Embed Size (px)

Citation preview

Financial Markets

By Huanli Li

Part One

Introduction

Chapter 1

Why Study Financial Markets and Institutions?

Chapter Preview

The evening news features a segment about interest rates, the Fed Chairman Ben Bernanke, and liquidity in credit markets.

What does all this mean? Do I care about interest rates? What is “the Fed?” Will this impact my firm’s ability to get a bank loan?

Chapter Preview

These are good questions. Of course, the answer to these questions can be found in this book. In fact, this books touches on a variety of topics, including the Fed, stocks markets, bond markets, and banks. We will begin to appreciate many exciting issues related to these topics during the course of this term

Chapter Preview

To start, we preview subjects of interest to anyone who is a part of a productive society. We motivate how financial markets and institutions have significant impact on important questions about our financial well-being. Topics include:

Why Study Financial Markets?

Why Study Financial Institutions?

Applied Managerial Perspective

How Will We Study Financial Markets and Institutions

Why Study Financial Markets?

Financial markets, such as bond and stock markets, are crucial in our economy.

1. These markets channel funds from savers to investors, thereby promoting economic efficiency.

2. Market activity affects personal wealth, the behavior of business firms, and economy as a whole

Why Study Financial Markets?

Well functioning financial markets, such as the bond market, stock market, and foreign exchange market, are key factors in producing high economic growth.

We will briefly examine each of these markets, key statistics, and how we will examine them throughout this course.

Why Study Financial Markets? Debt Markets & Interest Rates

Debt markets, or bond markets, allow governments, corporations, and individuals to borrow to finance activities.

In this market, borrowers issue a security, called a bond, that promises the timely payment of interest and principal over some specific time horizon.

The interest rate is the cost of borrowing.

Why Study Financial Markets? Debt Markets & Interest Rates

There are many different types of market interest rates, including mortgage rates, car loan rates, credit card rates, etc.

The level of these rates are important. For example, mortgage rates in the early part of 1983 exceeded 13%. Financing a house was quite expensive at this time.

Why Study Financial Markets? Debt Markets & Interest Rates

Because interest rates are important to individuals and business, understanding the history of interest rates is beneficial.

The next slide shows historical interest rates in various sectors of the bond market: Long-Term U.S. Government rates, Short-Term U.S. Government rates, and corporate rates.

We will study these further in several chapters, examining the types and characteristics of bonds, as well as theories on how rates are determined.

Bond Market and Interest Rates

Complete list of interest rateshttp://www.federalreserve.gov/releases

Why Study Financial Markets? Debt Markets & Interest Rates

For the moment, we will turn to other topics, but revisit these topics.

In chapters 2, 9, 10, and 12, we will examine the role of debt markets in the economy.

In chapters 3 through 5, we will examine the characteristics of interest rates.

Why Study Financial Markets? The Stock Market

The stock market is the market where common stock (or just stock), representing ownership in a company, are traded.

Companies initially sell stock (in the primary market) to raise money. But after that, the stock is traded among investors (secondary market).

Of all the active markets, the stock market receives the most attention from the media, probably because it is the place where people get rich (and poor) quickly.

Why Study Financial Markets? The Stock Market

The next slide shows the level of the Dow Jones Industrial Average over the last 55 years. Note how volatile stock prices have been, especially over the last five years.

In future chapters, we will examine the role of the stock market, as well as how prices react to information in the marketplace.

Stock Market

Why Study Financial Markets? The Stock Market

Companies, not just individuals, also watch the market. Although corporations don’t typically “invest” in the market, they often seek additional funding in equity markets after going public. The success of these seasoned-equity offerings (SEOs) is very dependent on the current price of the company’s stock.

Why Study Financial Markets? The Foreign Exchange Market

The foreign exchange market is where international currencies trade and exchange rates are set.

Although most people know little about this market, it has a daily volume around $1 trillion!

View historical financial data and forecasts athttp://www.forecasts.org/data/index.htm

Why Study Financial Markets? The Stock Market

The next slide shows how the U.S. dollar has fluctuated in price against a basket of foreign currencies.

These fluctuations matter!

In recent years, consumers have found that vacationing in Europe is expensive, due to a weakening dollar relative to the Euro.

When the dollar strengthens, foreign purchase of domestic goods falls, and US manufacturers experience a decreased demand for their goods.

Foreign Exchange Market

Why Study Financial Markets? The Stock Market

In future chapters, we will examine how exchange rates are determined in both the short- and long-run.

Why Study Financial Institutions?

We will also spend considerable time discussing financial institutions—the corporations, organizations, and networks that operate the so-called “marketplaces.” These institutions play a crucial role in improving the efficiency of the economy. We will look at:

1. Central Banks and the Conduct of Monetary Policy The role of the Fed and foreign counterparts

2. Structure of the Financial System Helps get funds from savers to investors

Why Study Financial Institutions?

3. Banks and Other Financial Institutions Includes the role of insurance companies, mutual funds,

pension funds, etc.

4. Financial Innovation Focusing on the improvements in technology and its

impact on how financial products are delivered

5. Managing Risk in Financial Institutions Focusing on risk management in the

financial institution.

Applied Managerial Perspective

Financial institutions are among the largest employers in the U.S. and often pay high salaries.

Knowing how financial institutions are managed may help you better deal with them.

How We Study Financial Markets and Institutions

Basic Analytic Framework1. Simplified models are constructed, explained,

and then manipulated to illustrate various phenomena.

2. “Practicing Manager” cases are used to tie theoretical and empirical aspects.

How We Study Financial Markets and Institutions

Basic Analytic Framework3. Actual articles from the Wall Street Journal

reinforcing the concepts from the book, and explanations of articles, helping you develop critical skills to identify key concepts from the day’s news.

How We Study Financial Markets and Institutions

Other features1. Case studies

2. Applications and Numerical Examples

3. Special Interest Boxes

4. Hundred of analytical end-of-chapter problems

5. Predicting the Future problems

Chapter Summary

Why Study Financial Markets?: the three primary markets (bond, stock, and foreign exchange) were briefly introduced.

Why Study Financial Institutions?: the market, institutions, and key changes affecting these were outlined.

Chapter Summary (cont.)

Applied Managerial Perspective: the book will often present material to better understand how actual managers use the information in daily operations.

How We Will Study Financial Markets and Institutions: we outlines the three key components: analytical framework, features, and web exercises.

Chapter 2

Overview of the Financial System

Chapter Preview

Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds.

At the same time, Walter has money he wishes to invest for his retirement.

If the two of you could get together, perhaps both of your needs can be met. But how does that happen?

Chapter Preview

As simple as this example is, it highlights the importance of financial markets and financial intermediaries in our economy.

We need to acquire an understanding of their general structure and operation before we can appreciate their role in our economy.

Chapter Preview

In this chapter, we examine the role of the financial system in an advanced economy. We study the effects of financial markets and institutions on the economy, and look at their general structure and operations. Topics include: Function of Financial Markets Structure of Financial Markets Internationalization of Financial Markets Function of Financial Intermediaries Financial Intermediaries Regulation of the Financial System

Function of Financial Markets

Channels funds from person or business without investment opportunities (i.e., “Lender-Savers”) to one who has them (i.e., “Borrower-Spenders”)

Improves economic efficiency

Financial Markets Funds Transferees

Lender-Savers

1. Households

2. Business firms

3. Government

4. Foreigners

Borrower-Spenders

1. Business firms

2. Government

3. Households

4. Foreigners

Segments of Financial Markets

1. Direct Finance• Borrowers borrow directly from lenders in financial

markets by selling financial instruments which are claims on the borrower’s future income or assets

2. Indirect Finance• Borrowers borrow indirectly from lenders via financial

intermediaries (established to source both loanable funds and loan opportunities) by issuing financial instruments which are claims on the borrower’s future income or assets

Function of Financial Markets

Importance of Financial Markets

This is important. For example, if you save $1,000, but there are no financial markets, then you can earn no return on this – might as well put the money under your mattress.

However, if a carpenter could use that money to buy a new saw (increasing her productivity), then she’d be willing to pay you some interest for the use of the funds.

