Embed Size (px)

Citation preview

Published in association with:

Deloitte IrelandKPMG SwedenPwC NorwaySteevensz |Beckers Tax LawyersTax Partner – Taxand SwitzerlandWhite & Case

T A X R E F E R E N C E L I B R A R Y N O 1 0 0

Financial Services 2nd edition

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1

5 Latin America | Curaçao fund structuringFund structuring for the LatAm market: The Curaçao fund for mutual accountEmile Steevensz, partner at Steevensz|Beckers Tax Lawyers in Curaçao, provides a guide to fundstructuring in the Caribbean region and assesses the advantages of the Curaçao fund for mutualaccount.

10 Europe | Insurance taxInsurance tax changes loom on the horizonConor Hynes and Ronan Connaughton of Deloitte Ireland explore the impending changes aris-ing from BEPS Action 7 and the Skandia case and provide insight on the potential tax impact forthe insurance industry.

14 Norway | Collective investment fundsCollective investments funds – new tax treatment on the wayOn April 14 2015 the Ministry of Finance issued a public consultation proposal for new rules con-cerning the tax treatment of collective investment funds. Bodil Marie Myklebust, Stian RoskaRevheim and Dag Saltnes of PwC Norway flesh out the proposals as they stand, and look to thelikely future changes that will occur before implementation.

19 Sweden | Insurance taxSwedish insurer taxation: A sector under scrutinyKristofer Brodin of KPMG Sweden explores the insurance and tax regulatory environment, out-lining why those in the wider financial services sector need to keep track of potential incoming taxchanges.

24 Switzerland | Withholding taxPlanned reform of the Swiss withholding taxOn December 17 2014 the Swiss Federal Council published new draft legislation on the reform ofSwiss withholding tax, proposing an exemption for interest payments to non-residents and an exten-sion of the taxable basis for Swiss resident individuals. The draft’s consultation period ended onMarch 31 2015. Alberto Lissi and Monika Gammeter of Tax Partner – Taxand Switzerland outlinethe latest developments.

28 UK | Withholding taxPrivate placement: New withholding tax exemption to stimulate UK marketPeita Menon and Prabhu Narasimhan, partners of White & Case who advised the UK governmentin its creation of a new UK withholding tax exemption for private placements, look at the primarylegislation for the exemption and analyse what the future holds for the UK private placement market.

3 Taxpayer insight | Suspended interestTax issues in the Peruvian Financial SystemRamón Esquives Espinoza, head of tax processes in the management and tax advisory unit ofBBVA’s finance area, takes a look at current points of contention between the Peruvian financialsector and the country’s tax authorities, which relate to suspended interest and the applicableincome tax rate for interest paid to non-residents.

Financial Services

E D I T O R I A L

2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

8 Bouverie StreetLondon EC4Y 8AX UKTel: +44 20 7779 8308Fax: +44 20 7779 8500

Managing editor Ralph [email protected]

Editor Matthew [email protected]

Reporter Joe [email protected]

Managing editor, TPWeek.com Sophie [email protected]

Production editor João [email protected]

Publisher Oliver [email protected]

Associate publisher Andrew [email protected]

Online associate publisher Megan [email protected]

Marketing manager Kendred [email protected]

Marketing executive Sophie [email protected]

Subscriptions manager Nick [email protected]

Account manager James [email protected]

Divisional director Greg Kilminster

© Euromoney Trading Limited, 2015. The copyright of all editorialmatter appearing in this Review is reserved by the publisher. No matter contained herein may be reproduced, duplicated orcopied by any means without the prior consent of the holder of thecopyright, requests for which should be addressed to the publisher.Although Euromoney Trading Limited has made every effort toensure the accuracy of this publication, neither it nor anycontributor can accept any legal responsibility whatsoever forconsequences that may arise from errors or omissions, or anyopinions or advice given. This publication is not a substitute forprofessional advice on specific transactions.

Chairman Richard Ensor

Directors Sir Patrick Sergeant, The Viscount Rothermere,Christopher Fordham (managing director), Neil Osborn, Dan Cohen,John Botts, Colin Jones, Diane Alfano, Jane Wilkinson, MartinMorgan, David Pritchard, Bashar AL-Rehany, Andrew Ballingal,Tristan Hillgarth.

International Tax Review is published 10 times a year byEuromoney Trading Limited.

This publication is not included in the CLA license.

Copying without permission of the publisher is prohibitedISSN 0958-7594

Customer services:+44 20 7779 8610

UK subscription hotline:+44 20 7779 8999

US subscription hotline:+1 800 437 9997

A s part of a continuing focus on the tax issues impacting the asset man-agement industry, International Tax Review brings you the second edi-tion of the Financial Services supplement publication.

Over the past 12 months, when the first edition was published (replacingthe longstanding annual publication on capital markets tax developments),much has happened in the area of financial services taxation. We are nowapproaching the first anniversary of the implementation of the US ForeignAccount Tax Compliance Act (FATCA), for example, and firms are continu-ing to size up their own requirements with a view to increasing complianceand reporting efficiencies on a platform that will stand up in the long term. One trend identified in 2014 – gaining extra revenues from the financial

sector through bank levies – has continued. Some authorities, notably the UKgovernment, have engaged in a touch of mission creep, with 2015 seeing fur-ther gradual hikes to bank levy rates.However, governments may need to resist the temptation to continue

looking at such levies as an easy revenue-raiser, or at least curb rate rises, asthe financial sector begins to kick back. In the UK specifically, where thebank levy rate has been raised eight times since its inception – most recent-ly to 0.21% in the March Budget – HSBC and Standard Chartered areamong those considering the viability of relocating away from the Londonfinancial centre in favour of Asia. After HSBC announced it was undertak-ing a review of its headquarter location, the bank’s share price rose, sug-gesting that shareholders would support a relocation.Progress on the proposed financial transaction tax in Europe (EU FTT)

has stalled, meanwhile, with recent meetings of the 11 participating memberstates characterised by wrangling over revenue collection (both volume andprocesses) and over which trades to tax. However, the rhetoric of PierreMoscovici, European tax commissioner, remains upbeat, so taxpayers shouldexpect further announcements in the coming months.And while relatively new structures and mechanisms like the exchange-

traded fund (ETF) continue to grow, the associated tax and regulatory chal-lenges must not be overlooked. The main tax challenges for ETFs, and otherasset management vehicles, stem from the proposals in the OECD’s BEPSproject, increased investor reporting in general, and the proposed EU FTT. We hope that this guide will help you to effectively manage such chal-

lenges, along with your other financial services tax issues.

Matthew GilleardEditor, International Tax Review

Editorial

T A X PA Y E R I N S I G H T | S U S P E N D E D I N T E R E S T

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 3

Tax issues in the PeruvianFinancial System

Ramón EsquivesEspinoza, head of taxprocesses in themanagement and taxadvisory unit ofBBVA’s finance area,takes a look at currentpoints of contentionbetween the Peruvianfinancial sector and thecountry’s taxauthorities, which relateto suspended interestand the applicableincome tax rate forinterest paid to non-residents.

Suspended interest according to regulatory financial rulesPeruvian financial entities (banks) are required to prepare regulatory finan-cial statements that comply with supervisory authority regulations(Banking Regulations). These rules usually require banks not to recogniseuncollected accrued interest on a loan as income and to reverse any uncol-lected interest previously recognised as income if certain conditions aremet. The most common requirement is that the principal or interest pay-ment is default. Banks characterise any payment received on that non-accrual loan receivable as a recovery of principal, accrued interest andexpenses. According to Banking Regulations, such recovery is acknowl-edged as income. Banks determine taxable income in their regulatoryfinancial statements by using the accrual method of accounting states andfile their income tax returns in the same way.

Since January 1 2008, the Peruvian Tax Law (PTL) has had special reg-ulations for suspended interest, which are determined according toBanking Regulations. According to Legislative Decree N° 979, suspendedinterest is not considered as accrued for tax purposes and should be recog-nised as income when recovered.

The applicable laws do not cast much light on the aforementionedsituation. Banks argue that, for tax purposes, they should apply theaccrual criteria and the method of income recognition stated by theBanking Regulations. However, the tax authority considers that sus-pended interest is accrued when accounting of provision has to bemade. This is the most important tax litigation issue for banks at themoment.

