Embed Size (px)

Citation preview

FinScope MSME Survey Mozambique 2012

Table of contents

Acknowledgements 1

List of figures 2

List of tables 3

List of case studies 3

Acronyms and abbreviations 4

Definitions 5

Executive summary 7

1 Introduction and background 8

1.1 Background to the FinScope MSME study 8

1.2 Methodology of the study 9

2 Country context: MSMEs and the financial sector in Mozambique 11

2.1 Socio-economic context 11

2.2 MSME support 11

2.3 Financial services sector 12

3 Overview of the size and scope of the MSME sector in Mozambique 13

3.1 MSME owners 14

3.2 Employees 18

3.3 Nature of businesses 19

4 Financial inclusion 23

4.1 Overview 23

4.2 Banking 28

4.3 Borrowing and credits/loans 30

4.4 Savings and investments 33

4.5 Insurance and risk management 34

5 Key challenges 36

5.1 Starting the business 36

5.2 Operation and management 38

5.3 Growing the business 39

6 Conclusions and recommendations 41

6.1 General recommendations 41

6.2 Financial inclusion specific recommendations 44

Appendix A: Survey methodology and approach 46

Appendix B: Analytical framework for financial inclusion 50

1

Acknowledgements

This report was written jointly by ICC Mozambique Lda and FinMark Trust (FMT).

FinScope MSME Mozambique was designed to involve a range of stakeholders engaging in a comprehensive consultation process,

thereby enriching the survey and ensuring appropriateness and buy-in. We would like to thank all individuals who participated in this

project in their personal and institutional capacity, without which the project would not have been successful.

The survey was carried out under the auspices of the Ministry of Finance and funded by the German Development Cooperation

through the KfW Development Bank (KfW).

A Steering Committee chaired by the Ministry of Finance was set up which comprised representatives from the of the Ministry of

Finance (Piedade Macamo, Deputy National Director of Treasury and Emília Coutinho), FinMark Trust (Sabine Strassburg and Jabulani

Khumalo), the FSTAP Coordinator (Gabriel Mambo), Bank of Mozambique (Esselina Mausse and Esmeralda Fumo from the Foreign

and Research Department, respectively), Instituto Nacional de Estatistica – INE (Saide Dade, Director of National Accounts and General

Indicators), Ministry of Planning and Development (Finório Castigo from the Research Department), IPEME (David Matambo from the

Research and Statistics Department), the Confederation of Business Associations of Mozambique – CTA (Otília Pacule), as well as the

FMT Local Project Coordinator (Tânia Saranga) who coordinated the entire project locally which ensured the smooth running of all

survey stages. These stakeholders performed an integral role in the design of the survey questionnaire and provided valuable insight

into the MSME sector in Mozambique.

Further, we would like to thank INE for their vital contributions (especially Saide Dade and Carlos Creva) in providing statistical oversight

of the survey, including sampling and weighting of the data. In addition, INE played an important role in the training of the enumerators

and the quality control process during fieldwork.

Last but not least we would like to acknowledge the research suppliers GfK Intercampus (Luis Couto and team – fieldwork) and ICC

(Henriqueta Hunguana and team – analysis) who implemented the survey, and thank their staff including their supervisors and

coordinators, provincial supervisors, team leaders and enumerators, as well as the office staff who worked tirelessly on this survey.

Republic of Mozambique

2

List of figuresFigure 1: Methodological overview 10

Figure 2: Key statistics (World Bank) 11

Figure 3: MSME sector in Mozambique – overview 13

Figure 4: Distribution of the MSME owner population by province 14

Figure 5: Percentage of MSME owners among the total adult population by province 15

Figure 6: Distribution of MSME owners by location and gender 15

Figure 7: Distribution of MSME owners by levels of education 16

Figure 8: Distribution of MSME owners by source of skills acquirement 16

Figure 9: Distribution of MSME owners by monthly income 17

Figure 10: Paid versus unpaid employees 18

Figure 11: Business sector (self-classified) 19

Figure 12: Specific business activities 19

Figure 13: Age of businesses 20

Figure 14: Main operating locations 20

Figure 15: Proportion of MSME owners with registered/licensed businesses 20

Figure 16: Reasons for not registering 21

Figure 17: Financial inclusion overview 23

Figure 18: Overlaps in product usage 24

Figure 19: Construction of the Access Strand 24

Figure 20: Access Strand by location and region 25

Figure 21: Access Strand by gender 25

Figure 22: Access Strand by province 26

Figure 23: Access Strand by business size and business type 27

Figure 24: Access Strand – country comparison 27

Figure 25: Bank status – account usage for business purpose 28

Figure 26: Key drivers for banking choice 28

Figure 27: Key barriers to having a bank account in the name of the business 29

Figure 28: Distance from business to bank 29

Figure 29: Borrowing overview 30

Figure 30: Credit Strand 30

Figure 31: Borrowing mechanisms (of those who borrow) 31

Figure 32: Reasons for borrowing (key drivers) 31

Figure 33: Reasons for not borrowing (key barriers) 32

Figure 34: Requirements to access business loan from a commercial bank 32

Figure 35: Savings overview 33

Figure 36: Savings Strand 33

Figure 37: Savings mechanisms (of those who save) 33

Figure 38: Reasons for saving (key drivers) 34

Figure 39: Reasons for not saving (key barriers) 34

Figure 40: Main risks 34

Figure 41: Reasons for not having insurance (key barriers) 35

Figure 42: Main constraints to starting the business 36

Figure 43: Finance required for starting the business 36

Figure 44: Main sources of money to start the business 37

Figure 45: Motivation to start the business versus realities 37

Figure 46: Main constraints to managing the business 38

Figure 47: Main constraints to growing the business 39

Figure 48: Perceptions of MSME owners 40

Figure 49: Need for formalisation – costs versus benefits 44

Figure 50: Sampling approach 48

3

List of tablesTable 1: Distribution of MSME owners by business type 15

Table 2: Overview of demographics – individual entrepreneurs versus business owners

with employees 17

Table 3: Profile of employees 18

Table 4: Size and scope of the MSME sector – country comparison of key statistics 22

Table 5: Questionnaire structure 47

Table 6: Sample allocation 48

List of case studiesCase study 1: Vicente, successful shoe shiner 13

Case study 2: Isabel, student selling weaves at the market 17

Case study 3: Josefina, experienced entrepreneur in the construction business 22

Case study 4: Tania, young entrepreneur 37

Case study 5: Cacilda, versatile business woman 40

4

Acronyms and abbreviationsAIMO Associação Industrial de Moçambique

AMOMIF Associação Moçambicana de Microfinanças

APCM Associação para Promoção do Cooperativismo Moçambicano

BAU Balcão de Atendimento Único

BSM Business Sophistication Measure

CAE Classificação das Actividades Económicas

CEMPRE Censo de Empresas

COrE Centro de Orientação do Empresário

CPI Centro de Promoção de Investimentos

CSCs Credit and Saving Cooperatives

CTA Confederação das Associações Económicas de Moçambique

DFID Department for International Development

EAs Enumeration Areas

FARE Fundo Anual de Reabilitação Económica

FDD Fundo de Desenvolvimento Distrital

FDH Fundo de Desenvolvimento da Habitação

FDI Foreign Direct Investment

FMT FinMark Trust

FSTAP Financial Sector Technical Assistance Project

GDP Gross Domestic Product

GNI Gross National Income

ICC International Capital Corporation

ICT Instituto de Ciencia e Tecnologia

IFAD International Fund for Agricultural Development

INE Instituto Nacional de Estatística

INNOQ Instituto Nacional de Normalização e Qualidade

INPI Instituto Nacional de Propriedade

INSS Instituto Nacional de Segurança Social

IPEME Instituto de Promoção da Pequena e Média Empresa

IRPC Imposto sobre o Rendimento de Pessoas Colectivas

IRPS Imposto Sobre Resndimento de Singulares

ISPC Imposto Simplificado para Pequenos Contribuintes

KfW KfW Development Bank (German Development Bank)

M&E Monitoring and Evaluation

MFIs Microfinance Institutions

MFSDS Mozambique Financial Sector Development Strategy

MIC Ministério da Indústria e Comércio

MSME Micro, Small and Medium Enterprises

PARP Plano Anual para a Redução da Pobreza

PDRHCT Plano Estratégico de Formação e Desenvolvimento de Recursos Humanos para a Área de Ciência e Tecnologia

PPS Probability Proportional to Size

PRONASAR Programa Nacional de Abastecimento de Água e Saneamento Rural

PSAA Pequeno Sistema de Abastecimento de Água

RFSP Rural Finance Support Program

ROSCA Rotating Savings and Credit Associations

SGs Savings Groups

UKaid United Kingdom Department for International Development

UN United Nations

UNAC União Nacional de Camponeses

UNCTAD United Nations Conference on Trade and Development

VAT Value Added Tax

5

Definitions

TERM DEFINITION

Access Strand A measurement of financial inclusion across the formal-informal institutional provider continuum

Adults Those people aged 18 years or older

Banked Individuals using one or more traditional financial products supplied by commercial banks

Credit Obtaining funds from a third party with the promise of repayments of principal and, in most cases,with interest and arrangement charges in exchange for the money

Demand-side barriersDemand-side barriers to access financial services relate to characteristics inherent to individualsthat prevent them from using financial services such as perceived insufficient income, low levels offinancial literacy and lack of trust in financial institutions

Enumeration Area (EA)

Enumeration area (EA) is a well identified territorial unit containing the prescribed population size(usually about 80 to 120 households) in which enumeration is to be carried out by a singleenumerator within a specified period of enumeration. Each EA has a unique 10 digit geo-codethat reflects the province, district, ward and land use sector in which it is located

Formal other Financial products/services supplied by formal financial institutions which are not banks

Formal productsProducts provided by government regulated financial institutions such as commercial banks,insurance companies and microfinance institutions

Formally includedMSME owners using formal financial products supplied by institutions governed by a legalprecedent of any type. This is not exclusive usage, as these individuals may also be using informalproducts

Financial access landscapeA measurement of usage of both formal and informal products across the four main productgroups: transactions, savings, credit and insurance

Financially served MSME owners using one or more formal and/or informal financial products/services

Financially excluded MSME owners who are not using any formal or informal financial products/services

Financial inclusionThe extent to which the adult population in the country engages with financial products andservices, such as savings, transaction banking, credit and insurance, whether formal or informal

Informal productsFinancial services provided by individuals and/or associations which are not regulated bygovernment such as savings clubs and private moneylenders

Informally only servedMSME owners who are not using any formal financial products but who are using one or morefinancial products/services supplied from an informal source, such as a savings club or informalmoneylender

Informally servedMSME owners who make use of informal financial products (regardless of whether or not theyuse formal financial services and products)

Note: Some graphs add up to more than 100% due to multiple mentions, i.e. the respondent could give more than one answer. As

such, the graph includes overlaps in responses and cannot be added to 100%.

6

TERM DEFINITION

MSME

Micro, small and medium enterprises (MSMEs) are defined by the number of employees(according to the “Estatuto Geral das MPMEs” approved by the Council of Minsters Decree no.44/2011 of September 21st). This includes individual entrepreneurs (without any employees),micro businesses (with 1 to 4 employees), as well as small businesses (5 to 49) and medium-sizebusinesses (50 to 100 employees). For the purposes of this survey, the term MSME includesformal and informal businesses. Informal businesses refers to enterprises that are not registeredand/or licenced with any government institution within Mozambique. MSMEs also includeagricultural activities if 50% or more of the produced goods are sold.

InsurancePayment of a premium for risk of an event happening, where payout is made if or when the eventoccurs

Rural Rural area is the territorial zone not covered by the 23 cities (Resolution No. 7/87) and 68 urbanvillages / towns (Resolution 9/87)http://www.ine.gov.mz/documentacao/classificadores

Savings Safeguarding and accumulating wealth for future use

Supply-side barriersSupply-side barriers to access to financial services relate to factors inherent to financial serviceproviders that prevent individuals from using their services such as location of access points andthe cost of using their services

TransactionalFinancial services that use cash or other means (such as cheques, credit cards, debit cards or otherelectronic means) to send or receive payments

7

Executive summaryThis report provides a synthesis of the findings from the FinScope MSME Survey, which was carried out in Mozambique in 2012. Thisstudy was initiated by the Ministry of Finance and FinMark Trust, with funding provided by the German Development Cooperationthrough the KfW Development Bank (KfW). The primary aim of the research was to describe the micro-, small-, and medium- businesssector in Mozambique as well as the key challenges MSME owners face (with particular focus on their financial service’s needs) – andas such close the information gap, which exists especially for unregistered businesses (mainly individual and micro-entrepreneurs).These MSME owners may be identified under the General Statutes of Small and Medium Enterprises and also extend to the informalsector – individuals that are not formally registered. This information helps to identify and design appropriate support programmesfor the whole sector, determining policy direction and relevant financial products and services to address the needs of the MSMEowners in Mozambique.

The survey involved a comprehensive listing exercise and interviewing a nationally representative sample of 3 429 MSME owners (18years and older, including those who employ 100 people or less, as well as individual entrepreneurs without any employees). Turnoveris also included under the General Statutes of Small and Medium Enterprises for their classification, however for the purposes of thisstudy, turnover was not used as a selection criteria due to high subjectivity and reluctance to disclose reliable income figures.

This research report provides an overview of the project, its topline findings and the issues arising from the study. In particular itprovides an insight and contributes to the understanding of critical factors impacting small-scale entrepreneurial activity in Mozambique.

Key take-outsPEOPLE: An estimated 5.4 million people work in the MSME sector in Mozambique, including 4.5 million MSME owners (18 yearsand older) and about 850 000 employees (any age). That means that almost every second adult in Mozambique engages in MSMEactivities1. The employees are mainly male (75%), but unpaid workers are mainly female. The MSME owners are usually young (41%are 30 years or younger), mainly male (60%), with basic levels of education (85% have primary education or less), and are usually headof households (75%). Often, the entrepreneurial activity is the only source of income (84%). The main motivation to start the businessis driven by need, meaning the businesses are survivalist rather than opportunistic. Although business owners have largely positiveattitudes towards the business, many are worried about sustainability. MSME owners usually work long hours but have low levels ofincome.

BUSINESSES: The 4.5 million MSME owners own an estimated 4.9 million businesses (meaning, some business owners havemore than one business). They are mainly individual entrepreneurs (without any employees – 93.3%) and microbusinesses (1 – 4employees – 6.6%). The sector is driven by wholesale and retail (44%), as well as agricultural activities, forestry and fishing (22%). Mostof the businesses are located in the rural areas (87%), and operate mainly from residential premises (46%). They are largely informal(not registered – 89%) and relatively young (mainly start up and growth phase, 66% are in operation for 5 years or less).

FINANCIAL INCLUSION: About 25% of MSME owners are financially included, meaning they use/have financial products/servicesto manage their business finances (formal and/or informal). This means that 75% of MSME owners are financially excluded, i.e. theydo not use any financial products/services (neither formal nor informal) to manage their business finances. Only 11% are served byformal institutions (bank and other formal non-bank). The informal sector pushes out the boundaries of inclusion as 18% MSMEowners use informal mechanisms (e.g. savings groups) to manage their business finances. A total of 46% of MSME owners save(mainly at home), but only 5% borrow money (mainly from family and friends). Main drivers for savings and borrowing relate togrowing/expanding the business. Main barriers, in turn, relate to monetary reasons (low/irregular income). Although MSME ownersface a number of risks, most are not insured (99%). Financial inclusion is higher among small and medium size businesses, women, amongservice providers, as well as in urban areas and main urban centres (Maputo Cidade).

CHALLENGES: Main challenges reported by MSME owners relate to access to finance/sourcing money (i.e. mobilizing funds),infrastructure and sales/marketing. The following challenges affect financial inclusion: accessibility/proximity in rural areas (banks aretoo far away), affordability (income from MSME is too low/irregular, bank charges are too high, insurance is too expensive), andappropriateness (many MSMEs lack required formality and documentation such as business address and financial records to open abank account). Other challenges include limited use of sophisticated marketing strategies, and the fact that many businesses arenecessity driven (rather than opportunistic) which affects growth and sustainability of the businesses.

1 MSME owners aged 18 years and older and employees aged 16+ = Total 5,4 million people (about 49% of Mozambique’s adult population)

8

1 Introduction and background1.1 Background to the FinScope MSME study

It is widely acknowledged that micro-, small-, and medium-enterprises (MSMEs) are significant contributors to job creation,development and poverty alleviation. Given the crucial role of MSMEs in the national economy, it is in the common interestto harness and optimise this potential by putting into place strategies to mobilise and enable MSME growth and development.To do so, it is imperative that these interventions are targeted and evidence-based. However, the lack of accurate and reliableinformation about the sector and the challenges it faces, have been identified as the key constraints in achieving this objective.

It is in pursuit of this objective that the Ministry of Finance with support from the KfW and FMT initiated the FinScope MSMESurvey Mozambique 2012.

The FinScope MSME Survey is a nationally representative survey developed by FinMark Trust focusing on MSME owners andtheir financial services’ needs. The aim of this survey is to build a comprehensive body of evidence. The objectives of theMozambique FinScope MSME Survey include the following:

n To assess the size and scope of both formal and informal micro-, small-, and medium-enterprises (MSMEs) in Mozambiquen To describe the levels and landscape of access to financial products and services (both formal and informal)n To identify the most binding constraints to MSMEs development and growth with a focus on access to financial marketsn To identify and describe different market segments with specific development needs in order to stimulate segment-related

innovationn To propose recommendations regarding financial assistance to MSMEs and financial policies

FinScope MSME Mozambique was designed to engage a broad range of stakeholders in a comprehensive and intensiveconsultative process. This process has enriched the survey and the shared results have contributed meaningfully to memberswho have a common interest in MSME development and financial inclusion, as well as to the overall growth and developmentof the country. The study was funded by the German Development Cooperation through the KfW Development Bank (KfW),and implemented by GfK Intercampus (fieldwork) and ICC (analysis) with the support of INE and FinMark Trust. A SteeringCommittee chaired by the Ministry of Finance was set up which comprised representatives from the Ministry of Finance,FinMark Trust, the FSTAP Coordinator, Bank of Mozambique, Instituto Nacional de Estatistica – INE, Ministry of Planning andDevelopment, IPEME, as well as the Confederation of Business Associations of Mozambique. These stakeholders performedan integral role in the design of the survey questionnaire and provide valuable insight into the MSME sector.

This report summarises the findings of the FinScope MSME Survey Mozambique 2012. It has been written with the followingobjectives in mind:

1. To provide background information on FinScope MSME as a tool and to describe how it can be used to build inclusivefinancial markets;

2. To provide insight on the methodology used in the FinScope MSME Survey Mozambique 2012 so that users of the surveycan understand the implementation arrangements and the rigorous approach to sampling that produced the data set;

3. To present high level findings of FinScope MSME Mozambique 2012 to enhance stakeholders’ understanding of the currentstate of financial access, and to use this understanding as a baseline to inform and guide future developments; and

4. To make recommendations to stakeholders (financial sector and policymakers) as to how to improve financial access.

Findings are reported in a manner comparable to FinScope reports in other countries. However, there is a wealth of data containedin this survey that has not been covered in this report. It is therefore recommended that stakeholders review the data available to seehow it can help them to address financial and development questions that are significant to them.

This report is complemented by a brochure and a launch presentation.

9 2 Note: The term ‘employees’ here includes all people working in the business – both paid and unpaid (excluding the business owners).

About KfWThe KfW German Development Bank is Germany's leading development bank and is an integral part of KfW Bankengruppe.Together with other countries, the organisations of the international community and local institutions, KfW helps people indeveloping and emerging nations to make lasting improvements to their basic conditions of life and to protect the climate. Assuch, KfW works worldwide to implement development cooperation programmes and projects for the Federal Ministry forEconomic Cooperation and Development (BMZ), the European Commission, and other Governments in various countries.In large, the requisite funds for the promotion of developing countries are allocated from the German Federal budget. Inaddition, KfW raised additional resources on the capital markets and deploying these for the development and climateprotection finance. Financial know-how is matched by long-standing development-policy expertise providing technical assistanceand know-how from diverse disciplines to drive dialogue with local partners and provide advice to the Federal Government.

About FinMark TrustFinMark Trust, an independent trust based in Johannesburg, South Africa, was established in March 2002 and is funded primarilyby UKaid from the Department for International Development (DFID) through its Southern Africa office. FinMark Trust is anot-for-profit independent trust whose purpose is ‘Making financial markets work for the poor, by promoting financial inclusionand regional financial integration’. In pursuit of its purpose, FinMark Trust supports institutional and organisational developmentwhich increases access to financial services in Africa, by conducting research to identify the systemic constraints that preventfinancial markets from reaching out to poor consumers and MSME owners, and by advocating for change on the basis ofresearch findings.

About the FinScope MSME SurveyThe FinScope MSME Survey is a research tool developed by FinMark Trust focusing on small businesses and their financialservices’ needs. It was first piloted in South Africa in 2006 and since then the survey methodology has been applied in Zambia(2008), South Africa (2010), Tanzania (2010), Malawi (2012), and Zimbabwe (2012).

1.2 Methodology of the studyIn this survey, MSMEs are defined by the number of employees (according to the “Estatuto Geral das MPMEs” approved by

the Council of Ministers Decree no. 44/2011 of September 21st) including individual entrepreneurs (0 employees),

microbusinesses (1 to 4 employees), as well as small- (5 to 49) and medium-size businesses (50 to 100)2. For this study, MSMEs

also include informal businesses which refers to enterprises that are not registered or licenced with any government institution

within Mozambique. A nationally representative sample of MSME owners was drawn, including those who:

n Are 18 years or older ;n Perceive themselves to be business owners/generating an income through business activities; andn Employing 100 people or less as well as entrepreneurs without any employees.n Turnover was not used as a selection criteria due to the high subjectivity and reluctance of respondents to disclose reliable

income figures.

FinScope MSME Survey Mozambique 2012 is representative on national, urban/rural, and provincial levels. The sample frameand weighting of the data was conducted by INE based on the Master Sample 2010 (updated Census 2007 data). A total of523 Enumeration Areas (EAs) were sampled using probability proportional to household size (PPS), including 162 urban and361 rural areas. All households in the selected EAs were then listed. As such over 54 000 households were listed. Within thehouseholds, all MSME owners were identified (18 years and older, employing 100 people or less, as well as individualentrepreneurs). Within each selected EA, six to eight qualifier households (with MSME owners) were systematically selectedfrom the listed MSMEs. Within the selected households, where there was more than one business owner, a Kish Grid was usedto randomly select the qualifying household member with whom to complete the interview (this individual was the ultimatesampling unit). A total of 3 429 interviews with MSME owners were conducted during September to December 2012 by GfKIntercampus. In addition, a number of in-depth interviews were conducted with MSME owners to generate case studies which complementthe survey findings.

10

The table below provides a summary of the methodology applied.

Logistics Details

Methodology Face-to-face, pen and paper interviews were conducted among MSME owners inMozambique

Definition of MSME owners

Survey of MSME owners, defined as individuals who are:

n 18 years or older

n Perceived themselves to be business owners/generating an income through businessactivities

n Employing 100 people or less, as well as individual entrepreneurs without any employees

n Turnover was not used as a selection criteria due to the high subjectivity and reluctance ofrespondents to disclose reliable income figures.

Sample sizen=3 429, representative on national, urban/rural, and provincial levelSample drawn by INE based on the Master Sample 2010 (updated Census 2007 data)

Sampling frame Listing exercise, population stratified by location (urban/rural)

Sample area selection523 Enumerator Areas (EAs) were selected using probability proportional to size (PPS),interviews were conducted in 162 urban and 361 rural EAs

Household qualification 6 – 8 households were selected from each EA using systematic random sampling

Respondent selection Final respondent to interview was selected using a Kish Grid

Questionnaire length ± 75 minutes

Fieldwork September to December 2012

Quality control and datamanagement

Field checks and quality control checks conducted by GfK, FMT, and INE, data capturing inSPSS, weighting was done by INE, data validation against Census data 2012

ImplementationThe study was implemented by GfK Intercampus and ICC with support from INE and FinMarkTrust

Funding partnersThe study was funded by the German Development Cooperation through theKfW Development Bank

Figure 1: Methodological overview

11

2 Country context: MSMEs and the financial sector inMozambiqueThis section is based on a literature review conducted by the Local Project Coordinator Tania Saranga, and ICC contextualisingthe financial and MSME sector in Mozambique. It contains an overview of a range of financial services and mechanisms availableto MSMEs in Mozambique, including both formal and informal mechanisms. An understanding of the structure of the financialservices system in Mozambique is critical to the understanding of the state of financial inclusion in Mozambique. The tablebelow summarises other key statistics from Mozambique.

3 Source: http://www.worldbank.org/en/country/mozambique 4 Available online at URL: http://www.imf.org/external/pubs/ft/scr/2011/cr11132.pdf

2.1 Socio-economic contextPost-conflict policy interventions, economic reforms, as well as substantial donor support and Foreign Direct Investment (FDI)has led to robust growth in Mozambique. Despite considerable improvements, the Mozambican economy has undergoneminimal structural transformation. The country is still characterised by low levels of education, widespread poverty and highlevels of unemployment, as well as deficient infrastructure and basic services, especially in the rural areas where the majorityof the population resides.

In response to these challenges, the government restructured its development agenda around an Action Plan for ReducingPoverty (PARP 2011 – 2014)4, focused on increased agricultural production, promotion of employment linked to thedevelopment of micro-, small- and medium-size enterprises (MSMEs) and investment in human and social development.

2.2 MSME supportThere are a number of strategies to support the formal MSME sector. However, these efforts by the government have positivespillover effects to informal businesses eg. the increase in the need to register and benefit from these government strategies.In Mozambique, the government’s poverty reduction strategy (PARP 2011:17ff), for example, aims to support MSMEs by:

n Creating an environment favourable to the creation and development of MSMEs and the attraction of domestic and foreigninvestment into labour-intensive industries;

n Ensuring comprehensive access to credit and services for the support and development of MSMEs;n Promoting linkages between small and big firms, with particular emphasis on megaprojects;n Facilitating market access (including infrastructure development);n Encouraging labour-intensive public works that will offer temporary low-cost jobs in areas such as construction and local

infrastructure maintenance; n Implementing the Human Resource Development Plan for Science and Technology (PDRHCT) in the context of

strengthening the technical and scientific capacities of MSMEs and meeting the needs of emerging industries in theproductive sectors; and

n Facilitating access to financial services in rural areas and ensuring better scope for women.

Population Key statistics

Total population 25.2 million (2012)

Total adult population (18+) 10.8 million (2012)

Life expectancy 50 years (2011)

Adult literacy (15+) 56% (2010)

GDP US$ 14.59 billion (2012)

GDP growth 7.4% (2012)

Ease of doing business rank139 out of 185 countries (2012)146 out of 185 countries (2013)

Figure 2: Key statistics (World Bank)3

12

The 2007 – 2012 SMEs Strategy defines three strategic efforts to SME development: (i) improvement of the business environment; (ii) development of technological and management capacities; and (iii) development of strategic support to SMEs.

Each of these strategic efforts implies a set of multidimensional actions. Under the ‘improvement of the business environment’effort, a few financial sector policy actions are envisioned, namely:

n Introduction of a credit guarantee system;n The implementation of a leasing system;n Encourage the use of investment funds;n Stimulate banks to increase funding and other services for SMEs;n Encourage banks to strengthen links and networks with rural credit and micro-credit institutions; andn Provision of government credit to refinance rural and micro-credit institutions.

2.3 Financial services sectorThere are 18 commercial banks registered by the Bank of Mozambique (in 2012)5, some of which provide microfinance services.The banking system lacks competition since about 75% of the total financial sector’s assets are concentrated in the threelargest banks, which are closely linked to the Portuguese banking industry.

According to the FinScope Consumer Survey Mozambique 2009, Mozambique has very low levels of financial inclusion,especially uptake of banking products and services, i.e. only 12% of the adult population (16 years and older) use financialproducts/services from a commercial bank. A total of 78% of adults do not use any financial products/services neither formalnor informal (= financially excluded). Financial exclusion is particularly high in rural areas. The strong urban bias of formalfinancial services (including microfinance), in a country where the majority of MSMEs operate in rural areas, is a particular areaof concern. As such, reaching out to the un- and under-served rural population is one of the industry’s major challenges.

The Ministry of Finance of Mozambique, with funds from the World Bank FIRST Initiative, introduced the Mozambique FinancialSector Development Strategy (MFSDS) 2011 – 2020. The pillars of the strategy include maintaining financial sector stability,supporting inclusive economic growth, developing formal financial services and rapidly expanding financial access. One of thestrategy’s focuses is the development and delivery of new financial products for rural areas through use of, for example,community based savings models to lower the costs of providing financial services to rural populations (MoF, 2011)6. In addition,the Rural Finance Strategy was introduced to improve rural finance, e.g. to expand the access to credit for rural individuals,groups and MSMEs, especially women and the poor. The strategy recognises the challenges of bringing financial services to ruralareas (perceived risk, high transaction costs, and the informality and low levels of income), but points to promising methodsfor developing the sector. It calls for continued support for accumulated savings and credit associations (ASCA’s), recognisingthat they often originate as informal groups. Additionally, the plan proposes the development of alternative models that haveworked elsewhere, namely the creation of networks of credit cooperatives by grouping associations along value chains.7

The Central Bank has also introduced initiatives to improve presence in the provinces and as such reduce the cost of cashhandling by institutions facilitating the licensing process of new branches and new institutions. The Local Initiative InvestmentBudget (Orçamento de Investimento de Iniciativa Local – OIIL or 7 bilhoes), for example, has been used to transfer money fromthe central budget to lend to projects in each of Mozambique’s 128 districts. Despite these interventions and considerableimprovements in the network coverage of financial institutions over the years (the number of districts with branches grew from27 in 2005 to 63 in 2012), many areas in Mozambique are still un- and under-served, i.e. there are still 65 districts in the countrythat are unbanked, although some of these have access to microfinance services8. Rural areas9 have only 0.6 branches per100,000 adults, compared to a national average of 4.2. Increasing the geographical spread of the banking sector remains oneof the main priorities. The goal is that 80% of all districts should have branches of financial institutions by 2016.

5 Source: http://www.bancomoc.mz/Instituicoes_en.aspx?id=GINS0001&ling=en6 Ministry of Finance (MoF), Government of the Republic of Mozambique (GRM), 2011. Mozambique Financial Sector Development Strategy (MFSDS)

2011 – 2020.7 Source: FinMark Trust 2012. The Status of Agricultural and Rural Financial Services in Mozambique. Available online at [URL]:

http://www.finmark.org.za/wp-content/uploads/pubs/Rep_statusofAgRuFin_MOZ1.pdf 8 Banco de Moçambique, Desafios da Inclusão Financeira em Moçambique – Uma abordagem do lado da oferta, February 20139 Rural areas are the territorial zones not covered by the 23 cities (Resolution No. 7/87) and 68 urban villages / towns (Resolution 9/87)

http://www.ine.gov.mz/documentacao/classificadores

Employing850 000 people (excluding MSME owners)

13

3 Overview of the size and scope of the MSME sector inMozambiqueThe size of the MSME sector in Mozambique is portrayed by a number of indicators, such as the number of MSME owners,the number of businesses they own, and the number of people they employ in their main businesses, who may or may not beregistered as a formal business in Mozambique. The following figure gives a broad overview of the sector.

There are 4.5 million MSME owners in Mozambique (18 years and older), owning 4.9 million businesses, employing a total of850 000 people (all ages, excluding the business owners themselves). As such, the sector contributes significantly to employmentwith a total of 5.4 million people working in the sector, i.e. almost every second adult in Mozambique engages in MSMEactivities10. Furthermore, it contributes to poverty alleviation as survivalist businesses play a vital role, especially as a buffer againstslipping into deeper poverty and as such reducing individual and household vulnerability.

10 MSME owners aged 18 years and older and employees aged 16+ = Total 5,4 million people (about 49% of Mozambique’s adult population)

4,5 million MSME owners

Owning4,9 million

MSMEs

Figure 3: MSME sector in Mozambique – overview

Case study 1: Vicente, successful shoe shiner

Vicente, successful shoe shiner

Vicente is 43 years old. He lives with his wife, two daughters, and his sister.Supporting a household of 5, he is the only breadwinner in the family, contributingabout MT 8 000 a month (about US$ 270). When his brother left to work in SouthAfrica, he took over his brother’s business as a shoe shiner. In addition, he workspart-time as a private real-estate agent. The business activities have helped him tomake a living for himself and his family for the last 27 years.

“I got to buy a plot of land, build my 3-bedroom house, bought the houses furniture, [and]got officially married […] all thanks to this business.”

Business Sophistication MeasureThe Business Sophistication Measure (BSM) is a segmentation tool developed by FinMark Trust to identify and describe differentmarket segments and to assess the degree of sophistication of MSMEs in Mozambique. As such, 7 groups of businesses wereidentified from a wide range of aspects measured in this survey using core questions relating to what the business had and did,rather than questions that related to a business owner’s perceptions, attitudes, opinions and/or concerns about the business.Indicators used in the segmentation include, e.g. type of the business (number of employees), nature of the business activities,registration, licensing and compliance, ownership structure and assets, financial records, type of financial services used, etc. Usingthese variables, a principle component analysis was used to create an index. The scores on the first principle component

14

obtained from these variables formed the BSM score. The higher the score, the more sophisticated is the business (accordingto the selected variables). The table below gives an overview of the BSM segments for the MSME data. Most of the businessesare in BSM 1 – 4 with about 2 in 5 of the businesses in BSM 1. Given the small sub-sample sizes for some of the BSM segments,however, further analysis of the BSMs would not be representative.

The general trend indicates that the incidence of the following variables increase slightly with higher BSM: incidence ofregistration/licence, compliance with IRPS and VAT, incidence of service providers, number of employees (businesses in lowerBSM segments tend to be individual entrepreneurs), business owners with higher levels of education, cell phones and otherbusiness assets (e.g. website, internet access, company car), and uptake of financial products/services (including credit, savings,and transactional products/services). The South (mainly in Maputo City and Province) showed a higher number of sophisticatedbusinesses compared to the Centre and North; possibly as result of proximity to South Africa and more exposure to bigenterprises. There seems to be little correlation between BSM and years of operation, as well as BSM and operating locationwith the majority of businesses operating from residential premises (except BSM 7).

