Embed Size (px)

Citation preview

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS’ REPORTS

THE CENTRE FOR WOMEN, INC.

September 30, 2012 and 2011

TABLE OF CONTENTS

Independent Auditors’ Report 3 Financial Statements

Statements of Financial Position 4 Statements of Activities and Changes in Net Assets 5 Statements of Cash Flows 6 Statements of Functional Expenses 7 - 8 Notes to Financial Statements 9 - 16

Supplemental Information 17 Schedule of Expenditures of Federal Awards and State

Financial Assistance 18 - 20 Notes to Schedule of Expenditures of Federal Awards and State Financial Assistance 21 Schedule of State Earnings 22 - 23 Schedule of Related Party Transaction Adjustments 24 - 25 Schedule of Bed-Day Availability Payments 26 - 27 Program/Cost Center Actual Expenses and Revenue Schedule 28 - 30 Note to Schedule of State Earnings and Program / Cost Center

Actual Expenses and Revenue Schedule 31 Statement of Functional Expenses - Department of Elder Affairs 32 - 33 Note to Statement of Functional Expenses - Department of

Elder Affairs 34 Independent Auditors’ Report on Internal Control Over Financial

Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 35 - 37

Independent Auditors’ Report on Compliance with Requirements

that Could Have a Direct and Material Effect on Each Major Federal Program and State Project and on Internal Control Over Compliance in Accordance with OMB Circular A-133 and Chapter 10.650, Rules of the Auditor General 38 - 40

Schedule of Findings and Questioned Costs - Federal Programs

and State Projects 41 - 43 Management Letter 44 - 45

3

INDEPENDENT AUDITORS’ REPORT Board of Directors The Centre for Women, Inc.

We have audited the accompanying statements of financial position of The Centre for Women, Inc. (the “Organization”) as of September 30, 2012 and 2011 and the related statements of activities and changes in net assets, cash flows, and functional expenses for the years then ended. These financial statements are the responsibility of the Organization’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the

United States of America and Government Auditing Standards issued by the Comptroller General of the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material

respects, the financial position of the Organization as of September 30, 2012 and 2011, and the changes in its net assets, its cash flows, and its functional expenses for the years then ended in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated

January 16, 2013 on our consideration of the Organization’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

Our audit was conducted for the purpose of forming an opinion on the basic financial

statements taken as a whole. The accompanying supplemental information, identified in the table of contents, is presented for purposes of additional analysis as required by the U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Chapter 10.650, State of Florida Rules of the Auditor General, and is not a required part of the basic financial statements. Such information, including the Schedule of Expenditures of Federal Awards and State Financial Assistance, has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, is fairly stated, in all material respects, in relation to the basic financial statements taken as whole. Tampa, Florida January 16, 2013

RIVERO, GORDIMER & COMPANY, P.A.

CERTIFIED PUBLIC ACCOUNTANTS

ONE TAMPA CITY CENTER • SUITE 2600 • 201 N. FRANKLIN STREET • P. O. BOX 172359 • TAMPA, FLORIDA 33672 • 813- 875-7774 FAX 813-874-6785

Member

American Institute of Certified Public Accountants

Florida Institute of Certified Public Accountants

Cesar J. Rivero Sam A. Lazzara

Herman V. Lazzara Stephen G. Douglas

Marc D. Sasser Michael E. Helton

Richard B. Gordimer, of Counsel

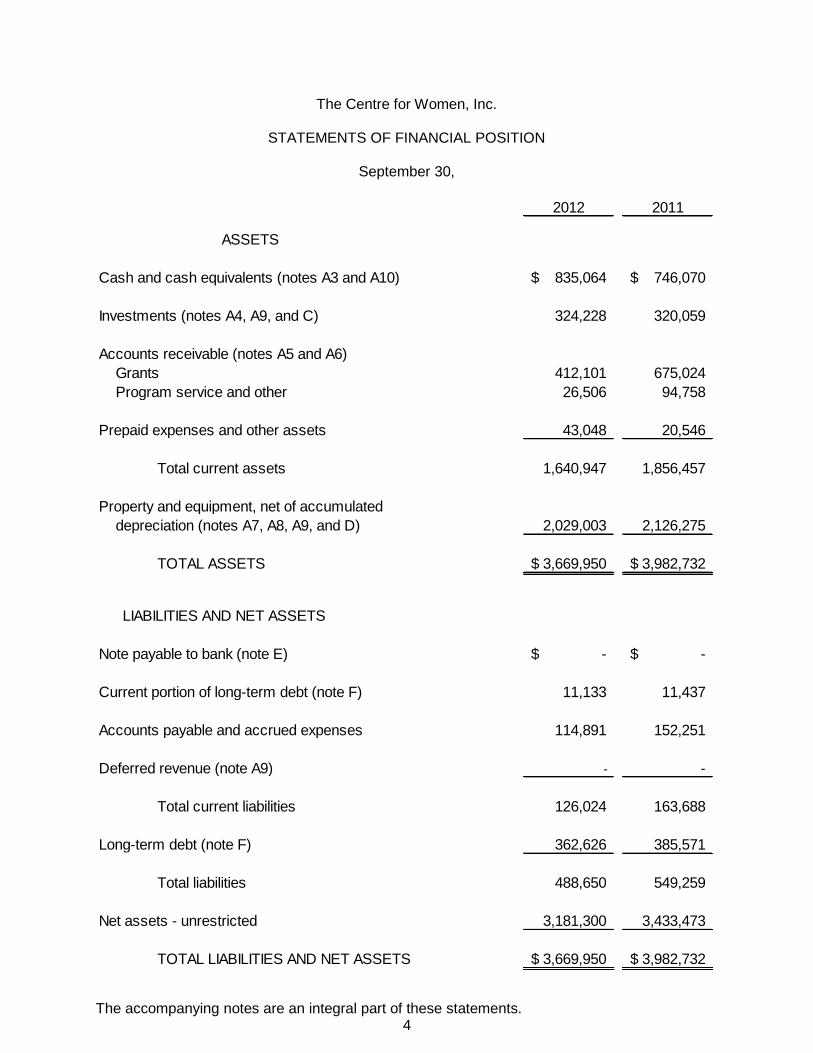

The accompanying notes are an integral part of these statements. 4

The Centre for Women, Inc.

STATEMENTS OF FINANCIAL POSITION

September 30,

2012 2011

Cash and cash equivalents (notes A3 and A10) 835,064$ 746,070$

Investments (notes A4, A9, and C) 324,228 320,059

Accounts receivable (notes A5 and A6)

Grants 412,101 675,024

Program service and other 26,506 94,758

Prepaid expenses and other assets 43,048 20,546

Total current assets 1,640,947 1,856,457

Property and equipment, net of accumulated

depreciation (notes A7, A8, A9, and D) 2,029,003 2,126,275

TOTAL ASSETS 3,669,950$ 3,982,732$

Note payable to bank (note E) -$ -$

Current portion of long-term debt (note F) 11,133 11,437

Accounts payable and accrued expenses 114,891 152,251

Deferred revenue (note A9) - -

Total current liabilities 126,024 163,688

Long-term debt (note F) 362,626 385,571

Total liabilities 488,650 549,259

Net assets - unrestricted 3,181,300 3,433,473

TOTAL LIABILITIES AND NET ASSETS 3,669,950$ 3,982,732$

LIABILITIES AND NET ASSETS

ASSETS

The accompanying notes are an integral part of these statements. 5

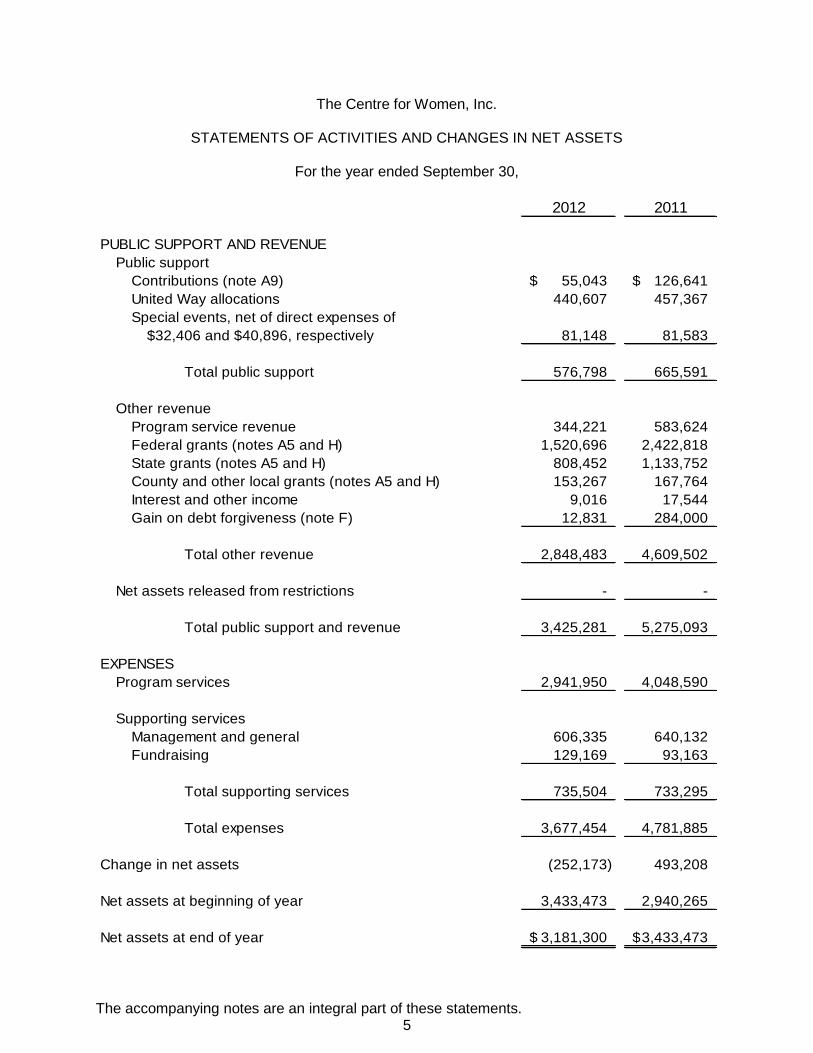

The Centre for Women, Inc.

STATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

For the year ended September 30,

2012 2011

PUBLIC SUPPORT AND REVENUE

Public support

Contributions (note A9) 55,043$ 126,641$

United Way allocations 440,607 457,367

Special events, net of direct expenses of

$32,406 and $40,896, respectively 81,148 81,583

Total public support 576,798 665,591

Other revenue

Program service revenue 344,221 583,624

Federal grants (notes A5 and H) 1,520,696 2,422,818

State grants (notes A5 and H) 808,452 1,133,752

County and other local grants (notes A5 and H) 153,267 167,764

Interest and other income 9,016 17,544

Gain on debt forgiveness (note F) 12,831 284,000

Total other revenue 2,848,483 4,609,502

Net assets released from restrictions - -

Total public support and revenue 3,425,281 5,275,093

EXPENSES

Program services 2,941,950 4,048,590

Supporting services

Management and general 606,335 640,132

Fundraising 129,169 93,163

Total supporting services 735,504 733,295

Total expenses 3,677,454 4,781,885

Change in net assets (252,173) 493,208

Net assets at beginning of year 3,433,473 2,940,265

Net assets at end of year 3,181,300$ 3,433,473$

The accompanying notes are an integral part of these statements. 6

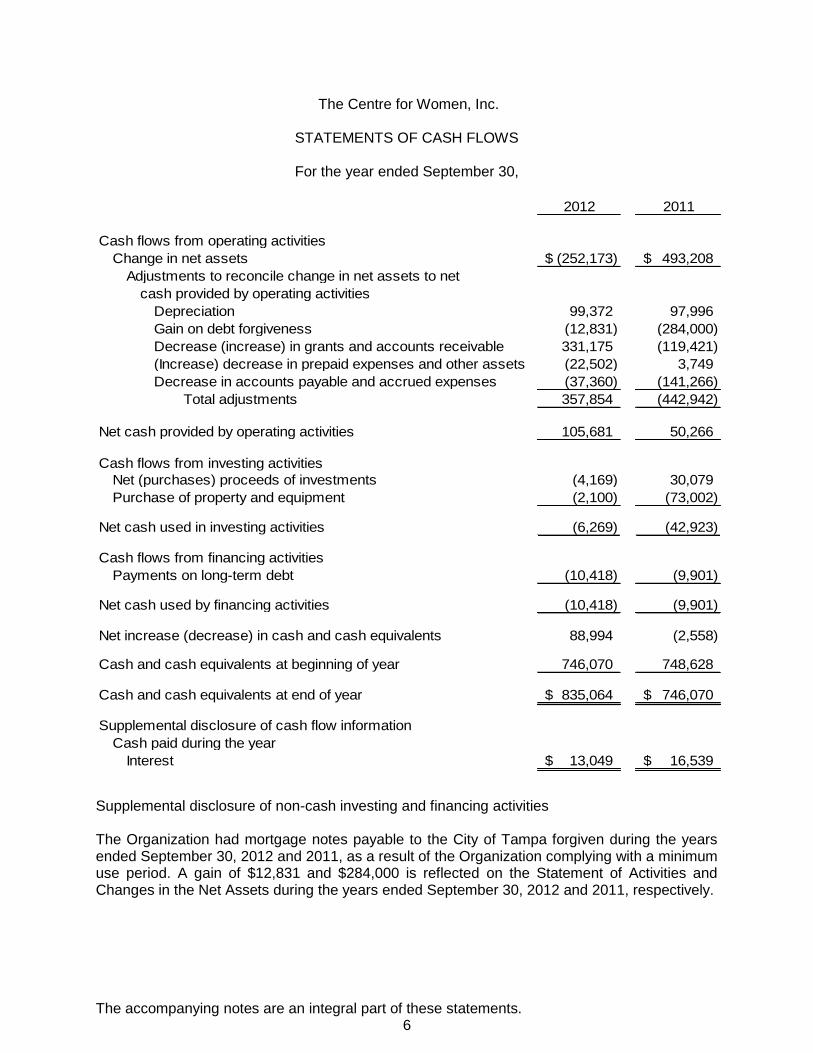

The Centre for Women, Inc.

