Embed Size (px)

Citation preview

Financial Project Metrics in Feasibility Study

Cost Estimation - Factors Hardware and Software costs

including maintenance Travel and Training costs Effort costs (costs of paying SW engineers)

Heating lighting and office space Support staff (accountants, cleaners etc) Infrastructure (network + communications) Facilities (library, refreshments, recreation) Social security, employee benefits, pensions

etc

Cost Benefit Analysis Compare the costs of carrying out

a project with the estimated benefits

Identify all costs Development Costs Running Costs – annual costs

Cost Benefit Analysis Include all direct benefits of the project

Will normally accrue on completion – but not always

May be annual benefits/savings

Express costs and benefits in a common unit

£, €, $ etc

What about intangible benefits?

Cost Benefit Analysis Example layout

Project Costs Direct Costs – Costs that can be

directly attributed to a project task (labour, materials etc.)

Indirect Costs – Overheads that do not directly contribute to the project (rent, heating, lighting, admin)

Pricing vs. Costing Price to charge for software

= Cost + Profit Other factors may effect the pricing e.g. competitive environment, loss

leader project Pricing therefore involves:

project managers for costing senior management for pricing

strategies

Costs vs. Budget Cost = how much it will cost to

produce system Budget = how much you will be

allowed to spend on producing system

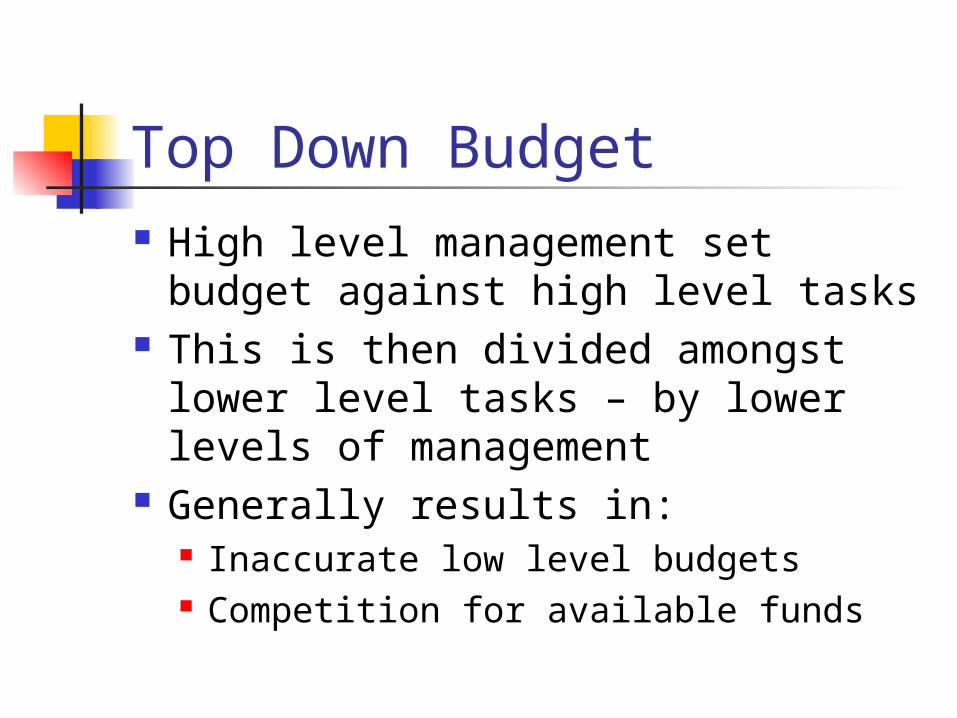

Top Down Budget High level management set budget

against high level tasks This is then divided amongst lower

level tasks – by lower levels of management

Generally results in: Inaccurate low level budgets Competition for available funds

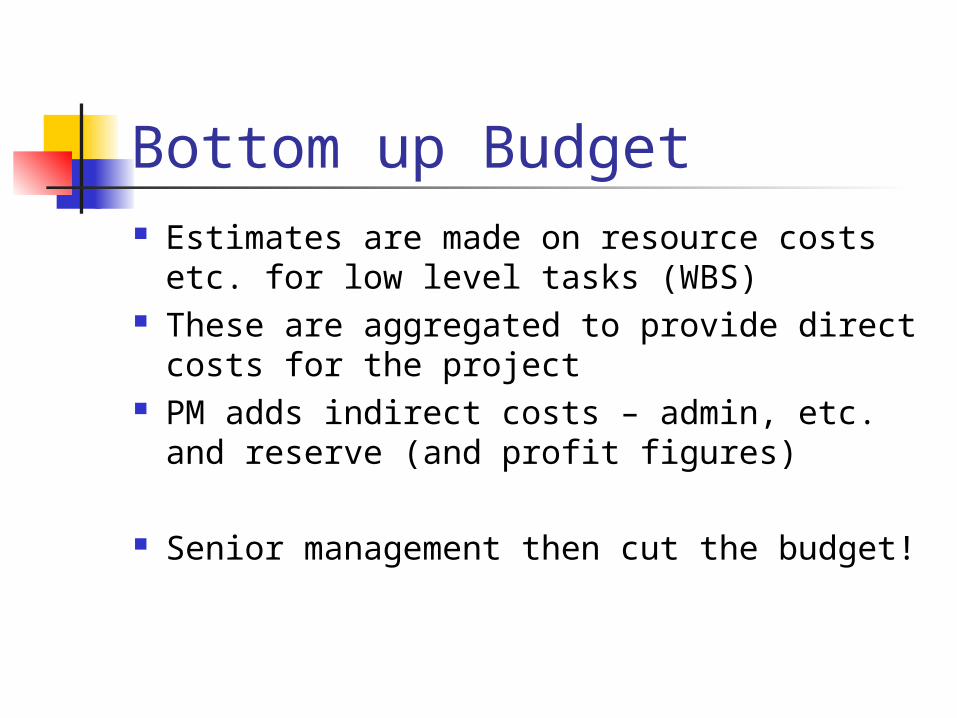

Bottom up Budget Estimates are made on resource costs

etc. for low level tasks (WBS) These are aggregated to provide direct

costs for the project PM adds indirect costs – admin, etc. and

reserve (and profit figures)

Senior management then cut the budget!

