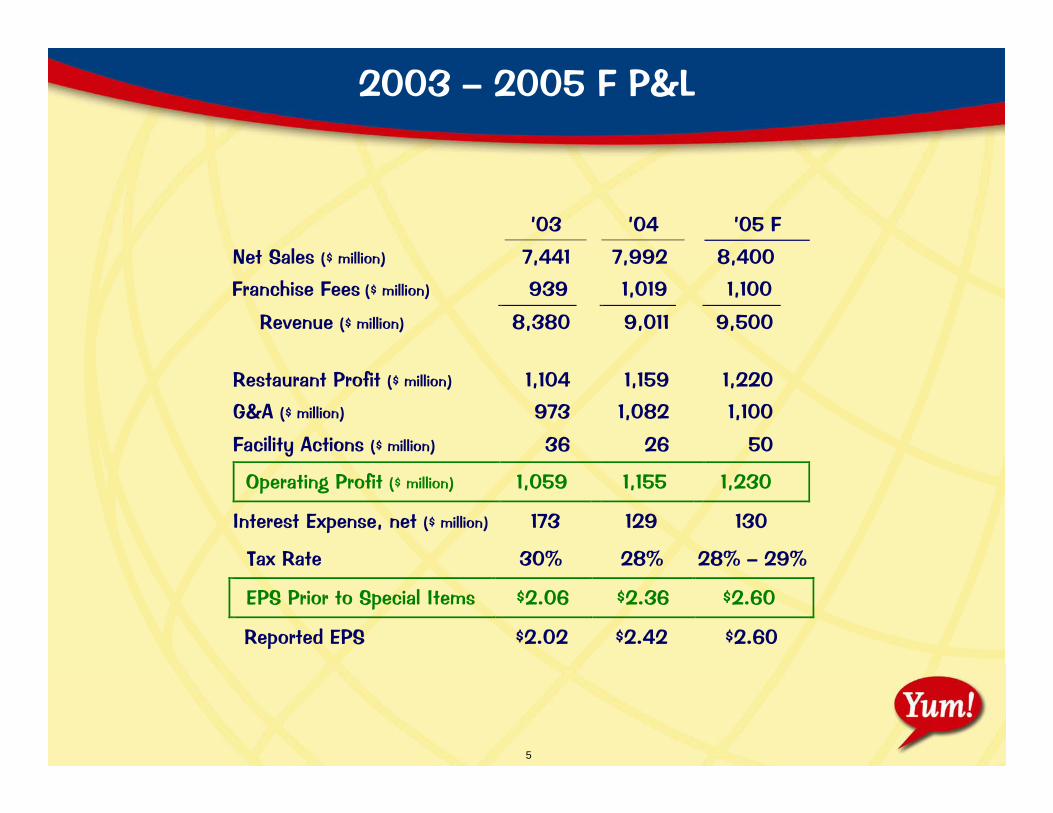

’03 ’04 ’05 F

Net Sales ($ million) 7,441 7,992 8,400

Franchise Fees ($ million) 939 1,019 1,100

Revenue ($ million) 8,380 9,011 9,500 Restaurant Profit ($ million) 1,104 1,159 1,220

G&A ($ million) 973 1,082 1,100

Facility Actions ($ million) 36 26 50

Operating Profit ($ million) 1,059 1,155 1,230

Interest Expense, net ($ million) 173 129 130

Tax Rate 30% 28% 28% – 29%

EPS Prior to Special Items $2.06 $2.36 $2.60

Reported EPS $2.02 $2.42 $2.60

2003 – 2005 F P&L

6

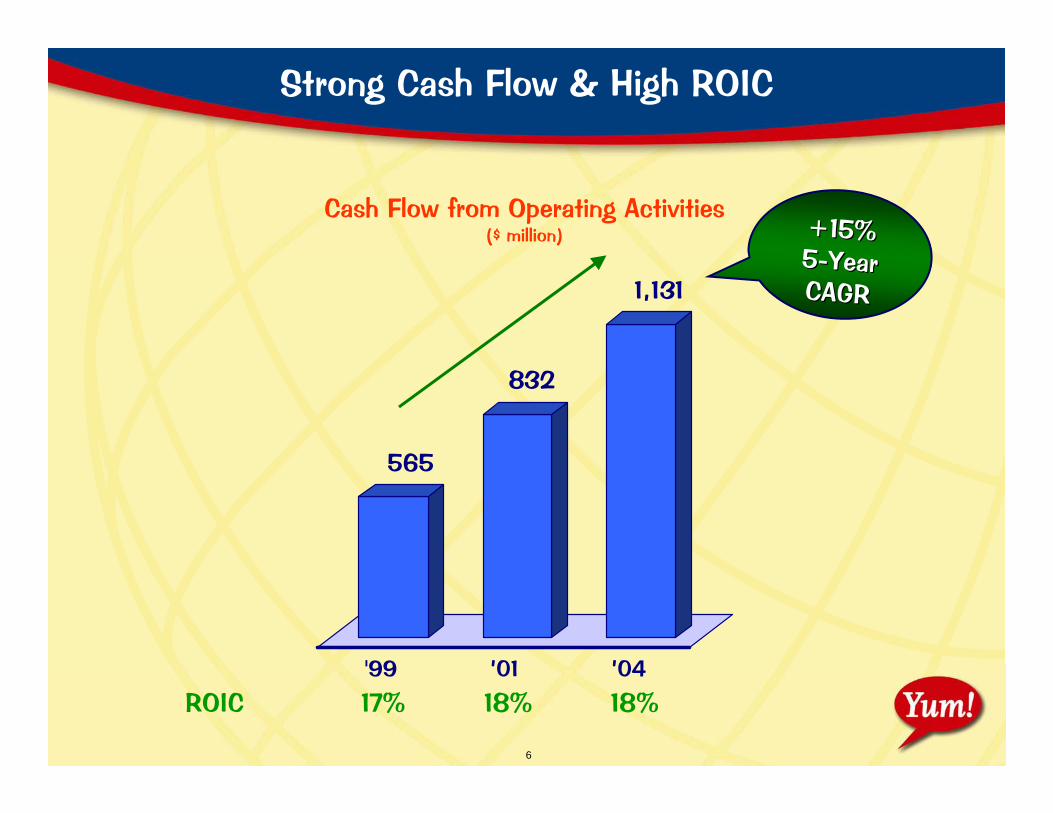

Strong Cash Flow & High ROIC

565

832

1,131

'99 ’01 ’04

Cash Flow from Operating Activities($ million)

ROIC 17% 18% 18%

+15% +15% 55--YearYearCAGRCAGR

7

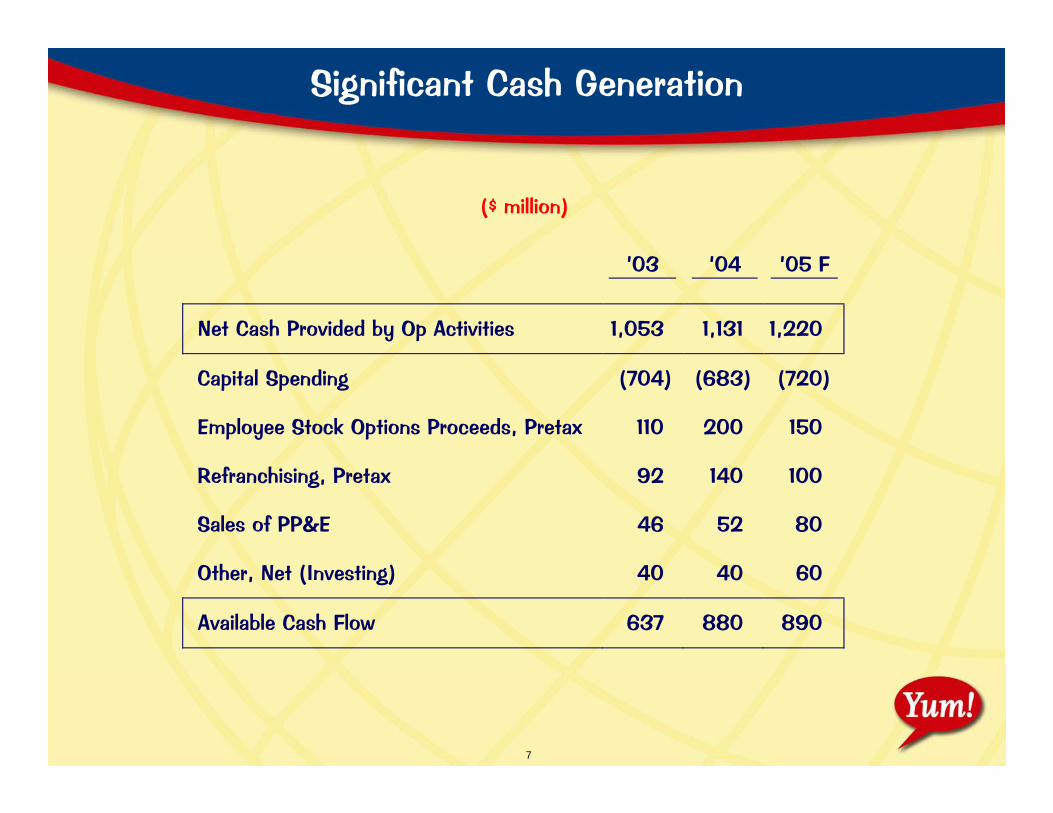

Significant Cash Generation

’03 ’04

’05 F

Net Cash Provided by Op Activities 1,053 1,131 1,220

Capital Spending (704) (683) (720)

Employee Stock Options Proceeds, Pretax 110 200 150

Refranchising, Pretax 92 140 100

Sales of PP&E 46 52 80

Other, Net (Investing) 40 40 60

Available Cash Flow 637 880 890

($ million)

8

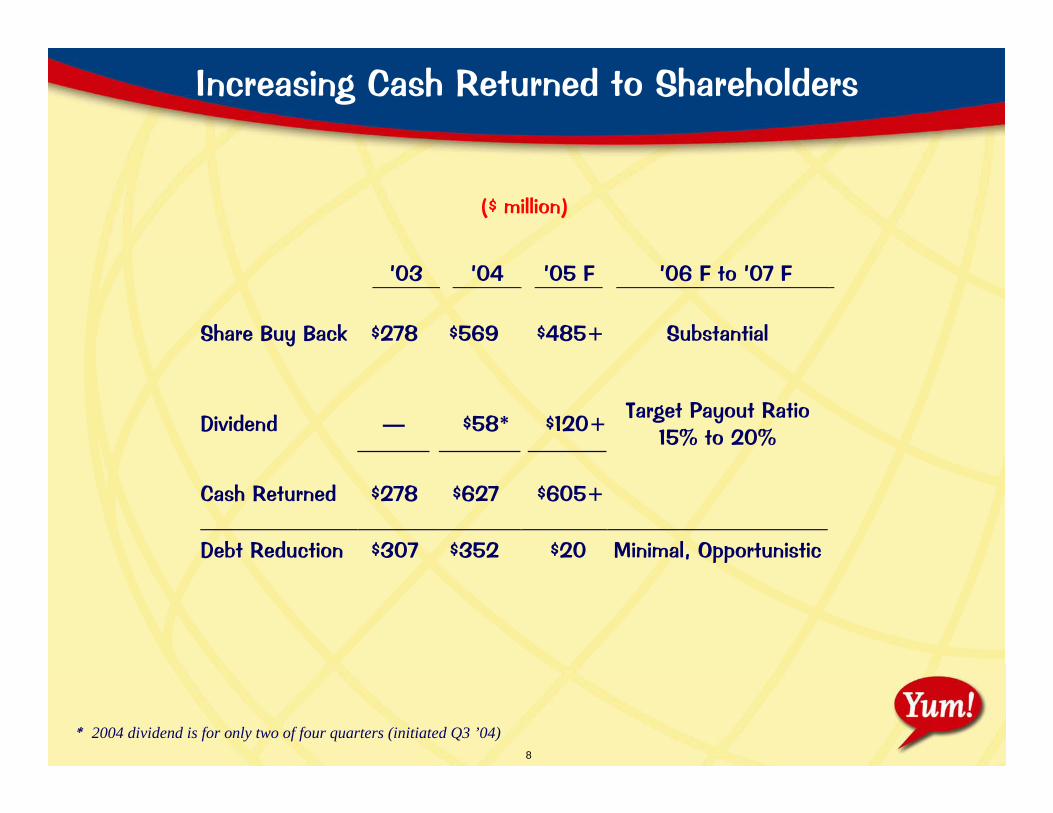

Increasing Cash Returned to Shareholders

’03 ’04 ’05 F ’06 F to ’07 F Share Buy Back $278 $569 $485+ Substantial

Dividend — $58* $120+ Target Payout Ratio 15% to 20%

Cash Returned $278 $627 $605+

Debt Reduction $307 $352 $20 Minimal, Opportunistic

* 2004 dividend is for only two of four quarters (initiated Q3 ’04)