STATEMENTS OF CASH FLOWS

For the year ended September 30,

2012 2011

Cash flows from operating activities

Change in net assets (252,173)$ 493,208$

Adjustments to reconcile change in net assets to net

cash provided by operating activities

Depreciation 99,372 97,996

Gain on debt forgiveness (12,831) (284,000)

Decrease (increase) in grants and accounts receivable 331,175 (119,421)

(Increase) decrease in prepaid expenses and other assets (22,502) 3,749

Decrease in accounts payable and accrued expenses (37,360) (141,266)

Total adjustments 357,854 (442,942)

Net cash provided by operating activities 105,681 50,266

Cash flows from investing activities

Net (purchases) proceeds of investments (4,169) 30,079

Purchase of property and equipment (2,100) (73,002)

Net cash used in investing activities (6,269) (42,923)

Cash flows from financing activities

Payments on long-term debt (10,418) (9,901)

Net cash used by financing activities (10,418) (9,901)

Net increase (decrease) in cash and cash equivalents 88,994 (2,558)

Cash and cash equivalents at beginning of year 746,070 748,628

Cash and cash equivalents at end of year 835,064$ 746,070$

Supplemental disclosure of cash flow information

Cash paid during the year

Interest 13,049$ 16,539$

Supplemental disclosure of non-cash investing and financing activities The Organization had mortgage notes payable to the City of Tampa forgiven during the years ended September 30, 2012 and 2011, as a result of the Organization complying with a minimum use period. A gain of $12,831 and $284,000 is reflected on the Statement of Activities and Changes in the Net Assets during the years ended September 30, 2012 and 2011, respectively.

The accompanying notes are an integral part of this statement. 7

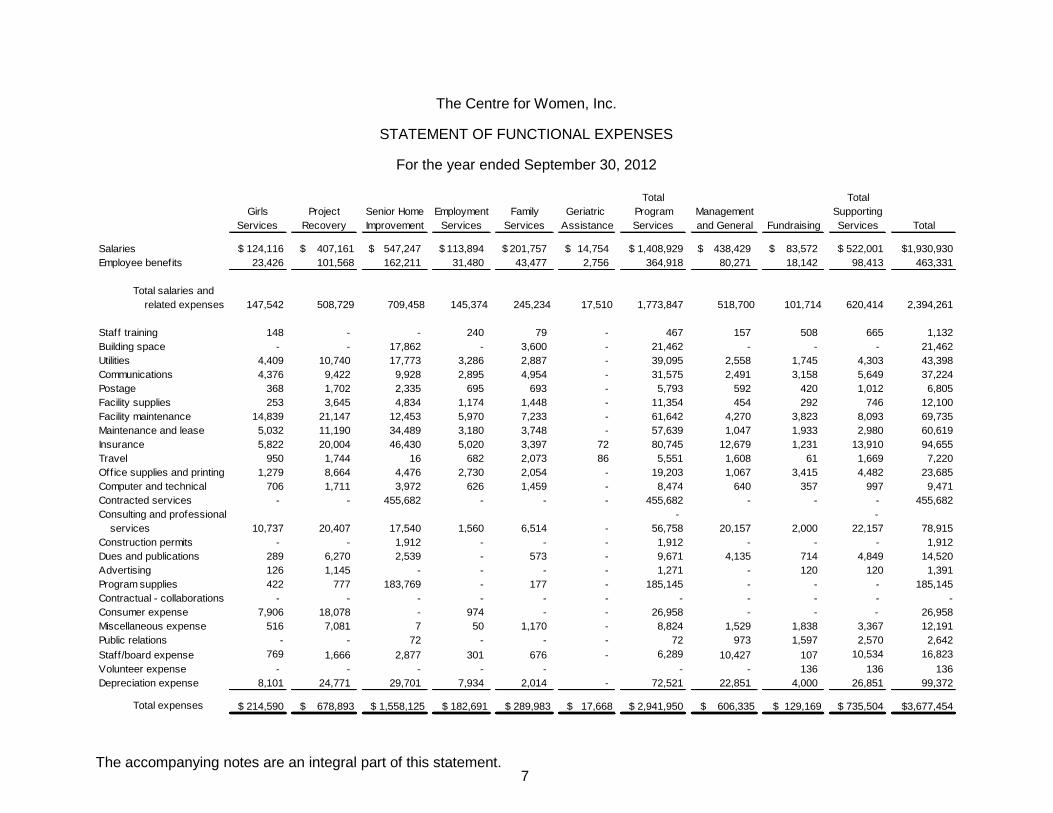

The Centre for Women, Inc.

STATEMENT OF FUNCTIONAL EXPENSES

For the year ended September 30, 2012

Total Total

Girls Project Senior Home Employment Family Geriatric Program Management Supporting

Services Recovery Improvement Services Services Assistance Services and General Fundraising Services Total

Salaries $ 124,116 $ 407,161 547,247$ 113,894$ 201,757$ 14,754$ $ 1,408,929 438,429$ 83,572$ $ 522,001 $1,930,930

Employee benefits 23,426 101,568 162,211 31,480 43,477 2,756 364,918 80,271 18,142 98,413 463,331

Total salaries and

related expenses 147,542 508,729 709,458 145,374 245,234 17,510 1,773,847 518,700 101,714 620,414 2,394,261

Staff training 148 - - 240 79 - 467 157 508 665 1,132

Building space - - 17,862 - 3,600 - 21,462 - - - 21,462

Utilities 4,409 10,740 17,773 3,286 2,887 - 39,095 2,558 1,745 4,303 43,398

Communications 4,376 9,422 9,928 2,895 4,954 - 31,575 2,491 3,158 5,649 37,224

Postage 368 1,702 2,335 695 693 - 5,793 592 420 1,012 6,805

Facility supplies 253 3,645 4,834 1,174 1,448 - 11,354 454 292 746 12,100

Facility maintenance 14,839 21,147 12,453 5,970 7,233 - 61,642 4,270 3,823 8,093 69,735

Maintenance and lease 5,032 11,190 34,489 3,180 3,748 - 57,639 1,047 1,933 2,980 60,619

Insurance 5,822 20,004 46,430 5,020 3,397 72 80,745 12,679 1,231 13,910 94,655

Travel 950 1,744 16 682 2,073 86 5,551 1,608 61 1,669 7,220

Office supplies and printing 1,279 8,664 4,476 2,730 2,054 - 19,203 1,067 3,415 4,482 23,685

Computer and technical 706 1,711 3,972 626 1,459 - 8,474 640 357 997 9,471

Contracted services - - 455,682 - - - 455,682 - - - 455,682

Consulting and professional - -

services 10,737 20,407 17,540 1,560 6,514 - 56,758 20,157 2,000 22,157 78,915

Construction permits - - 1,912 - - - 1,912 - - - 1,912

Dues and publications 289 6,270 2,539 - 573 - 9,671 4,135 714 4,849 14,520

Advertising 126 1,145 - - - - 1,271 - 120 120 1,391

Program supplies 422 777 183,769 - 177 - 185,145 - - - 185,145

Contractual - collaborations - - - - - - - - - - -

Consumer expense 7,906 18,078 - 974 - - 26,958 - - - 26,958

Miscellaneous expense 516 7,081 7 50 1,170 - 8,824 1,529 1,838 3,367 12,191

Public relations - - 72 - - - 72 973 1,597 2,570 2,642

Staff/board expense 769 1,666 2,877 301 676 - 6,289 10,427 107 10,534 16,823

Volunteer expense - - - - - - - 136 136 136

Depreciation expense 8,101 24,771 29,701 7,934 2,014 - 72,521 22,851 4,000 26,851 99,372

Total expenses $ 214,590 $ 678,893 $ 1,558,125 $ 182,691 $ 289,983 $ 17,668 $ 2,941,950 $ 606,335 $ 129,169 $ 735,504 $3,677,454

The accompanying notes are an integral part of this statement. 8

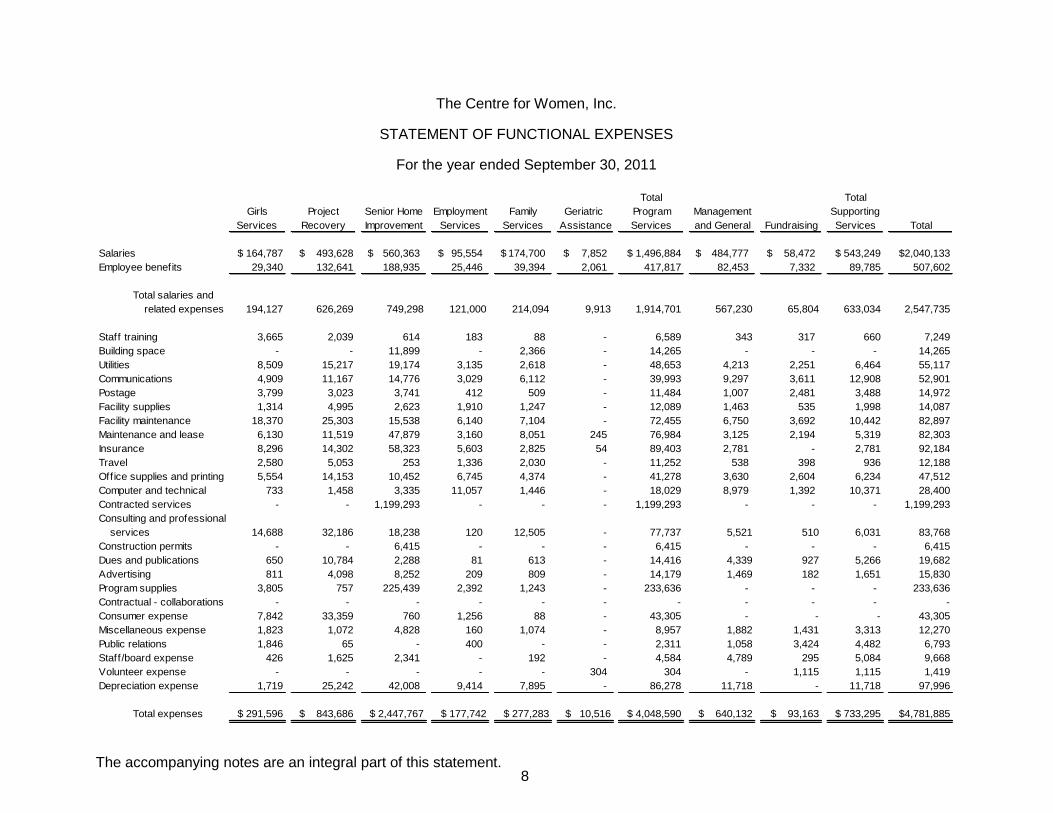

The Centre for Women, Inc.

