Embed Size (px)

Citation preview

1

‘FINANCIALIZATION’ AND THE FUTURE OF THE NEOLIBERAL GROWTH MODEL

Terrence Casey, Rose-Hulman Institute of Technology Paper presented at the Political Studies Association Annual Conference April 2011

INTRODUCTION

The Global Financial Crisis (GFC) that struck in September 2008 was not just (to paraphrase Andrew Gamble [2009a]) a crisis of the financial sector, it was a crisis of the neoliberal growth model. Since the early 1980s, neoliberalism has reigned supreme, emerging from its Anglo-American heartlands to colonize much of the globe. Yet the global financial crisis produced obituaries that were swift and unequivocal: “…the Anglo-liberal growth model is irretrievably and irreversibly compromised” (Hay, 2010a, pp. 25-26.); “…neoliberalism has self-destructed” (Mykhnenko and Birch, 2010, p. 255); “The current crisis, and the responses to it, seem to have delivered a death blow to neo-liberalism” (Fine, 2009, p. 1). The death of the king, of course, usually signals the coronation of a new monarch. Yet alternative modes of economic governance are noteworthy in their absence (Wilson, forthcoming; Gamble, 2010).

This paper examines the role of financialization as a component of the neoliberal growth model with an eye to understanding its future. Yet this is a tough nettle to grasp. Financialization itself is a slippery concept with multiple and overlapping meanings and held in greater or lesser significance by different scholars. The role of financialization within the neoliberal growth model is equally contested, particularly its connection between neoliberal theory and neoliberal practice. Then there is the complicated question of the causal role of financialization (as opposed to the actions of specific actors in the financial sector) in the global financial crisis and what, therefore, this implies about the future of the neoliberal growth model. The sections below will examine these issues in turn and use this discussion to offer some insights on the current challenges and potential directions of economic management in the US and UK. Far from precipitating neoliberalism’s demise, events since the crash have shown the model to be politically resilient in both Britain (with a budget-slashing Conservative-led coalition government) and America (with Republican Party pushed back into fiscal conservatism by the Tea Party movement). Elements of financialization also remain firmly in place. The open question is whether growth (short-term and long-term) can be revived within terms of this unreformed model.

UNDERSTANDING FINANCIALIZATION

Copyright PSA 2011

2

Grasping the role of financialization in the neoliberal growth model is confounded by the lack of agreement among scholars on either its definition or significance. Gerald Epstein (2005, p. 3) reviews the array of definitions on offer: the ascendency of ‘shareholder value’ as a mode of corporate governance; the growing dominance of financial markets; the increasing political and economic power a new rentier class; the explosion of new financial instruments; and increased profit making through financial activity rather than trade or commodity production. Bringing these together Epstein describes financialization as the “…increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of domestic and international economies.” (2005, p. 3). Ben Fine offers a somewhat more extensive definition, echoing some of the points of Epstein. Financialization is: (1) the expansion and proliferation of financial markets over the past thirty hears; (2) the expansion of speculative assets as opposed to investment in the ‘real economy’; (3) the expansion and proliferation of financial instruments and services; (4) the increasing dominance of finance over industry; (5) a strategy of redistribution to an international rentier class (a point made more emphatically by Duménil and Lévy, 2005 and Harvey, 2005).; and (6) a strategy of debt- fuel consumption (Fine, 2009). Johnna Montgomerie highlights the systemic and relational aspects: “…financialisation offers an account of the present day capitalist dynamics where individuals, firms, and the macro-economy are increasingly mediated by new relationships within financial markets” (Montgomerie, 2008, p.234). Much like globalization (a concept which overlaps), financialization cannot easily be reduced to a simple definition without losing descriptive and analytical power. It is not one thing, but a collectivity of changes.

The most basic change is quantitative – the vast increase in the size and importance of the financial sector. Finance and insurance industries accounted for 2.5% of GDP in the United States in 1947, rising only to 4% by the late 1970s. By 2006 they commanded an 8.3% share (Philippon, 2008, p. 6). The trends were similar in the UK, with finance accounting for 5% of gross value added in 1970 and 8% in 2007 (Haldane, 2010, p. 4).1 Moving from output to profits, the US financial sector accounted for 15% of corporate profits in 1980. On the eve of the crisis in 2006 it was 27% (Financial Crisis Inquiry Commission, 2001, p. xvii).2 The change was even more dramatic in the UK. Financial intermediation accounted for around 1.5% of whole economy profits from 1948 and 1978. By 2008 it had rocketed up to 15% (Haldane, 2010, p.4). Martin Weale notes that from 1987-2007, the UK financial services sector grew at 4.7% per annum while the whole economy grew at 2.6%. The growth of the American and British financial sectors were intimately tied to increasing flows of international capital as the major exporting economies, especially Japan and (more recently) China have recycled their trade surpluses into the bond and stock markets of New York and London. However one looks at it, from the early eighties up to the present, economic growth in the US and UK has become increasingly dependent on the financial sector.

These quantitative changes were matched by even deeper qualitative changes. Financial activity is penetrating into an ever widening range of economic and social activities – not only

1 Rates were similar in other Anglo-Saxon economies, pushing around 8% of GVA in Australia and 10% in Ireland (Weale, 2009, p. 6). 2 Using pre-tax profits, Kotz finds that financial corporations rose from 13.9% of all corporate profits in the 1960s, 19.4% in the 1970s, dipping slightly to 17.2% in the 1980s, then shooting up to 25.3% in the 1990s and to 36.8% from 2000-06 (Kotz, 2008, p. 5).

Copyright PSA 2011

3

housing, but pensions, health care, etc. (Fine, 2009). Particularly in the United States, the shift from defined benefit to defined contribution pension schemes – which now constitute around 70% of all American pensions (The Economist, 9 April 2011) -- serves to provide an expanded pool of funds to institutional investors and connect individuals’ financial security directly to market movements. The primary economic role of individuals in society is thus transformed from workers-consumers to workers-consumers-investors. These changes are often (negatively) portrayed in Polanyian terms, the conceit of the neoliberal era being to abandon the security of “embedded liberalism” and expose individuals to the risks and disciplines of financial markets (Konings, 2009, p. 112).3 Thus the distance between high finance and everyday life, between global banking and household finance, has been drastically reduced (Finlayson, 2009, p. 402). A similar transformation has occurred at the corporate level, wherein the business strategies of major non-financial corporations have increasingly turned to financial intermediation rather than trade or production as a source of profit, an illustrative example being the relationship between General Motors and GMAC,4 which delivered grand profits in the bubble years and brought it to near bankruptcy in the crash. In this way even firms traditionally thought of as outside of the financial sector are ‘financialized’ in their primary activities.

This points to perhaps the most significant element of financialization: the idea of financial activity becoming a (if not the) driver of economic growth under neoliberalism. Purely as a description of events, this is a tough point to contest, as outlined above. In the major Anglo-Saxon economies, the growth in the financial sector played a major role in keeping the economy humming from the early 1990s through 2008. One can, of course, interpret these trends either positively or negatively. For those predisposed to free market approaches, increased profits in financial intermediation indicate an increased economic (and hence social) value to those activities and it is thus appropriate for investors (both large and small) to direct their resources into that sector. It is simply economic actors (rationally) following market signals. Negative interpretations note the fragile nature of growth built upon financial speculation, with its tendencies to produce bubbles – impressive looking until they burst. This, of course, is exactly what happened in this case. In this light, the spectacular growth of the financial sector was much more mirage than miracle (Haldane, 2010). When losses in the banking sector are deducted, Weale (2009, p. 7) calculates that UK GDP growth from 2000-08 would have dropped to 2.1% rather than the recorded 2.5%. To say the least, the negative interpretation has become the predominant view.

Even with this, the policy implications are less clear. One view would suggest that reliance on the financial sector is inherently unstable, and that the economy should be ‘rebalanced’ toward other sectors, mainly manufacturing – a view that has gained credence even among erstwhile free marketeers like David Cameron (Fround, et. al., 2011). Alternately the solution may be more to tinker with financial regulation and economic governance, fixing the specific problems that produced excessive and systemic risk– not a shift away from finance, but a recalibration of finance. Even here, depending on one’s interpretation of the causes of the crisis, one can adopt either a maximilist approach that calls for substantially more government

3 Viewed in Polanyian terms, this will implicitly produce a political backlash -- a new “double-movement” -- against the financialization of everyday life. 4 GMAC was originally develop to finance car purchases. By the mid-2000s it was a full-scale financial operation, with significant investment in the housing market. In the wake of GM’s government bailout under the TARP, GMAC has since been sold off as Ally Financial.

