Embed Size (px)

Citation preview

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Section 962 Election of The Corporate Tax Rate by Individuals For

Global Intangible Low-Taxed Income ( GILTI) And Subpart F

Income Inclusions

TUESDAY, JULY 10, 2018, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

TUESDAY, JULY 10, 2018

Section 962 Election of The Corporate Tax Rate by Individuals For Global Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions

Thomas M. Giordano-Lascari, Atty

Karlin & Peebles, Los Angeles

William K. Norman, J.D., LL.M. (Taxation), Partner

Ord & Norman, Los Angeles

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Section 962 Election of The Corporate Tax Rate by Individuals For Global

Intangible Low-Taxed Income ( GILTI) And Subpart F Income Inclusions

Thomas M. Giordano-LascariKarlin & Peebles, LLP5900 Wilshire Boulevard, Suite 500Los Angeles, CA 90036Telephone: (323) 648-4649Facsimile: (310) [email protected]

William K. NormanOrd & Norman11377 West Olympic Boulevard, 5th Fl.Los Angeles, CA 90064Telephone: (310) 473-8067Facsimile: (310) [email protected]

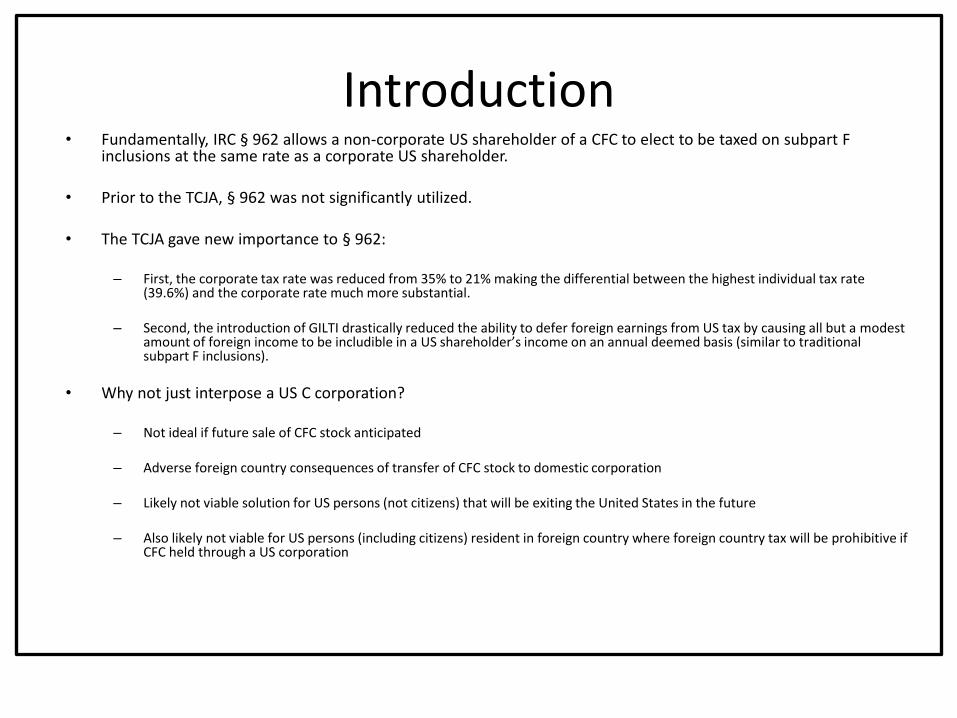

Introduction• Fundamentally, IRC § 962 allows a non-corporate US shareholder of a CFC to elect to be taxed on subpart F

inclusions at the same rate as a corporate US shareholder.

• Prior to the TCJA, § 962 was not significantly utilized.

• The TCJA gave new importance to § 962:

– First, the corporate tax rate was reduced from 35% to 21% making the differential between the highest individual tax rate (39.6%) and the corporate rate much more substantial.

– Second, the introduction of GILTI drastically reduced the ability to defer foreign earnings from US tax by causing all but a modest amount of foreign income to be includible in a US shareholder’s income on an annual deemed basis (similar to traditional subpart F inclusions).

• Why not just interpose a US C corporation?

– Not ideal if future sale of CFC stock anticipated

– Adverse foreign country consequences of transfer of CFC stock to domestic corporation

– Likely not viable solution for US persons (not citizens) that will be exiting the United States in the future

– Also likely not viable for US persons (including citizens) resident in foreign country where foreign country tax will be prohibitive if CFC held through a US corporation

Global Intangible Low Taxed Income (GILTI)§ 951A

Effective for TYs of foreign corps. beginning after 12/31/17 and the TYs of U.S. Shareholders in which or with which the TY of the foreign corp. ends. P.L. 115-97, § 14201(a)

7

GILTI (Cont)

“U.S. Shareholder” of any CFC includes in its gross income the shareholder’s “Global Intangible Low Taxed Income” (GILTI).

§ 951A(a)

8

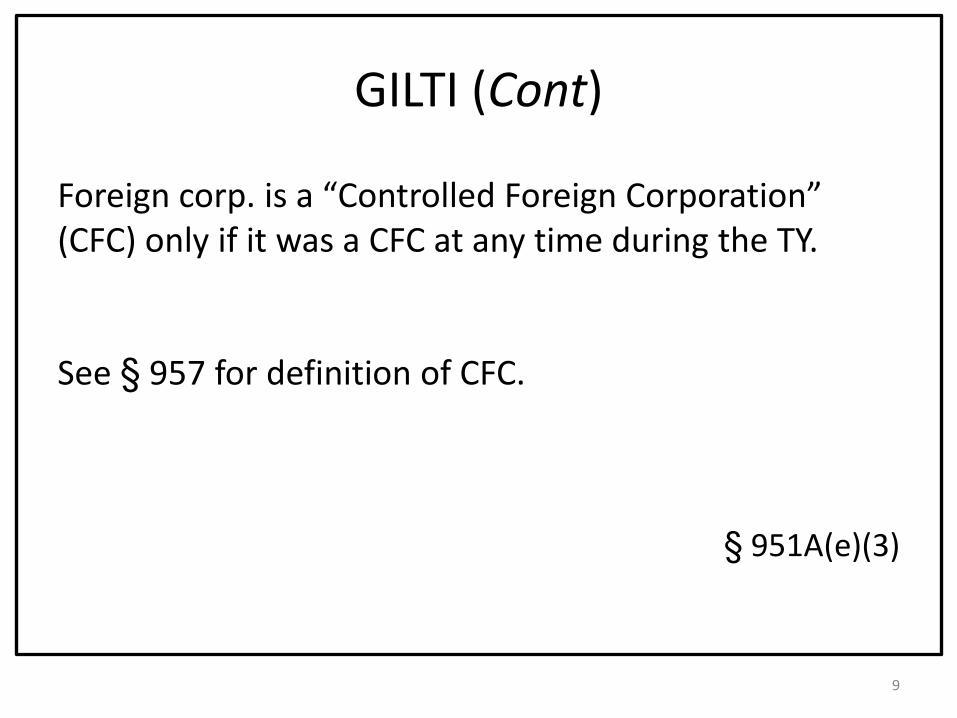

GILTI (Cont)

Foreign corp. is a “Controlled Foreign Corporation” (CFC) only if it was a CFC at any time during the TY.

See § 957 for definition of CFC.

§ 951A(e)(3)

9

GILTI (Cont)

A U.S. Person is a “U.S. Shareholder” if the person owns (w/in meaning of § 958(a) i.e., directly or indirectly through foreign entities) stock in the foreign corp. on the last day in the taxable year of the foreign corp. on which it is a CFC.

See § 951(b) for definition of U.S. Shareholder.

