Embed Size (px)

Citation preview

Financial Market Report

Poland

In cooperation with AUSSENWIRTSCHAFT AUSTRIA.

A U S S E N W I R T S C H A F T A U S T R I A

32

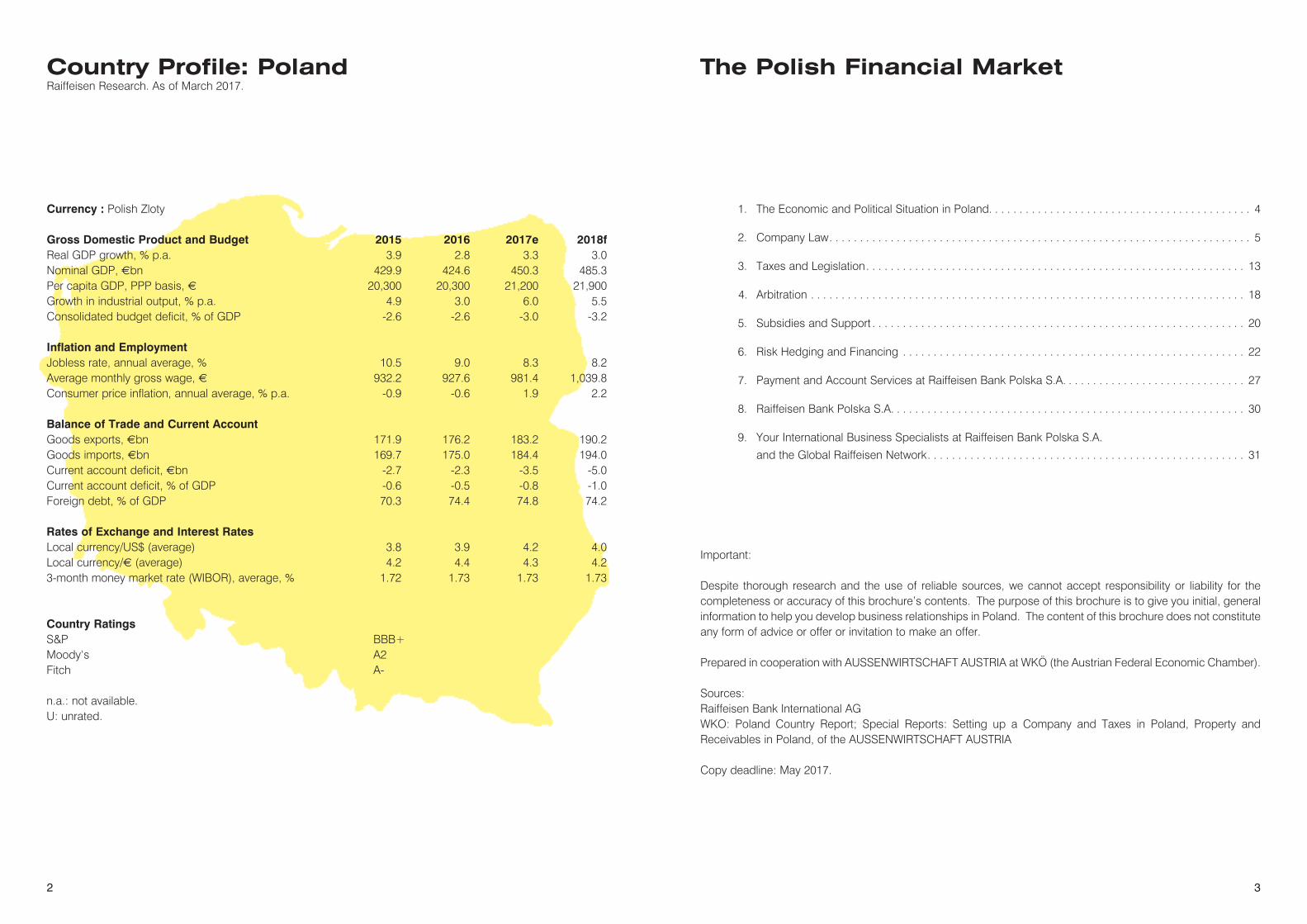

Country Profile: Poland Raiffeisen Research. As of March 2017.

The Polish Financial Market

1. The Economic and Political Situation in Poland. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2. Company Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

3. Taxes and Legislation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

4. Arbitration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

5. Subsidies and Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

6. Risk Hedging and Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

7. Payment and Account Services at Raiffeisen Bank Polska S.A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

8. Raiffeisen Bank Polska S.A. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

9. Your International Business Specialists at Raiffeisen Bank Polska S.A.

and the Global Raiffeisen Network . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Important:

Despite thorough research and the use of reliable sources, we cannot accept responsibility or liability for the completeness or accuracy of this brochure’s contents. The purpose of this brochure is to give you initial, general information to help you develop business relationships in Poland. The content of this brochure does not constitute any form of advice or offer or invitation to make an offer.

Prepared in cooperation with AUSSENWIRTSCHAFT AUSTRIA at WKÖ (the Austrian Federal Economic Chamber).

Sources:Raiffeisen Bank International AGWKO: Poland Country Report; Special Reports: Setting up a Company and Taxes in Poland, Property and Receivables in Poland, of the AUSSENWIRTSCHAFT AUSTRIA

Copy deadline: May 2017.

Currency : Polish Zloty Gross Domestic Product and Budget 2015 2016 2017e 2018fReal GDP growth, % p.a. 3.9 2.8 3.3 3.0Nominal GDP, €bn 429.9 424.6 450.3 485.3Per capita GDP, PPP basis, € 20,300 20,300 21,200 21,900Growth in industrial output, % p.a. 4.9 3.0 6.0 5.5Consolidated budget deficit, % of GDP -2.6 -2.6 -3.0 -3.2 Inflation and Employment Jobless rate, annual average, % 10.5 9.0 8.3 8.2Average monthly gross wage, € 932.2 927.6 981.4 1,039.8Consumer price inflation, annual average, % p.a. -0.9 -0.6 1.9 2.2 Balance of Trade and Current Account Goods exports, €bn 171.9 176.2 183.2 190.2Goods imports, €bn 169.7 175.0 184.4 194.0Current account deficit, €bn -2.7 -2.3 -3.5 -5.0Current account deficit, % of GDP -0.6 -0.5 -0.8 -1.0Foreign debt, % of GDP 70.3 74.4 74.8 74.2 Rates of Exchange and Interest Rates Local currency/US$ (average) 3.8 3.9 4.2 4.0Local currency/€ (average) 4.2 4.4 4.3 4.23-month money market rate (WIBOR), average, % 1.72 1.73 1.73 1.73

Country Ratings S&P BBB+ Moody‘s A2Fitch A-

n.a.: not available. U: unrated.

54

Poland has a GDP per capita equivalent to EUR 11,238, which is approximately 35% of GDP per capita in the Eurozone; in terms of purchasing power parity, this corresponds to EUR 20,300, or approximately 65% of GDP per capita in the Eurozone. GDP per capita has increased markedly in recent years. In 2016, GDP in Poland grew by 2.8% compared to the previous year. Economic growth has therefore decreased somewhat compared to the previous years, which saw strong growth of over 3%. This moderate economic downturn was mainly caused by weak domestic investment activity. We expect an increase in GDP in 2017 and 2018 of 3.3% and 3.0% compared to the respective previous years. This outlook is supported by increasing investments. Average inflation for 2016 was -0.6% compared to the previous year. In view of this deflationary development, the “growth in price levels” was significantly below the long-term trend. We expect inflation to return in 2017 and increase to around 2%. The unemployment rate in 2016 was 9.0% (which included significant structural components).

