Embed Size (px)

Citation preview

Bringing Smart Policies to Life

Financial Inclusion: A Snapshot

Financial Inclusion: importance, benefits and

issues

• Financial inclusion, providing access to financial services for all has gain prominence

in the past few years; it is broader than just providing access to credit.

• World Bank, CGAP, DFID, AFI and others have taken serious look at the issue.

CGAP’s ―Access to Finance 2009‖ presents indicators of access to savings, credit,

and payment services in banks and in regulated nonbank financial institutions.

• Measuring access— getting more and better data on regulated financial institutions is

a first major step. Seventy percent of the 139 countries being surveyed rely on

savings accounts data.

• Increasing access to saving and payment services—policies successful only if

financial institutions are on board.

• Increasing access to credit—consumer protection is key.

• Extending the reach of financial services— new technologies and simplified branch

regulations hold promise

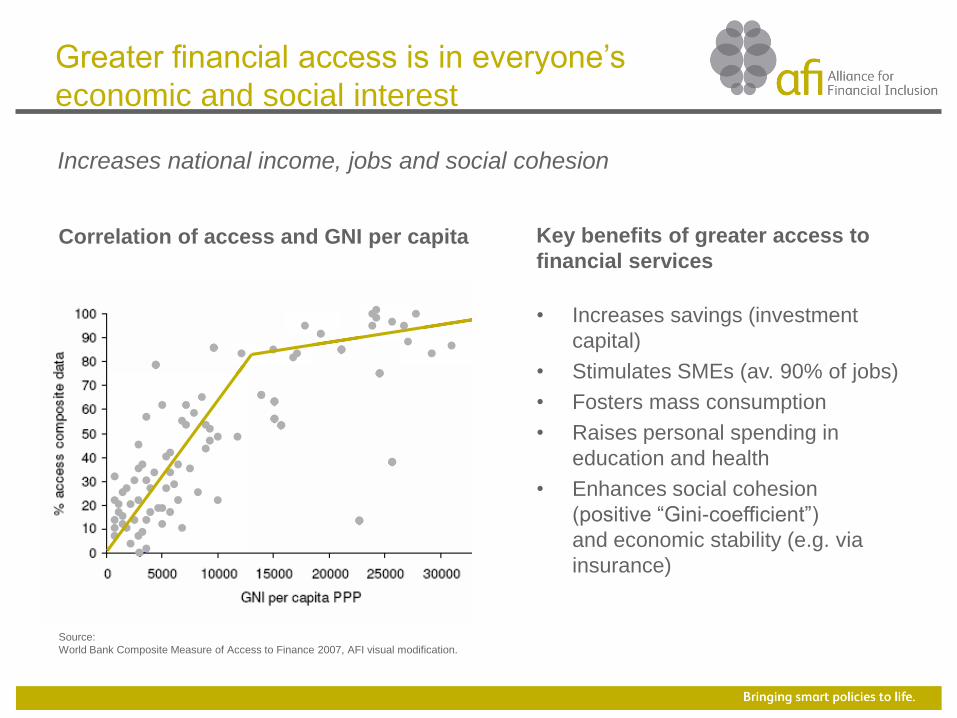

Greater financial access is in everyone’s

economic and social interest

Increases national income, jobs and social cohesion

Correlation of access and GNI per capita

• Increases savings (investment

capital)

• Stimulates SMEs (av. 90% of jobs)

• Fosters mass consumption

• Raises personal spending in

education and health

• Enhances social cohesion

(positive ―Gini-coefficient‖)

and economic stability (e.g. via

insurance)

Key benefits of greater access to

financial services

Source:

World Bank Composite Measure of Access to Finance 2007, AFI visual modification.

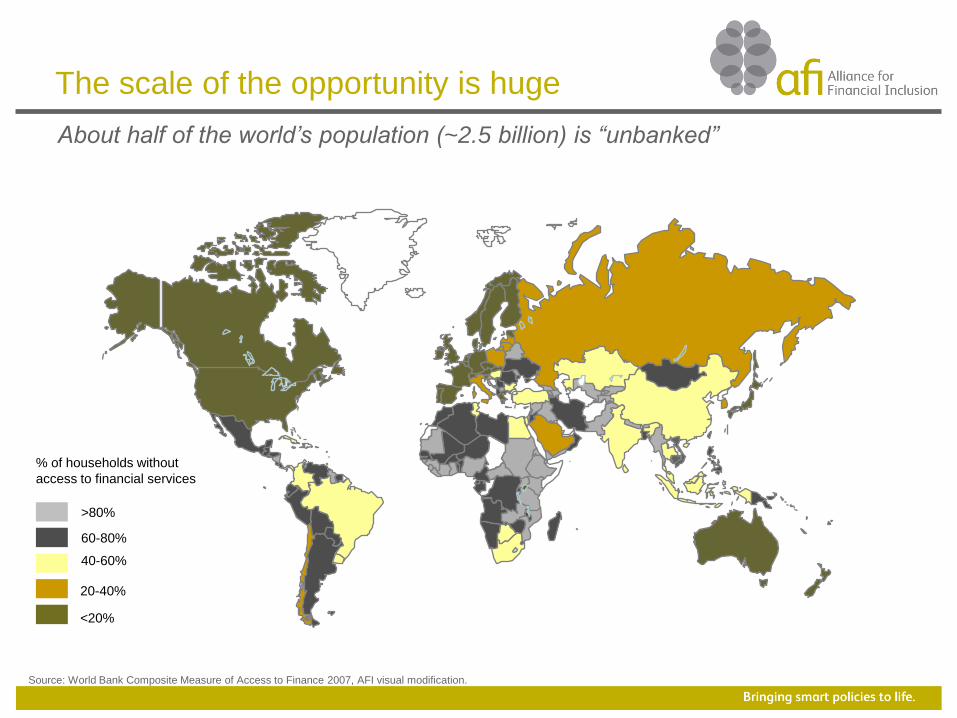

The scale of the opportunity is huge

About half of the world’s population (~2.5 billion) is “unbanked”

<20%

20-40%

40-60%

60-80%

>80%

% of households without

access to financial services

Source: World Bank Composite Measure of Access to Finance 2007, AFI visual modification.

• AFI is a global network of policymakers in developing countries.

• We provide our members with the tools and resources to share, developand implement their knowledge of cutting-edge financial inclusion policies that work.

• Established 2008, our goal is to enable an extra 50 million people living on less than $2 a day to have access to savings accounts, insurance and other formal financial services by 2012.

