Embed Size (px)

Citation preview

FINANCIAL SECTOR ASSESSMENT TRINIDAD AND TOBAGO

FEBRUARY 2006

LATIN AMERICA & THE CARIBBEAN REGION VICE PRESIDENCY F~ANCIAL SECTOR VICE PRESIDENCY

BASED ON THE J O ~ T IMF-WORLD BANK FINANCIAL SECTOR ASSESSMENT PROGRAM

This Financial Sector Assessment summarizes the findings o f a joint IMF-World Bank Financial Sector Assessment Program (FSAP) mission, which visited Trinidad and Tobago (T&T) from February 21 to March 4,2005, and from May 2 to May 10,2005.’ The point o f departure for the FSAP team’s analysis was a detailed self-diagnosis o f the financial system undertaken by the authorities as part o f their vision o f establishing Trinidad and Tobago as a regional financial center by the year 2020. The diagnostic and assessment o f the FSAP validate many findings that resulted from the self-diagnosis, enhance the analysis in a number o f directions, and add proposals to support the aims o f the authorities.

, I. OVERALL ASSESSMENT

1. the T&T financial system has been expanding rapidly. The buoyancy in the energy sector has resulted in the accumulation o f significant savings. Limited domestic investment opportunities and declining interest rates on bank deposits have led to the public and private sectors’ significant increases in holdings o f foreign assets, especially in the Caribbean region.

Facilitated by a vibrant energy sector and a favorable macroeconomic environment,

2. Increased savings and limited domestic investment has put upward pressure on asset prices and balance sheet values o f pension funds, mutual funds, and insurance companies. Some financial assets issued are backed by investments in related companies. Asset growth in the credit union sector i s partly attributable to investments in real estate and noncore activities. The presence o f mixed conglomerates with intra-group exposures makes

’ The team comprised: Mr. Udaibir S. Das, Mission Chief (IMF), Ms. Anjali Kumar, Deputy Mission Chief (World Bank), Messrs. Roger, Espinosa, Samuel, Surti, and Ms. Cgrdenas (IMF); Messrs. Kyle, Cirasino, and Mmes. Randhawa, Love, and N’Daw-Amany, with headquarter assistance from Mmes. Klapper, Martinez-Peria and Zekhri (World Bank); Messrs. Mi les (BOE, U.K.), Chua (MAS, Singapore), McNabb (FSA, U.K.), Carmichael (ex-APRA, Australia), and McIsaac (ex-OSFI, Canada).

35530

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

- 2 -

transparency difficult. Taken together, these factors suggest a change in the profile o f risks affecting the financial system.

3. geared to cope with the evolution o f the financial system. Financial sector laws, in many cases, do not provide sufficient regulatory powers to oversee the complexity o f the financial system. Currently oversight o f complex conglomerate structures poses supervisory challenges for the authorities in the absence o f consolidated supervision. A part o f the financial system in the form o f statutory corporations l ies beyond the purview o f regular regulatory oversight.

The authorities recognize that current legal and supervisory practices are not yet fully

4. The authorities have begun an ambitious program to strengthen the financial sector and upgrade the framework o f financial oversight to address the structural changes and the new risks it faces. Key elements of the program include a far-reaching overhaul o f several financial sector laws; strengthening o f supervision within the Central Bank o f Trinidad and Tobago (CBTT); implementation o f consolidated and cross-border supervision o f financial conglomerates, bringing less regulated and supervised institutions under closer supervision; enhancing disclosure requirements; and developing market infrastructure. When fully implemented, these measures will fortify current financial system oversight. Significant attention has already been devoted to strengthening banking supervision. With CBTT recently becoming the insurance and pension regulator, similar efforts for the insurance and pensions sector are envisaged.

