Embed Size (px)

Citation preview

Financing Franchising Business

DR. HATEM ZAKI Board Member – EFDA

November 6-7, 2013Abu Dhabi, U.A.E.

THE EGYPTIAN FRANCHISE DEVELOPMENT ASSOCIATION

“EFDA ”

EFDA is a non-profit NGO formed by top group of businesspeople with the support of the Egyptian Government, to encourage and promote entrepreneurship and business through franchising.

FULL MEMBER IN WFC 2005

THE EGYPTIAN FRANCHISE DEVELOPMENT ASSOCIATION (EFDA)

• One of the most difficult problems in becoming a franchisor is obtaining finance.

• Expansion requires capital and that is not often readily available, particularly when a business is relatively young.

FINANCING THE FRANCHISE SYSTEM

• There are two types of financing options a potential franchisor can consider for the expansion program. These are:

Debt Financing: loan / interest / collateral.

Equity Financing: ownership in business / share in risk and rewards.

THE NEED FOR FINANCE

• Franchising is about expanding a tried, tested and proven concept. The franchisor will therefore need financial resources to carry him/her through the initial phases of development to avoid a possible breakdown in the planned growth .

• The costs may include the establishment of basic services that franchisees require, the preparation of documents and systems. Capital to develop a prototype.

HOW MUCH FUNDING IS NEEDED?

• Differentiate between financing a new franchise from financing a franchise expansion .

• If financing a Franchise system for expansion a “Disclosure Document” is a must.

HOW MUCH FUNDING IS NEEDED?

• Key Franchise Details

• Background to Franchise

• Current franchisees

• Franchise agreement summary

• Franchisor obligations

• Financial information

WHAT IS A DISCLOSURE DOCUMENT ?

• A small business owner needs to recognize and understand the tradeoffs between debt and equity: High Equity and Low Debt Financing:

o Voting Control: Owners share control with equity investors.

o Financial Risk: Lower.o Potential Profitability: Lower potential return on

investment.

High Debt and Low Equity Financing:o Voting Control: Owner maintains control without

making large investment.o Financial risk: Higher.o Potential profitability: Higher potential return on

investment.

HOW TO OBTAIN FUNDING ?

• Family or Friends: a common source to obtain capital. The downside is that personal relationships may be placed in jeopardy.

• Business Angels: These are private individuals who invest in young and relatively small to medium sized companies. As a private investor they frequently also contribute know-how and experience to the business they invest in.

VARIOUS CHANNELS OF FINANCING THE FRANCHISOR

• Employee Funding: potential employees particularly those with whom the franchisor have worked with in the past or those the franchisor have known in the industry in return for some equity ( rare).

• Venture Capital: They usually demand part ownership of the franchise, full repayment over a predetermined period (typically five years) and a high rate of return. They normally focus on companies who are in a growth phase.

VARIOUS CHANNELS OF FINANCING THE FRANCHISOR

• Commercial Banks: The funds provided by the commercial banks are in the form of debt financing. As such, tangible collateral or guarantees are required to secure a loan.

• Small enterprises in particular are perceived by banks as high risk mainly due to a relatively high failure rate.

VARIOUS CHANNELS OF FINANCING THE FRANCHISOR

Banks criteria to evaluate application for funding:

• The track record of the business to be franchised.

• The credit worthiness of the company.

• How much collateral can be offered.

• Financial statements including a cash flow budget, income and expenditure statement and a balance sheet for the current and 2 to 3 prior years.

• A business plan.

VARIOUS CHANNELS OF FINANCING THE FRANCHISOR

Financial Institutions:

Such as leasing companies. These institutions operate basically on the same lines as Commercial Banks. They do not however, have the variety of financial services offered by commercial banks.

VARIOUS CHANNELS OF FINANCING THE FRANCHISOR

• Proven business concepts with a track record.

• Support from the Franchisor.

• Source of good business.

• Risk minimization.

• Entrepreneurial development.

WHY FINANCIAL INSTITUTIONS ARE SUPPORTING FRANCHISED BUSINESSES ?

