Embed Size (px)

Citation preview

Financial Accounting

Course Text

Professional, Practical, Proven

www.AccountingTechniciansIreland.ie

iii

Table of Contents

FOREWORD ...............................................................................................................xi

SYLLABUS: FINANCIAL ACCOUNTING ................................................................xiii

CHAPTER 1: INTRODUCTION TO ACCOUNTING ....................................................1

1.1 INTRODUCTION .........................................................................................................................2

1.2 ACCOUNTING ............................................................................................................................2

1.3 ACCOUNTABILITY .....................................................................................................................3

1.4 TYPES OF BUSINESS ENTITY ..................................................................................................51.4.1 Sole trader ....................................................................................................................51.4.2 Partnership ....................................................................................................................61.4.3 Limited Company ..........................................................................................................71.4.4 Public and Private Limited Companies .........................................................................9

1.5 USERS OF ACCOUNTING INFORMATION .............................................................................10

1.6 USERS OF FINANCIAL STATEMENTS .................................................................................... 111.6.1 Investors ..................................................................................................................... 111.6.2 Lenders ....................................................................................................................... 111.6.3 Suppliers ..................................................................................................................... 111.6.4 Customers ...................................................................................................................121.6.5 Employees ..................................................................................................................121.6.6 Government ................................................................................................................121.6.7 Analysts ......................................................................................................................121.6.8 Public at large .............................................................................................................13

1.7 TYPES OF ACCOUNTING .......................................................................................................13

1.8 THE MAIN FINANCIAL ACCOUNTING STATEMENTS ............................................................15

Table of Contents

iv

Financial Accounting

1.9 ACCOUNTING TERMINOLOGY ...............................................................................................15

1.10 THE ACCOUNTANT’S ROLE AND FUNCTION IN AN ORGANISATION .................................17

1.11 AUDITING .................................................................................................................................18

1.12 ACCOUNTING ETHICS ............................................................................................................19

1.13 ACCOUNTING SCANDALS ......................................................................................................20

1.14 RESPONSES TO SCANDALS ..................................................................................................21

1.15 ETHICAL ISSUES AND THE ACCOUNTING TECHNICIAN .....................................................211.15.1 Codes of ethics ...........................................................................................................21

1.16 WHISTLE BLOWING ................................................................................................................22

CHAPTER 2: ACCOUNTING CONCEPTS & CONVENTIONS .................................25

2.1 INTRODUCTION .......................................................................................................................26

2.2 REGULATION AND STANDARDS ............................................................................................26

2.3 PROFESSIONAL SELF-REGULATION ....................................................................................26

2.4 COMPANIES ACTS ...................................................................................................................27

2.5 A TRUE AND FAIR VIEW ..........................................................................................................27

2.6 THE BASIC PRINCIPLES OF ACCOUNTING: CONVENTIONS AND CONCEPTS ................282.6.1 Accounting conventions ..............................................................................................282.6.2 Accounting concepts ...................................................................................................29

2.7 WHAT MAKES ACCOUNTING INFORMATION USEFUL? ......................................................31

2.8 A FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS ...........................................................................................................................32

2.9 RELEVANCE .............................................................................................................................33

2.10 RELIABILITY .............................................................................................................................33

2.11 COMPARABILITY .....................................................................................................................33

2.12 UNDERSTANDABILITY ............................................................................................................34

2.13 CONFLICTS IN THE QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION ................................................................................................34

2.14 ACCOUNTING POLICIES ........................................................................................................35

2.15 ESTIMATION TECHNIQUES ....................................................................................................35

2.16 MEASUREMENT BASES .........................................................................................................35

2.17 SELECTING ACCOUNTING POLICIES ...................................................................................36

2.18 REVIEWING AND CHANGING ACCOUNTING POLICIES ......................................................36

2.19 IAS 8 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING, ESTIMATES AND ERRORS .....................................................................................................36

Table of Contents

v

Financial Accounting

CHAPTER 3: DOUBLE ENTRY BOOK-KEEPING ....................................................39

3.1 DOUBLE ENTRY BOOK-KEEPING AND THE DUALITY CONCEPT .......................................40

3.2 THE ACCOUNTING EQUATION ...............................................................................................41

3.3 LEDGER ACCOUNTS, DEBITS AND CREDITS ......................................................................42

3.4 RECORDING CASH TRANSACTIONS ....................................................................................45

3.5 RECORDING CREDIT SALES AND PURCHASES TRANSACTIONS. ...................................46

3.6 RECORDING SALES AND PURCHASES RETURNS .............................................................47

3.7 ACCOUNTING FOR DISCOUNTS ...........................................................................................48

3.8 DOUBLE ENTRY CHECKLIST .................................................................................................49

3.9 BALANCING OFF LEDGER ACCOUNTS ................................................................................493.9.1 Opening and Closing balances in the ledger accounts ...............................................503.9.2 Statement of Profit and Loss Account, ledger accounts .............................................513.9.3 Capital account ...........................................................................................................52

3.10 EXAMPLE 8 CLOSING OFF GEORGE’S ACCOUNTS ...........................................................523.10.1 Next step - trial balance ..............................................................................................553.10.2 The limitations of a trial balance .................................................................................563.10.3 The process steps in producing a trial balance from a set of ledger accounts. ..........56

3.11 EXAMPLE 9 EXTRACTING A TRIAL BALANCE FROM GEORGE’S ACCOUNTS .................56

3.12 SELF-TEST QUESTIONS .........................................................................................................57

3.13 SOLUTIONS TO SELF-TEST QUESTIONS .............................................................................59

CHAPTER 4: VAT, PAYROLL, BOOKS OF PRIME ENTRY ....................................69

4.1 ELEMENTS OF VALUE ADDED TAX (VAT) .............................................................................704.1.1 The VAT system ..........................................................................................................704.1.2 Rates of VAT ...............................................................................................................704.1.3 Principles of VAT .........................................................................................................704.1.4 The Exception: Irrecoverable VAT ...............................................................................714.1.5 Calculation of VAT .......................................................................................................714.1.6 Accounting entries for VAT ..........................................................................................73

4.2 PAYROLL ..................................................................................................................................754.2.1 The accounting entries for Payroll ..............................................................................76

4.3 BOOKS OF PRIME ENTRY ......................................................................................................774.3.1 Sales day book ...........................................................................................................784.3.2 Sales returns day book ...............................................................................................794.3.3 Purchases day book ...................................................................................................804.3.4 Purchases returns day book .......................................................................................814.3.5 The cash book ............................................................................................................824.3.6 Cash Receipts Book ...................................................................................................844.3.7 The petty cash book ....................................................................................................854.3.8 The journal ..................................................................................................................86

Table of Contents

vi

Financial Accounting

4.4 SELF-TEST QUESTIONS .........................................................................................................86

4.5 SOLUTIONS TO SELF-TEST QUESTIONS .............................................................................88

CHAPTER 5: INTRODUCTION TO FINANCIAL STATEMENTS ..............................95

5.1 INTRODUCTION TO FINANCIAL STATEMENTS.....................................................................96

5.2 THE STATEMENT OF PROFIT AND LOSS ..............................................................................975.2.1 The trading income section. ........................................................................................975.2.2 The business expenditure section ..............................................................................995.2.3 Revenue income, capital income and revenue expenditure in the Statement of

Profit and Loss ............................................................................................................99

5.3 THE STATEMENT OF FINANCIAL POSITION .......................................................................1015.3.1 Assets and liabilities ..................................................................................................1025.3.2 Link between Statement of Financial Position and the Statement of

Profit and Loss ..........................................................................................................1035.3.3 Capital Expenditure in the Statement of Financial Position ......................................1035.3.4 Loans (Capital and Revenue elements) ....................................................................104

5.4 AN INTRODUCTION TO ACCOUNTING FOR OPENING AND CLOSING INVENTORY ......1055.4.1 Closing inventory ......................................................................................................1055.4.2 Opening inventory .....................................................................................................106

5.5 GEORGE’S TRIAL BALANCE (CONTINUED FROM SECTION 3.11, CHAPTER 3) ..............................................................108

5.6 SELF-TEST QUESTIONS .......................................................................................................112

5.7 SOLUTIONS TO SELF-TEST QUESTIONS ........................................................................... 114

CHAPTER 6: INVENTORY ......................................................................................123

6.1 ACCOUNTING FOR INVENTORY ..........................................................................................1246.1.1 The accruals concept ................................................................................................1246.1.2 Valuation of Inventory ...............................................................................................1256.1.3 The prudence concept ..............................................................................................1256.1.4 Cost ...........................................................................................................................1266.1.5 Net Realisable value (NRV) ......................................................................................126

6.2 METHODS OF VALUING INVENTORY – IAS 2 REQUIREMENTS .......................................1286.2.1 First in – First out (FIFO) ...........................................................................................1286.2.2 Average cost – AVCO ...............................................................................................129

6.3 THE IMPACT OF VALUATION METHODS ON THE STATEMENT OF PROFIT AND LOSS AND THE STATEMENT OF FINANCIAL POSITION...............................................................132

6.4 SELF-TEST QUESTIONS .......................................................................................................135

6.5 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................136

Table of Contents

vii

Financial Accounting

CHAPTER 7: ACCRUALS AND PREPAYMENTS ..................................................141

7.1 THE ACCRUALS CONCEPT ..................................................................................................142

7.2 ACCRUED EXPENDITURE ....................................................................................................143