We expect unemployment to fall further during 2017 and 2018, which, in turn, could contribute to increased inflationary pressure. The budget deficit for 2016 amounted to 2.6% of GDP. Considering the current economic policy orientation and the structural fiscal relaxation measures which have already been put in place, we expect the budget deficit to increase slightly in 2017 and 2018. However, the national debt ratio was low in 2016, at 52.8% of GDP (i.e. a lot lower than the EU benchmark of 60%). In view of the above described development in the budget deficit, we expect the national debt ratio to increase in the coming years. Poland’s current account had a deficit of 0.5% of GDP in 2016, which, historically, is rather low. Taking account of the upswing in the economy and investment momentum, we expect current account deficits to increase again slightly in the next few years. Foreign debt amounted to 74.1% of GDP (2016) and has therefore increased in the last few years. We expect the foreign debt ratio to rise in the coming years, although in Poland’s case, this figure is heavily biased upwards because of strong foreign trade links with the EU (high volume of foreign direct investments, many financing projects done within international cor-porate structures). The local currency weakened moderately against the euro in 2016 because of political uncertainty (relating mainly to the country’s policies towards the EU).

We expect the zloty to get marginally stronger in the coming years because of its moderate valuation. At the end of the year, the base rate was low at 1.5%; this was due to the deflationary environment mentioned. Despite the moderate increases in inflation rates during 2017, the base rate should remain stable, because the central bank has not been pursuing any ultra-expansive monetary policies in recent years. The political situation in the country is stable and concerns about the orientation of Poland’s current nationalist-conser-vative government in terms of its economic and EU policies have eased a little. Policies favouring continuity and pragmatism have been chosen, especially in terms of economic policy.

1. The Economic and Political

Situation in Poland

Polish company law is essentially regulated by the Companies Code, which came into force on 1 January 2001 (Kodeks spólek handlowych – Law Gazette 2000 no. 94, pos. 1037). The capital stock requirement for a Polish limited liability company (Sp. z o. o.) is PLN 5,000 (around EUR1,190).

2.1. Choosing The Right Form Of Company To choose the right form of company for a particular investor, one must, among other things, look at the following: the scale of the business activities planned by the foreign business proprietor or enterprise, the regulations governing the formation of the particular kind of company (including the variations in formation costs) and the options that are available when it comes to deciding the contents of the memorandum and articles of association and the fiscal treatment of a particular form of company.

2.2. Setting Up Corporations

Limited Liability Company (Sp. z o.o.) Formation Process A limited liability company formed in accordance with Polish law can act as a company for both legal and tax purposes once the following have occurred: • adoption of a memorandum and articles of association; and once it has done the following: • concluded a lease; • applied to the statistical office for a REGON number; • opened a bank account and deposited the entirety of its capital stock; • applied for the company’s registration in the register at the regional court (KRS); • applied to the tax office responsible for the company for a NIP (tax reference) number and for the com-

pany’s registration for VAT; • updated the information held by the statistical office (receipt of a REGON number for the limited liability

company) and by the inland revenue service.

Signature Of The Memorandum And Articles Of Association The memorandum and articles of association of a Polish limited liability company must take the form of a notarial deed. However, it is not necessary to travel to Poland in person to sign the memorandum and arti-

2. Company Law

76

Supervisory Board And Audit Committee In general, the right of supervision in the company belongs to the shareholders, but it can also be assigned to a supervisory board or audit committee. A supervisory board or audit committee must be appointed if the company’s capital stock exceeds PLN500,000 and if it has more than 25 shareholders.

The Partners’ MeetingPursuant to mandatory legislative provisions, the most important company decisions are reserved for the partners’ meeting, including, for instance, decisions regarding the auditing and adoption of the managing board’s report, the income statement, usufructuary rights and acquiring or selling interests in real estate. In general, partners’ decisions are made during ordinary or extraordinary partners’ meetings. A written bal-lot can take place outside the scope of a partners’ meeting if all the partners give their written consent to a written ballot and if the written ballot is not inadmissible. In addition, decisions can be made without a meeting being formally convened if all the capital stock is represented and none of those present objects to holding the partners’ meeting and including the various matters in question on the agenda. An ordinary partners’ meeting must be held within six months of the close of each financial year. Partners’ meetings are normally held at the company’s registered office, but the memorandum and articles of association can specify another location. This must lie within the borders of the Republic of Poland.

The partners’ rights and duties In general, partners can only be obliged to make the payments laid down in the memorandum and articles of association. Their principal duties are to pay the contributions, to make up for contributions in kind that have been overvalued and to return disbursements that have been wrongly received. Their rights in assets include their interests in the net profit that has been set aside for distribution by the partners’ meeting. Their corporate rights are, among others, the right to participate in decisions by the partners and a far-reaching right of control that can only be restricted if the company has a supervisory board or audit committee.

Tax Rates Legal entities must pay corporation tax at a rate of 19%. Currently, tax at a rate of 19% is also charged on dividends.

The Cost Of Setting Up A Limited Liability Company The cost of setting up a company consists of third-party costs (e.g. notary’s fee, any taxes) and the lawyer’s fee if one wishes to consult a lawyer specialized in this field. Experience shows that it is advisable to consult a lawyer, especially as the necessary applications must be made using official forms and in Polish. As a rule, law firms in Warsaw charge fixed prices for helping set up a limited liability company. However, one should still reckon with fees of between roughly €1,500 and €3,000 for setting up a company in Warsaw. The third-party costs described above are an example put together for the formation of a company with the minimum required capital stock of PLN5,000.

cles of association. One can also give someone else appropriate authority (in the form of a notarial deed). When the memorandum and articles of association have been adopted, what is known as a limited liability company in formation (Sp. z o.o. w organizacji) exists. It can, in its own name, acquire rights, including real estate and other property rights, enter into obligations, sue and be sued. Once it has been registered in the register of the regional court, the limited liability company acquires the rights and obligations of the limited liability company in formation. Among other things, the memorandum and articles of association must state the company’s name and registered office, the amount of its capital stock, information as to whether a partner can subscribe to one share or more than one share, the number of shares subscribed to by the individual partners and their nominal values and, if the company has not been formed for an indefinite period, the period for which it is to exist. One must bear in mind that a limited liability company can be set up by an individual or legal entity but not by another “one-man” limited liability company.

Capital Stock, Capital Contributions And Company Shares The company must have capital stock of at least PLN5,000, and it must be fully paid in before the company can be registered. For as long as the company exists, it must be maintained in at least this amount. The partners cannot receive any payments out of the company’s assets if those assets are needed to maintain the full amount of its capital stock. Capital stock can be maintained by either contributions in cash or con-tributions in kind. The partners can agree in the memorandum and articles of association that, alongside their obligation to make contributions, they are also obliged to make subsequent, additional contributions. Each stake in the business corresponds to the proportion of the capital stock held, expressed in Polish cur-rency. It embodies membership of the company. The minimum nominal value of a business share is PLN50. Shares can be in equal or differing amounts. If the provisions of the memorandum and articles of associa-tion allow a partner to subscribe for more than one share, the shares must be the same and indivisible.

The Company’s Boards And Bodies The company’s mandatory boards and bodies are the managing board and the partners’ meeting. A super-visory board or audit committee can be appointed to supervise the company.

Managing Board The managing board is responsible for the conduct of business and for representing the company (in court and out of court). It can have one member or more than one. They are appointed or dismissed by way of decisions made by the partners. The partners’ meeting can, at any time, decide to dismiss a member of the managing board, regardless of the managing board member’s rights under an existing contract of employ-ment or other legal relationship. When contracts are concluded between a member of the managing board and the company and during legal disputes between a member of the managing board and the company, the company must be repre-sented by a member of the supervisory board, or by a representative appointed by the partners’ meeting. Power to represent the company can be granted to one member of the managing board on his or her own (sole representation) or together with other members of the managing board or authorized signatories (col-lective representation).

98

Joint-Stock Company (S.A.)

Formation Process (Formal Steps) A joint-stock company set up in accordance with Polish law can act as a corporation for both legal and tax purposes once the following have occurred: • preparation and signature of the notarized memorandum and articles of association by the founders,

subscription to the shares; and once it has done the following: • concluded a lease; • applied to the statistical office for a REGON number; • opened a bank account and deposited the cash contributions to its capital stock; • applied for registration in the register at the regional court (KRS); • applied to the inland revenue office responsible for the corporation for a NIP (tax reference) number and

for the corporation’s registration for VAT; • updated the information held by the statistical office (receipt of a REGON number for the joint-stock

company) and by the inland revenue service.

Preparation And Signature Of The Memorandum And Articles Of Association By The Founders, Subscription To The Shares The memorandum and articles of association of a Polish joint-stock company must take the form of a notar-ial deed. The individuals and/or legal entities who sign the memorandum and articles of association are the company’s founders. They can sign the memorandum and articles of association in person or through their authorized representatives. Here too, an appropriate power of attorney must be granted in the form of a notarial deed. If the memorandum and articles of association do not stipulate a minimum or maximum amount of capital stock, wht is known as a joint-stock company in formation (Spólka akcyjna w organizacji) comes into being when the shareholders have subscribed to the appropriate number of shares. Their total par value must be at least PLN100,000 (the minimum amount of capital stock), and prior to applying for the company’s registration, the managing board must declare the amount of capital stock that has been sub-scribed to in a notarial deed. Once it has been registered in the register of the regional court, the joint-stock company acquires the rights and obligations of the joint-stock company in formation. A joint-stock company can be set up by more than one individual and/or legal entity or by just one individual or legal entity, but a joint-stock company cannot be set up exclusively by a “one-man” limited liability company. Application For The Company’s Registration In The Regional Court’s Register Once the joint-stock company in formation has been given its REGON number and has concluded a lease or other agreement for premises, and once the cash contributions needed to constitute the requisite por-tion of the capital stock have been deposited in the account of the joint-stock company in formation, this application can be submitted to the regional court’s register. The entry will then be published in the Monitor Sa¸dowy i Gospodarczy. Registering a company in a regional court’s register currently takes about three weeks. The company will gain legal personality upon being registered. In addition to the formal steps we have already described, the following actions are required to set up a joint-stock company:

• payment by the shareholders of contributions to constitute the capital stock; • appointment of the managing board and supervisory board; • preparation of the report on the company’s formation and the formation audit.

Payment By The Shareholders Of Contributions To Constitute The Capital Stock The company must have capital stock of at least PLN100,000, and it must be maintained for as long as the joint-stock company exists. As in the case of a limited liability company, contributions to constitute the capital stock can take the form of contributions in cash or in kind. Contributions in cash must take the form of equal payments on all the shares deposited in the account of the joint-stock company in formation. A shareholder must pay the contributions for the respective shares in full. The deadlines for payments will be laid down by the memorandum and articles of association or by a resolution of the shareholders’ meeting.

Appointment Of The Managing Board And Supervisory Board Once the company has been set up, the managing board and supervisory board must be appointed as the company’s boards. The managing board is responsible for the conduct of business and for representing the joint-stock company (in court and out of court). The number of managing board members (at least one) will be laid down in the joint-stock company’s memorandum and articles of associations. Both sharehold-ers and non-shareholders can be appointed to the managing board. The supervisory board is responsible for appointing the members of the managing board. As a supervisory body, it monitors the activities of the joint-stock company in every area. Unless otherwise specified in the memorandum and articles of associa-tions, it must have at least three members. They are appointed and dismissed by the shareholders’ meeting.

Preparation of the report on the company’s formation and the formation auditThe company’s founders must prepare a written report on its formation, for instance stating whether contri-butions in kind are to be made to constitute part of its capital stock or if assets are to be purchased from the company. The report on the company’s formation will then be audited by the formation auditor appointed by the registry court competent for the company’s registered office to verify the formation process.

The Joint-Stock Company’s Name A joint-stock company can be given any name. However, the name must include the supplement spólka akcyjna (joint-stock company). For the purposes of legal relations, the abbreviation S.A. (plc) can also be used.

The Shareholders’ Legal Position A share embodies a shareholder’s rights and duties. The principal duty of a shareholder is to punctually pay the par value of the shares. The shareholders’ corporate rights include the right to participate with a voting right at the shareholders’ meeting, to challenge decisions by the shareholders’ meeting and to be elected to the company’s boards. The most important property right is the right to share in profit for the year.

1110

The Shareholders’ Meeting As the joint-stock company’s senior decision-making body, the shareholders’ meeting has the right to make fundamental decisions. Polish law differentiates between ordinary and extraordinary shareholders’ meetings. Like that of a limited liability company, the ordinary shareholders’ meeting of a joint-stock com-pany must be held within six months of the close of each financial year.

The Cost Of Setting Up A Joint-Stock Company Like the cost of setting up a limited liability company, the cost of setting up a joint-stock company consists of third-party costs (e.g. notary’s fee, any taxes) and the lawyer’s fee (which will depend on the particular law firm).

2.3. Setting up partnerships General partnership

A general partnership is a partnership that carries on business under its own name and is not any other kind of company. A general partnership differs from a civil law company in that contributing to a general partnership is one of the partners’ principal duties. A general partnership can act as a corporation for both legal and tax purposes once the following have occurred: • adoption of a memorandum and articles of association; and once it has done the following: • concluded a lease or other agreement for business premises; • applied to the statistical office for a REGON number; • opened a company bank account; applied to the inland revenue office responsible for the partnership for

a NIM (tax reference) number and for the partnership’s registration for VAT; applied for the partnership’s registration in the register at the regional court (KRS) followed by registration therein.

The memorandum and articles of association need merely be in writing to take effect. Consequently, when a company of this type is formed, no notary fees will be incurred for notarizing the memorandum and articles of association. Following the adoption of the memorandum and articles of association, the same steps are required as when forming a limited liability company or joint-stock company. Each partner is entitled and obliged to apply for the partnership’s registration in the register at the regional court. This type of company also only comes into being upon entry in the register at the regional court. The general partner-ship’s name must contain the surname(s) of the partner(s) (all or several thereof) as well as the supplement spólka jawna (general partnership). For the purposes of legal relations, the abbreviation sp.j. can be used. Since 1 January 2004, the rate of income tax payable by individuals and business proprietors has been optionally 19% (flat tax) or 18% and 32% (progressive tax).

Limited Partnership

A limited partnership is a partnership set up to carry on business under its own name. It consists of at least one partner with unlimited liability for the partnership’s debts to its creditors (general partner) and at least one partner whose liability to creditors is limited to the amount of that limited partner’s contribution. The personally liable partner(s) can also be a legal entity or legal entities, including in particular a limited liability company or limited liability companies. In general, the steps needed to make the company capable of acting for legal and tax purposes are the same as those we have described for a general partnership. The memorandum and articles of association must take the form of a notarial deed. The memorandum and articles of association must state the company’s name and registered office, its object, its duration if it is only being formed for a limited period, the contributions to be made by the individual partners and their value, and the limited partner’s contribution to be made by each limited partner. The limited partnership comes into being upon entry in the register at the regional court. If the partnership commences its busi-ness activities before being registered, it acts as a civil law company. The limited partnership’s name must contain the surname(s) of the general partner(s) (all or several thereof) as well as the supplement spólka komandytowa (limited partnership). For the purposes of legal relations, the abbreviation sp.k. can be used.