Copyright PSA 2011

4

regulation of the financial sector (FCIC, 2011), or a more minimalist approach that seeks targeted correction of both governmental and private sector failings (Roach, 2009).

For the purposes of the argument laid out here, then, financialization can best conceived of as a multifaceted phenomenon encompassing an expanding financial sector, the extension of webs of financial relationships connecting individual consumers all the way up to major corporations, and the fact that the output of the financial sector was a major factor driving economic growth for the last 20 years, at least in the US and UK (see Epstein, 2005 for a discussion of other aspects of financialization).

FINANCIALIZATION AND THE GLOBAL FINANCIAL CRISIS

The common wisdom explanation of the financial crisis goes something like this: starting with the governments of Margaret Thatcher and Ronald Reagan, the financial markets in both Britain and American were steadily deregulated, the ‘Big Bang’ deregulation of the City in 1986 and the repeal of Glass-Steagall in 1999 under President Bill Clinton (which separated commercial and investment banking) being major milestones along the way. On both sides of the Atlantic, economic policymakers – Larry Summers, Ben Bernanke, Mervyn King, and most especially Alan Greenspan – were guided by the belief that economic innovation, efficiency, and growth were best nurtured through minimal regulation. No matter how complex and opaque financial instruments were becoming, market actors would be much more effective at regulating themselves. This opened the door for financial firms to take riskier and riskier investments – investments that would ultimately create a major financial bubble.

The conditions for this came first from the expansionary monetary policies pursued by Alan Greenspan and later Ben Bernanke. Seeking to keep the economy growing in the wake of the dot.com bust and 9-11, the Federal Reserve kept interest rates too low for too long: 2001-2004 was the longest sustained expansionary monetary policy since the early 1950s (Gjerstad and Smith, p. 277). This created a flood of cheap credit, which fed into the US housing market,5 making it possible for those who would not previously qualify (for lack of a down payment, for example) to get a (subprime) mortgage. Rather than sit on these risky loans, banks then bundled these into mortgage backed securities (MBSs) and sold them on to others (the ‘originate and distribute’ strategy). Credit rating agencies facilitated this process by slapping subprime MBSs with AAA ratings. This would not have been a problem if the major Wall Street firms had just passed these risky bets on to some other sucker. Yet the capital-adequacy guidelines favored asset-backed securities and allowed firms heavily invested in them to increase their leverage, which allowed for greater profits in a booming market. Once the market crashed, on the other hand, it left these same firms dangerously exposed – and with them, the entire global financial system. The global financial crisis of 2008 was, in short, the outcome of financial markets run amok, having been cut loose from the tether of state regulation by 30 years of neoliberal reform.

5 Greenspan expressed concern about the unsustainability of the rise in house prices in mid-2005, but stopped short of calling it a bubble, suggesting there was ‘froth’ in the market (New York Times, May 21, 2005).

Copyright PSA 2011

5

Given the depths of the calamity, so the story goes, neoliberalism has been fully, finally, and forever discredited as a mode of economic governance.

There already exists a mountain of books delving into the causes of the crash (Posner, 2009, Stiglitz, 2010, and Cassidy, 2009 are perhaps the most useful books on the subject. For more concise analyses, see Coates and Dickstein, Forthcoming, and Casey, Forthcoming).6 There is neither the space to rehash the arguments here nor would be any closer to agreement on the causes of these events, no more so than we are after 80 years on the causes of the Great Depression.7 The battling concurring and dissenting opinions between the Democratic and Republican-appointed members on the Financial Crisis Inquiry Commission illustrate that we are far from a consensus in analyzing this crisis (see FCIC 2011). Moreover, it is not really necessary to retroactively discern the causes of the crisis as the central concern of this paper is prospective: Do the events of the global financial crisis, driven as it was by the financialization of the Anglo-American economies, fatally undermine the neoliberal growth model? In contrast to the common wisdom interpretation, and despite the best wishes of those who have longed for the demise of neoliberalism, I would suggest that the answer to that question is ‘no’.

FINANCIALIZATION AND THE NEOLIBERAL GROWTH MODEL

Is financialization a core element of the neoliberal growth model? If judged in terms of how the advocates of neoliberalism have described their ideas, it certainly is not. One will search in vain, for example, for any extended discussion of finance, financialization, or even the banking system in The Road to Serfdom, F.A. Hayek’s (1994 [1944]) magnum opus and semi-official bible of the liberal movement. Even though the “neoliberal experiment” has been underway for three decades, the concept of financialization is a relatively new phenomenon (Epstein, 2005, p. 3). A pre-crash elaboration of the core ideas behind neoliberalism as a model of economic governance would include:

the liberalization of markets, removing the barriers to the free movement of goods, services, and capital

the privatization of state-owned industries and the outsourcing of public services to the private sector

fiscal retrenchment through attempted reductions in overall state spending8 and reduced marginal tax rates aimed at spurring private sector investment

deregulation9 of product, labor (including through policies to reduce the power of organized labor), and capital markets (domestic and international) so as to enhance competition and innovation

6 Coates and Dickstein pin more of the blame on the lack of market regulation. Casey suggests that it was more a combination of irresponsible actions on the part of the financial sector spurred by (perverse) incentives created by government regulations. 7 Montgomerie and Williams (2009, p. 100) usefully remind us that most analysts explain the crisis within the problematic which they endorsed before the crisis began 8 This is the area where neoliberalism had the least success. See Figure 3.

Copyright PSA 2011

6

The marketization of society though the withdrawal of the state from direct economic management

a general belief in the benefits of ‘self-regulating’ free markets to deliver growth and prosperity (see Kotz, 2008, p.3; Birch and Mykhnenko, p. 5)

These ideas only gained ground after the contradictions of postwar Keynesianism, manifesting as stagflation of the 1970s, offered a political opening. The practical application of these ideas varied across the Thatcher, Reagan, and other governments, but the basic rationale was that by shifting resources out of the government’s control – where political pressures led to economically inefficient decision making – and into the private – where competition and market forces provided appropriate signals – these policies would remove the barriers to (private) investment, spur entrepreneurialism and innovation, and increase the trend growth rate of the private economy. As a description of the model, there is nothing particularly new or controversial in the above (the implications of all of this are something else entirely, of course). Certainly what has been described more recently as financialization is as a logical outgrowth of this approach to economic governance, both at the domestic and international levels. Financialization as a theoretical central tenet of the neoliberal growth model, however, is really a post hoc addition -- an addition that predates the financial crisis, but an addition that was accentuated by it.

What matters, of course, is whether this it is intellectually legitimate or practically useful to conflate neoliberalism and financialization (Duménil and Lévy, 2005; Harvey, 2005). For many analysts this connection provides both explanation and solution. The crisis began in the financial sector; it occurred because of this broad phenomenon called ‘financialization’; financialization is the heart of neoliberalism; therefore, neoliberalism is finished as a mode of economic governance and a more economically stable (and, one might add, more just) alternative will take its place. The difficulty with these stylized facts is that they largely do not fit the ‘facts on the ground’. Politicians and pundits in both London and Washington may wring their hands over the excesses of Wall Street and the City and call for the state to reassert control over financial markets, but in the actual regulatory reforms being implemented will not radically reconfigure finance in either state (see Casey, Forthcoming). Nor have the political parties and movements previously opposed to free market economics (strongly or weakly) managed to muster up any sort of viable alternative that has gained electoral traction, not yet anyway.10 Assuming that the critics are correct, we are left with the perverse result of an economic model that has been thoroughly discredited and yet remains firmly in place (Tomlinson, 2009; Hay, 2010). Rather than simplistically conflating neoliberalism and financialization, a better understanding of the rather more complex and nuanced part that finance plays in neoliberalism will help us to grapple with this conundrum.

Manfred Steger and Ravi Roy (2010, p. 11) note that there are three distinct yet intertwined manifestation of neoliberalism: (1) an ideology; (2) a mode of economic governance; and (3) a policy package. In other words, neoliberalism exists both as a set of ideas and a collection of practices, both in terms of clearly identifiable public policies and the dominant

9 ‘Deregulation’ is something of a misnomer as none of these markets – including capital markets – were really unregulated. Reduced or less restrictive regulation is perhaps more accurate. 10 Colin Hay (2010, p. 3) makes the viable argument that the current political juncture is more like 1973-74 than 1978-79. Radical change may come yet.

Copyright PSA 2011

7

ethos through which public policy questions are addressed (modes of governance). The reason that the understanding of financialization within neoliberalism has become so muddled is that far too many analysts carelessly equate neoliberal discourse and neoliberal practice (Konings, 2009, p. 110), thus falsely inferring practice from theory or theory from practice. Both serve to obscure the functioning and potential of finance within the neoliberal growth model.

