Embed Size (px)

Citation preview

Financial Management for Non-Profit Program Staff

The Painless, Common-Sense Approach

Learning Objectives• Describe the role that program staff play in budgeting and

financial management

• Understand basic accounting principles

• Understand the importance of the fiscal budgeting process in the financial management of an organization

• Describe the steps involved in program planning from outcomes to evaluation, and a methodology for translating work plan activities into a budget

• Learn how to monitor and manage a budget, including the use of a variance analysis to spot unfavorable trending

• Understand how to effectively communicate financial information at each level of the organization

2

• Describe the different types of audits and the circumstances under which they would apply

• Define fraud and describe ways that fraud can be perpetrated and prevented

• Discuss the most important elements of an internal control system and how financial controls evolve as an organization matures

• Learn how to monitor and manage slippage and overages

• Describe the differences between a grant and Contribution Agreement

• Understand the organization’s obligations under a Contribution Agreement and the processes associated with claiming expenses

3

Learning Objectives

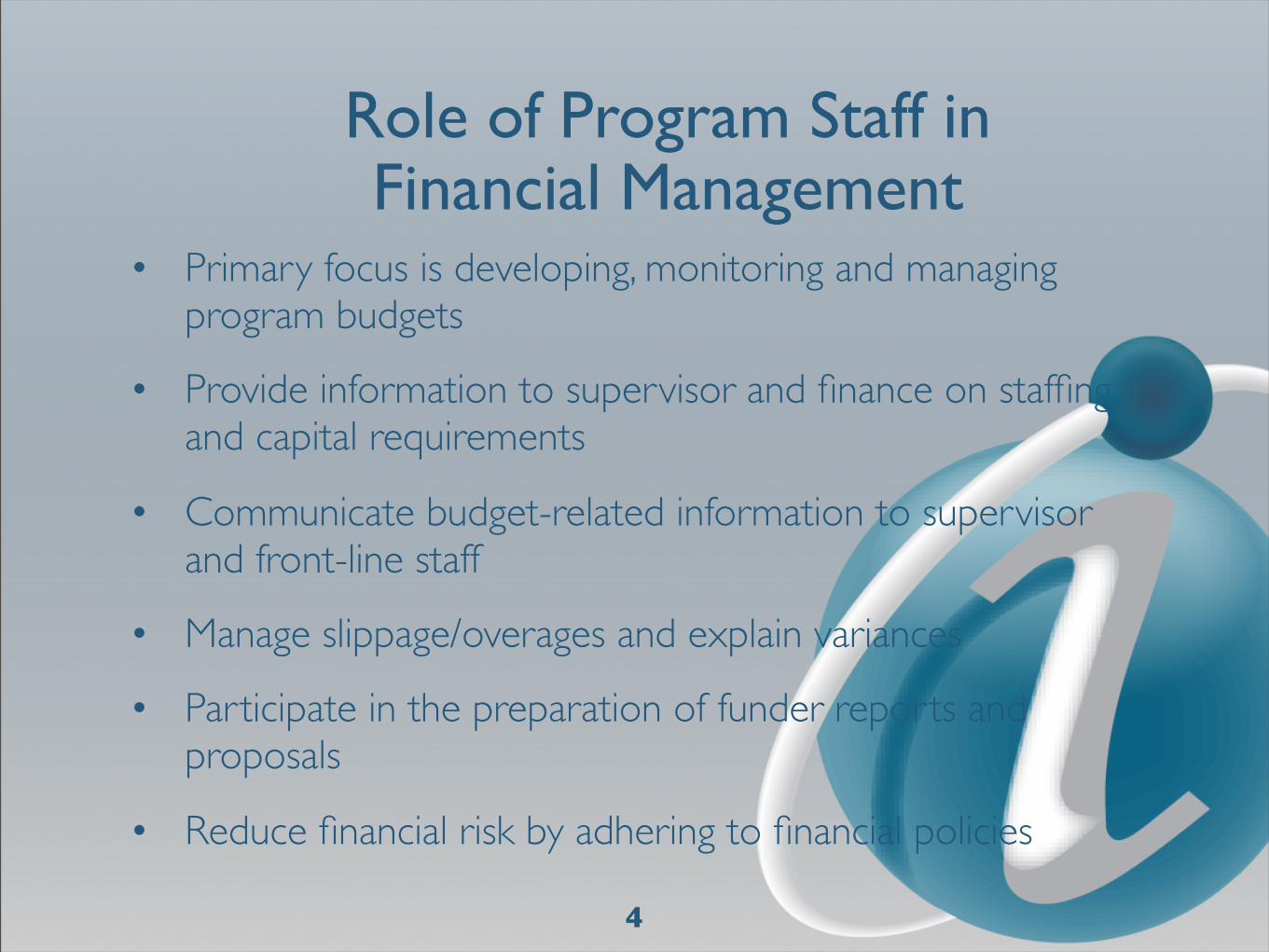

• Primary focus is developing, monitoring and managing program budgets

• Provide information to supervisor and finance on staffing and capital requirements

• Communicate budget-related information to supervisor and front-line staff

• Manage slippage/overages and explain variances

• Participate in the preparation of funder reports and proposals

• Reduce financial risk by adhering to financial policies

4

Role of Program Staff inFinancial Management

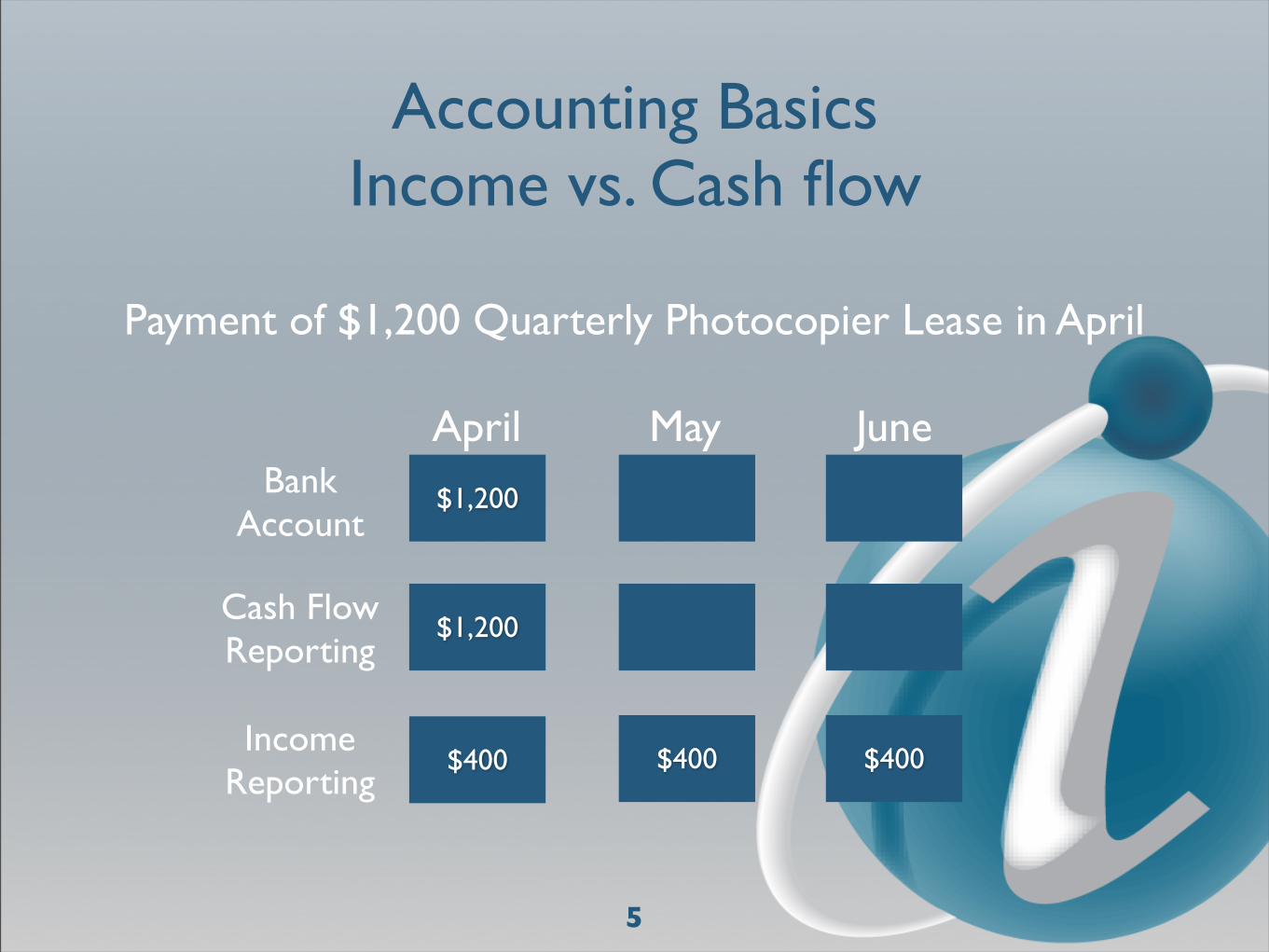

Accounting BasicsIncome vs. Cash flow

Payment of $1,200 Quarterly Photocopier Lease in April

$1,200

$1,200

BankAccount

Cash FlowReporting

April May

$400 $400 $400Income

Reporting

June

5

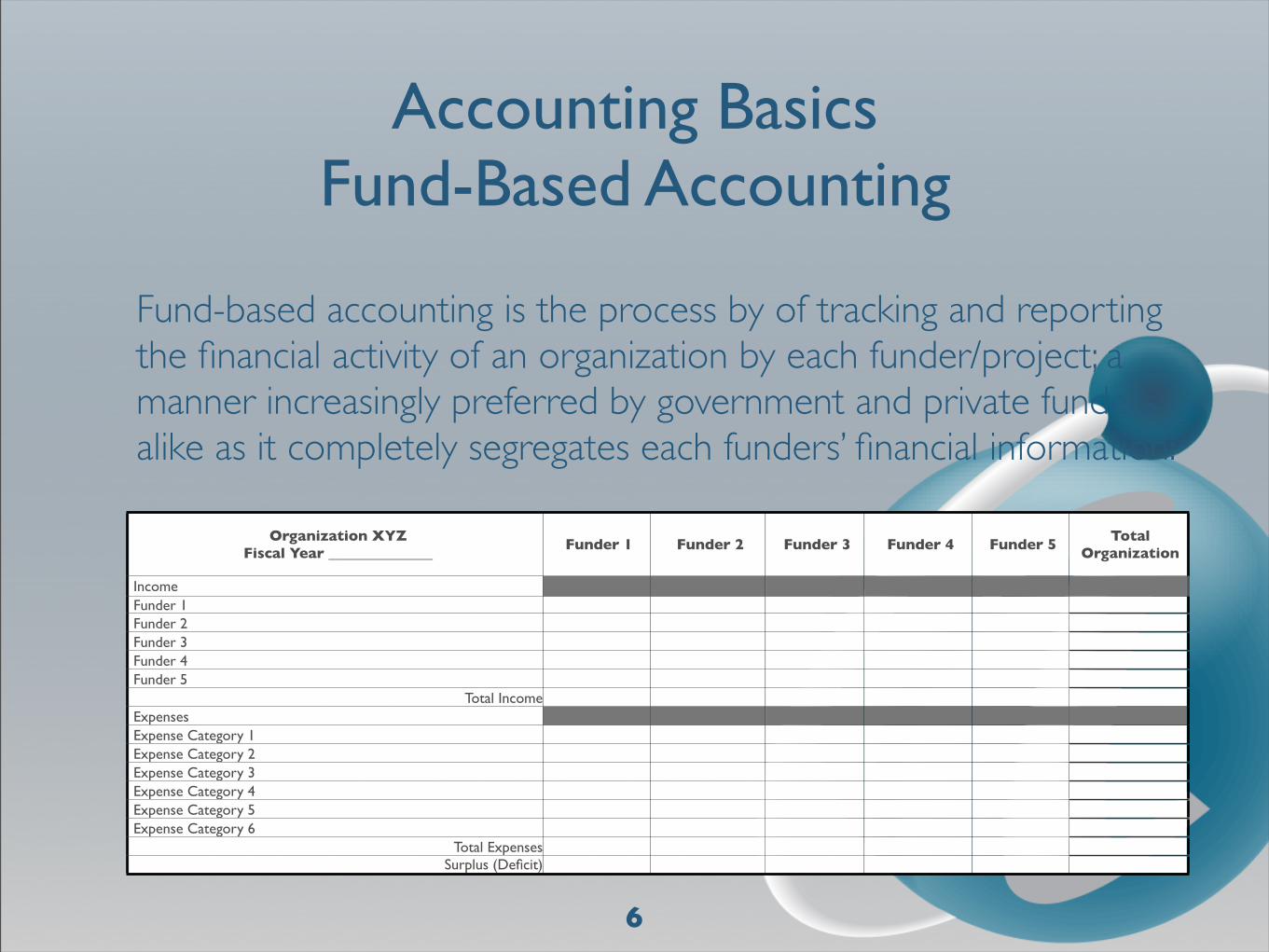

Accounting BasicsFund-Based Accounting

Fund-based accounting is the process by of tracking and reporting the financial activity of an organization by each funder/project; a manner increasingly preferred by government and private funders alike as it completely segregates each funders’ financial information:

6

Organization XYZ Fiscal Year ______________

Funder 1 Funder 2 Funder 3 Funder 4 Funder 5Total

Organization

IncomeFunder 1Funder 2Funder 3Funder 4Funder 5

Total IncomeExpensesExpense Category 1Expense Category 2Expense Category 3Expense Category 4Expense Category 5Expense Category 6

Total ExpensesSurplus (Deficit)

Why Bother Budgeting?• The budget is the organization’s single most important tool in

financial management and its primary financial control mechanism

• Ensures that the organization is able to pay its bills today in order to offer services tomorrow

• Demonstrates that donated resources and funding dollars have been used efficiently and effectively

• Demonstrates accountability to funders and stakeholders

• Confirms ability to use scarce resources wisely

• Ensures present resources are managed effectively for the long term survival of organization

7

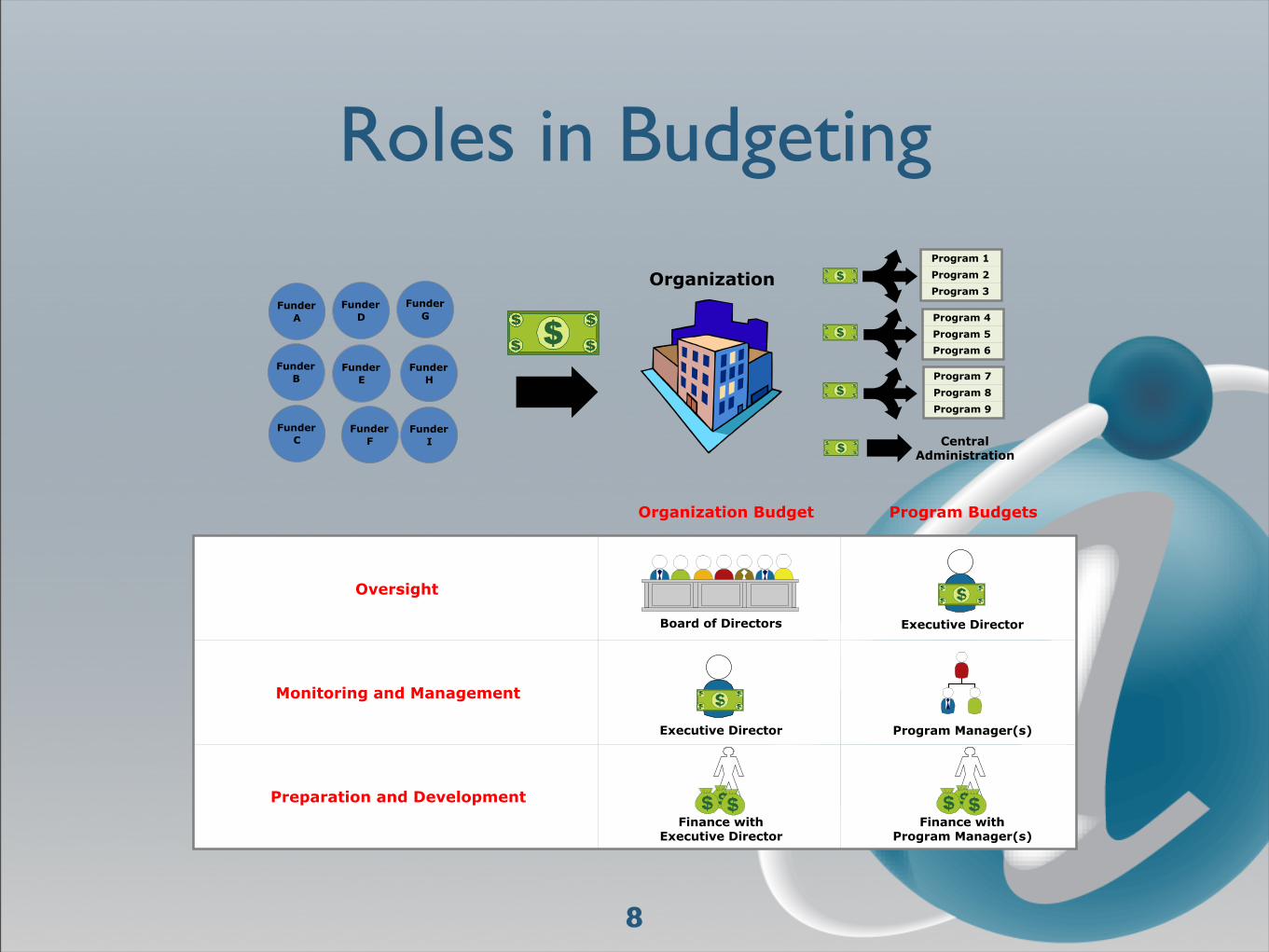

Roles in Budgeting

8

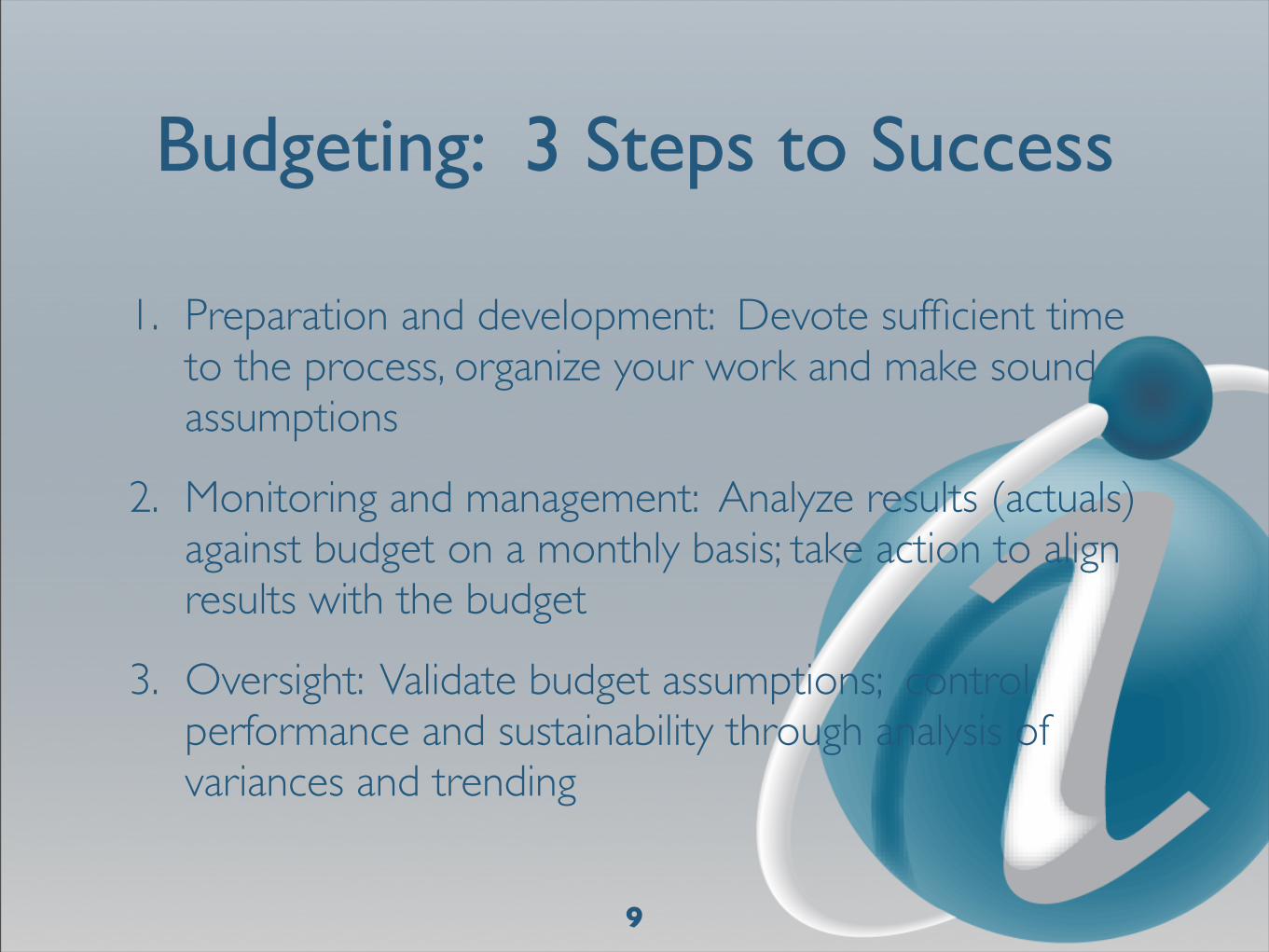

Budgeting: 3 Steps to Success

1. Preparation and development: Devote sufficient time to the process, organize your work and make sound assumptions

2. Monitoring and management: Analyze results (actuals) against budget on a monthly basis; take action to align results with the budget

3. Oversight: Validate budget assumptions; control performance and sustainability through analysis of variances and trending

9

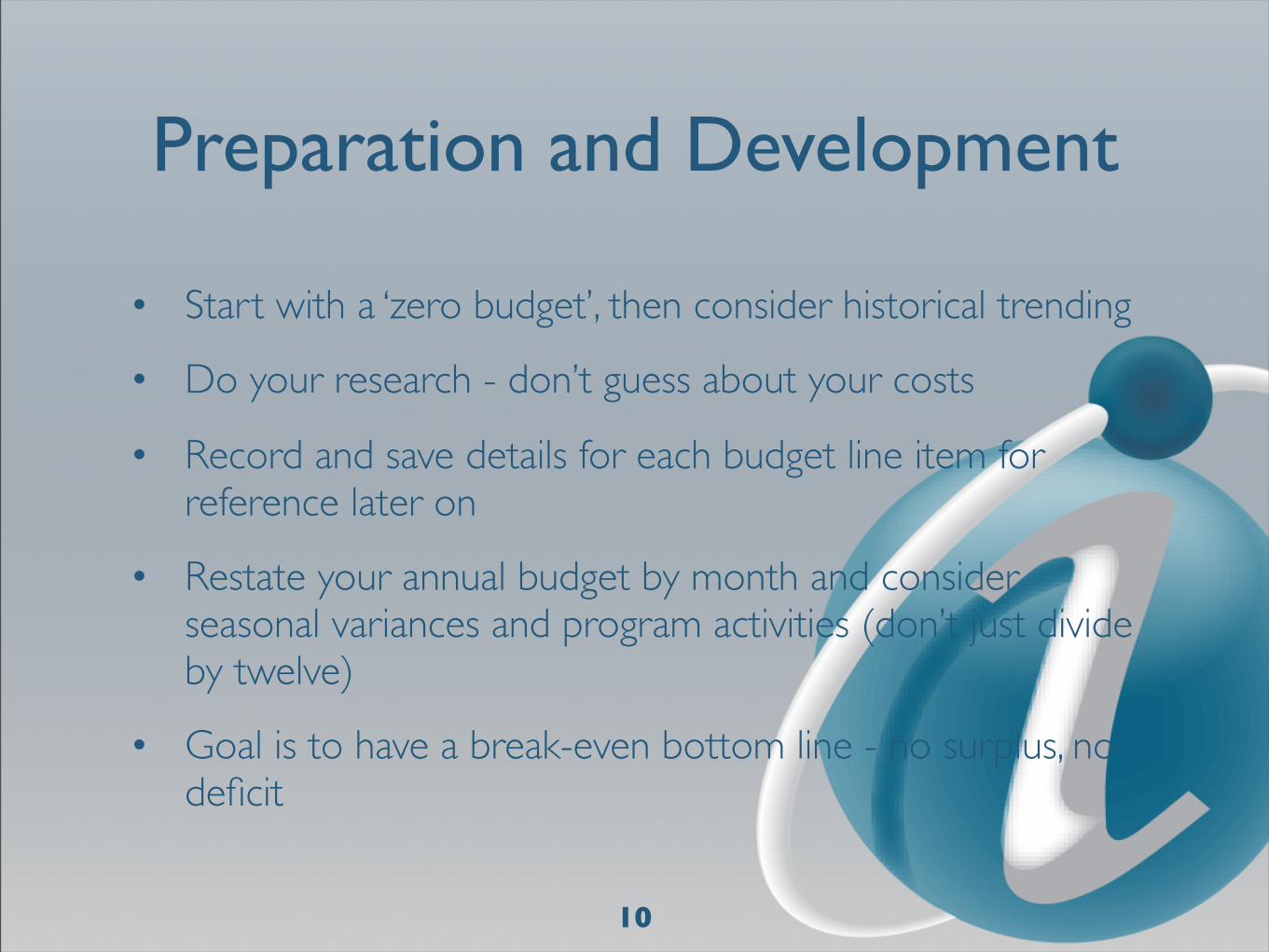

Preparation and Development

• Start with a ‘zero budget’, then consider historical trending

• Do your research - don’t guess about your costs

• Record and save details for each budget line item for reference later on

• Restate your annual budget by month and consider seasonal variances and program activities (don’t just divide by twelve)