STATEMENT OF FUNCTIONAL EXPENSES

For the year ended September 30, 2011

Total Total

Girls Project Senior Home Employment Family Geriatric Program Management Supporting

Services Recovery Improvement Services Services Assistance Services and General Fundraising Services Total

Salaries $ 164,787 $ 493,628 560,363$ 95,554$ 174,700$ 7,852$ $ 1,496,884 484,777$ 58,472$ $ 543,249 $2,040,133

Employee benefits 29,340 132,641 188,935 25,446 39,394 2,061 417,817 82,453 7,332 89,785 507,602

Total salaries and

related expenses 194,127 626,269 749,298 121,000 214,094 9,913 1,914,701 567,230 65,804 633,034 2,547,735

Staff training 3,665 2,039 614 183 88 - 6,589 343 317 660 7,249

Building space - - 11,899 - 2,366 - 14,265 - - - 14,265

Utilities 8,509 15,217 19,174 3,135 2,618 - 48,653 4,213 2,251 6,464 55,117

Communications 4,909 11,167 14,776 3,029 6,112 - 39,993 9,297 3,611 12,908 52,901

Postage 3,799 3,023 3,741 412 509 - 11,484 1,007 2,481 3,488 14,972

Facility supplies 1,314 4,995 2,623 1,910 1,247 - 12,089 1,463 535 1,998 14,087

Facility maintenance 18,370 25,303 15,538 6,140 7,104 - 72,455 6,750 3,692 10,442 82,897

Maintenance and lease 6,130 11,519 47,879 3,160 8,051 245 76,984 3,125 2,194 5,319 82,303

Insurance 8,296 14,302 58,323 5,603 2,825 54 89,403 2,781 - 2,781 92,184

Travel 2,580 5,053 253 1,336 2,030 - 11,252 538 398 936 12,188

Office supplies and printing 5,554 14,153 10,452 6,745 4,374 - 41,278 3,630 2,604 6,234 47,512

Computer and technical 733 1,458 3,335 11,057 1,446 - 18,029 8,979 1,392 10,371 28,400

Contracted services - - 1,199,293 - - - 1,199,293 - - - 1,199,293

Consulting and professional

services 14,688 32,186 18,238 120 12,505 - 77,737 5,521 510 6,031 83,768

Construction permits - - 6,415 - - - 6,415 - - - 6,415

Dues and publications 650 10,784 2,288 81 613 - 14,416 4,339 927 5,266 19,682

Advertising 811 4,098 8,252 209 809 - 14,179 1,469 182 1,651 15,830

Program supplies 3,805 757 225,439 2,392 1,243 - 233,636 - - - 233,636

Contractual - collaborations - - - - - - - - - - -

Consumer expense 7,842 33,359 760 1,256 88 - 43,305 - - - 43,305

Miscellaneous expense 1,823 1,072 4,828 160 1,074 - 8,957 1,882 1,431 3,313 12,270

Public relations 1,846 65 - 400 - - 2,311 1,058 3,424 4,482 6,793

Staff/board expense 426 1,625 2,341 - 192 - 4,584 4,789 295 5,084 9,668

Volunteer expense - - - - - 304 304 - 1,115 1,115 1,419

Depreciation expense 1,719 25,242 42,008 9,414 7,895 - 86,278 11,718 - 11,718 97,996

Total expenses $ 291,596 $ 843,686 $ 2,447,767 $ 177,742 $ 277,283 $ 10,516 $ 4,048,590 $ 640,132 $ 93,163 $ 733,295 $4,781,885

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS

September 30, 2012 and 2011

9

NOTE A - NATURE OF THE ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A summary of the organization’s significant accounting policies consistently applied in the preparation of the accompanying financial statements follows: 1. Nature of the Organization The Centre for Women, Inc. (the “Organization”) is a not-for-profit corporation located in Tampa, Florida. The Organization was established in 1977 and provides innovative services that strengthen our community, promote self-sufficiency, and enrich the lives of women, girls, families, and the elderly. These services include supportive counseling, personal development seminars, substance abuse treatment, educational opportunities, employment preparation, emergency home repairs and girls’ prevention groups.

2. Basis of Accounting The Organization follows the provisions of the Financial Accounting Standards Board Accounting Standards Codification (“FASB ASC”) and the standards of financial reporting for not-for-profit organizations as described in the American Institute of Certified Public Accountants’ Industry Guide for Not-for-Profit Organizations. Accordingly, the financial statements are prepared on an accrual basis of accounting. The financial statements of The Centre for Women, Inc. are the representation of management and include estimates of amounts and judgments it believes are reasonable under the circumstances. FASB ASC 958-205 establishes standards for general purpose external financial statements of not-for-profit organizations and requires a statement of financial position, a statement of activities and changes in net assets, and a statement of cash flows. FASB ASC 958-605 requires the Organization to distinguish between contributions that increase permanently restricted net assets, temporary restricted net assets, and unrestricted net assets. It also requires recognition of contributed services meeting certain criteria at fair value.

3. Cash Equivalents Cash equivalents consist of highly liquid short-term money market instruments with a maturity of three months or less when purchased. 4. Investments Investments consist of certificates of deposit with a maturity of three months or more when purchased.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

10

NOTE A - NATURE OF THE ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

5. Grants Receivable

The Organization receives support from various federal, state, and local grants. None of the grants receivable at September 30, 2012 and 2011 are deemed to be uncollectible. Therefore, no provision for uncollectible grants receivable has been made in the accompanying financial statements.

6. Accounts Receivable Accounts receivable consist of program service fees billed to third parties. The Organization provides for accounts receivable at an estimated net realizable value. All accounts receivable were deemed to be fully collectible and an allowance for doubtful accounts was not necessary at September 30, 2012 and 2011, respectively. 7. Property and Equipment Property and equipment are recorded at cost or at estimates of fair market value by management at the time of donation. The Organization capitalizes all expenditures for property and equipment in excess of $500. 8. Depreciation Depreciation is provided for in amounts sufficient to relate the cost of depreciable assets to operations over their estimated service lives by the straight-line method. Estimated service lives for the Organization’s property and equipment range from 3 to 40 years.

9. Contributions The Organization reports gifts of cash and other assets as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restriction. Restricted contributions are reported as unrestricted support if the restrictions are met in the same reporting period. The Organization reports gifts of land, buildings, and equipment as unrestricted support, unless donor stipulations specify how the donated assets must be used. Gifts of long-lived assets with specific restrictions that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long-lived assets are reported as restricted support. Absent explicit donor stipulations about how these long-lived assets must be maintained, the Organization reports expirations of donor restrictions when the donated or acquired long-lived assets are placed in service.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

11

NOTE A - NATURE OF THE ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - Continued

The Organization records the value of donated materials and services when there is an objective basis available to measure their value. Contributions are considered to be available for unrestricted use, unless specifically restricted by the donor, and have been treated as in-kind contributions for purposes of meeting state matching requirements. Donated materials are reflected in the accompanying financial statements at their estimated fair market values at date of receipt. The value of contributed services meeting the requirements for recognition in the financial statements was not material and has not been recorded during the years ended September 30, 2012 and 2011, respectively. The Organization also receives donated services from a variety of volunteers assisting in various fundraising events. No amounts for volunteer services have been recognized in the accompanying Statement of Activities and Changes in Net Assets since there is no objective basis to measure the value of such services. 10. Concentration of Credit Risk The Organization maintains the majority of its cash, cash equivalents and certificates of deposit with one bank that participates in the FDIC’s Transaction Account Guarantee Program. As such these funds are fully insured at September 30, 2012 and 2011.

11. Functional Expenses The costs of providing program services and other activities have been summarized on a functional basis in the Statement of Functional Expenses. Accordingly, certain costs have been allocated among the program services and supporting services benefited. 12. Reclassification Certain amounts previously reported in the financial statements for the prior year have been reclassified in order for them to be in conformity with the current year presentation.

NOTE B - INCOME TAX STATUS The Organization is exempt from federal and state income taxes under Section 501(c)(3) of the Internal Revenue Code and Chapter 220.13 of the Florida Statutes, respectively. The Organization is not aware of any tax positions it has taken that are subject to a significant degree of uncertainty. Tax years after September 30, 2009 remain subject to examination by taxing authorities.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

12

NOTE C - FAIR VALUE MEASUREMENTS

FASB ASC 820 establishes a framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (level 1 measurement) and the lowest priority to unobservable inputs (level 3 measurements).

The three levels of the fair value hierarchy under FASB ASC 820 are described below:

Level 1 Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active markets that The Centre For Women has the ability to access.

Level 2 Inputs to the valuation methodology include:

Quoted prices for similar assets or liabilities in active markets;

Quoted prices for identical or similar assets or liabilities in inactive markets;

Inputs other than quoted prices that are observable for that asset or liability;

Inputs that are derived principally from or corroborated by observable market data by correlation or other means;

If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability.

Level 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

13

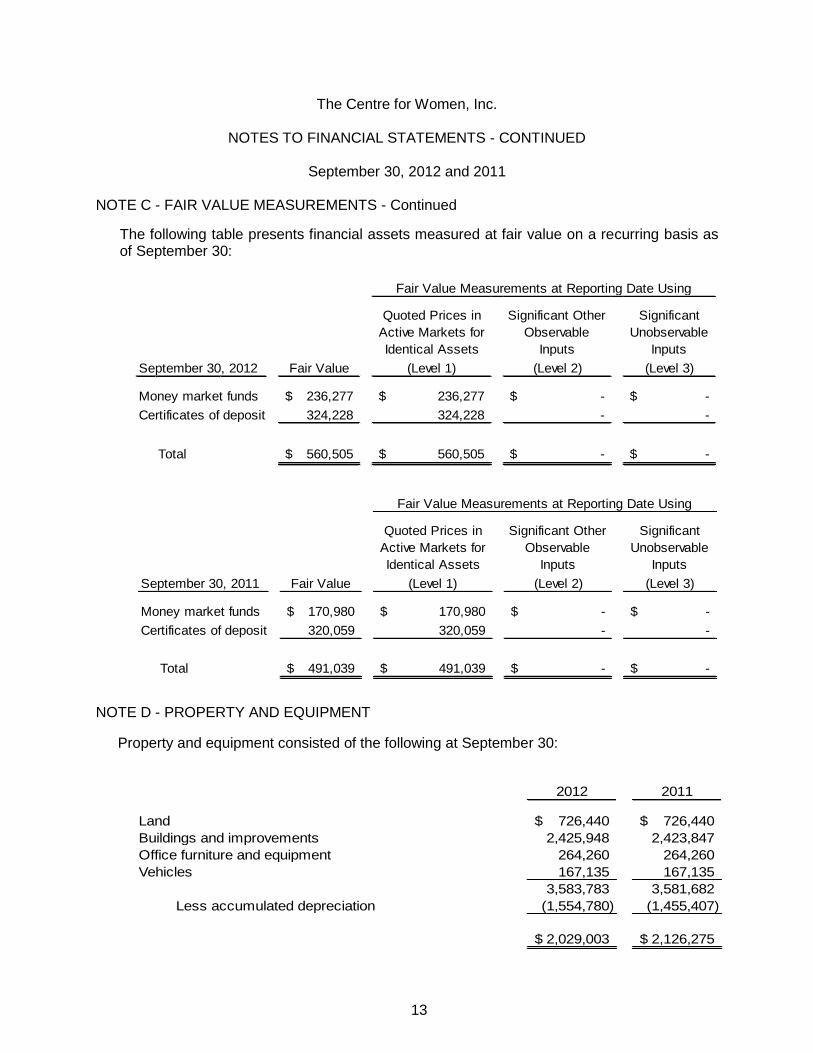

NOTE C - FAIR VALUE MEASUREMENTS - Continued

The following table presents financial assets measured at fair value on a recurring basis as of September 30:

Quoted Prices in

Active Markets for

Identical Assets

Significant Other

Observable

Inputs

Significant

Unobservable

Inputs

Fair Value (Level 1) (Level 2) (Level 3)

Money market funds 236,277$ 236,277$ -$ -$

Certificates of deposit 324,228 324,228 - -

Total 560,505$ 560,505$ -$ -$

Fair Value Measurements at Reporting Date Using

September 30, 2012

Quoted Prices in

Active Markets for

Identical Assets

Significant Other

Observable

Inputs

Significant

Unobservable

Inputs

Fair Value (Level 1) (Level 2) (Level 3)

Money market funds 170,980$ 170,980$ -$ -$

Certificates of deposit 320,059 320,059 - -

Total 491,039$ 491,039$ -$ -$

Fair Value Measurements at Reporting Date Using

September 30, 2011

NOTE D - PROPERTY AND EQUIPMENT

Property and equipment consisted of the following at September 30:

2012 2011

Land 726,440$ 726,440$

Buildings and improvements 2,425,948 2,423,847

Office furniture and equipment 264,260 264,260

Vehicles 167,135 167,135

3,583,783 3,581,682

Less accumulated depreciation (1,554,780) (1,455,407)