Although it seems to be only a temporary difference, in our case wehave to consider that taxpayers must pay monthly income tax advancepayments during the calendar year and, therefore, banks should considerit all as accrual interest. So, if their income tax returns are filed with alower amount of advance payments, then the tax authority requires inter-ests to be calculated from the omission date until the payment date. Also,the PTL prescribes a penalty for filing tax returns with false information,which is 50% of the omitted advance payment along with the correspon-ding interest.

We have information pending to solve 2011 income tax cases, so thecontingency is huge. The tax authority and the tax court considered thatsuspended interests are accruals for tax purposes, but the judicial branchas a last resort has stated that taxation applies when suspended interestsare recovered.

T A X PA Y E R I N S I G H T | S U S P E N D E D I N T E R E S T

4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Applicable income tax rate for interest paid to non-residentsThe PTL states that interests paid by banks for using their‘lines of credit’ abroad are subject to a 4.99% tax rate andbanks are described as withholding agents for that incometax. However, financial contracts state that the borroweralways pays every applicable tax in their country. Therefore,the PTL considered the tax assumed by banks as deductible.

The PTL does not have a definition for ‘line of credit’, sothe tax authority has interpreted for their audits that, toapply this tax rate, banks should have signed a line of creditcontract agreement with non-resident lenders. The taxauthority has determined that if banks do not have that kindof contract then a 30% tax rate must be applied.

The Peruvian tax authority does not seem to understandthat every bank or equivalent entity has a line of credit withtheir counterparties (the maximum amount that you canborrow). Also the PTL does not mention any line of credit‘contract’ or ‘agreement’, so the term ‘line of credit’ isdefined as a financial term. On the other hand, the acceptedpractice for international loans is not to submit this kind ofagreement because it implies a guarantee of loan for the bor-rower (if the borrower pays an additional fee to the lender).

Also, the line of credit could change at any moment accord-ing to several circumstances, so the lender would not feelmotivated to sign an agreement with a maximum amount tobe borrowed.

Ramón Esquives Espinoza is head oftax processes in the managementand tax advisory unit of BBVA’sFinance area. He is a qualified lawyerfrom the Pontificia UniversidadCatólica del Perú. He is a member ofthe Peruvian Institute of Tax Law(IPDT). He has eight years’ experienceas counselor on tax matters in thePeruvian financial sector, which he

has accumulated while working at both HSBC and BBVA BankPerú. He has experience advising corporate and institutionalcompanies on tax solutions for their business, as well as oncapital markets and financial transactions. He has also served ascounsel on tax procedures with the National Tax Administration,the Municipal Tax Administration and the Judiciary.

L A T I N A M E R I C A | C U R A Ç A O F U N D S T R U C T U R I N G

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 5

Fund structuring for the LatAmmarket: The Curaçao fund formutual accountEmile Steevensz,partner atSteevensz|Beckers TaxLawyers in Curaçao,provides a guide tofund structuring in theCaribbean region andassesses the advantagesof the Curaçao fund formutual account.

I n 2014 the Bahamas introduced the Bahamian investment condomini-um Fund (ICON) as an alternative for non-resident high net worth indi-viduals (HNWIs) and more specifically for Brazilian HNWIs. The

Curaçao fund for mutual account (Fonds voor gemenerekening), however,has many positive features as an alternative to the Bahamian ICON.

Bahamian ICONThe ICON is not a legal entity but a contractual relationship between par-ticipants under which they agree to pool assets for the purpose of collec-tive investment. Despite not being a legal entity, it can hold assets in itsown name, can enter into agreements in its own name and it can sue or besued in its own name.

GovernanceThe ICON is governed by an administrator which, under Bahamian law,must be the fund administrator under the Bahamian Investment FundsAct. The ICON may choose to split the role of the administrator into thatof general administrator and governing administrator. In such a case thegoverning administrator is the operator of the fund. The role of the gov-erning administrator can be compared with a managing director of a com-pany. As such the governing administrator has the power to bind theICON and bears fiduciary responsibility to the participants.

Bahamian tax The ICON is not subject to tax in the Bahamas provided that it does nothold Bahamian assets.

The ICON is not allowed to distribute dividends or profits under theBahamian ICON Act. Profits are distributed when the ICON is dissolvedor the participant chooses to dispose of its interest in the ICON.

Curaçao fund for mutual account (Fonds voor gemenerekening) Contrary to the ICON, the fund for mutual account (Fonds voorgemenerekening, hereafter FGR) does not have a legal basis in the CuraçaoCivil Code. The FGR is, however, a known figure in Curaçao’s Ordinanceon Profit Tax.

Curaçao tax aspects of the FGRThe FGR is defined in the Curaçao Ordinance on Profit Tax as “a fund toobtain benefits for the participants by investing or otherwise using money,

L A T I N A M E R I C A | C U R A Ç A O F U N D S T R U C T U R I N G

6 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

provided that the entitlement of participation appears from cer-tificates of participation that can be transferred”. Participationsin a FGR are not considered freely transferable if:• the participations can only be transferred with the permis-

sion of all other participants; or• the participations can only be repurchased by the FGR or

transferred to relatives in the direct line. In this case it isnot necessary to obtain the permission of the other partic-ipants.For Curaçao tax purposes, the FGR can be tax transparent

or it can be a taxable entity. In case of tax transparency, theFGR needs to be a ‘closed’ FGR (besloten FGR). This meansthat all members have to approve the admittance of newmembers or the resignation of present members or the partic-ipations can only be repurchased by the FGR or transferred torelatives in the direct line.

In case of tax transparency, the profits of the FGR will betaxed at the hand of the members at a rate which is propor-tional to their interest in the FGR. Whether the non-residentparticipants are taxed in Curaçao for their interest depends onwhether the FGR has any Curaçao source income.

Whether the non-resident participants are taxed for theirinterest in the FGR or only upon receipt of income from theFGR depends on the country of residence of the participants.

An open FGR is a taxable entity. It is not explicitly men-tioned in the Ordinance on Profit Tax that the profit of theopen FGR is subject to tax, but from the articles relating tothe special purpose investment company (doelvermogen) it canbe derived that the open FGR is indeed subject to tax. Thespecial purpose investment company can, on request and pro-vided that it meets certain demands, be subject to an effectivetax rate of 10% instead of the normal tax rate of 25%. TheOrdinance on Profit Tax explicitly states that only the openFGR can opt for the lower 10% rate. I therefore conclude thatthe open FGR, like the open partnership, will be subject to25% profit tax if it does not meet the demands for a taxablespecial purpose investment company and does not file therequest to be considered as special purpose investment com-pany.

In order to be considered a special purpose investmentcompany, the FGR must meet the following demands:• The management must keep a register with the names and

addresses of all participants in the FGR;• The management of the FGR consists of an individual res-

ident of Curaçao or a certified fiduciary office in Curaçao;• The purpose of the FGR must be limited to investing in

shares, bonds and deposits, finance and license activities;• The financial statements must include an expert statement;

and• The FGR may not be a bank or financial institution subject

to the supervision of the Central Bank of Curaçao and St.Maarten. Note that an exception is made for investmentfunds which are under the supervision of the Central Bank

of Curaçao and St. Maarten. Note that the above demands are only applicable on a tax-

able FGR that wishes to qualify as a special investment pur-pose company and not for the closed FGR, which is taxtransparent.

The open FGR and closed FGR must not be confused withthe terms ‘closed-end fund’ or ‘open-end fund’. The terms‘open-end’ or ‘closed-end’ determine the extent to which thefund is obligated to repurchase participations in its own capi-tal. As we have seen before, from a tax point of view the terms‘closed fund’ or ‘open fund’ determine that the extent towhich participations can be freely sold and the extent towhich new members can freely join the FGR without theexpress permission of the other participants.

