Embed Size (px)

Citation preview

www.arcelormittalsa.com

Financial results for the six months ended June 2014

1

www.arcelormittalsa.com Overview

2

Agenda

• Overview CEO, Paul O’Flaherty

• Steel market overview CEO, Paul O’Flaherty

• Finance CFO, Matthias Wellhausen

• Operating results COO, Hans Ludwig Rosenstock

• Other key issues and outlook CEO, Paul O’Flaherty

• Questions

www.arcelormittalsa.com

Overview Paul O’Flaherty, CEO

3

www.arcelormittalsa.com Overview

4

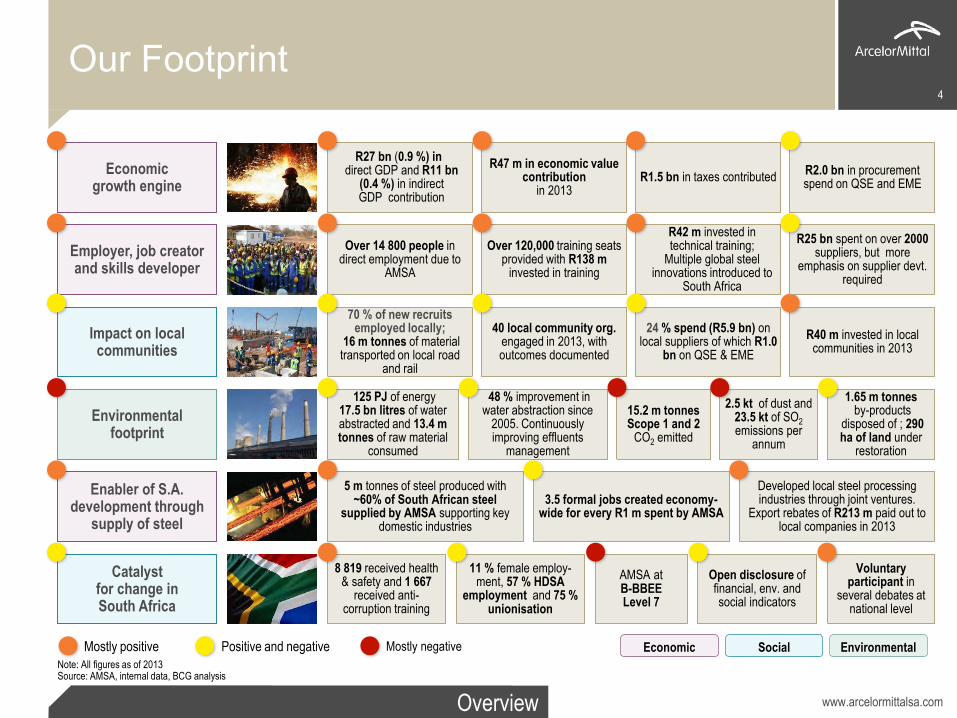

70 % of new recruits employed locally;

16 m tonnes of material transported on local road

and rail

R40 m invested in local communities in 2013

40 local community org. engaged in 2013, with outcomes documented

24 % spend (R5.9 bn) on local suppliers of which R1.0

bn on QSE & EME

5 m tonnes of steel produced with ~60% of South African steel

supplied by AMSA supporting key domestic industries

3.5 formal jobs created economy-wide for every R1 m spent by AMSA

Developed local steel processing industries through joint ventures.

Export rebates of R213 m paid out to local companies in 2013

Our Footprint

Note: All figures as of 2013 Source: AMSA, internal data, BCG analysis

Employer, job creator and skills developer

Impact on local communities

Environmental footprint

Enabler of S.A. development through

supply of steel

Catalyst for change in South Africa

Economic growth engine

R27 bn (0.9 %) in direct GDP and R11 bn

(0.4 %) in indirect GDP contribution

R1.5 bn in taxes contributed

R42 m invested in technical training;

Multiple global steel innovations introduced to

South Africa

Over 14 800 people in direct employment due to

AMSA

Over 120,000 training seats provided with R138 m

invested in training

Economic Social Environmental Mostly positive Positive and negative Mostly negative

R2.0 bn in procurement spend on QSE and EME

R47 m in economic value contribution

in 2013

15.2 m tonnes Scope 1 and 2

CO2 emitted

1.65 m tonnes by-products

disposed of ; 290 ha of land under

restoration

48 % improvement in water abstraction since

2005. Continuously improving effluents

management

125 PJ of energy 17.5 bn litres of water abstracted and 13.4 m tonnes of raw material

consumed

2.5 kt of dust and 23.5 kt of SO2 emissions per

annum

11 % female employ-ment, 57 % HDSA

employment and 75 % unionisation

8 819 received health & safety and 1 667

received anti-corruption training

Open disclosure of financial, env. and social indicators

AMSA at B-BBEE Level 7

Voluntary participant in

several debates at national level

R25 bn spent on over 2000 suppliers, but more

emphasis on supplier devt. required

www.arcelormittalsa.com Overview

Our value creation model 5

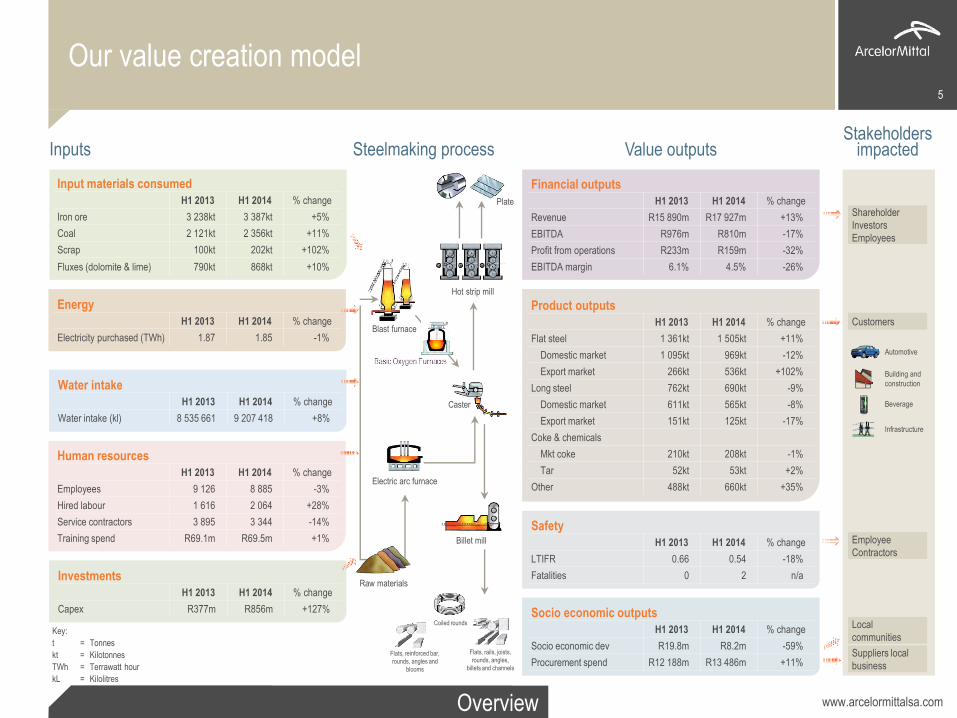

Key:

t = Tonnes

kt = Kilotonnes

TWh = Terrawatt hour

kL = Kilolitres

Inputs

Input materials consumed

H1 2013 H1 2014 % change

Iron ore 3 238kt 3 387kt +5%

Coal 2 121kt 2 356kt +11%

Scrap 100kt 202kt +102%

Fluxes (dolomite & lime) 790kt 868kt +10%

Energy

H1 2013 H1 2014 % change

Electricity purchased (TWh) 1.87 1.85 -1%

Water intake

H1 2013 H1 2014 % change

Water intake (kl) 8 535 661 9 207 418 +8%

Human resources

H1 2013 H1 2014 % change

Employees 9 126 8 885 -3%

Hired labour 1 616 2 064 +28%

Service contractors 3 895 3 344 -14%

Training spend R69.1m R69.5m +1%

Investments

H1 2013 H1 2014 % change

Capex R377m R856m +127%

Financial outputs

H1 2013 H1 2014 % change

Revenue R15 890m R17 927m +13%

EBITDA R976m R810m -17%

Profit from operations R233m R159m -32%

EBITDA margin 6.1% 4.5% -26%

Stakeholders impacted

Shareholder

Investors

Employees

Customers

Automotive

Building and

construction

Beverage

Infrastructure

Employee

Contractors

Local

communities

Suppliers local

business

Product outputs

H1 2013 H1 2014 % change

Flat steel 1 361kt 1 505kt +11%

Domestic market 1 095kt 969kt -12%

Export market 266kt 536kt +102%

Long steel 762kt 690kt -9%

Domestic market 611kt 565kt -8%

Export market 151kt 125kt -17%

Coke & chemicals

Mkt coke 210kt 208kt -1%

Tar 52kt 53kt +2%

Other 488kt 660kt +35%

Safety

H1 2013 H1 2014 % change

LTIFR 0.66 0.54 -18%

Fatalities 0 2 n/a

Value outputs

Socio economic outputs

H1 2013 H1 2014 % change

Socio economic dev R19.8m R8.2m -59%

Procurement spend R12 188m R13 486m +11%

Steelmaking process

Plate

Hot strip mill

Caster

Blast furnace

Electric arc furnace

Billet mill

Raw materials

Coiled rounds

Flats, rails, joists,

rounds, angles,

billets and channels

Flats, reinforced bar,

rounds, angles and

blooms

www.arcelormittalsa.com Overview

6

Strategic imperatives and strategies

• Protecting the health and safety of our employees

• Driving profitability

– Customer focus

– Eliminate excessive raw material costs

– Improve operational efficiencies

– Improve supplier efficiencies

– Optimise our industrial footprint

– Improve energy efficiencies

• Government relations

• Managing our people

• Environmental responsibility

• Engaging with local communities

www.arcelormittalsa.com Overview

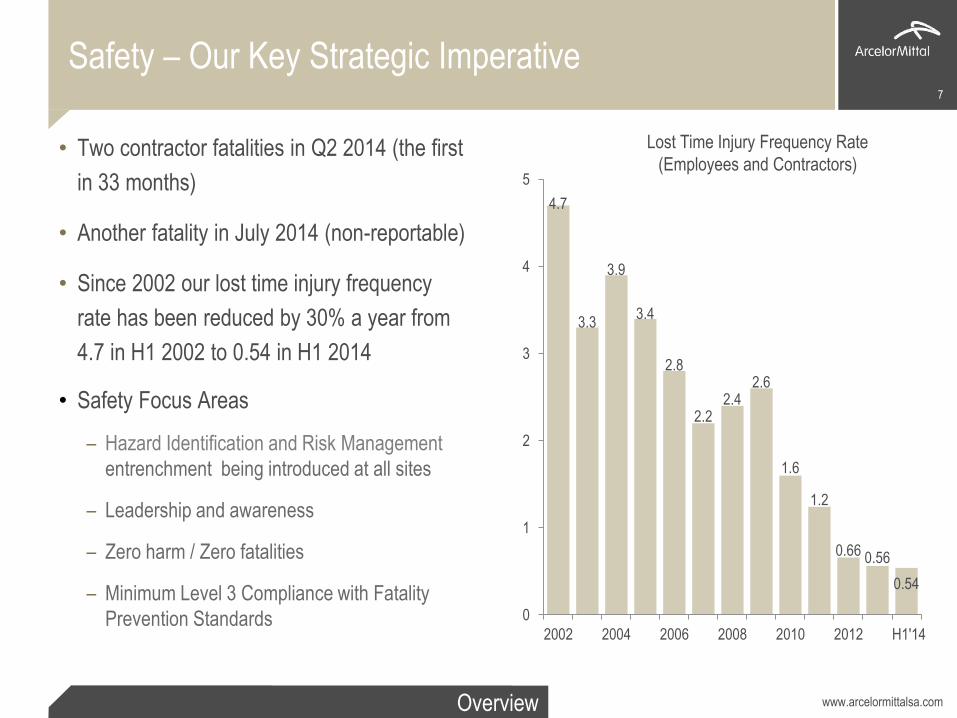

Safety – Our Key Strategic Imperative

• Two contractor fatalities in Q2 2014 (the first

in 33 months)

• Another fatality in July 2014 (non-reportable)

• Since 2002 our lost time injury frequency

rate has been reduced by 30% a year from

4.7 in H1 2002 to 0.54 in H1 2014

• Safety Focus Areas

– Hazard Identification and Risk Management

entrenchment being introduced at all sites

– Leadership and awareness

– Zero harm / Zero fatalities

– Minimum Level 3 Compliance with Fatality

Prevention Standards

7

4.7

3.3

3.9

3.4

2.8

2.2 2.4

2.6

1.6

1.2

0.66 0.56

0.54

0

1

2

3

4

5

2002 2004 2006 2008 2010 2012 H1'14

Lost Time Injury Frequency Rate

(Employees and Contractors)

www.arcelormittalsa.com Overview

8

Environmental investment program

• R1 452m spent on environmental capital since 2007

– Air emission compliance (44%)

– Water management (47%)

– Others such as waste management (9%)

• Rehabilitation of legacy sites remains important

• Energy efficiency

– Investigate alternative suppliers for electricity and gas

– Mitigating options to replace natural gas and/or generate own electricity

www.arcelormittalsa.com Overview

9

Socio Economic activities

• R8.2m (R19.8m) spent

– 100 houses re-roofed in Boipatong bringing the total to 3 000 since 2010

– 10 new homes in Blaaubosch near Newcastle were built by employees bringing the total of

new homes built near our plants to 54 since our volunteering program in 2009

– Grants for NGO’ s mostly involved in health and education related activities and up-skilling at

the North West University around the Vaal area

– Science centers

• 1 500 pupils attend science centers in the Vaal Triangle, Saldanha and Newcastle

• Vanderbijlpark Works recruits graduates from the program with 34 learners already on the

workforce pipeline for various engineering fields

• 500 local communities benefited from computer lessons offered by the centers

• Early childhood development programs offered by the centers

• Signed an MOU for the Newcastle Science Center to assist the Department of Education

with teacher development training

www.arcelormittalsa.com Overview

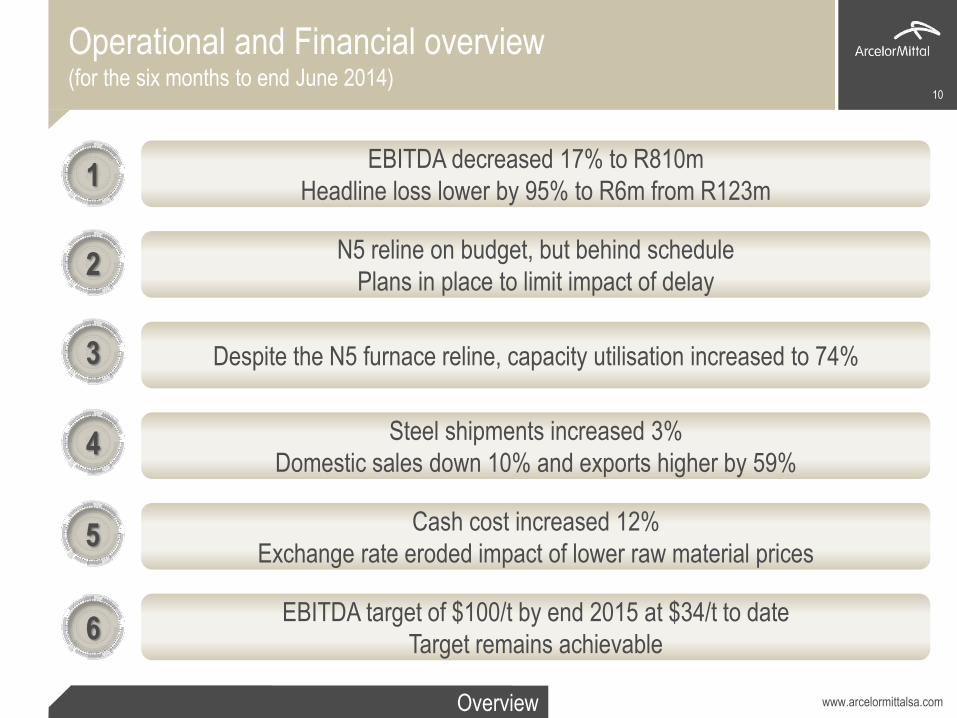

Operational and Financial overview (for the six months to end June 2014)