2,029,003$ 2,126,275$

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

14

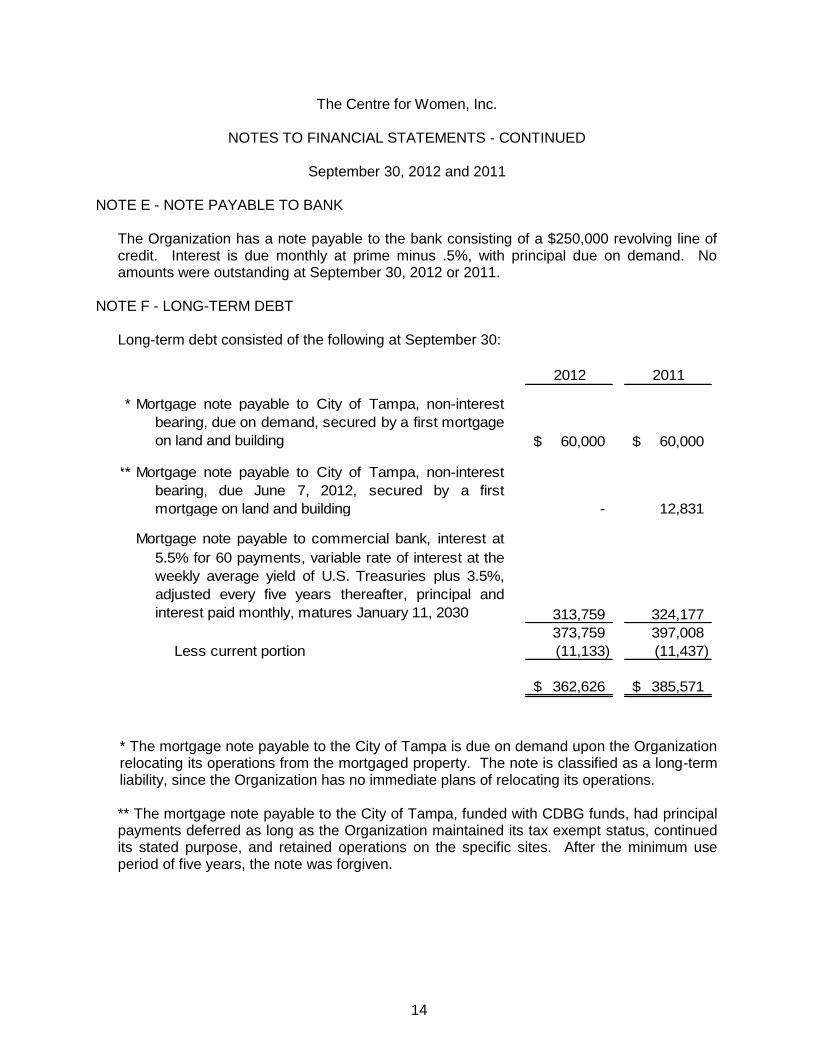

NOTE E - NOTE PAYABLE TO BANK The Organization has a note payable to the bank consisting of a $250,000 revolving line of credit. Interest is due monthly at prime minus .5%, with principal due on demand. No amounts were outstanding at September 30, 2012 or 2011.

NOTE F - LONG-TERM DEBT

Long-term debt consisted of the following at September 30:

2012 2011

*

60,000$ 60,000$

**

- 12,831

313,759 324,177

373,759 397,008

Less current portion (11,133) (11,437)

362,626$ 385,571$

Mortgage note payable to commercial bank, interest at

5.5% for 60 payments, variable rate of interest at the

weekly average yield of U.S. Treasuries plus 3.5%,

adjusted every five years thereafter, principal and

interest paid monthly, matures January 11, 2030

Mortgage note payable to City of Tampa, non-interest

bearing, due June 7, 2012, secured by a first

mortgage on land and building

Mortgage note payable to City of Tampa, non-interest

bearing, due on demand, secured by a first mortgage

on land and building

* The mortgage note payable to the City of Tampa is due on demand upon the Organization relocating its operations from the mortgaged property. The note is classified as a long-term liability, since the Organization has no immediate plans of relocating its operations. ** The mortgage note payable to the City of Tampa, funded with CDBG funds, had principal payments deferred as long as the Organization maintained its tax exempt status, continued its stated purpose, and retained operations on the specific sites. After the minimum use period of five years, the note was forgiven.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

15

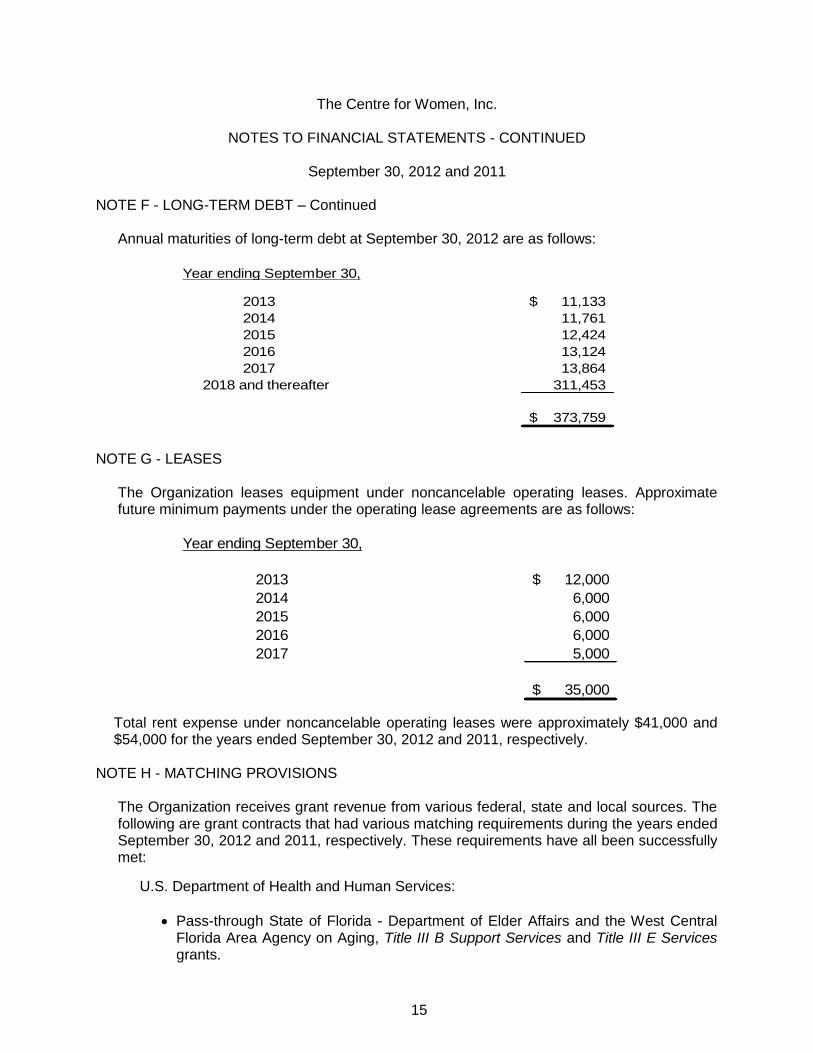

NOTE F - LONG-TERM DEBT – Continued

Annual maturities of long-term debt at September 30, 2012 are as follows:

Year ending September 30,

2013 11,133$

2014 11,761

2015 12,424

2016 13,124

2017 13,864

2018 and thereafter 311,453

373,759$

NOTE G - LEASES

The Organization leases equipment under noncancelable operating leases. Approximate future minimum payments under the operating lease agreements are as follows:

Year ending September 30,

2013 12,000$

2014 6,000

2015 6,000

2016 6,000

2017 5,000

35,000$

Total rent expense under noncancelable operating leases were approximately $41,000 and $54,000 for the years ended September 30, 2012 and 2011, respectively.

NOTE H - MATCHING PROVISIONS The Organization receives grant revenue from various federal, state and local sources. The following are grant contracts that had various matching requirements during the years ended September 30, 2012 and 2011, respectively. These requirements have all been successfully met:

U.S. Department of Health and Human Services:

Pass-through State of Florida - Department of Elder Affairs and the West Central Florida Area Agency on Aging, Title III B Support Services and Title III E Services grants.

The Centre for Women, Inc.

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2012 and 2011

16

NOTE H - MATCHING PROVISIONS – Continued

Pass-through State of Florida Department of Children and Families, and Central Florida Behavioral Network Block Grant for Prevention and Treatment of Substance Abuse.

State of Florida Agency for Workforce Innovation Displaced Homemaker Project.

Hillsborough County, Florida - Department of Health and Social Services, Success Strategies Grant.

NOTE I - 401(k) SAVINGS PLAN

The Organization leases its employees through a Professional Employer Organization (PEO). Furthermore, the Organization participates in the PEO’s 401(k) savings plan (the “Plan”) to provide a fund for retirement, disability, or death benefits. The Plan allows for discretionary matching contributions without a required mandatory matching provision.

Contributions to the Plan are determined by the Organization on an annual basis. Approximately $13,000 and $37,000 of contributions were made for the years ended September 30, 2012 and 2011, respectively.

NOTE J - SUBSEQUENT EVENTS

The Organization has evaluated events and transactions occurring subsequent to September 30, 2012 as of January 16, 2013, which is the date the financial statements were available to be issued.

17

SUPPLEMENTAL INFORMATION

18

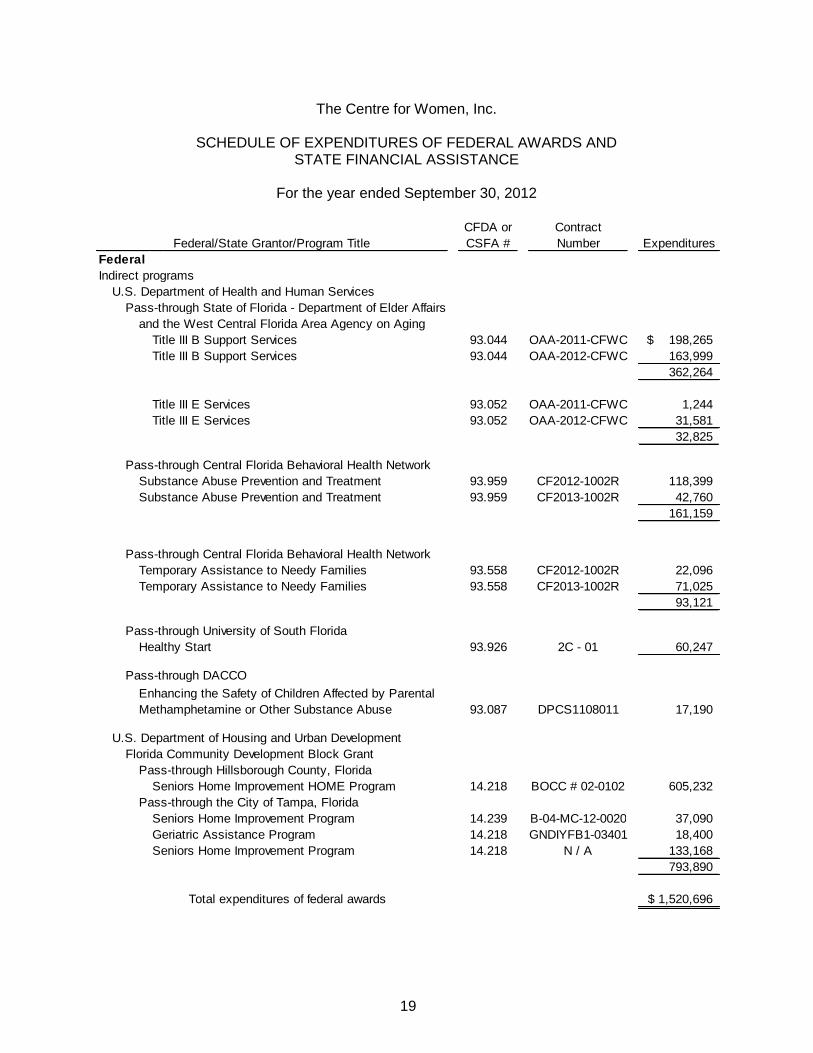

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE

THE CENTRE FOR WOMEN, INC.

For the year ended September 30, 2012

19

The Centre for Women, Inc.