Emile SteevenszPartner Steevensz|Beckers Tax Lawyers

CuraçaoOffice: +599 9 736 05 06Mobile: +599 9 522 29 42Fax: +599 9 736 05 [email protected]

Emile is a tax lawyer and partner with Steevensz|Beckers TaxLawyers in Curaçao. Emile holds a BA in tax law from theAcademy of the Dutch Federation of Tax Advisers and holds anLLM in tax law from the University of Leiden. He started his career with Deloitte in the Netherlands, moving

to Curaçao in 2001. He continued his career at the Curaçaooffice of Loyens & Loeff and, since April 1 2011, he has been atax partner of Steevensz|Beckers Tax Lawyers.Emile is working in the general tax practice with a focus on

international tax structures and international tax planning, privateequity structures, ruling practice, due diligence, aircraft lease,mergers and acquisitions, international trading structures andasset protection. Emile frequently advises high net worth individ-uals and their companies. In his work he frequently representsclients for foreign law offices in Europe, the US and LatinAmerica.Emile is associated as of counsel tax lawyer with Kraaijveld

Coppus Legal, an international tax boutique in Amsterdam, TheNetherlands. Emile is a contributor to the Bloomberg/BNA VAT Monitor for

Curaçao, St. Maarten and the Caribbean Netherlands.Emile has published on Curaçao tax topics in International Tax

Review, the Dutch Caribbean Legal Portal, Tax Notes International,Bloomberg/BNA and International Law Review, among others. Inhis most recent publication in International Tax Review hedescribes the M&A landscape in Curaçao.

L A T I N A M E R I C A | C U R A Ç A O F U N D S T R U C T U R I N G

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 7

Governance and civil law aspects of the FGRThough the FGR is not regulated in the Curaçao Civil Code,the National Ordinance on Supervision Investment Institutionsand Administrators (NOSIIA) recognises that an investmentfund is either an investment company with legal personality(beleggingsmaatschappij) or an investment fund (beleggings-fonds) without legal personality. The NOSIIA defines the fundwithout legal personality as a “non-incorporated capital com-prising pecuniary means or other property raised or obtainedfor collective investment with the objective of allowing the par-ticipants to benefit from the revenues of the investments”. Theexplanatory notes of the NOSIIA do not give any examples ofinvestment funds without legal personality but the definition inthe NOSIIA contains the same elements as the definition of theFGR, that is, investing or using money for mutual account inorder to obtain benefits for the participants. The definition ofthe fund without legal personality does not mention that thefund has a legally separated capital. As the investment fund doesnot have any legal personality it cannot hold any rights orduties. The NOSIIA however provides that in such cases therights and duties are directed at management of the fund.

The investment fund without legal personality is governedby a fund manager (beheerder) and a depositary (bewaarder).

Legally separated capitalAs mentioned above, the investment fund without legal per-sonality does not have a separated capital. However, for theprotection of the participants, the NOSIIA provides for amechanism to separate the capital of the investment fundfrom receivables of participants or third parties and creditorsof the fund.

The capital of the fund must be held by the depositary(bewaarder) to whom it is entrusted and therefore separatedfrom the capital of the fund manager (beheerder) who isentrusted with the management of the fund. The fund man-ager as well as the depositary must be legal entities as a resultof which the capital of the fund is separated from the capitalof the management and depositary. The depositary has a cru-cial role as it is his responsibility to see to it that the fund man-ager acts according the articles of association and regulationsof the fund. The fund manager needs the cooperation of thedepositary and it is therefore important that both the deposi-tary and fund manager are independent from each other.

Is the FGR a partnership?As the FGR is not a legal entity, the question rises whether theFGR is a partnership. The answer to this question is impor-tant as the participants might be held liable in such case.

The Dutch Supreme Court ruled in the Union case that aninvestment fund is a partnership. However this decision doesnot mean that this is always the case.

The agreement under which the FGR is formed is impor-tant. The FGR agreement must be drafted in such a way that

the participants of the FGR are not held obligated towardseach other to make a capital contribution, but are held obli-gated to make a capital contribution towards the fund man-ager or depositary. In such a case there should not exist amutual obligation to make a capital contribution as is the casein a partnership. The ratio or relation between the fund man-ager and depositary and the participants should not be quali-fied as a partnership as the investment fund is managed for theaccount of the participants.

This brings us to the question of whether participants in anFGR that cannot be qualified as a partnership can be heldseverely liable for the obligations of the fund. The liability of theparticipants on a FGR is closely related with the question of wholegally represents the FGR. Usually the fund manager closes thetransactions. But does the fund manager do this in his ownname or in the name of the depositary or on behalf of the fund?

As mentioned, under the rules of the NOSIIA, the capitalof the fund is entrusted to a depositary. The assets and liabil-ities of the fund are in his name. To prevent a situation wherethe participants of the FGR could be held severally liable forthe obligations of the FGR, the transactions for the fund mustbe performed on behalf of the depositary. Transaction profitsand losses fall in the capital of the depositary.

When transactions are performed, it must be disclosed thatthe depositary (or the fund manager on behalf of the deposi-tary) acts with regard to, or concerning (inzake), the FGR inorder to realise that the goods belong the separate capital ofthe FGR and the counterparty can redress his receivable onthe fund. See Example 1. As a result the obligations of theFGR are obligations of the depositary and the participantscannot be held severally liable.

It is not always clear for the counterparty with whom hedeals. Under Curaçao case law it is important to understandwhether it is known to the counterparty that the depositary is

Example 1The depositary opens an investment account with a prime bro-ker in his name but with regard to the FGR. He deposits 100.In connection with pre-financing buy and sell transactions of

stocks, the fund manager has entered into a debt with the primebroker in name of the depositary. The debt is also 100. Theprime broker can redress his receivable of 100 on the depositary.The fund manager enters into a derivate contract with the bro-

ker in name of the depositary with regard to the fund. Under thiscontract the depositary holds a receivable of 50 on the broker.The depositary and the broker can set off 50 against each

other’s debt/receivable. What remains is a receivable of 50 thatthe broker holds on the depositary. The broker can redress the50 on the investment account of the depositary (which has avalue of 100).

L A T I N A M E R I C A | C U R A Ç A O F U N D S T R U C T U R I N G

8 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

appointed as owner by way of management and it is clear tothe counterparty that the depositary acts as depositary withregard to the fund.

To prevent the liability of the participants of the FGR it istherefore essential that:• the depositary becomes the owner of the capital of the

FGR; and• with transaction on behalf of the FGR such transactions are

done by the depositary or by the fund manager on behalf ofthe depositary with regard to the FGR. In such case the depositary is fully liable toward the coun-

terparty.

Cost benefit analysis• The FGR has many similarities with the Bahamian ICON

and can therefore be an interesting alternative fund struc-turing tool for the Latin American market.

• From a Curaçao tax perspective, the closed FGR is taxtransparent if the transferability of the participation isdependent on the approval of all participants or by obligat-ing the FGR to repurchase the certificates of participationsor restrict the transferability to relatives in the direct line, orthe FGR is not tax transparent and becomes subject to tax.

• The participants of the closed FGR are taxed for their inter-est in the closed FGR. Non-resident participants will onlybe subject for Curaçao income tax if the FGR has Curaçaosource income.

• The open FGR is subject to profit tax and on request it canbe qualified as a special purpose investment company(doelvermogen). In such case the profits will be subject toan effective tax rate of 10% provided certain conditions aremet.

• Participations in an open FGR may qualify for the partici-pation exemption rules provided certain conditions aremet.

• The FGR is not a legal entity.• Under the rules of the NOSIIA, the capital of the fund is

legally separated from the receivables from the participantsand creditors of the fund.

• The capital of the fund is entrusted to a depositary whomust be a legal entity and a fund manager who is entrust-ed with the management of the fund. Fund managementand depositary must be separated.

• Though the FGR has many characteristics of a partnership,the agreement of the FGR should be drafted in such a waythat the participants do not have any obligations towardseach other, but have an obligation to contribute capitaltowards the depositary.

• The participants of an FGR are not severally liable for theobligations of the FGR, such as in a partnership, providedthat the depositary becomes the owner of the assets andliabilities of the FGR and the depositary, or the fund man-ager on his behalf, acts with regard to the fund (and noton behalf of the fund).

E U R O P E | I N S U R A N C E T A X

1 0 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Insurance tax changes loomon the horizon

Conor Hynes andRonan Connaughton ofDeloitte Irelandexplore the impendingchanges arising fromBEPS Action 7 and theSkandia case andprovide insight on thepotential tax impact forthe insurance industry.