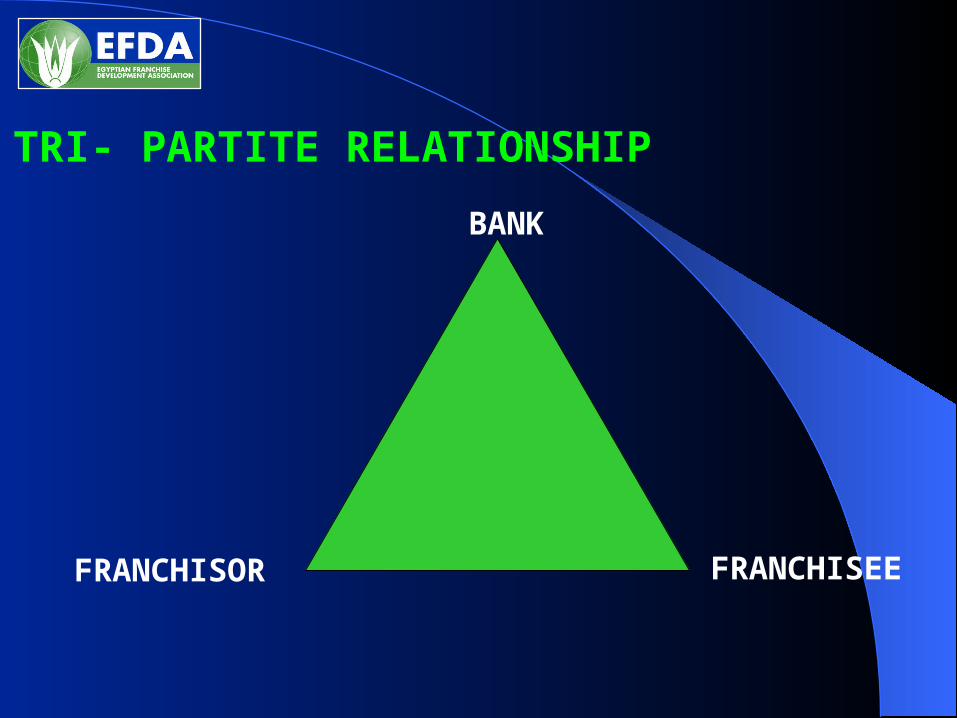

TRI- PARTITE RELATIONSHIP

BANK

FRANCHISOR FRANCHISEE

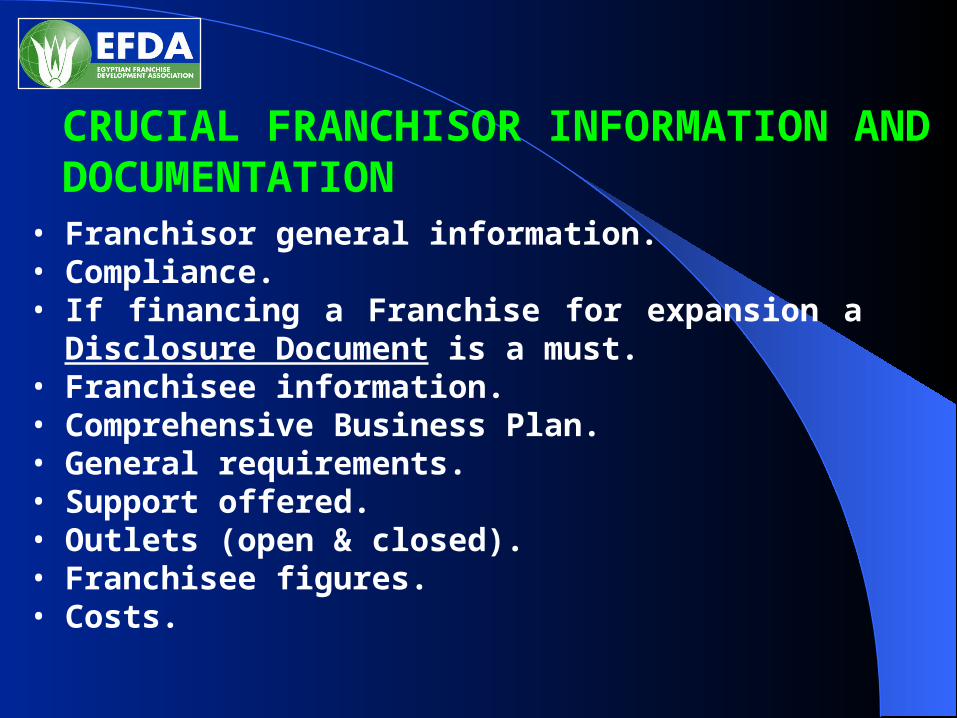

• Franchisor general information.• Compliance.• If financing a Franchise for expansion a Disclosure

Document is a must.• Franchisee information.• Comprehensive Business Plan.• General requirements.• Support offered.• Outlets (open & closed).• Franchisee figures.• Costs.