10

1

2

3

4

6

5

EBITDA decreased 17% to R810m

Headline loss lower by 95% to R6m from R123m

N5 reline on budget, but behind schedule

Plans in place to limit impact of delay

Despite the N5 furnace reline, capacity utilisation increased to 74%

Steel shipments increased 3%

Domestic sales down 10% and exports higher by 59%

Cash cost increased 12%

Exchange rate eroded impact of lower raw material prices

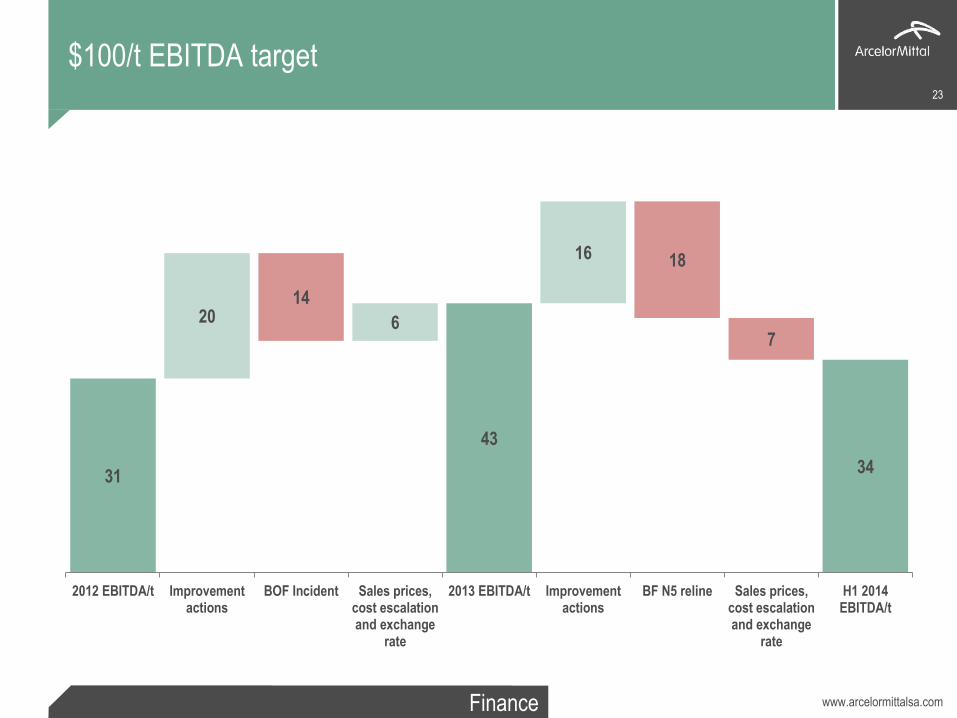

EBITDA target of $100/t by end 2015 at $34/t to date

Target remains achievable

www.arcelormittalsa.com Overview

Key result drivers 11

H1 2013 H1 2014

Flat steel product prices in rand R6 676/t R7 170/t +7%

Long steel product prices in rand R6 818/t R7 382/t +8%

Liquid steel production 2 481kt 2 386kt -4%

Total sales volume 2 123kt 2 195kt +3%

Export sales volume 417kt 661kt +59%

Domestic sales volume 1 706kt 1 534kt -10%

Cash cost per ton liquid steel (Total) R5 983 R6 710 +12%

Fixed R1 377 R1 559 +13%

Variable R4 607 R5 151 +12%

ZAR movement (average rate) R9.22 R10.71 -16%

www.arcelormittalsa.com

Steel market overview Paul O’Flaherty, CEO

12

www.arcelormittalsa.com Steel market overview

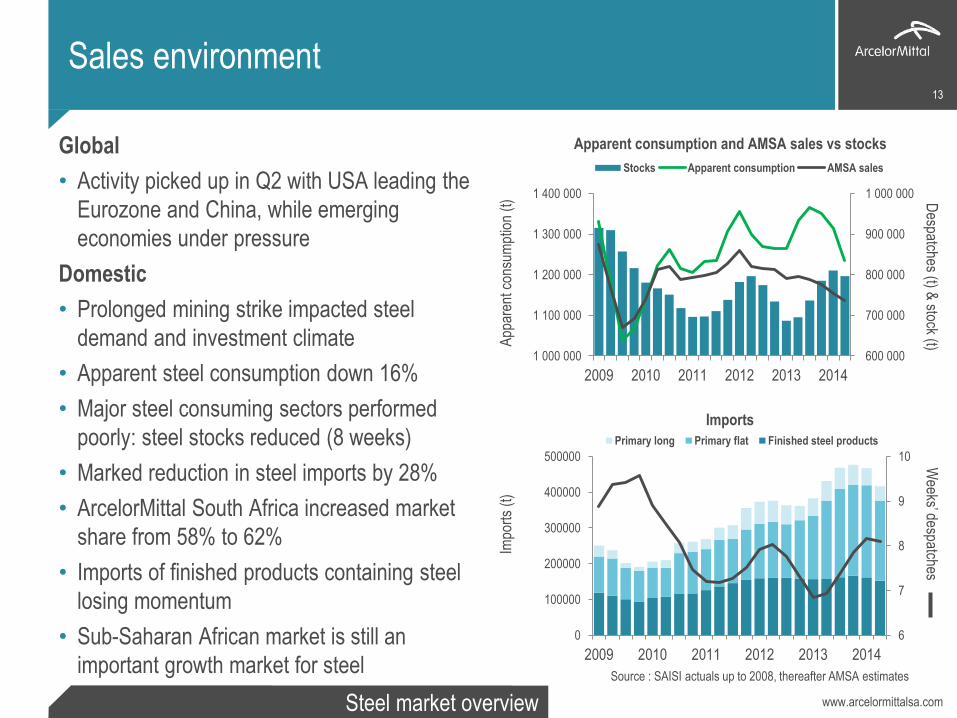

Sales environment

Global

• Activity picked up in Q2 with USA leading the

Eurozone and China, while emerging

economies under pressure

Domestic

• Prolonged mining strike impacted steel

demand and investment climate

• Apparent steel consumption down 16%

• Major steel consuming sectors performed

poorly: steel stocks reduced (8 weeks)

• Marked reduction in steel imports by 28%

• ArcelorMittal South Africa increased market

share from 58% to 62%

• Imports of finished products containing steel

losing momentum

• Sub-Saharan African market is still an

important growth market for steel

13

6

7

8

9

10

0

100000

200000

300000

400000

500000

2009 2010 2011 2012 2013 2014

Primary long Primary flat Finished steel products

Imports

Source : SAISI actuals up to 2008, thereafter AMSA estimates

Weeks’ despatches

Impo

rts

(t)

600 000

700 000

800 000

900 000

1 000 000

1 000 000

1 100 000

1 200 000

1 300 000

1 400 000

2009 2010 2011 2012 2013 2014

Stocks Apparent consumption AMSA sales

Apparent consumption and AMSA sales vs stocks

Despatches (t) &

stock (t) App

aren

t con

sum

ptio

n (t

)

www.arcelormittalsa.com Steel market overview

Raw material price environment

Global

• Iron ore prices decreased from $137/t to $112/t

(record low of $93/t in June 2014)