On one level, the idea that the crash was the obvious consequence of neoliberal ideology stumbles on the fact that financialization is not an element of neoliberal theory per se. This is not to say that free market ideology did not matter in the development of financialization, as it certainly did. But it is to say, as it were, that the strong version of this argument is weak and the weak version of this argument is strong. The stronger version of this argument focuses on how the general predisposition toward free markets was channeled into the specific concepts espoused by economists. The economics profession has been much maligned (with cause) for creating the crash and/or failing to warn us of its approach (likening them to zombies appears to be the favorite allusion; see Fine, 2010, and Quiggin, 2010; also Cassidy, 2009 and Posner, 2009 for less horrifying analysis). Economists are admonished for building elegant mathematical models of perfectly self-regulating markets, especially financial markets, that were disconnected from the messier reality of actually functioning markets. One of the primary theoretical culprits is the “efficient markets hypothesis”, which implied that the prices generated by stock and other asset markets were the best possible estimate of the ‘right’ price. The dangers of this perspective are made frightfully clear by John Quiggin: “The Efficient Market Hypothesis implies that there can be no such thing as a bubble in the prices of assets such as stocks or houses” (Quiggin, 2010, p. 44). It is implied that bankers plunged in deeper because economists told them there was no danger. This sort of correlative formulation pervades discussions of economists and the crash. What is generally not done, however, is to look for concrete evidence that actors in the financial sector shaped their business strategies based on economic models.11 Did anybody, most especially the major players on Wall Street, truly believed that asset bubbles cannot occur? Indeed, the bulk of the evidence points to the opposite and perhaps more disturbing conclusion: that they continued highly risky strategies even though they knew they were on a bubble. As Citigroup’s CEO Charles Prince famously told the Financial Times in July 2007, “As long as the music is playing, you’ve got to get up and dance”. It is not that they deluded themselves with the safety of theory; they just expected to get off the dance floor before the music stopped. The case that financial actors absorbed the principles of economic scholars and integrated them directly into their business strategies is at best unproven.

The weaker yet more powerful version of this argument focuses less on specific concepts developed by economists and more on the generalized and diffuse idea of a self-regulating market. As applied to the financial sector, if individual financial firms took excessive risks and found themselves overleveraged, markets were supposed to punish that behavior, driving the firm out of the market and penalizing investors who sought to reap profits on bad advice. Other firms would see the error of this approach and adjust their strategies accordingly. To the extent that such defaults would pose risks of contagion to the rest of the financial sector, these could be isolated through ad hoc responses by other private actors, perhaps with the encouraging hand of the state. In a sense, this is exactly what happened in perhaps the most notorious episode of over- 11 The one undoubted counterexample would be the case of Long Term Capital Management, headed up by Nobel Prize winning economists Myron Scholes and Robert C. Merton. LTCM, of course, collapsed ignominiously in 1998 as a result of following the investment model developed by the two Nobel laureates.

Copyright PSA 2011

8

leveraging prior to the crisis, the collapse of Long Term Capital Management in 1998. LTCM had bet heavily on a convergence between the prices of Western government and emerging-market bonds. When the Russian ruble crisis hit in the summer of 1998, LTCM was caught out, leading to a decline in its asset base and a leverage ratio that climbed to 45 to 112 (Dowd, 1999, pp. 3-4). Unable to meet margin calls and on the brink of collapse, LTCM’s management sought outside assistance. Given volatility in the markets, the Federal Reserve began to fear that a collapse of LTCM would shake the markets. In September 1998 it organized a bailout among the major creditors. After a full private-sector (but less lucrative) offer was turned down by LTCM management,13 the Fed-led consortium – including UBS, Goldman Sachs, and Merrill Lynch – exchanged $3.65 billion in equity for a 90% stake in the firm. This event only served to reinforce the idea that, come what may, private actors in the financial sector could be relied upon to clean up the mess. Markets, as neoliberal theory predicted, had regulated themselves.

Where that theory goes off the rails is in the inability to foresee huge swathes of the financial sector, at least the really big players (now popularized as ‘too big to fail’), making the same mistake all at once. It is not that neoliberals lacked the imagination to foresee the crisis per se; it is that the expectation was that financial institutions would pursue a diversity of strategies rather than synchronizing their behavior to each other’s actions. Such events would be therefore isolated and manageable. Systemic failure would require a catastrophic adjustment in the markets, but the neoliberal framework saw this as far less probable. Why actively intervene and inhibit innovative financial markets to prevent a highly improbably outcome?

Distinguishing between the institutional tools of control versus the philosophical inclination to regulate is also important. “If there is a single root cause that has predominated in explanations of the current global financial crisis, it is ‘deregulation’” (Panitch and Konings, 2009, p. 67). New regulatory bodies and re-regulation become the order of the day. As the majority (Democrat) report of the Financial Crisis Inquiry Commission put it, “More than 30 years of deregulation and reliance on self-regulation by financial institutions…has stripped away key safeguards, which could have helped to avoid the catastrophe” They go on to say, “Yet we do not accept the view that regulators lacked the power to protect the financial systems. They had ample power in many arenas and they chose not to use it” (FCIC, 2011, p. xviii). The latter is a crucial and underappreciated point. Policymakers had proper regulatory tools available to them, not the least of which was the ability to tighten monetary policy, to constrain market behavior if they chose to do so. They saw no need to constrain markets; they fully expected that markets would correct themselves and thus prevent any systemic crisis from looming. It might be more accurate to suggest that the deregulatory ideology that guided policymakers was more important than the legal incidence of deregulation. The implication is that what is needed is less an overhaul of the regulatory structure – toward which progress in the US and UK has been at best moderate – and more a reappraisal of the potential for systemic failure.

12 LTCM was hardly the worst offender. By the end of 2007, the combined leverage ratio of Fannie Mae and Freddie Mac was 75 to 1. The Financial Crisis Inquiry Commission report (FCIC, 2011, p. xx) dubbed them the “kings of leverage”. 13 Dowd, a Cato Institute scholar, notes, “Had it been accepted, that offer would have ended the crisis without any further involvement of the Federal Reserve – a textbook example of how private-sector parties can resolve financial crises on their own, without the Federal Reserve or any other regulatory involvement” (Dowd, 1999, p. 5). Crises may come, but the private sector could handle it.

Copyright PSA 2011

9

Presenting that same idea in a more scholarly vein, deregulation is characterized as an attempt to break from the ‘embedded liberalism’ of the postwar era and separate financial markets from their state and societal roots – to ‘disembed’ markets in Polanyian terms (Jessop, 2010, p.176). The crushing impact of the market and the social backlash are captured by Robert Wade:

Governmental responses to the crisis further suggest that we have entered the second leg of Polanyi’s ‘double movement’, the recurrent pattern in capitalism whereby (to oversimplify) a regime of free markets and increasing commodification generates such suffering and displacement as to prompt attempts to impose closer regulation of markets and de-commodification (hence ‘embedded liberalism’). The first leg of the current double movement was the long reign of neoliberalism and its globalization consensus. The second as yet has no name, and may turn out to be a period marked more by a lack of agreement than any new consensus (Wade, 2008, p. 6-7).

In short, bodies of collective authority and control were pushed aside by the atomizing forces of the market. Yet, as Leo Panitch and Martijn Konings (2009) note, the idea that laissez-faire managed to separate finance from the state is only true if one takes neoliberal self-representation without question. “Neoliberalism and financial expansion did not lift the market out if its social context; rather, they embedded financial forms and principles more deeply in the fabric of American society” (Panitch and Konings, 2009, p. 68). Financialization was not so much about ripping financial markets free from the constraining tethers of society and the state; it was about remaking the relationships and institutions that connected both society and state to the world of finance. The market did not become disembedded, it became differently embedded, and in most respects more deeply entrenched in the fabric of society. Elizabeth Warren and her Consumer Financial Protection Bureau can regulate credit card and other consumer finance fees all they want, but if American consumers continue to rely on credit to support consumption, then financialization will have shifted very little.