T he Greek philosopher Heraclitus is attributed with the saying, “theonly thing that is constant is change”. Recent developments in theinternational tax landscape would certainly show the truth of this

statement. Significant changes are afoot in the international tax arena,including developments in the OECD’s base erosion and profit shifting(BEPS) action plans, the EU’s transparency initiatives (including country-by-country reporting), and a renewed impetus among policy makers toimplement an EU financial transaction tax (FTT). In an insurance context, two of the most topical – yet potentially far-

reaching – tax issues facing insurance groups are: the suggested changes tothe definition of what constitutes a permanent establishment (PE) underBEPS Action 7; and the implications of the Court of Justice of theEuropean Union’s (CJEU) judgment in a case involving Skandia AmericaCorporation, which has sought to depart from the well-established princi-ple that intra-entity transactions do not give rise to a supply.

BEPS Action 7: Preventing the artificial avoidance of PE statusThe ambition of the OECD and G20 to reform international taxation hasseen significant progress to date. The initial discussion draft on Action 7 ofthe OECD’s action plan to tackle BEPS contained a variety of proposedoptions dealing with concerns around possible artificial avoidance of PEstatus. The options detailed broadly sought to lower the PE threshold andnarrow the exemptions to PE status contained in article 5 of the OECDModel Tax Convention. While the focus of the initial discussion draftreleased in October 2014 sought primarily to target centralised principalcompany/entrepreneur models, somewhat unexpectedly it also includedspecific proposals targeting perceived permanent establishment issues inthe insurance industry.On May 15, a revised discussion draft on Action 7 was released. This

followed consideration of more than 800 pages of commentary from vari-ous stakeholders on the initial draft, and a subsequent public consultationheld in January in which opinions were expressed on the proposedchanges. In an insurance context, major concerns centred on the need forless ambiguity and subjectivity in the proposals and the likelihood of theproposals increasing compliance costs. Indeed, many questioned why spe-cific proposals were included for the insurance industry and why it hadbeen singled out from other sectors of the economy.Following an analysis of all of the stakeholder input received, the revised

discussion draft selects some of the proposals, and in some instances refines

E U R O P E | I N S U R A N C E T A X

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 1

them, from the alternatives put forward in the initial draft. Itsets out proposed amendments to article 5 of the OECDModel Tax Convention and its associated commentary.While the discussion draft covers many issues, ranging

from fragmentation of activities to specific activity exemptionsand the splitting of contracts, changes to the dependent andindependent agent rules are of particular interest to those inthe insurance industry. The proposals seek to alter the PEthreshold and would be a significant shift in relation to whatconstitutes a taxable presence for insurance enterprises.

PE threshold for insuranceThe initial concern raised was that insurance enterprises mayconduct large scale business in a jurisdiction without having aPE. To date, an insurance enterprise, for example, operatingon an EU cross-border freedom of services basis, without afixed place of business or a dependent agent concluding con-tracts, is not sufficient to constitute a PE.To the relief of many in the industry, the revised discus-

sion draft concludes that insurance should not be singledout for specific proposals (despite such proposals beingincluded in the initial draft). This restores a level playingfield for insurance enterprises vis-à-vis other industry sec-tors, as now all entities are subject to the general changesproposed. In particular, the discussion draft proposes gener-al changes to the rules on dependent and independentagents contained in the OECD Model Tax Conventionwhereby broadly:• Paragraph 5 of article 5 is broadened, extending the ‘con-clude contracts’ threshold to situations where the agent“habitually concludes contracts, or negotiates the materialelements of contracts”; and

• Paragraph 6 of article 5 is strengthened in respect of therequirements for an agent to be considered ‘independent’.In particular, an agent will not be considered independentwhere it acts, “exclusively or almost exclusively for one ormore enterprises to which it is connected”.

ObservationsIf adopted, the proposals could have a substantial tax impacton those insurance entities selling insurance cross-border vialocally based agents and they could therefore result in a sig-nificant compliance burden, particularly in determining areasof uncertainty including by whom, and where, the materialelements of contracts are negotiated.Lowering the PE threshold beyond concluding contracts is

likely to create greater subjectivity in determining whether aPE exists, as the proposed language in Action 7 is open tointerpretation despite a number of examples being included toaid in understanding the new concepts. For example, “negoti-ating the material elements of contracts” would include wherea person acts as the sales force for the non-resident entity andwhere the negotiation of the material elements of the contract

is limited to convincing the account holder to accept standardterms. While some clarification and examples have been provided

on the meaning of the new concepts, this has been includedin the commentary rather than the treaty article itself. As aresult, revenue authorities in different countries may wellinterpret the proposed new language differently, which couldpotentially increase tax risk and tax liabilities for insurancecompanies. Broadening the scope of agents’ activities thatcould give rise to a PE would also likely lead to a greater num-ber of disputes over taxing rights involving tax administra-tions globally. It would also open up the potential forincreased instances of double taxation. Where such proposalsare recommended and adopted, there would clearly be a needfor materially improved dispute resolution mechanisms.

Next stepsComments were invited on the new discussion draft by June12 2015, before final recommendations are made on changesto the OECD Model Tax Convention. In a positive move, theOECD acknowledged that further guidance and examples arerequired in respect of attribution of profit to PEs, with guid-ance to be provided by the end of 2016.The insurance industry will have to pay close attention to

the proposed changes, as the widening of the PE thresholdbeyond ‘concluding contracts’ has the potential to affectexisting operations and raise a number of difficulties, specifi-cally in terms of interpretation of the new concepts put for-ward for inclusion in the revised article 5 of the OECD ModelTax Convention.

Skandia: The impact on VAT groupingThe September 2014 decision of the CJEU in the case ofSkandia America Corp. (USA), filial Sverige v Skatteverket(C-7/13) (Skandia) has left many international groupsreviewing what the potential tax cost could be. The casefocused on whether VAT was self-assessable on services pro-vided by a head office in the US to its Swedish branch, whichwas within a local VAT group. The CJEU concluded that inthe circumstances under consideration VAT was assessable onthose services under the reverse-charge mechanism. The deci-sion reached is of particular relevance to those in the financialservices and insurance sector where irrecoverable VAT can bea significant cost. It has the potential to cause widespread dis-ruption to cross-border structures that are in place for com-mercial reasons across the sector, but which generate VATsavings as a consequence.

Background and the CJEU’s decisionThe Skandia case focused on Skandia America Corporation, aUS-incorporated insurance company with a fixed establish-ment (a branch) in Sweden that was a member of a SwedishVAT group. The head office in the US purchased IT services

E U R O P E | I N S U R A N C E T A X

1 2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

from a third party and made those services available to theSwedish branch in return for a fee. While the Swedish tax authority accepted that transac-

tions between a head office and its branch are not consid-ered ‘supplies’ for VAT purposes (as per the FCE Bank(C-210/04) case), in the case of Skandia the Swedish taxauthority questioned whether the disregard provision hadequal application where the recipient was a member of aSwedish VAT group. In its judgment, the CJEU chose not to follow the opin-

ion issued by the Advocate General and found that:• The Swedish establishment/branch of Skandia AmericaCorporation was, as a result of being a member of aSwedish VAT group, effectively separated from its US headoffice for VAT purposes;

• The Swedish VAT group was a taxable person in its ownright – not directly identifiable with its members, but aseparate person from them; and

• Therefore, there was a difference between the facts inSkandia and the principle that intra-entity transactions donot give rise to a supply as established in FCE Bank.The conclusion reached was that the VAT group was

obliged to account for VAT on a reverse charge basis on thefees recharged to it from the US head office, given that theSwedish branch was found to no longer be part of the sametaxable person as its US head office. The judgment thus pre-sented the prospect of VAT being imposed on services andcost allocations provided on a cross-border basis where eitherthe supplier or recipient is a member of a local VAT grouparrangement.

