Embed Size (px)

Citation preview

F INDING VALUE IN DEBT AND EQUITY: HOW STRATEGY CAN RESPOND TO CHANGED PR IC ING

C B R E E U R O P E A N D E B T M A P Q 3 2 0 2 0

November 2020

2CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S U M M A R Y

Debt terms have changed,

reflecting new lending appetite. Retail has seen

the greatest adverse

movement, logistics the least.

Lenders have a renewed focus on risk, with much greater caution being taken on retail and to a lesser extent

office lending.

More expensive and/or lower LTV debt has reduced

geared real estate forecasts –

but has been compensated for

by upwards forecast revisions.

This is a cyclically advantageous

equity side entry-point. And with

risk/reward often disconnected,

attractive returns can also be found on the debt side.

Mezzanine, whole loan and

development financing have seen parallel

shifts in pricing to senior lending.

Attractive premia are available.

LENDER RETURNS

HOW DO Q3 2020 LENDING TERMS DIFFER TO THOSE REPORTED IN Q4 2019?

4CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

C H A N G E S I N P R I M E S E N I O R L E N D I N G F R O M Q 4 2 0 1 9 T O Q 3 2 0 2 0

Widespread decline in LTV.

Margins rise almost universally; falls where narrower definition of

prime.

Cost of debt rises in most markets (we assume 0% floor in

interest rate component).

Selected decline in LTV, but resilience or even increase in some (logistics) markets betrays “flight to quality”.

Margins stable in largest markets, rising in Nordics and CEE.

Margins rise in Western Europe. Margins fall in Western Europe.

Cost of debt falls in as many markets as it rises.

More markets see cost of debt rise than fall; UK (capturing benefit of falling rates) a notable exception.

5CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G K E Y T E R M S , P R I M E O F F I C E , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

In the bellwether prime office senior lending market, amidst a general pattern of LTVs falling and margins and cost of debt rising, a definite “flight to quality” was also evident, as lending terms in the largest markets saw less turbulence than elsewhere.

When comparing Q4 2019 and Q3 2020 lending terms for prime senior offices, the largest markets have seen comparatively little point-to-point change (though this of course masks turbulence through the period). LTVs are unchanged in the four G7 member countries, while Milan and London seen slight declines in margins. London has also benefitted from a fall in the five year swap rate.

In contrast, margins and total cost of debt rose (typically by 25-35bps or so) in five and LTVs fell (by 2.5pp to 15pp) in all seven of the Rest of West markets.

In the Nordics excluding Stockholm, we judge LTVs to be stable and margins either flat (Copenhagen) or higher (Helsinki and Oslo). Falling swap rates however have pushed the cost of debt down in Oslo.

Finally, CEE has seen fairly universal falls in LTV and increases in margins and total cost of debt. Across the five markets, the average LTV fell over 6pp while the average margin and cost of debt rose slightly.

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

G7 MEMBERS ↔ 58.75 (58.75) ↑ 1.29 (1.28) ↓ 1.46 (1.61) NORDICS ↔ 60.00 (60.00) ↑ 1.55 (1.30) ↓ 1.83 (1.98)

Paris ↔ 60.00 (60.00) ↑ 1.20 (1.00) ↑ 1.30 (1.10) Copenhagen ↔ 60.00 (60.00) ↔ 0.90 (0.90) ↓ 0.96 (0.97)

Frankfurt ↔ 60.00 (60.00) ↔ 1.00 (1.00) ↑ 1.14 (1.10) Helsinki ↔ 55.00 (55.00) ↑ 1.45 (1.25) ↑ 1.55 (1.35)

Milan ↔ 60.00 (60.00) ↓ 1.30 (1.40) ↓ 1.40 (1.50) Oslo ↔ 65.00 (65.00) ↑ 2.30 (1.80) ↓ 2.99 (3.89)

London ↔ 55.00 (55.00) ↓ 1.65 (1.70) ↓ 2.01 (2.72) Stockholm (60.00) (1.25) (1.72)

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

REST OF WEST GROUP ↓ 58.75 (65.00) ↑ 1.45 (1.28) ↑ 1.55 (1.37) CEE GROUP ↓ 61.88 (68.13) ↑ 2.33 (2.26) ↑ 2.44 (2.38)

Vienna ↓ 60.00 (75.00) ↓ 1.70 (1.90) ↓ 1.80 (2.00) Prague ↓ 62.50 (70.00) ↑ 2.05 (1.70) ↑ 2.15 (1.80)

Brussels ↓ 60.00 (62.50) ↑ 1.20 (0.95) ↑ 1.27 (1.02) Budapest ↓ 62.50 (70.00) ↑ 2.50 (2.35) ↑ 2.60 (2.45)

Dublin ↓ 55.00 (60.00) ↑ 1.70 (1.40) ↑ 1.86 (1.55) Warsaw ↓ 62.50 (70.00) ↑ 2.25 (2.00) ↑ 2.40 (2.15)

Amsterdam ↓ 60.00 (62.50) ↑ 1.20 (0.85) ↑ 1.27 (0.90) Bucharest ↓ 60.00 (62.50) ↓ 2.50 (3.00) ↓ 2.60 (3.10)

Lisbon ↓ 57.50 (65.00) ↑ 2.13 (1.83) ↑ 2.28 (1.98) Bratislava ↓ 67.50 (70.00) ↑ 2.15 (1.90) ↑ 2.25 (2.00)

Madrid ↓ 55.00 (60.00) ↑ 2.00 (1.75) ↑ 2.15 (1.95) *Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.Zurich ↓ 60.00 (70.00) ↓ 1.00 (1.50) ↓ 1.00 (1.52)

6CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G K E Y T E R M S , P R I M E R E T A I L , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Turbulence in retail occupational and investment markets has fed through to lending. LTVs have fallen and margins risen – though in some markets a narrowing of the definition of what constitutes prime is responsible for apparently contradictory movements.

As with offices, the largest markets have seen the least point-to-point change in retail lending terms when comparing Q4 2019 and Q3 2020. LTVs are static in three G7 member countries (having already been more modest), while Milan and London record lower margins. This does not indicate renewed confidence in retail lending, rather a narrowing of what each market considers “prime” to the most defensive assets (which thus attract better pricing).

In contrast, margins and total cost of debt rose (typically by 20-50bps or so) in five and LTVs fell (by 2.5pp to 15pp) in all seven of the Rest of West markets.

In the Nordics markets excluding Stockholm, we judge LTVs and margins to be flat in Copenhagen. However both Helsinki and Oslo have seen LTVs fall 5bps and margins rise considerably.

Finally, CEE has seen fairly universal falls in LTV and increases in margins and total cost of debt. Across the five markets, the average LTV fell over 6pp while the average margin and cost of debt rose around 20bps.

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

G7 MEMBERS ↓ 53.75 (55.00) ↓ 1.64 (1.89) ↓ 1.85 (2.26) NORDICS ↓ 56.67 (58.75) ↑ 1.97 (1.48) ↑ 2.25 (2.16)

Paris ↓ 55.00 (60.00) ↑ 1.30 (1.25) ↑ 1.40 (1.35) Copenhagen ↔ 60.00 (60.00) ↔ 0.90 (0.90) ↓ 0.96 (0.97)

Frankfurt ↔ 60.00 (60.00) ↔ 1.00 (1.00) ↑ 1.14 (1.10) Helsinki ↓ 50.00 (55.00) ↑ 2.50 (1.30) ↑ 2.60 (1.40)

Milan ↔ 50.00 (50.00) ↓ 2.25 (2.80) ↓ 2.45 (3.00) Oslo ↓ 60.00 (65.00) ↑ 2.50 (2.00) ↓ 3.19 (4.09)

London ↔ 50.00 (50.00) ↓ 2.00 (2.50) ↓ 2.40 (3.58) Stockholm (55.00) (1.70) (2.17)

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

REST OF WEST GROUP ↓ 57.50 (65.63) ↑ 1.73 (1.49) ↑ 1.85 (1.59) CEE GROUP ↓ 60.00 (66.25) ↑ 2.63 (2.44) ↑ 2.73 (2.55)

Vienna ↓ 60.00 (75.00) ↓ 1.90 (2.10) ↓ 2.00 (2.20) Prague ↓ 60.00 (70.00) ↑ 2.20 (1.80) ↑ 2.30 (1.90)

Brussels ↓ 60.00 (65.00) ↑ 1.50 (1.10) ↑ 1.60 (1.17) Budapest ↓ 60.00 (70.00) ↑ 2.70 (2.45) ↑ 2.80 (2.55)

Dublin ↓ 50.00 (60.00) ↑ 2.00 (1.50) ↑ 2.20 (1.65) Warsaw (65.00) (2.10) (2.25)

Amsterdam ↓ 60.00 (62.50) ↑ 1.50 (1.25) ↑ 1.60 (1.32) Bucharest ↔ 60.00 (60.00) ↓ 3.00 (3.40) ↓ 3.10 (3.50)