11. FINANCIAL SYSTEM STATUS AND FUTURE DEVELOPMENT

5. The financial system i s diverse and appears large with assets at 170 percent o f GDP in 2004. Apart from commercial banking sector, merchant banking, insurance, and pensions businesses are significant. The latter three possessed an asset base larger than commercial banks by end-2004. Another unique feature i s the dominance o f the system by a small number o f financial or mixed activity groups that are sponsors o f mutual funds and asset managers. Other major institutions include two statutory corporations: the National Insurance Board (NIB), which represents the public pension system, and the Unit Trust Corporation (UTC).

6. period 1998-2003, interest rate spreads in T&T averaged around 8.5 percentage points, about one percentage point below the rest o f the Caribbean region. These spreads are very high by developed country standards, but are comparable to spreads in other developing island- economies. During the last two years, spreads have declined almost 2 percentage points following the reduction o f the cash reserve requirement from 18 to 1 1 percent. Measured by the net interest margin, spreads appear more reasonable, averaging about 4 percentage points.

Bank intermediation spreads are slightly below the average for the region. Over the

Business Conglomerates and Regional Integration

7. official and private channels. The T&T and other CARICOM members are moving towards

The cross-border integration o f the T&T financial system i s taking place through both

the removal o f all restrictions on the establishment o f financial institutions, provision o f financial services, and free movement o f capital by year-end 2005. A regional rating agency has been established recently, and T&T hosts several foreign private financial f i rms .

8. spread over 20 countries, concentrated within the region. CARICOM countries account for 85 percent o f the T&T banking system’s loans and investments abroad. Regionally active business groups have control over a substantial proportion o f financial system assets and business.

As o f December 2004, the banking system’s loans and investments abroad were

9. around 18 percent o f new equity issues on the Trinidad and Tobago Stock Exchange (TTSE) have been accounted for by cross-listings o f CARICOM companies. These cross-listings have given regional companies access to capital in T&T and provided an important outlet for domestic savings. Currently, there are I 1 firms cross-listed in the Caribbean exchanges. Regional bond issuers have been slower to gain market share. Important steps have been taken in establishing common trading and depository systems and in adopting the U.S. dollar as a common currency for settlement o f cross-border transactions.

Regional integration has progressed through the securities markets. Since 1997,

Banking Sector

10. despite asset growth averaging nearly 10 percent annually, reflecting the faster growth o f nonbank institutions. Six commercial banks had 3 8 percent o f total assets at end-2004, down from 50 percent in 1995.

Over the last decade, commercial bank share in the financial system has eroded

1 1. weighted assets, the average capital adequacy ratio o f the system i s well in excess o f the minimum 10 percent regulatory requirement. Loans to the private sector constitute over 40 percent o f total banking assets, with consumer lending being the single largest item at 40 percent o f all loans. Loans to the domestic corporate sector constitute the bulk o f the remainder, other important items being manufacturing, trade, real estate, and mortgage.

Overall, the banking sector i s well-capitalized and provisioned. At 23 percent o f risk-

Insurance and Pensions

12. by two f i rms, which together account for over 85 percent o f the market. Insurance penetration ratios are quite favorable relative to both regional and middle-income country comparators. Profit and liquidity indicators for l i f e insurers appear satisfactory.

L i f e insurance constitutes about 70 percent o f the insurance industry. I t i s dominated

13. shares o f another corporation. However, this ratio appears to have been substantially exceeded in some cases. Investments in affiliate companies may have been partly in response to the limited opportunities offered on domestic capital markets. This requirement results in increased asset prices, as well as a “buy and hold” strategy with respect to local investments. Together, these limit secondary trading and make it difficult to establish a fair market value for securities after issue.

Regulations limit insurance companies from acquiring more than 30 percent o f the

- 4 -

14. Retirement security i s provided through a variety o f platforms. These include a national insurance system, private occupational pension plans, plans for civi l servants, and a social assistance program. The assets o f the private pension plans are mostly managed by bank-owned trust companies and have grown annually by over 13 percent between 200 1 and 2003, with a large part o f the investment in the domestic equity market. Both the national pension scheme and the majority o f private sector schemes are currently over funded. However, this partly reflects asset price increases in the local stock and property markets, which could be eroded by price volatility in these markets.