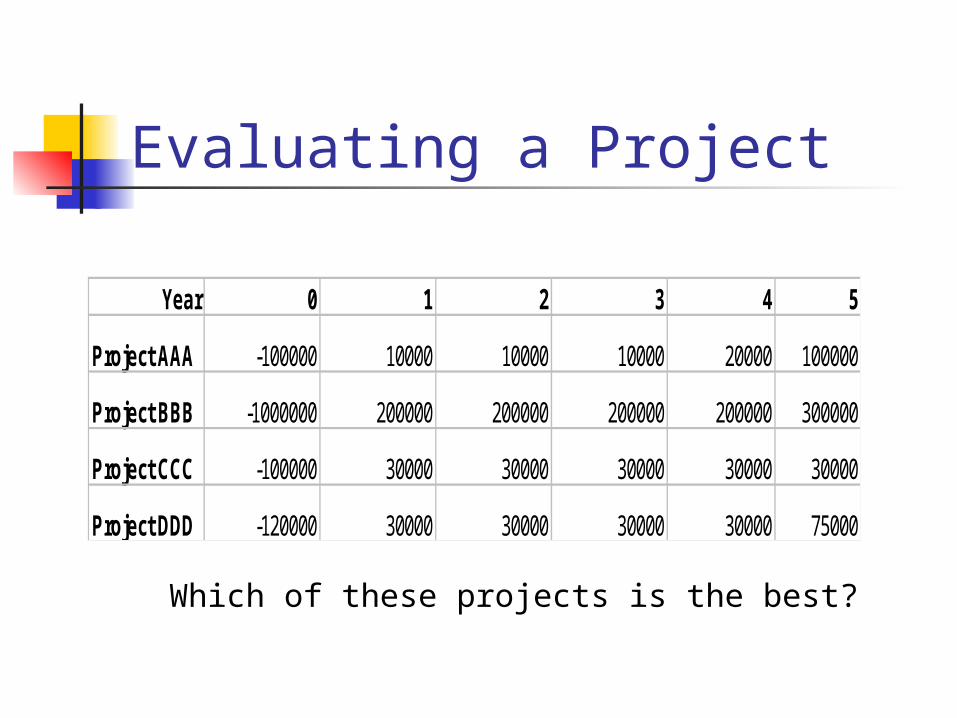

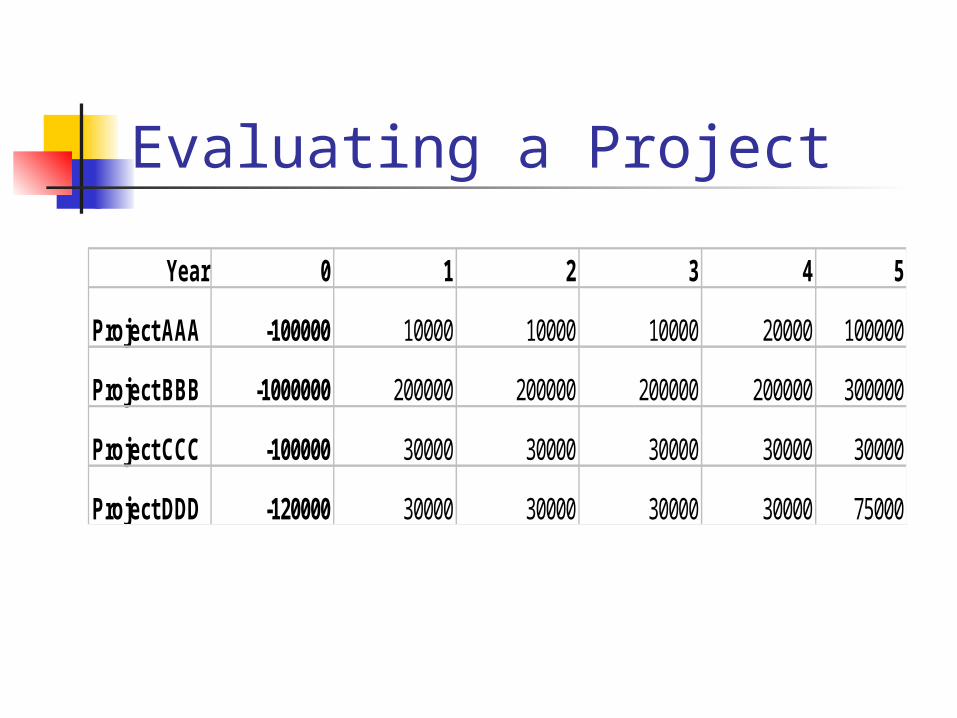

Evaluating a Project

Year 0 1 2 3 4 5

Project AAA -100000 10000 10000 10000 20000 100000

Project BBB -1000000 200000 200000 200000 200000 300000

Project CCC -100000 30000 30000 30000 30000 30000

Project DDD -120000 30000 30000 30000 30000 75000

Which of these projects is the best?

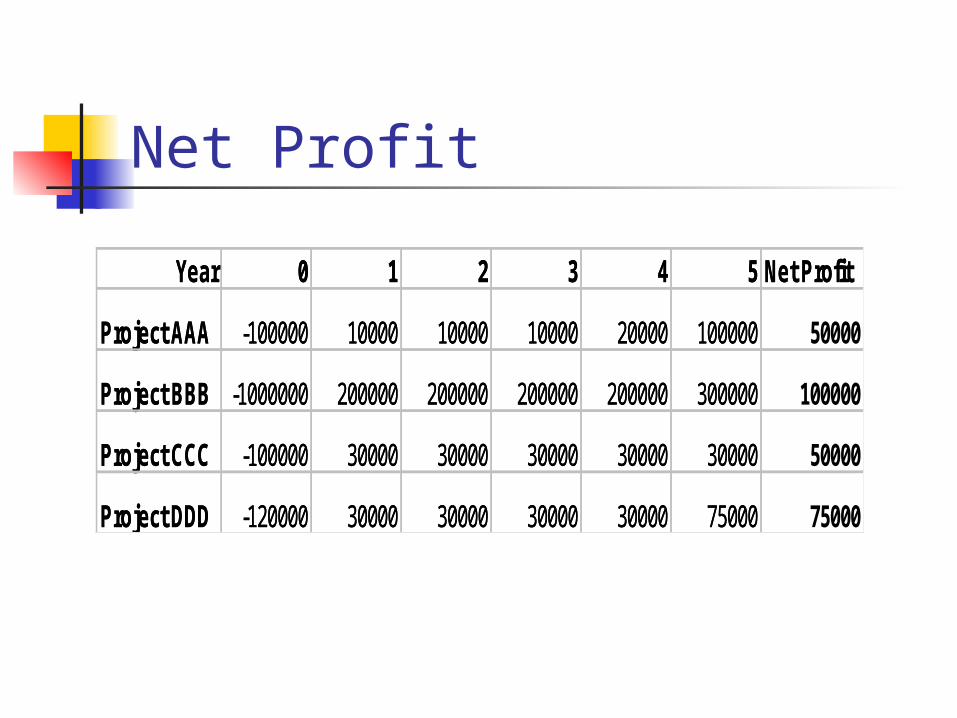

Net Profit

Year 0 1 2 3 4 5 Net Profit

Project AAA -100000 10000 10000 10000 20000 100000 50000

Project BBB -1000000 200000 200000 200000 200000 300000 100000

Project CCC -100000 30000 30000 30000 30000 30000 50000

Project DDD -120000 30000 30000 30000 30000 75000 75000

Year 0 1 2 3 4 5 Net Profit

Project AAA -100000 10000 10000 10000 20000 100000

Project BBB -1000000 200000 200000 200000 200000 300000

Project CCC -100000 30000 30000 30000 30000 30000

Project DDD -120000 30000 30000 30000 30000 75000

Net Profit The most obvious criteria for

comparison Does not give the full picture

regarding the viability of the project

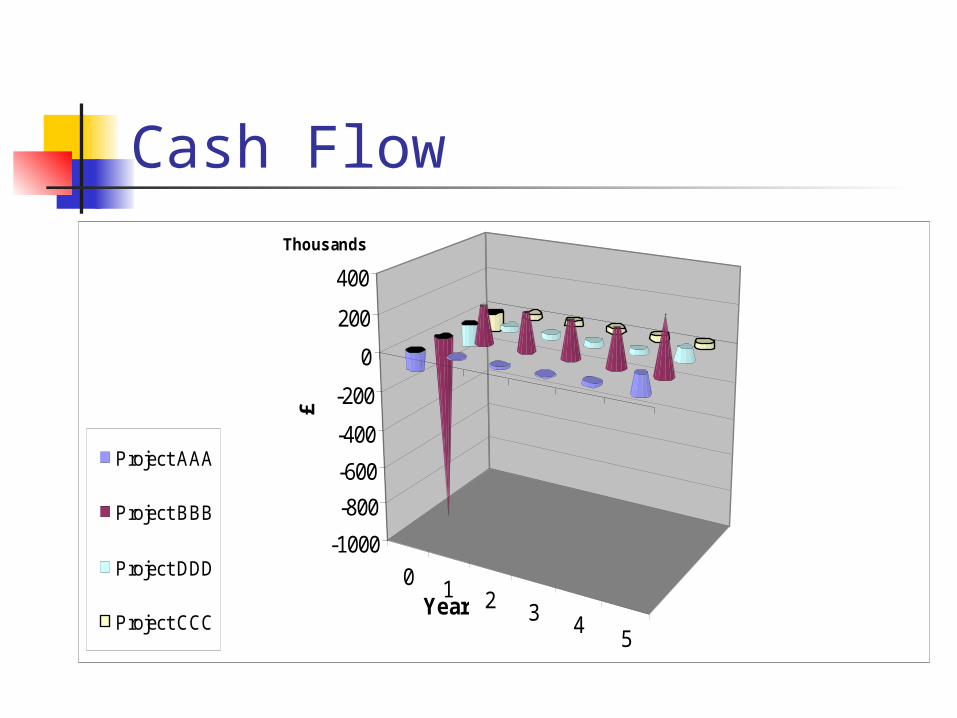

Cash Flow Can the organisation afford the –ve

cash flow required for the development of the project e.g. Project BBB requires an initial