• Hard coking coal peaked during H1 13 ($154/t) and

decreased in H1 14, while Chinese coke

decreased by 23%

• Excess Chinese capacity and slowing economic

growth to add price pressure

ArcelorMittal South Africa

• Exchange rate absorbed most of the price

weakness

• Iron ore prices exceeded expectations

• Other local price increases continue at above

inflation rates

• Tshikondeni closure at end 2014

• Rail performance improving marginally

14

International H1 2014 Change

Iron ore $112/t -19%

Scrap $371/t -6%

Pellets $128/t -15%

Hard coking coal $117/t -24%

Coke $219/t -23%

Tin $22 915/t +2%

Sources: Platts, AME, AMS and TEX Report

ArcelorMittal

South Africa H1 2014 Change

Iron ore R759/t +14%

Scrap R3 276/t +11%

Pellets R1 510/t +11%

Local coal (AP14) R818/t +8%

Coke R2 655/t +7%

Local met coal R1 423/t -4%

www.arcelormittalsa.com Steel market overview

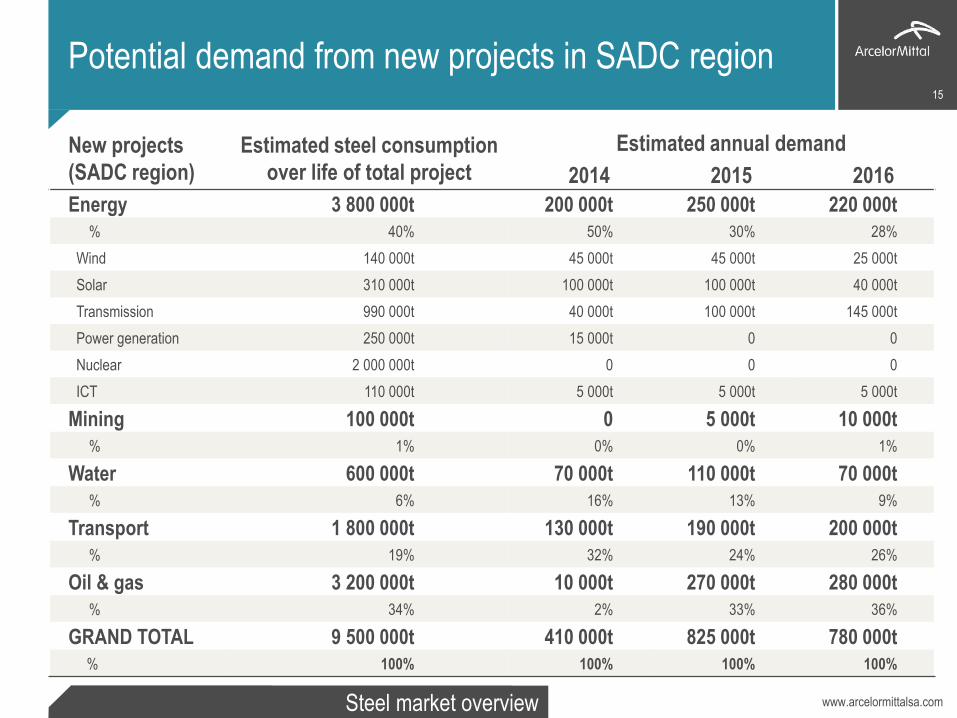

Potential demand from new projects in SADC region 15

New projects

(SADC region)

Estimated steel consumption

over life of total project

Estimated annual demand

2014 2015 2016

Energy 3 800 000t 200 000t 250 000t 220 000t

% 40% 50% 30% 28%

Wind 140 000t 45 000t 45 000t 25 000t

Solar 310 000t 100 000t 100 000t 40 000t

Transmission 990 000t 40 000t 100 000t 145 000t

Power generation 250 000t 15 000t 0 0

Nuclear 2 000 000t 0 0 0

ICT 110 000t 5 000t 5 000t 5 000t

Mining 100 000t 0 5 000t 10 000t

% 1% 0% 0% 1%

Water 600 000t 70 000t 110 000t 70 000t

% 6% 16% 13% 9%

Transport 1 800 000t 130 000t 190 000t 200 000t

% 19% 32% 24% 26%

Oil & gas 3 200 000t 10 000t 270 000t 280 000t

% 34% 2% 33% 36%

GRAND TOTAL 9 500 000t 410 000t 825 000t 780 000t

% 100% 100% 100% 100%

www.arcelormittalsa.com 16

Finance Matthias Wellhausen, CFO

www.arcelormittalsa.com Finance

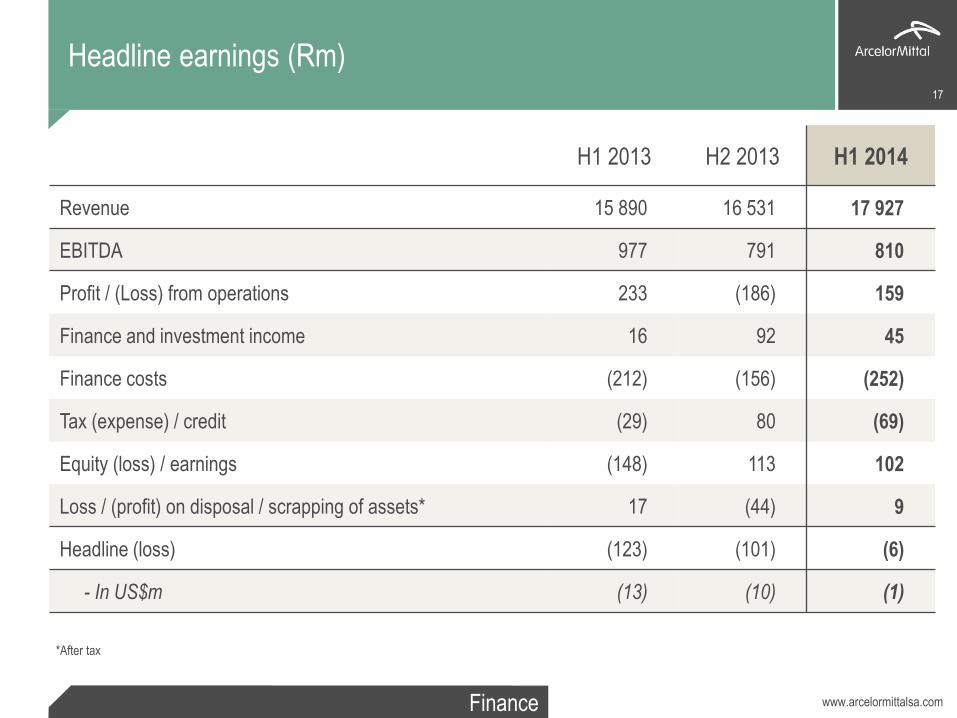

Headline earnings (Rm)

H1 2013 H2 2013 H1 2014

Revenue 15 890 16 531 17 927

EBITDA 977 791 810

Profit / (Loss) from operations 233 (186) 159

Finance and investment income 16 92 45

Finance costs (212) (156) (252)

Tax (expense) / credit (29) 80 (69)

Equity (loss) / earnings (148) 113 102

Loss / (profit) on disposal / scrapping of assets* 17 (44) 9

Headline (loss) (123) (101) (6)

- In US$m (13) (10) (1)

17

*After tax

www.arcelormittalsa.com Finance

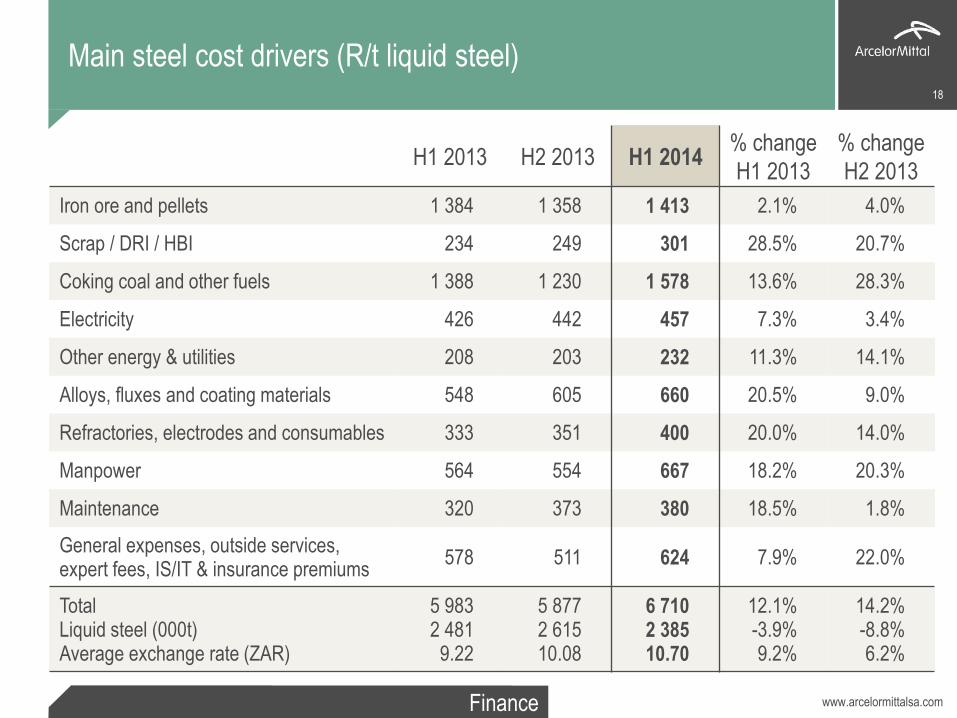

Main steel cost drivers (R/t liquid steel)

H1 2013 H2 2013 H1 2014 % change

H1 2013

% change

H2 2013

Iron ore and pellets 1 384 1 358 1 413 2.1% 4.0%

Scrap / DRI / HBI 234 249 301 28.5% 20.7%

Coking coal and other fuels 1 388 1 230 1 578 13.6% 28.3%

Electricity 426 442 457 7.3% 3.4%

Other energy & utilities 208 203 232 11.3% 14.1%

Alloys, fluxes and coating materials 548 605 660 20.5% 9.0%

Refractories, electrodes and consumables 333 351 400 20.0% 14.0%

Manpower 564 554 667 18.2% 20.3%

Maintenance 320 373 380 18.5% 1.8%

General expenses, outside services, expert fees, IS/IT & insurance premiums

578 511 624 7.9% 22.0%

Total Liquid steel (000t) Average exchange rate (ZAR)

