Embed Size (px)

Citation preview

Financing SMEs in Asia and the

Pacific: Trends and Challenges

Workshop on International Trade Finance, Logistics and Business Development

Session 7 (1)28 November 2015, Yangon, Myanmar

Shigehiro Shinozaki

Financial Sector Specialist (SME Finance)

Sustainable Development and Climate Change Department

Asian Development Bank

This presentation was prepared under the author’s responsibility. The views expressed here do not necessarily reflect

the views or policies of ADB, its Board of Directors, or the governments they represent. ADB does not guarantee the

accuracy of the data included in this presentation and accepts no responsibility for any consequences of their use.

Agenda

I. SMEs in ADB Economies

II. Access to Bank Credit

III. Access to NBFIs

IV. SME Capital Markets

V. Access to Finance by Development Stage

VI. SME Finance Policies

VII. Challenges

VIII. Policy Implications

2

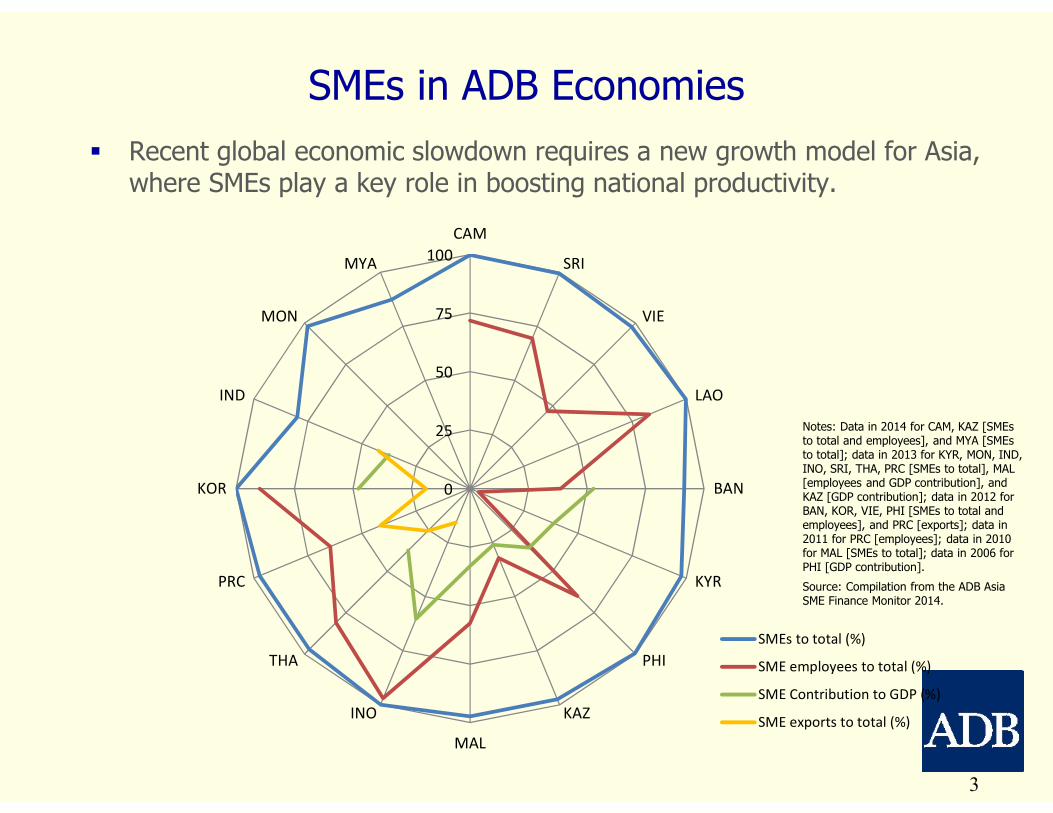

SMEs in ADB Economies

Notes: Data in 2014 for CAM, KAZ [SMEs to total and employees], and MYA [SMEs to total]; data in 2013 for KYR, MON, IND, INO, SRI, THA, PRC [SMEs to total], MAL [employees and GDP contribution], and KAZ [GDP contribution]; data in 2012 for BAN, KOR, VIE, PHI [SMEs to total and employees], and PRC [exports]; data in 2011 for PRC [employees]; data in 2010 for MAL [SMEs to total]; data in 2006 for PHI [GDP contribution].