Securities Markets

15. Securities markets in T&T are developing fast. Stock market capitalization has grown rapidly over the past 5 years and, at around TT$109 bil l ion at end-2004, i s approximately 140 percent o f GDP, comparable with developed country standards. Mutual fund investments have grown rapidly since the establishment o f Unit Trust Corporation o f T&T (UTC) as a statutory corporation in 198 1 and are currently around two-thirds o f bank assets. Despite the growth o f private sector issuers, UTC still accounts for around half o f all mutual fund investments. The number and range o f mutual funds are large for an economy the size o f T&T.

16. by the government, quasi-government agencies, foreign governments, and the private sector. Fixed-rate maturities extend as far as 20 years, and there i s an active business in stripping bonds. Although this market i s underdeveloped, the government has actively encouraged securitization through the creation o f the Home Mortgage Bank (HMB) as a statutory corporation along the lines o f Fannie Mae in the U.S. with a mandate and tax concessions to securitize mortgages.

The primary market for bonds i s relatively well developed. There i s active issuance

17. Notwithstanding the relatively high market capitalization in equities and active primary market in bonds, secondary market liquidity i s very low. Turnover in equities i s less than 3 percent per annum and in bonds around 6 percent per annum. Large portions o f both shares and bonds exchange hands between strategic investors on a private placement basis. Further, despite i t s growth in recent years, the equities market has provided very l i t t l e new capital to local f i r m s . O f the increase o f around TT$90 bil l ion since 1997, almost two-thirds i s accounted for by increases in share prices. O f the TT$3 1 billion worth o f new equities raised in the market, most reflected bonus issues and overseas cross-listings; less than 10 percent involved new capital raised for local firms.

18, companies i s small. While market infrastructure has been strengthened recently, by the introduction o f electronic trading and depositories in both equities and bonds, electronic registries are yet to be linked, and many securities are not yet a part o f the electronic registry systems. There i s overlapping o f directorships between related companies, which may lead to governance issues.

Ownership o f companies and equities i s concentrated, and effective free float o f listed

- 5 -

Financial Access

19. - suggest that there has been limited expansion o f financial access over the last decade. Credit and deposit market depth in T&T today i s somewhat below levels in other countries with similar GDP per capita. Both credit market depth and the ratio o f l iquid liabilities remain below comparable island economies such as Malta or Barbados, although it i s close to levels achieved by Chile or Costa Rica. The ratio o f liquid liabilities to GDP has fluctuated around 50 percent, while the share o f private credit to GDP has been close to 40 percent during the last two decades.

Aggregate measures o f financial depth - overall ratios o f credit and deposits to GDP

20. Credit unions, which provide financial services to small enterprises and individuals including the less well-off, have grown rapidly over the last decade, both in membership base and assets. A large part o f the recent increase in assets has taken the form o f investments rather than lending to members. The provision o f financial services to small businesses through other institutional channels has also not grown significantly.

Expansion o f financial access for households and small business has been mixed.

2 1. The 129 registered and active entities in the Credit Union sector play an important role in providing access to finance to their 534,000 members. Recent growth has been spurred by significant tax advantages, including a tax deduction plan reintroduced in 2003 which provides a deduction o f TT$ 10,000 against income on credit union deposits. Risk exposure o f this sector has increased because o f the expansion o f the largest credit unions into some risky investments including real estate. Diversification into risky investment i s being driven partly by high levels o f nonperforming loans. The sector i s in need o f a new legal framework in l ine with good international practice, with accompanying prudential regulations and a structure o f oversight commensurate with i t s present activities.