5 983 2 481

9.22

5 877 2 615 10.08

6 710 2 385 10.70

12.1% -3.9% 9.2%

14.2% -8.8% 6.2%

18

www.arcelormittalsa.com Finance

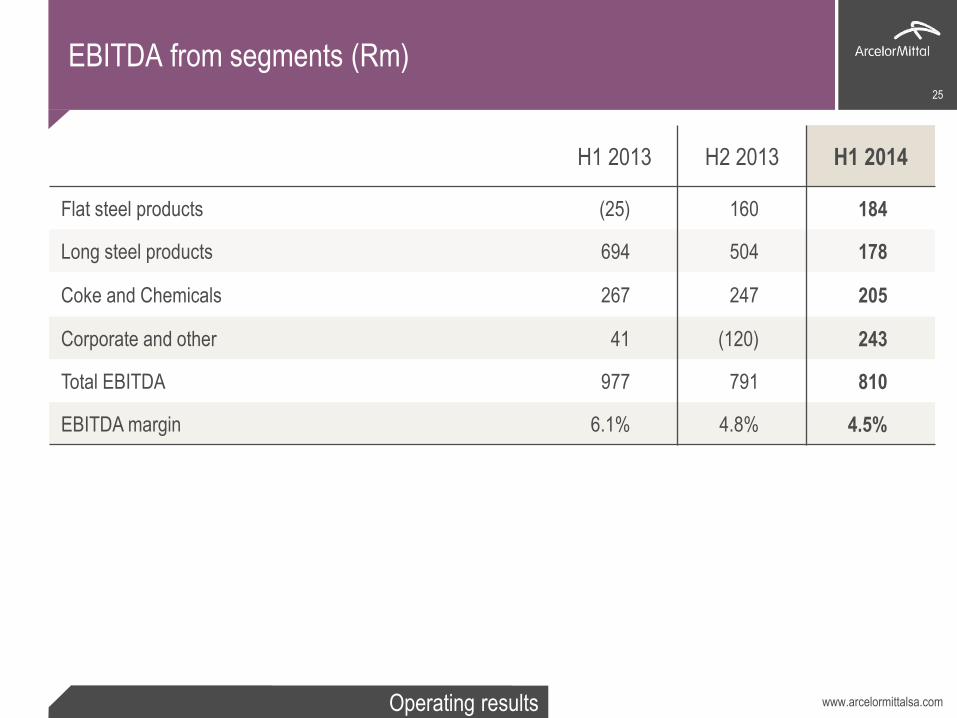

EBITDA from segments (Rm)

H1 2013 H2 2013 H1 2014

Flat steel products (25) 160 184

Long steel products 694 504 178

Coke and Chemicals 267 247 205

Corporate and other 41 (120) 243

Total EBITDA 977 791 810

EBITDA margin 6.1% 4.8% 4.5%

19

www.arcelormittalsa.com Finance

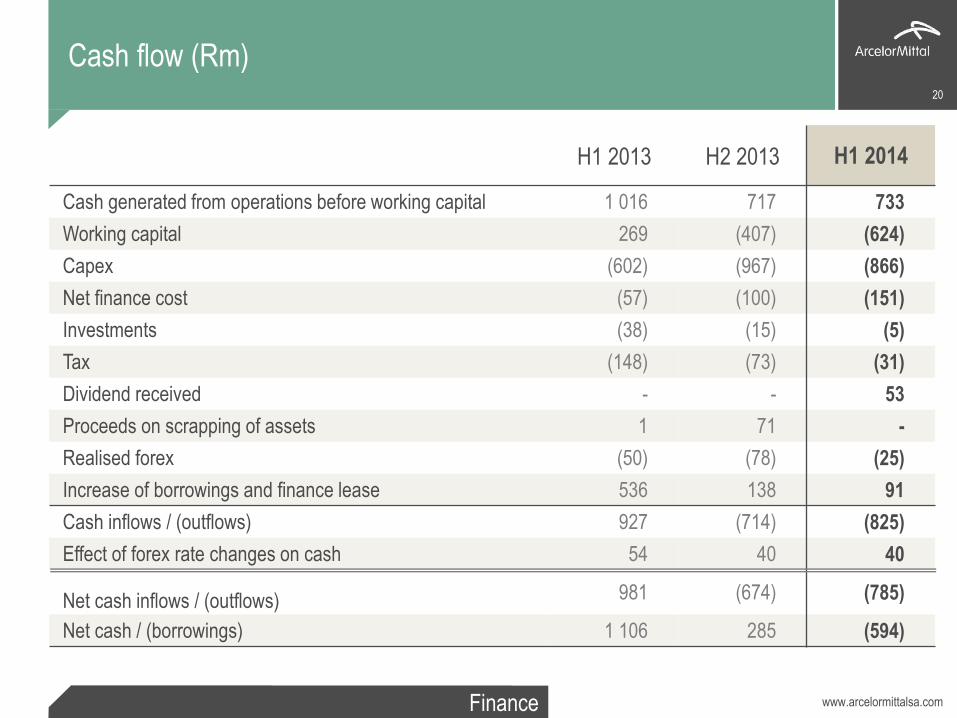

Cash flow (Rm)

H1 2013 H2 2013 H1 2014

Cash generated from operations before working capital 1 016 717 733

Working capital 269 (407) (624)

Capex (602) (967) (866)

Net finance cost (57) (100) (151)

Investments (38) (15) (5)

Tax (148) (73) (31)

Dividend received - - 53

Proceeds on scrapping of assets 1 71 -

Realised forex (50) (78) (25)

Increase of borrowings and finance lease 536 138 91

Cash inflows / (outflows) 927 (714) (825)

Effect of forex rate changes on cash 54 40 40

Net cash inflows / (outflows) 981 (674) (785)

Net cash / (borrowings) 1 106 285 (594)

20

www.arcelormittalsa.com Finance

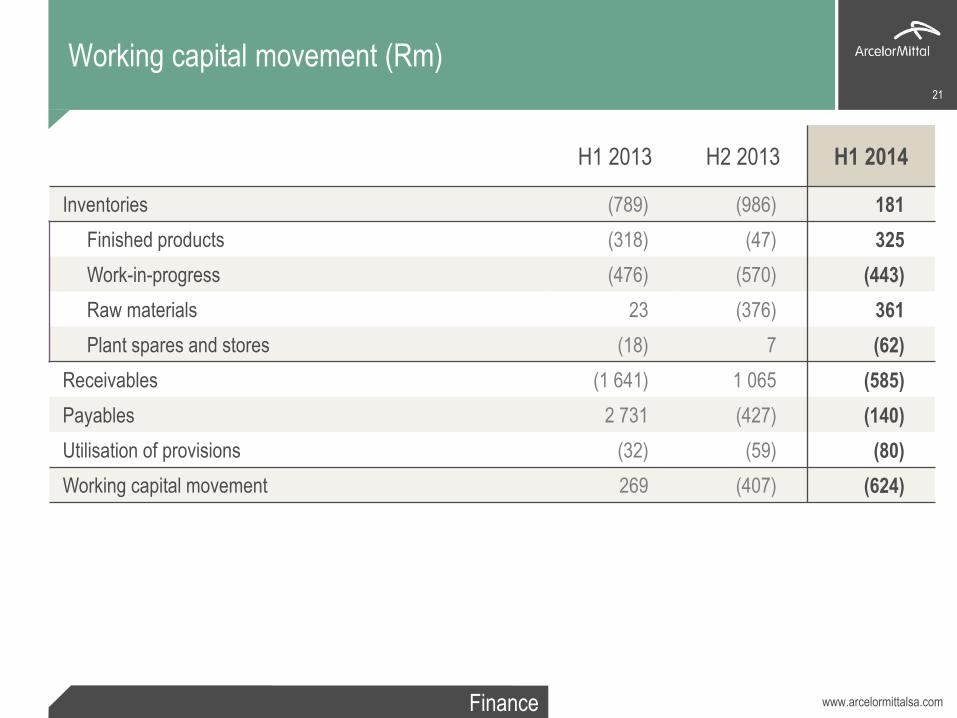

Working capital movement (Rm)

H1 2013 H2 2013 H1 2014

Inventories (789) (986) 181

Finished products (318) (47) 325

Work-in-progress (476) (570) (443)

Raw materials 23 (376) 361

Plant spares and stores (18) 7 (62)