($ million)

9

FOCUSED on High ROIC

Focus on franchise dominant new-unit expansion

Strategically refranchise markets, restaurants“Earn the Right to Own/Operate”

Continue to review capital-spending effectivenessDisciplined new-unit focusNUTS ABOUT CAPITAL

10

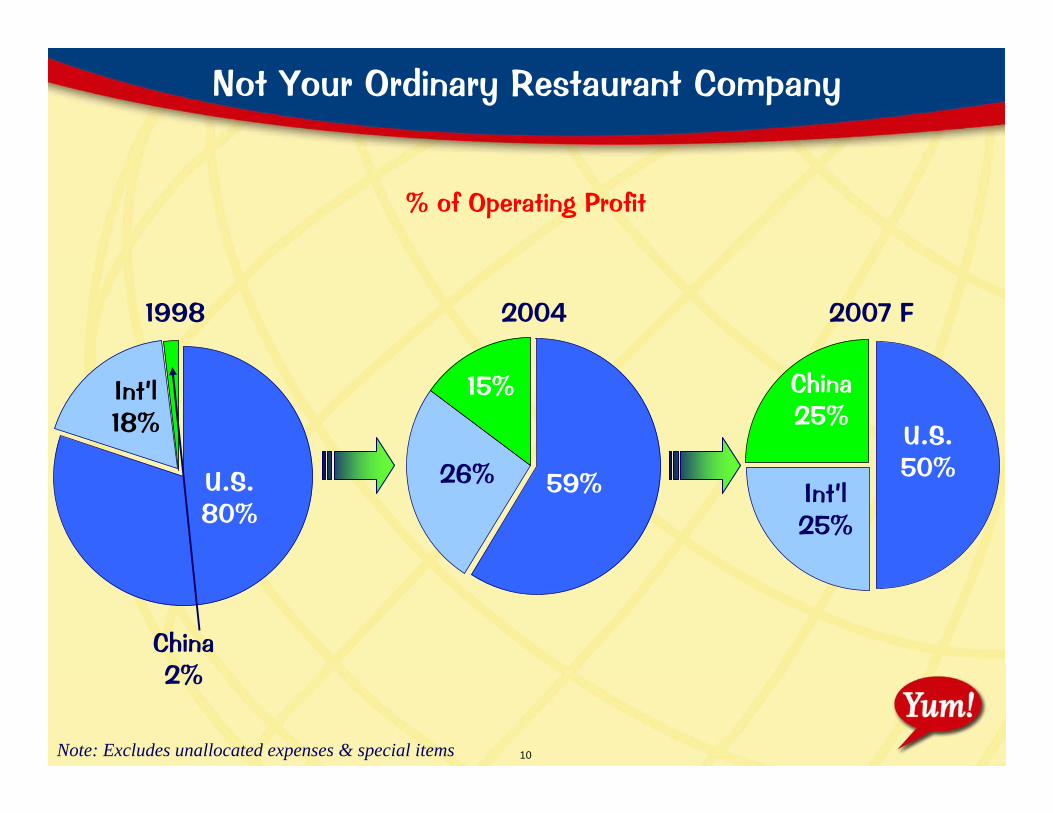

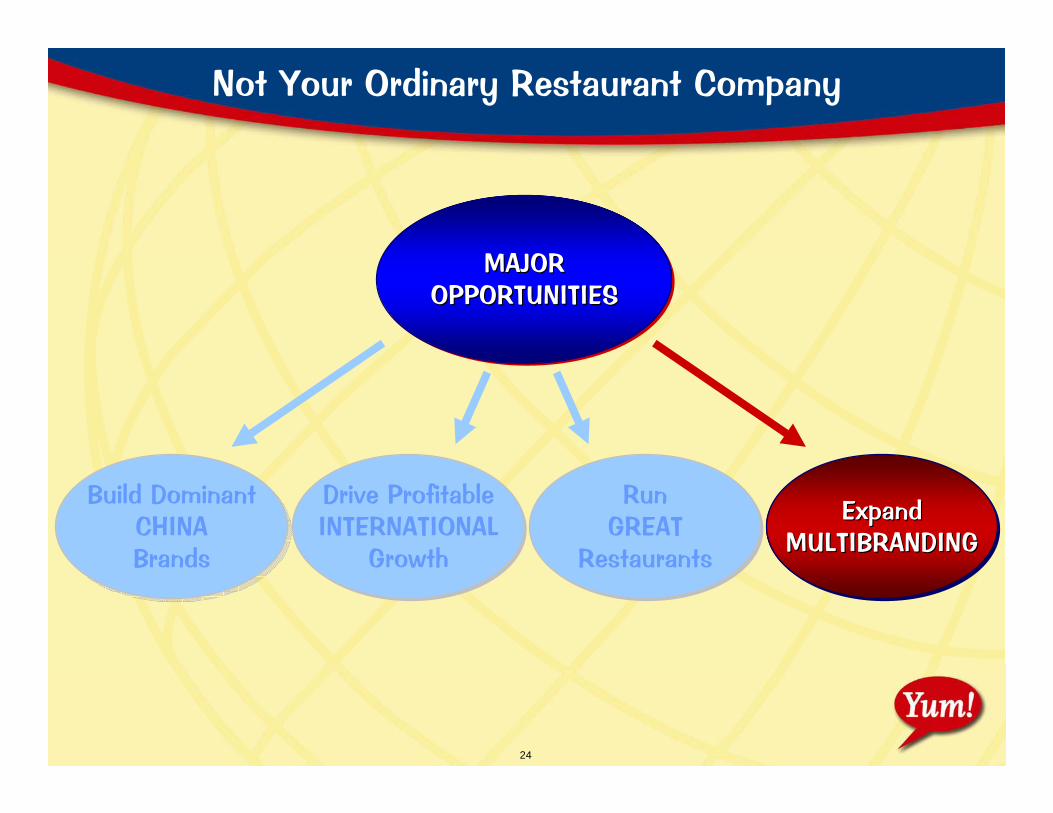

Not Your Ordinary Restaurant Company

1998 2004

Int’l18%

U.S.80%

26% 59%

% of Operating Profit

2007 F

Int’l25%

U.S.50%

China2%

15% China25%

Note: Excludes unallocated expenses & special items

11

Not Your Ordinary Restaurant Company

ExpandMULTIBRANDING

ExpandMULTIBRANDING

RunGREAT

Restaurants

RunGREAT

Restaurants

Drive ProfitableINTERNATIONAL

Growth

Drive ProfitableINTERNATIONAL

Growth

Build DominantCHINABrands

