Embed Size (px)

Citation preview

Financial management: Lecture 2

Financial marketsand review of some

concepts

Some important concepts

Financial management: Lecture 2

Today’s agenda

Some administrative issues Understand financial markets and their functions Understand the concept of the cost of capital and

the time value of money Learn how to compare:

• Cash flows or payments you get today

• Cash flows or payments you get in the future

Financial management: Lecture 2

Course materials

I have posted all the materials on my website: http://online.sfsu.edu/~li123456.

I am sorry that I don’t post things on I-learn

Financial management: Lecture 2

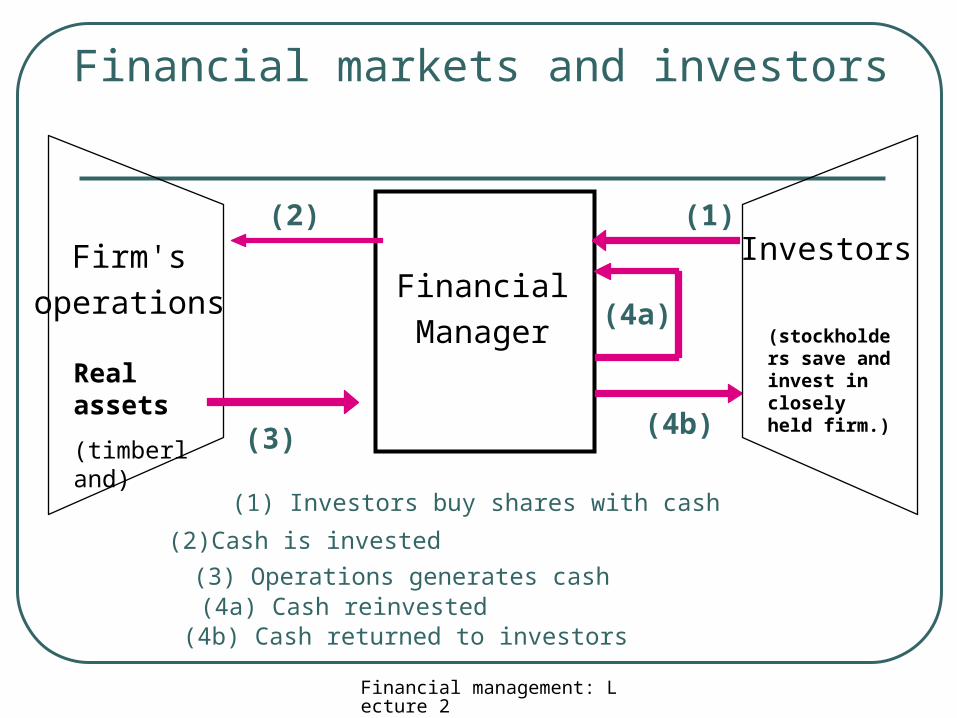

Financial

Manager

Firm's

operations

Investors

(1) Investors buy shares with cash

(1)

(2)Cash is invested

(2)

(3) Operations generates cash

(3)

(4a) Cash reinvested

(4a)

(4b) Cash returned to investors

(4b)

Financial markets and investors

Real assets

(timberland)

(stockholders save and invest in closely held firm.)