22. away from the o i l economy and in the reduction o f unemployment and poverty and has initiated several schemes to support SME financially. According to official estimates, there are between 20,000 and 30,000 small businesses operating in T&T. These businesses provide employment to 55,000 to 65,000 people (out o f a total population o f about 1,088,600) and contribute 5 to10 percent o f GDP. About 25 percent o f small f i r m s have obtained bank loans. The high costs and risks associated with small business lending as well as profitable investment opportunities available to commercial banks outside o f this sector inhibit expansion o f private lending to this sector. The presence o f subsidized public sector lending may also be inhibiting private lending. Some public sector programs have high risks, costs, and delinquencies. An evaluation o f such schemes supported by the application o f prudential criteria would be valuable, especially for institutions currently outside the purview o f the Financial Institutions Act (FIA).

The government o f T&T envisions the SME sector as a key catalyst in diversification

23. Quality can be improved by requiring the Central Statistical Office, the Registrar o f Companies, and banks to collect better data on the sector. Credit histories are also an integral part o f improving access to SMEs. The recently established Automated Credit Bureau marks

Absence o f high quality o f information about SMEs limits analysis o f the sector.

- 6 -

a major step forward, and it could be further strengthened by improving the accompanying regulation and i t s scope o f service. At present, it only collects information on personal loans but could expand i t s coverage to include business loans as well. Creditor rights would be strengthened by the establishment o f a small claims court.

Financial Infrastructure

24. The CBTT and other stakeholders have achieved significant results in the reform o f the payments system in T&T. The most important o f these was the launch o f a Real Time Gross Settlement (RTGS) system (safe-tt) in October 2004. Safe-tt i s a modern system and has several tools for managing liquidity pressures. In parallel, a custody and settlement system for government securities (GSS) was launched, which went live for bills and notes in December 2004 and for bonds in February 2005. The Automated Clearinghouse, owned jointly by the CBTT and commercial banks, was launched in January 2006. Additional steps planned include the creation o f a Virtual Private Network by the CBTT that will provide the banking community a secure network to share information and carry out several operations.

25. The legal framework for payments and settlement presents some important limitations. The legal basis i s incomplete in that i t supports paper-based payments systems but lacks the elements required for the operation o f a modern payments system. Full contingency arrangements are also s t i l l to be finalized. The system i s operated by the CBTT which i s in the process o f clarifying i t s participation policy. The National Payment System Council, established as a forum o f discussion on payment system matters, should help in the preparation o f the required additional regulations.

26. been prescribed. Currently, all financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) and certified by an independent auditor. Although IFRS provide an adequate framework for the preparation o f bank and insurance financial statements, they need to be complemented with detailed guidance issued by the supervisor to ensure that licensees apply the standards in a consistent and prudent manner. Verification o f bank records i s achieved periodically through on-site examinations rather than through the use o f external auditors. However, the proposed amendments to the Financial Institutions Act should result in a closer working relationship with licensees’ external auditors.

The accounting standards to be used by licensed financial institutions have not yet

Legal and Regulatory Issues

27. Supervision o f mutual hnds and the securities industry involves both the SEC and the CBTT, with the CBTT having responsibility for funds operated by banks. UTC operates under i t s own statute. The draft Securities Bill, if enacted, will bring supervision o f all mutual funds under the TTSEC. The TTSEC also has regulatory powers over the bond market. The TTSEC regulates the conduct o f all market participants in the capital markets and monitors activities in the primary and secondary markets. The TTSE plays a self-regulatory role over members o f the stock exchange, as does the T&T Central Depository over i t s members. Credit unions are supervised by the Minister o f Labor and the Minister o f Finance and

- 7 -

governed by the outmoded Cooperative Societies Act. However, the supervision i s largely administrative and organizational and not financial.

28. the recent diagnosis o f the financial system by the authorities established an ambitious program for strengthening the legal and regulatory framework for financial system oversight. Key elements o f the program include overhauling o f financial sector legislation, strengthening o f central bank’s supervision capacity, implementation o f consolidated and cross-border supervision o f financial conglomerates, bringing less regulated and supervised institutions under closer supervision, enhancing disclosure requirements, and developing market infrastructure. When implemented, these measures will address many o f the existing limitations o f the current financial system oversight. The consolidation o f supervision o f the banking, insurance, and pension sectors within the CBTT i s an important step forward.