outlay of £1000,000

Cash Flow We need to spend money during

the development of a product We hope to get it back once the

product is finished Therefore projects will have a –ve

cash flow during their development This should become +ve once the

project is complete

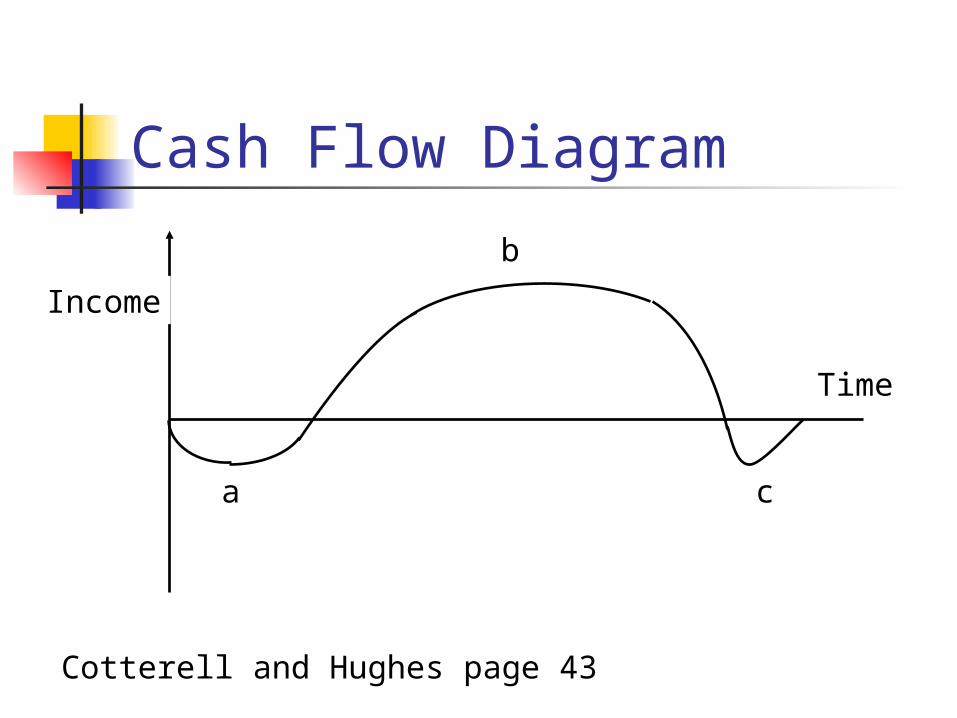

Cash Flow Diagram

Cotterell and Hughes page 43

Income

Time

a

b

c

Cash Flow

0 1 2 3 45

-1000

-800

-600

-400

-200

0

200

400£

Thousands

Year

Project AAA

Project BBB

Project DDD

Project CCC

Evaluating a Project

Year 0 1 2 3 4 5

Project AAA -100000 10000 10000 10000 20000 100000

Project BBB -1000000 200000 200000 200000 200000 300000

Project CCC -100000 30000 30000 30000 30000 30000

Project DDD -120000 30000 30000 30000 30000 75000

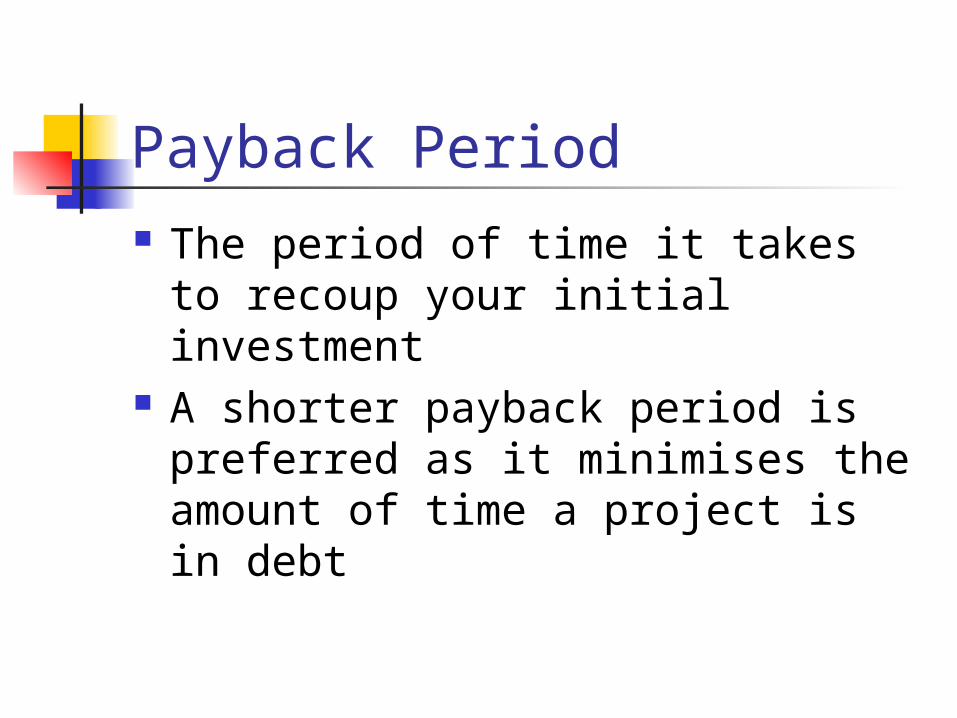

Payback Period The period of time it takes to

recoup your initial investment A shorter payback period is

preferred as it minimises the amount of time a project is in debt

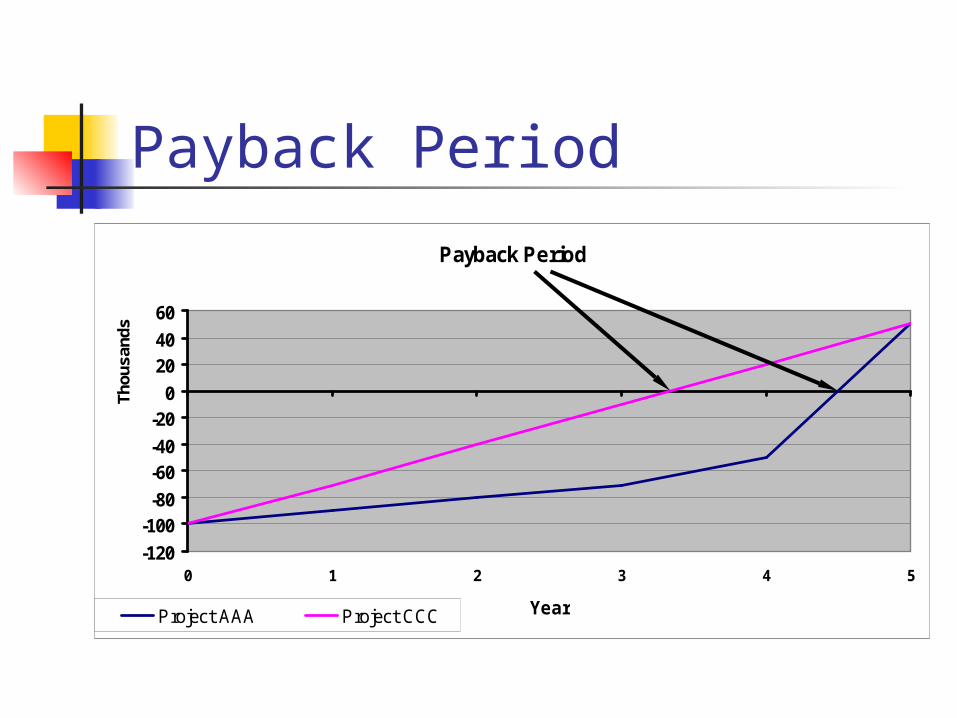

Payback Period

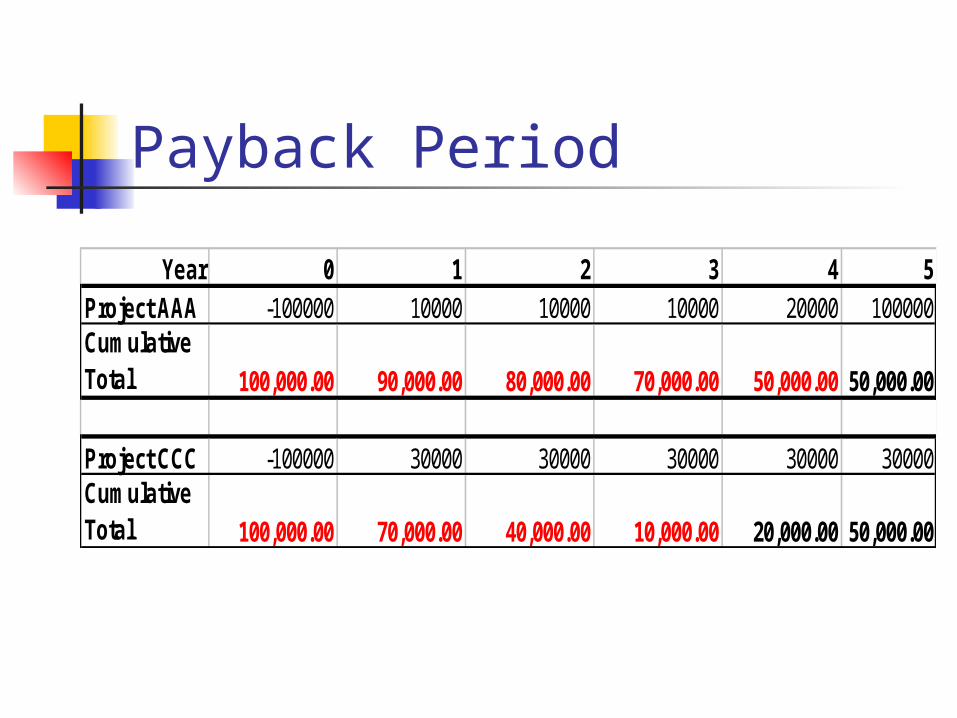

Year 0 1 2 3 4 5Project AAA -100000 10000 10000 10000 20000 100000Cumulative Total 100,000.00 90,000.00 80,000.00 70,000.00 50,000.00 50,000.00

Project CCC -100000 30000 30000 30000 30000 30000Cumulative Total 100,000.00 70,000.00 40,000.00 10,000.00 20,000.00 50,000.00

Payback Period

Payback Period

-120

-100-80

-60-40

-200

2040

60

0 1 2 3 4 5

Thou

sand

s

YearProject AAA Project CCC

Payback Period Find the payback period for

projects BBB and DDD

Payback Period

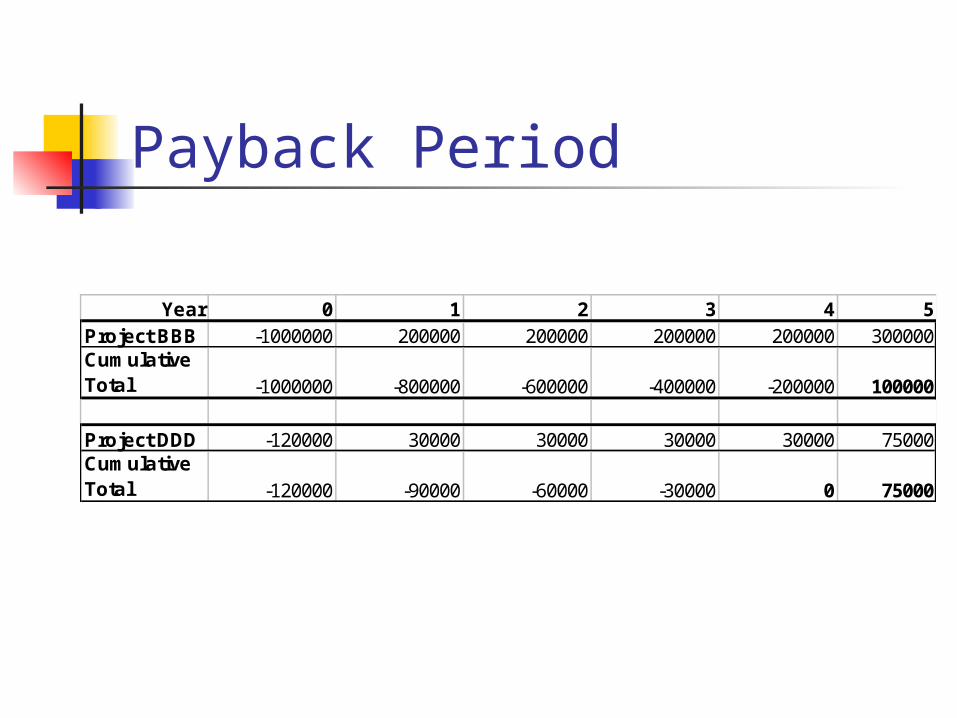

Year 0 1 2 3 4 5Project BBB -1000000 200000 200000 200000 200000 300000Cumulative Total -1000000 -800000 -600000 -400000 -200000 100000

Project DDD -120000 30000 30000 30000 30000 75000Cumulative Total -120000 -90000 -60000 -30000 0 75000

Return on Investment Is it really worth investing all that

time, money and effort into the project?