Financial management: Lecture 2

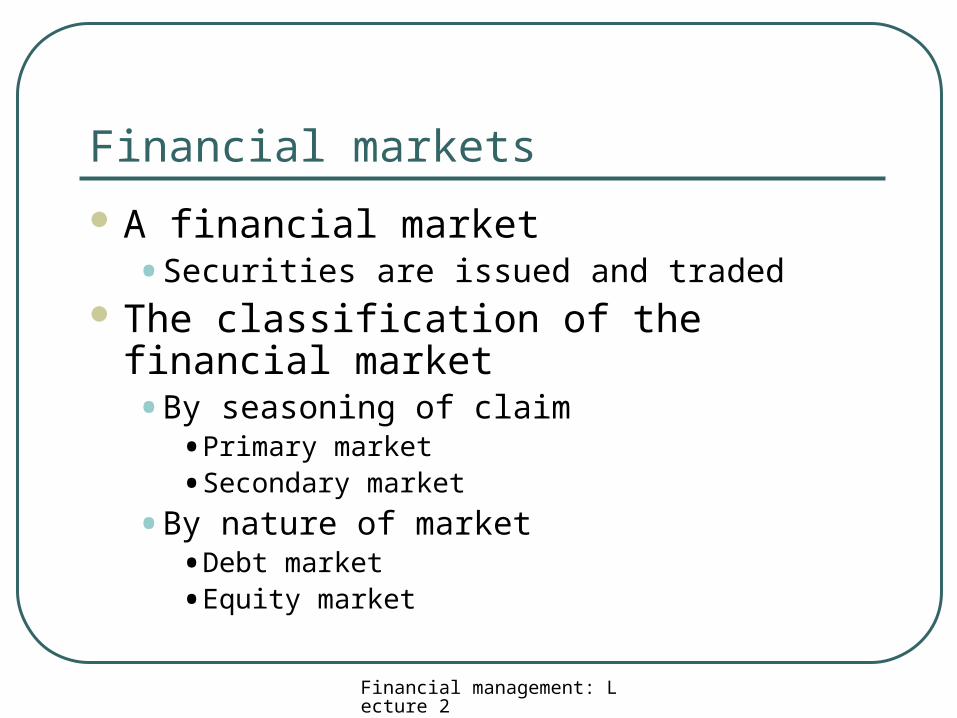

Financial markets

A financial market • Securities are issued and traded

The classification of the financial market• By seasoning of claim

• Primary market

• Secondary market

• By nature of market• Debt market

• Equity market

Financial management: Lecture 2

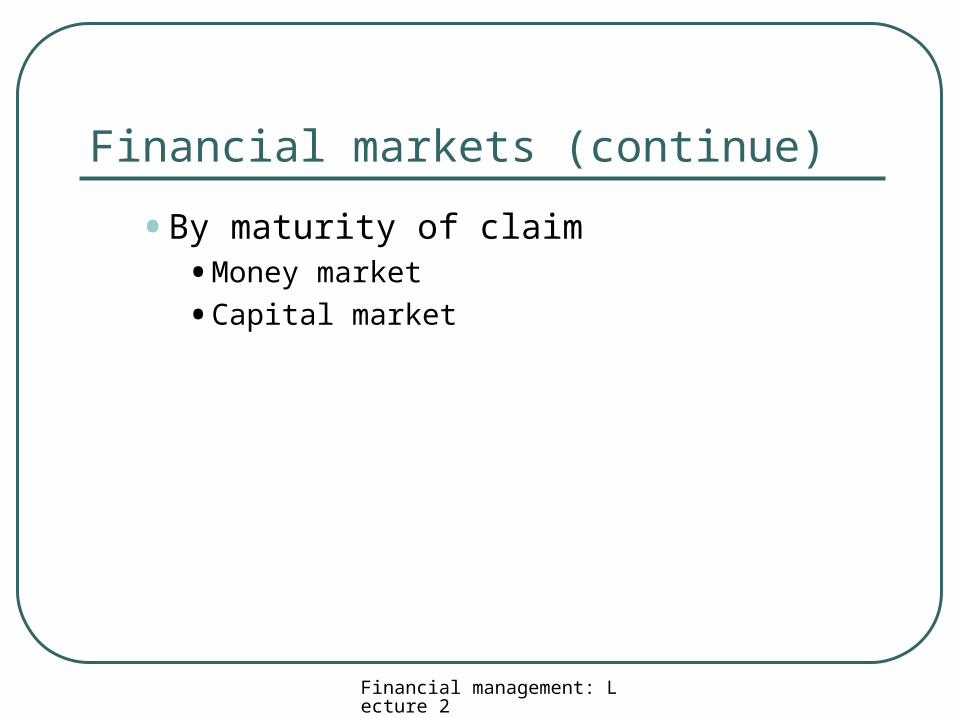

Financial markets (continue)

• By maturity of claim• Money market

• Capital market

Financial management: Lecture 2

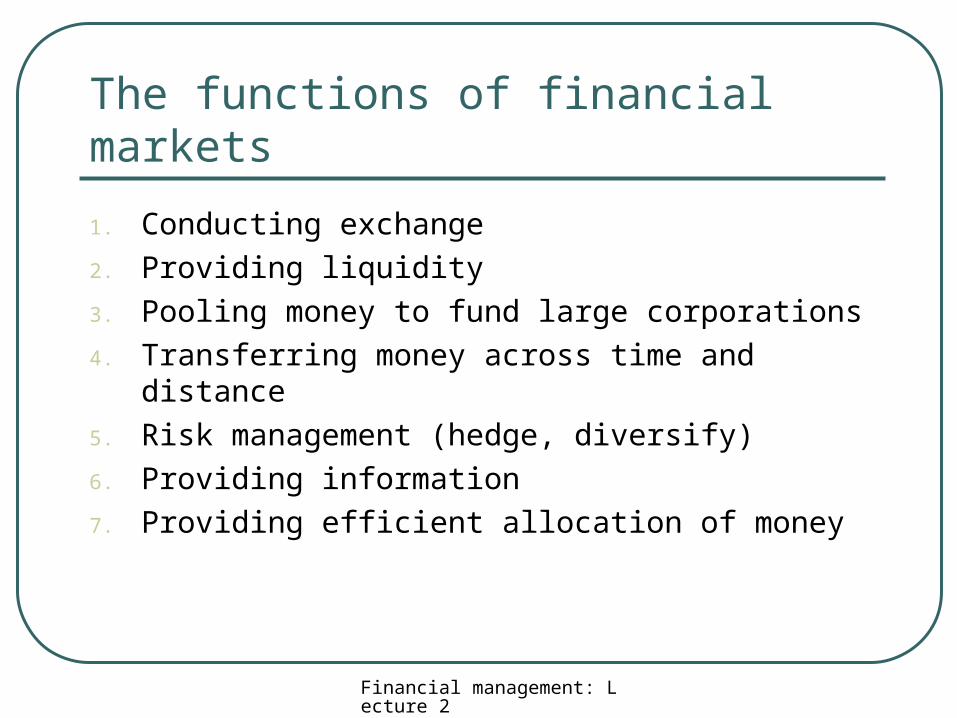

The functions of financial markets

1. Conducting exchange

2. Providing liquidity

3. Pooling money to fund large corporations

4. Transferring money across time and distance

5. Risk management (hedge, diversify)

6. Providing information

7. Providing efficient allocation of money

Financial management: Lecture 2

Conducting exchange

What does it mean ? Examples

Financial management: Lecture 2

Providing liquidity

What does this mean? Examples

Financial management: Lecture 2

Pooling money to fund large corporation investments

What does this mean? Examples

Financial management: Lecture 2

Transferring money across time and distance

What does this mean? Examples

Financial management: Lecture 2

Risk management

What does this mean? Examples

Financial management: Lecture 2

Providing information

What does this mean? Examples

Financial management: Lecture 2

Providing efficient allocation of money

What does this mean? Examples

Financial management: Lecture 2

The cost of capital

The cost of capital is a very important concept in capital budgeting.

It links investment opportunities in financial markets and investment opportunities in real assets markets.

Financial management: Lecture 2

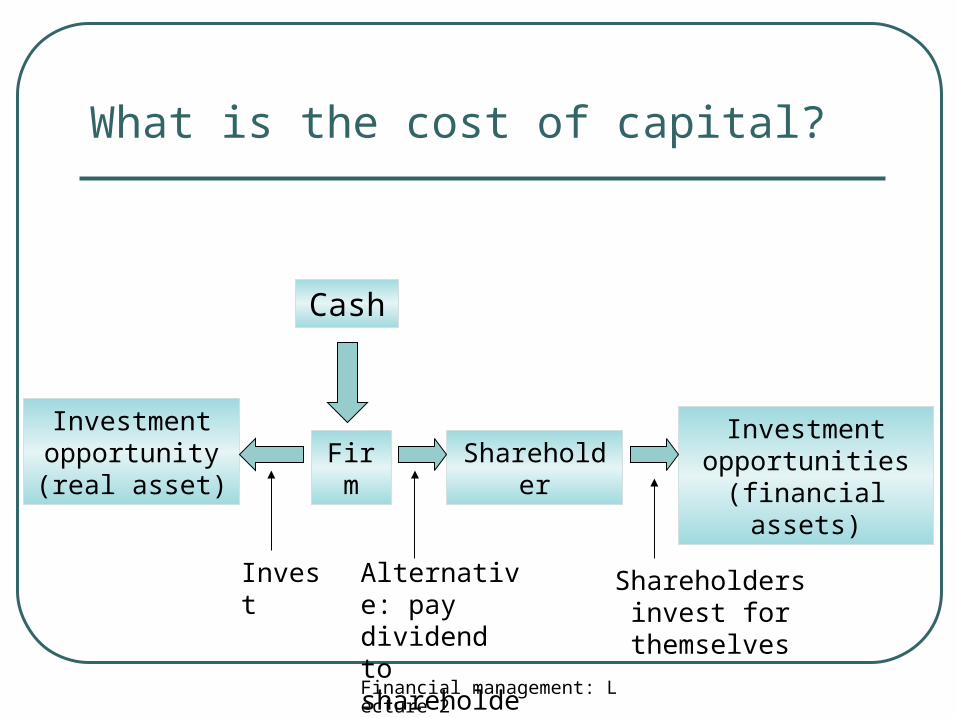

What is the cost of capital?