• Goal is to have a break-even bottom line - no surplus, no deficit

10

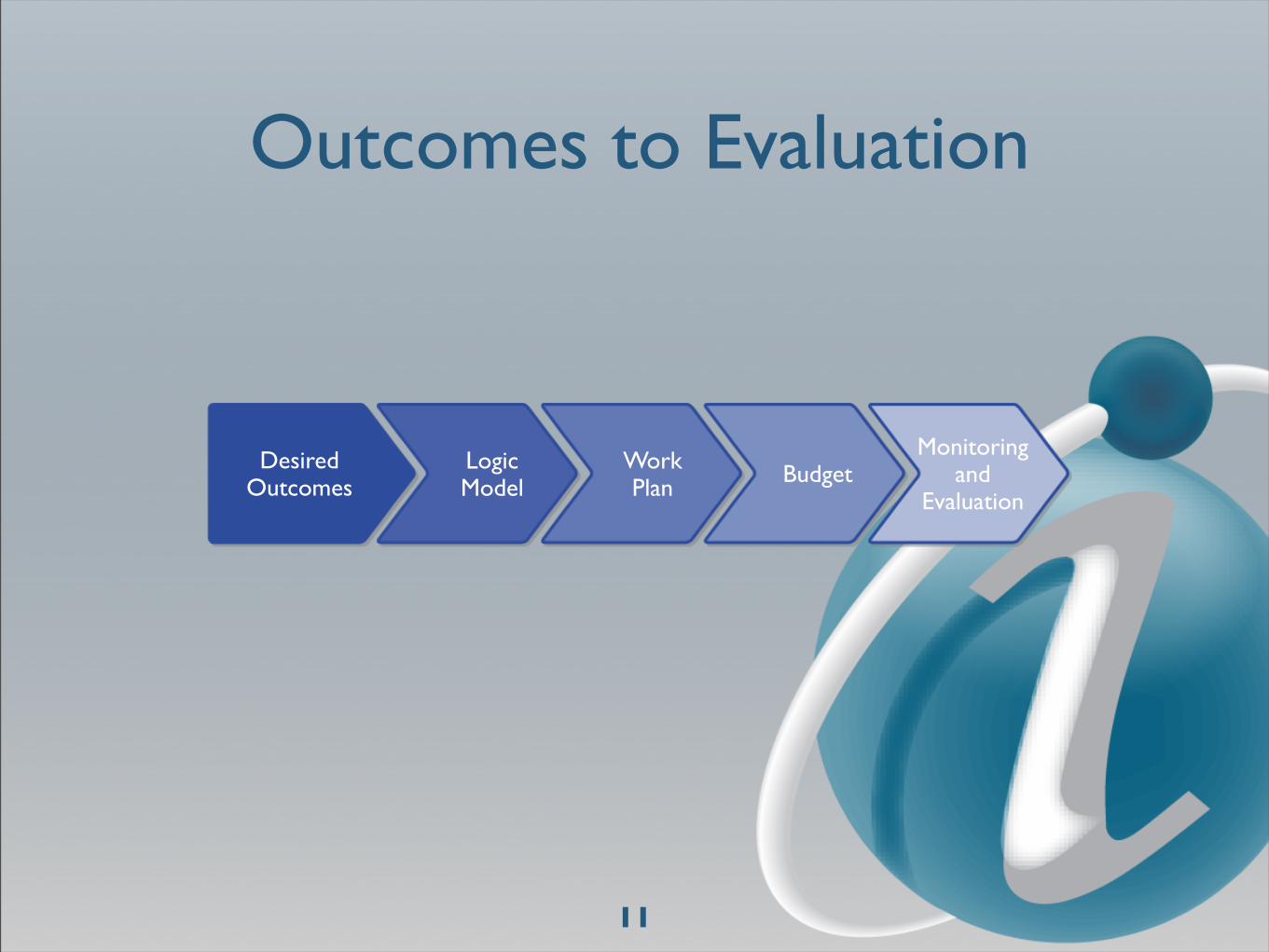

Outcomes to Evaluation

LogicModel

Desired Outcomes

Work Plan Budget

Monitoring and

Evaluation

11

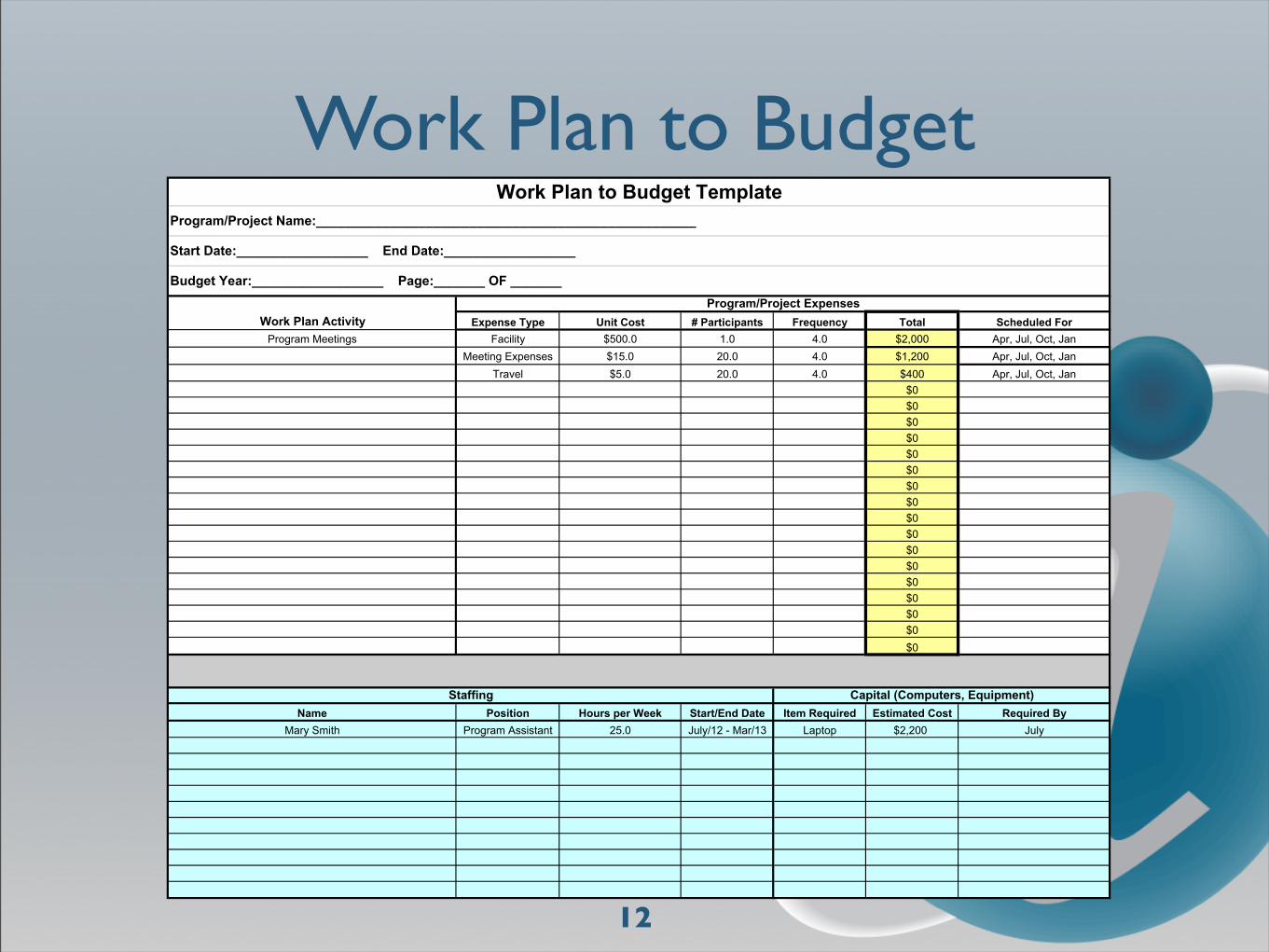

Work Plan to Budget

12

Expense Type Unit Cost # Participants Frequency Total Scheduled For

Program Meetings Facility $500.0 1.0 4.0 $2,000 Apr, Jul, Oct, Jan

Meeting Expenses $15.0 20.0 4.0 $1,200 Apr, Jul, Oct, Jan

Travel $5.0 20.0 4.0 $400 Apr, Jul, Oct, Jan

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Name Position Hours per Week Start/End Date Item Required Estimated Cost Required By

Mary Smith Program Assistant 25.0 July/12 - Mar/13 Laptop $2,200 July

Work Plan Activity

Program/Project Expenses

Staffing Capital (Computers, Equipment)

Work Plan to Budget Template

Program/Project Name:____________________________________________________

Start Date:__________________ End Date:__________________

Budget Year:__________________ Page:_______ OF _______

Central Administration CostsWhat are they and who is responsible for them?

• Direct costs are clearly and easily attributable to a specific program (e.g. program supplies, counsellors’ salaries, meeting costs, participant travel)

• Indirect costs are not exclusively associated with a specific program, but are necessary to the operation of the program; these costs are shared among programs and, in some cases, among departments in an organization (e.g. executive director’s salary, administrative and management salaries, occupancy costs, telephone, bookkeeping, insurance)

• Central Administration costs are considered in-direct or shared costs

• Central Administration budget is the responsibility of finance with input from supervisors and program coordinators

• Central Administration costs should be a part of every program budget

13

Central Administration CostsHow are they calculated and allocated to each program?