Nor did financialization come entirely from neoliberal reforms. As Martijn Konings (2009) eloquently argues, far from being a swing in the Polanyian pendulum away from commodification, the New Deal and postwar reforms were intended to integrate the lower classes into the capitalist order. Fannie Mae, the government-sponsored entity (GSE) that played a major role in the subprime crisis, was founded in 1938. American total private debt increased three times as fast from 1949-54 as it did in the five years prior to the global financial crisis (Konings, 2009, p. 114). As the expansion of the postwar years drew to a close, demand for private credit rose as baby boomers sought to borrow to cover homes, cars, colleges, etc. It was in this context that the turn to neoliberalism occurred (Konings, 2009, 117). The stagnant economic position of the lower strata during the neoliberal period only furthered the desire for easy private credit. Deregulation and the financialization that it produced was driven by a series of pragmatic decisions, such as the Clinton Administration’s repeal of the Glass-Steagall Act, to remove legal barriers to the financial dynamics that were already occurring (Panitch and Konings, 2009, pp. 68-69). Financialization was promoted and reinforced by neoliberal ideology, not created by it. Nor are we likely to regulate away financialization; it is too deeply embedded in the social structure.

Copyright PSA 2011

10

Scholars erred in understanding how neoliberal theory connected to actual economic governance. They equally erred in inferring theory off of practice. The basic problematic claim here is that the patterns and traits of neoliberal economies in general and financial markets in particular that have been evident for the past 30 years (or even the years immediately before the crash) are inherent elements of neoliberalism. A variation on this theme is to suggest that neoliberal modes of governance will inevitably produce the same outcome as 2008 -- debt crises and economic collapse. Certainly as a description of past events, such arguments are accurate. As elaborations of neoliberal ideas and the role of financialization in economic governance, they are awkward.

The most widely cited advocate of this perspective is Colin Crouch (2009) and his characterization of neoliberalism as ‘privatized Keynesianism’, particularly apropos as it puts financialization at the heart of the model. Crouch argues that capitalism faces a fundamental challenge: profitability requires labor flexibility, yet this renders workers insecure and less confident consumers, undermining profitability. The postwar Keynesian model both smoothed the business cycle and protected vulnerable workers through the extension of the welfare state, allowing them to become stable mass consumers. The problem for this model is that it faced an inherent “spending ratchet” – it was easy for governments to spread the fiscal goodies during the downturns, much harder to take them away in the booms (as Keynes advocated) – creating inflationary pressures and undermining growth in the 1970s. Hence the turn to neoliberalism. In Crouch’s depiction, Thatcher and Reagan did not alter the economic model nearly as much as is commonly portrayed. They merely shifted the locus of growth financing. Crouch precludes the possibility of uncontrolled markets delivering stable growth. “So the puzzle remains: if the instability of free markets had to be overcome to usher in the mass consumption society, how did the latter survive the return of the former?” The answer is that:

…two things came together to rescue the neo-liberal mode from the instability that otherwise would have been its fate: the growth of credit markets for poor and middle income people, and the derivatives and futures markets among the very wealthy. This combination produced a model of privatized Keynesianism….Instead of governments taking on debt to stimulate the economy, individuals did so. (Crouch, 2009, p. 390, emphasis added).

Colin Hay echoes this idea. The “Anglo-liberal growth model” that characterized the American, British, and indeed Irish economies, “…was largely consumer-led and financed by private debt…it was the easy access to credit, much of it secured against a rising property market, that was the most basic precondition (Hay, 2010a, pp. 4-5). Governments following a ‘privatized Keynesian’ needed to keep asset prices, particularly house prices, rising to ensure growth (Hay, 2009, p. 462). “In so far as – or, as we have recently discovered, only for as long as – a low inflation-low interest rate equilibrium persists, a virtuous and seemingly self-sustaining growth dynamic is established. This, in essence, is the growth model” (Hay, 2010a, p. 9, emphasis added). Thus the rise in private debt transforms from being the outcome of the policies pursued during a particular period of time into a central tenet – the driver of growth – in the neoliberal model. The corollary of this is that the asset bubble that occurred in the mid-2000s was not just an unfortunate event resulting from poor policy choices; it is the logical outcome of the neoliberal model. In addition to driving growth, private debt served as a cushion to replace

Copyright PSA 2011

11

the state-funded social safety nets that had been weakened by successive governments (Montgomerie, 2011). If the Achilles’ heel of Keynesianism was a politically-motivated spending ratchet, the weakness of neoliberalism is a market-motivated debt ratchet.

Note that this critique, constructed from the record of neoliberal practice, is quite different from those grounded in neoliberal theory. The latter suggests that ideology led decision-makers to mistakenly believe that markets could fix themselves. Here we find sins of commission; governments intentionally engendered a debt bubble because there was no other means of keeping the economy growing. This argument is problematic on multiple counts. It suffers first from a problem of periodization, extrapolating the trends of the pre-crash years to the entire era that preceded it. The key causes of the crisis -- the ratcheting up of house prices in the US, the promulgation of subprime mortgages, the rampant securitization of those mortgages – none of this was occurring for the first two decades of the neoliberal era. To be sure, the trends of advancing consumer credit and liberalizing financial markets were on track during this period. The problem for ‘privatized Keynesianism’ is that it does not take seriously that those trends might have developed along an alternate and potentially more economically stable path. Additionally, it presents a characterization of neoliberalism that few of its advocates would recognize. Financial liberalization is certainly central to the model, but Hayek, Thatcher, and others14 free marketeers would be aghast at the claim that prosperity is to be built upon mountains of debt. This begs the question of whether we are talking about simply a description of the practice of neoliberalism in the early 21st century in the Anglophone economies (which opens up possibilities for variations less reliant upon private debt), or is private debt conceptually and practically so central to this model that there are no other logical outcomes?

Take a simple counterfactual argument as a potential answer. The rise in asset prices in the 2000s was predicated on a loose monetary policy, a proposition that is hardly consistent with the bulk of neoliberal theory, which preaches the necessity of stable money to encourage investment. What if the US Federal Reserve had raised interest rates much earlier? Using the ‘Taylor Rule’,15 having lowered interest rates in the wake of the dot.com crash, the Federal Reserve should have begun to slowly raise them (from just under 2%) in early 2002 up to just over 5% by early 2005. In fact, the Fed continue to lower interest rates down to 1% until the second quarter of 2004, and then jacked them up to over 5% by early 2006. The housing market began its tumble in late 2007. Whether or not the Fed should have followed Professor Taylor’s advice is not the issue. The point is that a permissive monetary policy was a prerequisite for the global financial crisis. More effective macroeconomic management could have averted this crisis all else being held equal. The idea that neoliberalism inevitably would produce a crash simply does not hold water. In fairness, that only handles one side of the Crouch and Hay16 critique of the ability of neoliberalism to produce stable growth. Perhaps sounder macroeconomic management might have avoided instability, but would it have come at the cost of substantially 14 Although perhaps not Ronald Reagan; he didn’t seem to have much trouble running up federal debts! 15 Named for Professor John B. Taylor of Stanford University. The Taylor Rule formula uses the divergence between actual inflation and target inflation rates and actual versus potential GDP to determine the real short-term interest rate that is consistent with non-inflationary full-employment growth. And Taylor, it should be noted, would very much fit into the laissez-faire camp. 16 Hay argues that neoliberalism ignores the business cycle and offers not macro-economic stabilizers. This is absurd. Neoliberalism simply seeks macroeconomic control predominantly through monetary rather than fiscal policy, and the success of the Federal Reserve in stabilizing the economy in the wake of the dot.com crash shows that these tools can be used successfully to counter downturns in the business cycle.

Copyright PSA 2011

12

reduced growth, particularly compared to other industrialized states? This takes us to the question of where neoliberalism might go from here.