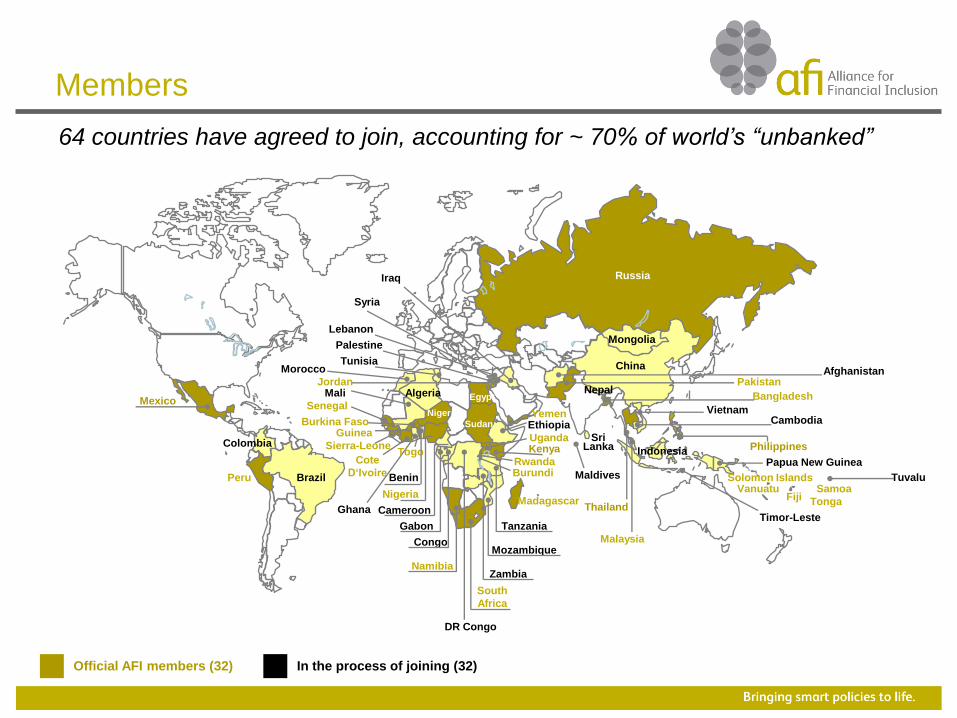

• So far, policymakers from 64 developing countries have agreed to become members of AFI, representing more than 70% of the world’s ―unbanked‖.

AFI at a glance

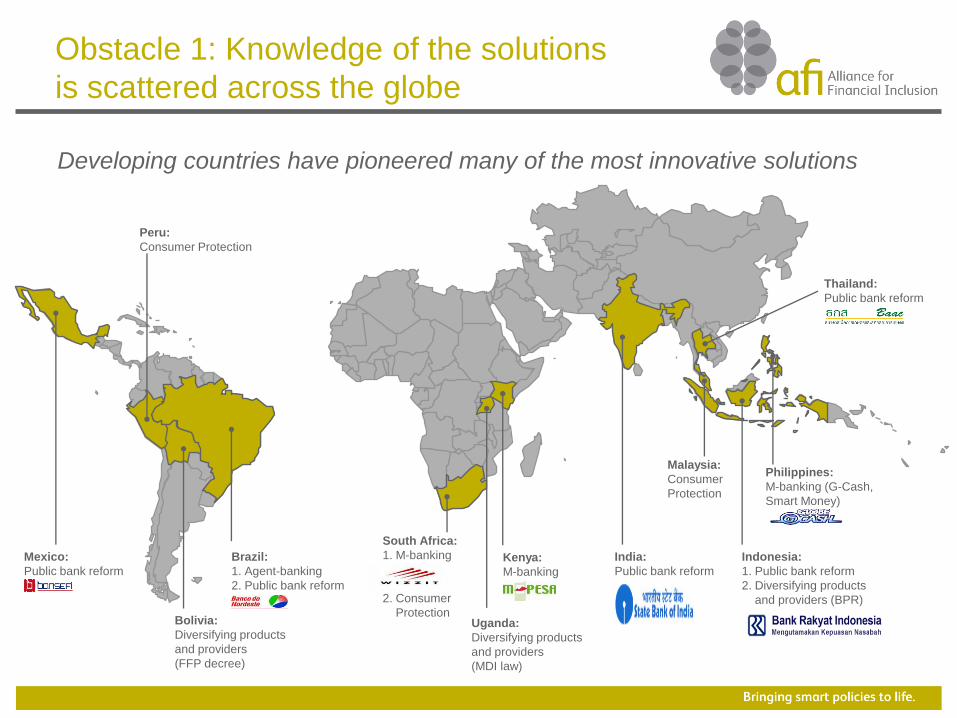

Obstacle 1: Knowledge of the solutions

is scattered across the globe

Developing countries have pioneered many of the most innovative solutions

Indonesia:

1. Public bank reform

2. Diversifying products

and providers (BPR)

India:

Public bank reformKenya:

M-banking

Uganda:

Diversifying products

and providers

(MDI law)

South Africa:

1. M-banking

2. Consumer

Protection

Mexico:

Public bank reform

Bolivia:

Diversifying products

and providers

(FFP decree)

Brazil:

1. Agent-banking

2. Public bank reform

Philippines:

M-banking (G-Cash,

Smart Money)

Peru:

Consumer Protection

Malaysia:

Consumer

Protection

Thailand:

Public bank reform

Obstacle 2: Policymakers face a

bewildering choice of partners

Nearly 200 financial inclusion players: who to use and when?

What we do

• Enable policymakers in developing countries to share and develop

their knowledge of cutting-edge policies that deliver tangible results

– Online and face-to-face meetings (regional and global)

– All learnings captured centrally so others can benefit

– Focused on evidence-based policy area (currently six)

