Embed Size (px)

Citation preview

3 r d Q u a r t e r 2 0 1 0 R e p o r t

The general economy is seeing mixed signs. GDP has been positive for

four quarters, consumer confidence is up, inflation remains under

control, and businesses have begun spending. However, consumer

spending has decreased from previous quarters, the recovery has been

jobless so far, credit remains tight, and the housing market remains a risk.

The general economy is seeing mixed signs.

GDP has been positive for four quarters,

consumer confidence is up, inflation remains

under control, and businesses have begun

spending. However, consumer spending has

decreased from previous quarters, the recov-

ery has been jobless so far, credit remains

tight, and the housing market remains a risk.

The outlook for put in place construction

for the remainder of 2010 also is bleak.

Total construction in 2010 will be down 7%

after declining 15% in 2009. Residential

construction is expected to begin recovering

in 2010. Nonresidential construction will

decline 18% in 2010 after declining 13% in

2009. An 18% increase in conservation and

development construction will offset losses

in nonbuilding construction.

The American Institute of Architects’ (AIA)

Architectural Billings Index hit its lowest

level since 1995 in the 4Q08 at 34.7. It

stood at 48.2 in August 2010. FMI’s

Non-Residential Construction Index

(NRCI) hit 34.1 in 4Q08, down from 52.6

(for the same time in 2007), and is at 51.3

in the 3Q10. Contractors are reporting

backlogs of 9 months in 3Q10 (up from 8

months in 2Q10), according to FMI’s NRCI.

The overall rates for project delays and

cancellations improved slightly, yet remain

at 3 times the normal rate and are currently

at 15% (the same rate as 3Q08). Project

cancellations are nearly 3 times the normal

rate and are currently at 8% of backlog

(less than doubled from 3Q08). While

credit is expected to loosen slightly

throughout 2010, delays and cancellations

are likely to remain high.

The construction industry should prepare for

another year of decline in nonresidential

construction. Construction gained 19,000

jobs in August (of which 10,000 were due

to the return of workers on strike in July).

There have been losses in 34 out of 37 con-

secutive months, bringing the construction

unemployment rate to 15.9%. That means

there are 1.5 million construction workers

out of work. An increase in residential

construction in 2010 could begin to turn

the employment situation, but it is unlikely

that it would do much to offset the losses

from nonresidential construction.

FMI’sC o n s t r u c t i o n O u t l o o k

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Mill

ions

of

Cur

rent

Dol

lars

Put in Place Construction

Recession Residential Nonresidential Buildings Nonbuilding Structures

The residential sector is expected to begin to

recover in 2010. However, the expiration of the

federal home buyer tax credit poses risk to the

recovery of the sector. Single-family put in place

construction will recover at a slower rate than

single-family housing starts. The quality mix of

new single-family homes is shifting. It takes five

$150,000 housing starts to equal one $750,000

start. Therefore, starts will recover at a faster rate.

Multi family construction has been impacted

severely by tight credit and will not recover

until credit loosens. Residential improvements

construction is expected to increase slightly in

2010 as consumers make improvements rather

than moving up, and the age of the housing

stock requires improvements.

The nonresidential sector will see a double-digit

decline in 2010. Transportation construction

will be the only segment likely to see actual

growth. Public safety will remain flat to slightly

down. The highly cyclical lodging, office and

commercial segments will experience severe

declines in 2010. Manufacturing construction,

which has remained strong mostly due to refinery

work, will turn down when many of these mega

projects are completed.

The nonbuilding sector will remain positive

again in 2010. The largest contributors to this

growth are sewage and waste disposal, and

conservation and development construction.

Cleanup from the Gulf oil spill will add almost

$500 million to the conservation and develop-

ment segment. Highway and street construction

is expected to remain flat as the remaining

stimulus funds are used and the highway bill is

extended rather than reauthorized. Water and

wastewater construction is expected to remain

flat as well.

The general economy is a main driver for both

residential and nonresidential construction. Real

GDP increased at an annual rate of 1.6% in the

second quarter of 2010, according to the "second"

estimate. Real GDP increased 3.7% in the first

quarter of 2010. Consensus Forecasts predicts

that GDP will increase 3.3% in 2010. We believe

that this estimate is reasonable, but that it is

extremely sensitive to the drivers discussed below.

2Construction Outlook

U.S. Employment U.S. Unemployment Rate

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

10%

9%

8%

7%

6%

5%

4%

3%

Jobs and Unemployment 1971–2010

150

140

130

120

110

100

90

80

70

60

6%

4%

2%

0%

-2%

-4%

-6%

-8%Q1-05 Q3-05 Q1-06 Q3-06 Q1-07 Q3-07 Q1-08 Q3-08 Q1-09 Q3-09 Q1-10

Per

cent

Inc

reas

e

% Increase in Real GDP 2005–2010

The employment situation decreased slightly. The unemploy-

ment rate ticked upward to 9.6% in August after spending two

consecutive months at 9.5%. The loss of 114,000 temporary

census jobs offset gains of 67,000 employed workers in private-

sector employment. Since the recession began in December

2007, payroll employment has fallen by more than 8 million.

The Advance Monthly Retail Sales Report for July estimates

that retail and food service sales were $362.7 billion. This is an

increase of 0.4% from the previous month and 5.5% above

July 2009. Total sales for May 2010 through July 2010 were

up 5.9% from the same period a year ago, and the May 2010

to June 2010 percent change was revised from -0.5% to -0.3%.

Retail trade sales were up 0.4% from June 2010 and were up

5.9% from last year. Gasoline station sales were up 12.2%

from July 2009, and nonstore retailers sales were up 12.6%

from last year.

Total retail and food service sales, excluding motor vehicles

and parts dealers (ex auto), were up 0.2% in July over last

month and up 4.9% from a year ago.

The Conference Board's Consumer Confidence Index improved

moderately in August. The Index is now 53.5, up from 51.0

in July. The Expectations Index increased to 72.5 from 67.5.

The Present Situation Index decreased to 24.9 from 26.4.

"Consumer confidence posted a modest gain in August, the

result of an improvement in consumers’ short-term outlook,"

says Lynn Franco, director of The Conference Board Consumer

Research Center. "Consumers’ assessment of current conditions,

however, was less favorable as employment concerns continue

3Third Quarter 2010

Total Retail and Food Service Sales

92 94 96 98 00 02 04 06 08 10

$450,000

$400,000

$350,000

$300,000

$250,000

$200,000

$150,000

$100,000

$50,000

$0

to weigh heavily on consumers’ attitudes. Expectations about

future business and labor market conditions have brightened

somewhat, but overall, consumers remain apprehensive about

the future. All in all, consumers are about as confident today

as they were a year ago."

The economy may show some signs of improving, but it is still

a downturn for nonresidential construction. Nonresidential

construction typically lags behind the general economy by

approximately 18 months. Intense competition that has been

bringing down prices has been reported. This is good for owners,

but not so good for contractors. Nonbuilding construction will

remain positive for the forecast period with conservation and

development leading the sector.

