Embed Size (px)

Citation preview

Information on this page is provided by Shakun & Company (Services) Private Limited, New Delhi, India to its subscribers against the annual subscription. Non-subscribers may visit www.shakun.com for more details.

F.No.354/28/2007-TRU Government of India Ministry of Finance

Department of Revenue (Tax Research Unit)

New Delhi ** ** **

8th March, 2007

New Delhi

NOTICE

T.R. Rustagi Report on Review of circulars, instructions and clarifications of issues relating to service tax

Taxation of services was introduced in 1994. Since then, a number of circulars/instructions/ clarifications have been issued from time to time by CBEC on various aspects of service tax. 2. Government decided to undertake review of all such circulars, instructions and clarifications issued on matters relating to levy and collection of service tax, keeping in view the changes in service tax law, the Court pronouncements and other material considerations. For this purpose, Government has asked Shri T.R. Rustagi, Chief Commissioner (Retd.) to undertake the aforesaid review and to make recommendations in this behalf to the Government. 3. Shri T.R. Rustagi has submitted his report to the Government on 22.2.2007. As per his report, circulars, instructions and clarifications are segregated into the following three categories: (i) To be withdrawn (Annexure A) (To view, click on Annexures) (ii) To be modified (Annexure B) (iii) To be retained (Annexure C) 4. Views, comments and suggestions from the trade and industry associations, departmental officers and from all others concerned are solicited on the recommendations made in the report. Suggestions in respect of circulars or instructions which could not be covered by this report are also invited. The views, comments, and suggestions may kindly be sent before 31st March, 2007 to the undersigned at the following address: Room No. 146 H, Tax Research Unit, North Block, New Delhi-110002 (E-mail: [email protected])

Sd/- (K. Balamurugan)

OSD - TRU

�/2

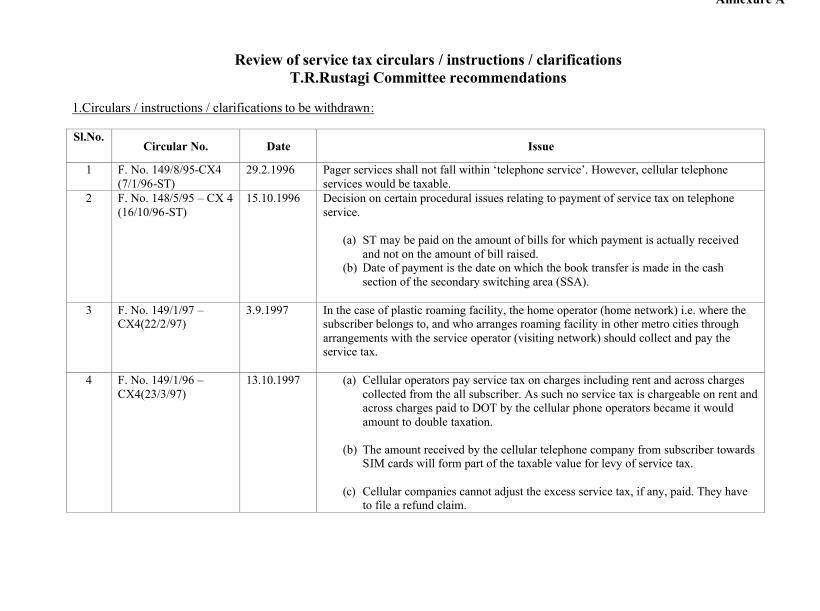

Annexure A

Review of service tax circulars / instructions / clarifications T.R.Rustagi Committee recommendations

1.Circulars / instructions / clarifications to be withdrawn: Sl.No.

Circular No. Date Issue

1 F. No. 149/8/95-CX4 (7/1/96-ST)

29.2.1996 Pager services shall not fall within ‘telephone service’. However, cellular telephone services would be taxable.

2 F. No. 148/5/95 – CX 4 (16/10/96-ST)

15.10.1996 Decision on certain procedural issues relating to payment of service tax on telephone service.

(a) ST may be paid on the amount of bills for which payment is actually received and not on the amount of bill raised.

(b) Date of payment is the date on which the book transfer is made in the cash section of the secondary switching area (SSA).

3 F. No. 149/1/97 –

CX4(22/2/97) 3.9.1997 In the case of plastic roaming facility, the home operator (home network) i.e. where the

subscriber belongs to, and who arranges roaming facility in other metro cities through arrangements with the service operator (visiting network) should collect and pay the service tax.

4 F. No. 149/1/96 – CX4(23/3/97)

13.10.1997 (a) Cellular operators pay service tax on charges including rent and across charges collected from the all subscriber. As such no service tax is chargeable on rent and across charges paid to DOT by the cellular phone operators became it would amount to double taxation.

(b) The amount received by the cellular telephone company from subscriber towards

SIM cards will form part of the taxable value for levy of service tax.

(c) Cellular companies cannot adjust the excess service tax, if any, paid. They have to file a refund claim.

2

(d) In certain cases, cellular telephone operators provide service to a category of

persons called “friendly users”, and only recover “land line charges”. No service tax is payable on the calls made as no amounts recovered by the telegraph authority.

(e) Companies give discount on their airtime charges. It is clarified that in such cases

the tax is payable only on the reduced amount.

5 28/2/99 (F. No. 149/6/97-CX4)

4.7.1999 The clarification issued for plastic roaming facility vide Circular No. 22/2/97 dated 3.9.1997 would apply mutatis mutandis to automatic roaming facility including International Automatic/plastic roaming facility provided by cellular phone operators.

6 33/1/2001 (F. No. 149/1/99 – CX4)

29.01.2001 Earlier, in Circular No. 5/5/94 dated 10.11.1994 it was classified that DOT can pay service tax by Book adjustment. Now that it has been corporatised into BSNL, with effect from 1.11.2000, service tax has to be paid in cash.

7 46/9/2002-ST (F. No. 149/2/2002-CX4)

8.8.2002 References have been received from the Cellular Operators Association of India, New Delhi, and the Department of Telecom (DOT). The services relating to which doubts have been raised are the following :

(i) ‘Inter-connection link charges’: These are charges relating to interconnectivity provided between the basic/cellular telephone providers and the BSNL/MTNL exchanges. This enables the private basic telephone operators or the mobile service providers to access BSNL telephone lines and vice-versa. This interconnection can be through a cable owned by the BSNL; in which case a monthly/annual rent is charged. If the cable has been laid/ provided by the private basic/cellular telephone service provider no rental is charged by BSNL.

(ii) ‘Rentals for junction links’: These relate to charges for using junction links of the BSNL/MTNL from one exchange to another.

(iii) ‘Port charges’: These are something like entry charges for allowing access into the BSNL network.

3

(iv) ‘Infrastructure charges’: Sometimes the basic as well as cellular telephone service providers need space to keep their own equipments to facilitate the interconnectivity. This space, when provided by the DOT, a rental is covered from them by the DOT.

It is clarified that in respect of services listed at (ii), (iii) and (iv) above no service tax is presently leviable. However, So far as ‘inter-connectivity linked charges’ are concerned these are nothing but charges for providing ‘leased circuits’. This service (leased circuits) has been brought under the coverage of service tax w.e.f. 16-7-2001. While issuing Board’s clarification dt. 14-3-2001 it was inter alia intimated that this service was not taxable. However, since ‘leased circuits’ have become taxable. However, since ‘leased circuits’ have become taxable w.e.f. 16-7-2001 only, Board’s clarification dated 14-3-2001 stands modified accordingly.

8 F. No. 150/1/94 – CX4 (3/3/94-ST)

28.07.1994 It is clarified that Kerala State Insurance Department (KSID) and all such other agencies are required to pay service tax as they provide taxable service in relation to general insurance.

9 F. No. 150/1/94 – CX4 (6/1/95-ST)

02.05.1995 Asking for information from the commissioners on the practice of adjustment of excess tax by United General Insurance Co. and similar other insurance companies.

10 F. No. 137/11/96 – CX4 21/1/97-ST

27.01.1997 Instruction on revised procedure for registration/collection of service tax from courier agencies.

11 64/13/2003-ST (F. No. 168/1/2003-CX4)

28.10.2003 It is clarified that if the canvassing is limited to space selling then such services would not be liable to any service tax. However, if canvassing is involving receiving the text of advertisement, estimating the space that such advertisement would occupy in the newspaper/periodical/magazine, negotiating the price, forming the general layout of the advertisement that would finally appear in the newspaper then such activity would be liable to service tax under the category of Advertising Agency Services.

12 F. No. 241/1/2004 – CX4 (78/8/2004-ST)

23.03.2004 It is clarified that selling the free commercial time (FCT) to a producer does not fall within the purview of ‘advertisement service’.

13 F. No. 354/128/97 – TRU

18.12.1997 Service rendered by architects would not fall within the scope of engineering consultancy service. Architects and engineers are governed by separate technical and statutory authorities. However if an engineer provides service as an engineering service as also an architectural service and he charges a lump sum amount, the lump sum amount shall be

4

the value, unless separate break up is given in the bill. 14 34/2/2001-CX 30.4.2001 Consulting engineer will not include those qualified engineers who act as insurance

surveyors and loss assessors within its scope hence not liable to service tax. The services provided by any qualified engineer in the area of insurance survey or loss assessment are not in the nature of services in an engineering discipline. Even as per the WTO classification of services, insurance survey and loss assessment is categorized as insurance auxiliary services and not as “consulting engineering services”

15 F. No. 177/5/2004 – CX

26.02.2002 Third party inspections and certifications carried out by certifying agencies in respect of marine as well non-marine equipment do not fall within the scope engineering consultancy. Such work is not in the category of advice, consultancy or technical assistance. If, however, a shipping company gets the ship surveyed or inspected by another agency before taking it for certification or by an authorize agency, only then can it be said that the first agency is providing some technical service.

16 F. No. 137/38/2003–CX4

13.05.2004 Charges for erection, installation and commissioning are not covered under the category of Consulting Engineering Service. In circular No. 137/13/2001–CX4 dated 18.12.2002 it was clarified that erection and commissioning charges are taxable because this service is in the nature of “technical assistance” to buyer of plant / machinery. This position does not hold good in any case after service tax was levied separately on erection and commissioning with effect from 1.7.2003.

17 B43/1/97 – TRU 06.06.1997 Payments made by CHA on behalf of the client such as statutory levies (cess, custom duties, port dues, etc.) and various others reimbursable expenses incurred are not to be included in the value for service tax.