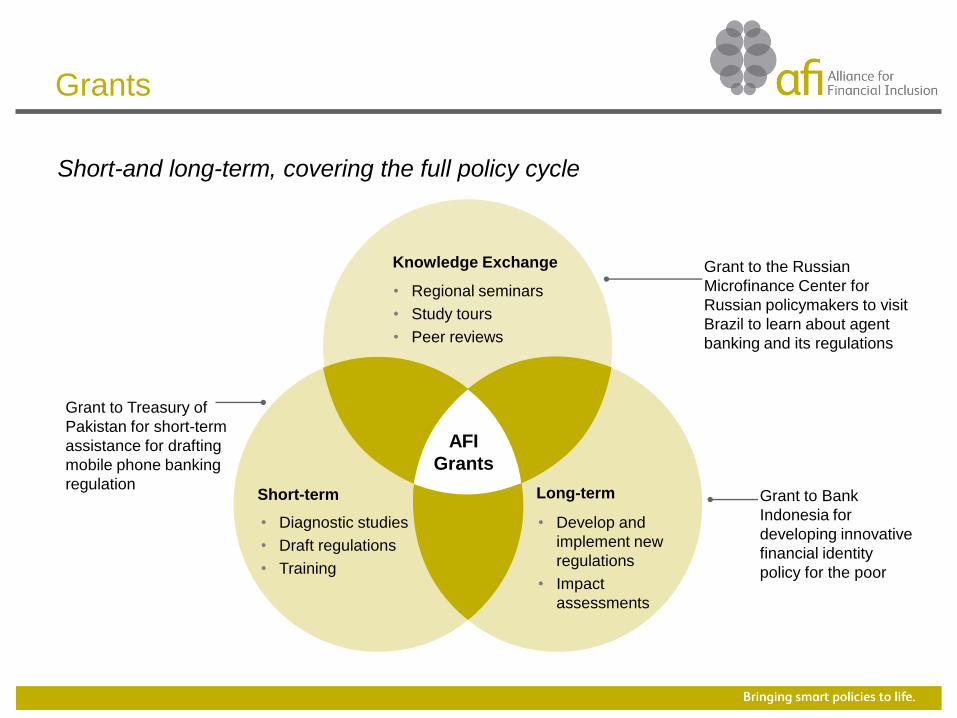

• Provide policymakers with grants to develop and implement their

chosen solutions

– Short-term grants: e.g. diagnostic studies, drafting regulations

– Longer-term grants: e.g. implementation and impact assessment

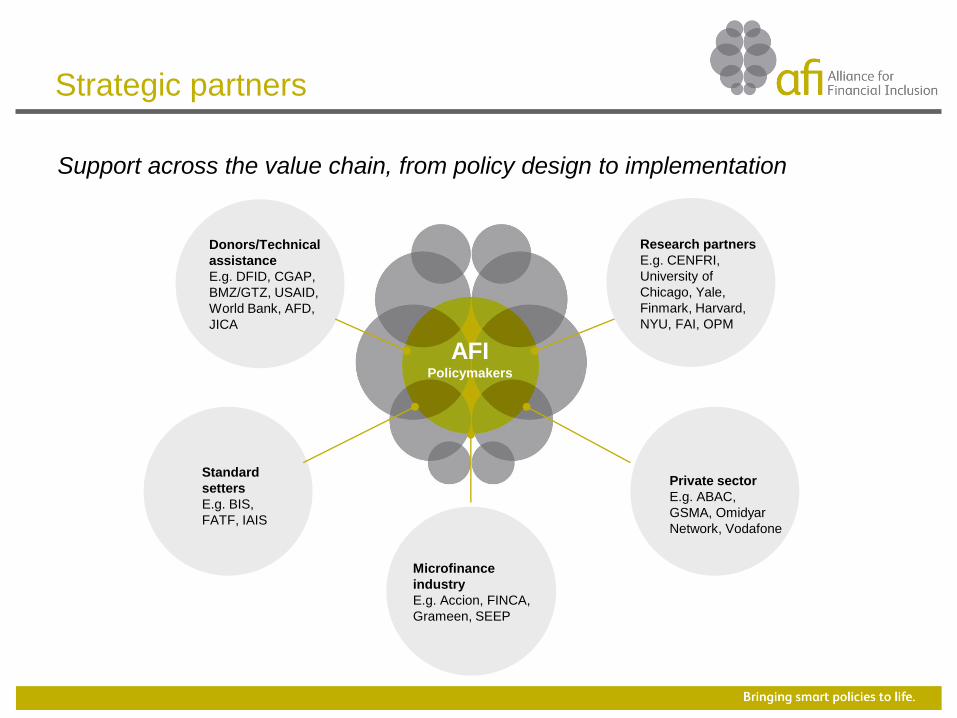

• Connect policymakers with the right partners across the value chain

– From research institutes (e.g. NYU) and technical experts (e.g. CGAP)

to funders (e.g. World Bank) and the private sector (e.g. GSMA)

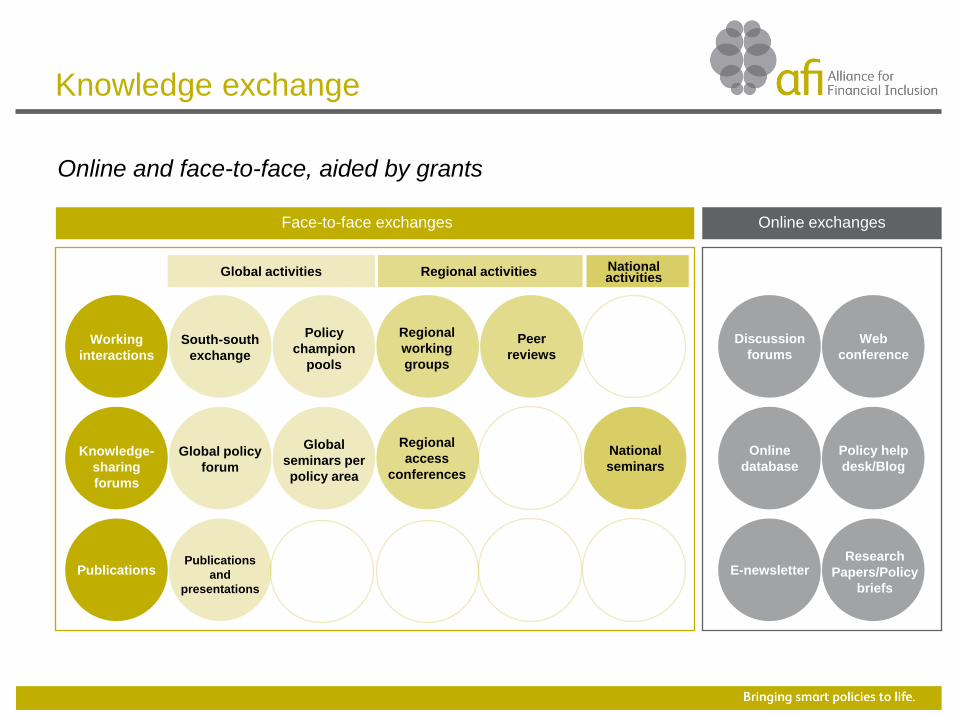

Knowledge exchange

Online and face-to-face, aided by grants

South-south

exchange

Policy

champion

pools

Regional

working

groups

Peer

reviewsWorking

interactions

Discussion

forums

Web

conference

Global policy

forum

Global

seminars per

policy area

Regional

access

conferences

Knowledge-

sharing

forums

Online

database

Policy help

desk/Blog

National

seminars

Publications

and

presentations

Publications E-newsletterResearch

Papers/Policy

briefs

Face-to-face exchanges Online exchanges

Global activities Regional activities National activities

Grants

Short-and long-term, covering the full policy cycle

AFI

Grants

Long-termShort-term

• Diagnostic studies

• Draft regulations

• Training

• Develop and

implement new

regulations

• Impact

assessments

• Regional seminars

• Study tours

• Peer reviews

Grant to the Russian

Microfinance Center for

Russian policymakers to visit

Brazil to learn about agent

banking and its regulations

Grant to Bank

Indonesia for

developing innovative

financial identity

policy for the poor

Grant to Treasury of

Pakistan for short-term

assistance for drafting

mobile phone banking

regulation

Knowledge Exchange

Strategic partners

Support across the value chain, from policy design to implementation

AFIPolicymakers

Donors/Technical

assistance

E.g. DFID, CGAP,

BMZ/GTZ, USAID,

World Bank, AFD,

JICA

Standard

setters

E.g. BIS,

FATF, IAIS

Private sector

E.g. ABAC,

GSMA, Omidyar

Network, Vodafone

Research partners

E.g. CENFRI,

University of

Chicago, Yale,

Finmark, Harvard,

NYU, FAI, OPM

Microfinance

industry

E.g. Accion, FINCA,

Grameen, SEEP

Maldives

Russia

Mongolia

China

IndonesiaPapua New Guinea

Nepal

Sri Lanka

Bangladesh

BrazilPeru

Colombia

Mexico

South

Africa

Namibia

Nigeria

Cameroon

Gabon

Congo

DR Congo

Egypt

Mozambique

Zambia

Tanzania

UgandaKenya

Madagascar

Mali

Senegal

GuineaBurkina Faso

Togo

BurundiRwanda

Ethiopia

VietnamCambodia

Philippines

Malaysia

Thailand

Pakistan

Official AFI members (32)

Benin

Timor-Leste

Palestine

Jordan

Lebanon

Syria

Iraq

Morocco

Algeria

Tunisia

SudanYemenNiger

Cote

D‘Ivoire

Afghanistan

Ghana

Sierra-Leone

Members

64 countries have agreed to join, accounting for ~ 70% of world’s “unbanked”

Fiji

TuvaluSamoaVanuatu

Tonga

Solomon Islands

In the process of joining (32)

