Embed Size (px)

Citation preview

Finding Growth in Challenging Times:Seven Indicators to Evaluate Population Growth

October 2008

growth

Executive Summary

During the past several years, the U.S. retail

industry has been reeling from a slow-growing

population and a protracted economic

downturn. Despite these challenging

conditions, there are areas of the country

that are experiencing population growth and

can offer opportunities for retail businesses.

To find these communities, analysts at

Nielsen Claritas developed a statistical

approach to score the growth potential of

all U.S. markets and suggest strategies for

expansion. By determining the key indicators

of growth in markets of all sizes, this approach

offers a significant advance for retailers

even in tough economic times.

Known collectively as Population Growth

Indicators, seven factors strongly

correlate with fast-growing markets:

1) large land areas, 2) booming suburban

rings, 3) widespread affluence, 4) an

increasing Hispanic population, 5) diversified

employment, 6) long commutes and 7) the

presence of lifestyle shopping centers.

When the Population Growth Indicators are

combined with demographic projections,

retailers have a robust tool to identify

locations with significant potential for

market expansion—markets that may even

lead the way to an economic recovery in

the coming years. Now more than ever,

retail success depends on the ability to

identify growing markets, whether the

task is retail expansion, current market

optimization, or street-level site planning.

Introduction

Across the nation and around the world,

the recent crisis in the U.S. financial sector

has thrown an already declining economy

into a tailspin. Home values have dropped,

foreclosures have skyrocketed, venerable

Wall Street firms have failed and lending

for even the creditworthy has dried up.

And, as if these woes are not enough,

another trend is compounding this down-

turn, particularly for companies with siz-

able retail operations—over the last

eight years the U.S. population has

experienced little growth, averaging only

0.9 percent annually.

Slow population growth is particularly

troubling to retailers, which rely on an

expanding consumer base to increase

earnings, extend into new trade territories

and satisfy shareholders—not to mention

Wall Street analysts expecting to see

comparable store sales rise each year.

Starbucks, Linens ’n Things and The Sharper

Image are just a few of the many retailers

recently forced to shutter stores and scale back

expansion plans as a result of disappointing

sales and flawed growth forecasts. And this

gloomy scenario shows no sign of abating

over the coming years, given the stagnating

economy and current social trends marked

by later marriages, smaller families and an

aging population.

Despite this troubling news, there are markets

and population segments within the U.S.

that are experiencing healthy population

growth, offering expansion opportunities

for retail businesses even in a weak national

economy. But finding these locations requires

a different approach to identifying growth

opportunities that goes beyond calculating

new housing starts—a typical metric

employed by site planners. Using a statistical

technique that evaluates population growth

along with historic trends, Nielsen Claritas

analysts have isolated seven demographic

and economic indicators that strongly correlate

to growing markets in both metropolitan

and micropolitan communities. (Metropolitan

areas have a population of at least 50,000;

micropolitan areas have a population

between 10,000 and 50,000.) These drivers

of growth are based on a variety of Nielsen

Claritas data products—including

Pop-Facts®, the Shopping Center Database

and Business-Facts®—in addition to the

PRIZM® segmentation system, which clas-

sifies Americans according to 66 lifestyle

types and 14 social groups.

By combining the seven indicators with real

world experience, this approach offers

retailers a new way of identifying areas for

market expansion in a challenging economic

environment. Businesses hoping to thrive in

this current recessionary period, or wanting

© 2008 The Nielsen Company. All rights reservedPage 1

By Terry Muñoz, Vice President & Industry Practice Leader, Retail, Restaurantand Real Estate Group, and Mike Mancini, Vice President of Data ProductManagement, Nielsen Claritas

Finding Growth in Challenging Times:Seven Indicators to Evaluate Population Growth

to position themselves for the future,

should look to these Population Growth

Indicators to identify prime markets for new

store openings, existing store renovations

and high-return marketing programs.

Challenging Market Conditions

During the last few years, retail expansion

opportunities have suffered greatly. The

high cost of capital required to develop

new locations, low consumer confidence

and growing unemployment have all caused

retailers to scale back their expansion plans

and shopping center developers to delay

new projects indefinitely. In the commercial

real estate industry, retail vacancies have

soared to the highest level since 1996. In

the first quarter of 2008, the vacancy rate

of neighborhood and community shopping

centers reached 7.7 percent—the highest level

in 12 years. This past May, the International

Council of Shopping Centers forecast 5,770

store closings in 2008—an increase of 25

percent from only a year ago. In addition,

discretionary consumer spending has

declined as the cost of fuel and food has

risen and home values have slumped.

But not all areas of the country are feeling

the pinch. Population growth is a local

phenomenon: one community can fare far

better than the country as a whole. To

evaluate the landscape, analysts examined

the nation’s 936 CBSAs (Core Based Statistical

Areas), which include both metropolitan

and micropolitan areas accounting for 93

percent of the U.S. population. Between

2000 and 2008, 316 CBSAs experienced

high population growth, defined by analysts

as a growth rate at least 10 percent above

the national average of 8.5 percent over

the eight-year period. Meanwhile, 371

CBSAs recorded average growth and 249

CBSAs experienced declining populations.

In general, the nation’s fastest growing

markets by population tended to be large

metros in the South and West—areas such

as Atlanta, GA; Dallas, TX and Phoenix, AZ.

Nine markets added more than 500,000

people over the last eight years. Many

benefited from retirees resettling to warmer

climates. With the oldest Baby Boomers

now in their early 60s, Sun Belt retirement

communities are likely to continue to

grow as the number of older Americans

steadily increases.

This population shift also reflects economic

forces at work. Since 1990, jobs have been

leaving the industrial heartland. In fact, only

four of the nation’s biggest cities actually

lost population since 2000: Three were

Rust Belt cities—Buffalo, NY; Pittsburgh, PA

and Cleveland, OH—and one metro market,

New Orleans-Metairie-Kenner, LA was

battered by Hurricane Katrina in 2005,

causing a 13.4 percent loss in population

between 2000 and 2008 to 1,140,234.

Hardly a permanent decline, the New

Orleans market already shows signs of

coming back: Between 2006 and 2007, its

population grew by 13.8 percent—faster

than any other U.S. city with more than

100,000 people.

Growing markets come in all sizes, ranging

dramatically from Los Angeles, CA (pop.

13,304,944) to Elko, NV (pop. 49,536). But

when businesses evaluate markets for

expansion, they typically select locations

with a population density similar to their

target audience. To reflect this industry

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 2

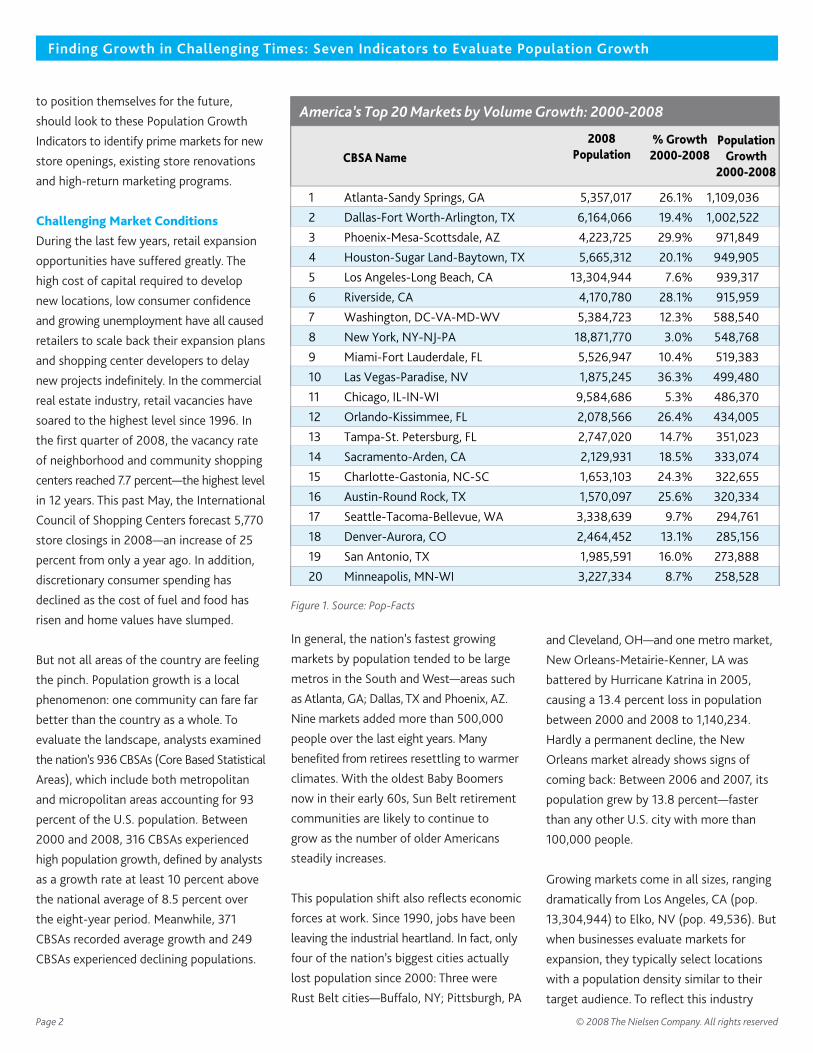

America’s Top 20 Markets by Volume Growth: 2000-2008

1 Atlanta-Sandy Springs, GA 5,357,017 26.1% 1,109,036

2 Dallas-Fort Worth-Arlington, TX 6,164,066 19.4% 1,002,522

3 Phoenix-Mesa-Scottsdale, AZ 4,223,725 29.9% 971,849

4 Houston-Sugar Land-Baytown, TX 5,665,312 20.1% 949,905

5 Los Angeles-Long Beach, CA 13,304,944 7.6% 939,317

6 Riverside, CA 4,170,780 28.1% 915,959

7 Washington, DC-VA-MD-WV 5,384,723 12.3% 588,540

8 New York, NY-NJ-PA 18,871,770 3.0% 548,768

9 Miami-Fort Lauderdale, FL 5,526,947 10.4% 519,383

10 Las Vegas-Paradise, NV 1,875,245 36.3% 499,480

11 Chicago, IL-IN-WI 9,584,686 5.3% 486,370

12 Orlando-Kissimmee, FL 2,078,566 26.4% 434,005

13 Tampa-St. Petersburg, FL 2,747,020 14.7% 351,023

14 Sacramento-Arden, CA 2,129,931 18.5% 333,074

15 Charlotte-Gastonia, NC-SC 1,653,103 24.3% 322,655

16 Austin-Round Rock, TX 1,570,097 25.6% 320,334

17 Seattle-Tacoma-Bellevue, WA 3,338,639 9.7% 294,761

18 Denver-Aurora, CO 2,464,452 13.1% 285,156

19 San Antonio, TX 1,985,591 16.0% 273,888

20 Minneapolis, MN-WI 3,227,334 8.7% 258,528

CBSA NamePopulation

Growth2000-2008

% Growth2000-2008

2008Population

Figure 1. Source: Pop-Facts

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

rate of population growth reveals a number

of Metro Towns and Micro Towns with

populations under 100,000 people. The

top three—Palm Coast, FL; Fernley, NV

and St. George, UT—all grew by more than

50 percent since 2000. Located beyond

congested metros, they’ve attracted jobs,

retailers and residents thanks to low crime

rates and fewer traffic jams. Some of the

smaller markets, like St. George, are close

to national parks and wilderness areas that

appeal to young families and retirees.

Many, like Palm Coast and Fernley, are

within commuting distance of a metropolitan

city center (Jacksonville, FL and Las Vegas,

NV respectively), attracting young families

to nearby jobs.

Population Growth Indicators

versus Traditional Measures

Traditionally, corporate real estate professionals

have assessed growth opportunities by

working with local planning boards to gather

data on new housing starts or planned

shopping centers. This approach, however,

Page 3 © 2008 The Nielsen Company. All rights reserved

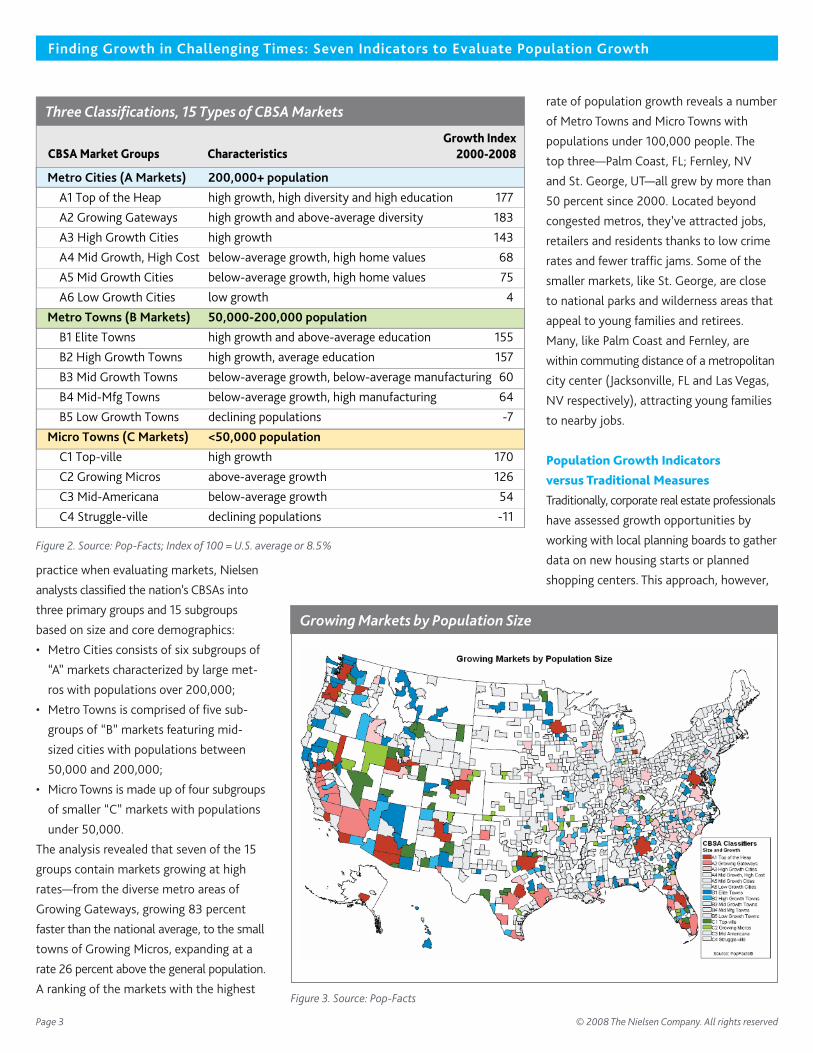

practice when evaluating markets, Nielsen

analysts classified the nation’s CBSAs into

three primary groups and 15 subgroups

based on size and core demographics:

• Metro Cities consists of six subgroups of

“A” markets characterized by large met-

ros with populations over 200,000;

• Metro Towns is comprised of five sub-

groups of “B” markets featuring mid-

sized cities with populations between

50,000 and 200,000;

• Micro Towns is made up of four subgroups

of smaller “C” markets with populations

under 50,000.

The analysis revealed that seven of the 15

groups contain markets growing at high

rates—from the diverse metro areas of

Growing Gateways, growing 83 percent

faster than the national average, to the small

towns of Growing Micros, expanding at a

rate 26 percent above the general population.

A ranking of the markets with the highest

Three Classifications, 15 Types of CBSA Markets

Metro Cities (A Markets) 200,000+ population

A1 Top of the Heap high growth, high diversity and high education 177

A2 Growing Gateways high growth and above-average diversity 183

A3 High Growth Cities high growth 143

A4 Mid Growth, High Cost below-average growth, high home values 68

A5 Mid Growth Cities below-average growth, high home values 75

A6 Low Growth Cities low growth 4

Metro Towns (B Markets) 50,000-200,000 population

B1 Elite Towns high growth and above-average education 155

B2 High Growth Towns high growth, average education 157

B3 Mid Growth Towns below-average growth, below-average manufacturing 60

B4 Mid-Mfg Towns below-average growth, high manufacturing 64

B5 Low Growth Towns declining populations -7

Micro Towns (C Markets) <50,000 population

C1 Top-ville high growth 170

C2 Growing Micros above-average growth 126

C3 Mid-Americana below-average growth 54

C4 Struggle-ville declining populations -11

CBSA Market GroupsGrowth Index

2000-2008Characteristics

Figure 2. Source: Pop-Facts; Index of 100 = U.S. average or 8.5%

Growing Markets by Population Size

Figure 3. Source: Pop-Facts

is far from foolproof: In Phoenix, AZ many

houses built in recent years were bought by

investors rather than residents. When the

housing market collapsed, speculators

couldn’t find buyers and lenders foreclosed

on their properties, resulting in more than

23,000 foreclosures this past May—the

seventh worst in the nation, according to

RealtyTrac, an online marketplace for

foreclosure properties. In a fast-changing

economy, relying on outmoded approaches to

assess opportunities means a developer may

have to wait years for consumers to appear.

The new method for identifying growth

areas allows marketers to extend their

knowledge by combining standard five-year

growth projections with new measures of

demographic data, employment variables

and lifestyle types. To uncover the most

useful metrics, analysts investigated which

factors strongly correlated with high-growth

communities. The research revealed the

seven key indicators, including demographic

drivers such as high incomes, educational

attainment and diversity. These Population

Growth Indicators also featured specific

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 4

economic traits such as a high concentration

of residents employed in construction,

business services and recreation. And

there were even some surprising criteria

among the indicators, such as the

presence of lifestyle-themed shopping

centers—those open-air malls built to

resemble a pedestrian-friendly urban village.

The most powerful indicators of growing

markets are described in the sections that

follow, accompanied by lists of the top

markets for each indicator.

1. Space to Grow: Larger Land Areas

Bigger is better when it comes to population

growth. According to the analysis, markets

with larger land areas tended to grow the

most over the last eight years. The 25

largest markets rose by an average 10.8

percent—23 percent higher than the

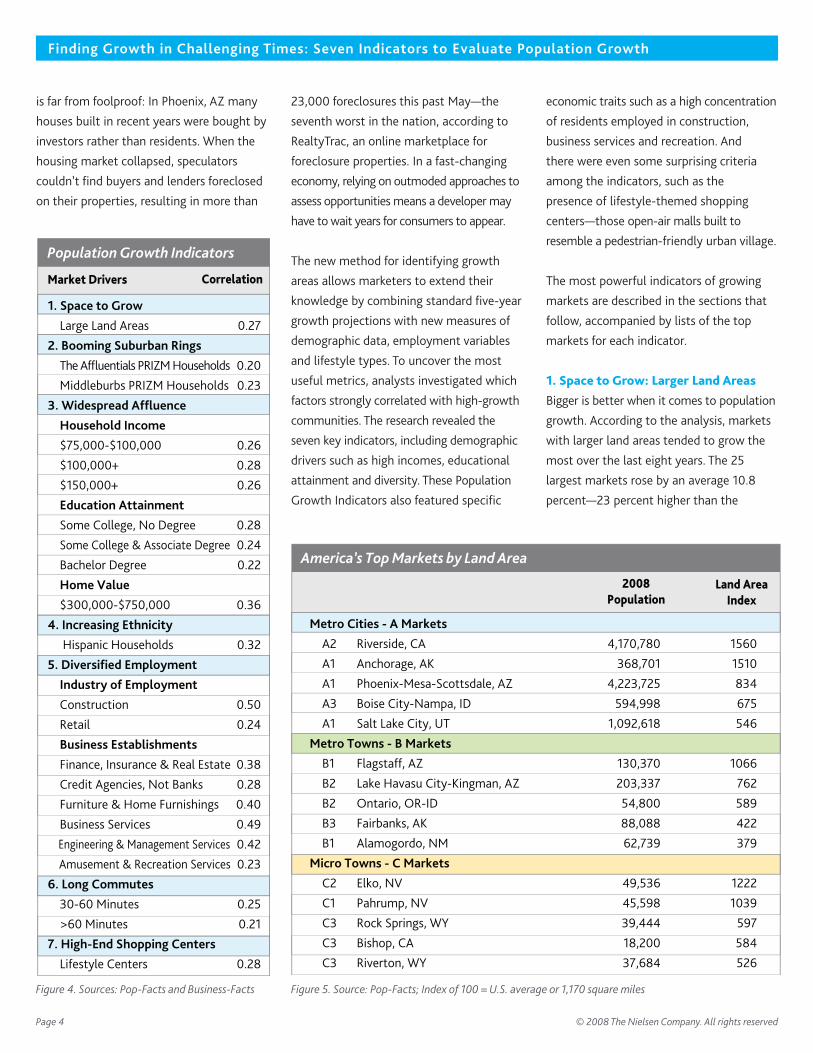

Population Growth Indicators

Correlation

1. Space to Grow

Large Land Areas 0.27

2. Booming Suburban Rings

The Affluentials PRIZM Households 0.20

Middleburbs PRIZM Households 0.23

3. Widespread Affluence

Household Income

$75,000-$100,000 0.26

$100,000+ 0.28

$150,000+ 0.26

Education Attainment

Some College, No Degree 0.28

Some College & Associate Degree 0.24

Bachelor Degree 0.22

Home Value

$300,000-$750,000 0.36

4. Increasing Ethnicity

Hispanic Households 0.32

5. Diversified Employment

Industry of Employment

Construction 0.50

Retail 0.24

Business Establishments

Finance, Insurance & Real Estate 0.38

Credit Agencies, Not Banks 0.28

Furniture & Home Furnishings 0.40

Business Services 0.49

Engineering & Management Services 0.42

Amusement & Recreation Services 0.23

6. Long Commutes

30-60 Minutes 0.25

>60 Minutes 0.21

7. High-End Shopping Centers

Lifestyle Centers 0.28

Market Drivers

Figure 4. Sources: Pop-Facts and Business-Facts

America’s Top Markets by Land Area

Metro Cities - A Markets

A2 Riverside, CA 4,170,780 1560

A1 Anchorage, AK 368,701 1510

A1 Phoenix-Mesa-Scottsdale, AZ 4,223,725 834

A3 Boise City-Nampa, ID 594,998 675

A1 Salt Lake City, UT 1,092,618 546

Metro Towns - B Markets

B1 Flagstaff, AZ 130,370 1066

B2 Lake Havasu City-Kingman, AZ 203,337 762

B2 Ontario, OR-ID 54,800 589

B3 Fairbanks, AK 88,088 422

B1 Alamogordo, NM 62,739 379

Micro Towns - C Markets

C2 Elko, NV 49,536 1222

C1 Pahrump, NV 45,598 1039

C3 Rock Springs, WY 39,444 597

C3 Bishop, CA 18,200 584

C3 Riverton, WY 37,684 526

Land AreaIndex

2008Population

Figure 5. Source: Pop-Facts; Index of 100 = U.S. average or 1,170 square miles

national average. Retailers should not

underestimate the importance of large

markets. Businesses that serve the nation’s

10 largest markets reach more than 80

million Americans—28 percent of the

nation’s total population.

Markets with larger land areas can absorb

growth more easily, leading to even faster

growth. While the average size of a CBSA is

1,710 square miles, analysts found a strong

correlation between growth and markets

like Riverside, CA, (15 times larger than

average); Elko, NV (12 times larger) and

Flagstaff, AZ (10 times larger). Many of

these markets are found in the Mountain

and Pacific states where relatively new

cities have had more room to spread out

before encroaching on the borders of other

CBSAs. (Geographical boundaries in the

desert and mountain areas may limit

expansion opportunities.)There are also plenty

of sparsely populated, but geographically

large communities that are growing thanks

to the allure of small-town charm. Tiny

Elko (pop. 49,536) grew by 34 percent in

the 1990s and another six percent since

2000, in part by offering an array of outdoor

activities like ice fishing, hunting, snowmobiling

and skiing. Accommodating zoning laws

also have helped some Western markets

grow by supporting sprawling development

without the burdensome regulation found

in older cities in the Northeast.

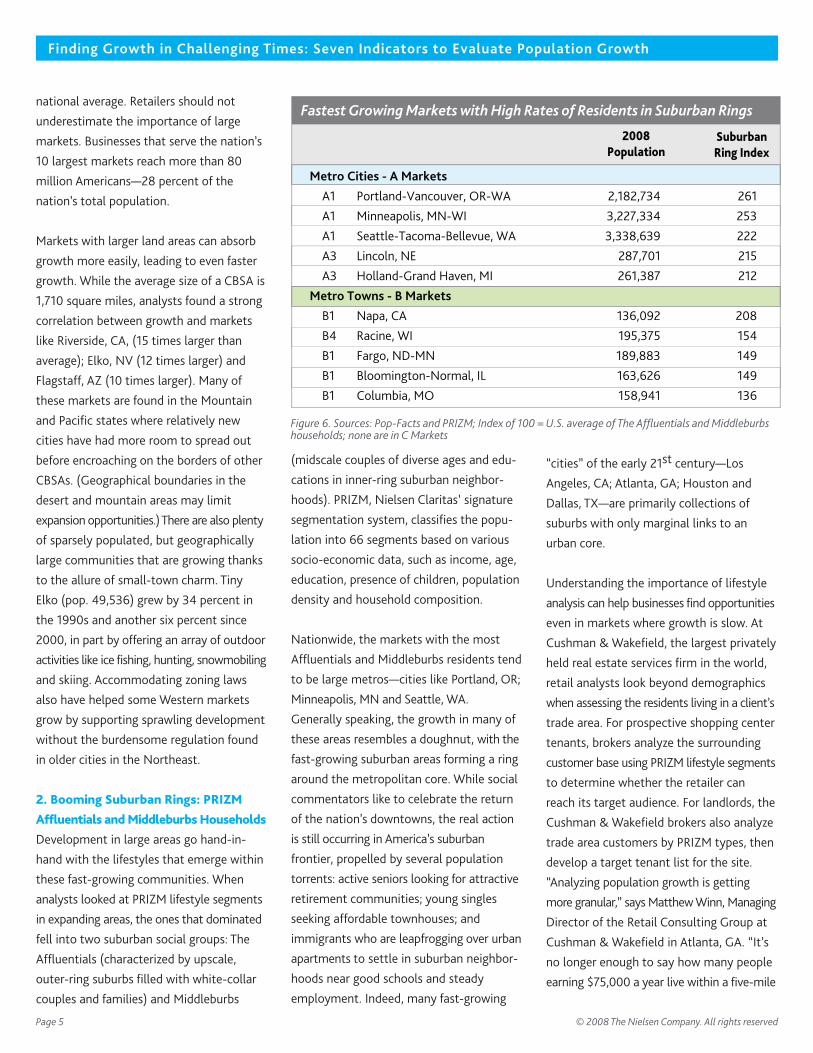

2. Booming Suburban Rings: PRIZM

Affluentials andMiddleburbsHouseholds

Development in large areas go hand-in-

hand with the lifestyles that emerge within

these fast-growing communities. When

analysts looked at PRIZM lifestyle segments

in expanding areas, the ones that dominated

fell into two suburban social groups: The

Affluentials (characterized by upscale,

outer-ring suburbs filled with white-collar

couples and families) and Middleburbs

(midscale couples of diverse ages and edu-

cations in inner-ring suburban neighbor-

hoods). PRIZM, Nielsen Claritas’ signature

segmentation system, classifies the popu-

lation into 66 segments based on various

socio-economic data, such as income, age,

education, presence of children, population

density and household composition.

Nationwide, the markets with the most

Affluentials and Middleburbs residents tend

to be large metros—cities like Portland, OR;

Minneapolis, MN and Seattle, WA.

Generally speaking, the growth in many of

these areas resembles a doughnut, with the

fast-growing suburban areas forming a ring

around the metropolitan core. While social

commentators like to celebrate the return

of the nation’s downtowns, the real action

is still occurring in America’s suburban

frontier, propelled by several population

torrents: active seniors looking for attractive

retirement communities; young singles

seeking affordable townhouses; and

immigrants who are leapfrogging over urban

apartments to settle in suburban neighbor-

hoods near good schools and steady

employment. Indeed, many fast-growing

“cities” of the early 21st century—Los

Angeles, CA; Atlanta, GA; Houston and

Dallas, TX—are primarily collections of

suburbs with only marginal links to an

urban core.

Understanding the importance of lifestyle

analysis can help businesses find opportunities

even in markets where growth is slow. At

Cushman & Wakefield, the largest privately

held real estate services firm in the world,

retail analysts look beyond demographics

when assessing the residents living in a client’s

trade area. For prospective shopping center

tenants, brokers analyze the surrounding

customer base using PRIZM lifestyle segments

to determine whether the retailer can

reach its target audience. For landlords, the

Cushman & Wakefield brokers also analyze

trade area customers by PRIZM types, then

develop a target tenant list for the site.

“Analyzing population growth is getting

more granular,” says MatthewWinn, Managing

Director of the Retail Consulting Group at

Cushman & Wakefield in Atlanta, GA. “It’s

no longer enough to say how many people

earning $75,000 a year live within a five-mile

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 5

Fastest Growing Markets with High Rates of Residents in Suburban Rings

Metro Cities - A Markets

A1 Portland-Vancouver, OR-WA 2,182,734 261

A1 Minneapolis, MN-WI 3,227,334 253

A1 Seattle-Tacoma-Bellevue, WA 3,338,639 222

A3 Lincoln, NE 287,701 215

A3 Holland-Grand Haven, MI 261,387 212

Metro Towns - B Markets

B1 Napa, CA 136,092 208

B4 Racine, WI 195,375 154

B1 Fargo, ND-MN 189,883 149

B1 Bloomington-Normal, IL 163,626 149

B1 Columbia, MO 158,941 136

SuburbanRing Index

2008Population

Figure 6. Sources: Pop-Facts and PRIZM; Index of 100 = U.S. average of The Affluentials and Middleburbshouseholds; none are in C Markets

radius of a shopping center. Now we want

to know their lifestyle and psychographics,

and whether the daytime population and

evening shoppers are a good match for tenants.

The goal is to give prospective tenants a

reason to choose your site rather than the

one two miles down the road.”

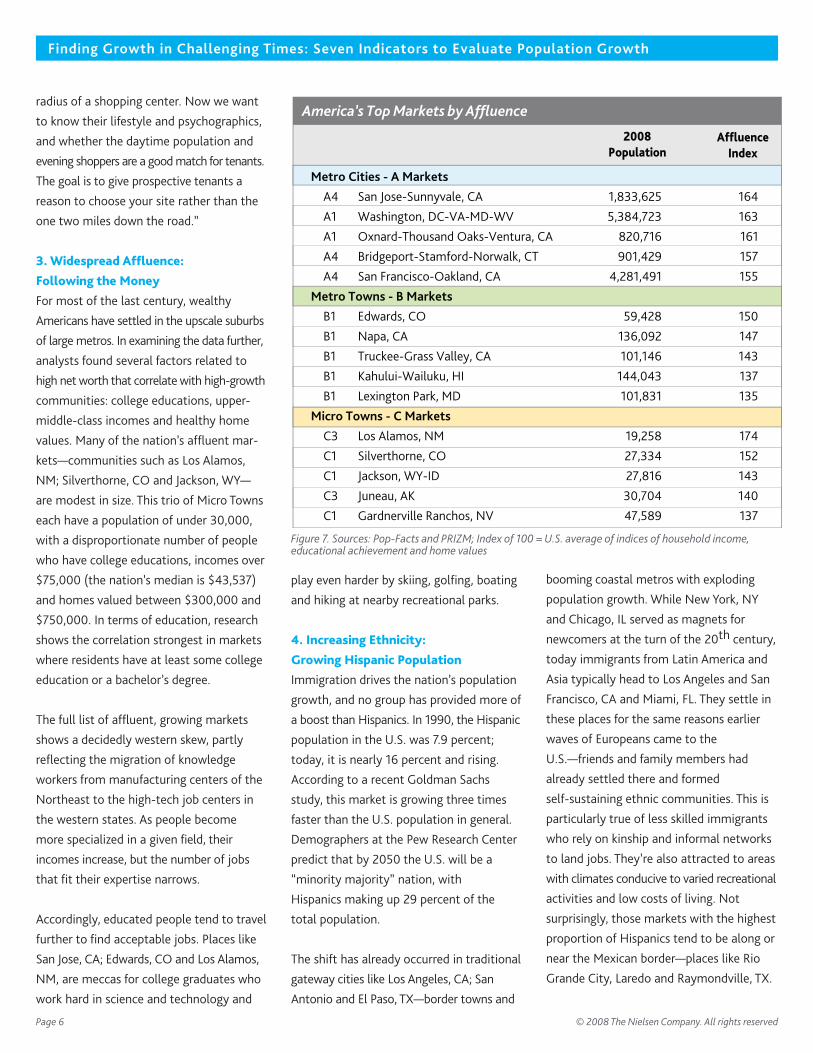

3.Widespread Affluence:

Following the Money

For most of the last century, wealthy

Americans have settled in the upscale suburbs

of large metros. In examining the data further,

analysts found several factors related to

high net worth that correlate with high-growth

communities: college educations, upper-

middle-class incomes and healthy home

values. Many of the nation’s affluent mar-

kets—communities such as Los Alamos,

NM; Silverthorne, CO and Jackson, WY—

are modest in size. This trio of Micro Towns

each have a population of under 30,000,

with a disproportionate number of people

who have college educations, incomes over

$75,000 (the nation’s median is $43,537)

and homes valued between $300,000 and

$750,000. In terms of education, research

shows the correlation strongest in markets

where residents have at least some college

education or a bachelor’s degree.

The full list of affluent, growing markets

shows a decidedly western skew, partly

reflecting the migration of knowledge

workers from manufacturing centers of the

Northeast to the high-tech job centers in

the western states. As people become

more specialized in a given field, their

incomes increase, but the number of jobs

that fit their expertise narrows.

Accordingly, educated people tend to travel

further to find acceptable jobs. Places like

San Jose, CA; Edwards, CO and Los Alamos,

NM, are meccas for college graduates who

work hard in science and technology and

play even harder by skiing, golfing, boating

and hiking at nearby recreational parks.

4. Increasing Ethnicity:

Growing Hispanic Population

Immigration drives the nation’s population

growth, and no group has provided more of

a boost than Hispanics. In 1990, the Hispanic

population in the U.S. was 7.9 percent;

today, it is nearly 16 percent and rising.

According to a recent Goldman Sachs

study, this market is growing three times

faster than the U.S. population in general.

Demographers at the Pew Research Center

predict that by 2050 the U.S. will be a

“minority majority” nation, with

Hispanics making up 29 percent of the

total population.

The shift has already occurred in traditional

gateway cities like Los Angeles, CA; San

Antonio and El Paso, TX—border towns and

booming coastal metros with exploding

population growth. While New York, NY

and Chicago, IL served as magnets for

newcomers at the turn of the 20th century,

today immigrants from Latin America and

Asia typically head to Los Angeles and San

Francisco, CA and Miami, FL. They settle in

these places for the same reasons earlier

waves of Europeans came to the

U.S.—friends and family members had

already settled there and formed

self-sustaining ethnic communities. This is

particularly true of less skilled immigrants

who rely on kinship and informal networks

to land jobs. They’re also attracted to areas

with climates conducive to varied recreational

activities and low costs of living. Not

surprisingly, those markets with the highest

proportion of Hispanics tend to be along or

near the Mexican border—places like Rio

Grande City, Laredo and Raymondville, TX.

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 6

America’s Top Markets by Affluence

Metro Cities - A Markets

A4 San Jose-Sunnyvale, CA 1,833,625 164

A1 Washington, DC-VA-MD-WV 5,384,723 163

A1 Oxnard-Thousand Oaks-Ventura, CA 820,716 161

A4 Bridgeport-Stamford-Norwalk, CT 901,429 157

A4 San Francisco-Oakland, CA 4,281,491 155

Metro Towns - B Markets

B1 Edwards, CO 59,428 150

B1 Napa, CA 136,092 147

B1 Truckee-Grass Valley, CA 101,146 143

B1 Kahului-Wailuku, HI 144,043 137

B1 Lexington Park, MD 101,831 135

Micro Towns - C Markets

C3 Los Alamos, NM 19,258 174

C1 Silverthorne, CO 27,334 152

C1 Jackson, WY-ID 27,816 143

C3 Juneau, AK 30,704 140

C1 Gardnerville Ranchos, NV 47,589 137

AffluenceIndex

2008Population

Figure 7. Sources: Pop-Facts and PRIZM; Index of 100 = U.S. average of indices of household income,educational achievement and home values

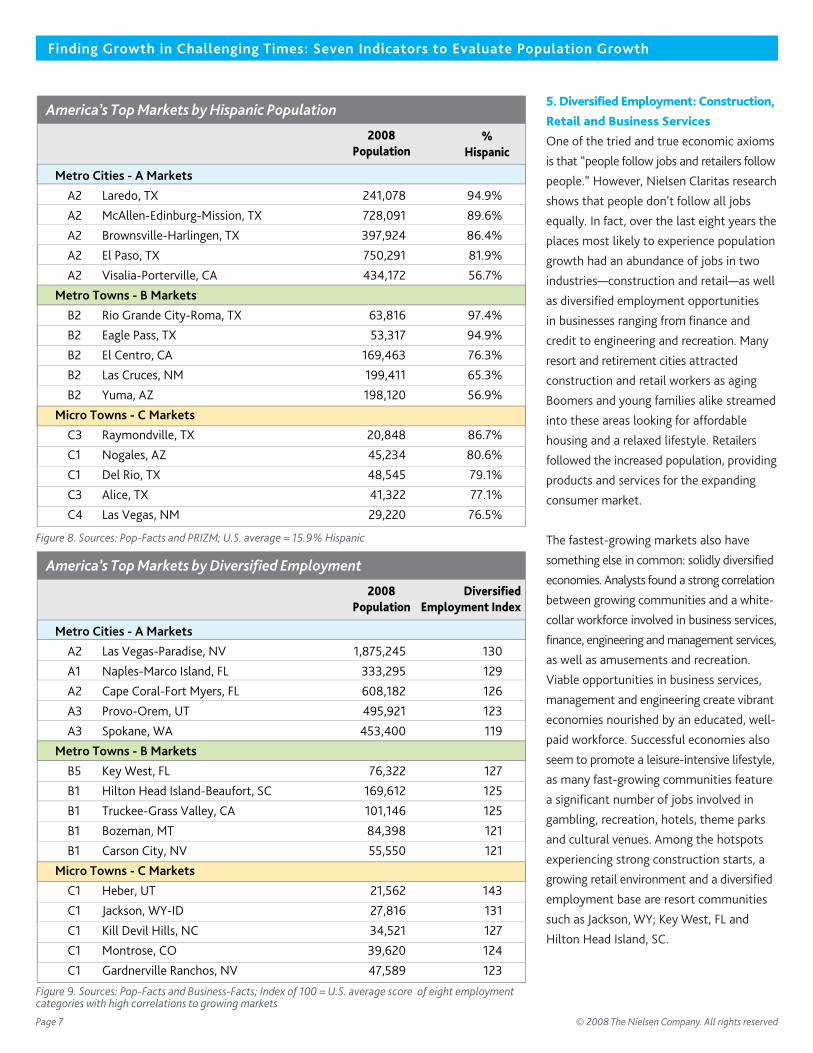

5.Diversified Employment:Construction,

Retail and Business Services

One of the tried and true economic axioms

is that “people follow jobs and retailers follow

people.” However, Nielsen Claritas research

shows that people don’t follow all jobs

equally. In fact, over the last eight years the

places most likely to experience population

growth had an abundance of jobs in two

industries—construction and retail—as well

as diversified employment opportunities

in businesses ranging from finance and

credit to engineering and recreation. Many

resort and retirement cities attracted

construction and retail workers as aging

Boomers and young families alike streamed

into these areas looking for affordable

housing and a relaxed lifestyle. Retailers

followed the increased population, providing

products and services for the expanding

consumer market.

The fastest-growing markets also have

something else in common: solidly diversified

economies. Analysts found a strong correlation

between growing communities and a white-

collar workforce involved in business services,

finance, engineering and management services,

as well as amusements and recreation.

Viable opportunities in business services,

management and engineering create vibrant

economies nourished by an educated, well-

paid workforce. Successful economies also

seem to promote a leisure-intensive lifestyle,

as many fast-growing communities feature

a significant number of jobs involved in

gambling, recreation, hotels, theme parks

and cultural venues. Among the hotspots

experiencing strong construction starts, a

growing retail environment and a diversified

employment base are resort communities

such as Jackson, WY; Key West, FL and

Hilton Head Island, SC.

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 7

America’s Top Markets by Hispanic Population

Metro Cities - A Markets

A2 Laredo, TX 241,078 94.9%

A2 McAllen-Edinburg-Mission, TX 728,091 89.6%

A2 Brownsville-Harlingen, TX 397,924 86.4%

A2 El Paso, TX 750,291 81.9%

A2 Visalia-Porterville, CA 434,172 56.7%

Metro Towns - B Markets

B2 Rio Grande City-Roma, TX 63,816 97.4%

B2 Eagle Pass, TX 53,317 94.9%

B2 El Centro, CA 169,463 76.3%

B2 Las Cruces, NM 199,411 65.3%

B2 Yuma, AZ 198,120 56.9%

Micro Towns - C Markets

C3 Raymondville, TX 20,848 86.7%

C1 Nogales, AZ 45,234 80.6%

C1 Del Rio, TX 48,545 79.1%

C3 Alice, TX 41,322 77.1%

C4 Las Vegas, NM 29,220 76.5%

%Hispanic

2008Population

Figure 8. Sources: Pop-Facts and PRIZM; U.S. average = 15.9% Hispanic

America’s Top Markets by Diversified Employment

Metro Cities - A Markets

A2 Las Vegas-Paradise, NV 1,875,245 130

A1 Naples-Marco Island, FL 333,295 129

A2 Cape Coral-Fort Myers, FL 608,182 126

A3 Provo-Orem, UT 495,921 123

A3 Spokane, WA 453,400 119

Metro Towns - B Markets

B5 Key West, FL 76,322 127

B1 Hilton Head Island-Beaufort, SC 169,612 125

B1 Truckee-Grass Valley, CA 101,146 125

B1 Bozeman, MT 84,398 121

B1 Carson City, NV 55,550 121

Micro Towns - C Markets

C1 Heber, UT 21,562 143

C1 Jackson, WY-ID 27,816 131

C1 Kill Devil Hills, NC 34,521 127

C1 Montrose, CO 39,620 124

C1 Gardnerville Ranchos, NV 47,589 123

DiversifiedEmployment Index

2008Population

Figure 9. Sources: Pop-Facts and Business-Facts; Index of 100 = U.S. average score of eight employmentcategories with high correlations to growing markets

But an over-reliance on construction and

finance jobs can have a downside risk. Both

industries have been hurt by the housing

crisis and credit crunch. As construction jobs

grow scarce during a protracted downturn

in the housing industry, workers leave

town. In markets that relied too heavily on

construction—such as Las Vegas, NV;

Phoenix, AZ and Naples, FL—analysts

expect to see a marked slowdown in popu-

lation growth and a rise in housing foreclo-

sures. Las Vegas, whose population grew

36 percent over the last eight years, is pro-

jected to expand by less than half, 17 per-

cent, between now and 2013—still a

respectable growth rate, but not likely

enough to fill the city’s inventory of empty

homes. In Naples, a glut of vacation proper-

ties has forced builders to lay off workers as

the pace of population growth is expected

to decline from 52 percent during the last

eight years to 16 percent for the next five.

As one Naples real estate broker put it,

“We’ve gone from an extraordinary real

estate market to a merely normal one.”

6. Long Commutes: A Price of Growth

Infrastructure is also important in growing

communities. Fast growth correlates with

significant numbers of air transport jobs,

workers with home offices and, unfortunately,

long commutes. Obviously, thriving

communities need good airport connections

to accommodate business and vacation

travelers, as well as high-speed Internet

access so workers can connect to employers

from home offices. Fast-growing communities

also tend to saddle workers with long commute

times, typically much longer than the

national average of 25 minutes. The long

commute likely reflects many workers living

in the more affordable suburban fringes of

metro areas. It’s not just the miles, though,

that lengthen these commutes. More

frustrating are the minutes spent in traffic

jams caused by the undesirable side effects

of fast growth: feeder roadways not built

to accommodate rush hour traffic, the

absence of public transit in the hinterlands

and uncontrolled sprawl that did not

account for car-dependent lifestyles. These

are the ills of life in the fast-growth lane,

though they can be mitigated by planners

who recognize the presence of Population

Growth Indicators in their communities

and address the issues accordingly.

7. High-End Shopping Centers:

Lifestyle Centers

One unexpected result of the boom in

affluent commuter suburbs is the emergence

of high-end shopping centers known as

“lifestyle centers.” A kind of outdoor mall,

they feature natural sunshine, tree-lined

streets, stress-relieving fountains and plenty

of shops and restaurants. Unlike the massive,

windowless suburban malls anchored by a

department store, these centers resemble

quaint villages filled with high-end retailers

like Talbots, Coach, Chico’s, Banana Republic

and Starbucks. And they’re designed for

upscale suburban professionals who want

the convenience of driving up to the shops,

parking their cars and downing a

Frappuccino® while lounging on an over-

stuffed chair. Ironically, these suburban

creations are designed to resemble the

downtown commercial districts that shop-

pers fled long ago.

At a time when mall expansion is declining,

lifestyle centers are growing at a rate of

several dozen annually. Today, there are

more than 400 of these tabernacles of con-

sumerism, with their narrow pedestrian

streets and little plazas. And they’re

sprouting up in growing mid-sized metros

and college towns like Yakima, WA; Ann

Arbor, MI and Bend, OR. Because lifestyle

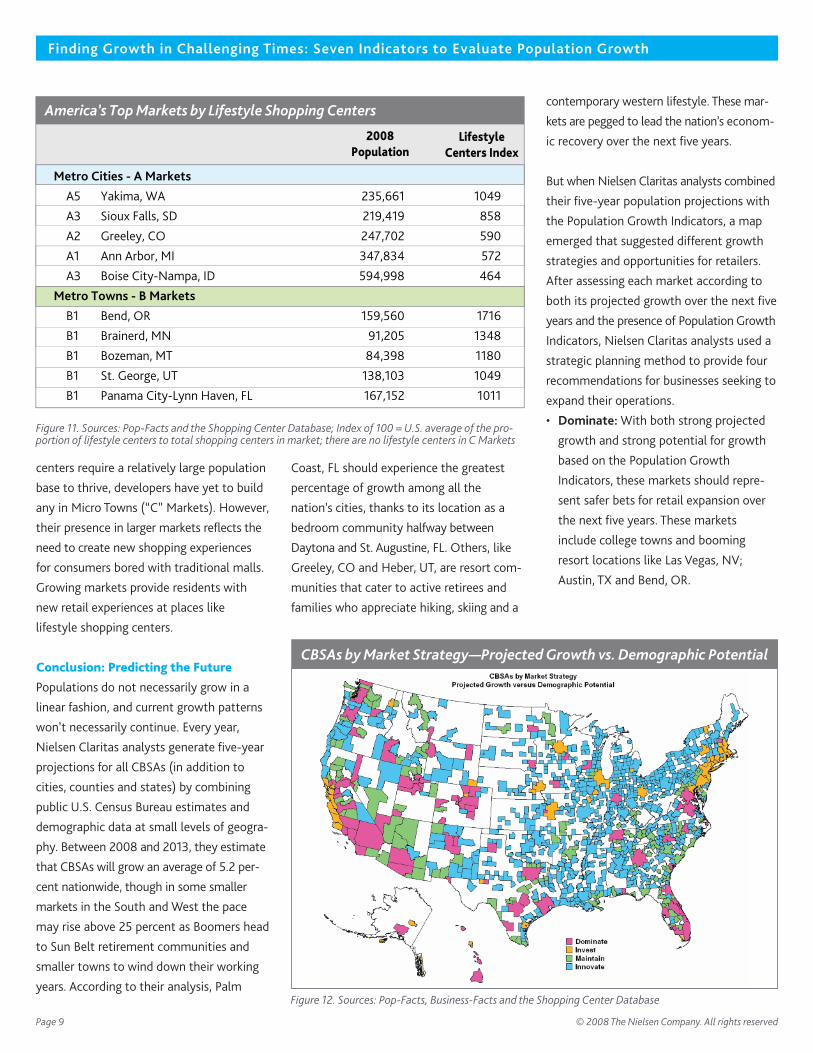

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

Page 8 © 2008 The Nielsen Company. All rights reserved

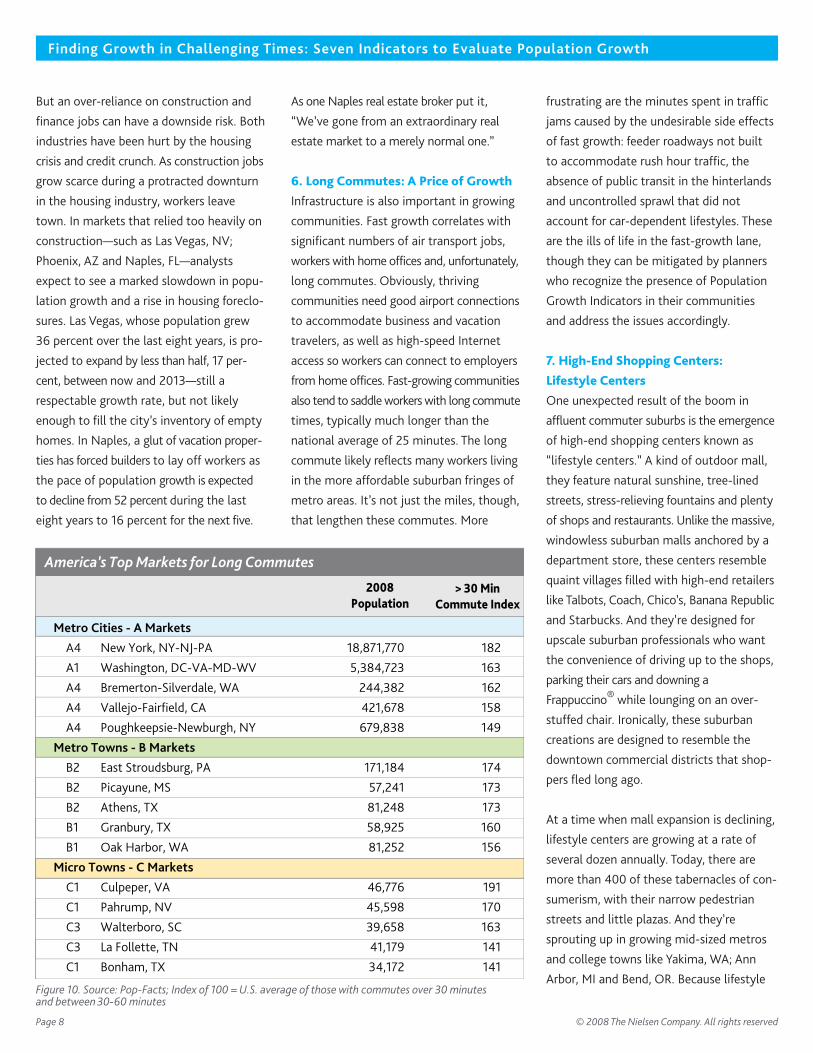

America’s Top Markets for Long Commutes

Metro Cities - A Markets

A4 New York, NY-NJ-PA 18,871,770 182

A1 Washington, DC-VA-MD-WV 5,384,723 163

A4 Bremerton-Silverdale, WA 244,382 162

A4 Vallejo-Fairfield, CA 421,678 158

A4 Poughkeepsie-Newburgh, NY 679,838 149

Metro Towns - B Markets

B2 East Stroudsburg, PA 171,184 174

B2 Picayune, MS 57,241 173

B2 Athens, TX 81,248 173

B1 Granbury, TX 58,925 160

B1 Oak Harbor, WA 81,252 156

Micro Towns - C Markets

C1 Culpeper, VA 46,776 191

C1 Pahrump, NV 45,598 170

C3 Walterboro, SC 39,658 163

C3 La Follette, TN 41,179 141

C1 Bonham, TX 34,172 141

> 30 MinCommute Index

2008Population

Figure 10. Source: Pop-Facts; Index of 100 = U.S. average of those with commutes over 30 minutesand between30-60 minutes

centers require a relatively large population

base to thrive, developers have yet to build

any in Micro Towns (“C” Markets). However,

their presence in larger markets reflects the

need to create new shopping experiences

for consumers bored with traditional malls.

Growing markets provide residents with

new retail experiences at places like

lifestyle shopping centers.

Conclusion: Predicting the Future

Populations do not necessarily grow in a

linear fashion, and current growth patterns

won’t necessarily continue. Every year,

Nielsen Claritas analysts generate five-year

projections for all CBSAs (in addition to

cities, counties and states) by combining

public U.S. Census Bureau estimates and

demographic data at small levels of geogra-

phy. Between 2008 and 2013, they estimate

that CBSAs will grow an average of 5.2 per-

cent nationwide, though in some smaller

markets in the South and West the pace

may rise above 25 percent as Boomers head

to Sun Belt retirement communities and

smaller towns to wind down their working

years. According to their analysis, Palm

Coast, FL should experience the greatest

percentage of growth among all the

nation’s cities, thanks to its location as a

bedroom community halfway between

Daytona and St. Augustine, FL. Others, like

Greeley, CO and Heber, UT, are resort com-

munities that cater to active retirees and

families who appreciate hiking, skiing and a

contemporary western lifestyle. These mar-

kets are pegged to lead the nation’s econom-

ic recovery over the next five years.

But when Nielsen Claritas analysts combined

their five-year population projections with

the Population Growth Indicators, a map

emerged that suggested different growth

strategies and opportunities for retailers.

After assessing each market according to

both its projected growth over the next five

years and the presence of Population Growth

Indicators, Nielsen Claritas analysts used a

strategic planning method to provide four

recommendations for businesses seeking to

expand their operations.

• Dominate: With both strong projected

growth and strong potential for growth

based on the Population Growth

Indicators, these markets should repre-

sent safer bets for retail expansion over

the next five years. These markets

include college towns and booming

resort locations like Las Vegas, NV;

Austin, TX and Bend, OR.

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 9

America’s Top Markets by Lifestyle Shopping Centers

Metro Cities - A Markets

A5 Yakima, WA 235,661 1049

A3 Sioux Falls, SD 219,419 858

A2 Greeley, CO 247,702 590

A1 Ann Arbor, MI 347,834 572

A3 Boise City-Nampa, ID 594,998 464

Metro Towns - B Markets

B1 Bend, OR 159,560 1716

B1 Brainerd, MN 91,205 1348

B1 Bozeman, MT 84,398 1180

B1 St. George, UT 138,103 1049

B1 Panama City-Lynn Haven, FL 167,152 1011

LifestyleCenters Index

2008Population

Figure 11. Sources: Pop-Facts and the Shopping Center Database; Index of 100 = U.S. average of the pro-portion of lifestyle centers to total shopping centers in market; there are no lifestyle centers in C Markets

CBSAs by Market Strategy—Projected Growth vs. Demographic Potential

Figure 12. Sources: Pop-Facts, Business-Facts and the Shopping Center Database

• Invest:With moderate projected growth,

but strong potential based on their

Population Growth Indicators, these

markets may grow faster than expected,

indicating possible opportunities for

retailers. Among these markets are such

knowledge worker havens as Los Alamos,

NM; San Jose, CA; Boulder, CO and

Minneapolis, MN.

• Maintain: Markets in this category may

be riskier for retailers because, though

their projected growth is above average,

their potential according to the Population

Growth Indicators is below average. In

markets like New Orleans, LA; Coeur

d’Alene, ID and Brownsville, TX, retailers

may want to more thoroughly research any

expansions plans.

• Innovate: With weak scores for both

projected and potential growth, the many

small markets in this group would need

extra money and attention—perhaps a

new retail concept or a different product

mix—to become a promising retail oppor-

tunity. Among the communities in this

category are college towns like

Columbia, MO; Corvallis, OR and

Greensboro, NC.

Admittedly, any strategic plan that combines

historical indicators with future estimates

has inherent limitations. The hallmarks of

growth can evolve over time. And as the

Population Growth Indicators show, growth

can manifest itself in unexpected ways.

In addition, the importance of specific

indicators can vary depending on a retailer’s

target audience.

Nevertheless, retailers can use this analysis

to quickly assess a market’s potential and

determine where it fits into their overall

development strategy. Even in a sluggish

economy with slow population growth, this

innovative modeling approach can suggest

expansion opportunities in overlooked markets.

With this new approach to analysis based on

the Population Growth Indicators, retailers

now have a tool to help them identify these

rising stars and stake out the best locations

to attract their target customers. For those

retailers willing to embrace this paradigm shift

in understanding growth, many may be in a

position to reap the rewards for their expansion

efforts—or at least avoid costly mistakes.

Behind the Numbers

For the methodology, Nielsen Claritas

analysts examined hundreds of variables

before determining several dozen that were

correlated to percent growth from 2000 to

2008. Variables with strong positive and

negative correlations were grouped by vari-

able type and selected to reflect collineari-

ty (e.g., variables like income and educa-

tion that tend to track together). This

process reduced the set of Population

Growth Indicators to the core seven that

were then used to score and classify CBSA

markets. And the maps and tables reflect

markets that are outperforming others,

according to a proprietary population growth

analytical approach that utilizes Pop-Facts

demographic estimates and projections

data.

Inverse or negative correlations (such as high

school education) were not used because

analysts did not want to “double-count”

against low growth markets; by definition,

markets with fewer college graduates will

have a higher percentage of residents with

only a high school education or less.

While correlations provide valuable insight,

a strict cause and effect relationship should

not be inferred. For example, a high percentage

of construction workers in a market may be

highly correlated to growth, but it’s doubtful

that simply having an abundance of

construction workers will create high

growth. More likely, construction workers

are attracted to markets that are already

growing and need new homes, roads and

shopping centers—as well as the workers

to build them.

For other variables, like income, education

and business services employment, the

cause versus effect is less clear. While high

growth markets are more likely to attract

educated professionals in search of opportunity,

an abundance of well-educated professionals

may also lead to high growth in a market

as potential employers are drawn by the

talent pool. In this case, the presence of

educated residents is a cause, rather than

an effect, of growth. Diversity is another fac-

tor that could be a cause—diverse markets

are more dynamic and grow faster—or an

effect, because growing markets tend to

attract more immigrants.

Ultimately, markets with an educated and

diverse work force likely will attract busi-

ness services and technology innovators

and, because people tend to follow jobs—

growth will follow. These assumptions were

made when scoring, classifying and organ-

izing CBSA markets along the Dominate-

Invest-Maintain-Innovate dimensions cited

in the conclusion.

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

© 2008 The Nielsen Company. All rights reservedPage 10

Finding Growth in Challenging Times: Seven Indicators to Evaluate Population Growth

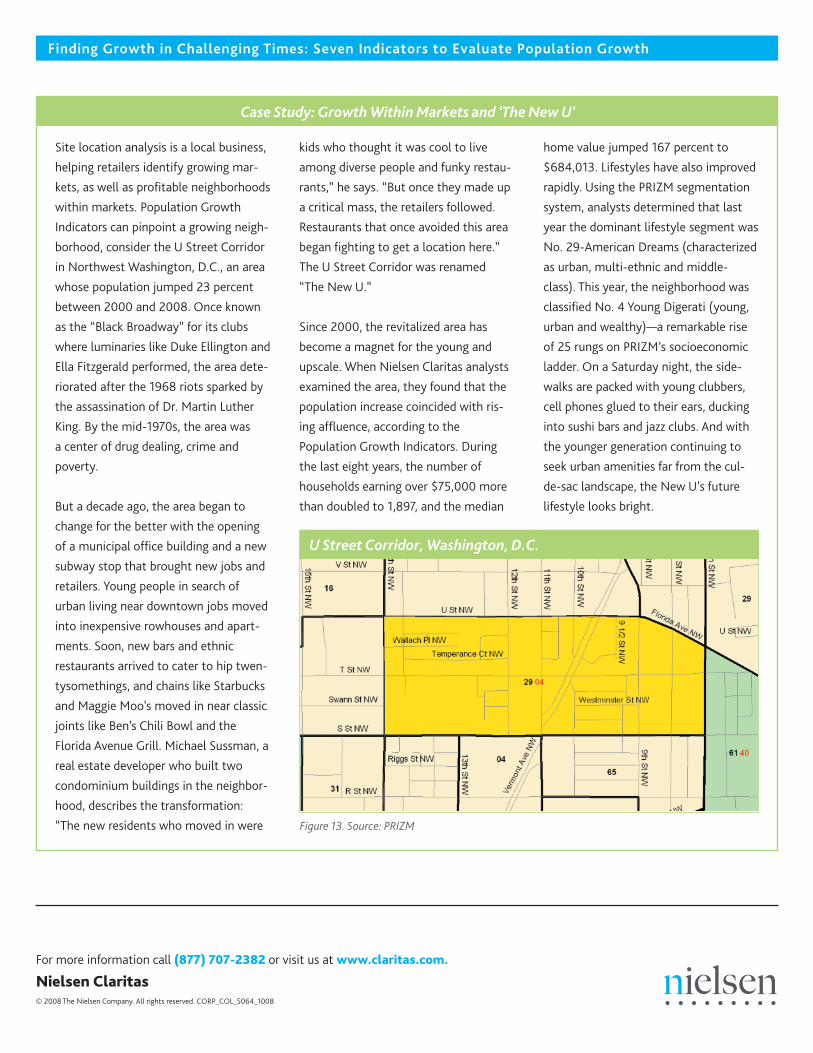

U Street Corridor, Washington, D.C.

Figure 13. Source: PRIZM

Site location analysis is a local business,

helping retailers identify growing mar-

kets, as well as profitable neighborhoods

within markets. Population Growth

Indicators can pinpoint a growing neigh-

borhood, consider the U Street Corridor

in Northwest Washington, D.C., an area

whose population jumped 23 percent

between 2000 and 2008. Once known

as the “Black Broadway” for its clubs

where luminaries like Duke Ellington and

Ella Fitzgerald performed, the area dete-

riorated after the 1968 riots sparked by

the assassination of Dr. Martin Luther

King. By the mid-1970s, the area was

a center of drug dealing, crime and

poverty.

But a decade ago, the area began to

change for the better with the opening

of a municipal office building and a new

subway stop that brought new jobs and

retailers. Young people in search of

urban living near downtown jobs moved

into inexpensive rowhouses and apart-

ments. Soon, new bars and ethnic

restaurants arrived to cater to hip twen-

tysomethings, and chains like Starbucks

and Maggie Moo’s moved in near classic

joints like Ben’s Chili Bowl and the

Florida Avenue Grill. Michael Sussman, a

real estate developer who built two

condominium buildings in the neighbor-

hood, describes the transformation:

“The new residents who moved in were

kids who thought it was cool to live

among diverse people and funky restau-

rants,” he says. “But once they made up

a critical mass, the retailers followed.

Restaurants that once avoided this area

began fighting to get a location here.”

The U Street Corridor was renamed

“The New U.”

Since 2000, the revitalized area has

become a magnet for the young and

upscale. When Nielsen Claritas analysts

examined the area, they found that the

population increase coincided with ris-

ing affluence, according to the

Population Growth Indicators. During

the last eight years, the number of

households earning over $75,000 more

than doubled to 1,897, and the median

home value jumped 167 percent to

$684,013. Lifestyles have also improved

rapidly. Using the PRIZM segmentation

system, analysts determined that last

year the dominant lifestyle segment was

No. 29-American Dreams (characterized

as urban, multi-ethnic and middle-

class). This year, the neighborhood was

classified No. 4 Young Digerati (young,

urban and wealthy)—a remarkable rise

of 25 rungs on PRIZM’s socioeconomic

ladder. On a Saturday night, the side-

walks are packed with young clubbers,

cell phones glued to their ears, ducking

into sushi bars and jazz clubs. And with

the younger generation continuing to

seek urban amenities far from the cul-

de-sac landscape, the New U’s future

lifestyle looks bright.

For more information call (877) 707-2382 or visit us at www.claritas.com.

Nielsen Claritas© 2008 The Nielsen Company. All rights reserved. CORP_COL_5064_1008

Case Study: Growth Within Markets and ‘The New U’