Source: Compilation from the ADB Asia SME Finance Monitor 2014.

3

� Recent global economic slowdown requires a new growth model for Asia, where SMEs play a key role in boosting national productivity.

0

25

50

75

100

CAM

SRI

VIE

LAO

BAN

KYR

PHI

KAZ

MAL

INO

THA

PRC

KOR

IND

MON

MYA

SMEs to total (%)

SME employees to total (%)

SME Contribution to GDP (%)

SME exports to total (%)

KAZ

PRC

KOR

MON

BAN

INDSRI

INO

MAL

PHI

THA

FIJ

PNG

SOL

0

10

20

30

40

50

0 10 20 30 40 50

SM

E L

oans to T

ota

l Loans (

%)

SME Loans to GDP (%)

� Limited access to bank credit decelerates growth pace of SMEs.

Access to Bank Credit

4

SME Loans, 2014

Source: ADB Asia SME Finance Monitor 2014.

Access to Bank Credit

5

� Lending to SMEs has declined over the course of the GFC and in 2014.

SME received only 18.7% of total bank loans. SME NPLs ranged 2%-18%.

SME Bank Loans to Total Loans (%)

* March/2014 (IND), June/2014 (FIJ [Q2] and KOR), September/2014 (KAZ, PNG, PHI, and SOL), December/2014 (BAN, PRC, INO, MAL, MON, and THA).Notes: For PRC, data based on SME loans outstanding until 2012; while after 2013, based on micro and small enterprise (MSE) loans outstanding. For PHI, data based on total funds set aside for MSMEs (mandatory lending; 10%).Source: Asia SME Finance Monitor 2014.

KAZ

PRCKOR

MON

BAN

IND SRI

INO

MAL

PHI

THA

FIJ PNG

SOL

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013 2014*

(%)

KOR

KOR

BAN

BAN

INO

INO

THATHA

PNG

0.1

1.0

10.0

100.0

2007 2008 2009 2010 2011 2012 2013 2014*

(%) SME NPLs (%)

— SME NPLs to SME loans, - - - SME NPLs to total loans.* June/2014 (KOR), September/2014 (PNG [Q3]), December/2014 (BAN, INO, and THA).Notes: NPLs based on the national loan asset classification. For BAN, the ratio of borrowers with SME NPLs to total SME borrowers. For KOR, the ratio of SME classified loans to total SME loans.Source: Asia SME Finance Monitor 2014.

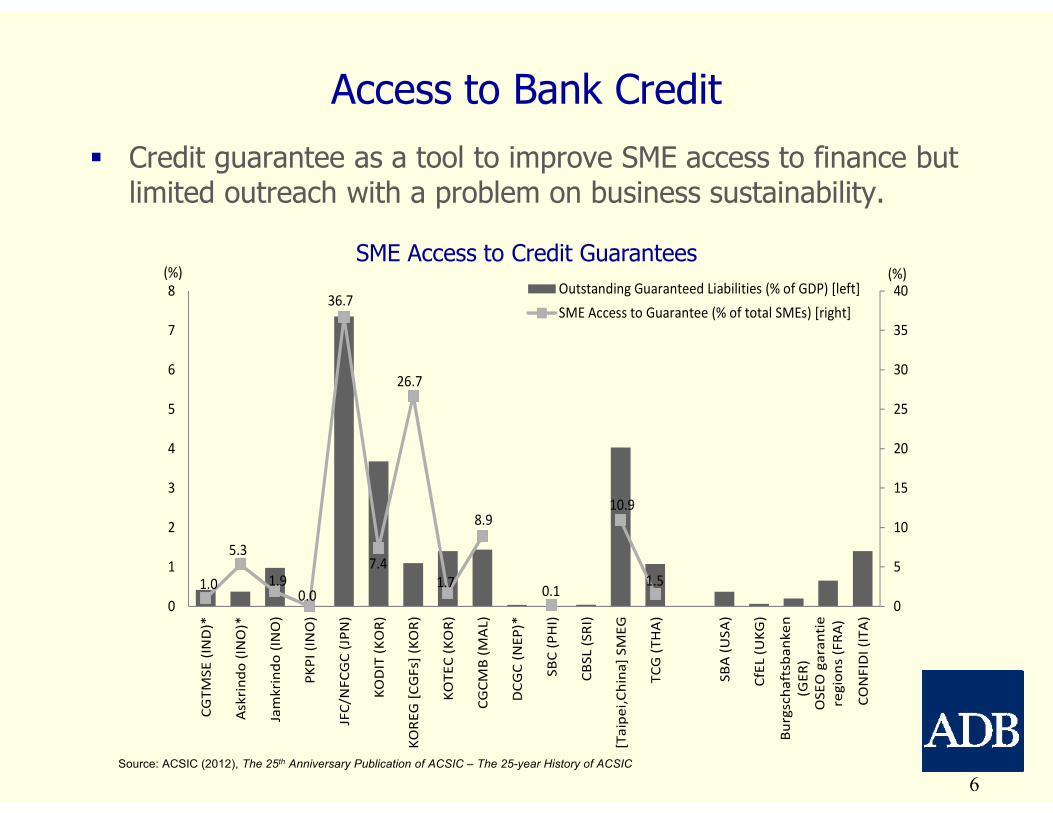

� Credit guarantee as a tool to improve SME access to finance but limited outreach with a problem on business sustainability.

1.0

5.3

1.90.0

36.7

7.4

26.7

1.7

8.9

0.1

10.9

1.5

0

5

10

15

20

25

30

35

40

0

1

2

3

4

5

6

7

8

CG

TM

SE

(IN

D)*

Ask

rin

do

(IN

O)*

Jam

kri

nd

o (

INO

)

PK

PI

(IN

O)

JFC

/NF

CG

C (

JPN

)

KO

DIT

(K

OR

)

KO

RE

G [

CG

Fs]

(K

OR

)

KO

TE

C (

KO

R)

CG

CM

B (

MA

L)

DC

GC

(N

EP

)*

SB

C (

PH

I)

CB

SL (

SR

I)

[Ta

ipe

i,C

hin

a]

SM

EG

TC

G (

TH

A)

SB

A (

US

A)

CfE

L (

UK

G)

Bu

rgsc

ha

ftsb

an

ke

n

(GE

R)

OSE

O g

ara

nti

e

reg

ion

s (F

RA

)

CO

NF

IDI

(IT

A)

Outstanding Guaranteed Liabilities (% of GDP) [left]

SME Access to Guarantee (% of total SMEs) [right]

(%) (%)

6

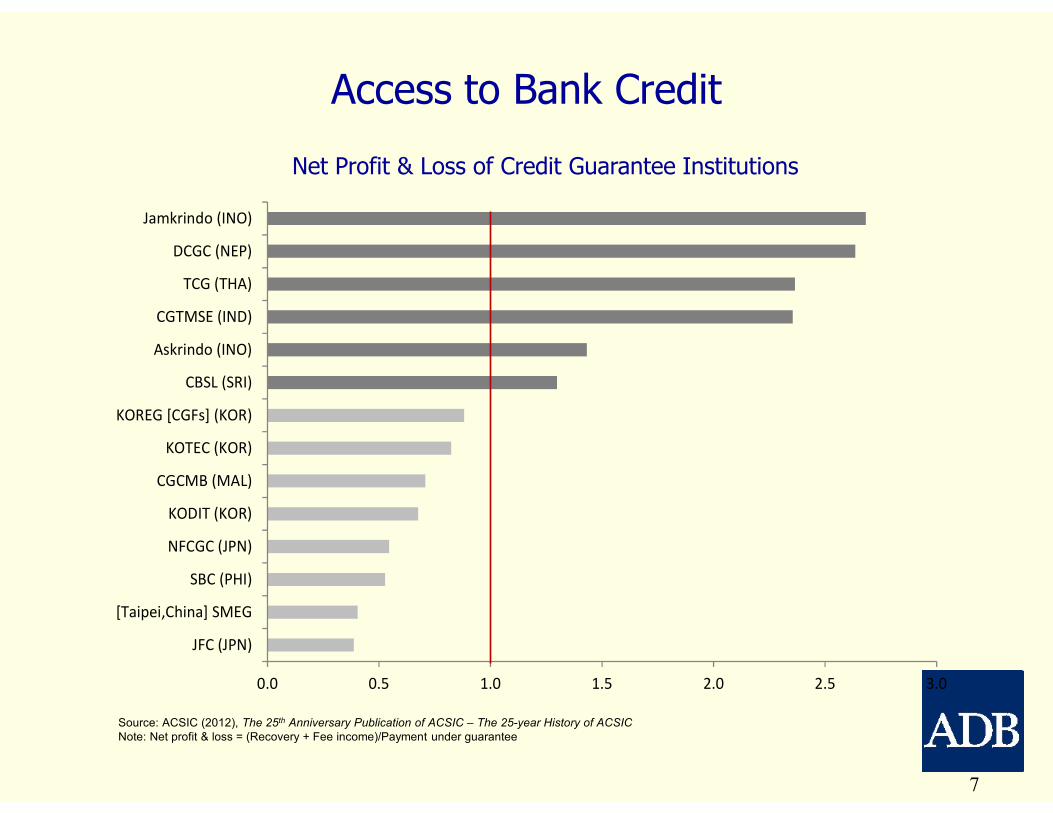

Source: ACSIC (2012), The 25th Anniversary Publication of ACSIC – The 25-year History of ACSIC

Access to Bank Credit

SME Access to Credit Guarantees

0.0 0.5 1.0 1.5 2.0 2.5 3.0

JFC (JPN)

[Taipei,China] SMEG

SBC (PHI)

NFCGC (JPN)

KODIT (KOR)

CGCMB (MAL)

KOTEC (KOR)

KOREG [CGFs] (KOR)

CBSL (SRI)

Askrindo (INO)

CGTMSE (IND)

TCG (THA)

DCGC (NEP)

Jamkrindo (INO)

Source: ACSIC (2012), The 25th Anniversary Publication of ACSIC – The 25-year History of ACSIC

Note: Net profit & loss = (Recovery + Fee income)/Payment under guarantee

Net Profit & Loss of Credit Guarantee Institutions

Access to Bank Credit

7

Access to Bank Credit

8

� Basel III may negatively affect bank lending attitude to SMEs.

� Basel III requires banks to have tighter risk management as well as greater capital and liquidity.

� Resulting asset preference and deleveraging of banks could limit the availability of funding for SMEs.

- Capital requirements: Banks may encourage finance to large firms with good ratings (investment grade) rather than unrated SMEs to reduce total high-risk assets.

- Liquidity framework: Banks may be willing to hold “easy-to-sell assets” or high quality liquid assets, resulting in constraining the provision of long-term credit.

- Leverage ratio framework: Controlled leverage of banks including off-balance transaction may limit financing options for SMEs, e.g., trade finance availability.

KYR

TAJ

PRC

MON

BAN

CAM

INOFIJ

SOL

0

10

20

30

40

50

60

70

80

90

100

0 2 4 6 8 10 12

NB

FI F

inancin

g to B

ank L

oan

s (

%)

NBFI Financing to GDP (%)

LAO, IND,

and MAL

� The nonbank finance industry is small in scale. 11.5% of bank loans.

Access to NBFIs

9

NBFI Financing, 2014

Source: ADB Asia SME Finance Monitor 2014.

Access to NBFIs

10

� The nonbank finance industry is influenced by bank performance.

NBFI financing accounted for 3.1% of GDP. NPF stood at 2.7%

NBFI Financing to GDP (%)

* March/2014 (MYA), April/2014 (LAO), June/2014 (BAN and FIJ [Q2]), September/2014 (CAM and SOL), November 2014 (KYR), December/2014 (INO and MON). Notes: Microfinance institution (MFI) loans disbursed (KYR, IND, and TAJ), MFI loans outstanding (BAN [NGO-MFIs], CAM, PRC, LAO, and MYA), NBFI financing (FIJ, INO, MAL, MON, and SOL). Source: Asia SME Finance Monitor 2014.

NBFI Nonperforming Financing (%)

*end of year data except for KYR (November 2014).Notes: Ratio of nonperformig financing (NPF) to total financing by NBFIs including MFIs, based on the national loan asset classification. Unrecovery ratio of loans (BAN). Based on doubtful plus bad debts (INO). Source: Asia SME Finance Monitor 2014.

KYR

TAJ

PRC MON

BAN

CAM

INO

MAL

FIJ

SOL

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014*

(%)

LAO, IND,

and MYA

KYR

MON

BAN

CAM

INO

0.0

2.0

4.0

6.0

8.0

10.0

2007 2008 2009 2010 2011 2012 2013 2014*

(%)

11

GDP = gross domestic product; SME = small and medium-sized enterprise. *Data as of 31 Oct for KOSDAQ, 28 Nov for ACE, and end-2014 for others.Note: Emerging Asia comprises the People’s Republic of China; Hong Kong, China; the Republic of Korea; Malaysia, Singapore, and Thailand.Source: Author’s calculation based on data from respective stock exchange websites and the ADB Asia SME Finance Monitor 2014 (provisional data).

SME Capital Markets - Equity

SME Board/PRC

ChiNext/PRC

GEM/HKG

KOSDAQ/KOR

ACE/MAL

CATALIST/SIN

mai/THA

0.0

2.0

4.0

6.0

8.0

10.0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

% of GDP

SME Board/PRC

ChiNext/PRC

GEM/HKG

KOSDAQ/KOR

ACE/MALCATALIST/SIN

mai/THA

0

200

400

600

800

1,000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

*

Number

� Although still in the trial stages, positive performances on SME equity markets and government reform efforts have been seen in Asia

Market Capitalization (% of GDP) Number of Listed Companies

12

China, People’s Rep. of Korea, Rep. of

SME Capital Markets - Bonds

� A new movement of creating an SME bond market.

0.00

0.04

0.08

0.12

0.16

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2009 2010 2011 2012 2013 2014

SME Joint Bond SME Collective Note SME bonds to total (%)

(CNY bil.) (%)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0.0

0.5

1.0

1.5

2.0

2.5

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

*

SME bond issuance SME bonds to total (%)

(W tril.) (%)

* Data as of 31 Oct 2014.Source: Author’s compilation from the ADB Asia SME Finance Monitor 2014 (provisional data).

13

Access to Finance by Development Stage� Diversified SME financing tools can push up economic development.

TAJ

BAN

BAN

CAM

MYA MYA -

2

4

6

8

10

12

SME bank loans to GDP

(%)

Nonbank financing to

GDP (%)

SMEequity market -

capitalization to GDP (%)

(%)

KYR

MON

IND

IND IND

SRI

SRI SRI

INO

INO

INO

LAO

PHI

PHIPHI

VIEPNGPNG

SOL

SOL

-

1

2

3

4

5

6

7

8

9

10

SME bank loans to GDP

(%)

Nonbank financing to

GDP (%)

SME equity market -

capitalization to GDP (%)

(%)

PRC

PRC

PRC

KAZ

MAL

MAL MAL

THA

THA

FIJ

FIJ

KOR

KOR

KOR

-

5

10

15

20

25

30

35

40

SME bank loans to GDP

(%)

Nonbank financing to

GDP (%)

SME equity market -

capitalization to GDP (%)

(%)

Low-income Economies Lower-middle-income Economies

Upper-middle-income & High-income Economies

Notes: Data in 2013. Nonbank financing includes financing by microfinance institutions, finance companies, credit unions, leasing, factoring, and venture capital investments. SME equity markets include SME exchanges in BSE & NSE (IND), Diri Savi/CSE (SRI), IDX (INO [10 SMEs listed]), SME Board/PSE (PHI), UPCoM (VIE), SME Board & ChiNext/SZSE (PRC), ACE (MAL), mai (THA), and KOSDAQ/KRX (KOR). Country classification refers to the World Bank classification for FY2015.Source: Author’s calculation based on data extracted from the ADB Asia SME Finance Monitor 2014.

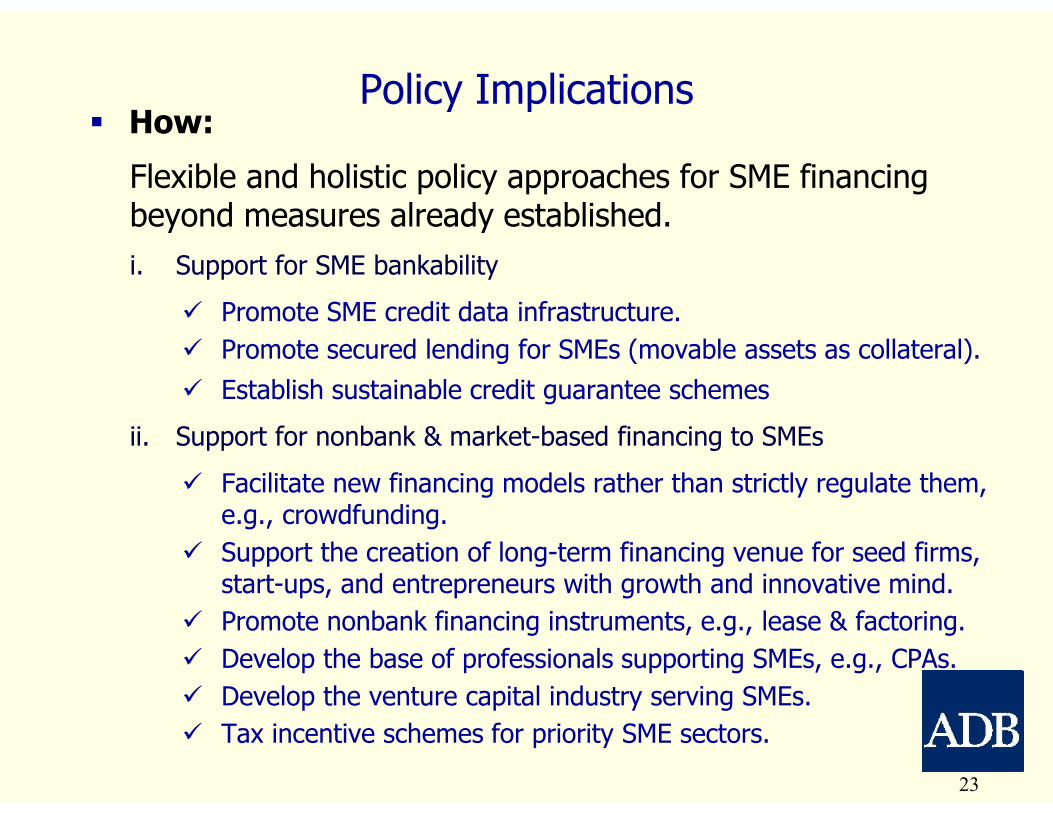

SME Finance Policies

14

� A balanced approach is required to design extensive policy measures for improving SME access to finance and for safeguarding their financial stability.

National SME Finance Policies in Selected Asian Countries

* Funded by private and public sectors. ** TReDS in India: Trade Receivables Discounting System for facilitating trade receivable finance for MSMEs, proposed by the central bank. *** Mandatory creation of microfinance units in banks.Source: ADB Asia SME Finance Monitor 2014.

Public Sector

Refinancing

facility to

banks

Public credit

guarantee

scheme

Mandatory

lending to

MSMEs

Interest rate

subsidy

Public credit

bureau

Secured

transaction

law

Direct

lending/

soft loans

Refinancing

facility to

leasing firms

Refinancing

facility to

factoring

firms

MFI

development

program

NBFI industry

development

(except MFIs)

Equity market

development

for SMEs

Bond market

development

for SMEs

Venture

capital

development

for SMEs

Tax incentive

for SME issuers

and/or

investors

TAJ √ √ √

BAN √ √ √ √ √ √

CAM √ √ √ (pawn business)

MYA √

KYR √ √ √ √

MON √ √ √ √ √

IND √ √ √ √* √ √ (TReDS)** √ √

SRI √ √ √ √ √

INO √ √ √ √ √ √

LAO √ √

PHI √ √ √ √ √ √ √ √

VIE √ √ √ √

PNG √ √ √ √ √

SOL √ √ √ √ √ (credit unions)

PRC √ √ √ √ √ √ √ √ √ √

KAZ √ √ √ √ √

MAL √ √ √ √* √ √ √ √

THA √ √* √ (draft) √ √ √ √

FIJ √ √ √*** √ √ √ √

High-income

economiesKOR √ √ √ √ √ √

Upper-middle-

income

economies

Capital MarketsBanking Sector Nonbank Sector

Low-income

economies

Lower-middle-

income

economies

� Financial infrastructurei. Credit data infrastructure (credit bureau)

ii. Legal framework for secured transactions (collateral registry)

� Sustainable credit guarantee systems

� Innovative product designi. Asset based finance (ABL, factoring, financial lease, and ABS)

ii. Credit score based lending

iii. SME cluster financing

iv. Debtor-in-possession (DIP)/Exit financing

v. Crowdfunding

� Trade finance & supply chain financei. Foster the supporting industries

ii. Stimulate internationalization of SMEs

Challenges: Financing Sophistication and Diversification

15

� Diverse players not yet involved in SME finance spacei. Specialized financiers (e.g., factors and leasing firms)

ii. Market organizers

iii. Risk-taking/contractual savings institutions

� Capital market financing for SMEsi. Respond to long-term funding needs of growth-oriented SMEs

ii. Equity finance, bond issuance, and mezzanine finance

iii. Develop the venture capital industry as a growth capital provider

� Roles of public financial institutions in SME financei. Outreach to the underserved

ii. Timely response to external shocks, e.g., financial crisis and disaster

16

Challenges: Financing Sophistication and Diversification

� In developing Asia, many countries still suffer a lack of legal framework to promote secured transactions.

� Broadening the range of pledgeable assets help enhance SME access to finance, especially women-owned SMEs.

� Pledgeable assets: movable assets, e.g., machinery/equipment, inventory of final goods, and receivables; intellectual property rights, etc.

� For the legal reform on secured transactions:

� A wide-range of pledgeable assets as collateral covered by the secured transaction law/collateral law.

� A sound registration system on movable assets.

� A speedy & efficient collateral enforcement mechanism.

Issue 1: Secured Lending for SMEs

17

Issue 2: Sustainable Credit Guarantee Systems

18

� Business sustainability� Cost efficiency & profitability

� Diversified & demand-driven business approach

� Self-funding (shift from public-dependent to market-based)

� Risk control arrangements� Develop re-guarantee system (credit insurance)

� Develop risk-sharing schemes (partial credit guarantee)

� Strengthen second credit screening by guarantee institutions

� Decentralization or centralization� Promote a regional CG system with a proper legal framework

� Develop product design for the centralized CG system (e.g., Portfolio CG)

� Infrastructure� Establish a credit risk database or credit bureau

� Credit database supports proper pricing and risk-based management by guarantee institutions.

China-Korea Currency Swap Trade Settlement

� Enable importers & exporters to settle their trade transactions in their local currencies.

� Promote LCY invoicing & settlement, reduce transaction costs for importers & exporters, and potentially benefit SME exporters & importers, especially in ASEAN countries after AEC establishment in 2015.

� ...but not yet an established system.

Issue 3: Trade Finance Facilitation for SMEs

BOK PBOC

PBOC A/C BOK A/C

Korean

BankChinese Bank

Korean Importer Chinese Exporter

① KRW ① CNY

③ CNY③

⑧ CNY⑧

⑥ CNY④ CNY Loan⑦ Repayment

② Commodity Import

⑤ Payment Instruction

① KRW / CNYCurrency Swap

Source: Extracted from the ADB presentation material “LCY Trade Settlement in ASEAN+3” prepared by D. Park and I. Shin in the ABMI Task Force Meeting, Myanmar, 27 February 2014. 19

20

Seed/Start-up/Early Expansion Steadily growing

Founders, family

& friends

Sophisticated investors

-VC funds

-Financial institutions

-Institutional investors

-Listed large firms with sufficient

investment experiences, etc.

Venture capital

Size of

investment

capital

Growth

capital

needed

Firms’

life

cycle

Exchange markets

IPO

Organized OTC

Private equity,

mezzanine finance,

etc.

Angel investors

Formal & informal

lending

-Domestic market for

emerging corporations

(SME board)

-International market for

smaller growing firms

(AIM)

-Trading venue for

unlisted SME shares

(non-exchange markets)

Source: Author’s illustration.

Growth Capital Funding and Risk Capital Providers

Issue 4: SME Capital Markets

� What:

Provide timely financing opportunities for SMEs while responding to their needs with flexibility and innovation.

� Poor access to finance limits the ability of SMEs to survive and grow.

� Limitations of bank lending under global financial uncertainty, e.g., possible negative impact of Basel III.

� No one-size-fits-all financing solution. Diversification of SME finance models is needed.

� Long-term funding needs increase as SMEs grow further. Potential for developing SME capital markets in Asia.

Policy Implications

21

� Why:

New environment requires new financing solutions for SMEs.

� Economic integration and increasing FDI inflows to Asia stimulate the structural change of SME business models.

� A globalized economy will bring more SME internationalization and new financing demands from SMEs.

� Increased importance of supply chain finance and trade finance to involve SMEs in global value chains.

Limitations to relying on own- or quasi-capital for SMEs to sustain their business.

� Diversified financing models besides traditional bank credit should be developed for healthy debt-equity structure of SMEs.

� Long-term financing for growth-oriented SMEs is key.

22

Policy Implications

� How:

Flexible and holistic policy approaches for SME financing beyond measures already established.

i. Support for SME bankability

� Promote SME credit data infrastructure.

� Promote secured lending for SMEs (movable assets as collateral).

� Establish sustainable credit guarantee schemes

ii. Support for nonbank & market-based financing to SMEs

� Facilitate new financing models rather than strictly regulate them, e.g., crowdfunding.

� Support the creation of long-term financing venue for seed firms, start-ups, and entrepreneurs with growth and innovative mind.

� Promote nonbank financing instruments, e.g., lease & factoring.

� Develop the base of professionals supporting SMEs, e.g., CPAs.

� Develop the venture capital industry serving SMEs.

� Tax incentive schemes for priority SME sectors.

23

Policy Implications

� Roles of policymakers to improve SME access to finance in your country. What are key policy components and challenges for financing SMEs?

� Ways of enhancing bankability for SMEs. What kind of innovative product design can be considered with technology?

� Potential of developing nonbank and market-based financing for SMEs. What are challenges and solutions for developing trade finance and supply chain finance?

24

Discussions

Asia SME Finance Monitor 2014

[http://www.adb.org/publications/asia-sme-finance-monitor-2014]

Asia SME Finance Monitor 2013 [http://www.adb.org/publications/asia-small-and-medium-sized-enterprise-sme-finance-monitor-2013]

References

25

Thank you for your attention.

For further questions:

Shigehiro Shinozaki

Financial Sector Specialist (SME Finance)

Sustainable Development and Climate Change Department

Asian Development Bank

Email: [email protected]

26