Cash

Investment opportunity (real

asset)Firm Shareholder

Investment opportunities

(financial assets)

Invest Alternative: pay dividend to shareholders

Shareholders invest for themselves

Financial management: Lecture 2

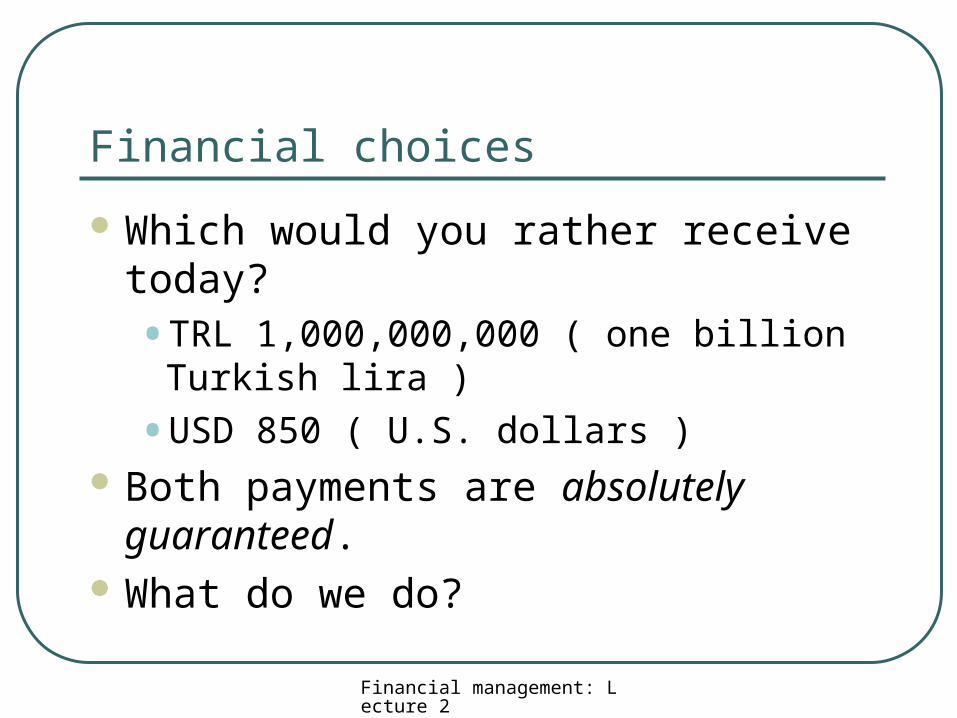

Financial choices

Which would you rather receive today?

• TRL 1,000,000,000 ( one billion Turkish lira )

• USD 850 ( U.S. dollars ) Both payments are absolutely

guaranteed. What do we do?

Financial management: Lecture 2

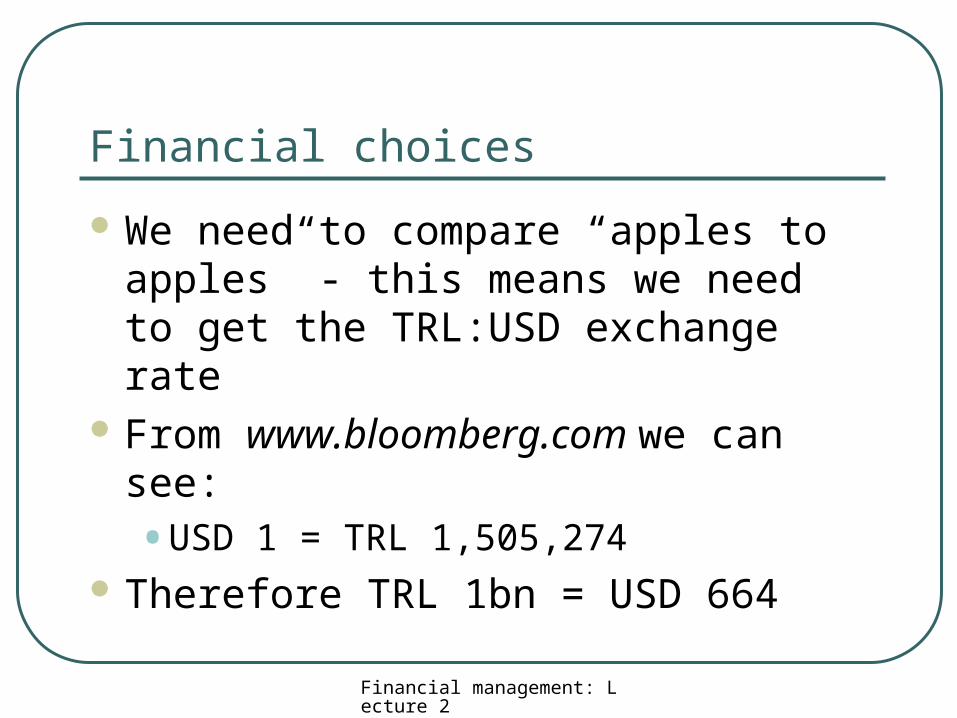

Financial choices

We need to compare “apples to apples” - this means we need to get the TRL:USD exchange rate

From www.bloomberg.com we can see:

• USD 1 = TRL 1,505,274 Therefore TRL 1bn = USD 664

Financial management: Lecture 2

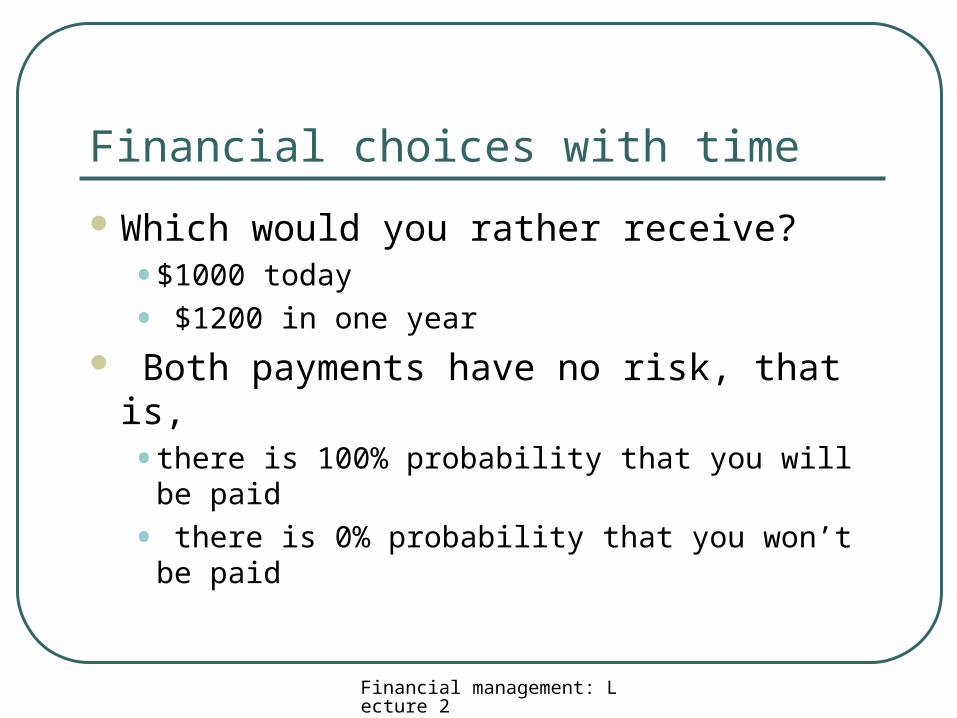

Financial choices with time

Which would you rather receive?• $1000 today

• $1200 in one year

Both payments have no risk, that is, • there is 100% probability that you will be paid

• there is 0% probability that you won’t be paid

Financial management: Lecture 2

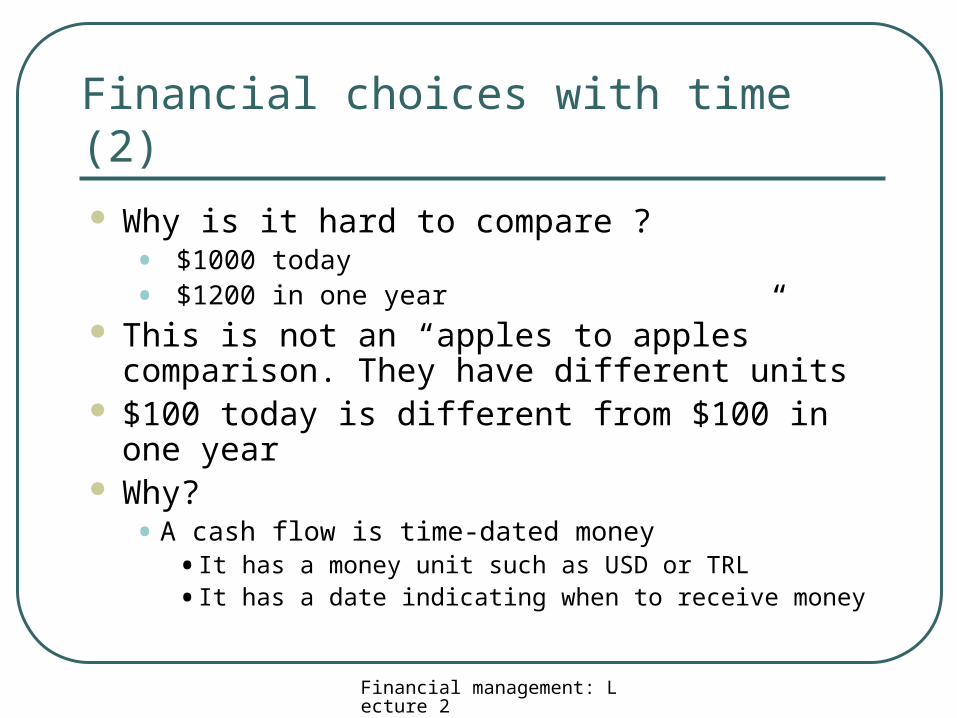

Financial choices with time (2)

Why is it hard to compare ?• $1000 today

• $1200 in one year This is not an “apples to apples” comparison.

They have different units $100 today is different from $100 in one year Why?

• A cash flow is time-dated money• It has a money unit such as USD or TRL

• It has a date indicating when to receive money

Financial management: Lecture 2

Present value

In order to have an “apple to apple” comparison, we convert future payments to the present values• this is like converting money in TRL to money in USD

• Certainly, we can also convert the present value to the future value to compare payments we get today with payments we get in the future.

• Although these two ways are theoretically the same, but the present value way is more important and has more applications, as to be shown in stock and bond valuations.

Financial management: Lecture 2

Present value (2)

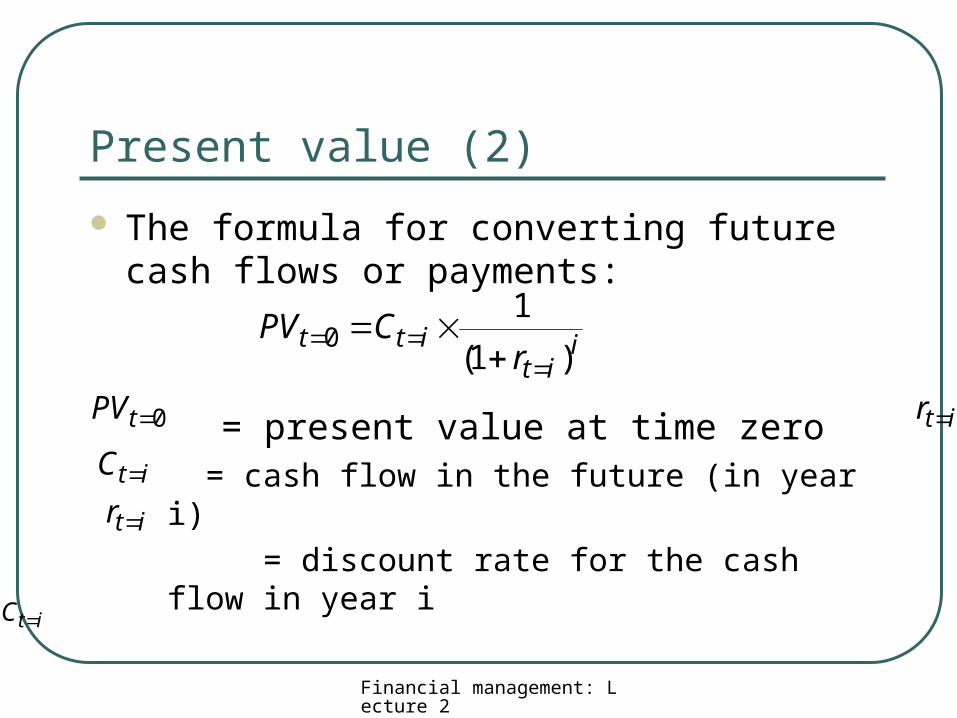

The formula for converting future cash flows or payments:

= present value at time zero = cash flow in the future (in year i)

= discount rate for the cash flow in year i

iit

ittr

CPV)1(

10

0tPV

itr

itC

itC

itr

Financial management: Lecture 2

Example 1

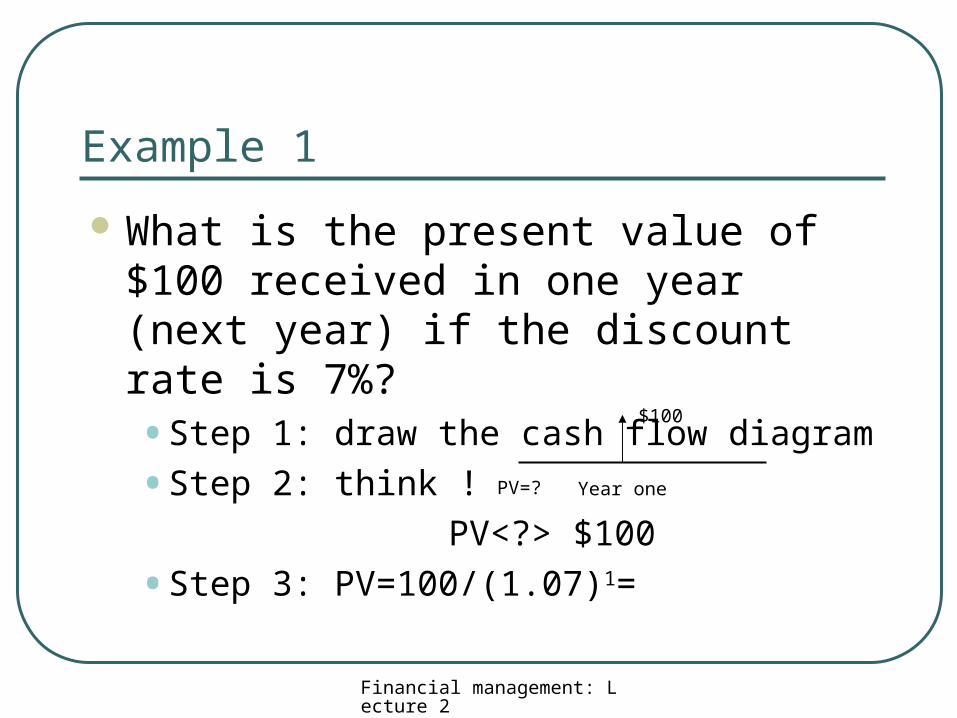

What is the present value of $100 received in one year (next year) if the discount rate is 7%?• Step 1: draw the cash flow diagram

• Step 2: think !

PV<?> $100

• Step 3: PV=100/(1.07)1=

Year one

$100

PV=?

Financial management: Lecture 2

Example 2

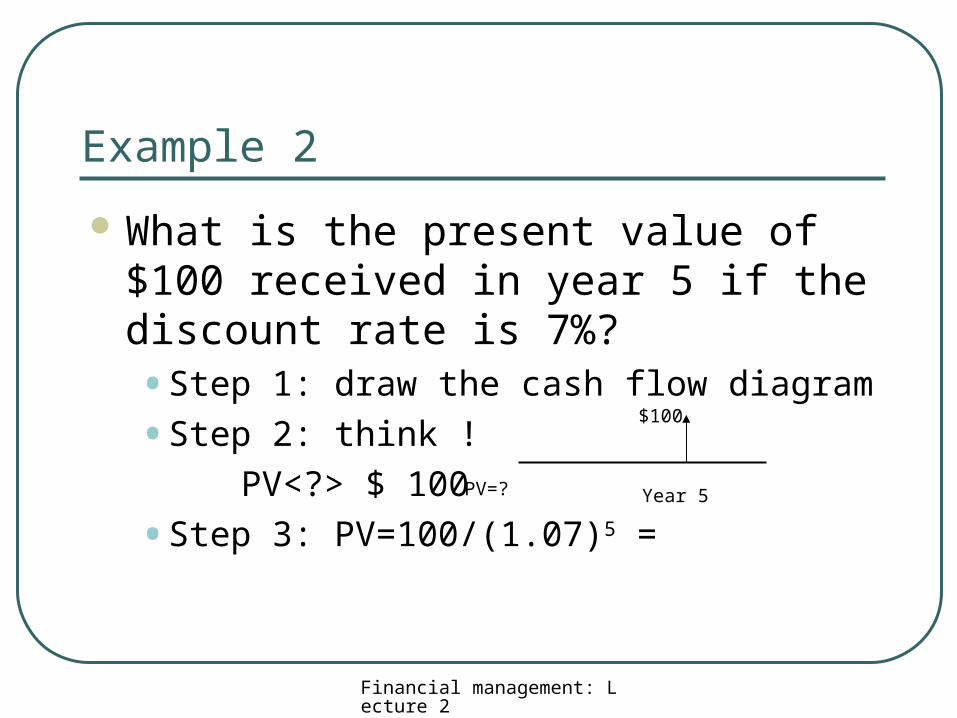

What is the present value of $100 received in year 5 if the discount rate is 7%?• Step 1: draw the cash flow diagram

• Step 2: think !

PV<?> $ 100

• Step 3: PV=100/(1.07)5 = Year 5

$100

PV=?

Financial management: Lecture 2

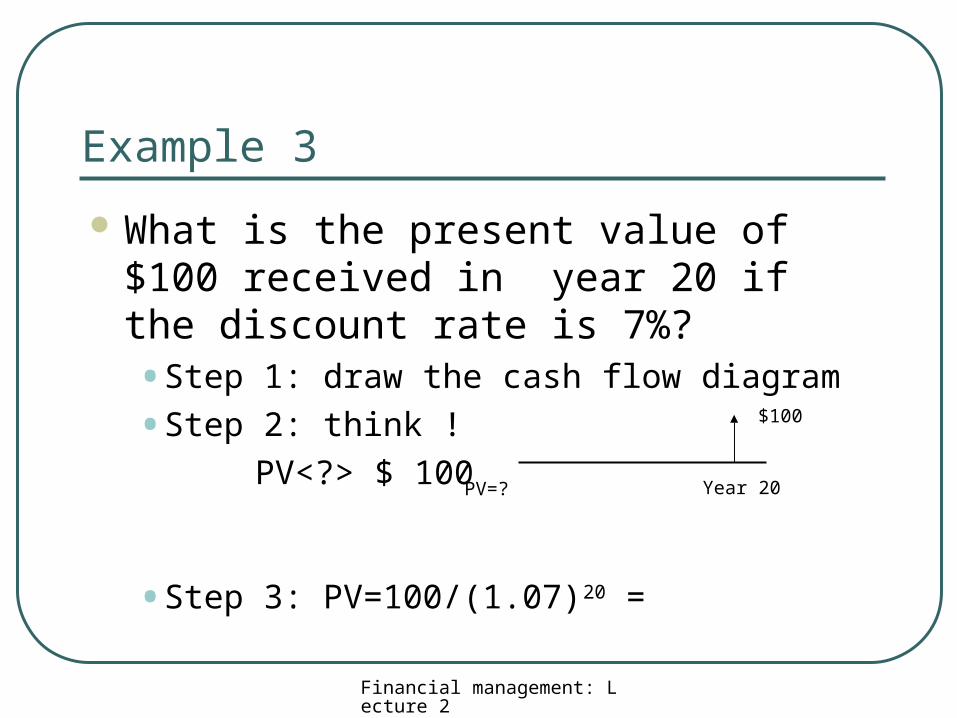

Example 3

What is the present value of $100 received in year 20 if the discount rate is 7%?• Step 1: draw the cash flow diagram

• Step 2: think !

PV<?> $ 100

• Step 3: PV=100/(1.07)20 =

Year 20

$100

PV=?

Financial management: Lecture 2

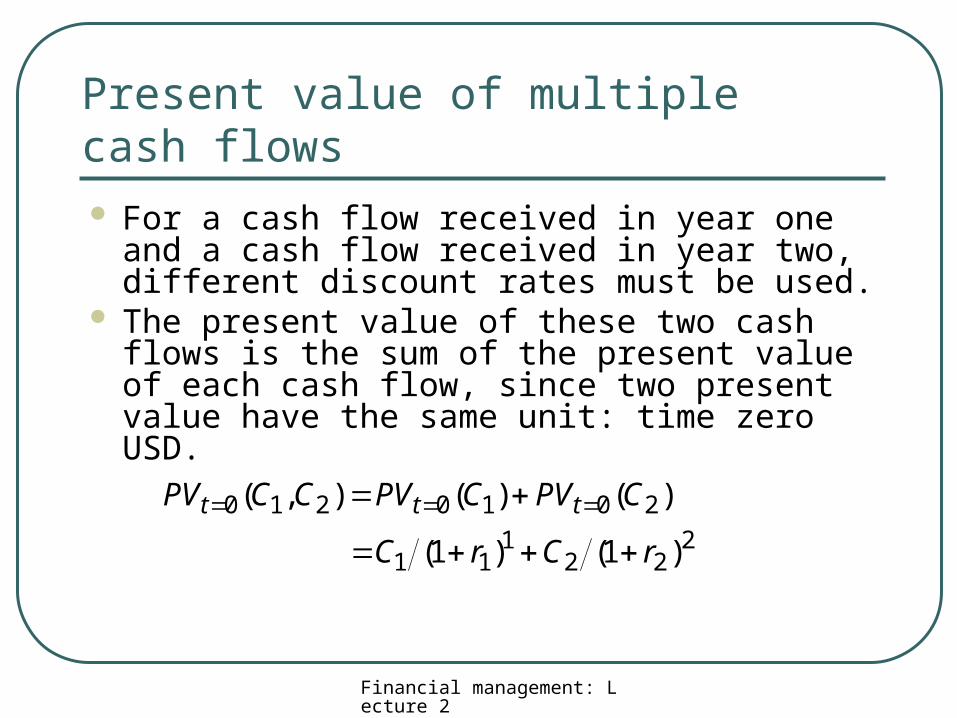

Present value of multiple cash flows For a cash flow received in year one and a

cash flow received in year two, different discount rates must be used.

The present value of these two cash flows is the sum of the present value of each cash flow, since two present value have the same unit: time zero USD.

2

221

11

2010210

)1()1(

)()(),(

rCrC

CPVCPVCCPV ttt

Financial management: Lecture 2

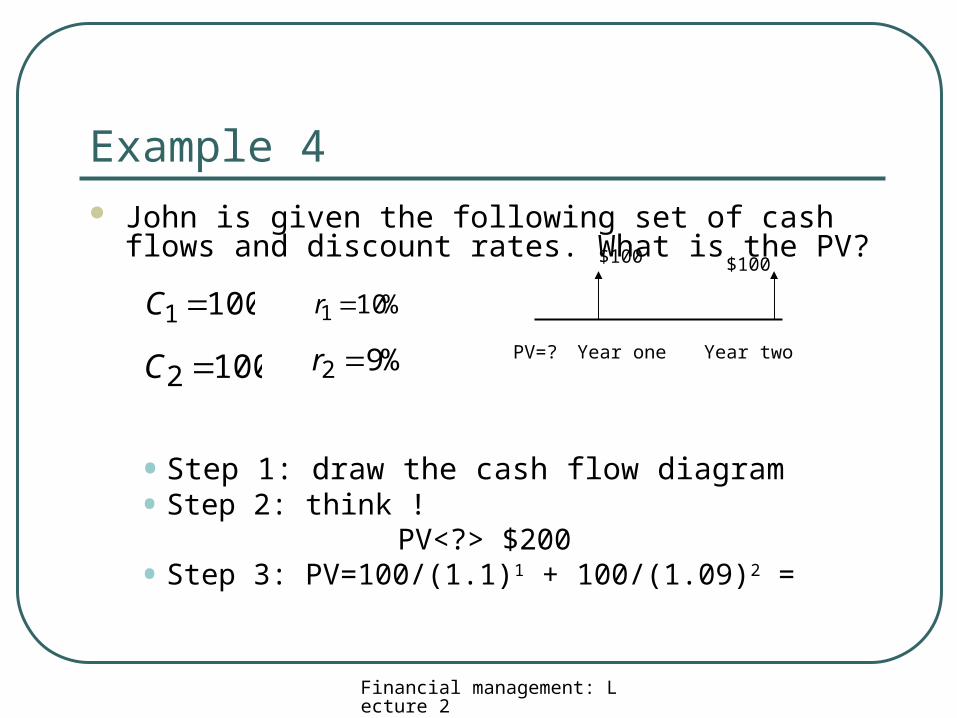

Example 4 John is given the following set of cash flows and

discount rates. What is the PV?

• Step 1: draw the cash flow diagram• Step 2: think ! PV<?> $200• Step 3: PV=100/(1.1)1 + 100/(1.09)2 =

%101 r

Year one

$100

PV=?

1001 C

%92 r1002 C

$100

Year two

Financial management: Lecture 2

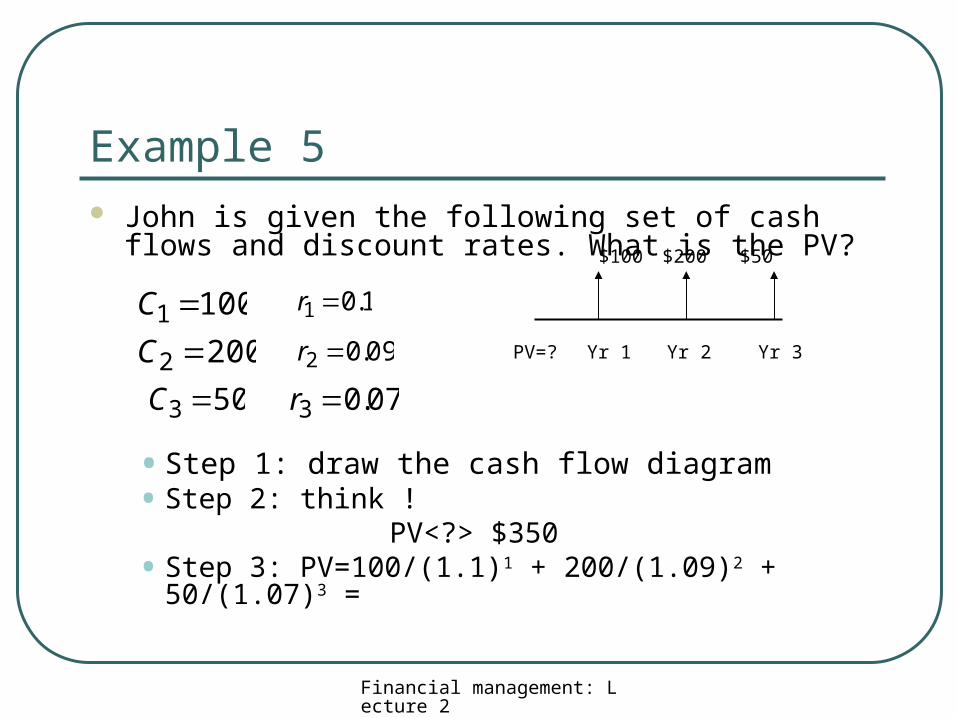

Example 5 John is given the following set of cash flows and

discount rates. What is the PV?

• Step 1: draw the cash flow diagram• Step 2: think ! PV<?> $350• Step 3: PV=100/(1.1)1 + 200/(1.09)2 + 50/(1.07)3 =

503 C

1.01 r

Yr 1

$100

PV=?

1001 C

09.02 r2002 C

$50

Yr 3

07.03 r

Yr 2

$200

Financial management: Lecture 2

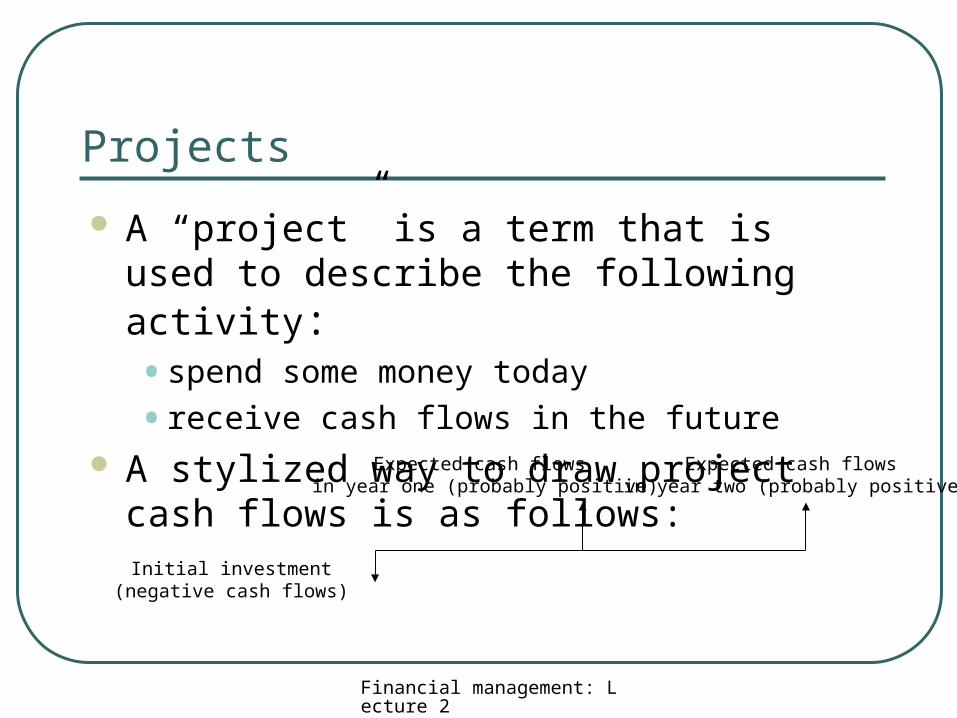

Projects

A “project” is a term that is used to describe the following activity:• spend some money today

• receive cash flows in the future A stylized way to draw project cash flows is

as follows:

Initial investment(negative cash flows)

Expected cash flows in year one (probably positive)

Expected cash flows in year two (probably positive)

Financial management: Lecture 2

Examples of projects An entrepreneur starts a company:

• initial investment is negative cash outflow.