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE

For the year ended September 30, 2012

CFDA or Contract

CSFA # Number Expenditures

FederalIndirect programs

U.S. Department of Health and Human Services

Pass-through State of Florida - Department of Elder Affairs

and the West Central Florida Area Agency on Aging

Title III B Support Services 93.044 OAA-2011-CFWC 198,265$

Title III B Support Services 93.044 OAA-2012-CFWC 163,999

362,264

Title III E Services 93.052 OAA-2011-CFWC 1,244

Title III E Services 93.052 OAA-2012-CFWC 31,581

32,825

Pass-through Central Florida Behavioral Health Network

Substance Abuse Prevention and Treatment 93.959 CF2012-1002R 118,399

Substance Abuse Prevention and Treatment 93.959 CF2013-1002R 42,760

161,159

Pass-through Central Florida Behavioral Health Network

Temporary Assistance to Needy Families 93.558 CF2012-1002R 22,096

Temporary Assistance to Needy Families 93.558 CF2013-1002R 71,025

93,121

Pass-through University of South Florida

Healthy Start 93.926 2C - 01 60,247

Pass-through DACCO

93.087 DPCS1108011 17,190

U.S. Department of Housing and Urban Development

Florida Community Development Block Grant

Pass-through Hillsborough County, Florida

Seniors Home Improvement HOME Program 14.218 BOCC # 02-0102 605,232

Pass-through the City of Tampa, Florida

Seniors Home Improvement Program 14.239 B-04-MC-12-0020 37,090

Geriatric Assistance Program 14.218 GNDIYFB1-03401 18,400

Seniors Home Improvement Program 14.218 N / A 133,168

793,890

Total expenditures of federal awards 1,520,696$

Federal/State Grantor/Program Title

Enhancing the Safety of Children Affected by Parental

Methamphetamine or Other Substance Abuse

20

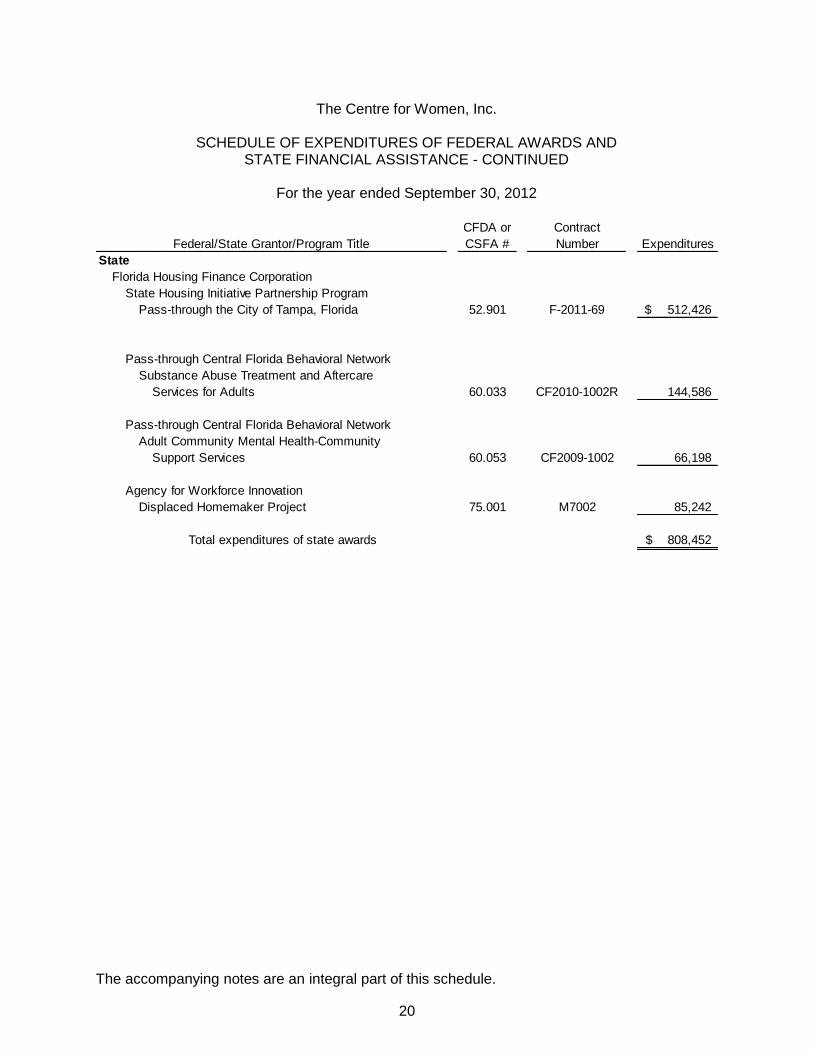

The Centre for Women, Inc.

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE - CONTINUED

For the year ended September 30, 2012

CFDA or Contract

CSFA # Number Expenditures

StateFlorida Housing Finance Corporation

State Housing Initiative Partnership Program

Pass-through the City of Tampa, Florida 52.901 F-2011-69 512,426$

Pass-through Central Florida Behavioral Network

Substance Abuse Treatment and Aftercare

Services for Adults 60.033 CF2010-1002R 144,586

Pass-through Central Florida Behavioral Network

Adult Community Mental Health-Community

Support Services 60.053 CF2009-1002 66,198

Agency for Workforce Innovation

Displaced Homemaker Project 75.001 M7002 85,242

Total expenditures of state awards 808,452$

Federal/State Grantor/Program Title

The accompanying notes are an integral part of this schedule.

21

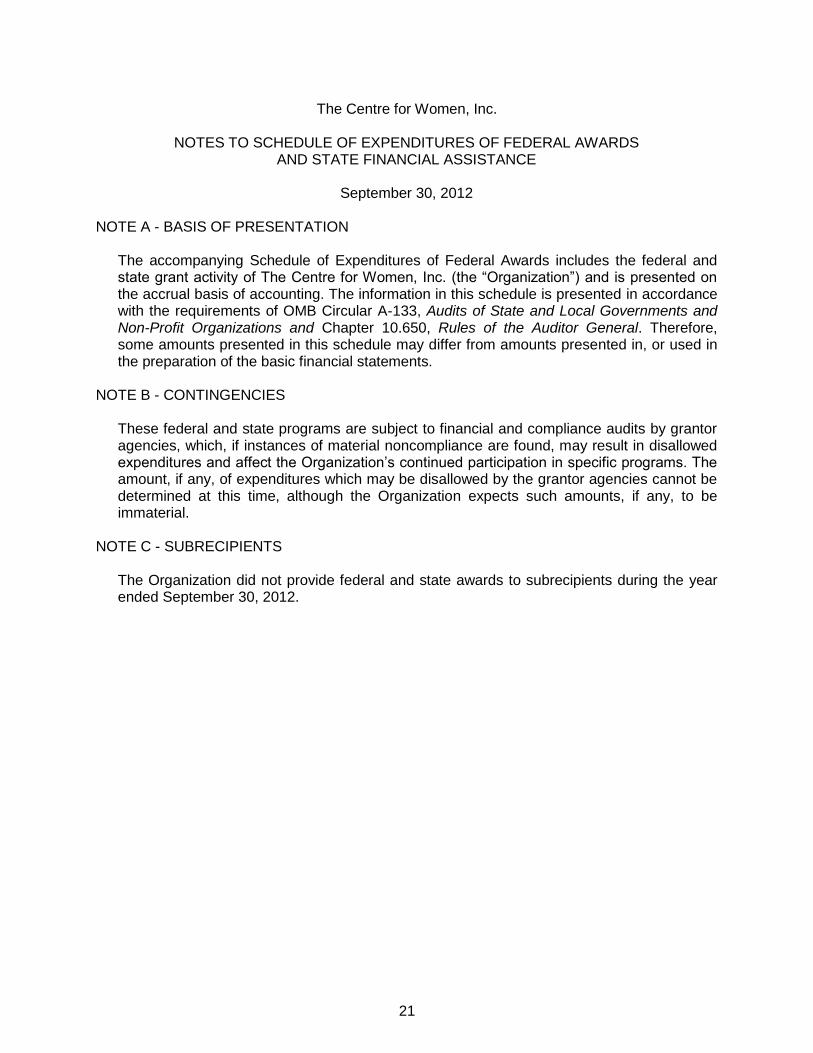

The Centre for Women, Inc.

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE

September 30, 2012

NOTE A - BASIS OF PRESENTATION

The accompanying Schedule of Expenditures of Federal Awards includes the federal and state grant activity of The Centre for Women, Inc. (the “Organization”) and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of OMB Circular A-133, Audits of State and Local Governments and Non-Profit Organizations and Chapter 10.650, Rules of the Auditor General. Therefore, some amounts presented in this schedule may differ from amounts presented in, or used in the preparation of the basic financial statements.

NOTE B - CONTINGENCIES These federal and state programs are subject to financial and compliance audits by grantor agencies, which, if instances of material noncompliance are found, may result in disallowed expenditures and affect the Organization’s continued participation in specific programs. The amount, if any, of expenditures which may be disallowed by the grantor agencies cannot be determined at this time, although the Organization expects such amounts, if any, to be immaterial.

NOTE C - SUBRECIPIENTS The Organization did not provide federal and state awards to subrecipients during the year ended September 30, 2012.

22

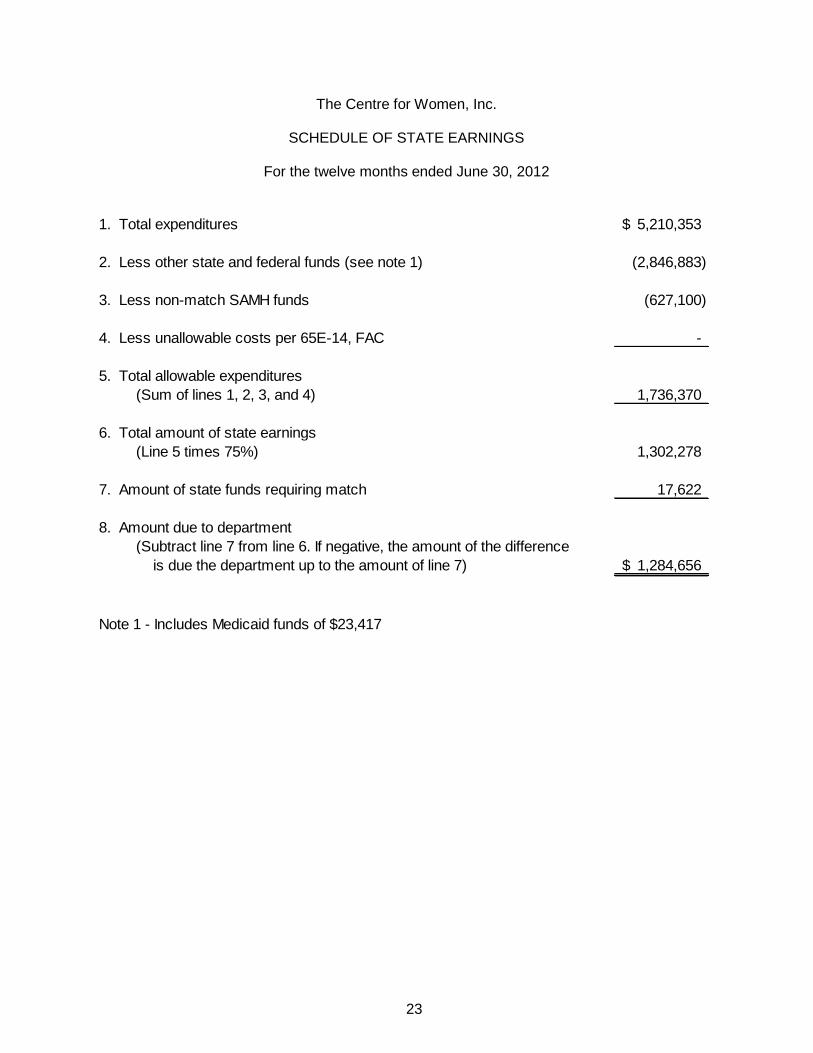

SCHEDULE OF STATE EARNINGS

THE CENTRE FOR WOMEN, INC.

For the twelve months ended June 30, 2012

23

The Centre for Women, Inc.

SCHEDULE OF STATE EARNINGS

For the twelve months ended June 30, 2012

1. Total expenditures 5,210,353$

2. Less other state and federal funds (see note 1) (2,846,883)

3. Less non-match SAMH funds (627,100)

4. Less unallowable costs per 65E-14, FAC -

5. Total allowable expenditures

(Sum of lines 1, 2, 3, and 4) 1,736,370

6. Total amount of state earnings

(Line 5 times 75%) 1,302,278

7. Amount of state funds requiring match 17,622

8. Amount due to department

(Subtract line 7 from line 6. If negative, the amount of the difference

is due the department up to the amount of line 7) 1,284,656$

Note 1 - Includes Medicaid funds of $23,417

24

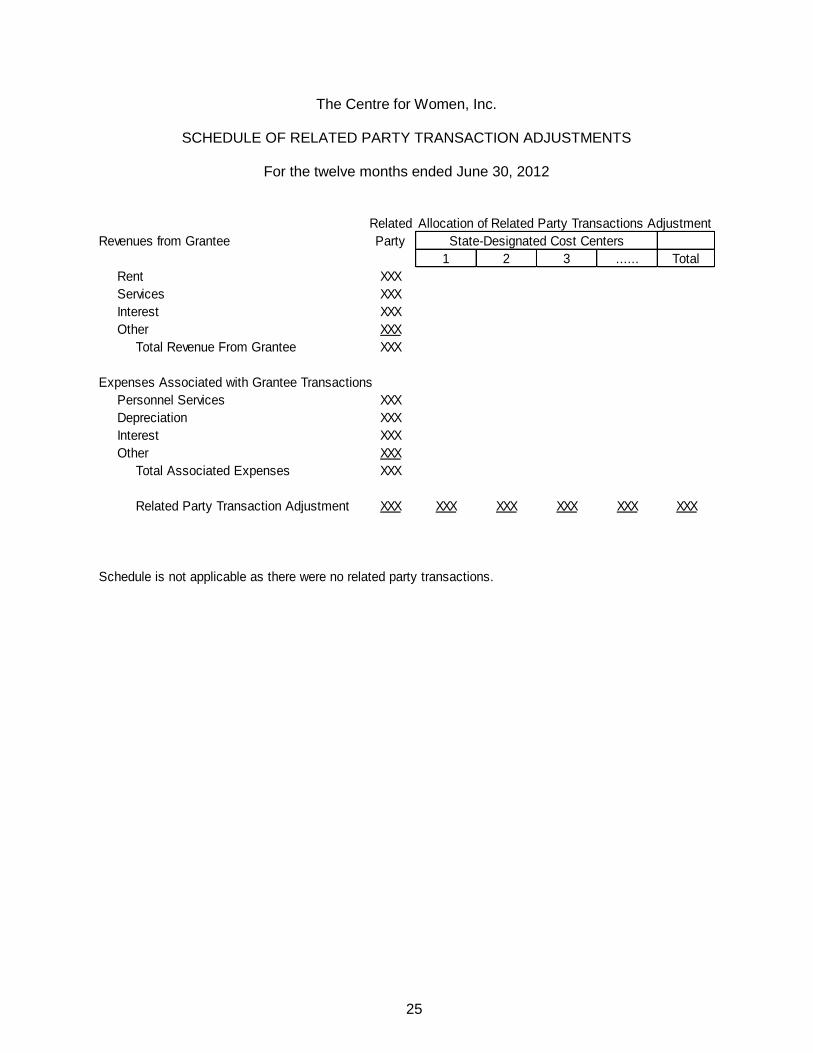

SCHEDULE OF RELATED PARTY TRANSACTION ADJUSTMENTS

THE CENTRE FOR WOMEN, INC.