To help make that decision we use the return on investment

The investment will be the initial development costs of the project

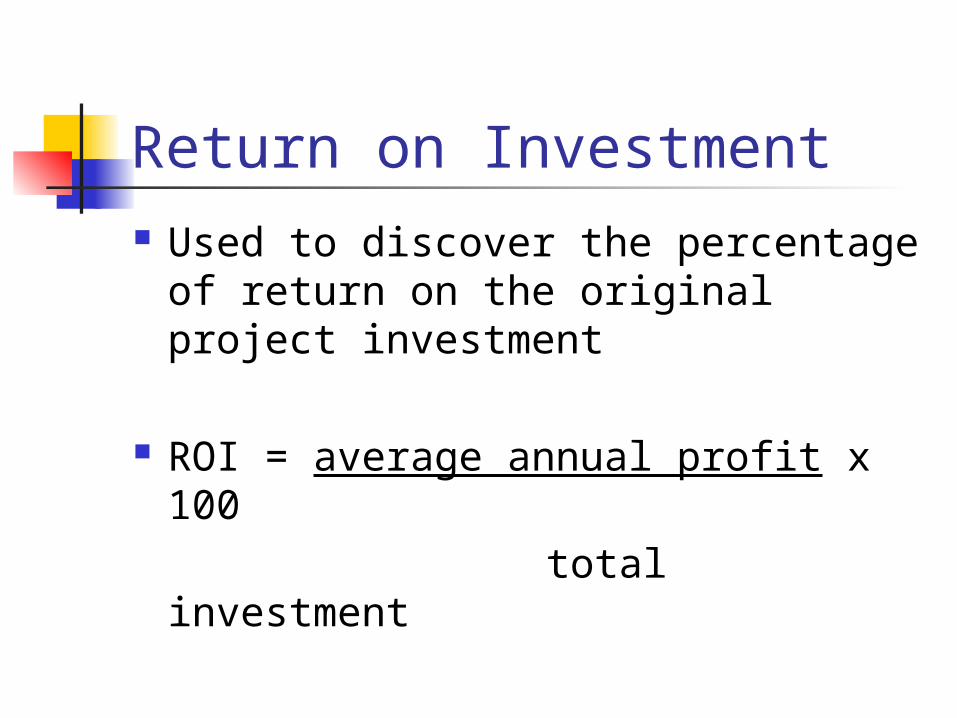

Return on Investment Used to discover the percentage of

return on the original project investment

ROI = average annual profit x 100 total investment

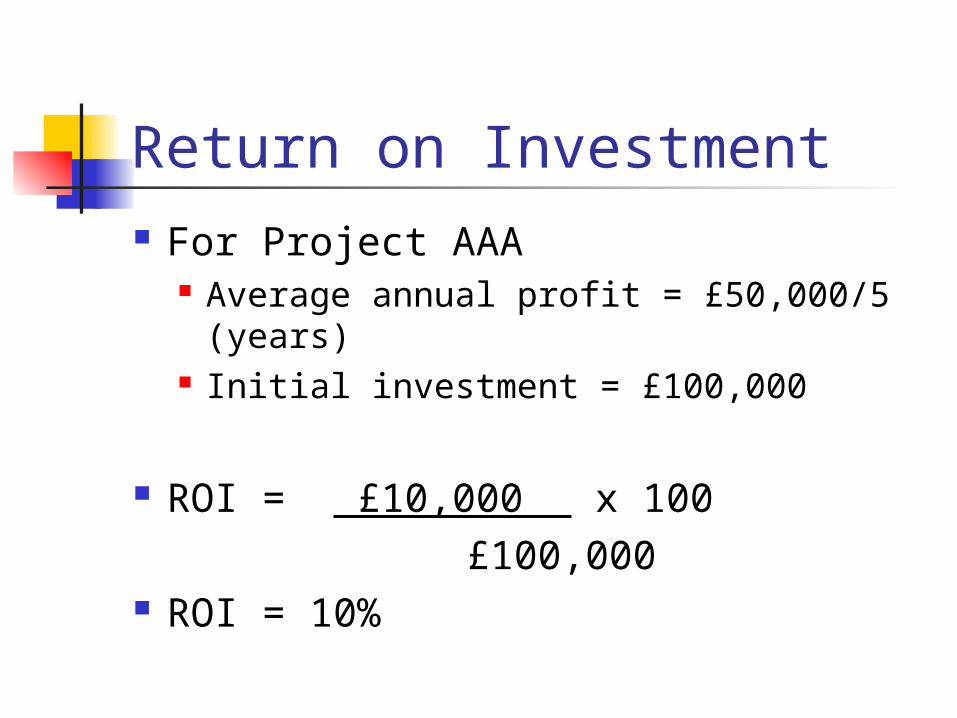

Return on Investment For Project AAA

Average annual profit = £50,000/5 (years)

Initial investment = £100,000

ROI = £10,000 x 100 £100,000 ROI = 10%

Return on Investment Calculate the ROI for the remaining

projects and show which one provides the best return

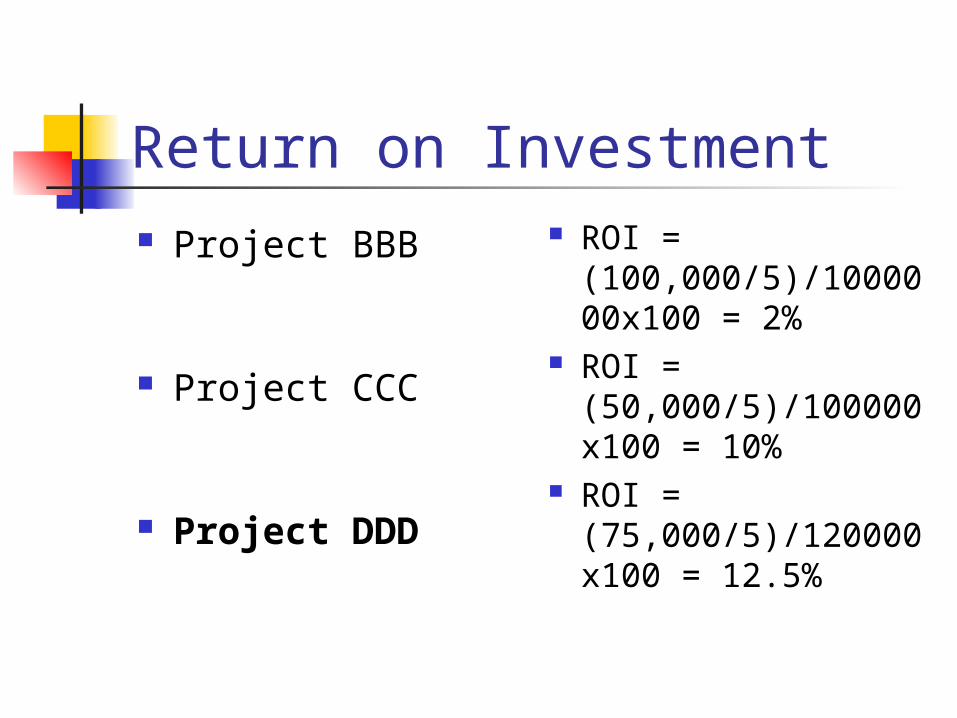

Return on Investment Project BBB

Project CCC

Project DDD

ROI = (100,000/5)/1000000x100 = 2%

ROI = (50,000/5)/100000x100 = 10%

ROI = (75,000/5)/120000x100 = 12.5%

Project BBB

Project CCC

Project DDD

Net Present Value Takes into account the profitability

of a project and the timing of cash flows

Receiving £1000 today is better then receiving £1000 next year Inflation – things will cost more Investment – we lose a year’s interest

Net Present Value - Examples If we invested £100 this year it would

be worth £110 next year (assuming 10% interest rate – not likely)

Therefore if we were given £100 next year it would have been the same as investing £90(ish) this year.

This 10% is called the discount rate

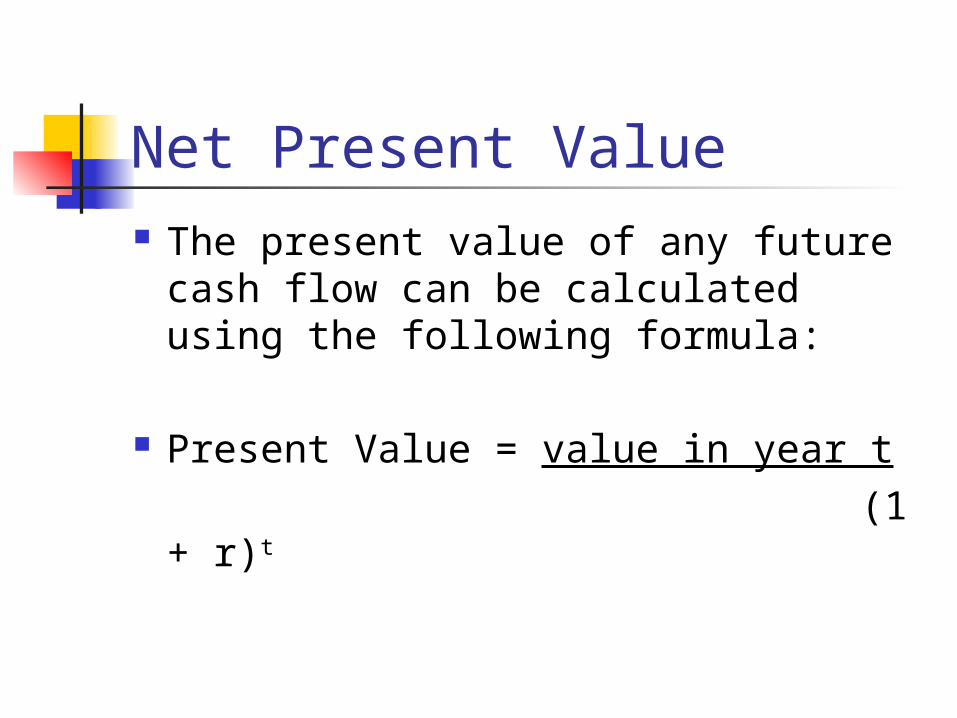

Net Present Value The present value of any future

cash flow can be calculated using the following formula:

Present Value = value in year t (1 + r)t

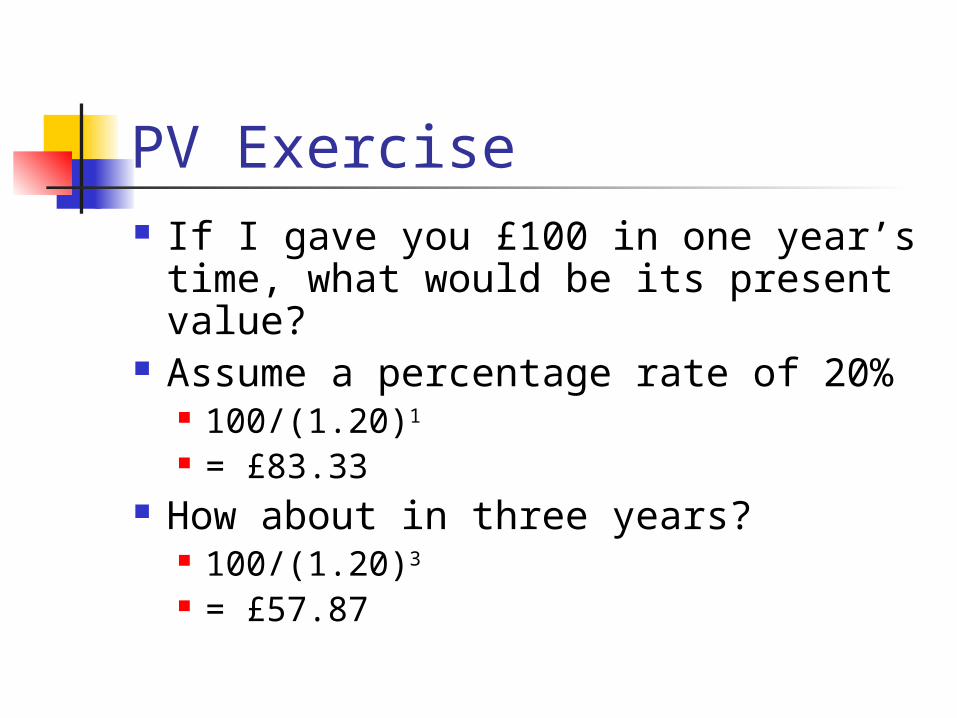

PV Exercise If I gave you £100 in one year’s

time, what would be its present value?