§ 951A(e)(2)

10

GILTI (Cont)

GILTI = “Net CFC - “NetFor Any Tested Income” DeemedU.S. Shareholder of the U.S. TangibleFor Any TY Shareholder Incomeof the Shareholder Return”

(NDTIR”) ofthe U.S.Shareholder

>0

§ 951A(b)(1)

11

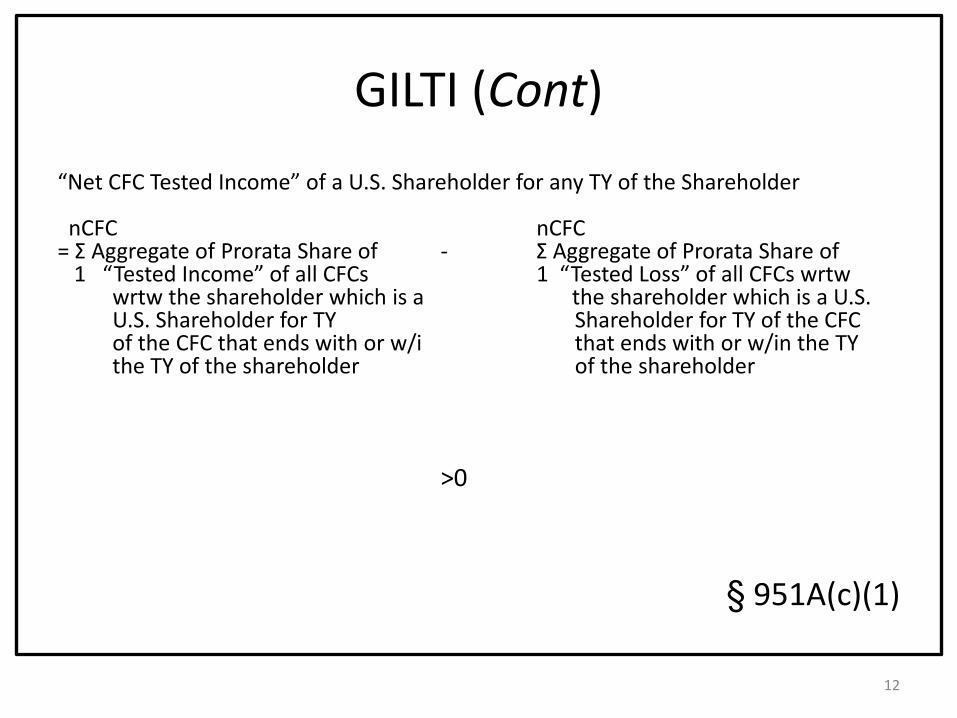

GILTI (Cont)

“Net CFC Tested Income” of a U.S. Shareholder for any TY of the Shareholder

nCFC nCFC= Ʃ Aggregate of Prorata Share of - Ʃ Aggregate of Prorata Share of

1 “Tested Income” of all CFCs 1 “Tested Loss” of all CFCs wrtwwrtw the shareholder which is a the shareholder which is a U.S.U.S. Shareholder for TY Shareholder for TY of the CFC of the CFC that ends with or w/i that ends with or w/in the TY the TY of the shareholder of the shareholder

>0

§ 951A(c)(1)

12

GILTI (Cont)

“Tested Loss” of a CFCfor any TY of the CFC = Deductions Gross Income of the

including taxes CFC computed w/oallocated to GI - regard to excludedof the CFC under items in rules similar to § 951A(c)(2)(i)§ 954(b)(5) w/o (I) through (V)excluded itemsin § 951A(c)(2)(i)(I) through (V)

< 0

§ 951A(c)(2)(B)(i)

13

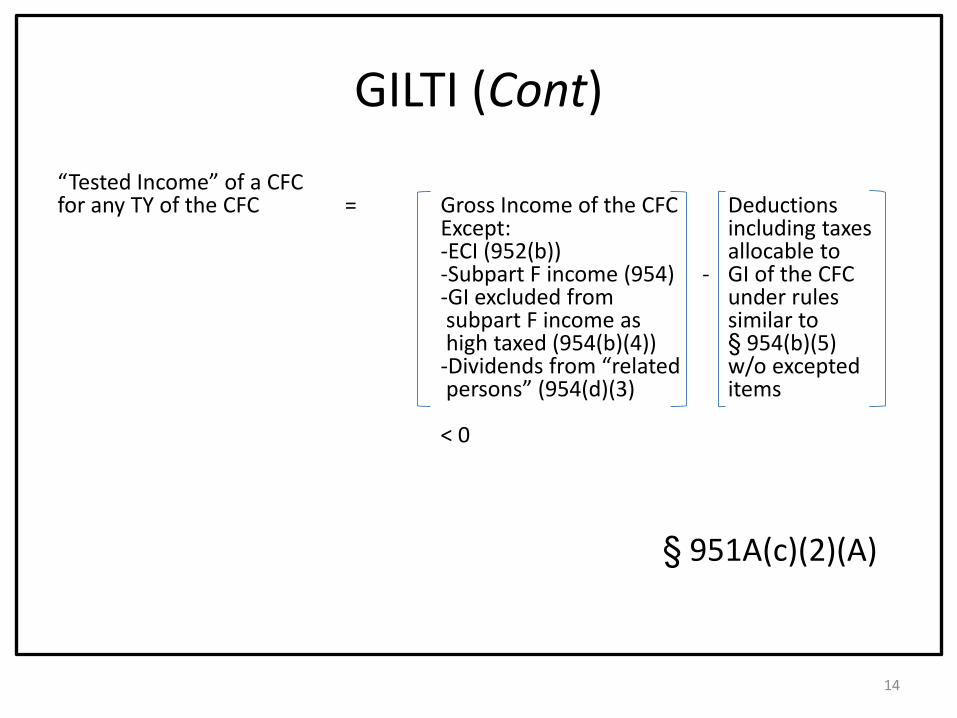

GILTI (Cont)

“Tested Income” of a CFCfor any TY of the CFC = Gross Income of the CFC Deductions

Except: including taxes-ECI (952(b)) allocable to-Subpart F income (954) - GI of the CFC -GI excluded from under rulessubpart F income as similar tohigh taxed (954(b)(4)) § 954(b)(5)

-Dividends from “related w/o exceptedpersons” (954(d)(3) items

< 0

§ 951A(c)(2)(A)

14

GILTI (Cont)

NDTIR of n

U.S. Shareholder = .10 Ʃ QBAI Interest expense allocable toFor Any TY 1 of all - “Net CFC Tested Income” to

CFCs extent interest income attributable wrtw to the expense is not taken intoSH is account in determining Net CFCa U.S. SH Tested Income of the shareholderused toproduceTested Income

>0

§ 951A(b)(2)

15

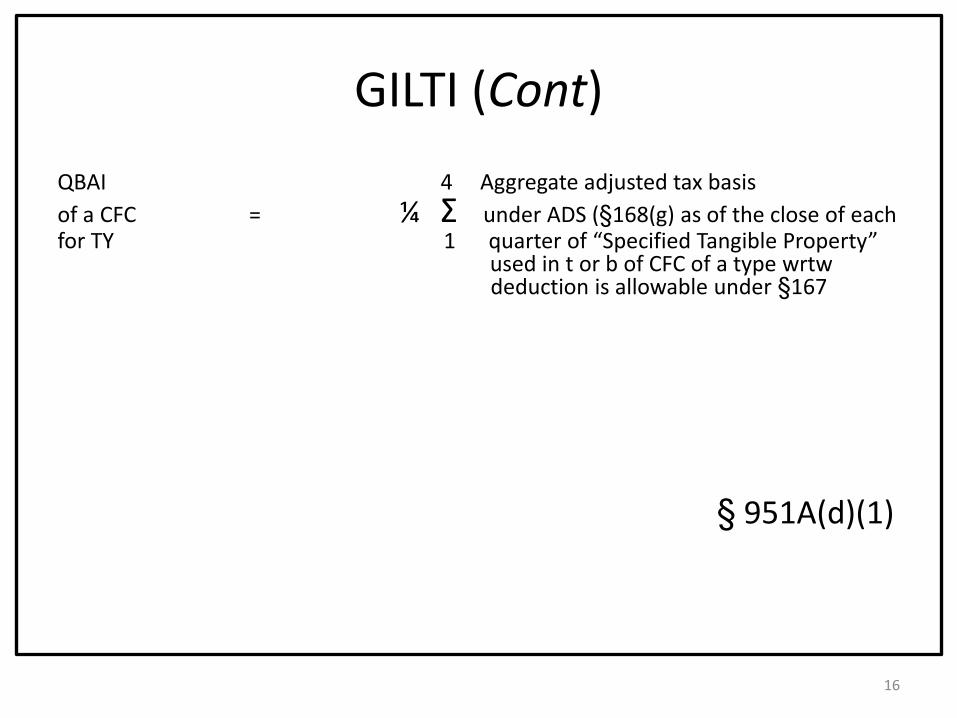

GILTI (Cont)