Lisbon ↓ 50.00 (55.00) ↑ 2.25 (2.00) ↑ 2.40 (2.20) Bratislava ↓ 65.00 (70.00) ↑ 2.40 (2.25) ↑ 2.50 (2.35)

Madrid ↓ 50.00 (60.00) ↑ 2.25 (2.00) ↑ 2.40 (2.20) *Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.Zurich ↓ 60.00 (65.00) ↓ 1.50 (1.75) ↓ 1.50 (1.80)

7CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

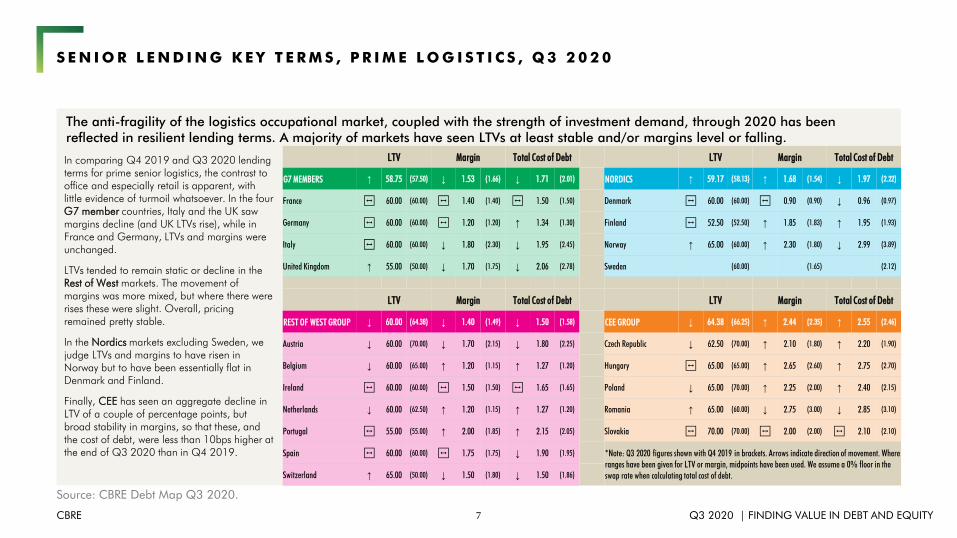

S E N I O R L E N D I N G K E Y T E R M S , P R I M E L O G I S T I C S , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

The anti-fragility of the logistics occupational market, coupled with the strength of investment demand, through 2020 has been reflected in resilient lending terms. A majority of markets have seen LTVs at least stable and/or margins level or falling.

In comparing Q4 2019 and Q3 2020 lending terms for prime senior logistics, the contrast to office and especially retail is apparent, with little evidence of turmoil whatsoever. In the four G7 member countries, Italy and the UK saw margins decline (and UK LTVs rise), while in France and Germany, LTVs and margins were unchanged.

LTVs tended to remain static or decline in the Rest of West markets. The movement of margins was more mixed, but where there were rises these were slight. Overall, pricing remained pretty stable.

In the Nordics markets excluding Sweden, we judge LTVs and margins to have risen in Norway but to have been essentially flat in Denmark and Finland.

Finally, CEE has seen an aggregate decline in LTV of a couple of percentage points, but broad stability in margins, so that these, and the cost of debt, were less than 10bps higher at the end of Q3 2020 than in Q4 2019.

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

G7 MEMBERS ↑ 58.75 (57.50) ↓ 1.53 (1.66) ↓ 1.71 (2.01) NORDICS ↑ 59.17 (58.13) ↑ 1.68 (1.54) ↓ 1.97 (2.22)

France ↔ 60.00 (60.00) ↔ 1.40 (1.40) ↔ 1.50 (1.50) Denmark ↔ 60.00 (60.00) ↔ 0.90 (0.90) ↓ 0.96 (0.97)

Germany ↔ 60.00 (60.00) ↔ 1.20 (1.20) ↑ 1.34 (1.30) Finland ↔ 52.50 (52.50) ↑ 1.85 (1.83) ↑ 1.95 (1.93)

Italy ↔ 60.00 (60.00) ↓ 1.80 (2.30) ↓ 1.95 (2.45) Norway ↑ 65.00 (60.00) ↑ 2.30 (1.80) ↓ 2.99 (3.89)

United Kingdom ↑ 55.00 (50.00) ↓ 1.70 (1.75) ↓ 2.06 (2.78) Sweden (60.00) (1.65) (2.12)

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

REST OF WEST GROUP ↓ 60.00 (64.38) ↓ 1.40 (1.49) ↓ 1.50 (1.58) CEE GROUP ↓ 64.38 (66.25) ↑ 2.44 (2.35) ↑ 2.55 (2.46)

Austria ↓ 60.00 (70.00) ↓ 1.70 (2.15) ↓ 1.80 (2.25) Czech Republic ↓ 62.50 (70.00) ↑ 2.10 (1.80) ↑ 2.20 (1.90)

Belgium ↓ 60.00 (65.00) ↑ 1.20 (1.15) ↑ 1.27 (1.20) Hungary ↔ 65.00 (65.00) ↑ 2.65 (2.60) ↑ 2.75 (2.70)

Ireland ↔ 60.00 (60.00) ↔ 1.50 (1.50) ↔ 1.65 (1.65) Poland ↓ 65.00 (70.00) ↑ 2.25 (2.00) ↑ 2.40 (2.15)

Netherlands ↓ 60.00 (62.50) ↑ 1.20 (1.15) ↑ 1.27 (1.20) Romania ↑ 65.00 (60.00) ↓ 2.75 (3.00) ↓ 2.85 (3.10)

Portugal ↔ 55.00 (55.00) ↑ 2.00 (1.85) ↑ 2.15 (2.05) Slovakia ↔ 70.00 (70.00) ↔ 2.00 (2.00) ↔ 2.10 (2.10)

Spain ↔ 60.00 (60.00) ↔ 1.75 (1.75) ↓ 1.90 (1.95) *Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.Switzerland ↑ 65.00 (50.00) ↓ 1.50 (1.80) ↓ 1.50 (1.86)

8CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

40 50 60 70 80

Mar

gin

LTV

Prime Logistics, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

40 50 60 70 80

Mar

gin

LTV

Prime Retail, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

40 50 60 70 80

Mar

gin

LTV

Prime Office, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average

C H A N G E I N S E N I O R L E N D I N G K E Y T E R M S , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

The shift in lending terms heat maps reveals changes in lender pricing and risk strategy from Q4 2019 to Q3 2020 – in offices and retail there has been notable de-risking in the form of reduction in LTVs, but this has not really been the case in logistics.

Heatmap moves left and contracts in size, indicating lenders’ retreat from higher

LTVs

Average terms see LTVs fall 4% and

margins rise 11bps Average terms see LTVs fall 5% and

margins rise 10bps

Redefinition of prime appears to show margins falling, but

this is not like-for-like

Heatmap clearly retreats left as lenders no longer countenance

high LTV retail exposure Average terms

essentially unchanged

Heatmap contracts a little perhaps reflecting tightening of pricing. If

anything, gradient of new shape is a shade more “risk-on” than

previously.

Each dot represents an individual market Each dot represents an individual market

9CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G M A R G I N , R A N K O F G 7 M E M B E R A N D R E S T O F W E S T M A R K E T S

Source: CBRE Debt Map Q3 2020.

Showing the movement in ranking of margins in G7 member and Rest of West markets reveals the flight to quality and the shift from retail and towards logistics that the lending market has taken over the nine months to Q3 2020.

The chart shows the rankings of senior lending margins, from lowest to highest, for the 11 G7 member and Rest of West markets, for office, retail and logistics. This is a simplistic approach but it helps to identify broad relative shifts.

At a high level, it can be seen that more retail markets have become relatively expensive, and more logistics markets relatively cheap. Offices have seen little change. But within and across the sectors the G7 member markets have become relatively cheap, while Rest of West have become relative expensive.

The average office market rank fell by 0.1. Within this, G7 member office market rankings rose by 0.8; Rest of West declined by -0.6.

In retail, the above trend was magnified; an overall fall of -0.7 masked average G7 member improvement of 2.5 and Rest of West decline of -2.6 ranking places. Six of the nine highest margin markets are now retail.

In logistics the average ranking improvement was almost identical, at 3.3 for G7 member and 3.6 for Rest of West.

