-

8/8/2019 Financial Law Links

1/5

Commercial Paper Chase

If banks have to come clean about their off-balance-sheet

leverage, get

ready to pay more for money.

Andrew Osterland - CFO Magazine

June 1, 2002

The structured-finance geeks on Wall Street used to ply their

trade in relative obscurity.Not anymore.

The annual Bond Market Association meeting in New York on April

25 drew four timesthe audience it did last year. Such speakers as

Treasury Secretary Paul O'Neill, Securitiesand Exchange Committee

chairman Harvey Pitt, and capital-markets mainstay Paul

Volcker undoubtedly helped the turnout, but a swarm of reporters

also turned up to askquestions about special-purpose entities

(SPEs) and other means of moving risk offcorporate balance sheets.

The media, of course, were looking for the next Enron.

Related Articles

Will Governance Metrics Catch On? Pensions as Earnings Drag?

S&P Unveils New Earnings Gauge Reining In SPEs

"How do we help the market distinguish between what we do and

what Enron did?" oneassociation member asked Pitt. He had no ready

answer. The off-balance-sheet genie isout of the bottle, and for

the time being there's no easy way to put it back in. With

theFinancial Accounting Standards Board (FASB) currently

deliberating on new rules forconsolidating SPEs and disclosing

off-balance-sheet activities, structured finance is in

thespotlight. Even if regulators don't curb the activities, the hue

and cry from investors islikely to keep it there.

The activities conducted through SPEs in the asset-backed

securities market may indeedbe a far cry from what Enron did, but

they raise the same issues of disclosure and hiddenrisk. And given

that more than a trillion dollars of assets were taken off

corporate balance

sheets last year and put into SPEs and vehicles known as

commercial-paper conduits, theissue may extend beyond comparisons

to Enron.

The subjects of greatest concern are the commercial banks. They

use SPEs to securitizetheir own assets, and also sponsor

asset-backed commercial-paper conduits, whichpurchase and

securitize assets from third parties. New accounting rules for

these activitieswill cost both banks and their corporate borrowers.

"All the major banks sponsor CPconduits," says Jeff Allen, a senior

manager with PricewaterhouseCoopers. "If they are

http://www.cfo.com/index.cfm/l_emailauthor/3004888/c_3046524/2984983http://www.cfo.com/article.cfm/3005096?f=relatedhttp://www.cfo.com/article.cfm/3004736?f=relatedhttp://www.cfo.com/article.cfm/3004688?f=relatedhttp://www.cfo.com/article.cfm/3004484?f=relatedhttp://www.cfo.com/index.cfm/l_emailauthor/3004888/c_3046524/2984983http://www.cfo.com/article.cfm/3005096?f=relatedhttp://www.cfo.com/article.cfm/3004736?f=relatedhttp://www.cfo.com/article.cfm/3004688?f=relatedhttp://www.cfo.com/article.cfm/3004484?f=related

-

8/8/2019 Financial Law Links

2/5

forced to consolidate them, there are going to be a lot more

assets on their balancesheets." And probably a need for more

capital to meet regulatory reserve requirements. Inthat case, banks

and near-banks may be compelled to rein in their SPEs and

conduitprograms, and the terms for both loans and asset-backed

commercial paper would tighten.Moreover, without the liquidity

guarantees provided in bank-sponsored conduits, many

companies might lose their access to the asset-backed market

altogether. Can you say"credit crunch"?

Know-Nothings

At stake for the business community is the ability to make

illiquid assets liquid bypackaging them into securities the most

significant innovation in the capital markets inthe past two

decades. Since Fannie Mae and Freddie Mac got the ball rolling in

themortgage market as part of their mandate to foster home

ownership in America,securitization has expanded into a variety of

markets, including credit-card debt, auto andhome-equity loans,

commercial mortgages, and trade receivables. The practice

allowsoriginators to sell assets from their balance sheets and

devote their capital to generating

new business. The good thing about securitization is that it has

enabled the extension ofcredit to far more individuals and

businesses in the United States. The bad thing aboutsecuritization

is that financial-reporting practices haven't kept up with the

innovation.Because the programs are executed in SPEs

off-balance-sheet, investors know next tonothing about the risks

involved in the activities.