The White Paper on the Financial System of Trinidad and Tobago that resulted from

29. The authorities may also wish to consider the creation o f a single tribunal to hear appeals from financial and nonfinancial parties engaged in transactions with financial institutions. Some progress has been made in this direction with the recent introduction o f a financial ombudsman position and i ts extension to the insurance sector.

Finalization and passage o f laws building on the legislative reform agenda i s critical.

30. changes being proposed to the Securities Industry Act and FIA. The opportunity might well be taken to address certain conflicts with the tax legislation and to update it in some specific areas o f corporate governance. Concerns exist in relation to the corporate governance practices o f conglomerates, mutual funds, and other entities that are not subject to proper regulatory oversight. To some extent, these concerns will be addressed in the proposed Securities Industry (Amendment) Act and in the proposed Fair Trading Act.

Some amendments will be required to the Companies Act to harmonize it with the

3 1. In the absence o f an insolvency law, T&T relies on the winding up and liquidation provisions o f the Companies Act. While this seems to have worked reasonably well, insolvency law and practice has advanced considerably in recent years. I t i s recommended that T&T consider introducing a modern insolvency law regime that would include a reorganization procedure, perhaps based on the U.K. administration model.

32, The system o f land registration also needs improvement. Average searches take two to three weeks, which i s too long for a modern market economy. New laws designed to bring all land under the Torrens system were enacted in 2000, but the new system has not become operational yet. Computerization o f land records i s continuing. The register i s open to the public. Registration i s inexpensive and reported to be free o f corruption. In many countries, land registries are now self-funding rather than a charge on the budget. I t i s recommended that T&T consider moving towards a user-pays basis o f financing for i t s property registers.

33. different registry systems, and this impedes access to credit for small businesses and consumers. However, an improved framework for secured transactions in personal property i s to be introduced, including an electronic recording system capable o f being accessed

Charges over movable property are presently subject to registration under several

- 8 -

remotely. Security interests in all types o f collateral can be registered in this registry. Consequential amendments will be required to the legislation dealing with hire purchase and consumer protection.

34. The legal framework governing the taking and enforcement o f security appears to be generally sound, but court processes need to be worked more quickly. Personal bankruptcies are rare, mainly owing to a formalistic process. In the case o f corporate defaults, procedures for enforcement o f creditor rights over collateral are clear and well-tested. No reference to a court i s required, and the secured assets are usually disposed o f without loss to the creditor.

35. fail to meet prudential requirements, i ts exit policy needs to be updated. The exit policy envisions a ladder o f regulatory responses to deterioration o f a bank’s performance, including a decline in capital adequacy and asset quality. Responses vary from moral suasion to the closure o f an insolvent institution. However, while most o f the exit policy i s rules based, it states that, in cases o f systemic crises, the CBTT may exercise regulatory forbearance.

Although the CBTT has devoted considerable attention to the actions on banks that

111. MAIN PRIORITIES FOR FINANCIAL DEVELOPMENT

36. The overall thrust o f reforms outlined in the White Paper i s in the right direction. Within that framework, work in two areas needs to be accelerated on a priority basis: (i) adoption and implementation o f the revised Financial Institutional Act, Insurance Act, the CBTT Act, and the Securities Industry Act; and, (ii) strengthening o f supervision and oversight of financial conglomerates and their cross-border and cross-market operations within the limits o f existing laws and regulations, as well as through informal agreements pending passage o f new legislation.

37. and measures to improve intermediation o f household savings and finance to small and medium-sized enterprises.