Build DominantBuild DominantCHINACHINABrandsBrands

MAJOROPPORTUNITIES

MAJORMAJOROPPORTUNITIESOPPORTUNITIES

12

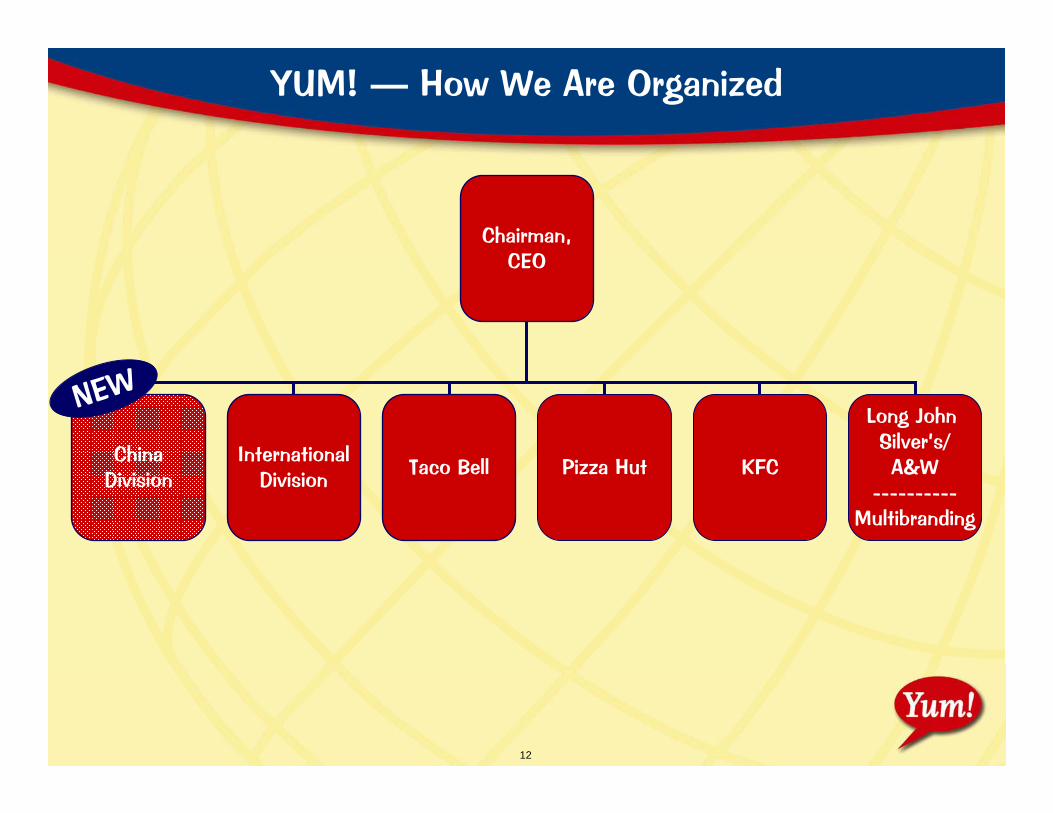

Chairman,CEO

ChinaDivision

InternationalDivision Taco Bell Pizza Hut KFC

Long John Silver’s/A&W

----------Multibranding

2004 F

YUM! — How We Are Organized

NEW

13

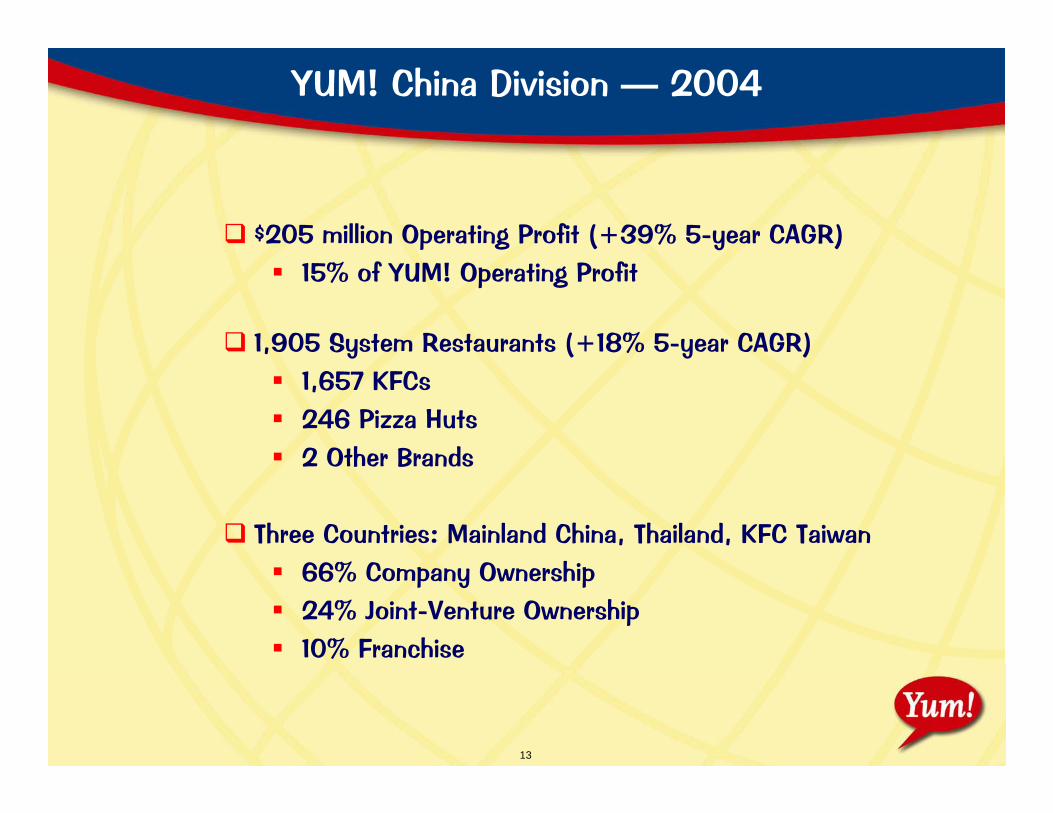

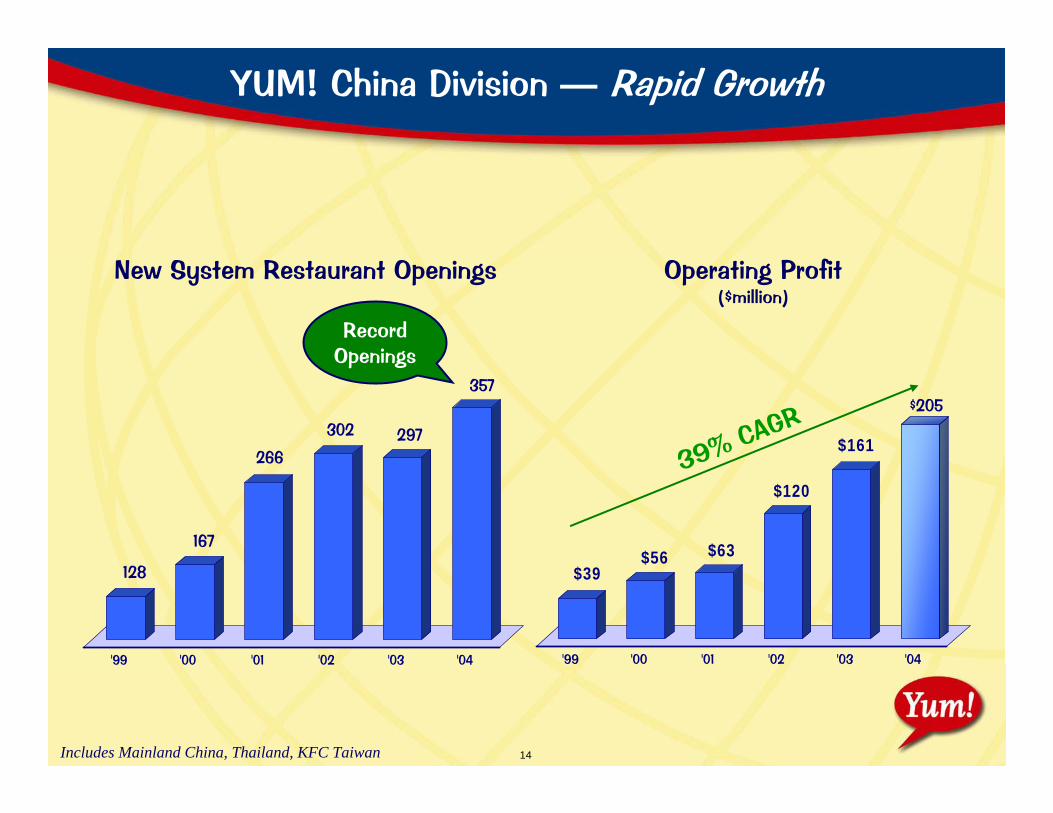

YUM! China Division — 2004

$205 million Operating Profit (+39% 5-year CAGR)15% of YUM! Operating Profit

1,905 System Restaurants (+18% 5-year CAGR)1,657 KFCs246 Pizza Huts2 Other Brands

Three Countries: Mainland China, Thailand, KFC Taiwan66% Company Ownership24% Joint-Venture Ownership10% Franchise

14

YUM! China Division — Rapid Growth

New System Restaurant Openings Operating Profit($million)

$39$56 $63

$120

$161

$205

'99 '00 '01 '02 '03 '04

128

167

266

302 297

357

'99 '00 '01 '02 '03 '04

39% CAGR

Includes Mainland China, Thailand, KFC Taiwan

Record Openings

15

Not Your Ordinary Restaurant Company

ExpandMULTIBRANDING

ExpandMULTIBRANDING

RunGREAT

Restaurants

RunGREAT

Restaurants

Drive ProfitableINTERNATIONAL

Growth

Drive ProfitableDrive ProfitableINTERNATIONALINTERNATIONAL

GrowthGrowth

Build DominantCHINABrands

Build DominantCHINABrands

MAJOROPPORTUNITIES

MAJORMAJOROPPORTUNITIESOPPORTUNITIES

16

Only Two True International Restaurant Players

$205 million(’04)

YUM! China Division4.

Approximately$50 million

or lessfor each brand

Burger King5.

Outback Steakhouse13.

Brinker12.

Darden11.

TGI Friday’s10.

Wendy’s9.

Starbuck’s8.

Domino’s7.

Pizza HutPizza Hut3.3.

6.

2.2.1.