For the twelve months ended June 30, 2012

25

The Centre for Women, Inc.

SCHEDULE OF RELATED PARTY TRANSACTION ADJUSTMENTS

For the twelve months ended June 30, 2012

Related Allocation of Related Party Transactions Adjustment

Revenues from Grantee Party State-Designated Cost Centers

1 2 3 ...... Total

Rent XXX

Services XXX

Interest XXX

Other XXX

Total Revenue From Grantee XXX

Expenses Associated with Grantee Transactions

Personnel Services XXX

Depreciation XXX

Interest XXX

Other XXX

Total Associated Expenses XXX

Related Party Transaction Adjustment XXX XXX XXX XXX XXX XXX

Schedule is not applicable as there were no related party transactions.

26

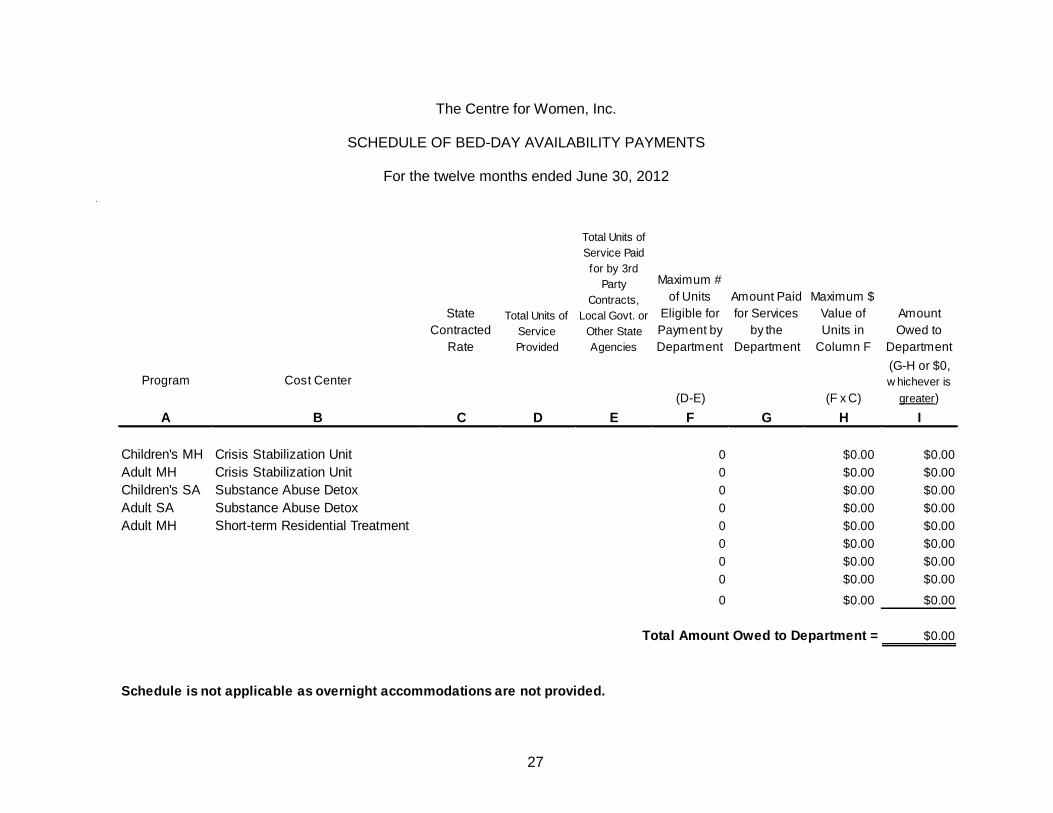

SCHEDULE OF BED-DAY AVAILABILITY PAYMENTS

THE CENTRE FOR WOMEN, INC.

For the twelve months ended June 30, 2012

27

The Centre for Women, Inc.

SCHEDULE OF BED-DAY AVAILABILITY PAYMENTS

For the twelve months ended June 30, 2012

State

Contracted

Rate

Total Units of

Service

Provided

Total Units of

Service Paid

for by 3rd

Party

Contracts,

Local Govt. or

Other State

Agencies

Maximum #

of Units

Eligible for

Payment by

Department

Amount Paid

for Services

by the

Department

Maximum $

Value of

Units in

Column F

Amount

Owed to

Department

Program Cost Center

(D-E) (F x C)

(G-H or $0,

w hichever is

greater)

A B C D E F G H I

Children's MH Crisis Stabilization Unit 0 $0.00 $0.00

Adult MH Crisis Stabilization Unit 0 $0.00 $0.00

Children's SA Substance Abuse Detox 0 $0.00 $0.00

Adult SA Substance Abuse Detox 0 $0.00 $0.00

Adult MH Short-term Residential Treatment 0 $0.00 $0.00

0 $0.00 $0.00

0 $0.00 $0.00

0 $0.00 $0.00

0 $0.00 $0.00

Total Amount Owed to Department = $0.00

Schedule is not applicable as overnight accommodations are not provided.

28

PROGRAM / COST CENTER ACTUAL EXPENSES AND REVENUE SCHEDULE

THE CENTRE FOR WOMEN, INC.

For the twelve months ended June 30, 2012

29

The Centre for Women, Inc.

SUBSTANCE ABUSE AND MENTAL HEALTH SERVICES PROGRAM / COST CENTER ACTUAL EXPENSES AND REVENUE SCHEDULE

For the twelve months ended June 30, 2012 CONTRACT # CF 1329-1017

FUNDING SOURCES & REVENUES AssessmentCase

Management Outpatient Prevention Intervention Aftercare Incentives Outreach

Total for Project

Recovery

Total for State

SAMH-Funded

Cost Centers

Total for Non-

State-Funded SAMH Cost

Centers

Total for all State-

Designated SAMH Cost

Centers

Non-SAMH Cost

CenterTotal

FundingIA . ST A T E SA M H F UN D IN G

(1) Central Florida Behavioral Health Network 22,948$ 4,645$ 294,336$ -$ 101,497$ 12,279$ 1,838$ 22,345$ 459,888$ 459,888$ -$ 459,888$ 459,888$

(2) Department o f Children and Familes - - - - - - - - - - - - 30,833 30,833

(3) - - - - - - - - - - - - - -

(4) - - - - - - - - - - - - - -

(5) - - - - - - - - - - - - - -

(6) From other districts - - - - - - - - - - - - - -

22,948 4,645 294,336 - 101,497 12,279 1,838 22,345 459,888 459,888 - 459,888 30,833 490,721

IB . OT H ER GOVER N M EN T F UN D IN G

(1) Other state agency funding - - - - - - - - - - - - - -

(2) M edicaid 420 - 18,649 - - - - - 19,069 19,069 - 19,069 - 19,069

(3) Local government - - 47,524 - - - - - 47,524 47,524 - 47,524 - 47,524

(4) Federal grants and contracts - - - - - - - - - - - - - -

(5) In-kind from local government only - - - - - - - - - - - - - -

420 - 66,173 - - - - - 66,593 66,593 - 66,593 - 66,593

IC . A LL OT H ER R EVEN UES

(1) First & second party payments 1,049 - 15,524 - 4,406 - - - 20,979 20,979 - 20,979 - 20,979

(2) Third party payments (except M edicare) - - - - - - - - - - - - - -

(3) M edicare - - - - - - - - - - - - - -

(4) Contributions and donations - - 56 - - - - - 56 56 - 56 - 56

(5) Other 16,325 3,304 226,567 - 72,197 8,734 - - 327,127 327,127 - 327,127 - 327,127

(6) In-kind - - - - - - - - - - - - - -

17,374 3,304 242,147 - 76,603 8,734 - - 348,162 348,162 - 348,162 - 348,162

T OT A L F UN D IN G 40,742$ 7,949$ 602,656$ -$ 178,100$ 21,013$ 1,838$ 22,345$ 874,643$ 874,643$ -$ 874,643$ 30,833$ 905,476$

T OT A L ST A T E SA M H F UN D IN G

T OT A L OT H ER GOVER N M EN T F UN D IN G

T OT A L A LL OT H ER R EVEN UES

30

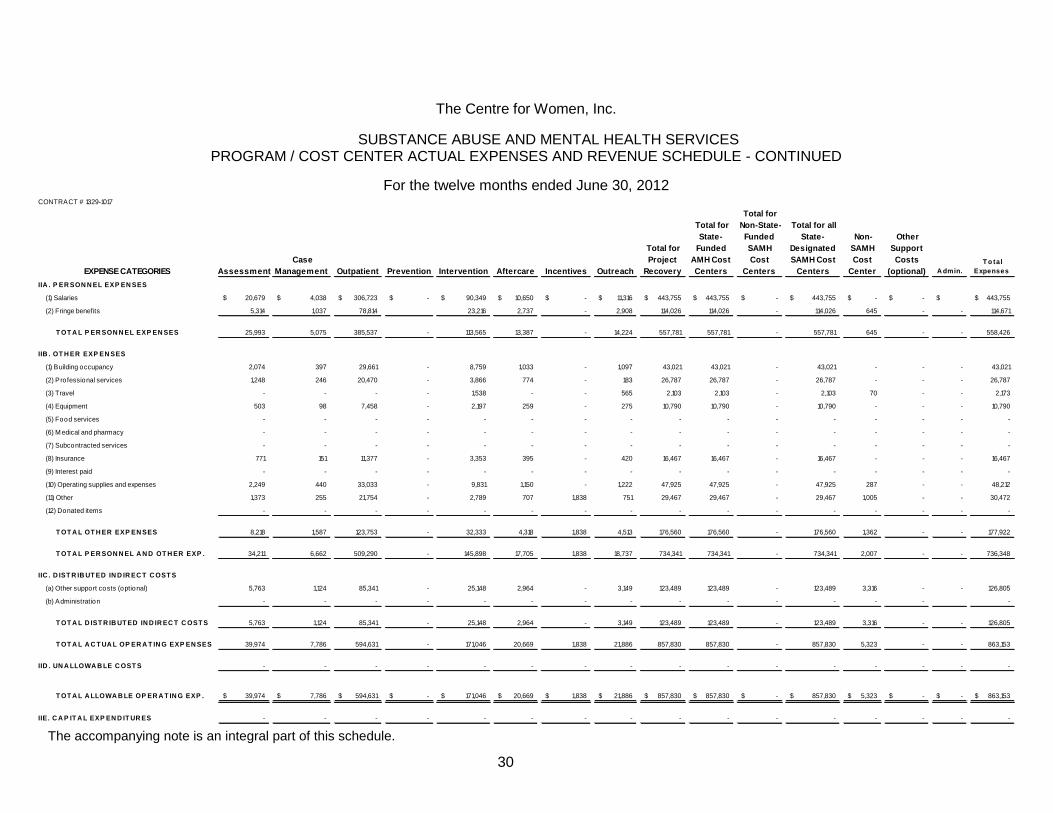

The Centre for Women, Inc.