2002 2003 2004 2005 2006 2007 2008 2009 2010

Consumer Confidence Index

120

100

80

60

40

20

0

4Construction Outlook

The residential construction market has been

decimated. For housing starts, 2009 was the

worst year since we began keeping records in

1959. Total residential construction will be

$268.7 billion in 2010, down from its 2006

high of $619.8 billion. At its peak, residential

construction accounted for 53% of total con-

struction. It will account for 31% in 2010.

Single-family construction has plummeted from

a 2005 high of $434.9 billion to $123.4 billion in

2010. Multi family construction and improve-

ments have seen declines as well, however not

of this magnitude. Multi family construction

peaked in 2006 at $54.3 billion; it will be

$20.9 billion in 2010. Improvements are down

to $124.2 billion from $147.9 billion in 2006.

R e s i d e n t i a l

Single-family Multi family

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

500,000

450,000

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

Mill

ions

of

Cur

rent

Dol

lars

Value of Residential Construction

60,000

50,000

40,000

30,000

20,000

10,000

0

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Residential Improvements

5Third Quarter 2010

Trends:Total Occupied Units

Approximately 85.6% of the housing units

in the United States in 2Q 2010 were

occupied, and 14.4% were vacant. The

owner-occupied housing units were 57.3%

of total housing units, and renter-occupied

units made up 28.3% of total housing

units in 2Q 2010. Vacant housing units

comprised 14.4% of total housing units.

Housing AffordabilityHome ownership is currently much more

affordable to households earning the

median income. The March index was 161.8.

The median priced, existing single-family

home, mortgage rate and qualifying

income are at lows since the housing boom.

Share of Adjustable Rate Loans At the peak in April 2005, adjustable

loans accounted for 35% of all mortgage

applications. That share fell to about 2%

by the end of 2008, but has been edging

back up since. At the beginning of

September 2010, adjustable loans

accounted for 6.1% of all applications.

Household FormationHousehold formation has slowed to a growth

rate of 0.34% in 2009, down from 0.67% in

2008 and down from 2001’s high of 3.35%.

Some 398,000 households were formed in

2009, down from 772,000 in 2008 and

2001’s high of 3.5 million.

Homeownership Rate The homeownership rate is down from the

previous quarter and the same time a year

ago at 66.9%. The rate peaked at 69.2% in

4Q 2004. The current rate is in line with

early 2000.

Supply of Unsold HomesInventory of new homes for sale has been

trending up since January 2010 and

stands at a 9.1 months’ supply for July.

The volume of new homes for sale

(currently SA 276,000 homes) is down

59% from its peak in July 2006.

Vacant Homes for SaleVacant homes for sale in the 2nd quarter

were 1.9 million. This is slightly above the

lowest level in the 3rd quarter of 2006.

However, nearly 350,000 of this number

are considered an excess that needs to be

worked through before the housing market

can recover. Further, there is an additional

block of homes (unknown quantity) that

is owned by banks, but is being held off

the market at this time. In addition, there

is a large inventory of 2007 adjustable-rate

mortgages that will reset over the next two

quarters. If interest rates are to rise, it will

result in a new round of foreclosures.

Construction MixQuality mix is shifting strongly toward

smaller, more affordable homes with

reduced amenities.

Drivers:— Unemployment Rate

— Core CPI

— Income

— Mortgage Rate

Home Prices

Housing Starts

Housing Permits

ÔÔ

Ô

2,500

2,000

1,500

1,000

500

0

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2010

Housing Starts

Trends:Securing financing remains the primary obstacle to new hotel construction

Minimal projects are progressing through the construction pipeline; many are postponed until

conditions improve.

All key-sector metrics forecast to continue sliding in 2010.

The green movement is losing traction due to greater initial cost perceptions.

Business and leisure travel are both down Technology is reducing need for

business travel.

Hotel performance is linked to local

economies.

Travelers are demanding rate concessions.

Hotels coming online in 2010 heavily concentrated on upscale as well as midscale without F&B chain segments

Midscale and upscale segments will be

the first to be renovated.

Lobby transformation is becoming a

differentiator and epicenter of hotels.

6Construction Outlook

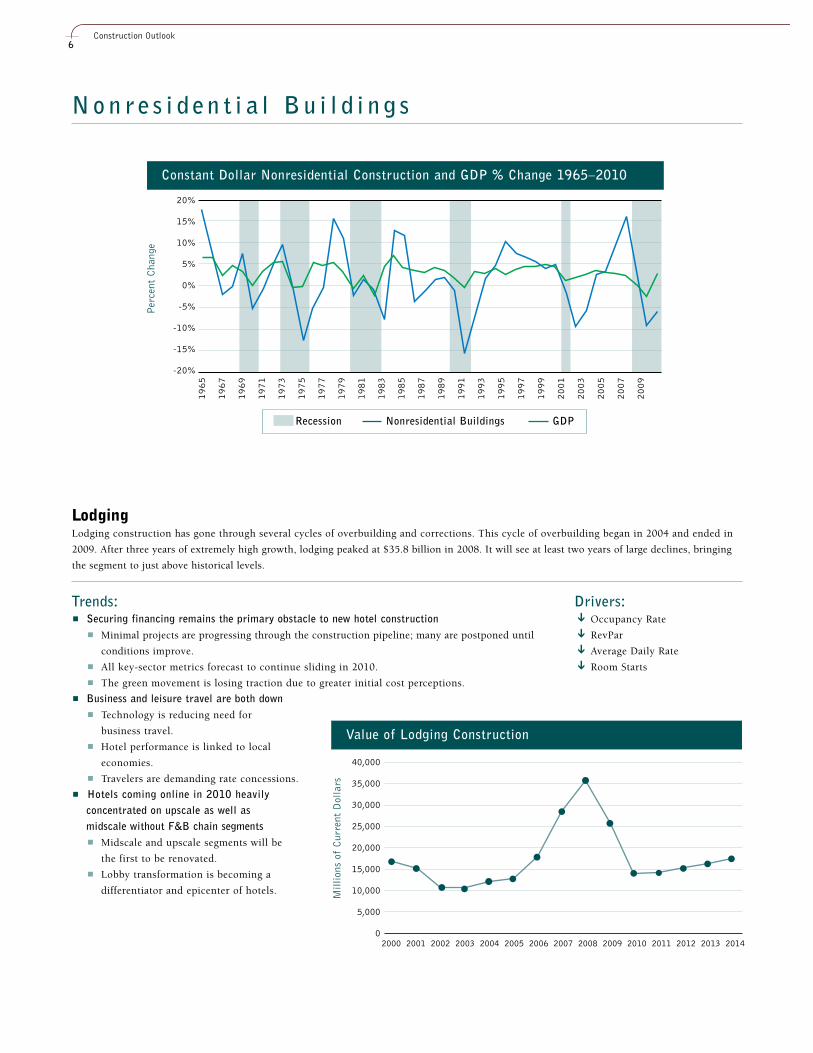

N o n r e s i d e n t i a l B u i l d i n g s

Recession Nonresidential Buildings GDP

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Per

cent

Cha

nge

Constant Dollar Nonresidential Construction and GDP % Change 1965–2010

Drivers:Occupancy Rate

RevPar

Average Daily Rate

Room Starts

ÔÔ

ÔÔ

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Lodging Construction

LodgingLodging construction has gone through several cycles of overbuilding and corrections. This cycle of overbuilding began in 2004 and ended in

2009. After three years of extremely high growth, lodging peaked at $35.8 billion in 2008. It will see at least two years of large declines, bringing

the segment to just above historical levels.