VAT grouping rules and impact across bordersIn arriving at its judgment, the CJEU did not make referenceto how article 11 of the Principal VAT Directive (Dir.2006/112) on VAT grouping has been interpreted and imple-mented across different EU member states. Two differentapproaches have broadly been taken by member states that havechosen to implement local VAT grouping provisions:• A number of member states have introduced local VATgrouping rules and operate an arrangement whereby onlythe local establishment of the members of the group areregarded as part of the local VAT group (that is, a ‘Swedishstyle’ VAT grouping); and

• Some member states extend VAT grouping to the entire legalentities in the group whereby the local VAT group includesthe foreign establishments of all the entities that are membersof the group (that is, an ‘Irish/UK style’ VAT grouping).Given the divergence in interpretation of the VAT group-

ing rules across the EU, the practical impact of the Skandiadecision will likely be equally divergent. In the UK, HMRC has taken a narrow interpretation of

the Skandia decision, seeking to limit its application. It issuedguidance to the effect that VAT will apply to supplies when aforeign establishment of a UK-established entity is in a for-eign VAT group, only to the extent it is in a member state thathas implemented legislation and practices similar to Sweden’s(that is, in a member state which applies ‘Swedish style’ VATgrouping). Other member states have also moved. For instance,

Belgium has recently become the latest member state toannounce that it will fully uphold and apply the decisionreached in Skandia. The Netherlands, however, in direct contrast has indicated

that it will not apply the Skandia judgment on the basis thatthe Dutch VAT grouping rules differ from the Swedish rules. In an Irish context, Irish Revenue has initiated a consulta-

tion process with existing practice being maintained untilsuch time as the process is complete and new guidance is

Conor HynesPartner, International Tax and FinancialServicesDeloitte Ireland

Tel: +353 (0)1 417 2205Fax: +353 (0)1 417 [email protected]

Conor is a tax partner with Deloitte Ireland with more than 20years’ experience advising clients in financial services and interna-tional tax. He advises on Irish and international taxation issues aris-ing on the location of operations in Ireland and has been involvedin advising on numerous international group reorganisations.He has assisted a number of large insurance companies in

Ireland in relation to Revenue queries and audits. Conor also hasextensive experience in advising on the life taxation regime thatapplies to insurance companies in Ireland and the tax implica-tions for both Irish resident and non-resident policyholders.Conor reviews Irish multinationals to assess the tax risks in

their business and recommends structural changes, including taxplanning for cash utilisation, planning overseas acquisitions, fac-toring, repatriation of profits, financing and structuring outboundoperations. He has provided advice to a number of clients inrelation to inbound and outbound investment and utilising taxplanning opportunities. Conor has presented at a number of seminars on the implica-

tions of BEPS for insurance and financial services companies. Hehas also spoken at international tax conferences on inboundinvestment into Ireland and Irish corporate tax planning, andwritten a number of articles on the taxation of financial servicescompanies in Ireland. He was part of the industry grouping thatnegotiated the drafting of the 2003 securitisation legislation inIreland.

E U R O P E | I N S U R A N C E T A X

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 3

published. While the final outcome remains to be seen, IrishRevenue is likely to be anxious not to be out of step with theUK approach. In light of the divergence in interpretation arising across

member states, the European Commission (EC) recentlypublished a working paper (No 845) setting out its views onthe Skandia judgment, including whether the judgmentapplies in circumstances which differ from the specific facts ofthe case. The EC, in consultation with the VAT Committee,aims to reach a common and consistent position on the con-sequences of the judgment. Interestingly, the Commission’sinitial view appears to call into question the legitimacy ofIrish/UK style VAT grouping and its compatibility with EUlaw. This in turn raises significant questions in respect of thenarrow interpretation of the Skandia case taken by both UKand Dutch tax authorities to date; a narrow interpretationwhich potentially may also be the position Irish Revenue isconsidering on the matter.

Where to now?For insurers, the potential outcomes will vary across jurisdic-tions depending on how Skandia is interpreted in each mem-ber state, the nature of activities being undertaken and theoutcome of the EC’s consultation. In future, insurance com-panies will need to:• Understand the services/cost allocations or charges madebetween different establishments of the same legal entity;

• Analyse VAT recovery methods to ensure the methodadopted takes account of any potential additional inputVAT together with the value of any new supplies recog-nised between establishments within the same legal entity;

• Become more aware of the interpretation of Skandia takenby all member states relevant to existing operations and theresulting VAT rules in respect of previously disregardedsupplies now being recognised; and

• Consider whether maintaining a VAT group remains themost efficient way to structure activities or if alteringunderlying contracts or delivery arrangements could deliv-er VAT savings.It will likely be a considerable time before the full extent of

the ramifications of the Skandia case become apparent andbefore certainty is provided in terms of interpretation in dif-fering member states, particularly in light of the EC’s currentworking paper on the issue. However, what is clear is thatbusinesses will need to better understand their cross-borderintercompany transactions, with a view to ensuring VAT isappropriately charged on these following the outcome of theSkandia case.

Potential changes on the horizonThe proposals under BEPS Action 7 and the judgment hand-ed down in Skandia represent two potentially substantial taxchanges on the horizon for the insurance sector. BEPS Action

7 may result in the redrawing of international rules in relationto when permanent establishments will arise. This raises ques-tions for insurance entities on potential tax exposures thatmay arise as a result of the types of activities being undertak-en across jurisdictions, as well as associated profit attribution.The CJEU decision in Skandia may have profound impactson cross-border arrangements, where such arrangements pre-viously allowed the VAT grouping of branches. What is clear is insurance groups will need to become much

more aware of the potential tax impact of their activities in eachjurisdiction in which they operate. Such groups may need toconsider methods to mitigate any potential unanticipated PErisk and, where VAT grouping of branches has occurred, if nec-essary, how to alter or unwind such cross-border arrangements.While there is still a long way to go before there is certain-

ty on either issue, now is the time for insurance entities toexamine their cross-border activities and to prepare torespond to the likely eventualities of a rapidly changing inter-national tax landscape.

Ronan ConnaughtonManager, International Tax and FinancialServicesDeloitte Ireland

Tel: + 353 1 417 2854Fax: +353 1 417 2300Email: [email protected]

Ronan Connaughton is a tax manager with Deloitte, specialisingin international tax and financial services. Ronan has a numberof years of financial services and international corporate taxexperience and advises a broad range of clients in the insur-ance, reinsurance, securitisation, banking, and investment man-agement sectors. Ronan has extensive experience in advising a range of both

domestic and multinational companies on tax planning aspectsof doing business in Ireland and advising on tax consultingassignments including M&A projects, the restructuring of groupoperations, migrations and inward investments. He also man-ages and co-ordinates the provision of tax services to Irish sub-sidiaries of multinationals and Irish indigenous companies withoverseas operations and has specific experience of working withgeneral and life insurance companies in the provision of taxationconsulting and compliance advice.Ronan is an associate of the Institute of Chartered

Accountants in Ireland and an associate of the Irish TaxationInstitute and also holds a bachelor of arts degree in accountingand finance and a master of business studies degree inaccounting from Dublin City University.

N O R W A Y | C O L L E C T I V E I N V E S T M E N T F U N D S

1 4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Collective investments funds –new tax treatment on the way

On April 14 2015 theNorwegian Ministry ofFinance issued a publicconsultation proposalfor new rulesconcerning the taxtreatment of collectiveinvestment funds.Bodil Marie Myklebust,Stian Roska Revheimand Dag Saltnes ofPwC Norway flesh outthe proposals as theystand, and look to thelikely future changesthat will occur beforeimplementation.

T he background motivation for the proposal is to: prevent tax-motivat-ed adaptions when investing in foreign combination funds (owning atleast one share) which primarily invest in interest bearing securities,

which under existing rules are fully considered as share income and thuscovered by the participation exemption method and the shareholder modelwith various tax benefits; prevent economic double taxation of interestincome for personal unit holders in collective investment funds; and sim-plify the tax rules for collective investment funds.The most important changes are: all collective investment funds will be

taxed according to the same rules; all collective investment funds are cov-ered by the participation exemption method; classification of the unit hold-er’s type of income and tax liability will be determined by the split of shareinterest and interest income in fund; and the total share interest in the fundmust be determined and reported annually.The Ministry proposes that collective investment funds must report the

fund’s share interest annually to the tax authorities. If the share interest isnot reported and the unit holders do not report their share interest, all dis-tributions from the fund will be treated as interest income for the unitholders and currently taxed at 27%.The consultation period is set to end on July 14 2015. The rules are

proposed to enter into force from the fiscal year 2016.