Importance of Financial Markets

Financial markets are critical for producing an efficient allocation of capital, allowing funds to move from people who lack productive investment opportunities to people who have them.

Financial markets also improve the well-being of consumers, allowing them to time their purchases better.

Structure of Financial Markets

It helps to define financial markets along a variety of dimensions (not necessarily mutually exclusive). For starters, …

Structure of Financial Markets

1. Debt Markets Short-Term (maturity < 1 year) Long-Term (maturity > 10 year) Intermediate term (maturity in-between) Represented $41 trillion at the end of 2007.

2. Equity Markets Pay dividends, in theory forever Represents an ownership claim in the firm Total value of all U.S. equity was $18 trillion at the end

of 2005.

Structure of Financial Markets

1. Primary Market New security issues sold to initial buyers Typically involves an investment bank who underwrites

the offering

2. Secondary Market Securities previously issued are bought

and sold Examples include the NYSE and Nasdaq Involves both brokers and dealers (do you know the

difference?)

Structure of Financial Markets

Even though firms don’t get any money, per se, from the secondary market, it serves two important functions:

• Provide liquidity, making it easy to buy and sell the securities of the companies

• Establish a price for the securities

Structure of Financial Markets

We can further classify secondary markets as follows:

1. Exchanges Trades conducted in central locations

(e.g., New York Stock Exchange, CBT)

2. Over-the-Counter Markets Dealers at different locations buy and sell Best example is the market for Treasury securities

NYSE home pagehttp://www.nyse.com

Classifications of Financial Markets

We can also further classify markets by the maturity of the securities:1. Money Market: Short-Term (maturity < 1 year)

2. Capital Market : Long-Term (maturity > 1 year) plus equities

Internationalization of Financial Markets

The internationalization of markets is an important trend. The U.S. no longer dominates the world stage.

International Bond Market Foreign bonds

Denominated in a foreign currency Targeted at a foreign market

Eurobonds Denominated in one currency, but sold in a different

market now larger than U.S. corporate bond market) Over 80% of new bonds are Eurobonds.

Internationalization of Financial Markets

Eurocurrency Market Foreign currency deposited outside of home country Eurodollars are U.S. dollars deposited, say, London. Gives U.S. borrows an alternative source for dollars.

World Stock Markets U.S. stock markets are no longer always the largest—at

one point, Japan's was larger

Internationalization of Financial Markets

As the next slide shows, the number of international stock market indexes is quite large. For many of us, the level of the Dow or the S&P 500 is known. How about the Nikkei 225? Or the FTSE 100? Do you know what countries these represent?

Internationalization of Financial Markets

Global perspectiveRelative Decline of U.S. Capital Markets

The U.S. has lost its dominance in many industries: auto and consumer electronics to name a few.

A similar trend appears at work for U.S. financial markets, as London and Hong Kong compete. Indeed, many U.S. firms use these markets over the U.S.

Global perspectiveRelative Decline of U.S. Capital Markets

Why?

1. New technology in foreign exchanges

2. 9-11 made U.S. regulations tighter

3. Greater risk of lawsuit in the U.S.

4. Sarbanes-Oxley has increased the cost of being a U.S.-listed public company

Function of FinancialIntermediaries: Indirect Finance

We now turn our attention to the top part of Figure 2.1 – indirect finance.

Function of FinancialIntermediaries : Indirect Finance

Instead of savers lending/investing directly with borrowers, a financial intermediary (such as a bank) plays as the middleman:

the intermediary obtains funds from savers the intermediary then makes

loans/investments with borrowers

Function of FinancialIntermediaries : Indirect Finance

This process, called financial intermediation, is actually the primary means of moving funds from lenders to borrowers.

More important source of finance than securities markets (such as stocks)

Needed because of transactions costs, risk sharing, and asymmetric information

Function of FinancialIntermediaries : Indirect Finance

Transactions Costs

1. Financial intermediaries make profits by reducing transactions costs

2. Reduce transactions costs by developing expertise and taking advantage of economies of scale

Function of FinancialIntermediaries : Indirect Finance

• A financial intermediary’s low transaction costs mean that it can provide its customers with liquidity services, services that make it easier for customers to conduct transactions

1. Banks provide depositors with checking accounts that enable them to pay their bills easily

2. Depositors can earn interest on checking and savings accounts and yet still convert them into goods and services whenever necessary

Global Perspective

• Studies show that firms in the U.S., Canada, the U.K., and other developed nations usually obtain funds from financial intermediaries, not directly from capital markets.

• In Germany and Japan, financing from financial intermediaries exceeds capital market financing 10-fold.

• However, the relative use of bonds versus equity does differ by country.

Function of FinancialIntermediaries : Indirect Finance

Another benefit made possible by the FI’s low transaction costs is that they can help reduce the exposure of investors to risk, through a process known as risk sharing FIs create and sell assets with lesser risk to one

party in order to buy assets with greater risk from another party

This process is referred to as asset transformation, because in a sense risky assets are turned into safer assets for investors

Function of FinancialIntermediaries : Indirect Finance

Financial intermediaries also help by providing the means for individuals and businesses to diversify their asset holdings.

Low transaction costs allow them to buy a range of assets, pool them, and then sell rights to the diversified pool to individuals.

Function of FinancialIntermediaries : Indirect Finance

Another reason FIs exist is to reduce the impact of asymmetric information.

One party lacks crucial information about another party, impacting decision-making.

We usually discuss this problem along two fronts: adverse selection and moral hazard.

Function of FinancialIntermediaries : Indirect Finance

Adverse Selection

1. Before transaction occurs

2. Potential borrowers most likely to produce adverse outcome are ones most likely to seek a loan

3. Similar problems occur with insurance where unhealthy people want their known medical problems covered

Asymmetric Information: Adverse Selection and Moral Hazard

Moral Hazard1. After transaction occurs

2. Hazard that borrower has incentives to engage in undesirable (immoral) activities making it more likely that won't pay loan back

3. Again, with insurance, people may engage in risky activities only after being insured

4. Another view is a conflict of interest

Asymmetric Information: Adverse Selection and Moral Hazard

Financial intermediaries reduce adverse selection and moral hazard problems, enabling them to make profits. How they do this is the covered in many of the chapters to come.

Types of Financial Intermediaries

Types of Financial Intermediaries

Types of Financial Intermediaries

Depository Institutions (Banks): accept deposits and make loans. These include commercial banks and thrifts.

Commercial banks (7,500 currently) Raise funds primarily by issuing checkable, savings, and

time deposits which are used to make commercial, consumer and mortgage loans

Collectively, these banks comprise the largest financial intermediary and have the most diversified asset portfolios

Types of Financial Intermediaries

Thrifts: S&Ls, Mutual Savings Banks (1,500) and Credit Unions (8,900) Raise funds primarily by issuing savings, time, and

checkable deposits which are most often used to make mortgage and consumer loans, with commercial loans also becoming more prevalent at S&Ls and Mutual Savings Banks

Mutual savings banks and credit unions issue deposits as shares and are owned collectively by their depositors, most of which at credit unions belong to a particular group, e.g., a company’s workers

Contractual Savings Institutions (CSIs)

All CSIs acquire funds from clients at periodic intervals on a contractual basis and have fairly predictable future payout requirements. Life Insurance Companies receive funds from policy

premiums, can invest in less liquid corporate securities and mortgages, since actual benefit pay outs are close to those predicted by actuarial analysis

Fire and Casualty Insurance Companies receive funds from policy premiums, must invest most in liquid government and corporate securities, since loss events are harder to predict

Contractual Savings Institutions (CSIs)

All CSIs acquire funds from clients at periodic intervals on a contractual basis and have fairly predictable future payout requirements. Pension and Government Retirement Funds hosted by

corporations and state and local governments acquire funds through employee and employer payroll contributions, invest in corporate securities, and provide retirement income via annuities

Types of Financial Intermediaries

Finance Companies sell commercial paper (a short-term debt instrument) and issue bonds and stocks to raise funds to lend to consumers to buy durable goods, and to small businesses for operations

Mutual Funds acquire funds by selling shares to individual investors (many of whose shares are held in retirement accounts) and use the proceeds to purchase large, diversified portfolios of stocks and bonds

Types of Financial Intermediaries

Money Market Mutual Funds acquire funds by selling checkable deposit-like shares to individual investors and use the proceeds to purchase highly liquid and safe short-term money market instruments

Investment Banks advise companies on securities to issue, underwriting security offerings, offer M&A assistance, and act as dealers in security markets.