7Third Quarter 2010

Trends:The rise in vacancy rates has led to a reduction in rents and increases in incentives and concessionsoffered by landlords

New space entering supply only compounds vacancy rate issues.

Many tenants are “trading up” by relocating or upgrading to higher-quality space.

National employment a key factor in demand for office building constructionUnemployment rate is expected to remain

near 10% in 2010.

The current recession has eliminated a net of

9.0 million jobs since it began in December

2007. 15.0 million Americans remain unem-

ployed.

New construction at a standstillSecured projects continue to enter inventory.

Many projects will be put on hold or

abandoned until economy and employment

situations improve.

OfficeOffice construction is highly dependent on employment. It will take several years until there is enough employment growth to

spur new construction. Office construction will fall from its 2008 high of $70.3 billion down to $35.4 billion at its low in 2011.

CommercialCommercial construction relies heavily on consumer spending and new housing construction. It will not return to high levels until the employment

situation improves. Commercial construction will follow a turnaround in the housing market by 12 to 18 months and is not expected to pick up

until 2012.

Trends:Increase in residential building activity

Commercial construction lags residential by 12 to 18 months.

Open-air centers replacing traditional, enclosed mallsOccupancy costs are lower.

Store chains are lost.

Renovation of vacant big-box storesStores are repositioned for health care and educational purposes.

Major expansion plans for discount and foodretailers.

Expansion meets the demand of

price-conscious shoppers.

Increasing online retail sales National retail square footage could

decrease by as much as 15% in 2010.

Drivers:Office Vacancy Rate

— Unemployment Rate

— Employment

Ô

Drivers:Retail Sales

— CPI

— Unemployment

— Employment

Income

Housing Starts

Ô

ÔÔ

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Office Construction

100,000

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Commercial Construction

8Construction Outlook

Drivers:Population

Population Change Age 75+

— Government Spending

Uninsured Population

Nonresidential Structure Investment

ÔÔ

ÔÔ

Trends:Aging population requires medical care

Elderly population (i.e., older than 65 years of age) is expected to double by 2040.

Retirement of baby boomersLife expectancy in the U.S. has climbed from 75 to 78 over the last 20 years.

People are migrating to suburban areas, particularly warmer climates.

Increased consumerism for health careA growing number of consumers are

seeking primary care at retail store clinics

(e.g., Walmart, Walgreens).

Multi-specialty ambulatory care centers are

more profitable.

Inadequate, aging facilitiesARRA provides more than $1 billion for

the Veterans Health Administration’s

Non-Recurring Maintenance (NRM)

projects and energy initiatives.

New building technologies and facility upgrades

increase.

Seismic retrofits in California grow.

Single-bed hospital rooms requirement

Health CareHealth care construction will decline in 2010. However, it will remain at a historically high level. Hospital construction will allow the segment to

maintain its volume. Special care construction will help to drive future growth.

Drivers:Population Change Below 18

Population Change Ages 18-24

Stock Market

— Government Spending

Nonresidential Structure Investment

Ô

ÔÔ

ÔEducationalEducational construction is expected to decline in 2010. State revenues are down, which affects K-12 construction, but the stock

market is recovering, which impacts endowments and spending at universities. It is expected that privately owned construction will

wait until 2011 before expanding.

Trends:Government investment in public education

21st Century Green High-Performing Public School Facilities Act (H.R. 2187) would

authorize $6.4 billion for school renovation and modernization projects in fiscal year 2010.

Additional renovation funding could come from nearly $40 billion in the ARRA for the State

Fiscal Stabilization Fund.

State bonds have passed (e.g., California, Texas).

Aging school facilitiesThousands of schools built more than 50 years

ago are in need of modernization or replacement.

Security enhancements are needed to meet

school concerns.

Increasing student enrollmentsU.S. Department of Education predicts that

enrollment in elementary and secondary

schools will grow by 7% to reach nearly 60

million by 2016.

Growth is slower for grades nine through 12.

Growing market for green constructionEducation is one of the top-three vertical markets

for green construction, in terms of volume.

University capital spending put on hold

70,000

60,000

50,000

40,000

30,000

20,000

10,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Health Care Construction

140,000

120,000

100,000

80,000

60,000

40,000

20,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Education Construction

9Third Quarter 2010

Churches are buildings that religious communities aresaving for and investing in for the long haul

Energy efficiency, green sustainability and long-lasting

quality are becoming top features many congregations

want in worship houses.