Taxation of the collective investment fundCollective investment funds shall remain as a separate tax subject and shall,as a general rule, follow the tax rules applicable to companies. However, thespecial rule that collective investment funds are exempt from tax on capitalgains and are not entitled to deduct losses on realisation of shares in com-panies domiciled in countries outside the EEA is proposed to be continued. As under current rules for bond funds, distributions of interest income

to the unit holders will be entitled to tax deductions for the fund. The partof the distributions that will be considered as interest income will be cal-culated based on a proportionate rate depending on the ratio between thevalues of the share investments and the other investment in the fund. Today, only share investment funds are covered by the participation

exemption method. The Ministry proposes to change the rules and includeall collective investment funds under the participation exemption method.This means that funds will be able to minimise or avoid tax in the fund

by making sufficient distributions of deductible interest income to the unitholders.

N O R W A Y | C O L L E C T I V E I N V E S T M E N T F U N D S

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 5

Taxation of unit holdersTaxation of unit holders will depend on classification of incomefrom the fund. The classification will be defined as follows:• Distributions from collective investment funds with morethan 90% share interest will be taxed as dividends.

• Distributions from collective investment funds with lessthan 10% share interest will be taxed as interest income.

• Distributions from collective investment funds with a shareinterest between 10% and 90% will be split between divi-dend and interest income calculated on a pro rata basisbased on the share interest in the fund.This means that unit holders mainly will be taxed as if they

had made a direct investment in the same instruments.

Reporting obligationsIt is proposed that the fund must report, on an annual basis,information to the tax authorities that is necessary to deter-mine the portion of share interest in the investment at year-end. If the fund does not file the information, the unit holdermust document the share interest. If sufficient documenta-tion is not filed, the distributions will be taxed as interestincome (at 27%) irrespective of the nature of the distributionfrom the fund. If documentation is only missing for an invest-ment in an underlying fund, that investment will be consid-ered as other securities rather than shares.The Ministry does not specify whether the fund will be able

to deduct distributions reclassified from dividends to interestincome if the reporting duty is not met. It must be assumedthat this will apply, but this should be clarified by the Ministry.

Non-Norwegian investment fundsThe proposed new rules will also apply to foreign investmentfunds, although the tax treatment in many cases will be differ-ent from Norwegian funds as the proposal involvesNorwegian-specific tax rules.This causes various differences and challenges. The foreign

funds will, to a large extent, be exempt from tax liability (forinstance Sweden, Denmark, Ireland and Luxembourg) andthere will therefore not be any tax consequences for the fundas a result of transactions or distributions. This is in contrastto Norwegian collective investment funds with interestincome where distributions to unit holders must be carriedout to prevent taxable income in the fund. Accordingly there will still be a difference between

Norwegian and foreign funds, where the Norwegian fundmust make distributions, while the foreign fund may be accu-mulating also for interest income. This implies that certainforeign funds will retain favourable outcomes compared withNorwegian funds because the taxation of interest income maybe deferred when investing in foreign funds.In regards to the terms of reporting, it might be challenging

to get access to sufficient information and documentation aboutthe split between the funds’ investments in shares and other

securities at the correct time as it will mainly be Norwegian unitholders who are interested in such information.

General tax reforms to come? The Scheel Committee’sreport The Norwegian Ministry of Finance appointed a committeeto assess the Norwegian corporate tax regime and the com-mittee provided its report in late 2014. The report includedseveral proposals for changes. It remains unclear as to whetherthe report will lead to tax reform in Norway but the Ministryof Finance has announced that they are working on propos-ing a tax reform package during the autumn of 2015. The main proposal from the Scheel Committee is to

reduce the corporate income tax rate from 27% to 20%. Tomaintain neutrality to capital gains tax and the general tax rateon net income, the committee also proposes to reduce therate for these incomes to 20% as well. Accordingly the cost ofimplementing such reform is very high and the committeeproposes a high number of tax increases to finance thereduced tax rates mentioned.

Proposed changes to the taxation of cross-border incomefrom sharesThe Scheel Committee proposes important revisions of therules concerning taxation of cross-border income from shares,

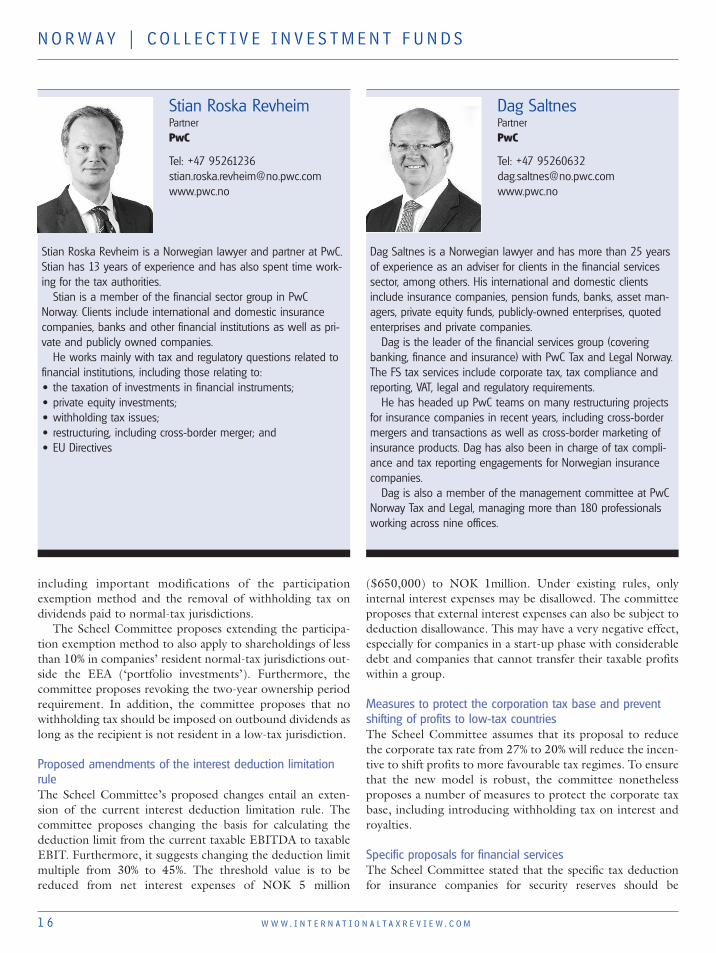

Bodil Marie Myklebust Senior manager PwC

Tel: +47 95261323 [email protected] www.pwc.no

Bodil is a lawyer in PwC Tax and Legal services where she hasbeen employed since she finished law school in 2007.

Bodil is a member of the financial sector group in PwCNorway. Clients include both domestic and international financialinstitutions and private and publicly owned companies.

Bodil is responsible for FATCA advisory services in PwC Norway.She has extensive experience working with national and interna-tional taxation and corporate law questions, including on struc-turing. She also has extensive experience in M&A transactionsboth in terms of assistance with due diligence and preparationof contracts in connection with the transactions.

In addition to her law degree, Bodil holds a master’s degree inaccounting and auditing from NHH and a diploma in internation-al financial law from London.

Bodil has also worked on FATCA projects at PwC in New York.

N O R W A Y | C O L L E C T I V E I N V E S T M E N T F U N D S

1 6 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

including important modifications of the participationexemption method and the removal of withholding tax ondividends paid to normal-tax jurisdictions.The Scheel Committee proposes extending the participa-

tion exemption method to also apply to shareholdings of lessthan 10% in companies’ resident normal-tax jurisdictions out-side the EEA (‘portfolio investments’). Furthermore, thecommittee proposes revoking the two-year ownership periodrequirement. In addition, the committee proposes that nowithholding tax should be imposed on outbound dividends aslong as the recipient is not resident in a low-tax jurisdiction.

Proposed amendments of the interest deduction limitationruleThe Scheel Committee’s proposed changes entail an exten-sion of the current interest deduction limitation rule. Thecommittee proposes changing the basis for calculating thededuction limit from the current taxable EBITDA to taxableEBIT. Furthermore, it suggests changing the deduction limitmultiple from 30% to 45%. The threshold value is to bereduced from net interest expenses of NOK 5 million

($650,000) to NOK 1million. Under existing rules, onlyinternal interest expenses may be disallowed. The committeeproposes that external interest expenses can also be subject todeduction disallowance. This may have a very negative effect,especially for companies in a start-up phase with considerabledebt and companies that cannot transfer their taxable profitswithin a group.