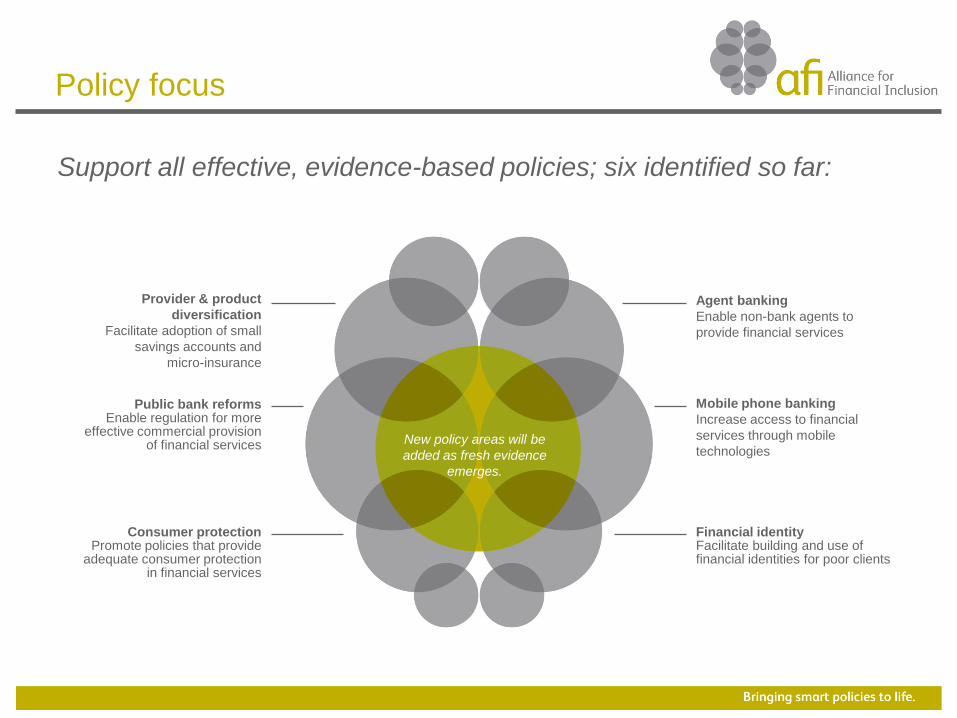

Policy focus

Support all effective, evidence-based policies; six identified so far:

Agent banking

Enable non-bank agents to

provide financial services

Mobile phone banking

Increase access to financial

services through mobile

technologies

Financial identityFacilitate building and use of financial identities for poor clients

Provider & product

diversification

Facilitate adoption of small

savings accounts and

micro-insurance

Public bank reformsEnable regulation for more

effective commercial provision of financial services

Consumer protectionPromote policies that provide

adequate consumer protection in financial services

New policy areas will be

added as fresh evidence

emerges.

Financial Inclusion and Financial Stability

• In time of financial crises, it is crucial to maintain the goal of increasing access to

appropriate financial services for the unbanked to alleviate poverty and achieve

strong growth, and to avoid a backlash against financial inclusion.

• Financial inclusion poses risks, but these are hardly systemic in nature. Empirical

evidence suggests poor savers and borrowers tend to maintain solid financial

behavior in circumstances of financial crisis, keeping deposits in a safe place and

paying back their loans

• The bottom end of the financial market is characterized by large numbers of

vulnerable clients who own limited balances and transact small volumes: may raise

more concerns regarding reputational risks for the central bank and consumer

protection than for financial instability.

• Risks prevalent at the institutional level are manageable with prudential tools and

more effective customer protection.

• Financial inclusion delivers dynamic benefits that enhance financial stability over time

through a deeper and more diversified financial system.

Kenya – Mobile Payment

Solution from other countries:

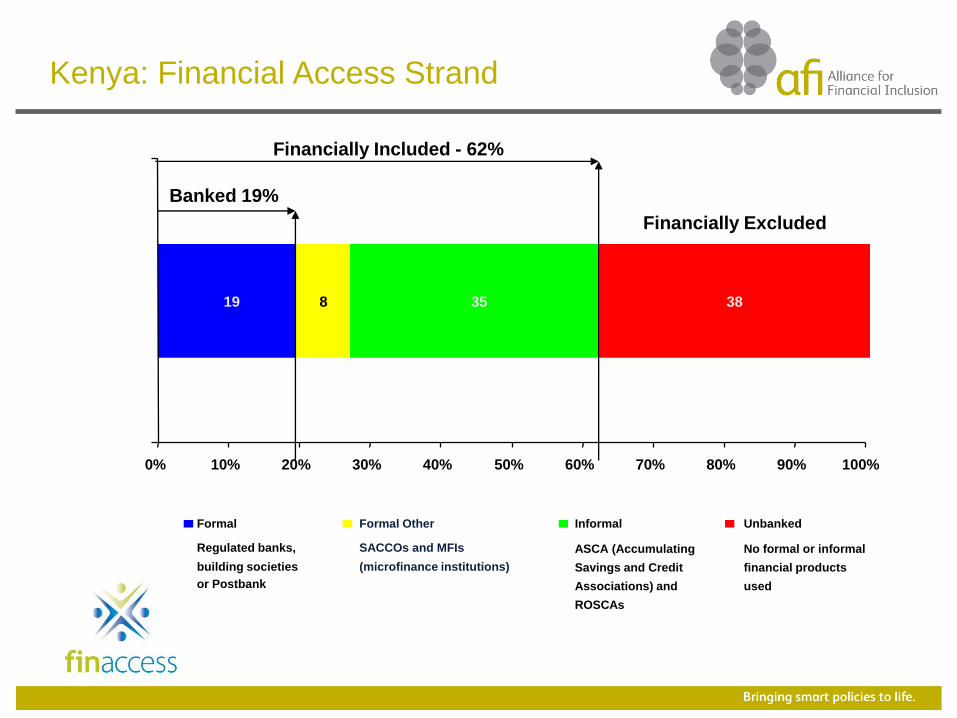

Kenya: Financial Access Strand

19 8 35 38

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Formal

Regulated banks,

building societies

or Postbank

Formal Other

SACCOs and MFIs

(microfinance institutions)

Informal

ASCA (Accumulating

Savings and Credit

Associations) and

ROSCAs

Unbanked

No formal or informal

financial products

used

Financially Included - 62%

Financially Excluded

Banked 19%

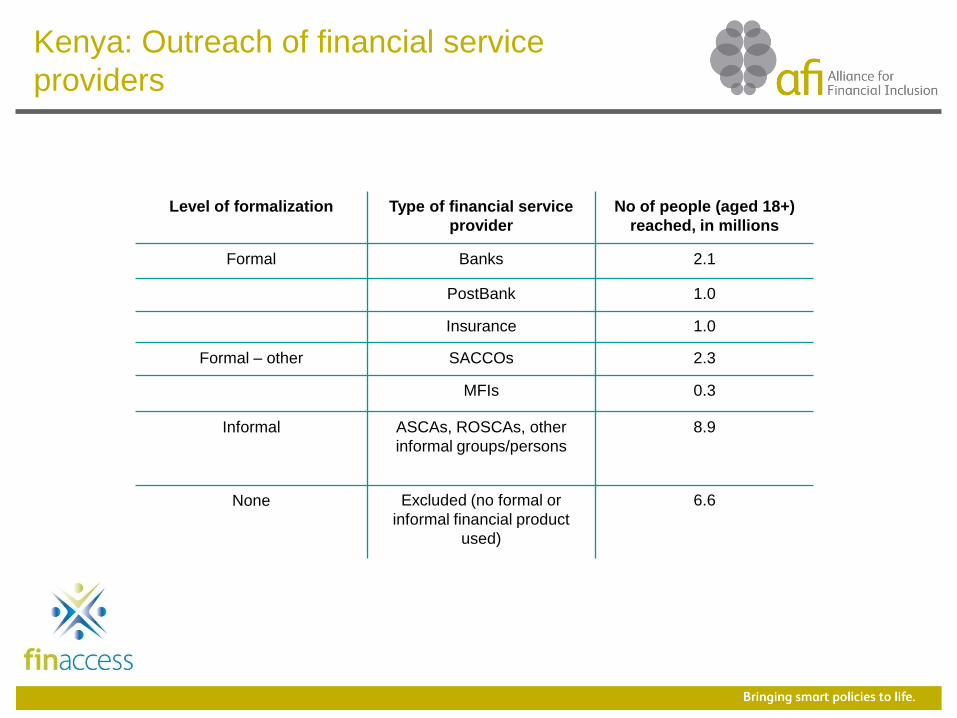

Kenya: Outreach of financial service

providers

Level of formalization Type of financial service

provider

No of people (aged 18+)

reached, in millions

Formal Banks 2.1

PostBank 1.0

Insurance 1.0

Formal – other SACCOs 2.3

MFIs 0.3

Informal ASCAs, ROSCAs, other

informal groups/persons

8.9

None Excluded (no formal or

informal financial product

used)

6.6

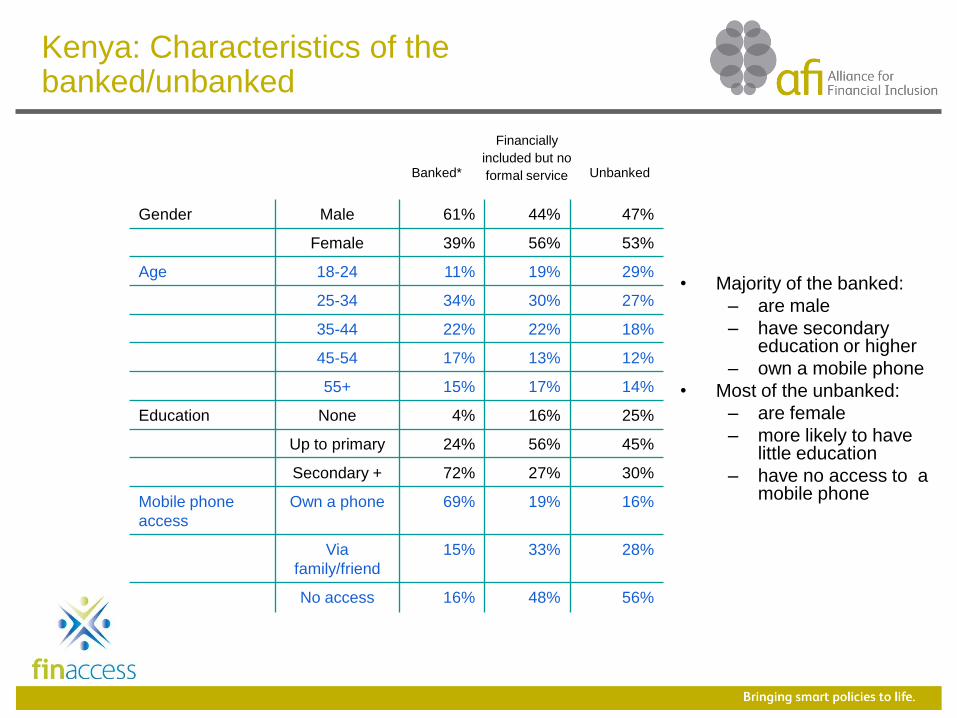

Kenya: Characteristics of the banked/unbanked

• Majority of the banked:

– are male

– have secondary education or higher

– own a mobile phone

• Most of the unbanked:

– are female

– more likely to have little education

– have no access to a mobile phone

Gender Male 61% 44% 47%

Female 39% 56% 53%

Age 18-24 11% 19% 29%

25-34 34% 30% 27%

35-44 22% 22% 18%

45-54 17% 13% 12%

55+ 15% 17% 14%

Education None 4% 16% 25%

Up to primary 24% 56% 45%

Secondary + 72% 27% 30%

Mobile phone

access

Own a phone 69% 19% 16%

Via

family/friend

15% 33% 28%

No access 16% 48% 56%

Banked*

Financially

included but no

formal service Unbanked

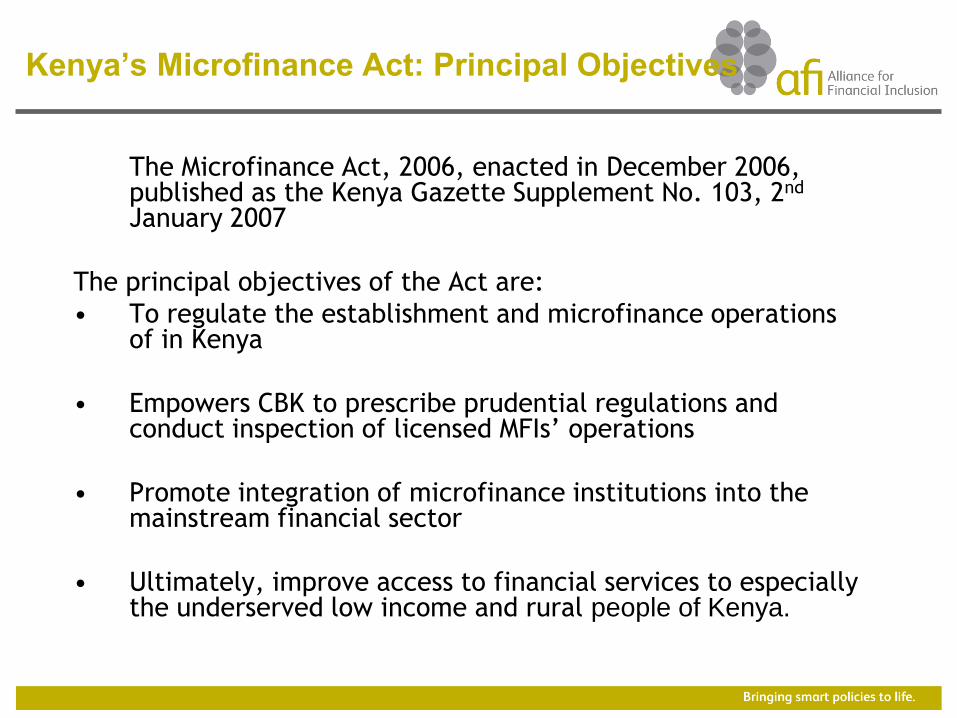

The Microfinance Act, 2006, enacted in December 2006, published as the Kenya Gazette Supplement No. 103, 2nd

January 2007

The principal objectives of the Act are:

• To regulate the establishment and microfinance operations of in Kenya

• Empowers CBK to prescribe prudential regulations and conduct inspection of licensed MFIs’ operations

• Promote integration of microfinance institutions into the mainstream financial sector

• Ultimately, improve access to financial services to especially the underserved low income and rural people of Kenya.

Kenya’s Microfinance Act: Principal Objectives

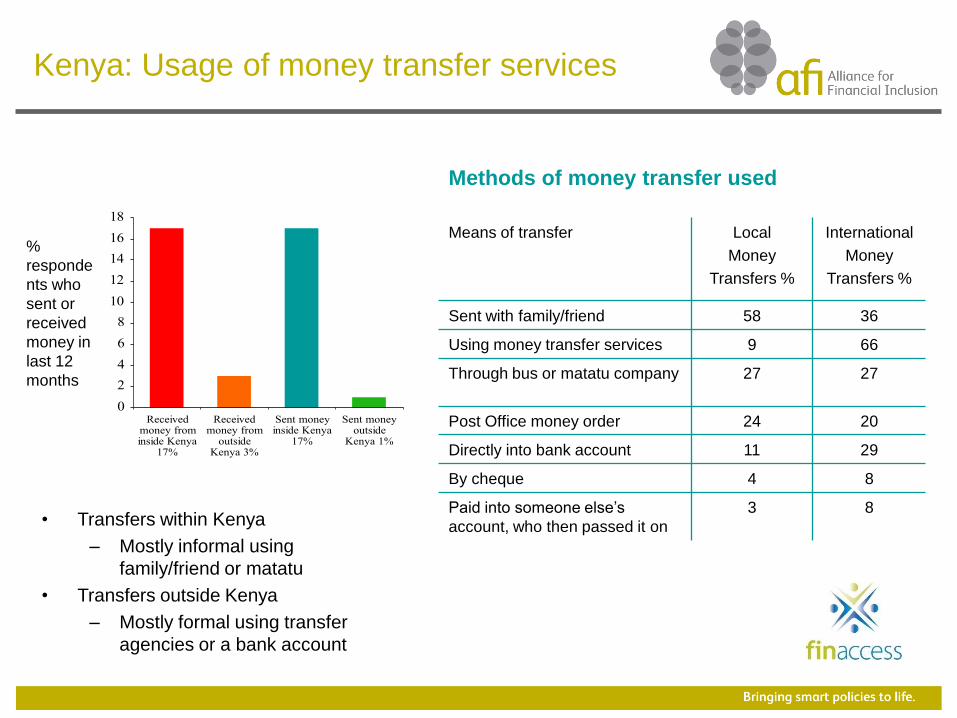

Kenya: Usage of money transfer services

• Transfers within Kenya

– Mostly informal using

family/friend or matatu

• Transfers outside Kenya

– Mostly formal using transfer

agencies or a bank account

Means of transfer Local

Money

Transfers %

International

Money

Transfers %

Sent with family/friend 58 36

Using money transfer services 9 66

Through bus or matatu company 27 27

Post Office money order 24 20

Directly into bank account 11 29

By cheque 4 8

Paid into someone else’s

account, who then passed it on

3 8

0

2

4

6

8

10

12

14

16

18

Receivedmoney frominside Kenya

17%

Receivedmoney from

outsideKenya 3%

Sent moneyinside Kenya

17%

Sent moneyoutside

Kenya 1%

Methods of money transfer used

%

responde

nts who

sent or

received

money in

last 12

months

23%

19%

27%

35%

33%

38%8%

18%

0% 20% 40% 60% 80% 100%

2009

2006

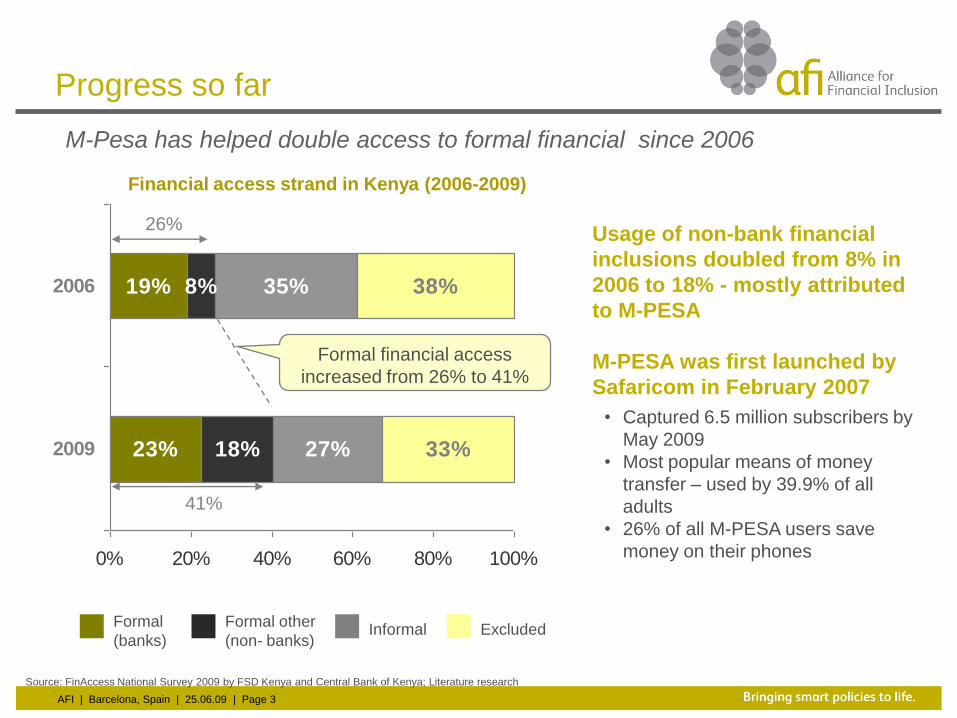

AFI | Barcelona, Spain | 25.06.09 | Page 3

Progress so far

Formal financial access

increased from 26% to 41%

Financial access strand in Kenya (2006-2009)

Source: FinAccess National Survey 2009 by FSD Kenya and Central Bank of Kenya; Literature research

41%

26%

Formal

(banks)

Formal other

(non- banks)Informal Excluded

M-Pesa has helped double access to formal financial since 2006

Usage of non-bank financial

inclusions doubled from 8% in

2006 to 18% - mostly attributed

to M-PESA

M-PESA was first launched by

Safaricom in February 2007

• Captured 6.5 million subscribers by

May 2009

• Most popular means of money

transfer – used by 39.9% of all

adults

• 26% of all M-PESA users save

money on their phones

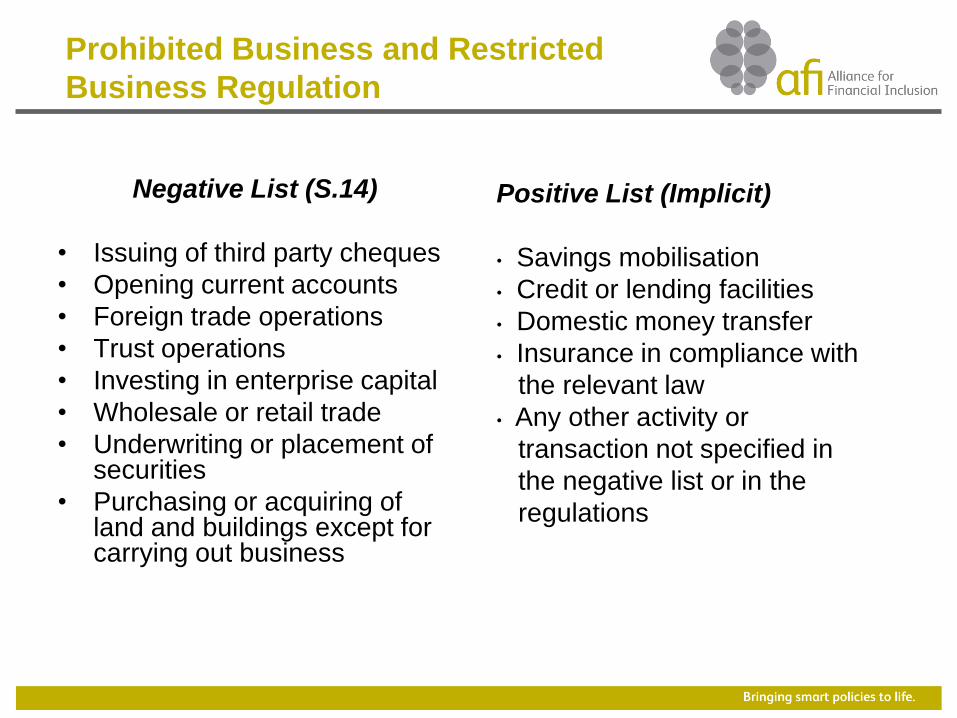

Negative List (S.14)