18 B43/1/97 – TRU 06.06.1997 Where CHA undertakes “turnkey” imports and exports and where as lump sum amount is charged from the client for undertaking various service the lump sum amounts covers not only the “agency commission” fee but also other expenses and no separate breakup is available. In such cases the value of taxable service is to be taken as 15% of the lump sum amount charged from the client.

19 B43/1/97-TRU 6.6.1997 Sub-contracting of CHA will not be required to pay service tax on the bills raised by him on the main CHA.

20 B43/1/97 – TRU 06.06.1997 No service tax is leviable on payment received by CHA from shipping lines for canvassing of import/export cargo.

21 B43/1/97 – TRU 06.06.1997 It is clarified that in relation to steamer agent, the service charges will constitute the

5

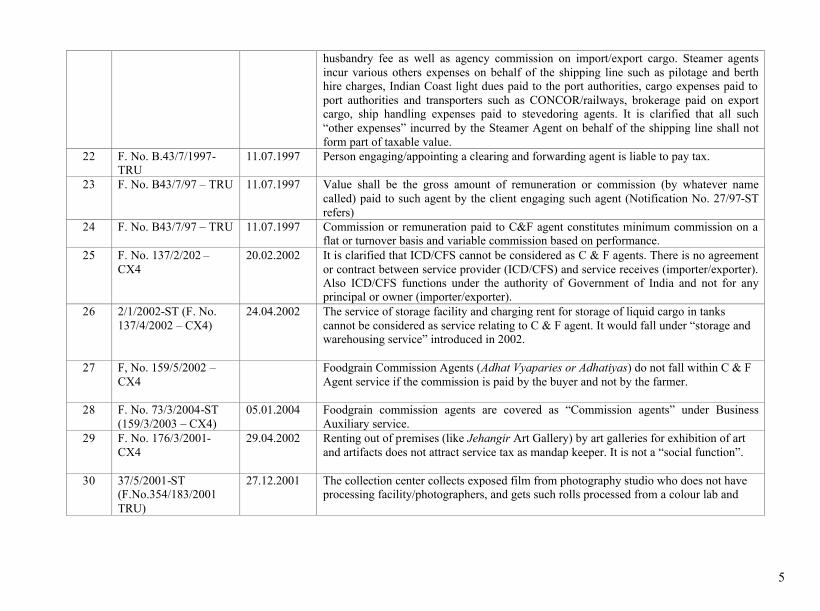

husbandry fee as well as agency commission on import/export cargo. Steamer agents incur various others expenses on behalf of the shipping line such as pilotage and berth hire charges, Indian Coast light dues paid to the port authorities, cargo expenses paid to port authorities and transporters such as CONCOR/railways, brokerage paid on export cargo, ship handling expenses paid to stevedoring agents. It is clarified that all such “other expenses” incurred by the Steamer Agent on behalf of the shipping line shall not form part of taxable value.

22 F. No. B.43/7/1997- TRU

11.07.1997 Person engaging/appointing a clearing and forwarding agent is liable to pay tax.

23 F. No. B43/7/97 – TRU 11.07.1997 Value shall be the gross amount of remuneration or commission (by whatever name called) paid to such agent by the client engaging such agent (Notification No. 27/97-ST refers)

24 F. No. B43/7/97 – TRU 11.07.1997 Commission or remuneration paid to C&F agent constitutes minimum commission on a flat or turnover basis and variable commission based on performance.

25 F. No. 137/2/202 – CX4

20.02.2002 It is clarified that ICD/CFS cannot be considered as C & F agents. There is no agreement or contract between service provider (ICD/CFS) and service receives (importer/exporter). Also ICD/CFS functions under the authority of Government of India and not for any principal or owner (importer/exporter).

26 2/1/2002-ST (F. No. 137/4/2002 – CX4)

24.04.2002 The service of storage facility and charging rent for storage of liquid cargo in tanks cannot be considered as service relating to C & F agent. It would fall under “storage and warehousing service” introduced in 2002.

27 F, No. 159/5/2002 – CX4

Foodgrain Commission Agents (Adhat Vyaparies or Adhatiyas) do not fall within C & F Agent service if the commission is paid by the buyer and not by the farmer.

28 F. No. 73/3/2004-ST (159/3/2003 – CX4)

05.01.2004 Foodgrain commission agents are covered as “Commission agents” under Business Auxiliary service.

29 F. No. 176/3/2001- CX4

29.04.2002 Renting out of premises (like Jehangir Art Gallery) by art galleries for exhibition of art and artifacts does not attract service tax as mandap keeper. It is not a “social function”.

30 37/5/2001-ST (F.No.354/183/2001 TRU)

27.12.2001 The collection center collects exposed film from photography studio who does not have processing facility/photographers, and gets such rolls processed from a colour lab and

6

hands over the prints to the photography studio/photographer.

For rendering this service they normally receive commission/handling charges from the processing labs and in some cases they may recover handling charges from the customers also. They act merely as a courier/commission agent. Therefore, the services provided by the collection center is not taxable in the category of photography service

31 232/2/2003-CX4 3.3.2006 It is clarified that in case, the goods are consumed during the provisions of service and are not available for sale, the provisions of the notification (No. 12/2003) would not be applicable. Therefore, in super- session of clarification to the contrary (issued by field officers), it is clarified that goods consumed during the provisions of service, that are not available for sale, by the service provider would not be entitled to benefit under Notification No. 12/2003-S.T., dated 20.06.2003.

32 F. No. 241/1/2004 – CX4

23.03.2004 In the case of FCT (Free Commercial Time) selling the time allotted to a producer does not fall within the preview of “advertisement service” since this activity is not connected to making, preparation, display or exhibition of advertisement. This is akin to providing space in a newspaper and magazine for publishing and advertisement and has nothing to do with actual presentation of the advertisement.

33 699/15/2003-CX (F. No. 248/1/2002 – CX4)

05.03.2003 Service of motor vehicles of any other make is not liable to service tax.

34 F. No. 341/43/2001-TRU

18.10.2001 Doubts have been raised as to whether the "value of taxable service" in respect of broadcasting services will include the commission paid by the broadcasting agency to the advertising agency or not. The Value of taxable service is the amount received by the broadcaster for providing the broadcasting service. Therefore, Service Tax is leviable only on the amount received by the broadcaster for the services rendered. Since the amount received by the broadcaster is net of the commission or discount paid to the advertising agency, service tax will be payable on this amount. However, such abatement towards commission/discount shall be allowed only when the same is clearly indicated in the invoice/bill raised by the broadcasting agency on the advertising agency.

35 F. No. 165/2/2003-CX4 27.3.2003 Prasar Bharati is not liable to pay service tax.

7

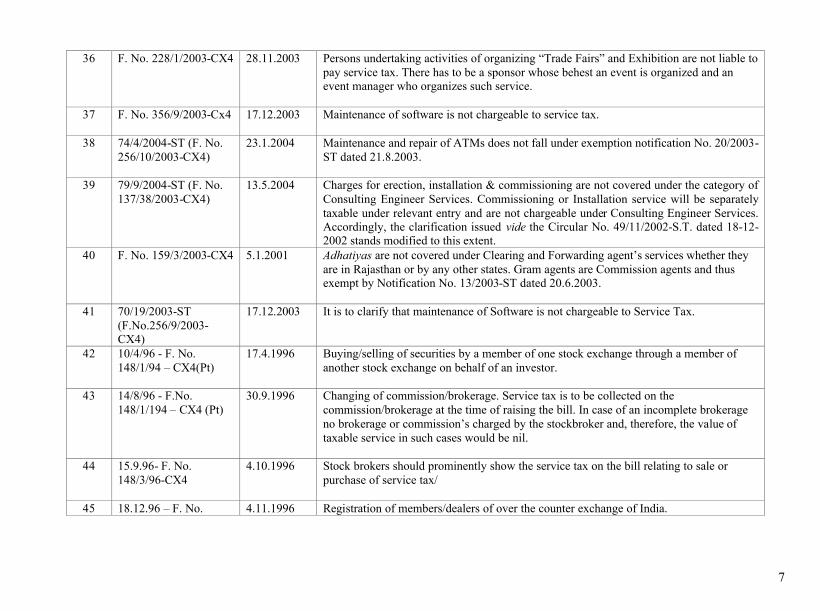

36 F. No. 228/1/2003-CX4 28.11.2003 Persons undertaking activities of organizing “Trade Fairs” and Exhibition are not liable to pay service tax. There has to be a sponsor whose behest an event is organized and an event manager who organizes such service.

37 F. No. 356/9/2003-Cx4 17.12.2003 Maintenance of software is not chargeable to service tax.

38 74/4/2004-ST (F. No. 256/10/2003-CX4)

23.1.2004 Maintenance and repair of ATMs does not fall under exemption notification No. 20/2003-ST dated 21.8.2003.

39 79/9/2004-ST (F. No. 137/38/2003-CX4)

13.5.2004 Charges for erection, installation & commissioning are not covered under the category of Consulting Engineer Services. Commissioning or Installation service will be separately taxable under relevant entry and are not chargeable under Consulting Engineer Services. Accordingly, the clarification issued vide the Circular No. 49/11/2002-S.T. dated 18-12-2002 stands modified to this extent.

40 F. No. 159/3/2003-CX4 5.1.2001 Adhatiyas are not covered under Clearing and Forwarding agent’s services whether they are in Rajasthan or by any other states. Gram agents are Commission agents and thus exempt by Notification No. 13/2003-ST dated 20.6.2003.

41 70/19/2003-ST (F.No.256/9/2003-CX4)

17.12.2003 It is to clarify that maintenance of Software is not chargeable to Service Tax.

42 10/4/96 - F. No. 148/1/94 – CX4(Pt)

17.4.1996 Buying/selling of securities by a member of one stock exchange through a member of another stock exchange on behalf of an investor.

43 14/8/96 - F.No. 148/1/194 – CX4 (Pt)

30.9.1996 Changing of commission/brokerage. Service tax is to be collected on the commission/brokerage at the time of raising the bill. In case of an incomplete brokerage no brokerage or commission’s charged by the stockbroker and, therefore, the value of taxable service in such cases would be nil.

44 15.9.96- F. No. 148/3/96-CX4

4.10.1996 Stock brokers should prominently show the service tax on the bill relating to sale or purchase of service tax/

45 18.12.96 – F. No. 4.11.1996 Registration of members/dealers of over the counter exchange of India.

