-

7/29/2019 Findings H L Yadav

1/13

The Chairman & Disciplinary Authority

Gramin Bank Of Aryavart

Head Office,

A2/46, Vijay Khand, Gomti Nagar

Personnel & Industrial Law Department,

Lucknow

Sir,

Ref-Submission of findings in respect of departmental enquiry

conducted into the

charges against Shri Hriday Lal Yadav,Staff Officer (under

Suspension), Khushal Ganj Branch, Distt.

Lucknow

I was appointed Enquiry Officer vide letter number

HO/VIG/P-699/C-20/(2011-12)/153 dated

20/06/2012 by the disciplinary authority to conduct the

departmental enquiry into alleged acts of

misconduct as communicated to him vide Article of Charges

bearing number HO/VIG/P-699/C-20/(2011-

12)/150-A dated 20/06/2012, supported by Statement of Allegation

bearing reference number

HO/VIG/P-699/C-20/(2011-12)/150 -B dated 20/06/2012 along with

memorandum bearing reference

number HO/VIG/P-699/C-20/(2011-12)/150 dated 20/06/2012.In

compliance of instructions I issued the letter of commencement of

Enquiry fixing the first date of

enquiry on 16/08/2012.. Enquiry was concluded on 11/03/2013

after 23 sitting in between. Proceedings

of enquiry were recorded in 206 pages. Management side presented

28 documents in support of

charges out of which one document was disallowed as it was not

found relevant. Management side

presented 7 witnesses to substantiate the charges.

Defence side presented in all 19 documents beside a few enquiry

documents. Defense side presented

only one witness. Management side was presented by Shri R.P.

Verma, Senior Manager at FI department

at Head Office. Shri Yadav preferred to present his own defence

personally although he was given

option to engage defense representative at any point of time in

the enquiry.

Management side was asked to submit its written brief by

26/03/2013 which was delayed and was

finally submitted on 10/04/2013. Copy of the briefs submitted by

management side was made availableto Shri Yadav On 10/04/2013 it

self. Defence side submitted its brief on 23/04/2013.

Gist of charges

1.CSO has been alleged to have violated Banks guidelines

pertaining to retention limit of cash. He kept

cash at the branch in excess to the maximum retention limit of

Rs.4.00 Lakhs on 25 occasions, which

subsequently led to exposing the Bank to theft of Rs.28,46,477/-

at the Branch on 08.11.2011.

2. CSO is alleged to have failed to adhere to security norms as

well as the systems and procedures of the

Bank and acted in a total casual manner leading to theft of

Rs.28,46,477/- at the branch on 08-11-2011,

in as much as he failed to ensure that

Cash Receipt Book and Cash Payment Book has been maintained at

the Branch. Failed to ensure control and supervision over the role

of Cashier Sh. B.K.Mishra, who used to

take out the entire kept in the vault, for transacting days

business

Failed to ensure that dual cash control book of the branch is

being maintained properly at theBranch. .

-

7/29/2019 Findings H L Yadav

2/13

Failed to ensure that the Bait Money is maintained at the cash

vault of the Branch. Allowed Shri Ajay Kumar S/O Ram Pratap, R/O

Vill. Maunda, Distt. Lucknow, casual labour, to

retain one set of keys of locks of outer shutter and channel, on

regular basis.

CSO on 05-11-2011, at the close of the business, did not

accompany the branch Cashier Sh.B.K.Mishra to the strong room for

lodgement of cash in the Branchs cash safe, instead he

handed over Managers cash safe master key to casual labour Sh.

Ajay Kumar

CSO failed to keep the safe vault master key under proper

control; instead he handed over thesame to said Shri Ajay Kumar,

which facilitated him to use the same to the detriment of Banks

interest.

3. On 05.11.2011, being Saturday, CSO did not ensured that the

locks of cash safe, strong room, channel

and shutter are properly locked and instead he along with

Cashier Sh. B.K.Mishra left the branch

opened,leaving the Banks property at the disposal of casual

labor Sh. Ajay Kumar.

In the aforesaid manner, CSO failed to adhere to the norms of

the Bank, acted negligently and

breached the Regulation 18 and 20 read with Regulation 39 of

Aryavart Gramin Bank, (Officers and

Employees) Service Regulations, 2010.