Measures to protect the corporation tax base and preventshifting of profits to low-tax countriesThe Scheel Committee assumes that its proposal to reducethe corporate tax rate from 27% to 20% will reduce the incen-tive to shift profits to more favourable tax regimes. To ensurethat the new model is robust, the committee nonethelessproposes a number of measures to protect the corporate taxbase, including introducing withholding tax on interest androyalties.

Specific proposals for financial servicesThe Scheel Committee stated that the specific tax deductionfor insurance companies for security reserves should be

Stian Roska Revheim Partner PwC

Tel: +47 95261236 [email protected] www.pwc.no

Stian Roska Revheim is a Norwegian lawyer and partner at PwC.Stian has 13 years of experience and has also spent time work-ing for the tax authorities.

Stian is a member of the financial sector group in PwCNorway. Clients include international and domestic insurancecompanies, banks and other financial institutions as well as pri-vate and publicly owned companies.

He works mainly with tax and regulatory questions related tofinancial institutions, including those relating to: • the taxation of investments in financial instruments; • private equity investments; • withholding tax issues; • restructuring, including cross-border merger; and • EU Directives

Dag SaltnesPartner PwC

Tel: +47 95260632 [email protected] www.pwc.no

Dag Saltnes is a Norwegian lawyer and has more than 25 yearsof experience as an adviser for clients in the financial servicessector, among others. His international and domestic clientsinclude insurance companies, pension funds, banks, asset man-agers, private equity funds, publicly-owned enterprises, quotedenterprises and private companies.

Dag is the leader of the financial services group (coveringbanking, finance and insurance) with PwC Tax and Legal Norway.The FS tax services include corporate tax, tax compliance andreporting, VAT, legal and regulatory requirements.

He has headed up PwC teams on many restructuring projectsfor insurance companies in recent years, including cross-bordermergers and transactions as well as cross-border marketing ofinsurance products. Dag has also been in charge of tax compli-ance and tax reporting engagements for Norwegian insurancecompanies.

Dag is also a member of the management committee at PwCNorway Tax and Legal, managing more than 180 professionalsworking across nine offices.

N O R W A Y | C O L L E C T I V E I N V E S T M E N T F U N D S

1 8 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

assessed. The Ministry of Finance has reacted on this andissued a public consultation process, which is addressed below.The Scheel Committee has proposed to impose VAT on

non-interest income. The rate is not explicitly mentioned.Additionally the committee suggests imposing a specific

duty on interest margin. The duty is technically quite similarto a VAT.

Tax on asset management activities (carried interest)So-called carried interest payments are an issue that has beenbrought before the courts in Norway. Borgarting High Courthas decided that (part of) the carried interest payments in thecase in question were to be considered as personal income forthe principal employers. Hence, the taxation was quite exten-sive. The decision has been appeled to the Supreme Court,which has decided to admit the case to be heard.Further, with regard to fund structures and whether or not

a fund is to be considered as a foreign partnership, theNorwegian Tax Directorate has issued a statement that a fundset up with a general partner (GP) having less than 1% own-ership can be regarded as a partnership under the NorwegianTax Act. Previously, the Norwegian Tax Authorities held thegeneral view that a fund where the GP has less than 1% own-ership is not to be considered as a partnership underNorwegian law. The Tax Directorate now states that there arethree main conditions for being considered as a partnership: • The fund must have an economic activity;• The economic activity must be carried out for two or morepartners with common account and risk; and

• At least one partner must have an unlimited liability for thefunds obligations.

Proposed changes in the Norwegian Tax Act due toSolvency II – tax increase for insurance companies On May 21 2015, the Norwegian Ministry of Finance issueda proposal for changing the Norwegian Tax Act section 8-5with regard to the right to deduct security reserves for insur-ance companies. The changes are proposed due to the EU’sSolvency II Directive, which will come into force from 2016to harmonise EU insurance regulation. The Ministry ofFinance proposes to change the tax regulation to be in linewith the Solvency II regulation allowing tax deductions limit-ed to the technical reserves. According to the current tax regulation, insurance compa-

nies can deduct all security reserves that the company consid-ers ‘necessary’. The proposed regulation suggests that onlysecurity reserves that are in line with the technical reservesunder Solvency II shall be deductible for tax purposes. Accordingly, previously deducted reserves exceeding the

security reserves under Solvency II have to be recognised astaxable income at the hand of the insurance company at thetime Solvency II is put into force in 2016. No transitional ruleis proposed. Consequently, insurance companies holding highsecurity reserves will receive a tax bill for the income year2016. There is still scope for the tax regulation to be put intoforce in a manner other than that which has already been pro-posed, because the deadline for presenting comments underthe consulting process is not until July 2 2015.

S W E D E N | I N S U R A N C E T A X

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 9

Swedish insurer taxation:A sector under scrutiny

Kristofer Brodin ofKPMG Swedenexplores the insuranceand tax regulatoryenvironment, outliningwhy those in the widerfinancial services sectorneed to keep track ofpotential incoming taxchanges.

I n Sweden, companies in the financial services sector are generally taxedas ordinary corporations under the Income Tax Act (ITA), but there are,nevertheless, limited special rules and regimes that apply to the sector.

The main exceptions for the financial services sector concern the insuranceindustry, which has special rules for life as well as non-life insurance. Thisarticle aims at providing a general overview of the Swedish tax regime forinsurance companies of both kinds. The article is only intended as an intro-duction to the Swedish taxation of ongoing insurance business. Issueswhen commencing or winding-down insurance business are not discussed.

Corporate income taxFirst, a distinction should be made between the taxation of life insurancebusiness and non-life insurance business (general/property and casualtyinsurance). While the former generally is subject to notional yield taxation,the latter is subject to ordinary income taxation – with certain exceptions.

Life insuranceFor corporate income tax purposes, income attributable to assets and lia-bilities managed on behalf of policyholders and premiums should not berecognised under the ITA if the policy is a life insurance policy under theInsurance Business Act (försäkringsrörelselagen) (IBA). Certain exceptionsexist, however, for group-life policies, for example.

Any cost related to income attributable to assets and liabilities managedon behalf of policyholders and premiums is non-deductible under the ITA.For policies qualifying as life insurance for this purpose, the insurer isinstead taxed on a notional yield under the Yield Tax Act (lag om avkast-ningsskatt på pensionsmedel m.m.) (YTA).

The yield tax is calculated on the basis of assets managed on behalf ofthe relevant policyholders at year entry less certain financial liabilities (thecapital base). The YTA provides different valuation methods for differenttypes of assets. For life policies other than pension policies, premiumsreceived during the year are also included in the tax base (50% of premi-ums received in the second half of the year).

The capital base multiplied by the Swedish ‘government borrowingrate’ (the average interest rate on government bonds with a remainingmaturity of at least five years) equals the taxable notional yield and thus thetax base. Notably, the government borrowing rate as well as the tax rate tobe applied differ between policies considered pension policies for tax pur-poses and other life policies. A tax rate of 15% applies to pension policies.

S W E D E N | I N S U R A N C E T A X

2 0 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

For other life policies, such as unit-linked endowment poli-cies, the applicable tax rate is 30%.

Non-life insuranceFor non-life insurance, most items of income and expenditurefollow the ITA’s general corporate income tax rules. Thismeans that the timing for recognition of income and expen-diture normally follows Swedish generally accepted account-ing principles (GAAP).

With the exception of shares in subsidiaries and associatedcompanies and office properties mainly used for the insurancebusiness, investment assets are treated as stock (current assets)for tax purposes. Investment assets considered financialinstruments for tax purposes may be valued at either marketvalue or total acquisition cost on a collective basis and otherinvestment assets may be valued at the lowest of net sales priceand cost on an item-per-item basis for tax purposes.

Insurers offering non-life insurance are allowed specialdeductions, including deduction for provisions to technicalreserves for own account and contingency reserves. The term‘technical reserves for own account’ in the ITA refers to tech-nical reserves under the Annual Accounts for Insurers Act(lag om årsredovisning i försäkringsföretag) less the value ofreinsurers’ responsibility. The contingency reserve is discussedin more detail below as this may be considered a distinctivefeature of Swedish insurance and tax regulation.

Moreover, deduction is granted for bonuses paid to policy-holders (återbäring), premiums and fees repaid and contribu-tions to parties supporting undertakings to prevent damageswithin the area of risks insured.