8

148/5/96-CX4 46 19/13/93 F. No.

137/8/94-CX4 21.11.1996 Visits of Central Excise Offices to premises of assesses for conducting Audit.

47 20/14/96 (F. No.

148/1/94-CX4(Pt)) 31.12.1996 When the transaction is on principal to principal basis between brokers, no investor is

involved and as such no taxable service is provided and therefore, no service tax is chargeable.

Where a broker enters into a transaction on his own account with an investor who is a non-member of the stock exchange the service provided will be taxable service and subject to service tax.

In case of arbitrage transaction i.e. the transaction between two brokers of different stock exchanges, the service is provided by a broker i.e. the member of a stock exchange to a non-member of that stock exchange even though the investor may be a member of another stock exchange. Their being an investor involved in the transaction, the service so provided to the investor will be a taxable service subject to service tax.

48 148/3/97 – CX4 9.9.1997 When a member enters into a transaction with another member, it is jobbing and thus not liable to service tax.

49 51/13/2002-ST 7.1.2003 Guidelines on classification of services

50 57/6/2003-ST

(F.No.254/1/2003-CX4)

20.5.2003 Clarification on export of services, including on secondary services consumed in export services.

51 57/6/2003-ST (F.No.254/1/2003-CX4)

20.5.2003 If the bill is raised after the rate increase comes into force and even if the service was provided earlier, the increased rate would apply.

52 No. 77/07/2004 (F. No. 137/04/2004-CX-4)

10.3.2004 It is to clarify that where an assessee does not maintain separate accounts, input service tax credit can be utilized only to the extent of 35% of the total service tax payable on all the taxable output services.

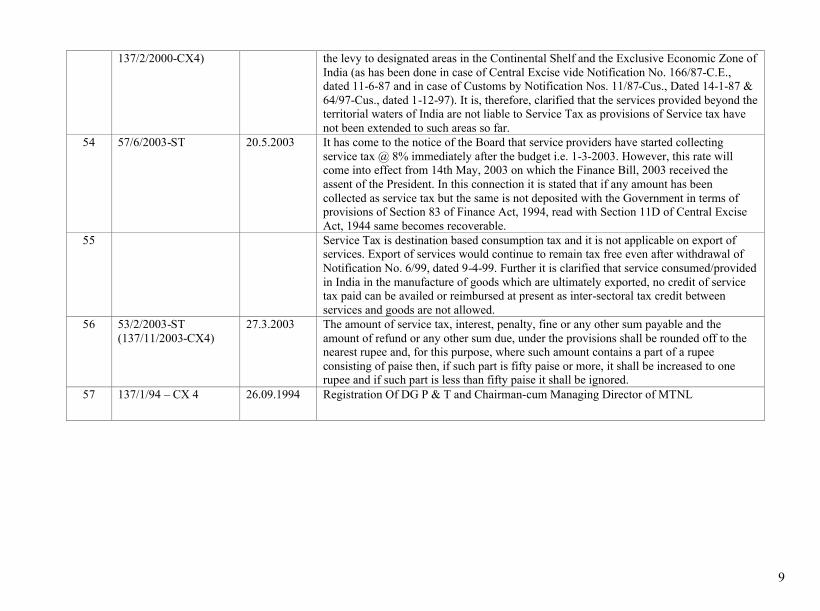

53 36/4/2001 (F. No. 8.10.2001 Chapter V of the Finance Act which governs the levy of Service Tax has not extended to

9

137/2/2000-CX4) the levy to designated areas in the Continental Shelf and the Exclusive Economic Zone of India (as has been done in case of Central Excise vide Notification No. 166/87-C.E., dated 11-6-87 and in case of Customs by Notification Nos. 11/87-Cus., Dated 14-1-87 & 64/97-Cus., dated 1-12-97). It is, therefore, clarified that the services provided beyond the territorial waters of India are not liable to Service Tax as provisions of Service tax have not been extended to such areas so far.

54 57/6/2003-ST 20.5.2003 It has come to the notice of the Board that service providers have started collecting service tax @ 8% immediately after the budget i.e. 1-3-2003. However, this rate will come into effect from 14th May, 2003 on which the Finance Bill, 2003 received the assent of the President. In this connection it is stated that if any amount has been collected as service tax but the same is not deposited with the Government in terms of provisions of Section 83 of Finance Act, 1994, read with Section 11D of Central Excise Act, 1944 same becomes recoverable.

55 Service Tax is destination based consumption tax and it is not applicable on export of services. Export of services would continue to remain tax free even after withdrawal of Notification No. 6/99, dated 9-4-99. Further it is clarified that service consumed/provided in India in the manufacture of goods which are ultimately exported, no credit of service tax paid can be availed or reimbursed at present as inter-sectoral tax credit between services and goods are not allowed.

56 53/2/2003-ST (137/11/2003-CX4)

27.3.2003 The amount of service tax, interest, penalty, fine or any other sum payable and the amount of refund or any other sum due, under the provisions shall be rounded off to the nearest rupee and, for this purpose, where such amount contains a part of a rupee consisting of paise then, if such part is fifty paise or more, it shall be increased to one rupee and if such part is less than fifty paise it shall be ignored.

57 137/1/94 – CX 4 26.09.1994 Registration Of DG P & T and Chairman-cum Managing Director of MTNL

Annexure B

Review of service tax circulars / instructions / clarifications T.R.Rustagi Committee recommendations

2.Circulars / instructions / clarifications to be modified:

Sl.No. Circular No. Date Issue Comments

1 B3/7/2003-TRU 20.6.2003 In regard to credit of service tax on telephone connection, queries have been raised as to whether service tax credit would be admissible on telephone sets installed only in the business premises. The answer is in the affirmative, and credit will be allowed only on telephone sets installed in the business premises. Mobile phones are not covered.

The tribunal and the Courts may not buy this argument. Cenvat Rules do not make an exception. Some solution has to be found to resolve this controversy. Either it be disallowed legally, or be allowed legally—say a specific proportion of the tax paid on mobile phones in the name of the company.

2 F. No. 137/1/94 – CX4 (1/1/94)

29.06.1994 It is clarified that branches and divisions of the insurance companies will not pay the service tax and it’s their head office, which have been made responsible for payment of service tax.

Clarification no longer needed in view of comprehensive rules on registration.

3 F. NO. 341/43/96 – TRU

31.10.1996 It is a Budget Circular covering different service including courier service.

(a) Transporters undertaking door to door services (like “Express Cargo Service”) are covered by the definition of “Courier”.

(b) Department of Post is not a

“Commercial concern”. Hence speed post is not taxable are courier service.

(c) Co-loaders are not covered in the

definition of courier service. They are

May be retained. No longer valid now. The words ‘commercial concern’ have been replaced by ‘person’. May be abolished. This may be withdrawn. The words “commercial concern” has been replaced by

2

not required to pay service tax.

(d) Any document received in India from abroad and for which no charge is made to the recipient is not liable to service tax as “courier agency”.

(e) It is clarified that courier agency is liable to pay service tax on the amount charged in India from the customer even if the documents, goods or articles are delivered abroad.

(f) If any facilities like warehousing, packing, inventory management, etc is provided by a courier agency the charges for same are includible in value as they are relatable to door to door transportation.

“person” in the definition of courier service. Business Auxiliary Service is very wide in scope, covering such activities. Also Cenvat credit is admissible. Thus, co-loaders are legally liable to pay service tax. Continues to be valid. Continues to be valid. Comprehensive valuation rules take care of it now. No longer needed.

4 F. No. 341/43/96 – TRU

31.10.1996 It is clarified that the amount paid, excluding their own commission, by the advertising agency for space and time in getting the advertisement published in the print media or electronic media will not be includible with value of taxable service.

May be withdrawn. The position has changed now on account of the fact that the display of advertisements through electronic media is covered by a separate taxable service (Broadcasting service) and Cenvat credit rules have come in.

5 F. No. 341/43/96 – TRU

31.10.1996 It is clarified that expenses incurred by the advertising agency on account of travel, transportation and stay in hotels, etc. are to be included in value.

No longer needed. Now, comprehensive valuation rules are to be followed for determining value of a taxable service.

3

6 F. No. 341/43/96 – TRU

31.10.1996 It is clarified that if market research conducted by an advertising agency relates to advertisement, then its charges form part of value.

No longer needed. Now, comprehensive valuation rules are to be followed for determining value of a taxable service.

7 F. No. 341/43/96 – TRU

31.10.1996 A film producer engaged by an advertising agency for making a documentary or film in relation to an advertisement is not liable to pay service tax where the advertiser includes film producer’s charges into his value to the client.

Clarification no longer valid now, after the words “commercial concern” have been replaced by “person” and the Cenvat rules have came. May be withdrawn.

8 F. No. 341/43/96 – TRU

31.10.1996 DAVP not being a commercial concern is not liable to pay service tax as an advertising agency.

Clarification no longer valid now. May be withdrawn.

9 F. No. B43/5/97 – TRU

02.07.1997 The levy does not fall on the sub-consultant, associate consultant or another consulting engineer. It falls only on to prime consultant or main consulting engineer who raises a bill on his client (which includes the charge for services rendered by the sub-consultant).

The clarification no longer holds good now. Sub-contractors are liable to pay tax.

10 F. No. B43/5/97 – TRU

02.07.1997 Expenses incurred by the consulting engineer as reimbursable expenses on behalf of the client and for which the documentary evidence is available do not form part of taxable value.

Clarification is not relevant after valuation rules have come in. Now, whether any such expenses are excludable or not is to be determined by application of these rules to a given situation.

11 F. No. B43/5/97 – TRU

02.07.1997 Service tax on manpower recruitment agencies shall be on the gross amount charged to the client for services rendered in relation to the recruitment of manpower excluding the amount incurred by the manpower recruitment agency on behalf of the client towards expenses, which are reimbursed on actual basis.

Instructions may be withdrawn. After the Valuation Rules have come into effect, the value is to be determined as per these rules.

4

12 F. No. B43/3197 – TRU

26.06.1997 Option to pay service tax at the rate of 0.25% of the basis fare in the case of domestic tickets and 0.5% of the basic fare in the case of international tickets.

May be deleted. Percentages have been revised. No need of issuing any Circular on this aspect.