QBAI 4 Aggregate adjusted tax basis

of a CFC = ¼ Ʃ under ADS (§168(g) as of the close of each for TY 1 quarter of “Specified Tangible Property”

used in t or b of CFC of a type wrtwdeduction is allowable under §167

§ 951A(d)(1)

16

GILTI (Cont)

Specified tangible property (STP) of a CFC is (except for “dual use property”) any tangible property used in the production of “tested income”

§ 951A(d)(1)

17

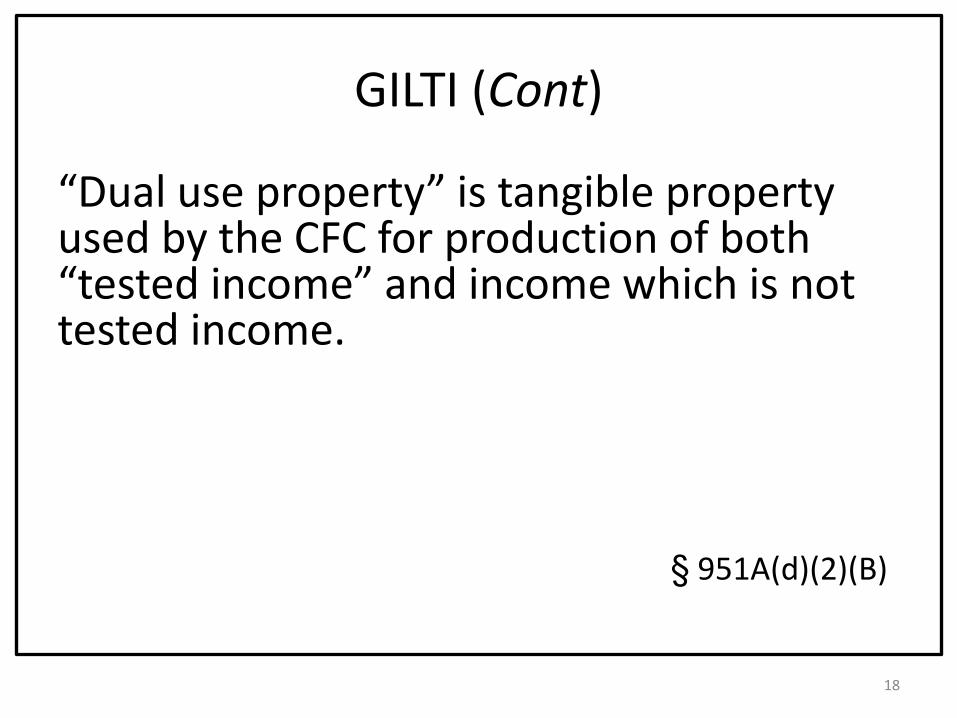

GILTI (Cont)

“Dual use property” is tangible property used by the CFC for production of both “tested income” and income which is not tested income.

§ 951A(d)(2)(B)

18

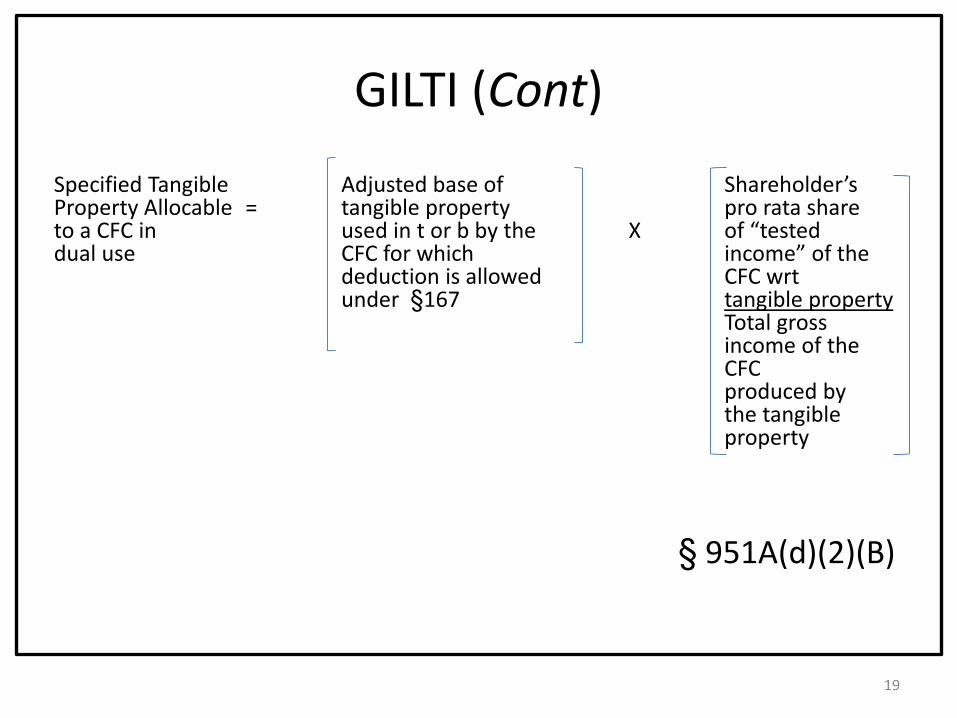

GILTI (Cont)

Specified Tangible Adjusted base of Shareholder’sProperty Allocable = tangible property pro rata shareto a CFC in used in t or b by the X of “tested dual use CFC for which income” of the

deduction is allowed CFC wrtunder §167 tangible property

Total gross income of the CFCproduced bythe tangibleproperty

§ 951A(d)(2)(B)

19

GILTI (Cont)

Allocation of CFC’s distributive AdjustedAdjusted basis = share of income basis ofof STP of a of the partnership as X items of partnership to a percentage wrt STP heldCFC partner the STP by partnership

of which theCFC is a partner

§ 951A(d)(3)

20

GILTI (Cont)

Deemed Paid GILTI * AggregateCredit for = .80 Aggregate Tested ForeignGILTI Inclusion Tested X Income Taxof a U.S. Shareholder Income of CFCs

of CFCs

*Fraction is called “inclusion percentage”.

§ 960(d)(2)

21

GILTI (Cont)

See 78 = GILTI * X AggregateGross Up Aggregate Tested ForeignRelated Tested Income Income Taxto GILTI of CFCs of CFCsInclusionof a U.S.Shareholder

*Fraction is called “inclusion percentage”. § 960(d)(2)

§ 78 and § 960(d)

22

GILTI (Cont)

“Tested Foreign Income Taxes” of a domestic (C) corporation which is a U.S. Shareholder of one or more CFCs is the sum of:

Foreign income taxes paid or accrued by each CFC with “tested income” that are “properly attributable” to the “tested income” of the CFC included in GILTI.

