Embed Size (px)

Citation preview

Financiers and their habits

by Mr Ties van der LaanTies Corporate Finance

10, rue des Alouettes, L-1121 Luxembourg-CentsLuxembourg

m +352 091 427 566, t/f +352 427 566e [email protected], i www.ties.lu

Equity investors

Who am I?

After nearly ten years in Dutch venture capital companies (ING Group) I am coaching

since 1999 entrepreneurs and management teams to raise finance, first through LIFT

and from mid 2002 as an independent business coach

Where to look? - depends on where you areBUY OUT / M&A

= COMPANY'S LIFE CYCLE= FINANCE Growth, profit= FINANCIERS EXPANSION= EXIT

Growth MBO, MBI , IBO, LBO

M&A = Mergers & Acquisitions EARLY STAGE Merger, Acquisition

IPO = Initial Public Offering and TurnaroundMBO = Management Buy Out Accelerated growth Third, Fourth, ….. Loans, Mezzanine,MBI = Management Buy In START-UP Equity (expansion Equity (later stage capital),

IBO = Investor Buy Out capital), Loans GrantsLBO = Leveraged Buy Out Marketing Second round

RESEARCH & DEVELOPMENT Equity (early stage capital)

Concept Research Project plan Design Prototype First Roundspecification Equity Management team, Management team,

(start-up capital) Corporate investors, Venture capitalists, Seed round Venture capitalists, Mezzanine providers,

Grants, Gifts, Goods, Services, Loans, Equity (seed capital) Management team, Banks, Banks,Management team, Corporate investors, IPO. Institutional investors,

Business angels, Venture capitalists. Public sector.Public sector, Sponsors, Founder & friends & family, Corporate investors,

Banks, Venture capitalists.Business angels, Corporate investors, Venture capitalists.

License or sale (Trade) sale (Trade) sale (Trade) sale, IPO, (Trade) sale, IPO,secondary buy out secondary buy out

Life cycle/finance/financiers

Life Cycle Finance FinanciersResearch Grants Public sectorStart-upEquity SponsorsEarly stage Seed capital Founder, friends, familyExpansion Venture capital BanksBuy-out/in Private equity Business angelsTurnaround Mezzanine Corporate venturers

Loans Venture capitalists

And will finish with a summary and a step-by-step plan!

General characteristics: Focus is on future Seek risk, expect high return Buy shares Temporary involvement Seek (serial) managers/entrepreneurs

Equity investors

Business angels Corporate investors Venture capitalists (Institutional investors)

Types of equity investors

Characteristics Who are they? What do they seek? How do they operate?

Business angels

BA’s: characteristics

Successful business(wo)men “Have been there, done that” Invest their own money Funds: up to € 1m, few larger Deals: from € 15-200k, typically € 75k Aged between 50-70 years, few younger Driven by “giving something back” Other agendas - fun, involvement Profit less significant

Executive angel Active entrepreneurs, executives or consultants Investments between € 50k - € 100k Extra turnover, networking, hobby

Job seeking angel Redundant executives Work in the € 30k - € 70k area Busy, active

Retired angel Workaholics Smaller amounts (€ 15k - € 50k) Busy, active

Who are the BAs?

Small companiesMostly active in markets they knowGrowth in growing, large, empty niche markets In 7-10 years potential turnover >100mAlso invest in seed phaseNearby

ReturnProfit through tradesale or IPODividend, interest and fees

Likeable persons In business (entrepreneur) and private (talk)Mutual trust

What do BAs seek?

IntakeVia friends, family or business (angel) networksLow due diligence

The dealStraightforward structureVeto rights, minority protection, anti-dilutionTime frame from several weeks to one month

After the dealClose involvement: 1-3 days/weekHands on unless going badlyBusiness devils

How do BAs operate?

Characteristics? Who are they? What do they seek? How do they operate?

Corporate venturers

Large, operating companies Successful, cash rich Invest company’s money Funds: active € 10, passive € 200m Deals: small (< € 0,2m) or large (> € 5m) Active managers 30-60 years old Objective strategic: market reconnaissance Outside (but close) to own market Profit less important

CV’s: characteristics

Market leaders (or just below) in:Technology (ICT: Intel, Life Science: BASF)Telecom (Vodafone)Consumer products (Unilever)Capital goods (Siemens)

Quoted on the stock exchange See www.evca.com

Who are the CVs?

