Embed Size (px)

Citation preview

Finding our Voice with ShareholdersPresentation to Marketing Executives ConferenceOklahoma City, Oklahoma

September 29, 2014

Doug Petitt

Chief Information Officer

Vice President Information Technology and Customer Service

Gas55%

Gas55%

Page 2

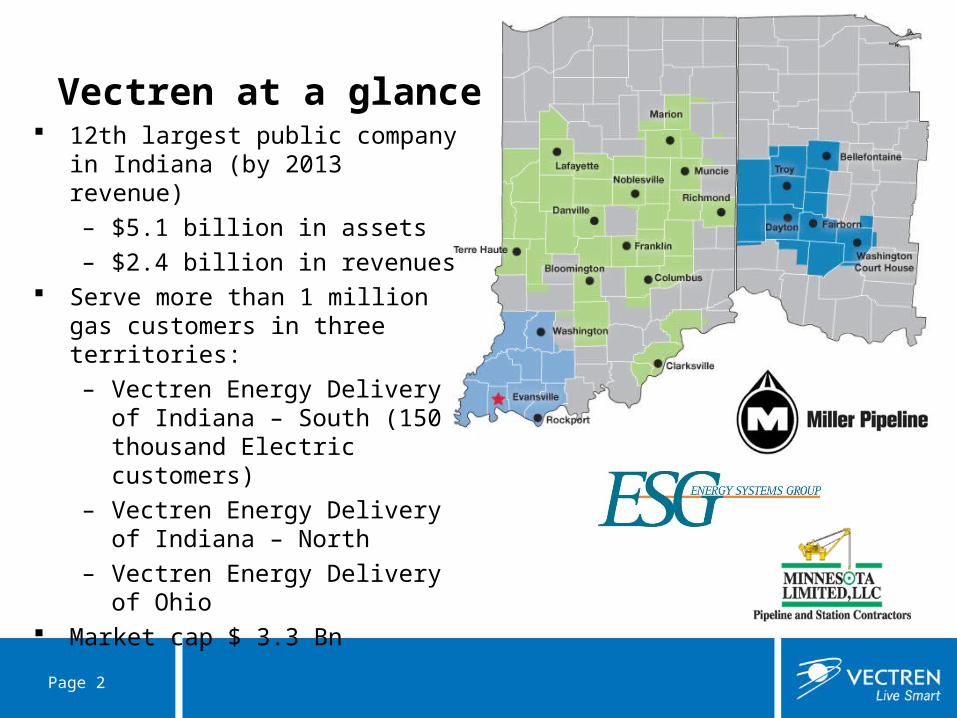

12th largest public company in Indiana (by 2013 revenue)– $5.1 billion in assets– $2.4 billion in revenues

Serve more than 1 million gas customers in three territories:– Vectren Energy Delivery of

Indiana – South (150 thousand Electric customers)

– Vectren Energy Delivery of Indiana – North

– Vectren Energy Delivery of Ohio Market cap $ 3.3 Bn

Vectren at a glance

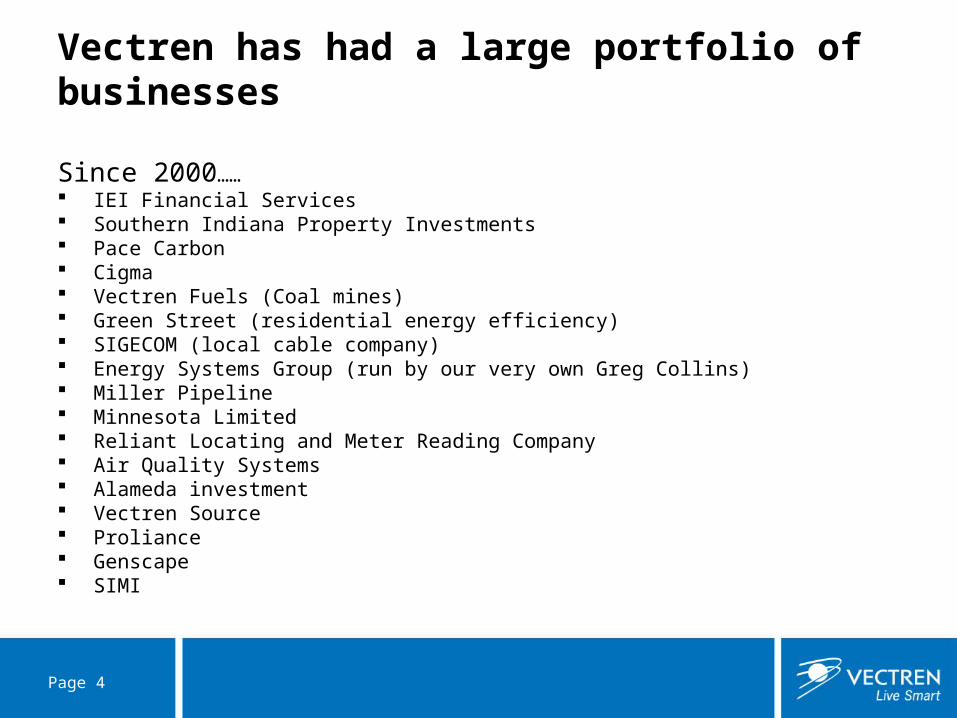

Vectren has had a large portfolio of businesses

Since 2000…… IEI Financial Services Southern Indiana Property Investments Pace Carbon Cigma Vectren Fuels (Coal mines) Green Street (residential energy efficiency) SIGECOM (local cable company) Energy Systems Group (run by our very own Greg Collins) Miller Pipeline Minnesota Limited Reliant Locating and Meter Reading Company Air Quality Systems Alameda investment Vectren Source Proliance Genscape SIMI

Page 4

We have been on the path of De-risking our Company,

resulting in consistent Earnings Growth

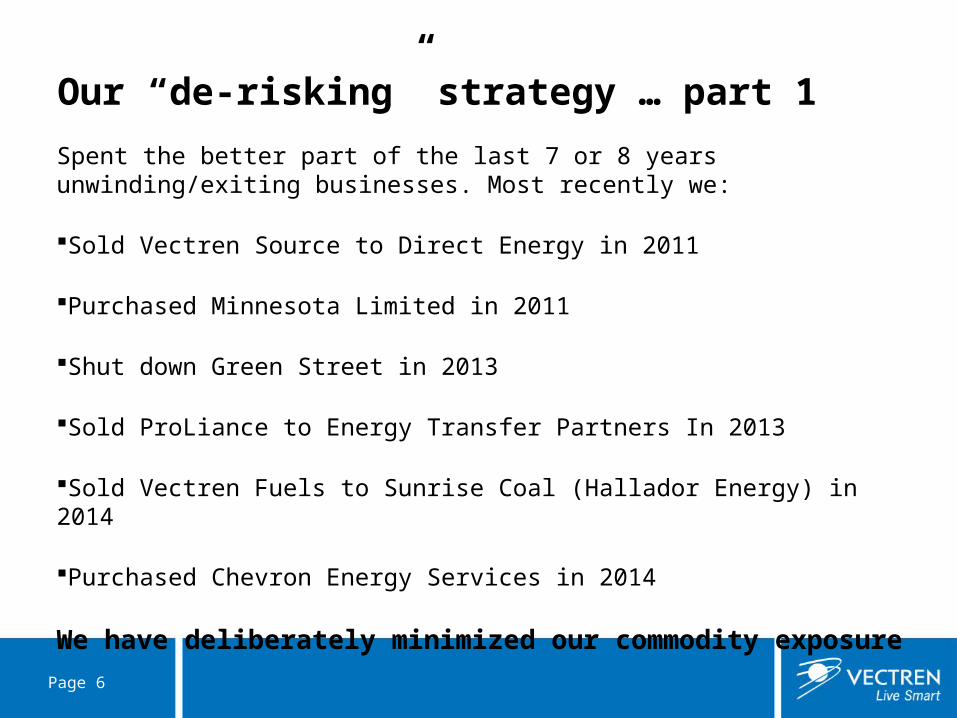

Our “de-risking” strategy … part 1

Spent the better part of the last 7 or 8 years unwinding/exiting businesses. Most recently we:

Sold Vectren Source to Direct Energy in 2011

Purchased Minnesota Limited in 2011

Shut down Green Street in 2013

Sold ProLiance to Energy Transfer Partners In 2013

Sold Vectren Fuels to Sunrise Coal (Hallador Energy) in 2014

Purchased Chevron Energy Services in 2014

We have deliberately minimized our commodity exposure

Page 6

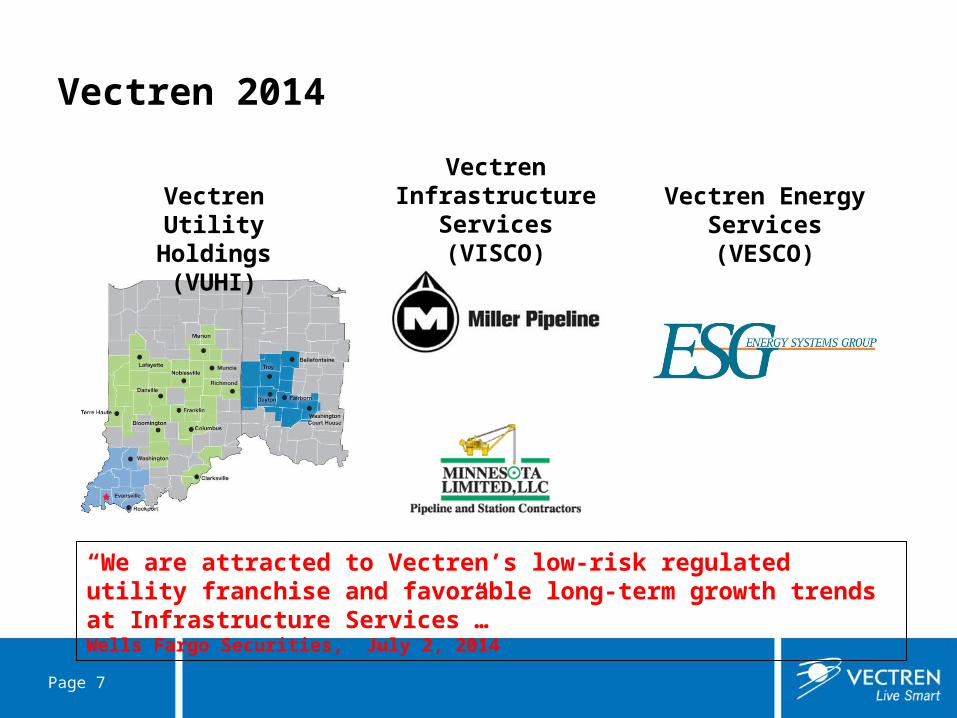

Vectren 2014

Page 7

Vectren Utility Holdings (VUHI)

Vectren Infrastructure

Services (VISCO)Vectren Energy

Services (VESCO)

“We are attracted to Vectren’s low-risk regulated utility franchise and favorable long-term growth trends at Infrastructure Services”…Wells Fargo Securities, July 2, 2014

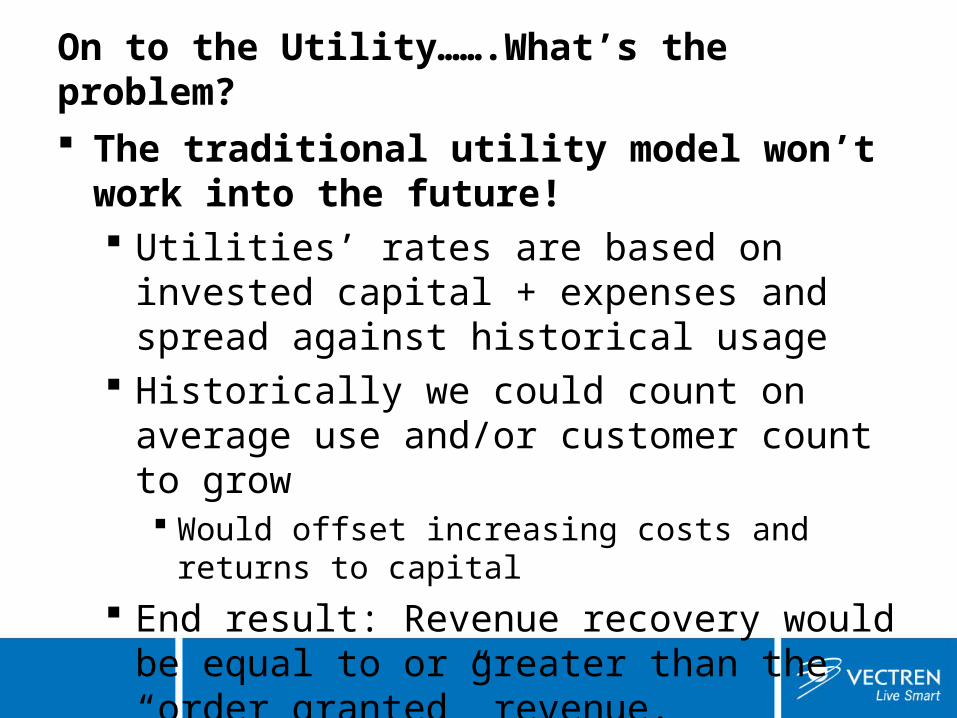

On to the Utility…….What’s the problem? The traditional utility model won’t work into

the future! Utilities’ rates are based on invested capital +

expenses and spread against historical usage Historically we could count on average use

and/or customer count to grow Would offset increasing costs and returns to capital

End result: Revenue recovery would be equal to or greater than the “order granted” revenue.