13 B43/3/97 – TRU 26.06.1997 Service tax is to be paid not only on the hire charges for the mandap but also on charges for electricity, whether on actual basis or otherwise, charged to the customers. It is immaterial that bills are issued separately. Also charges for providing furniture, fixtures, lighting fittings, etc. to be included.

May be omitted. Now that the Valuation Rules have come into effect, value of any taxable service is to be determined as per these rules.

14 F. No. B43/3/97 – TRU

26.06.1997 If booking for mandap is cancelled no service tax is payable as no service has been rendered.

It is not needed. It is so obvious.

15 F. No. B43/3197 – TRU

26.06.1997 Even if mandap is located or situated in the premises of any public place of worship such as temple, church, etc. service tax’s payable.

May be withdrawn. Since then exemption has been provided by notification No. 14/2003-ST dated 20.6.2003, effective from 1.7.2003.

16 F. No. B43/3197 – TRU

26.06.1997 In case Mandap keeper provides catering service also, the tax is payable on 60% of the total charges, by virtue of notification No. 21/97-ST.

Now the exemption is contained in notification No. 1/2006-ST

17 F. No. 332/82/97 – TRU

24.09.1997 In case no charges/rental is paid i.e. the premises are given out free of cost to hold such functions, there would be no service tax liability.

May be omitted now.

18 F. No. B43/10/97 – TRU

22.08.1997 State Roadways Corporations who ply passengers in neighbouring State will not be covered by the levy as they do not require a tourist permit but operate on the strength of

It appears that in the wake of several show cause notices issued, the issue had been kept in abeyance for a decision vide Board’s letter F. No. 354/15/2004-TRU dated 30.1.2004. The

5

agreements between the concerned State authorities.

issue needs to be clarified. It is not justified to charge service tax on such routine journeys. If need be, it may be exempted.

19 F. No. B43/10/97 – TRU

22.08.1997 In the case of a composite tour which combines tour within India and also outside India, service tax would be leviable only on services rendered for tours within India provided separate billing has been done by the tour operator for services provided in respect of tours within India.

It seems to lack legality. The scope of tour operator service has been widened in 2004. Exports of Service Rules have also come in. The clarification requires to be re-examined in the light of changes. These instructions were issued when service tax was yet to ‘settle’. Prima facie, in this case, tax would fall on the full value.

20 F. No. B43/7/97 – TRU

11.07.1997 Service tax will not be payable in case where a bill has been raised on a Rent-a-Cab Scheme operator by another such operator who has sub-let the motor cab to the latter operator provided he pays service tax on the amount billed to his client for renting out the motor cab so obtained by him.

The clarification does not seem to be legally correct. This clarification was in the context of service tax system when Cenvat credit scheme was not applicable. With Cenvat scheme now applicable to service tax the instruction may be withdrawn.

21 F. No. B11/1/98 – TRU

07.10.1998 If an architect sub-contracts the work to another architect no service tax is payable by the sub-contractor provided the principal architect pays the service tax.

The clarification is not legally correct. This clarification was given when Cenvat credit scheme was not applicable. The instruction may be withdrawn.

22 F. No. B11/1/98 – TRU

07.10.1998 Service tax is not leviable on supply of materials, items of furniture or decoration, per se, but on service rendered in any manner concerning planning, design or beautification of spaces. Also the service rendered by Art directors of films and others who render services of design etc. for setting up temporary structures/ setting for shooting etc. do not attract the service tax levy as such interior decoration

Instruction may be withdrawn. Some services may now come within the scope of Business Auxiliary Service, depending upon the facts.

6

has no permanency and is only of a temporary nature.

23 F, No. B11/1/98 – TRU

07.10.1998 If architect sub-contracts the work to another architect no service tax is payable by the sub-contractor provided the principal architect pays the service tax.

The clarification is not legally correct. This clarification was given when Cenvat credit scheme was not applicable. The instruction may be withdrawn.

24 B11/1/98 – TRU 07.10.1998 Services in respect of sale/purchase/leasing of real estate, evaluation of a proposal real estate scheme/project by conducting techno-economic studies, providing feasibility reports and even helping in marketing real estate projects are all covered in the service tax. However, it is clarified that activity of actual construction of building, carried out by builders/developers does not attract service tax.

Latter part no longer valid. Service tax is now applicable to construction of building also.

25 F. No. B11/1/98 – TRU

7.10.1998 It is clarified that no abatement in respect of Salary to the employee, employee’s EST and EFP contribution, income tax deduction at source, payment towards professional tax and labour welfare fund and other non-statutory charges such as bonus, leave, uniforms, incidental expenses and other administrative and miscellaneous expenses is allowed from value of taxable service, except an account of statutory levies and taxes provided the same has direct relation with the services rendered to the client and is specifically billed to the client and is reimbursable by the client on actual basis. EPF, ESI contributions are also not admissible. These contributions are generally applicable and not confined to security agency alone.

Clarification may be withdrawn. Now that Comprehensive Valuation Rules have come into existence, value of a taxable service is to be determined by applying these rules.

7

26 F. No. B11/1/98 – TRU

07.10.1998 Service of providing safe deposit lockers or security/safe vaults either by the banks or by others is taxable but exempt by notification No. 56/98-ST dated 7.10.1998

No longer valid now. Notification No. 56/98 was rescinded on 9.7.2004.

27 F. No. B11/1/98 – TRU

7.10.1998 Information and advisory services, if any, rendered by credit rating agencies would not attract service tax for the reason that “taxable service” in respect of a credit rating agency means services provided to a client only in relation to credit rating of any financial obligation, instrument or security. Similar is the case of services of research and information such as analysis of industries in specific sectors, of financial and business out look of the company etc.

May be withdrawn. It is now covered under Banking and Other Financial Services.

28 F.No.B11/1/98-TRU 7.10.1998 A sub-contractor of a market research agency is not required to pay service tax.

The clarification is no longer valid now. Sub-contractor has to pay the tax and the main contractor can take the credit.

29 F. No. B11/1/98-TRU

7.10.1998 Services rendered by a market research agency to a person abroad shall not attract service tax as service tax levy extends only to services provided within India.

May be withdrawn. Now whether it attracts the tax has to be decided in the context of Export of Service Rules.

30 F. No. B11/1/98-TRU

7.10.1998 The fee of the rating agency is generally expressed as a percentage of the amount of debt sought to be raised. The fees on any assignment are usually paid at the time of entering with an agreement are usually paid at the time of entering into an agreement i.e. in advance. Such amounts are kept as advance against rating fee and is recognized as income only when the rating is assigned. After the rating is given it is

Instruction was issued to explain the nature of activity when the tax was introduced.

8

communicated to the client. The rating of any instrument remains under surveillance until the entire debt is repaid. The surveillance is a mandatory exercise for rating agencies. After surveillance the client is billed as per the agreed fee structure. Service tax is payable both on the fees received for credit rating of the debt instrument and the surveillance fees.

31 F. NoB11/1/98-TRU 7.10.1998 Reimbursable out-of-pocket expenses charged to the client on actual basis, such as traveling, boarding and lodging expenses, are not to be included in the value of taxable service.

Clarification may be omitted. Value of taxable service is now governed by application of Valuation Rules.

32 F. No/ B11/1/2001 – TRU

09.07.2001 If scientific or technical consultancy is provided to government departments or public sector undertakings for which consultant fees are received, then service tax has to be paid on such service.

Not needed. It is obvious.

33 F. No. B11/1/2001 – TRU

09.07.2001 The cost of unexposed photography film sold to customer is to be excluded from value if the cost is shown separately in the invoice along with description and value of film.

Not needed. Valuation is governed by detailed provisions now.

34 F. No. B11/1/2001 – TRU

09.07.2001 Individual professional photographers and others providing photographic service but who do not have fixed place of business will not be liable to pay service tax.

May be omitted. This was valid when notification No. 6/2001 was in force. Now they have to pay tax subject to exemption under notification No. 20/2005 dated 7.6.2005.

35 F. No. B11/1/2001 – TRU

09.07.2001 No service tax is applicable to convention held by the Chambers of Commerce and Industry for the reason that Chambers of Commerce and Industry are not commercial concerns.

The clarification is no longer relevant now. The words “commercial concern” have been replaced by “person”. It may be withdrawn.

36 F. No. B11/1/2001 – TRU

09.07.2001 Service tax is not be payable in respect of facsimile services where service charges are

The clarification is based on the consideration that telephone calls are already covered under

9

based on the number of telephone calls consumed. Private Fax operators are providing this kind of service and, therefore, they are not liable to service tax again.

service tax. However, there is no good logic for not levying service tax on private Fax operators. They charge more than charges for telephone calls. If need be the definition of “taxable services” may be modified and the taxability in respect of fax service need not be confined to service provided by a “telegraph authorities”. However, it may also be seen whether this service has any revenue potential. If not, it may be better to withdraw tax on this service.

37 F. No. B11/1/2001 – TRU

09.07.2001 ISPs are liable to pay service tax. Paid websites are also liable to pay service tax. It is clarified that in e-commerce transactions no service of online information and data base access/retrieval is involved. Therefore e-commerce transactions will not ordinarily be covered under the service tax net.

Continues to be valid.

38 F. No. B11/1/2001 – TRU

09.07.2001 Cyber cafes are not liable to pay service tax. Clarification is no longer valid now. Service tax has been imposed on Cyber cafes.

39 F. No. B11/1/2001 – TRU

09.07.2001 Interconnection charges paid by one ISP to another are not liable to service tax.

This clarification lacks legality. Now that Cenvat credit rules are in existence, this may be withdrawn.

40 54/3/2003-ST (F. No. 149/9/2002 – CX4)

21.04.2003 Internet telephony service falls in the category of on line information and data base access and/or retrieval service.

No longer valid. Now it falls under separately defined service.

41 F. No. B11/1/2001 – TRU

09.07.2001 The scope of taxable service covers any service in relation to videotape production in any manner. Thus facilitation activities such as providing studios, others facilities as light, gadgets, instruments, devices, providing technical person for operating the recording devices or for any other activity in relation to

Continues to be valid.

10

video tape production are taxable. Similarly editing, colouring, dubbing, printing titles and special effects, film processing etc. by a video production agency will come within the scope of this service.

42 F. No. B11/1/2001 – TRU

09.07.2001 It is clarified that reproduction of original master to make further copies of a video tape will not be taxable.

May not be valid now. Definition of taxable service now covers any post-production service also.

43 F. No. B11/1/2001 – TRU

09.07.2001 Services provided by individual photographers do not attract service tax. Tax is payable by studios, shops, and other establishments carrying on business of rendering services in the field of videography.

Individuals are also liable to pay service tax now, subject to exemption limit vide notification No. 20/2005 dated 7.6.2005.

44 F. No. B11/1/2001 – TRU

09.07.2001 The activities which fall under this category of service are providing the facility of studio, technical persons, musical instrument and other devices or any other facility or all the facilities in a consolidated manner, required for recording sound, editing thereof, providing different kinds of sounds from the sound library for use in theater film and radio, etc. services of mixing of sounds etc.

Explains the scope of taxable service. May be retained.

45 F. No. B11/1/2001 – TRU

09.07.2001 It is clarified that reproduction of original master to make further copies of the audio tape or CDs etc. will not come within the preview of service tax.

Requires examination. Any audio post-production activity is now covered by the definition of “taxable service”.

46 F. No. B11/1/2001 – TRU

09.07.2001 It may be emphasized that only such services are taxable which are in relation to general insurance business such as motor vehicle insurance, insurance of buildings and other properties, marine insurance, fire insurance and other miscellaneous insurance. Services

Not valid now. Since then service provided in relation to life insurance has become taxable as a separate service.

11

provided in relation to life insurance are not taxable.

47 F. No. B11/1/2001 – TRU

09.07.2001 The service providers are insurance agents, insurance surveyors and loss adjusters, actuaries and insurance consultants. They are liable to pay service tax in respect of the service provided to the insurance companies (insurer). However, in the case of insurance agents, the tax is to be paid by the insurance company.

Continues to be valid.

48 F. No. B11/1/2001 – TRU

09.07.2001 It is clarified that the amount billed to the client on account of out of pocket expenses which are reimbursable on actual basis such as traveling, boarding and lodging expenses, are not subject to service tax.

May be omitted. Such cases are now to be considered in the light of Valuation Rules.

49 F. No. 160/3/2002 – CX4

01.07.2003 Ship chandlers engaged in supply of “Ship stores” to the used or undertaking minor repair work to clear technical snag of the vessel through their locally arranged resources as work ship etc. are liable to pay service tax. These are services rendered in relation to the vessel under authorization form port authorities.

To be examined.

50 F. No. B11/1/2001 – TRU

09.07.2001 Cost of parts and accessories supplied during course of repair and servicing of which will not be includible in the taxable value. Such cost should be shown separately in the bill/invoice.

May be withdrawn. Value depends on facts of the case. They get consumed in the service provided. Thus, arguably, their value should form part of the value of the service provided. Cenvat credit is also admissible.

51 F. No. 281/1/2002 – CX4

05.03.2003 Cost of engine oil, gear oil, coolants is not be to be included in value. However paints used for painting body, etc. during the course of providing service forms an intrinsic part and

Instruction needs revision. Now that Cenvat Credit Scheme is applicable, there is no logic for excluding value of lubricating oils, paints, etc. from the value of taxable service.

12

parcel of service and it is not distinctly and separately identifiable. Therefore value of such terms which form intrinsic part of service is to be included in value.

52 F. No. B11/1/2002-TRU

1.8.2002 It has been provided in the Service Tax Rules that in the case of an insurance agent for life insurance, the person liable to pay service tax will be the concerned insurance company who has appointed the agent. Notification No. 12/2002 – ST refers.

Not needed. It is mentioned in the Rules.

53 F. No. B11/1/2002-TRU

1.8.2002 As a result of notification No. 9/2002, no service tax is payable on the service provided by an insurer to a policy holder in relation to life insurance business.

No longer valid. It is now taxable.

54 F. No. B11/1/2002-TRU

1.8.2002 The service tax is applicable to services provided on or after 16.8.2002 and any payment made for the services provided prior to this date will not be liable to tax though payment is made on or after 16.8.2002.

May be withdrawn. No longer needed now.

55 F. No. B11/1/2002-TRU

1.8.2002 If lump sum amount is charged for both transportation and cargo handling, the tax will be payable on the entire amount, unless the bill indicates the amounts separately on actual basis (verifiable by documentary evidence).

May be omitted. Valuation provisions are quite elaborate now.

56 F. No. B11/1/2002-TRU (Para 6)

1.8.2002

It is clarified that service provided in relation to any cargo which is meant for export, would not be taxable irrespective of the fact that it reaches the place of export after transshipment. However, relevant documents should show that the goods are for export.

May be retained. However, if the cargo is handled within the port area, it would attract tax as a port service, even if it is an export cargo.

13

57 F. No. B11/1/2002-TRU (Para 8)

1.8.2002

It is clarified that unaccompanied baggage of a passenger will not be leviable to service tax.

Not needed. It follows from the definition of ‘taxable service’ in this case.

58 F. No. B11/1/2002-TRU (Para 11)

18.2.2002

Where the CFS offers a total package rate, which includes transportation and handling in respect of imported laden containers from port to CFS, if the cost of transportations is claimed on actual basis, then it will not be includible in taxable value of cargo handling service.

May be omitted. Valuation provisions are elaborate now.

59 F. No. B/11/1/2002-TRU (Para 13)

1.8.2005

Marketing or canvassing for cargo for airlines does not come within the ambit of cargo handling service.

May be withdrawn. It may come in Business Auxiliary Service.

60 F. No. N11/1/2002-TRU (Para 15)

1.8.2002

If someone hires labour/labourer for loading or unloading of goods in his individual capacity, it will not come under the preview of service tax as a cargo handling agency.

Not needed. It is so obvious.

61 F. No. B11/1/2002-TRU (Para 5)

1.8.2002 Mere renting of space cannot be said to be in the nature of service provided for storage of warehousing of goods. Essential test is whether the storage keeper provides security of goods, stacking, loading/ unloading of goods in the storage are.

Arguably, it may not be correct. Rent could be payment in lieu of storage charges.

62 F. No. B11/1/2002-TRU (Para 6)

1.8.2002 Service provided by Airport Authority of India (AAI) for cold storage of perishable goods at cargo complexes is not taxable because Cold Storage has been specifically excluded from the tax net.

Not needed. It follows from the definition itself

63 F. No. B11/1/2002-TRU (Para 11)

1.8.2002

Terminal charges charged by Airport Authority of India (AAI) as facilitation charges for providing a terminal does not involve any

May be omitted now. Value is to be determined as per valuation provisions

14

service but as per notification No. Cargo/13519/PEI dated 4.6.1993 of the Airport Authority of India, “Storage and processing charges” specifically include terminal charges also. Hence terminal charges are to be included in the value.

64 F. No. B11/1/2002-TRU (Para 8)

1.8.2002

Cloak room service for passenger baggage in railway stations, bus stations, etc. is incidental to rail transport or road transport. They do not come within the preview of “storage and warehousing” service.

Arguably, it seems to lack legality. Storage of goods may be for short period or longer period. In both cases it is storage.

65 F. No. B11/1/2002-TRU (Para 10)

1.8.2002

CWC engages handling and transport contractors (H & T Contractors). H & T contractors have to pay service tax on cargo handling service and charge it to CWC. CWC adds supervision charges and raises the bill to the customers. For warehousing they raise a separate bill. The question is whether CWC is liable to pay service tax on cargo handling services and if so whether they can take credit of the tax paid on cargo handling services by the H&T contractor. Similar situation may exist in respect of storage and warehouse keepers. It is clarified that if the storage and warehouse keeper undertakes cargo handling services also and raises its own bill to the customer for such service, then he would be liable to pay service tax under the category of cargo handling services also. However, he would be eligible to take credit of service tax paid on cargo handling services rendered by the H&T contractors and

Credit Scheme has become liberal now. Credit can be taken across services. Such clarification is not really needed now.

15

adjust the same against his service tax liability on cargo handling services provided he raises a separate bill for the same to his client. In other words, he can not adjust the credit against storage and warehousing service charges.

66 F. No. B11/1/2002-CX4

10.7.2003 Handling/Storage and warehousing of empty containers would be covered within the scope of storage and warehousing service. Clarification issued vide F. No. B11/1/2002-TRU dated 1.8.2002 regarding empty containers not to be considered as cargo for cargo handling service has no relevance in this case.

Does not seem to be convincing. There is apparently contradiction in the approach in the two Circulars.

67 F. No. B11/1/2002-TRU (Para 4)

1.8.2002

Charges paid by the event manager to the photographer, videographer, sound recording studio, advertising agency, mandap keeper, security agency etc. will be included in the value of service.

This clarification is saying the obvious. It follows from the definition of value itself. Not needed now.

68 F. No. B11/1/2002-TRU (Para 5)

1.8.2002

In a case where the event is organized / managed by the Sponsor himself, no service tax is payable as “event management”.

Not needed. Too trivial a clarification.

69 F. No. B11/1/2002-TRU (Para 5)

1.8.2002

It is clarified that service tax under the category of event management is not leviable on the sale proceeds of tickets or revenue generated from the sale of space.

May be retained. However, whether sale of tickets would attract service tax as Business Auxiliary Service requires to be looked into.

70 B11/1/2002-TRU 1.8.2002 Service tax is payable whether the rail travel agent is registered with railways or not.

Not needed. Too trivial a clarification.

71 F. No. B11/1/2002-TRU (Para 4)

1.8.2002

No abatement towards cost of material used is allowed. Tax is to be computed on the gross amount charged by beauty parlour.

Not needed now. The law relating to valuation is comprehensive.

16

72 B11/1/2002-TRU (Para 3)

1.8.2002

Hair cutting and shaving is not taxable.

Not valid now. Hair cutting is now specifically included in the definition. Shaving also should fall in beauty treatment.

73 F. No. B11/1/2002-TRU (Para 4)

1.8.2002

Tailor is involved only in stitching of clothes. He is not liable to pay service tax. Similarly, jweller essentially makes jwellery and sells it. He is also not liable to pay service tax.

May be retained.

74 F. No. B11/1/2002-TRU (Para 6)

1.8.2002

At times fashion designer provides stitching service also if the bill shows the design charges separately, service tax is payable on the designing charges alone.

Not needed now. The law relating to valuation is comprehensive.

75 F. No. B11/1/2002-TRU (Para 5)

1.8.2002

Entertainment tax collected and paid for the government will not be includable in the value of taxable service provided the cable operator clearly indicates the entertainment tax element in his bill to the customer.

May be retained. Although why such clarification only for cable operator service? There should be general clarification regarding status of other taxes vis a vis value of taxable service, including advance tax.

76 F. No. B11/1/2002-TRU

1.8.2002 Service tax is not applicable to wet cleaning / washing provided the dry cleaner clearly mentions it in the bill. If details are not mentioned in the bill, it would normally be understood that cloth have been dry cleaned and in such situation service tax is liable to be paid.

As an anti-avoidance measure, service tax should be imposed on wet cleaning done by establishments commercially known as “Dry Cleaners” and the like.

77 F. No. B11/1/2002-TRU

1.8.2002 Service tax is not applicable to job of dyeing.

As an anti-avoidance measure, service tax should be imposed on wet cleaning done by establishments commercially known as “Dry Cleaners” and the like.

78 F. No. B7/3/2003-TRU

20.7.2003 For contracts entered into prior to 1.7.2003, service tax is payable on payments received after 1.7.2003. Similar will be the situation for payments made for continuing services.

This has been modified by Circular of even number dated 21.8.2003.

17

If service is provided free to the customer during the guarantee period but payment is made by the company, service tax would be payable on the payment so received irrespective of the fact that the receiver of the service is different from the person making the payment for such service.

79 F. No. B7/3/2003-TRU

21.8.2003 No service tax is payable on maintenance or repair service rendered prior to 1.7.2003 even though bill for payment was raised after 1.7.2003.

Not needed now. The clarification only states the general principle.

80 F. No. B3/7/2003-TRU

20.6.2003 Unless all the ingredient of definition of “franchise” are sales for an agreement is not a franchise. For example, the mere fact that a principal manufacturer has allowed production of goods bearing his brand name by another person under ‘License Production Agreement’ does not make the agreement a Franchise Agreement.

The Circular may be withdrawn. Definition of “Franchise” was changed in 2005 Budget.

81 F. NO. B3/7/2003-TRU

20.6.2003 In the case of turnkey project, service tax is leviable on commissioning or installation charges only and not on the initial and goods supplied. However, it is upto the service provider to show the break-up of commissioning or installation charges. In case service provider shows consolidated charges, service tax would be leviable on such consolidated amount.

There is confusion about applicability of service tax to turnkey projects. They should be covered under a separate service.

82 F. No. B3/7/2003-TRU

20.6.2003 Charges for erecting of plant are not covered by the service tax.

No longer valid now.

83 F. No. B3/7/2003-TRU

21.8.2003 Commissioning or installation service provided by an individual is exempt from service tax under notification No. 18/2003 dated 21.8.2003.

No longer valid now.

18

84 F. NO. B3/7/2003-TRU

20.6.2003 Business Auxiliary services provided by call centers and medical transcription centers have been fully exempt by notification No. 8/2003-ST dated 20.6.2003.

Not valid now.

85 F. NO. B3/7/2003-TRU

20.6.2003 Services of commission agent have been exempted by notification No. 13/2003-ST dated 20.6.2003. However, services of the consignment agent are taxable under the category of Clearing and Forwarding series.

Not valid now.

86 F. No. B3/7/2003-TRU

20.6.2003 Insurance agent, C & F agents working on commission basis do not fall under this category. They are controlled by respective separately defined taxable services.

Continues to be valid. Not needed now.

87 F. No. B3/7/2003-TRU

20.6.2003 Definition does not cover information technology service.

Not needed. It is by definition.

88 B1/6/2005-TRU 27.7.2005 It has been requested that in cases where liability for tax payment is on the consignor or consignee, the procedure as to how it should be confirmed by such consignor or consignee that the goods transport agency has not availed credit or benefit of notification No. 12/2003-Service Tax may be prescribed. In such cases it is clarified that a declaration by the goods transport agency in the consignment note issued, to the effect that neither credit on inputs or capital goods used for provision of service has been taken nor the benefit of notification No. 12/2003-Service Tax has been taken by them may suffice for the purpose of availment of abatement by the person liable to pay service tax.

Abatement is now provided by notification No. 1/2006-ST dated 1.3.2006. It is cumbersome to obtain the declaration for each transaction. Some trade-friendly approach, like quarterly declaration, is needed. Also, there is lot of hue and cry on this subject. The officers have not allowed benefit to those who pay the tax as service receiver. The DGST Circular created the avoidable confusion. Now, it is understood that C&AG has also taken objection. This matter needs to be resolved—by resorting to retrospective amendment, if need be. The intention can not be to deny the benefit of exemption.

19

89 137/3/2006-CX4 2.2.2006 In the case of depot sale of goods, the credit of service tax paid on the transportation of goods upto such depot would be eligible, irrespective of the fact whether the goods were chargeable to excise duty at specific rates or ad valorem rates on the basis of valuation under section 4 or 4A of the Central Excise Act.

This issue requires some serious consideration. There is significant confusion on the credit of service tax paid on transportation of goods from factories, when tax is paid by the consigner-manufacturer. Ideally, credit of service tax should be paid to whoever bears the incidence of tax.

90 80/10/2004-St 17.9.2004 In addition to the actual air freight charges, all charges collected towards storing, handling, loading / unloading (done in relation to air transportation of cargo) by an airlines are also chargeable to this levy.

Such instructions not needed now in view of comprehensive valuation rules.

91 80/10/2004-ST 17.9.2004 The service tax under this category would be limited to the services rendered in relation to survey and exploration only and not to any activity of the actual extraction after the survey and exploration is complete. The transport, refining, processing or production of the extracted products would also be out of the ambit of service tax. Activities such as seismic survey, collection/processing/interpretation of data and drilling or testing in relation to survey and exploration would, however, fall within the ambit of taxable service.

From Circular F. No. B1/6/2005-TRU dated 27.7.2005 issued while explaining the scope of “Survey and map making” it appears from para 8.2 of that circular that the term “other prospecting services” does not cover drilling. Thus, it appears that in relation to the survey and exploration of mineral service also, it was wrong to say that it covers ‘drilling’. This requires to be examined for necessary clarification.

92 80/10/2004-ST 17.9.2004 A permanent transfer of intellectual property does not amount to rendering of service. On such transfer, the person selling their rights no longer remains a “holder of intellectual property right”, so as to come under the preview of taxable service. Thus, there would not be any service tax on permanent transfer of IPRs.

The clarification not valid now. The definition of “intellectual property service” amended in 2005 has omitted reference to ‘permanent transfer’ of intellectual property right.

20

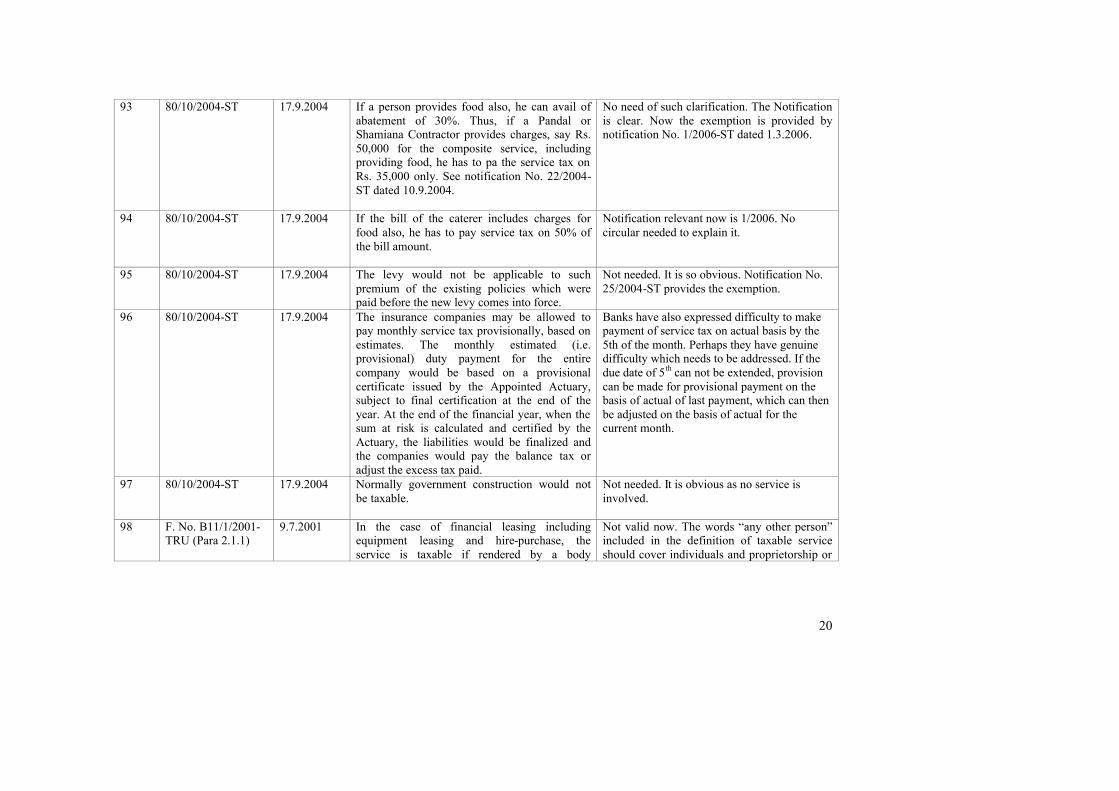

93 80/10/2004-ST 17.9.2004 If a person provides food also, he can avail of abatement of 30%. Thus, if a Pandal or Shamiana Contractor provides charges, say Rs. 50,000 for the composite service, including providing food, he has to pa the service tax on Rs. 35,000 only. See notification No. 22/2004-ST dated 10.9.2004.

No need of such clarification. The Notification is clear. Now the exemption is provided by notification No. 1/2006-ST dated 1.3.2006.

94 80/10/2004-ST 17.9.2004 If the bill of the caterer includes charges for food also, he has to pay service tax on 50% of the bill amount.

Notification relevant now is 1/2006. No circular needed to explain it.

95 80/10/2004-ST 17.9.2004 The levy would not be applicable to such premium of the existing policies which were paid before the new levy comes into force.

Not needed. It is so obvious. Notification No. 25/2004-ST provides the exemption.

96 80/10/2004-ST 17.9.2004 The insurance companies may be allowed to pay monthly service tax provisionally, based on estimates. The monthly estimated (i.e. provisional) duty payment for the entire company would be based on a provisional certificate issued by the Appointed Actuary, subject to final certification at the end of the year. At the end of the financial year, when the sum at risk is calculated and certified by the Actuary, the liabilities would be finalized and the companies would pay the balance tax or adjust the excess tax paid.