Partnership Limited By Shares

The purpose of this form of partnership is to have an enterprise carrying on business under its own name in which at least one partner (general partner) is liable to creditors for the partnership’s debts without limit and at least one partner is a shareholder. At the moment, the partnership must have capital stock of at least PLN50,000. The partnership’s memorandum and articles of association must take the form of a notarial deed. The partnership comes into being upon entry in the register at the regional court. Unlike the limited partners in a limited partnership, the shareholders are not liable for the company’s debts.

2.4. Other forms of investmentIn addition to the possible ways of setting up corporations and partnerships that we have already described, two other legally dependent forms of investment are also available to business proprietors, namely the branch and the commercial agency (representative office).

1312

Overview: Choosing The Right Form Of Investment

Setting up one of the corporations or partnerships described above involves administrative expense. It is particularly advisable to do so if one wants to employ a large number of staff and have a well-developed organizational structure or if one is setting up a special purpose entity in order to buy real estate. Moreover, one must not neglect the issue of limited liability in Poland. A (legally dependent) branch of an enterprise in Poland has many of the same duties as a corporation, such as maintaining a balance sheet, but contri-butions to its capital are not mandatory. A branch is deemed to be inseparable from the enterprise itself. Because of this inseparability, its liability cannot be limited to Poland. An Austrian enterprise can only set up a (legally dependent) commercial agency or representative office for marketing purposes. We therefore recommend setting up a commercial agency if an enterprise initially wants to establish ties with Polish part-ners with the intention of subsequently entering the market by way of a subsidiary formed at a later date.

2.5. Sole trader An individual can commence a business activity for profit in his or her own name and carry on that activity (sole trader). The prerequisite is registration in the commercial register. This register is kept by the munici-pality competent for the sole trader’s place of residence. The application for registration is free. Registration can either be carried out directly at the competent authority without delay or via the internet. The municipal-ity must issue the sole trader with a confirmation of the registration within 3 days of the application being made. Once entry in the commercial register has taken place, the sole trader must apply for REGON and NIP numbers. He or she can either do this in person or make use of a solution that has just been introduced, namely the option of applying for REGON and NIP numbers at the same time as applying for registration in the commercial register. If this option is taken, the municipality will pass the necessary documents on to the responsible statistical office (REGON number) and inland revenue office (NIP number) within three days of registration.

3.1. TaxesThe Polish tax system can be classed as investment-friendly in a legal sense; however, the enforcement of the taxation laws frequently creates problems for foreign and Polish firms in Poland.

The corporate tax rate was still 30% in 2000; since 2004 it has been only 19%. The tax and contribution ratio for companies is lower than in Austria.

For investors, additional tax incentives exist such as the possibility of exemption from income tax in special economic zones, or exemption from property tax.

Taxation Of CompaniesThe Corporate Tax Law contains the fundamental principles for taxation of legal persons and of corpora-tions in the process of formation. The provisions of this law do not apply to companies under civil law, or to commercial partnerships. What is taxed is the sum of all operational income achieved during the course of the tax year minus the operational expenditure. The Corporate Tax Law considers operational expenditure to be all costs that were expended for the purposes of achieving the operational income.

The Corporate Tax Rate Is A Flat 19%Like the Income Tax Law, the Corporate Tax Law distinguishes between limited and unlimited tax liability. According to this law, all companies that are domiciled in Poland have unlimited tax liability. Unlimited tax liability refers to the total income of the company in question, regardless of the location of the source of the income (worldwide income principle). Firms that are not domiciled in the territory of the Republic of Poland, on the other hand, are subject to limited tax liability, meaning that only the income that they have attained in Poland is subject to tax there.

The Corporate Tax Law defines the business year as the calendar year (basic principle) or as a time period of twelve consecutive calendar months. If the taxpayer chooses a business year which is not the calendar year, the relevant tax office must be informed of this fact within 30 days of the start of activities. When a legal person begins its business activities for the first time, the business year lasts from the day that its business activities started until the last day of the business year elected in the firm’s articles of association, but not

3. Taxes and Legislation

1514

longer than twelve consecutive months. Additionally, it is possible to extend the first business year of a legal person up until the end of the following business year, if the legal person selects the calendar year as the business year and only starts its business activities in the second half of the first business year.

Value Added Tax / VAT NumberIn Poland there are various different rates of VAT. As of 1 January 2011, the base rate has been 23%, with reduced rate bands of• 0% (e.g. for exports, intra-EU trade, and international transportation services)• 5% (e.g. for unprocessed food)• 8% (e.g. for processed food, construction materials and services)

Reverse Charge SystemIn the case of intra-Community acquisition of goods with a receiver of goods (importer) in Poland, the VAT can be settled tax-neutrally by the Polish importer (reverse charge procedure).The Austrian supplier of the goods and the receiver of the goods in Poland both have to have EU VAT ID numbers. The Austrian supplier must produce a net invoice in accordance with Austrian VAT regulations.In order to utilise the reverse charge procedure in Poland, the following prerequisites must be met:1. The buyer in Poland must be a company that is liable for tax, and must have a Polish tax number as well

as an EU VAT ID number.2. The seller must be a taxpayer registered in a foreign country, and must also have an EU VAT ID number.3. The Polish buyer must either be domiciled or have a fixed place of business in Poland.

Excise Tax

Excise tax is levied on the production of goods that are liable for excise tax, the importation of such goods into a tax warehouse, their importation, their intra-Community acquisition, and their removal from the tax warehouse (Exception – excise suspension procedure).

Examples (as of 2014)

• Diesel: 1,196 PLN/1,000 litres• Cigarettes: in this case the excise tax consists of two elements:- on a value basis: 206.76 PLN/1,000 units- by percentage: 31.41% of the retail price of a packet of cigarettes

The minimum excise tax rate for cigarettes is 592.49 PLN/1,000 units. If the sum of the two excise tax ele-ments is lower than the minimum excise tax rate, then the minimum excise tax rate is applied instead.When importing new cars (passenger cars) into Poland from another EU country, the buyer incurs excise tax depending on the engine displacement of the vehicle (engine displacement = 2000 cc – 3.1% of the vehicle value, engine size > 2000 cc – 18.6% of the vehicle value).

Important!

Some excisable goods, such as alcohol and tobacco products, have to have an excise tax label (excise stamp) affixed to them before they enter into goods traffic. The excise stamp must be affixed by the time the product crosses the border. An exception to this is the delayed excise procedure. In this case, delivery of the product is carried out from the tax warehouse of the producer in one EU state to a tax warehouse in Poland; excise stamps are only affixed to the product in this tax warehouse prior to the completion of the delayed excise procedure. Excise stamps can only be requested from the customs office by a company registered in Poland; these are then transferred to the foreign supplier by the Polish firm (generally the importer) by affixing them on the packaging of each unit.

Double Taxation TreatiesCompanies that are active in Poland and Austria should note the provision concerning corporate profits in the new double taxation treaty between Poland and Austria that came into effect on 1 April 2005.

Pursuant to the treaty, the profits of a company domiciled in Austria can generally only be taxed in Austria, unless this company carries out its activities in Poland within the framework of a permanent establishment situated in Poland. If this is the case, the profits that can be attributed to this permanent establishment can be taxed in Poland.A permanent establishment for the purposes of the aforementioned double taxation treaty is a fixed place of business through which a company’s activities are carried out, whether wholly or in part. In particular, the term ‘permanent establishment’ covers:• a management location• a regional office• a branch office• a production location• a workshop

1716

• a mining location, an oil or gas location, a quarry or any another location for the exploitation of natural resources.

A construction project or installation only becomes a permanent establishment when its duration exceeds twelve months.You can read the text of the double taxation treaty on the website of the RIS (Austrian legal information system).