§ 960(d)(3)

23

GILTI (Cont)

GILTI (except for passive category income) is assigned to a separate basket for FTC limitation purposes.

§ 904(d)(1)(A)

24

GILTI (Cont)

Foreign TaxCredit = .50 (GILTI + Gross Up) X U.S. FederalLimitation Entire Taxable Income Income Taxfor the GILTI - .50(GILTI + Gross Up) Before FTCBasket(Category)Other than Passive

§§ 904(a), (d)(1)(A) and

861(b)

25

GILTI (Cont)

GILTI allocated GILTI from U.S. S/H’sto a U.S. = all CFCs pro rata share ofShareholder wrtw the X “tested income”of a CFC for shareholder is of the CFC purposes of a U.S. Shareholder Ʃ aggregate of§951A(f)( 1) “tested income”

of all CFCswrtw theshareholder is a U.S.Shareholder

§ 951A(f)(2)

26

GILTI (Cont)

GILTI Is Generally Treated In the Same Manner as Subpart F Income for Purposes of:

951(a)(1)(A) – Subpart F inclusion 996(f)(1) – E and P of IC DISC168(h)(2)(B) – not tax exempt prop. 1248(b)(1) – limitation on dividend treatment535(b)(10) - deduction for AET 1248(d)(1) – exclusion for E & P904(h)(1) - resourcing 6501(e)(1)(C) – 6 year S of L952(c)(1)(A) – E & P limitation 6654(d)(2)(D) – estimated tax 959 – PTI stock and ordering 6655(e)(4) – estimated tax961 – adjustments to basis962 – election of corporate rates993(a)(1)(E) – dividends and inclusions

wrt foreign export corporations

§ 951A(f)(1)

27

IRC § 962• A US shareholder of a CFC who is an individual

(including a trust or estate (see treas. reg. §1.962-2(a)) can make a 962 election, which provides:– Tax imposed on subpart F inclusions of said individual,

including GILTI inclusions (see § 951A(f)(1)), will be subject to tax as calculated under section 11 (i.e., taxes imposed on corporations).

– A deemed paid credit under IRC § 960 shall be allowed on such amounts.

– Basis step-up under § 961 allowable to the extent of tax paid

29

IRC § 962 – Legislative History (S. Rep. No. 1881, 87th Cong., 2d Sess. (1962))

• “The purpose of this provision is to avoid what might otherwise be a hardship in taxing a U.S. individual at high bracket rates with respect to earnings in a foreign corporation which he does not receive. This provision gives such individuals assurance that their tax burdens, with respect to these undistributed foreign earnings, will be no heavier than they would have been had they invested in an American corporation doing business abroad.”

30

IRC § 962 – Application

• Application of section 11 for inclusions subject to a 962 election (treas. reg. § 1.962-1(b)(1)):– Section 11 is limited under 962 and the above cited regulation.

Specifically, for 962 purposes, “taxable income” means the sum of:• The amounts required to be included in gross income as traditional

subpart F income and GILTI; plus• The section 78 “gross-up” with respect to those amounts.

– “such sum shall not be reduced by any deduction of the United States shareholder even if such shareholder’s deductions exceed his gross income”

• “Taxable Income” under Section 11 refers to section 63, which provides taxable income means gross income minus allowable deductions

31

IRC § 962 – Foreign Tax Credit (Treas. Reg. § 1.962-1(b)(2)

• Allowance of foreign tax credit:

– There shall be allowed a foreign tax credit under §960(a)(1) for amounts which are the subject of a §962 election (subject to the applicable limitation of § 904)

• To the extent the foreign tax credit exceeds the § 904 limitation, the excess can be carried back or carried forward, except can only offset other income for which a 962 election is in place

32

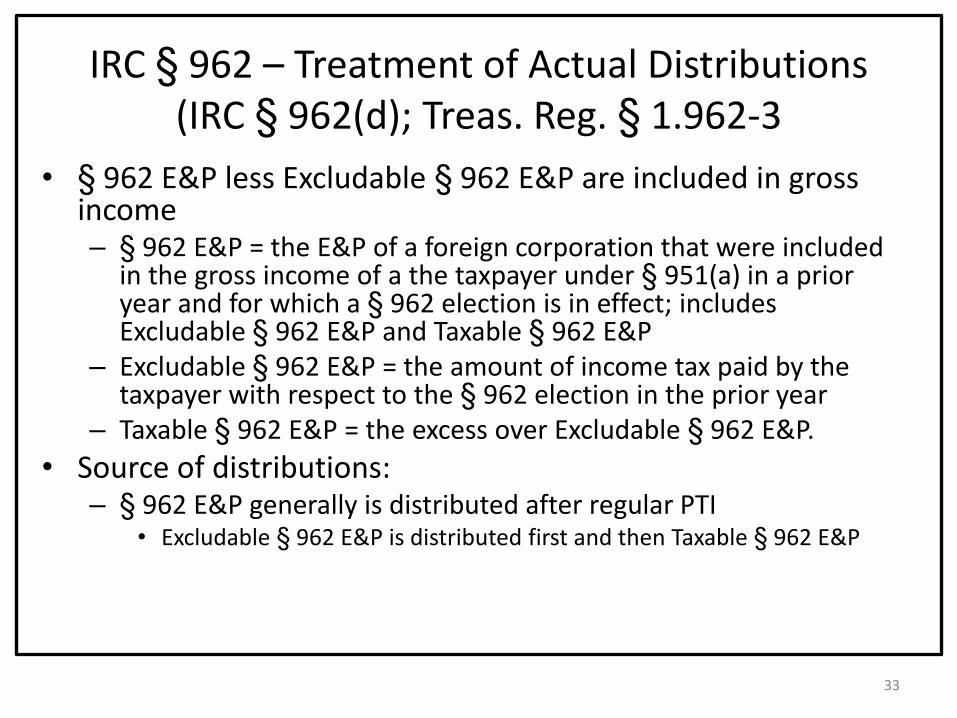

IRC § 962 – Treatment of Actual Distributions (IRC § 962(d); Treas. Reg. § 1.962-3

• § 962 E&P less Excludable § 962 E&P are included in gross income– § 962 E&P = the E&P of a foreign corporation that were included

in the gross income of a the taxpayer under § 951(a) in a prior year and for which a § 962 election is in effect; includes Excludable § 962 E&P and Taxable § 962 E&P

– Excludable § 962 E&P = the amount of income tax paid by the taxpayer with respect to the § 962 election in the prior year

– Taxable § 962 E&P = the excess over Excludable § 962 E&P.

• Source of distributions:– § 962 E&P generally is distributed after regular PTI

• Excludable § 962 E&P is distributed first and then Taxable § 962 E&P

33

IRC § 962 – Procedure (Treas. Reg. §1.962-2)

• Only individuals, trusts or estates may make the election.• Election made by filing a statement with taxpayer’s return:

– Name, address, and taxable year of each CFC with respect to which the electing shareholder is a US shareholder and all other corporations, partnerships, trusts, or estates in any applicable chain of ownership described in § 958(a)

– The amounts, on a corporation-by-corporation basis, which are included in such shareholder’s gross income for his taxable year under § 951(a)

– Taxpayer’s pro rata share of E&P of such CFC with respect to which the taxpayer as an inclusion under § 951(a) and the foreign taxes with respect to such E&P

– The amount of distributions received by the taxpayer from each CFC which are (1) excludable § 962 E&P; (2) taxable § 962 E&P; and (3) E&P other than § 962 E&P, showing the source of such amounts by taxable year

• Effect of election– A § 962 election when made is applicable to all CFCs owned by the taxpayer and is binding for

the taxable year for which the election is made– An election may be revoked with the approval of the Commissioner. Approval will not be

granted unless a material and substantial change in circumstances occurs which could not have been anticipated.

34

IRC § 962 – Areas of Uncertainty

• Can individuals who own CFC through an S corporation or partnership make a § 962 election?

• Availability of § 250 Deduction for GILTI Inclusions

• Are subsequent distributions qualified dividends if distributed from a foreign corporation not located in a treaty jurisdiction?

35

36

Comparative Examples

- GILTI -

Prepared By:

William K. Norman

Ord & NormanLos Angeles

Tel: 310-473-8067

Email: [email protected]

37

GILTI Comparative Examples:

US Co

USICase 1

Facts:

For Co

Domestic net income θ

Tested income 1,150

Foreign income taxes θ

Adjusted basis of QGAI 1,500

38

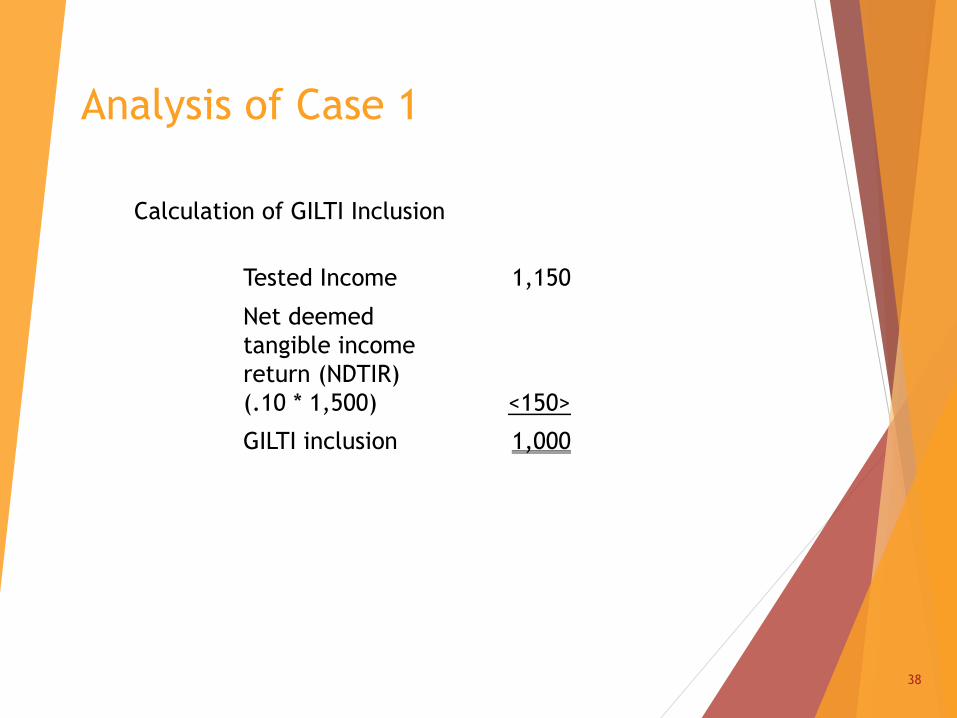

Analysis of Case 1

Calculation of GILTI Inclusion

Tested Income 1,150

Net deemed

tangible income

return (NDTIR)

(.10 * 1,500) <150>

GILTI inclusion 1,000

39

Analysis of Case 1 (cont.)

Calculation of Tax Liability of USCO:

GILTI inclusion 1000

Dividend of NDTIR 150

1,150

GILTI deduction <500>

650

Taxable income corp tax rate .21

136.5

40

Analysis of Case 1 (cont.)

Calculation of Tax Liability of Ultimate Shareholder:

E & P of USCO:

Distribution of GILTI 1000

Dividend of NDTIR 150

1,150

Less Corp. tax <136.5>

E & P available for dividend

to Ultimate Shareholder

1,013.5

Combined ordinary

and unearned rate .238

Ultimate Shareholder tax 241.2

Corp. level tax 136.5

Total tax burden 377.7

Effective tax rate

377.7/1,150

32.8%

41

GILTI Comparative Examples:

USICase 1A

Facts:

For

Co

Domestic net income θ

Tested income 1,150

Foreign income taxes θ

Adjusted basis of QGAI 1,500

42

Analysis of Case 1A (cont.)

Calculation of Tax Liability of Ultimate Shareholder:

GILTI inclusion 1000

Dividend from For Co 150

Taxable income 1,150

Combined ordinary

and unearned rate .408

Ultimate shareholder tax

to Ultimate Shareholder

469.2

Effective tax rate

469.2/1,150

40.8%

44

GILTI Comparative Examples:

USICase 1B – Section 962(b) election

Facts:

Domestic net income θ

Tested income 1,150

Foreign income taxes θ

Adjusted basis of QGAI 1,500

§ 962(a)

fictional

domestic

corporation

For Co

45

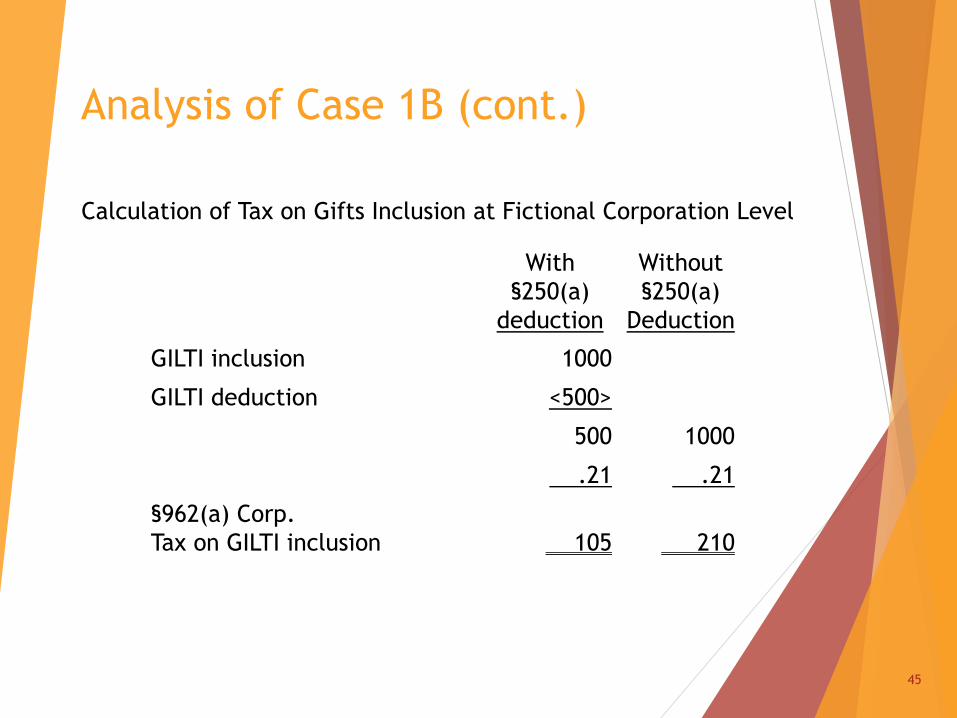

Analysis of Case 1B (cont.)

Calculation of Tax on Gifts Inclusion at Fictional Corporation Level

With

§250(a)

deduction

Without

§250(a)

Deduction

GILTI inclusion 1000

GILTI deduction <500>

500 1000

.21 .21

§962(a) Corp.