• Calculate total, annual Central Administration costs

• Fairly and equitably allocate these total costs by funder/program

• Rationale for allocated must be documented, clear and substantiated:

‣ Based on actual costs:

- Actual expenditures and staff time records

- Time consuming with considerable record-keeping

- Difficult to deal with shared resources

‣ Based on a cost factor or rate:

- Number of full-time project staff (FTEs)

- Program direct costs as a % of total direct costs

- Program funding as a % of total organization’s funding

14

Monitoring and Management

• Involve front-line staff in the development and ongoing monitoring of the budget

• Year-to-year comparisons are effective at spotting problems if the same program is run again

• Keep year-to-date spending at the same percentage of budget as year-to-date funding income, to avoid a deficit

• Know the high risk areas of the budget and have a contingency plan

15

Monitoring and Management

• Prepare and review a budget variance report every month; variances are significant at 5 -10% over or under budget

• Expect few variances if the budget is well prepared

• Explain all significant variances; act on those that could jeopardize the year-end outcome

• Prepare a year-end estimate at the half-way point of the budget year and make spending adjustments as required

16

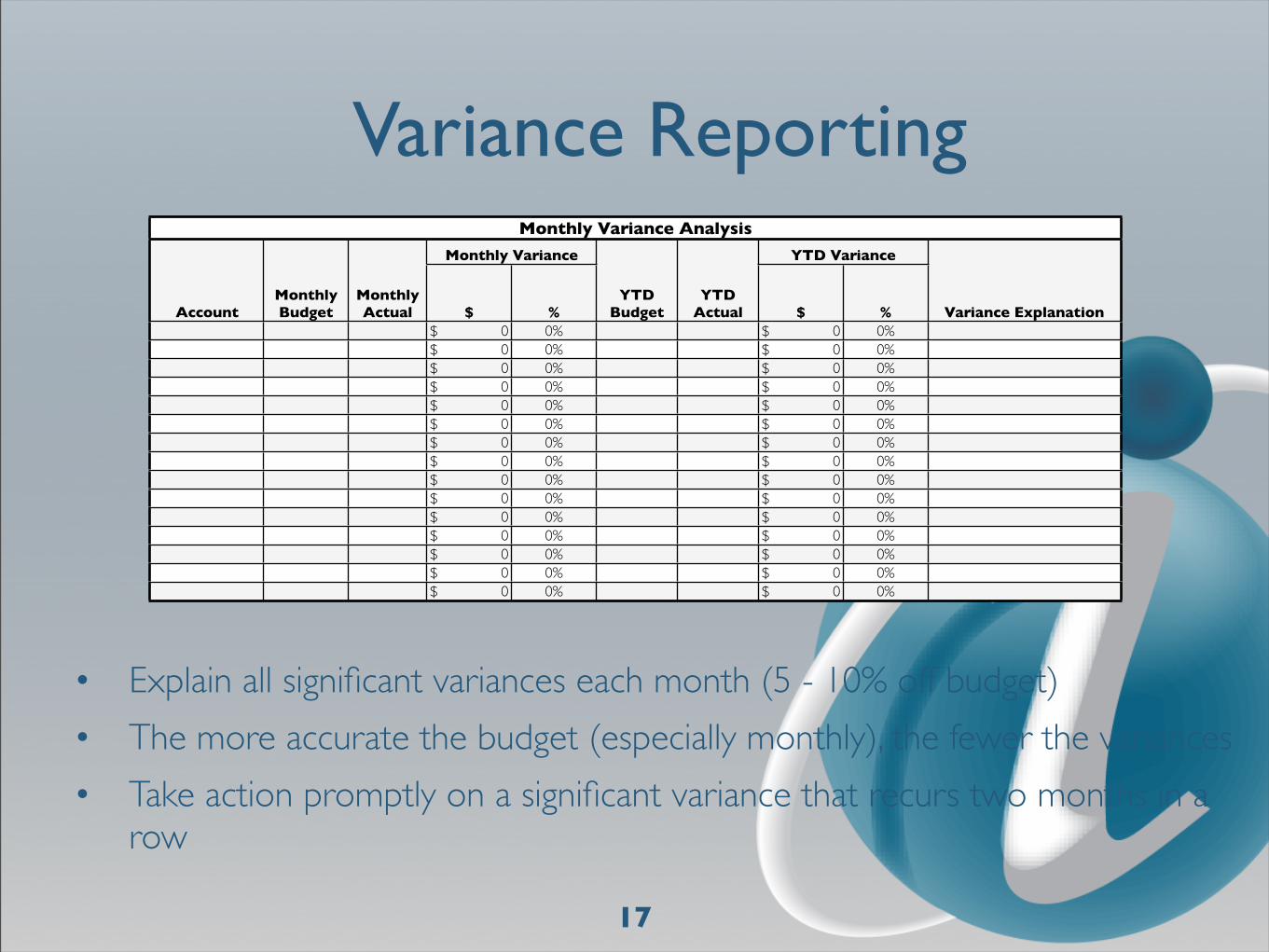

• Explain all significant variances each month (5 - 10% off budget)

• The more accurate the budget (especially monthly), the fewer the variances

• Take action promptly on a significant variance that recurs two months in a row

17

Variance ReportingMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance AnalysisMonthly Variance Analysis

AccountMonthly Budget

Monthly Actual

Monthly VarianceMonthly Variance

YTD Budget

YTD Actual

YTD VarianceYTD Variance

Variance ExplanationAccountMonthly Budget

Monthly Actual $ %

YTD Budget

YTD Actual $ % Variance Explanation

$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%$ 0 0% $ 0 0%

Communicating Financial Information

18

• Consult with the program team in developing the program budget

• Inform the team about the program budget, actual results and variances

• Coach the team on how to make the best use of available funds

• Report on actual results versus budget

• Advise the supervisor/manager of all significant variances to budget

• Talk to front-line workers about the program budget; let them know how much is available to spend in areas key to their work

• Don’t get caught by surprise - regular monitoring ensures a proactive response

• Hold others accountable for their part of the communication cycle

• Remember, budget problems cannot be resolved in one month

19

Communicating Financial Information

Communicating Financial Information

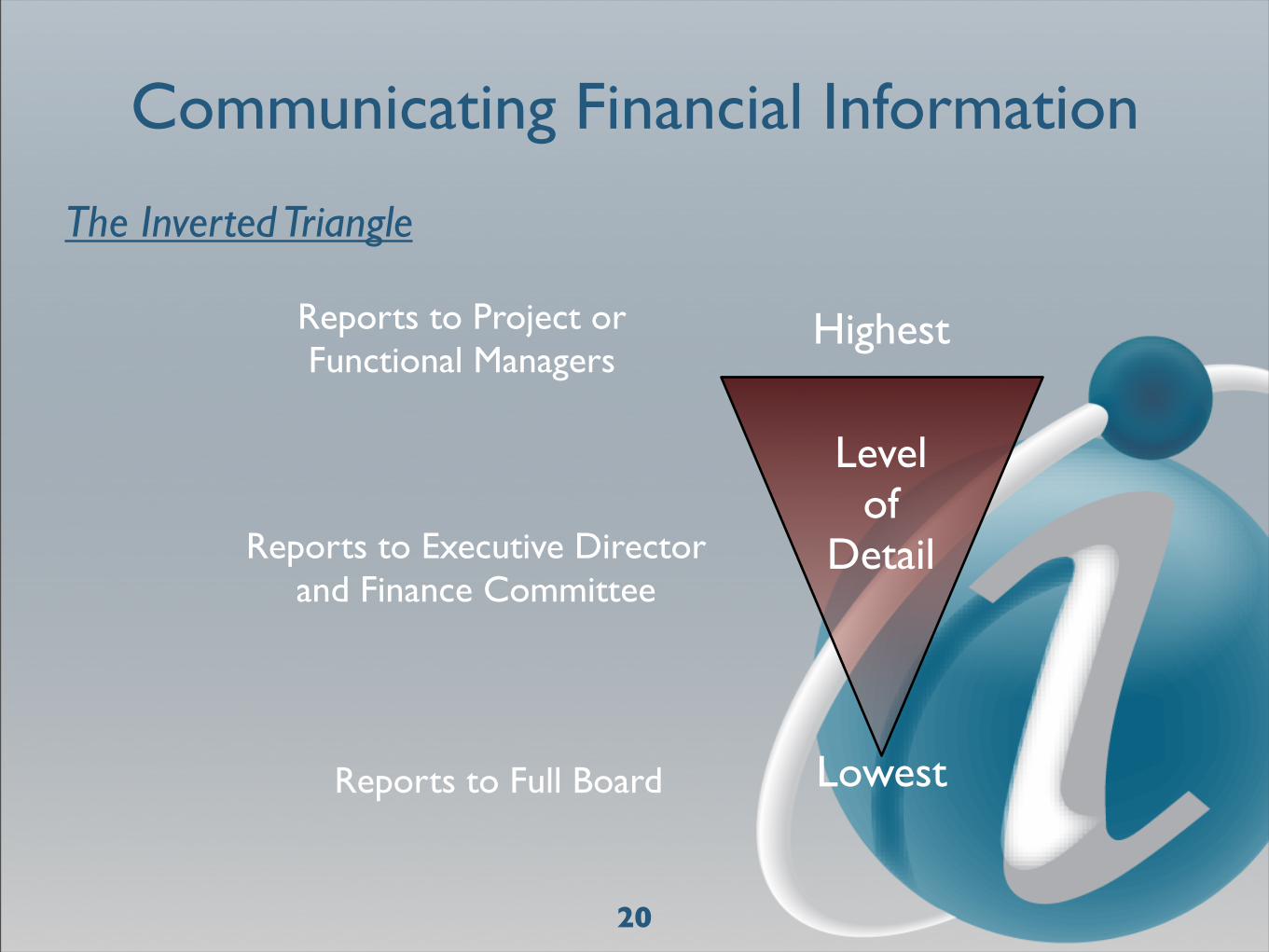

The Inverted Triangle

Reports to Full Board

Reports to Executive Directorand Finance Committee

Reports to Project orFunctional Managers

Highest

Lowest

20

Levelof

Detail

21

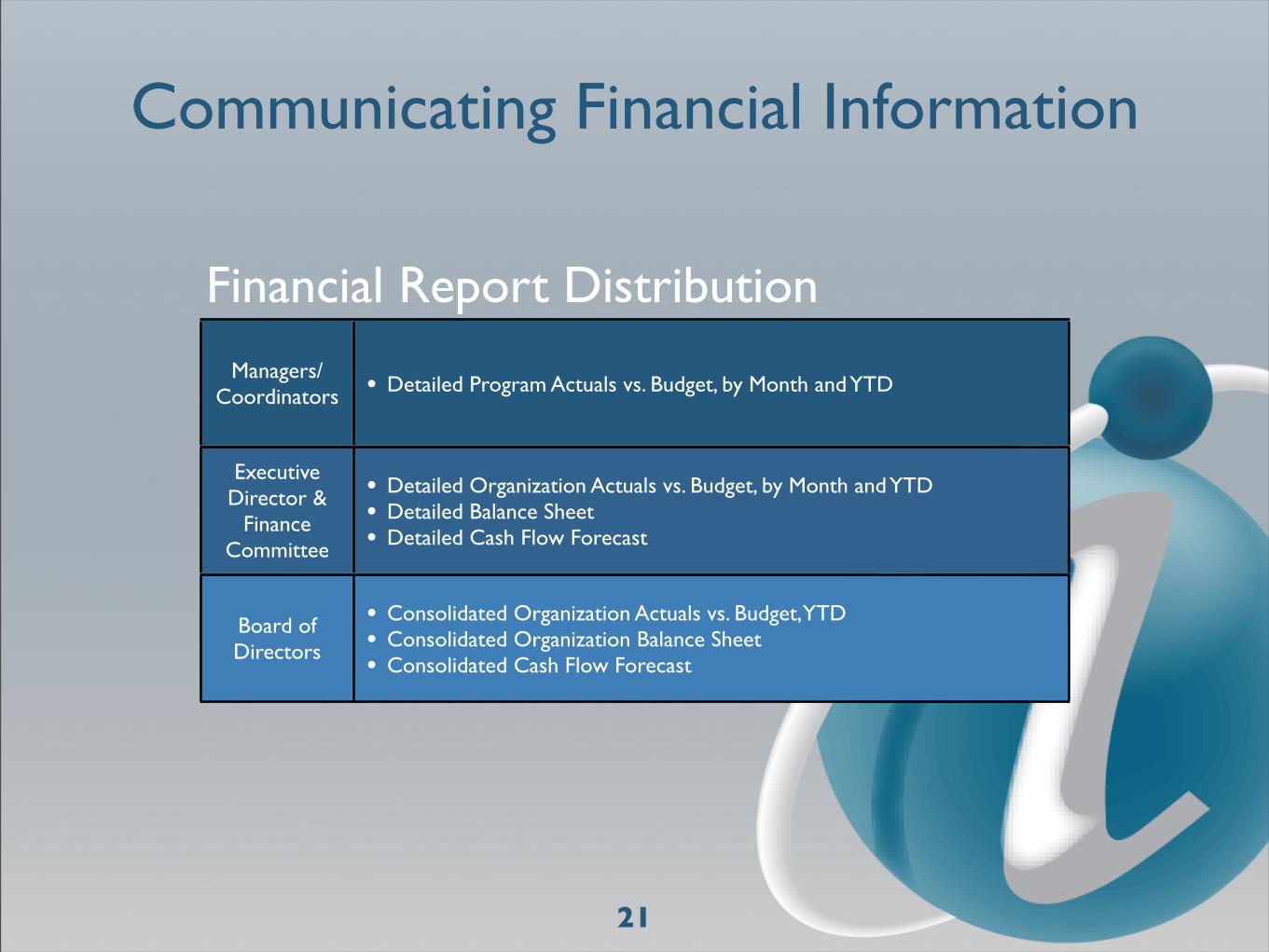

Communicating Financial Information

Managers/Coordinators

• Detailed Program Actuals vs. Budget, by Month and YTD

Executive Director &

Finance Committee

• Detailed Organization Actuals vs. Budget, by Month and YTD• Detailed Balance Sheet• Detailed Cash Flow Forecast