Receivables (1 641) 1 065 (585)

Payables 2 731 (427) (140)

Utilisation of provisions (32) (59) (80)

Working capital movement 269 (407) (624)

21

www.arcelormittalsa.com Finance

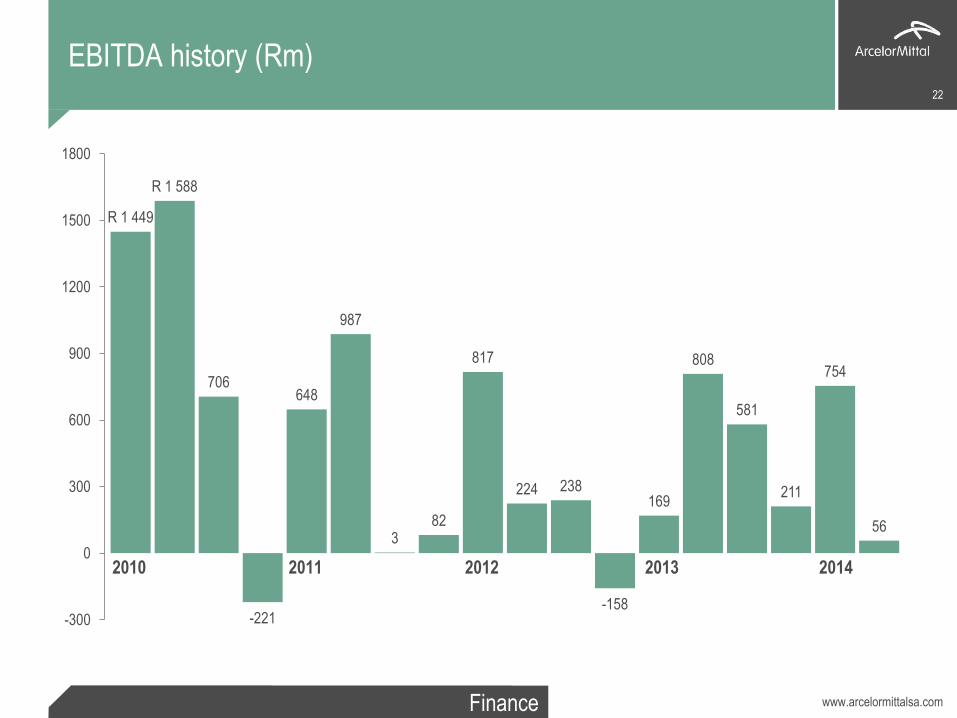

R 1 449

R 1 588

706

-221

648

987

3 82

817

224 238

-158

169

808

581

211

754

56

-300

0

300

600

900

1200

1500

1800

2010 2011 2012 2014 2013

22

EBITDA history (Rm)

www.arcelormittalsa.com Finance

$100/t EBITDA target 23

31

20 14

6

43

16 18

7

34

2012 EBITDA/t Improvementactions

BOF Incident Sales prices,cost escalationand exchange

rate

2013 EBITDA/t Improvementactions

BF N5 reline Sales prices,cost escalationand exchange

rate

H1 2014EBITDA/t

www.arcelormittalsa.com 24

Operating results Hans Ludwig Rosenstock, COO

www.arcelormittalsa.com Operating results

EBITDA from segments (Rm)

H1 2013 H2 2013 H1 2014

Flat steel products (25) 160 184

Long steel products 694 504 178

Coke and Chemicals 267 247 205

Corporate and other 41 (120) 243

Total EBITDA 977 791 810

EBITDA margin 6.1% 4.8% 4.5%

25

www.arcelormittalsa.com Operating results

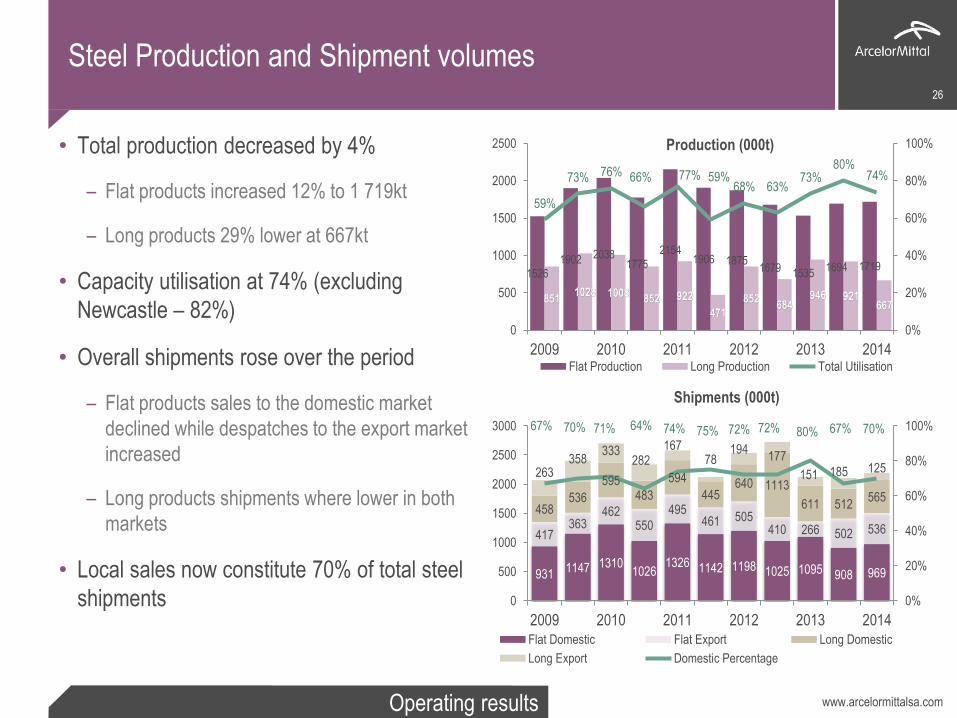

Steel Production and Shipment volumes

• Total production decreased by 4%

– Flat products increased 12% to 1 719kt

– Long products 29% lower at 667kt

• Capacity utilisation at 74% (excluding

Newcastle – 82%)

• Overall shipments rose over the period

– Flat products sales to the domestic market

declined while despatches to the export market

increased

– Long products shipments where lower in both

markets

• Local sales now constitute 70% of total steel

shipments

26

931 1147 1310

1026 1326 1142 1198 1025 1095 908 969

417 363

462 550

495 461 505

410 266 502 536

458 536

595 483

594

445 640 1113

611 512 565

263 358

333 282

167 78

194 177

151 185 125

67% 70% 71% 64% 74% 75% 72% 72% 80% 67% 70%

0%

20%

40%

60%

80%

100%

0

500

1000

1500

2000

2500

3000

2009 2010 2011 2012 2013 2014Flat Domestic Flat Export Long Domestic

Long Export Domestic Percentage

1526

1902 2038 1775

2154 1906 1875

1679 1535 1694 1719

851 1028 1008

852 922

471

852 684

946 921 667

59%

73% 76% 66% 77% 59% 68% 63%

73% 80%

74%

0%

20%

40%

60%

80%

100%

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013 2014Flat Production Long Production Total Utilisation

Production (000t)

Shipments (000t)