For a number of reasons that assumption isn’t true anymore…..we won’t recover our order-granted margins

These reasons include:

Energy Efficiency– Naturally occurring– Utility driven (full cost and margin recover?)

Distributed generation – Including solar, wind and co-generation

Net meteringDemand responseMicrogridsetc.,

Interestingly enough, Shareholders are NOT asking for a new model

Page 10

“The solar industry belongs with the natural gas industry – those industries go together. They just don’t know it yet”

“At present, we believe that electric industry credit spreads are pricing in virtually no risk of a significant industry disruption”

Source. Quote from NRG CEO Crane, Bloomberg New Energy Finance conference, April, 2013, Barclays, May 20, 2014

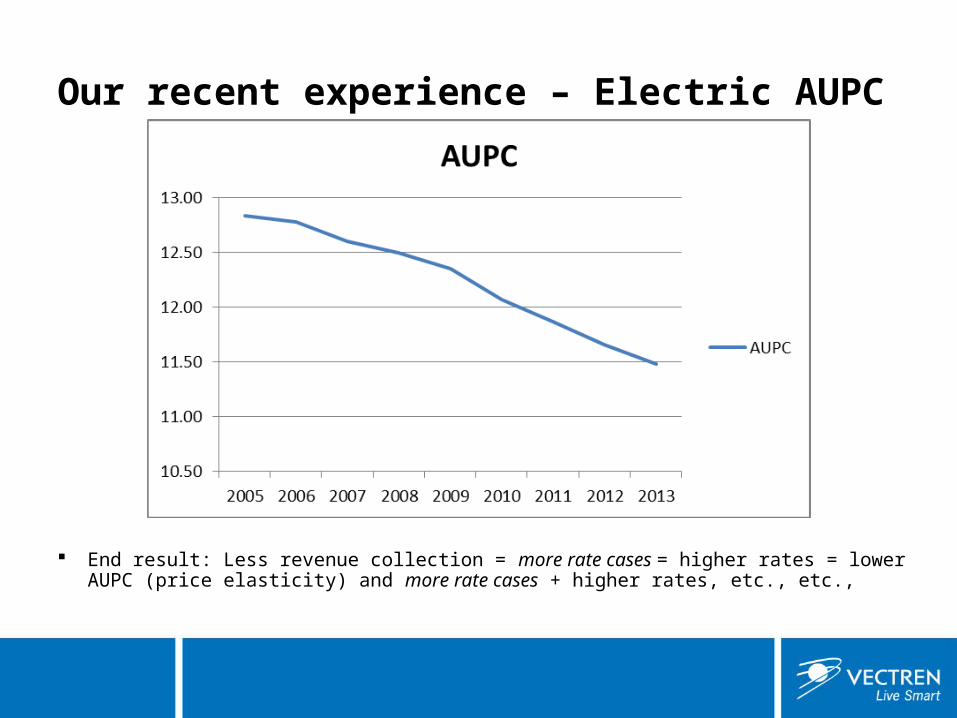

Our recent experience – Electric AUPC

End result: Less revenue collection = more rate cases = higher rates = lower AUPC (price elasticity) and more rate cases + higher rates, etc., etc.,

The challenge …

Page 12

We’ve dealt with this in the past

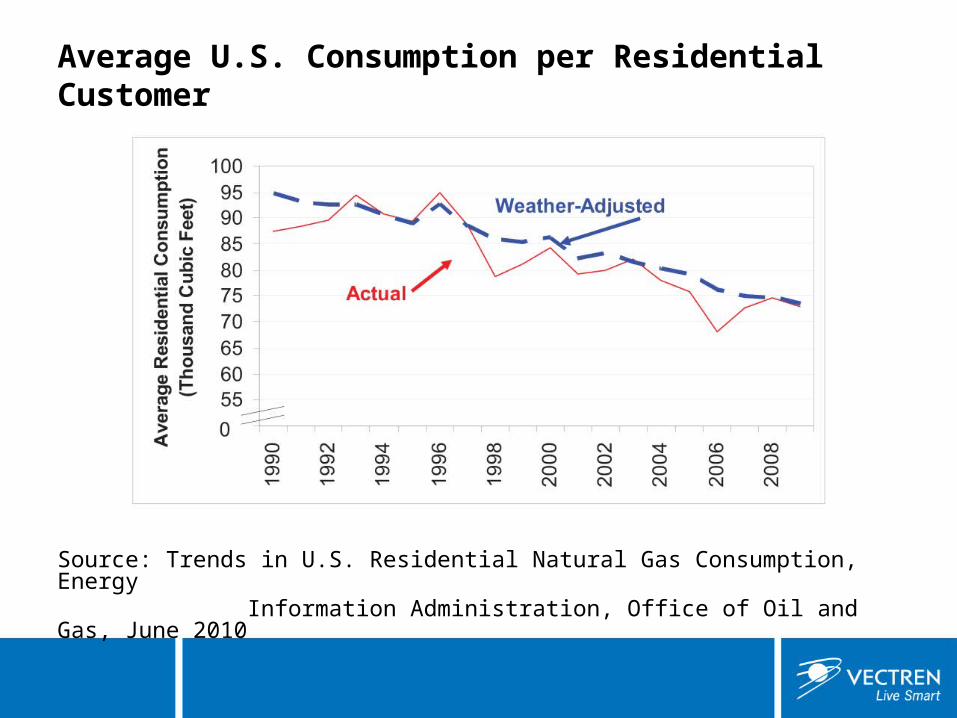

Average U.S. Consumption per Residential Customer

Source: Trends in U.S. Residential Natural Gas Consumption, Energy Information Administration, Office of Oil and Gas, June 2010

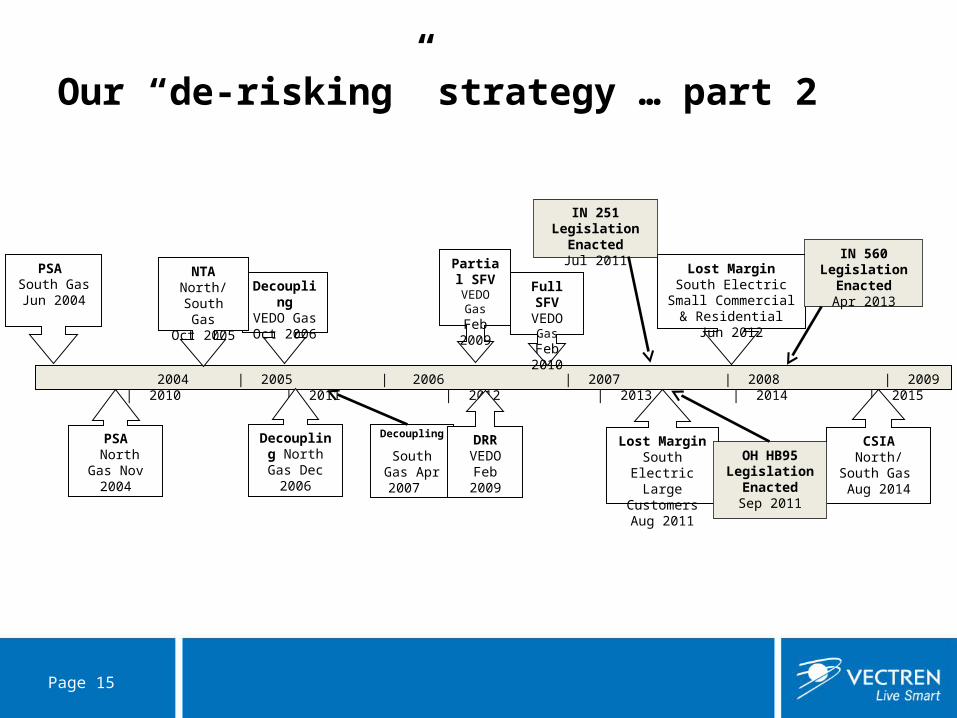

Our “de-risking” strategy … part 2

Page 15

D Decoupling North Gas

Decoupling

South Gas Apr 200706

ecoupling North Gas Dec 2006

2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015

DecouplingVEDO GasOct 2006

NTANorth/South

GasOct 2005

PSA South Gas Jun

2004

PSA North Gas Nov 2004

Lost MarginSouth Electric

Large CustomersAug 2011

Partial SFV

VEDO GasFeb 2009

Lost MarginSouth Electric

Small Commercial & Residential Jun 2012

Decoupling North Gas Dec 2006

Full SFVVEDO GasFeb 2010

CSIANorth/South

Gas Aug 2014

DRRVEDO

Feb 2009

IN 251 Legislation EnactedJul 2011

IN 560 Legislation EnactedApr 2013

OH HB95 Legislation

EnactedSep 2011

Favorable Regulatory Mechanisms/Legislation for Vectren PSA North and South Recovers incremental non-capital expenses incurred due to requirements of the federal Pipeline Safety Improvement

Act of 2002. PSA includes Costs captured through December 2013. Costs incurred from January 2014 and beyond will be in new CSIA infrastructure mechanism described below. PSA expenses will transition into the new CSIA mechanism.

NTA adjusts each Customer's monthly billed amount to reverse the impact on margin recovery caused by non-normal temperatures during the billing period, as measured by actual heating degree day variations from normal heating degree days.

Decoupling mechanisms normalizes customer margin recovery to equal the level used to establish rates. February 2009 marked the last period to true up margin variance to base rates in VEDO due to adoption of SFV rate design. North and South Gas decoupling mechanism will expire in December 2015 unless we file for an extension by March, which we will do.

CSIA – 7-year investment plan approved August 2014; first tracker rates will become effective in January 2015 and will recover costs beginning in January 2014.– Indiana SEA 251 – Recovery of federally mandated costs. – Vectren’s Order approved 7 Year Capital Spend:– Vectren North $369,693– Vectren South $173,677

Indiana SEA 560 – Transmission, Distribution, and Storage System Improvement Charge (TDSIC) – Vectren’s Order approved 7 Year Capital Spend Plan:– Vectren North $277,442– Vectren South $43,103

DRR recovers infrastructure replacement. PUCO Order in February 2014 extended DRR through program investments through end of 2017. Must file base rate case in order to further extend.

HB95 allows for deferred accounting treatment of capital expenditures related to:

1. Any infrastructure expansion, infrastructure improvement, or infrastructure replacement program;

2. Any Program to install, upgrade, or replace information technology system;

3. Any program reasonably necessary to comply with any rules, regulations, or orders of the commission or other governmental entity having jurisdiction.”

4. Capital Expenditure Plans must be submitted annually in March.

So, what do we do with the electric utility?

Load as much into the fixed monthly charge as possible– SFV loads 100% into the fixed charge. All variable costs (fuel costs) are

passed through volumetrically– Decoupling allows the utility to collect revenues volumetrically and trues

up periodically The intent is to recover fixed costs of generation, transmission and distribution If you can’t achieve full SFV or Decoupling, nibble around the edges. Attempt

to get incremental costs recovered in trackers (outside of the traditional rate cases).

Taking on the Frog … getting started Develop “points of view” (POVs) on key drivers on trends

– Right to left– Focus on customers and markets … not your in-the-ground/air assets

Develop long-term driver-based financial forecasts (use POVs)– Drive estimates of long-term EPS, cash flow / cap ex requirements

Develop scenarios, what-if and / or probabilistic analytics

Obtain senior management time commitment – Debate and alignment on POVs – Implications for change

Bring along the Board

Begin the Journey– Resources– Vision

Page 18

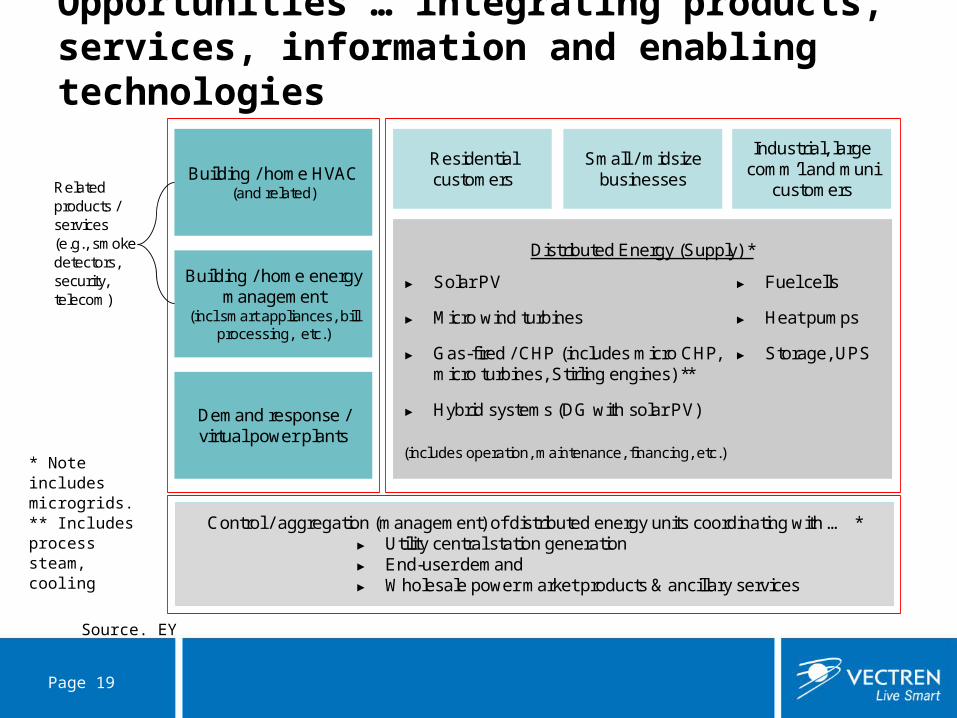

Opportunities … integrating products, services, information and enabling technologies

Page 19

Related products / services (e.g., smoke detectors, security, telecom)

Control / aggregation (management) of distributed energy units coordinating with … *► Utility central station generation► End-user demand► Wholesale power market products & ancillary services

Building / home HVAC(and related)

Building / home energy management

(incl smart appliances, bill processing, etc.)

Demand response / virtual power plants

Residential customers

Small / midsize businesses

Industrial, large comm’l and muni

customers

Distributed Energy (Supply) *

► Solar PV

► Micro wind turbines

► Gas-fired / CHP (includes micro CHP, micro turbines, Stirling engines) **

► Hybrid systems (DG with solar PV)

► Fuel cells

► Heat pumps

► Storage, UPS

(includes operation, maintenance, financing, etc.)* Note includes microgrids.** Includes process steam, cooling

Source. EY

20

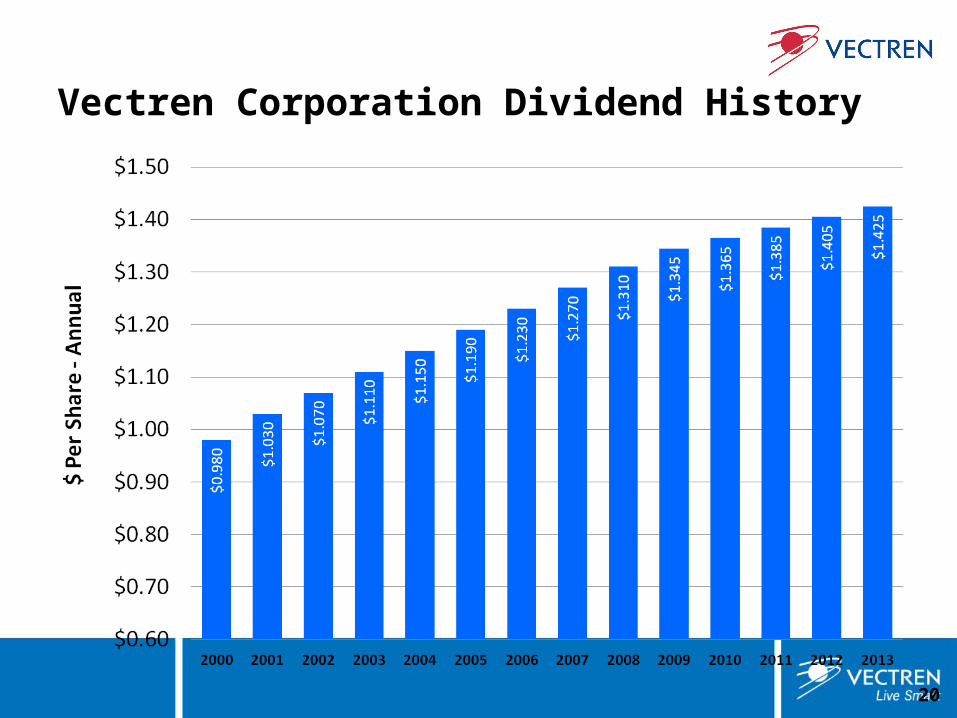

Vectren Corporation Dividend History

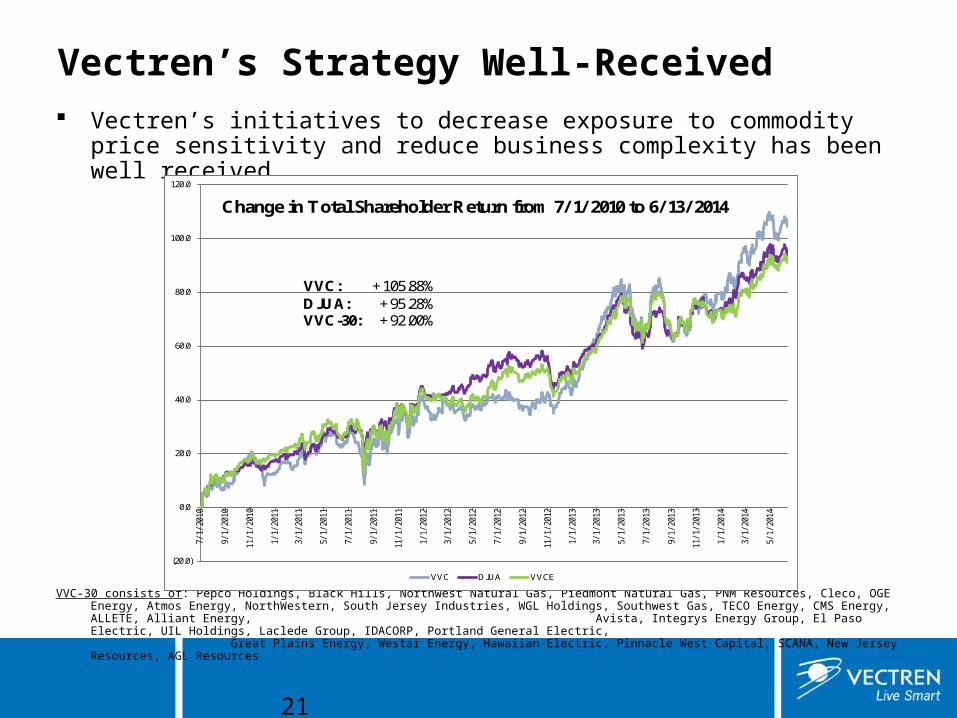

Vectren’s initiatives to decrease exposure to commodity price sensitivity and reduce business complexity has been well received

VVC-30 consists of: Pepco Holdings, Black Hills, Northwest Natural Gas, Piedmont Natural Gas, PNM Resources, Cleco, OGE Energy, Atmos Energy, NorthWestern, South Jersey Industries, WGL Holdings, Southwest Gas, TECO Energy, CMS Energy, ALLETE, Alliant Energy, Avista, Integrys Energy Group, El Paso Electric, UIL Holdings, Laclede Group, IDACORP, Portland General Electric, Great Plains Energy, Westar Energy, Hawaiian Electric, Pinnacle West Capital, SCANA, New Jersey Resources, AGL Resources

(20.0)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

7/1/2010

9/1/2010

11/1/2010

1/1/2011

3/1/2011

5/1/2011

7/1/2011

9/1/2011

11/1/2011

1/1/2012

3/1/2012

5/1/2012

7/1/2012

9/1/2012

11/1/2012

1/1/2013

3/1/2013

5/1/2013

7/1/2013

9/1/2013

11/1/2013

1/1/2014

3/1/2014

5/1/2014

VVC DJUA VVCE

Change in StockPrice from 7/ 1/ 2010 to 6/ 13/ 2014

VVC: +105.88%DJUA: +95.28%VVC-30: +92.00%

Vectren’s Strategy Well-Received

21

(20.0)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

7/1/2010

9/1/2010

11/1/2010

1/1/2011

3/1/2011

5/1/2011

7/1/2011

9/1/2011

11/1/2011

1/1/2012

3/1/2012

5/1/2012

7/1/2012

9/1/2012

11/1/2012

1/1/2013

3/1/2013

5/1/2013

7/1/2013

9/1/2013

11/1/2013

1/1/2014

3/1/2014

5/1/2014

VVC DJUA VVCE

Change in TotalShareholder Return from 7/ 1/ 2010 to 6/ 13/ 2014

VVC: +105.88%DJUA: +95.28%VVC-30: +92.00%

The game is changing…..

Conclusion

How do you satisfy Shareholders?– Satisfy your Customers!– Have constructive relationships with your Regulators!– Focus on long term shareholder value creation

o Consistent and predictable earnings (do what you said you were going to do

o Appreciable stock growtho Dividend growth o Predictable earnings