Regulatory Agencies

Regulation of Financial Markets

Main Reasons for Regulation

1. Increase Information to Investors

2. Ensure the Soundness of Financial Intermediaries

SEC home pagehttp://www.sec.gov

Regulation Reason: Increase Investor Information

• Asymmetric information in financial markets means that investors may be subject to adverse selection and moral hazard problems that may hinder the efficient operation of financial markets and may also keep investors away from financial markets

• The Securities and Exchange Commission (SEC) requires corporations issuing securities to disclose certain information about their sales, assets, and earnings to the public and restricts trading by the largest stockholders (known as insiders) in the corporation

SEC home pagehttp://www.sec.gov

Regulation Reason: Increase Investor Information

• Such government regulation can reduce adverse selection and moral hazard problems in financial markets and increase their efficiency by increasing the amount of information available to investors. Indeed, the SEC has been particularly active recently in pursuing illegal insider trading.

Regulation Reason: Ensure Soundness of Financial Intermediaries

Providers of funds to financial intermediaries may not be able to assess whether the institutions holding their funds are sound or not.

If they have doubts about the overall health of financial intermediaries, they may want to pull their funds out of both sound and unsound institutions, with the possible outcome of a financial panic.

Such panics produces large losses for the public and causes serious damage to the economy.

Regulation Reason: Ensure Soundness of Financial Intermediaries (cont.)

To protect the public and the economy from financial panics, the government has implemented six types of regulations: Restrictions on Entry Disclosure Restrictions on Assets and Activities Deposit Insurance Limits on Competition Restrictions on Interest Rates

Regulation: Restriction on Entry

Restrictions on Entry Regulators have created very tight regulations as to who is

allowed to set up a financial intermediary

Individuals or groups that want to establish a financial intermediary, such as a bank or an insurance company, must obtain a charter from the state or the federal government

Only if they are upstanding citizens with impeccable credentials and a large amount of initial funds will they be given a charter.

Regulation: Disclosure

Disclosure Requirements

There are stringent reporting requirements for financial intermediaries Their bookkeeping must follow certain strict principles, Their books are subject to periodic inspection, They must make certain information available to

the public.

Regulation: Restriction on Assets and Activities

There are restrictions on what financial intermediaries are allowed to do and what assets they can hold

Before you put your funds into a bank or some other such institution, you would want to know that your funds are safe and that the bank or other financial intermediary will be able to meet its obligations to you

Regulation: Restriction on Assets and Activities

One way of doing this is to restrict the financial intermediary from engaging in certain risky activities

Another way is to restrict financial intermediaries from holding certain risky assets, or at least from holding a greater quantity of these risky assets than is prudent

Regulation: Deposit Insurance

The government can insure people depositors to a financial intermediary from any financial loss if the financial intermediary should fail

The Federal Deposit Insurance Corporation (FDIC) insures each depositor at a commercial bank or mutual savings bank up to a loss of $100,000 per account ($250,000 for IRAs)

Regulation: Deposit Insurance

Similar government agencies exist for other depository institutions: The National Credit Union Share Insurance Fund

(NCUSIF) provides insurance for credit unions

Regulation: Past Limits on Competition

Although the evidence that unbridled competition among financial intermediaries promotes failures that will harm the public is extremely weak, it has not stopped the state and federal governments from imposing many restrictive regulations

In the past, banks were not allowed to open up branches in other states, and in some states banks were restricted from opening additional locations

Regulation: Past Restrictions on Interest Rates

Competition has also been inhibited by regulations that impose restrictions on interest rates that can be paid on deposits

These regulations were instituted because of the widespread belief that unrestricted interest-rate competition helped encourage bank failures during the Great Depression

Later evidence does not seem to support this view, and restrictions on interest rates have been abolished

Regulation Reason: Improve Monetary Control

Because banks play a very important role in determining the supply of money (which in turn affects many aspects of the economy), much regulation of these financial intermediaries is intended to improve control over the money supply

One such regulation is reserve requirements, which make it obligatory for all depository institutions to keep a certain fraction of their deposits in accounts with the Federal Reserve System (the Fed), the central bank in the United States

Reserve requirements help the Fed exercise more precise control over the money supply

Financial Regulation Abroad

Those countries with similar economic systems also implement financial regulation consistent with the U.S. model: Japan, Canada, and Western Europe Financial reporting for corporations is required Financial intermediaries are heavily regulated

However, U.S. banks are more regulated along dimensions of branching and services than their foreign counterparts.

Chapter Summary

Function of Financial Markets: We examined the flow of funds through the financial system and the role of intermediaries in this process.

Structure of Financial Markets: We examined market structure from several perspectives, including types of instruments, purpose, organization, and time horizon.

Chapter Summary (cont.)

Internationalization of Financial Markets: We briefly examined how debt and equity markets have expanded in the international setting.

Function of Financial Intermediaries: We examined the roles of intermediaries in reducing transaction costs, sharing risk, and reducing information problems.

Chapter Summary (cont.)

Financial Intermediaries: We outlined the numerous types of financial intermediaries to be further examined in later chapters.

Regulation of the Financial System: We outlined some of the agencies charged with the oversight of various institutions and markets.

Part Two

Fundamentals of Financial Markets

Chapter 3

What Do Interest Rates Mean and What Is

Their Role in Valuation?

Chapter Preview

Interest rates are among the most closely watched variables in the economy. It is imperative that what exactly is meant by the phrase interest rates is understood. In this chapter, we will see that a concept known as yield to maturity (YTM) is the most accurate measure of interest rates.

Chapter Preview

Any description of interest rates entails an understanding certain vernacular and definitions, most of which will not only pertain directly to interest rates but will also be vital to understanding many other foundational concepts presented later in the text.

Chapter Preview So, in this chapter, we will develop a better

understanding of interest rates. We examine the terminology and calculation of various rates, and we show the importance of these rates in our lives and the general economy. Topics include:

Measuring Interest Rates

The Distinction Between Real and Nominal Interest Rates

The Distinction Between Interest Rates and Returns

Present Value Introduction

Different debt instruments have very different streams of cash payments to the holder (known as cash flows), with very different timing.

All else being equal, debt instruments are evaluated against one another based on the amount of each cash flow and the timing of each cash flow.

This evaluation, where the analysis of the amount and timing of a debt instrument’s cash flows lead to its yield to maturity or interest rate, is called present value analysis.

Present Value

The concept of present value (or present discounted value) is based on the commonsense notion that a dollar of cash flow paid to you one year from now is less valuable to you than a dollar paid to you today. This notion is true because you could invest the dollar in a savings account that earns interest and have more than a dollar in one year.

The term present value (PV) can be extended to mean the PV of a single cash flow or the sum of a sequence or group of cash flows.

Present Value Applications

There are four basic types of credit instruments which incorporate present value concepts:

1. Simple Loan

2. Fixed Payment Loan

3. Coupon Bond

4. Discount Bond

Present Value Concept: Simple Loan Terms

Loan Principal: the amount of funds the lender provides to the borrower.

Maturity Date: the date the loan must be repaid; the Loan Term is from initiation to maturity date.

Interest Payment: the cash amount that the borrower must pay the lender for the use of the loan principal.

Simple Interest Rate: the interest payment divided by the loan principal; the percentage of principal that must be paid as interest to the lender. Convention is to express on an annual basis, irrespective of the loan term.

Simple loan of $100

Year: 0 1 2 3 n

$100 $110 $121 $133 100(1+i)n

PV of future $1 =$1

1+ i n

Present Value Concept: Simple Loan

Present Value Concept: Simple Loan (cont.)

The previous example reinforces the concept that $100 today is preferable to $100 a year from now since today’s $100 could be lent out (or deposited) at 10% interest to be worth $110 one year from now, or $121 in two years or $133 in three years.