• future net revenue is cash inflow . An investor buys a share of IBM stock

• cost is cash outflow; dividends are future cash inflows. A lottery ticket:

• investment cost: cash outflow of $1

• jackpot: cash inflow of $20,000,000 (with some very small probability…)

Thus projects can range from real investments, to financial investments, to gambles (the lottery ticket).

Financial management: Lecture 2

Firms or companies

A firm or company can be regarded as a set of projects.• capital budgeting is about choosing the best

projects in real asset investments.

How do we know one project is worth taking?

Financial management: Lecture 2

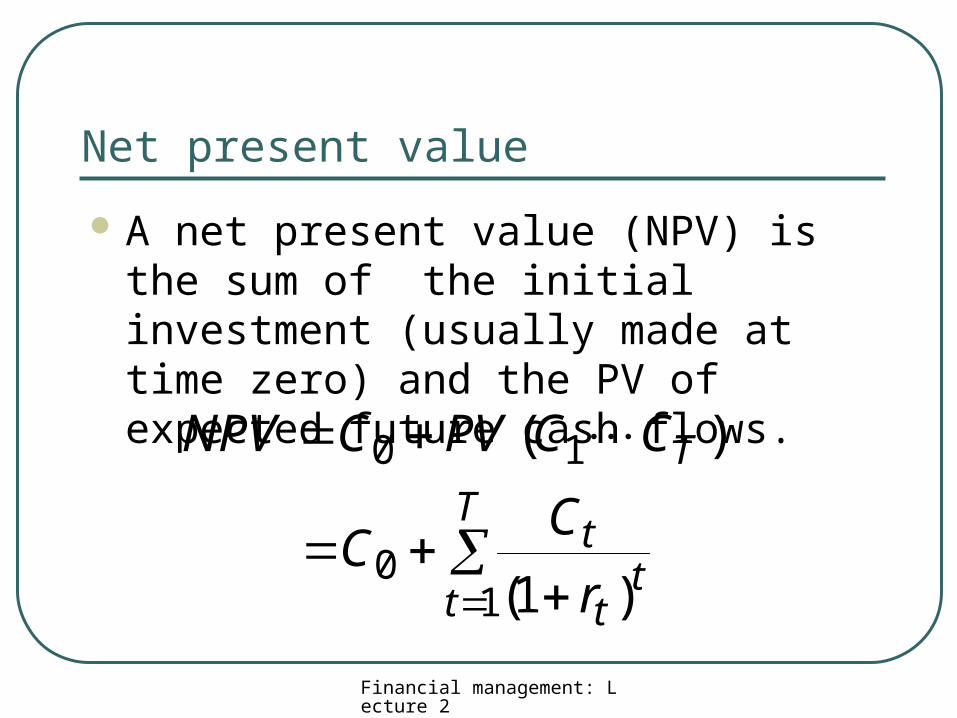

Net present value

A net present value (NPV) is the sum of the initial investment (usually made at time zero) and the PV of expected future cash flows.

T

tt

t

t

T

r

CC

CCPVCNPV

10

10

)1(

)(

Financial management: Lecture 2

NPV rule

If NPV > 0, the manager should go ahead to take the project; otherwise, the manager should not.

Financial management: Lecture 2

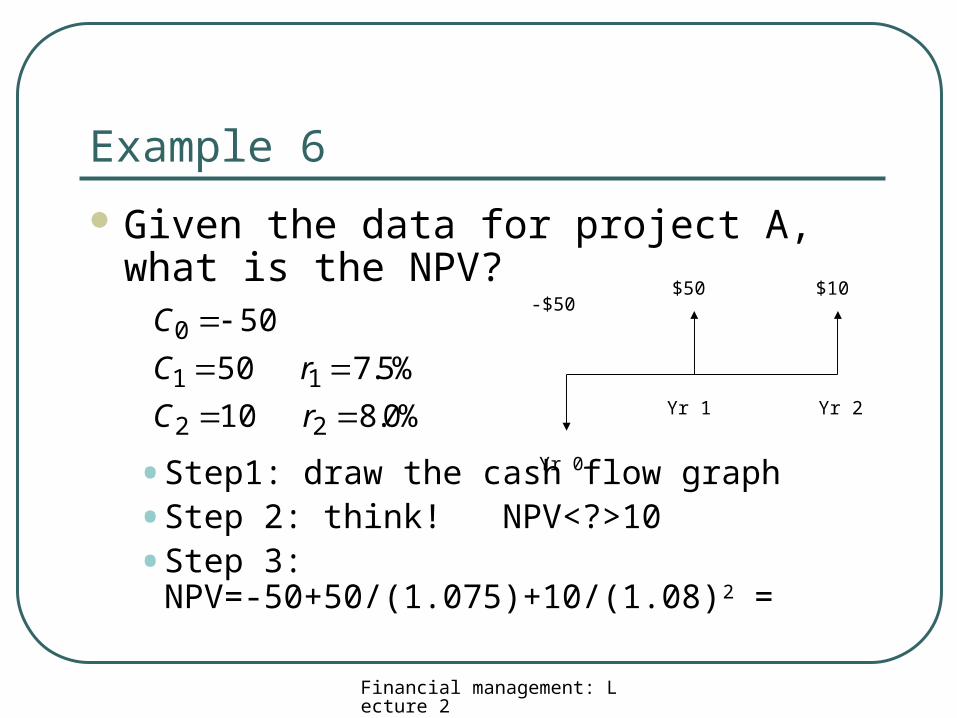

Example 6

Given the data for project A, what is the NPV?

• Step1: draw the cash flow graph

• Step 2: think! NPV<?>10

• Step 3: NPV=-50+50/(1.075)+10/(1.08)2 =

%0.810

%5.750

50

22

11

0

rC

rC

C

Yr 0

Yr 1 Yr 2

$10$50-$50