THE FUTURE OF THE NEOLIBERALISM AND THE POLITICS OF AUSTERITY

It is not hard to find scholarly work on neoliberalism. What is difficult if to find authors who are not critics of the model. A collective schadenfreude in the wake of the crash is thus to be understood. What is puzzling, however, is how so many scholars who have been so critical for so long seem now to have very little to say about what should replace the neoliberal model. Critical analyses of neoliberalism and the crash too frequently end with generic invocations of the need to develop some sort of just, stable alternative to global free market capitalism without every spelling out just want that alternative is (Gamble, 2009; Panitch and Konings, 2009; Mykhnenko and Birch, 2010). The only coherently argued alternative, advocated most vocally by Paul Krugman, is a return to old-fashioned Keynesian reflation. Given the deficit and debt situations of the US and UK, this is tantamount to saying the solution for an unsustainable private debt-fueled growth is public debt-fueled public Keynesianism that is somehow rendered sustainable – even though the baby boom generation will be straining state coffers in a few years, a point that was true even before the crisis hit. There were substantial stimulus packages from both Washington and London in the immediate aftermath of the crisis. These stabilized teetering economies, but certainly did not revive output or employment. There seems to be little appetite for or confidence in another big Keynesian push, even in Democrat or Labour circles.17 Even if there was support in the UK, the markets want to see deficit reduction and that there has been little serious discussion of state promotion of strategically significant industries (Hay, 2010b, p. 399). Yet even if the latter route were chosen – and calls for “green Keynesianism” (Patomäki, 2010, p. 81) fit this bill – it is unlikely that a new strategic industrial policy would be any more successful than similar attempts in the past (Grant, Forthcoming). As a practical matter, there are simply no serious alternatives to the neoliberal model (and, implicitly, the financialization that is a part of it) that have gained political traction in the US or UK, at least not yet (Wilson, Forthcoming; Gamble, 2010). There has long been a desire those on the left for America to develop into a European-style social democratic welfare state or for Britain to mimic Scandinavian corporatism or transform into an Anglicized Modell Deutschland. But these views have no politically consequential champions, and the range of institutional, cultural, and policy barriers to such a political-economic metamorphosis are enormous. Thus the “neoliberalism versus (some yet to be defined) alternative” is really not the primary question. Despite the depths of the crash and the widespread declaration of its demise, neither Britain nor America has yet to abandon the neoliberal model of growth. For pessimists this portends an extended period of economic stagnation (Hay, 2010a and 2010b) or the creation of an even more disastrous crash in

17 The FY2011 budget deal struck with the GOP on 8 April 2011 saw President Obama labeling a $38 billion spending cut “historic”. Ed Miliband attacked George Osborne’s budget for the weakness of its growth claims and the “swinging cuts” being made, but Labour (having created the fiscal mess) only promises to cut not as fast. Paul Krugman, for his part, continues to advocate increased spending with all the misguided confidence of a World War I general, convinced that ‘one more big push’ will win the day.

Copyright PSA 2011

13

the near future (Patomäki, 2010, p. 79).18 The important question is whether neoliberalism -- with the financial sector playing a significant role -- can revive itself, delivering growth19 without again falling victim to a debt ratchet like that which plunged us into a crisis in 2008? More importantly, are the politics on either side of the Atlantic moving in a direction that is likely to produce such an outcome?

Recall that financialization in practice has encompassed three interrelated phenomenon: a large (and growing) financial sector, the extension of financial relationships throughout the economic and social structure, and the financial sector as an engine of growth. In the near and medium term, the first two of these aspects are unlikely to change significantly. Trimming the financial sector in the near term would have negative impact on GDP at a time when these economies desperately need growth. Thus it is not surprising that the financial regulatory reforms promulgated on both sides of the Atlantic have done little to limit the industry. The Dodd-Frank Wall Street Reform and Consumer Protection Act passed in July 2010 is an unwieldy 2,319 page document that left many of the details of key regulations to be written by bureaucrats and regulators. It grants the Federal Deposit Insurance Corporation (FDIC) power to unwind failing firms deemed a threat to financial stability (partially addressing the “too big to fail” problem), places some limitations on proprietary trading and derivatives, and creates a Financial Stability Oversight Council, headed up by the Treasury Secretary and the Chairman of the Federal Reserve. The Act also created a new Consumer Financial Protection Bureau housed inside the Federal Reserve which will have broad powers to write new rules for a variety of consumer products. Wall Street offered only perfunctory resistance to these changes, indicating that they see plenty of profit-making opportunities within these new rules. Unaddressed so far are the monumental problems of the two powerful GSEs, Fannie Mae and Freddie Mac, with the Treasury only just releasing a set of options in February 2011 that foresees a winding down or elimination of the government’s guarantee of private mortgages. As for wider reforms, none are likely to be forthcoming given large Republican gains in the 2010 elections.20

The results were similar in the UK. Starting with the Labour Government and extended by the Coalition, reforms have been passed to dissolve the old “tripartite system”21 and concentrate regulatory responsibility for both banking regulation and systemic monitory with the Bank of England. The elements of regulation will come from the Independent Banking Commission headed by Sir John Vickers to examine the structure of the banking system and systemic risk. The main issue for the Vickers’s Commission is whether retail and investment banking in the UK should be separated along the lines of the old US Glass-Steagall Act. Their final report is not due until September 2011, but an interim report in April suggested only “ring-fencing” retail banking operations from riskier trading operations (Independent Commission on

18 Patomäki predicts a “super bubble” forming that will burst in about 10 years, producing a deep depression and finally signaling neoliberalism’s death. 19 That is, growth that is superior or at least equal to Britain and America’s major industrialized competitors (i.e., France, Germany, Japan, but not China, India, or Brazil). 20 The political limits on reform are highlighted by the appointment of Elizabeth Warren to head of the new Consumer Financial Protection Bureau. President Obama appointed her as a “special advisor” assigned to the CFPB rather than as the formal head, thus skirting (in a constitutionally questionable manner) the necessity of submitting Professor Warren to nomination hearings. 21 Pre-crisis the Financial Services Authority had the primary responsibility for regulating the banking and financial sector, alongside the Bank of England and the Treasury. The criticism is that this left gaps in the system, particularly when it came to “macro-prudential oversight”.

Copyright PSA 2011

14

Banking, 2011), rather than formally breaking up universal banks, a proposal that is purportedly creating a rift between Chancellor Osborne and Liberal Democrat Business Secretary Vince Cable, who wants to see the big banks broken up (The Telegraph [Online Edition], 9 April 2011).

Nor are we likely to see a substantial decoupling of consumers from the financial sector. As noted above, many of the trends that created this situation long predate the neoliberal era and are so deeply embedded in both British and American society at this point that they would be difficult to dislodge. Central to this is the emphasis on homeownership, a goal intimately connected to the “American Dream” and Briton’s conception of a “property owning democracy”. These are ideas that have long had bipartisan support in both states. In the United States, the proliferation of defined contribution pension schemes means that millions of individuals have a direct financial incentive to support relatively deregulated financial markets that can provide greater returns to their savings. Americans have not rejected the idea of financial intermediaries playing a significant role in both national and personal finances. What they are opposed to is poorly managed financial intermediation. (Indeed, it is rather surprising how relatively little political opprobrium has been leveled at bankers in the US despite the enormous bailouts.) Most importantly, neither the British nor American publics have witnessed a sweeping backlash against liberal market capitalism. In recent Rasmussen polling 75% of Americans say free markets are better than government management of the economy, 60% say capitalism is better than socialism, and 38% support a one-year moratorium on new government regulations (www.rasmussenreports.com). President Obama and the Democrats “got a shellacking” in the 2010 midterm elections because of, not in spite of, their more activist policies. On the eve of the Chancellor’s Emergency Budget in June 2010, nearly three-quarters of voters in a Guardian/ICM poll favored greater cuts in spending over higher taxes (The Guardian [Online] 21 June 2010). Although it can only suggested rather than substantiated here, it appears that the liberal movement begun 30 years ago has managed to establish an intellectual hegemony in the Gramscian sense which, although shaken by the financial crisis, remains intact (Castree, 2009).

Within this framework there is room for reform. It would be prudent for policymakers to avoid policies that serve to inflate asset prices, particularly housing. In the United States in particular, taxpayers can write off mortgage interest (even on multiple homes), incentivizing not only initial purchases, but also refinancing. Fannie Mae and Freddie Mac continue to subsidize the mortgage market via secondary market purchases, and the Obama Administration is hesitant to remove such guarantees entirely. Reducing or eliminating these kinds of policies would be sensible, constraining the potential for housing bubbles and bringing much-needed tax revenue, but they would also place a drag on an already moribund housing market in a sluggish economy. Still, the point is that while we are unlikely to see a ‘de-financialization’ of consumption in the Anglophone economies, there are moderate policy reforms that could be implemented to hinder the worst from happening.