Banks have also expressed difficulty to make payment of service tax on actual basis by the 5th of the month. Perhaps they have genuine difficulty which needs to be addressed. If the due date of 5th can not be extended, provision can be made for provisional payment on the basis of actual of last payment, which can then be adjusted on the basis of actual for the current month.

97 80/10/2004-ST 17.9.2004 Normally government construction would not be taxable.

Not needed. It is obvious as no service is involved.

98 F. No. B11/1/2001-TRU (Para 2.1.1)

9.7.2001

In the case of financial leasing including equipment leasing and hire-purchase, the service is taxable if rendered by a body

Not valid now. The words “any other person” included in the definition of taxable service should cover individuals and proprietorship or

21

corporate. In other words, individuals, proprietorship or partnership firm will not come under the tax net. The leasing or hire-purchase may be of motor vehicles, machinery and equipment or other goods.

partnership firms.

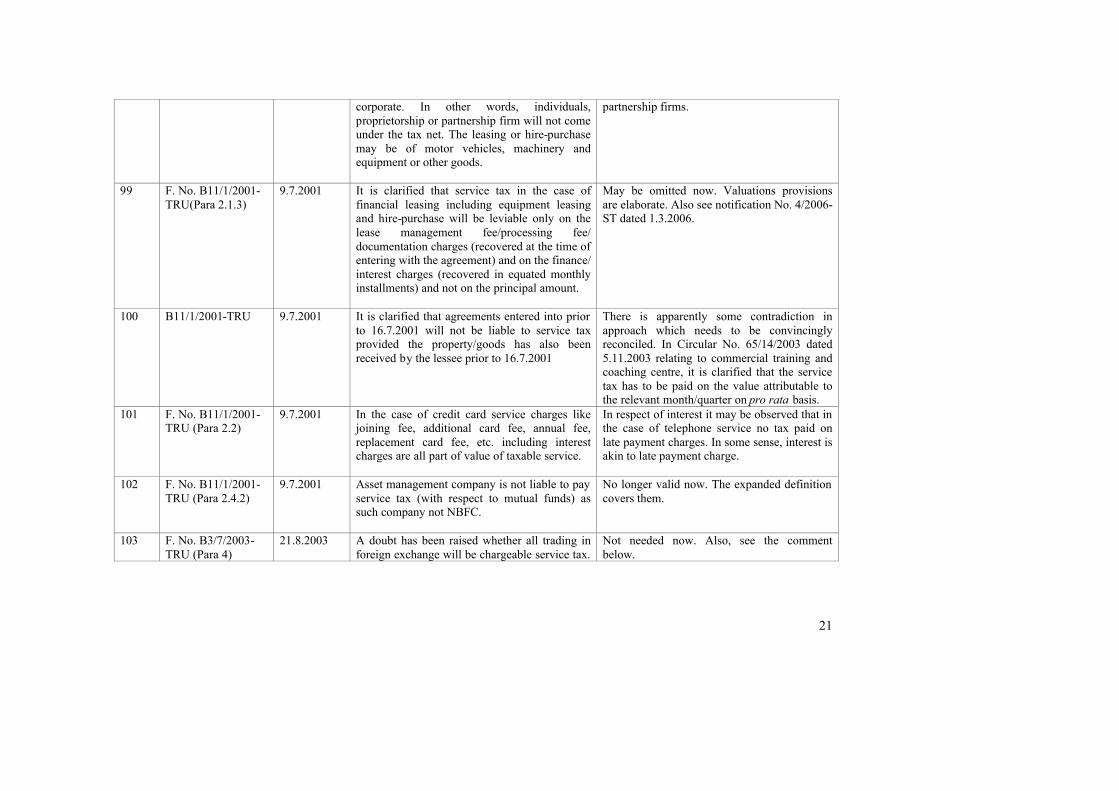

99 F. No. B11/1/2001-TRU(Para 2.1.3)

9.7.2001

It is clarified that service tax in the case of financial leasing including equipment leasing and hire-purchase will be leviable only on the lease management fee/processing fee/ documentation charges (recovered at the time of entering with the agreement) and on the finance/ interest charges (recovered in equated monthly installments) and not on the principal amount.

May be omitted now. Valuations provisions are elaborate. Also see notification No. 4/2006-ST dated 1.3.2006.

100 B11/1/2001-TRU 9.7.2001 It is clarified that agreements entered into prior to 16.7.2001 will not be liable to service tax provided the property/goods has also been received by the lessee prior to 16.7.2001

There is apparently some contradiction in approach which needs to be convincingly reconciled. In Circular No. 65/14/2003 dated 5.11.2003 relating to commercial training and coaching centre, it is clarified that the service tax has to be paid on the value attributable to the relevant month/quarter on pro rata basis.

101 F. No. B11/1/2001-TRU (Para 2.2)

9.7.2001

In the case of credit card service charges like joining fee, additional card fee, annual fee, replacement card fee, etc. including interest charges are all part of value of taxable service.

In respect of interest it may be observed that in the case of telephone service no tax paid on late payment charges. In some sense, interest is akin to late payment charge.

102 F. No. B11/1/2001-TRU (Para 2.4.2)

9.7.2001

Asset management company is not liable to pay service tax (with respect to mutual funds) as such company not NBFC.

No longer valid now. The expanded definition covers them.

103 F. No. B3/7/2003-TRU (Para 4)

21.8.2003

A doubt has been raised whether all trading in foreign exchange will be chargeable service tax.

Not needed now. Also, see the comment below.

22

Prior to 1.7.2003 the service of “securities and foreign exchange (forex) broking” when provided by banking company/financial institution/body corporate was liable to service tax. Though Finance Act, 2003 “foreign exchange broking” when provided by foreign exchange brokers, other than banking company/financial institution /body corporate were also brought under the tax net w.e.f. 1.7.2003. As per the definition in law foreign exchange broker include authorize dealer of foreign exchange. Authorised dealer of foreign exchange has been assigned the meaning of “authorized person” under the FEMA, 1999. Accordingly autorised dealer/money changers, etc. which are authorized to deal in foreign exchange are covered in the definition of “foreign exchange broker” under service tax provisions. However, as explained above only the service of “foreign exchange broking” when provided by foreign exchange broker (other then banking company/financial institutions/body corporate which are already covered) has been brought under the tax net.

104 341/44/2005-TRU 6.10.2005 Service tax on foreign exchange broking services is applicable to services provided by any foreign exchange broker including banking company, financial institution, non banking finance company any body corporate, or commercial concern. Statutory provisions are the same in respect of all these entities which are engaged in the same activity. Money changers cannot go out of the purview of

There are large numbers of representations in the context of this clarification. Some Commissioners have also supported the representations. It is argued that money changers do not deal in foreign exchange broking. They may have to take license from RBI, but, it is contended, they are not ‘authorised dealers’. It is also argued that no separate amount is charged by the money

23

service tax on the plea that they are merely selling and purchasing foreign currency and not dealing or brokering on foreign exchange. Under Sale of Goods Act, Goods means every kind of moveable property but excludes money. Therefore transactions in foreign exchange do no fall under scope of sale. In view of the statutory provisions, the services provided by money changers in relation to foreign exchange is covered under Banking and financial services as defined under 65(12) of the Finance Act and leviable to service tax under Section 65(105)(zm) or Section 65(105) (zzk) of the Finance Act, 1994.

changers. Their profit is only difference on account of buying rate and selling rate. Considering the numerous representations, matter deserves to be re-examined in consultation with RBI.

105 12/6/96 -F. No. 148/5/96-CX4

16.9.1996 Registration of Stock Brokers of National Stock Exchange.

Position to be examined with reference of new registration provisions.

106 B1/6/2005-TRU 27.7.2005 This service would generally cover construction services in respect of residential complexes developed by builders, promoters or developers.

Many have represented against DGST’s Circular No. V/DGST/22/Audit/Misc/1/2004 dated 16.2.2006 in the context of Raheja judgment that the inference drawn by DGST is incorrect. This matters deserves clarification by the Board. It seems that facts are important. Prima facie construction of flats by builders is not a service.

107 64/14/2003-ST (F.No.B3/3/2003-TRU (Pt.)

5.11.2003 It has been clarified in this Circular that where the value of taxable service has been received in advance for a service which became taxable subsequently, service tax has to be paid on the value of service attributable to the relevant month/quarter which may be worked out on pro rata basis.

It seems that the Valuation rules should contain specific legal provision to deal with such situation. Also, a question arises as to how to deal with cases of life membership—like membership of clubs.

24

108 56/5/2003-ST 25.4.2003 It is clarified that date of issue of invoice would be the date for deciding the applicability of service tax.

It requires consideration. Some Chief Commissioners/Commissioners have argued that the date on which service is provided is the relevant date. In Central Excise lot of litigation had taken place on the date of levy. It is desirable that on such fundamental issues suitable and clear cut legal provision in service tax law should deal with such matter.

Annexure C

Review of service tax circulars / instructions / clarifications T.R.Rustagi Committee recommendations

3.Circulars / instructions / clarifications to be retained:

Sl.No. Circular No. Date Issue Comments

1 F. No. 341/1/2000 – TRU (32/3/2000-ST)

20.12.2000 Service tax is not payable on the amount of surcharge charged on late payment of telephone bills.

May be retained as surcharge is not part of value of taxable service.

2 F. No. 341/16/2000-TRU

10.08.2000 Public Mobile Radio Trucking Service (PMRTS) System does not provide any service in relation to a telephone connection. Hence it is not covered within the scope of taxable service provided in relation to “a telephone connection”.

May be continued

3 334/4/2006-TRU 28.2.2006 “General insurance service” amended in 2006 Budget to include service provided to a policy holder or any person by an insurer, including a re –insurer.

Just a statement of fact.

4 F. No. 168/1/96 – CX4 10.10.1997 It is clarified that “Angadias”, who undertake to deliver the documents, goods or articles received from customers to the other end, are liable to pay service tax as “courier agency”.

Continues to be valid.

5 F. No. 345/4/97-TRU 16.8.1999 In the case of persons who are printing and publishing telephone directories, yellow pages or business directories, their activities is essentially of printing a readymade advertisement from the advertisers and publishing the same in the directory. Their activities are similar to those carried out by

Continues to be valid.