7.3 PREPAID EXPENDITURE ......................................................................................................148

7.4 ACCRUED INCOME ...............................................................................................................153

7.5 PREPAID INCOME .................................................................................................................155

7.6 ACCRUALS AND PREPAYMENTS – FINANCIAL STATEMENTS EFFECT ..........................1577.6.1 The Statement of Profit and Loss .............................................................................1577.6.2 The Statement of Financial Position .........................................................................158

7.7 SELF-TEST QUESTIONS .......................................................................................................160

7.8 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................163

CHAPTER 8: IRRECOVERABLE DEBTS AND ALLOWANCE FOR RECEIVABLES ........................................................................................................173

8.1 ACCOUNTING CONCEPTS ...................................................................................................1748.1.1 Accruals concept .......................................................................................................1748.1.2 Prudence concept .....................................................................................................174

8.2 AGED RECEIVABLE ANALYSIS .............................................................................................1758.2.1 Advantages and Disadvantages of Selling on Credit ................................................1768.2.2 Credit limits ...............................................................................................................176

8.3 IRRECOVERABLE DEBTS .....................................................................................................1768.3.1 Irrecoverable debts recovered ..................................................................................178

8.4 ALLOWANCE FOR RECEIVABLES .......................................................................................1798.4.1 Specific allowance ....................................................................................................1808.4.2 General allowance ....................................................................................................1808.4.3 Accounting for Allowance for Receivables ................................................................180

8.5 IRRECOVERABLE DEBTS AND THE ALLOWANCE FOR RECEIVABLES – TRIAL BALANCE ADJUSTMENTS. .....................................................................................186

8.6 SELF-TEST QUESTIONS .......................................................................................................189

8.7 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................190

CHAPTER 9: NON-CURRENT ASSETS AND DEPRECIATION ............................199

9.1 CURRENT AND NON-CURRENT ASSETS ............................................................................200

9.2 CAPITAL AND REVENUE EXPENDITURE ............................................................................2019.2.1 Capital expenditure ...................................................................................................2019.2.2 Revenue expenditure ................................................................................................202

9.3 NON-CURRENT ASSET REGISTERS ...................................................................................202

9.4 ACCOUNTING FOR NON-CURRENT ASSETS .....................................................................203

9.5 DEPRECIATION ......................................................................................................................204

Table of Contents

viii

Financial Accounting

9.6 ESTIMATING DEPRECIATION ...............................................................................................2059.6.1 Straight line depreciation ..........................................................................................2069.6.2 Reducing balance depreciation .................................................................................206

9.7 ACCOUNTING FOR DEPRECIATION ....................................................................................209

9.8 DISPOSAL OF NON-CURRENT ASSETS ..............................................................................212

9.9 DISPOSAL THROUGH A PART-EXCHANGE .........................................................................216

9.10 NON-CURRENT ASSETS AND THE FINANCIAL STATEMENTS ..........................................219

9.11 SOME ADDITIONAL INFORMATION ON DEPRECIATION OF NON-CURRENT ASSETS ...220

9.12 SELF-TEST QUESTIONS .......................................................................................................221

9.13 SOLUTIONS TO SELF- TEST QUESTIONS ..........................................................................223

CHAPTER 10: BANK RECONCILIATION STATEMENTS ......................................235

10.1 NATURE AND PURPOSE OF BANK RECONCILIATION STATEMENTS ..............................236

10.2 METHODOLOGY FOR PREPARING BANK RECONCILIATION STATEMENTS ...................237

10.3 DETAILED DIFFERENCES BETWEEN THE BANK ACCOUNT AND THE BANK STATEMENT ........................................................................................................239

10.4 PREPARATION OF A BANK RECONCILIATION STATEMENT ..............................................24310.4.1 The Proforma for a bank reconciliation .....................................................................24410.4.2 The Proforma for a bank reconciliation with a Bank Overdraft .................................244

10.5 EXAMPLES OF BANK RECONCILIATIONS, INCLUDING AN OVERDRAFT. .......................245

10.6 BANK DEBIT AND CREDIT BALANCES IN THE STATEMENT OF FINANCIAL POSITION .252

10.7 SELF-TEST QUESTIONS .......................................................................................................252

10.8 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................253

CHAPTER 11: PREPARATION OF FINANCIAL STATEMENTS ............................263

11.1 FROM TRIAL BALANCE TO FINANCIAL STATEMENTS .......................................................264

11.2 THE STATEMENT OF PROFIT AND LOSS ............................................................................265

11.3 THE STATEMENT OF FINANCIAL POSITION .......................................................................266

11.4 SOLE TRADER ACCOUNTS ..................................................................................................267

11.5 EXAMPLE 1: GINA O’HALLORAN ..........................................................................................268

11.6 EXAMPLE 2: RORY JAMESON’S FINANCIAL STATEMENTS ..............................................272

11.7 EXAMPLE 3: T. HIGGINS (A MORE COMPLICATED EXAMPLE) .........................................278

CHAPTER 12: ACCOUNTING FOR “NOT-FOR-PROFIT” ORGANISATIONS ......291

12.1 “NOT-FOR-PROFIT” ORGANISATIONS .................................................................................292

12.2 THE RECEIPTS AND PAYMENTS ACCOUNT .......................................................................292

Table of Contents

ix

Financial Accounting

12.3 THE INCOME AND EXPENDITURE ACCOUNT ....................................................................293

12.4 ACCUMULATED FUND STATEMENT ....................................................................................295

12.5 ANNUAL SUBSCRIPTIONS ...................................................................................................29612.5.1 Entrance fees ............................................................................................................29812.5.2 Life membership subscriptions/payments .................................................................298

12.6 DIFFERENCES BETWEEN THE RECEIPTS AND PAYMENTS ACCOUNT AND THE INCOME AND EXPENDITURE ACCOUNT. ...........................................................................................301

12.7 SELF-TEST QUESTIONS .......................................................................................................302

12.8 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................304

CHAPTER 13: CONTROL ACCOUNTS & INTRODUCTION TO CONTROL ACCOUNT RECONCILIATIONS .............................................................................313

13.1 NATURE AND PURPOSE OF CONTROL ACCOUNTS .........................................................31413.1.1 Receivables ledger control account ..........................................................................31413.1.2 Payables ledger control account ...............................................................................31413.1.3 The purpose of control accounts ...............................................................................314

13.2 CONTROL ACCOUNTS AND DOUBLE ENTRY .....................................................................315

13.3 RECEIVABLES/SALES LEDGER CONTROL ACCOUNTS ....................................................31713.3.1 Explaining the Proforma Receivables Control Account .............................................31813.3.2 Applied Example of Receivables Control Account ....................................................320

13.4 PAYABLES/PURCHASES LEDGER CONTROL ACCOUNTS ................................................32113.4.1 Explaining the Proforma Payables Control Account .................................................32213.4.2 Applied Example of Payables Control Account .........................................................32313.4.3 Supplier statements ..................................................................................................324

13.5 INTRODUCTION TO CONTROL ACCOUNT RECONCILIATIONS ........................................324

13.6 CONTROL ACCOUNTS – THE STATEMENT OF FINANCIAL POSITION .............................327

13.7 SELF-TEST QUESTIONS .......................................................................................................328

13.8 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................330

CHAPTER 14: INCOMPLETE RECORDS ..............................................................337

14.1 INCOMPLETE RECORDS ......................................................................................................338

14.2 NET ASSETS APPROACH .....................................................................................................338

14.3 THE BALANCING FIGURE APPROACH ................................................................................34214.3.1 Deriving Sales – the missing figure ...........................................................................34414.3.2 Deriving Purchases – the missing figure ...................................................................34514.3.3 Deriving expenses – missing figures ........................................................................34714.3.4 Deriving Opening Capital ..........................................................................................352

14.4 MARGIN AND MARK-UP ........................................................................................................35314.4.1 Gross Profit Margin ...................................................................................................35314.4.2 Gross Profit Mark-up .................................................................................................354

Table of Contents

x

Financial Accounting

14.4.3 When Mark-up is known, what is the Margin? ..........................................................35514.4.4 When Margin is known, what is the Mark-Up? ..........................................................356

14.5 STEPS TO FOLLOW TO PREPARE FINANCIAL STATEMENTS FROM INCOMPLETE RECORDS. .............................................................................................................................359

14.6 SELF-TEST QUESTIONS .......................................................................................................362

14.7 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................365

CHAPTER 15: CORRECTION OF ERRORS ..........................................................379

15.1 IDENTIFICATION OF ERRORS ..............................................................................................38015.1.1 Types of errors and their impact on the Trial Balance ...............................................38015.1.2 The effect of errors on the Statement of Profit. .........................................................381

15.2 ERRORS WHICH DO NOT AFFECT THE BALANCING OF THE TRIAL BALANCE .............38115.2.1 Error of omission .......................................................................................................38115.2.2 Error of commission ..................................................................................................38615.2.3 Error of principle ........................................................................................................38815.2.4 Compensating errors ................................................................................................39115.2.5 Error of original entry ................................................................................................39515.2.6 Reversal of entries error ...........................................................................................398

15.3 CONTROL ACCOUNT RECONCILIATION AND CORRECTION OF ERRORS .....................401

15.4 SELF-TEST QUESTIONS .......................................................................................................405

15.5 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................407

CHAPTER 16: SUSPENSE ACCOUNT ..................................................................419

16.1 SUSPENSE ACCOUNT ..........................................................................................................42016.1.1 Method employed to correct errors ...........................................................................422

16.2 IDENTIFYING ERRORS CAUSING THE CREATION OF THE SUSPENSE ACCOUNT .......42316.2.1 Same sided entry error .............................................................................................42316.2.2 Single sided entry error .............................................................................................42516.2.3 Transposition error ....................................................................................................426

16.3 EXAMPLE 5: CONTROL ACCOUNT RECONCILIATION, WITH A SUSPENSE ACCOUNT ..427

16.4 EXAMPLE 6: JOHN O’CONNOR’S TRIAL BALANCE ............................................................430

16.5 ADJUSTMENT TO PROFIT ....................................................................................................437

16.6 SELF-TEST QUESTIONS .......................................................................................................438

16.7 SOLUTIONS TO SELF-TEST QUESTIONS ...........................................................................439

INDEX.......................................................................................................................451

xi

FOREWORD

Foreword

This text has been developed by Accounting Technicians Ireland for use by students participating in our programme of study and preparing for our examinations. While every effort is made to ensure that the information outlined in this text is accurate, Accounting Technicians Ireland and

the Author cannot accept the responsibility for lack of, or perceived lack of, information contained herein.