Subway

$337 million$337 million(Int(Int’’l Division l Division ’’04, excludes China Division)04, excludes China Division)

KFCKFC$1.8 billionMcDonald’s

International Operating Profit Estimates

17

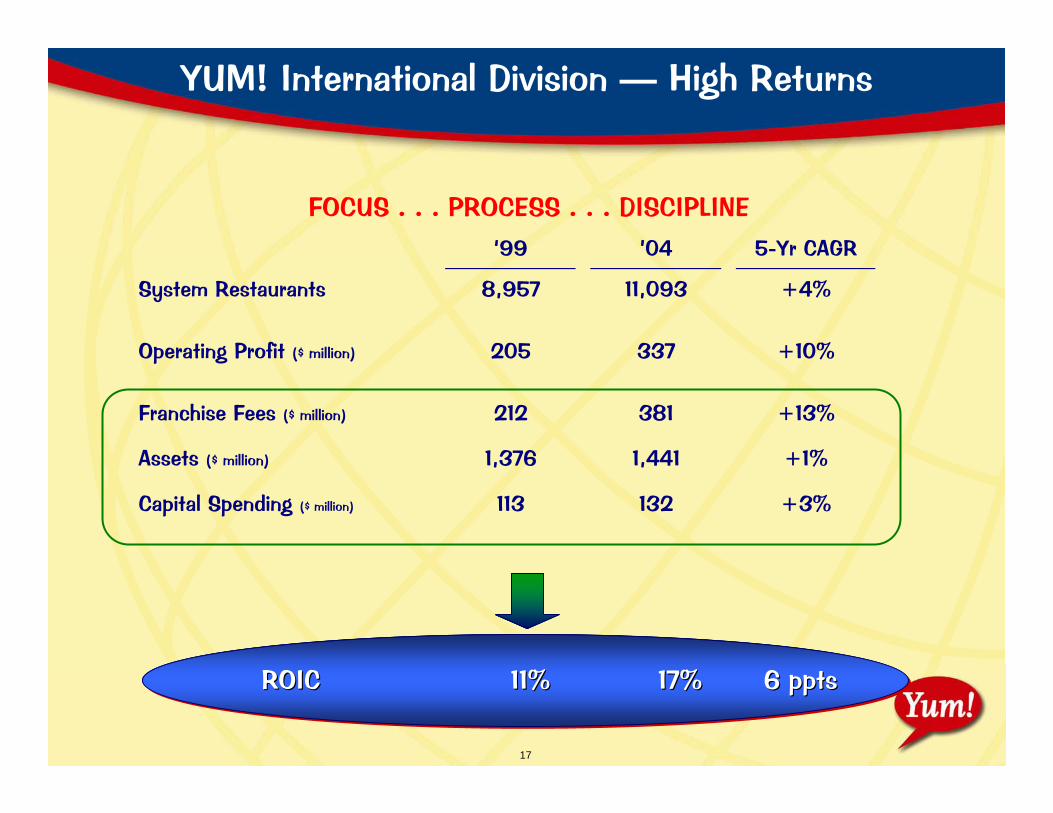

YUM! International Division — High Returns

‘99 ’04 5-Yr CAGR

System Restaurants 8,957 11,093 +4%

Operating Profit ($ million) 205 337 +10%

Franchise Fees ($ million) 212 381 +13%

Assets ($ million) 1,376 1,441 +1%

Capital Spending ($ million) 113 132 +3%

FOCUS . . . PROCESS . . . DISCIPLINE

ROIC 11% 17% 6 pptsROICROIC 11%11% 17%17% 6 6 pptsppts

18

Not Your Ordinary Restaurant Company

ExpandMULTIBRANDING

ExpandMULTIBRANDING

RunGREAT

Restaurants

RunRunGREATGREAT

RestaurantsRestaurants

Drive ProfitableINTERNATIONAL

Growth

Drive ProfitableINTERNATIONAL

Growth

Build DominantCHINABrands

Build DominantCHINABrands

MAJOROPPORTUNITIES

MAJORMAJOROPPORTUNITIESOPPORTUNITIES

19

GREAT

Run Great Restaurants

Execute with Urgency & Focus

. . . Steady Improvement

. . . Better this year

Poor(at spin-off)

Mediocre(last year)

Good

China

Malaysia

Taco Bell U.S.U.K.

Pizza Hut U.S.

KFC U.S.

Long John Silver’s U.S.