Assume a percentage rate of 20% 100/(1.20)1

= £83.33 How about in three years?

100/(1.20)3

= £57.87

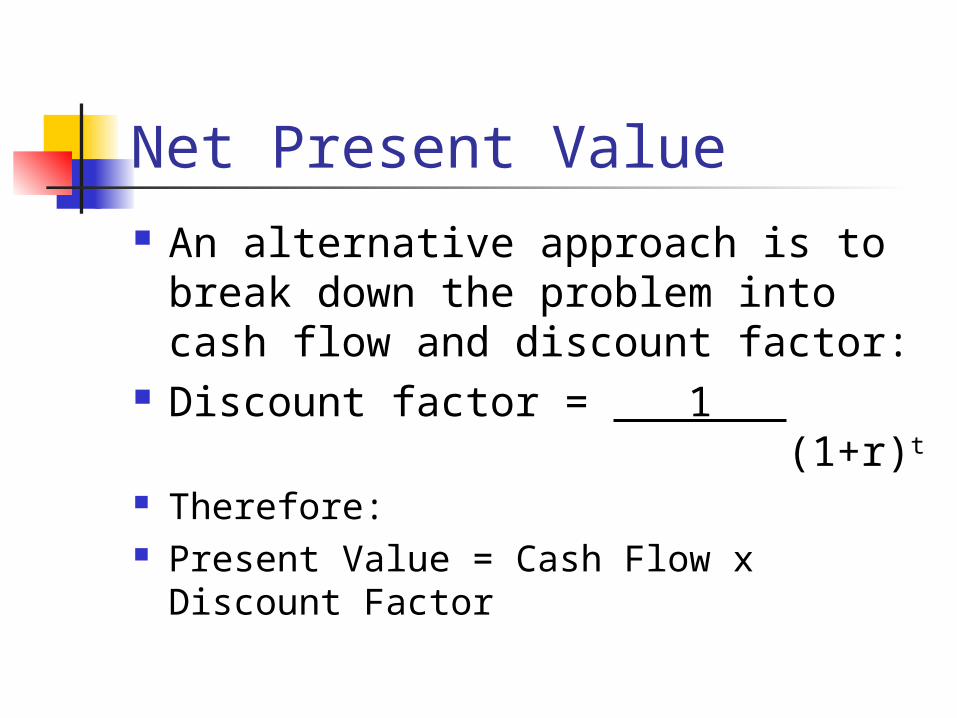

Net Present Value An alternative approach is to break

down the problem into cash flow and discount factor:

Discount factor = 1 (1+r)t

Therefore: Present Value = Cash Flow x Discount

Factor

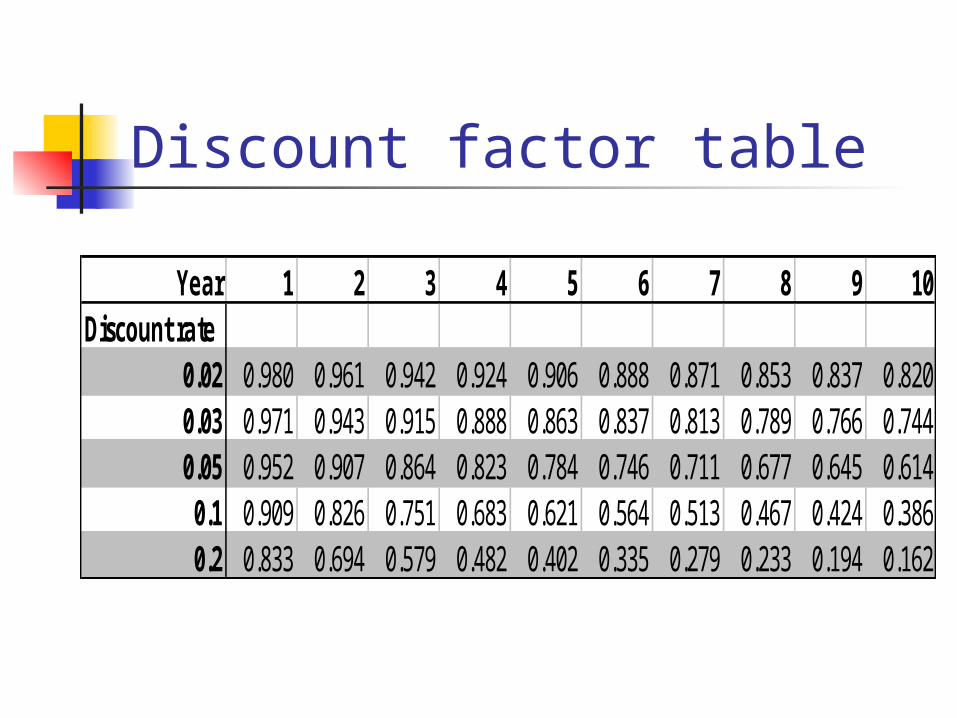

Discount factor table

Year 1 2 3 4 5 6 7 8 9 10Discount rate

0.02 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.8200.03 0.971 0.943 0.915 0.888 0.863 0.837 0.813 0.789 0.766 0.7440.05 0.952 0.907 0.864 0.823 0.784 0.746 0.711 0.677 0.645 0.6140.1 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.3860.2 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162

Net Present Value Net Present Value is the sum of the

present values (aka discounted cash flows)

As can be seen on the next slide, the profit figures can differ significantly using Net PV instead of Net Profit

The payback period may also be effected

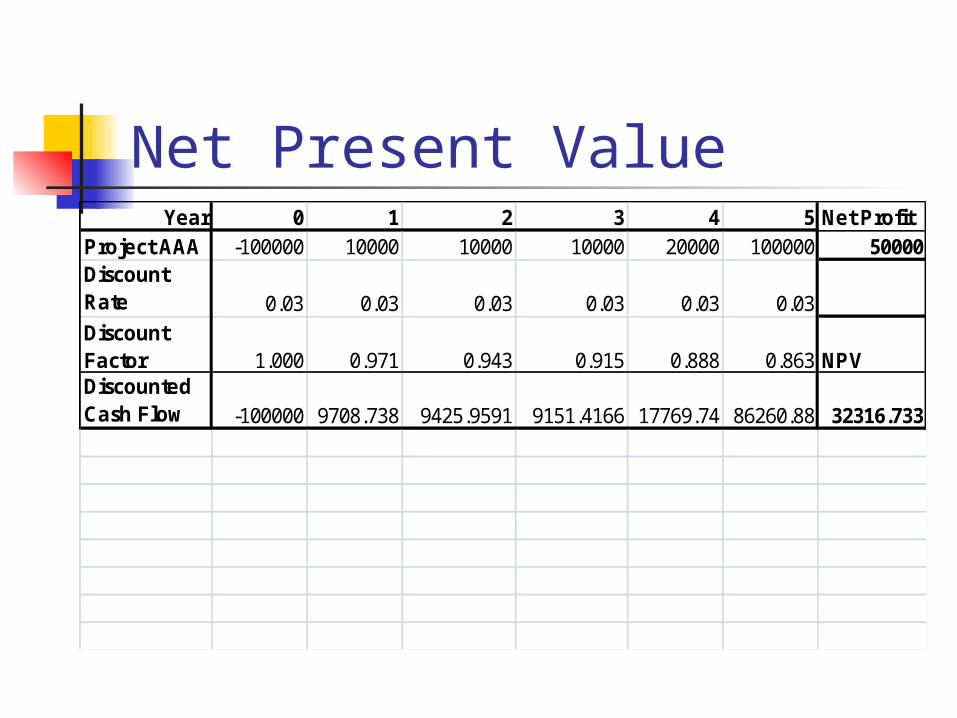

Net Present ValueYear 0 1 2 3 4 5 Net Profit

Project AAA -100000 10000 10000 10000 20000 100000 50000Discount Rate 0.03 0.03 0.03 0.03 0.03 0.03Discount Factor 1.000 0.971 0.943 0.915 0.888 0.863 NPVDiscounted Cash Flow -100000 9708.738 9425.9591 9151.4166 17769.74 86260.88 32316.733