CRUCIAL FRANCHISOR INFORMATION AND DOCUMENTATION

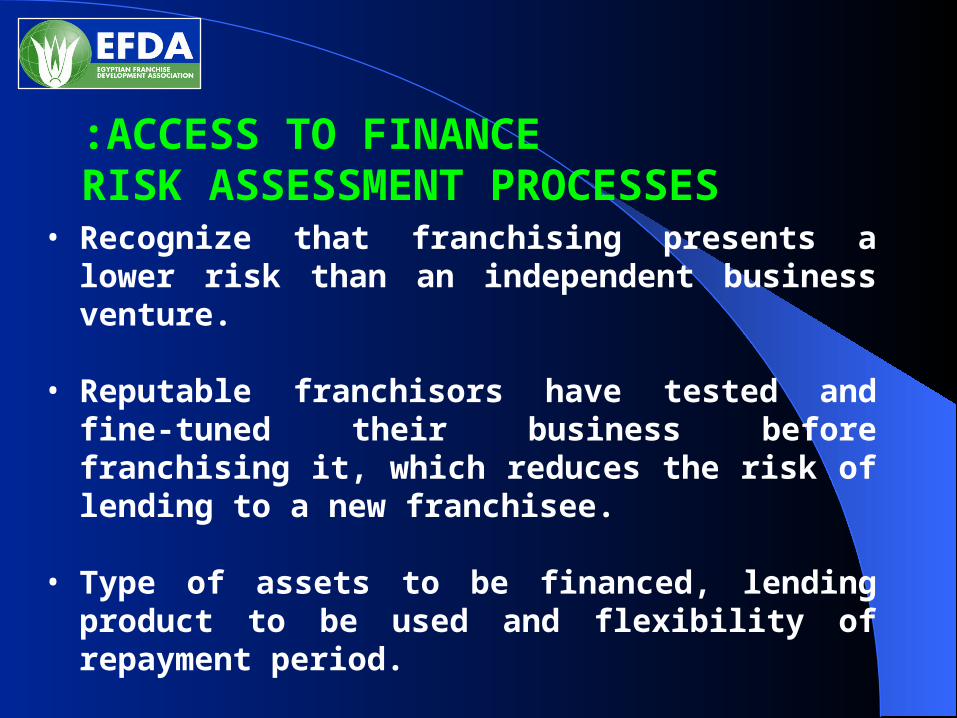

• Recognize that franchising presents a lower risk than an independent business venture.

• Reputable franchisors have tested and fine-tuned their business before franchising it, which reduces the risk of lending to a new franchisee.

• Type of assets to be financed, lending product to be used and flexibility of repayment period.

ACCESS TO FINANCE:RISK ASSESSMENT PROCESSES

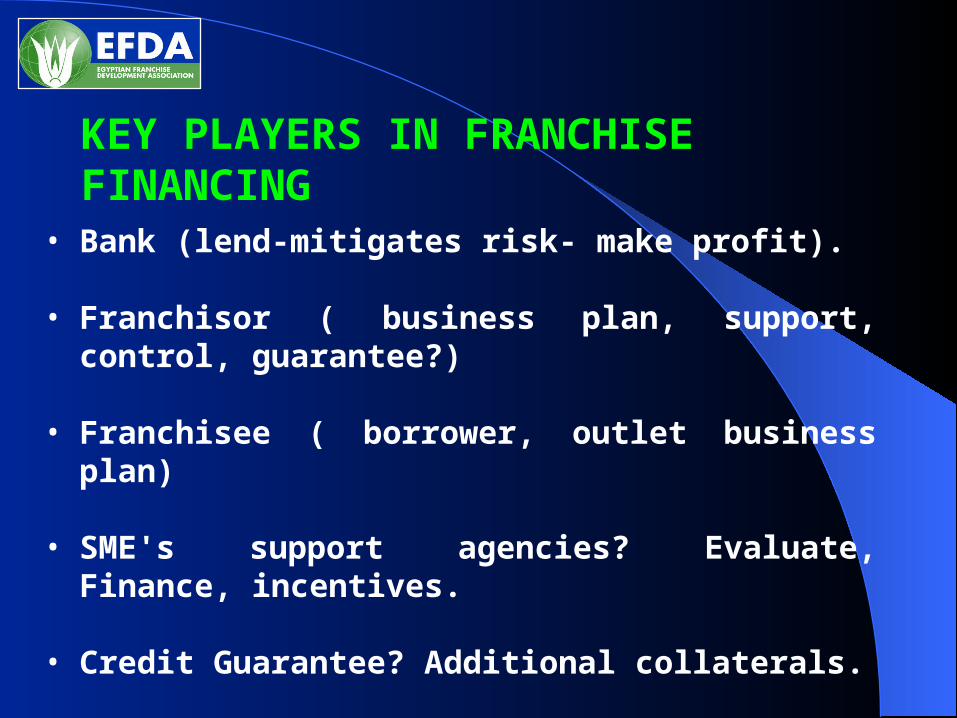

• Bank (lend-mitigates risk- make profit).

• Franchisor ( business plan, support, control, guarantee?)

• Franchisee ( borrower, outlet business plan)

• SME's support agencies? Evaluate, Finance, incentives.

• Credit Guarantee? Additional collaterals.

• Franchise Association? Info, training, industry norms, professional opinion, mediation, code of ethics.

KEY PLAYERS IN FRANCHISE FINANCING

SEE YOU AT MIFE 2014

Middle East and North Africa InternationalFranchising and Licensing Exhibition

May 22nd – 25th, 2014Cairo, Egypt

www.efda.org.eg

THANK YOU