Drivers:GDP

Population

Income

Personal Savings ÔÔ

ÔÔ

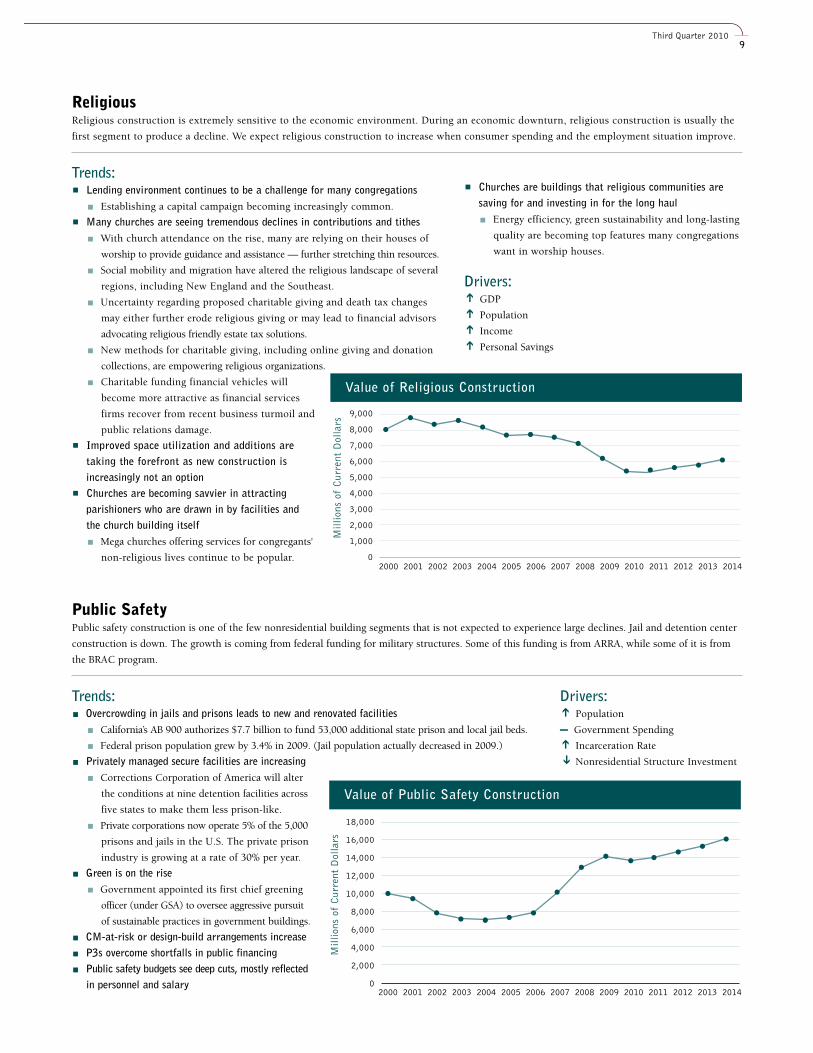

ReligiousReligious construction is extremely sensitive to the economic environment. During an economic downturn, religious construction is usually the

first segment to produce a decline. We expect religious construction to increase when consumer spending and the employment situation improve.

Trends:Lending environment continues to be a challenge for many congregations

Establishing a capital campaign becoming increasingly common.

Many churches are seeing tremendous declines in contributions and tithesWith church attendance on the rise, many are relying on their houses of

worship to provide guidance and assistance — further stretching thin resources.

Social mobility and migration have altered the religious landscape of several

regions, including New England and the Southeast.

Uncertainty regarding proposed charitable giving and death tax changes

may either further erode religious giving or may lead to financial advisors

advocating religious friendly estate tax solutions.

New methods for charitable giving, including online giving and donation

collections, are empowering religious organizations.

Charitable funding financial vehicles will

become more attractive as financial services

firms recover from recent business turmoil and

public relations damage.

Improved space utilization and additions aretaking the forefront as new construction isincreasingly not an optionChurches are becoming savvier in attractingparishioners who are drawn in by facilities andthe church building itself

Mega churches offering services for congregants'

non-religious lives continue to be popular.

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Religious Construction

Drivers:Population

— Government Spending

Incarceration Rate

Nonresidential Structure Investment

Ô

ÔÔ

Public SafetyPublic safety construction is one of the few nonresidential building segments that is not expected to experience large declines. Jail and detention center

construction is down. The growth is coming from federal funding for military structures. Some of this funding is from ARRA, while some of it is from

the BRAC program.

Trends:Overcrowding in jails and prisons leads to new and renovated facilities

California’s AB 900 authorizes $7.7 billion to fund 53,000 additional state prison and local jail beds.

Federal prison population grew by 3.4% in 2009. (Jail population actually decreased in 2009.)

Privately managed secure facilities are increasingCorrections Corporation of America will alter

the conditions at nine detention facilities across

five states to make them less prison-like.

Private corporations now operate 5% of the 5,000

prisons and jails in the U.S. The private prison

industry is growing at a rate of 30% per year.

Green is on the riseGovernment appointed its first chief greening

officer (under GSA) to oversee aggressive pursuit

of sustainable practices in government buildings.

CM-at-risk or design-build arrangements increaseP3s overcome shortfalls in public financingPublic safety budgets see deep cuts, mostly reflectedin personnel and salary

18,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Public Safety Construction

10Construction Outlook

Trends:Slowed by uncertain economic conditions

There is a lack of disposable income.

Activity surrounding new and expansion casino constructionSeveral projects were delayed in 2009 and 2010.

The new Greenbrier Resort Casino opened in

July 2010.

Several new stadiums (e.g., MeadowlandsStadium, Twins Ballpark) for professional sportsteams came online in 2009 and 2010

Other stadiums are facing funding concerns.

Drivers:Income

Personal Savings Rate

— Unemployment Rate

— Employment

ÔÔ

Amusement and RecreationAmusement and recreation construction is expected to decline as casino projects are delayed and canceled, sports stadiums are completed and a

spate of convention centers are finished. Tight credit, declining state revenues and decreases in consumer spending are a drag on this segment.

Trends:Growing population is putting increased pressure on the capacity of our currenttransportation infrastructure

This increases the need for mass transit.

Aviation spending is uncertainThe authorization of a federal aviation bill

is under consideration.

High-speed rail has yet to catch on, but is likely to eventually

Drivers:Population

— Government Spending

— Transportation Funding

Ô

TransportationAfter being flat in 2009, transportation construction is expected to recover in 2010 and remain at an elevated level. The size of the market should

double between 1999 and 2013. The growth will come mainly from rail and airport construction.

25,000

20,000

15,000

10,000

5,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Amusement and Recreation Construction

60,000

50,000

40,000

30,000

20,000

10,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Transportation Construction

11Third Quarter 2010

CommunicationCommunication construction had strong growth for four years before declining in 2008. It will decrease again in 2010. After the declines,

communication construction will be around historical levels at $186 billion in 2011.

Drivers:Innovation / Technology

Global Mobility

Population

Security/ Regulatory Standards

— Private Investment

ÔÔ

ÔÔ

ManufacturingManufacturing construction has experienced six years of strong growth, almost doubling the size of the market. We expect that it will decline from

2010 through 2012, but remains at an elevated level. Manufacturing has changed over the years. It is no longer textiles and autos. The growth has come

from billion dollar refinery projects, materials and electronic manufacturing. Investment from ARRA may spur some battery manufacturing projects.

Drivers:PMI

Industrial Production

Capacity Utilization

— Factory Orders

— Durable Goods Orders

— Manufacturing Inventories

Ô

ÔÔ

Trends:All signs would point to increased communication investment over the next five years, but reducedspending across the national nonresidential construction markets has significantly slowed privateinvestment in communication constructionGovernment and military are the two key parties supplying investments

Schools, BRAC and war efforts are large markets.

Immigration and anti-terrorism remain at high overall levels.

Much of the private market’s investment over thenext few years in communication will be toincrease securityThere will be more fiber-optic utilization anddeployment

Manufacturers, installers and builders using

fiber will see high growth.

Google is entering the networking market by

creating an ultra high-speed network for an

entire 50,000- to 500,000- person community.

United States established the NationalBroadband Plan on March 16, 2010

Trends:Over the last two years, manufacturing has been driven through the demand for upgraded technology and thereplacement of aging plants

Construction put in place for 2008 and 2009 are the high years for this segment.

After 2009, construction tapers and falls into a cycle much like the cycle nonresidential is in currently Economic effects such as the cost of natural gas and oil are expected to increase, and funding options are

expected to continue.