Tax on GILTI inclusion 105 210

46

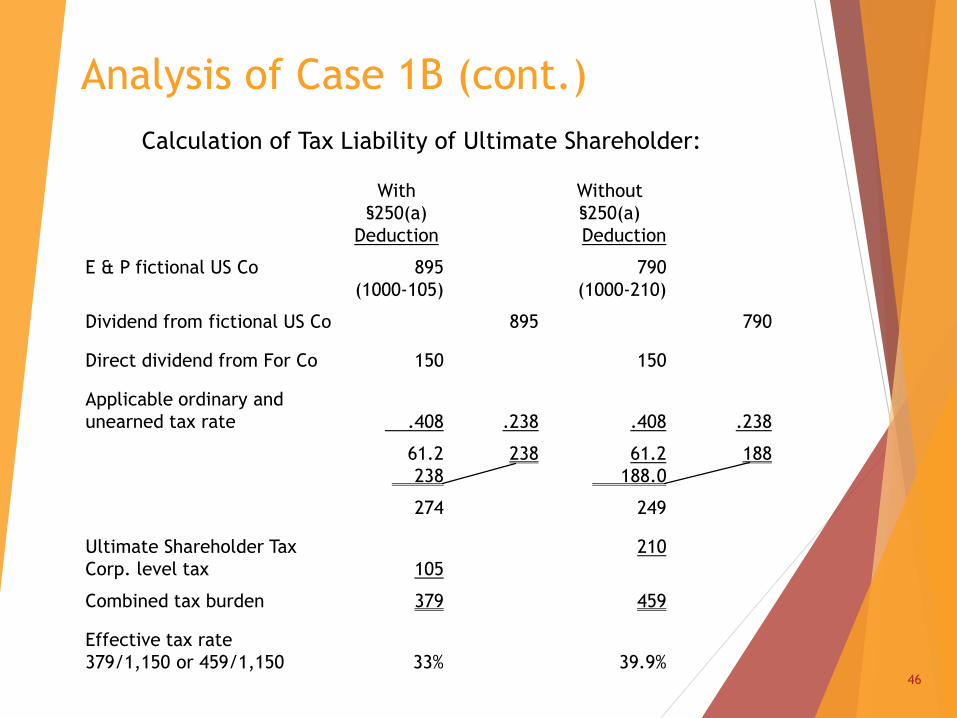

Analysis of Case 1B (cont.)

Calculation of Tax Liability of Ultimate Shareholder:

With

§250(a)

Deduction

Without

§250(a)

Deduction

E & P fictional US Co 895

(1000-105)

790

(1000-210)

Dividend from fictional US Co 895 790

Direct dividend from For Co 150 150

Applicable ordinary and

unearned tax rate .408 .238 .408 .238

61.2

238

238 61.2

188.0

188

274 249

Ultimate Shareholder Tax

Corp. level tax 105

210

Combined tax burden 379 459

Effective tax rate

379/1,150 or 459/1,150 33% 39.9%

47

GILTI Comparative Examples:

US

Co

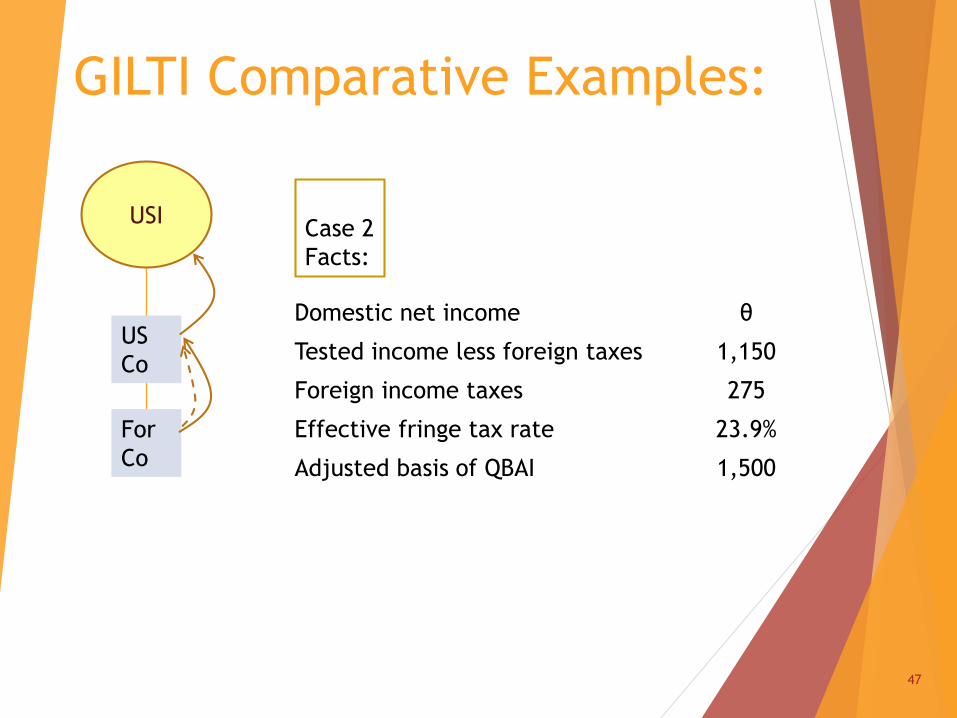

USICase 2

Facts:

For

Co

Domestic net income θ

Tested income less foreign taxes 1,150

Foreign income taxes 275

Effective fringe tax rate 23.9%

Adjusted basis of QBAI 1,500

48

Analysis of Case 2

Calculation of GILTI Inclusion for US Co:

Tested income

before foreign taxes

1,500

Foreign income taxes <275>

NDTIR

(.10 * 1,500)

<150>

GILTI inclusion 725

Calculation of Foreign Tax Credit Amounts:

DPTTC =725

1,150 - 275.80 275 = 182

Gross Up = 275 = 227.9725

1,150 - 275

.875

.875

49

Analysis of Case 2 (cont.)Calculation of Tax Liability of US Co:

GILTI inclusion 725

Gross Up 227.9

952.9

GILTI deduction

<476.45

>

476.45

.21

Corp. tax before FTC 100.1

FTC as limited <100.1>

Corp. Tax 0

Receipt of distribution of NDTIR net of allocated foreign income

taxes is eligible for participation exemption. §245A

50

Analysis of Case 2 (cont.)

Calculation of Tax Liability of Ultimate Shareholder:

Available E & P for distribution:

Tested income before foreign tax 1,150

Foreign income taxes <275>

Dividend to Ultimate Shareholder 875

.238

Ultimate Shareholder tax 208.25

Foreign income taxes 275.00

Total tax burden 483.25

Effective tax rate

483.25/1,150 42%

51

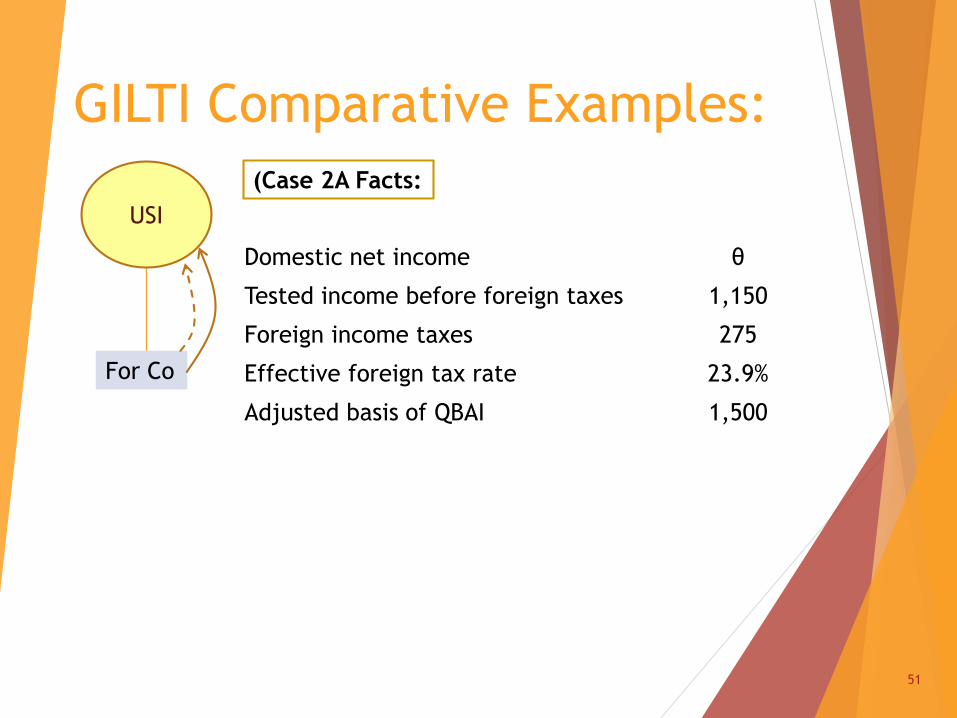

GILTI Comparative Examples:

USI

(Case 2A Facts:

For Co

Domestic net income θ

Tested income before foreign taxes 1,150

Foreign income taxes 275

Effective foreign tax rate 23.9%

Adjusted basis of QBAI 1,500

52

Analysis of Case 2ACalculation of GILTI Inclusion for USI:

Total income before foreign taxes 1,150

Foreign income taxes <275>

N D T I R

(-.10* 1,500)

<150>

GILTI Inclusion 725

53

Analysis of Case 2A (cont.)

Calculation of Tax Liabilities of Shareholder:

GILTI inclusions 725

Dividend of NDTIR 150+(150/1150) 275

35.9

185.9

910.9

Combined ordinary and unearned rate .408

Ultimate shareholder tax 371.6

Foreign tax 275.0

Total tax burden 646.6

Effective tax rate

646.6/1,150

56.2%

54

GILTI Comparative Examples:

USICase 2B Facts:

Domestic net income θ

Tested income before foreign taxes 1,150

Foreign income taxes 275

Effective foreign tax rate 23.9%

Adjusted basis of QBAI 1,500

§ 962(a)

fictional

domestic

corporation

For Co

55

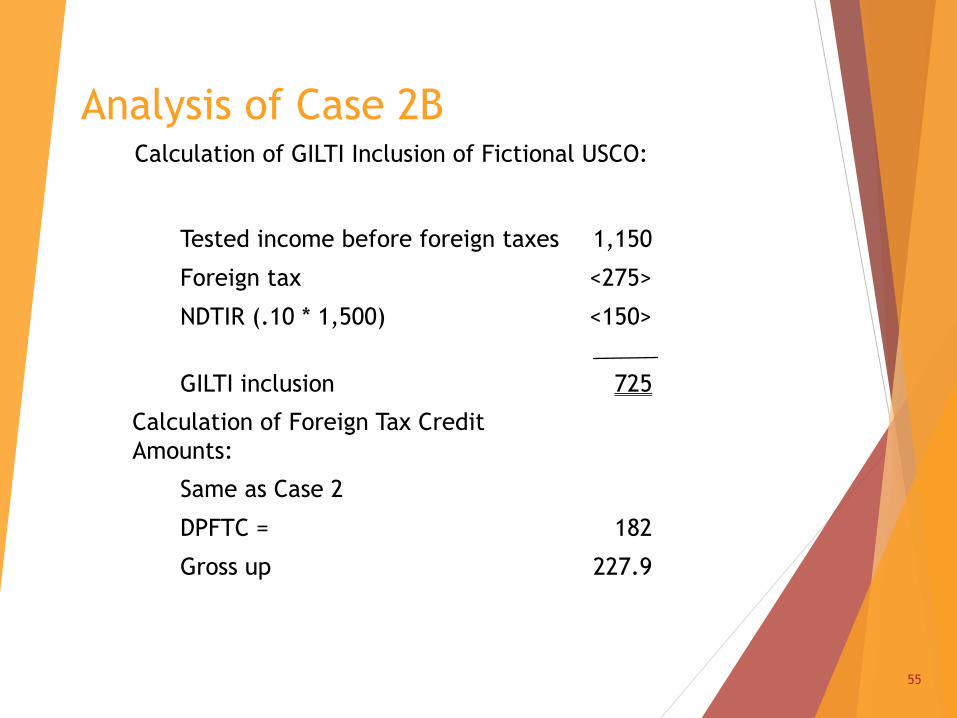

Analysis of Case 2BCalculation of GILTI Inclusion of Fictional USCO:

Tested income before foreign taxes 1,150

Foreign tax <275>

NDTIR (.10 * 1,500) <150>

GILTI inclusion 725

Calculation of Foreign Tax Credit

Amounts:

Same as Case 2

DPFTC = 182

Gross up 227.9

56

Analysis of Case 2B (cont.)Calculation of Tax Liability of Shareholders:

E&P and Tax Pool Allocations --

E&P of ForCo

PTI Other Total

725* 150 875

Allocation of tax pool

725/875 X 275 228 47 275

*Gross up is excluded from E&P. Regs §1.78-1(a)

57

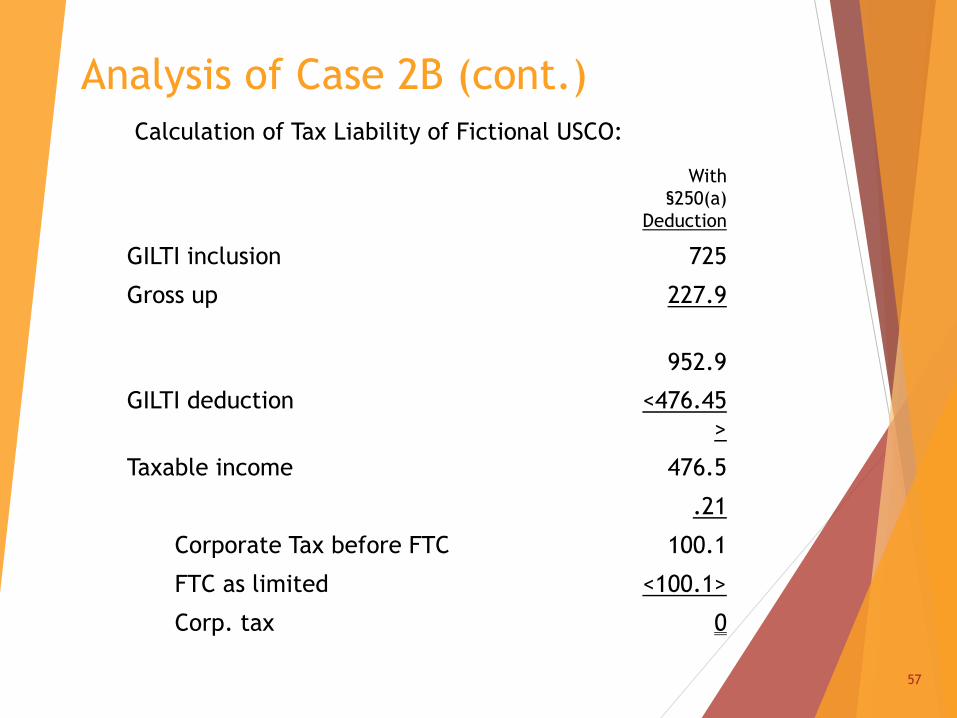

Analysis of Case 2B (cont.)

Calculation of Tax Liability of Fictional USCO:

With

§250(a)

Deduction

GILTI inclusion 725

Gross up 227.9

952.9

GILTI deduction <476.45

>

Taxable income 476.5

.21

Corporate Tax before FTC 100.1

FTC as limited <100.1>

Corp. tax 0

58

Analysis of Case 2B (cont.)

Calculation of Tax Liability of Shareholder (cont.):

Dividend from GILTI

(inclusion of fictional USCO) 725

Dividend from ForCo 150

Tax rate on distribution from

fictional USCO .238

Tax rate on actual distribution

for ForCo

.408

Partial Tax 172.6

61.2

61.2

Shareholder Tax Total 233.8

Foreign Tax 275

Total of U.S. and foreign

taxes

508.8

Effective tax rate

508.8 / 1,150

44.2%

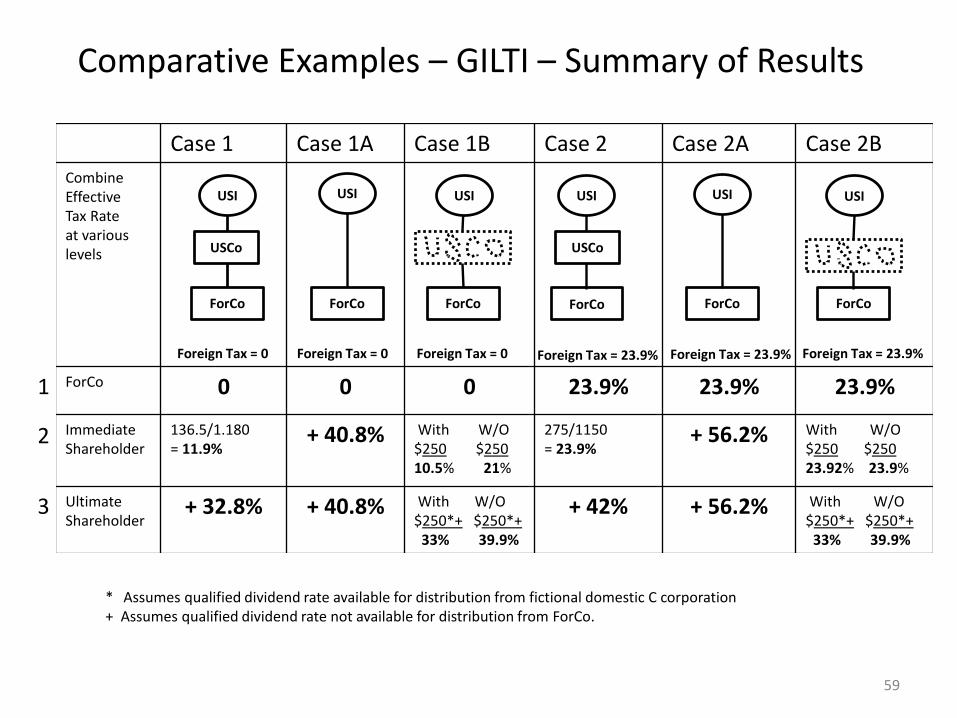

Comparative Examples – GILTI – Summary of Results

Case 1 Case 1A Case 1B Case 2 Case 2A Case 2B

Combine Effective Tax Rate at various levels

ForCo 0 0 0 23.9% 23.9% 23.9%

Immediate Shareholder

136.5/1.180= 11.9%

+ 40.8% With W/O$250 $25010.5% 21%

275/1150 = 23.9%

+ 56.2% With W/O$250 $25023.92% 23.9%

Ultimate Shareholder

+ 32.8% + 40.8% With W/O$250*+ $250*+

33% 39.9%

+ 42% + 56.2% With W/O$250*+ $250*+

33% 39.9%

1

3

2

* Assumes qualified dividend rate available for distribution from fictional domestic C corporation+ Assumes qualified dividend rate not available for distribution from ForCo.

USI USI USI USI USI USI

ForCo

USCo

ForCo ForCo ForCo ForCo ForCo

USCo

Foreign Tax = 0 Foreign Tax = 23.9%Foreign Tax = 23.9%Foreign Tax = 23.9%Foreign Tax = 0Foreign Tax = 0

59

Comparative Examples – GILTIComments on Summary of Results

Case 1 Case 1A Case 1B Case 2 Case 2A Case 2B

ForCo 0 0 0 23.9% 23.9% 23.9%1

Row 1 ▪ This row merely states the foreign tax rate for each case.

Because of a U.S. Shareholder in every case, the combined U.S. foreign tax rate with or without a distribution is reflected in Row 2.

60

Comparative Examples – GILTIComments on Summary of Results

Case 1 Case 1A Case 1B Case 2 Case 2A Case 2B

Immediate Shareholder

136.5/1.180= 11.9%

+ 40.8% With W/O$250 $25010.5% 21%

275/1150 = 23.9%

+ 56.2% With W/O$250 $25023.92% 23.9%

2

Row 2 ▪ The results under Cases 1 and 1B, assuming the § 250 deduction is allowed, are

essentially the same. The reason the effective tax rate in Case 1 is higher than Case 1B (11.9% v. 10.5%) is that in Case 1 we assume the earnings attributed to NDTIR are distributed. If the § 250 deduction is not allowed in Case 1B, the tax burden in Case 1B is almost double the result in Case 1.

▪ The results in Cases 2 and 2B at the domestic corporation level reflect only the foreign tax burden of 23% which completely offsets the domestic corporate tax.

▪ The results in Cases 1A and 2A reflect the disadvantage of an individual U.S. shareholder under the GILTI regime.

61

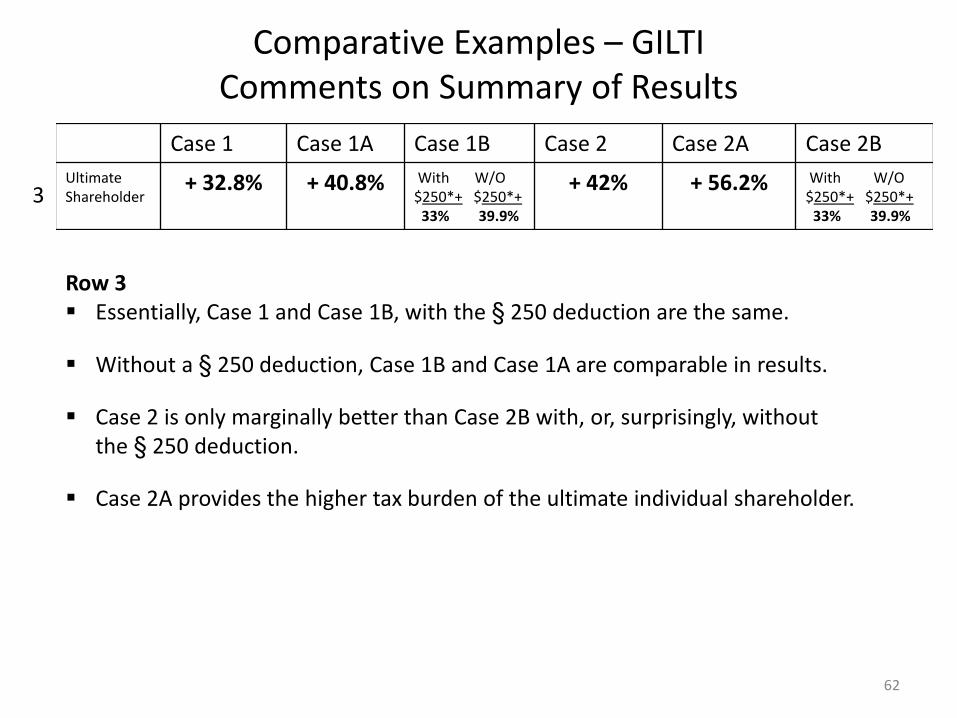

Comparative Examples – GILTIComments on Summary of Results

Case 1 Case 1A Case 1B Case 2 Case 2A Case 2B

Ultimate Shareholder

+ 32.8% + 40.8% With W/O$250*+ $250*+

33% 39.9%

+ 42% + 56.2% With W/O$250*+ $250*+

33% 39.9%3

Row 3 ▪ Essentially, Case 1 and Case 1B, with the § 250 deduction are the same.

▪ Without a § 250 deduction, Case 1B and Case 1A are comparable in results.

▪ Case 2 is only marginally better than Case 2B with, or, surprisingly, without the § 250 deduction.

▪ Case 2A provides the higher tax burden of the ultimate individual shareholder.

62