Net Present Value

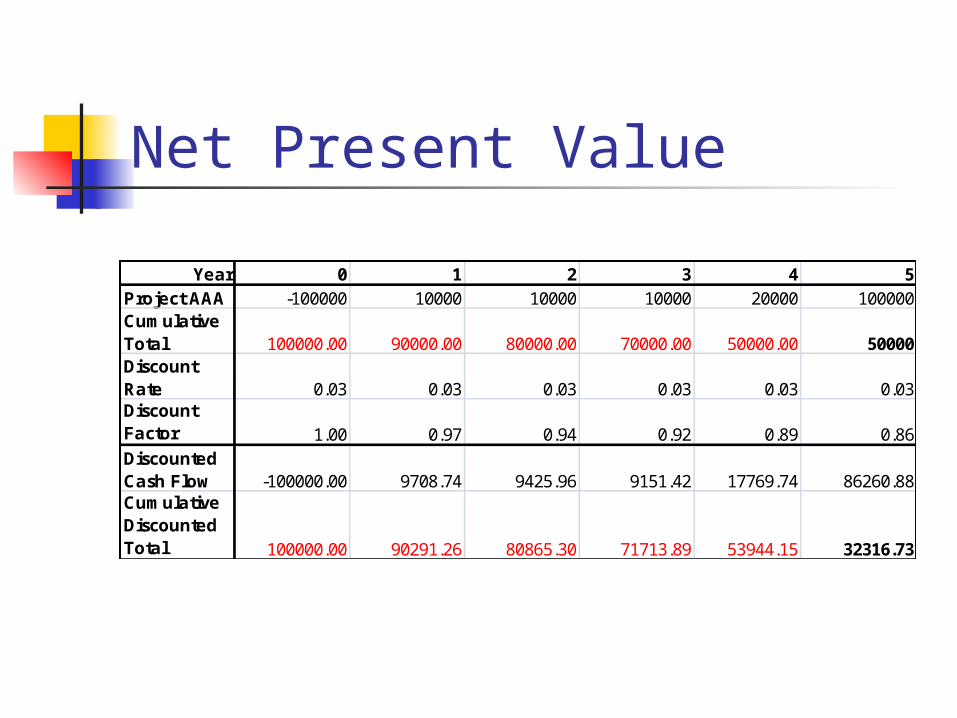

Year 0 1 2 3 4 5Project AAA -100000 10000 10000 10000 20000 100000Cumulative Total 100000.00 90000.00 80000.00 70000.00 50000.00 50000Discount Rate 0.03 0.03 0.03 0.03 0.03 0.03Discount Factor 1.00 0.97 0.94 0.92 0.89 0.86Discounted Cash Flow -100000.00 9708.74 9425.96 9151.42 17769.74 86260.88Cumulative Discounted Total 100000.00 90291.26 80865.30 71713.89 53944.15 32316.73

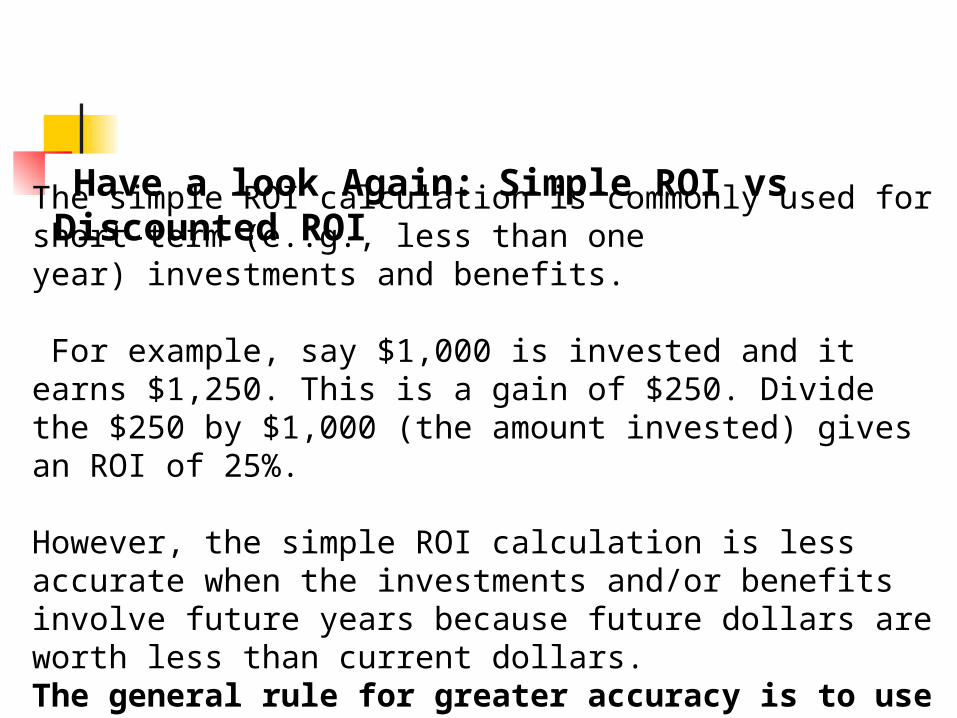

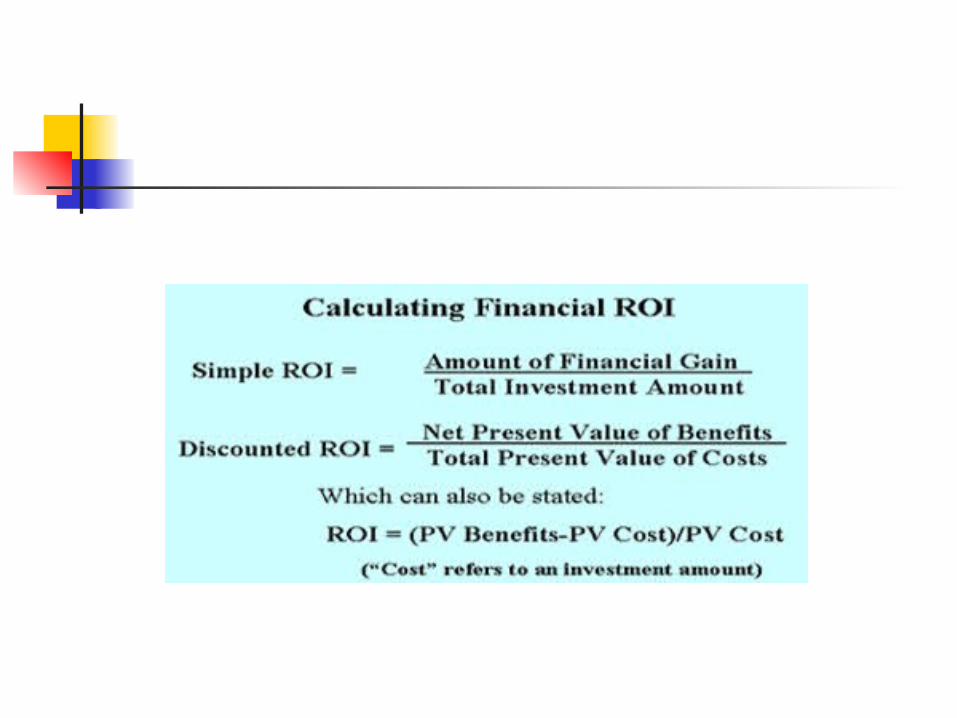

Have a look Again: Simple ROI vs Discounted ROI The simple ROI calculation is commonly used for short-term (e..g., less than one year) investments and benefits.

For example, say $1,000 is invested and it earns $1,250. This is a gain of $250. Divide the $250 by $1,000 (the amount invested) gives an ROI of 25%.

However, the simple ROI calculation is less accurate when the investments and/or benefits involve future years because future dollars are worth less than current dollars.The general rule for greater accuracy is to use the discounted ROI calculation method when the investments and/or the benefits involve future years.

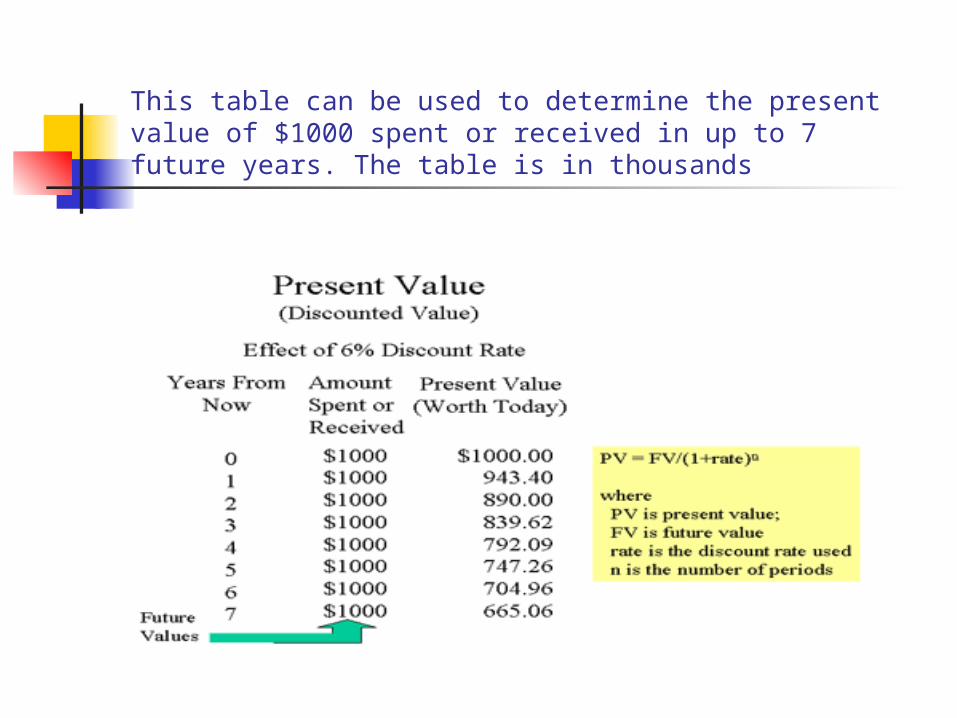

This table can be used to determine the present value of $1000 spent or received in up to 7 future years. The table is in thousands

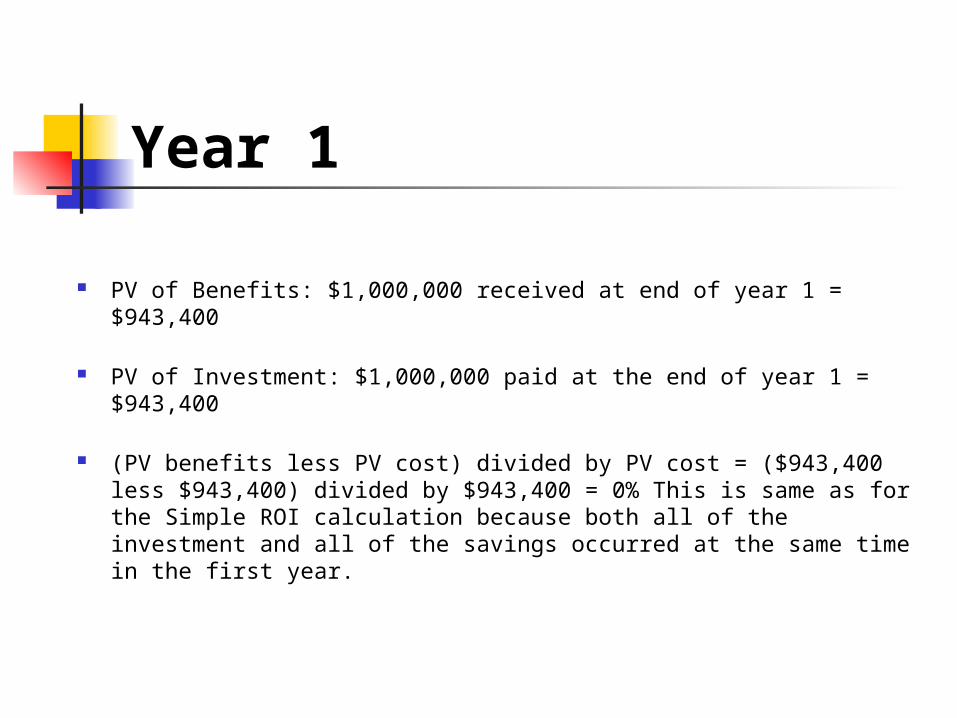

Year 1

PV of Benefits: $1,000,000 received at end of year 1 = $943,400

PV of Investment: $1,000,000 paid at the end of year 1 = $943,400

(PV benefits less PV cost) divided by PV cost = ($943,400 less $943,400) divided by $943,400 = 0% This is same as for the Simple ROI calculation because both all of the investment and all of the savings occurred at the same time in the first year.

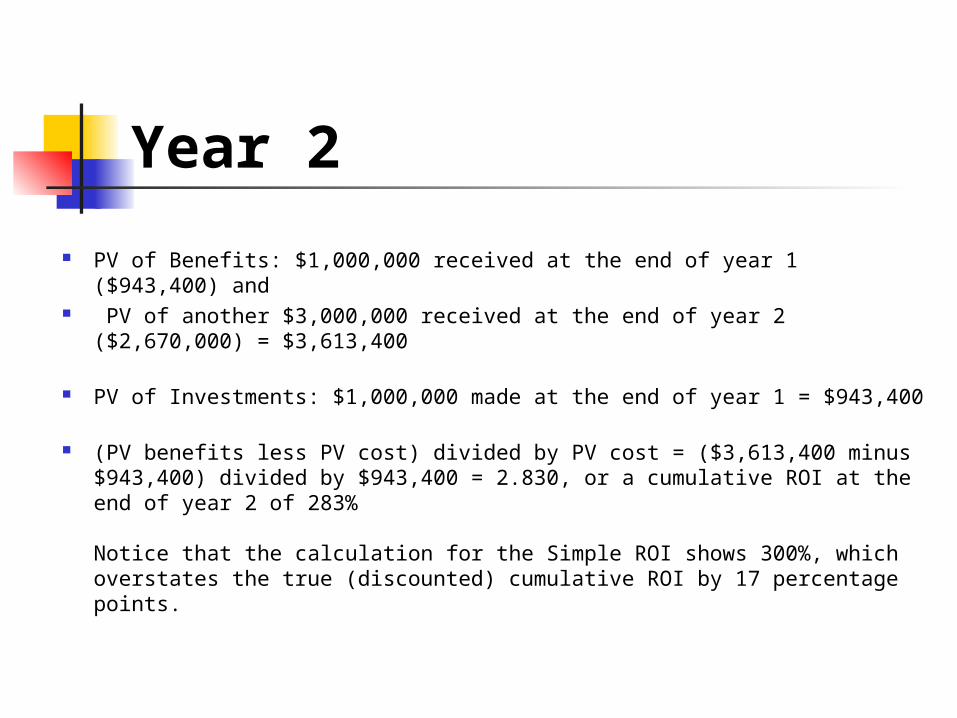

Year 2

PV of Benefits: $1,000,000 received at the end of year 1 ($943,400) and PV of another $3,000,000 received at the end of year 2 ($2,670,000) =

$3,613,400

PV of Investments: $1,000,000 made at the end of year 1 = $943,400

(PV benefits less PV cost) divided by PV cost = ($3,613,400 minus $943,400) divided by $943,400 = 2.830, or a cumulative ROI at the end of year 2 of 283%

Notice that the calculation for the Simple ROI shows 300%, which overstates the true (discounted) cumulative ROI by 17 percentage points.