20

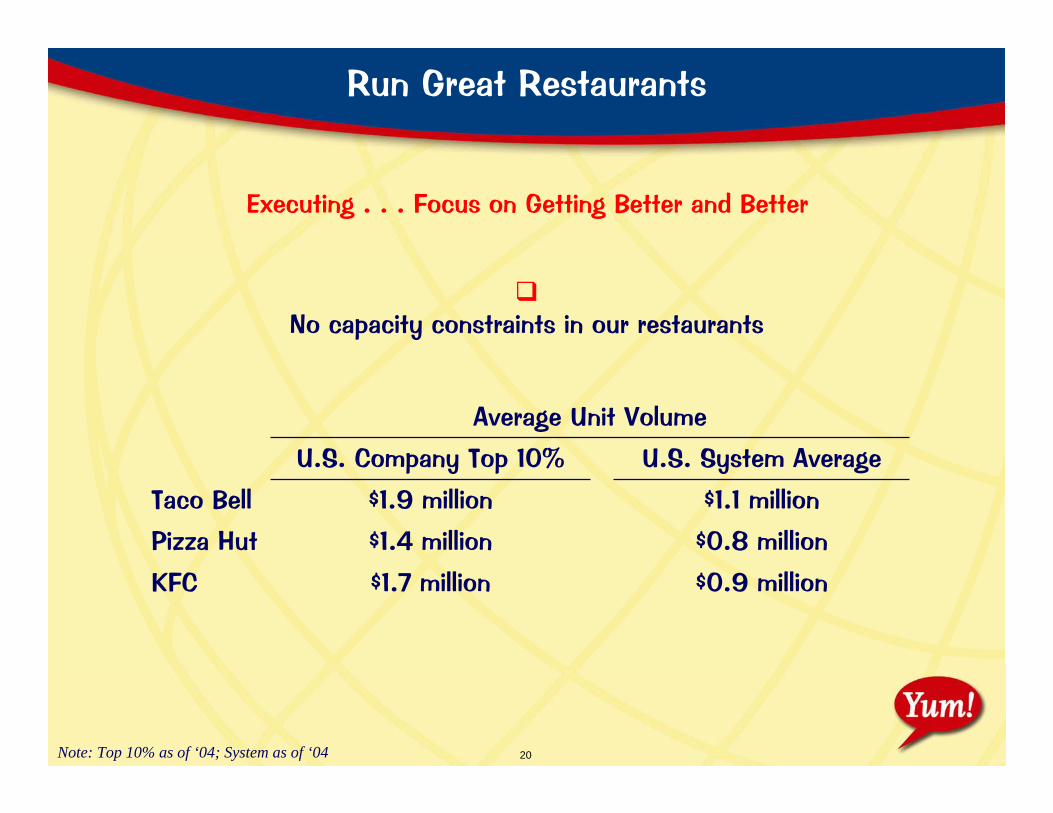

Run Great Restaurants

No capacity constraints in our restaurants

Average Unit Volume

$0.9 million$1.7 millionKFC

$0.8 million$1.4 millionPizza Hut

$1.1 million$1.9 millionTaco Bell

U.S. System AverageU.S. Company Top 10%

Executing . . . Focus on Getting Better and Better

Note: Top 10% as of ‘04; System as of ‘04

21

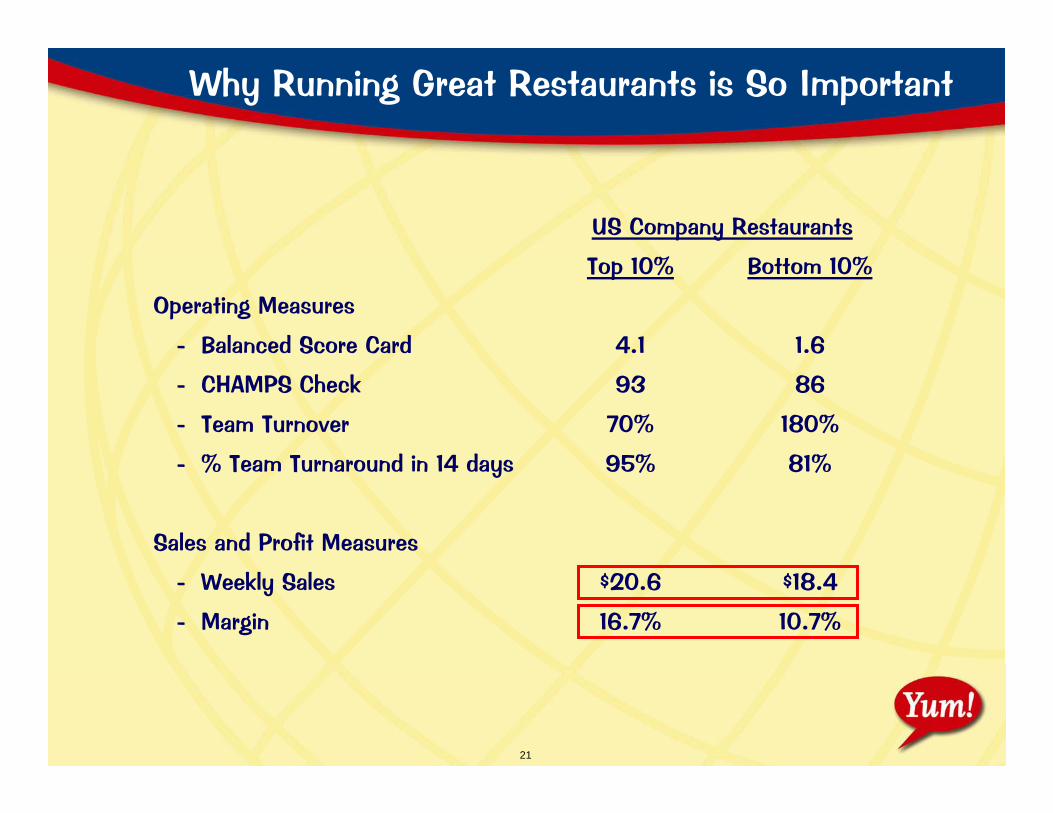

Why Running Great Restaurants is So Important

10.7%16.7%- Margin

$18.4$20.6- Weekly Sales

Sales and Profit Measures

81%95%- % Team Turnaround in 14 days

180%70%- Team Turnover

8693- CHAMPS Check

1.64.1- Balanced Score Card

Operating Measures

Bottom 10%Top 10%

US Company Restaurants

22

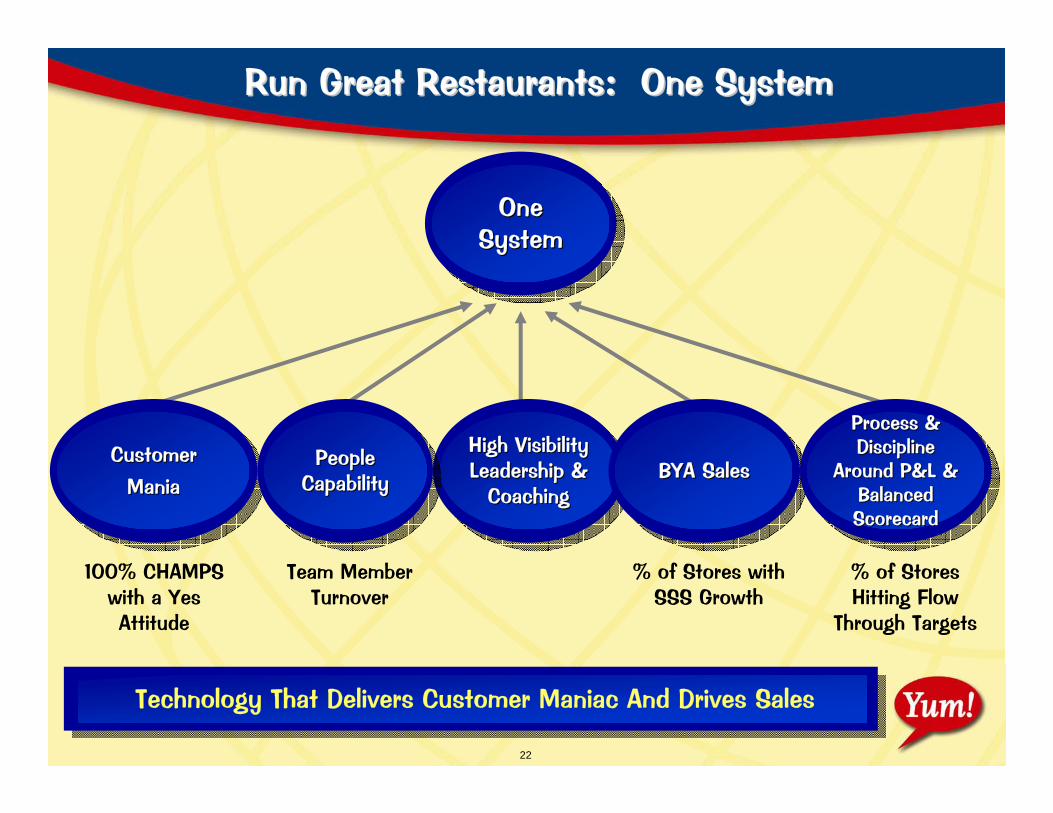

Technology That Delivers Customer Maniac And Drives Sales

Run Great Restaurants: One SystemRun Great Restaurants: One System

One One SystemSystem

Customer Customer Mania Mania

High Visibility High Visibility Leadership & Leadership &

CoachingCoachingBYA SalesBYA Sales

Process & Process & Discipline Discipline

Around P&L & Around P&L & Balanced Balanced ScorecardScorecard

People People CapabilityCapability

100% CHAMPS with a Yes Attitude

Team Member Turnover

% of Stores with SSS Growth

% of Stores Hitting Flow

Through Targets

23

Steady Improvement — 2004 U.S. Results