SUBSTANCE ABUSE AND MENTAL HEALTH SERVICES PROGRAM / COST CENTER ACTUAL EXPENSES AND REVENUE SCHEDULE - CONTINUED

For the twelve months ended June 30, 2012

CONTRACT # 1329-1017

EXPENSE CATEGORIES Assessment Case

Management

Outpatient

Prevention

Intervention Aftercare Incentives Outreach

Total for Project

Recovery

Total for State-

Funded AMH Cost Centers

Total for Non-State-Funded SAMH Cost

Centers

Total for all State-

Designated SAMH Cost

Centers

Non-SAMH Cost

Center

Other Support Costs

(optional) A dmin. T o tal

Expenses

IIA . P ER SON N EL EXP EN SES

(1) Salaries 20,679$ 4,038$ 306,723$ -$ 90,349$ 10,650$ -$ 11,316$ 443,755$ 443,755$ -$ 443,755$ -$ -$ $ 443,755$

(2) Fringe benefits 5,314 1,037 78,814 23,216 2,737 - 2,908 114,026 114,026 - 114,026 645 - - 114,671

25,993 5,075 385,537 - 113,565 13,387 - 14,224 557,781 557,781 - 557,781 645 - - 558,426

IIB . OT H ER EXP EN SES

(1) Building occupancy 2,074 397 29,661 - 8,759 1,033 - 1,097 43,021 43,021 - 43,021 - - - 43,021

(2) Professional services 1,248 246 20,470 - 3,866 774 - 183 26,787 26,787 - 26,787 - - - 26,787

(3) Travel - - - - 1,538 - - 565 2,103 2,103 - 2,103 70 - - 2,173

(4) Equipment 503 98 7,458 - 2,197 259 - 275 10,790 10,790 - 10,790 - - - 10,790

(5) Food services - - - - - - - - - - - - - - - -

(6) M edical and pharmacy - - - - - - - - - - - - - - - -

(7) Subcontracted services - - - - - - - - - - - - - - - -

(8) Insurance 771 151 11,377 - 3,353 395 - 420 16,467 16,467 - 16,467 - - - 16,467

(9) Interest paid - - - - - - - - - - - - - - - -

(10) Operating supplies and expenses 2,249 440 33,033 - 9,831 1,150 - 1,222 47,925 47,925 - 47,925 287 - - 48,212

(11) Other 1,373 255 21,754 - 2,789 707 1,838 751 29,467 29,467 - 29,467 1,005 - - 30,472

(12) Donated items - - - - - - - - - - - - - - - -

8,218 1,587 123,753 - 32,333 4,318 1,838 4,513 176,560 176,560 - 176,560 1,362 - - 177,922

34,211 6,662 509,290 - 145,898 17,705 1,838 18,737 734,341 734,341 - 734,341 2,007 - - 736,348

IIC . D IST R IB UT ED IN D IR EC T C OST S

(a) Other support costs (optional) 5,763 1,124 85,341 - 25,148 2,964 - 3,149 123,489 123,489 - 123,489 3,316 - - 126,805

(b) Administration - - - - - - - - - - - - - - -

5,763 1,124 85,341 - 25,148 2,964 - 3,149 123,489 123,489 - 123,489 3,316 - - 126,805

39,974 7,786 594,631 - 171,046 20,669 1,838 21,886 857,830 857,830 - 857,830 5,323 - - 863,153

IID . UN A LLOWA B LE C OST S - - - - - - - - - - - - - - - -

39,974$ 7,786$ 594,631$ -$ 171,046$ 20,669$ 1,838$ 21,886$ 857,830$ 857,830$ -$ 857,830$ 5,323$ -$ -$ 863,153$

IIE. C A P IT A L EXP EN D IT UR ES - - - - - - - - - - - - - - - -

T OT A L D IST R IB UT ED IN D IR EC T C OST S

T OT A L A LLOWA B LE OP ER A T IN G EXP .

T OT A L A C T UA L OP ER A T IN G EXP EN SES

T OT A L P ER SON N EL EXP EN SES

T OT A L OT H ER EXP EN SES

T OT A L P ER SON N EL A N D OT H ER EXP .

The accompanying note is an integral part of this schedule.

31

The Centre for Women, Inc.

NOTE TO SCHEDULE OF STATE EARNINGS AND PROGRAM / COST CENTER ACTUAL EXPENSES AND REVENUE SCHEDULE

June 30, 2012

NOTE A - BASIS OF PRESENTATION

The accompanying Schedule of State Earnings and Program / Cost Center Actual Expenses and Revenue Schedule includes activities of The Centre for Women, Inc.’s Project Recovery Program and is required by the State of Florida Department of Children and Families (DCF) Alcohol, Drug Abuse and Mental Health Contract. The information in the schedule is presented on the accrual basis of accounting. The Schedule of Related Party Transaction Adjustments and Schedule of Bed-Day Availability Payments is also required schedules by DCF. However, the schedule is not applicable to The Centre for Women, Inc. as there were no related party transactions, nor does The Centre for Women, Inc. provide overnight accommodations. The DCF requires that these schedules be presented for the twelve months ended June 30, 2012. As such, the date of these schedules does not coincide with the date of the financial statements.

32

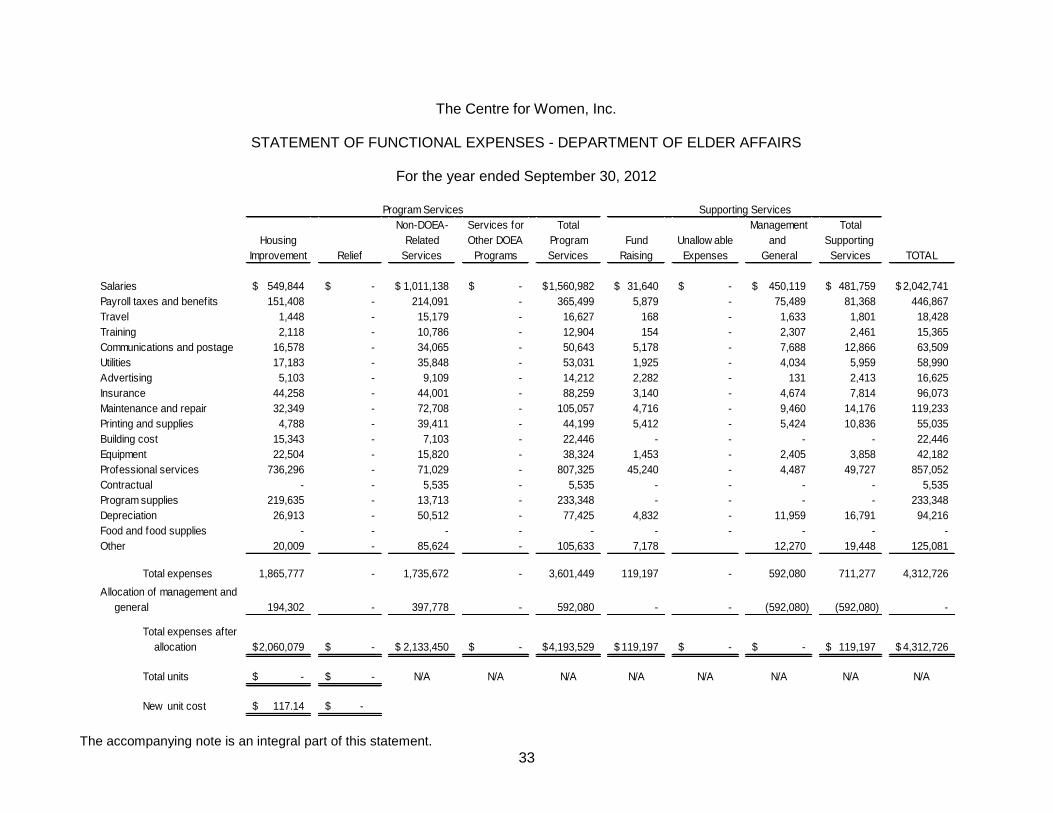

STATEMENT OF FUNCTIONAL EXPENSES - DEPARTMENT OF ELDER AFFAIRS

THE CENTRE FOR WOMEN, INC.

For the year ended September 30, 2012

The accompanying note is an integral part of this statement.

33

The Centre for Women, Inc.

STATEMENT OF FUNCTIONAL EXPENSES - DEPARTMENT OF ELDER AFFAIRS

For the year ended September 30, 2012

Non-DOEA- Services for Total Management Total

Housing Related Other DOEA Program Fund Unallow able and Supporting

Improvement Relief Services Programs Services Raising Expenses General Services TOTAL

Salaries 549,844$ -$ 1,011,138$ -$ 1,560,982$ 31,640$ -$ 450,119$ 481,759$ 2,042,741$

Payroll taxes and benefits 151,408 - 214,091 - 365,499 5,879 - 75,489 81,368 446,867

Travel 1,448 - 15,179 - 16,627 168 - 1,633 1,801 18,428

Training 2,118 - 10,786 - 12,904 154 - 2,307 2,461 15,365

Communications and postage 16,578 - 34,065 - 50,643 5,178 - 7,688 12,866 63,509

Utilities 17,183 - 35,848 - 53,031 1,925 - 4,034 5,959 58,990

Advertising 5,103 - 9,109 - 14,212 2,282 - 131 2,413 16,625

Insurance 44,258 - 44,001 - 88,259 3,140 - 4,674 7,814 96,073

Maintenance and repair 32,349 - 72,708 - 105,057 4,716 - 9,460 14,176 119,233

Printing and supplies 4,788 - 39,411 - 44,199 5,412 - 5,424 10,836 55,035

Building cost 15,343 - 7,103 - 22,446 - - - - 22,446

Equipment 22,504 - 15,820 - 38,324 1,453 - 2,405 3,858 42,182

Professional services 736,296 - 71,029 - 807,325 45,240 - 4,487 49,727 857,052

Contractual - - 5,535 - 5,535 - - - - 5,535

Program supplies 219,635 - 13,713 - 233,348 - - - - 233,348

Depreciation 26,913 - 50,512 - 77,425 4,832 - 11,959 16,791 94,216

Food and food supplies - - - - - - - - - -

Other 20,009 - 85,624 - 105,633 7,178 12,270 19,448 125,081

Total expenses 1,865,777 - 1,735,672 - 3,601,449 119,197 - 592,080 711,277 4,312,726

Allocation of management and

general 194,302 - 397,778 - 592,080 - - (592,080) (592,080) -

Total expenses after

allocation 2,060,079$ -$ 2,133,450$ -$ 4,193,529$ 119,197$ -$ -$ 119,197$ 4,312,726$

Total units -$ -$ N/A N/A N/A N/A N/A N/A N/A N/A

New unit cost 117.14$ -$

Program Services Supporting Services

34

The Centre for Women, Inc.

NOTE TO STATEMENT OF FUNCTIONAL EXPENSES - DEPARTMENT OF ELDER AFFAIRS

September 30, 2012

NOTE A - BASIS OF PRESENTATION

The accompanying Statement of Functional Expenses - Department of Elder Affairs includes expenses incurred by The Centre for Women, Inc. through the Caregiver and Housing Improvement Programs, and is required by the State of Florida Department of Elder Affairs. The information in this schedule is presented on the accrual basis of accounting. These funds are passed through from the West Central Florida Area Agency on Aging and are included in the Statement of Activities and Changes in Net Assets as part of federal grants. The expenses of the programs are included on the Statement of Functional Expenses as part of Community Based Services.

35

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN

AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

THE CENTRE FOR WOMEN, INC.

September 30, 2012

36

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of Directors The Centre for Women, Inc.

We have audited the financial statements of The Centre for Women, Inc. (the “Organization”) as of and for the year ended September 30, 2012, and have issued our report thereon, dated January 16, 2013. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States of America. Internal Control Over Financial Reporting

Management of the Organization is responsible for establishing and maintaining effective internal control over financial reporting. In planning and performing our audit, we considered the Organization’s internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Organization’s internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the Organization’s internal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not

allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement will not be prevented, or detected and corrected, on a timely basis.

Our consideration of internal control over financial reporting was for the limited purpose

described in the first paragraph of this section and would not necessarily identify all deficiencies in internal control that might be significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over financial reporting that we consider to be material weaknesses, as defined above.

RIVERO, GORDIMER & COMPANY, P.A.

CERTIFIED PUBLIC ACCOUNTANTS

ONE TAMPA CITY CENTER • SUITE 2600 • 201 N. FRANKLIN STREET • P. O. BOX 172359 • TAMPA, FLORIDA 33672 • 813- 875-7774 FAX 813-874-6785

Member

American Institute of Certified Public Accountants

Florida Institute of Certified Public Accountants

Cesar J. Rivero Sam A. Lazzara

Herman V. Lazzara Stephen G. Douglas

Marc D. Sasser Michael E. Helton

Richard B. Gordimer, of Counsel

37

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Organization’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

This report is intended for the information and use of management, the Board of Directors, and others within the entity, and federal and state awarding agencies and is not intended to be and should not be used by anyone other than these specified parties. Tampa, Florida January 16, 2013

38

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR FEDERAL PROGRAM

AND STATE PROJECT AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133 AND CHAPTER 10.650,

RULES OF THE AUDITOR GENERAL

THE CENTRE FOR WOMEN, INC.

