Embed Size (px)

Citation preview

Dis cus si on Paper No. 14-034

Fiscal Rules and Compliance Expectations –

Evidence for the German Debt Brake Friedrich Heinemann, Eckhard Janeba, Christoph Schröder, and Frank Streif

Dis cus si on Paper No. 14-034

Fiscal Rules and Compliance Expectations –

Evidence for the German Debt Brake Friedrich Heinemann, Eckhard Janeba, Christoph Schröder, and Frank Streif

Download this ZEW Discussion Paper from our ftp server:

http://ftp.zew.de/pub/zew-docs/dp/dp14034.pdf

Die Dis cus si on Pape rs die nen einer mög lichst schnel len Ver brei tung von neue ren For schungs arbei ten des ZEW. Die Bei trä ge lie gen in allei ni ger Ver ant wor tung

der Auto ren und stel len nicht not wen di ger wei se die Mei nung des ZEW dar.

Dis cus si on Papers are inten ded to make results of ZEW research prompt ly avai la ble to other eco no mists in order to encou ra ge dis cus si on and sug gesti ons for revi si ons. The aut hors are sole ly

respon si ble for the con tents which do not neces sa ri ly repre sent the opi ni on of the ZEW.

FiscalRulesandComplianceExpectations‐EvidencefortheGermanDebtBrake

FriedrichHeinemann(ZEWMannheimandUniversityofHeidelberg)

EckhardJaneba*(UniversityofMannheim,CESifoandZEW)

ChristophSchröder(ZEWMannheim)

FrankStreif(ZEWMannheim)

May2014

Abstract: Fiscal ruleshavebecomepopular to limit deficits andhighdebtburdens inindustrializedcountries.Agrowingliteratureexaminestheirimpactbasedonaggregatefiscalperformance.Sofar,noevidenceexistsonhowfiscalrulesinfluencedeficitexpec‐tationsof fiscalpolicymakers. In thecontextof theGermandebtbrake,westudy thisexpectationdimension.Inafirststep,weintroduceasimpledynamicmodelinanenvi‐ronmentcharacterizedbythelaggedimplementationofanewrule.Laggedimplementa‐tioncharacterizesthesetupoftheGermandebtbrakeandraisescredibilityissues.Inasecondstep,weanalyzeauniquesurveyofmembersofall16Germanstateparliamentsandshowthatthedebtbrake’scredibilityisfarfromperfect.Theheterogeneityofcom‐pliance expectations in the survey closely corresponds to our theoretical predictionsregarding states’ initial fiscal conditions, specific state fiscal rules and bailout percep‐tions.Inaddition,thereisarobustasymmetryincomplianceexpectationsbetweenin‐sidersandoutsiders(bothforin‐statevsout‐of‐statepoliticiansandthegovernmentvsopposition dimension),whichwe attribute to overconfidence rather than noisy infor‐mation.Theseresultssuggestthatnationalfiscalrulescanbestrengthenedthroughno‐bailoutrules,sustainableinitialfiscalconditionsandcomplementarysub‐nationalrules.JELClassificationCode:H6,H7Keywords:BudgetDeficits,DebtBrake,Credibility,Survey,FiscalRules Acknowledgement: The authors gratefully acknowledge support from the Collaborative Research Center (SFB) 884 “Political Economy of Reforms”, funded by the German Research Foundation (DFG).*Correspondingauthor:

EckhardJaneba,DepartmentofEconomics,UniversityofMannheim,L7,3‐5,68131Mannheim,Germany,++49‐621‐1811795,janeba@uni‐mannheim.de.

1

1.Introduction

Constitutional fiscal rules such as a balanced budget requirement have been used for

decadesinfederalcountriessuchasSwitzerlandandtheUSstatestolimitdeficitsand

debtsofsub‐nationaljurisdictions(forasurveyofcurrentfiscalrulesseeIMF,2012).On

thenational level, theeuroareadebtcrisishas triggeredawaveofnewstatutoryand

constitutionalbudgetconstraintsinordertoboostpublicborrowerreputation.TheFis‐

calCompact,acceptedbyallEUcountriesexcepttheUKandtheCzechRepublicin2012,

hasbeenanothermilestoneforthespreadofnumericalfiscalconstraints.Thesignatory

countriescommittotheintroductionofnationaldebtbrakeswithwell‐definednumeri‐

calcontents(i.e.governmentsarerequiredtolimitstructuraldeficitstoamaximumof

0.5%ofGDP,andtolowerdebtlevelssystematicallywhenexceeding60%ofGDP,Euro‐

peanCouncil,2011).

Agrowing literatureexaminesthe impactofnumerical fiscalrulesbasedonaggregate

fiscalperformanceindifferentregionalcontexts.Thestandardapproachistheestima‐

tionof cross‐sectionorpanelmodels for the selected jurisdictionsand theirdeficitor

debtperformance (for theUS seeEichengreenandBayoumi,1994,Poterba,1996; for

Europe seeDebrun,2000,LagonaandPadovano,2007,Debrunet al., 2008; forOECD

countriesseeDahanandStrawczynski,2010;andforSwisscantonsandmunicipalities

see Feld andKirchgässner, 2008;Krogstrup andWälti, 2008).A shortcomingof these

highlyaggregatedapproachesisthattheydonotrevealhowfiscalrulesimpactonthe

beliefs of fiscal decisionmakers regarding the credibility of the fiscal rule and hence

theirexpectationsforcompliance.Thepresentpaperaimstofillthisholebyexamining

theoreticallyandempiricallytheintermediatestepbetweenfiscalrulesontheonehand

anddecisionmakers’expectationsonfuturefiscaloutcomesontheotherhand.

Adefiningcharacteristicofaneffectiveandcredibleruleisthatitanchorsexpectations

consistent with the rule’s constraints. This logic has long been the key for assessing

monetaryrules. In themonetarycontext, incentivestogeneratesurprise inflationmay

undermine the credibility of an inflation rule (Kydland andPrescott, 1977;Barro and

Gordon,1983).Hence,amonetaryrule’seffectivenesscanbeassessedbyanalyzingits

impactoninflationaryexpectations.Forfiscalpolicy,ananalogyappliesforadeficitrule

anditsimpactoncomplianceexpectations.Duetothepoliticalcostsoffiscalconsolida‐

tion, politiciansmay face incentives not to complywith the deficit rule in the future.

2

Whetherandtowhatextentthenewruleisseenasabindingconstraintshouldbede‐

tectable fromcompliance expectations.This shouldhold inparticular for the expecta‐

tionsofthosepoliticalactorswhotaketherelevantbudgetarydecisions.Therefore,the

impactoffiscalrulesonpoliticians’expectationsoffersanaturalwaytoassessthecred‐

ibilityandeffectivenessofanewrule‐basedfiscalregime.

Althoughtheunderlying idea isofobviousandfundamental importance,ourcontribu‐

tionisthefirsttostudythroughasurveyofpoliticianstowhatextentpolicymakersex‐

pectcompliancewithanewfiscalrule.Thus,itservestofillastrikinggapinthelitera‐

tureonfiscalrules’effectiveness.Theapproachhasafurtherstrength:Whilestudieson

the linkbetweenrulesandobservable fiscalperformanceareonlyapplicableonanex

post‐basis(i.e.aftermanyyearsofexperiencewithanexistingrule)ourmethodcanbe

employedexante(i.e.oncearulehascomeintoexistencebutperformancedataarenot

yetavailable).Furthermore,itopenstheblackboxofaggregationand,instead,looksinto

theimpactofafiscalruleonthe(heterogeneous)expectationsofthoseindividualpoliti‐

cianswhoactuallytakethebudgetarydecisions.

TheinstitutionalcontextofouranalysisistheGermandebtbrake.Weexploreexpecta‐

tion formation for themembersof allGerman stateparliaments regardinganexisting

fiscal rule that becomes binding only several years from now. The case of Germany’s

debtbrakeisofinterestfortheunderstandingoffiscalrulesmoregenerallyandbeyond

Germany:First,theGermangovernmenthasbeenamajoradvocateforestablishingthe

FiscalCompactinEurope.Infact,inmanydimensionstheprovisionsoftheFiscalCom‐

pactare similar to thatofGermany’sdebtbrake.Therefore,abetterunderstandingof

theGermandebtbrakewillalsobehelpfulforassessingtheCompact’sconsequencesfor

other EU countries. Second, the German debt brake is characterized by lagged imple‐

mentationsinceitsbindingconstraintsarephasedinoveralongerperiod(forthecen‐

tralleveluntiltheyear2016andforthestatelevelin2020).Laggedimplementationisa

frequentstrategytorealizefarreachinginstitutionalreformssinceithelpstoovercome

reformresistance(seeBuchanan,1994,forageneraldiscussion).Atthesametime,the

transition process raises substantial credibility questions and the German debt brake

exampleofferstheopportunitytobetterunderstandthegeneralconditionsunderwhich

laggedimplementationcanneverthelessbecredible.

Ouranalysisofexpectationformationcomprisesatheoreticalandanempiricalcontribu‐

tion.Firstwedevelopatheoreticalmodelwiththreeperiods(labelled0,1,2)describing

3

thedynamic fiscal decision situation in an environment characterizedbyphasing in a

zerodeficit rule.Decisionsondeficits aredynamicbynatureand imply trade‐offsbe‐

tween instantand futurepoliticalcosts fromfiscalconsolidation.Themodel’skey fea‐

tureistheexistenceofafiscalrulewhichtakeseffectonlyinthefuture(period2).Afis‐

calshockinthenearfuture(period1)makescompliancewiththefiscalruleuncertain

whenthefiscalruleisnotcredible.Inperiod1,thegovernmenttradesoffthebenefits

andcostsofadheringtothefiscalrule.Complianceismorelikelytheloweristheinitial

deficit inperiod0 , thehigher isthegovernment’scompetence insmoothingthe fiscal

shock,thelowerarebailoutexpectations,thetighterisafiscalruleatthestatelevelin

period1,andthehigher thedeficit reduction inperiod0.Themodelalsoallowsus to

consider noisy information about a government’s ability and overconfidencewith re‐

specttocompliancewiththefiscalrule,whichcanexplainheterogeneousbeliefsofpoli‐

ticians.ThemodelthuscaptureskeyfeaturesoftheGermandebtruleaswellassimilar

institutionalinnovationselsewhereandguidestheempiricalanalysis.

Inasecondstep,wetestthesemodelpredictionsonthedriversofcomplianceexpecta‐

tions based on a unique survey ofmembers of all 16 German state parliaments,who

havebeencontactedwithaquestionnairerelatingtothenewdebtbrake.Inthesurvey

weelicitedresponsesforthepoliticians’expectationsontheownstatecomplyingwith

the new rule by the year 2020, on other states’ compliance, and on the likelihood of

sanctionsorbailout if a state violates thenewrule in2020. Since the surveywasnot

anonymous, individualcharacteristics (suchaseducation,partymembership,etc.)and

statecharacteristics(suchascurrentfiscalpositionandfutureneedforfiscalconsolida‐

tion)canbeusedtosystematicallystudythedeterminantsofcomplianceexpectations.

Thesurveyshowsthatthedebtbrake’scredibilityisfarfromperfect.Theheterogeneity

ofcomplianceexpectationsinthesurveycloselycorrespondstoourtheoreticalpredic‐

tions. States’ initial fiscal conditions, specific state fiscal rules andbailout perceptions

matter. In addition, there is a robust asymmetry in compliance expectations between

insidersandoutsiders(bothforin‐stateversusout‐of‐statepoliticiansandthegovern‐

ment versus opposition dimension). Insiders tend to be significantly more optimistic

thanoutsidersregardingthelikelihoodofstate’scompliance.Basedontheguidanceof

our theoretical model we diagnose overconfidence of insiders (and not noisy infor‐

mation)asdrivingthisasymmetry.Thesedetailedinsightsimproveourunderstanding

onhowthecredibilityofanewnationalfiscalrulecanbestrengthenedingeneral.Our

4

resultspoint to the importanceofno‐bailout rules, sustainable initial fiscal conditions

andcomplementarysub‐nationalrules.

Ourpaperisrelatedtovariousotherliteratures.Afewrecentpapersanalyzetheoreti‐

cally the role of fiscal rules in a political economy framework, such as Azzimonti,

BattagliniandCoate(2008).Janeba(2012)considerstheroleofdelayinmakingaGer‐

man type debt brake bindingwhen the fiscal rule itself is credible. The incentives of

bailoutsinafederalcontextareconsideredbyGoodspeed(2002).Kirchgässner(2002)

andVoigtandBlume(2011)examineempiricallytheeffectsoffiscalconstraintsonfiscal

outcomes.Expectationeffectsoffiscalruleswithrespecttobondmarketinvestorsplaya

roleforstudieswhichlookintotheimpactoffiscalrulesonriskpremiaofgovernment

bonds (Heinemann,Osterloh andKalb, 2014; Iara andWolff, 2014). Surveys of politi‐

cianshavebeenusedinrecentresearchbytwoofthepresentauthors.Heinemannand

Janeba(2011)useasurveyofmembersofGermany’snationalparliamenttostudyideo‐

logicalbiasintaxpolicy.JanebaandOsterloh(2013)useasurveyofmayorsintheGer‐

manstateofBaden‐Württemberg toempiricallymotivate thespatial structureof local

taxcompetitioninatheoreticaltaxcompetitionmodel.HeinemannandOsterloh(2013)

surveymembersoftheEuropeanParliamentregardingtheintroductionofaminimum

taxforcompaniesintheEUinordertodisentangleideologicalandnationalpreferences

ofpoliticians.

Therestofthepaperisorganizedasfollows.Section2setsupthetheoreticalmodeland

derivescomparativestaticsforthelikelihoodofcompliancewiththedebtbrake.Section

3describesouroriginalsurveyandprovidesbackgroundinformationonGermany’spo‐

litical and fiscal systemand thedebtbrake.Ourmain findings arepresented anddis‐

cussedinsection4.Finally,section5concludes.

2.AModelofFiscalRuleCompliance

Wemodelthedynamicfiscaldecisionofanincumbentgovernmenttoreduceitsdeficit

inordertomeetthetargetofafiscalrulebecomingeffectiveonlyinthedistantfuture.

Politicalcostsofdeficitreductionaremodeledinareducedforminordertofocusonthe

likelihoodofcompliancewiththefiscalrule.Lackofgovernmentcommitmentanddefi‐

citshocksmakecompliancenon‐trivialanduncertain.Specifically,weassumethat the

economylasts for threeperiods, 0,1,2.Themainvariableof interest is thegovern‐

mentdeficit .Theinitialdeficitisgivenby 0andisexogenousfromtheviewpoint

5

oftheincumbentgovernmentinperiod0.Thefiscalrule(i.e.,thedebtbrake)requires

thegovernmenttorunabalancedbudgetinperiod2.Ifthistargetismet(thatis,

0), thegovernmentobtainspayoff (c forcompliance).Otherwise thegovernment is

noncompliant andobtains payoff .Wedefine as the gross gain from

compliance.Thisdynamicset‐upcorrespondstothelaggedimplementationoftheGer‐

mandebtbrake.Periods0and1representthetime inwhichthedebtbrakehasbeen

implementedbutnotyettakeneffect.Period2,fromtheperspectiveofGermanstates,

wouldbetheyear2020inwhichthezerodeficitlimitfortheGermanstatesentersinto

force.

Thegovernmentcanreducethedeficitintwostepstowardthegoalbyreducingthedef‐

icitinperiods0and1bytheamounts 0and 0,respectively.Wemodeldeficit

reductioninareducedformwithoutspecifyingthenatureofthefiscaladjustment(i.e.,

taxincreasesand/orexpenditurecuts).Deficitreductioniscostlyforthegovernmentin

theperiodwhenittakesplacebecauseapprovalratingsofthegovernmentorreelection

chancesareharmed.Wefocusontheconcurrentcosteventhoughthecostofpermanent

deficitreductionmayspillovertofutureperiods.Wethusimplicitlyassumethatvoters

andpoliticianscaremostlyaboutthechangeofthedeficit,ratherthanitslevel.Thecost

functionforpermanentlyreducingthedeficitisc(r)intheperiodwhentheadjustment

ismade,andhasthepropertiesc’≥0,c’’>0,c(0)=0,andc’(0)=0.Strictconvexityim‐

pliesthatspreadingagivendeficitreductionovertimeisefficient,allelsebeingequal.

Thedeficitinperiod1isafunctionoftheinitialdeficitd0minusthereductionr0under‐

takeninperiod0.Thedeficitd1isstochasticduetoashockinfluencingthedeficitinpe‐

riod1.Theshockislabeledsandisdrawnfromtheuniformdistributionwithsupport

[0,S],whereS>0.Theprobabilitydensityfunctionisthus1/S.Therealizeddeficitshock

istheproductofsandanexogenousgovernmentcompetencemeasureq>0,whichre‐

flectstheabilityofthegovernmenttomoderateshocks.Lowerlevelsofqreflecthigher

ability.Whenputtingtheseelementstogethertheactualdeficitinperiod1is

. (1)

Inperiod1thegovernmentreducesthedeficitfurtherbychoosingr1sothat

. (2)

6

Byassumptionnoshockisassumedtotakeplaceinperiod2.Thegovernmentpayoffis

givenby

, (3)

where whenthegovernmentiscompliantinperiod2,thatisd2≤0,and

whennot.Let 1bethediscountfactor.1

2.1CredibleFiscalRule

Westartwithabenchmarksituationinwhichthefiscalrule 0iscredibleandthe

governmentmustcomplywith it regardlessof therealizationof theshock inperiod1

Therefore deficit reduction in period 1 is . The expected utility from

complianceisthen

, (4)

wherewemadeuseof theassumption that shocksareuniformlydistributedover the

interval[0,S].Thecostsofcompliancecomefromthecostofdeficitreductioninthefirst

periodplusthediscounted,probabilityweightedcostinperiod1,whichdependonthe

initialdeficitd0,period0deficitreductionr0,andthemagnitudeoftherealizedshockqs.

Thegovernmentinfluencestheexpectedutilitybychoosingr0,whichaffectsthedistri‐

butionofdeficitreductioncostsovertime.Theoptimalfirstperioddeficitreductionis

foundbymaximizing (4)with respect to r0.Theoptimum is implicitly givenby the

condition

. (5)

Strictconvexityofthecostfunctionensuresthatthesecondorderconditionholds.The

righthandsideof(5)representsthemarginalcostofincreasingdeficitreductioninpe‐

riod0.Thelefthandsidecapturesthemarginalbenefitofdoingso.Anincreaseinperiod

0deficitreductiondecreasestherangeoffeasibledeficitsinperiod1,whichonnetsaves

cost .

Insertingtheoptimalvalue into(4)givesthemaximalutilityfromcompliancewitha

credibledeficitruleandisdenoted . Weliketonotethatthereisnoguarantee

1 We could discount utility in period 2 by instead of . Doing so would simply rescale the utility level v, without affecting results. We omit the complication in order to save on notation.

7

thatagovernmentisbetteroffcomparedtonotcomplyingwiththefiscalrule(thelatter

isbyassumptionnotachoice,though).

2.2Lackofcommitment

Incontrasttotheprevioussection,wenowassumethatthecompliancedecisionisnot

forcedbyacrediblerule.Thecostofcomplianceinperiod1maybecomehighifthelevel

ofdeficitreductioninperiod0islowand/ortherealizationofthebudgetshockinperi‐

od1 isbad. Insuchasituation,agovernmentmayfinditattractivetonotcomply.We

analyze the conditions underwhich it is in the government’s interest to (not) comply

withthefiscaltarget,andifso,howthedeficitreductionisdistributedovertime.Forthe

timebeingwefocusonthepoliticaldecisionmakerandherinterestincompliance.Later

we consider how other individuals (such as opposition politicians or observers from

outsideofstate)assessthelikelihoodofcompliance.

Thestochasticnatureofthegovernmentdeficitinperiod1makesituncertainwhether

complianceoccurs.Animportantvariableinoursubsequentanalysisistheprobability

ofcompliancep.Weareinterestedintherelationshipbetweenpandexogenousparam‐

etersofthemodel,suchastheinitialdeficitd0,thegrossgainfromcomplianceu,gov‐

ernmentcompetenceq,possiblebailoutexpectations, aswell asadditional fiscal rules

restrictingthemaximumdeficitlevelinperiod1(priortotheexistingfiscalruleinperi‐

od2).Thelackofcommitmentrequiresthatwesolvethemodelbybackwardinduction.

Note that thegrossgainumustbepositive forcompliancewith the fiscal rule to take

placewithpositiveprobabilitybecausedeficitreductioniscostly.

Period1.

Thebinarypayoffstructure( , )combinedwithcostlydeficitreductionimpliesthat

wecanreducethegovernmentchoicesettotwooptions:Eithernotreachingthedeficit

goalinperiod2(andthereforenotspendinganyeffort,r1=0)orjustreachingthegoal

(withtheneedtosetr1=d1).Thelatterdominatestheformerif

, (6)

that is, the cost of reducing the deficit to zero is not higher than the gross gain from

compliance.Sincethecostofdeficitreductionc(r) isamonotonefunctionofr,wecan

invert(6)whenitholdswithequality,anddefineacritical leveloftheperiod1deficit

8

forcompliancetooccur,namely, ∗ .Ford1lessthanorequaltod1*,thegov‐

ernmentwill choose tobe compliant, otherwisenot.Using (1), the threshold levelde‐

finesimplicitlyamaximumlevelofthedeficitshocks,calleds*,thatisconsistentwithd2

=0.Thecriticallevelisgivenby

∗∗

. (7)

Insteadof statinggovernment compliance in termsofperiod1deficit (d1*), condition

(7)allowsustorestatethesamedecisionintermsoftherealizedvalueoftheshocks:

Fors≤s*thegovernmentwillbecompliant,otherwisenot.Thethreshold levels* isa

positivefunctionoftheadditionalgainfromcomplianceandofthedeficitreductionin

period 0, but depends negatively on initial deficit d0 and the inverse of government

competenceq(thelatteronlyunderappropriateassumptionsmadefurtherbelow).We

thuswrites*=s(r0;u,d0,q).Notethatr0isexogenousfromtheviewpointofperiod1,but

endogenousexante(unliketheotherthreevariables)anddeterminedinperiod0.

Givenauniformprobabilitydensityfunctionforswenowuse(7)tointroducetheprob‐

abilityofcompliancewiththefiscalrule

∗

. (8)

Theprobabilitypisthekeyobjectforourfurtheranalysisandliesbetween0and1un‐

dersuitableassumptionsonthesizeofd0andS.2Itdependson(r0;u,d0,q,S).Noteinpar‐

ticularthat

0, (9)

thatis,pincreases(decreases)withthelevelofperiod0deficitreduction(initialdeficit)

andthechangeisgivenbythecompetenceweightedprobabilitydensityofthevariable

s.Moredeficitreductioninperiod1makescompliancewiththefiscalrulemorelikely.

2 First, we assume that , which is sufficient to make s* in (7) nonnegative (because we assume r0 ≥ 0). The condition holds, if the initial deficit is not too large relative to the gross gain of compliance. Second, we assume that the maximally possible shock S is sufficiently large so that s* ≤ S always holds. This assumption requires the initial deficit to be large enough.

9

Period0.

Wenowturntotheanalysisofperiod0,inwhichthegovernmentchoosesr0andthere‐

fore affects the probability of compliance via (9). From the incumbent government’s

viewinperiod0theutilityisuncertainduetotheshocks.Theexpectedpayoffis

∗

∗

∗

(10)

The first lineshows insquarebrackets theutility (periods1and2)undercompliance

andnon‐compliance,respectively,dependingontherealizationoftheshocks.For low

levelsofs,s≤s*,thegovernmentcompliesinperiod1bydeficitreductionleadingtod2

=0(thefirstintegral).Ifsishigherthans*,thegovernmentdoesnotcomply(thesecond

integral).3Rewritingterms,thesecondlinein(10)showsinbracketsthesameexpres‐

sionasbefore,nowasthesumoftheguaranteedutilityundernon‐complianceandthe

expected gross gain from compliance,minus the cost of deficit reduction in period 1

whensissufficientlysmall(s<s*).

Firstperioddeficit reductionr0affects (10)via thecostofeffort inperiod0 (the first

termin(10)),theprobabilityofrealizingthegrossgainofcompliancep,andthecostof

effortinperiod2inthelattercase.Recallthatthethresholdlevels*isafunctionofr0via

(7)and(9).Thederivativeofexpectedutilitywithrespecttor0is

1

∗

1 ∗∗

(11)

Derivative(11)hasthefollowinginterpretation:Anincreaseinr0increasesthemarginal

costofdeficit reduction in the currentperiod.Themarginalbenefit ofdoing so is the

discounted increase in the expected gross gain of compliance (due to the increase in

probabilityofcompliance)adjustedforthecostofreducingthedeficitbyd0‐r0.Recall

3 This assumes implicitly that d1 >0, which holds, if r0<d0.

10

that (qS)‐1 represents the increase in the probability of compliancewhen r0 is raised

marginally.4

Evaluating(11)attwovaluesofr0providesadditionalinsight:Ontheonehand,atr0=0

themarginalcostofdeficitreductioninperiod0iszerobyassumption,andhencethe

expectedutilitygaindE[U]/dr0ispositivewhenthegrossgainuislargerthanthecostof

reducingtheoriginaldeficitd0(u>c(d0)).Wemakethatassumption,whichinsuresthat

r0≤0cannotbeasolutionto(11)(whensetequaltozero).Atr0=d0,ontheotherhand,

thegovernmentfaceshighmarginalcostinitially,butgainsbyincreasingtheprobability

of compliance (1/(qS))weightedby thegrossgainu.Weassumec’(d0)> δu/(qS), so

thatdE[U]/dr0<0atr0=d0.Thusalocalmaximummustobtainintheintervalbetween

0andd0.Theoptimal levelof firstperioddeficit reduction is foundby setting (11)

equaltozero,whichgives

. (12)

Givenourassumptionsjustmade,thesecondorderconditionisfulfilledat :

0. (13)

2.3Results

We now study the effects of exogenous variables on the probability of compliance p,

whichdependsonexogenousmodelparametersbothdirectly,asshownin(8),butalso

indirectlyviatheoptimallevelofinitialdeficitreductionr0,asimplicitlydefinedin(12).

Thelatteristheperiod0anticipationeffect,whereastheformeristheperiod1compli‐

anceincentiveeffect.

1. Initial deficit: Differentiation of (12) shows that an increase in the initial deficit d0

leadstoalowergovernmenteffortininitialdeficitreduction,thatis

0, (14)

4 The difference between the optimal deficit reduction under credible and non-credible fiscal rules is twofold. First, the utility gain from compliance u appears in (11) but not in (5) because with a credible rule the govern-ment always obtains uc. Second, the marginal benefit of extending r0 does not contain the cost term c(d1) in (11) because an increase in r0 reduces the cost of deficit reduction for given probability of compliance (p or s* in (10)), but at the same time makes compliance more likely (s* goes up). The two effects cancel out.

11

whichisnegativebythesecondordercondition.Theprobabilityofcompliancepisalso

loweredbythedirect(complianceincentive)effectsothatthetotaleffectbecomes

1 0. (15)

Stateswithalargerinitialdeficitarelesslikelytocomplywiththebalancedbudgetre‐

quirementinperiod2(Hypothesis1:H1).

2.Bailoutexpectations: Up to nowwedidnot explicitly address the role of a possible

bailoutincaseofnon‐compliancewiththefiscalrule.Ratherweassignedautilitylevel

forthecaseofnon‐compliance,assumingittobelowerthanincaseofcompliance.Sup‐

posenow that a bailout is possible but less than certain (sonon‐compliance isworse

than compliance in expected terms: unc< uc), and consider that the probability of a

bailoutgoesup.Thisaffectsthegovernmenteffortinreachingthedeficittarget.Formal‐

ly,wecapturethebailoutprobabilitybyinterpretingtheutilityfromnon‐complianceunc

asexpectedutility,whichcomprisestheutilitywhennobailoutoccursandwhenitdoes

occur.Anincreaseinthebailoutprobabilitythusleadstoahigherlevelofunc,andthus

lowernetutilitygainu.Thecomparativestaticsare

0, (16)

thusloweringtheeffortininitialdeficitreduction.Moreover,ahigherbailoututilityre‐

duces theprobabilityof compliancebecauseadecrease inudecreasespbothdirectly

andindirectly:

0. (17)

Weconcludethathigherbailoutexpectationsmakecompliancewiththebalancedbudg‐

etrequirementlesslikely(Hypothesis2:H2).

3.State fiscalrule inperiod1:The fiscalruleunderconsiderationbecomeseffective in

period2.SomestatesinGermanyhaveintroducedfiscalrulesatthestatelevelwithcon‐

straintsbecomingeffectiveprior to thenationaldebtbrake’scrucialyear2020.These

state rules are supposed to strengthen the effort and likelihood of compliance. In the

present frameworkwecapture this ideabyallowing foranadditional fiscalrule tobe

alreadyeffectiveinperiod1.Weassumethattheadditionalfiscalruleiscredible,per‐

12

hapsbecausethereisnoonetobailoutthegovernmentwithinthestate.Yetweallow

for the possibility that the fiscal rule may be of different strictness. We express the

strictness in termsof themaximum feasibledeficit that canoccur inperiod1,d0+qS.

Theupperlimitofthedeficitinperiod1mustobey

. (18)

Theparameterαfrom[0,1]representsthestrengthofthefiscalrule.Thefiscalrulehas

nobitewhatsoeverwhenα=1becausenodeficitreductionisnecessaryinperiod0tobe

compliantwiththenewruleinperiod1.Bycontrast,α=0meansthatthegovernmentis

notallowedtorunagovernmentdeficitinperiod1regardlessofswhenthenewfiscal

ruleiscredible.Thiswouldmandatedeficitreductioninperiod0of ,thusinduc‐

ingd1 0.Lowervaluesofαthuscorrespondtoatighterfiscalruleinperiod1.Using(2)

wecanreformulatetherequirementin(18)intermsofinitialdeficitreduction:

1 : . (19)

Notethat isdecreasinginα.Atighterfiscalruleinperiod1requiresahigherdeficit

reductioneffortinperiod0.Whethertheadditionalfiscalrulehasbitedependsonthe

magnitudesof and ,wherethelatteristakenfrom(12)andrepresentstheoptimal

choiceofinitialdeficitreductionintheabsenceofthefiscalruleinperiod1.When

,thenewfiscalruleisbinding,otherwiseitisnot.Thisresulthasfurtherramifications

fortheprobabilityofcompliancewiththeoriginal fiscalrule inperiod2.Probabilityp

dependspositivelyonr0.

We conclude that the likelihoodof compliance (weakly) increases in the strengthof a

crediblefiscalruleatstatelevelwhichrestrictstheperiod1deficit(Hypothesis3:H3).

4.IndividualBeliefs:Considernowthebeliefsingovernmentcomplianceafterthedeci‐

sion onperiod0 deficit reductionhas been takenbut before the shock s realizes.We

thus focus on the expectations at an interim stage for a given level of r0.Wewish to

compare the beliefs in compliance of two types of politicians: the incumbent govern‐

mentorin‐statelegislaturesontheonehand,andoppositionpoliticiansorout‐of‐state

politiciansontheotherhand.

Thepsychologicalliterature(seeMooreandHealy,2008)suggeststhatalargenumber

of individuals (more than half) believe to perform better than the average/median,

13

which is impossible. This is termed overconfidence. In the present context this could

mean that the incumbentgovernmentbelieves its competency tobehigher thanwhat

theoppositionasserts,thatis,thegovernmentbelievestohavealowervalueofqthan

what theopposition thinks thisvalue tobe.Thisassumptiondoesnotrequireastate‐

mentabout the truecompetence,only that the twobeliefsdiffer.Equation(8) implies

immediately that for given r0 the incumbent’s subjective probability of compliance is

higherthanthatoftheopposition.Thiseffectisreinforcedwhenperiod0deficitreduc‐

tionisendogenous.Toseethis,notethattheeffectfromhighervaluesofqondeficitre‐

ductioninperiod0isfoundbydifferentiationof(12),assumingthatqisthetruevalue:

0, (20)

which is negative by the second order condition. The incumbent government ismore

optimisticaboutthelikelihoodofcomplianceinperiod1andthusundertakesmoreef‐

fortinperiod0,whichinturnmakescompliancemorelikely.

Alternatively,wemayassumethat insiders(whichmaybe the incumbentgovernment

or in‐state legislators) know the government’s competence exactly, denoted by q, but

outsiders (whichmay be the opposition or out‐of‐state politicians) have only a noisy

signal about the government’s competence. Specifically,we assume that outsiders be‐

lieve that government competence is qlwithprobability z andqhwithprobability1‐z

suchthatE[q]=zql+(1‐z)qh=q.Theexpectedvalueoftheoutsiders’subjectivebeliefof

government competence equals therefore the true government competence.We now

comparetheexpectedcomplianceofthegovernmentbycomparingthebeliefsofinsid‐

ersandoutsiders,againataninterimstagewhenr0hasbeensetalready.Theinsider’s

beliefissimply

. (21)

Bycontrast,theoutsider’sexpectedlikelihoodofcompliancebythegovernmentis

1 (22)

.

Comparisonof(21)and(22)showsthatpout>pins.Inotherwords,theoutsiderbelieves

undernoisyinformationthatthegovernmentismorelikelytocomplythantheinsider.

14

Theintuitioncomesfromtheobservationthattheprobabilitypin(8)isaconvexfunc‐

tionofq.

Weconcludethattheoutsiders(politicaloppositionorout‐of‐statepoliticians)aremore

optimisticaboutcompliancethaninsiders(theincumbentorin‐statepoliticians)under

noisy information about the incumbent government’s competence but less optimistic

underoverconfidence(Hypothesis4:H4).

Thus,ourmodelarrivesathypothesesontheheterogeneityofcomplianceexpectations

acrossindividualpoliticians.Thesehypothesesarederivedforasettingwherejurisdic‐

tionsareconfrontedwithanidenticalfiscalrule,asitisthecaseforGermanstatesand

thenationaldebtbrake.OursurveyamongmembersofGermanstateparliamentsoffers

thebasisfortestingtheirrelevance.

3.Institutionalandsurveydetails

3.1.Germany’sfederalsystemandtheconstitutionaldebtbrake

BeforeweintroducethesurveyweprovideabriefintroductiontoGermany’selectoral,

politicalandfiscalsystem(foramoredetaileddescriptionoftheGermanpartyandelec‐

toralsystemthereaderisreferredtoRoberts,1988,andPoguntke,1994).

Democracy. Germany is a parliamentarydemocracywith two chambers at the federal

level:thelowerchambercalledBundestag,whichiselectedbyallcitizens,andtheupper

chambercalledBundesrat,whichrepresentsthe16statesofGermanyandwhosemem‐

bersaredelegatesofstategovernments.Thedebtbrakewasapprovedin2009bymore

thanthe2/3requiredmajorityinbothchambersinordertochangetheconstitution.At

thestatelevel,thereexistsonlyonechamberlikethelowerchamberatthefederallevel.

Wesurveyedmembersofthesestateparliaments,calledMSPhenceforth.

Parties. The number of political parties has some regional variation.We describe the

mainparties:TheChristianDemocrats(CDU/CSU)areacentre‐rightparty,whichpur‐

suesarelativelymarketorientedpolicybutwhichissociallyconservativeinsomestates

(likeBavaria)andonsomepolicyissues(suchasthetraditionalroleofthefamily).The

SocialDemocratic Party (SPD) is the othermajor party and represents the center‐left

(lessmarketorientedthantheChristianDemocrats,sociallyprogressiveandinfavorof

more intense redistribution than CDU/CSU). The Free Democratic Party (FDP) is the

mostmarket oriented partywhich favors small government and low taxes. On social

15

issuesitismoreprogressivethantheChristianDemocrats.TheLeftPartyunitesformer

communists in East Germany (mostly pragmatic) and disappointed Social Democrats

fromtheleftwinginWestGermany(moreideological).TheGreenPartyisalsoonthe

centre‐leftandpushesforenvironmentalandsocialreformswithdiverseviewsoneco‐

nomicissues.Thepartyispopularwithwell‐educatedindividualsfromthemiddleclass.

FiscalFederalism.TheGermanstatefeaturesthreegovernmentlayerswithpartlyover‐

lapping areas of policy responsibility: (1) the federal level, (2) the states, and (3) the

municipallevel.Taxautonomyatthestatelevelisrelativelylow.Revenuesareequalized

toasignificantdegreeacrossstatesandinadditionthroughverticaltaxsharing.Differ‐

ences in state revenuespercapitaare reducedviaa fiscalequalizationsystem,whose

legalfoundationissetinArticle106oftheGermanconstitution(Grundgesetz),accord‐

ing to which material living conditions should be comparable across German states.

ThroughthelargedegreeofrevenuesharingtheGermanfederalsystemisclosertobe‐

ing an example of cooperative fiscal federalism rather than competitive federalism

(Braun, 2007; for details on equalization and tax sharing see also Heinemann et al.,

2013).

FiscalRules.ThefiscalruleistheGermandebtbrake(“Schuldenbremse”),whichbecame

part of theGerman constitution (the “Grundgesetz”) in 2009. Itwasmotivated by the

continuingbuildupofpublicdebtacrossall levelsofgovernmentsincethe1970s.The

new constitutional rule requires the federal government to run a (cyclically adjusted)

budgetdeficitofnomorethan0.35%ofGDPstartingin2016(seeBundesministerium

für Finanzen, 2009 for a detailed description). For German states (“Länder”) the new

ruleismorestringentandrequiresthemtorunazerodeficit(cyclicallyadjusted).The

zerodeficitconstraintforthestatesdoesnotbecomelegallyeffectiveuntilthebudget‐

aryyear2020.Theruleforthefederalgovernmentisaccompaniedwithaspecificplan

detailinghowthestructuraldeficitshallbereducedbetween2011and2015sothatthe

targetisreachedin2016.Forthestates,nospecificpathexistsingeneral.However,five

states (Berlin,Bremen, Saarland, Saxony‐AnhaltundSchleswig‐Holstein) receive “con‐

solidationaids”intotalof€800millionannuallyuntil2019.Inreturntheyarerequired

toreducetheir2010budgetdeficit inequalstepsuntil2020.Asareactiontothenew

national constitutional rule, several states have adjusted their state constitutions or

statebudgetarylawswithrulesechoingorevensharpeninigthenationalrule(forasur‐

veyseeCiagliaandHeinemann,2013).

16

Enforcement.TheStabilityCouncil(“Stabilitätsrat”)hasthetasktosupervisefiscalper‐

formanceandcompliancebothatthefederalandthestatelevel.Itrepresentsthefederal

ministers for financeandeconomicsaswellasall state financeministers.TheCouncil

hasrelativelylittlepowertoenforcefiscalrulesandimprovefiscalperformancebecause

itisnotallowedtoimposemonetarysanctionsdirectly.Inthecaseofthefivestatesre‐

ceiving consolidation aids the Council is entitled to withhold aids in case of non‐

compliance.Non‐monetarysanctionsforallstatesoriginatefromthepossiblepublicity

oftheStabilityCouncil’sstatementsorfrompoliticalcostsmaterializingifastatebudget

isruledasunconstitutionalbytheFederalConstitutionalCourt.

Economic Performance. The lack of comprehensive monetary sanctions and the long

transitoryperiodraiseseriousquestionsaboutthenewrule’scredibility.Inaddition,the

highly diverse fiscal situation of states feeds diverging expectations. Table 1 provides

informationonkeyindicatorsandshowsthelargedifferenceineconomicactivity.GDP

percapitainHamburg,forexample,ismorethantwiceaslargeasinmosteasternstates.

Debt to state GDP is particularly high for the city states of Berlin and Bremen (both

above60%).Oftenhighdebt levelsgohand inhandwith largeprojected fiscaladjust‐

ments,asidentifiedbytheGermanCouncilofEconomicAdvisors’calculationofconsoli‐

dation need (an index ranging from ‐0.6 +3.5,whereBerlin andBremen are near the

maximum).Inthelightofthesefiscalperformancesitissomewhatsurprisingthatcredit

ratings are fairly positive in all states (all in theA range).One explanation consistent

withtheseobservationsisthatbailoutexpectationsexist.Becausetheserankingsappar‐

entlydonotreflectthestrengthofthedebtruleatthestatelevelingreatdetail,thelast

columnofTable1providesanindexforthestringencyofGermanindividualstates’fis‐

calrulesasdevelopedbyCiagliaandHeinemann(2013).Thisindextakesaccountofthe

rule’scontentsandprecision,legalbasisandenforcement.

17

Table1:EconomicandFiscalIndicators

Popula‐tion2011(inmil‐lions)

GDPpercapita2011(inthousandsof€)

TotaldebttoGDPratio2011(in%)

NeedforConsoli‐dation2011‐2020(in%ofGDP)

BondRating2012a

Indexofstringen‐cyofstatedebtrule

FederalGovernment

81.84 44.02 49.79e ‐ AAAd,e

Baden‐Württemberg

10.79 34.89 17.16 0.10 AAAd 0.62

Bavaria 12.60 35.44 6.79 ‐0.60 AAAd 0.48Berlin 3.50 28.95 61.64 3.50 Aa1c 0.65Brandenburg 2.50 22.08 35.77 2.10 Aa1c 0.51Bremen 0.66 42.39 73.63 3.40 ‐ 0.64Hamburg 1.80 52.49 26.86 0.30 ‐ 0.47Hesse 6.09 37.51 17.28 1.30 AAd 0.50Mecklenburg‐WestPomerania

1.63 21.40 29.11 1.70 ‐ 0.46

LowerSaxony 7.91 28.35 25.42 1.30 ‐ 0.55NorthRhine‐Westphalia

17.84 31.88 33.22 1.60 AA‐d 0.45

Rhineland‐Palatinate

4.00 28.31 32.49 1.80 AAAb 0.69

Saarland 1.01 30.10 41.83 2.80 ‐ 0.70Saxony 4.14 22.98 9.99 0.60 AAAd 0.76Saxony‐Anhalt 2.31 22.43 39.84 2.50 AA+d 0.77Schleswig‐Holstein

2.84 25.95 38.57 1.30 AAAb 0.77

Thuringia 2.22 21.66 35.04 2.30 AAAb 0.66Notes: a from http://www.welt.de/finanzen/article107267058/Bundeslaender‐profitieren‐von‐Deutschland‐Bonds.htmllastaccesson23July2013;bFitch;cMoody’s;dS&P,ereferringtofederallevelalone,nottoaggregateforGermany.Needforconsolidation is taken fromSachverständigenrat (2011)and isbasedon theaveragebudgetdeficits from2007 to2010.Itindicatestheextentofconsolidationnecessarytocomplywiththedebtbrakeby2020.Forthatpurpose,ittakesaccountforpensionobligationsandthereductionoftransfersfromthefederallevel(SpecialPurposeGrants)whichwillbothcomeintoeffectuntil2020.TheIndexofstringencyofthedebtrule isnormalizedbetween0and1,wherehighervaluesindicateamorestringentdebtrule(CiagliaandHeinemann,2013).

Hence,boththelegalsettingandthefiscaldivergenceleaveamplespaceforhighlyhet‐

erogeneous expectations on state compliance which we study through our survey

amongmembersofparliament.

18

3.2.Thesurveyamongmembersofstateparliaments

Oursurveywassenttoallmembersofthe16Germanstateparliamentsduringaperiod

of14months in2011and2012.Weconducted the survey in threewaves inorder to

makesurethatitdidnotcollidewithelectiontimes(surveyswereconductedapproxi‐

mately atmid‐term of an electoral cycle).We approachedmembers of parliament by

writtenlettersandsubsequentfollow‐upemails.Ifstillunsuccessful,wecontactedthem

byphone.Takenallthreewavestogether639politiciansfinallyparticipatedinthesur‐

veywhichresultedinaresponserateof34%.Responseratesdifferalongstateandpar‐

tyaffiliation.Table2providesanoverview.Possibleconcernsabouttheeffectofdiffer‐

entresponseratesaredealtwithintheeconometricanalysisbelow.

Table 2: Response rates and survey waves Number

ofMSPsNumberofresponses

Responserate

Surveywavea

Lastelectionbeforesurvey

Overall 1861 639 34.34% Baden‐Württemberg 138 77 55.80% 3 3/2011Bavaria 187 75 40.11% 1 9/2008Berlin 149 30 20.13% 3 9/2011Brandenburg 88 19 21.59% 1 9/2009Bremen 83 18 21.69% 3 5/2011Hamburg 124 39 31.45% 2 2/2011Hesse 114 50 43.86% 2 1/2009Mecklenburg‐WestPomerania 71 17 23.94% 3 9/2011LowerSaxony 152 54 35.53% 1 1/2008NorthRhine‐Westphalia 181 51 28.18% 2 5/2010Rhineland‐Palatinate 101 50 49.50% 3 3/2011Saarland 51 20 39.22% 1 8/2009Saxony 133 45 33.83% 2 8/2009Saxony‐Anhalt 106 47 44.79% 2 3/2011Schleswig‐Holstein 95 29 30.53% 1 9/2009Thuringia 88 36 40.91% 1 8/2009Notes:aThefirstwave(1)tookplaceinMarchandApril2011,thesecondwave(2)tookplaceinDecember2011andJanuary2012,andthethirdwave(3)tookplaceinAprilandMay2012

Thesurveywasnon‐anonymousbutpoliticianswereguaranteedconfidentialityforin‐

dividual responses. Thus, we are able to match the survey responses with personal

characteristicssuchaseducation,committeemembership,etc.frompublicsources(per‐

19

sonalorparliamentarywebsites)andwithstatecharacteristicssuchasGDPpercapita,

debt,needforfiscalconsolidation,etc.(seeTableA1intheappendixforallvariables).

Thequestionnaireconsistedofeightquestionscoveringpreferencesforrevenueauton‐

omy and fiscal equalization, spending preferences aswell as questions related to the

debtbrake(forafulldescriptionseeHeinemannetal.,2014).Forourstudy,wefocuson

thefollowingtwoquestions:

Questioncomplianceexpectation:Whichofthe16Germanstateswillcomplywiththeconstitutionaldebtbrakeasof2020withhighprobability?Eachofthe16statescouldbetickedindividuallyoroptions“all”or“none”couldbecho‐

sen.

Inordertoilluminatetheexpectedimpactofthedebtbrakewealsoaskedforthecon‐

sequencesofnon‐compliance:

Questionconsequencesofnon‐compliance:WhatwillhappenifGermanstatesdonotcomplywiththeconstitutionaldebtbrakeasof2020?(multipleanswerspossible)o Constitutionalcourts(onstateandfederallevels)willenforcebudgetconsolidationo Theconstitutionwillbechangedsoastorelaxthedebtbrakeo Transferpaymentstonon‐complyingstatesaregiven,whichhelptolowerthedeficito There will be sanctions against non‐complying states, e.g., lower transfers within the

federalfiscalequalizationschemeo There will be ordinary legal or constitutional interventions in non‐complying states’

budgetautonomyo Mergerofstateso Nothingwillhappeno Other:___________

Figure1indicatesthatthedebtrulecredibilityisimperfectandcomplianceexpectations

differremarkablyacrossstates.WhileBavariaisseenasanalmostcertaincaseofcom‐

pliance (85%believe it is highly probable) the prospects of the city states ofBremen

(3%) and Berlin (4%) are highly pessimistic. These expectations obviously correlate

closelywith current consolidation needs and debt levels (see Table 1). In addition, a

strongasymmetryemergesforinsider/outsiderexpectationsonfinanciallyweakstates

(see Figure 2with the example forMecklenburg‐West Pomerania):WhileMSPs from

otherstatesarehighlyskeptical,alargemajorityofpoliticiansfromeconomicallyweak‐

erstatesexpecttheirstatetorespectthedebtbrakezerodeficitcapbytheyear2020

(seeTableA2intheappendixforfullinformationoncross‐stateexpectationswhichcon‐

20

firms this asymmetry in general). Figure 3 summarizes the results for the non‐

compliance question: For this scenario, a significant number of politicians expect a

strongroleofconstitutionalcourts(bothfromfederalandstatelevel)toenforceconsol‐

idation or sanction. However, a large fraction of politicians expect the government

budget constraint to be soft due to bailout‐transfers or a relaxation of the strict debt

brake.Overall,thesedescriptivefindingspointtothepossiblerelevanceofourmodel’s

predictionontheroleoftheinitialfiscalsituation,bailoutexpectationsortheexpected

asymmetry between insiders and outsiders.We substantiate themodel’s explanatory

powerinthesubsequentregressionanalysis.

Figure 1: Compliance across states

BB=Brandenburg, BE=Berlin, BW=Baden‐Württemberg, BY=Bavaria, HB=Bremen,HE=Hesse, HH=Hamburg, MV=Mecklenburg‐West Pomerania, NI=Lower Saxony, NW=North Rhine‐Westphalia, RP=Rhineland‐Palatinate, SH=Schleswig‐Holstein,SL=Saarland,SN=Saxony,ST=Saxony‐Anhalt,TH=Thuringia

21

Figure2:ComplianceexpectationMecklenburg‐WestPomerania

BB=Brandenburg, BE=Berlin, BW=Baden‐Württemberg, BY=Bavaria, HB=Bremen,HE=Hesse, HH=Hamburg, MV=Mecklenburg‐West Pomerania, NI=Lower Saxony, NW=North Rhine‐Westphalia, RP=Rhineland‐Palatinate, SH=Schleswig‐Holstein,SL=Saarland,SN=Saxony,ST=Saxony‐Anhalt,TH=Thuringia

Figure3:ConsequencesofNon‐Compliance

22

4.Regressionanalyses

Our database is sufficiently rich to test whether the predictions from our theoretical

model on expectation heterogeneity are consistentwith the observable response pat‐

tern.Ourmodelpredictsthatcomplianceexpectationsofpoliticiansshouldberelatedto

theinitialdeficit,ormoregeneral,theinitialeconomicandfiscalconditionsofthestate

inquestion(H1),theindividualpolitician’sbailoutexpectations(H2),theexistenceand

characteristicsof state ruleswhich complement thenationaldebtbrake (H3), and the

individualpolitician’sinsider/outsiderstatus(duetoeitherasymmetricinformationor

overconfidenceonthesideofincumbents,H4).Wecoverthesefourdimensionsasfol‐

lows(forprecisevariableinformationseeTableA1intheappendix):

- Thestatecharacteristicsmergedtothepolitician’sresponsesincludeGDPpercapita

andtheneedforconsolidation(seeTable1).The lattergivesacomprehensivepic‐

tureofthecurrentfiscalandeconomicconditions(H1).Theneedforconsolidationis

taken from theGermanCouncil ofEconomicAdvisors (Sachverständigenrat,2011)

andreflectstheextenttowhichstatesneedtoconsolidatetheirbudgetsuntil2020

whenthedebtbrakecomesintoeffect.

- Forbailout‐expectations(H2)weexploitthesurveyquestionontheexpectedconse‐

quences of non‐compliance (Figure 3). From this question we construct an index

whichcapturestheindividualperceptionofthestrengthofthebudgetconstraint.A

larger indicatorvaluerepresentstheperceptionofastricterbudgetconstraintand

lowerbailout‐expectations.5

- Fortheexistenceandstringencyofastaterule(H3)wemergedatafromCiagliaand

Heinemann (2013)who develop an index for the stringency of German individual

states’fiscalrules,whichtakesaccountoftherule’scontentsandprecision,legalba‐

sisandenforcement.

- The insider‐outsider‐differentiation (H4) has twodimensions: First,we candistin‐

guish between incumbents as insiders and all others,where “incumbents” are de‐

finedasmembersofoneofthegoverningpartiesintherespectivestate.Second,we

5 Indicator construction is as follows: We add one point if a politician expects one of the “tough” reactions to a state non-complying (i.e. “enforcement through constitutional courts”, “sanctions”, “intervention in budget au-tonomy” or “merger of states”) and subtract one point for each of these reactions which is not expected. Analo-gously, we subtract one point for each of the expected “soft” reactions to a state-non complying (i.e. “change of constitution”, “transfers” or “nothing”) and add one point for each of these reaction which is not expected.

23

cancomparetheexpectationsforaspecificstate’scompliancebetweenin‐stateand

out‐of‐statelegislators.Weincludebothdimensionsinourtesting.

Weenrich this theory‐guidedchoiceofvariables throughthe inclusionof further indi‐

vidual and state controls because a growing empirical literature points to the im‐

portanceofthesevariablesforeconomic,monetaryandfiscalperformance(Besleyetal.,

2011, Göhlmann and Vaubel, 2007,Moessinger, 2014).We take account of the politi‐

cian’s gender, age, education (tertiary degree, type of degree, such as in busi‐

ness/economics),roleinparliament(membershipinbudgetcommittee)andexperience

(numberofyearsinparliament).Interalia,thesevariablesproxydifferencesintheindi‐

vidualinformationlevel.Furthermore,weaddpartydummiestoallowfortheimpactof

ideology. Ideology might influence expectations since perceptions of economic con‐

straintscanbebiasedbystrongideologicalpositions(see,forexample,Heinemannand

Janeba,2011,fortheperceptionofglobalizationconstraintontaxpolicy).Amongstate

controlsweincludeadummyforthosestatesreceivingconsolidationaidandtheextent

offiscalequalizationtransfersreceived.Thesevariablescovertransferdependency.Fi‐

nally,weaddadummyforthepoliticalorientationoftheincumbentgovernmentwhich

allows for the possibility that the incumbent’s political orientation has an impact on

complianceexpectationsfortherespectivestate.

4.1Baselineresults

We estimate a probit model with the compliance expectation as dependent variable

(dummyequals1:Politicianexpectsastatetocomplywiththedebtbrakeasof2020;0:

expectastatenottocomply).Sincewehaveexpectationsof639politicianson16states

wecanexploitatotalof10,224observations.Weclusterstandarderrorsforstatepairs.

Column(1) inTable3summarizesourstartingpointwiththefullsetofcontrolvaria‐

bles.Theresults showthat complianceexpectationsare relatedboth to the individual

andownstatecharacteristicsofrespondents.WeincludefixedeffectsforMSPs’statesof

origintoaccountforthepossibilitythatpoliticiansofparticularstatesmaybemoreor

lessoptimisticingeneral(asitissuggestedbythedescriptiveanalysis,seeTableA2in

theappendix).

Allproxiesrelated toour fourhypothesesarehighly significant. Signsare in linewith

thetheoreticalexpectationsfortheH1‐,H2‐andH3‐relatedindicators:Complianceex‐

24

pectationsforstateswithunfavorablestartingpositions(lowerGDPpercapitaorlarger

needforconsolidation)arelessoptimistic.Thebeliefinbailout‐transfersorotherrelax‐

ationsof the fiscalrule(lower index forstrengthofbudgetconstraint) lowerscompli‐

anceexpectations.Astricterstate‐individualfiscalruleiscorrelatedwithamorefavora‐

bleviewforthisparticularstate.Thesizeoftheeffectsissubstantialjudgedonthebasis

of averagemarginal effects:Aonepercentagepoint increaseof a state’s consolidation

need(H1)lowerstheprobabilitythatthisstateisexpectedtobecompliantbyabout10

percentagepoints.Thedifferencebetweenaverysoft (‐7)andveryhard(+7)percep‐

tionof thebudgetconstraint (H2)amounts toan impactof24percentagepoints.And

thedifference between theweakest (0.45) and strongest (0.78) observable state debt

rule(H3)isassociatedwithaprobabilityincreaseof16percentagepointsthatastateis

predictedtocomply.6H4‐relatedproxiesarehighlysignificantforbothinsider‐outsider‐

dimensions: Insiders (members of parties who form a state’s government/in‐state‐

politicians)aremoreoptimisticthanoutsiders(membersofoppositionparties/out‐of‐

state‐MSPs). The size of the effect is much larger for the in‐state vs. out‐of‐state‐

dimension (21 percentage points) than for the government‐opposition‐distinction (4

percentagepoints).Inthelightofourtheory,thepositivesignofinsiderstatuspointsto

the role of overconfidence as driving insider‐outsider‐asymmetry. If outsiders had an

informationdisadvantage they should sometimes over‐ and sometimesunderestimate

thecompetenceofinsidersbutnotnecessarilybesystematicallymorepessimisticthan

insiders. Therefore, the systematically larger optimism of insiders is consistent with

over‐confidenceratherthanwithnoisyinformation.

Theothercontrolvariablesare important tounderstandtheheterogeneityofexpecta‐

tions, as well. The observed education characteristics do not show up significantly.

Membersof thebudgetcommitteeviewadherencetothedebtbrakeasmoredifficult.

Equally,alongerparliamentaryexperiencereducescomplianceexpectation.Thisfinding

isnotdrivenbyanageeffectwhichpointsintotheoppositedirectionwitholdermem‐

bersbeingmoreconfident.Femalelegislatorsaremorepessimisticthantheirmalecol‐

leagues.Partyimprintoncomplianceexpectationsismoderate:Forexample,thereare

nosignificantdifferencesbetweenpartiesfromtheoppositeendsofthepoliticalspec‐

6 (0.78-0.45)*49 = 16 where 0.78 is the largest observed value of the index and 0.45 is the smallest observed value.

25

trum (i.e. between themarket‐liberal FDP and the socialist Left Party).7 Stateswith a

government consisting of right parties (i.e. ChristianDemocrats and/or FDP) are per‐

ceivedtohaveahigherchanceofcompliance.Consolidationaiddoesnotseemtocom‐

pensate for the less favorableeconomicand fiscal conditionsof the five related states

sincetherelateddummyissignificantlynegative.

Weemployvariousmodelvariants:Incolumn(2)weallowforindividualfixedeffects.8

Thisspecificationaccounts for therisk thatunobserved individualcharacteristicsmay

bias the results for state indicators. No substantial differences emerge. Table 4 takes

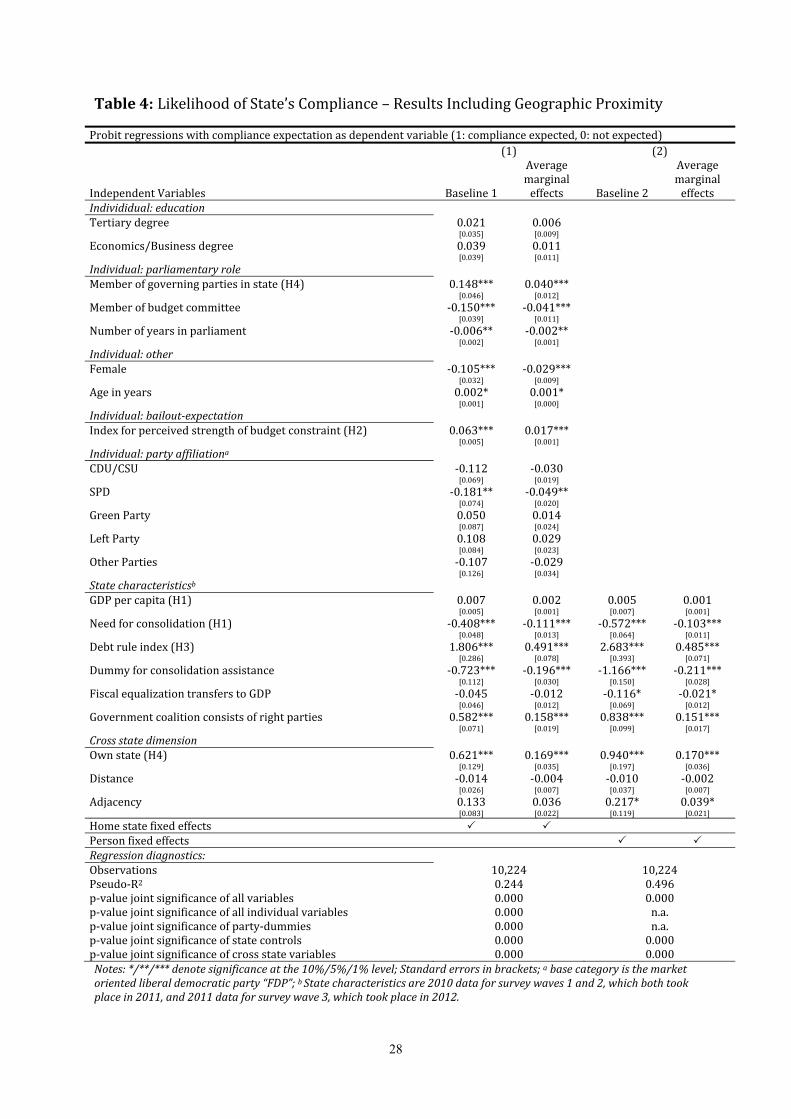

accountofthespatialdimensionofourcross‐stateanalysis. Inparticular,weallowfor

moredifferentiatedinformationasymmetriesacrossstates.Forthatpurpose,weinclude

twomeasuresof geographicproximitybetweenstates:First thedistancebetween the

ownstate’scapitalandthatofthestatetobeassessedandsecondadummyforacom‐

monborder.Thehypothesisisthatproximityandacommonbordermatterformutual

information.Again,column(1)includesourfullsetofindividualcontrolswhilecolumn

(2)replacesthembyindividualfixedeffects.Onlythedistanceindicatoris(weakly)sig‐

nificantintheindividualfixedeffectsspecifications.Complianceexpectationstendtobe

moreoptimisticformoredistantstatesthanforcloseneighbors.Thisisinlinewiththe

predictionof thetheoreticalmodelwithrespect to informationasymmetries.Allother

resultshardlychange,neitherintermsofsignificancenorinthesizeofmarginaleffects.

4.2Robustnessofregressionresults

First, theresultspresentedabovearerobustwithrespecttotheuseofdifferentvaria‐

blescapturingstatefiscalconditions(Hypothesis1).Nomatterwhetherweincludeei‐

therastate’stotaldebtstockrelativetoitsGDPortheaveragebudgetdeficit(overthe

lastthreeyears)relativetoGDPinsteadoftheneedforconsolidation,ourabovefindings

areconfirmed(seeTableA3 in theAppendix). Just like theneed for consolidation the

debt stock and the average deficit enter highly significantly andwith a negative sign.

Higherdebtordeficitsalsodecreasethecomplianceexpectationsoflegislators.Theim‐

pactofalmostallothervariablesremainsasinthebaselineregressions.Thecoefficient

for GDP per capita becomes significant, thereby providing additional evidence for the

7 Weighted regressions, however, indicate that Left Party politicians are more confident that the debt brake will be respected than politicians from the FDP, see below section 4.2. 8 Due to perfect collinearity of individual and home state fixed effects, we have to exclude the latter in this speci-fication.

26

validityofamoregeneralformulationofhypothesis1:Thehighertheincomeperinhab‐

itant,thelessfinanciallyconstrainedisastateandthehighertheprobabilityofcompli‐

ance. Only the coefficients to the fiscal equalization transfers change significance and

signsacrossspecifications.Webelief thatthiscanbeexplainedbythefactthatdebt is

highly correlatedwith financial equalization transfers9,whereas the average deficit is

not.

Second,aconcernaboutthevalidityofourdatacouldoriginatefromsampleselection.

Foroursurvey,Heinemannetal. (2013)haveconductedaunitnon‐responseanalysis.

Theymakeuseofdataonthepersonalcharacteristicsforall1683legislators,notonly

thosewhoresponded.10Thenon‐responseanalysisidentifiesvariablesattheindividual

andstatelevelthataffectpoliticians’participationdecision.Accordingtotheseresults,

significantdriversofsurveyparticipationare:education(degreeineconomicsorbusi‐

ness),budgetcommitteemembership,membershipingovernmentcoalitionpartiesand

gender.Thus, our regressions comprise as controls those factorswhichare important

drivers of non‐response. This greatly reduces the potential for selection bias. Yet,we

cannot fully exclude that we might still have a selection bias (Little and Vartivarian,

2005).Asa furtherrobustnesscheck,wethereforeemployaweightedregression(see

TableA4 in theappendix).For theweighting,weuse the inverseresponseprobability

basedonpartyandstateaffiliation.Theweightedregressionslightlychangesthefind‐

ings for party dummies: The Social Democrats dummy loses significancewhereas the

differencebetweentheLeftPartyandtheFreeDemocratsnowbecomessignificant.In‐

terestingly, in this regressionvariant left‐ leaningpoliticiansaremoreoptimistic than

their right‐leaning colleagues. The essential findings for our key hypotheses are con‐

firmed.Comparedtothenon‐weightedregressionthereareonlyminorchanges inthe

sizeofaveragemarginaleffects.

9 The correlation coefficient amounts to 0.76. 10 We do not face severe item non-response but predominantly unit non-response. Item non-response amounts to less than 1% of respondents and is therefore negligible for the survey at hand.

27

Table3: LikelihoodofState’sCompliance–ResultsExcludingGeographicProximity

Probitregressionswithcomplianceexpectation asdependentvariable (1:complianceexpected,0:notexpected) (1) (2)

IndependentVariables Baseline1

Averagemarginaleffects Baseline2

Averagemarginaleffects

Individidual:education Tertiarydegree 0.020 0.006

[0.035] [0.009]

Economics/Businessdegree 0.040 0.011 [0.039] [0.011]

Individual:parliamentaryrole Memberofgoverningpartiesinstate(H4) 0.149*** 0.040***

[0.046] [0.013]

Memberofbudgetcommittee ‐0.150*** ‐0.041*** [0.039] [0.011]

Numberofyearsinparliament ‐0.006** ‐0.002** [0.002] [0.001]

Individual:other Female ‐0.106*** ‐0.029***

[0.032] [0.009]

Ageinyears 0.002* 0.001* [0.001] [0.000]

Individual:bailout‐expectation Indexforperceivedstrengthofbudgetconstraint(H2) 0.063*** 0.017***

[0.005] [0.001]

Individual:partyaffiliationa CDU/CSU ‐0.112 ‐0.030

[0.068] [0.019]

SPD ‐0.181** ‐0.049** [0.074] [0.020]

GreenParty 0.050 0.013 [0.087] [0.024]

LeftParty 0.109 0.030 [0.084] [0.023]

OtherParties ‐0.109 ‐0.030 [0.125] [0.034]

Statecharacteristicsb GDPpercapita(H1) 0.007 0.002 0.005 0.001

[0.005] [0.001] [0.007] [0.001]

Needforconsolidation(H1) ‐0.386*** ‐0.105*** ‐0.541*** ‐0.098*** [0.048] [0.013] [0.063] [0.011]

Debtruleindex(H3) 1.860*** 0.506*** 2.736*** 0.497*** [0.292] [0.079] [0.398] [0.072]

Dummyforconsolidationassistance ‐0.767*** ‐0.209*** ‐1.220*** ‐0.222***[0.110] [0.030] [0.147] [0.027]

FiscalequalizationtransferstoGDP ‐0.067 ‐0.018 ‐0.151** ‐0.027** [0.047] [0.013] [0.070] [0.013]

Governmentcoalitionconsistsofrightparties 0.605*** 0.165*** 0.870*** 0.158***[0.074] [0.020] [0.103] [0.018]

Crossstatedimension: Ownstate(H4) 0.759*** 0.207*** 1.121*** 0.204*** [0.104] [0.028] [0.169] [0.030]

Distance ‐‐ ‐‐ ‐‐ ‐‐

Adjacency ‐‐ ‐‐ ‐‐ ‐‐

Homestatefixedeffects Personfixedeffects Regressiondiagnostics: Observations 10,224 10,224Pseudo‐R2 0.243 0.491p‐valuejointsignificanceofallvariables 0.000 0.000p‐valuejointsignificanceofallindividualvariables 0.000 n.a.p‐valuejointsignificanceofparty‐dummies 0.000 n.a.p‐valuejointsignificanceofstatecontrols 0.000 0.000p‐valuejointsignificanceofcrossstatevariables n.a. n.a.Notes:*/**/***denotesignificanceatthe10%/5%/1%level;Standarderrorsinbrackets;abasecategoryisthemarketorientedliberaldemocraticparty“FDP”;bStatecharacteristicsare2010dataforsurveywaves1and2,whichbothtookplacein2011,and2011dataforsurveywave3,whichtookplacein2012.

28

Table4: LikelihoodofState’sCompliance–ResultsIncludingGeographicProximity

Probitregressionswithcomplianceexpectationas dependentvariable(1:complianceexpected,0:notexpected) (1) (2)

IndependentVariables Baseline1

Averagemarginaleffects Baseline2

Averagemarginaleffects

Individidual:education Tertiarydegree 0.021 0.006

[0.035] [0.009]

Economics/Businessdegree 0.039 0.011 [0.039] [0.011]

Individual:parliamentaryrole Memberofgoverningpartiesinstate(H4) 0.148*** 0.040***

[0.046] [0.012]

Memberofbudgetcommittee ‐0.150*** ‐0.041*** [0.039] [0.011]

Numberofyearsinparliament ‐0.006** ‐0.002** [0.002] [0.001]

Individual:other Female ‐0.105*** ‐0.029***

[0.032] [0.009]

Ageinyears 0.002* 0.001* [0.001] [0.000]

Individual:bailout‐expectation Indexforperceivedstrengthofbudgetconstraint(H2) 0.063*** 0.017***

[0.005] [0.001]

Individual:partyaffiliationa CDU/CSU ‐0.112 ‐0.030

[0.069] [0.019]

SPD ‐0.181** ‐0.049** [0.074] [0.020]

GreenParty 0.050 0.014 [0.087] [0.024]

LeftParty 0.108 0.029 [0.084] [0.023]

OtherParties ‐0.107 ‐0.029 [0.126] [0.034]

Statecharacteristicsb GDPpercapita(H1) 0.007 0.002 0.005 0.001

[0.005] [0.001] [0.007] [0.001]

Needforconsolidation(H1) ‐0.408*** ‐0.111*** ‐0.572*** ‐0.103*** [0.048] [0.013] [0.064] [0.011]

Debtruleindex(H3) 1.806*** 0.491*** 2.683*** 0.485*** [0.286] [0.078] [0.393] [0.071]

Dummyforconsolidationassistance ‐0.723*** ‐0.196*** ‐1.166*** ‐0.211***[0.112] [0.030] [0.150] [0.028]

FiscalequalizationtransferstoGDP ‐0.045 ‐0.012 ‐0.116* ‐0.021* [0.046] [0.012] [0.069] [0.012]

Governmentcoalitionconsistsofrightparties 0.582*** 0.158*** 0.838*** 0.151***[0.071] [0.019] [0.099] [0.017]

Crossstatedimension Ownstate(H4) 0.621*** 0.169*** 0.940*** 0.170*** [0.129] [0.035] [0.197] [0.036]

Distance ‐0.014 ‐0.004 ‐0.010 ‐0.002 [0.026] [0.007] [0.037] [0.007]

Adjacency 0.133 0.036 0.217* 0.039* [0.083] [0.022] [0.119] [0.021]

Homestatefixedeffects Personfixedeffects Regressiondiagnostics: Observations 10,224 10,224Pseudo‐R2 0.244 0.496p‐valuejointsignificanceofallvariables 0.000 0.000p‐valuejointsignificanceofallindividualvariables 0.000 n.a.p‐valuejointsignificanceofparty‐dummies 0.000 n.a.p‐valuejointsignificanceofstatecontrols 0.000 0.000p‐valuejointsignificanceofcrossstatevariables 0.000 0.000Notes:*/**/***denotesignificanceatthe10%/5%/1%level;Standarderrorsinbrackets;abasecategoryisthemarketorientedliberaldemocraticparty“FDP”;bStatecharacteristicsare2010dataforsurveywaves1and2,whichbothtookplacein2011,and2011dataforsurveywave3,whichtookplacein2012.

29

5.Conclusion

Fiscalrulesaredesignedtoinfluencefiscalperformanceofstates.Whenafiscalruleis

effective,itmustimpactontheexpectationsandbeliefsofthosepoliticianswhodecide

onthegovernmentbudget.OurstudyofthenewdebtbrakeinGermanyrevealsanim‐

perfectcredibilityofthefiscalruleandpointstohighlyheterogeneousexpectationswith

respecttosub‐nationalcompliance.

Anessentialresultrelatestotheasymmetricexpectationsofinsidersandoutsiders.This

holds both for the government versus opposition and the in‐state versus out‐of‐state

dimension.Thisresultmightbeconsideredunproblematic,ifthegoverningpartiesand

politicians in the state under considerationwere better informed and thereforemore

trustworthyintheirjudgmentsthanoutsiders.Ourempiricalfindingsbasedonatheo‐

retical model point into a different direction, however. Insiders (in state politicians,

membersfromgoverningcoalitionparties)aremoreoptimisticthanoutsidersandare

likelytobesubjecttoanoverconfidencebias,whichcouldleadtotoolittleconsolidation

effort.Theasymmetryhas thepotential tounderminea fiscal rule’seffectiveness:The

prevalentexpectationthatother jurisdictionsmightnotcomplycouldalsoweakenthe

perceivedpressurefortheownstate.

Ouranalysisallowsustodrawafewtentativeconclusionsthatshouldbetakenintoac‐

countinthedesignoffiscalrulesalsointheEuropeancontext.First,aweakinitialfiscal

situationisaburdenforrulecredibility.Thephasing‐inofanewruleshouldbeparal‐

leledbyattemptstoremoveoratleastreducetheproblemofunsustainablebudgetary

legaciessuchashighinitialdebt.Second,sub‐nationalrulesmightbeahelpfulcomple‐

menttoanationalruleinafederalcontextlikeGermanywherestateshavesubstantial

spendinganddeficitautonomy.Andthird,clearandcomprehensivesanctionsandcon‐

sequencesincaseofnon‐complianceareimportanttoanchorcomplianceexpectations.

30

References

Azzimonti,M.,Battaglini,M.andS.Coate "AnalyzingtheCaseforaBalancedBudgetAmendmenttotheU.S.Constitution",mimeo,2008.

Barro,R. J.andD.B.Gordon"APositiveTheoryofMonetaryPolicy inaNatural‐RateModel",JournalofPoliticalEconomy91(4),1983,589–610.

Besley,T.,Montalvo,J.G.andM.Reynal‐Querol“DoEducatedLeadersMatter?”,TheEconomicJournal121,2011,205–227.

Braun,D.“HowtoMakeGermanFiscalFederalismSelf‐Enforcing:AComparativeAna‐lysis“,ZeitschriftfürStaats‐undEuropawissenschaften2,2007,235‐262.

Buchanan, J.M. "Lagged implementationasanelement inconstitutional strategy",Eu‐ropeanJournalofPoliticalEconomy10,1994,11‐26.

Bundesministerium der Finanzen “Reform der verfassungsrechtlichen Verschul‐dungsregeln von Bund und Ländern, Die Empfehlungen der Föderalismusreform II“,MonthlyReportMarch2009,36‐44.

Ciaglia,S.andF.Heinemann“DebtRuleFederalism:TheCaseofGermany”,ZeitschriftfürStaats‐undEuropawissenschaften11(4),2013,570‐602.

Dahan,M. andM. Strawczynski “Fiscal Rules and Composition Bias in OECD Coun‐tries”,CESifoWorkingPaperSeries3088,Munich,2010.

Debrun,X. “Fiscal rules in amonetary union: a short‐run analysis”, Open EconomiesReview11(4),2010,323–358.

Debrun,X.,Moulin, L.,Turrini,A.,Ayuso‐i‐Casals, J. andM.S.Kumar “Tied to themast?NationalfiscalrulesintheEuropeanUnion”,EconomicPolicy23(54),2008,297–362.

Eichengreen,B.andT.Bayoumi“Thepoliticaleconomyoffiscalrestrictions:implica‐tions forEurope from theUnited States”, EuropeanEconomicReview38 (3–4), 1994,783–791.

EuropeanCouncil"StatementbytheEuroAreaHeadsofStateorGovernment,Brussels,December9,2011.

Feld,L.P.andG.Kirchgässner"OntheEffectivenessofDebtBrakes:TheSwissExperi‐ence", inR.Neckand J.‐E. Sturm (eds.), SustainabilityofPublicDebt, Cambridge,USA,MITPress,2008,223‐255.

Fink,A. andT.Stratmann“InstitutionalizedBailoutsandFiscalPolicy:ConsequencesofSoftBudgetConstraints”,mimeoApril2010.

Göhlmann,S.andR.Vaubel“TheEducationalandOccupationalBackgroundofCentralBankersandItsEffectonInflation:AnEmpiricalAnalysis”,EuropeanEconomicReview51(4),2008,925‐941.

Goodspeed,T. J. “Bailouts in a Federation”, International Tax and Public Finance, 9,2002,409–421.

Heinemann,F.andS.Osterloh “ThePoliticalEconomyofCorporateTaxHarmoniza‐tion‐WhyDoEuropeanPoliticians(Dis)likeMinimumTaxRates?”EuropeanJournalofPoliticalEconomy29,2013,18‐37.

31

Heinemann,F.,Osterloh, S.andA.Kalb “Sovereign Risk Premia: The Link betweenFiscalRulesandStabilityCulture”,JournalofInternationalMoneyandFinance41,2014,110‐127.

Heinemann, F. and E. Janeba “Viewing Tax Policy Through Party‐Coloured Glasses:WhatGermanPoliticiansBelieve”,GermanEconomicReview12(3),August2011,286‐311.

Heinemann,F., Janeba,E.,Moessinger,M.‐D.,Schröder,C.andF.Streif “Föderalis‐mus‐PräferenzenindendeutschenLandesparlamenten“,PerspektivenderWirtschafts‐politik,15(1),2014,56‐74.

Heinemann,F., Janeba,E.,Moessinger,M.‐D.andC.Schröder “RevenueAutonomyPreferenceinGermanStateParliaments”,ZEWDiscussionPaper,2013,No.03‐090.

Iara,A.andG.Wolff “RulesandRisk in theEuroArea”,European JournalofPoliticalEconomy34,2014,222‐236.

InternationalMonetary Fund “Balancing Fiscal Policy Risks”, Fiscal Monitor, April2012.

Janeba,E.andS.Osterloh“TaxandtheCity–Atheoryoflocaltaxcompetitionandevi‐denceforGermany”,JournalofPublicEconomics106,2013,89‐100.

Janeba, E. “Germany’s New Debt Break Rule: A Blueprint for Europe?” Finanzar‐chiv/PublicFinanceAnalysis68(4),2012,383‐405.

Kirchgässner,G. ”TheEffectsofFiscal InstitutionsonPublicFinance:ASurveyof theEmpiricalEvidence”, in:S.L.WinerandH.Shibata (eds.),PoliticalEconomyandPublicFinance:TheRoleofPoliticalEconomyintheTheoryandPracticeofPublicEconomics,EdgarElgar,Cheltenham2002,S.145‐177.

Krogstrup,S.andS.Wälti “Do fiscal rulescausebudgetaryoutcomes?”PublicChoice136(1),2008,123–138.

Kydland, F.E. and E.E.Prescott “Rules Rather than Discretion: The Inconsistency ofOptimalPlans”,TheJournalofPoliticalEconomy,85/3,1977,473‐492.

Lagona,F.andF.Padovano“Anonlinearprincipalcomponentanalysisoftherelation‐shipbetweenbudgetrulesandfiscalperformanceintheEuropeanUnion,”PublicChoice130(3–4),2007,401–436.

Little,RandS.Vartivarian“DoesWeightingforNonresponseIncreasetheVarianceofSurveyMeans?”,Michigan,September2005.

Moessinger,M.‐D.“DothePersonalCharacteristicsofFinanceMinistersAffectChangesofPublicDebt?”,PublicChoice,2014,DOI10.1007/s11127‐013‐0147‐x.

Moore,D.A.and J.P.Healy “TheTroublewithOverconfidence”,PsychologicalReview115,2008,502‐517.

Poguntke,T.”PartiesinaLegalisticCulture:TheCaseofGermany”,in:R.S.KatzandP.Mair(eds.),HowPartiesOrganize,SagePublications,London,1994,185–215.

Poterba,J.M.“BudgetinstitutionsandfiscalpolicyintheU.S.states”,AmericanEconom‐icReview86(2),1996,395–400.

Roberts,G. ‘TheGerman Federal Republic: TheTwo‐LaneRoute toBonn’, in:M. Gal‐lagherandM.Marsh(eds.),CandidateSelectioninComparativePerspective,Sage

32

Publications,London,1988,94–118.

Sachverständigenrat “Verantwortung für Europa wahrnehmen – Jahresgutachten2011/12“,SachverständigenratzurBegutachtungdergesamtwirtschaftlichenEntwick‐lung,Wiesbaden,2011.

Voigt, S. and L.Blume “The Economic Effects of Constitutional Budget Institutions”,mimeo.2011.

33

AppendixA.TablesTableA1:IndividualandStateVariables

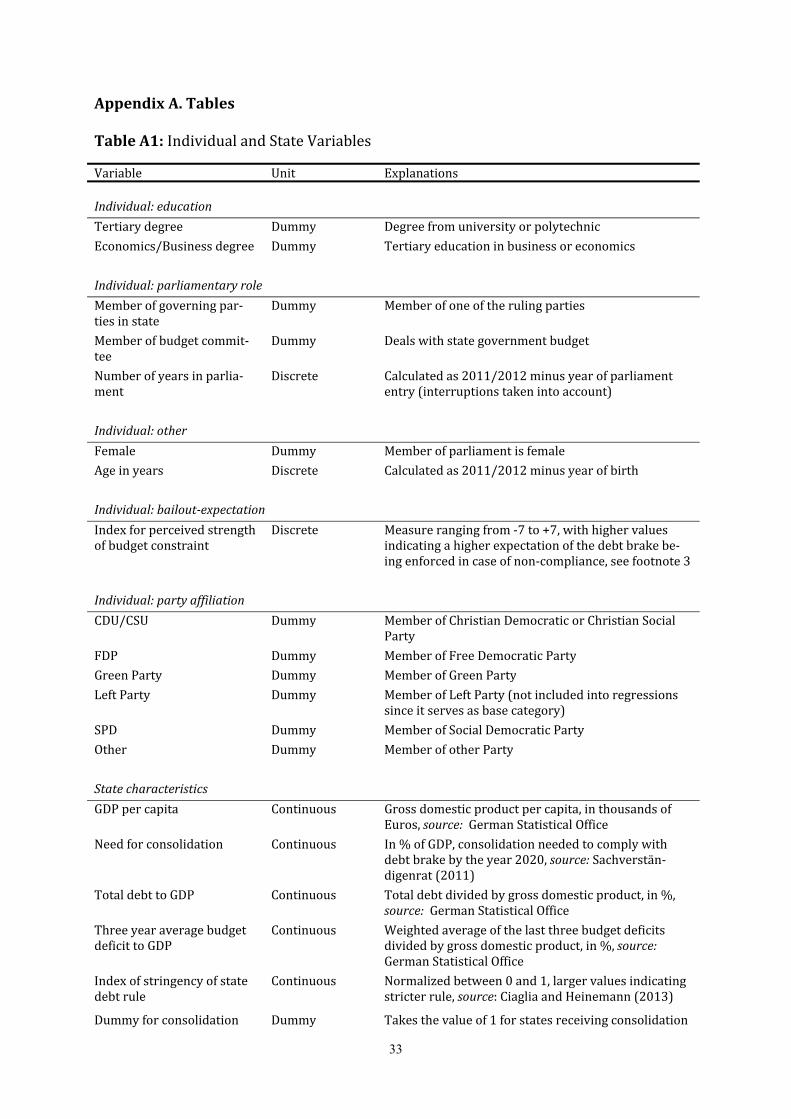

Variable Unit Explanations Individual:education

Tertiarydegree Dummy Degreefromuniversityorpolytechnic

Economics/Businessdegree Dummy Tertiaryeducationinbusinessoreconomics

Individual:parliamentaryrole

Memberofgoverningpar‐tiesinstate

Dummy Memberofoneoftherulingparties

Memberofbudgetcommit‐tee

Dummy Dealswithstategovernmentbudget

Numberofyearsinparlia‐ment

Discrete Calculatedas2011/2012minusyearofparliamententry(interruptionstakenintoaccount)

Individual:other

Female Dummy Memberofparliamentisfemale

Ageinyears Discrete Calculatedas2011/2012minusyearofbirth

Individual:bailout‐expectation

Indexforperceivedstrengthofbudgetconstraint

Discrete Measurerangingfrom‐7to+7,withhighervaluesindicatingahigherexpectationofthedebtbrakebe‐ingenforcedincaseofnon‐compliance,seefootnote3

Individual:partyaffiliation

CDU/CSU Dummy MemberofChristianDemocraticorChristianSocialParty

FDP Dummy MemberofFreeDemocraticParty

GreenParty Dummy MemberofGreenParty

LeftParty Dummy MemberofLeftParty(notincludedintoregressionssinceitservesasbasecategory)

SPD Dummy MemberofSocialDemocraticParty

Other Dummy MemberofotherParty

Statecharacteristics

GDPpercapita Continuous Grossdomesticproductpercapita,inthousandsofEuros,source:GermanStatisticalOffice

Needforconsolidation Continuous In%ofGDP,consolidationneededtocomplywithdebtbrakebytheyear2020,source:Sachverstän‐digenrat(2011)

TotaldebttoGDP Continuous Totaldebtdividedbygrossdomesticproduct,in%,source:GermanStatisticalOffice

ThreeyearaveragebudgetdeficittoGDP

Continuous Weightedaverageofthelastthreebudgetdeficitsdividedbygrossdomesticproduct,in%,source:GermanStatisticalOffice

Indexofstringencyofstatedebtrule

Continuous

Normalizedbetween0and 1,largervaluesindicatingstricterrule,source:CiagliaandHeinemann(2013)

Dummyforconsolidation Dummy Takesthevalueof1forstatesreceivingconsolidation

34

assistance assistance

Fiscalequalizationtransferstototalspending

Continuous Totalnetintra‐statetransferpaymentsdividedbytotalspending,in%,sources:FederalMinistryofFinance,GermanStatisticalOffice

Governmentcoalitioncon‐sistsofrightparties

Dummy Takesthevalueof1forapurelyright‐leaninggov‐ernment(coalition),avalueof0.5foramixedgov‐ernmentcoalitionandavalueof0forapurelyleft‐leaninggovernment(coalition)

Crossstatedimension

Distance Continuous Distancein100kmbetweenanytwostatecapitalcities

Adjacency Dummy Takesonthevalueof1 ifthehomestateofthere‐spondentandthestatetobeevaluatedshareacom‐monborder(andifthestatetobeevaluatedisthehomestateoftherespondent)

Ownstate Dummy Takesonthevalueof1 ifthestatetobeevaluateditthehomestateoftherespondent

TableA2:Cross‐statecomplianceexpectations

Evaluatedstates BB BE BW BY HB HE HH MV NI NW RP SH SL SN ST TH ∅

Evaluatingstates

BB 53 5 68 89 0 58 53 11 37 16 32 5 11 68 16 37 35BE 13 33 70 73 0 67 37 30 47 10 23 13 10 57 27 50 35BW 5 0 75 93 1 58 22 16 17 9 19 8 4 71 5 19 26BY 3 3 57 89 3 53 21 4 25 5 17 7 4 61 5 32 24HB 11 0 67 72 11 56 28 28 50 11 28 6 6 56 28 22 30HE 10 2 56 76 2 78 26 18 34 10 16 8 8 58 16 32 28HH 21 8 72 74 0 62 67 31 44 15 36 8 3 54 21 28 34MV 6 0 72 78 0 53 41 83 24 0 12 0 6 78 12 29 31NI 4 0 74 91 2 57 24 19 56 11 26 11 6 54 20 26 30NW 6 4 67 82 0 53 10 24 45 16 29 10 4 61 20 31 29RP 14 0 76 78 4 64 28 20 36 14 52 12 4 64 22 40 33SH 10 7 65 86 10 55 17 24 38 10 21 66 10 52 28 31 33SL 20 5 95 100 5 85 45 20 55 10 35 20 30 55 25 35 40SN 11 0 67 80 2 42 11 29 20 0 13 4 0 89 16 42 27ST 24 3 76 83 7 52 28 45 35 14 28 17 17 72 59 45 38TH 22 11 67 97 11 69 22 31 47 19 33 28 11 89 28 47 40

∅MSP∅State

12 4 69 85 3 59 27 23 36 10 26 13 7 65 19 33 3115 5 70 84 4 60 30 27 38 11 26 14 8 65 22 34 32

#oftimeswhereout‐sidersaremoreopti‐misticthaninsiders

0 0 3 4 0 1 0 0 0 1 0 0 0 0 0 1

Note:FiguresareinpercentandindicatetheshareofMSPswhoexpectthattheevaluatedstatewillbecompliant.∅MSPindicatestheaverageoverallMSPs.∅Stateindicatestheunweightedaverageoverthestatefigures.

35

TableA3: LikelihoodofAnyState’sCompliance–RobustnessChecks1(alternativevar‐iables)

Probitregressionswithcomplianceexpectationasdependentvariable(1:complianceexpected,0:notexpected) (1) (2)

IndependentVariables

Baseline1(withtotaldebt)

Averagemarginaleffects

Baseline1(withbudgetdeficit)

Averagemarginaleffects

Individidual:education Tertiarydegree 0.023 0.006 0.023 0.006

[0.035] [0.009] [0.035] [0.010]

Economics/Businessdegree 0.038 0.010 0.037 0.010[0.039] [0.011] [0.039] [0.011]

Individual:parliamentaryrole Memberofgoverningpartiesinstate(H4) 0.127*** 0.034*** 0.106** 0.029**

[0.046] [0.012] [0.049] [0.013]

Memberofbudgetcommittee ‐0.152*** ‐0.041*** ‐0.149*** ‐0.041***[0.039] [0.011] [0.039] [0.011]

Numberofyearsinparliament ‐0.006*** ‐0.002*** ‐0.006*** ‐0.002*** [0.002] [0.001] [0.002] [0.001]

Individual:other Female ‐0.105*** ‐0.028*** ‐0.106*** ‐0.029***

[0.033] [0.009] [0.032] [0.009]

Ageinyears 0.002* 0.001* 0.002* 0.001*[0.001] [0.000] [0.001] [0.000]

Individual:bailout‐expectation Indexforperceivedstrengthofbudgetconstraint(H2) 0.063*** 0.017*** 0.062*** 0.017***

[0.005] [0.001] [0.005] [0.001]

Individual:partyaffiliationa CDU/CSU ‐0.110 ‐0.030 ‐0.103 ‐0.028

[0.068] [0.018] [0.067] [0.018]

SPD ‐0.177** ‐0.048** ‐0.167** ‐0.046** [0.074] [0.020] [0.073] [0.020]

GreenParty 0.047 0.013 0.046 0.013 [0.088] [0.024] [0.087] [0.024]

LeftParty 0.103 0.028 0.097 0.026[0.085] [0.023] [0.085] [0.023]

OtherParties ‐0.115 ‐0.031 ‐0.117 ‐0.032[0.128] [0.034] [0.126] [0.034]

Statecharacteristicsb GDPpercapita(H1) 0.022*** 0.006*** 0.027*** 0.007***

[0.005] [0.001] [0.005] [0.001]

TotaldebttoGDP(H1) ‐0.053*** ‐0.014*** [0.005] [0.001]

Averagebudgetdeficitoverlastthreeyears(H1) ‐0.314*** ‐0.086*** [0.034] [0.009]

Debtruleindex(H3) 0.896*** 0.241*** 2.581*** 0.706*** [0.324] [0.087] [0.285] [0.077]

Dummyforconsolidationassistance ‐0.100 ‐0.027 ‐0.734*** ‐0.201***[0.117] [0.031] [0.094] [0.025]

FiscalequalizationtransferstoGDP 0.148*** 0.040*** ‐0.315*** ‐0.086*** [0.053] [0.014] [0.051] [0.014]

Governmentcoalitionconsistsofrightparties 0.145* 0.039* 0.590*** 0.161***[0.075] [0.020] [0.073] [0.020]

Crossstatedimension Ownstate(H4) 0.627*** 0.169*** 0.731*** 0.200*** [0.106] [0.028] [0.129] [0.035]

Distance ‐0.015 ‐0.004 0.011 0.003 [0.021] [0.006] [0.025] [0.007]

Adjacency 0.147** 0.040** 0.136* 0.037* [0.073] [0.020] [0.083] [0.023]

Homestatefixedeffects Regressiondiagnostics: Observations 10,224 10,224Pseudo‐R2 0.253 0.242p‐valuejointsignificanceofallvariables 0.000 0.000p‐valuejointsignificanceofallindividualvariables 0.000 0.000p‐valuejointsignificanceofparty‐dummies 0.000 0.000p‐valuejointsignificanceofstatecontrols 0.000 0.000p‐valuejointsignificanceofcrossstatevariables 0.000 0.000Notes:*/**/***denotesignificanceatthe10%/5%/1%level;Standarderrorsinbrackets;abasecategoryisthemarketorientedliberaldemocraticparty“FDP”;bStatecharacteristicsare2010dataforsurveywaves1and2,whichbothtookplacein2011,and2011dataforsurveywave3,whichtookplacein2012.

36

TableA4: LikelihoodofAnyState’sCompliance–RobustnessChecks2(Weighting)

Probitregressionswithcomplianceexpectationasdependentvariable(1:complianceexpected,0:notexpected) (1) (2)

IndependentVariables

Baseline1(Weightedregression)

Averagemarginaleffects

Baseline1(Weightedregression)

Averagemarginaleffects

Individidual:education Tertiarydegree 0.008 0.002 0.009 0.002

[0.039] [0.011] [0.040] [0.011]

Economics/Businessdegree 0.077* 0.021* 0.076* 0.021*[0.042] [0.012] [0.042] [0.012]

Individual:parliamentaryrole Memberofgoverningpartiesinstate(H4) 0.138*** 0.038*** 0.140*** 0.039***

[0.047] [0.013] [0.047] [0.013]