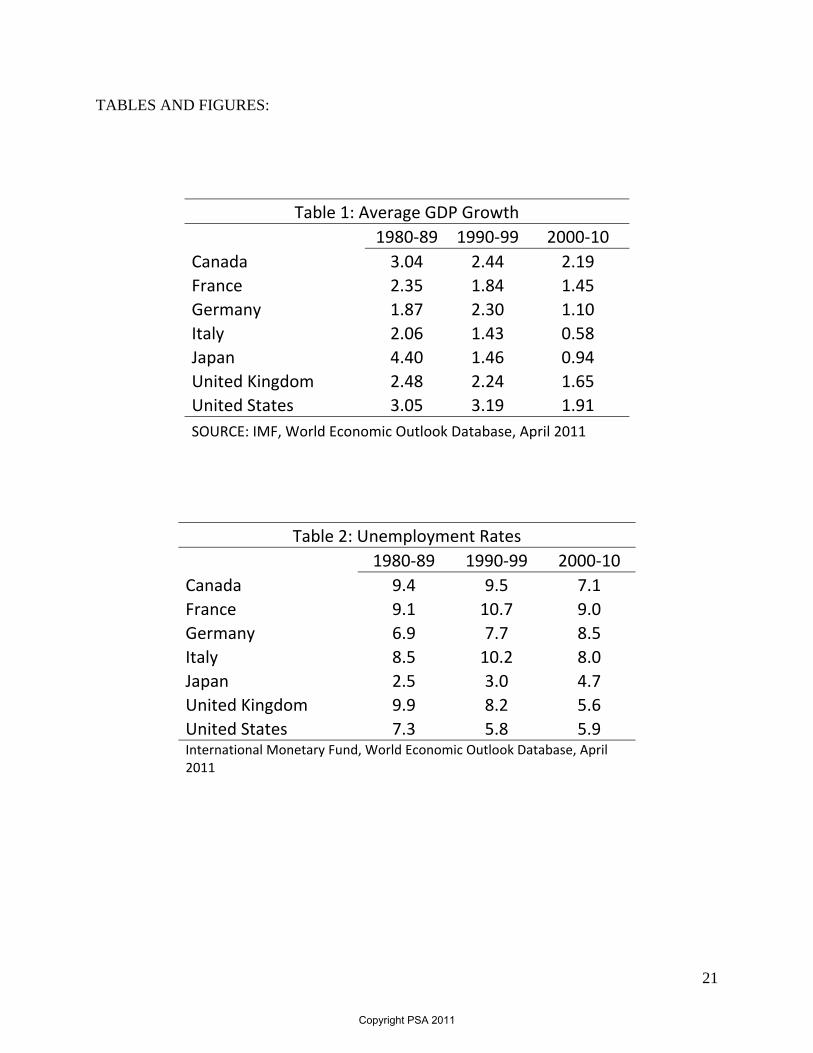

If the contours of neoliberal financialization remain largely intact, and the financial sector was responsible for bringing down the Anglo-Saxon economies, can the neoliberal model again return produce vibrant and sustainable growth? It is useful to first get a sense of the comparative baseline for getting at these questions. Particularly for the British economy, the Keynesian era was one of relative decline. On many basic measures of economic performance, such as output and employment (Tables 1 and 2), both economies saw improved relative performance after the

Copyright PSA 2011

15

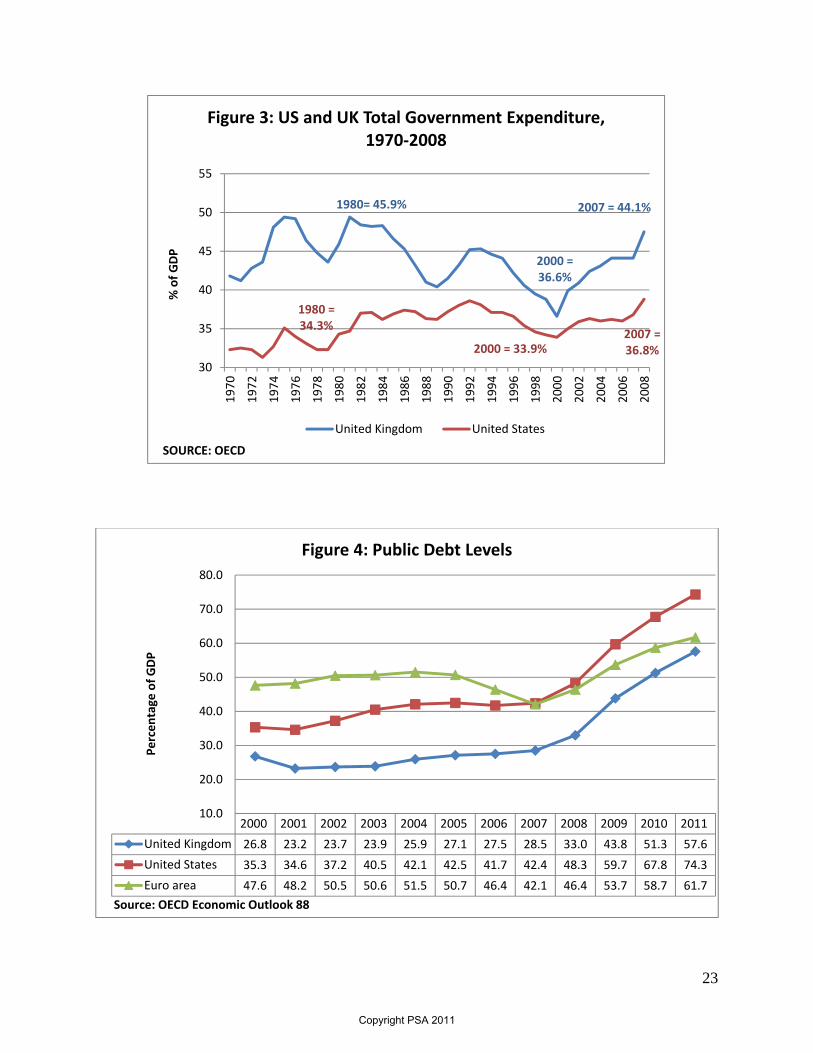

switch to neoliberalism, leading to a reversal of the downward trends in comparative per capita incomes (see Figures 1 and 2) experienced in the decades prior. The crash of 2008 certainly did wipe out gains made during the neoliberal era, but it is not accurate to say that it completely negated that all that preceded it. To this end one must distinguish between the drivers of growth in different periods. Policies in the 1980s are best characterized as “shock therapy” (Fine, 2009); breaking the market impediments of the Keynesian era. Both the US and UK saw improvement growth rates, followed by economic overheating and a recession in the late eighties and early nineties. The nineties saw a much more positive period of growth, built upon the expansion of developing markets and the realization of cost advantages by globalizing production, as well as a general boost to productivity through the integration of a wave of information technology into existing industries and the development of new product markets. The last decade, however, saw diminishing returns to both globalization and technology. Combined with a recession, the disruption of 9/11, and the challenges of two wars, there was great potential for an extended slowdown. In this environment policy-makers chose the easy options for continuing growth via loose credit and fiscal stimulus, even if it was not identified as such at the time. In the US, taxes were cut, domestic spending increased (borrowed), and loose monetary policy fueled a housing boom that encouraged equity withdraws that could be turned into immediate consumption. The UK followed suit, albeit without the tax cuts and with vastly higher spending increases (see Figure 3).22 Low unemployment in the latter New Labour years was brought about by a vast increase in public sector jobs (Froud, et al., 2011). Overall, growth in the decade was fueled by debt, both public and private. To simplify the point, the 1980s were a period of neoliberal transition, the 1990s an era of “good growth”, and the 2000s a decade where policy-makers relied on the quick, easy, but ultimately unsustainable growth formula.

The post-crash economies in both states are face with two great challenges. First and foremost is the debt crisis, which is actually two concurrent problems: public debt and private (particularly consumer) debt. As Figure 4 illustrates, public debt has risen very sharply in both states since 2007 and, under current budgetary guidelines, would be reaching 100% of GDP in the United States by the end of the decade. At the same time the last ten years saw a sharp rise in consumer debt (Figure 5), especially in the UK, where it currently stands at 170% of nominal disposable income, after having peaked at 183% in 2007.23 The task, of course, is to find policies that resolve the former without exacerbating the latter. The second great challenge – and this harkens back to what was the original rationale for neoliberal policies – is to create an environment for stable, productive investment. It is necessary to deal with the debt crises first in order to create the conditions for renewed investment and growth. Equally, the major failing of the financial sector in the run up to the crisis is that it pursued a good deal of investment that was deemed purely speculative, not adding to the productive capacities of economies – a charge leveled equally at the non-financial sector, enamored with corporate strategies that drove up stock prices and short-term profits without improving the long-term productive prospects of these firms. Can (or will) the financial sector, undisciplined by a reformed regulatory framework avoid, again being drawn into another speculative bubble and guide capital into productive investment?

22 Note that while state spending hit a low in both countries in 2000, by 2007 it was back to the same levels as at the beginning of the “budget slashing” neoliberal era. 23 About three-quarters of this debt in both the US and UK is in mortgages.