"The banks are a lot more leveraged than we think," says Ohio

State University professorof finance Anthony Sanders. "If they

fully disclosed their risks, some people would betelling them to

pare back their exposure." Indeed, some people, notably

PacificInvestment Management Co. (PIMCO) bond fund manager Bill

Gross, are already doingso. The heaviest hitter in the bond market

recently accused General Electric of using off-

balance-sheet activities to manipulate its reported earnings,

and also suggested that thecompany's heavy dependence on the

short-term commercial paper market was becomingprecarious. GE CFO

Keith Sherin has indicated that the company will reduce the

liquiditysupport it provides for its commercial-paper conduits, and

the company has begunrefinancing its debt structure in favor of

longer maturities.

As the biggest players in the structured-finance market,

commercial banks in the UnitedStates and Europe may have to do the

same or more. A recent study of securitizationprograms by Standard

& Poor's showed that all the major banks, and many minor

ones,conduct significant off-balance-sheet securitizations through

their own SPEs and throughcommercial paper conduits. Conduit

programs alone financed approximately $500 billionin assets last

year none of which appeared on corporate or bank balance sheets.

Notmuch appeared in the footnotes, either. While Citigroup devoted

some ink in its 2001annual report to its securitizations of

credit-card debt, it revealed next to nothing aboutthe performance

of $51 billion in assets residing in Citigroup-sponsored

commercialpaper conduits and other securitization structures.

While securitization has enabled banks to finance assets through

the capital markets, theprocess hasn't eliminated the risks

associated with those assets. In fact, in most cases,

-

8/8/2019 Financial Law Links

3/5

banks and asset-sellers have retained the majority of the risk

of assets transferred off-balance-sheet. The process works fine

when the economy is strong and credit losses aresmall, as was the

case through most of the last decade. And to hear the

bankingcommunity tell it, the asset pools serving as collateral for

asset-backed bonds are stillperforming well. But no one knows for

sure.

Commercial Paper Chase

(continued)

"We're comforted somewhat by the fact that regulators are

looking at these thingsclosely," says S&P bank-rating analyst

Tanya Azarchs. Indeed, in January, the SEC andthe Federal Reserve

Board forced PNC Bank to consolidate distressed loans it

hadtransferred into three SPEs. The result was a $155 million hit

to PNC's first-quarterearnings.

FASB is determined that investors should be looking at these

things more closely as well.Under current rules regarding SPE

accounting, neither financial-services firms nor othertypes of

businesses need disclose much about their off-balance-sheet

activities. Even therating agencies have to essentially take banks

at their word about the performance of theassets in their SPEs and

conduits. If the economy's uncertain recovery falters, or

aSeptember 11like event shocks the market again, the portfolios are

almost certain todeteriorate. Now, says Sanders, is the time to be

providing details about risk exposuresand potential liabilities. "I

shudder to think of the litigation they may face if they don'tstart

disclosing things now," he says. "If they keep this game going,

there could be amassive Wall Street panic down the road."

Immortal Risk

Alarmist? Perhaps, but Sanders has a point. No matter how

finance engineers slice anddice it, risk cannot be extinguished, it

can only be transferred or redistributed. In the

assetsecuritization process, companies create a hierarchy of

different securities or tranches with varying degrees of credit

risk associated with a pool of assets. The tranchesproduced in a

typical asset-backed deal range from AAA credits down to BB.

Related Articles

Will Governance Metrics Catch On?

Pensions as Earnings Drag? S&P Unveils New Earnings Gauge

Reining In SPEs

The investor community certainly loves the practice. With the

federal government issuingless debt, and only a handful of

corporations still holding a AAA credit rating, highlyrated,

asset-backed paper is an easy sell with institutional investors.