www.arcelormittalsa.com Operating results

88

345

309 321

376

255 233 227

210

335

273

50 50 62 63 60 57 56 53 52 57 54

0

100

200

300

400

500

600

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014

Commercial coke Speciality chemicals

Coke price

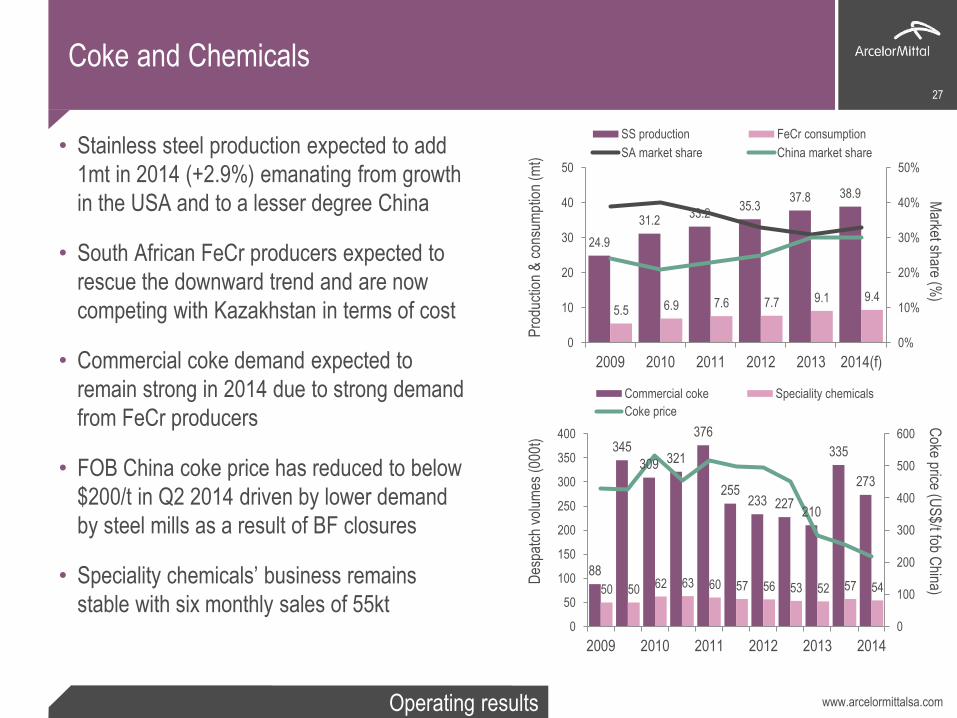

Coke and Chemicals

• Stainless steel production expected to add

1mt in 2014 (+2.9%) emanating from growth

in the USA and to a lesser degree China

• South African FeCr producers expected to

rescue the downward trend and are now

competing with Kazakhstan in terms of cost

• Commercial coke demand expected to

remain strong in 2014 due to strong demand

from FeCr producers

• FOB China coke price has reduced to below

$200/t in Q2 2014 driven by lower demand

by steel mills as a result of BF closures

• Speciality chemicals’ business remains

stable with six monthly sales of 55kt

27

24.9

31.2 33.2

35.3 37.8 38.9

5.5 6.9 7.6 7.7 9.1 9.4

0%

10%

20%

30%

40%

50%

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014(f)

SS production FeCr consumption

SA market share China market share

Pro

duct

ion

& c

onsu

mpt

ion

(mt)

D

espa

tch

volu

mes

(00

0t)

Coke price (U

S$/t fob C

hina) M

arket share (%)

www.arcelormittalsa.com Operating results

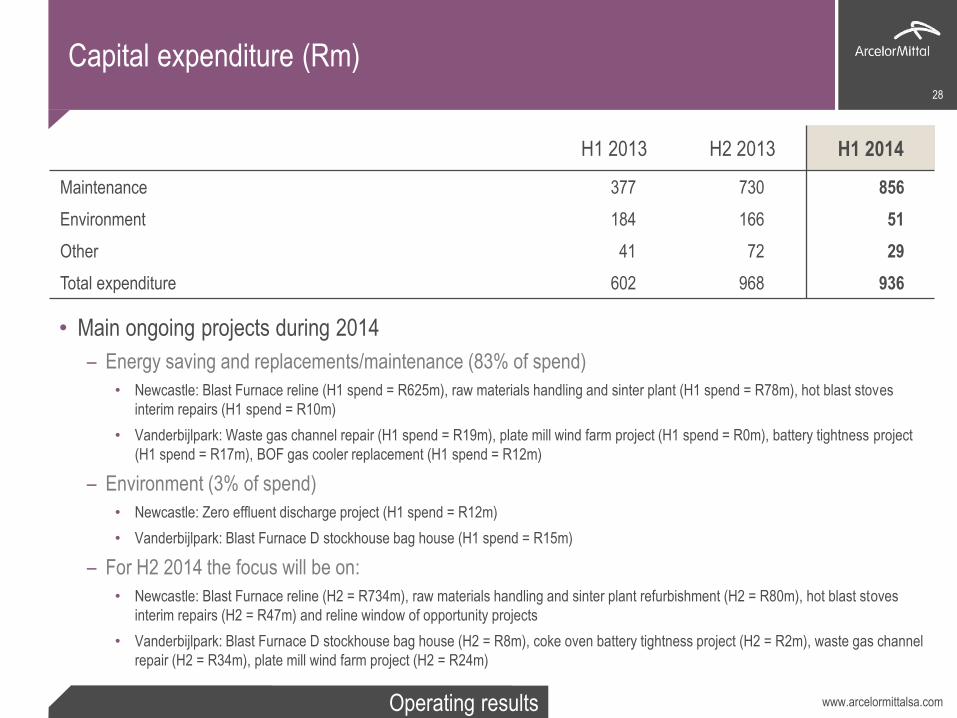

H1 2013 H2 2013 H1 2014

Maintenance 377 730 856

Environment 184 166 51

Other 41 72 29

Total expenditure 602 968 936

28

• Main ongoing projects during 2014

– Energy saving and replacements/maintenance (83% of spend)

• Newcastle: Blast Furnace reline (H1 spend = R625m), raw materials handling and sinter plant (H1 spend = R78m), hot blast stoves

interim repairs (H1 spend = R10m)

• Vanderbijlpark: Waste gas channel repair (H1 spend = R19m), plate mill wind farm project (H1 spend = R0m), battery tightness project

(H1 spend = R17m), BOF gas cooler replacement (H1 spend = R12m)

– Environment (3% of spend)

• Newcastle: Zero effluent discharge project (H1 spend = R12m)

• Vanderbijlpark: Blast Furnace D stockhouse bag house (H1 spend = R15m)

– For H2 2014 the focus will be on:

• Newcastle: Blast Furnace reline (H2 = R734m), raw materials handling and sinter plant refurbishment (H2 = R80m), hot blast stoves

interim repairs (H2 = R47m) and reline window of opportunity projects

• Vanderbijlpark: Blast Furnace D stockhouse bag house (H2 = R8m), coke oven battery tightness project (H2 = R2m), waste gas channel

repair (H2 = R34m), plate mill wind farm project (H2 = R24m)

Capital expenditure (Rm)

www.arcelormittalsa.com Operating results

29

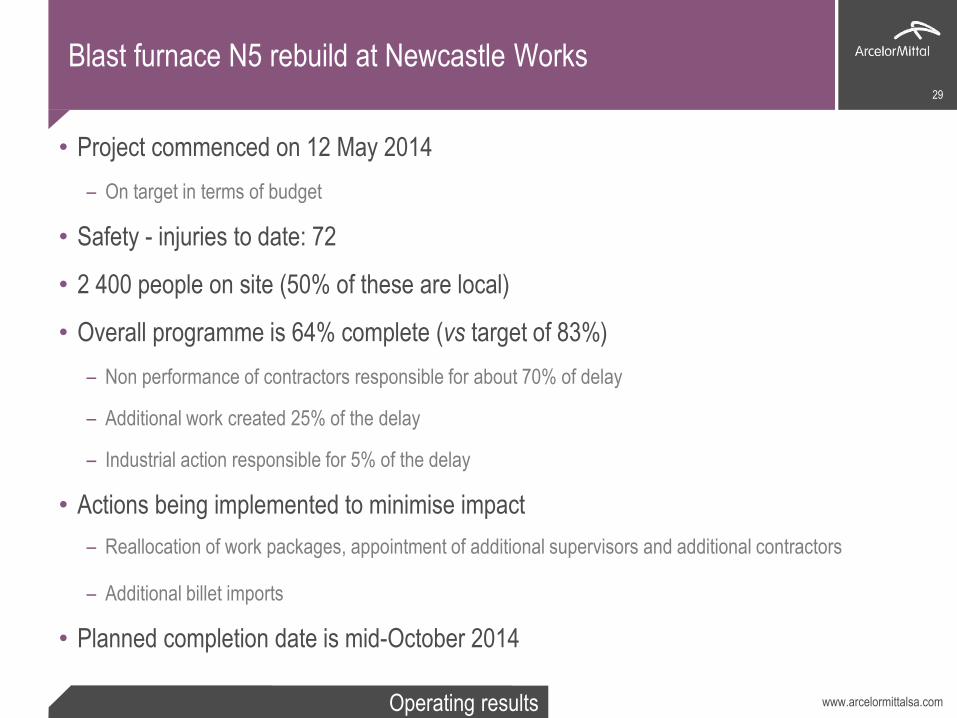

Blast furnace N5 rebuild at Newcastle Works

• Project commenced on 12 May 2014

– On target in terms of budget

• Safety - injuries to date: 72

• 2 400 people on site (50% of these are local)

• Overall programme is 64% complete (vs target of 83%)

– Non performance of contractors responsible for about 70% of delay

– Additional work created 25% of the delay

– Industrial action responsible for 5% of the delay

• Actions being implemented to minimise impact

– Reallocation of work packages, appointment of additional supervisors and additional contractors

– Additional billet imports

• Planned completion date is mid-October 2014

29

www.arcelormittalsa.com Operating results

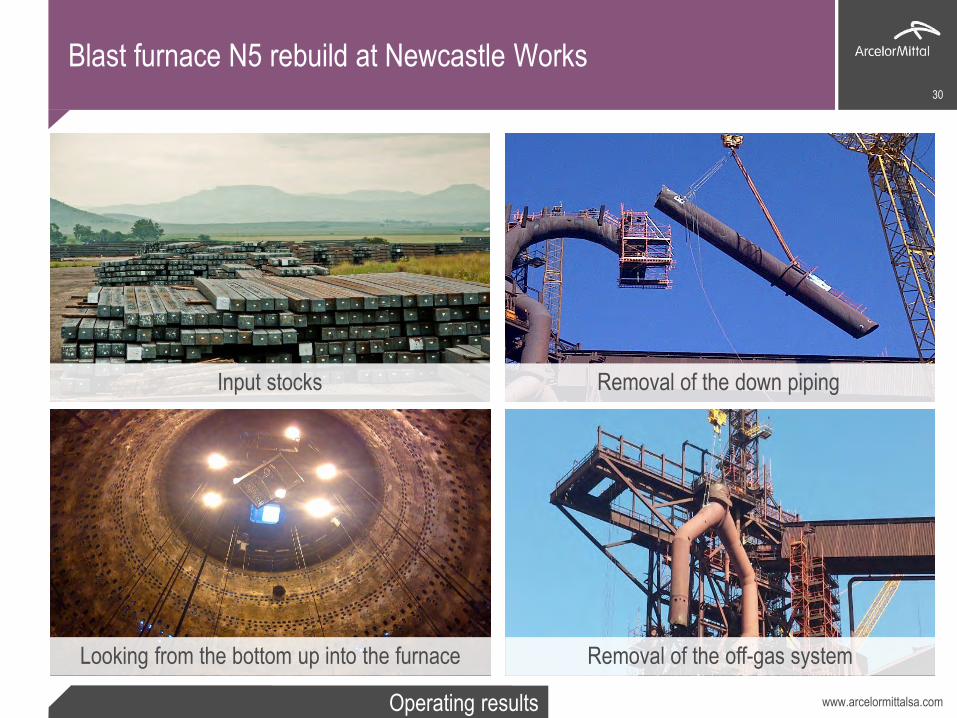

Blast furnace N5 rebuild at Newcastle Works 30

Input stocks

Rebar inventory ready for rolling to customer

specifications

Looking from the bottom up into the furnace

Removal of the down piping

Removal of the off-gas system

www.arcelormittalsa.com Operating results

31

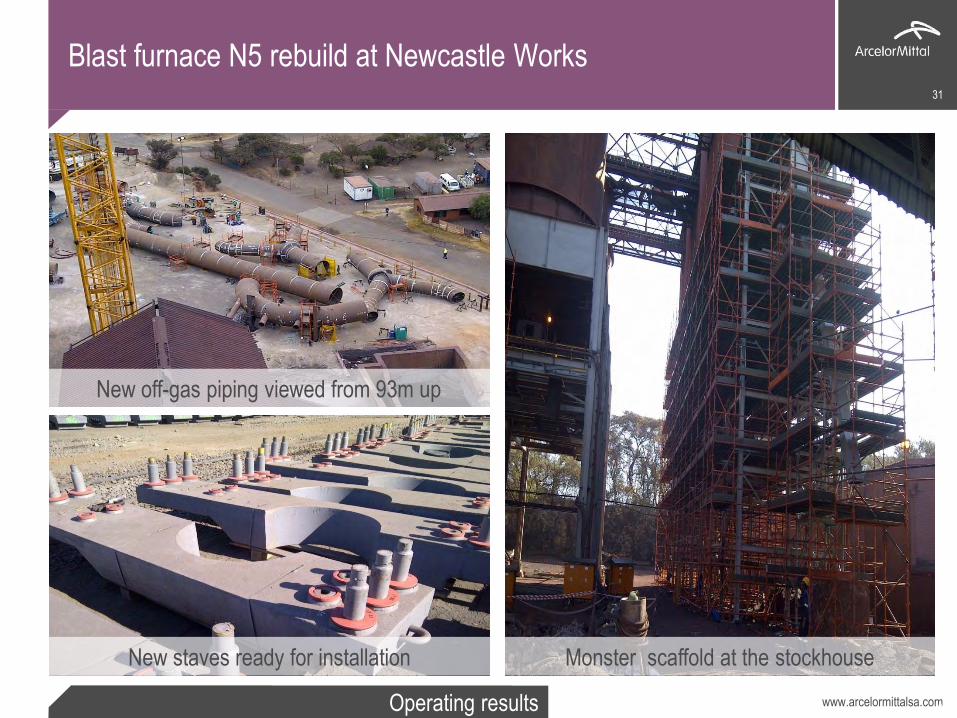

Blast furnace N5 rebuild at Newcastle Works

31

New off-gas piping viewed from 93m up

New staves ready for installation Monster scaffold at the stockhouse

www.arcelormittalsa.com Operating results

32

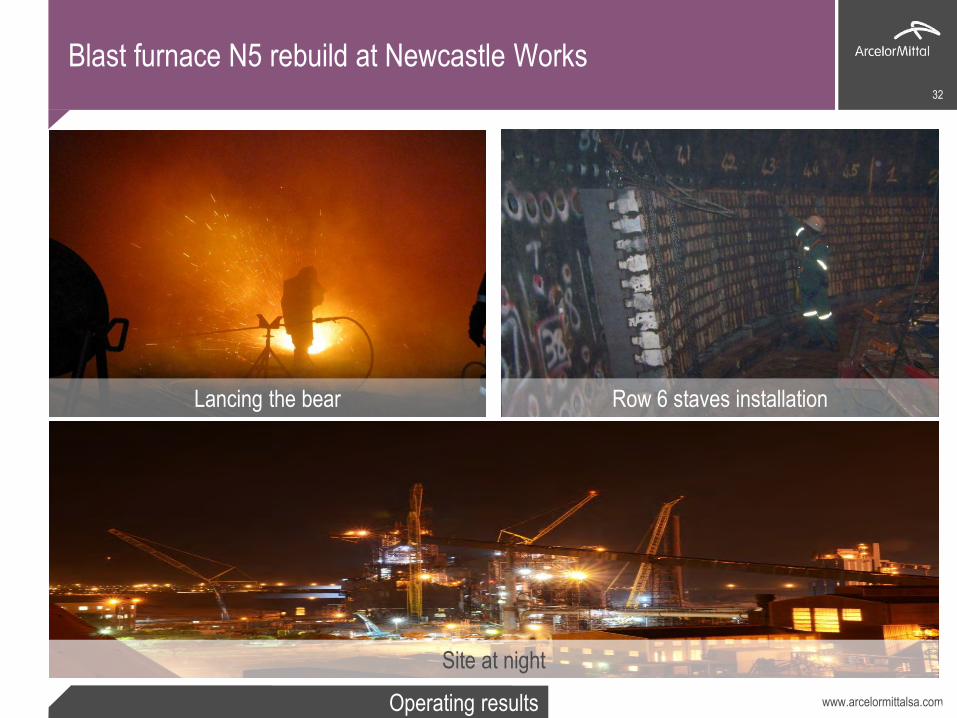

Blast furnace N5 rebuild at Newcastle Works

32

Removal of old hopper

New staves ready for installation

Arrival of a portion of the new cyclone Row 6 staves installation Lancing the bear

Site at night

www.arcelormittalsa.com 33

Other key issues and outlook Paul O’Flaherty, CEO

www.arcelormittalsa.com Other key issues

Focus going forward 34

1 Key strategic objectives and focus areas

Production ramp up at Newcastle post reline

Competition Commission issues

BBBEE compliance

Vanderbijlpark turnaround

Transnet performance

Sales strategy in challenging market

2 Key fundamental decisions by government

Inclusion of steel in localisation - steel now included as designated product

Confirmation of infrastructure as key for future development

Challenge is to align and fulfil BBBEE objectives

www.arcelormittalsa.com Other key issues

Outlook for 3Q 35

1 Outlook for Q3 2014

Electricity winter tariffs applicable this quarter

Domestic economy remain subdued

Seifsa strike a major concern

Reline in full swing for the quarter

Results expected to remain under pressure

www.arcelormittalsa.com

Financial results for the six months ended June 2014

36

Questions