The contingency reserveUnder the ITA’s definition, the ‘contingency reserve’ (säker-hetsreserv) is a reserve for arbitrary, random or otherwiseimponderable losses in the insurance operations to the extentthe reserve does not exceed what is necessary for satisfactoryconsolidation. The purpose of the contingency reserve is thata Swedish insurer should have sufficient capital for its businessoperations. The guiding principle of the Swedish FinancialSupervisory Authority’s (SFSA) regulations on allocation tothe contingency reserve is that a Swedish insurer should beable to sustain heavy losses in two consecutive years.

The contingency reserve is recognised as an untaxedreserve in the balance sheet of the insurer. Allocations to andfrom the reserve are recognised in the income statementunder Swedish GAAP. The maximum allocation to the con-tingency reserve is governed by regulations issued by theSFSA.

The standard calculation of the maximum allocation to thecontingency reserve allowed at year-end is based on formulasspecific to each class of insurance business. For instance, theformula for commercial property and casualty insurance is50% of retained premiums plus 20% of the claims reserve for

own account. As an alternative, the insurer or reinsurer maymake a contingency reserve allocation that equals either threetimes the highest retained individual risk or a hundred timesthe ‘price base amount’ (prisbasbeloppet – the price baseamount for 2015 is SEK 44,500 ($5,500), so the limit equalsSEK 4,450,000, around $537,000).

For insurers allowed to exchange tax deductible groupcontributions (koncernbidrag, the Swedish method for taxconsolidation), the sum of the group members’ contingencyreserves may not exceed the sum of contingency reserves ifcalculated individually per insurer. The group’s total contin-gency reserve capacity may thus be allocated freely betweengroup members taxable in Sweden.

Insurers with mixed businessIf a life insurer offers non-life insurance policies, the same taxrules generally apply for that part of the business as for non-lifeinsurance companies. Nevertheless, as for contingencyreserves, it should be stressed that life insurers are not allowedto make allocations under the SFSA’s regulations as it is explic-itly stated that these apply to non-life insurers. Additionally,any item of income or expenditure shared between businessessubject to corporate income tax and business subject to yieldtax should be allocated in a reasonable way. Precedents fromthe Supreme Administrative Court on the issue of what can beregarded as ‘reasonable’ in this context exist.

Indirect taxesAs in all EU member states, the supply of insurance policies isexempt from VAT in Sweden. This entails a restriction oninsurers’ right to recover input VAT on goods and servicespurchased from third parties. Notably, services provided tocustomers outside the EU, however, give right to input VATrecovery. Sweden currently has VAT grouping rules, which iswhy intra-group supplies may be made outside of the scope ofVAT.

Sweden only applies insurance premium tax (IPT) to cer-tain group life policies and to motor vehicle insurance, whichrenders IPT, generally, a limited issue in Sweden.

Recently proposed changesContingency reserve for non-life insurersOn June 12 2014, the Swedish Committee on CorporateTaxation published its Swedish Government Official Report –‘Neutral corporate taxation’. The amendments proposedinclude the introduction of a taxable notional interest incomecomputed on the year entry balance of non-life insurers’ con-tingency reserves. In the committee’s view, the contingencyreserve is seemingly comparable to the general tax equalisa-tion reserve (periodiseringsfond), which already is subject to ataxable notional interest income supposed to compensate forthe ‘tax credit’ received by postponing corporate income tax-ation. This proposal was severely criticised by the sector as the

S W E D E N | I N S U R A N C E T A X

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 2 1

purpose of the contingency reserve is not to provide taxequalisation but to ensure sufficient consolidation amonginsurers.

On April 28 2015, the government proposed new tax ruleson when a release of the contingency reserve is mandatory.The new rules are intended to apply in situations not coveredby the SFSA’s regulations and may generally be considered acodification of what already applies but is not yet expressed inlaw. In its proposal, the Swedish government again underlinesthe similarities between the contingency reserve and the gen-eral tax equalisation reserve. The main difference in this pro-posal, however, is that the government included a wording onthe purpose of the contingency reserve showing that it hastaken some notice of the feedback received on the officialreport from June 2014.

Taxation of life insurersA government committee tasked with reviewing tax issuesrelating to occupational pensions is due to publish its officialreport on June 30 2015. The committee’s terms of referenceinclude reviewing whether the existing dividing line thatapplies to life insurance business’ items of income and expen-diture subject to corporate tax vis-à-vis yield tax is appropri-ate. If not considered appropriate, the committee shouldsuggest amendments to the regime. The extent to whichchanges might be deemed necessary by the committee isimpossible to predict. It is, however, clear that the issue is verycomplex and will need in-depth analysis.

Financial services sector taxOn May 8 2015, the Swedish government published terms ofreference for an inquiry chairperson on financial services sec-tor taxation. The inquiry chairperson is tasked with present-ing a proposal for a financial services sector tax whichmitigates the sector’s supposed tax advantage. The proposalshould be presented no later than November 1 2016.

Under the terms of reference, the inquiry chairperson istasked with quantifying the size of any tax advantage for thesector due to financial services being VAT exempt. Based onthat quantification, the inquiry chairperson should suggest afinancial services sector tax which mitigates the tax advantageidentified. The terms of reference do not stipulate the exactdesign of the tax and the inquiry chairperson may, for instance,seek some guidance from the Danish lønsumsafgift, a payroll-based financial activity tax (FAT). Nevertheless, the terms ofreference do require that the tax be easy to apply and impossi-ble to circumvent. When designing the tax, the inquiry chair-person should consider the potential impact on Sweden froma financial transaction tax (FTT), implemented on an EU level.

It should be stressed that the Moderate Party(Moderaterna), the largest opposition party, recently expressedthat it is in favour of a financial services sector tax, pointing ata payroll-based FAT as an one option. This indicates some

degree of consensus across the political blocks and might entailan increased probability of a financial services sector-specifictax actually being introduced.

VAT groupingAs mentioned above, the Swedish financial services sector cur-rently has access to VAT grouping rules. Parties in oppositionto the government have, however, proposed that these rules beabolished. Sweden was recently also subject to EU court pro-ceedings initiated by the European Commission, which claimedthe Swedish implementation of VAT groups to be in conflictwith EU law. The EU court however held that the Commissionfailed to show convincingly that, in the light of the need tocombat tax evasion and avoidance, the questioned restrictionsin the Swedish rules were not well founded. The EU court’sruling was thus to Sweden’s benefit. The government, which isin minority, reportedly wants to keep the VAT grouping rulesin place. But given the political situation the basis for the rulesbeing kept in force might not be rock-solid, so it is advisable forany stakeholder to closely monitor the situation.

Tax burden likely to increaseAs follows from the above, the Swedish tax landscape is beingscrutinised by different domestic committees that may suggestamendments which increase or otherwise alter the taxation of

Kristofer BrodinKPMG

Tel: +46 8 723 61 [email protected]

Kristofer Brodin is a senior tax manager in the KPMG financialservices (FS) tax practice and is based in Stockholm, Sweden. Hespecialises in Swedish and international corporate taxation. Healso advises on taxes and duties specific to the financial sectorsuch as the FTT, FAT, IPT and the Swedish bank levy (stabilitet-savgift). Brodin is responsible for banking in the FS tax practice inSweden.Brodin has experience in a vast variety of tax issues arising

within the financial services industry, including issues specific tobanking, non-life and life insurance. He advises domestic andinternational clients on restructurings, mergers & acquisitions,cross-border investments, outsourcing projects, asset finance,structured finance transactions etc.Before joining KPMG, Brodin served as head of corporate income

tax and products with one of the major Nordic banking groups.

S W E D E N | I N S U R A N C E T A X

2 2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

the insurance sector. In my view, it is highly likely that we willsee changes which may increase the tax burden for the sectorin the near future. In addition to these initiatives there are sev-eral external factors which may also impact the taxation ofinsurers, in particular the European Solvency II requirementsas well as the upcoming changes to accounting standards

(IFRS 4) and the Institutions for Occupational RetirementProvision (IORP II) draft directive. Bearing this in mind, for-eign insurers and insurance groups conducting business inSweden through branches or subsidiaries have every reason topay close attention to the Swedish development throughoutthe next few years.

S W I T Z E R L A N D | W I T H H O L D I N G T A X

2 4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Planned reform of the Swisswithholding tax