2

newspapers or periodicals. As such this activity shall not attract service tax. However, if the persons also undertake any activity relating to making or preparation of advertisement, such as designing, visualizing, conceptualizing etc then they will be liable to pay service tax on the charges thereon.

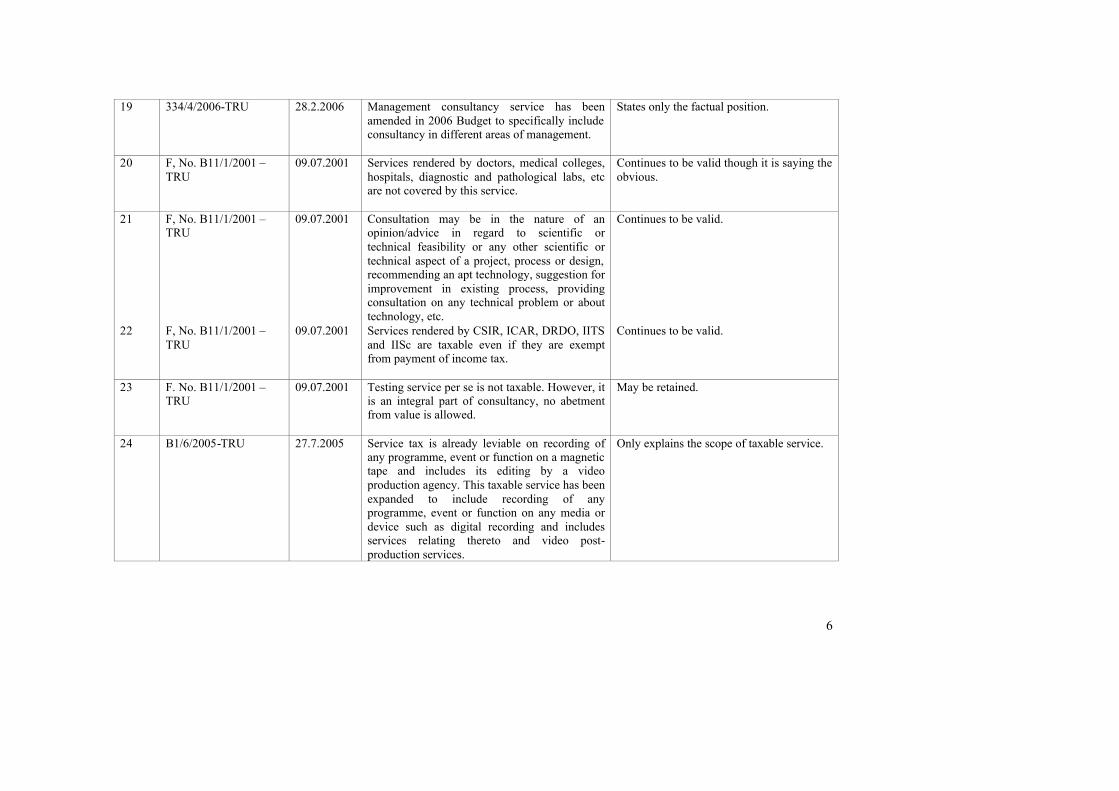

6 F. No. B43/5/97 – TRU 02.07.1997 Consulting engineers shall include self-employed professionally qualified engineer who may or may not have employed others to assist him or it could be an engineering firm-weather as a sole proprietorship, partnership, a private or a public limited company.

Continues to be valid. Definition is also self explanatory now.

7 334/4/2006-TRU 28.2.2006 Consulting engineer service to include engineering consultancy services provided by any firm or body corporate

It only states the change made in 2006 Budget.

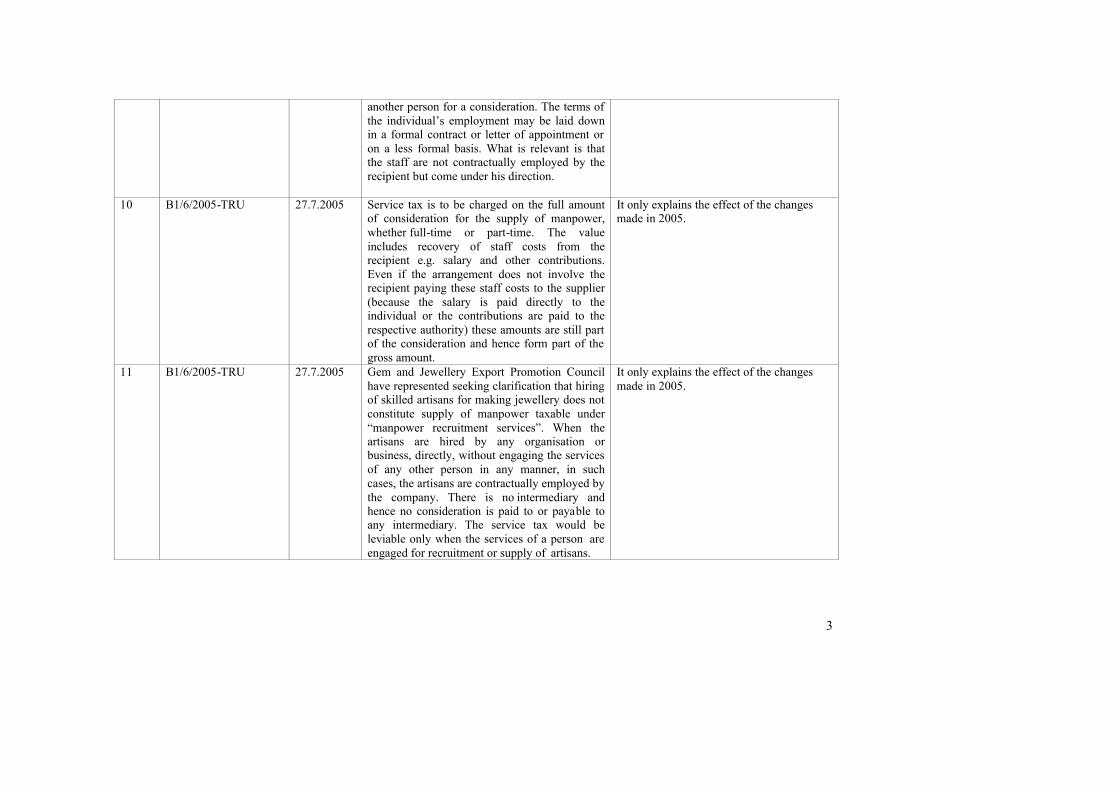

8 B1/6/2005-TRU 27.7.2005 Amendments have been made (effective from 16.6.2005) to levy service tax on temporary supply of manpower by manpower recruitment or supply agencies.

Statement of fact only.

9 B1/6/2005-TRU 27.7.2005 A large number of business or industrial organizations engage the services of commercial concerns for temporary supply of manpower which is engaged for a specified period or for completion of particular projects or tasks. Services rendered by commercial concerns for supply of such manpower to clients would be covered within the purview of service tax. In these cases, the individuals are generally contractually employed by the manpower supplier. The supplier agrees for use of the services of an individual employed by him to

It only explains the effect of the changes made in 2005.

3

another person for a consideration. The terms of the individual’s employment may be laid down in a formal contract or letter of appointment or on a less formal basis. What is relevant is that the staff are not contractually employed by the recipient but come under his direction.

10 B1/6/2005-TRU 27.7.2005 Service tax is to be charged on the full amount of consideration for the supply of manpower, whether full-time or part-time. The value includes recovery of staff costs from the recipient e.g. salary and other contributions. Even if the arrangement does not involve the recipient paying these staff costs to the supplier (because the salary is paid directly to the individual or the contributions are paid to the respective authority) these amounts are still part of the consideration and hence form part of the gross amount.

It only explains the effect of the changes made in 2005.

11 B1/6/2005-TRU 27.7.2005

Gem and Jewellery Export Promotion Council have represented seeking clarification that hiring of skilled artisans for making jewellery does not constitute supply of manpower taxable under “manpower recruitment services”. When the artisans are hired by any organisation or business, directly, without engaging the services of any other person in any manner, in such cases, the artisans are contractually employed by the company. There is no intermediary and hence no consideration is paid to or payable to any intermediary. The service tax would be leviable only when the services of a person are engaged for recruitment or supply of artisans.

It only explains the effect of the changes made in 2005.

4

12 86/4/2006-ST 1.11.2006 The principal activity of institutes like IITs or IIMs is to impart education without the objective of making profit. Therefore, these institutes cannot be called a “commercial concern”, even if on some of their activities (like holding campus interviews), they charge fee. Accordingly, these institutes were not liable to pay service tax prior to 1.5.2006 under the category of “manpower recruitment or supply service”. As regards the period after 1.5.2006, decision should be taken after taking into account all material facts on case to case basis.

This is a recent Circular. This Circular gives an interpretation to the expression “commercial concern”. Incidentally, it might have implication on disputes concerning the meaning of “commercial concern” in respect of some other taxable services which also used this expression prior to 1.5.2006.

13 F. No. B43/3197 – TRU

26.06.1997 Commission is adjusted automatically on cancellation or modification of tickets. As such question of claiming separately refund of service tax may not arise.

Continues to be valid.

14 F. No. B43/3197 – TRU

26.06.1997 Hotels and restaurants which let out their banquet halls, rooms, garden, etc. for holding/organizing any marriage, parties, conferences, shows, etc. are covered by the definition of mandap keeper.

Continues to be valid.

15 F. No. 332/82/97-TRU 24.09.41997 The activity of mere reservation of seat in a restaurant shall not attract service tax. To attract service tax on service rendered by mandap keeper it is mandatory that the mandap keeper has let out some room, space or hall for some period of time and during such period the room, space of hall is essentially in exclusive (temporary) possession of the person to whom it has been let out.

Continues to be valid.

5

16 F. No. 332/82/97 – TRU

24.09.1997 Service tax is payable as “mandap keeper” on renting out of hall etc. for the purposely holding a dance, drama or music programme or competition. These are social functions.

Continues to be valid.

17 341/21/99-TRU 20.8.1999 Services provided by the ESI, PF and other industrial law practitioners are in the nature of providing secretarial assistance in filling up of various returns and forms, maintenance of records which do not involve any chance of improvement in the existing system of management of organizations. Accordingly it is clarified that such ESI, PF and other industrial law practitioners will not be covered within the scope of the term “Management Consultant”.

Continues to be valid.

18 F. No. 177/2/2001 – CX4