That's whysecuritization can lower the cost of capital for

companies, say proponents.

http://www.cfo.com/article.cfm/3005096?f=relatedhttp://www.cfo.com/article.cfm/3004736?f=relatedhttp://www.cfo.com/article.cfm/3004688?f=relatedhttp://www.cfo.com/article.cfm/3004484?f=relatedhttp://www.cfo.com/article.cfm/3005096?f=relatedhttp://www.cfo.com/article.cfm/3004736?f=relatedhttp://www.cfo.com/article.cfm/3004688?f=relatedhttp://www.cfo.com/article.cfm/3004484?f=related

-

8/8/2019 Financial Law Links

4/5

But in most cases, the originator of the asset whether it is a

manufacturing companyfinancing trade receivables or a specialty

finance lender securitizing loans retains aresidual interest in the

performance of the assets. This interest obligates the issuer

tocover losses in the asset pool up to a certain percentage. If

losses exceed that percentage,other low-rated, subordinate tranches

of the issuance begin to absorb them. "The post-

Enron fear is that there's all sorts of stuff out there we

didn't know existed," says Azarchs."Now you wonder about what you

don't know." Not exactly a confidence booster forinvestors. The

billion-dollar question is, who holds those subordinate

tranches?

With riskier slices of asset-backed securitizations harder to

sell these days, the answer is,fewer and fewer investors. In many

cases, collateralized debt and bond obligation (CDOand CBO)

vehicles, many of them sponsored by European banks such as ABN Amro

andDeutsche Bank, buy the lower tranches. CDOs and the like control

about $400 billion inassets. Again, however, no one knows for sure.

"It's all innuendo and rumor," saysAzarchs. A particularly

troubling possibility is that the banks are scratching one

another'sbacks. "It may be that a given financial institution has

held not its own subordinate

tranches, but similar ones in deals sponsored by others," wrote

Azarchs in a recent report.

The risks for banks don't end there. The banks also agree to

provide liquidity support ifcash flow from the conduit isn't enough

to pay off the paper as it matures. If enough loansin a conduit go

bad, the sponsor bank could be liable. That may appeal to both

conduitinvestors and the companies they help finance, but the risks

are substantial, says OhioState's Sanders, and should be made

transparent to the market. "The S&L crisis almostcrippled the

economy wait until we have a banking crisis," he says.

Hopefully, more disclosure won't be the very thing that

precipitates it.

Andrew Osterland is a senior editor atCFO.

In-securitization

Even a Triple-A-rated company like General Electric could be

vulnerable if it wereunable to securitize assets easily. Through

its finance subsidiary, GE currently usessponsored special-purpose

entities (SPEs) and conduits to securitize its own and others'loans

and receivables. The company's most recent annual report asserts

that, if required(presumably in the event of an accounting change

regarding the consolidation of SPEs),GE could use "alternative

securitization techniques...at an insignificant incremental

cost."Why not already do so? "It would still be an incremental

cost," says CFO Keith Sherin.

"When you have the option, you go with the lowest cost."

Still, critics say that GE's statement in its annual report

about SPEs is misleading,because such an accounting change would

likely affect all off-balance-sheet financingalternatives. And if

GE has to finance the assets on the balance sheet, the impact on

itsfinancial statements will be more than incremental.A.O.

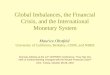

Paper Pushers

-

8/8/2019 Financial Law Links

5/5

The 10 largest securitizers among financial service

providers.Source: Standard & Poor's

Company Total

securitizations

including CP, in$millions

% of book

assets

CP conduits, in

$millions

Citigroup 129,452 12.1 51,441

ABN Amro Bank 92,304 17.8 46,955

J.P. Morgan Chase 80,652 10.1 42,350

Bank One 78,998 29.2 36,972

MBNA 73,534 170.6 0

Bank of America 43,066 6.7 18,301

Wachovia 39,757 12.2 4,278

Countrywide Credit 36,032 100.6 0

Deutsche Bank 33,041 6.4 5,245

Morgan Stanley Dean Witter 30,650 6.4 0