3.1 MSME ownersAs illustrated below, Nampula has the highest number of MSME owners in Mozambique accounting for 22% of the totalbusiness owner population. However, comparing the number of business owners with the total adult population (18 years andolder) per province11 shows that Cabo Delgado has the highest proportion of MSME owners. Here, about 49% of adults areMSME owners which exceed the national average of 42%. Whereas Niassa province has the lowest proportion of MSMEowners (only every third adult in Niassa owns an MSME).

BSM 1 BSM 2 BSM 3 BSM 4 BSM 5 BSM 6 BSM 7

Number ofBusiness

About 1,97 million

About 750 000

About 490 000

About 480 000

About412 000

About 390 000

About 52 000

Number ofBusiness

43% 17% 11% 11% 9% 8% 1%

11 Using population figures per province from the FinScope Consumer Survey Mozambique 2009

Figure 4: Distribution of the MSME owner population by province

15

The vast majority of MSME owners (93%) are individual entrepreneurs, meaning they do not have any employees in theirbusiness (about 4.2 million) while about 7% of MSME owners employ people in their business (about 300 000). Using theMSME definition by number of employees as explained above, 6.6% of MSME owners run microbusinesses (employing 1 to 4people), while 0.7% can be classified as small businesses (employing 5 to 49 people), and only 0.02% are medium-size businesses(employing up to 100 people).12

The majority of MSME owners are male (60% are female, compared to 40% who are female) and reside mainly in rural areas13

(87% of MSME owners reside in rural areas, compared to 13% in urban areas) – which broadly reflects the distribution of thetotal adult population in Mozambique.

Table 1: Distribution of MSME owners by business type

Number of employeesPercentage of MSME owners

Estimated number ofbusinesses owners

Individual entrepreneurs 0 92.7% 4.2 million

Micro 1 – 4 6.6% 300 000

Small 5 – 49 0.7% 31 000

Medium 50 – 100 0.02% 750

12 Note: The sub-sample sizes for small and medium size businesses are very small. Further analysis would be unstable and hence is not recommended.13 Rural areas are the territorial zones not covered by the 23 cities (Resolution No. 7/87) and 68 urban villages / towns (Resolution 9/87)

http://www.ine.gov.mz/documentacao/classificadores

Figure 5: Percentage of MSME owners among the total adult population by province

Maputo Cidade

Maputo Province

Gaza

Inhambane

Sofala

Manica

Tete

Zambezia

Nampula

Cabo Delgado

Niassa

40

%

40

41

45

37

42

47

43

44

49

33

Urban/rural

13%

87%n 87% Ruraln 13% Urban

Figure 6: Distribution of MSME owners by location and gender

n 60% Malen 40% Female

Gender

60%

40%

16

Consistent with the low literacy levels in the country, the majority of MSME owners have low levels of education: 84% of MSME owners

have primary education or less (including 14% without any formal education). The majority acquired their business skills mainly informally,

taught themselves, through internal networks (family, friends, and/or other business owners) or whilst managing the business, which

indicates that a great need for business training exists.

The survey shows that 41% of MSME owners are 30 years or younger, which might indicate that they are less experienced and not

economically settled yet. At the same time, these business owners are often heads of households (75%). Thus, many started their

business to provide for their families, wanting to generate more income, escape unemployment and poverty. This needs-driven

motivation (63%), however, does not fulfil its promise as many MSME owners in fact have low levels of monthly income (56% have a

personal monthly income of less than MT 2 500 a month (equivalent to about US$ 80), 5% do not have a monthly income) even though

many work full-time, i.e. more than 8 hours a day (49%), six to seven days a week (72%). Nevertheless, survivalist businesses play a

vital role acting as a buffer against slipping into deeper poverty and as such reducing individual and household vulnerability. For 84%,

these businesses are their only source of income.

Figure 7: Distribution of MSME owners by levels of education

Superior

Formação de professores

Técnico médio

Técnico básico

Técnico elementar

Secundário esg2 (11a/12a classe)

Secundário esg1 (8a/10a classe)

Primário ep2 (6a/7a classe)

Primário ep1 (1a/5a classe)

Alfabetização

None

14.6

%

35.7

14.4

0.3

3.3

10.2

19.0

0.3

0.1

0.2

0.1

Figure 8: Distribution of MSME owners by source of skills acquirement

Taught myself

Family (other than spouse)

Whilst managing the business itself/on the job

Previous job or work experience

Mentor/advisor

Spouse

School

Training programmes/courses

University/college

55.2

%

13.7

11.6

0.6

6.9

0.1

2.2

5.5

1.0

Looking at individual entrepreneurs and MSME owners with employees separately reveals small differences in demographics as

summarised in the table below.

17

Case study 2: Isabel, student selling weaves at the market

Isabel, student selling weaves in the market

Isabel is 26 years old. She sells weaves at a stall in the market, working from 8am to 5pmevery day, and going to lectures in the evening during weekdays (studying Economics atthe university). She lives with her mother, 5 brothers, and her daughter (4 years old). Havinggrown up in a business environment, she learned a lot from her mother who has a stall inthe same market. The business is the main source of income (in addition to some rentalincome) – which pays for stall rent and taxes, contributing to household consumption, food,clothing, water and electricity, university fees, and her daughter’s kindergarten.

Figure 9: Distribution of MSME owners by monthly income14

No personal monthly income

1 – 2 500 MT

2 501 – 5 000 MT

5 001 – 10 000 MT

10 001 – 25 000 MT

Over 25 000 MT

Refused/don’t know

%

18

56

5

12

6

2

1

14 This includes all sources of personal monthly income and is not limited to the income generated by the business. Those who do not have a monthlyincome might engage in seasonal business activities (e.g. agriculture).

Business owners: 4.5 million

4.2 million (93%)Individual entrepreneurs

Over 300 000 (7%)Business owners with employees

Gender 59% are male 69% are male

Age 41% are 30 years or younger 38% are 30 years or younger

Education85% have primary education or less (including15% without any formal education)

69% have primary education or less (including13% without any formal education)

Position in the household 75% are heads of households 75% are heads of households

Sources of income85% reported that the business is their onlysource of income

70% reported that the business is their onlysource of income

93%

7%

Table 2: Overview of demographics – individual entrepreneurs versus business owners with employees

18

Employees are relatively young (84% are 30 years or younger, including 12% who are younger than 16 years) with low levels

of education (74% have primary education or less, including 21% without any formal education). The figure below summarises

the information on employees.

3.2 EmployeesThe majority of MSME owners do not have any employees (92.7%). The remaining 7.3% of MSME owners (about 300 000)employ a total of 850 000 people. About 6.6% of MSME owners employ 1 to 4 employees (= microbusinesses). The remaining0.7% employ 5 people or more (= small- and medium-size businesses)15. It is interesting to note that 30% of employees arefamily members – many of which are unpaid (79%). The majority of employees are male (75%) but the majority of unpaidworkers are female (69%). In total, 10% of employees are unpaid. Although the majority of employees are full-time paid(60%), only a quarter of all employees (25%) have written contracts. The following figure summarises some of the key statisticsregarding paid versus unpaid employees.

Figure 10: Paid versus unpaid employees

Paid in kind and money

Paid in kind/services

Temporary/seasonal/contract paid

Part-time paid

Full-time paid

Unpaid

%

8

6

4

10

12

60

850 000 Employees

Gender75% are male But 70% of unpaid workers are female

Age 84% are 30 years or younger (including 12% who are younger than 16 years)

Education 74% have primary education or less (including 21% without any formal education)

Family 30% are family members

Contracts 25% have written contracts

Table 3: Profile of employees

15 Note: This includes all people working in the business (paid and un-paid workers).

19

Specific business activities: The majority of MSME owners in Mozambique are retailers (94%) – many sell products in the

same form either that they are bought or that they have collected from nature, without adding value. Only 6% classify

themselves as service providers, providing mainly skilled services, e.g. mechanic or plumber, followed by professional services,

e.g. medical, legal and accounting services.

16 Note: Business sector classification is self-reported. Agricultural activity was taken into consideration here if 50% or more of the produced goods aresold.

17 Classification according to their main economic activitySource: CLASSIFICAÇÃO DAS ACTIVIDADES ECONÓMICAS DE MOÇAMBIQUE (CAE-REV.2) 2008

3.3 Nature of businessesBusiness sector: The MSME sector in Mozambique is largely driven by wholesale and retail as well as agriculture. About 22%of MSME owners work in agriculture16, while 44% of MSME owners reported to work in wholesale and retail. Another 12%of MSME owners work in manufacturing.

Figure 11: Business sector (self-classified)17

12%

22%

44%

7%n 44% Wholesale and retail trade

(including repair of vehicles and motorcycles)n 22% Agriculture, forestry and fishingn 12% Manufacturingn 12% Other service activitiesn 7% Other sectorsn 3% Mining and quarrying

12%

3%

Figure 12: Specific business activities

Sell something in the same form that I buy

Sell something that I buy but add value to

Sell something that I collect from nature

Grow something and sell

Sell something that I make

Sell by-products of animals

Rear livestock/poultry and sell

Sell somthing that I get for free

Render a skilled service

Render a professional service

Render other services

Render building/construction services

Render tourism-related services

%

46

7

6

2

1

1

3

1

1

0

12

19

1

Retailers94%

Service providers6%

20

Business location: Many MSME owners operate their business from residential premises (46%), indicating that there might bea lack of available and/or affordable operational space. It might also be out of choice considering the nature of the business(e.g. small, informal). A further 28% operate from a stall/table/container which relates to the high percentage of MSME ownersthat engage in wholesale and retail activities. While 16% operate as street vendors, only 3% work in a shopping mall.

Age of the business: MSMEs in Mozambique are relatively young. As shown in the figure below, the majority of MSME owners(66%) reported that their business is 5 years or younger, including 40% that are in the start-up phase (0 to 2 years in operation),as well as 26% that are in the growth phase (3 to 5 years in operation). About 15% of MSMEs are in operation for 6 to 10years and a further 19% are in operation for more than 10 years at the time of the survey.

Start-up0 to 2 years

Growth phase3 to 5 years

Established6 to 10 years

MatureMore than 10 years

40

26

1519

Figure 13: Age of businesses

Figure 14: Main operating locations

Residential premises

Stall/table/container

Street

Shopping Mall

Door to door

Mobile

Other

Farm/small holding

46

%

28

16

2

3

1

2

2

Registration/licensing: Registered companies have their name and statutes published in the Official Government Gazette andare allocated a fiscal number, whereas an operating license can be obtained at the district or municipal level. In total, only 6%of MSME owners reported that their business is registered i.e. they have “Alvara” and “Articles of Association” (mainly as soleproprietors – 78%), and 14% reported that their business is licensed (mainly with district administration 48% and localmunicipalities 22%).

Registered Not registered Do not know Licensed Not licensed

6

89

5 14

86

Figure 15: Proportion of MSME owners with registered/licensed businesses

21 18 Source: http://www.doingbusiness.org/data/exploreeconomies/mozambique#starting-a-business

According to the ‘Doing Business in Mozambique’ study conducted by the World Bank, the registration process has beenrevised and appears to be less time consuming with an average duration of 13 days. However, taking into account that about56% of MSME owners have a personal monthly income of less than MT 2 500, the registration process is still relatively expensivewith a minimum cost of MT 3 000 (= about US$ 100)18 (excluding travel expenses and other additional cost the MSME ownermight incur). This reflects the challenges raised by MSME owners who have not registered/licensed their business. The mainbarriers to registration/licence as reported by MSME themselves relate to monetary reasons (‘Business is too small’ as reportedby 30% and ‘No money to register’ 16%) and a lack of knowledge/complexity of the registration process (22% do not knowhow to register and 6% reported that it is too complicated) as shown in the figure below. As such, the majority of MSME ownersdo not comply with many regulations. For example, a very small percentage of MSME owners (4%) pay corporate, personalor employee compensation tax. Municipal tax, a requirement for an operating license, is paid by 17% of MSMEs. Only 1% ofbusinesses pay social security tax (INSS) – which indicates a huge opportunity for the Government of Mozambique.

Figure 16: Reasons for not registering

Business is too small

Don’t know how

Don’t have money to register

It is too complicated

No benefit

Don’t have time

Tried but was not successful

Registration is being processed

Don’t want to pay tax

Other

Don’t know

Refuse to answer

30

%

22

16

4

4

2

19

3

3

6

1

1

On the other hand, the perceived benefits do not seem to outweigh these challenges. Access to finance, new clients, and rawmaterials can be used as proxy for ‘real’/tangible benefits, whereas compliance with the law (as reported by 36% of MSMEowners), avoiding harassment from authorities (10%), and avoiding fines (7%) might not seem as attractive, yet was reportedby more than a quarter of MSME owners.

22

Case study 3: Josefina, experienced entrepreneur in the construction business

Josefina, experienced entrepreneur in the construction business

Josefina is 52 years old. She runs three businesses, including a construction business, a metalworkshop which produces pots, as well as a rental business. From the income of thesebusinesses, Josefina supports her 2 children and 3 grandchildren. Josefina holds a license forher construction business as this allows her to access public tenders. As such, she is alsoable to access Government support. During the floods in Xai-Xai in 2000, for example, shehelped displaced people to build new homes and received a donation of 1 800 sacks ofcement which significantly boosted her business activity.

Country comparison: Comparing Mozambique with other countries in the region shows that Mozambique has a much higherproportion of individual entrepreneurs (93%) compared to other countries in the region. On average 42% of adults (18 yearsand older) are MSME owners in Mozambique which is similar to Zimbabwe (46%), compared to 17% in South Africa (16 yearsand older), and 13% in Malawi. Levels of registration/licence in Mozambique can also be compared with those of Zimbabwe.

South Africa (2010) Malawi (2012) Zimbabwe (2012)Mozambique

(2012)

Business owners16 years and older

200 employees or less

18 years and older 100 employees

or less

18 years and older 75 employees

or less

18 years and older100 employees

or less

Estimated adult population 33,5 million 6,1 million 5,9 million 10,8 million

Estimated % of adult populationthat owns MSMEs

17% 13% 46% 42%

Number of MSME owners 5,6 million 760 000 2,8 million 4,5 million

Number of MSMEs they own 6 million 1 million 3,5 million 4,9 million

% of MSME owners withregistered/licensed businesses

17% (only CIPC)

3% 15% 6% registered 14% licensed

Number of employees 6 million 1 million 2,9 million 850 000

% of individual entrepreneurs% of businesses with employees

67%33%

59%41%

71%29%

93%7%

Table 4: Size and scope of the MSME sector – country comparison of key statistics

23

19 The analytical framework used here is explained in Appendix A.20 Note: Overlaps in product usage are taken out here, i.e. some people might use both formal and informal products/services and mechanisms to manage

their financial lives.

4 Financial inclusion19

4.1 OverviewIn total, 75% of MSME owners (about 3.4 million which are formally registered and/or informal businesses) are financiallyexcluded, i.e. they do not use any financial products or services (neither formal nor informal) to manage their business finances.If they borrow, they borrow from friends and family; if they save, they save at home. On the other hand, 25% of MSME ownersare financially included (about 1.1 million), i.e. they use financial products or services (either formal and/or informal) to managetheir business finances. While 18% of MSME owners (= 800 000) have/use informal mechanisms to manage their businessfinances, only 11% are formally served (= 500 000), including both banked and other formal non-bank products/services (9%of business owners are banked = 430 000 and 2% of business owners have/use other formal non-bank products/services =70 000). The overlaps in product usage need to be considered here. Thus, the figure below adds up to more than 100%. Theoverlaps are depicted using circles, whereas the dark blue depicts the banked, yellow describes the usage of other formal non-bank products/services, and green the uptake of informal products/services such as savings groups. Product uptake for thosewho use bank products/services is driven by bank savings and transaction products. While other formal non-bankproducts/services are driven by credit and savings products, informal mechanisms are also largely driven by savings (e.g. savingsgroups), particularly among female MSME owners.

Figure 17: Financial inclusion overview

Banked9% (430 000)

Driven by transactions andsavings

Served by other formal financial institutions 2% (70 000)

Driven by credit and savings

Financially excluded 75% (3,4 million)

Informally served 18% (800 000)

Driven by informal savings

Formally served 11% (500 000)

Total business owner (BO) population100% (4,5 million)

Financially included25% (1,1 million)

Formally served

Banked

Other formal

Informal

Excluded

11

%

9

2

18

75

Product uptake is driven by

n Bank savings and transaction productsn Credit and savings productsn Informal savings products

24

BankedOther formal

Informal

Excluded

5.5 0.6 1.0

0.5

0.2

3.2

14.1

74.9

Figure 18: Overlaps in product usage

Figure 19: Access Strand – MSME and Consumer Survey comparison

9 75

78

2 14

12 1 9

n Banked n Formal other n Informal only n Excluded

In calculating the Access Strand, the overlaps are removed and a hierarchical approach is used in order to depict:

n The percentage of business owners who are banked (banked) – identifying business owners using commercial bankproducts. This is not necessarily exclusive usage – these individuals could also be using financial products from other formalfinancial institutions or informal products as well as bank products = 9%

n The percentage of business owners who are formally served but who are not banked (other formal) – identifying businessowners using financial products from formal financial institutions which are not commercial banks such as microfinanceinstitutions or insurance companies. This excludes bank usage, but is not exclusive in terms of informal usage – thesebusiness owners could also be using informal products = 2%

n The percentage of business owners who are not formally served but who are informally served (informal only) – businessowners using informal financial products or mechanisms only. This is exclusive informal usage and does not include businessowners who are within the banked or other formal categories of the access strand that also use informal services = 14%

n The percentage of business owners who are excluded/un-served – business owners using no financial products to managetheir financial lives – neither formal nor informal and depend only on family/friends for borrowing and save at home if theysave for business purposes = 75%

FinScope MSMEMozambique 2012

FinScope ConsumerMozambique 2009

As shown above, informal financial mechanisms play a vital role for MSME owners in Mozambique, pushing out the boundariesof financial inclusion.

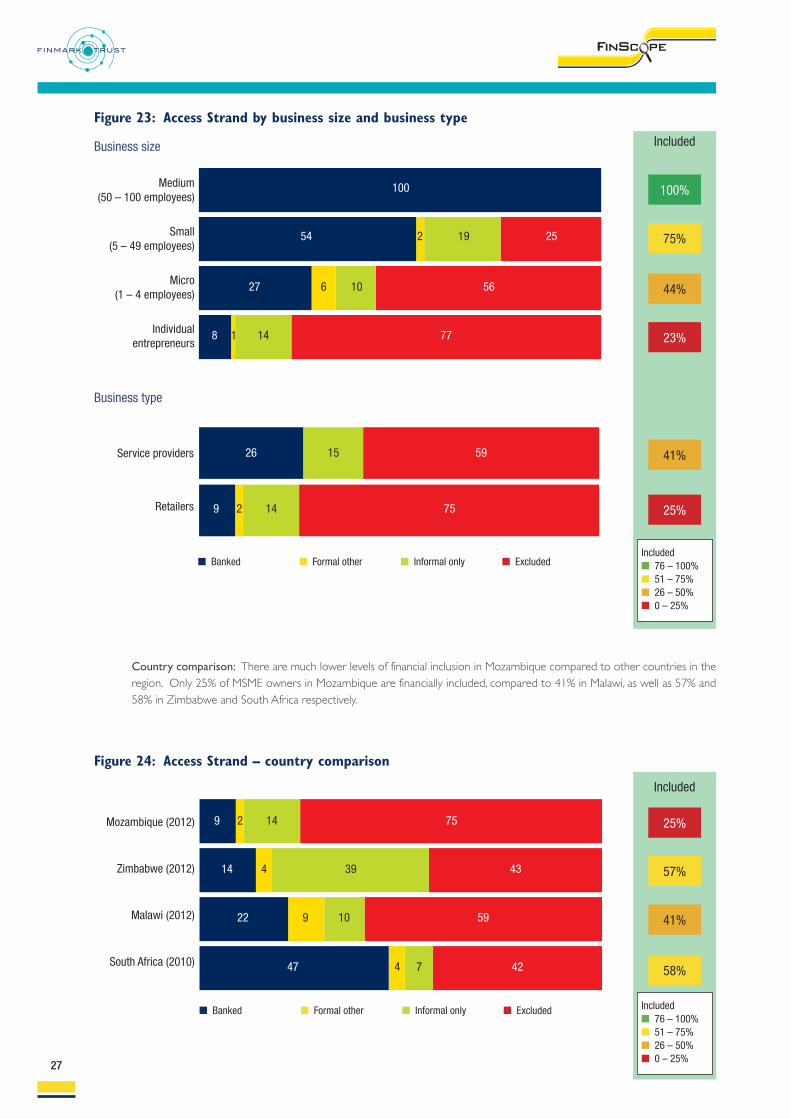

Comparing the Access Strand across location, provinces, business size, and gender reveals that levels of financial inclusion arehigher:

n In urban areas (61%) compared to rural areas (20%):n In the South such as Maputo Cidade (80%) compared to provinces in the Nampula (12%):n Among medium-size businesses (100%) compared to small- (75%) and micro-businesses (44%), as well as individual

entrepreneurs (23%);n Among service providers (41%) compared to retailers (25%); andn Among women (35%) compared to men (19%).

25

Rural

Urban 24 39361

7 802 11

South

Centre

North

8 8381

7 8571

18 442 36

Included

20%

56%

17%

15%

61%

Includedn 76 – 100%n 51 – 75%n 26 – 50%n 0 – 25%

Figure 20: Access Strand by location and region

Rural/urban

Region

n Banked n Formal other n Informal only n Excluded

n Banked n Formal other n Informal only n Excluded

Male

Female 11 65222

8 812 9

Included

19%

35%

Includedn 76 – 100%n 51 – 75%n 26 – 50%n 0 – 25%

Figure 21: Access Strand by gender

Gender

26

Included

80%

35%

62%

25%

45%

41%

17%

19%

16%

12%

10%

Includedn 76 – 100%n 51 – 75%n 26 – 50%n 0 – 25%

Maputo Cidade

Manica

Maputo Province

Niassa

Gaza

Inhambane

Tete

Sofala

Cabo Delgado

Nampula

Zambezia

34 20442

18 65134

17 38441

14 7574

12 55294

11 59291

9 8371

8 81101

6 8410

5 8861

3 9061

Figure 22: Access Strand by province

n Banked n Formal other n Informal only n Excluded

27

n Banked n Formal other n Informal only n Excluded

Included

100%

44%

23%

41%

25%

75%

Includedn 76 – 100%n 51 – 75%n 26 – 50%n 0 – 25%

Figure 23: Access Strand by business size and business type

Business size

54 25192

27 56106

8 77141

100Medium (50 – 100 employees)

Small (5 – 49 employees)

Micro (1 – 4 employees)

Individualentrepreneurs

Business type

Service providers

Retailers 9 75142

26 5915

Country comparison: There are much lower levels of financial inclusion in Mozambique compared to other countries in theregion. Only 25% of MSME owners in Mozambique are financially included, compared to 41% in Malawi, as well as 57% and58% in Zimbabwe and South Africa respectively.

n Banked n Formal other n Informal only n Excluded

Included

57%

25%

58%

41%

Includedn 76 – 100%n 51 – 75%n 26 – 50%n 0 – 25%

14 43394

9 75142

22 59109

47 4274

Mozambique (2012)

Zimbabwe (2012)

Malawi (2012)

South Africa (2010)

Figure 24: Access Strand – country comparison

28

4.2 Banking The majority of MSME owners do not use any products or services from a commercial bank (90.5%). Only 9.5% of MSMEowners use products/services offered by a commercial bank and only 0.3% use an account in the name of the business.

Do not use a bank account at all

Use a personal account but notmainly for business banking

Use personal bank account mainly for business banking

Use a bank account which is in the name of the business mainly for business banking

Use someone else’s bankaccount mainly for business banking

%

4.6

4.4

0.3

0.2

90.5

4,9%

use a bank accountmainly for business

purposes

Figure 25: Bank status – account usage for business purpose

Banking is largely driven by savings and cash related transactions (withdrawals and deposits). Cash withdrawals and depositsaccount for 44% of all transactions. Mozambique is a largely cash based economy: 94% of MSME customers make theirpayments in cash and 93% of business owners pay their employees in cash.

Drivers: The main reasons given for opening a bank account in the name of the business at a particular bank relate to thereferrals/recommendations (from friends and family) and advertising (19%). Availability (only bank available at the place –19%) and convenience (16%) were also reported as important reasons for choosing a particular bank. Only 4% chose to opena bank account in the name of the business at a particular bank because of its product offering.

Figure 26: Key drivers for banking choice

Recommended by friend/family

Only bank available at the place

Advertising

Convenience

Previously used/have personal bank accounts there

Bank charges

Friend/family works there

Products/services

Recommended by another small business

Interest rates/the best rates on savings

Interest rates/best rates on credit/loans/borrowing

Other

Don’t know

27

%

19

19

4

10

4

4

3

4

16

4

2

7

29

Barriers: On the other hand, the main barriers to having a bank account in the name of the business relate to monetary reasons,i.e. because the income is too low/irregular as shown in the figure below – which is not surprising given the low levels ofmonthly income. 19% of MSME owners reported that they are not banked because banks are too far away (accessibility –proximity) while 4% reported that they do not know anything about it which indicates a lack of financial literacy / knowledgeabout banks and their products. In addition, MSME owners require numerous documents to open their account, such asidentification document, proof of business address, business registration/licence, other business documents (e.g. Articles ofAssociation etc.), as well as a certain income to cover bank charges, minimum balance required, etc.

Figure 27: Key barriers to having a bank account in the name of the business

Business/income too small

Banks are too far

Irregular income

Can’t afford the minimum balance

Not enough money from business

Don’t qualify

Don’t need one

Planning to in future

Don’t know anything about it

Bank charges

Don’t have business address

Too complicated

I use my personal bank account

Have not registered my business

Don’t know

Refused to answer

Other

27

%

19

12

5

6

6

5

3

2

1

1

10

4

13

2

2

Looking at the accessibility to amenities reveals, that 63% of MSME owners in rural areas have to travel more than 1 hour toget to the nearest bank. There is a great opportunity for alternative distribution channels (e.g. mobile banking).

10 minutes orless

2910

Between 11 and20 minutes

31

8Between 21 and

30 minutes

262

Between 31minutes and 1

hour

7 15

More than an hour

3

63

Don’t know

3 1

n Urbann Rural

Figure 28: Distance from business to bank

4

30

4.3 Borrowing and credits/loans In total, only 5% of MSME owners borrowed money/have taken goods on credit in the past 12 months for business purposes(that excludes money used to start or take over the business), or are currently repaying or owing money/goods for theirbusiness. Only 1% of MSME owners borrow from a bank and 1% borrow from other formal non-bank institutions. On theother hand, 1% borrow from informal groups, and 2% borrow from family and friends as illustrated in the figure below.

Figure 29: Borrowing overview

Banked

Formal other

Informal

Family/friends

Excluded

1

%

1

1

2

95

In constructing the Credit Strand the overlaps in financial product/service usage are removed, resulting in the following segments:

n MSME owners who do not borrow (95%);n MSME owners who only borrow from friends and family (2%) and do not use any formal or informal mechanisms to

obtain credit;n MSME owners who borrow from informal sources such as money lenders but do not borrow from formal sources (bank

or other formal non-bank institutions) (1%) – however, they might also borrow from friends and family; andn MSME owners who borrow from formal institutions (total 2%: 1% from other formal non-bank and 1% obtain credit from

commercial banks) – they might also borrow from friends and family.

Comparing the overview of borrowing and the Credit Strand reveals that there are no overlaps in product update.

n Bankedn Formal other

n Informal n Friends and family only

n Excluded

Figure 30: Credit Strand

1 9511 2

31

Borrowing mechanisms: Of those who borrow (5%), about 32% borrow from friends, family or colleagues. Almost a quarterof MSME owners who borrow obtained loan(s) from Fundo de Desenvolvimento Distrital (24%) and 19% borrow frominformal money-lenders. Only 18% borrow from a commercial bank or micro-bank, and 3% borrow from the GovernmentAgency.

Drivers: MSME owners mainly borrow to grow their business (60%) and for day-to-day business needs (14%), while 10%borrow to finance stock, 10% to buy new machinery or new equipment, and 3% borrow to pay for loss caused by a naturaldisaster.

Barriers: A majority of MSME owners do not borrow (95%), mainly because they fear that they won’t be able to pay it back.24% are scared to borrow, while 18% are afraid to borrow as business is slow. And 9% reported that they do not think thatthey have the necessary collateral/security. 20% reported that they do not have the need to borrow. Many of those whoreported that they do not have the need to borrow cover expenses with savings rather than borrowing.

Friends/family or colleagues

Fundo de Desenvolvimento Distrital

Informal money-lender

Commercial banks and Micro banks

Government Agency

NGO

Cooperative de Crédito

Obtain goods on credit

Empresa de Forento

Employer

32

%

24

19

18

2

1

1

0.5

1

3

Figure 31: Borrowing mechanisms (of those who borrow)

Figure 32: Reasons for borrowing (key drivers)

Growing my business

Day-to-day business needs

To finance stock

To buy machinery

Personal reasons

To upgrade business facilities

New equipment

To buy property

Loss caused by natural disasters/damages

To pay debts

Other

Refused

60

%

14

10

5

5

5

12

2

3

10

3

3

32

In addition to the reasons reported by MSME owners as to why they do not borrow, other barriers might relate to therequirements as set out by formal financial institutions. In order to obtain a business loan from a commercial bank, for example,the MSME owner often requires21 formal registration, a bank account, a business plan, financial records, collateral, and being inoperation for more than one year. However, as illustrated below, many MSME owners do not meet these requirements andhence do not qualify for a loan by design.

Figure 33: Reasons for not borrowing (key barriers)

Figure 34: Requirements22 to access business loan from a commercial bank

I am scared

Don’t need to

Business is slow so I am afraid to borrow

I don’t have collateral/security

I don’t qualify

I’ve tried but was turned down

Borrowed in the past and paid back

I don’t believe in borrowing money

I have collateral/security, but I am not prepared to risk it

My earnings change from month to month

Other

Don’t know

24

%

20

18

9

8

3

7

2

11

9

3

3

21 Note: The requirements might vary. 22 Note: Requirements might vary from bank to bank.

6% 9% 2% 18% 46% 87%

FORMALREGISTRATION*

BANKACCOUNT**

BUSINESS PLAN

FINANCIALRECORDS

COLLATERAL(SAVINGS***)

OPERATING FOR MORE THAN A YEAR

n Yesn No/Don’t know

n Yesn No

n Yesn No

n Yesn No

n Yesn No

n Yesn No/Don’t know

Note*: 6% are registered, i.e. they have a “Alvara” and “Articles of Association”, 89% are not registered, 5% don’t know.Note**: Bank account includes any bank account. 9,5% of business owners are banked, but only 4,9% use a bank account mainly for business purposes.Note***: Do you save or put money away or invest for business purposes. Other assets that could be used as collateral have not been considered here.

33

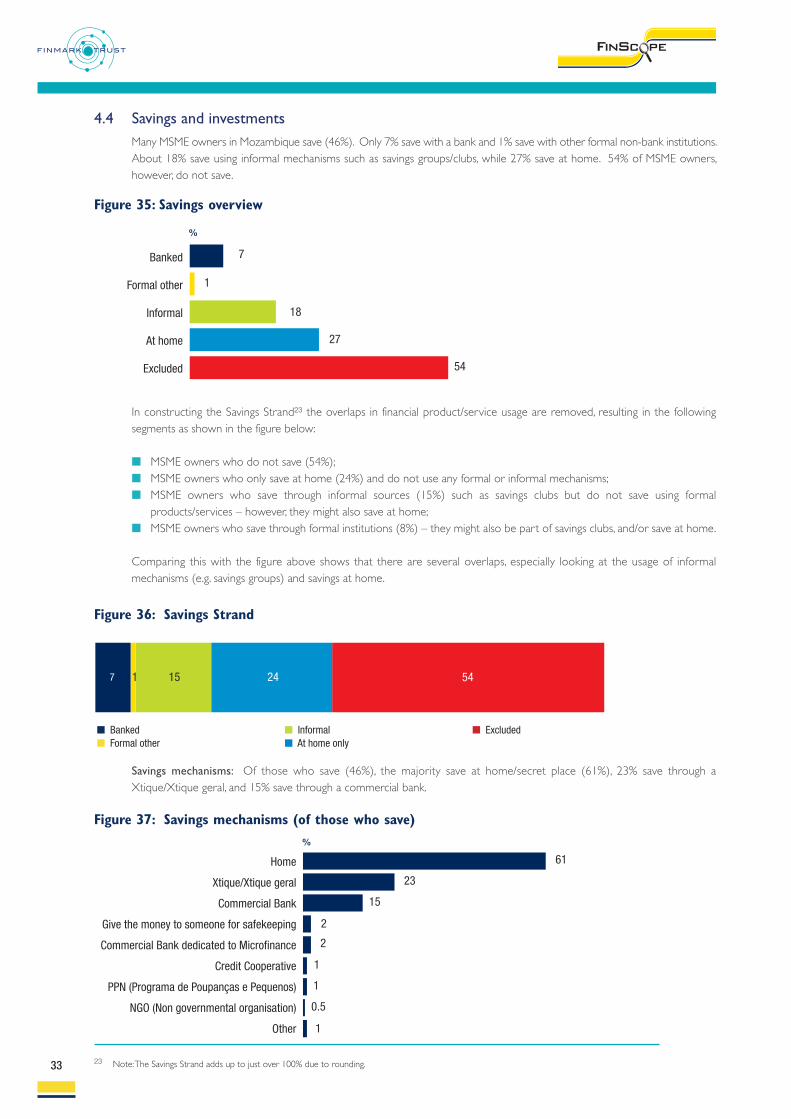

4.4 Savings and investmentsMany MSME owners in Mozambique save (46%). Only 7% save with a bank and 1% save with other formal non-bank institutions.About 18% save using informal mechanisms such as savings groups/clubs, while 27% save at home. 54% of MSME owners,however, do not save.

Banked

Formal other

Informal

At home

Excluded

7

%

1

18

27

54

Figure 35: Savings overview

In constructing the Savings Strand23 the overlaps in financial product/service usage are removed, resulting in the followingsegments as shown in the figure below: