Embed Size (px)

Citation preview

Focused Energy Report

Year - 2017

Edition - IV

Monthly Report – April 2017

Energy Desk

GAIL (India) Ltd.

1

Table of Contents

I. Energy Prices 3

II. Under-Recoveries on Petroleum Products 3

III. Country Analysis – Saudi Arabia 4

A. Energy Mix ...................................................................................................................................................... 4

B. SWOT Analysis ............................................................................................................................................... 4

C. Oil and Gas Reserves ................................................................................................................................... 5

D. Oil and Gas Infrastructure ......................................................................................................................... 6

IV. Company Analysis – Kuwait Petroleum Corporation (KPC) 7

A. Organisational Structure ............................................................................................................................ 7

B. SWOT ................................................................................................................................................................ 7

C. Operations ...................................................................................................................................................... 7

D. Strategy ............................................................................................................................................................ 8

E. Market Position ............................................................................................................................................. 9

V. LNG Industry Review 2016 10

A. Key Facts 2016 ............................................................................................................................................. 10

B. China, India and Emerging Importers Driving Demand Growth ............................................... 10

C. Spot & Short Term ..................................................................................................................................... 11

D. LNG Shipping ............................................................................................................................................... 11

E. Liquefaction Plants ..................................................................................................................................... 11

F. Regasification Terminals .......................................................................................................................... 12

VI. LNG Trade Outlook In Australia, US & Mexico 13

A. Australian LNG Export ............................................................................................................................... 13

B. MEXICO: US LNG DESTINATION ........................................................................................................... 13

2

Executive Summary

The Focused Energy Report for the month of April 2017 reviews the Energy Prices taking in consideration the

comparison with last month. There’s decrease of around 6.3 % in the WTI oil prices, the prices of natural

gas Henry Hub have increased by 15 % and crude oil prices of Brent decreased by around 5%.

The next discussion in the report is about “Saudi Arabia”. Saudi Arabia has 16% of the world's proved oil

reserves, is the largest exporter of total petroleum liquids in the world, and maintains the world's largest

crude oil production capacity. Saudi Arabia is the world's second largest holder of crude oil proved

reserves and was among the largest exporter of total petroleum liquids. In 2015, Saudi Arabia was the world's

second-largest petroleum liquids producer behind the United States and was the world's second-largest

crude oil producer behind Russia. Saudi Aramco does not operate any major functioning international

pipelines.

The analysis covers Energy Mix, SWOT Analysis, Oil and Gas Reserves and Oil and Gas Infrastructure.

In the next section “Company Analysis – Kuwait Petroleum Corporation (KPC)” is analysed. Kuwait

Petroleum Corporation (KPC) was formed in January 1980. KPC is a wholly state-owned organisation

responsible for Kuwait's oil and gas businesses. The shares of KOC, KNPC, PIC and KOTC were transferred

to the new Corporation. KPC successfully took all the oil companies under its umbrella and formed one

integrated oil industry in Kuwait. International downstream assets now comprise around 250,000b/d of

refining capacity in Europe, which includes the 75,500b/d Europort facility in Rotterdam and half of the

capacity of Eni's 300,000b/d Milazzo refinery

It covers Energy Productivity, Energy and electricity consumption, Electricity generation mix, Electric

generating, Renewable energy, Greenhouse gas emissions and Retail and wholesale power prices (2016

$/MWh)

In this section there is a discussion about “LNG Industry Review 2016”. In 2016, global LNG trade recorded a

growth rate of around 7.5% compared to 2015, returning to a robust pace experienced before 2011.

Primarily driven by new Australian volumes, additional supply was not as abundant as expected due to

production delays, slower ramp-ups and lower exports from historical suppliers. Sluggish oil prices have

continued to exert downward pressure on LNG contract prices. In the Pacific Basin, a combination of more

than adequate supply and of slow demand growth also pushed spot prices to a seven-year low. This situation

and the looming supply overhang are causing a slow-down in investment with several FIDs being cancelled or

deferred. Key Facts 2016:

• 263.6 million tons imported or a 7.5% increase vs. 2015

• 74.6 million tons traded on a spot or short term basis or 28% of total trade

• 4 New Importing Countries 11 New LNG Regasification Terminals, 39 Importing Countries

• 830 MTPA Total Regasification Capacity, 340 MTPA Total Nameplate Liquefaction Capacity

The analysis covers Key Facts 2016, China, India and Emerging Importers Driving Demand Growth, Spot &

Short Term, LNG Shipping, Liquefaction Plants and Regasification Terminals.

In the last section an analysis on “LNG Trade Outlook In Australia, US & Mexico “is covered. Despite

temporary outages at the first two trains, Train 3 of Australia’s Gorgon LNG project progressed well,

enabling an early start date. Chevron has announced that Train 3 will begin operations before the end of

March. The MANZANILLO terminal on Mexico’s Pacific Coast has become an eager customer for LNG from

the Sabine Pass plant in the United States. Moreover, trade relations are expected to deepen over the coming

months as the US continues to provide cheap and abundant LNG to the terminal. Manzanillo is importing

more and more cargoes, even though the prospects for LNG in Mexico as a whole are bleak.

The analysis covers Australian LNG Export and MEXICO: US LNG destination.

3

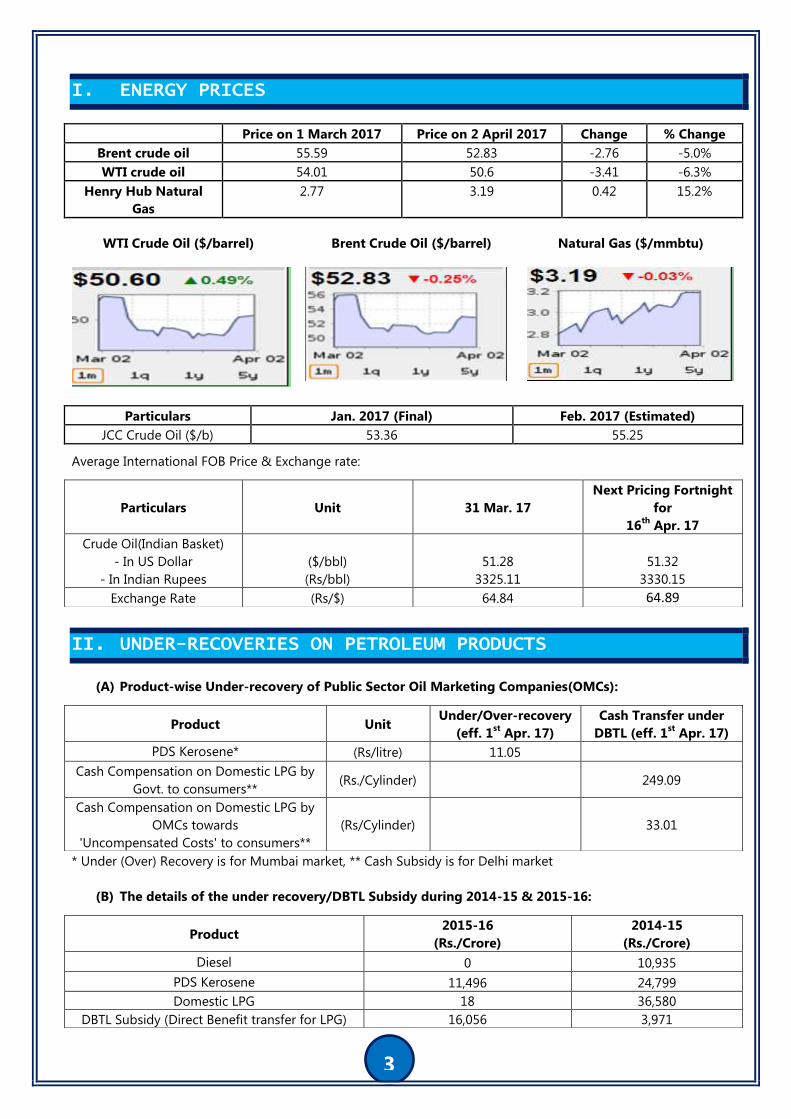

ENERGY PRICES I.

Price on 1 March 2017 Price on 2 April 2017 Change % Change

Brent crude oil 55.59 52.83 -2.76 -5.0%

WTI crude oil 54.01 50.6 -3.41 -6.3%

Henry Hub Natural

Gas

2.77 3.19 0.42 15.2%

WTI Crude Oil ($/barrel) Brent Crude Oil ($/barrel) Natural Gas ($/mmbtu)

Particulars Jan. 2017 (Final) Feb. 2017 (Estimated)

JCC Crude Oil ($/b) 53.36 55.25

Average International FOB Price & Exchange rate:

UNDER-RECOVERIES ON PETROLEUM PRODUCTS II.

(A) Product-wise Under-recovery of Public Sector Oil Marketing Companies(OMCs):

* Under (Over) Recovery is for Mumbai market, ** Cash Subsidy is for Delhi market

(B) The details of the under recovery/DBTL Subsidy during 2014-15 & 2015-16:

Particulars Unit 31 Mar. 17

Next Pricing Fortnight

for

16th

Apr. 17

Crude Oil(Indian Basket)

- In US Dollar

- In Indian Rupees

($/bbl)

(Rs/bbl)

51.28

3325.11

51.32

3330.15

Exchange Rate (Rs/$) 64.84 64.89

Product Unit Under/Over-recovery

(eff. 1st Apr. 17)

Cash Transfer under

DBTL (eff. 1st Apr. 17)

PDS Kerosene* (Rs/litre) 11.05

Cash Compensation on Domestic LPG by

Govt. to consumers** (Rs./Cylinder)

249.09

Cash Compensation on Domestic LPG by

OMCs towards

'Uncompensated Costs' to consumers**

(Rs/Cylinder) 33.01

Product 2015-16

(Rs./Crore)

2014-15

(Rs./Crore)

Diesel 0 10,935

PDS Kerosene 11,496 24,799

Domestic LPG 18 36,580

DBTL Subsidy (Direct Benefit transfer for LPG) 16,056 3,971

4

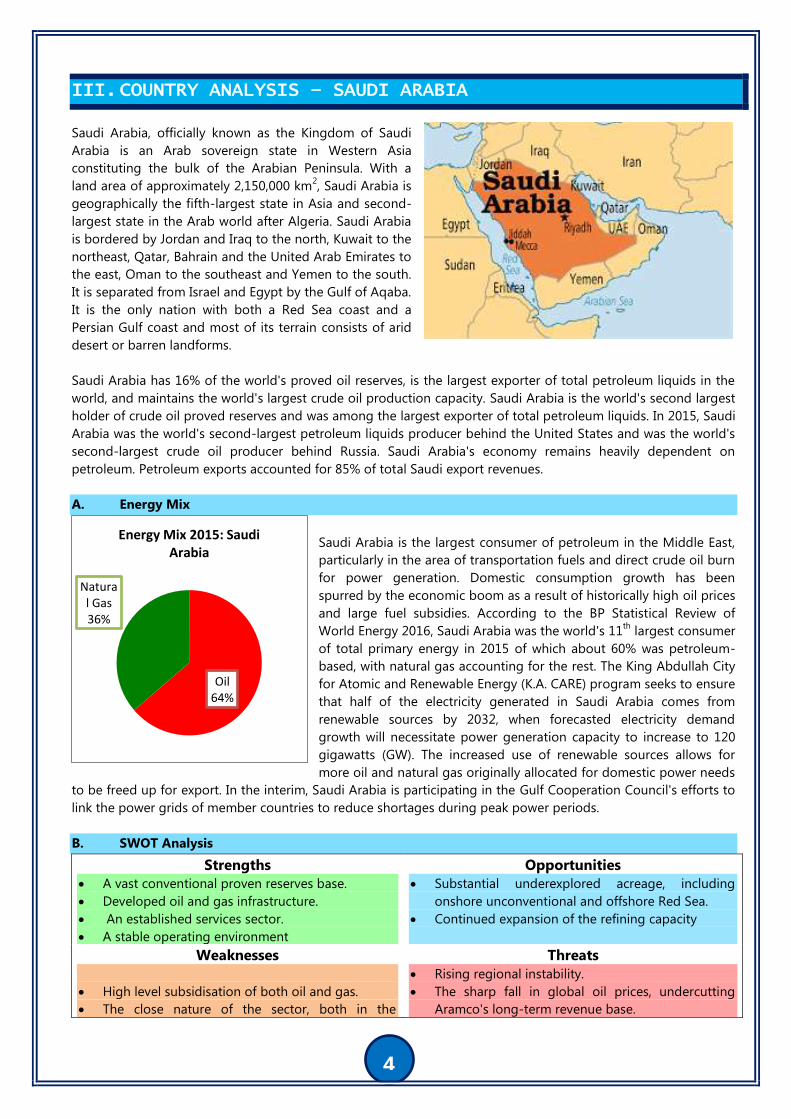

Oil 64%

Natural Gas 36%

Energy Mix 2015: Saudi Arabia

COUNTRY ANALYSIS – SAUDI ARABIA III.

Saudi Arabia, officially known as the Kingdom of Saudi

Arabia is an Arab sovereign state in Western Asia

constituting the bulk of the Arabian Peninsula. With a

land area of approximately 2,150,000 km2, Saudi Arabia is

geographically the fifth-largest state in Asia and second-

largest state in the Arab world after Algeria. Saudi Arabia

is bordered by Jordan and Iraq to the north, Kuwait to the

northeast, Qatar, Bahrain and the United Arab Emirates to

the east, Oman to the southeast and Yemen to the south.

It is separated from Israel and Egypt by the Gulf of Aqaba.

It is the only nation with both a Red Sea coast and a

Persian Gulf coast and most of its terrain consists of arid

desert or barren landforms.

Saudi Arabia has 16% of the world's proved oil reserves, is the largest exporter of total petroleum liquids in the

world, and maintains the world's largest crude oil production capacity. Saudi Arabia is the world's second largest

holder of crude oil proved reserves and was among the largest exporter of total petroleum liquids. In 2015, Saudi

Arabia was the world's second-largest petroleum liquids producer behind the United States and was the world's

second-largest crude oil producer behind Russia. Saudi Arabia's economy remains heavily dependent on

petroleum. Petroleum exports accounted for 85% of total Saudi export revenues.

A. Energy Mix

Saudi Arabia is the largest consumer of petroleum in the Middle East,

particularly in the area of transportation fuels and direct crude oil burn

for power generation. Domestic consumption growth has been

spurred by the economic boom as a result of historically high oil prices

and large fuel subsidies. According to the BP Statistical Review of

World Energy 2016, Saudi Arabia was the world's 11th

largest consumer

of total primary energy in 2015 of which about 60% was petroleum-

based, with natural gas accounting for the rest. The King Abdullah City

for Atomic and Renewable Energy (K.A. CARE) program seeks to ensure

that half of the electricity generated in Saudi Arabia comes from

renewable sources by 2032, when forecasted electricity demand

growth will necessitate power generation capacity to increase to 120

gigawatts (GW). The increased use of renewable sources allows for

more oil and natural gas originally allocated for domestic power needs

to be freed up for export. In the interim, Saudi Arabia is participating in the Gulf Cooperation Council's efforts to

link the power grids of member countries to reduce shortages during peak power periods.

B. SWOT Analysis

Strengths

A vast conventional proven reserves base.

Developed oil and gas infrastructure.

An established services sector.

A stable operating environment

Opportunities

Substantial underexplored acreage, including

onshore unconventional and offshore Red Sea.

Continued expansion of the refining capacity

Weaknesses

High level subsidisation of both oil and gas.

The close nature of the sector, both in the

Threats

Rising regional instability.

The sharp fall in global oil prices, undercutting

Aramco's long-term revenue base.

5

upstream and downstream segments.

Cumbersome bureaucracy.

Source: BMI

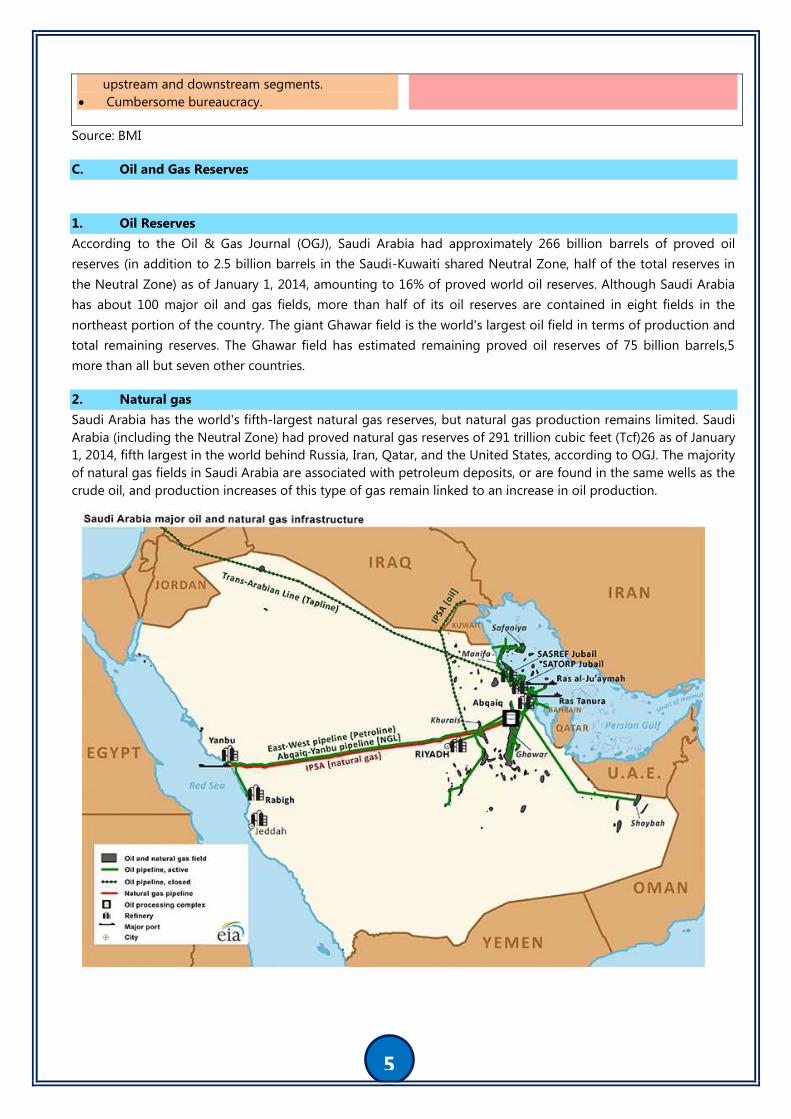

C. Oil and Gas Reserves

1. Oil Reserves

According to the Oil & Gas Journal (OGJ), Saudi Arabia had approximately 266 billion barrels of proved oil

reserves (in addition to 2.5 billion barrels in the Saudi-Kuwaiti shared Neutral Zone, half of the total reserves in

the Neutral Zone) as of January 1, 2014, amounting to 16% of proved world oil reserves. Although Saudi Arabia

has about 100 major oil and gas fields, more than half of its oil reserves are contained in eight fields in the

northeast portion of the country. The giant Ghawar field is the world's largest oil field in terms of production and

total remaining reserves. The Ghawar field has estimated remaining proved oil reserves of 75 billion barrels,5

more than all but seven other countries.

2. Natural gas

Saudi Arabia has the world's fifth-largest natural gas reserves, but natural gas production remains limited. Saudi

Arabia (including the Neutral Zone) had proved natural gas reserves of 291 trillion cubic feet (Tcf)26 as of January

1, 2014, fifth largest in the world behind Russia, Iran, Qatar, and the United States, according to OGJ. The majority

of natural gas fields in Saudi Arabia are associated with petroleum deposits, or are found in the same wells as the

crude oil, and production increases of this type of gas remain linked to an increase in oil production.

6

D. Oil and Gas Infrastructure

1. Major ports

Saudi Arabia has three primary oil export terminals:

The port of Ras Tanura on the Persian Gulf has an average handling capacity of 3.4 million bbl/d, and it

handles most of Saudi Arabia's exports.

The Ras al-Ju'aymah facility on the Persian Gulf has an average handling capacity of about 3 million bbl/d

and because of the availability of various Single Point Mooring buoys, the largest oil tankers can be

accommodated for crude loadings.

The Yanbu terminal on the Red Sea, from which most of the remaining volumes are exported, has an average

handling capacity of 1.3 million bbl/d. In addition to these primary export terminals, Saudi Arabia has other

smaller ports including Ras al-Khafji, Jubail, and Jeddah.

2. Major domestic petroleum pipelines

Saudi Aramco operates more than 12,000 miles of crude and petroleum product pipelines throughout the

country, including two major pipelines:

Saudi Arabia has the 746-mile-long East-West Pipeline, also known as Petroline, which runs across Saudi

Arabia from its Abqaiq complex to the Red Sea. The Petroline system consists of two pipelines with a total

nameplate capacity of about 4.8 million bbl/d. The 56-inch pipeline has a nameplate capacity of 3 million

bbl/d, and its current throughput is about 2 million bbl/d. In recent years, the 48-inch pipeline had been

operating as a natural gas pipeline, but Saudi Arabia moved to convert it back to an oil pipeline. The switch

could increase Saudi Arabia's spare oil pipeline capacity to bypass the Strait of Hormuz from 1 million bbl/d

to 2.8 million bbl/d, which is only attainable if the system is able to operate at its full nameplate capacity.

Running parallel to the Petroline is the 290,000-bbl/d Abqaiq-Yanbu NGL pipeline, which serves

petrochemical plants in Yanbu.

A 236-mile multi-products line between Dhahran in the Eastern Province and Riyadh and a smaller 220-mile

multi-products line between Riyadh and Qassim to the north were also built in the 1980s.

3. International petroleum pipelines

Saudi Aramco does not operate any major functioning international pipelines.

The Trans-Arabian Pipeline (Tapline), built in 1947 to transport crude oil from Qaisumah through Jordon to

Sidon, Lebanon, has been closed, in part, since 1984. The portion of the pipeline that runs to Jordan was

closed in 1990.

The Iraqi Pipeline in Saudi Arabia (IPSA) has a capacity of 1.65 million bbl/d and runs from Iraq, through

Saudi Arabia parallel to the East-West Pipeline, and ends at the port of Mu'ajjiz, south of Yanbu. The pipeline

was built in 1989 but was closed in 1990 during the Persian Gulf War. Saudi Arabia then seized IPSA in 2001.

The portion of the pipeline that runs parallel to the East-West Pipeline was converted to transport natural

gas to power plants, while the portion of the pipeline that goes north into Iraq remains a closed, inactive oil

pipeline.

Saudi Arabia's only functioning international crude pipeline system is a 60-year old complex of four small

underwater pipelines carrying Arabian Light crude from Saudi Arabia's Abu Safah field to Bahrain.20 This

aging pipeline system is expected to be decommissioned after the construction of a new pipeline with a

capacity of 350,000 running between Abqaiq and Bahrain's refinery at Sitra. The new pipeline is expected to

be completed in the third quarter of 2016.

7

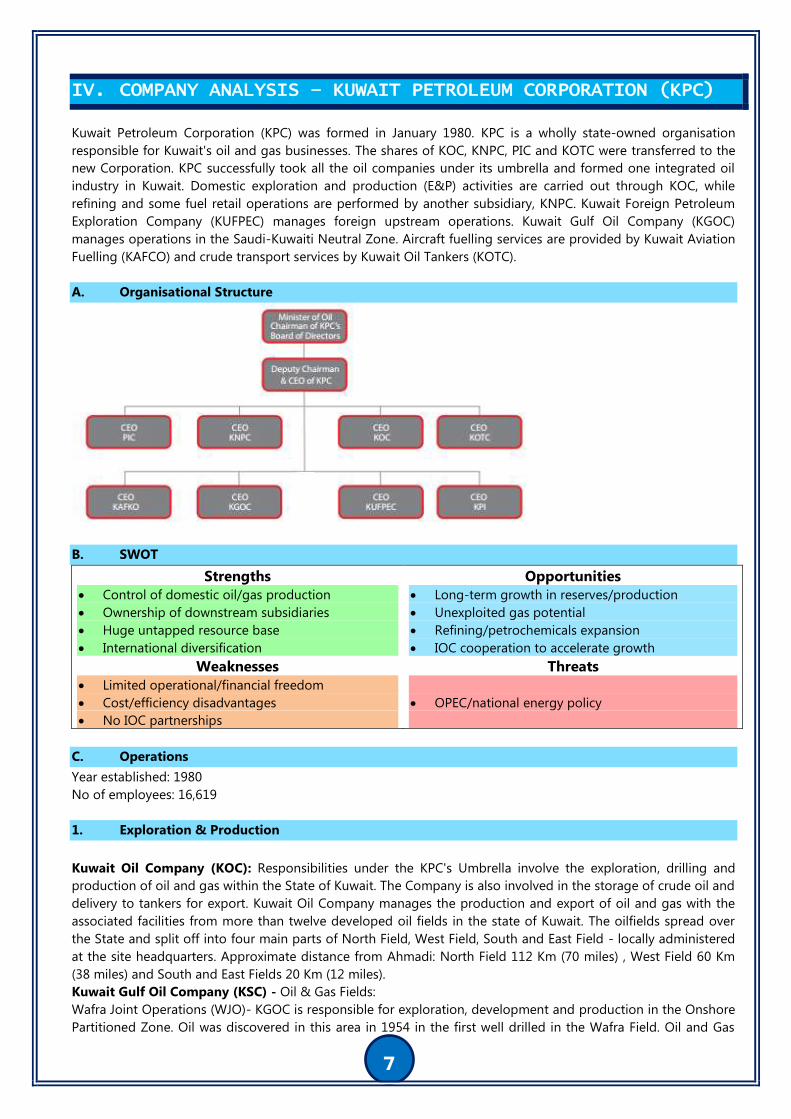

COMPANY ANALYSIS – KUWAIT PETROLEUM CORPORATION (KPC) IV.

Kuwait Petroleum Corporation (KPC) was formed in January 1980. KPC is a wholly state-owned organisation

responsible for Kuwait's oil and gas businesses. The shares of KOC, KNPC, PIC and KOTC were transferred to the

new Corporation. KPC successfully took all the oil companies under its umbrella and formed one integrated oil

industry in Kuwait. Domestic exploration and production (E&P) activities are carried out through KOC, while

refining and some fuel retail operations are performed by another subsidiary, KNPC. Kuwait Foreign Petroleum

Exploration Company (KUFPEC) manages foreign upstream operations. Kuwait Gulf Oil Company (KGOC)

manages operations in the Saudi-Kuwaiti Neutral Zone. Aircraft fuelling services are provided by Kuwait Aviation

Fuelling (KAFCO) and crude transport services by Kuwait Oil Tankers (KOTC).

A. Organisational Structure

B. SWOT

Strengths

Control of domestic oil/gas production

Ownership of downstream subsidiaries

Huge untapped resource base

International diversification

Opportunities

Long-term growth in reserves/production

Unexploited gas potential

Refining/petrochemicals expansion

IOC cooperation to accelerate growth

Weaknesses

Limited operational/financial freedom

Cost/efficiency disadvantages

No IOC partnerships

Threats

OPEC/national energy policy

C. Operations

Year established: 1980

No of employees: 16,619

1. Exploration & Production

Kuwait Oil Company (KOC): Responsibilities under the KPC's Umbrella involve the exploration, drilling and

production of oil and gas within the State of Kuwait. The Company is also involved in the storage of crude oil and

delivery to tankers for export. Kuwait Oil Company manages the production and export of oil and gas with the

associated facilities from more than twelve developed oil fields in the state of Kuwait. The oilfields spread over

the State and split off into four main parts of North Field, West Field, South and East Field - locally administered

at the site headquarters. Approximate distance from Ahmadi: North Field 112 Km (70 miles) , West Field 60 Km

(38 miles) and South and East Fields 20 Km (12 miles).

Kuwait Gulf Oil Company (KSC) - Oil & Gas Fields:

Wafra Joint Operations (WJO)- KGOC is responsible for exploration, development and production in the Onshore

Partitioned Zone. Oil was discovered in this area in 1954 in the first well drilled in the Wafra Field. Oil and Gas

8

Fields in this area include:South Umm Ghudair (SUG),Wafra,South Fuwaris (SF),Humma,ARQ. Two types of crude

oil are produced from PZ Fields: Ratawi Crude, which has 24 ̊ API Gravity, and Eocene Crude, 18 ̊ API Gravity.

Khafji Joint Operations (KJO)-KGOC is responsible for exploration and production in the Offshore Divided Zone,

in water depths of 100 to 150 feet, shared by Kuwait and the Kingdom of Saudi Arabia. The first discovery in this

area was made in 1960 with the drilling of Khafji Field Well #1.Oil and Gas Fields in this area

include:Khafji,Lulu,Hout,Dorra. Oil production from Khafji Field is comprised of two qualities; Hout Crude (Ratawi

Formation) of 32 API and Khafji Crude (Other Formations) of 28 API.Lulu Field has been delimited by four

wellbores and is under evaluation for further development. The Hout Field is presently shut-in. Evaluation for

pressure maintenance is underway. Field Development Plan (FDP) for Dorra Field has been prepared.

Kuwait Foreign Petroleum Exploration Company (KUFPEC) is currently active in 15 countries, in 3 core

regions spanning over 5 continents. Major areas are:

Europe, Middle East & Africa (EMEAR)

South East Asia (SEAR)

Far East & Australia (FEAR)

2. Refining & Industry

Kuwait National Petroleum Company (KNPC) was established in October 1960 as a shareholder company owned

by the government and the private sector. It operates following refineries:

Mina Abdullah Refinery - Crude processing capacity of 270 MBPD

Mina Al Ahmady Refinery - Crude processing capacity of 460 MBPD

Shuaiba Refinery - Crude processing capacity of 200 MBPD

3. Petrochemicals

Petrochemical Industries Company is a global manufacturer and marketer of petrochemicals and is the

petrochemical arm of Kuwait Petroleum Corporation (KPC). PIC owns two fertilizer plants for the production of

ammonia and urea. It also owns a 100,000 metric ton per annum propylene plant.

4. Transportation

Kuwait Oil Tanker Company (KOTC) as the transportation arm of KPC it operates, on a commercial basis, a

modern balanced fleet of Very Large Crude Carriers (VLCCs), petroleum product tankers and LPG carriers to

maintain a strategic coverage of KPC’s oil exports to all corners of the globe. KOTC Fleet capacity:

Very Large Crude Carriers (VLCC's): Total Capacity 4,184,408.20 m3

Product Carriers: Total Capacity 1,030,920.40 m3

Liquified Petroleum Gas (LPG) Carriers: Total Capacity 314,850.00 m3

Bunker Vessels: Total Capacity 9,488.00 m3

D. Strategy

Domestic Upstream

Achieve sustainable crude oil production capacities in the State of Kuwait 4.0 MM bpd by 2020 and maintain

through 2030

Achieve sustainable non-associated gas production capacities in the State of Kuwait 2.5 Bcf/d by 2030

Compensate for produced Hydrocarbons by annually adding proven reserve through improvement of

hydrocarbons recovery from existing reservoirs and pursue an aggressive onshore and offshore exploration

program to compensate for the 3-years average hydrocarbons production in order to meet the needs of

future production targets (100% Reserve Replacement Ratio).

Domestic Downstream

Grow KPC domestic refining capacity up to 1.4 MM bpd in the medium term

Maximize conversion complexity of KPC domestic refineries, while meeting local energy demand

9

Provide petroleum products that meet domestic energy requirements and international market needs in

terms of quantity and quality

International Upstream

Achieve crude oil and gas production outside Kuwait of 200 MBOEPD by 2020 and maintain through 2030

and reserves of 650 MMBOE by 2020 and maintain through 2030

Give preference for investments which facilitate technology and capability transfer between domestic and

international upstream businesses

Become operator of international upstream assets by reaching 20% operatorship by 2030

International Downstream

Grow KPC international refining capacity while ensuring secure outlet for 800 mbpd by 2020 of Kuwaiti

hydrocarbon

Enter into economically viable investment opportunities through partnership with an international partner or

alliance with oil company, focusing on high growth market, specifically Asia

Divest unprofitable investments that do not provide acceptable returns in the short term in Europe and

merge current operations with competitors operations through JV(s)/partnership(s) to improve performance

Petrochemicals

Pursue growth in petrochemical core business inside and outside the State of Kuwait by new builds or

acquisitions to maintain leading position in the high growth Olefins and Aromatics products through

partnerships, with a focus on Asia and other emerging markets

Maximize value-added integration between petrochemicals and KPC’s operations inside and outside the

State of Kuwait

Transportation

Maintain the size and the configuration of the fleet that meet long-term strategic cover and KPC marketing

requirements for crude oil, petroleum products and LPG in-line with targeted domestic production

Midstream

Maximize the value of Kuwaiti hydrocarbons in secure, long-term, and diverse outlets

Improve the value chain optimization of KPC’s operations

E. Market Position

International downstream assets now comprise around 250,000b/d of refining capacity in Europe, which includes

the 75,500b/d Europort facility in Rotterdam and half of the capacity of Eni's 300,000b/d Milazzo refinery. KPC

also operates a network of around 5,000 service stations in Italy, Germany, the UK, Sweden, Denmark, the

Netherlands, Belgium, Luxembourg and Thailand under the Q8 brand. Q8-branded lubricants are marketed

directly in the Benelux countries, Denmark, France, Germany, Italy, Spain and the UK, and exported to more than

75 countries. Airport refuelling operations are offered throughout Western Europe and in Hong Kong. Assets in

Indonesia and Pakistan contribute the bulk of output. E&P assets are located in Algeria, Egypt, Sudan, Tunisia,

Qatar, Yemen, Australia, Indonesia, Malaysia, China, Vietnam and Pakistan. KUFPEC in December 2012 agreed to

acquire an additional 34.3% interest in the Yacheng gas field in the South China Sea from BP. The Yacheng 13-1

field was discovered in 1983 and is the largest offshore natural gas producing field in China. KUFPEC has been a

participant in Yacheng 13-1 since 1990. Following completion, the Yacheng partnership will consist of KUFPEC

(49%) and CNOOC (51%).

10

LNG INDUSTRY REVIEW 2016 V.

In 2016, global LNG trade recorded a growth rate of around 7.5% compared to 2015, returning to a robust pace

experienced before 2011. Primarily driven by new Australian volumes, additional supply was not as abundant as

expected due to production delays, slower ramp-ups and lower exports from historical suppliers. Sluggish oil

prices have continued to exert downward pressure on LNG contract prices. In the Pacific Basin, a combination of

more than adequate supply and of slow demand growth also pushed spot prices to a seven-year low. This

situation and the looming supply overhang are causing a slow-down in investment with several FIDs being

cancelled or deferred.

In order to respond to market changes and cope with the uncertainty of future supply and demand, LNG

contracting strategies have grown in importance. In this respect, most buyers pay particular attention to flexibility

–in terms of destination as well as off-take obligations– and price competitiveness. In a well supplied market and

given the significant quantities under long-term contracts which are due to expire in the medium-term –

particularly in Japan– the share of spot and short-term volumes (which remained stable at around 28% of total

trade) could increase further in the coming years.

A. Key Facts 2016

263.6 million tons imported or a 7.5% increase vs. 2015

74.6 million tons traded on a spot or short term basis or 28% of total trade

73% of global LNG demand in Asia

30% of global LNG volumes supplied from Qatar

45% of global LNG volumes supplied from the Pacific Basin

4 New Importing Countries 11 New LNG Regasification Terminals

39 Importing Countries

830 MTPA Total Regasification Capacity

19 Exporting Countries

340 MTPA Total Nameplate Liquefaction Capacity

B. China, India and Emerging Importers Driving Demand Growth

After a moderate growth performance in 2015, Chinese demand soared in 2016 due to an increase in gas-fired

power generation and in demand from the industrial sector. As a result, China experienced a strong rally in LNG

imports in 2016, with an impressive 36.9% growth. Thanks in part to low spot prices and to a price sensitive LNG

demand, Indian imports also jumped (+30%), reaching 19MT and confirming the country’s rank of 4th largest

LNG buyer worldwide. Emerging importers recorded strong gains in 2016. For their second year as LNG

importers, Egypt, Pakistan and Jordan imported a combined 13.5MT in 2016 vs 5.5MT in 2015. Growth was led by

Egypt, who experienced a steep increase in 2016 with 7.5MT imported (almost tripling from its 2015 level) mainly

via spot and short-term imports.

In contrast,

demand in

mature

importing

markets such as

Japan, South

Korea and

Europe

remained

sluggish. In

Japan, LNG

imports

11

declined for the second year in a row to 83.3 MT (-1.7 MT) due to the restart of several nuclear units, to energy

conservation efforts and to the uptake in renewable power generation. Against expectations, Europe did not

function as a sink for the production increase in 2016. The UK recorded the largest decline in imports year-on-

year (-2.6MT or -26%), due to higher supply of pipeline gas and domestic production. Belgium and the

Netherlands also recorded declines of respectively –58% and – 42%. France showed an opposite trend (+1.2MT

or +28%, net of re-exports).

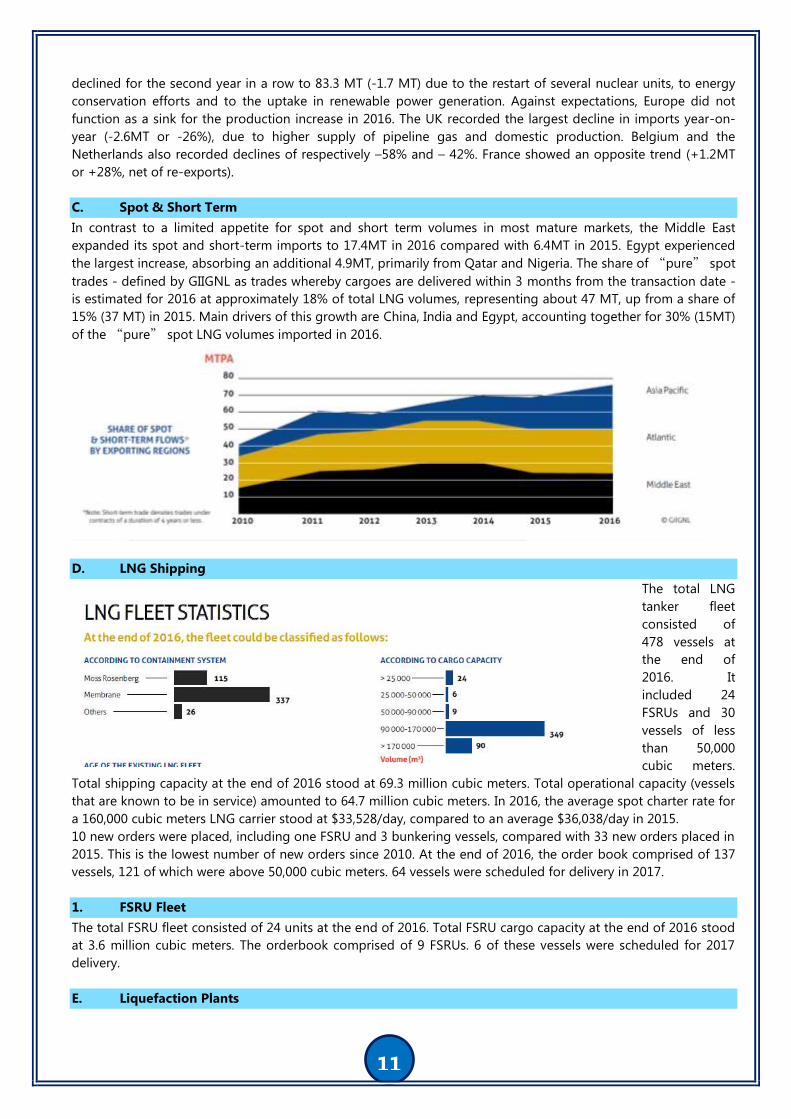

C. Spot & Short Term

In contrast to a limited appetite for spot and short term volumes in most mature markets, the Middle East

expanded its spot and short-term imports to 17.4MT in 2016 compared with 6.4MT in 2015. Egypt experienced

the largest increase, absorbing an additional 4.9MT, primarily from Qatar and Nigeria. The share of “pure” spot

trades - defined by GIIGNL as trades whereby cargoes are delivered within 3 months from the transaction date -

is estimated for 2016 at approximately 18% of total LNG volumes, representing about 47 MT, up from a share of

15% (37 MT) in 2015. Main drivers of this growth are China, India and Egypt, accounting together for 30% (15MT)

of the “pure” spot LNG volumes imported in 2016.

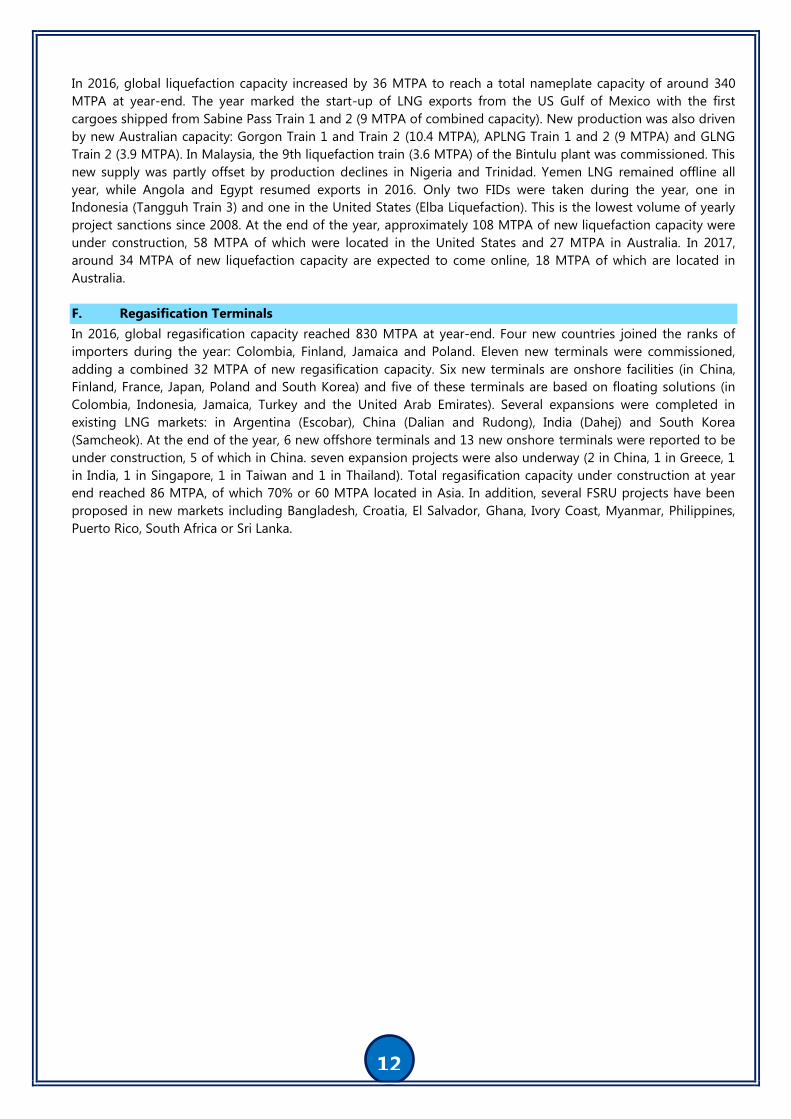

D. LNG Shipping

The total LNG

tanker fleet

consisted of

478 vessels at

the end of

2016. It

included 24

FSRUs and 30

vessels of less

than 50,000

cubic meters.

Total shipping capacity at the end of 2016 stood at 69.3 million cubic meters. Total operational capacity (vessels

that are known to be in service) amounted to 64.7 million cubic meters. In 2016, the average spot charter rate for

a 160,000 cubic meters LNG carrier stood at $33,528/day, compared to an average $36,038/day in 2015.

10 new orders were placed, including one FSRU and 3 bunkering vessels, compared with 33 new orders placed in

2015. This is the lowest number of new orders since 2010. At the end of 2016, the order book comprised of 137

vessels, 121 of which were above 50,000 cubic meters. 64 vessels were scheduled for delivery in 2017.

1. FSRU Fleet

The total FSRU fleet consisted of 24 units at the end of 2016. Total FSRU cargo capacity at the end of 2016 stood

at 3.6 million cubic meters. The orderbook comprised of 9 FSRUs. 6 of these vessels were scheduled for 2017

delivery.

E. Liquefaction Plants

12

In 2016, global liquefaction capacity increased by 36 MTPA to reach a total nameplate capacity of around 340

MTPA at year-end. The year marked the start-up of LNG exports from the US Gulf of Mexico with the first

cargoes shipped from Sabine Pass Train 1 and 2 (9 MTPA of combined capacity). New production was also driven

by new Australian capacity: Gorgon Train 1 and Train 2 (10.4 MTPA), APLNG Train 1 and 2 (9 MTPA) and GLNG

Train 2 (3.9 MTPA). In Malaysia, the 9th liquefaction train (3.6 MTPA) of the Bintulu plant was commissioned. This

new supply was partly offset by production declines in Nigeria and Trinidad. Yemen LNG remained offline all

year, while Angola and Egypt resumed exports in 2016. Only two FIDs were taken during the year, one in

Indonesia (Tangguh Train 3) and one in the United States (Elba Liquefaction). This is the lowest volume of yearly

project sanctions since 2008. At the end of the year, approximately 108 MTPA of new liquefaction capacity were

under construction, 58 MTPA of which were located in the United States and 27 MTPA in Australia. In 2017,

around 34 MTPA of new liquefaction capacity are expected to come online, 18 MTPA of which are located in

Australia.

F. Regasification Terminals

In 2016, global regasification capacity reached 830 MTPA at year-end. Four new countries joined the ranks of

importers during the year: Colombia, Finland, Jamaica and Poland. Eleven new terminals were commissioned,

adding a combined 32 MTPA of new regasification capacity. Six new terminals are onshore facilities (in China,

Finland, France, Japan, Poland and South Korea) and five of these terminals are based on floating solutions (in

Colombia, Indonesia, Jamaica, Turkey and the United Arab Emirates). Several expansions were completed in

existing LNG markets: in Argentina (Escobar), China (Dalian and Rudong), India (Dahej) and South Korea

(Samcheok). At the end of the year, 6 new offshore terminals and 13 new onshore terminals were reported to be

under construction, 5 of which in China. seven expansion projects were also underway (2 in China, 1 in Greece, 1

in India, 1 in Singapore, 1 in Taiwan and 1 in Thailand). Total regasification capacity under construction at year

end reached 86 MTPA, of which 70% or 60 MTPA located in Asia. In addition, several FSRU projects have been

proposed in new markets including Bangladesh, Croatia, El Salvador, Ghana, Ivory Coast, Myanmar, Philippines,

Puerto Rico, South Africa or Sri Lanka.

13

LNG TRADE OUTLOOK IN AUSTRALIA, US & MEXICO VI.

A. Australian LNG Export

Despite temporary outages at the first two trains, Train 3 of Australia’s Gorgon LNG project progressed well,

enabling an early start date. Chevron has announced that Train 3 will begin operations before the end of March.

Although this will not add absolute volumes to the market above those already anticipated, it will bring ramp-up

cargoes to the spot market earlier than previously expected. With the early commissioning cargoes set to be

available during a period of weak demand, there could be further pressure on spot prices in the short term.

Gorgon’s third train will bring Australia’s export capacity up to around 66 mtpa when it is fully operational.

Gorgon will have an overall capacity of 15.6 mtpa when all three trains are fully ramped up.

Spot LNG prices in Asia have come under sustained pressure in recent weeks, with the spot price for March and

April deliveries down to around $6.5-7.0/MMBtu – a significant drop from the highs of $9.5/MMBtu seen during

the peak of winter.

Although China saw a significant jump in spot LNG imports in December and is expected to remain active on the

spot market over the coming months, requirements for spot cargoes will likely remain weak elsewhere in

Northeast Asia before the peak summer demand period.

Train 1 at Chevron’s Wheatstone LNG project is scheduled to start operations by the middle of this year and

looks likely to be commissioned before the end of Q3, 2017. This would add another 4.5 mpta of capacity to

Australia’s LNG exports.

Ichthys LNG and Prelude FLNG are also scheduled to start up within the next 12 months, but delays to the

commissioning schedules are a risk.

1. Australia LNG Export Projects – Existing and Planned

Project Capacity, mtpa Status

North West Shelf 16.3 Operational

Darwin 3.7 Operational

Pluto 4.9 Operational

Queensland Curtis 8.5 Operational

Australia Pacific 9 Operational

Gladstone 7.8 Operational

Gorgon Trains 1 & 2 10.4 Operational

Gorgon Train 3 5.2 Operational by March 2017

Wheatstone 8.9 Planned 2017/2018

Prelude FLNG 3.6 Planned 2017/2018

Ichthys 8.9 Planned 2017/2018

Total 87.2 –

Source: GIIGNL, IGU, GGA

B. MEXICO: US LNG DESTINATION

The MANZANILLO terminal on Mexico’s Pacific Coast has become an eager customer for LNG from the Sabine

Pass plant in the United States. Moreover, trade relations are expected to deepen over the coming months as the

14

US continues to provide cheap and abundant LNG to the terminal. Manzanillo is importing more and more

cargoes, even though the prospects for LNG in Mexico as a whole are bleak.

The startup of the third train at Sabine Pass has seen a sharp rise in the volume of US LNG arriving at Manzanillo,

and this trend is expected to continue for the rest of 2017. Train 3 exported its first commissioning cargo in

January and is expected to reach substantial completion by the end of March.

South Korea’s Kogas has a 20-year sales-and-purchase agreement to take 3.5 mtpa of LNG from Train 3. The

company also has a stake in Manzanillo, enabling it to supply the fuel to Mexico from Sabine Pass. In addition,

Manzanillo received LNG from Sabine Pass last year via Shell’s portfolio position at trains 1 and 2.

Australia is increasing its dominance over the Asian LNG market, making it increasingly difficult for South Korea

to import US volumes despite the long term Kogas contract with Sabine Pass. Consequently, Kogas is

increasingly acting as a portfolio player and is looking to market volumes sourced from the US in regions other

than Asia. Manzanillo’s healthy demand for LNG gives Kogas a golden opportunity to market US LNG there,

helped by its stake at the terminal.

Manzanillo imported 10 LNG cargoes between January and February this year, all of which were sourced from

Sabine Pass. Two more shipments, also from Sabine Pass, have arrived at the terminal so far in March.

Kogas has supplied most of Manzanillo’s LNG so far this year via its portfolio position at Sabine Pass’s third train.

In contrast, Manzanillo received no LNG from the US between January and February 2016 but instead took in

cargoes from Peru, Trinidad & Tobago and Australia. However, non-US suppliers have lost their advantage now

Train 3 is online.

Manzanillo imported 500,000 tons of LNG in the first two months of 2017, much more than the 370,000 tons it

imported during the same period in 2016.

1. Mexico’s declining LNG demand

Mexico’s overall LNG imports are under pressure, despite the healthy demand at Manzanillo, because of the

increasing popularity of pipeline gas from the US. Consequently, the country’s other two LNG terminals –

Altamira and Costa Azul – have been severely underutilized so far in 2017 and are expected to remain so for the

rest of the year.

Altamira has received no LNG since September 2016, whereas Costa Azul imported a single cargo from Indonesia

in February 2017 – its first import since June 2016. Mexico’s LNG imports declined by 16.8% on an annual basis in

2016, to 4.11 mt.

The low cost of US pipeline gas is reinforcing its popularity in Mexico. US pipeline gas exports to Mexico cost

$2.64/MMBtu on average in 2016 while the average landed price for LNG in Mexico was $5.73/MMBtu.

Consequently, Mexico imported 38.41 billion cubic metres of pipeline gas from the US in 2016, an increase of

almost 29% on an annual basis.

Manzanillo’s thirst for LNG is not guaranteed in the medium to- long term as the popularity of US pipeline gas

grows. Mexico’s pipeline infrastructure is not sufficiently developed to carry gas from the US to southwest

Mexico, which will continue to depend on supplies from Manzanillo for the time being. However, Mexico is

improving its infrastructure, and this will weigh on the terminal’s imports in the longer term.

Note:

The data and information in the report is sourced from websites and documents available in public

domain and doesn’t purport to be official view of government or any organization. Sincere efforts have

been made to present correct data; however, errors and omissions, if any, are regretted and the same may

please be brought to the notice of Energy Desk for necessary corrective action.

![FOCUSED ENERGY REPORT - gailcorintra.gail.co.in...Monthly Report-December Energy Desk . December 1, 2012 [FOCUSED ENERGY REPORT] E N E R G Y D e s k Page 1 Table of Content ... A recent](https://img.pdfslide.net/doc/110x75/5ea9763e9d133867c471f81b/focused-energy-report-monthly-report-december-energy-desk-december-1-2012.jpg)

![High Intensity Focused Ultrasound Facial Skin Lifting · HIFU Mechanism HIFU [High Intensity Focused Ultra-sound] • Non-invasive treatment with thermal energy that focused ultrasound](https://img.pdfslide.net/doc/110x75/5fd8347ce1f6a6277a18bb54/high-intensity-focused-ultrasound-facial-skin-hifu-mechanism-hifu-high-intensity.jpg)

![FOCUSED ENERGY REPORT - gailcorintra.gail.co.in · November 9, 2012 [FOCUSED ENERGY REPORT] ... WTI crude oil 92.29 85.26 -7.03 -7.61% ... Hassi Messaoud basin, located in the eastern](https://img.pdfslide.net/doc/110x75/5f5be53420dbde111b489dc3/focused-energy-report-november-9-2012-focused-energy-report-wti-crude-oil.jpg)