Manufacturing efforts are expected to continue to move out of the country or overseas where lower costsbenefit businessRate of growth for manufacturing exports is faster than for importsDraw-downs in business inventories are slowing, resulting in less opportunity for future manufacturing growthElectronic chip manufacturing is up as RFID use by retailers increases as marketers and advertisers arefinding more applications for these devicesA slowdown in defense and nondefense aircraftnew orders occurs after great gains for previouseight monthsAn end to the stimulus could point to slowdownin this segmentNew plants are being built to accommodateproduction of "green" energy makers (batteries,solar panels and wind turbines)Could "green" manufacturing fill the gap createdby auto and auto supplier manufacturing inMichigan and the Rust Belt?

30,000

25,000

20,000

15,000

10,000

5,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Communication Construction

70,000

60,000

50,000

40,000

30,000

20,000

10,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Manufacturing Construction

12Construction Outlook

N o n b u i l d i n g S t r u c t u r e s

PowerPower construction has seen four years of phenomenal growth. It has grown from $35.5 billion in 2005 to $88.7 billion in 2009. It is expected to

decline in 2010 before recovering in 2011 and reaching $127.5 billion in 2014. Environmental regulation and transmission and distribution projects

are mainly driving the growth. A spate of nuclear power projects is likely in the future, but it is unlikely to happen during the forecast period.

Trends:Call for a “nuclear renaissance”

EPA Administrator Christine Todd Whitman believes that the U.S. needs 25 to 27 new

reactors by 2030 for nuclear power to continue to produce 20% of the nation’s electricity.

The U.S. Nuclear Regulatory Commission expects applications for as many as 34 new

reactors by 2010.

The cost of building nuclear power plants is prohibitive without guaranteed loans,

changing regulations and solving waste disposal.

NEI lobbyist Richard Myers said a new, two-unit nuclear power plant could cost

as much as $14 billion; by comparison, the entire market capitalization of many

companies in the industry is barely double this, or smaller.

Obama pledges power loan guarantees.

Wind Power Generation will increaseToday only 1% of America’s power needs are generated by wind power. Experts believe

that it will generate 20% of America’s electricity needs by 2030.

The Pickens project was delayed due to lower energy prices from traditional sources.

Power grids are insufficient to handle the output of wind farms, especially in remote

areas where there is the most wind potential.

Solar Power is an alternativeFlorida Power & Light, the state's largest energy supplier, is building three solar plants.

It will take Florida from not being on the solar map to being the second-largest producer

in the nation (after California). By the end of next year, the plants will produce 110

megawatts of electricity, enough for 35,000 homes and businesses.

Big Solar will generate jobs as well as

electricity: solar thermal and photovoltaic

power plants.

Lower cost of traditional energy will slow

advancement of alternative energy plants.

Drivers:Industrial Production

Population

Nonresidential Structure Investment

Ô

ÔÔ

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Power Construction

13Third Quarter 2010

Highway and StreetHighway and street construction is facing a tough climate as state revenues decline. The funding from ARRA is just enough to offset these losses,

although funding is mostly for paving projects. The ARRA funding along with the extension of the highway bill will be enough to keep highway and

street construction flat. A new highway bill along with increases in state revenues has the potential to increase the level of construction.

Trends:AASHTO estimated in 2008 that it would cost roughly $140 billion to repair everydeficient bridge in the country—about $48 billion to repair structurally deficientbridges and $91 billion to improve functionally obsolete bridgesThe Highway Bill was extended through December 31, 2010

The Highway Bill transfers $19.5 billion to the Highway Trust Fund.

It restores states ability to spend money that had been rescinded.

Tax revenues decline as economy is in recession, resulting in a decrease inavailable state fundsPPP funding and more toll roads may seeincreased interestSlow residential construction in 2009 and 2010will decrease need for new roads in the near termNew funding sources are needed, possibledebates for more toll construction Continued loss of gas tax revenue as mileagestandards are increased through 2016; newrevenue source model neededAmerican Trucking Association projects increasesin over-the-road trucking Hauling of nonconcentrated detergents lessens (seeconservation and development construction below)

Drivers:Population

— Government Spending

Nonresidential Structure Investment

Ô

Ô

120,000

100,000

80,000

60,000

40,000

20,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Highway and Street Construction

Drivers:Population

Industrial Production

— Government Spending

ÔÔ

Trends:In need of replacement and upgrades, the 16,000 wastewater systems nationwide discharge morethan 850 billion gallons of untreated sewage into surface waters each year

Combined sewer systems (storm water and sewage) serve roughly 950 communities with about

40 million people. Most communities with CSOs are located in the Northeast and Great Lakes regions.

The EPA’s Storm Water Phase II Final Rule, published on December 8, 1999, expands the

Phase I storm water runoff regulations program by requiring programs and practices to control

polluted storm water runoffs.

The American Society of Civil Engineers (ASCE)gave Drinking Water and Wastewater “D”grades in its 2009 American InfrastructureReport CardThe Clean Water State Revolving Fund (CWSRF)programs have provided more than $5 billionannually in recent years to fund water qualityprotection projects

ARRA contributed $4 billion to the CWSRF.

The March 2010 U.S. Conference of MayorsWater Council report forecasts that futurespending for public water and wastewater systemswill range between $2.5 and $4.8 trillion over thenext 20-year period, 2009 to 2028

35,000

30,000

25,000

20,000

15,000

10,000

5,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Sewage and Waste Disposal Construction

Sewage and Waste DisposalSewage and waste disposal construction will remain at a historically high level. The market has more than doubled in size over the last decade

from $10.1 billion in 1999 to $25.9 billion in 2010. Slow, steady growth will push the market to reach $30.5 billion in 2014.

14Construction Outlook

Water SupplyWater supply construction will remain flat for the next two years. It has grown from $7.6 billion in 1999 to $15.5 billion in 2010. It will

grow to $19.8 billion in 2014. The aging water supply systems, along with many large EPA consent decrees, will eventually spur increases in

construction levels.

Drivers:Population

Industrial Production

— Government Spending

ÔÔ

Trends:Seven billion gallons of clean drinking water are lost to leaking pipes each day, owing to an annualinvestment shortfall of $11 billion (EPA) to replace old systemsApproximately 17 million people in the U.S. are served by substandard water facilities

The EPA is in the process of improving numerous drinking water standards for various impurities.

The agency is considering further revisions to

the lead and copper rule.

Federal assistance for the safe drinking waterState Revolving Fund (SRF) in the 11-year periodbetween 1997 and 2008 totaled $9.5 billion, justslightly more than the investment gap for each ofthose yearsARRA contributed just less than $2 million to theClean Water State Revolving Fund through the EPADesign-build and construction management at-riskproject delivery are continuing to grow and nowrepresent about 20% -30% of all U.S. water andwastewater projects

25,000

20,000

15,000

10,000

5,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Water Supply Construction

Conservation and DevelopmentConservation and development construction is one of the few surprise winners from the stimulus bill. The Army Corps of Engineers received

$4.6 billion from the stimulus. However, not all of these funds will be used for what we consider construction. It will take several years for the funds

to be worked into construction as it is a large amount of money, considering that the market was approximately $5.4 billion before the stimulus.