Amsterdam Office Frankfurt Office

Brussels Office Zurich Office

Paris Office Frankfurt Retail

Frankfurt Office Brussels Office

Frankfurt Retail Paris Office

Brussels Retail Amsterdam Office

Belgium Logistics Belgium Logistics

Netherlands Logistics Germany Logistics

Germany Logistics Netherlands Logistics

Paris Retail Milan Office

Amsterdam Retail Paris Retail

Dublin Office France Logistics

Milan Office Brussels Retail

France Logistics Amsterdam Retail

Zurich Office Zurich Retail

Dublin Retail Ireland Logistics

Ireland Logistics Switzerland Logistics

London Office London Office

Madrid Office Vienna Office

Zurich Retail Dublin Office

Spain Logistics Austria Logistics

United Kingdom Logistics United Kingdom Logistics

Switzerland Logistics Spain Logistics

Lisbon Office Italy Logistics

Portugal Logistics Vienna Retail

Vienna Office Madrid Office

Lisbon Retail Dublin Retail

Madrid Retail London Retail

Vienna Retail Portugal Logistics

Austria Logistics Lisbon Office

Italy Logistics Milan Retail

London Retail Lisbon Retail

Milan Retail Madrid Retail

G7 Members office

Rest of West Group office

G7 Members retail

Rest of West Group retail

G7 Members logistics

Rest of West Group logistics

LENDER RISK

WHAT DO KEY METRICS OF LENDING RISK LOOK LIKE IN Q3 2020, AND HOW HAVE THEY SHIFTED OVER THE COURSE OF THE YEAR?

11CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

T H E E V O L U T I O N O F L E N D E R R I S K A P P E T I T E O V E R 2 0 2 0 , C H A N G E I N K E Y M E T R I C S

Debt yieldDebt yield premium

vs property yieldInterest

Cover RatioDebt Service Cover Ratio

Nominal lender exposure Overall

Note: Arrow indicates direction of risk appetite, not movement in metric. For example, a high debt yield is (all other things being equal) lower risk, and would be represented on the graphic above by the dial leaning to the left.

Risk appetite Much weaker Weaker No change A little stronger Much stronger

12CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

0

1

2

3

4

5

6

2 4 6 8 10 12 14

debt

yiel

d pr

emiu

m vs

pro

perty

yiel

d, p

erce

ntag

e po

ints

debt yield, %

Prime Logistics, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0

1

2

3

4

5

6

2 4 6 8 10 12 14

debt

yiel

d pr

emiu

m vs

pro

perty

yiel

d, p

erce

ntag

e po

ints

debt yield, %

Prime Retail, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0

1

2

3

4

5

6

2 4 6 8 10 12 14

debt

yiel

d pr

emiu

m vs

pro

perty

yiel

d, p

erce

ntag

e po

ints

debt yield, %

Prime Office, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average

S E N I O R L E N D I N G D E B T Y I E L D , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

In retail there has been a marked increase (and in office a slighter one) in the debt yield and debt yield premium versus property yield demanded by lenders – a clear sign of de-risking. Logistics has seen hardly any change in these measures.

Average metrics if anything move up the

risk curve

Heatmap shape barely changes indicating lenders’ comfortable maintaining risk appetite in logistics

Very significant rise in average metrics betrays significant reduction in risk appetite

Heatmap moves up and right: lenders demanding higher debt yields and greater cushion over property yields

Outlier lending terms seen in Q4 2019 are “off the map” in Q3 2020

Easing in average metrics shows some reduction in risk appetite

Heatmap edges upwards, showing a small increase in debt yield and cushion to underlying property pricing

Each dot represents an individual market Each dot represents an individual market

Average risk metrics on retail and logistics about to reach cross-over point

13CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

1 2 3 4 5 6 7

DSC

R

ICR

Prime Logistics, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

1 2 3 4 5 6 7

DSC

R

ICR

Prime Retail, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

1 2 3 4 5 6 7

DSC

R

ICR

Prime Office, primary market, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average

S E N I O R L E N D I N G I C R A N D D S C R , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Falling LTVs and rising property yields have combined to raise ICR and DSCR metrics considerably in retail (on the assumption that underlying property yields reflect passing income). Movement has been less aggressive in office and logistics.

Each dot represents an individual market Each dot represents an individual market

Reduction in LTVs has seen serviceability

improve (assuming income being received): ICR and DSCR have both

risen significantly.

Aside from one outlier, the range of serviceability observations has narrowed, with a slight increase in both average ICR and DSCR.

Lenders have been prepared to relax ICR and DSCR for logistics, likely a result of inward movement in property

yields outstripping any increased caution in lending terms.

14CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

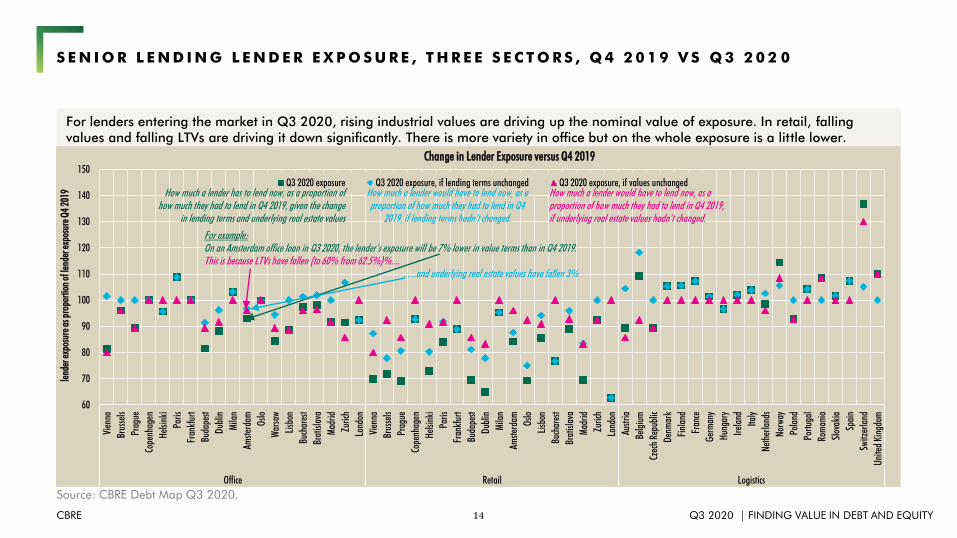

S E N I O R L E N D I N G L E N D E R E X P O S U R E , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

For lenders entering the market in Q3 2020, rising industrial values are driving up the nominal value of exposure. In retail, falling values and falling LTVs are driving it down significantly. There is more variety in office but on the whole exposure is a little lower.

60

70

80

90

100

110

120

130

140

150

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

War

saw

Lisb

on

Buch

ares

t

Brat

islav

a

Mad

rid

Zuric

h

Lond

on

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

Lisb

on

Buch

ares

t

Brat

islav

a

Mad

rid

Zuric

h

Lond

on

Austr

ia

Belg

ium

Czec

h Re

publ

ic

Denm

ark

Finl

and

Fran

ce

Germ

any

Hung

ary

Irela

nd

Italy

Neth

erla

nds

Norw

ay

Pola

nd

Portu

gal

Rom

ania

Slov

akia

Spai

n

Switz

erla

nd

Unite

d Ki

ngdo

m

Office Retail Logistics

lend

er e

xpos

ure

as p

ropo

rtion

of l

ende

r exp

osur

e Q

4 20

19

Change in Lender Exposure versus Q4 2019

Q3 2020 exposure Q3 2020 exposure, if lending terms unchanged Q3 2020 exposure, if values unchangedHow much a lender has to lend now, as a proportion of

how much they had to lend in Q4 2019, given the change in lending terms and underlying real estate values

How much a lender would have to lend now, as a proportion of how much they had to lend in Q4

2019, if lending terms hadn’t changed.

How much a lender would have to lend now, as a proportion of how much they had to lend in Q4 2019, if underlying real estate values hadn’t changed.

For example:On an Amsterdam office loan in Q3 2020, the lender’s exposure will be 7% lower in value terms than in Q4 2019.This is because LTVs have fallen (to 60% from 62.5%)%....

….and underlying real estate values have fallen 3%

(GEARED) INVESTOR RETURNS

FOR AN INVESTOR LOOKING AT THE DEC-20 TO DEC-25 PERIOD, HOW HAVE CHANGED FORECASTS AND DIFFERENCES IN DEBT TERMS CONTRIBUTED AFFECTED THE OUTLOOK FOR UNGEARED AND GEARED RETURNS?

16CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

T H E C H A N G E D O U T L O O K F O R P R I M E R E A L E S T A T E P E R F O R M A N C E , D E C - 2 0 T O D E C - 2 5

Forecasts for the Dec-20 to Dec-25 period have seen significant improvement.

Retail Now 5.1%Was 4.0%*

Office Now 5.8%Was 4.3%*

Logistics Now 7.9%Was 6.4%*

*Average of selected prime markets

Debt terms have got less borrower-friendly in retail and

office, but stayed about the same in logistics.

LTV & Margin

Margin

LTV

But overall, in spite of more challenging debt conditions,

forecasts of geared performance for Dec-20 to Dec-25 have

improved significantly

Retail Now 10.5%

Was 7.3%*

Office Now 12.3%

Was 8.8%*

Logistics Now 16.7%Was 13.4%*

17CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

T H E C H A N G E D O U T L O O K F O R P R I M E O F F I C E P E R F O R M A N C E , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

The chart on the left shows our forecasts of prime office total returns, for the five year period Dec-20 to Dec-25, made at two points, Q4 2019 and most recently Q3 2020. We have used Debt Map data as at these points to show geared returns for the period also. The chart on the right shows how geared returns forecasts have changed, and attributes the cause of any change to either changes in the forecast or changes in debt terms.