Medium-term priorities include the development o f financial and capital markets

e Progress has been made in developing the domestic inter-bank money market, but establishing comparably efficient foreign exchange and government securities markets remains a challenge. The development o f supporting payments and settlements infrastructure i s an important step forward in facilitating liquidity management. Additional efforts to develop the secondary market in government securities are needed to improve short-term liquidity management. Establishing a competitive interbank market in foreign exchange and developing foreign exchange risk management instruments will require changes in supply o f liquidity to the foreign exchange market and permitting some flexibility in the exchange rate.

e Appropriate disclosures, business conduct, conflict o f interest, and governance rules need to be strengthened. These should be harmonized across sectors, and it must be ensured that information on financial risks i s disclosed. These measures will allow the markets to play a more effective role in monitoring and disciplining financial f i r m s

- 9 -

and will also help in assuring confidence in the fairness and integrity o f the financial services industry in T&T.

a Expanding financial access for householders and small enterprises requires some basic building blocks. Collecting information on small depositors and creditors at banks i s a f irst step towards understanding how the formal financial system could support this segment and also better support the SME sector. Commercial bank lending to this segment would be greatly facilitated by enabling the newly established credit bureau to extend i ts coverage to small enterprises.

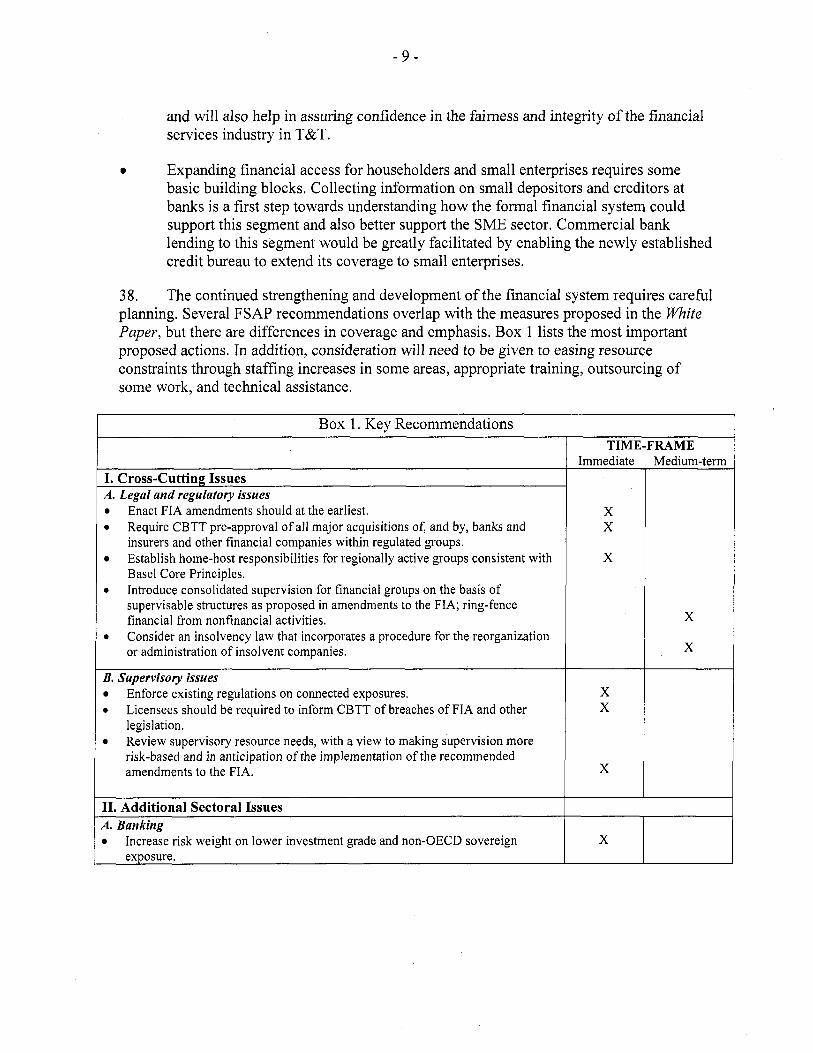

3 8. planning, Several FSAP recommendations overlap with the measures proposed in the White Paper, but there are differences in coverage and emphasis. Box 1 l is ts the most important proposed actions. In addition, consideration will need to be given to easing resource constraints through staffing increases in some areas, appropriate training, outsourcing o f some work, and technical assistance.