Yield to Maturity: Loans

Yield to maturity = interest rate that equates today's value with present value of all future payments

1. Simple Loan Interest Rate (i = 10%)

$100 $110 1 i

i $110 $100

$100

$10

$100.10 10%

Present Value of Cash Flows: Example

Present Value Concept: Fixed-Payment Loan Terms

Simple Loans require payment of one amount which equals the loan principal plus the interest.

Fixed-Payment Loans are loans where the loan principal and interest are repaid in several payments, often monthly, in equal dollar amounts over the loan term.

Present Value Concept: Fixed-Payment Loan Terms

Installment Loans, such as auto loans and home mortgages are frequently of the fixed-payment type.

Yield to Maturity: Loans

2. Fixed Payment Loan (i = 12%)

$1000 $126

1 i

$126

1 i 2 $126

1 i 3 ... $126

1 i 25

LV FP

1 i

FP

1 i 2 FP

1 i 3 ... FP

1 i n

Yield to Maturity: Bonds

3. Coupon Bond (Coupon rate = 10% = C/F)

P $100

1 i

$100

1 i 2 $100

1 i 3 ... $100

1 i 10 $1000

1 i 10

P C

1 i

C

1 i 2 C

1 i 3 ... C

1 i n F

1 i n

Consol: Fixed coupon payments of $C forever

P C

ii

C

P

Yield to Maturity: Bonds

4. One-Year Discount Bond (P = $900, F = $1000)

$900 $1000

1 i

i $1000 $900

$900.111 11.1%

i F P

P

Relationship Between Price and Yield to Maturity

Three interesting facts in Table 3-11. When bond is at par, yield equals coupon rate2. Price and yield are negatively related3. Yield greater than coupon rate when bond price

is below par value

Relationship Between Price and Yield to Maturity It’s also straight-forward to show that the value of a

bond (price) and yield to maturity (YTM) are negatively related. If i increases, the PV of any given cash flow is lower; hence, the price of the bond must be lower.

Current Yield

Current yield (CY) is just an approximation for YTM – easier to calculate. However, we should be aware of its properties:

1. If a bond’s price is near par and has a long maturity, then CY is a good approximation.

2. A change in the current yield always signals change in same direction as yield to maturity

ic C

P

idb (F - P)

F

360

(number of days to maturity)

idb $1000 - $900

$1000

360

365.099 9.9%

Two Characteristics1. Understates yield to maturity; longer the maturity,

greater is understatement

2. Change in discount yield always signals change in same direction as yield to maturity

Yield on a Discount Basis

One-Year Bill (P = $900, F = $1000)

Bond Page of the Newspaper

Global perspective

In November 1998, rates on Japanese 6-month government bonds were negative! Investors were willing to pay more than they would receive in the future.

Best explanation is that investors found the convenience of the bills worth something – more convenient than cash. But that can only go so far – the rate was only slightly negative.

Distinction Between Real and Nominal Interest Rates

Real interest rate1. Interest rate that is adjusted for expected

changes in the price level

ir i e

2. Real interest rate more accurately reflects true cost of borrowing

3. When the real rate is low, there are greater incentives to borrow and less to lend

Distinction Between Real and Nominal Interest Rates

Real interest rate

ir i e

We usually refer to this rate as the ex ante real rate of interest because it is adjusted for the expected level of inflation. After the fact, we can calculate the ex post real rate based on the observed level of inflation.

Distinction Between Real and Nominal Interest Rates (cont.)

If i = 5% and πe = 0% then

ir 5% 0% 5%

ir 10% 20% 10%

• If i = 10% and πe = 20% then

U.S. Real and Nominal Interest Rates

Sample of current rates and indexeshttp://www.martincapital.com/charts.htm

Distinction Between Interest Rates

and Returns

Rate of Return: we can decompose returns into two pieces:

giP

PPc

t

tt

1CReturn

tc P

Ci where = current yield, and

t

tt

P

PP 1g = capital gains.

Key Facts about the Relationship Between Rates and Returns

Sample of current coupon rates and yields on government bondshttp://www.bloomberg.com/markets/iyc.html

Maturity and the Volatility of Bond Returns

Key findings from Table 3-2

1. Only bond whose return = yield is one with maturity = holding period

2. For bonds with maturity > holding period, i P implying capital loss

3. Longer is maturity, greater is price change associated

with interest rate change

Maturity and the Volatility of Bond Returns (cont.)

Key findings from Table 3-2 (continued)

4. Longer is maturity, more return changes with change in interest rate

5. Bond with high initial interest rate can still have negative return if i

Maturity and the Volatility of Bond Returns (cont.)

Conclusion from Table 3-2 analysis

1. Prices and returns more volatile for long-term bonds because have higher interest-rate risk

2. No interest-rate risk for any bond whose maturity equals holding period

Reinvestment Risk

1. Occurs if hold series of short bonds over long holding period

2. i at which reinvest uncertain

3. Gain from i , lose when i

Calculating Durationi =10%, 10-Year 10% Coupon Bond

126

Calculating Durationi = 20%, 10-Year 10% Coupon Bond

DUR tCPt

1 i tt 1

n

CPt

1 i tt 1

n

Formula for Duration

Key facts about duration1. All else equal, when the maturity of a bond

lengthens, the duration rises as well

2. All else equal, when interest rates rise, the duration of a coupon bond fall

Formula for Duration

1. The higher is the coupon rate on the bond, the shorter is the duration of the bond

2. Duration is additive: the duration of a portfolio of securities is the weighted-average of the durations of the individual securities, with the weights equaling the proportion of the portfolio invested in each

%P DURi

1 i

%P 6.76 0.01

1 0.10

%P 0.0615 6.15%

Duration and Interest-Rate Risk

i 10% to 11%: Table 3-4, 10% coupon bond

Duration and Interest-Rate Risk (cont.)

i 10% to 11%: 20% coupon bond, DUR = 5.72 years

%P 5.72 0.01

1 0.10

%P 0.0520 5.20%

The greater is the duration of a security, the greater is the percentage change in the market value of the security for a given change in interest rates

Therefore, the greater is the duration of a security, the greater is its interest-rate risk

Duration and Interest-Rate Risk (cont.)

Chapter Summary

Measuring Interest Rates: We examined several techniques for measuring the interest rate required on debt instruments.

The Distinction Between Real and Nominal Interest Rates: We examined the meaning of interest in the context of price inflation.

Chapter Summary (cont.)

The Distinction Between Interest Rates and Returns: We examined what each means and how they should be viewed for asset valuation.

Chapter 4

Why Do Interest Rates Change?

Chapter Preview

In the early 1950s, short-term Treasury bills were yielding about 1%. By 1981, the yields rose to 15% and higher. But then dropped back to 1% by 2003.

What causes these changes?

Chapter Preview

In this chapter, we examine the forces the move interest rates and the theories behind those movements. Topics include: Determining Asset Demand Supply and Demand in the Bond Market Changes in Equilibrium Interest Rates

Determinants of Asset Demand

An asset is a piece of property that is a store of value. Facing the question of whether to buy and hold an asset or whether to buy one asset rather than another, an individual must consider the following factors:

1. Wealth, the total resources owned by the individual, including all assets

2. Expected return (the return expected over the next period) on one asset relative to alternative assets

3. Risk (the degree of uncertainty associated with the return) on one asset relative to alternative assets

4. Liquidity (the ease and speed with which an asset can be turned into cash) relative to alternative assets

EXAMPLE 1: Expected Return

What is the expected return on an Exxon-Mobil bond if the return is 12% two-thirds of the time and 8% one-third of the time?

Solution

The expected return is 10.68%.

Re = p1R1 + p2R2

where

p1 = probability of occurrence of return 1 = 2/3 = .67

R1 = return in state 1 = 12% = 0.12

p2 = probability of occurrence return 2 = 1/3 = .33

R2 = return in state 2 = 8% = 0.08

Thus

Re = (.67)(0.12) + (.33)(0.08) = 0.1068 = 10.68%

EXAMPLE 2: Standard Deviation (a)

Consider the following two companies and their forecasted returns for the upcoming year:

F ly-by-Night F eet-on-the-G roundP robability 50% 100%R eturn 15% 10%P robability 50%R eturn 5%

O utcome 1

O utcome 2

EXAMPLE 2: Standard Deviation (b)

What is the standard deviation of the returns on the Fly-by-Night Airlines stock and Feet-on-the-Ground Bus Company, with the return outcomes and probabilities described above? Of these two stocks, which is riskier?

EXAMPLE 2: Standard Deviation (c)

Solution Fly-by-Night Airlines has a standard deviation of returns of 5%.

EXAMPLE 2: Standard Deviation (d)

Feet-on-the-Ground Bus Company has a standard deviation of returns of 0%.

EXAMPLE 2: Standard Deviation (e)

Fly-by-Night Airlines has a standard deviation of returns of 5%; Feet-on-the-Ground Bus Company has a standard deviation of returns of 0%

Clearly, Fly-by-Night Airlines is a riskier stock because its standard deviation of returns of 5% is higher than the zero standard deviation of returns for Feet-on-the-Ground Bus Company, which has a certain return

A risk-averse person prefers stock in the Feet-on-the-Ground (the sure thing) to Fly-by-Night stock (the riskier asset), even though the stocks have the same expected return, 10%. By contrast, a person who prefers risk is a risk preferrer or risk lover. We assume people are risk-averse, especially in their financial decisions

Determinants of Asset Demand (2) The quantity demanded of an asset differs by factor.

1. Wealth: Holding everything else constant, an increase in wealth raises the quantity demanded of an asset

2. Expected return: An increase in an asset’s expected return relative to that of an alternative asset, holding everything else unchanged, raises the quantity demanded of the asset

3. Risk: Holding everything else constant, if an asset’s risk rises relative to that of alternative assets, its quantity demanded will fall

4. Liquidity: The more liquid an asset is relative to alternative assets, holding everything else unchanged, the more desirable

it is, and the greater will be the quantity demanded

Determinants of Asset Demand (3)

Supply & Demand in the Bond Market

We now turn our attention to the mechanics of interest rates. That is, we are going to examine how interest rates are determined – from a demand and supply perspective. Keep in mind that these forces act differently in different bond markets. That is, current supply/demand conditions in the corporate bond market are not necessarily the same as, say, in the mortgage market. However, because rates tend to move together, we will proceed as if there is one interest rate for the entire economy.

The Demand Curve

Let’s start with the demand curve.

Let’s consider a one-year discount bond with a face value of $1,000. In this case, the return on this bond is entirely determined by its price. The return is, then, the bond’s yield to maturity.

Point B: if the bond was selling for $900.

i Re F P

P

P $950

i $1000 $950

$950.053 5.3%

Bd 100

P $900

i $1000 $900

$900.111 11.1%

Bd 200

Derivation of Demand Curve

Point A: if the bond was selling for $950.

Derivation of Demand Curve

How do we know the demand (Bd) at point A is 100 and at point B is 200?

Well, we are just making-up those numbers. But we are applying basic economics – more people will want (demand) the bonds if the expected return is higher.

Derivation of Demand Curve

To continue …

Point C: P = $850 i = 17.6% Bd = 300

Point D: P = $800 i = 25.0% Bd = 400

Point E: P = $750 i = 33.0% Bd = 500

Demand Curve is Bd in Figure 1 which connects points A, B, C, D, E. Has usual downward slope

Supply and Demand for Bonds

Derivation of Supply Curve

In the last figure, we snuck the supply curve in – the line connecting points F, G, C, H, and I. The derivation follows the same idea as the demand curve.

Derivation of Supply Curve

Point F: P = $750 i = 33.0% Bs = 100 Point G: P = $800 i = 25.0% Bs = 200 Point C: P = $850 i = 17.6% Bs = 300 Point H: P = $900 i = 11.1% Bs = 400 Point I: P = $950 i = 5.3% Bs = 500 Supply Curve is Bs that connects points F, G,

C, H, I, and has upward slope

Derivation of Demand Curve

How do we know the supply (Bs) at point P is 100 and at point G is 200?

Again, like the demand curve, we are just making-up those numbers. But we are applying basic economics – more people will offer (supply) the bonds if the expected return is lower.

Market Equilibrium

The equilibrium follows what we know from supply-demand analysis:

1. Occurs when Bd = Bs, at P* = 850, i* = 17.6%

2. When P = $950, i = 5.3%, Bs > Bd (excess supply): P to P*, i to i*

3. When P = $750, i = 33.0, Bd > Bs (excess demand): P to P*, i to i*

Market Conditions

Market equilibrium occurs when the amount that people are willing to buy (demand) equals the amount that people are willing to sell (supply) at a given price

Excess supply occurs when the amount that people are willing to sell (supply) is greater than the amount people are willing to buy (demand) at a given price

Excess demand occurs when the amount that people are willing to buy (demand) is greater than the amount that people are willing to sell (supply) at a given price

Supply & Demand Analysis

Notice in Figure 1 that we use two different verticle axes – one with price, which is high-to-low starting from the top, and one with interest rates, which is low-to-high starting from the top.

This just illustrates what we already know: bond prices and interest rates are inversely related.

Also note that this analysis is an asset market approach based on the stock of bonds. Another way to do this is to examine the flows. However, the flows approach is tricky, especially with inflation in the mix. So we will focus on the stock approach.

Changes in Equilibrium Interest Rates

We now turn our attention to changes in interest rate. We focus on actual shifts in the curves. Remember: movements along the curve will be due to price changes alone.

First, we examine shifts in the demand for bonds. Then we will turn to the supply side.

Factors That Shift Demand Curve

How Factors Shift the Demand Curve

1. Wealth/saving Economy , wealth Bd , Bd shifts out to right

OR

Economy , wealth Bd , Bd shifts out to right

How Factors Shift the Demand Curve

2. Expected Returns on bonds i in future, Re for long-term bonds Bd shifts out to right

OR πe , relative Re Bd shifts out to right

How Factors Shift the Demand Curve

2. …and Expected Returns on other assets ER on other asset (stock) Re for long-term bonds Bd shifts out to left

These are closely tied to expected interest rate and expected inflation from Table 4.2

How Factors Shift the Demand Curve

3. Risk Risk of bonds , Bd Bd shifts out to rightOR Risk of other assets , Bd Bd shifts out to right

How Factors Shift the Demand Curve

4. Liquidity Liquidity of bonds , Bd Bd shifts out to rightOR Liquidity of other assets , Bd Bd shifts out to right

Shifts in the Demand Curve

Summary of Shifts in the Demand for Bonds

1. Wealth: in a business cycle expansion with growing wealth, the demand for bonds rises, conversely, in a recession, when income and wealth are falling, the demand for bonds falls

2. Expected returns: higher expected interest rates in the future decrease the demand for long-term bonds, conversely, lower expected interest rates in the future increase the demand for long-term bonds

Summary of Shifts in the Demand for Bonds (2)

3. Risk: an increase in the riskiness of bonds causes the demand for bonds to fall, conversely, an increase in the riskiness of alternative assets (like stocks) causes the demand for bonds to rise

4. Liquidity: increased liquidity of the bond market results in an increased demand for bonds, conversely, increased liquidity of alternative asset markets (like the stock market) lowers the demand for bonds

Factors That Shift Supply CurveWe now turn to the supply curve. We summarize the effects in this table:

Shifts in the Supply Curve

1. Profitability of Investment Opportunities

Business cycle expansion, investment opportunities , Bs , Bs shifts out to right

Shifts in the Supply Curve

2. Expected Inflation πe , Bs Bs shifts out

to right

3. Government Activities

– Deficits , Bs – Bs shifts out to right

Shifts in the Supply Curve

Summary of Shifts in the Supply of Bonds

1. Expected Profitability of Investment Opportunities: in a business cycle expansion, the supply of bonds increases, conversely, in a recession, when there are far fewer expected profitable investment opportunities, the supply of bonds falls

2. Expected Inflation: an increase in expected inflation causes the supply of bonds to increase

3. Government Activities: higher government deficits increase the supply of bonds, conversely, government surpluses decrease the supply of bonds

Case: Fisher Effect

We’ve done the hard work. Now we turn to some special cases. The first is the Fisher Effect. Recall that rates are composed of several components: a real rate, an inflation premium, and various risk premiums.

What if there is only a change in expected inflation?

Changes in πe: The Fisher Effect

If πe 1. Relative Re ,

Bd shifts in to left

2. Bs , Bs shifts out to right

3. P , i

Evidence on the Fisher Effect in the United States

Summary of the Fisher Effect

1. If expected inflation rises from 5% to 10%, the expected return on bonds relative to real assets falls and, as a result, the demand for bonds falls

2. The rise in expected inflation also means that the real cost of borrowing has declined, causing the quantity of bonds supplied to increase

3. When the demand for bonds falls and the quantity of bonds supplied increases, the equilibrium bond price falls

4. Since the bond price is negatively related to the interest rate, this means that the interest rate will rise

Case: Business Cycle Expansion

Another good thing to examine is an expansionary business cycle. Here, the amount of goods and services for the country is increasing, so national income is increasing.

What is the expected effect on interest rates?

Business Cycle Expansion

1. Wealth , Bd , Bd shifts out to right

2. Investment , Bs , Bs shifts right

3. If Bs shifts more than Bd then P , i

Evidence on Business Cycles and Interest Rates

Case: Low Japanese Interest Rates

In November 1998, Japanese interest rates on six-month Treasury bills turned slightly negative. How can we explain that within the framework discussed so far?

It’s a little tricky, but we can do it!

Case: Low Japanese Interest Rates

1. Negative inflation lead to Bd • Bd shifts out to right

2. Negative inflation lead to in real rates• Bs shifts out to left

Net effect was an increase in bond prices (falling interest rates).

Case: Low Japanese Interest Rates

3. Business cycle contraction lead to in interest rates

• Bs shifts out to left• Bd shifts out to left

But the shift in Bd is less significant than the shift in Bs, so the net effect was also an increase in bond prices.

Case: WSJ “Credit Markets”

Everyday, the Wall Street Journal reports on developments in the bond market in its “Credit Markets” column.

Let’s look at an example and how to interpret what it says.

WSJ article

Case: WSJ “Credit Markets”

What is this article telling us? Strength in a sector helped lower T-bond

prices (increase rates). That follows what we learned!

A stronger economy shifts both curves to the right, but the supply curve by more, so prices will fall.

Case: WSJ “Credit Markets”

Article also points out that yields on gov’t bonds in Germany and Japan are rising. Money will move from the U.S. Treasury market to these markets, shifting the demand curve to the left (falling prices).

The strong economy also suggests a lower chance of future Fed rate cuts, further shifting the demand curve to the left.

The Practicing Manager

We now turn to a more practical side to all this. Many firms have economists or hire consultants to forecast interest rates. Although this can be difficult to get right, it is important to understand what to do with a given interest rate forecast.

Profiting from Interest-Rate Forecasts

Methods for forecasting1. Supply and demand for bonds: use Flow of

Funds Accounts and judgment

2. Econometric Models: large in scale, use interlocking equations that assume past financial relationships will hold in the future

Profiting from Interest-Rate Forecasts (cont.)

Make decisions about assets to hold1. Forecast i , buy long bonds

2. Forecast i , buy short bonds

Make decisions about how to borrow1. Forecast i , borrow short

2. Forecast i , borrow long

Chapter Summary

Determining Asset Demand: We examined the forces that affect the demand and supply of assets.

Supply and Demand in the Bond Market: We examine those forces in the context of bonds, and examined the impact on interest rates.

Chapter Summary (cont.)

Changes in Equilibrium Interest Rates: We further examined the dynamics of changes in supply and demand in the bond market, and the corresponding effect on bond prices and interest rates.

Chapter 5

How Do The Risk and Term Structure Affect Interest Rates

Chapter Preview

In the last chapter, we examined interest rates, but made a big assumption – there is only one economy-wide interest rate. Of course, that isn’t really the case.

In this chapter, we will examine the different rates that we observe for financial products.

Chapter Preview

We will fist examine bonds that offer similar payment streams but differ in price. The price differences are due to the risk structure of interest rates. We will examine in detail what this risk structure looks like and ways to examine it.

Chapter Preview

Next, we will look at the different rates required on bonds with different maturities. That is, we typically observe higher rates on longer-term bonds. This is known as the term structure of interest rates. To study this, we usually look at Treasury bonds to minimize the impact of other risk factors.

Chapter Preview

So, in sum, we will examine how the individual risk of a bond affects its required rate. We also explore how the general level of interest rates varies with the maturity of the debt instruments. Topics include:

Risk Structure of Interest Rates

Term Structure of Interest Rates

Risk Structure of Interest Rates

To start this discussion, we first examine the yields for several categories of long-term bonds over the last 85 years.

You should note several aspects regarding these rates, related to different bond categories and how this has changed through time.

Risk Structure of Long Bonds in the U.S.

Risk Structure of Long Bonds in the U.S.

The figure show two important features of the interest-rate behavior of bonds.

Rates on different bond categories change from one year to the next.

Spreads on different bond categories change from one year to the next.

Factors Affecting Risk Structure of Interest Rates

To further examine these features, we will look at three specific risk factors.

Default Risk

Liquidity

Income Tax Considerations

Default Risk Factor One attribute of a bond that influences its interest

rate is its risk of default, which occurs when the issuer of the bond is unable or unwilling to make interest payments when promised.

U.S. Treasury bonds have usually been considered to have no default risk because the federal government can always increase taxes to pay off its obligations (or just print money). Bonds like these with no default risk are called default-free bonds.

Default Risk Factor (cont.) The spread between the interest rates on bonds

with default risk and default-free bonds, called the risk premium, indicates how much additional interest people must earn in order to be willing to hold that risky bond.

A bond with default risk will always have a positive risk premium, and an increase in its default risk will raise the risk premium.

Increase in Default Risk on Corporate Bonds

Analysis of Figure 5.2: Increase in Default on Corporate Bonds

Corporate Bond Market1. Re on corporate bonds , Dc , Dc shifts left2. Risk of corporate bonds , Dc , Dc shifts left3. Pc , ic

Treasury Bond Market4. Relative Re on Treasury bonds , DT , DT shifts right5. Relative risk of Treasury bonds , DT , DT shifts right6. PT , iT

Outcome Risk premium, ic - iT, rises

Default Risk Factor (cont.) Default risk is an important component of the size of

the risk premium. Because of this, bond investors would like to know

as much as possible about the default probability of a bond.

One way to do this is to use the measures provided by credit-rating agencies: Moody’s and S&P are examples.

Bond Ratings

Case: Enron and the Baa-Aaa spread

Enron filed for bankruptcy in December 2001, amidst an accounting scandal.

Because of the questions raised about the quality of auditors, the demand for lower-credit bonds fell, and a “flight- to-quality” followed (demand for T-securities increased.

Result: Baa-Aaa spread increased from 84 bps to 128 bps.

Liquidity Factor

Another attribute of a bond that influences its interest rate is its liquidity; a liquid asset is one that can be quickly and cheaply converted into cash if the need arises. The more liquid an asset is, the more desirable it is (higher demand), holding everything else constant.

Let’s examine what happens if a corporate bond becomes less liquid (Figure 1 again).

Decrease in Liquidity of Corporate Bonds

Figure 5.2 Response to a Decrease in the Liquidity of Corporate Bonds

Analysis of Figure 5.1: Corporate Bond Becomes Less Liquid

Corporate Bond Market1. Liquidity of corporate bonds , Dc , Dc shifts left

2. Pc , ic Treasury Bond Market

1. Relatively more liquid Treasury bonds, DT , DT shifts right

2. PT , iT Outcome

Risk premium, ic - iT, rises Risk premium reflects not only corporate bonds' default risk but

also lower liquidity

Liquidity Factor (cont.)

The differences between interest rates on corporate bonds and Treasury bonds (that is, the risk premiums) reflect not only the corporate bond’s default risk but its liquidity too. This is why a risk premium is sometimes called a risk and liquidity premium.

Income Taxes Factor

An odd feature of Figure 1 is that municipal bonds tend to have a lower rate the Treasuries. Why?

Munis certainly can default. Orange County (California) is a recent example from the early 1990s.

Munis are not as liquid a Treasuries.

Income Taxes Factor

However, interest payments on municipal bonds are exempt from federal income taxes, a factor that has the same effect on the demand for municipal bonds as an increase in their expected return.

Treasury bonds are exempt from state and local income taxes, while interest payments from corporate bonds are fully taxable.

Income Taxes Factor

For example, suppose you are in the 35% tax bracket. From a 10%-coupon Treasury bond, you only net $65 of the coupon payment because of taxes

However, from an 8%-coupon muni, you net the full $80. For the higher return, you are willing to hold a riskier muni (to a point).

Tax Advantages of Municipal Bonds

Analysis of Figure 5.3: Tax Advantages of Municipal Bonds

Municipal Bond Market1. Tax exemption raises relative Re on municipal bonds,

Dm , Dm shifts right2. Pm

Treasury Bond Market1. Relative Re on Treasury bonds , DT , DT shifts left2. PT

Outcomeim < iT

Case: Bush Tax Cut and Interest Rates

The 2001 tax cut called for a reduction in the top tax bracket, from 39% to 35% over a 10-year period.

This reduces the advantage of municipal debt over T-securities since the interest on T-securities is now taxed at a lower rate.

Term Structure of Interest Rates

Now that we understand risk, liquidity, and taxes, we turn to another important influence on interest rates – maturity.

Bonds with different maturities tend to have different required rates, all else equal.

The WSJ: Following the News

For example, the WSJ publishes a plot of the yield curve (rates at different maturities) for Treasury securities.

The picture on the following slide is a typical example, from May 14, 2007.

What is the 3-month rate? The two-year rate?

Reading the Wall St. Journal

Dynamic yield curve that can show the curve at any time in historyhttp://stockcharts.com/charts/YieldCurve.html

Term Structure Facts to Be Explained

Besides explaining the shape of the yield curve, a good theory must explain why:

Interest rates for different maturities move together. We see this on the next slide.

Interest Rates on Different Maturity Bonds Move Together

Term Structure Facts to Be Explained

Besides explaining the shape of the yield curve, a good theory must explain why:

Interest rates for different maturities move together.

Yield curves tend to have steep upward slope when short rates are low and downward slope when short rates are high.

Yield curve is typically upward sloping.

Three Theories of Term Structure

1. Expectations Theory Pure Expectations Theory explains 1 and 2,

but not 3

2. Market Segmentation Theory Market Segmentation Theory explains 3, but not 1 and 2

3. Liquidity Premium Theory Solution: Combine features of both Pure Expectations

Theory and Market Segmentation Theory to get Liquidity Premium Theory and explain all facts

Expectations Theory

Key Assumption: Bonds of different maturities are perfect substitutes

Implication: Re on bonds of different maturities are equal

Expectations Theory

To illustrate what this means, consider two alternative investment strategies for a two-year time horizon.

1. Buy $1 of one-year bond, and when it matures, buy another one-year bond with your money.

2. Buy $1 of two-year bond and hold it.

Expectations Theory

The important point of this theory is that if the Expectations Theory is correct, your expected wealth is the same (a the start) for both strategies. Of course, your actual wealth may differ, if rates change unexpectedly after a year.

We show the details of this in the next few slides.

(1 it)(1 i

t1e ) 11 i

t i

t1e i

t(i

t1e ) 1

Expectations Theory

Expected return from strategy 1

Since it(iet+1) is also extremely small, expected return is approximately

it + iet+1

(1 i2t

)(1 i2t

) 11 2(i2t

) (i2t

)2 1

Since (i2t)2 is extremely small, expected return is approximately 2(i2t)

Expectations Theory

Expected return from strategy 2

i2t it it1

e

2

Expectations Theory

From implication above expected returns of two strategies are equal

Therefore

2 i2t it it1e

Solving for i2t

(1)

Expectations Theory

To help see this, here’s a picture that describes the same information:

int it it1 it2 ... it n 1

n

More generally for n-period bond…

Don’t let this seem complicated. Equation 2 simply states that the interest rate on a long-term bond equals the average of short rates expected to occur over life of the long-term bond.

(2)

More generally for n-period bond…

Numerical example One-year interest rate over the next five years

are expected to be 5%, 6%, 7%, 8%, and 9%

Interest rate on two-year bond today:(5% + 6%)/2 = 5.5%

Interest rate for five-year bond today:(5% + 6% + 7% + 8% + 9%)/5 = 7%

Interest rate for one- to five-year bonds today:5%, 5.5%, 6%, 6.5% and 7%

Expectations Theory and Term Structure Facts

Explains why yield curve has different slopes1. When short rates are expected to rise in future, average

of future short rates = int is above today's short rate; therefore yield curve is upward sloping.

2. When short rates expected to stay same in future, average of future short rates same as today's, and yield curve is flat.

3. Only when short rates expected to fall will yield curve be downward sloping.

Expectations Theory and Term Structure Facts

Pure expectations theory explains fact 1—that short and long rates move together

1. Short rate rises are persistent

2. If it today, iet+1, iet+2 etc. average of future rates int

3. Therefore: it int (i.e., short and long rates move together)

Expectations Theory and Term Structure Facts

Explains fact 2—that yield curves tend to have steep slope when short rates are low and downward slope when short rates are high

1. When short rates are low, they are expected to rise to normal level, and long rate = average of future short rates will be well above today's short rate; yield curve will have steep upward slope.

2. When short rates are high, they will be expected to fall in future, and long rate will be below current short rate; yield curve will have downward slope.

Expectations Theory and Term Structure Facts

Doesn't explain fact 3—that yield curve usually has upward slope Short rates are as likely to fall in future as rise, so

average of expected future short rates will not usually be higher than current short rate: therefore, yield curve will not usually slope upward.

Market Segmentation Theory Key Assumption: Bonds of different maturities are not

substitutes at all

Implication: Markets are completely segmented;interest rate at each maturity aredetermined separately

Market Segmentation Theory

Explains fact 3—that yield curve is usually upward sloping People typically prefer short holding periods and thus have

higher demand for short-term bonds, which have higher prices and lower interest rates than long bonds

Does not explain fact 1or fact 2 because its assumes long-term and short-term rates are determined independently.

Liquidity Premium Theory

Key Assumption: Bonds of different maturities are substitutes, but are not perfect substitutes

Implication: Modifies Pure Expectations Theory with features of Market Segmentation Theory

Liquidity Premium Theory

Investors prefer short-term rather than long-term bonds. This implies that investors must be paid positive liquidity premium, int, to hold long term bonds.

int

it it1e it 2

e ... it n 1 e

nnt

Liquidity Premium Theory

Results in following modification of Expectations Theory, where lnt is the liquidity premium.

(3)

We can also see this graphically…

Liquidity Premium Theory

Numerical Example

1. One-year interest rate over the next five years: 5%, 6%, 7%, 8%, and 9%

2. Investors' preferences for holding short-term bonds so liquidity premium for one- to five-year bonds: 0%, 0.25%, 0.5%, 0.75%, and 1.0%

Numerical Example

Interest rate on the two-year bond:0.25% + (5% + 6%)/2 = 5.75%

Interest rate on the five-year bond:1.0% + (5% + 6% + 7% + 8% + 9%)/5 = 8%

Interest rates on one to five-year bonds:5%, 5.75%, 6.5%, 7.25%, and 8%

Comparing with those for the pure expectations theory, liquidity premium theory produces yield curves more steeply upward sloped

Liquidity Premium Theory: Term Structure Facts

Explains All 3 Facts Explains fact 3—that usual upward sloped yield

curve by liquidity premium for long-term bonds

Explains fact 1 and fact 2 using same explanations as pure expectations theory because it has average of future short rates as determinant of long rate

247

Market Predictions of Future Short Rates

Evidence on the Term Structure

Initial research (early 1980s) found little useful information in the yield curve for predicting future interest rates.

Recently, more discriminating tests show that the yield curve has a lot of information about very short-term and long-term rates, but says little about medium-term rates.

Case: Interpreting Yield Curves

The picture on the next slide illustrates several yield curves that we have observed for U.S. Treasury securities in recent years.

What do they tell us about the public’s expectations of future rates?

Case: Interpreting Yield Curves, 1980–2008

Case: Interpreting Yield Curves

The steep downward curve in 1981 suggested that short-term rates were expected to decline in the near future. This played-out, with rates dropping by 300 bps in 3 months.

The upward curve in 1985 suggested a rate increase in the near future.

Case: Interpreting Yield Curves

The slightly upward slopes in the remaining years can be explained by liquidity premiums. Short-term rates were stable, with longer-term rates including a liquidity premium (explaining the upward slope).

Mini-case: The Yield Curve as a Forecasting Tool

The yield curve does have information about future interest rates, and so it should also help forecast inflation and real output production. Rising (falling) rates are associated with

economic booms (recessions) [chapter 4]. Rates are composed of both real rates and

inflation expectations [chapter 3].

The Practicing Manager: Forecasting Interest Rates with the Term Structure

Pure Expectations Theory: Invest in 1-period bonds or in two-period bond

1 it 1 it1e 1 1 i2t 1 i2t 1

Solve for forward rate, iet+1

it1e

1 i2t 2

1 it 1 (4)

Numerical example: i1t = 5%, i2t = 5.5%

it1e

1 0.055 2

1 0.05 1 0.06 6%

Forecasting Interest Rates with the Term Structure

Compare 3-year bond versus 3 one-year bonds

Using iet+1 derived in (4), solve for iet+2

1 it 1 it 1e 1 it2

e 1 1 i3t 1 i3t 1 i3t 1

it2e

1 i3t 3

1 i2t 2 1

Forecasting Interest Rates with the Term Structure

Generalize to:

Liquidity Premium Theory: int - = same as pure expectations theory; replace int by int - in (5) to get adjusted forward-rate forecast

itne

1 in1t n 1

1 int n 1 (5)

itn

e 1 in1t n 1t n1

1 int nt n 1 (6)

Forecasting Interest Rates with the Term Structure

Numerical Example

2t = 0.25%, 1t=0, i1t=5%, i2t = 5.75%

Example: 1-year loan next year T-bond + 1%, 2t = .4%, i1t = 6%, i2t = 7%

Loan rate must be > 8.2%

it1e

1 0.0575 0.0025 2

1 0.05 1 0.06 6%

it1e

1 0.07 0.004 2

1 0.06 1 0.072 7.2%

Chapter Summary

Risk Structure of Interest Rates: We examine the key components of risk in debt: default, liquidity, and taxes.

Term Structure of Interest Rates: We examined the various shapes the yield curve can take, theories to explain this, and predictions of future interest rates based on the theories.

Part 3

Financial Markets

Chapter 6

The Money Markets

Chapter Preview

Topics include: The Money Markets Defined

The Purpose of Money Markets

Who Participates in Money Markets?

Money Market Instruments

Comparing Money Market Securities

The Money Markets Defined

Money Markets Defined

1. Money market securities are usually sold in large denominations ($1,000,000 or more) 交易的数额巨大 --------wholesale markets

2. They have low default risk 违约风险低

3. They mature (到期) in one year or less from their issue date (初始发行日)

The Money Markets Defined: Cost Advantages

Reserve requirements (Required Deposit Reserve) create additional expense for banks that money markets do not have

Regulations on the level of interest banks could offer depositors lead to a significant growth in money markets

The Purpose of Money Markets

Investors in Money Market: Provides a place for warehousing surplus funds for short periods of time (cash- opportunity cost)

Borrowers: money market provide low-cost source of temporary funds

Who Participates in the Money Markets?

Money Market Instruments

We will examine each of these in the following slides:

Treasury Bills

Federal Funds

Repurchase Agreements

Negotiable Certificates of Deposit

Money Market Instruments (cont.)

Commercial Paper

Banker’s Acceptance

Eurodollars

Money Market Instruments: Treasury Bills

T-bills have 28-day maturities through 12- month maturities.

Discounting: When an investor pays less for the security than it will be worth when it matures

Discount rate

Yield rate

Money Market Instruments: Treasury Bills Discounting Example

You pay $996.37 for a 28-day T-bill. It is worth $1,000 at maturity. What is its discount rate?

(1)n

xF

PFi discount

536

%665.428

536

000,1

73.996000,1

xi discount

Money Market Instruments: Treasury Bills Discounting Example

You pay $996.37 for a 28-day T-bill. It is worth $1,000 at maturity. What is its annualized yield?

iyt F P

P

365

n(1)

%76.428

536

37.996

73.996000,1

xi yt

Money Market Instruments: Treasury Bill Auctions

T-bills are auctioned (拍卖) by

competitive bids (竞价招标)

noncompetitive bids (非竞价招标)

Money Market Instruments: Treasury Bill Auctions Example

The Treasury auctioned $2.5 billion par value 91-day T-bills, the following bids were received:

Bidder Bid Amount Bid Price 1 $500 million $0.9940 2 $750 million $0.9901 3 $1.5 billion $0.9925 4 $500 million $0.9936 5 $600 million $0.9939

The Treasury also received in competitive bids. Who will receive T-bills, what quantity, and at what price?

Money Market Instruments: Treasury Bill Auctions Example

The Treasury accepts the following bids:

Bidder Bid Amount Bid Price

1 $500 million $0.9940

5 $500 million $0.9939

4 $650 million $0.9936

Money Market Instruments: Fed Funds

Short-term funds transferred (loaned or borrowed) between financial institutions, usually for a period of one day.

Used by banks to meet short-term needs to meet reserve requirements:

主要目的就是为准备金短缺的银行提供可立即拆入的资金.

Federal Funds Interest Rates

How to set ?

Fed sell securities: higher iFed buy securities: lower i

Money Market Instruments: Repurchase Agreements

These work similar to the market for fed funds, but nonbanks can participate.

A firm sells Treasury securities, but agrees to buy them back at a certain date (usually 3–14 days later) for a certain price.

Money Market Instruments: Repurchase Agreements

This set-up makes a repo agreements essentially a short-term collateralized( 抵押) loan.

This is one market the Fed may use to conduct its monetary policy, whereby the Fed purchases/sells Treasury securities in the repo market.

Money Market Instruments: Negotiable Certificates of Deposit

A bank-issued security that documents a deposit and specifies the interest rate and the maturity date

Denominations range from $100,000 to $10 million

Money Market Instruments: Commercial Paper

Unsecured promissory notes, issued by corporations, that mature in no more than 270 days.

The use of commercial paper increased significantly in the early 1980s because of the rising cost of bank loans.

Money Market Instruments: Commercial Paper

The next slide shows actual commercial paper rates and the prime rates 1990 through 2007.

Although the two track closely in terms of movements, notice that difference between the two remains roughly 200 basis points.

Money Market Instruments: Commercial Paper

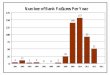

The next slide shows actual commercial paper volume by year from 1990 through 2006.

Notice that the volume has only begun to fall during the recent economic recession in the economy. Even so, the annual market is still quite large, at well over $1 trillion outstanding.

Money Market Instruments: Commercial Paper Volume

Money Market Instruments: Banker’s Acceptances

An order to pay a specified amount to the bearer on a given date if specified conditions have been met, usually delivery of promised goods.

These are often used when buyers / sellers of expensive goods live in different countries.

Money Market Instruments: Banker’s Acceptances Advantages

1. Exporter paid immediately

2. Exporter shielded from foreign exchange risk

3. Exporter does not have to assess the financial security of the importer

4. Importer’s bank guarantees payment

5. Crucial to international trade

Money Market Instruments: Banker’s Acceptances

As seen, banker’s acceptances avoid the need to establish the credit-worthiness of a customer living abroad.

There is also an active secondary market for banker’s acceptances until they mature. The terms of note indicate that the bearer, whoever that is, will be paid upon maturity.

Money Market Instruments: Eurodollars