The text is intended to be a sufficiently detailed synopsis of the current syllabus material (and knowledge level required thereof) in relation to this module.

Students should take particular note of the weighting attaching to this module, as clearly outlined in the syllabus. It is on the basis of this weighting that students should prepare their own timetable for study.

On the completion of each chapter, students should refer to the relevant questions dealing with that chapter. Ideally, students should not continue with subsequent chapters until they have completed the questions attaching to the chapter currently under review.

The solutions to the questions are provided under separate cover and although they are the suggested solutions, tutors and students should recognise and appreciate that there might very well be different approaches which would, under examination conditions, be perfectly acceptable.

We recommended that, in order to get the full benefit of the question and answer concept, students should not refer to the solution until they have made a full and genuine attempt at each question.

We also recommend that when students have attained an understanding of each chapter studied, in addition to the questions provided, they should access the Accounting Technicians Ireland website (www.accountingtechniciansireland.ie) for past papers and “sit them under exam conditions”. This will allow students to improve their time management skills and their approach to each type of question.

xii

Referencing

For the purposes of consistency, all references to “he” or “she” will be referred to as “he” in this publication. No other implication whatsoever is implied from this policy.

For the purposes of presentation, all references to “euro” or “sterling” will be referred to as “euro” in this publication. No other implication whatsoever is implied from this policy.

Copyright

This text is issued by Accounting Technicians Ireland to students taking its examinations. It may not be used in whole, or in part, for any course of study and/or examination of any other body whatsoever without prior permission in writing from Accounting Technicians Ireland. This publication, or any part thereof, may not be made available in any library, and it may not be reproduced, in whole or in part, stored in a retrieval system or transmitted in any form or by any means – photocopying, electronic, electrostatic, magnetic, pdf, mechanical, recording or otherwise, without prior permission in writing from Accounting Technicians Ireland, 47-49 Pearse Street, Dublin 2.

Acknowledgement

The 2013-2014 edition was edited and updated by Dr. Antoinette Flynn. Antoinette is a lecturer in Accounting and Finance with the Department of Accounting and Finance, University of Limerick. Her profile is available at www.ul.ie.

xiii

SYLLABUS: FINANCIAL ACCOUNTING

SYLLABUS

Financial Accounting

Mandatory Module

Syllabus : Mandatory Module

xiv

Financial Accounting

Financial Accounting

Subject Status Mandatory

Terminal Exam 100%

Module Pass Mark 50%

Learning Modes Direct Lectures, Workshops, Tutorials, Self Directed Learning

Pre-requisite Programme Entry Requirements

Key Learning Outcome

The key objective of this module is to provide learners with knowledge of accounting concepts and principles of accounting and the technical competency in the area of double entry accounting and accounts preparation for various types of business.

Key Syllabus Elements and Weightings

1. Accounting Fundamentals ......................................................................................................15%

2. Double-Entry Bookkeeping and Accounting Systems ............................................................50%

3. Accounts Preparation .............................................................................................................35%

Syllabus : Mandatory Module

xv

Financial Accounting

Learning Outcomes linked to Syllabus Elements

Accounting Fundamentals

On completion of this aspect of the module, learners will have acquired the following knowledge, competencies and know-how:

(a) An appreciation of and an ability to describe the function of and differences between financial accounting and management accounting

(b) An understanding of the different types of business entity and the accountant’s role in an organisation

(c) An ability to identify the various user groups which need accounting information and an appreciation of the characteristics of such information required to meet the objectives of each user group

(a) An understanding of accounting terminology, basic accounting concepts and principles

Double-Entry Bookkeeping and Accounting Systems

On completion of this aspect of the module, participants will have acquired the following knowledge, competencies and know-how:-

(a) A knowledge of the form and content of accounting records and the ability to record financial transactions in the books of original entry

(b) The ability to demonstrate an understanding of and use the double entry system of bookkeeping to prepare a trial balance

(c) An understanding of the distinction between capital and revenue expenditure

(d) An ability to understand, explain and use control accounts, bank reconciliation statements and suspense accounts as part of the internal control of an organisation

Accounts Preparation

On completion of this aspect of the module, learners will have acquired the following knowledge, competencies and know-how:

(a) An appreciation and understanding of the key features of financial statements;

(b) An ability to prepare financial statements for sole traders and ‘not for profit’ organisations.

Syllabus : Mandatory Module

xvi

Financial Accounting

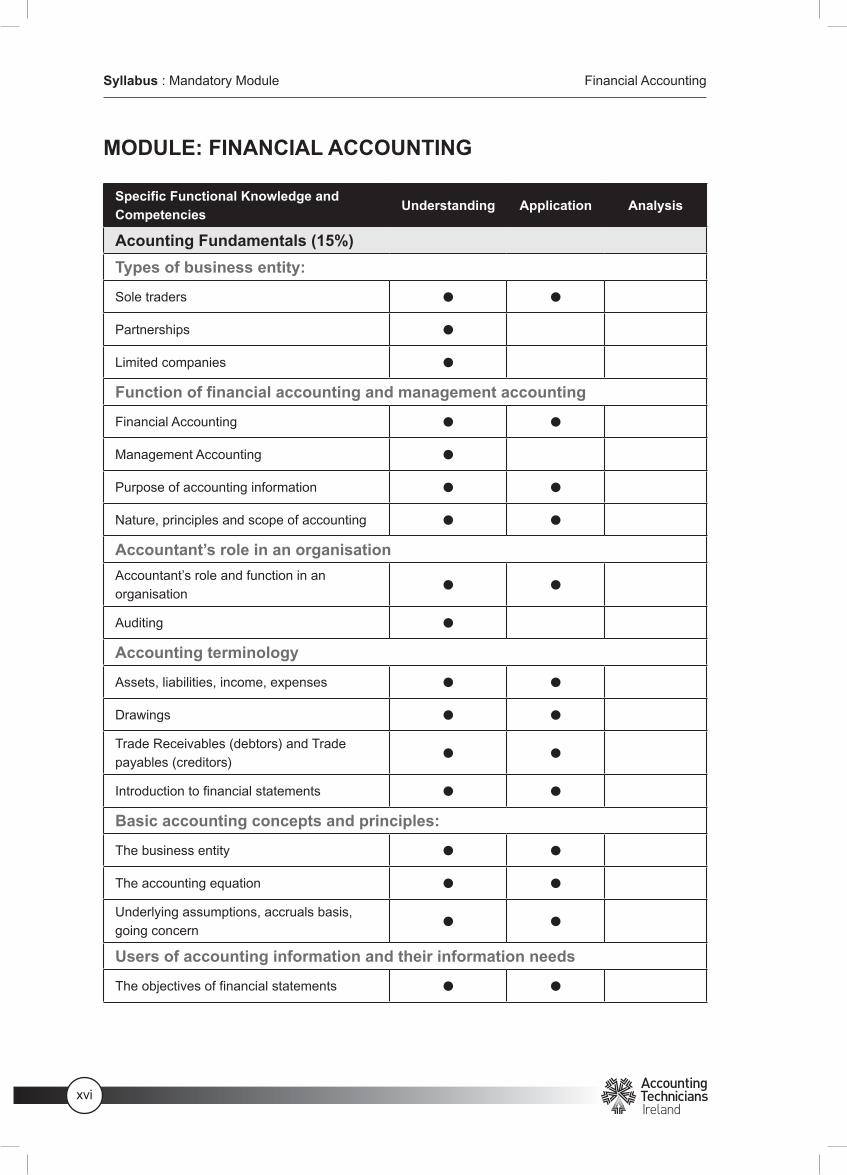

MODULE: FINANCIAL ACCOUNTING

Specific Functional Knowledge and Competencies

Understanding Application Analysis

Acounting Fundamentals (15%)

Types of business entity:

Sole traders l l

Partnerships l

Limited companies l

Function of financial accounting and management accounting

Financial Accounting l l

Management Accounting l

Purpose of accounting information l l

Nature, principles and scope of accounting l l

Accountant’s role in an organisation

Accountant’s role and function in an organisation

l l

Auditing l

Accounting terminology

Assets, liabilities, income, expenses l l

Drawings l l

Trade Receivables (debtors) and Trade payables (creditors)

l l

Introduction to financial statements l l

Basic accounting concepts and principles:

The business entity l l

The accounting equation l l

Underlying assumptions, accruals basis, going concern

l l

Users of accounting information and their information needs

The objectives of financial statements l l

Syllabus : Mandatory Module

xvii

Financial Accounting

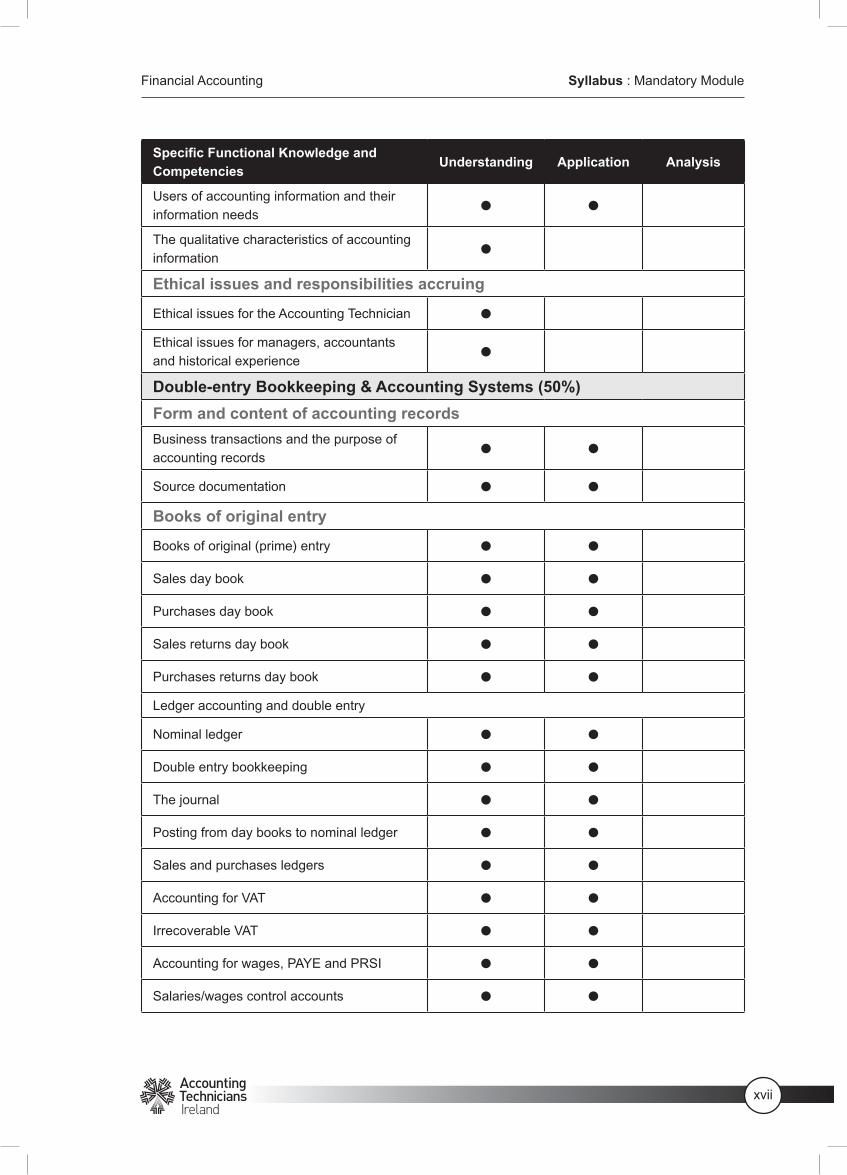

Specific Functional Knowledge and Competencies

Understanding Application Analysis

Users of accounting information and their information needs

l l

The qualitative characteristics of accounting information

l

Ethical issues and responsibilities accruing

Ethical issues for the Accounting Technician l

Ethical issues for managers, accountants and historical experience

l

Double-entry Bookkeeping & Accounting Systems (50%)

Form and content of accounting records

Business transactions and the purpose of accounting records

l l

Source documentation l l

Books of original entry

Books of original (prime) entry l l

Sales day book l l

Purchases day book l l

Sales returns day book l l

Purchases returns day book l l

Ledger accounting and double entry

Nominal ledger l l

Double entry bookkeeping l l

The journal l l

Posting from day books to nominal ledger l l

Sales and purchases ledgers l l

Accounting for VAT l l

Irrecoverable VAT l l

Accounting for wages, PAYE and PRSI l l

Salaries/wages control accounts l l

Syllabus : Mandatory Module

xviii

Financial Accounting

Specific Functional Knowledge and Competencies

Understanding Application Analysis

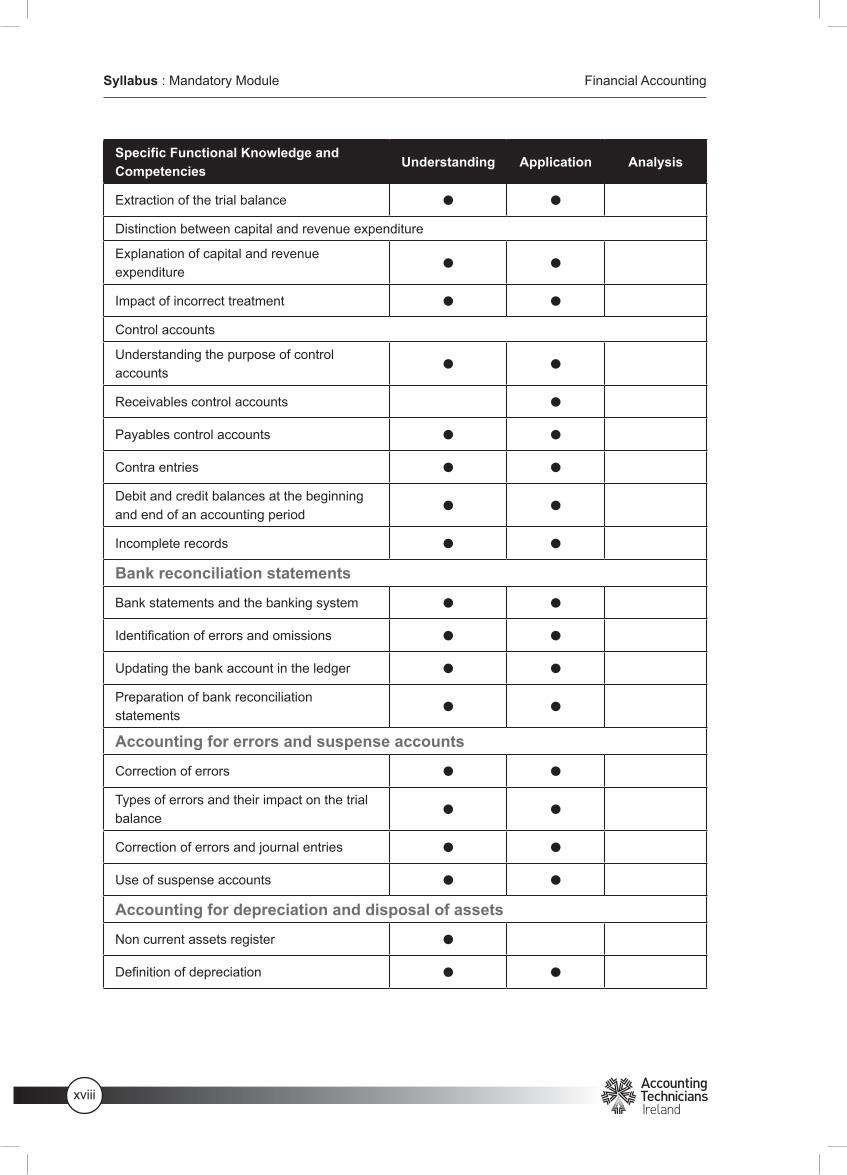

Extraction of the trial balance l l

Distinction between capital and revenue expenditure

Explanation of capital and revenue expenditure

l l

Impact of incorrect treatment l l

Control accounts

Understanding the purpose of control accounts

l l

Receivables control accounts l

Payables control accounts l l

Contra entries l l

Debit and credit balances at the beginning and end of an accounting period

l l

Incomplete records l l

Bank reconciliation statements

Bank statements and the banking system l l

Identification of errors and omissions l l

Updating the bank account in the ledger l l

Preparation of bank reconciliation statements

l l

Accounting for errors and suspense accounts

Correction of errors l l

Types of errors and their impact on the trial balance

l l

Correction of errors and journal entries l l

Use of suspense accounts l l

Accounting for depreciation and disposal of assets

Non current assets register l

Definition of depreciation l l

Syllabus : Mandatory Module

xix

Financial Accounting

Specific Functional Knowledge and Competencies

Understanding Application Analysis

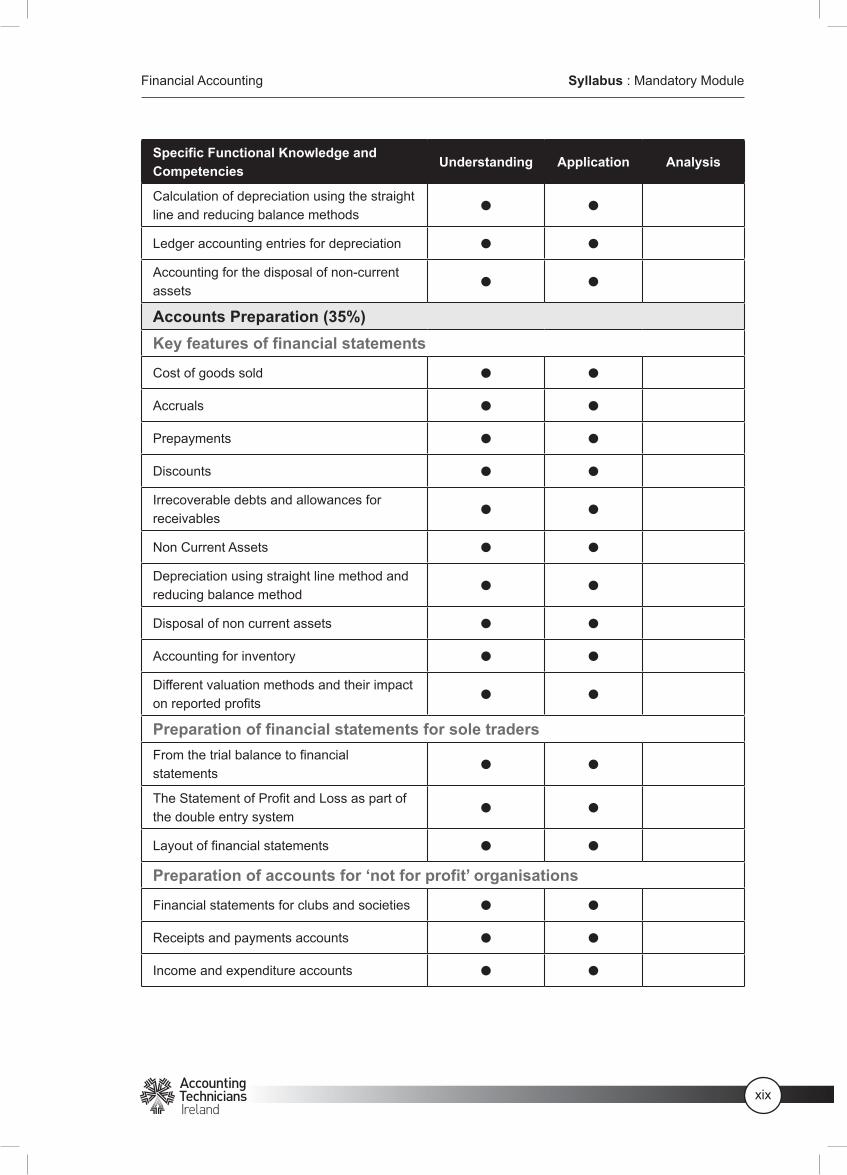

Calculation of depreciation using the straight line and reducing balance methods

l l

Ledger accounting entries for depreciation l l

Accounting for the disposal of non-current assets

l l

Accounts Preparation (35%)

Key features of financial statements

Cost of goods sold l l

Accruals l l

Prepayments l l

Discounts l l

Irrecoverable debts and allowances for receivables

l l

Non Current Assets l l

Depreciation using straight line method and reducing balance method

l l

Disposal of non current assets l l

Accounting for inventory l l

Different valuation methods and their impact on reported profits

l l

Preparation of financial statements for sole traders

From the trial balance to financial statements

l l

The Statement of Profit and Loss as part of the double entry system

l l

Layout of financial statements l l

Preparation of accounts for ‘not for profit’ organisations

Financial statements for clubs and societies l l

Receipts and payments accounts l l

Income and expenditure accounts l l

Syllabus : Mandatory Module

xx

Financial Accounting

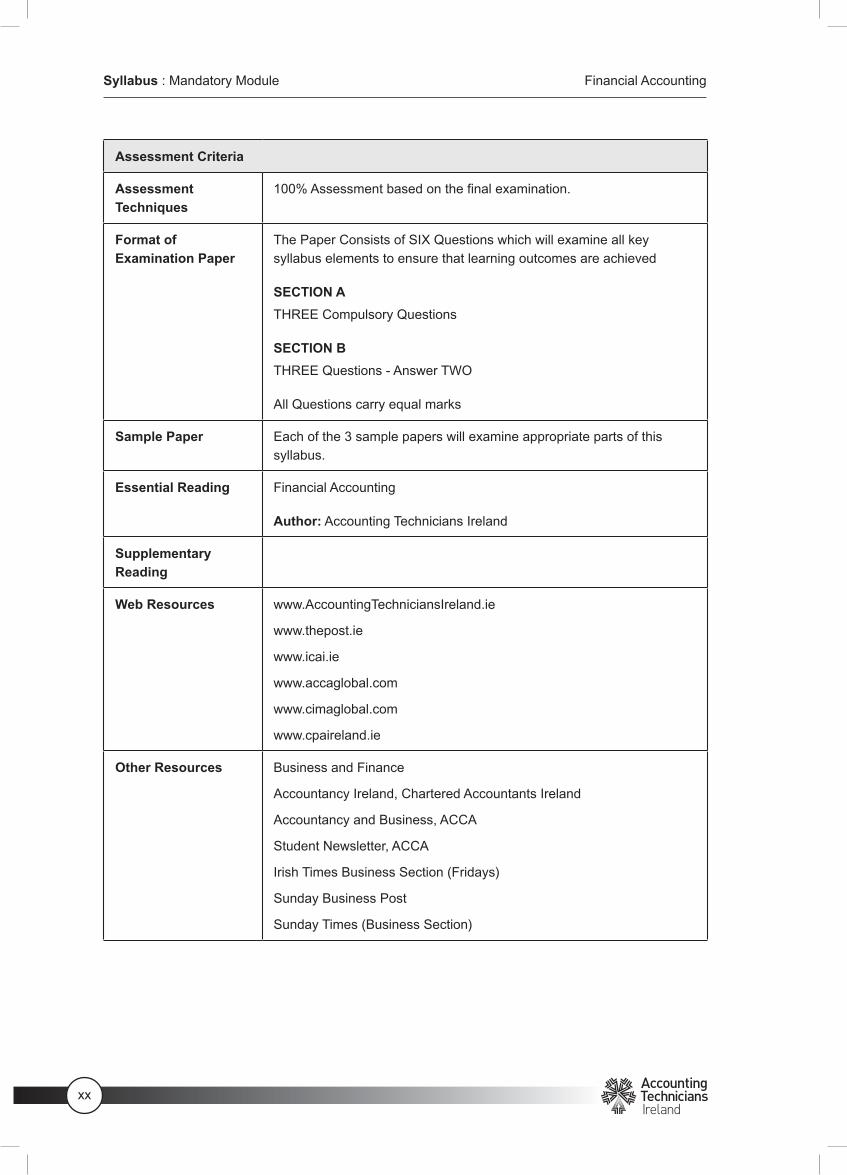

Assessment Criteria

Assessment Techniques

100% Assessment based on the final examination.

Format of Examination Paper

The Paper Consists of SIX Questions which will examine all key syllabus elements to ensure that learning outcomes are achieved

SECTION A

THREE Compulsory Questions

SECTION B

THREE Questions - Answer TWO

All Questions carry equal marks

Sample Paper Each of the 3 sample papers will examine appropriate parts of this syllabus.

Essential Reading Financial Accounting

Author: Accounting Technicians Ireland

Supplementary Reading

Web Resources www.AccountingTechniciansIreland.ie

www.thepost.ie

www.icai.ie

www.accaglobal.com

www.cimaglobal.com

www.cpaireland.ie

Other Resources Business and Finance

Accountancy Ireland, Chartered Accountants Ireland

Accountancy and Business, ACCA

Student Newsletter, ACCA

Irish Times Business Section (Fridays)

Sunday Business Post

Sunday Times (Business Section)

1

CHAPTER 1: INTRODUCTION TO ACCOUNTING

CHAPTER 1

Introduction to Accounting

LEARNING OUTCOMES

On completion of this chapter students should be able to:

1. Understand and define accounting

2. Explain the different types of business entity

3. List the users of the financial statements and their information needs

4. Differentiate between Financial and Management accounting

5. Understand Accounting terminology

6. Explain the accountants role in an organisation

7. Explain Auditing

8. Understand Professional Ethics and the accountant

REVISION RESOURCES

EXAM QUESTIONS: Sample and Past papers are available from the website of Accounting Technicians Ireland and are essential aids when studying Advanced Financial Accounting topics.

Chapter 1 : Introduction to Accounting

2

Financial Accounting

The objective of this module is to provide students with the knowledge to enable them to prepare a set of financial statements, for a sole trader. The purpose of financial statements is to provide information about the reporting entity’s performance and financial position in a useful manner for a wide range of users. It is important to note here that international professional accounting regulations are followed in this module.

The Financial Accounting syllabus (and this manual) has been written and will be examined under International Accounting Standards professional regulations. This is an important point to note in advance of commencing this module. The table below charts the terminology changes from UK/Irish GAAP to International Accounting Standards.

Terminology changes from UK/Irish GAAP to International Accounting Standards

UK/Irish GAAP International Accounting Standards

Trading, Profit and Loss A/C Statement of Profit and Loss

Balance Sheet Statement of Financial Position

Fixed Assets Non-Current Assets

Stock Inventory

Debtors Receivables

Provision for bad debts Allowance for Receivables

Creditors Payables

1.1 INTRODUCTION

It is not easy to provide a concise definition of accounting since the word has a broad application within business. Accountancy or accounting is the art of communicating financial information about a business entity to users such as the owners of the business and the government. The information is generally in the form of financial statements that show in money terms the economic resources under the control of management. This chapter explores the concept of accounting, the different types of business entities and the users of these financial statements, in addition to their information needs. The key accounting concepts and their importance in preparing financial statements will also be defined.

1.2 ACCOUNTING

Accounting can be defined as the process of identifying, measuring and communicating economic information to permit informed judgments and decisions by users of the information.

This definition suggests that accounting is about providing information to others. A key concept is that accounting information is economic information – it relates to the financial or economic activities of the business or organisation. This definition implies that accounting information can be identified and measured. This is done by way of a set of accounts, based on a system of accounting known as double-

Chapter 1 : Introduction to Accounting

3

Financial Accounting

entry bookkeeping. The accounting system identifies and records accounting transactions (economic activity).

However, the measurement of accounting information is not a straight forward process. It involves making judgments about the value of assets owned by a business or liabilities owed by a business. It is also about accurately measuring how much profit or loss has been made by a business in a particular period. Later in this module, it will become clear that the measurement of accounting information often requires subjective judgment to come to a conclusion.

The definition identifies the need for accounting information to be communicated. The way in which this communication is achieved may vary. There are several forms of accounting communication (e.g. annual reports and accounts, management accounting reports), each of which serve a slightly different purpose. The choice of communication channel is about understanding who are the users of the information and what are their information needs.

Accounting information is communicated using financial statements. The dual purposes of financial statements are as follow:

1. To report on the financial position of an entity (e.g. a business, an organisation).

2. To show how the entity has performed (financially) over a particular period of time (an accounting period).

The most common measurement of financial performance is profit (broadly, income after paying various costs). Financial statements are explored in more detail later in the chapter.

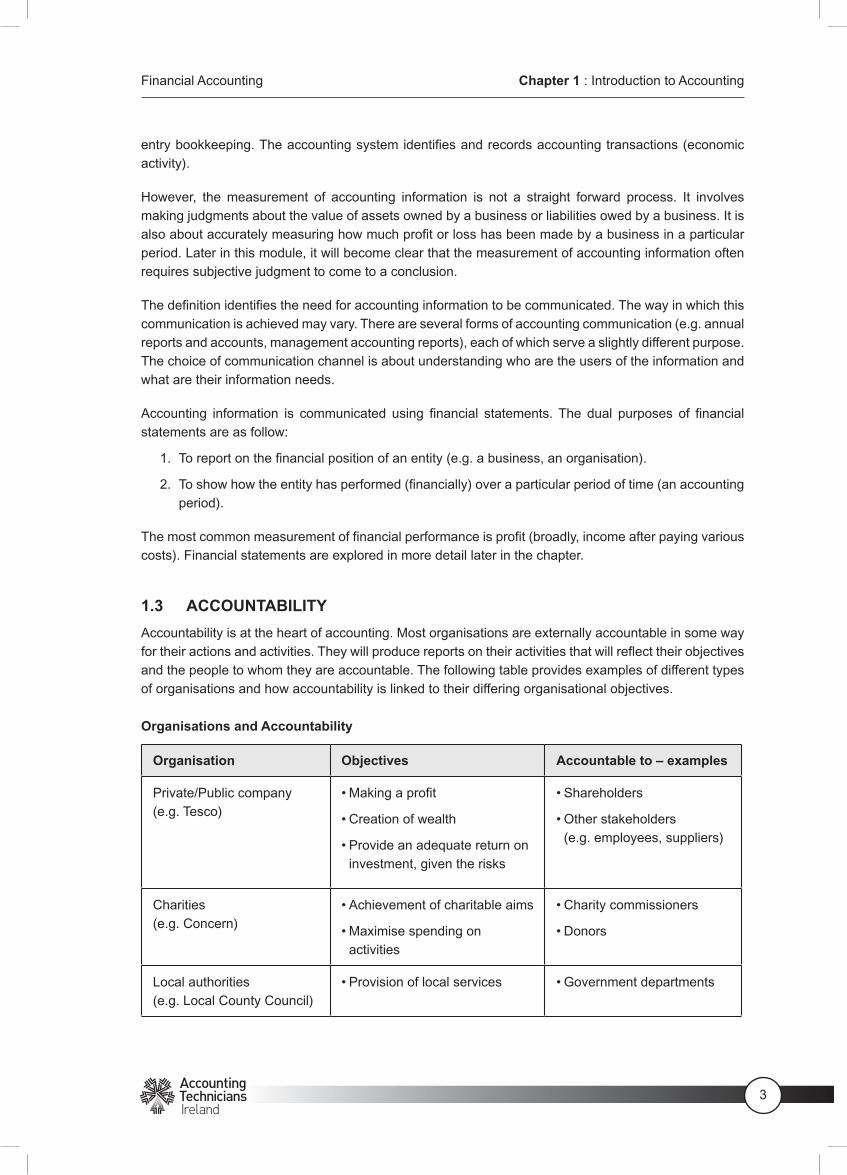

1.3 ACCOUNTABILITY

Accountability is at the heart of accounting. Most organisations are externally accountable in some way for their actions and activities. They will produce reports on their activities that will reflect their objectives and the people to whom they are accountable. The following table provides examples of different types of organisations and how accountability is linked to their differing organisational objectives.

Organisations and Accountability

Organisation Objectives Accountable to – examples

Private/Public company (e.g. Tesco)

• Making a profit

• Creation of wealth

• Provide an adequate return on investment, given the risks

• Shareholders

• Other stakeholders (e.g. employees, suppliers)

Charities (e.g. Concern)

• Achievement of charitable aims

• Maximise spending on activities

• Charity commissioners

• Donors

Local authorities (e.g. Local County Council)

• Provision of local services • Government departments

Chapter 1 : Introduction to Accounting

4

Financial Accounting

All of the above organisations have a significant role to play in society and have multiple stakeholders to whom they are accountable. All require systems of financial management to enable them to produce accounting information.

How does accounting information help businesses be accountable? As previously outlined in the introductory definition, accounting is essentially an information process that serves several purposes and outcomes:

1. Provides a record of assets owned, amounts owed to others and monies invested.

2. Provides reports showing the financial position of an organisation and the profitability of its operations.

3. Helps management actually manage the organisation.

4. Enables potential investors to evaluate an organisation and make decisions.

There are five overall accounting information objectives that drive this process, described below.

1. Collection: Collection in money-terms, of information relating to transactions that have resulted from business operations.

2. Recording and classifying: Recording and classifying data into a permanent and logical form. This is usually referred to as book-keeping.

3. Summarising: Summarising data to produce statements and reports that will be useful to the various users of accounting information – both external and internal.

4. Interpreting and communicating: Interpreting and communicating the performance of the business to the management and its owners.

5. Forecasting and planning: Forecasting and planning for the future operation of the business by providing management with evaluations of the viability of proposed operations. The key forecasting and planning tool is the budget.

The management process by which accounting information is collected, reported, interpreted and acted on, is called Financial Management. In preparing accounting information, care should be taken to ensure that the information presents an accurate and true reflection of the business performance and position. To impose some order on what is a subjective task, accounting has adopted certain conventions which should be applied in preparing accounts (all of which will be explored later in this module).

For financial accounting, the regulation or control of what kind of information is prepared and presented goes much further. Ireland, the UK and international companies are required to comply with a wide range of Accounting Standards that define the way in which business transactions are disclosed and reported. Accounting standards also address the calculations around transactions, which we explore in greater detail in Chapter 5. These are applied by businesses through their Accounting Policies, which will be addressed in chapter 2. The next section examines the different types of business entity and outlines their respective advantages and disadvantages.

Chapter 1 : Introduction to Accounting

5

Financial Accounting

1.4 TYPES OF BUSINESS ENTITY

A business can be organised in one of several ways:

• Sole Trader – a business owned and operated by one person.

• Partnership – a business owned and operated by two or more people.

• Company – a business owned by its shareholders and operated by its directors, who are not necessarily the same people.

1.4.1 Sole trader

The simplest form of business is the sole trader; a sole trader is a business that is owned by one person. It may have one or more employees. It offers the least personal protection. Under law, a sole trader and the business are the same legal entity. Essentially, the sole trader and his business are one and the same thing – the sole trader is personally liable if his business is sued or owes any money, i.e. his liability is unlimited. Becoming a sole trader can be risky as the entrepreneur will be liable to repay the business’s debt from his personal wealth if necessary. Profits from the business are considered income and are taxed accordingly; essentially, the sole trader is treated as self-employed for tax purposes.

The main advantages of setting up as a sole trader are:

• Total control of the business by the owner.

• Cheap and easy to start-up - there are less forms to fill in and to start trading, the sole trader does not need to employ any specialist services, other than setting up a bank account and informing the tax authorities.

• Keep all the profit – as the owner, all the profit belongs to the sole trader.

• Business affairs are private – competitors cannot see what the business is earning, so will know less about how the business works and how it succeeds.

• No obligation to produce a set of published financial statements.

The legal requirements of a sole trader are to:

• Keep proper business accounts and records for the Revenue Commissioners (who will collect the tax on profits) and if necessary VAT accounts.

• Comply with legal requirements that concern the protection of the customer (e.g. Sale of Goods and Supply of Services Act).

The main disadvantages of being a sole trader are:

• Unlimited Liability – A sole trader is liable for any debts that the business incurs. This means that any money that the owner has put into the business could be lost, but most importantly, if the business continues to incur further costs then the owner has to pay these as well. In some cases they may have to sell some of their own possessions to pay suppliers. Such a risk often puts potential sole traders off setting up businesses, and also makes them consider the other forms of business structure.

Chapter 1 : Introduction to Accounting

6

Financial Accounting

• As a result of the sole trader and the business being the same legal form, the sole trader is taxed based on income tax not corporation tax. Corporation tax rates are more favourable than income tax rates.

• It can be difficult to raise finance. Because they are small, banks may not lend large sums of money to sole traders who may be unable to avail of other forms of long-term finance unless they change their ownership status.

• It can be difficult to enjoy economies of scale, i.e. lower costs per unit due to higher levels of production. A sole trader, for instance, may not be able to buy in bulk and enjoy the same discounts as larger businesses.

• There is a problem of continuity if the sole trader retires or dies – what happens to the business?

The reasons for being a sole trader are often a balance between business and personal costs and benefits.

1.4.2 Partnership

A partnership is a business where there are two or more owners of the enterprise. Most partnerships are between two and twenty members though there are examples, like accountancy firms and solicitors firms, where there are more partners.

A partnership is normally set up using a Deed of Partnership. This contains:

• Amount of capital each partner should provide (i.e. starting capital).

• How profits and losses should be divided.

• How many votes each partner has (usually based on the proportion of capital invested).

• Rules on how to take on new partners.

• How the partnership is brought to an end, or how a partner leaves.

In the absence of this deed of partnership, the Partnership Act of 1890 (amended in 1907) will apply to avoid any disputes in the future. The Limited Partnership Act of 1907 encompasses the UK, Scotland and Northern Ireland. It provides a legal framework for Republic of Ireland partnerships. The act states that:

• No interest is paid on capital of the partners.

• No remuneration is paid to partners for acting in the business.

• Profits and losses are to be shared equally between partners.

• Interest at the rate of 5% per annum is paid on loans made by the partners to the partnership in excess of their agreed capitals.

The main advantages of a sole trader becoming a partnership are:

• It spreads the risk across more people, so if the business gets into difficulty then there are more people to share the burden of debt.

• Partners may bring money and resources to the business (e.g. better premises to work from).

• A new partner may bring other skills and ideas to the business, complementing the work already done by the original partner.

Chapter 1 : Introduction to Accounting

7

Financial Accounting

• Partnership increases credibility with potential customers and suppliers – who may see dealing with the business as less risky than trading with just a sole trader.

For example, a builder, working originally as a sole trader, may team up with an architect or carpenter to form a partnership. Either would bring added expertise, but also might bring added capital and/or contacts. Of course the builder could team up with another builder as well – sharing the risk, and potentially the workload.

The main disadvantages of becoming a partnership are:

• Having to share the profits.

• Less control of the business for the individual.

• Disputes over workload.

• Problems if partners disagree over the direction of the business.

The next step for a partnership is to move towards becoming a private limited company. However some partnerships do not want to move to this stage.

The advantages of remaining a partnership rather than becoming a private limited company are:

• It costs money to set-up a limited company (may need to employ a solicitor/accountant to set up the paper work).

• Company accounts are filed so the public can view them (and competitors).

• Additional cost of an auditor to check the accounts before they are filed.

When a partnership finishes, depending on how the Deed of Partnership is set up, each partner has an agreed portion of the business. Partnership accounts are not examinable in the Financial Accounting examination.

1.4.3 Limited Company

A Limited Company is a business that is owned by its shareholders, run by directors and most importantly its liability is limited. There can be one shareholder or many thousands of shareholders. Shareholders are also known as members. Each shareholder owns part of the company. As a group they select the directors who run the business. Directors often own shares in the company, but not all shareholders have to be directors.

Limited Liability means that investors can only lose the money they have invested and no more. This encourages people to finance the company, and/or set up such a business, knowing they can only lose what they have put in, if the company fails. For people or businesses who have a claim against the company, limited liability means that they can only recover money from the existing assets of the business. They cannot claim the personal assets of the shareholders to recover amounts owed by the company.

A Limited Company has to possess a separate legal entity from its shareholders, meaning that the company is seen as separate from its shareholders. To set up a limited company, a company has to

Chapter 1 : Introduction to Accounting

8

Financial Accounting

register with the Registrar of Companies, who maintains a separate file for every company, and is issued with a Certificate of Incorporation. It also needs to have a Memorandum of Association which sets out what the company has been formed to do, and Articles of Association which are internal rules including what the directors can do and voting rights of the shareholders.

The distinguishing factor that differentiates a limited company from a sole trader and a partnership is that a limited company has to prepare annual “statutory accounts”; this is the price to be paid for the benefit of limited liability. Limited companies must produce such accounts annually and may have to appoint an independent person to audit and report on them depending on certain size criteria. Once prepared, a copy of the accounts must be sent to the Registrar of Companies which maintains a separate file for every company. The file for any company can be inspected at the Companies Registration Office for a nominal fee by a member of the general public. This is why the statutory accounts are often referred to as the published accounts.

The advantages of a limited company can be summarised as follows:

• Limited liability.

• Separate legal entity.

• The company’s trading profits are taxed at the corporation tax rate of 12.5% in Ireland, which is considerably lower that the top personal income tax rate of 41%, paid by sole traders and partnerships.

• The company’s name is protected, as two companies cannot have a similar name.

• The company continues despite the death or resignation of management and members.

• The interests and obligations of management are defined.

• Appointment, retirement or removal of directors is straightforward.

• It is easier to procure new shareholders and investors.

• A larger number of investors can own the company than, say, partners in a firm.

• The members’ rights are usually comprehensively defined in the memorandum and articles of association.

The disadvantages of a limited company can be summarised as follows:

• Initial costs of registering a company name with the Companies Registration Office.

• Additional administration costs related to the annual preparation and submission of an ‘annual return’, to the Registrar of Companies, according to statutory requirements. Fees and other penalties apply if companies don’t comply.

• Companies must hold an Annual General Meeting (AGM) within 18 months of incorporation and thereafter on an annual basis (must be an AGM in each calendar year). There are exemptions for single member companies.

• A Corporation Tax Return must be made every year and if the company is VAT Registered, VAT Returns must be made every two months.

• Every company whose turnover exceeds Euro €7.3 million must prepare and file audited financial statements with the Companies Registration Office.

• The potential separation of ownership and control which requires additional corporate governance mechanisms within the company, to monitor internal management.

Chapter 1 : Introduction to Accounting

9

Financial Accounting

1.4.4 Public and Private Limited Companies

Limited companies are governed very tightly, namely through the Companies Acts. Limited companies can either be private limited companies or public limited companies. The difference between the two is that shares in a Public Limited Company (Plc) can be traded on the Stock Exchange and be bought by members of the general public. Shares in a Private Limited Company are not available to the general public.

A private limited company may wish to become a Plc because shares in a private limited company cannot be offered for sale to the general public, thereby restricting the availability of finance, especially if the business wants to expand. Therefore, it is attractive to change status. It is also easier to raise money through other sources of finance, e.g. from banks. It is important to note that a “Plc” does not necessarily mean that the company is quoted on the Stock Exchange. In order to have a listing on the Stock Exchange, the company must undergo a flotation or Initial Public Offering (IPO).

Flotation or Initial Public Offering (IPO)

A company may float on the stock market. This means selling all or part of the business to outside investors. This generates additional funds for the business and can be a major form of fundraising. When shares in a “Plc” are first offered for sale to the general public the company is given a “listing” on the stock exchange. This is called an Initial Public Offering (IPO).

The advantages of being a public limited company (Plc) are:

• Better access to financial resources to support growth objectives i.e. raising share capital from existing and new investors.

• Better liquidity – shareholders are able to buy and sell their shares (if they are quoted on a stock exchange).

• Large Plc’s may find it easier to borrow from banks.

• The value of the firm is readily shown by the market capitalisation (based on the share price).

• Companies can more easily acquire other firms – e.g. by offering shares to the shareholders of the target firm.

• Going public gives a company a more prestigious profile.

The disadvantages of being a public limited company (Plc) are:

• Costly and complicated to set up as a Plc – The business owners need to employee specialist bankers and lawyers to help organise the converting to the Plc.

• Certain financial information must be available for all parties, competitors and customers included (this publication of financial information risks attracting further competition and arming existing competitors).

• Shareholders in public companies expect a steady stream of income from dividends, which might mean that the business has to concentrate on short term objectives of creating profit, whereas it might be better to work on longer term objectives, such as growth and investment.

• The threat of takeover, as another company can buy up a large number of shares because shares are traded publicly (can be sold to anyone). If they buy enough, they can then persuade other shareholders to join with them to vote in a new management team.

Chapter 1 : Introduction to Accounting

10

Financial Accounting

The reasons shareholders buy share are as follows:

• Shares sometimes pay dividends to the shareholders, which is a share of the profits at the end of the year. Companies on the Stock Exchange usually pay dividends twice each year.

• Over time the value of the share might increase and can be sold for a profit – this is known as a “capital gain”. Of course, the price of the shares can go down as well as up, so investing in shares can be risky.

• If they have enough shares they can influence the management of the company. A good example is a “venture capitalist” that will often buy up to an average of between 10% to 50% of the shares of a company and insist on choosing some of the directors.

Separation of Ownership and Control and the need for Corporate Governance

As a business becomes larger, the ownership and control of the business may become separated. This is because the shareholders may have the money, but not the time or management skills to run the company. Therefore, the day-to-day running of the business is entrusted to the directors, who are employed for their skills, by the shareholders. This agency relationship between the shareholders and the directors is referred to as Corporate Governance.

The shareholders are therefore “divorced” from the running of the business for 364 days of the year. They will have their say at the Annual General Meeting (AGM) of the company, where the directors present the accounts and the results. In practice directors tend to have at least a modest shareholding in the company. This provides the director with an incentive to achieve good dividends and capital growth for the share (an increase in the share price).

NOTE: Company accounts are not examinable in the Financial Accounting examination.

In summary for all three types of entity, the money invested by the individual, the partners or the shareholders, is referred to as the business capital. In the case of a company, this capital is divided into shares (Share Capital).

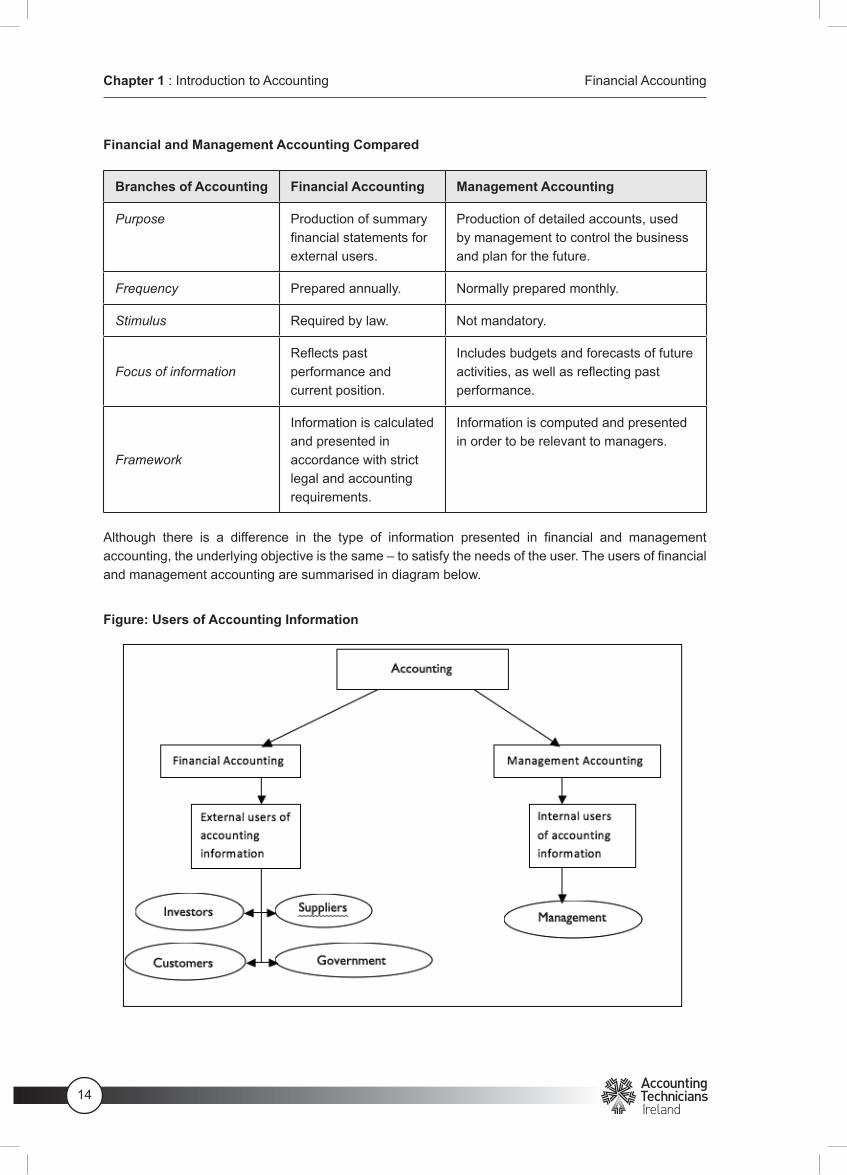

1.5 USERS OF ACCOUNTING INFORMATION

There are many potential users of accounting information, including shareholders, lenders, customers, suppliers, government departments (e.g. Revenue), employees and their organisations, and society at large. Anyone with an interest in the performance and activities of an organisation is traditionally called a stakeholder.

For a business or organisation to communicate its results and position to stakeholders, it needs a language that is understood by all in common. Hence, accounting has come to be known as the language of business. There are two broad types of accounting information and two broad groups of information users:

1. Financial Accounting: geared towards external users of accounting information.

2. Management Accounting: geared more at internal users of accounting information.

Chapter 1 : Introduction to Accounting

11

Financial Accounting

Although there is a difference in the type of information presented in financial and management accounts, the underlying objective is the same – to satisfy the information needs of the user. These needs can be described in terms of the overall accounting information objectives stated in section 1.3.

1.6 USERS OF FINANCIAL STATEMENTS

It is easy to assume that the only users of accounting information are shareholders – since it is a requirement of company law that shareholders must receive financial statements. However, in reality there are many users of accounts. The following subsections summarises the main users groups and provides examples of their areas of interest in accounts.

1.6.1 Investors

Investors are concerned about risk and return in relation to their investments. They require information to decide whether they should continue to invest in a business. They also need to be able to access whether a business will be able to pay dividends, and measure the performance of the business’ management team.

The key accounting information for an investor is therefore:

• Information about growth, sales, volumes.

• Profitability (profit margins, overall level of profit).

• Investment (amounts invested, assets owned).

• Business value (share price).

• Comparative information of competitors.

1.6.2 Lenders

Banks and loan stockholders who lend money to a business require information that helps them determine whether loans and interest will be paid when due.

The key accounting information for lenders is therefore:

• Level of existing debt

• Cash flow.

• Security of assets against which the lending may be secured.

• Investment requirements in the business.

1.6.3 Suppliers

Suppliers and trade payables require information that helps them understand and assess the short-term liquidity of a business. For example is the business able to pay short-term debt when it falls due?

The key accounting information for suppliers is therefore:

• Cash flow.

• Management of working capital.

• Payment policy.

Chapter 1 : Introduction to Accounting

12

Financial Accounting

1.6.4 Customers

Customers and trade receivables require information about the ability of the business to survive and prosper. As customers of the company’s products, they have a long-term interest in the company’s range of products and services. They may even be dependent on the business for certain products and services.

The key accounting information for customers is therefore:

• Sales growth.

• New product development.

• Investment in the business (e.g. production capacity).

1.6.5 Employees

Employees (and organisations that represent them – e.g. trade unions) require information about the stability and continuing profitability of the business. They are very interested in information about employment prospects and the maintenance of pension funding and retirement benefits. They are also likely to be interested in the pay and benefits obtained by senior management.

The key accounting information for employees is therefore:

• Revenue and profit growth.

• Levels of investment in the business.

• Overall employment data (numbers employed, wages and salary costs).

• Status and valuation of the company pension schemes/levels of company contributions.

1.6.6 Government

There are many government agencies and departments that are interested in accounting information. For example, the Revenue Commissioners need information on business profitability in order to levy and collect Corporation Tax. Customs and Excise need accounting information to verify Value Added Tax (VAT) returns; local government need similar information to levy local taxes and rates. Various regulatory agencies (i.e. the Environment Agency) need information to support decisions about grants, for example.

1.6.7 Analysts

Investment analysts are an important user group – specifically for companies quoted on the Stock Exchange. They require very detailed financial and other information in order to analyse the competitive performance of a business and its sector. Much of this is provided by the detailed accounting disclosures that are required by authorities such as the London Stock Exchange. However, additional accounting information is usually provided to analysts via informal company briefings and media interviews.

Chapter 1 : Introduction to Accounting

13

Financial Accounting

1.6.8 Public at large

Interest groups, formed by various individuals who have a specific interest in the activities and performance of businesses, will also require accounting information, e.g. resident committees where the business is located in a residential area.

1.7 TYPES OF ACCOUNTING

As stated earlier there are two broad types of accounting information, financial and management accounting.

Financial Accounting is geared towards external users of accounting information. External users are, as discussed above, investors, creditors, debtors, lenders and the government.

Such reporting is usually accomplished through the preparation and presentation of financial statements. In order to facilitate comparison, financial accounts are prepared using accepted accounting conventions and standards. International Accounting Standards (IAS) help to reduce the differences in the way companies draw up their financial statements. The financial statements are public documents, and therefore they will not reveal details about product profitability.

Management need much more detailed and up-to-date information in order to control the business and plan for the future.

Management accounting is geared towards internal users of accounting information. Internal users are, as discussed above, management and employees.

Such reporting is accomplished through custom designed reports. Management accounts provide information to enable costing products and production methods, assessing profitability and so on. In order to facilitate this, management accounts present information in any way which may be useful to management, for example by operating unit or by product line.

Management accounting is an integral part of management activity concerned with identifying, presenting and interpreting information used for:

• Formulation of strategy.

• Planning and controlling activities.

• Decision making.

• Optimising the use of resources.

Students will study Management Accounting as a complete subject in Second Year. The table below outlines a comparison of the branches of accounting.

Chapter 1 : Introduction to Accounting

14

Financial Accounting

Financial and Management Accounting Compared

Branches of Accounting Financial Accounting Management Accounting

Purpose

Production of summary financial statements for external users.