% Restaurants CHAMPS @ 100 58 50 45 % Pts. B/(W) Vs. ’03 9

Even

2

% Restaurants Positive SSS Growth 84 69 39 % Pts. B/(W) Vs. ’03 18

23

3

% Restaurants @ Flow-Thru Profits Vs. Target 67 64 67 % Pts. B/(W) Vs. ’03 17

14

17

Team Member Turnover % 108 100 115 % Pts. B/(W) Vs. ’03 9

2

23

Company results as of Period 13 ’04

24

Not Your Ordinary Restaurant Company

ExpandMULTIBRANDING

ExpandExpandMULTIBRANDINGMULTIBRANDING

RunGREAT

Restaurants

RunGREAT

Restaurants

Drive ProfitableINTERNATIONAL

Growth

Drive ProfitableINTERNATIONAL

Growth

Build DominantCHINABrands

Build DominantCHINABrands

MAJOROPPORTUNITIES

MAJORMAJOROPPORTUNITIESOPPORTUNITIES

25

Portfolio of Category-Leading Brands

1,2005,4506,3065,030US System Restaurants (Q4 ’04 –exclude licensed units)

6528967941,069System Average Unit Volume(’04, $ thousand)

35%46%16%64%U.S. Category Market Share*

Four Category Leaders

*Source: The NPD Group, Inc.; NPD Food World: Crest for 2004

26

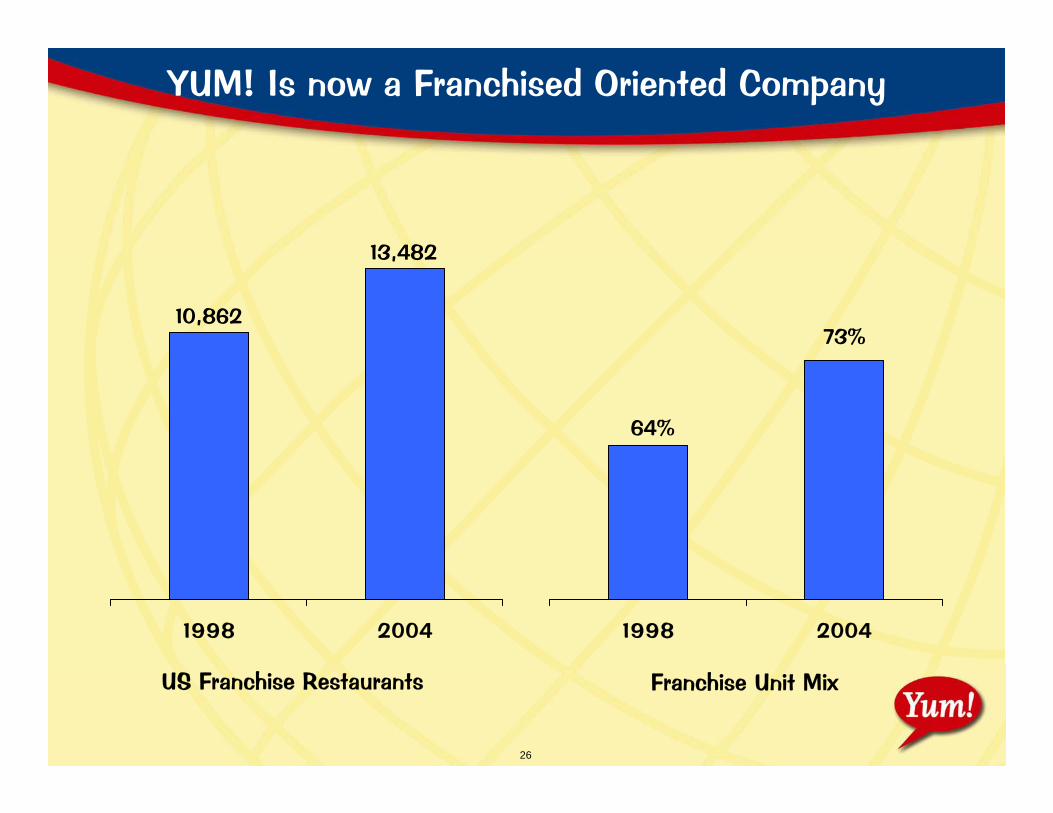

YUM! Is now a Franchised Oriented Company

1998 20041998 2004

Franchise Unit MixUS Franchise Restaurants

13,482

64%

73%10,862

27

Summary

Consistent Financial Results

Strong Cash Flow and Returns

Not Your Ordinary Restaurant CompanyChina, International, Run Great Restaurants, Multibranding

Embrace Franchise Development and Growth