Gist of the defence of the employee on each Article Of

Charge

1. Management side tried to prove the charges on the basis of

two documents i.e, MEx-10 and ME.x- 11which were verified by the

management witness 2, Shri Manjeet Singh who was the manager of

the

KhushalGanj branch at the time of his witness. Main defence

against this charge are-

Witness MW2 is neither maker nor checker of these documents

therefore he is not justified ingiving his opinion on the

subject.

Document Mex-11 was never received at the KhushalGanj branch.

Initials of receiving on MEx-11, leaves many question unanswered

and document is disputed in

itself.

Doubt regarding date of applicability of instructions as per

document MEx-11. Has taken plea of customer service for maintaining

cash beyond retention limit.. He has taken plea of cash balance

maintained at Khushalganj branch before and after his period

of stay as manager of the branch.

He has also quoted the heavy withdrawals as reason of

maintaining cash beyond retentionlimit.

He has also taken plea of audit report and notes in balance

sheet regarding position of overallcash retention limit of Bank

during 2010-11 and 2011-12.

-

7/29/2019 Findings H L Yadav

3/13

After implementation of CBS, RO/HO could have easily monitored

the position of cash retentionat branch level.

2. a. After migration from TBM to CBS writing of these books was

discontinued at the most of the

branches. Writing of books was discontinued before he took over

as Manager of the branch.

b .Cash retention limit at counter and safe was not communicated

so there can be no violation of

retention limit by the cashier while withdrawing cash from the

safe for routine transaction.

c Dual control book was being maintained in the same format

before he joined as manager. Book was

maintained on SB pass book and there was not sufficient space

for signing by the two persons. Audit

report does not mention any adverse comment on this issue.

d. He has based his defence on the cross examination of

management witness MW7.

e. That the key of shutter and channel was given by the cashier

and not by him.

f. He has tried to confuse the issue by raising many issues not

connected with the charge directly.

g. Has denied the charge without giving any concrete reason.

3. CSO has himself taken the responsibility of EO has declared

the documents MEx-15, MEx-16, MEx-28

as disputed and not acceptable in the enquiry on the basis of

which management side tried to prove this

charge.

Article-1

Documents and oral evidence presented by PO

1. Management side presented document MEx-10 & MEx-11 which

are cash retention limit intimation

letter dt 12/08/2011 issued by Lucknow Regional ,Office to

Khushalganj Branch and daily cash balance

book for the period 21/02/2011 to 05/11/2011 respectively. Both

these documents have been verified

by witness MW2. According to management side CSO received

document MEx-11 on 18/08/2011 and

put a initial to acknowledge receiving. Even though CSO was well

aware of the Cash Retention Limit he

did not took required necessary steps to maintain cash within

limit.

2. Witness MW2 verified the initials of CSO on MEx-11 on page

number 58 of the enquiry proceedings.

3 Thus on the basis of above two documents and oral evidence of

witness MW2 charge is proved

beyond any doubt.

Arguments of defence side

1. MW2 is neither maker nor checker of the document MEx-11. He

neither received the document

therefore he cannot express any opinion on the document

2. Document MEx-11 was never received at the branch.

3. CSO wanted to inspect the registers of dispatch of Regional

Office, Lucknow, permission of which was

denied by the enquiry Officer.

4. Witness MW2 is not the custodian of Document MEx-11.

5. CSO has certain doubts regarding his acknowledgement marked

on MEx-11.He wanted to examine

certain documents permission of which was not given by EO.

-

7/29/2019 Findings H L Yadav

4/13

6. There are some contradictions as to the applicability of

instructions mentioned in MEx-11

7. CSO referred to document MEx-19 and tried to justify the

retaining cash beyond limit on the plea of

providing better customer service. No circular has ever

prohibited keeping cash beyond the retention

limit.

8. Basic sum insured of the branch is 50 lac as per document

MEx-19.

9. CSO has also referred to grading for cash management by the

audit work sheet attached with

document DEx-10.

10. He has tried to justify the practice of keeping cash beyond

the cash limit on the basis of business

growth during his tenure as branch manager. He introduced

customers who were involved in purchase

and sale of land which necessitated heavy in and outflow of cash

in the branch. It was not possible to

cater to the demands of such customers by maintaining cash

within retention limit.