September 30, 2012

39

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH

REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133 AND CHAPTER 10.650, RULES OF THE AUDITOR GENERAL

Board of Directors The Centre for Women, Inc.

Compliance

We have audited The Centre for Women, Inc.’s (the “Organization") compliance with the types of compliance requirements described in the OMB Circular A-133 Compliance Supplement, and the requirements described in the Florida Department of Financial Services’ State Projects Compliance Supplement, that could have a direct and material effect on each of the Organization’s major federal programs and state projects for the year ended September 30, 2012. The Organization's major federal programs and state projects are identified in the summary of auditor's results section of the accompanying Schedule of Findings and Questioned Costs. Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs and state projects is the responsibility of the Organization’s management. Our responsibility is to express an opinion on the Organization's compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States of America, OMB Circular A-133, Audits of State, Local Governments, and Non-Profit Organizations and Chapter 10.650, Rules of the Auditor General. Those standards, OMB Circular A-133 and Chapter 10.650, Rules of the Auditor General, require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program or state project occurred. An audit includes examining, on a test basis, evidence about the Organization's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not provide a legal determination on the Organization's compliance with those requirements.

In our opinion, the Organization complied, in all material respects, with the compliance requirements referred to above that could have a direct and material effect on each of its major federal programs and state projects for the year ended September 30, 2012.

RIVERO, GORDIMER & COMPANY, P.A.

CERTIFIED PUBLIC ACCOUNTANTS

ONE TAMPA CITY CENTER • SUITE 2600 • 201 N. FRANKLIN STREET • P. O. BOX 172359 • TAMPA, FLORIDA 33672 • 813- 875-7774 FAX 813-874-6785

Member

American Institute of Certified Public Accountants

Florida Institute of Certified Public Accountants

Cesar J. Rivero Sam A. Lazzara

Herman V. Lazzara Stephen G. Douglas

Marc D. Sasser Michael E. Helton

Richard B. Gordimer, of Counsel

40

Internal Control Over Compliance

Management of the Organization is responsible for establishing and maintaining effective internal control over compliance with requirements of laws, regulations, contracts and grants applicable to federal programs and state projects. In planning and performing our audit, we considered the Organization’s internal control over compliance with requirements that could have a direct and material effect on a major federal program or state project to determine our auditing procedures for the purpose of expressing our opinion on compliance and to test and report on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.650, Rules of the Auditor General, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the Organization’s internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program or state project on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program or state project will not be prevented, or detected and corrected, on a timely basis.

Our consideration of internal control over compliance was for the limited purpose

described in the first paragraph of this section and was not designated to identify all deficiencies in internal control over compliance that might be deficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses, as defined above.

This report is intended solely for the information and use of the Organization’s

management, the Board of Directors, others within the entity, federal and state awarding agencies, and pass-through entities and is not intended to be and should not be used by anyone other than these specified parties. Tampa, Florida January 16, 2013

41

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FEDERAL PROGRAMS AND STATE PROJECTS

THE CENTRE FOR WOMEN, INC.

For the year ended September 30, 2012

42

The Centre for Women, Inc.

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

For the year ended September 30, 2012

Section I - Summary of Auditors' Results

Type of auditors' report issued

Internal control over financial reporting

Material weakness(es) identified? yes X no

Significant deficiency(s) identified that are not

considered to be material weakness(es)? yes X

Noncompliance material to financial statements noted? yes X no

Federal Awards and State Financial Assistance

Internal control over major federal programs and state projects

Material weakness(es) identified? yes X no

Significant deficency(s) identified that are not

considered to be material weakness(es)? yes X none reported

Type of auditors' report issued on compliance for

major programs

Any audit findings disclosed that are required to be reported

in accordance with section 510(a) of Circular A-133 and

Chapter 10.650, Rules of the Auditor General? yes X no

Identification of major programs and state projects:

Federal

14.218 U.S. Department of Housing and Urban Development

Community Development Block Grant

93.044 U.S. Department of Health & Human Services

Special Program for the Aging Title IIIB

State

52.901 Florida Housing Finance Corporation

State Housing Initiative Partnership Program

CFSA Number Name of State Project

CFDA Number

Financial Statements

none reported

Unqualified

Unqualified

Name of Federal Program

43

The Centre for Women, Inc.

SCHEDULE OF FINDINGS AND QUESTIONED COSTS - CONTINUED

For the year ended September 30, 2012

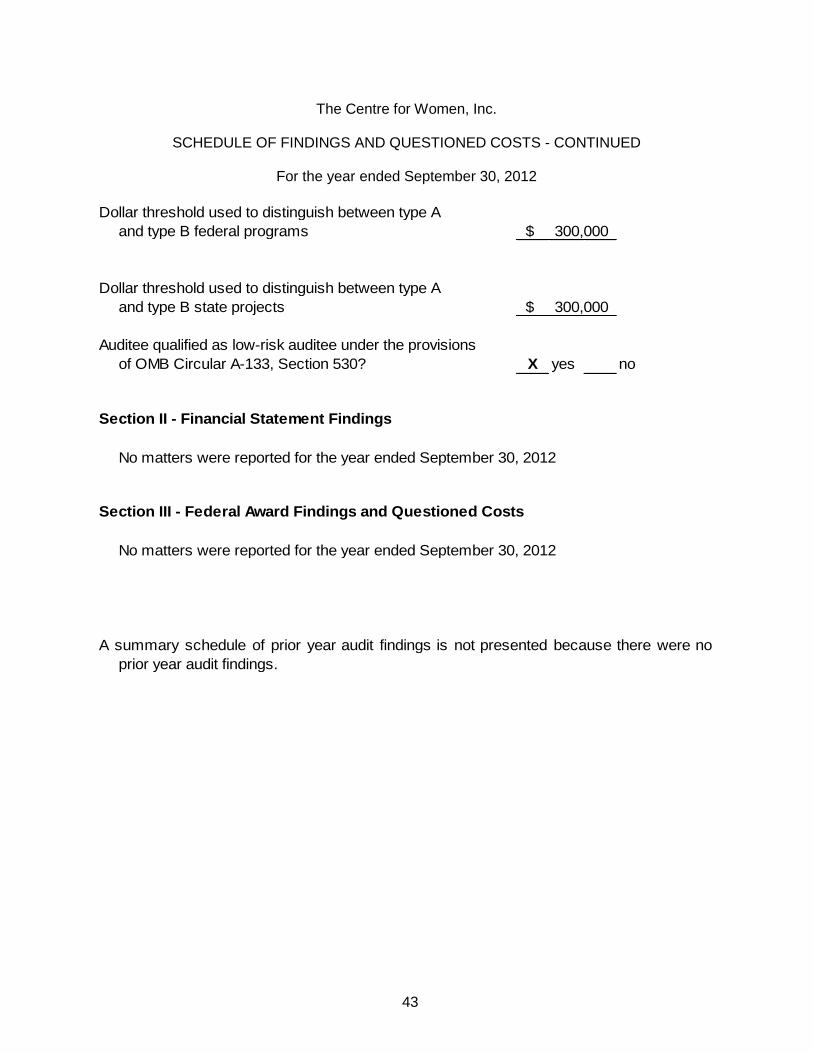

Dollar threshold used to distinguish between type A

and type B federal programs

Dollar threshold used to distinguish between type A

and type B state projects

Auditee qualified as low-risk auditee under the provisions

of OMB Circular A-133, Section 530? X yes no

Section II - Financial Statement Findings

No matters were reported for the year ended September 30, 2012

Section III - Federal Award Findings and Questioned Costs

No matters were reported for the year ended September 30, 2012

prior year audit findings.

300,000$

A summary schedule of prior year audit findings is not presented because there were no

300,000$

44

MANAGEMENT LETTER

THE CENTRE FOR WOMEN, INC.

For the year ended September 30, 2012

45

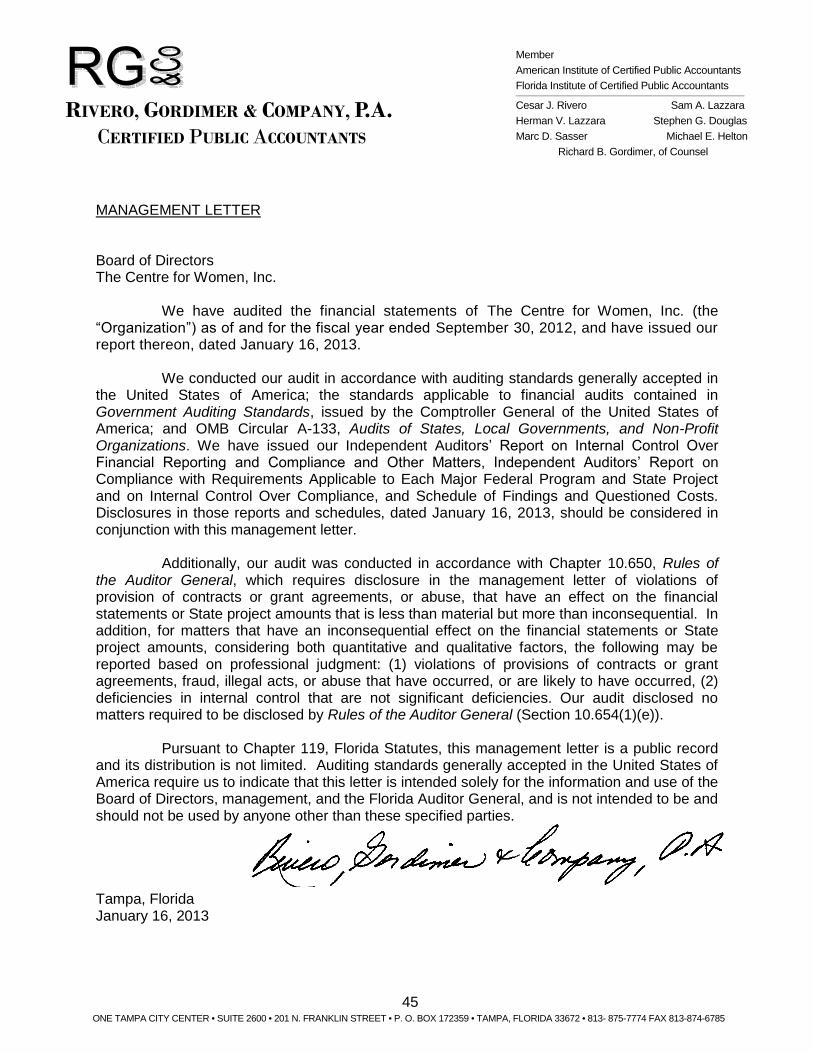

MANAGEMENT LETTER Board of Directors The Centre for Women, Inc.

We have audited the financial statements of The Centre for Women, Inc. (the “Organization”) as of and for the fiscal year ended September 30, 2012, and have issued our report thereon, dated January 16, 2013.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States of America; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. We have issued our Independent Auditors’ Report on Internal Control Over Financial Reporting and Compliance and Other Matters, Independent Auditors’ Report on Compliance with Requirements Applicable to Each Major Federal Program and State Project and on Internal Control Over Compliance, and Schedule of Findings and Questioned Costs. Disclosures in those reports and schedules, dated January 16, 2013, should be considered in conjunction with this management letter.

Additionally, our audit was conducted in accordance with Chapter 10.650, Rules of

the Auditor General, which requires disclosure in the management letter of violations of provision of contracts or grant agreements, or abuse, that have an effect on the financial statements or State project amounts that is less than material but more than inconsequential. In addition, for matters that have an inconsequential effect on the financial statements or State project amounts, considering both quantitative and qualitative factors, the following may be reported based on professional judgment: (1) violations of provisions of contracts or grant agreements, fraud, illegal acts, or abuse that have occurred, or are likely to have occurred, (2) deficiencies in internal control that are not significant deficiencies. Our audit disclosed no matters required to be disclosed by Rules of the Auditor General (Section 10.654(1)(e)).

Pursuant to Chapter 119, Florida Statutes, this management letter is a public record

and its distribution is not limited. Auditing standards generally accepted in the United States of America require us to indicate that this letter is intended solely for the information and use of the Board of Directors, management, and the Florida Auditor General, and is not intended to be and should not be used by anyone other than these specified parties.

Tampa, Florida January 16, 2013

RIVERO, GORDIMER & COMPANY, P.A.

CERTIFIED PUBLIC ACCOUNTANTS

ONE TAMPA CITY CENTER • SUITE 2600 • 201 N. FRANKLIN STREET • P. O. BOX 172359 • TAMPA, FLORIDA 33672 • 813- 875-7774 FAX 813-874-6785

Member

American Institute of Certified Public Accountants

Florida Institute of Certified Public Accountants

Cesar J. Rivero Sam A. Lazzara

Herman V. Lazzara Stephen G. Douglas

Marc D. Sasser Michael E. Helton

Richard B. Gordimer, of Counsel