This analysis shows overwhelmingly that the Dec-20 to Dec-25 period appears to be a very favourable investment window for prime offices. Across the 19 markets covered:

• Ungeared total returns have improved from an average of 4.3%pa to 5.8%pa.

• Geared total returns have improved from an average of 8.8%pa to 12.3%pa.

• More adverse debt terms have reduced geared total return expectations in most markets, and by -0.7%pa on average.

• This has been more than offset by rising forecasts; 17 out of 19 markets have seen forecasts improve, by 3.5%pa on average.

On average, we expect geared total returns on prime office to be 3.5% per year better than was the case when making forecasts at the end of 2019, despite generally more expensive and lower leverage debt reducing performance expectations by -0.7% per year.

-5

0

5

10

15

20

25

30

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

War

saw

Lisb

on

Buch

ares

t

Brat

islav

a

Mad

rid

Zuric

h

Lond

on

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Total return forecasts, Q4 2019 and Q3 2020, prime offices, five year period Dec-20 to Dec-25,

Q4 2019, Ungeared Q3 2020, Ungeared Q4 2019, Geared Q3 2020, Geared

-15

-10

-5

0

5

10

15

20

25

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

War

saw

Lisb

on

Buch

ares

t

Brat

islav

a

Mad

rid

Zuric

h

Lond

on

Chan

ge in

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Drivers of change in geared prime office forecast

Debt market driven change Forecast driven change Total change

In almost every case, gearing is accretive to performance (hence the triangles are above the bars).

In most instances, the outlook for the Dec-20 to Dec-25 period has improved, so most blue bars are positive.

Most markets have seen debt become more expensive, and/or lower LTV, which has had a small negative impact on forecast

geared performance – hence most pink bars are negative.

Generally, improvement in forecasts has outweighed the negative impact of costlier / lower debt, so most markets

have seen net increase in forecasts – most diamonds

are in positive territory

18CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

T H E C H A N G E D O U T L O O K F O R P R I M E R E T A I L P E R F O R M A N C E , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

On average, we expect geared total returns on prime retail to be 3.2% per year better than was the case when making forecasts at the end of 2019, despite generally more expensive and lower leverage debt reducing performance expectations by -0.8% per year.

-5

0

5

10

15

20

25

30

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

Lisb

on

Buch

ares

t

Mad

rid

Zuric

h

Lond

on

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Total return forecasts, Q4 2019 and Q3 2020, prime retail, five year period Dec-20 to Dec-25,

Q4 2019, Ungeared Q3 2020, Ungeared Q4 2019, Geared Q3 2020, Geared

-15

-10

-5

0

5

10

15

20

25

Vien

na

Brus

sels

Prag

ue

Cope

nhag

en

Helsi

nki

Paris

Fran

kfur

t

Buda

pest

Dubl

in

Mila

n

Amste

rdam Os

lo

Lisb

on

Buch

ares

t

Mad

rid

Zuric

h

Lond

on

Chan

ge in

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Drivers of change in geared prime retail forecast

Debt market driven change Forecast driven change Total change

In most cases, gearing is accretive to performance (hence the triangles are above the bars).

In most instances, the outlook for the Dec-20 to Dec-25 period has improved, so most blue bars are positive.

Most markets have seen debt become more expensive, and/or lower LTV, which has reduced forecast geared performance – hence most pink bars are negative.

Generally, improvement in forecasts has outweighed the

negative impact of costlier / lower debt, so most markets have seen net increase in forecasts – most

diamonds are in positive territory

The chart on the left shows our forecasts of prime retail total returns, for the five year period Dec-20 to Dec-25, made at two points, Q4 2019 and most recently Q3 2020. We have used Debt Map data as at these points to show geared returns for the period also. The chart on the right shows how geared returns forecasts have changed, and attributes the cause of any change to either changes in the forecast or changes in debt terms.

This analysis shows that the Dec-20 to Dec-25 period appears to be a favourable investment window for prime retail. Across the 17 markets covered:

• Ungeared total returns have improved from an average of 4.0%pa to 5.1%pa.

• Geared total returns have improved from an average of 7.3%pa to 10.5%pa.

• More adverse debt terms have reduced geared total return expectations in most markets, and by -0.8%pa on average.

• This has been more than offset by rising forecasts; 12 out of 17 markets have seen forecasts improve, by 3.2%pa on average.

19CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

T H E C H A N G E D O U T L O O K F O R P R I M E L O G I S T I C S P E R F O R M A N C E , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

-5

0

5

10

15

20

25

30

Austr

ia

Belg

ium

Czec

h Re

publ

ic

Denm

ark

Finl

and

Fran

ce

Germ

any

Hung

ary

Irela

nd

Italy

Neth

erla

nds

Norw

ay

Pola

nd

Portu

gal

Rom

ania

Slov

akia

Spai

n

Switz

erla

nd

Unite

d Ki

ngdo

m

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Total return forecasts, Q4 2019 and Q3 2020, prime logistics, five year period Dec-20 to Dec-25,

Q4 2019, Ungeared Q3 2020, Ungeared Q4 2019, Geared Q3 2020, Geared

-15

-10

-5

0

5

10

15

20

25

Austr

ia

Belg

ium

Czec

h Re

publ

ic

Denm

ark

Finl

and

Fran

ce

Germ

any

Hung

ary

Irela

nd

Italy

Neth

erla

nds

Norw

ay

Pola

nd

Portu

gal

Rom

ania

Slov

akia

Spai

n

Switz

erla

nd

Unite

d Ki

ngdo

m

Chan

ge in

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Drivers of change in geared prime logistics forecast

Debt market driven change Forecast driven change Total change

In all cases, gearing is accretive to performance (hence the triangles are above the bars).

In most instances, the outlook for the Dec-20 to Dec-25 period has improved, so most blue bars are positive.

With debt terms pretty stable, the impact on outlook has generally been minimal.

Generally, improvement in forecasts has outweighed the negative impact of costlier / lower debt, so most markets

have seen net increase in forecasts – more diamonds

are in positive territory

The chart on the left shows our forecasts of prime logistics total returns, for the five year period Dec-20 to Dec-25, made at two points, Q4 2019 and most recently Q3 2020. We have used Debt Map data as at these points to show geared returns for the period also. The chart on the right shows how geared returns forecasts have changed, and attributes the cause of any change to either changes in the forecast or changes in debt terms.

This analysis shows overwhelmingly that the Dec-20 to Dec-25 period appears to be a very favourable investment window for prime logistics. Across the 19 markets covered:

• Ungeared total returns have improved from an average of 6.4%pa to 7.9%pa.

• Geared total returns have improved from an average of 13.4%pa to 16.7%pa.

• The impact from changed debt terms at the average level has been zero, but some markets have seen an impact.

• 15 out of 19 markets have seen forecasts improve, by 3.3%pa on average.

On average, we expect geared total returns on prime logistics to be 3.3% per year better than was the case when making forecasts at the end of 2019. There has been no adverse impact from changing debt terms, as change has been minimal (at the aggregate level).

A BORROWER OR A LENDER BE? OR BOTH? OR NEITHER…?

HOW MIGHT AN AGNOSTIC INVESTOR ASSESS THE RETURNS FROM DEBT AND EQUITY (UNGEARED AND GEARED) FOR THE DEC-20 TO DEC-25 PERIOD?

21CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

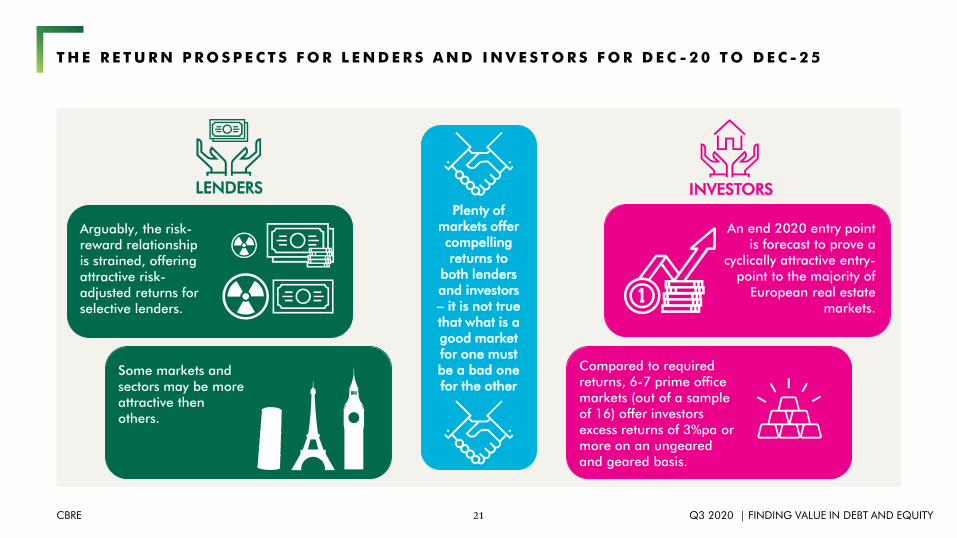

T H E R E T U R N P R O S P E C T S F O R L E N D E R S A N D I N V E S T O R S F O R D E C - 2 0 T O D E C - 2 5

LENDERS INVESTORS

Arguably, the risk-reward relationship is strained, offering attractive risk-adjusted returns for selective lenders.

Some markets and sectors may be more attractive then others.

Plenty of markets offer compelling returns to

both lenders and investors – it is not true that what is a good market for one must be a bad one for the other

Specific markets

An end 2020 entry point is forecast to prove a

cyclically attractive entry-point to the majority of

European real estate markets.

Compared to required returns, 6-7 prime office markets (out of a sample of 16) offer investors excess returns of 3%pa or more on an ungeared and geared basis.

22CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G , A B S O L U T E A N D P R O P O R T I O N A L R E T U R N S , T H R E E S E C T O R S , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

There is not a uniform relationship between the returns from real estate lending (simplified as margin+fee) and exposure (LTV) or the proportion of return earned by real estate above the risk free. This offers opportunities for lenders able to select sectors and markets.

Vienna

BrusselsPrague

Copenhagen

HelsinkiParisFrankfurt

Budapest

Dublin

Milan

Amsterdam

Oslo

Warsaw

Lisbon

Bucharest

Bratislava

Madrid

Zurich

London

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.8 1.2 1.6 2.0 2.4 2.8 3.2

mar

gin+

fee

as p

ropo

rtion

of p

rope

rty yi

eld

min

us G

over

nmen

t bon

d, %

senior lending margin+fee, %

Prime Office, lending returns, absolute and as proportion of property premium over risk free

Vienna

BrusselsPrague

Copenhagen

Helsinki

Paris

Frankfurt

Budapest

Dublin

Milan

AmsterdamOslo

Lisbon

Bucharest

Bratislava

Madrid

Zurich

London

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.8 1.2 1.6 2.0 2.4 2.8 3.2

Mar

gin+

fee

as p

ropo

rtion

of p

rope

rty yi

eld

min

us G

over

nmen

t bon

d, %

senior lending margin+fee, %

Prime Retail, lending returns, absolute and as proportion of property premium over risk free

Austria

Belgium Czech Republic

Denmark

FinlandFrance

Germany

Hungary

Ireland

Italy

Netherlands

Norway

PolandPortugal

Romania

Slovakia

Spain

SwitzerlandUnited Kingdom

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.8 1.2 1.6 2.0 2.4 2.8 3.2

Mar

gin+

fee

as p

ropo

rtion

of p

rope

rty yi

eld

min

us G

over

nmen

t bon

d, %

senior lending margin+fee, %

Prime Logistics, lending returns, absolute and as proportion of property premium over risk free

Some markets offer relatively high absolute and proportional returns at relatively low LTV

In others, LTVs are higher but returns a somewhat lower

A number of markets offer similar proportional returns but are

differentiated on margin & fee (and LTV)

Some markets offer relatively high absolute and proportional returns at relatively low LTV

In others, LTVs are higher but returns a somewhat lower

50% LTV 60% LTV 70% LTV50% LTV 60% LTV 70% LTV50% LTV 60% LTV 70% LTV

23CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G , S T A N D A R D S C O R E O F A B S O L U T E A N D P R O P O R T I O N A L R E T U R N S , Q 3 2 0 2 0 , W I T H I N T H R E E S E C T O R S

Source: CBRE Debt Map Q3 2020.

Expressing the return real estate debt receives in absolute terms, in relative terms (compared to that which equity receives) and accounting for the level of exposure in a single metric is not easy. This chart attempts to do so by expressing absolute and proportional return relative to LTV on a standard score basis. The scores themselves are not specially meaningful, but their relativities are.

Initially, we look at scores within each sector –evaluating real estate debt return within but not across office, retail and logistics.

In prime office, London is the only G7 member market with a positive score overall. Smaller markets with strong scores include Dublin, Oslo, Warsaw, Lisbon and Madrid.

For prime retail, the best scores are achieved by Helsinki, Milan, London, Lisbon and Dublin. Paris and Frankfurt area again weak.

In logistics, Finland, Norway, Portugal and the UK score well; Austria, Denmark and Netherlands score poorly.

On a standard score basis, some markets stand out as offering above or below par returns. London and Madrid consistently appear attractive to lenders. The reverse is true for Paris, Frankfurt and Amsterdam.

-4

-3

-2

-1

0

1

2

3

4

Vien

naBr

usse

lsPr

ague

Cope

nhag

enHe

lsink

iPa

risFr

ankf

urt

Buda

pest

Dubl

inM

ilan

Amste

rdam Os

loW

arsa

wLi

sbon

Buch

ares

tBr

atisl

ava

Mad

ridZu

rich

Lond

onVi

enna

Brus

sels

Prag

ueCo

penh

agen

Helsi

nki

Paris

Fran

kfur

tBu

dape

stDu

blin

Mila

nAm

sterd

am Oslo

Lisb

onBu

char

est

Brat

islav

aM

adrid

Zuric

hLo

ndon

Austr

iaBe

lgiu

mCz

ech

Repu

blic

Denm

ark

Finl

and

Fran

ceGe

rman

yHu

ngar

yIre

land

Italy

Neth

erla

nds

Norw

ayPo

land

Portu

gal

Rom

ania

Slov

akia

Spai

nSw

itzer

land

Unite

d Ki

ngdo

m

Office Retail Logistics

stan

dard

scor

e

Standard score of absolute and proportional senior lending return, calculated within sectors

Margin & Fee / LTV Share of Premium over 5yr Gov Bond / LTV Sum

Methodology: (Margin + Fee)/LTV and ((Margin+Fee)/(Property Yield–Risk Free))/LTV calculated for each market. Standard score of each metric then calculated within each sector.

24CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

S E N I O R L E N D I N G , S T A N D A R D S C O R E O F A B S O L U T E A N D P R O P O R T I O N A L R E T U R N S , Q 3 2 0 2 0 , A C R O S S T H R E E S E C T O R S

Source: CBRE Debt Map Q3 2020.

High returns and low LTVs make retail lending returns appear attractive relative to other sectors – but capital decline risk is of course not equal across sectors.

-4

-3

-2

-1

0

1

2

3

4

Vien

naBr

usse

lsPr

ague

Cope

nhag

enHe

lsink

iPa

risFr

ankf

urt

Buda

pest

Dubl

inM

ilan

Amste

rdam Os

loW

arsa

wLi

sbon

Buch

ares

tBr

atisl

ava

Mad

ridZu

rich

Lond

onVi

enna

Brus

sels

Prag

ueCo

penh

agen

Helsi

nki

Paris

Fran

kfur

tBu

dape

stDu

blin

Mila

nAm

sterd

am Oslo

Lisb

onBu

char

est

Brat

islav

aM

adrid

Zuric

hLo

ndon

Austr

iaBe

lgiu

mCz

ech

Repu

blic

Denm

ark

Finl

and

Fran

ceGe

rman

yHu

ngar

yIre

land

Italy

Neth

erla

nds

Norw

ayPo

land

Portu

gal

Rom

ania

Slov

akia

Spai

nSw

itzer

land

Unite

d Ki

ngdo

m

Office Retail Logistics

stan

dard

scor

e

Standard score of absolute and proportional senior lending return, calculated across all sectors

Margin & Fee / LTV Share of Premium over 5yr Gov Bond / LTV Sum

Methodology: (Margin + Fee)/LTV and ((Margin+Fee)/(Property Yield–Risk Free))/LTV calculated for each market. Standard score of each metric then calculated across all 56 markets.

Expressing the return real estate debt receives in absolute terms, in relative terms (compared to that which equity receives) and accounting for the level of exposure in a single metric is not easy. This chart attempts to do so by expressing absolute and proportional return relative to LTV on a standard score basis. The scores themselves are not specially meaningful, but their relativities are.

Here, we look at scores across each sector –evaluating real estate debt return across office, retail and logistics. With higher margins and lower LTVs, more retail markets (11) have positive scores than any other sector – however for some this may be a false position, given the widespread perception of greater potential for adverse value movement. (The methodology’s implicit assumption that value decline risk is equal is a limitation in this respect).

Eight office and four logistics markets have positive scores. Finland, Norway, Portugal and UK are represented in both sectors, Vienna, Dublin, Warsaw and Madrid additionally so in the office sector.

25CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

P R I M E O F F I C E S , R E Q U I R E D A N D E X P E C T E D R E T U R N , U N G E A R E D , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

For 16 prime office markets for which we have a view on risk premium we show a comparison of required return (risk premium plus the risk free rate) with expected return (our total return forecast) on an ungeared basis. This shows the extent to which market level returns should meet typical investment targets – of course, individual assets within these markets may perform significantly differently to the average.

The analysis shows that expected returns exceed required returns in 13 out of 16 markets, matching them in one (Milan) and under-delivering in two (Budapest and Bucharest). Furthermore, in six cases – Vienna, Brussels, Copenhagen, Frankfurt, Oslo and London – excess return is greater than 3%pa, offering significant comfort.

For so many markets to be delivering excess return shows the cyclically favourable entry-point prevailing across European office markets.

Most prime office markets will deliver ungeared returns above – and in the case of Vienna, Brussels, Copenhagen, Frankfurt, Oslo and London more than 3% per year above – required returns.

-10

-5

0

5

10

15

20

25

30

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Vienna Brussels Prague Copenhagen Helsinki Paris Frankfurt Budapest Dublin Milan Amsterdam Oslo Warsaw Bucharest Madrid London

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Required and Expected Return, ungeared, prime offices, Dec-20 to Dec-25

Risk free rate Ungeared risk premium Expected ungeared return Required ungeared return Excess ungeared return

Only two markets have expected returns below required returns.

In six markets, expected returns exceed required returns by at least 3%pa – a considerable margin.

26CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

P R I M E O F F I C E S , R E Q U I R E D A N D E X P E C T E D R E T U R N , G E A R E D , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

-10

-5

0

5

10

15

20

25

30

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Requ

ired

Retu

rn

Expe

cted

Retu

rn

Vienna Brussels Prague Copenhagen Helsinki Paris Frankfurt Budapest Dublin Milan Amsterdam Oslo Warsaw Bucharest Madrid London

tota

l ret

urn,

Dec

-20

to D

ec-2

5, %

pa

Required and Expected Return, geared, prime offices, Dec-20 to Dec-25

Risk free rate Geared risk premium Expected geared return Required geared return Excess geared return

For 16 prime office markets for which we have a view on risk premium we show a comparison of required return (risk premium plus the risk free rate) with expected return (our total return forecast) on a geared basis. To account for gearing, we adjust the ungeared risk premium according to the level of additional volatility in capital growth at the LTV prevailing in each market has produced. This shows the extent to which market level returns should meet typical investment targets – of course, individual assets within these markets may perform significantly differently to the average.

The analysis shows that expected returns exceed required returns in 11 out of 16 markets. Brussels, Copenhagen, Frankfurt and Oslo deliver excess geared return of 9-11%pa, London of 5.5%pa and Vienna and Amsterdam of around 4%pa.

This emphasises the extent to which gearing, on historically very affordable terms, can be used to enhance performance in markets where values are expected to increase.

Five markets have expected geared returns below required geared returns.

Four markets have expected geared returns around 10%pa above required geared returns.

Most prime office markets will deliver geared returns above – and in the case of Brussels, Copenhagen, Frankfurt and Oslo more than 10% per year above – required returns.

27CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

P R I M E O F F I C E S , R E Q U I R E D A N D E X P E C T E D R E T U R N , D E C - 2 0 T O D E C - 2 5

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q4 2019 and Q3 2020.

To summarise, we plot excess return on an ungeared against a geared basis, with the size of the bubble reflecting transaction volume in the 2017-19 period as a measure of liquidity –after all, performance is once thing but that performance must be accessible. We also rank the markets covered on each basis – this latter shows that there is limited difference in the positioning of the markets.

This layout suggests that investors looking to access large, liquid markets set to deliver high levels of positive excess return may target Frankfurt and London, followed by Paris. Amsterdam – by no means a small market –will also appeal.

Oslo, Brussels, Copenhagen may prove more difficult to access but the high level of excess return should justify persistence. Thereafter, Vienna, Warsaw, Helsinki and Prague deserve attention.

The relative attractiveness of markets is similar on a geared and ungeared basis. Of the largest markets, Frankfurt and London offer most appeal; of the next tier Oslo, Brussels, Vienna and Amsterdam are also compelling.

Vienna

Brussels

Prague

Copenhagen

Helsinki

Paris

Frankfurt

Budapest

Dublin

Milan

Amsterdam

Oslo

Warsaw

Bucharest

Madrid

London

-8

-6

-4

-2

0

2

4

6

8

10

12

-4 -2 0 2 4 6 8

exce

ss e

xpec

ted

retu

rn ve

rsus

requ

ired

retu

rn, g

eare

d, %

pa

excess expected return versus required return, ungeared, %pa

Excess Expected Return, ungeared and geared, prime office, Dec-20 to Dec-25

Rank of excess return, ungeared Rank of excess return, geared

1 Frankfurt Oslo

2 Brussels Brussels

3 Oslo Copenhagen

4 Copenhagen Frankfurt

5 London London

6 Vienna Vienna

7 Amsterdam Amsterdam

8 Helsinki Warsaw

9 Warsaw Prague

10 Prague Helsinki

11 Paris Paris

12 Dublin Dublin

13 Madrid Madrid

14 Milan Budapest

15 Budapest Milan

16 Bucharest Bucharest

G7 Members

Rest of West Group

Nordics

CEE Group

Market does not deliver positive excess return

Market turnover averaged €30bn 2017-19

Market turnover averaged €5bn 2017-19

MEZZANINE, WHOLE LOAN AND DEVELOPMENT FINANCE

WHERE ARE LENDING TERMS FURTHER UP THE RISK CURVE NOW, AND WHICH MARKETS APPEAR ATTRACTIVE?

29CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

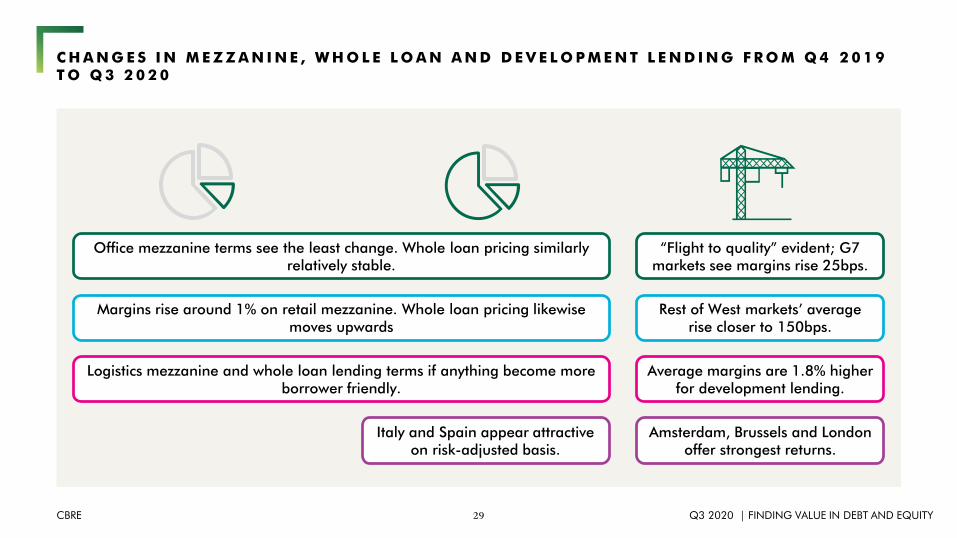

C H A N G E S I N M E Z Z A N I N E , W H O L E L O A N A N D D E V E L O P M E N T L E N D I N G F R O M Q 4 2 0 1 9 T O Q 3 2 0 2 0

Office mezzanine terms see the least change. Whole loan pricing similarly relatively stable.

Margins rise around 1% on retail mezzanine. Whole loan pricing likewise moves upwards

Logistics mezzanine and whole loan lending terms if anything become more borrower friendly.

Italy and Spain appear attractive on risk-adjusted basis.

“Flight to quality” evident; G7 markets see margins rise 25bps.

Rest of West markets’ average rise closer to 150bps.

Average margins are 1.8% higher for development lending.

Amsterdam, Brussels and London offer strongest returns.

30CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

M E Z Z A N I N E L E N D I N G K E Y T E R M S , T H R E E S E C T O R S , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Reflecting the pattern seen in senior lending, mezzanine lending terms have become significantly more expensive in the retail sector, slightly more onerous in the office market, but more borrower friendly in the logistics sector.

OFFICE RETAIL LOGISTICS

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

SAMPLE AVERAGE

↓ 75.56 (76.25) ↑ 7.22 (7.13) ↑ 7.52 (7.40)SAMPLE AVERAGE

↔ 75.00 (75.00) ↑ 8.94 (7.88) ↑ 9.24 (8.20)SAMPLE AVERAGE

↓ 76.67 (76.88) ↓ 7.44 (7.75) ↓ 7.77 (8.05)

Frankfurt ↔ 75.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25) Frankfurt ↔ 75.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25) Germany ↔ 75.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25)

Milan ↔ 70.00 (70.00) ↔ 7.50 (7.50) ↔ 7.80 (7.80) Milan ↔ 65.00 (65.00) ↔ 8.50 (8.50) ↔ 8.80 (8.80) Italy ↔ 70.00 (70.00) ↔ 8.00 (8.00) ↔ 8.30 (8.30)

London ↔ 70.00 (70.00) ↓ 5.00 (6.00) ↓ 5.30 (6.20) UK ↓ 70.00 (75.00) ↓ 5.00 (9.00) ↓ 5.30 (9.20)

Brussels ↓ 75.00 (80.00) ↑ 8.00 (7.50) ↑ 8.30 (7.80) Brussels ↓ 75.00 (80.00) ↑ 12.00 (8.50) ↑ 12.30 (8.80) Belgium ↓ 75.00 (80.00) ↔ 8.00 (8.00) ↔ 8.30 (8.30)

Dublin ↔ 75.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25) Dublin ↔ 75.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25) Ireland ↑ 80.00 (75.00) ↔ 7.00 (7.00) ↑ 7.30 (7.25)

Amsterdam ↓ 75.00 (80.00) ↑ 8.00 (7.00) ↑ 8.30 (7.30) Amsterdam ↓ 75.00 (80.00) ↑ 12.00 (9.00) ↑ 12.30 (9.50) Netherlands ↓ 75.00 (80.00) ↑ 8.00 (7.00) ↑ 8.30 (7.30)

Madrid 80.00 7.50 7.80 Madrid 75.00 10.00 10.30 Spain 85.00 8.00 8.30

Copenhagen ↔ 80.00 (80.00) ↔ 9.00 (9.00) ↔ 9.30 (9.30) Copenhagen ↔ 80.00 (80.00) ↔ 9.00 (9.00) ↔ 9.30 (9.30) Denmark ↔ 80.00 (80.00) ↔ 10.00 (10.00) ↔ 10.50 (10.50)

Oslo ↔ 80.00 (80.00) ↔ 6.00 (6.00) ↔ 6.30 (6.30) Oslo ↔ 80.00 (80.00) ↔ 6.00 (6.00) ↔ 6.30 (6.30) Norway ↔ 80.00 (80.00) ↔ 6.00 (6.00) ↔ 6.30 (6.30)

*Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.*Note: The absence of markets from the above does not necessarily indicate that debt is not available in those markets, just that we have chosen not to provide figures for those markets.

31CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

W H O L E L O A N L E N D I N G K E Y T E R M S , T H R E E S E C T O R S , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Combining senior and mezzanine lending terms gives whole loan lending terms. On average, the cost of office debt has risen slightly (7bps), while that of retail has risen by around the same than that of logistics has fallen (roughly 30bps).

OFFICE RETAIL LOGISTICS

LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt LTV Margin Total Cost of Debt

SAMPLE AVERAGE

↓ 75.56 (76.25) ↑ 2.72 (2.39) ↑ 2.96 (2.89)SAMPLE AVERAGE

↔ 75.00 (75.00) ↑ 3.47 (2.90) ↑ 3.71 (3.42)SAMPLE AVERAGE

↓ 76.67 (76.88) ↓ 2.78 (2.79) ↓ 3.03 (3.30)

Frankfurt ↔ 75.00 (75.00) ↔ 2.20 (2.20) ↑ 2.37 (2.33) Frankfurt ↔ 75.00 (75.00) ↔ 2.20 (2.20) ↑ 2.37 (2.33) Germany ↔ 75.00 (75.00) ↔ 2.36 (2.36) ↑ 2.53 (2.49)

Milan ↔ 70.00 (70.00) ↓ 2.19 (2.27) ↓ 2.31 (2.40) Milan ↔ 65.00 (65.00) ↓ 3.69 (4.12) ↓ 3.92 (4.34) Italy ↔ 70.00 (70.00) ↓ 2.69 (3.11) ↓ 2.86 (3.29)

London ↔ 70.00 (70.00) ↓ 2.33 (2.43) ↓ 2.71 (3.47) LondonUnited Kingdom

↓ 70.00 (75.00) ↓ 2.36 (3.87) ↓ 2.75 (4.92)

Brussels ↓ 75.00 (80.00) ↑ 2.56 (2.38) ↑ 2.68 (2.50) Brussels ↓ 75.00 (80.00) ↑ 3.60 (2.49) ↑ 3.74 (2.60) Belgium ↓ 75.00 (80.00) ↑ 2.56 (2.43) ↑ 2.68 (2.53)

Dublin ↔ 75.00 (75.00) ↑ 3.11 (2.52) ↑ 3.31 (2.69) Dublin ↔ 75.00 (75.00) ↑ 3.67 (2.60) ↑ 3.90 (2.77) Ireland ↑ 80.00 (75.00) ↑ 2.88 (2.60) ↑ 3.06 (2.77)

Amsterdam ↓ 75.00 (80.00) ↑ 2.56 (2.20) ↑ 2.68 (2.30) Amsterdam ↓ 75.00 (80.00) ↑ 3.60 (2.95) ↑ 3.74 (3.11) Netherlands ↓ 75.00 (80.00) ↑ 2.56 (2.43) ↑ 2.68 (2.53)

Madrid 80.00 3.72 3.92 Madrid 75.00 4.83 5.03 Spain 85.00 3.59 3.78

Copenhagen ↔ 80.00 (80.00) ↑ 2.93 (2.92) ↓ 3.05 (3.05) Copenhagen ↔ 80.00 (80.00) ↑ 2.93 (2.92) ↓ 3.05 (3.05) Denmark ↔ 80.00 (80.00) ↑ 3.18 (3.17) ↓ 3.35 (3.35)

Oslo ↔ 80.00 (80.00) ↑ 2.88 (2.21) ↓ 3.61 (4.34) Oslo ↔ 80.00 (80.00) ↑ 3.22 (2.37) ↓ 3.96 (4.50) Norway ↔ 80.00 (80.00) ↑ 2.88 (2.35) ↓ 3.61 (4.49)

*Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.*Note: The absence of markets from the above does not necessarily indicate that debt is not available in those markets, just that we have chosen not to provide figures for those markets.

32CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

60 65 70 75 80 85

Mar

gin

LTV

Prime, primary market, whole loan lending

Office, Q4 2019 Office, Q3 2020Retail, Q4 2019 Retail, Q3 2020Logistics, Q4 2019 Logistics, Q3 2020

C H A N G E I N W H O L E L O A N L E N D I N G K E Y T E R M S A N D R I S K M E T R I C S , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Pricing on the highest leverage debt (80% LTV) has generally increased, although logistics has seen margin contraction for debt at lower leverage points. On the risk side, lenders are demonstrably wariest of retail.

Each dot represents an individual market

By plotting (in the left hand chart) LTV and margin and (in the right hand chart) debt yield and ICR for Q4 2019 and Q3 2020, the change in risk and reward across the sectors can be understood.

Generally speaking, it can be seen that higher leverage (80% LTV) debt has got more expensive across the board, where it remains available. For slightly lower leverage debt (75% LTV) offices have also seen an increase in margin, although the reverse has been true for logistics.

On the risk side, the biggest change is discernible in retail, where the drift of the shape to the right betrays a significant de-risking – the average debt yield has risen more than half a percent to 4.9%. By contrast, office has seen hardly any change, while the homogenisation of outlying risk metrics across logistics has seen little change on average.

High leverage debt getting more

expensive

Dotted lines = Q4 2019 Solid lines = Q3 2020

Logistics shape moves down in middle – 75% LTV whole loans

cheaper – but reverse true for offices0.5

1.0

1.5

2.0

2.5

3.0

3 4 5 6 7 8

ICR

Debt yield

Prime, primary market, whole loan lending

Office, Q4 2019 Office, Q3 2020Retail, Q4 2019 Retail, Q3 2020Logistics, Q4 2019 Logistics, Q3 2020

Dotted lines = Q4 2019 Solid lines = Q3 2020

33CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

Milan

Madrid

Milan

Madrid

Italy

Spain

70

80

90

100

110

120

130

2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5

mar

gin+

fee

as p

ropo

rtion

of p

rope

rty yi

eld

min

us G

over

nmen

t bon

d, %

senior lending margin+fee, %

Whole loan returns, absolute and as proportion of property premium over risk free

Office Retail Logistics

C H A N G E I N W H O L E L O A N L E N D I N G K E Y T E R M S A N D R I S K M E T R I C S , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

Italy and Spain may offer relatively attractive risk/reward combination for whole loan lenders. But other markets will also appeal to lenders if they are deemed more defensive against potential value decline.

Expressing the return real estate debt receives in absolute terms, in relative terms (compared to that which equity receives) and accounting for the level of exposure in a single metric is not easy. The chart on the left shows these metrics, while the chart on the right expresses absolute and proportional return relative to LTV on a standard score basis across the here sectors. The scores themselves are not specially meaningful, but their relativities are – a high (positive) score should mean a relatively attractive risk/return, a low (negative) one a poor risk/return.

Thanks to high returns relative to the risk free rate, Milan / Italy is an attractive outlier, while the same is also true of Madrid/Spain, though this is more driven by higher nominal returns.

Frankfurt / Germany appears, although the drawback of this analysis is the implicit assumption that LTV covers all downside risk, whereas, if the risk of value decline is not equal across all markets, this does not capture everything. Therefore, defensiveness may explain some apparently poorer prospects.

70% LTV 75% LTV 80% LTV

-3

-2

-1

0

1

2

3

4

Brus

sels

Cope

nhag

enFr

ankf

urt

Dubl

inM

ilan

Amste

rdam Os

loM

adrid

Lond

onBr

usse

lsCo

penh

agen

Fran

kfur

tDu

blin

Mila

nAm

sterd

am Oslo

Mad

ridBe

lgiu

mDe

nmar

kGe

rman

yIre

land

Italy

Neth

erla

nds

Norw

aySp

ain

Unite

d Ki

ngdo

m

Office Retail Logistics

stan

dard

scor

e

Standard score of absolute and proportional whole loan return, calculated across all sectors

Margin & Fee / LTV Share of Premium over 5yr Gov Bond / LTV Sum

34CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

D E V E L O P M E N T L E N D I N G K E Y T E R M S , P R I M E O F F I C E , Q 3 2 0 2 0

Source: CBRE Debt Map Q3 2020.

As with lending to mature investments, when comparing Q4 2019 and Q3 2020 lending terms for prime senior office development, the largest markets have seen comparatively more stability. LTCs and margins are unchanged two of the G7 member markets (Frankfurt and Milan), while Paris and London have seen margins rise 50bps – albeit that LTCs have moved in different directions, with London also benefiting from a fall in the five year swap rate.

In contrast, other markets for which we have comparison figures available have generally seen margins and total cost of debt rise quite significantly (on average by 1.5% or so) and LTCs fall (on average by 7.5pp).

This is consistent of course with a lender community wishing to understand the more medium term impact on office demand of Covid-19, and the structural shifts it has potentially accelerated, before committing to speculative projects.

LTC Margin Total Cost of Debt LTC Margin Total Cost of Debt

G7 MEMBERS ↔ 62.50 (62.50) ↑ 3.41 (3.16) ↑ 3.67 (3.58) NORDICS ↓ 60.00 (62.50) ↑ 2.75 (2.25) ↑ 2.85 (2.35)

Paris ↓ 60.00 (70.00) ↑ 2.50 (2.00) ↑ 2.70 (2.20) Copenhagen

Frankfurt ↔ 70.00 (70.00) ↔ 2.25 (2.25) ↑ 2.39 (2.35) Helsinki ↓ 60.00 (65.00) ↑ 2.75 (2.25) ↑ 2.85 (2.35)

Milan ↔ 60.00 (60.00) ↔ 3.90 (3.90) ↔ 4.10 (4.10) Oslo

London ↑ 60.00 (50.00) ↑ 5.00 (4.50) ↓ 5.50 (5.68) Stockholm

LTC Margin Total Cost of Debt LTC Margin Total Cost of Debt

REST OF WEST GROUP ↓ 62.50 (70.00) ↑ 4.75 (3.33) ↑ 4.99 (3.52) CEE GROUP 64.17 2.95 3.05

Vienna 65.00 2.50 2.60 Prague 67.50 2.35 2.45

Brussels ↓ 60.00 (75.00) ↑ 6.00 (2.25) ↑ 6.30 (2.40) Budapest 62.50 2.80 2.90

Dublin ↑ 65.00 (60.00) ↓ 4.50 (5.50) ↓ 4.75 (5.75) Warsaw

Amsterdam ↓ 60.00 (75.00) ↑ 6.00 (2.25) ↑ 6.30 (2.40) Bucharest 62.50 3.70 3.80

Lisbon ↔ 70.00 (70.00) ↔ 3.50 (3.50) ↔ 3.70 (3.70) Bratislava 67.50 2.50 2.60

Madrid 50.00 3.25 3.55 *Note: Q3 2020 figures shown with Q4 2019 in brackets. Arrows indicate direction of movement. Where ranges have been given for LTV or margin, midpoints have been used. We assume a 0% floor in the swap rate when calculating total cost of debt.Zurich ↓ 60.00 (70.00) ↓ 2.25 (2.50) ↓ 2.25 (2.57)

The “flight to quality” evident in the lending market for prime office investment was all the more evident in that for prime office development, as lending terms in the largest markets saw less turbulence than elsewhere.

35CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

C H A N G E I N W H O L E L O A N L E N D I N G K E Y T E R M S A N D R I S K M E T R I C S , T H R E E S E C T O R S , Q 4 2 0 1 9 V S Q 3 2 0 2 0

On average, lenders receive a premium of 1.8% for development (rather than investment) lending at only slightly higher LTC. In Amsterdam, Brussels and London the relative risk/return is particularly attractive, especially given the solid outlook for capital growth.

Each dot represents an individual market

The chart to the left plots LTC against margin for senior prime office development lending, and confirms the broad shift of rising margins and falling LTCs. The chart to the right examines the premium that lenders receive from development lending versus investment lending, plotting the additional margin received against the LTV versus LTC differential. In addition, as a measure of risk, the size of each dot reflects forecast capital growth (larger dots are higher growth and therefore likely lower risk).

On average, lenders receive 1.81% higher margins for development lending, at the cost of an average LTC 2pp higher than the investment LTV. There is huge variation around this figure however, and the markets of Amsterdam, Brussels, London, Dublin and Milan stand out as offering above average returns. While Milan and Dublin are higher risk because of weaker growth forecasts (and Dublin LTCs are on the high side), the other three markets have above average growth forecasts and a margin premium of 3.35% (London) and 5% (Amsterdam and Brussels).

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

45 50 55 60 65 70 75 80

Mar

gin

LTC

Prime Office, primary market, development, senior lending

Q4 2019 Q3 2020 Q4 2019 average Q3 2020 average

Vienna

Brussels

Prague

Helsinki

Paris

Frankfurt

Budapest

DublinMilan

Amsterdam

LisbonBucharest

Bratislava

Madrid Zurich

London

-1

0

1

2

3

4

5

6

-10 -5 0 5 10 15

Dev

elop

men

t mar

gin

prem

ium

vers

us In

vestm

ent,

pp

Development LTC minus Investment LTV, pp

Comparison of lending terms, Prime Office, primary market, investment versus development

Office, Q3 2020

Average

-2%pa 0%pa +2%pa

Each dot represents an individual market

Size of dot represents forecast Dec-20 to Dec-25 capital growth

Source: CBRE Debt Map Q3 2020, CBRE EMEA prime office forecasts Q3 2020.

Similar return premium but huge range in LTC:LTV differential

High return premium at little additional LTC

36CBRE Q3 2020 | FINDING VALUE IN DEBT AND EQUITY

This presentation has been prepared in good faith based on CBRE’s current views of the commercial real-estate market. Although CBRE believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE’s control. In addition, many of CBRE’s views are opinion and/or projections based on CBRE’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE’s current views to later be incorrect. CBRE has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this presentation should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities – of CBRE or any other company – based on the views herein. CBRE disclaims all liability for securities purchased or sold based on information herein, and by viewing this presentation, you waive all claims against CBRE and the presenter as well as against CBRE’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein.

DISCLAIMERS AND WAIVERS

36

LO

ND

ON

EM

EA

DEBT & STRUCTURED FINANCEUK & EMEA

PAUL COATESHead of Debt and Structured Finance UK & EMEA

STEVE WILLIAMSONChairman of Debt and Structured Finance

EXECUTIVE & SENIOR DIRECTORS

ANDREA PITTALUGASENIOR DIRECTOREUROPE

CHIARA ZUCCONSENIOR DIRECTOR

DIRECTORS

MICHELLE QUINNDIRECTOR

CHRIS MARCHANTDIRECTOR

IRELAND

ANDY TALLONEXECUTIVE DIRECTOR

THE NETHERLANDS

ROBERT-JANPETERSEXECUTIVE DIRECTOR

PHILIP ZWARTSENIOR DIRECTOR

AARTVISSERDIRECTOR

REMKE MORAALDIRECTOR

GREGOIRECHALLESENIORDIRECTOR

FRANCE

MARTINAMUEHLHOFERHEAD OF CAPITALADVISORS ITALY

ITALY

JURAJBIELIKASSOCIATE DIRECTOR

SLOVAKIA

SWITZERLAND

AMINEHAMDANIEXECUTIVE DIRECTOR

FINLAND

ANNE LAUKIASENIOR DIRECTOR

PIOTR PIKIEWICZASSOCIATEDIRECTOR

POLAND

IGORBORREGOASSOCIATEDIRECTOR

PORTUGAL

DIRK RICHOLTMANAGING DIRECTOR

GERMANY

SPAIN

IÑIGOLASPIURNATIONAL DIRECTOR

ADAM LUCIUKHEAD OF DSF

POLAND

JOHN HARDIEDIRECTOR

STEPHEN BARRDIRECTOR

CHRISGOWEXECUTIVE DIRECTOR

CZECH REPUBLIC

JAKUBSTANISLAVDIRECTOR

SPAIN

IGNACIOMATIACCIDIRECTOR

DOMINIC SMITHSENIOR DIRECTOR

RESEARCH