11. With the help of documents DEx-4 & DEx-8, he has tried

to prove that cash was never maintained

either before or after his tenure as manager of the Khushalganj

branch.

12. CSO also tried to justify his action of keeping cash beyond

the retention limit by giving the amount of

money withdrawn on dates of alleged defaults.

13. DEx-15 clearly indicates that average holding of cash at

branch level is 2.44% which means ideal

situation of cash could not be maintained during the period

28/08/2009 to 29/04/2011.

14. During the tenure of CSO average cash holding remained at

the level of 1% vis a vis deposit level ofRs.10 crores.

15. Average cash holding of bank was 1.07% during 2011-11 and

0.99% during 2011-12 which is clear

from the exhibit DEx-9 (a & b), which are extracts from the

printed balance sheets of the periods under

reference.

16. Document DEx(b) which is Risk Based Management Report

mentions,

(observation} |

17. CSO has tried to give reasons of excess cash on 05/11/2011

on the basis of document MEx-13 and

MEx-16.

18. CSO on the basis of statement of Shri B.K.Mishra tried to

justify the retention limit between 5 lacs to7.50 lacs.

19. CSO tried to justify the retaining cash beyond the limit on

the basis of non receipt of any warning

Letter/Reminder from RO/HO in this regard.

Defence side while summing up said that from the perusal of

above points it is clear that CSO always

tried to maintain minimum balance keeping in mind the insurance

limit, Cash requirement of customers

due to growing business of branch and he never gave any reason

of complaint to the management, thus

charge is totally baseless and false.

Assessment/Observation

1. CSO has not denied his initials of receiving with date on

document MEx-11.

2. He also failed to explain under what circumstances he put his

initials with date on document MEx-11.

Can he deny the knowledge of contents of document MEx-11? Can he

be so irresponsible to receive a

letter without going through its contents?

3. Document MEx-10 clearly demonstrates the violation of cash

retention limit as spelled out in MEx-11

on 25 occasions as mentioned in the Statement Of Allegations in

Article-1.This document is Daily Cash

Balance Book for the period 21/02/2011 to 05/11/2011 and has

been verified by witness MW2, who was

the custodian of the document at the time of giving his oral

evidence.

-

7/29/2019 Findings H L Yadav

5/13

4. All the 25 occasions mentioned in the Statement of

Allegations in Article-1 pertain to the period after

date of receiving of document MEx-11 i.e. 18/08/2013.

6. He cannot justify his act of retaining the cash beyond

permitted limit because he did not get any

reminder in this regard from HO /RO or any mention of this

deficiency in the statutory audit report of

the branchfor the period before his tenure of managershipHe has

tried to argue at great lengths that his act of keeping cash beyond

retention limit was a general

practice in almost all the branches, he has also given ample

documentary evidences to prove his point.

He failed to produce any document to prove that he tried to get

the cash retention limit enhanced

keeping in mind the increased financial transactions at the

branch due to business growth of the branch.

Charge as enumerated in Article-1 and supported by Statement of

allegation is thus proved on the basis

of Documents MEx-10 & 11 read together with the oral

evidence of witness MW2.

ARTICLE-II(a)

Documents and oral evidence presented by PO

To support the allegation that CSO did not ensured to maintain

Cash Receipt and Cash payment book

during his tenure as Manager of Khushalganj Branch PO has relied

on documents MEx-2,MEx-7,MEx-9and oral evidences of witnesses MW2

and MW4. He has proved the charge on the basis of these

documents.

I am not discussing the PO side in detail as CSO has not

contradicted the charge. He has simply given

reasons for not maintaining these two book of accounts.

Arguments of defence side

1. Writing of both the books i.e. Cash Receipt and Cash Payment

books were discontinued much before

he joined as Branch Manager of Khushalganj Branch.

2. Through the oral evidences of witness MW-3, MW-4 and MW-7 CSO

has ably proved that practice of

writing these two books was discontinued before his tenure of

managership.

3. CSO himself admitted that he started and signed the Cash

Payment Book on 09/11/2011 for the first

time a day after the theft was detected.

4. Practice of writing these two books was discontinued at the

branch after migration of branch from

TBM to CBS , and this migration took place before he joined as

Branch Manager of Khushalganj Branch.

5. Document DEx-14(a) clearly indicates that writing of these

two books was discontinued at other

branches also.

5 Audit conducted on 11/05/2011 and 12/05/2011 did not made any

adverse remark on this point.

Therefore charge is totally false and baseless.

Assessment/Observation

Defence side failed to produce any document to show any

instructions / circular that these books be

discontinued after migration of the branches from TBM to CBS. I

agree that these books werediscontinued before CSO took over as

Branch Manager. Should a prudent manager overlook the

instructions of higher authorities and should not start a

practice which has been stopped without any

instructions to do so from the controlling offices.

There may be several reasons for not maintaining these books but

the fact remains that charge was

that No cash receipt or cash payment book was maintained during

the tenure of CSO as branch

manager and it is proved beyond any doubt by the documents and

oral evidences produced by the

management side

Therefore charge is proved.

-

7/29/2019 Findings H L Yadav

6/13

Article 2(b)

Documents and oral evidence presented by PO

1.Document MEx-11 by which cash retention limit of Khushalganj

branch was intimated and which was

received by the CSO on 18/08/2011 himself, clearly fix the

retention limit of branch at Rs.400000/-.

2. Document MEx-4, which is Dual Cash Control Book from

20/7/2011 to 05/11/2011 of Khushalganj

branch and which has been verified by the Management Witness MW2

clearly establishes the charge.

3. CSO did not produce any witness or the document to refute

this charge.

Arguments of defence side

CSO while denying this charge gave following reasons for such

denial-

1. It is said that cashier took out whole of cash for the first

time on 01/08/2011.

2. Cash retention limit for financial year 2011-12 is

Rs.400000/- as per document MEx-11 , which

according to CSO is a disputed document. Management side admits

that instructions of document wereapplicable from 01/04/2011 while

these were communicated to branch on 18/08/2011, then how it

can

be alleged that cashier violated the retention limit by taking

whole of cash from the safe on 01/08/2012.

3. MW7 clearly said in the answer to a question that he use to

take cash out of safe as per the demand

of the customers and instructions of the senior officer.

4. Audit conducted on 11/05/2011 and 12/05/2011 did not take

into cognizance taking out of all the

cash from the safe on certain dates prior to his joining as

branch manager of Khushal ganj branch.

5. Shri Yogesh Pandey predecessor of CSO could not reply the

question regarding cash retention limit of

branch for 2010-11 & 2011-12.

6. Bank could not provide the retention limits for the branch

for 2010-11 & 2012-13.

7. Management side could not produce any document which spell

out what is the limit for keeping cash

at the counter.

8. CSO has asked a question- if collective or demand of single

customer is more than Rs.400000/ then

what should branch do under these circumstances?

Assessment/Observation

First I would like to answer the question of CSO. If the demand

is more than Rs. 400000/ then branch

will process the withdrawal request of customer/customers and

then will pay whatever cash is available

at counter and rest of the cash along with cash for counter will

be taken out from the safe after making

proper entry in the dual cash control book. This process should

be repeated as per the cash

requirements of customers.

I would like to reproduce point 20 on page 14 of written briefs

submitted by the CSO-

-

?

. .

| . |It is clear, even if specific cash limit is not intimated

branches should adhere to general guidelines as

enumerated above and which was in the knowledge of branch

staff.

-

7/29/2019 Findings H L Yadav

7/13

CSO has targeted only one date i.e 01/08/2011 in his defence .

He is tactfully silent on other dates after

the date of MEx-11. Wrong practice by the previous manager or

omission by the auditor to point out a

wrong doing cannot be a ground for defence.

I am convinced that CSO has no control or supervision over the

cashier,who use to take entire cash

kept in the vault for daily transaction. Thus the Charge is

proved.

Article II c

Documents and oral evidence presented by PO

1 From the document MEx-2 and MEx-4 which have been verified by

the Management witness MW2

charge is self proved.

2Witness MW4 who was on deputation to khushalganj branch from

20/07/2011 to 28/07/2011 and

from 07/08/2011 to 10/08/2011 has testified on page 118 &119

that besides the period of his

deputation at Khushalganj branch nobody has signed as cashier

between the period 20/07/2011 to

05/11/2011 on the dual cash control book of the branch.

3. This charge is further proved by the cashier of branch Shri

B. K Mishra , who has himself testified on

page 167of enquiry proceedings as, dual control book

. |

INITIALS ,

| /

|

4. Since defence side has neither commented nor produced any

document to refute this charge, it isproved beyond any doubt.

Arguments of defence side

1. Bank has never issued instructions as regards to the proper

upkeep of Dual control book2. It is clear from the document DEx 7

that dual book was being maintained in the similar fashionprior to

his joining.

3. Audit report does not make any adverse remark on such upkeep

of Dual control book.4. He has mentioned certain dates on which

cashier has put his signatures on the book. Dual

control book was maintained on SB pass book and there was no

space for the initials of the

cashier.

Assessment/Observation

I am not convinced with the arguments of the CSO on the one hand

he says there were no instructions

regarding maintenance of dual control book and on the other hand

he is saying that cashier signed on

certain dates. If there were no instructions then how CSO choose

to maintain the book on SB pass book.

Who told him to draw those columns? Who told him to how and what

to write in those columns? If

there was no space for initials of cashier then how a cashier

who came on deputation ,put his initials onthe book during his

period of deputation at Khushalganj branch ? What imitative was

taken by CSO to

change the book with a new book with more space so that cashier

could have put his signatures on the

book? MW7 who was maker of this book has himself admitted that

he never put his initials on the book

and his Manager (CSO) never instructed him to do so otherwise he

could have started this practice.

(Point number 3 of POs documents and evidences mentioned

above).

-

7/29/2019 Findings H L Yadav

8/13

Therefore I find this charge as proved.

Article-II(D)

Documents and oral evidence presented by PO

1. PO presented the document MEx-5, Bait money book of the

branch. PO also presented twocirculars regarding Bait Money and

these were marked as MEx-17&18. all these documents

were verified by witnesses MW2 &MW6 respectively.2. It is

clear from the perusal of MEx-5, that predecessor of CSO, Shri

Yogesh Pandey and cashier

Shri B.K. Mishra prepared bait money using three packets of 10

rupee note on 09/10/2012. After

that no bait money was prepared by the CSO during his tenure as

Branch Manager of branch.

3. It is also clear that after 09/12/2012 bait money was

created, utilizing the two 100 rupeepackets on 31/07/2012 by the

witness MW2. MW2 also told that no bait money was handed

over to him at the time of taking charge of the branch after

CSO.

4. Document MEx clearly states-a. Bait Money packets should be

changed after every three months.b. Denomination lesser than 50

rupee note should not be used for making bait money.c. New packets

should not be used for preparing bait money.

Even after above clear instructions CSO neither replaced nor

changed the denomination of

notes used for preparing bait money.

5. CSO has himself admitted in his statement MEx13, Which has

been verified by the witness MW6that no bait money was prepared

during his tenure as Branch Manager Of the branch.

6. CSO fabricated a story and said that he prepared a register

and recorded the details of notes inthat register, because there

was no such register available at branch as is clear from the

document DEx-17. Why CSO did not mentioned this register in his

statement MEx-13.E. Even

MW7 did not collaborate any such register.

7. Even the audit report mention the making the bait money with

10 rupee note denominationinstead of 50 rupee note or higher .

8. CSO taking clue from his compliance to the audit report in

which he has remarked, . has fabricated this story and this remark

cant be relied upon

Thus charge is proved.

Arguments of defence side

1. In compliance of audit report CSO got prepared bait money of

rupee 50 denominations and recorded

in the register reference of which is recorded on page 179 of

proceedings of this enquiry.

2. CSO relied upon the statement of MW7 in which he said, :

Assessment/Observation

I am not at all convinced with the arguments of the defence

side. In the defence of previous charge CSO

was saying there were no clear instructions. Now there are two

clear cut circulars regarding bait money

and still he has not complied with the instructions.

There is no mention of this new register in the statement of CSO

(MEx-13) given to Investigating officer

on 11/11/2011. Even no question was asked from MW7 in this

regard who is supposed to be maker of

this register as well as joint signatory. In fact this register

is an imagination of CSO to create a false

-

7/29/2019 Findings H L Yadav

9/13

defence after getting the copy of audit report of branch with

compliance report on 14/12/2012. He has

fabricated thisstory around his compliance remark. .Witness MW2

who joined after CSO as Branch Manager of Khushalganj branch

entered the details of

bait money prepared during his tenure in the document MEx-5

itself. Then why a question was not

asked from the MW2 by the CSO as to why he (MW2) chose to enter

the details of fresh bait money on

the old bait money register, instead of new bait money register

started by him(CSO).Why did not CSO put a remark on old bait money

register, Continued in the new register started

from... It is painful to note that CSO concocted a false story

of starting a new bait money register to

refute the charge.

On the basis of above observations I found this charge as

proved.

Article II(e)

I am not going into much detail of this charge as CSO has not

denied that one set of keys of shutter and

channel locks used to remain with Shri Ajay Yadav, casual labour

of the branch. To quote from page

number 21 point 2 from the written briefs of defence side-

MW-5 . casual labour -

|

|It is clear that CSO has no objection in admitting that one set

of keys of locks of shutter and channel

were with casual labour Ajay Yadav. CSO is taking shelter behind

that part of statement which says that

keys were given by Shri B.K.Mishra.

If a subordinate staff is doing something which is not correct

as per systems and procedures of the

bank then should his controlling officer be a silent spectator

to his misdoing?Wht this should not beconstrued as implied consent

of CSO? Why Shri Mishra did not hand over the keys to casual

labour

during the period of Shri Yogesh Pandey?Answer is very clear,

CSO had a very casual approach as far as following systems and

procedures wasconcerned. This casual approach of CSO encouraged the

subordinate staff to take liberties in following

systems and procedures.

As a custodian of Banks property at branch level he can not be

absolved from his responsibility

Therefore I find this charge as proved.

Article II(f)

I have gone through the written briefs submitted by both the

sides and find as follows-

1. Management side has tried to prove this charge on the basis

of oral and written evidences ofwitnesses MW5 & MW7 .

2. In his defence CSO has tried his best to malign the

credibility of witnesses MW5&MW7. Accordingto him both of them

were accused in the case of theft of Banks money. Since he filed

the FIR on

the basis of which both were arrested and jailed. Naturally both

of them have grudges against the

CSO and will testify before the enquiry board with a biased mind

. Therefore their evidence either

oral or written should not be relied upon.

3. I wish to explore the oral evidence of witness DW1, which

according to defence side waseyewitness of events happened on

5/11/11 at Khushalganj branch. At this juncture I wish to

remind the defence side that CSO could produce the witness DW1

on the basis or oral evidence of

MW5 alone. Otherwise it could have been impossible for the

defence side to prove the presence of

-

7/29/2019 Findings H L Yadav

10/13

DW1 in the branch on 05/11/2011. Can defence side be selective

in accepting some portion of oral

evidence of MW5 and rejecting the remaining on the basis of lack

of credibility of the witness?

(page number 137MW5 replying a question of CSO.

)4. Now extracting some portions from the oral evidence of

witness DW1-

, , | .

|

-..... |

|

-..... ,

|

|

- // |

-...... , |From the foregoing evidence it is clear that on

05/11/2011 CSO did not accompanied the cashier

to strong room for lodging the cash in the safe. It may be

disputed whether Ajay Yadav took the

Managers key or Shri Mishra but one thing is abundantly clear

that CSO did not accompaniedthe cashier to the strong room on

05/11/2011. For knowing what happened inside the strong

room we have to rely on the statements and oral evidences of

Shri Ajay Yadav(MW5) and Shri

B.K. Mishra(MW7) because from the place ( before the CSO)

he(DW1) was sitting he could not

have observed the activities of Shri Mishra & Shri Ajay

Yadavinside the locker room.

I find this charge as proved

Article II(f)P PO has mainly relied on the written and oral

evidences of Shri Ajay Yadav & Shri B.K. Mishra for

proving this charge .According to CSO this charge is vague.

According to him PO has relied on thestatements of Shri Mishra

& Shri Ajay Yadav, who conspired to commit theft, and are main

accused

in the case. PO has misrepresented the facts as enumerated in

document MEx -15 to prove the

charge which is against the established procedures of Law.CSO

also said that PO failed to put before

the Enquiry board any circular/instructions regarding proper

control over Master Key.CSO also said

that no specific date has been mentioned in the charge.

MEx 25 states-

-

7/29/2019 Findings H L Yadav

11/13

. ( )

|

|

. |

Are these instructions not adequate? When CSO took over the

charge of branch he must have beenhanded over the master key of the

safe. Why he was not handed over the cashiers safe keys?

Reason is obvious; he was handed over the Master Key of the safe

because he was the new

custodian of it.

There are only three witnesses who can testify as to what the

practice was regarding the safe

custody of master key by its custodian, Shri Ajay Yadav, Shri

B.K. Mishra and CSO himself. If we keep

Shri Ajay Yadav and Shri B.K.Mishra away from this enquiry, then

,the CSO cannot be forced to give

evidence against him, then who will tell us the truth?

Even the witness DW1produced by the defence side clearly said

that on 05/11/2011 and on other

days when he was in the branch to withdraw cash, cashier use to

take managers master key to open

cash.

Circular 2/89 dated 19/09/2007 issued by the administration and

services department of headoffice which is placed before the

enquiry board as document DEx-25, clearly prohibits even the

travelling by the key holders together leave alone holding of

both the safe keys by a single person.

Once CSO hands over the keys to his cashier who was not

authorized to hold that master key, he

had practically no control over the key, so as to know who is

handling the master key,Shri Mishra or

the casual labour.

To know the truth I am compelled to allow the written and oral

witnesses of MW5 & MW7 . On the

basis of these written and oral evidences I find this charge as

proved.

Article III

It is painful to note that PO has once again relied on the

document MEx-28 which was disallowed

by me after much discussion and careful deliberation. If P.O was

not convinced he could haverepresented once again against my

ruling. But once document was disallowed, to rely on that

document to prove the charge, is neither acceptable nor in good

spirit.

PO has relied upon oral evidences of witness MW5,6&7 and

documents MEx15,16 &25 to prove

the charge.

CSO on the other hand termed documents MEx15, MEx-16 and MEx-28

as disputed and irrelevant

documents.

I wish to say-

1.On 05/11/2011 CSO does not accompanied the Cashier Shri Mishra

to strong room for lodging

cash. As per his own statement MEx-13, which has been verified

in the enquiry by witness MW6- //

|

- |

|As per CSO there was some difference in the cash books and he

started tallying the entries with

the vouchers. In the meantime Shri Mishra took CSOs safe key

from his drawer and entered the

strong room. By the time CSO was free from tracing the

difference Shri Misra and daily wager were

coming out of the strong room after locking the safe. What step

was taken by the CSO to ensure

that cash safe was properly locked?

-

7/29/2019 Findings H L Yadav

12/13

2.To quote once again from document MEx-13,Daily wager

| I havealready observed,

Once CSO hands over the Master key to his cashier who was not

authorized to hold that key, he

had practically no control over it, so as to know who is

handling the master key,Shri Mishra or thecasual labour.

3. MEx-13- |I am of the firm opinion that a little vigilant

approach in complying with the system and

procedures of the bank by CSO could have avoided the happening

of the incident.

I find this charge as proved.

CSO has raised certain other issues besides defending the

charges on which I would not like to

comment because I find these issues beyond my jurisdiction. CSO

also raised certain new issues and

facts in his written brief. I have not taken cognizance of these

new issues and facts.

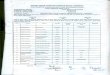

Article of charge wise Summary of findings

This report is submitted

Date-18/06/2013 Yours Faithfully

(Vikas Chandara Agrawal)

Senior Manager&

Enquiry Officer

Charge Number Proved not proved

1. Proved

2(a) proved

2(b) Proved

2(c) proved

2(d) proved

2(e) Proved

2(f) proved

2(g) proved

3. proved

-

7/29/2019 Findings H L Yadav

13/13

Enclosures-

1. All the original Management Exhibits and Defence Exhibits

2. Copies of correspondence with CSO and PO

3. Proceedings of the Departmental Enquiry in original from page

number 1 to 206.

4. Written Brief of PO dated 08/04/2013 from page number 1 to

24

5. Written Brief of CSO dated23/04/2013 from page number 1 to 28

along with 4 annexure

(Vikas Chandara Agrawal)

Senior Manager

&

Enquiry Officer