Input Tax Deduction / Rebate ProcedureThe provisions concerning input tax deduction, the refunds process and input tax reimbursement are cov-ered in detail in the specialist report on the subject of input tax reimbursement in the EU, in the EEA (Iceland, Liechtenstein, Norway) and in Switzerland. This can be referred to online.

Since 1 July 2001, foreign firms that acquire in Poland goods and services which are subject to Polish VAT, are entitled to request a direct reimbursement of the VAT as an input tax from the Polish tax authority (the Second Tax Office for Warsaw Central District).

Input tax deduction is generally subject to the same basic principles in Poland as it is in the other EU mem-ber states (EU Guideline 2006/112/WE of 28 November 2006), and is possible as long as:

1. You are subject to VAT, or tax of a similar nature, in the country where you are domiciled,2. You are not registered for Polish VAT, and3. You do not carry out any activities in the territory of the Republic of Poland that are liable for Polish VAT

(no supplier activities).

For the third condition (not carrying out activities that are liable for VAT), some exceptions are allowed; the most important of these is the case whereby the VAT is settled by the receiver of the goods or services by means of the reverse charge procedure.

This means that the deduction of input tax is possible if the purchased goods and services are used for activities which are subject to taxation by VAT. However, for Poland there are certain specific exceptions to this general rule, which are set out in Art. 88 of the Polish VAT Act:

• The purchase of fuel (petrol, diesel, gas) which is used to power passenger cars. Currently, it is only pos-sible to claim input tax deduction for fuel expenditure for company cars with built-in partition grids,

• The purchase of services in the hotel and catering industries,• The acquisition of goods as a gift or the acquisition of services free of charge.

There are also restrictions with regard to the input tax deduction for the purchase of a passenger car: only 60% of the input tax, and not more than PLN6,000, can be deducted.

There are no small-sum receipts (simplified receipts for small amounts) in Poland that entitle one to reim-bursement of input tax. As far as requests for reimbursement are concerned, the requested VAT refund amount must be at least the equivalent in PLN of• €400, if the request is in reference to a period of time shorter than a calendar year, but of at least three

months,• €50, if the request is in reference to the whole calendar year or a time period that is shorter than the last

three months of this year.

Since the start of 2010 the request (submitted electronically) has been made to the Polish tax authority via the tax administration of the applicant, i.e. in Austria via FinanzOnline.

Requests must be submitted to the Polish tax authority by 30th September of the following year at the latest (and not by 30th June, as was formerly the case).

Further information concerning the VAT reimbursement process is available from the Warsaw Centre for Foreign Trade.

Income TaxSince 1 January 2009, the income tax payable by entrepreneurs (natural persons) has been, selectively, either 19% (flat tax rate), or 18% or 32% (graduated tax rate). For employees who are not self-employed, only the graduated tax rate can apply.

Social insurance costs are about 34.45% of gross pay, with 20.74% being borne by the employer and the rest by the employee. The tax-exempt allowance for 2015 is PLN3,091 (approx. €734). This means that a gross wage of PLN2,860 (approx. €679), for example, results in total costs of PLN3,453.17 (approx. €820; +20.74% of the gross wage) for the employer. The employee receives approx. PLN2,058.78 (approx. €490) following deduction of the employee share of social insurance contributions and taxes.

1918

In Poland too, Polish and foreign contracting parties benefit from modern arbitration legislation based on the principles of the far-reaching procedural autonomy of the parties concerned, confidentiality, procedures that generally involve just one court or tribunal and the possibility of enforcing foreign arbitral awards. The oldest court of arbitration in Poland — and the one that has the most experience dealing with cross-border disputes — is that of the Polish Chamber of Commerce (KIG) in Warsaw. According to information provided by the court of arbitration, proceedings last between six and nine months.

The German-Polish Chamber of Trade and Industry, which is also based in Warsaw, also has a court of arbi-tration. The arbitration codes of both arbitral courts are available from the Warsaw Centre for Foreign Trade.Unlike the judgements of state courts, arbitral awards can be enforced practically worldwide. For a dispute to be settled by a court of arbitration, its jurisdiction must have been agreed upon beforehand in writing. It is therefore advisable to include an arbitration clause in the contract with your foreign counterparty.

The Austrian Federal Economic Chamber offers institutional arbitration as a service through the International Arbitral Centre of the Austrian Federal Economic Chamber.

The arbitration clause of the International Arbitral Centre of the Austrian Federal Economic Chamber reads as follows (versions are also available in the languages that are most important for Austrian exporters):

‘All disputes arising out of this contract or related to its violation, termination or nullity shall be finally settled under the Rules of Arbitration and Conciliation of the International Arbitral Centre of the Austrian Federal Economic Chamber in Vienna (Vienna Rules) by one or more arbitrators appointed in accordance with these Rules.’

Useful agreements to supplement this arbitration clause: • the number of arbitrators shall be .......................... (one or three); • the applicable law shall be ............................; • the language used during arbitration proceedings shall be ......................................

Detailed information:

Internationales Schiedsgericht der Wirtschaftskammer Österreich International Arbitral Centre of the Austrian Federal Economic Chamber Dr. Manfred Heider; Phone: +43-5-90 900-4398; Fax: +43-5-90 900-216. E-mail: [email protected]; Internet: wko.at/arbitration

4. Arbitration

The fact that you as an Austrian company are a member of the Federal Economic Chamber can in some cir-cumstances be a cause for concern for a strong foreign counterparty. In this case we recommend that you agree on a different arbitral court, such as the one belonging to the International Chamber of Commerce. This has its headquarters in Paris and is represented in Austria by ICC Austria.

Therefore you have the following options:• If your company has a strong starting position in contract negotiations or if you and your counterparty are

roughly equal, we recommend you use the arbitration clause of the Austrian Federal Economic Chamber.• If on the other hand your company holds a weaker position, or if your counterparty is of equal strength

and will not agree to the Austrian Federal Economic Chamber’s arbitration clause, then we recommend that you agree on a different arbitral court, such as that of the International Chamber of Commerce (ICC).

The arbitration clause of the International Chamber of Commerce (ICC) reads as follows: ‘All disputes aris-ing out of or in connection with the present contract shall be finally settled under the Rules of Arbitration of the International Chamber of Commerce by one or more arbitrators appointed in accordance with the said Rules.’ This arbitration clause is also available in other languages.

Detailed information:

ICC Austria, International Chamber of CommerceDr. Maximilian Burger-Scheidlin; Phone: +43-5-90 900-3701; Fax: +43-5-90 900-3703; E-mail: [email protected]; Internet: www.icc-austria.org

2120

5. Subsidies and Support

EU cohesion policy / regional policy 2014-2020Initial situation / status quoThe various regions of Europe, especially Central and Southeastern Europe, exhibit large differences in economic and social development. To strike a balance between the regions, the EU has set the following targets as part of its Europe 2020 strategy:

• Creation of jobs• Strengthening companies’ competitive position• Promotion of economic growth and sustainable development• Improvement in EU citizens’ life quality

The cohesion / regional policy is aimed at all regions in the EU in order to create intelligent, sustainable and integrative growth. The cohesion policy is defined for a seven-year period (2014-2020). A budget of EUR 351.8 billion, i.e. almost one third of the entire EU budget, is set aside for achieving the above targets in the timeframe mentioned. Within the scope of this budget, funding is granted in the form of non-repayable grants.

Structure of the funding programmes / from the EU target to the national funding programmeThe individual EU member states use the EU targets set under the Europe 2020 strategy to define their national and regional priorities, from which the individual Operational Programmes (OPs) are derived.The Operational Programmes are structured according to region and topic. Within these programmes “priority axes” are defined, which are subject to guidelines approved by the European Commission. The following topics are priorities for the individual countries: Innovation, research & development, job creation, environmental protection, education, SMEs, transport and regional development.

Dedicated national funding agencies (ministries and investment agencies) are responsible for awarding the grants. While grants can be applied for continuously in framework programmes in Austria, they are mostly awarded in the context of “calls” (tender exercises) in Eastern Europe.

For each priority axis mentioned above, tender exercises are held once or twice a year and are open for one to three months. The main assessment criteria for company grants are company size, location, content and impact of the funding project.

How can your company obtain funding?Clearly defined projects can be submitted during the period when the tender exercise is open. Only complete applications (project description, approvals, budget,...) in the respective national language are accepted. The submitted projects are then evaluated by assessors using a points system based on the guidelines specified/defined in the program. All projects within a “call” take part in a competition. Only those with the highest score are shortlisted for funding commitments.

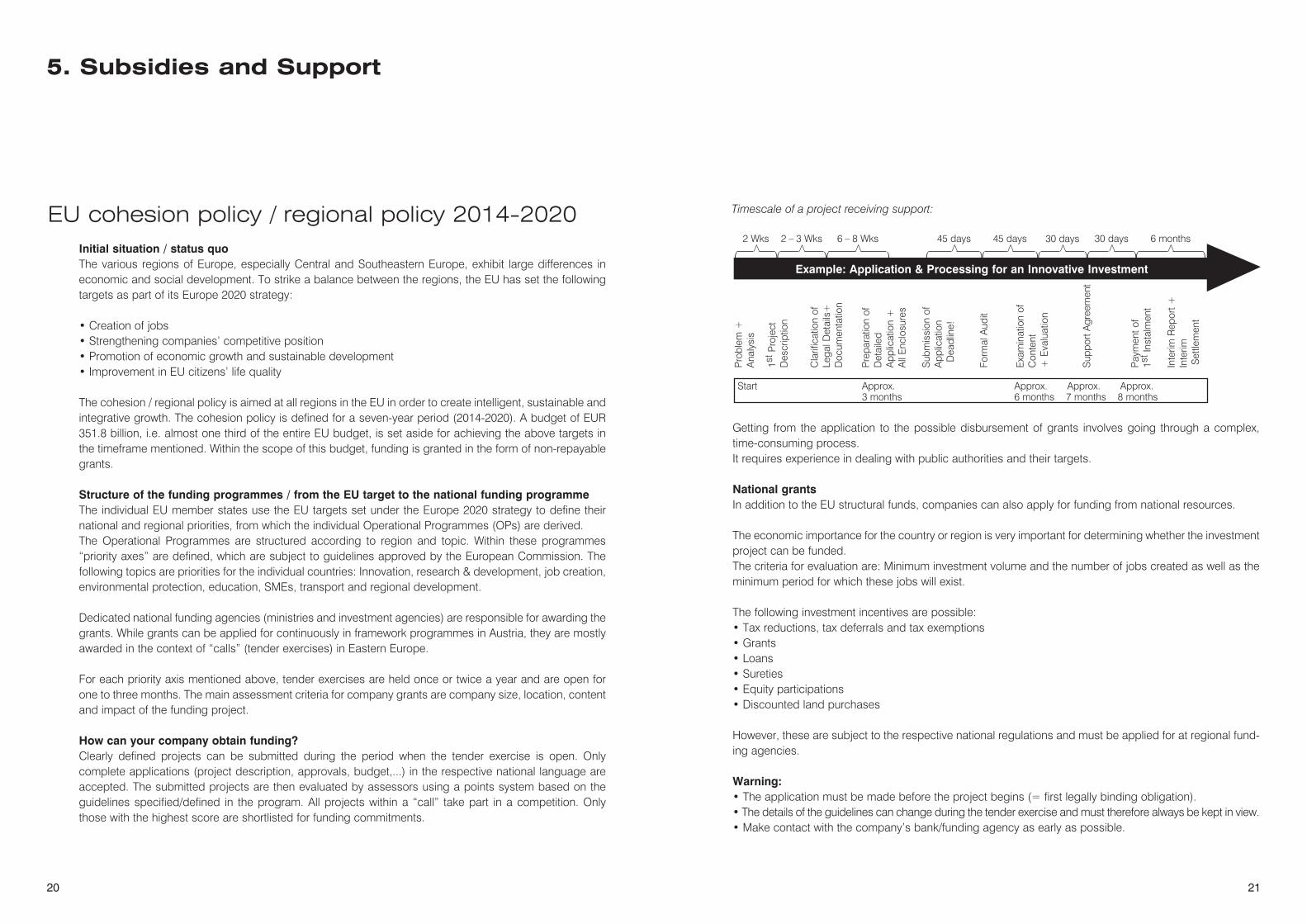

Getting from the application to the possible disbursement of grants involves going through a complex, time-consuming process.It requires experience in dealing with public authorities and their targets.

National grantsIn addition to the EU structural funds, companies can also apply for funding from national resources.

The economic importance for the country or region is very important for determining whether the investment project can be funded.The criteria for evaluation are: Minimum investment volume and the number of jobs created as well as the minimum period for which these jobs will exist.

The following investment incentives are possible:• Tax reductions, tax deferrals and tax exemptions• Grants• Loans• Sureties• Equity participations• Discounted land purchases

However, these are subject to the respective national regulations and must be applied for at regional fund-ing agencies.

Warning:• The application must be made before the project begins (= first legally binding obligation).• The details of the guidelines can change during the tender exercise and must therefore always be kept in view.• Make contact with the company’s bank/funding agency as early as possible.

Pro

blem

+A

naly

sis

1st P

roje

ctD

escr

iptio

n

Cla

rific

atio

n of

Lega

l Det

ails

+D

ocum

enta

tion

Pre

para

tion

ofD

etai

led

App

licat

ion

+A

ll E

nclo

sure

s

Sub

mis

sion

of

App

licat

ion

€ Dea

dlin

e!

Form

al A

udit

Exa

min

atio

n of

Con

tent

+ E

valu

atio

n

Sup

port

Agr

eem

ent

Pay

men

t of

1st I

nsta

lmen

t

Inte

rim R

epor

t +In

terim

Set

tlem

ent

Example: Application & Processing for an Innovative Investment( )

>

2 Wks

( )

>

2 – 3 Wks

( )

>

6 – 8 Wks

( )

>

6 months

( )

>

30 days

( )

>

30 days

( )

>

45 days

( )

>

45 days

Start Approx. Approx. Approx. Approx. 3 months 6 months 7 months 8 months

Timescale of a project receiving support:

2322

6. Risk Hedging and Financing

Risk hedging of Austria Wirtschaftsservice

Gesellschaft mbH (aws, federal funding agency)

Legal framework conditions:

The legal framework conditions of the guarantees issued by aws were redrafted on 1 January 2017.In detail, the regulations are based on the guidelines of the Austrian Federal Ministry of Finance (BMF) for accepting guarantees by aws pursuant to the Guarantees Act 1977, including supplementary conditions for grants.

The aws offers small and medium-sized companies (max. 3,000 employees) with their registered office and operating site in Austria guarantees for loans and lease financing as part of domestic and foreign invest-ments.

Guarantees for national investments:aws guarantees the financing of economically desirable projects by Austrian companies, i.e.: Construction/expansion investments, modernisation of production facilities, the innovation of processes and procedures, environmental measures or the purchase of, or participation in, companies.

aws guarantees up to 80% (max. EUR 25 m) of the financing amount in the form of a financing guarantee and covers the economic risk of the investor (loan default due to the insolvency of the domestic company) for the bank. In the case of large projects, aws guarantees up to a maximum of one third of the project volume.

Guarantees for international investments:aws supports Austrian companies (max. 3,000 employees) with direct investments abroad, i.e. establish-ment of subsidiaries/joint ventures, acquisition of companies/company shares, expansion investments and investments in environmental technologies.The risk hedging of aws is provided either in the form of a project guarantee or a financing guarantee.

Under the project guarantee, aws hedges the economic risks (insolvency or similar circumstances) of a company’s investment project and undertakes to provide a certain amount of capital up to the maximum guaranteed amount in the event of damage or loss.

aws guarantees up to 50% of the loan used (for large projects up to 1/3 of the project volume). The guar-antee fee is dependent on the ratings result calculated when examining the respective project, as well as the term of the guarantee.

Under the international financing guarantee, aws guarantees the financing of Austrian companies for eco-nomically desirable projects abroad, i.e.: construction/expansion investments, modernisation of production facilities, the innovation of processes and procedures, environmental measures or the purchase of, or participation in, companies.

aws guarantees up to 80% (max. EUR 25 m) of the financing volume and thereby covers the economic risk of the investor for the bank.

Conditions of the aws guarantee:

National guarantees: • Processing fee: 0.25% (one-off) of the assessment basis (max. EUR 30,000)• Guarantee fee: The guarantee fee depends on the ratings result calculated when examining the

respective project as well as the term of the guarantee

International guarantees:• Processing fee: 0.25% (one-off) of the assessment basis (max. EUR 50,000)• Guarantee fee: The guarantee fee depends on the ratings result calculated when examining the

respective project as well as the term of the guarantee.

Austria

Abroad

BANK

2524

OeKB (Oesterreichische Kontrollbank AG)In order to achieve sustainable success in the export business and for investments made abroad, com-panies need good risk management and attractive financing arrangements. With federal export guaran-tees and OeKB refinancing packages, the OeKB offers instruments via the respective house banks that strengthen Austrian companies and their partners in global competition. By processing export guarantees, the OeKB acts as the Export Credit Agency (ECA) of the Republic of Austria.

Export guarantees protect the entrepreneur against payment defaults (for economic or political reasons) related to export transactions. In the case of foreign investments, export guarantees provide protection against political risks.

Federal export guarantees also offer an attractive way to access financing for export and investment activi-ties. Export guarantees can be utilised by all large, medium and small companies whose guaranteed trans-actions have a positive impact on Austria’s current account balance or are in the national interest.

Companies can learn more about the ideal kinds of guarantee from the OeKB Export Service (www.exportservice.at) or from their house bank. OeKB’s export financing process provides the possibility of refi-nancing exports and equity participations abroad. This export financing process is available as a source of refinancing at domestic and foreign commercial banks and is offered to companies via these banks within the scope of their export business and foreign investments.

The prerequisites for this type of financing are• A federal guarantee as required by the Export Funding Act (EFA), or• A guarantee from a credit insurer within the meaning of the EFA• A guarantee from aws, or• A guarantee of an international organisation within the meaning of the EFA.Furthermore, the financing of the underlying supplies/services must bring about a direct or indirect improve-ment in the Austrian current account balance or be in the Austrian national interest.

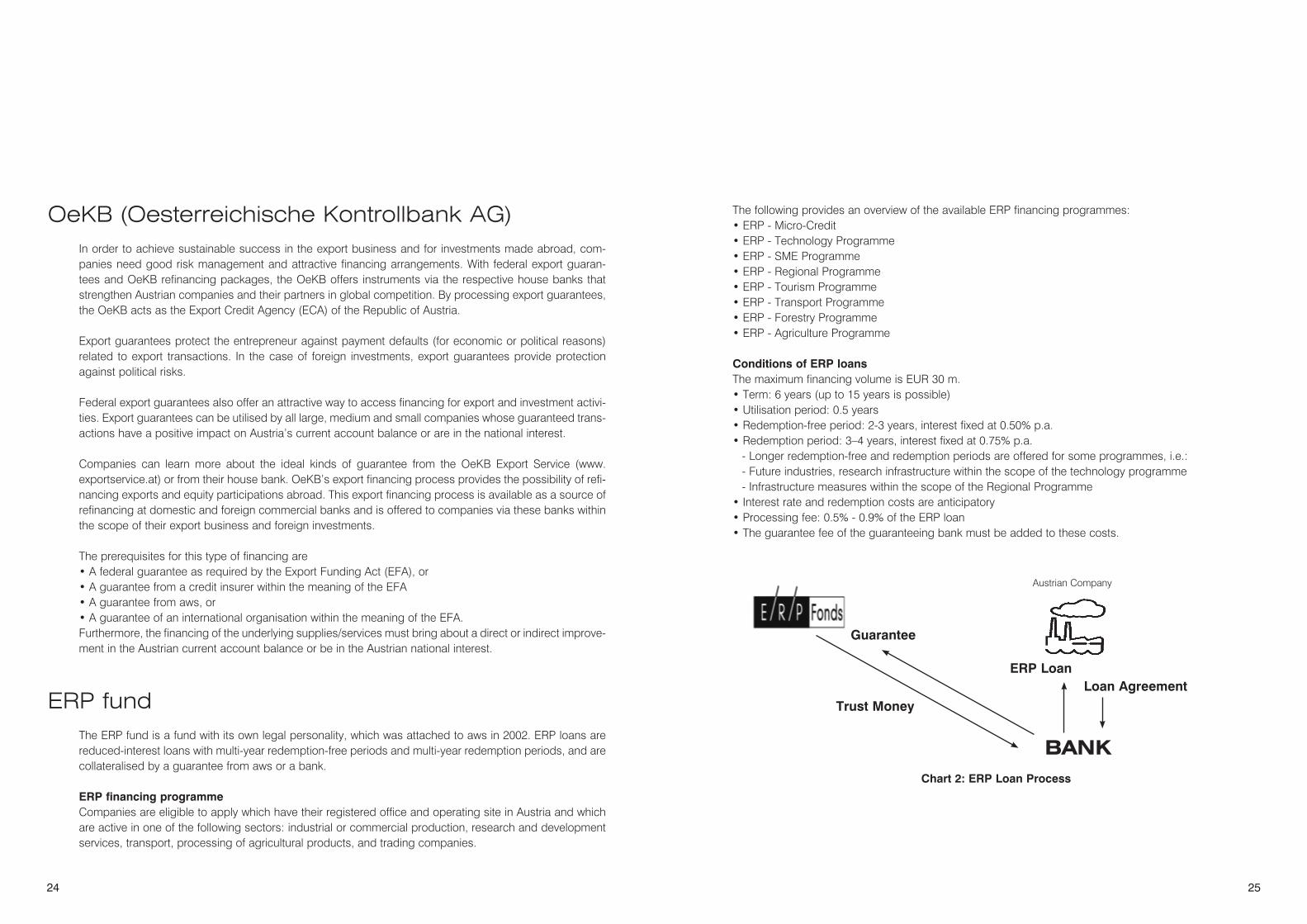

ERP fundThe ERP fund is a fund with its own legal personality, which was attached to aws in 2002. ERP loans are reduced-interest loans with multi-year redemption-free periods and multi-year redemption periods, and are collateralised by a guarantee from aws or a bank.

ERP financing programme Companies are eligible to apply which have their registered office and operating site in Austria and which are active in one of the following sectors: industrial or commercial production, research and development services, transport, processing of agricultural products, and trading companies.

The following provides an overview of the available ERP financing programmes:• ERP - Micro-Credit• ERP - Technology Programme• ERP - SME Programme• ERP - Regional Programme• ERP - Tourism Programme• ERP - Transport Programme• ERP - Forestry Programme• ERP - Agriculture Programme

Conditions of ERP loansThe maximum financing volume is EUR 30 m.• Term: 6 years (up to 15 years is possible)• Utilisation period: 0.5 years• Redemption-free period: 2-3 years, interest fixed at 0.50% p.a.• Redemption period: 3–4 years, interest fixed at 0.75% p.a.

- Longer redemption-free and redemption periods are offered for some programmes, i.e.:- Future industries, research infrastructure within the scope of the technology programme- Infrastructure measures within the scope of the Regional Programme

• Interest rate and redemption costs are anticipatory• Processing fee: 0.5% - 0.9% of the ERP loan• The guarantee fee of the guaranteeing bank must be added to these costs.

Austrian Company

BANK

Guarantee

Trust Money

ERP LoanLoan Agreement

Chart 2: ERP Loan Process

2726

The fundable projects/costs are dependent upon the respective ERP financing programmes, based on the purpose and mandate of the respective programme.

ERP loans for large companies:For large companies, ERP loan financing is provided by the ERP Regional Programme and the ERP Technology Programme. Within the scope of these two programmes, large companies in particular can apply for funding for the following projects/costs:

Fundable projects for large companies:• Initial investment in NEW economic activities (new NACE-4 provider)• Construction of a NEW independent operating site• Within the de minimis limits (max. fundable value of EUR 200,000 within the last 3 years), further projects

can also be funded (product and process innovations, innovative services through implementation of in-house research results, purchase and adaptation of new technologies, modernisation and expansion investments, construction/acquisition of start-up, technology and innovation centres)

• Research/development projects for the introduction of new/significantly improved products• Projects for prototype production• Construction of pilot/demonstration/testing facilities

Fundable costs for corporations:• New investments and in-house services to be capitalised• Construction investments• Land purchases for founding new companies, business expansion and business location to the extent

required by the business• Costs for intangible assets (patents, licences, etc.) and consultancy costs• Regarding R&D projects: Staff costs, laboratory facilities, costs of consultancy and provision

of services, equipment costs for pilot and demonstration facilities

7. Payment and Account Services at

Raiffeisen Bank Polska S.A.

7.1. Cash Management ProductsAccount Services Local Currency Foreign Currency (LCY) Current Acc. LCY Deposit (FCY) Current Acc. FC DepositResident 3 3 3 3

Non-resident 3 3 3 3

Credit interest 3 3 3 3

Overdraft Facility 3 3 3 3

Payments/Collections• Domestic payments LCY• Domestic payments FCY*• Foreign payments LCY*• Foreign payments FCY*• Domestic direct debits*• Mass Payment• Mass Collect• Payment Identification System• Mass direct debits• Cheques*• Cheques for collection*• Cash withdrawals LCY, FCY

(open/closed form)*• Cash Collection*• Cash Supply*• Cash Convoys• Purchase & Sale of FCY

Cash Management: Local Products and Services

• Bank cards (debit, credit and charge)

• Electronic postal transfers• Automated cash deposit

machines (DTM’s)

Electronic Banking• Internet Banking• ”R-Online Biznes”• MultiCash• R-connect (Web service)

• SWIFT MT 940 (send)

• SWIFT MT 942• SWIFT MT 101 (receive)

Liquidity Management• Overdraft facilities• Cash Pooling Zero Balancing • Cash Pooling National

Pooling (single and multi-currency)

• Net Balance/ Limit compensation

* However, restrictions due to local regulations

Cash Management: Group Products and Services • Cash Management International (CMI)• CMI@Web• International Account Reporting• International Disbursement Service• Cross-border Target Balancing• Cross-border Zero Balancing

• Cross-border Margin Pooling• Intra Group Payments (IGP)• UniCash Mitglied• Low Value Payments• Central Conversion Solution• SWIFT for Corporates (SCORE)

2928

7.2. Legal & Foreign Exchange RegulationsCurrent Accounts • No restrictions, available for resident and non-resident corporate customers in LCY and FCY.

Domestic Payments • LCY: There is no difference between foreign and local account holders with respect to domestic pay-

ments.

Foreign Payments • Foreign payments are not longer subject to the f/x control.

Cash Payments / Withdrawals • LCY, FCY: Should the cash transaction exceeds the equivalent of EUR 15,000.00 Raiffeisen Bank

Polska S.A. will require identification and is obliged to register details of the transaction.• High value cash transactions are to be advised:

– more than PLN 20,000.00 and more than 2,000.00 in case of EUR, USD, GBP - 24 hours in advance until 12 a.m.

– more than PLN 50,000.00 and more than 5,000.00 in case of EUR, USD, GBP as well as each amount of other foreign currencies collected by the Bank – 48 hours in advance until 1:00 p.m.

7.3. Clearing mechanismsMechanisms • Description: The majority of domestic payments is settled through KIR - the National Clearing

House (NCH) by means the electronic clearing system – ELIXIR (data are exchan-ged electronically).

Banks hold accounts with the National Bank of Poland. Based on information from NCH, the net position is settled three times a day (3 sessions) in case of Elixir.

Corporate high value payments can be settled via the RTGS (real time gross settlement) system SORBNET. The use of this system is obligatory for payments exceeding PLN 1,000,000.00.

• Type: Batch – Elixir RTGS – Sorbnet

• Routing: Up to 1mio via ELIXIR, more than 1 mio SORBNET2 – no restrictions

• Settlement cycle: Remitting bank 0 – 1 days Clearing centre 0 day Beneficiary bank 0 – 1 days

Banks’ clearing system memberships KIR (National Clearing House) SORBNET (RTGS system of Central Bank)

3130

9. Your International Business

Specialists at Raiffeisen Bank Polska S.A.

and the Global Raiffeisen Network

Your specialist at Raiffeisen Bank Polska S.A.Krzysztof [email protected]+48 691 33 5510

Your international business specialistsRaiffeisen Bank International AGHerwig [email protected]: +43 / 1 / 717 07 – 1574

Raiffeisen Bank International AGRudolf [email protected]: +43 / 1 / 717 07 – 3537

Raiffeisenlandesbank NÖ-Wien AGNadja [email protected]: +43 / 5 / 1700 – 92426

Irene [email protected]: +43 / 5 / 1700 – 92157

Raiffeisen-Landesbank Steiermark AGFranz [email protected]: +43 / 316 / 4002 – 7110

Beatrix [email protected]: +43 / 316 / 4002 – 7141

Assets, �m 12,000

Branches 299

Staff 4,242

Raiffeisen Bank Polska S.A. ranks among the strongest and most trusted financial institutions in Poland. At year-end 2016, Raiffeisen operated 299 business outlets across the country and served more than 760,000 customers. Raiffeisen Bank Polska offers a full range of banking products and services to individuals, afflu-ent clients, micro companies, small and medium companies, as well as big corporations. The bank was honoured as the best private-banking provider in Poland by EMEA Finance at the 2016 Europe Banking Awards. Its subsidiary Rkantor.com is one of the most innovative FX platforms in the country.

8. Raiffeisen Bank Polska S.A.

Shareholder structure:

Raiffeisen Bank International 100%

32 33

Raiffeisenlandesbank Oberösterreich AGHelmut [email protected]: +43 / 732 / 6596 – 23113

Artem [email protected]: +43 / 732 / 6596 – 23161

Raiffeisenverband SalzburgBernhard [email protected]: +43 / 662 / 8886 – 14161

Raiffeisen-Landesbank Tirol AGAndrea [email protected]: +43 / 512 / 5305 – 12230

Raiffeisenlandesbank VorarlbergAlexandra [email protected].: +43 / 5574 / 405 - 528

Raiffeisenlandesbank BurgenlandWilhelm [email protected]: +43 / 2682 / 691 – 605

Raiffeisenlandesbank KärntenMichael Stegmü[email protected]: +43 / 463 / 99300 – 2280

Herbert Schö[email protected]: +43 / 463 / 99300 – 2269

Notes

34 35

NotesNotes

Received from: