Embed Size (px)

DESCRIPTION

Bertelsmann Foundation Project Manager Samuel George and World Bank Associate Cornelius Fleischhaker lay out in this report the five measures that President Dilma Rousseff's second administration needs to take to spur Brazilian economic growth. These measures would help restore the dynamism that characterized the country in the early years of the 21st century before Brazil's current period of mediocre performance set in.

Citation preview

by Samuel George and Cornelius Fleischhaker

Table of Contents

The Country of Tomorrow, Today .................................. 5

1. Restore Fiscal Discipline ......................................... 7

2. Controlling Inflation............................ .................. 9

3. Closing the Infrastructure Gap ............................. 11

4. Educating a 21st-Century Workforce..................... 13

5. Opening Trade, Sparking Productivity ................... 15

The Country of Tomorrow, Tomorrow ............................ 17

Five Steps to Kickstart Brazil

11

22

Samuel George is the Latin America Project Manager with the Bertelsmann Foundation’s Global Economic Dynamics team. His previous studies include The Pacific Pumas: An Emerging Model for Emerging Markets (2014), Surviving a Debt Crisis: Five Lessons for Europe from Latin America (2013) and Brazil and Germany: A 21st-Century Relationship (2014, co-author).

Cornelius Fleischhaker is a junior professional associate specializing in Brazil at the World Bank. He previously worked as a research analyst at the International Monetary Fund. The opinions expressed here are his own and do not reflect those of the World Bank.

About the Authors / Foreword

About the Authors

The Bertelsmann Foundation expanded in 2012 its scope of trans-Atlantic relations to include Latin America in addition to the United States and Europe. This perspective stems from the belief that no single set of countries can lead the global economy in the 21st century. Rather, global growth may depend on the interaction of developed-world experience with emerging-market dynamism.

While our coverage of Latin America has been diverse, ranging from the Pumas of the Pacific Alliance to the depths of the 1980s debt crisis, Brazil engenders particular interest. South America’s BRIC has taken tremendous strides in recent years, but the country’s massive untapped potential captivates minds from Brasília to Washington to Brussels.

To explore Brazil’s importance, the Bertelsmann Foundation has a strategic partnership with the Fundação Getulio Vargas. The cooperation has led to the collaborative study Brazil and Germany: A 21st-Century Relationship Opportunities in Trade, Investment and Finance. This report underscores the opportunities that Brazil’s weighty economic potential could create for the rest of the world.

But what about the opportunities Brazil’s weighty economy represents for Brazilians? And how are these opportunities being managed? In this working paper, we take a closer look at the loss of Brazil’s economic momentum and offer five steps to get it back.

Annette Heuser Andreas EscheExecutive Director DirectorBertelsmann Foundation Bertelsmann Stiftung

February 2015

Foreword

33

44

8

6

4

2

0

-2

-4

Three-year average difference Brazil World

1994 2004 2009 20141999

The Country of Tomorrow, Today

The Country of Tomorrow, Today

On October 26, 2014, 108 million Brazilians voted in the second and final round of the country’s presidential election. Incumbent Dilma Rousseff defeated challenger Aécio Neves by a slim but definitive margin (52 percent to 48 percent), earning her a second term in office through 2018. The results suggest that the election was not about change but rather about continuation — the continuation of helping Brazil’s new middle class pursue upward mobility.

Over the last 20 years, Brazil has taken crucial strides towards achieving its weighty, if elusive, economic potential. Finance Minister (later President)

Fernando Henrique Cardoso’s Real Plan established a stable macroeconomic foundation in the 1990s, which allowed his successor, President Luiz Inácio Lula da Silva, to implement social programs that helped lift upwards of 40 million people out of poverty in the 2000s.

Strong growth gave Brasília fiscal leeway during the global financial crisis; an aggressive stimulus package in 2009 led to claims that Brazil was the last country in and first country out of the Great Recession. Investment poured in, and many wondered if a new day had finally dawned for the perennial “country of the future”.

Since 2011, however, Brazil’s burgeoning middle class has faced growing pains. For tens of millions of nouveau stable, simply participating in the country’s economy is no longer enough. They seek continued access to opportunity, and they fear a return to poverty.

A stagnating economy spurs disquiet. Growth, which averaged 4.5 percent annually from 2004 through 2010, has averaged just 1.6 percent since. When hundreds of thousands took to the streets to protest in 2013, and when 108 million people voted in October 2014, they demanded improved efficiency, transparency and, above all, a return to growth.

Brazilian Growth (Percent Change)

Source: IMF Data

55

WHAT HAppEnEd To BrAzil’s momEnTum?Prior to offering any prescription, we must consider the underlying cause of low growth.

International observers often attribute the Brazilian slowdown (current and expected), to a shifting external environment as commodi ty p r i ces and international financial conditions become less favorable. Much has been made of the risk of an economic “hard landing” in China and its potentially devastating consequences for the Latin American BRIC.

But this view has one major fallacy: External demand constitutes only a fraction of the Brazilian economy. Brazilian exports account for just 12 percent of GDP; in Mexico, by contrast, this figure eclipses 30 percent. Exports to China make up about a fifth of total Brazilian exports, accounting for less than three percent of GDP. A downward trend in commodity prices hurts, to be sure, but alone it cannot explain Brazil’s sluggish performance.1

Analysts also cite the absence of structural reforms, along the lines of what Mexican President Enrique Peña Nieto has pursued during his sexenio. Such reforms would address taxes, infrastructure, labor regulation and the overall business environment. Brazil would certainly benefit from such reforms, but somehow the country managed explosive growth from 2004 to 2010 without much progress on this front.

So why is the economy grinding to a halt now?

Imagine an economy as a shellfish, where the supply or production capacity is the shell and demand is the body filling the shell. The body can grow unimpeded as long as there is space left in the shell (economists call this space “slack” or “output gap”). At the same time, the productive capacity (the “shell”) can also grow by adding workers, by adding capital or by using the two more efficiently (total factor productivity).

In Brazil, the boom years started with plenty of wiggle room in this metaphorical shell. Lula-

era momentum can partially be attributed to a series of one-off events: the rapid rise of China, the commodity super-cycle, and the lifting of millions out of poverty and into formal employment.

These trends allowed Brazil to rapidly fill the output gap. At the same time, however, a growing labor force increased the size of the shell itself, and for several years the country was able to accommodate expanding demand. High growth observed in the 2000s was thus a transitional phenomenon that was bound to end in the absence of productivity-enhancing reforms regardless of the external environment.

This insight guides our prescription for a return to growth. Brazil’s malaise is nothing new, and it is not the outside world’s fault. Rather, it stems from a persistent need for improved efficiency and productivity. In her second administration, President Rousseff has an opportunity to pursue such ends.

Here are five ways to accomplish that:

66

Primary Balance Overall Balance Primary Surplus Target

MARCH2011

JUNE2011

SEPT.2011

DEC.2011

MARCH2012

JUNE2012

SEPT.2012

DEC.2012

MARCH2013

JUNE2013

SEPT.2013

DEC.2013

MARCH2014

JUNE2014

SEPT.2014

DEC.2014

4

3

2

1

0

-1

-2

-3

-4

-5

-6

-7

4

3

2

1

0

-1

-2

-3

-4

-5

-6

-7

1. Restore Fiscal Discipline

In November 2014, President Dilma Rousseff named former Treasury Secretary Joaquim Levy as her next finance minister. Both financial markets and economic analysts welcomed the appointment given Levy’s strong reputation as a skilled, orthodox economist and as a capable administrator. Levy has promised to restore fiscal balance in Brazil, but his job will not be easy.

Fiscal policy is at the heart of the current Brazilian malaise. Over the past decade, Brazil has parlayed strong growth into expansionary fiscal policy. Government spending leapt from 36 percent of GDP in 2004 to nearly 42 percent in 20142, financed in part by increasing revenues due to

the global commodity boom. This level of spending generally exceeds that of other upper-middle-income economies, but it was not alarming as long as growth was strong and Brazil’s terms of trade remained robust.

Yet while revenues have recently tapered, spending has not. The primary (pre-interest) surplus target, a crucial pillar of Brazil’s tripod3 of macroeconomic stability, has been continuously lowered and missed since 2011. In 2014 Brazil’s primary surplus flipped to a deficit for the first time since this measure was adopted in the 1990s. Meanwhile, rising interest costs have pushed the overall budget deficit to 6.7 percent of GDP. Brazil’s fiscal position will

face further stress given the country’s expanding debt portfolio, which has jumped from 53.4 percent of GDP in 2010 to 63.4 percent of GDP by the close of 2014.4

Deteriorating fiscal conditions create a negative environment for growth. As public-sector debt absorbs a greater percentage of precious savings, even fewer resources will be available for productive investment. Moreover, fiscal uncertainty could scare off market investors just when Brazil needs them most. Speculation already abounds that the country could lose its investment-grade status conferred by the big three credit-rating agencies. Another downgrade (S&P downgraded

Restore Fiscal Discipline1

Off Target: Brazil’s Public Spending

Source: Central Bank of Brazil

(Per

cent

of G

DP)

77

Brazilian sovereigns to a notch above junk in March 2014) could lead to still higher interest rates and make growth opportunities even more scarce.

Not all public spending in Brazil is wasteful. In fact, some government programs set global standards in terms of efficiency. For example, Bolsa Família, a conditional cash transfer program, benefits roughly 13 million poor families at the cost of just 0.5 percent of GDP. The Partido dos Trabalhadores (PT) governments of the past 12 years have also increased spending on health and education, achieving important advances, though the quality relative to cost remains low. Still it is not difficult to identify bloated line items on the public books, starting with the whopping 39 federal ministries, exorbitant public-sector pensions, and white-elephant projects such as an unfinished alien museum.5

Brasília will face structural challenges even if there is a concerted effort to cut the pork. Fiscal consolidation in times of lean growth is never easy. For example, since 2011, the government offered selective tax breaks for struggling industrial sectors. The idea was to spark growth, but state coffers took a hit while coddled sectors continued to lay off workers.6

Meanwhile, rolling back popular but costly programs implies significant political risk. In the summer of 2013, a modest 10-US-cent (R$ 0.20) hike in São Paulo’s bus fares ignited protests that brought millions to the streets, shaking Brazil to its core.7 Revising price freezes on electricity, for example, could prove similarly unpopular, though the new administration has announced plans to do just that.8

Finally, the government has provided large resources to public

banks, chiefly the Banco Nacional de Desenvolvimento Econômico e Social (BNDES), the massive national development bank. These off-budget (“below the line”) operations are not fully reflected in the primary surplus but ultimately have a significant fiscal cost as the treasury is forced to borrow at rates much higher than what it receives on its subsidized loans to BNDES.

EvEning THE sCAlEsThe new Rousseff administration must set a direction early, ideally with a multi-year plan of fiscal consolidation that begins with a focus on transparency. Since 2011, Brasília has leaned on various accounting measures to manipulate headline fiscal results, making the reported numbers increasingly irrelevant. For example, the 2014 the primary surplus target (1.9 percent of GDP) was eventually discarded altogether, allowing the government to deliver a deficit. The new administration should present a transparent and realistic picture of fiscal accounts, including below-the-line items. The announcement of ambitious but realistic primary surplus targets for 2015 and 2016 (1.2 and 2.0 percent of GDP respectively) is an important first step. Similarly, the announcement of initial measures to contain spending and raise revenue sends positive signals. However these moves alone do not yet add up to a coherent plan to restore fiscal balance.

A significant tax reform, which has been debated since the 1990s, would be a crucial second step. Brazil currently has a bizarre system of state-level value-added taxes based on the place of production. This model leads to high compliance costs: Mid-sized companies spend 2,600 growth-killing hours a year in tax-related work.9 The convoluted structure also generates market distortions as businesses choose

their locations based on taxation rather than economic efficiency. A tax reform that unifies value-added taxes would lower growth-dampening compliance costs and distortions. Given current fiscal conditions, an outright tax cut is not advisable. But a revenue-neutral reform should lower overall costs for business.

In the long term, pension reform could defuse a fiscal time bomb while encouraging savings. Brazil already spends as much of its national income on pensions as do richer and older European countries.10 As Brazil ages, pension expenditures will expand exponentially, crowding out other social spending and investment.

Moving away from the current pay-as-you-go system towards a capital-backed system could also help increase Brazil’s chronically low savings rate. Currently, those with higher incomes — the people who are actually in a position to save — often have little incentive to do so as they can simply await generous pensions that will weigh heavily on the state’s fiscal balance. A targeted reform could lower transfers to the wealthy while still protecting poorer retirees and easing the mounting pressure on the government’s books.

Brazil’s fiscal unraveling has been years in the making, and it will likely require several years to fix. While some costly policies could be rapidly addressed, the markets should be patient. Nevertheless, if President Rousseff sets a clear tone of fiscal consolidation early in her second term, she will ease short-term market jitters and position her country for long-term sustainability.

Fiscal reforms were always unlikely in 2014 — an election year for a left-leaning president. There is no such excuse in 2015.

88

TARGET BAND

10

9

8

7

6

5

4

3

2

1

0

10

9

8

7

6

5

4

3

2

1

0

DECEMBER2011

JUNE2012

DECEMBER2012

JUNE2013

DECEMBER2013

DECEMBER2014

JUNE2014

Headline Inflation Tradables Non-tradables Regulated

Brazil fought hard for macroeconomic stability in the 1990s. That effort must not go to waste.

At 6.4 percent, inflation ended 2014 barely below the country’s upper target-rate limit and has been near or above it for four years, creating a perception of inflation tolerance and, consequently, de-anchoring inflation expectations.

The bad news is that inflationary pressures will remain pronounced in 2015, given the recent depreciation of the real (roughly 12 percent over the past year)11 and the need to further raise domestic energy prices to bring them in line with the cost of production. Thus,

the 4.5-percent inflation target will likely remain out of reach in the near term, even if the Central Bank continues to raise interest rates.

I n c r e a s i n g m a c r o e c o n o m i c instability has a drag on growth. Inflation translates to constant appreciation pressure on the real exchange rate as the prices of Brazilian goods and services rise faster than prices elsewhere. This hampers the competitiveness of Brazilian firms, which in turn stifles growth.

Furthermore, once inflation takes hold, the medicine can do as much as harm as the ailment. Since 2012, in an effort to curtail rising prices, Brasília has set prices artificially

low on goods administered by the government such as fuel, electricity and public transportation. This created significant distortions in the economy. For example, the price freeze on fuel has challenged the ability of Petrobras (the state-owned oil company) to invest in oil exploration and infrastructure. At the same time, the policy severely damaging the once booming sugarcane-ethanol industry.

Most importantly, inflation hurts the poor who operate in cash and depend on the purchasing power of their earnings to make ends meet. The recent uptick in extreme poverty is a development of concern in this context.12

Controlling Inflation2

Inflation in Brazil (Annual Percentage)

Source: Central Bank of Brazil

2. Controlling Inflation 99

sETTing A nEW CoursEAs on the fiscal front, the first step to restore stability in the medium term is to recover credibility. While inflation may continue to run above target in the medium term, the authorities must send a strong signal that inflation will be controlled in a realistic timeframe through an appropriate mix of monetary and fiscal policies, and not through price fixes. This strategy has previously proved ineffective in Brazil.13

The Central Bank should be guaranteed the operational autonomy to bring inflation back to target in the medium term. Fiscal policy, quasi-fiscal operations through state-owned banks (especially BNDES), and government intervention in the credit market should support the inflation-control effort rather than contradicting it, as has been the case in recent years.

Controlling inflation without artificially setting prices will benefit growth in a number of ways. First, it would reduce the uncertainty under which investors and regular Joãos make decisions. Investors will be more willing to invest in productive assets, such as ethanol or electricity, if they can be assured that government intervention will not wash away their returns. Middle-class citizens will be better positioned to plan for the future if they know the purchasing power of their salaries will be protected.

Second, controlling inflation would help address the eternal dilemma of the Brazilian economy: low savings at the world’s highest interest rates (in mid-2014, the average lending rate for non-directed credit was more than 40 percent14).

Both these trends stem in part from the threat of inflation. There is

little incentive to save if that effort can erased by a bout of inflation. Meanwhile, the high interest rates reflect a risk premium associated with mistrust in the government’s ability to hit inflation targets.

If the new Rousseff administration can reaffirm the Central Bank’s autonomy while reining in government spending, inflation will come down eventually. Over the long run, Brazil’s absurdly high interest rates will follow suit. But such results require prudent macroeconomic management. They cannot be achieved through shortcuts.

1 01 0

From unpaved streets in the northeast to the overburdened ports of Santos, Brazil’s infrastructure deficit is ubiquitous and costly. Brazilian fields produce grain twice as fast as those elsewhere, but getting that grain to port can cost almost half its value. Meanwhile, vast mineral deposits remain buried deep within the earth (and vast numbers of people remain buried deep in São Paulo’s traffic) for want of better transportation.

Though Brazil has the world’s sixth largest economy, the 2013-2014 World Economic Competitiveness Report ranked the country 71st in terms of infrastructure.15 Investment in Brazilian infrastructure amounts to roughly 2.45 percent of GDP, short of the estimated three percent required simply to maintain the existing stock.16 Investment in Brazilian infrastructure is below the emerging-market average and a far cry from the levels of other major economies, which typically spend five to seven percent of GDP annually on infrastructure.17

This deficit hampers growth in established sectors and prevents full exploitation of new ones. Accessing the tremendous deep-sea oil fields off the Brazilian coast, for example, will require major investment. Excavation of the so-called “pre-sal” reserves presents significant engineering challenges and requires advanced infrastructure that could cost as

much as US$400 billion.18

Where this investment will come from remains to be seen. Recent developments have complicated the matter: Lower global oil prices could reduce interest in Brazil’s relatively expensive deep-sea reserves, while a corruption scandal has shaken Petrobras to its core.

Petrobras, for its part, was expected to contribute significantly, but the state-owned oil giant is suffering from the fuel price freeze and is buckling under a heavy debt load. Brazil also expected strong interest from foreign investors, but auctions so far have disappointed.19

Building BrAzilThe good news is that addressing the infrastructure gap can result in large gains for the economy. But Brazil must develop a long-term strategy. Projects associated with the recent World Cup and the upcoming Summer Olympic Games provide, at best, partial and short-term solutions. Meanwhile, chunks of the government’s PAC II infrastructure investment package, valued at US$885 billion, are earmarked for other problems, such as housing.20

This investment is crucial but cannot alone pave the way for future growth.

A long-term infrastructure plan that will kick-start growth should

focus on transportation — and not just roads. A 2013 study by Pricewaterhou se C o opers highlights the importance of freight rails and waterways as more efficient than roads for transporting goods in Brazil. With more than 17,000 miles of navigable water, moving 1,000 tons one kilometer by ship costs roughly a quarter of moving it by highway.21 Yet, with most of these waterways set deep within Brazil’s underdeveloped north and northeast, just one percent of the country’s freight volume is shipped this way.22 Developing waterway and railway infrastructure could improve transport efficiency and facilitate economic inclusion, two trends that would translate to increased growth.

Modernized ports can also expand Brazil’s export capacity. Prior to going bankrupt, Brazilian entrepreneur Eike Batista dreamed of a super-port that combines expanded capacity with on-site production facilities. Such a port would ensure that Brazil plays a role in processing — as opposed to simply exporting — commodities. Batista may no longer be in a position to execute such a strategy, but it is not a bad one.

The key question is who will finance these projects. BNDES currently plays a dominant role in underwriting infrastructure

Closing the Infrastructure Gap3

3. Closing the Infrastructure Gap 1 11 1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

0

20

40

60

80

100

investment.23 However, with a loan-portfolio value that eclipses that of the World Bank, BNDES may be crowding out private investment by creating an atmosphere of artificially low yields. Investors could be further put off by the belief that close ties to power are required to secure subsidized BNDES loans.24

These deterrents to private investment are concerning as,

simply put, the state cannot do it alone. BNDES has already proved incapable of single-handedly closing Brazil’s infrastructure deficit. Given forthcoming fiscal constraints, Brazil needs to involve the private sector.

Fortunately, investors worldwide have shown keen interest in Brazil, as demonstrated by continued FDI inflows. Securing this investment, however, will require an improved

framework for public-private partnerships and the removal of procedural burdens that slow down projects (the infamous custo Brasil).

If the second Rousseff administration can attract and manage high quality infrastructure investment, Brazil can clearly expand its production capacity, expanding the economy’s “shell” and generating room for growth.

Foreign Direct Investment in Brazil, Net Inflow - US$ (Billions, Current Prices)

Source: World Bank WDI Data

The Good News: Investors Still Want In

1 21 2

The 2007 discovery of the enormous pre-sal oil reserves off of Brazil’s coast appeared to represent a transformative moment for the South American giant. With the country already in the thick of a growth spurt, the finds suggested Brazil’s total reserves rival those of the North Sea. For President Rousseff, the fields offered “strong evidence that God is Brazilian.”25

In the wake of the discovery, Brazil implemented stiff local content laws for the advanced machinery and labor required to access oil wells more than 150 miles off the coast and buried beneath 3,000 meters of salt, rock and ocean. Contracts offered at auction in 2013 required “37 percent local content for goods and services used in the exploration phase, rising to 55 percent in the development phase and 59 percent after 2022.”26

The government’s approach arguably had Brazil’s best interest at heart: In theory, these local-content laws could stimulate domestic production and create valuable backward linkages. But the proponents of the strategy overlooked one crucial factor: Brazil lacks the educated workforce (in depth and breadth) to pull off such a complicated project alone. The domestic labor market’s inability to deliver is often cited as an explanation for delays in pre-sal oil excavation.

If Brazil wants to be a 21st-century

leader, it must educate a 21st-century workforce. The country has made impressive progress in education. Presidents Cardoso, Lula and Rousseff have pushed for universalized access to primary education. Cardoso raised teachers’ salaries and increased public-school funding. Lula’s cash transfer programs were conditional upon classroom attendance. He also emphasized the importance of technology in the classroom. President Rousseff has invested in vocational schools, especially in the underdeveloped northeast.

These improvements notwithstanding, the quality of Brazilian education remains poor by international standards. Primary and secondary institutions have struggled to prepare students to enter the workforce or to move on to higher education. Two-thirds of Brazilian teens can do little more than basic mathematics, while 50 percent have underdeveloped reading comprehension skills.27

Education expectations can differ widely across race and region: White Brazilians average more than eight years of education, while black students average six. Regionally, students from the southeast average more than seven years of education, while those in the poorer northeast average just five.

Most of the Brazil’s best universities are public and free. But

this system generates a regressive subsidy, as richer students from private secondary institutions tend to win spots at top-notch public universities, which they then attend on the taxpayers’ dime. Overall only 12 percent of the working-age population has a university degree — significantly below the OECD-average of 32 percent.28 Few of these individuals pursue the scientific degrees required to execute modern infrastructure projects, let alone to get oil from the bottom of the ocean.

KiCK-sTArTing EduCATion: iT’s morE THAn monEyUnfortunately, addressing the education gap requires a more nuanced approach than simply throwing money at the problem. Brasília already invests a reasonable amount in education. As of 2013, the country spent 5.6 percent of GDP on education — more than the OECD average, and up from 3.8 percent in 2002.29 This figure is set to jump to a globally unprecedented 10 percent by 2020.30

While more funding never hurts, Brazil’s key to building a qualified workforce lies in improved efficiency. A 2012 World Bank report highlights problems stemming from poor teacher quality (despite increasing salaries), outdated curricula and misallocated spending.

Educating a 21st-Century Workforce4

4. Educating a 21st-Century Workforce 1 31 3

In terms of teacher quality, rigid labor laws make it difficult to remove ineffective teachers. But limited opportunities for substantive wage increases make it difficult to reward effective teachers. In terms of curricula, Brazil invests in innovative p rograms (such as Lu la ’s one-laptop-per-child initiative), but the state does not have a comprehensive mechanism to determine which programs work best and are cost-effective.31 Regarding resource allocation, Brazil spends six times as much on

a student in university as it does on a student in primary school (the OECD average is 2-to-1).32 This spending disparity exacerbates what is, again, a regressive higher-education program.

These are some reasons that the Education Efficiency Index ranked Brazil by far the lowest of 30 countries reviewed in terms of value for money spent in education.33

The country must improve the quality of education not just

by investing more but also by systematically reviewing the effectiveness of existing government programs from pre-school to university. This may not be an easy fix, but it would not further strain Brasília’s fiscal position.

God may be Brazilian, as Rousseff posited, but the country needs higher education to take advantage of any divine gifts.

1 41 4

Brazil has enjoyed significant trade expansion thus far in the 21st century. This is not the sole explanation for years of strong growth, but it is certainly a factor. Total Brazilian exports expanded from US$50.77 billion in 2000 to US$243 billion in 2013. This period also featured flourishing trade relationships with some of the world’s most rapidly growing economies. In 2000, Brazil exported US$1.62 billion of goods to China. By 2013, that figure soared to US$46 billion.34

But Brazil did not experience tremendous gains in efficiency or competitiveness. Rather, the expansion stemmed from strong

global demand for commodities, which the country has in abundance.35

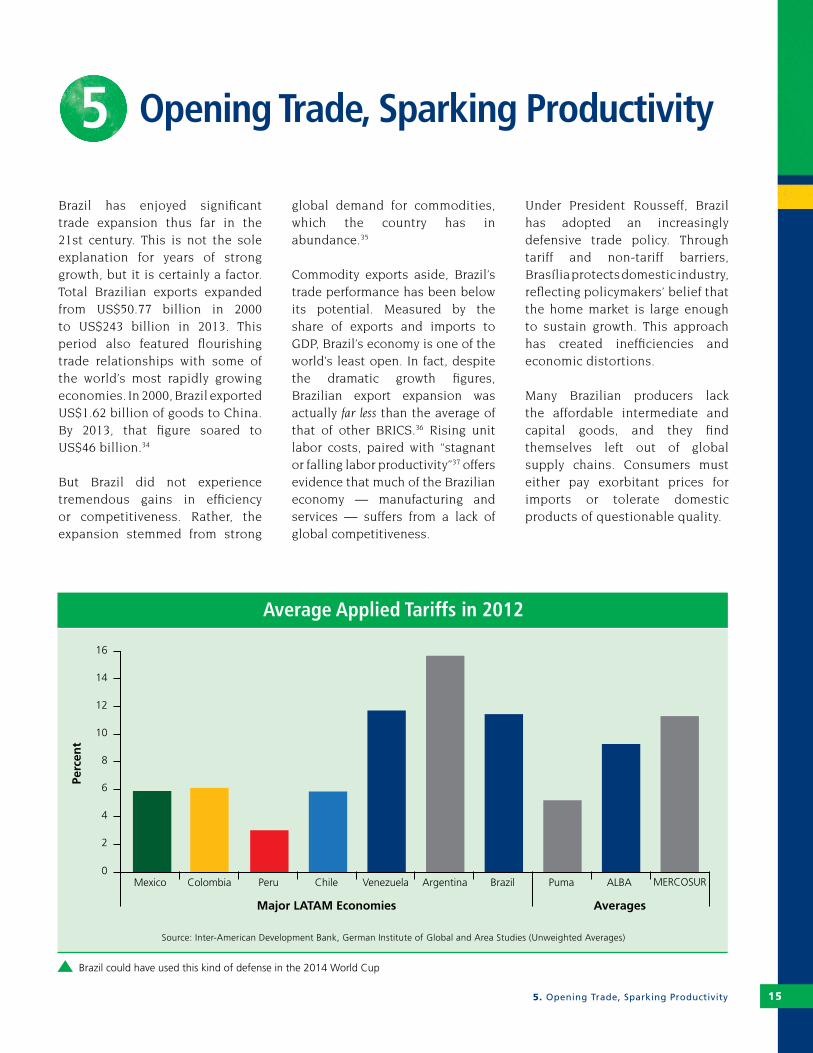

Commodity exports aside, Brazil’s trade performance has been below its potential. Measured by the share of exports and imports to GDP, Brazil’s economy is one of the world’s least open. In fact, despite the dramatic growth figures, Brazilian export expansion was actually far less than the average of that of other BRICS.36 Rising unit labor costs, paired with “stagnant or falling labor productivity”37 offers evidence that much of the Brazilian economy — manufacturing and services — suffers from a lack of global competitiveness.

Under President Rousseff, Brazil has adopted an increasingly defensive trade policy. Through tariff and non-tariff barriers, Brasília protects domestic industry, reflecting policymakers’ belief that the home market is large enough to sustain growth. This approach has created inefficiencies and economic distortions.

Many Brazilian producers lack the affordable intermediate and capital goods, and they find themselves left out of global supply chains. Consumers must either pay exorbitant prices for imports or tolerate domestic products of questionable quality.

Mexico Colombia Peru Chile Venezuela Argentina Brazil Puma ALBA MERCOSUR

AveragesMajor LATAM Economies

16

14

12

10

8

6

4

2

0

Perc

ent

Average Applied Tariffs in 2012

Source: Inter-American Development Bank, German Institute of Global and Area Studies (Unweighted Averages)

Opening Trade, Sparking Productivity5

5. Opening Trade, Sparking Productivity

Brazil could have used this kind of defense in the 2014 World Cup

1 51 5

Brazil’s struggling automobile sector — once a point of pride — attests to the country’s problems with competition. In 2002, Mercosur and Mexico signed the Complementación Económica No. 55 (ACE No. 55), which was meant to ensure liberalized trade in automobiles. In theory, Mexico would export larger vehicles to Brazil, which would export smaller cars to Mexico.38

But Mexico quickly established the upper hand. Between 2009 and 2011 alone, Mexican unit exports to Brazil increased 152 percent, generating US$2.1 billion revenue and a US$696 million bilateral trade surplus.39 In 2012, President Rousseff introduced a quota system and increased rules-of-origin requirements on Mexican automobiles. This move offered some protection, but it did not improve competitiveness: Mexico has since surpassed Brazil in car production.40

Joining THE pArTyFree trade is no panacea. Opening trade negotiations may be a good place to start, but Brazil cannot sign its way out of the competitiveness rut. Nevertheless, a stronger inclination to integrate globally would lead to gains that could

render Brazil more competitive in the long term. In the recent years that Brazil has struggled, some of its unheralded regional neighbors have thrived with a strategy based on integration. Chile, Colombia, Mexico and Peru, countries that the Bertelsmann Foundation has labeled The Pacific Pumas,41 have all signed free-trade agreements with the US, EU and Canada, while simultaneously integrating into East Asia’s “noodle bowl” of pacts. The Pumas have moved to eliminate tariffs on 92 percent of trade, a figure that will increase to 100 percent by 2030.

Chilean President Michelle Bachelet has extended an invitation for collaboration between the four countries that comprise the Pacific Alliance and Brazil.42 President Rousseff would do well to accept it. Closer ties would offer Brazil access to growing markets and the opportunity to find niches in emerging regional supply chains. Opening regionally would also be less of a shock than opening globally. Brazil could hone its competitiveness in Latin America before broaching free trade on a global scale.

Brasília could also push for a trade agreement between Mercosur and the EU. Mercosur-EU negotiations have been ongoing (and of little consequence) since the mid-1990s, so the notion of progress can seem far-fetched. Nevertheless, President Rousseff has insinuated interest in a deal,43 and she is not alone: Paraguay and Uruguay would also like an agreement. Even Argentine recalcitrance may be waning. In July 2014, Mercosur concluded a proposal for an agreement with the EU that could liberalize up to 90 percent of trade.44 Depending on the details, a successful agreement in 2015 could lead to significant growth in Brazil’s manufacturing and agricultural exports to Europe.

Free trade, be it with the Pacific Alliance or the EU, will not suddenly make Brazil competitive. But through global integration, Brazil would be better positioned to leverage areas in which it already has a comparative advantage. Increased competition would also force improved productivity. Both of these trends would translate to growth.

1 61 6

While Brazil faces trying circumstances, it does not face imminent crisis. Rather, the present situation presents policymakers with an opportunity to prove that they can enact meaningful economic reform in the absence of an economic emergency. But if these changes are not made, the result may well be a crisis down the road that forces policymakers’ hands.

Most observers agree that Brazil needs change, and most Brazilians want to see it. In the 2014 election, a narrow majority of Brazilians entrusted President Rousseff to manifest this change. With the pressure of re-election lifted from her shoulders, she should use her mandate to implement policies that will help the country grow again, even if this requires changing course on certain issues.

The direction of economic policy that the second Rousseff administration has taken in its first days in office is encouraging. So are the appointments of highly regarded technocrats such as Finance Minister Joaquim Levy. But appointments and proclamations must be followed by action and execution.

The recommendations presented in this study are not easy to implement and do not translate into growth overnight. They may not appeal to regional policymakers who all too often pursue short-term growth at the expense of long-term reform. Such an approach, in Brazil and elsewhere in Latin America, has resulted in cycles of boom followed by the inevitable busts, and centuries of unfulfilled promise.

Brazil’s impressive progress means it can no longer stimulate growth by helping newly middle-class families afford a refrigerator—they have one now and do not need another. Instead the middle class needs better jobs, more skills and a dependable economy. By implementing the recommendations we have discussed, the second Rousseff administration could kick-start the process.

The Country of Tomorrow, Tomorrow

The Country of Tomorrow, Tomorrow 1 71 7

1 See Otaviano Canuto and Philip Schellekens. “Three Perspectives on Brazilian Growth Pessimism.” The World Bank Economic Premise No. 148, June 2014. Available online at http://siteresources.worldbank.org/EXTPREMNET/Resources/EP148.pdf

2 IMF WEO Estimate http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/index.aspx 3 The other two are inflation targeting and a flexible exchange rate. 4 Joe Leahy. “Brazil reveals its largest monthly deficit on record.” The Financial Times, October 31, 2014. Available online at http://

www.ft.com/intl/cms/s/0/f85b049c-6123-11e4-8f87-00144feabdc0.html?siteedition=intl#axzz3ICjHgpCT. Central Bank of Brazil Data.

5 See Simon Romero. “Grand Visions Fizzle in Brazil.” The New York Times, April 12, 2014. Available online at http://www.nytimes.com/interactive/2014/04/12/world/americas/grand-visions-fizzle-in-brazil.html?_r=0

6 “Desoneração da folha não evitou demissões” Valor, October 11, 2014. Available online at http://www.valor.com.br/brasil/3772754/desoneracao-da-folha-nao-evitou-demissoes

7 Carlos Góes. “The Gringo’s Guide to Demonstrations in Brazil.” No Se Mancha, June 22, 2013. Available online at http://semancha.com/2013/06/22/the-gringos-guide-to-demonstrations-in-brazil/.

8 The government has found it easier to bail out struggling electricity providers—as the Brazilian Treasury did to the tune of US$5 billion (R$12 billion) in 2014—than reduce popular subsidies. See Julia Borba, Sofia Fernandes and Valdo Cruz. “Government and Consumers to Cover R$12 Billion Hole in Energy Sector.” Folha de S. Paulo, March 3, 2014. Available online at http://www1.folha.uol.com.br/internacional/en/business/2014/03/1425403-government-and-consumers-to-cover-r12-billion-hole-in-energy-sector.shtml

9 Herwin Lowman. “How to tackle the Custo Brasil.” Rabobank, January 9, 2014. Available online at https://economics.rabobank.com/publications/2014/january/how-to-tackle-the-custo-brasil/

10 “Brazil’s Pension system: Tick, tock.” The Economist. May 24, 2012. Available online at http://www.economist.com/node/2155109311 Filipe Pacheco. “Brazil’s Real Falls Most in Three Years on Record Budget Deficit.” Bloomberg, October 31, 2014. Available online

at http://www.bloomberg.com/news/2014-10-31/brazil-s-real-declines-on-concern-budget-deficit-is-deepening.html.12 Marina Rossi. “Extreme poverty rises in Brazil for first time in a decade.” El Pais, November 7, 2014. Available online at http://

elpais.com/elpais/2014/11/07/inenglish/1415374583_233630.html.13 For example, see the 1987 New York Times article “Economic Crisis Erodes Support for Brazil Chief”, available online at http://

www.nytimes.com/1987/02/15/world/economic-crisis-erodes-support-for-brazil-chief.html.14 Relatório de Estabilidade Financeira. Banco Central do Brasil Vol. 13 No. 2, September 2014. Available online at http://www.bcb.gov.

br/htms/estabilidade/2014_09/refP.pdf15 This is actually down from Brazil’s ranking of 64th recorded in the 2011-2012 review. See: Klaus Schwab. The Global Competitiveness

Report. World Economic Forum, 2011, Pg. 18.16 How to Revitalize Infrastructure Investments in Brazil – Public Policies for Better Private Participation. The World Bank, January 10, 2007.

Available online at http://siteresources.worldbank.org/INTBRAZIL/Resources/BrInfrstrct1.pdf17 “How to Decrease Freight Logistics Costs in Brazil.” World Bank Report No. 46885-BR, February 8, 2010. Available

online at http://siteresources.worldbank.org/BRAZILINPOREXTN/Resources/3817166-1323121030855/FreightLogistics.pdf?resourceurlname=FreightLogistics.pdf.

18 “All eyes on Brazil’s oil.” Global Post, June 25, 2012. Available online at http://www.globalpost.com/dispatch/news/regions/americas/brazil/120621/all-eyes-brazils-oil

19 Cornelius Fleischhaker. “Libra out of balance – International oil companies indifferent to Brazilian pre-salt oil.” No Se Mancha, October 21, 2013. Available online at http://semancha.com/2013/10/22/libra/.

20 “Gridlines: Crunch Time for Brazilian Infrastructure.” PWS, 2013. Available online at http://www.pwc.com.br/pt/publicacoes/setores-atividade/infraestrutura-grandes-projetos/infrastructure-investment-growth-in-brazil.jhtml

21 “Gridlines: Crunch Time for Brazilian Infrastructure.” See also: World Bank Report No. 46885-BR, February 8, 2010, p 47.22 “Gridlines: Crunch Time for Brazilian Infrastructure.” See also: World Bank Report No. 46885-BR, February 8, 2010, p 47.23 See Jonathan Wheatley. “Brazil’s BNDES: crowding out, not crowding in.” The Financial Times, January 24, 2013. Available online at

http://blogs.ft.com/beyond-brics/2013/01/24/brazils-bndes-crowding-out-not-crowding-in/24 For example, see James Stranko. “Eike Batista: The Symptom or the Cause?” No Se Mancha, August 7, 2013. Available online at

http://semancha.com/2013/08/07/eike-batista-the-symptom-or-the-cause/.25 “Brazil’s oil boom Filling up the future.” The Economist, November 5, 2011. Available online at http://www.economist.com/

node/21536570.

Endnotes

1 81 8

26 Doug Grey. “Local content challenges vex Brazil’s offshore operators.” Offshore, November 12, 2013. Available online at http://www.offshore-mag.com/articles/print/volume-73/issue-11/brazil/local-content-challenges-vex-brazil-s-offshore-operators.html.

27 “Pensions and education: Land of the setting sun.” The Economist, 28 September 2013. Available online at http://www.economist.com/news/special-report/21586682-brazil-country-future-spends-far-too-much-its-past-land-setting-sun.

28 “Brazil: Education at a Glance, 2013” OECD, 2013. Available online at http://www.oecd.org/edu/Brazil_EAG2013%20Country%20Note.pdf

29 See “Public spending on education - total (% of GDP) in Brazil” Available online at http://www.tradingeconomics.com/brazil/public-spending-on-education-total-percent-of-gdp-wb-data.html

30 “Education spending in Brazil Coming soon: the world’s priciest classrooms”. The Economist, October 28, 2012. Available online at http://www.economist.com/blogs/americasview/2012/10/education-spending-brazil

31 Burns, Evans and Luque, 53. 32 Barbara Burns, David Evans, and Javier Luque. Achieving World-Class Education in Brazil. (Washington DC: The World Bank, 2012).

Available online at http://www-wds.worldbank.org/external/default/WDSContentServer/WDSP/IB/2011/12/08/000333037_20111208235751/Rendered/PDF/656590REPLACEM0hieving0World0Class0.pdf

33 Peter Dolton, Oscar Marcenaro-Gutierrez and Adam Still. The Efficiency Index: Which education systems deliver the best value for money? GEMS Education Solutions, 2014. Available online at http://www.edefficiencyindex.com/book/files/assets/common/downloads/The%20Efficiency%20Index.pdf

34 Source: UN Comtrade, OECD Data. See also GED VIZ, available online at https://viz.ged-project.de/?lang=en35 As of 2010, raw materials accounted for 84 percent of Brazilian exports to China, while manufactured goods accounted for 98

percent of Brazilian imports from China. There is little reason to believe this makeup has changed much since then. See Paulo Prada. “Brazilian President to Visit China on a Trade Mission.” The Wall Street Journal, April 11, 2011. Available online at http://online.wsj.com/news/articles/SB10001424052748704366104576254904179874640?mg=reno64-wsj&url=http%3A%2F%2Fonline.wsj.com%2Farticle%2FSB10001424052748704366104576254904179874640.html.

36 Between 2000 and 2010, Brazilian exports grew by 262 percent. Russia, India, China and South African exports expanded by 439 percent. See Otaviano Canuto, Matheus Cavallari, and José Guilherme Reis. “The Brazilian Competitivness Cliff.” The World Bank Economic Premise No. 105, February 2013. Available online at https://ideas.repec.org/a/wbk/prmecp/ep105.html

37 See Canuto, Cavallari, and Reis.38 “Two ways to make a car.” The Economist, May 10, 2012. Available online at http://www.economist.com/node/2154995039 Hermino Blanco Mendoz, Jaime Zabludovsky Kuper, Adalberto García Rocha and Sergio Gómez Lorz. “Brazil’s Dutch Disease and

the Auto Trade War with Mexico: Stylized Facts.” Center for Economic Policy Research, June 14, 2012. Available online at http://www.globaltradealert.org/gta-analysis/brazil%E2%80%99s-dutch-disease-and-auto-trade-war-mexico-stylised-facts. See also Samuel George. The Pacific Pumas: An Emerging Model for Emerging Markets. (Washington DC: The Bertelsmann Foundation, 2014) Pg. 33. Available online at http://www.bfna.org/sites/default/files/publications/The%20Pacific_Pumas-Single%20(13Mar14).pdf

40 Jesse Rogers. “Car Wars: Mexico and Brazil.” No Se Mancha, September 9, 2014. Available online at http://semancha.com/2014/09/09/car-wars-mexico-and-brazil/

41 George. The Pacific Pumas: An Emerging Model for Emerging Markets42 Brazil initially brushed the Alliance aside; in 2013 then-Foreign Minister Antonio Patriota referred to the pact as a “marketing

success”. While there may be a grain of truth in Patriota’s assessment, there are also significant opportunities for mutually beneficial collaboration between a Brazil-led Mercosur and the Pacific Alliance. See “Pacific Alliance is a ‘marketing success’ and no concern for Mercosur, says Brazil,” MercoPress (June 22, 2013). Available online at http://en.mercopress.com/2013/06/22/pacific-alliance-in-a-marketing-success-and-no-concern-for-mercosur-says-brazil. On Bachelet’s overture to Brazil, see Samuel George. “Mercosur and the Pacific Alliance – do opposites attract?” The Financial Times, June 13, 2014. Available online at http://blogs.ft.com/beyond-brics/2014/06/13/guest-post-mercosur-and-the-pacific-alliance-do-opposites-attract/

43 Robin Emmot. “EU, Merocusr to unblock trade talks, hurdles remain.” Reuters, January 26, 2013. Available online at http://www.reuters.com/article/2013/01/27/us-eu-latinamerica-idUSBRE90P0GX20130127.

44 “Mercosur finally agrees on joint trade proposal to exchange with the EU.” MercoPress, August 1, 2014. Available online at http://en.mercopress.com/2014/08/01/mercosur-finally-agrees-on-joint-trade-proposal-to-exchange-with-the-eu.

Endnotes 1 91 9

2 02 0

Bertelsmann Foundation1101 New York Avenue, NW, Suite 901 Washington, DC 20005USAmain phone +1.202.384.1980main fax +1.202.384.1984

www.bfna.org