• Issuing of third party cheques

• Opening current accounts

• Foreign trade operations

• Trust operations

• Investing in enterprise capital

• Wholesale or retail trade

• Underwriting or placement of securities

• Purchasing or acquiring of land and buildings except for carrying out business

Prohibited Business and Restricted

Business Regulation

Positive List (Implicit)

• Savings mobilisation

• Credit or lending facilities

• Domestic money transfer

• Insurance in compliance with

the relevant law

• Any other activity or

transaction not specified in

the negative list or in the

regulations

Brazil – Correspondent Banking

Solution from other countries:

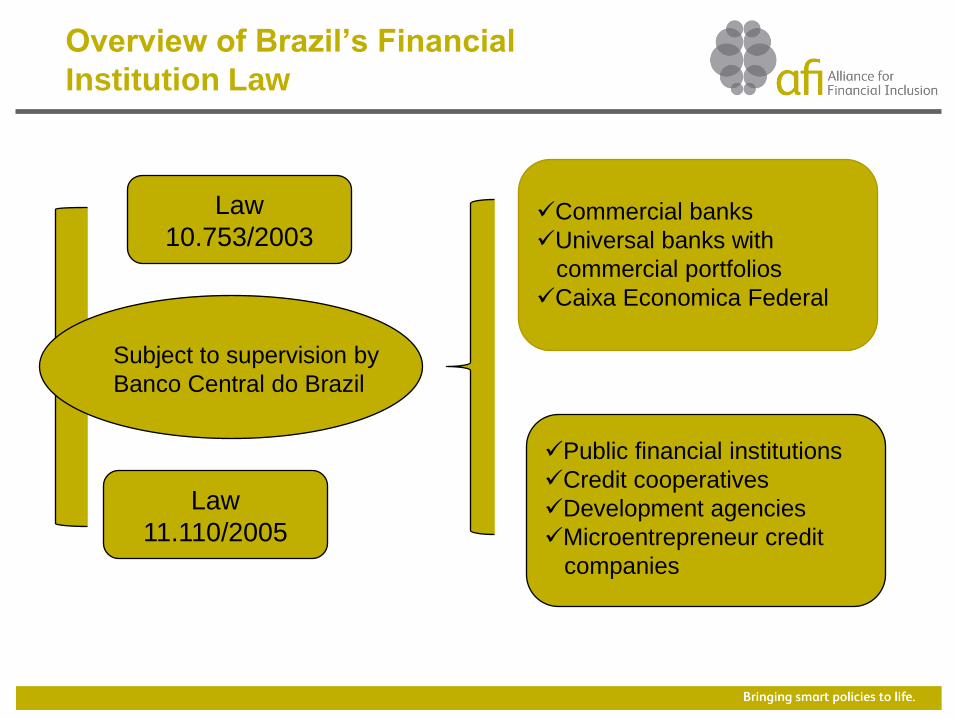

Overview of Brazil’s Financial

Institution Law

Law

10.753/2003

Law

11.110/2005

Subject to supervision by

Banco Central do Brazil

Commercial banks

Universal banks with

commercial portfolios

Caixa Economica Federal

Public financial institutions

Credit cooperatives

Development agencies

Microentrepreneur credit

companies

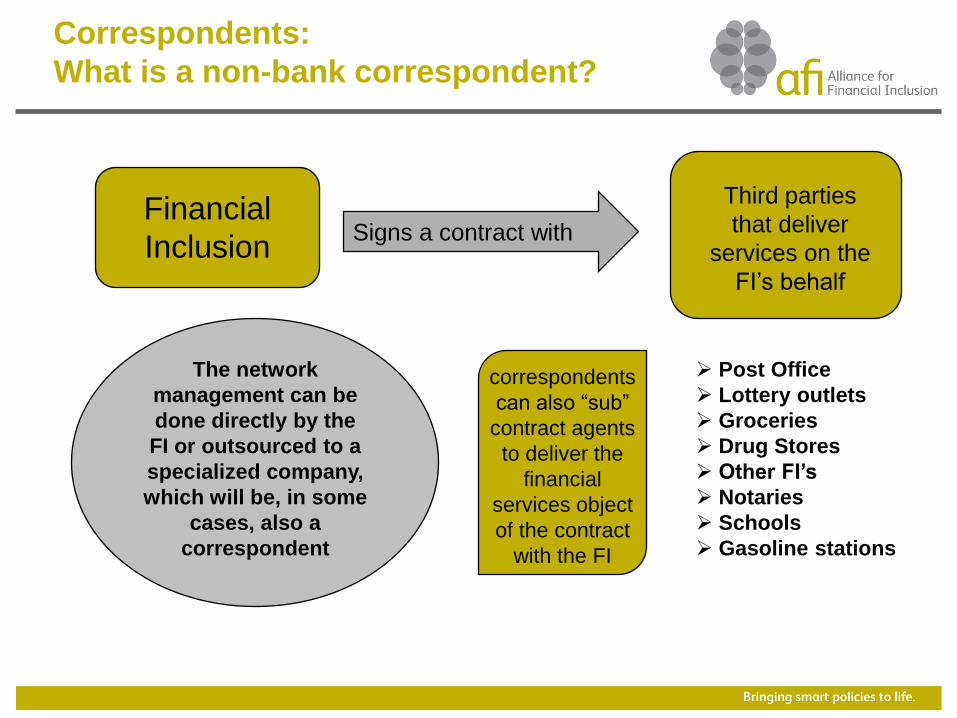

Correspondents:

What is a non-bank correspondent?

Financial

InclusionSigns a contract with

Third parties

that deliver

services on the

FI’s behalf

correspondents

can also ―sub‖

contract agents

to deliver the

financial

services object

of the contract

with the FI

The network

management can be

done directly by the

FI or outsourced to a

specialized company,

which will be, in some

cases, also a

correspondent

Post Office

Lottery outlets

Groceries

Drug Stores

Other FI’s

Notaries

Schools

Gasoline stations

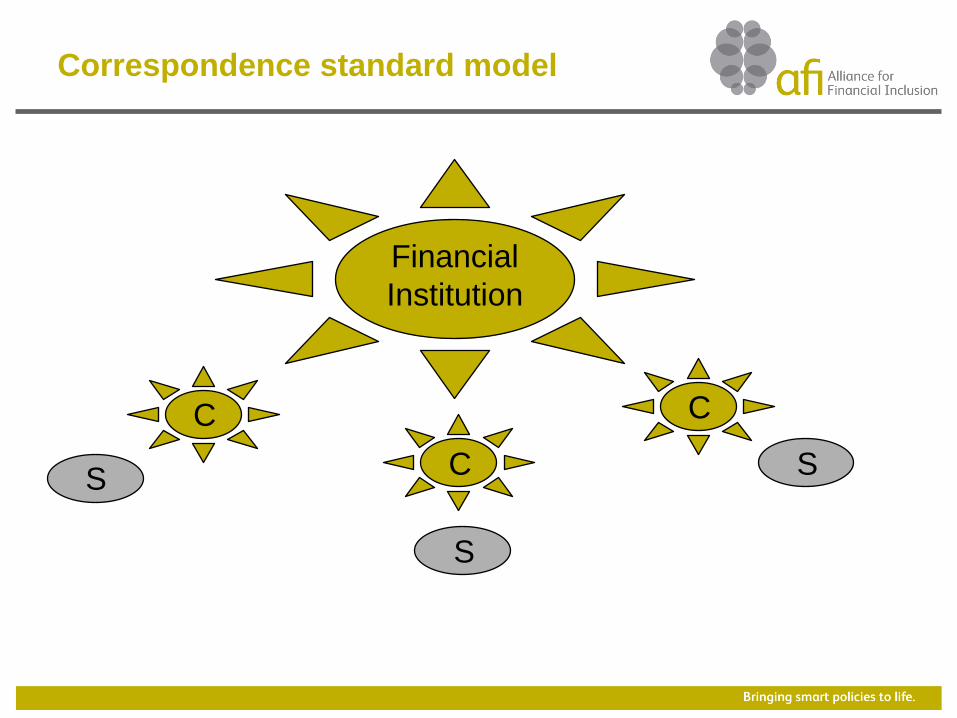

Correspondence standard model

Financial

Institution

C C

CS S

S

Correspondents:

Why bank-based model?

FOR THE SUPERVISION AND REGULATORS

• Total and unrestricted access to all correspondent’s information, data and

documents, also in case of subcontracting.

FOR THE CUSTOMERS

• Guarantee of a prudential supervised financial institution responsible for

the correspondent’s activities.

WHO IS RESPONSIBLE FOR CORRESPONDENT’S ACTIONS?

• The financial institution, which is authorized and supervised by the

Central Bank of Brazil, is always the one responsible for the financial

services and products provided by any of its distribution channels.

Main services provided by

correspondents

• Receive and forward applications for opening bank accounts,

obtaining credit cards and buying shares of mutual funds

• Receive and forward applications for loans perform credit analysis

• Make and receive payments related to bank accounts, loans,

government benefits, utility bills and taxes

• Transfer funds between parties

• Collection of bills related to the payment of public utilities services

• With Resolution 3.568/2008, since July 1, 2008, correspondents are

allowed to deal international transferring of money, from and to

abroad, limited to the amount of US$ 3 thousand per transaction,

according to contracts with banks authorized by the Central Bank of

Brazil to do so

• The correspondent is forbidden to subcontract third parties for this

specific service

Correspondents:

Why does it work?

• Financial stability, strong banking sector and modern

payment systems are preconditions for relaxing

regulatory framework for new or non conventional ways

of delivering services in a safe and efficient manner

• Strong political support for the financial inclusion

• Confidence in the model!!!

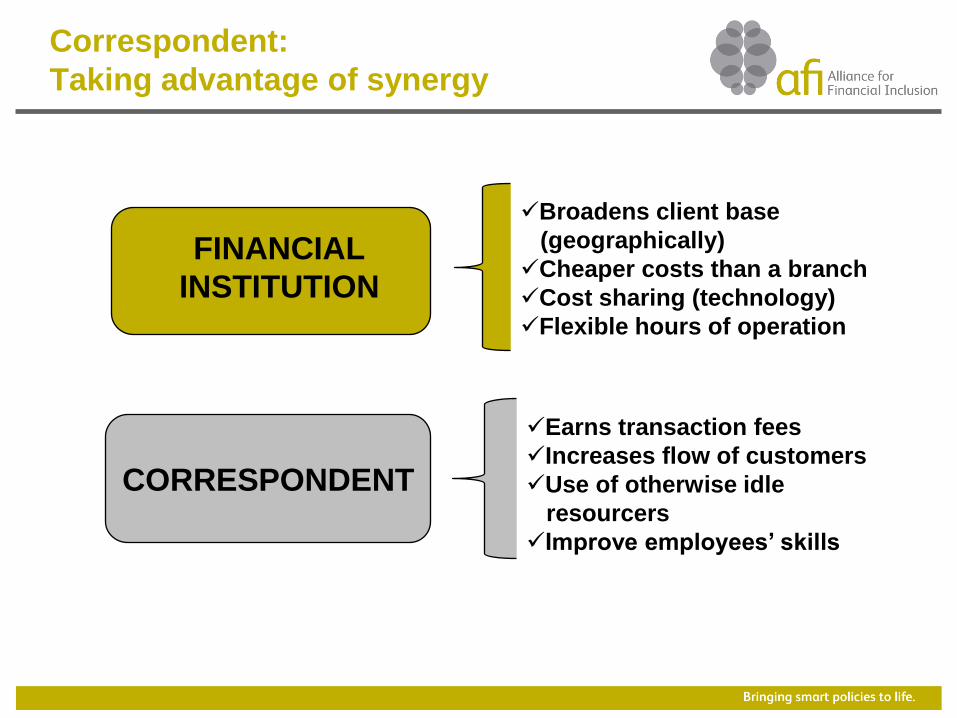

Correspondent:

Taking advantage of synergy

Broadens client base

(geographically)

Cheaper costs than a branch

Cost sharing (technology)

Flexible hours of operation

Earns transaction fees

Increases flow of customers

Use of otherwise idle

resourcers

Improve employees’ skills

FINANCIAL

INSTITUTION

CORRESPONDENT

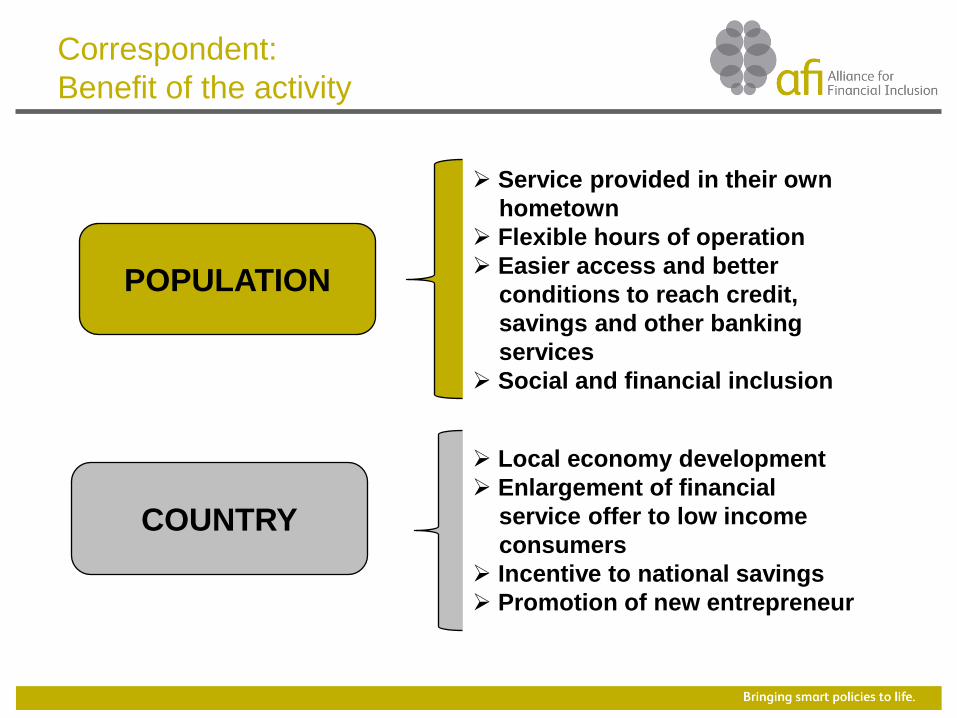

Correspondent:

Benefit of the activity

Service provided in their own

hometown

Flexible hours of operation

Easier access and better

conditions to reach credit,

savings and other banking

services

Social and financial inclusion

Local economy development

Enlargement of financial

service offer to low income

consumers

Incentive to national savings

Promotion of new entrepreneur

POPULATION

COUNTRY

Thank you !

Any question?

![Financial Inclusion: General Overview, Central Banks …...Financial Inclusion [General Overview] •Financial inclusion or inclusive financing is the delivery of financial services](https://img.pdfslide.net/doc/110x75/5e95eef43708446e852354fe/financial-inclusion-general-overview-central-banks-financial-inclusion-general.jpg)