ActiveSmall companies/individuals (in or external)Focussed on seed phase/technology Incubate until ready for VCsBuy when successful

Passive Mature businesses (MBOs, restructuring)Direct: partner with VC’s Indirect: fund of fundsBuy or trade sale (IPO)

What do CVs seek?

Active Intake through investment manager Fast decisions, little due diligence Simple deal structure Hands-on even when going badly Invest for the long run (> 5 years), buy when successful Enhance your credibility, give access to network

Passive Direct: passive in deal structuring (VC) Indirect: in investment committee Sometimes in Board of Directors or Supervisory Board Hands-off or buy when going badly

How do CVs operate?

History of venture capital Characteristics Who are they? What do they seek? How do they operate?

Venture capitalists

History of venture capital

Started in USA in early 1900 Rich families (e.g. Rockefellers) invested outside

own conglomerate as business angels 1st time distinction: ownership/management After WOII: professional VCs Early 60s: UK Early 80s: continental Europe (banks in NL)

Professional buyers of share in private companies Invest money of institutional investors (II) II = LP, fund manager = GP Funds: € 10m – € 15bn (!) Deals: € 1m – several € 100m Investment managers between 25–55 years old Dealmakers with financial background Objective is generating cash Driven by building profitable/sellable companies

VC: characteristics

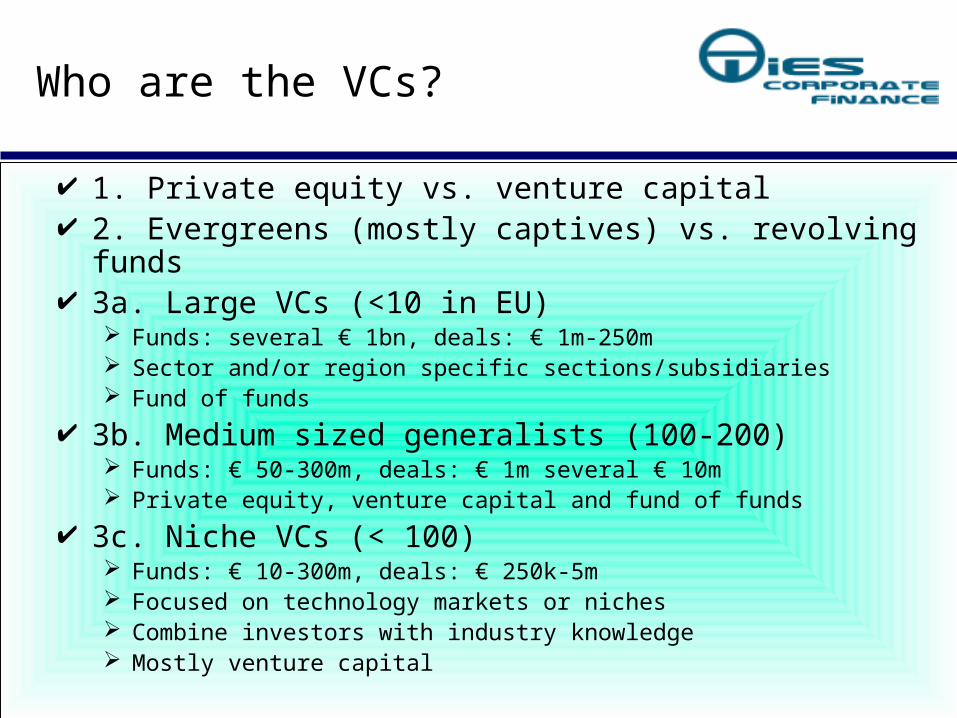

1. Private equity vs. venture capital 2. Evergreens (mostly captives) vs. revolving funds 3a. Large VCs (<10 in EU)

Funds: several € 1bn, deals: € 1m-250m Sector and/or region specific sections/subsidiaries Fund of funds

3b. Medium sized generalists (100-200) Funds: € 50-300m, deals: € 1m several € 10m Private equity, venture capital and fund of funds

3c. Niche VCs (< 100) Funds: € 10-300m, deals: € 250k-5m Focused on technology markets or niches Combine investors with industry knowledge Mostly venture capital

Who are the VCs?

Private equity 90% (!) of money yearly raised Mature companies with turnover > € 50m Buy-outs mostly (MBO, MBI, IBO, BIMBO etc.) No market specialisation Return > 20%: € 10 in, 4 years later € 20m out

Financial engineering Buy and build Sale

What do VCs seek? (I)

Venture capital Young companies: seed, start-up, early stage Large, global empty markets Experienced entrepreneurs Return > 50%: € 1m in, 4 years later € 5m out

Growth Sale (trade or IPO)

Investing is trust in people PE = balanced management teams VC = entrepreneurs

What do VCs seek? (II)

IntakeReceive more plans than read Introduction via networkSelective: invest in 1% of business plans readExtensive due diligence: 2 to 6 months

Market(ing), technology, management, legal, financialPE: mostly external specialists

Syndicates (so no competition between VCs)Deal-sourcing in other regionsFollow-on investmentsPrevent entrapmentControl with minority share

Cross-border only with local lead

How do VCs operate? (I)

The dealSometimes complex deals Management option schemeVeto-rights, minority protection, anti-dilution Board representation Monthly or quarterly reportingControl over exit Investment committee decidesTypically 2 months

How do VCs operate? (II)

After the dealReal work startsFrequent contact in beginningSupport: knowledge, experience and networkFocus on:

GrowthReportingExit

Hands-off unless going badlyNo good money for bad moneySell healthy part of company via network

How do VCs operate? (III)

BAs: money + market experience + network, long term, < € 0,2m in small fast growing companies, not for return only, local, hands-on

CVs: money + market knowledge + network + credibility, long term or short term, < € 0,2m or > € 5m in companies close to their market, active + hands-on or passive + VC, buy when successful

VCs: money + experience + network, professionals in private mostly mature companies (PE), PE: financial engineering & buy/build & exit, VC: growth & exit, return only, prefer syndication with local party, due diligence: 4-8 months

Conclusion equity investors

From start to finish (I)

The more steps you complete the easier it becomes to raise finance:

1. Finalise your product (grants)2. Find entrepreneur (yourself?)3. Found company (own money, house, FFF)4. Find business partners (sponsors)5. Find customers and sell (auto-finance)6. (Accelerated) growth (raise finance)

continued on next slide

From start to finish (II)

continued from the previous slide

7. Raising equity finance: 1. Prepare business plan/presentation/pitch

With help of dedicated professionals? 2. Research financial world

Business Angel Networks (BANs, www.eban.org) EVCA/local VCAs (www.evca.com) Networking

3. Approach chosen potential investors With help of dedicated professionals?

8. Later stage: MBO/MBI/Turnaround9. Raising equity finance: see 7.10. Sell: tradesale or IPO

Where to look? - depends on where you areBUY OUT / M&A

= COMPANY'S LIFE CYCLE= FINANCE Growth, profit= FINANCIERS EXPANSION= EXIT

Growth MBO, MBI , IBO, LBO

M&A = Mergers & Acquisitions EARLY STAGE Merger, Acquisition

IPO = Initial Public Offering and TurnaroundMBO = Management Buy Out Accelerated growth Third, Fourth, ….. Loans, Mezzanine,MBI = Management Buy In START-UP Equity (expansion Equity (later stage capital),

IBO = Investor Buy Out capital), Loans GrantsLBO = Leveraged Buy Out Marketing Second round

RESEARCH & DEVELOPMENT Equity (early stage capital)

Concept Research Project plan Design Prototype First Roundspecification Equity Management team, Management team,

(start-up capital) Corporate investors, Venture capitalists, Seed round Venture capitalists, Mezzanine providers,

Grants, Gifts, Goods, Services, Loans, Equity (seed capital) Management team, Banks, Banks,Management team, Corporate investors, IPO. Institutional investors,

Business angels, Venture capitalists. Public sector.Public sector, Sponsors, Founder & friends & family, Corporate investors,

Banks, Venture capitalists.Business angels, Corporate investors, Venture capitalists.

License or sale (Trade) sale (Trade) sale (Trade) sale, IPO, (Trade) sale, IPO,secondary buy out secondary buy out

Ties Corporate Finance

Business coach in raising finance

for the expansion of businesses

To create a winning business planTo approach investors professionallyTo negotiate with investors successfully

Ties Corporate Finance

Ties van der Laan10, rue des Alouettes

L-1121 Luxembourg-CentsMobile: (+352) 091 427 566

Fax: (+352) 427 566Email: [email protected]

Internet: www.ties.lu

Contact details