Copyright PSA 2011

16

In terms of public debt, politics in both the UK and US are now intensely focused on deficit reduction, with the Coalition unveiling its economic plans with the Spending Review announced in October 2010 and the budget presented March 2011. Chancellor Osborne’s “budget for growth”24 has as its central pillar the goal of eliminating the structural deficit within the term of this Parliament. Given the Tories manifesto commitment to ring-fence the NHS, this translates into cuts in other departments of 19% on average. To achieve this end up to a half a million public sector jobs are also to be cut by 2015 and there would be additional contributions (£3.5 billion total) required for public employee pension schemes. Cost control in state pensions would be achieved by moving forward the implementation of retirement at age 66 and indexing pensions to the CPI rather than the (generally higher) RPI. An additional £7 billion in savings come from reductions in welfare budgets through changes to incapacity, housing benefit and tax credits (BBC News, Online, 20 October 2010). To try and make this more palatable, individual tax allowances were increased by £600 and a proposed increase in fuel duty was scrapped in favor of a 1p per liter cut. New revenue would be gathered through an increase of VAT from 17.5% to 20%, purported to raise an additional £13 billion per year. While the overall corporate tax rate is to be cut, new levies will be imposed on North Sea oil producers and banks. As a direct means to enhance growth, twenty-one new “enterprise zones” with tax and regulatory breaks are also to be created. The Coalition conceives of this as “expansionary austerity”. Tightening fiscal policy is intended to increase the confidence of the market and encourage private spending and investment (Elliott, 2011). Whether successful or not is a point speculation, yet the pain will hit hard and fast in the near-term while strong growth is at least some years off.25 Given flat wages, declining public benefits, and rising inflation,26 the Office of Budget Responsibility (OBR) forecasts that the real standard of living for most British families will likely fall for the next two years (The Telegraph [Online] 24 March 2011). It is hardly surprising then that hundreds of thousands of protestors took to the streets in opposition to these cuts on 26 March 2011. In comparative terms, the Cameron Government has the all the advantages of a parliamentary system and a unified state with which to push its economic priorities. And while the Lib Dems appear to be fully onboard on the broad approach,27 the details may yet strain the Coalition, particularly Health Secretary Andrew Lansley’s proposals for NHS reform.

In the US, separation of powers and divided government complicate matters, as does the basic fiscal quandary. Serious deficit reduction must address entitlement programs: Social Security; Medicare, and Medicaid, which between them account for 43% of current federal outlays. (Add in other mandatory spending programs and interest on the debt and the figure rises to 60%; defense spending and non-defense discretionary spending account for about 20% each.) With healthcare costs rising and baby boomers aging, the fiscal burden of all three programs is set to increase exponentially without reform.28 All are politically very sensitive, however; hence the reticence of all sides up to this point. Yet the steep rise in the debt combined with the lack of

24 During which he announced without irony a reduction in the growth forecast for the following year. 25 The Office of Budget Responsibility forecasts growth of 2.8-2.9% for 2013-15. 26 Although the most recent inflation numbers were lower than expected. 27 After a Q&A session with David Cameron in Nottingham, Nick Clegg was caught on a still live microphone telling the Prime Minister, “If we keep doing this we won't have anything to bloody disagree on in the bloody TV debates.” 28 On current trajectories, the federal revenues would only cover Social Security, Medicare, Medicaid and the interest on the debt by 2025.

Copyright PSA 2011

17

a credible reduction plan was sufficient to draw an admonition from the IMF (IMF Fiscal Monitor, April 2011).

We are currently in “opening bids” phase of the debate, kicked off with the report of a bipartisan debt commission headed by Democrat Erskine Bowles and Republican Alan Simpsons (National Commission on Fiscal Responsibility and Reform, 2010). The Commission proposed cutting federal spending (to the tune of $200 billion by 2015) and capping taxation at 21% of GDP, with increased tax revenues coming from a higher gas tax and the elimination of various tax breaks. Total federal healthcare spending would be capped to the rate of economic growth plus 1%, although the Commission skirted the issue of the Obama reforms. Social Security would fixed by raising the retirement age, subjecting a higher level of income to the payroll tax, and reducing benefits for wealthier seniors. All told, the Commission’s proposals would slice $4 trillion off of federal spending over the next 10 years with the balance of spending cuts to tax increases (mainly by eliminating various tax breaks) roughly 3 to 1 (76% to 24%). Under the terms of the Commission’s establishment, a supermajority of 14 out of 18 commissioners would have forced congressional action on their proposals. In the end, 11 commissioners supported the proposal. While both the White House and leaders on Capitol Hill praised the work of the Commission, neither immediately embraced the recommendations.

The Republicans were next out of the chute with a proposal formulated by House Budget Committee Chairman Paul Ryan (The Path to Prosperity, 2011). Ryan’s proposal calls for much more aggressive deficit reduction, seeking to slice $6.2 trillion in spending over the next decade and bring overall federal spending below 20% of GDP, having risen to 24% in 2010. This would be accomplished by bringing domestic spending back to 2008 levels and freezing it for five years, transforming Medicare into a voucher program for the purchase of private health insurance (rather than direct federal payments for health services), and shifting Medicaid to a block grants to the states. Having staked a forward position on Medicare and Medicaid -- and remembering the political disaster that George W. Bush faced in his second term -- Rep. Ryan demurred in advocating any changes to the Social Security system. The GOP plan seeks to reform the tax code, reducing the top rate of individual and corporate taxation and cutting off various tax breaks and loopholes. The weight of the GOP plan falls on the spending side of the ledger and is premised on tax cuts increasing revenues by spurring economic growth. Adopting traditional “supply side” arguments, the Republicans are opposed to increasing taxes to cut the deficit.29

President Obama finally weighed in on the question on 13 April 2011 with a speech at George Washington University outlining a plan for $4 trillion in cuts over the next 12 years. (Despite having submitted a budget in December that increased spending overall with a deficit of $1.65 trillion.) Only about $3 trillion of those savings would come in the next 10 years, less than both the Debt Commission and Ryan proposals. Obama’s proposed savings come mainly through cuts in discretionary domestic and defense spending, as well as raising revenue through repealing tax benefits aimed at upper income Americans, which he portrayed as a more balance approach.30 Republican Speaker John Boehner immediately declared tax increases a “non-

29 The plan is likely to gain approval in the Republican controlled house, but be dead on arrival in the Democrat-controlled Senate. 30 All three proposals seek to raise revenue by closing tax loopholes. This is a challenging task given the ease with which interest groups can slip loopholes into tax law and the fact that many of the tax breaks which might yield the greatest revenue, such as mortgage interest relief, would effectively increase taxes for millions.

Copyright PSA 2011

18

starter” (Washington Post [Online] 14 April 2011). Also included is a proposal for a so-called “debt failsafe”, a triggering mechanism that would kick in automatic across-the-board spending reductions if deficits have not stabilized by 2014 – but excluding Social Security, Medicare, and other programs for low-income Americans (Bloomberg [Online] 13 April 2011). Indeed, Obama’s proposal offers no significant changes to the major entitlement programs other than some general proposals to seek greater efficiencies within Medicare. Notably President Obama set a goal of one dollar of tax increases for every three dollars of spending cuts, or a cuts-to-taxes ratio of 75% to 25%, the same as the Debt Commission recommendations (Washington Post, Online, 13 April 2011).

The first skirmish in this war ended with an eleventh hour compromise agreement to cut $38 billion from the FY2011 (current) budget. The next fight, due in early May 2011, will be on raising the debt ceiling, support for which some conservative Republicans have threatened to withhold barring some immediate agreement on deficit reduction. Action beyond that will focus on the big picture issues raised in the three competing proposals. The pros and cons of these respective plans are vital political questions, but need not concern us here. The key point to note is that fiscal necessity is pushing both Washington – and, as noted earlier, London -- to look much more seriously at reducing the size of the state (while avoiding such direct rhetoric) than at any point since the 1980s. Serious discussions have only just begun in earnest, yet what is immediately striking is that the debate is not whether government spending needs to be reduced, it is about how much and what should be the relative distribution between spending cuts versus tax increases. The center point is that the burden should fall predominantly on spending cuts. Even on the ratios the difference are relatively narrow – and much closer to the Republican side, leading to increasing disenchantment among liberals with Obama (Washington Post [Online] 13 April 2011). There is an enormous distance between spending cut proposals and cuts actually made, and the path between the two is strewn with political obstacles and landmines. But that debate is pushing in what is classically thought of as a more neoliberal direction. Assuming trends continue, then we may see the ironic result that the global financial crisis, billed by so many as the end of neoliberalism, may serve to fulfill one of the original yet unfulfilled promises of neoliberalism – to roll back the size of the state, a strategy Patrick Dunleavy calls the “shock doctrine path” (Dunleavy, 2011).

When it comes to private debt, the picture becomes much more muddled, particularly when comparing the America with Britain. As Figure 5 highlights, both the US and UK saw a steady rise in household indebtedness in the run-up to the crash, peaking in 2007 at 183% of disposable income in Britain and 138% in the US. Both numbers have fallen since then, but the OBR recently updated its projections for household debt to again rise to 173% of disposable income by 2015. At the same time the financial obligations ratio (the ratio of debt payments to disposable income) compiled by the US Federal Reserve fell from its peak of 18.8% in the second quarter of 2007 to 16.6% at the end of 2010, similar to where it was in the early 1990s. The most recent release from the Fed (7 April 2011) shows that while non-revolving consumer credit (especially in this case student loans) demand is rising; revolving credit (credit cards) demand is falling (Bloomberg, Online, 7 April 2011). American consumers, in short, seem reluctant to take on new credit obligations other than for educational purposes. It looks like UK consumer debt, having dropped off after the crisis, is heading back upwards while the downward trend in the US has yet to bottom out, although it is too soon to tell. Nevertheless, growth requires consumption and excessive debt burdens get in the way. Reducing the levels of debt

Copyright PSA 2011

19

(public and private) in the economic system is a prerequisite for renewed growth. The question is, if household debt continues to rise, will consumption be stifled as consumers (by choice or necessity) focus their money on debt servicing rather than new consumption?

Of course, the major wildcard in any sort of revived neoliberal strategy is the behavior of financial markets. The excesses of finance brought the British and American economies down while sticking taxpayers with the bill for their mistakes. Conservative politicians in both American and Britain have worked, quite successfully so far, to limit major regulatory encroachments into the financial sector – not quite the status quo ante, but close enough for most bankers’ liking. Does this mean that we are about to enter a new era of excess, with financiers profiting from purely speculative activity that draws needed resources away from the real economy, developing complicated financial instruments, and overleveraging in the search of profits until once again (and soon) the whole façade of finance comes crashing down – dragging us all along with it? (Patomäki, 2010). In the near term, at least, that is unlikely. The monster that turned on us in 2008 had to be fattened first, fed on a meaty diet of subprime mortgages digested into mortgage-backed securities. The “Masters of the Universe” on Wall Street or in the City could not have done this on their own; they relied on the disconnected activity of thousands of mortgage originators and millions of homeowners. While monetary policy is likely to remain loose for some time, credit conditions are much tighter than before the crash and unlikely to loosen soon. As such the underlying conditions for another housing or credit bubble are not present. Furthermore, bubbles require the illusion of safety. In their extensive study of histories booms and busts, Carmen Reinhart and Kenneth Rogoff (2009) note that the precondition for a crash is a sense that a crash cannot happen – the “this-time-its-different syndrome”.

It is rooted in the firmly held belief that financial crises are things that happen to other people in other countries at other times; crises do not happen to us, here, and now. We are doing things better, we are smarter, we have learned from past mistakes. The old rules of valuation no longer apply. The current boom, unlike the many booms that proceeded catastrophic collapses in the past (even in our country), is built on sound fundamentals, structural reforms, technological innovation, and good policy. Or so the story goes (Reinhart and Rogoff, 2009, p. 15).

One does not have to believe that actors in financial markets have suddenly converted to the joys of stable, low risk, long-term investment strategies; they have not. Given prevailing economic conditions and the “lessons of the crash”, the widespread, rampant, excessive risk-taking of the pre-crash years is unlikely to be resurrected in the near term.

Longer term the issue is whether financial market behaviors will produce negative or positive outcomes. The major knock on unregulated financial markets is that it creates strong imperatives for speculative activity and leveraged investment as the source of profit, raising the specter of growth subject to an inhibiting debt ratchet. Viewed in a more positive light, financial markets serve to funnel needed capital to productive investment. So which is it likely to be? That is an incredibly difficult question to answer because it requires defining concepts like “speculation” and “productive investment”. Is Facebook a productive investment? Are profits made from trading derivatives mere speculation if they have the result of increasing the value of individuals’ retirement accounts? In short, it is hard to say whether finance will play a predominantly negative or positive role, but the negative outcome – that tendency to fall into a debt ratchet – is far more likely unless the current debt situations are improved. But even under

Copyright PSA 2011

20

the most optimistic of scenarios, that will be a long, hard slog. Despite vocal protests by some, there is a general acceptance in the electorates of both Britain and America that the debt crises cannot be ignored, regardless of whose fault it was in the first place. This will require some years of relative austerity before the conditions for a renewed round of higher (i.e., greater than 3%) growth may obtain. The unanswered -- and at this point unanswerable -- political question is how many years of fiscal and personal austerity are voters willing to tolerate before they expect to see some return on this investment.

CONCLUSION

Neoliberalism, to borrow the old Monty Python line, is not dead yet. Perhaps the most striking reality in the wake of the current crisis – and certainly one that dismays those of progressive leanings – is how little both politics and policy seem to have been altered by this catastrophic event. Neither neoliberalism nor financialization looks to be leaving the stage anytime soon. For good or for ill, finance is well-embedded in the 21st century economies of Britain and America. The question that remains is whether the ailments that afflicted the Anglo-liberal economies in 2008 are acute or chronic; whether neoliberalism can again be a growth model after the current mountains of debt are expunged from the system. Both the Tories in Britain and the Republicans in America are making the bet that eliminating debt will create a positive investment environment that will breathe new life into these economies. We have a large and (somewhat) controlled experiment in which to test the utility of these ideas in which, for good or ill, we are all a part.

Copyright PSA 2011

21

TABLES AND FIGURES:

Table 1: Average GDP Growth

1980‐89 1990‐99 2000‐10

Canada 3.04 2.44 2.19

France 2.35 1.84 1.45

Germany 1.87 2.30 1.10

Italy 2.06 1.43 0.58

Japan 4.40 1.46 0.94

United Kingdom 2.48 2.24 1.65

United States 3.05 3.19 1.91

SOURCE: IMF, World Economic Outlook Database, April 2011

Table 2: Unemployment Rates

1980‐89 1990‐99 2000‐10

Canada 9.4 9.5 7.1

France 9.1 10.7 9.0

Germany 6.9 7.7 8.5

Italy 8.5 10.2 8.0

Japan 2.5 3.0 4.7

United Kingdom 9.9 8.2 5.6

United States 7.3 5.8 5.9 International Monetary Fund, World Economic Outlook Database, April 2011

Copyright PSA 2011

22

80

90

100

110

120

130

140

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008Germ

an/French per capita GDP = 100

(2009 $ at PPP)

SOURCE: US Bureau of Labor Statistics

Figure 1: UK per capita GDP Compared to Germany and France, 1960‐2009

UK per capita GDP relative to Germany UK pre capital GDP relative to France

90

100

110

120

130

140

150

160

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

G‐7 (minus US) per capita GDP = 100

(2009 $ at PPP)

SOURCE: US Bureau of Labor Statistics

Figure 2: US per capita GDP Compared to Rest of G‐7, 1960‐2009

G‐7 (minus US) United States

Copyright PSA 2011

23

1980= 45.9%

2000 = 36.6%

2007 = 44.1%

1980 = 34.3%

2000 = 33.9%2007 = 36.8%

30

35

40

45

50

55

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

% of GDP

SOURCE: OECD

Figure 3: US and UK Total Government Expenditure, 1970‐2008

United Kingdom United States

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

United Kingdom 26.8 23.2 23.7 23.9 25.9 27.1 27.5 28.5 33.0 43.8 51.3 57.6

United States 35.3 34.6 37.2 40.5 42.1 42.5 41.7 42.4 48.3 59.7 67.8 74.3

Euro area 47.6 48.2 50.5 50.6 51.5 50.7 46.4 42.1 46.4 53.7 58.7 61.7

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Percentage

of GDP

Source: OECD Economic Outlook 88

Figure 4: Public Debt Levels

Copyright PSA 2011

24

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

% of nominal disposable income

SOURCE: OECD

Figure 5: G‐7 Household Indebtedness, 1998‐09

Canada France Germany Italy

Japan United Kingdom United States

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

1980Q1

1981Q2

1982Q3

1983Q4

1985Q1

1986Q2

1987Q3

1988Q4

1990Q1

1991Q2

1992Q3

1993Q4

1995Q1

1996Q2

1997Q3

1998Q4

2000Q1

2001Q2

2002Q3

2003Q4

2005Q1

2006Q2

2007Q3

2008Q4

2010Q1

SOURCE: Federal Reserve "Household Debt Service and Financial Obligation Ratios"

Figure 6: US Household Financial Obligation Ratio

Copyright PSA 2011

25