Board of Directors

• Consolidated Organization Actuals vs. Budget, YTD• Consolidated Organization Balance Sheet• Consolidated Cash Flow Forecast

Financial Report Distribution

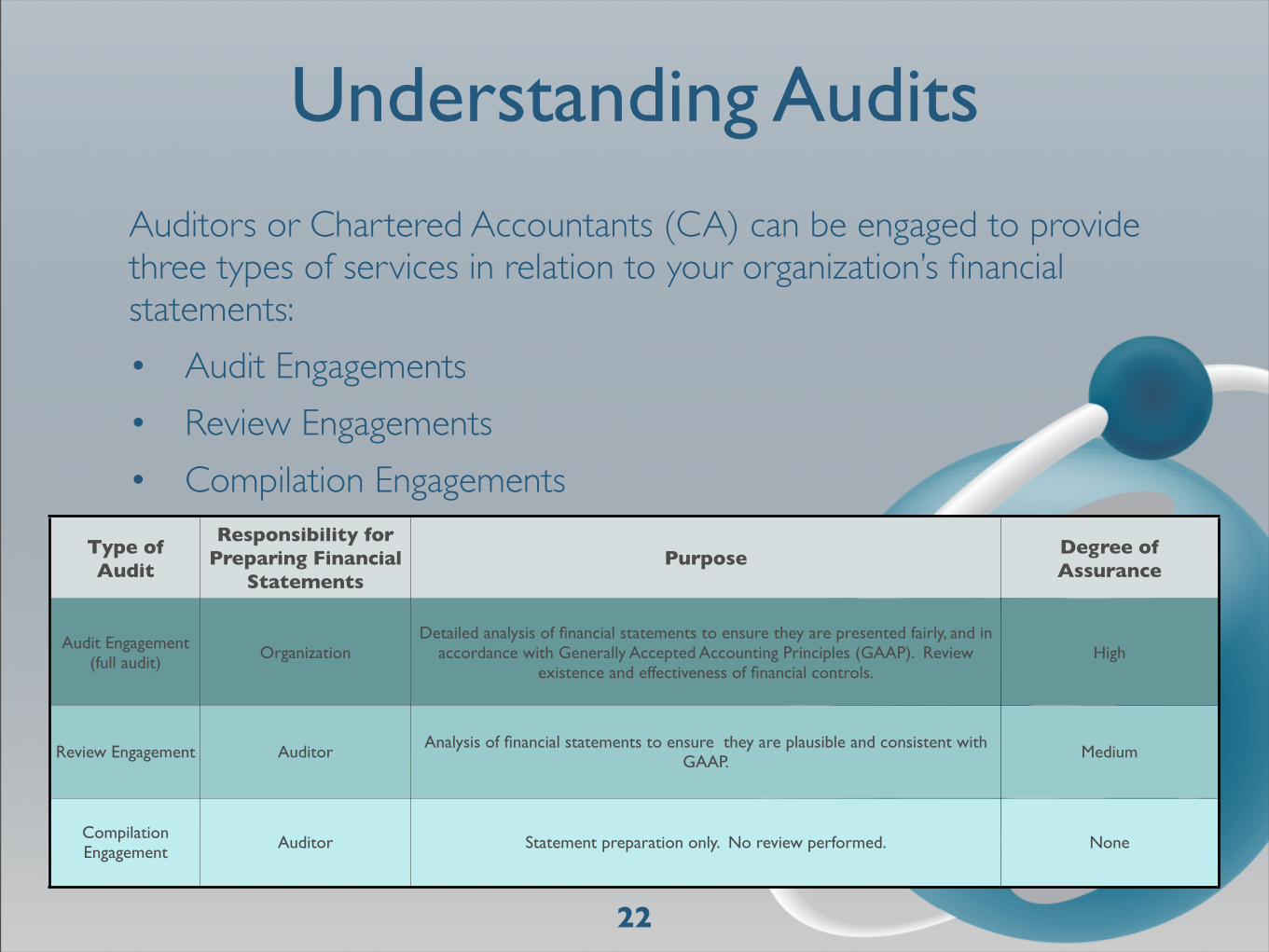

Understanding Audits

22

Type of Audit

Responsibility for Preparing Financial

StatementsPurpose Degree of

Assurance

Audit Engagement(full audit) Organization

Detailed analysis of financial statements to ensure they are presented fairly, and in accordance with Generally Accepted Accounting Principles (GAAP). Review

existence and effectiveness of financial controls.High

Review Engagement Auditor Analysis of financial statements to ensure they are plausible and consistent with GAAP. Medium

Compilation Engagement Auditor Statement preparation only. No review performed. None

Auditors or Chartered Accountants (CA) can be engaged to provide three types of services in relation to your organization’s financial statements:

• Audit Engagements

• Review Engagements

• Compilation Engagements

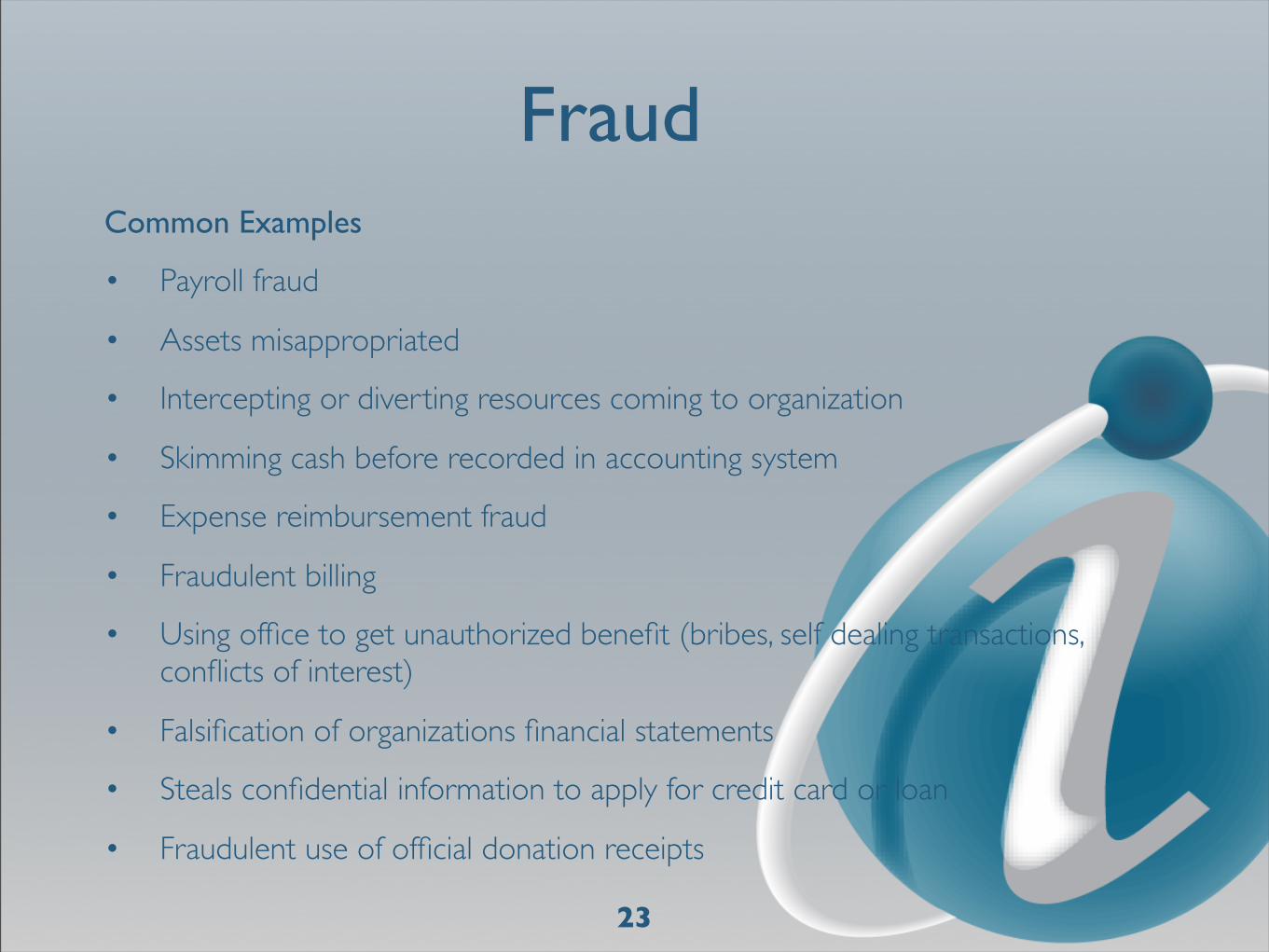

FraudCommon Examples

• Payroll fraud

• Assets misappropriated

• Intercepting or diverting resources coming to organization

• Skimming cash before recorded in accounting system

• Expense reimbursement fraud

• Fraudulent billing

• Using office to get unauthorized benefit (bribes, self dealing transactions, conflicts of interest)

• Falsification of organizations financial statements

• Steals confidential information to apply for credit card or loan

• Fraudulent use of official donation receipts

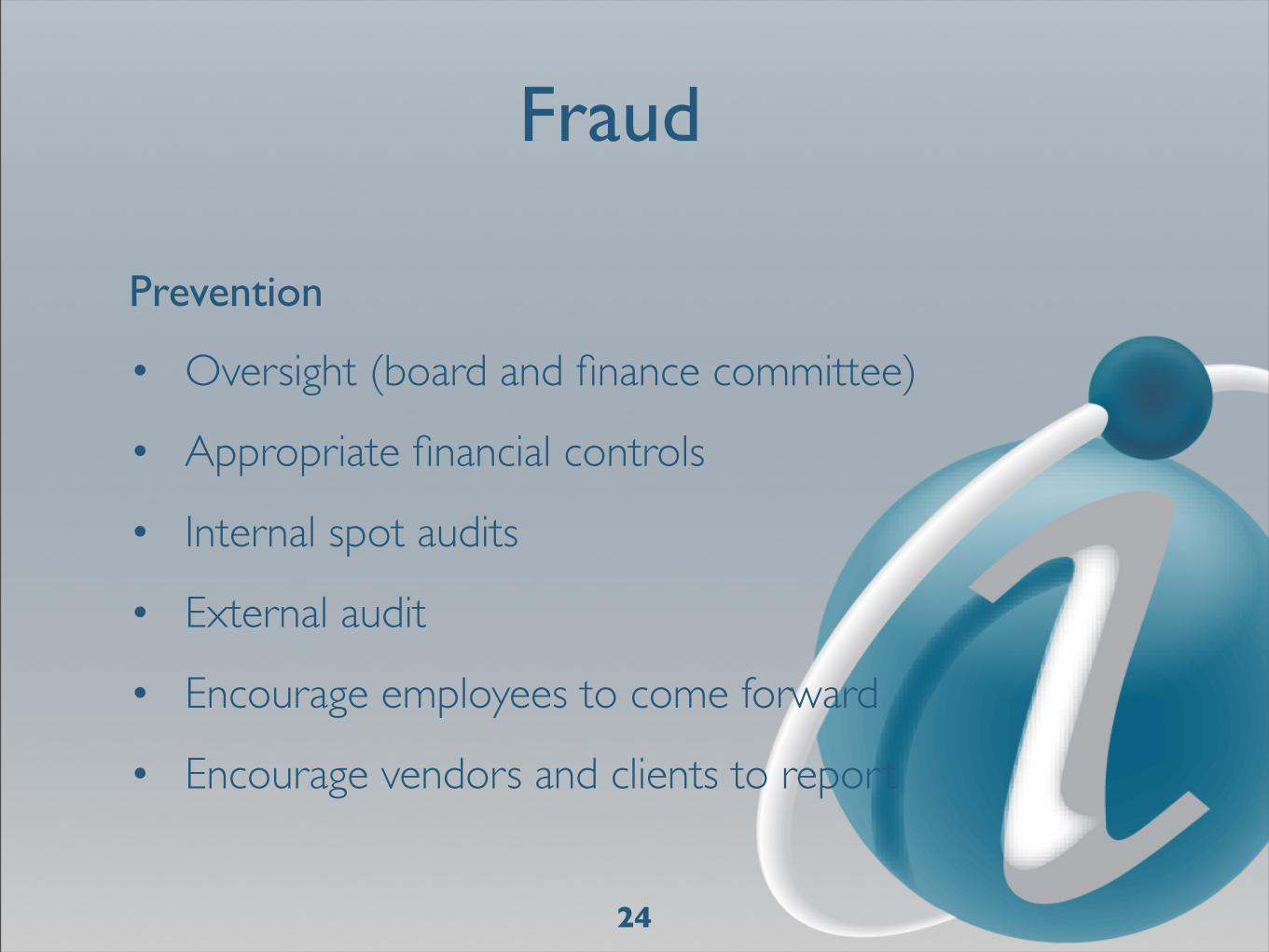

23

Prevention

• Oversight (board and finance committee)

• Appropriate financial controls

• Internal spot audits

• External audit

• Encourage employees to come forward

• Encourage vendors and clients to report

24

Fraud

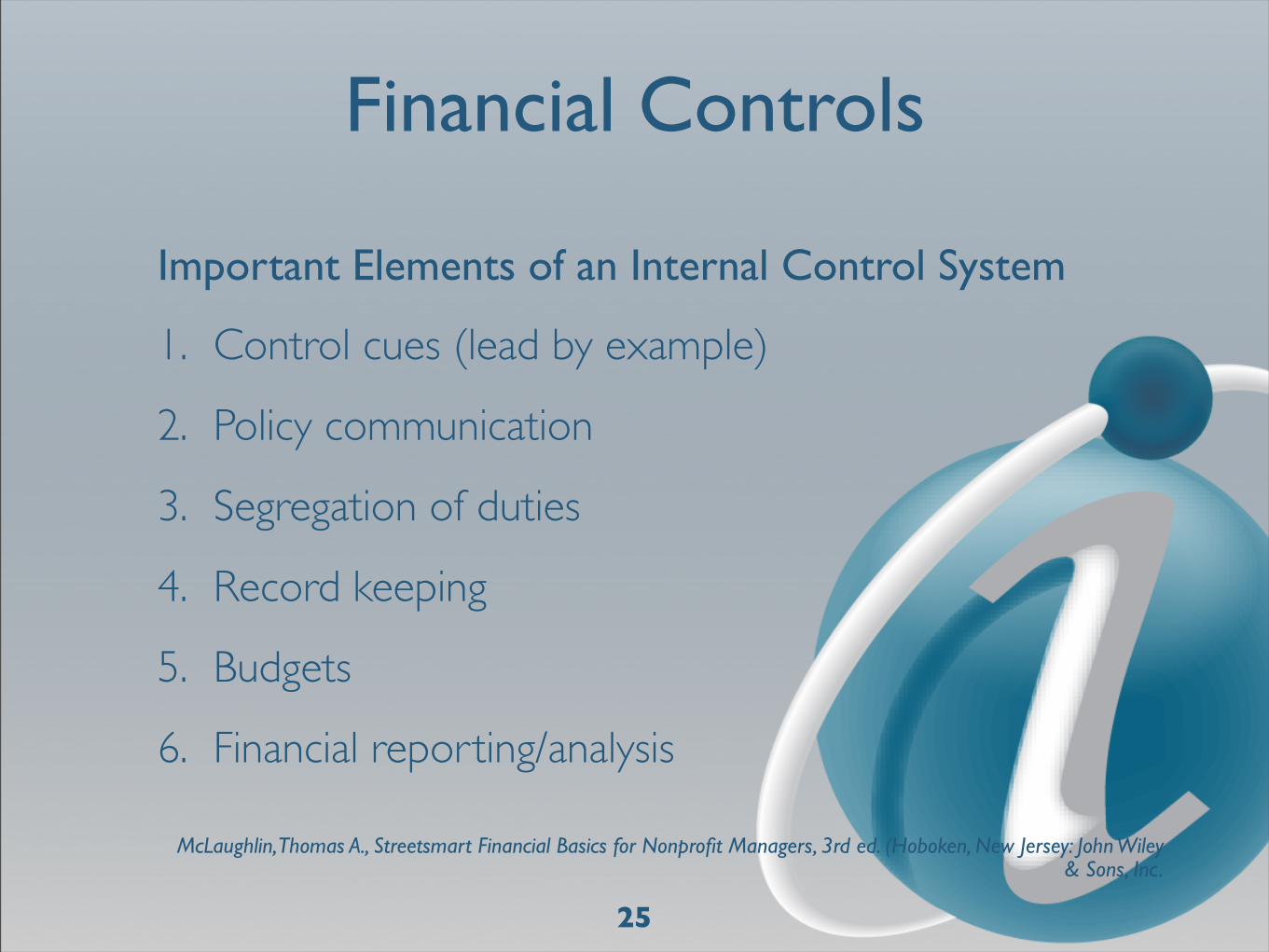

Financial Controls

Important Elements of an Internal Control System

1. Control cues (lead by example)

2. Policy communication

3. Segregation of duties

4. Record keeping

5. Budgets

6. Financial reporting/analysis

25

McLaughlin, Thomas A., Streetsmart Financial Basics for Nonprofit Managers, 3rd ed. (Hoboken, New Jersey: John Wiley & Sons, Inc.

Building Capacity through Financial Management: A Practical Guide by John Cammack

26

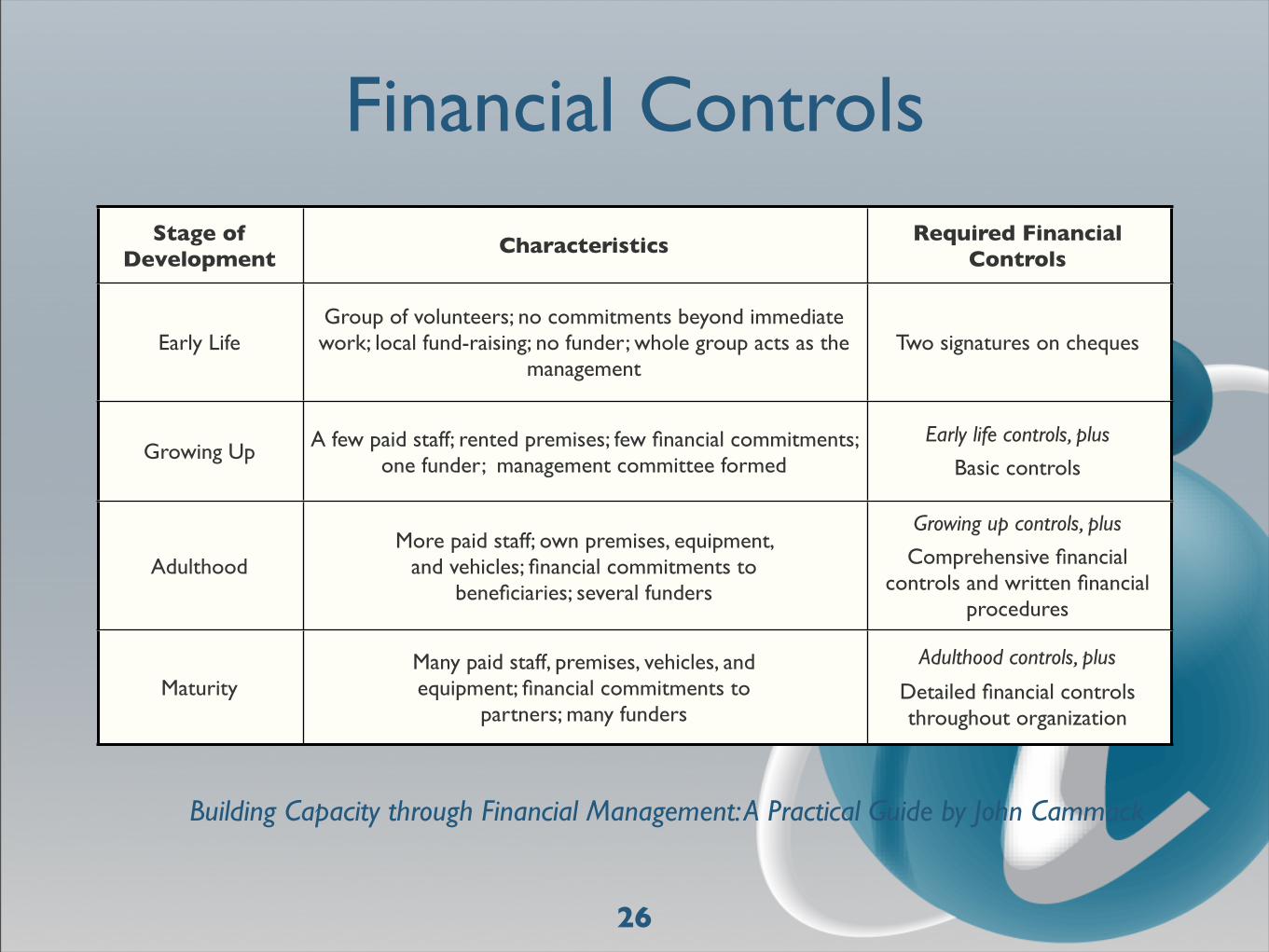

Financial ControlsStage of

DevelopmentCharacteristics Required Financial

Controls

Early LifeGroup of volunteers; no commitments beyond immediate work; local fund-raising; no funder; whole group acts as the

managementTwo signatures on cheques

Growing Up A few paid staff; rented premises; few financial commitments; one funder; management committee formed

Early life controls, plus

Basic controls

AdulthoodMore paid staff; own premises, equipment,

and vehicles; financial commitments to beneficiaries; several funders

Growing up controls, plus

Comprehensive financial controls and written financial

procedures

MaturityMany paid staff, premises, vehicles, and equipment; financial commitments to

partners; many funders

Adulthood controls, plus

Detailed financial controls throughout organization

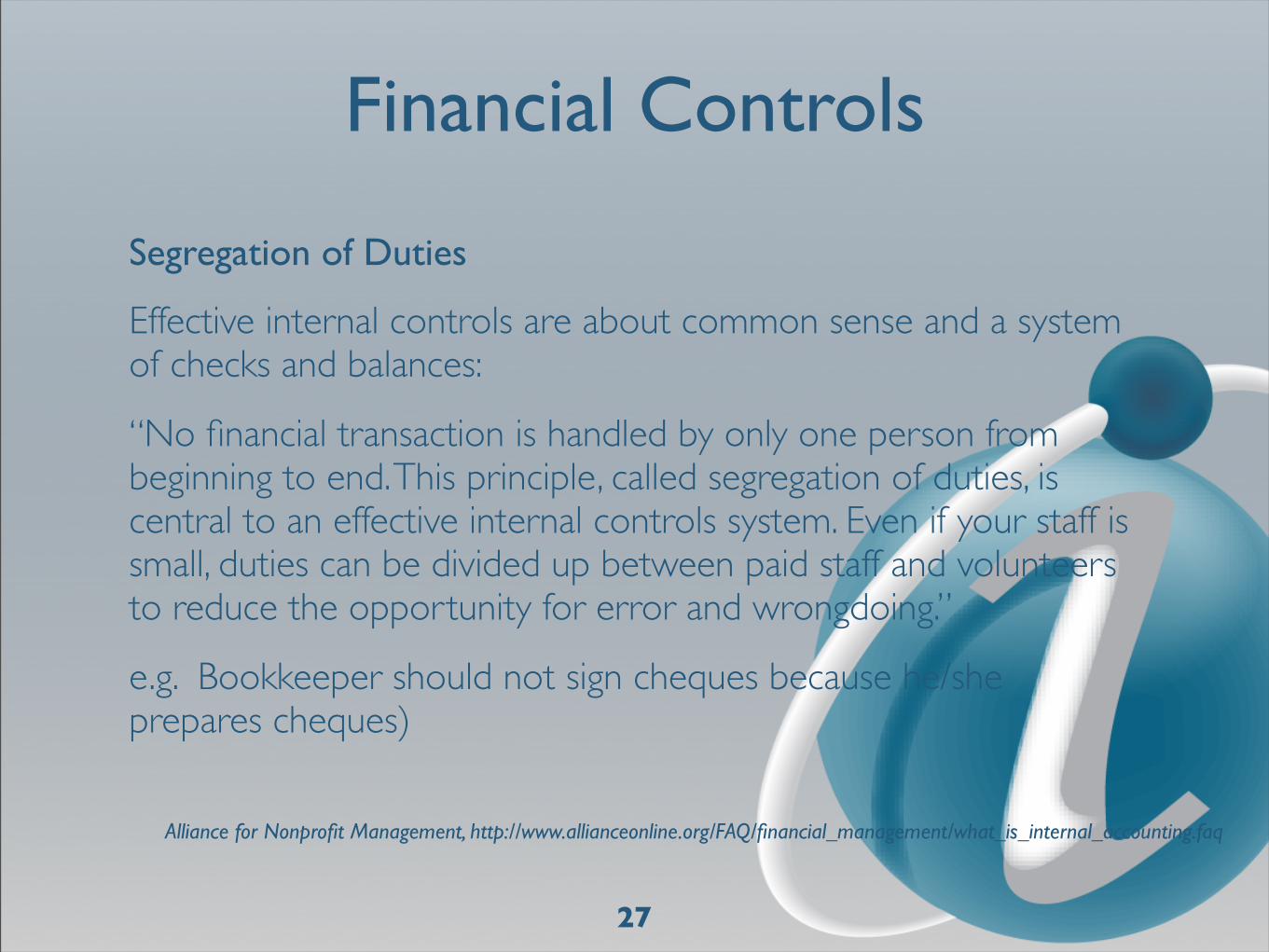

Segregation of Duties

Effective internal controls are about common sense and a system of checks and balances:

“No financial transaction is handled by only one person from beginning to end. This principle, called segregation of duties, is central to an effective internal controls system. Even if your staff is small, duties can be divided up between paid staff and volunteers to reduce the opportunity for error and wrongdoing.”

e.g. Bookkeeper should not sign cheques because he/she prepares cheques)

27

Alliance for Nonprofit Management, http://www.allianceonline.org/FAQ/financial_management/what_is_internal_accounting.faq

Financial Controls

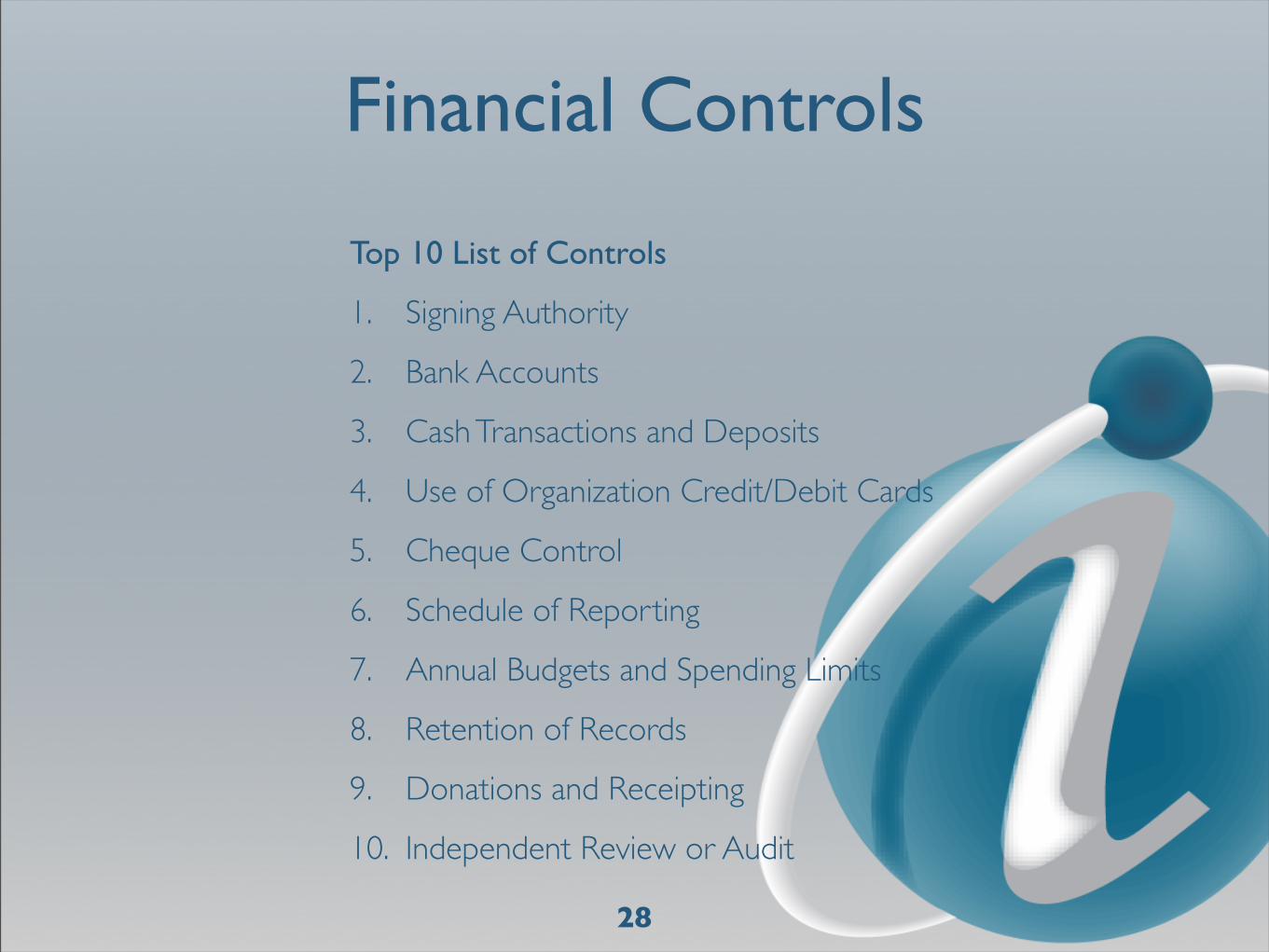

Top 10 List of Controls

1. Signing Authority

2. Bank Accounts

3. Cash Transactions and Deposits

4. Use of Organization Credit/Debit Cards

5. Cheque Control

6. Schedule of Reporting

7. Annual Budgets and Spending Limits

8. Retention of Records

9. Donations and Receipting

10. Independent Review or Audit

28

Financial Controls

1. Cash Transactions and Deposits

• Receiving, handling, and logging (segregation of duties)

• Endorsement of cheques

• Security (pre-deposit and at deposit)

• Cash collection at off-site events

• Petty cash/program advances

2. Use of Organization Credit/Debit Cards

• Organization cards vs. personal cards

• Eligibility and issuance

• Types of purchases

• Limits and approvals

• Transactions, receipts and statements

29

Financial Controls

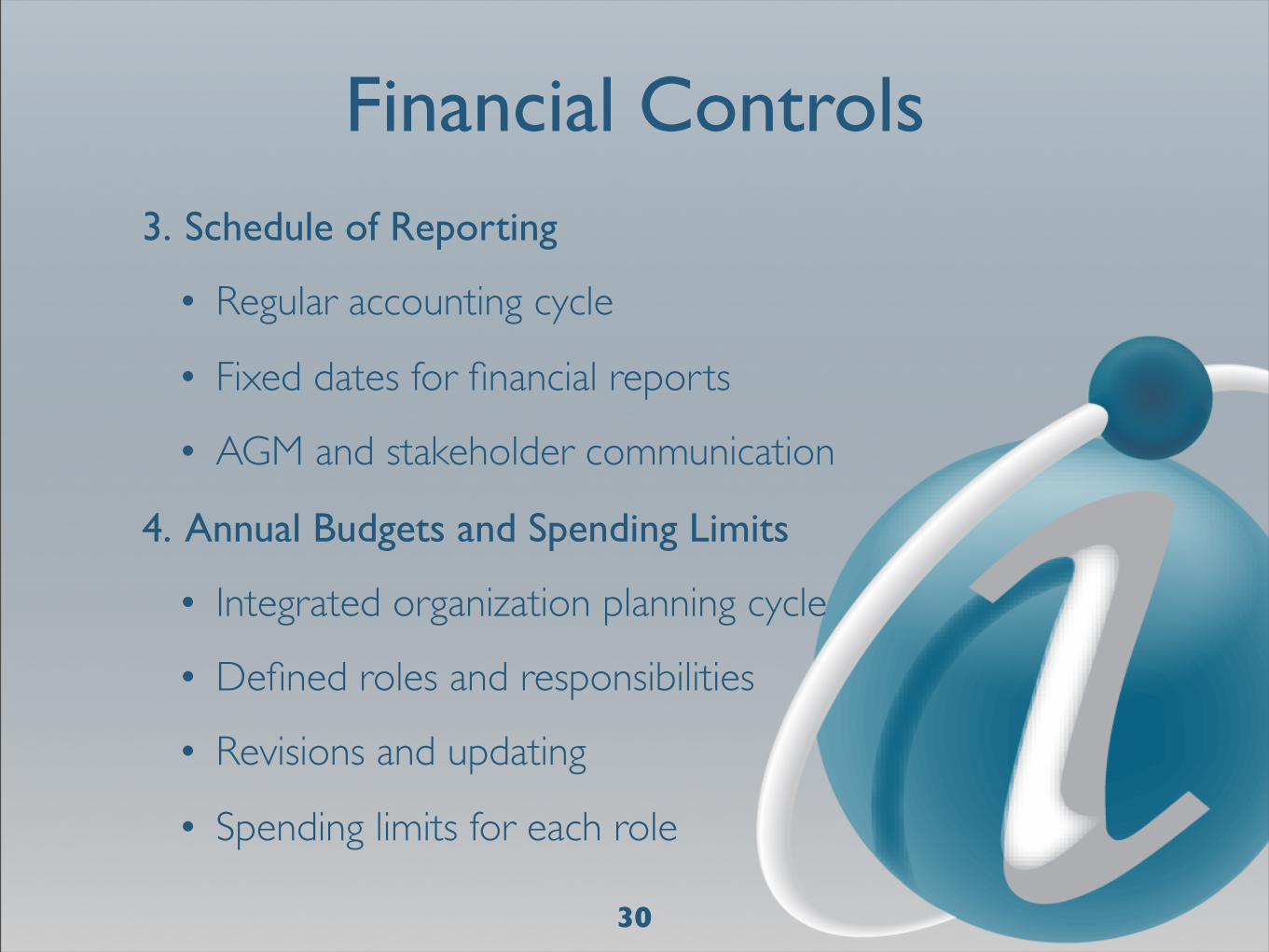

3. Schedule of Reporting

• Regular accounting cycle

• Fixed dates for financial reports

• AGM and stakeholder communication

4. Annual Budgets and Spending Limits

• Integrated organization planning cycle

• Defined roles and responsibilities

• Revisions and updating

• Spending limits for each role

30

Financial Controls

Important, related controls:

• Insurance coverage

• Business expense claims (travel, meals, mileage)

• Contractual/lease obligations

• Technology (passwords, asset security)

• Procurement/tendering

• Trusteeships and partnering

• Reserve funds (number, type, calculation of requirements)

• Finance committee

• Business continuity and disaster recovery planning

31

Financial Controls

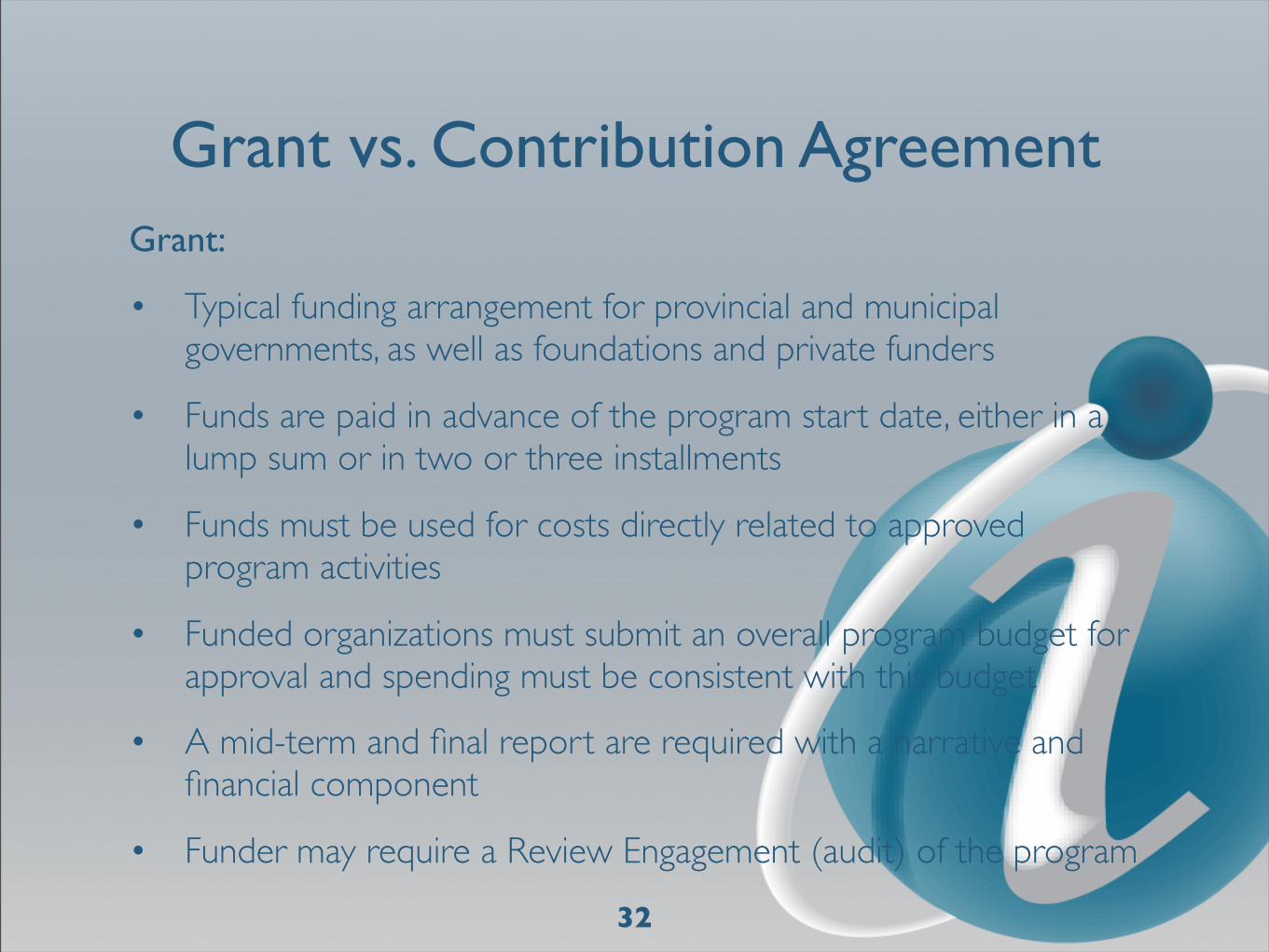

Grant vs. Contribution AgreementGrant:

• Typical funding arrangement for provincial and municipal governments, as well as foundations and private funders

• Funds are paid in advance of the program start date, either in a lump sum or in two or three installments

• Funds must be used for costs directly related to approved program activities

• Funded organizations must submit an overall program budget for approval and spending must be consistent with this budget

• A mid-term and final report are required with a narrative and financial component

• Funder may require a Review Engagement (audit) of the program

32

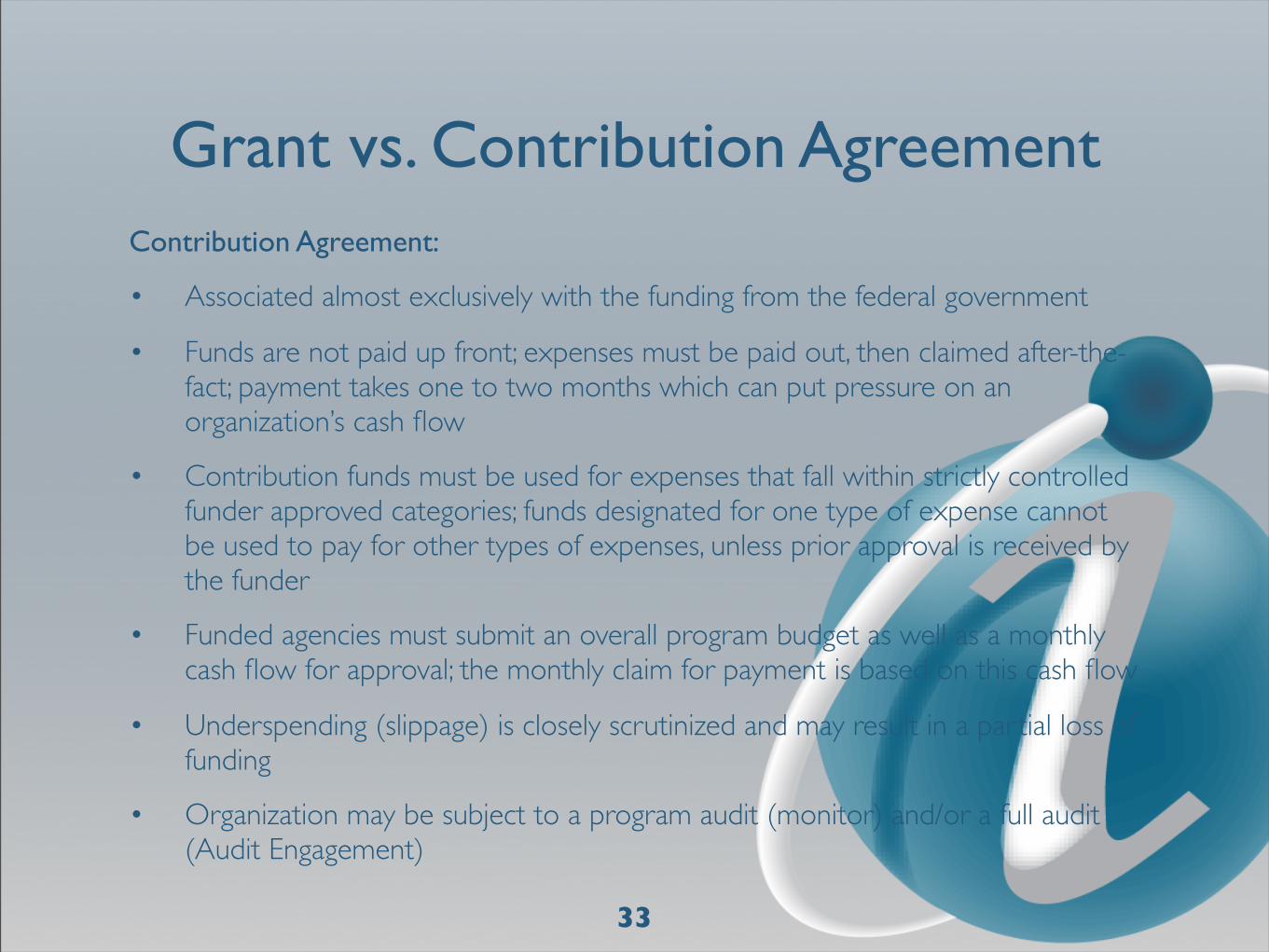

Grant vs. Contribution AgreementContribution Agreement:

• Associated almost exclusively with the funding from the federal government

• Funds are not paid up front; expenses must be paid out, then claimed after-the-fact; payment takes one to two months which can put pressure on an organization’s cash flow

• Contribution funds must be used for expenses that fall within strictly controlled funder approved categories; funds designated for one type of expense cannot be used to pay for other types of expenses, unless prior approval is received by the funder

• Funded agencies must submit an overall program budget as well as a monthly cash flow for approval; the monthly claim for payment is based on this cash flow

• Underspending (slippage) is closely scrutinized and may result in a partial loss of funding

• Organization may be subject to a program audit (monitor) and/or a full audit (Audit Engagement)

33

Principles of CIC FundingCitizenship and Immigration Canada:

• Will reimburse for approved, eligible costs associated with contracted services to eligible clients

• Is not intended to be the sole funding machine behind an organization

• Is not the employer and will not pay costs such as termination pay, severance or unused benefit entitlements

• Will not pay cancellation costs associated with third-party service contracts or lease agreements

• Will not guarantee continued funding beyond current cycle

• Can cancel or reduce its commitment if available funds are reduced by Parliament

34

Process for CIC Claims• Cost must be incurred and paid prior to claiming

• Costs can be claimed only if they relate to a particular line item on the Contribution Agreement

• Claimed amounts must be net of any discounts, rebates or off-setting income

• Maximum amounts (any line item) indicated on the Contribution Agreement cannot be exceeded without prior written approval by CIC

• Funds can be moved from one line item to another up to $1,000 (must be communicated to CIC Settlement Officer)

• All claimed amounts must be substantiated by supporting documents

• Claims are due by the 10th* of each month on, for the previous month

* Year-end reports typically are due earlier in the month

35

Monthly CIC Reporting Requirements

36

• Due by the 10th* of each month, for the previous month:

• Claim Form

• Statistical Form

• Activity Report

• CIC Forecast of Cash Flow/Variance Report (If applicable)

• CIC Slippage Report (If applicable)

* Year-end reports typically are due earlier in the month

Form provided by CIC

• Cannot generate a surplus from funded programs; any unspent funds must be returned to the funder

• Funders may consider under spending (slippage) or overspending (overage) to be an indication of poor financial management

• Funder will not automatically top-up an organization’s funding because of overspending

37

Managing Slippage and Overages

• Sound budget development and regular budget monitoring are the best ways to prevent slippage and overages

• Forecast program expenses at the halfway point of the program year to anticipate problems and make corrections to spending

• If slippage or overages are unavoidable, communicate to supervisor and funder in advance of the variance becoming significant

• Be prepared to offer an explanation and action plan to the funder for slippage and overages

38

Managing Slippage and Overages

Managing Slippage and Overages

Identify

Analyze

PlanCommunicate

Act

UnderstandCause(s) for Variance(s)

Develop a Plan to Resolve Variance(s)Communicate Plan

to CIC (Activity Report)

Prepare Claim and Variance Report

Take Action to Resolve Slippage or Overages

39

Common Reasons for CIC Claim Problems

40

• Claims for expenses that are incurred but not paid

• Claims based on cash flow, instead of actual expenditures

• Over claiming maximum amount allowed in Contribution Agreement

• Claims for costs that have not been approved by CIC (seek approvals in advance and keep all documentation)

• Claims based upon inappropriate ‘movement’ of costs from one line item to another

• Lack of supporting documentation for claimed amount

• Claimed amount not directly related to the program or otherwise considered ineligible

• Claims based upon costs in an Amendment that is not finalized

CIC Program Monitor• Monitors are mini-audits of CIC-funded programs, conducted by the Settlement Officer;

they typically cover a specific time frame (2 - 4 months)

• Advanced preparation is important to a satisfactory outcome:

‣ Make available all supporting documentation associated with claimed expenses, relevant bookkeeping records, and lease agreements for funded space and equipment

‣ For all funded staff, make available payroll records and personnel policies

‣ Provide rationale for allocating Central Administration costs

‣ Provide details/logs to substantiate claims for participant/client travel and program staff travel

‣ Provide a current list of funded capital assets with applicable details

‣ If the funded item is cost-shared with other funders, provide details on rationale for claimed amount

‣ Demonstrate how the HST claim is calculated, taking into consideration eligible HST rebates

‣ Provide copies of correspondence or file notes relating to CIC discussions/approvals for special arrangements, changes or modifications

41

Thank You

• Questions?

• Session Evaluation

• Finance Manual

• Blog

• Contact Information:

‣ Gina Vergilio

‣ www.gvconsult.ca

42