The Gulf oil spill will also contribute to the surging growth in this segment. The cleanup effort will contribute almost $500 million in 2010.

Drivers:Population

— Government Spending

Ô

Trends:The goal of EPA's Brownfields Program ($100 million) is to revitalize and restore neighborhoodsthrough environmental cleanup

The program has a proven history of attracting private investment, producing trained environmental

technicians, creating jobs and spurring local economic development.

Through the Recovery Act, EPA will issue competitive grants to evaluate and clean up brownfields,

which will in turn encourage redevelopment.

EPA's Superfund Hazardous Waste Cleanup($600 million) funds the cleanup of uncontrolledhazardous waste sites

The $600 million in Recovery Act funding will

further cleanup at Superfund National Priority

List sites, maximize job creation and retention,

and provide environmental and economic

benefits.

To speed cleanup conducted through the

Recovery Act, EPA will use the funds for sites

on the Superfund National Priority List and

use in-place, competitively awarded contracts;

interagency agreements; and cooperative agree-

ments for emergency response and cleanup activity.

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ions

of

Cur

rent

Dol

lars

Value of Conservation and Development Construction

15Third Quarter 2010

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RESIDENTIAL BUILDINGS

Single Family 238,269 251,123 267,205 311,879 378,934 434,912 417,518 306,990 187,609 107,487 123,610 148,332 183,932 211,522 232,674

Multi Family 29,740 32,342 34,268 36,420 41,321 48,699 54,324 52,570 47,823 35,499 31,239 28,740 36,787 39,730 43,306

Improvements* 84,054 89,096 100,487 102,952 118,153 133,896 147,973 140,909 121,977 116,235 119,722 125,708 129,479 133,364 140,032

Total Residential 352,063 372,561 401,960 451,251 538,408 617,507 619,814 500,468 357,408 259,221 274,571 302,780 350,198 384,615 416,012

NONRESIDENTIAL BUILDINGS

Lodging 16,850 15,486 10,869 10,712 12,363 12,840 18,139 28,706 35,818 25,174 16,363 15,381 16,150 17,281 18,663

Office 61,001 59,495 44,277 39,418 42,404 45,763 54,187 65,259 70,305 55,409 41,557 39,894 41,490 43,980 46,618

Commercial 67,873 68,506 62,520 61,529 67,057 70,242 76,713 89,684 84,942 57,473 40,806 38,357 40,659 43,505 47,421

Health Care 24,615 24,776 27,139 29,329 32,184 34,430 38,472 43,766 47,699 46,711 46,244 47,169 51,886 57,593 65,080

Educational 58,848 64,960 73,862 74,316 74,250 79,687 84,928 96,758 104,081 102,927 99,839 102,834 111,061 122,167 135,606

Religious 8,071 8,806 8,339 8,569 8,159 7,735 7,749 7,540 7,125 6,324 5,502 5,612 5,780 5,954 6,251

Public Safety 10,049 9,558 7,827 7,161 7,019 7,314 7,768 10,201 12,936 14,255 14,968 15,417 16,033 16,835 17,677

Amusement and Recreation 20,168 20,207 17,328 16,847 16,695 15,236 19,033 21,212 21,488 18,710 15,155 15,458 16,077 16,720 17,890

Transportation 22,887 24,409 25,781 24,710 25,059 25,052 27,964 31,877 33,953 35,308 36,720 38,924 41,259 44,147 48,120

Communication 18,958 20,173 18,457 14,550 15,546 18,906 22,219 27,580 25,649 20,302 18,475 19,214 20,175 21,385 22,668

Manufacturing 32,184 30,364 22,926 21,508 23,808 30,040 35,500 45,720 61,269 74,791 48,614 40,350 41,964 43,642 47,134

Total Nonresidential Buildings 341,503 346,739 319,325 308,649 324,544 347,245 392,672 468,303 505,265 457,384 384,243 378,610 402,534 433,209 473,128

NONBUILDING STRUCTURES

Power 32,289 35,025 36,804 41,450 35,395 35,466 39,754 59,305 80,160 88,912 94,247 102,729 113,002 125,432 142,992

Highway and Street 54,002 60,554 57,484 57,139 58,623 64,139 72,040 76,682 81,801 84,599 87,137 90,622 95,154 99,911 103,908

Sewage and Waste Disposal 10,949 12,006 16,237 16,581 17,929 19,867 23,186 24,872 25,143 24,920 25,668 26,694 28,029 29,711 31,493

Water Supply 8,587 9,397 12,442 12,492 12,620 14,028 14,960 15,798 16,951 15,804 15,962 16,441 17,592 18,823 20,329

Conservation and Development 3,362 3,967 3,621 3,935 4,044 4,453 5,130 5,260 5,405 5,855 6,382 6,893 7,168 7,455 7,679

Total Nonbuilding Structures 109,190 120,949 126,588 131,597 128,611 137,953 155,070 181,917 209,460 220,090 229,395 243,379 260,944 281,332 306,401

Total Put in Place 802,756 840,249 847,873 891,497 991,563 1,102,705 1,167,556 1,150,688 1,072,133 936,695 888,209 924,770 1,013,676 1,099,156 1,195,541

*Improvements include additions, alterations and major replacements. It does not include maintenance and repairs.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RESIDENTIAL BUILDINGS

Single Family 6% 5% 6% 17% 22% 15% -4% -26% -39% -43% 15% 20% 24% 15% 10%

Multi Family 2% 9% 6% 6% 13% 18% 12% -3% -9% -26% -12% -8% 28% 8% 9%

Improvements* 7% 6% 13% 2% 15% 13% 11% -5% -13% -5% 3% 5% 3% 3% 5%

Total Residential 6% 6% 8% 12% 19% 15% 0% -19% -29% -27% 6% 10% 16% 10% 8%

NONRESIDENTIAL BUILDINGS

Lodging 2% -8% -30% -1% 15% 4% 41% 58% 25% -30% -35% -6% 5% 7% 8%

Office 17% -2% -26% -11% 8% 8% 18% 20% 8% -21% -25% -4% 4% 6% 6%

Commercial 7% 1% -9% -2% 9% 5% 9% 17% -5% -32% -29% -6% 6% 7% 9%

Health Care 8% 1% 10% 8% 10% 7% 12% 14% 9% -2% -1% 2% 10% 11% 13%

Educational 12% 10% 14% 1% 0% 7% 7% 14% 8% -1% -3% 3% 8% 10% 11%

Religious 9% 9% -5% 3% -5% -5% 0% -3% -6% -11% -13% 2% 3% 3% 5%

Public Safety 3% -5% -18% -9% -2% 4% 6% 31% 27% 10% 5% 3% 4% 5% 5%

Amusement and Recreation 3% 0% -14% -3% -1% -9% 25% 11% 1% -13% -19% 2% 4% 4% 7%

Transportation 17% 7% 6% -4% 1% 0% 12% 14% 7% 4% 4% 6% 6% 7% 9%

Communication 2% 6% -9% -21% 7% 22% 18% 24% -7% -21% -9% 4% 5% 6% 6%

Manufacturing -3% -6% -24% -6% 11% 26% 18% 29% 34% 22% -35% -17% 4% 4% 8%

Total Nonresidential Buildings 8% 2% -8% -3% 5% 7% 13% 19% 8% -9% -16% -1% 6% 8% 9%

NONBUILDING STRUCTURES

Power 30% 8% 5% 13% -15% 0% 12% 49% 35% 11% 6% 9% 10% 11% 14%

Highway and Street 7% 12% -5% -1% 3% 9% 12% 6% 7% 3% 3% 4% 5% 5% 4%

Sewage and Waste Disposal 9% 10% 35% 2% 8% 11% 17% 7% 1% -1% 3% 4% 5% 6% 6%

Water Supply 13% 9% 32% 0% 1% 11% 7% 6% 7% -7% 1% 3% 7% 7% 8%

Conservation and Development 9% 18% -9% 9% 3% 10% 15% 3% 3% 8% 9% 8% 4% 4% 3%

Total Nonbuilding Structures 14% 11% 5% 4% -2% 7% 12% 17% 15% 5% 4% 6% 7% 8% 9%

Total Put in Place 8% 5% 1% 5% 11% 11% 6% -1% -7% -13% -5% 4% 10% 8% 9%

*Improvements include additions, alterations and major replacements. It does not include maintenance and repairs.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RESIDENTIAL BUILDINGS

Single Family 238,269 251,123 267,205 311,879 378,934 434,912 417,518 306,990 187,648 107,325 123,424 148,109 183,655 211,203 232,323

Multi Family 29,740 32,342 34,268 36,420 41,321 48,699 54,324 52,570 48,083 32,224 20,946 19,270 24,666 26,639 29,036

Improvements* 84,054 89,096 100,487 102,952 118,153 133,896 147,973 140,909 122,016 114,027 124,289 130,504 134,419 138,452 145,374

Total Residential 352,063 372,561 401,960 451,251 538,408 617,507 619,814 500,468 357,747 253,576 268,659 297,882 342,739 376,293 406,733

NONRESIDENTIAL BUILDINGS

Lodging 16,850 15,486 10,869 10,712 12,363 12,840 18,139 28,706 35,806 25,474 14,011 14,018 15,139 16,199 17,495

Office 61,001 59,495 44,277 39,418 42,404 45,763 54,187 65,259 68,563 52,717 36,902 35,426 36,843 39,053 41,397

Commercial 67,873 68,506 62,520 61,529 67,057 70,242 76,713 89,684 86,212 55,042 37,979 35,700 37,842 40,491 44,135

Health Care 24,615 24,776 27,139 29,329 32,184 34,430 38,472 43,766 46,902 45,111 41,051 43,104 47,414 52,629 59,471

Educational 58,848 64,960 73,862 74,316 74,250 79,687 84,928 96,758 104,890 102,907 92,616 95,395 103,026 113,329 125,795

Religious 8,071 8,806 8,339 8,569 8,159 7,735 7,749 7,540 7,225 6,206 5,399 5,507 5,672 5,843 6,135

Public Safety 10,049 9,558 7,827 7,161 7,019 7,314 7,768 10,201 13,083 14,099 13,676 14,086 14,650 15,382 16,151

Amusement and Recreation 20,168 20,207 17,328 16,847 16,695 15,236 19,033 21,212 21,829 18,901 15,499 15,809 16,441 17,099 18,296

Transportation 22,887 24,409 25,781 24,710 25,059 25,052 27,964 31,877 35,471 38,459 43,074 45,659 48,398 51,786 56,447

Communication 18,958 20,173 18,457 14,550 15,546 18,906 22,219 27,580 26,487 19,754 17,976 18,695 19,630 20,808 22,056

Manufacturing 32,184 30,364 22,926 21,508 23,360 28,568 32,677 40,633 53,234 58,513 42,129 33,703 32,355 34,620 37,390

Total Nonresidential Buildings 341,503 346,739 319,325 308,649 324,096 345,773 389,849 463,216 499,702 437,183 360,313 357,102 377,411 407,239 444,768

NONBUILDING STRUCTURES

Power 32,289 35,025 36,804 41,450 35,638 38,371 42,244 66,055 81,075 89,405 84,041 91,604 100,765 111,849 127,508

Highway and Street 54,002 60,554 57,484 57,139 58,623 64,139 72,040 76,682 81,361 82,028 82,110 85,394 89,664 94,147 97,913

Sewage and Waste Disposal 10,949 12,006 16,237 16,581 17,929 19,867 23,186 24,872 25,696 24,410 24,898 25,894 27,189 28,820 30,549

Water Supply 8,587 9,397 12,442 12,492 12,620 14,028 14,960 15,798 16,752 15,561 15,559 16,026 17,148 18,348 19,816

Conservation and Development 3,362 3,967 3,621 3,935 4,044 4,453 5,130 5,260 5,234 5,624 6,636 7,167 7,454 7,752 7,985

Total Nonbuilding Structures 109,190 120,949 126,588 131,597 128,854 140,858 157,560 188,667 210,118 217,028 213,245 226,086 242,220 260,917 283,771

Total Put in Place 802,756 840,249 847,873 891,497 991,358 1,104,138 1,167,223 1,152,351 1,067,567 907,787 842,216 881,070 962,370 1,044,450 1,135,273

*Improvements include additions, alterations and major replacements. It does not include maintenance and repairs.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RESIDENTIAL BUILDINGS

Single Family 6% 5% 6% 17% 22% 15% -4% -26% -39% -43% 15% 20% 24% 15% 10%

Multi Family 2% 9% 6% 6% 13% 18% 12% -3% -9% -33% -35% -8% 28% 8% 9%

Improvements* 7% 6% 13% 2% 15% 13% 11% -5% -13% -7% 9% 5% 3% 3% 5%

Total Residential 6% 6% 8% 12% 19% 15% 0% -19% -29% -29% 6% 11% 15% 10% 8%

NONRESIDENTIAL BUILDINGS

Lodging 2% -8% -30% -1% 15% 4% 41% 58% 25% -29% -45% 0% 8% 7% 8%

Office 17% -2% -26% -11% 8% 8% 18% 20% 5% -23% -30% -4% 4% 6% 6%

Commercial 7% 1% -9% -2% 9% 5% 9% 17% -4% -36% -31% -6% 6% 7% 9%

Health Care 8% 1% 10% 8% 10% 7% 12% 14% 7% -4% -9% 5% 10% 11% 13%

Educational 12% 10% 14% 1% 0% 7% 7% 14% 8% -2% -10% 3% 8% 10% 11%

Religious 9% 9% -5% 3% -5% -5% 0% -3% -4% -14% -13% 2% 3% 3% 5%

Public Safety 3% -5% -18% -9% -2% 4% 6% 31% 28% 8% -3% 3% 4% 5% 5%

Amusement and Recreation 3% 0% -14% -3% -1% -9% 25% 11% 3% -13% -18% 2% 4% 4% 7%

Transportation 17% 7% 6% -4% 1% 0% 12% 14% 11% 8% 12% 6% 6% 7% 9%

Communication 2% 6% -9% -21% 7% 22% 18% 24% -4% -25% -9% 4% 5% 6% 6%

Manufacturing -3% -6% -24% -6% 9% 22% 14% 24% 31% 10% -28% -20% -4% 7% 8%

Total Nonresidential Buildings 8% 2% -8% -3% 5% 7% 13% 19% 8% -13% -18% -1% 6% 8% 9%

NONBUILDING STRUCTURES

Power 30% 8% 5% 13% -14% 8% 10% 56% 23% 10% -6% 9% 10% 11% 14%

Highway and Street 7% 12% -5% -1% 3% 9% 12% 6% 6% 1% 0% 4% 5% 5% 4%

Sewage and Waste Disposal 9% 10% 35% 2% 8% 11% 17% 7% 3% -5% 2% 4% 5% 6% 6%

Water Supply 13% 9% 32% 0% 1% 11% 7% 6% 6% -7% 0% 3% 7% 7% 8%

Conservation and Development 9% 18% -9% 9% 3% 10% 15% 3% 0% 7% 18% 8% 4% 4% 3%

Total Nonbuilding Structures 14% 11% 5% 4% -2% 9% 12% 20% 11% 3% -2% 6% 7% 8% 9%

Total Put in Place 8% 5% 1% 5% 11% 11% 6% -1% -7% -15% -7% 5% 9% 9% 9%

*Improvements include additions, alterations and major replacements. It does not include maintenance and repairs.

Millions of Current Dollars 3rd Quarter 2010

Change From Prior Year - Current Dollar Basis3rd Quarter 2010

C o n s t r u c t i o n P u t i n P l a c e

Estimated for The United States)

16Construction Outlook

About FMIFMI is the largest provider of management consulting, investment banking and research to the design and con-struction industry. We work in all segments of the industry providing clients with value-added business solu-tions, including:

Strategy Development Market Research and Business Development Leadership and Talent DevelopmentProject and Process Improvement Mergers, Acquisitions and Financial Consulting

Founded by Dr. Emol A. Fails in 1953, FMI has professionals in offices across the U.S. FMI delivers innovative,customized solutions to contractors; construction materials producers; manufacturers and suppliers of buildingmaterials and equipment; owners and developers; engineers and architects; utilities; and construction industrytrade associations. FMI is an advisor you can count on to build and maintain a successful business, from your leadership to your site managers.

About FMI’s Research Services GroupAs the construction industry becomes increasingly competitive, market intelligence becomes an important toolfor the building industry. A more complete understanding of the market, market trends, customer perceptions,buying practices, competitor profiles and other market influencers will enhance craft labor studies.

Since 1953 FMI has provided consulting and training services specialized for the construction industry. FMI’smarket research includes both secondary and primary research designed to meet clients’ specific needs. Bothtypes of research are used to provide accurate assessments in a timely, efficient and concise manner for clients.

Typical project work performed includes customer buying practices, competitive analyses, market-size modeling,market forecasts and trends, channel performance analyses, customer satisfaction surveys and sales performanceevaluations.

J. Randall (Randy) GiggardManaging Director, Research Services

Randy Giggard is responsible for design,

management, and performance of

primary and secondary market

research projects and related research

activities, including economic analysis

and modeling, construction market

forecasting and database management.

Randy’s particular expertise is in the

areas of market sizing and modeling,

competitive analysis, sales and market

performance evaluations, buying

practices and trends analysis.

Randy holds undergraduate degrees in

mechanical engineering from Southern

Illinois University and English from

Illinois State University and a master

of marketing and management policy

degree from Northwestern University.

T 919.785.9268 F 919.785.9320E-mail: [email protected]_____________________________FMI CORPORATIONRaleigh5171 Glenwood Ave., Ste. 200Raleigh, NC 27612P 919.787.8400 F 919.785.9320

Denver210 University Boulevard, Ste. 800Denver, CO 80206P 303.377.4740 F 303.398.7291

Tampa308 South Blvd.Tampa, FL 33606P 813.636.1364 F 813.636.9601

Phoenix5080 N. 40th St., Suite 245Phoenix, AZ 85018T 602.381.8108 F 602.381.8228

BenefitsA Construction Market Forecast from FMI’s Research Services Group can:_____________________________________________

Supply the market-oriented, economy-drivendimension essential for preparing, implementingand monitoring strategic plans.Be a significant aid in defining, targeting, implementing and monitoring other critical corporate decisions, such as long- and short-termsales goals, or redirecting resources (i.e., on a geographic or a product-line basis).Provide the basis for estimating submarkets.Provide the basis for comparing performanceamong markets.Provide the basis for identifying activities that arebeneficial or detrimental to performance.

FeaturesEach Standard Construction Market Forecast:_____________________________________________

Details construction put in place in three residentialbuilding, 11 nonresidential building and five non-building structure categories. It covers the currentyear, eight previous years and five forecast years.It is available for any county in the U.S. or anycombination of counties, metropolitan statisticalareas, states, regions, etc.Includes both construction values and annualpercentage changes. Delivery time depends on thesize of the request but is usually only a few days.It can be delivered in printed or electronic form,and in most major text or spreadsheet formats.Graphs can be provided at additional cost.

FMI’s Construction Market ForecastsBasis_____________________________________________

Historical information in FMI’s standard ConstructionMarket Forecast is based on building permits andconstruction put in place data as provided by theU.S. Commerce Department. Forecasts are based oneconometric and demographic relationships devel-oped by FMI, on information from specific projectsgathered from trade sources, and on FMI’s analysisand interpretation of current and expected socialand economic conditions.

Other Reports_____________________________________________Reports on state and federally financed highway construction are available for most counties or combinations of counties.Custom reports on a wide variety of construction-related topics can be prepared by FMI.Reports are based on multiple sources and areappropriate for preliminary analytical and planningpurposes, but contain little or no direct observationof the area described and are not guaranteed byFMI to be accurate.

_________________________________________

For more information, call 919.785.9268

_________________________________________

Copyright 2010 FMI Corporation. All rights reserved. Printed in the United States of America.Notice of Rights: No part of this publication may be reproduced or transmitted in any form, or by any means, without permission from the publisher: 919.787.8400.To order additional copies of this book, please call 800.669.1364 or complete the order form at the back of this publication.