The continued strengthening and development o f the financial system requires careful

Box 1. Key Recommendations

I. Cross-Cutting Issues A. Legal and regulatory issues

0

0

Enact FIA amendments should at the earliest. Require CBTT pre-approval of all major acquisitions of, and by, banks and insurers and other financial companies within regulated groups. Establish home-host responsibilities for regionally active groups consistent with Base1 Core Principles. Introduce consolidated supervision for financial groups on the basis of supervisable structures as proposed in amendments to the FIA; ring-fence financial from nonfinancial activities. Consider an insolvency law that incorporates a procedure for the reorganization or administration o f insolvent companies.

0

B. Supervisory issues

0

Enforce existing regulations on connected exposures. Licensees should be required to inform CBTT of breaches o f FIA and other legislation. Review supervisory resource needs, with a view to making supervision more risk-based and in anticipation o f the implementation of the recommended amendments to the FIA.

11. Additional Sectoral Issues A. Banking

Increase risk weight on lower investment grade and non-OECD sovereign exposure.

TIME-FRAME Immediate

X X

X

X X

X

Medium-term

X

X

- 10 -

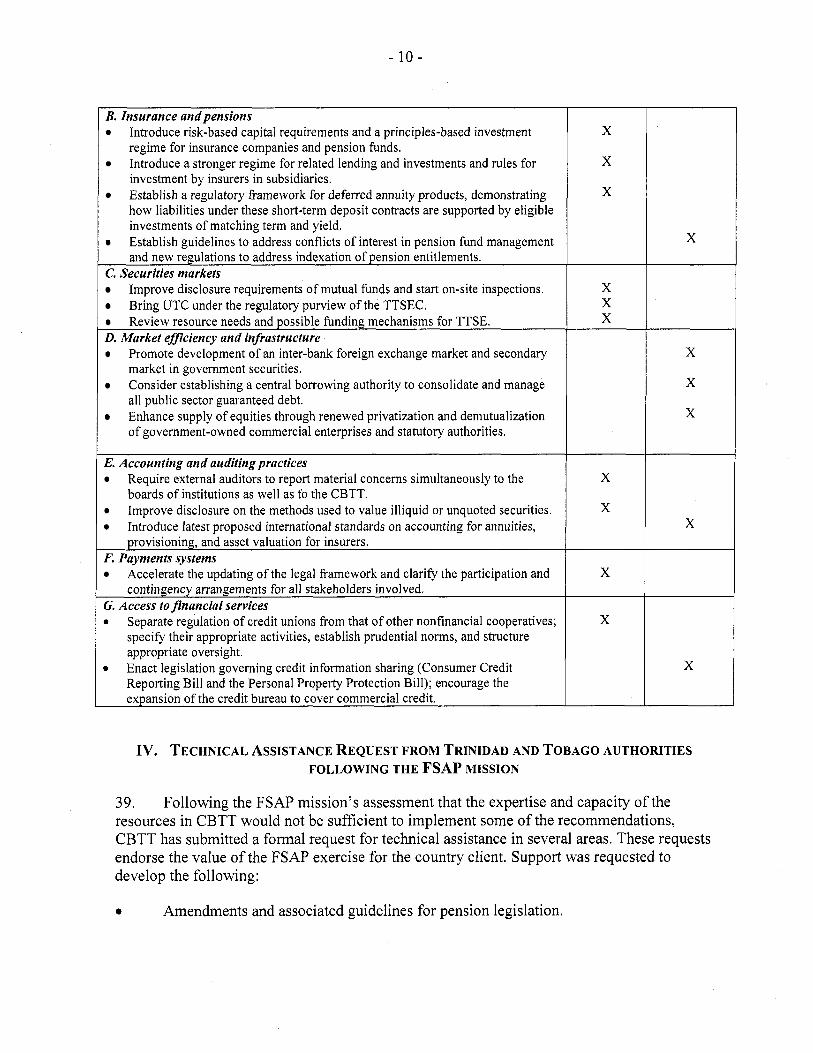

B. Insurance andpensions Introduce risk-based capital requirements and a principles-based investment regime for insurance companies and pension funds. Introduce a stronger regime for related lending and investments and rules for investment by insurers in subsidiaries. Establish a regulatory fi-amework for deferred annuity products, demonstrating how liabilities under these short-term deposit contracts are supported by eligible investments of matching term and yield. Establish guidelines to address conflicts of interest in pension fund management and new regulations to address indexation of pension entitlements.

C. Securities markets Improve disclosure requirements of mutual funds and start on-site inspections. Bring UTC under the regulatory purview of the TTSEC. Review resource needs and possible funding mechanisms for TTSE.

D. Market efficiency and infrastructure Promote development o f an inter-bank foreign exchange market and secondary market in government securities. Consider establishing a central borrowing authority to consolidate and manage al l public sector guaranteed debt. Enhance supply of equities through renewed privatization and demutualization o f government-owned commercial enterprises and statutory authorities.

E. Accounting and auditing practices

F. Payments systems

C. Access tofinancial services *

Require external auditors to report material concerns simultaneously to the boards of institutions as well as to the CBTT. Improve disclosure on the methods used to value illiquid or unquoted securities. Introduce latest proposed international standards on accounting for annuities, provisioning, and asset valuation for insurers.

Accelerate the updating of the legal framework and clarify the participation and contingency arrangements for all stakeholders involved.

Separate regulation of credit unions from that of other nonfinancial cooperatives; specify their appropriate activities, establish prudential norms, and structure appropriate oversight. Enact legislation governing credit information sharing (Consumer Credit Reporting Bil l and the Personal Property Protection Bill); encourage the expansion of the credit bureau to cover commercial credit.

B

X

X

X

X X X

X

X

X

X

X

X

X

X

X

X

Iv. TECHNICAL ASSISTANCE REQUEST FROM TRINIDAD AND TOBAGO AUTHORITIES FOLLOWING THE FSAP MISSION

39. Fol lowing the FSAP mission’s assessment that the expertise and capacity o f the resources in C B T T would not be sufficient to implement some o f the recommendations, C B T T has submitted a formal request for technical assistance in several areas. These requests endorse the value o f the FSAP exercise for the country client. Support was requested to develop the following:

e Amendments and associated guidelines for pension legislation.

- 11 -

e

e

e

e

e

40.

e

e

e

e

Risk-based supervisory framework for all financial institutions and specific secondary framework that cover conglomerate groups, credit unions, insurance intermediaries, and nonbank entities with multiple core activities.

Framework for monitoring key indicators, conducting stress testing, and implementing appropriate risk mitigants for maintaining financial stability.

Standardized reporting requirements o f all financial institutions.

Risk-based capital regimes for banks, insurance companies, and financial holding companies.

Intervention strategies and action plans for insurance companies and pension plans, including models for early detection o f problems.

Insurance protection plan, similar to the Deposit Insurance Corporation for banks.

Technical training for CBTT staff in ALM models, supervisory framework, risk- based capital adequacy model for insurance companies, and issues related to Basic I1 implementation.

Secondary market for government securities.

Foreign exchange market, auction system, interbank trading system and fledging mechanisms.

Additionally, the following areas o f support were requested for TTSEC:

Improvement o f capacity to regulate market conduct.

Development o f procedures for conduct o f investigations and administrative enforcement hearings.

Drafting o f by-laws governing areas identified in the draft legislation, including in such areas as Collective Investment Schemes and capital and risk-based requirements.

Conduct o f a study on the improvement o f governance at the commission and the assessment o f the human and other resource needs of the commission.

Assistance with Implementation o f the International Organization o f Securities Commission’s Objectives and Principles of Securities Regulation and preparation for assessment of eligibility for signing o f IOSCO’s Multilateral Memorandum o f Understanding by 20 10.