Embed Size (px)

Citation preview

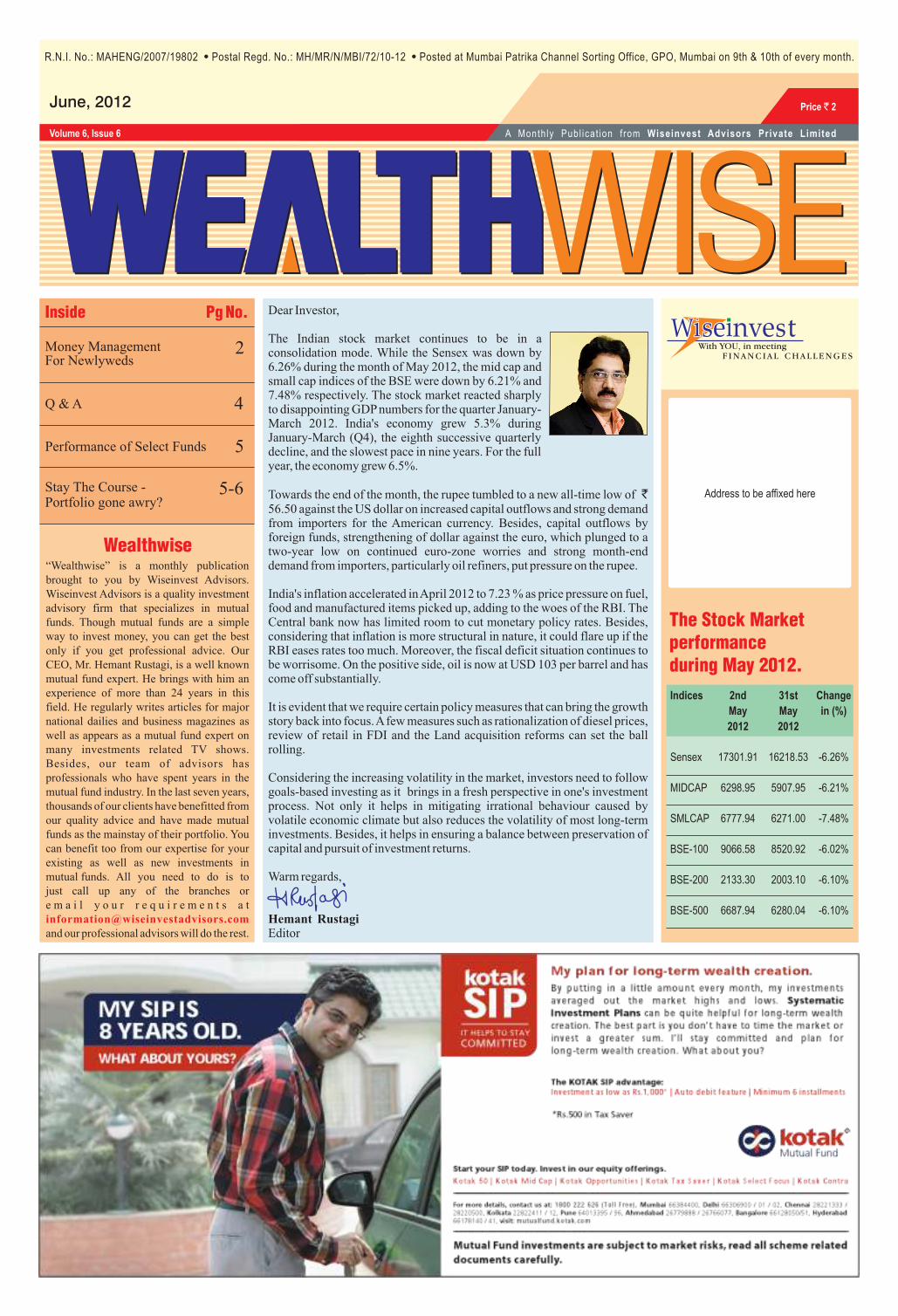

Indices 2nd 31st Change

May May in (%)

2012 2012

Sensex 17301.91 16218.53 -6.26%

MIDCAP 6298.95 5907.95 -6.21%

SMLCAP 6777.94 6271.00 -7.48%

BSE-100 9066.58 8520.92 -6.02%

BSE-200 2133.30 2003.10 -6.10%

BSE-500 6687.94 6280.04 -6.10%

The Stock Marketperformanceduring May 2012.

Address to be affixed here

R.N.I. No.: MAHENG/2007/19802 • Postal Regd. No.: MH/MR/N/MBI/72/10-12 • Posted at Mumbai Patrika Channel Sorting Office, GPO, Mumbai on 9th & 10th of every month.

Volume 6, Issue 6

June, 2012

A Month ly Publ icat ion f rom Wiseinvest Advisors Private Limited

Price ` 2

“Wealthwise” is a monthly publication brought to you by Wiseinvest Advisors. Wiseinvest Advisors is a quality investment advisory firm that specializes in mutual funds. Though mutual funds are a simple way to invest money, you can get the best only if you get professional advice. Our CEO, Mr. Hemant Rustagi, is a well known mutual fund expert. He brings with him an experience of more than 24 years in this field. He regularly writes articles for major national dailies and business magazines as well as appears as a mutual fund expert on many investments related TV shows. Besides, our team of advisors has professionals who have spent years in the mutual fund industry. In the last seven years, thousands of our clients have benefitted from our quality advice and have made mutual funds as the mainstay of their portfolio. You can benefit too from our expertise for your existing as well as new investments in mutual funds. All you need to do is to just call up any of the branches or e m a i l y o u r r e q u i r e m e n t s a t

and our professional advisors will do the [email protected]

Dear Investor,

The Indian stock market continues to be in a consolidation mode. While the Sensex was down by 6.26% during the month of May 2012, the mid cap and small cap indices of the BSE were down by 6.21% and 7.48% respectively. The stock market reacted sharply to disappointing GDP numbers for the quarter January- March 2012. India's economy grew 5.3% during January-March (Q4), the eighth successive quarterly decline, and the slowest pace in nine years. For the full year, the economy grew 6.5%.

Towards the end of the month, the rupee tumbled to a new all-time low of ̀ 56.50 against the US dollar on increased capital outflows and strong demand from importers for the American currency. Besides, capital outflows by foreign funds, strengthening of dollar against the euro, which plunged to a two-year low on continued euro-zone worries and strong month-end demand from importers, particularly oil refiners, put pressure on the rupee.

India's inflation accelerated in April 2012 to 7.23 % as price pressure on fuel, food and manufactured items picked up, adding to the woes of the RBI. The Central bank now has limited room to cut monetary policy rates. Besides, considering that inflation is more structural in nature, it could flare up if the RBI eases rates too much. Moreover, the fiscal deficit situation continues to be worrisome. On the positive side, oil is now at USD 103 per barrel and has come off substantially.

It is evident that we require certain policy measures that can bring the growth story back into focus. A few measures such as rationalization of diesel prices, review of retail in FDI and the Land acquisition reforms can set the ball rolling.

Considering the increasing volatility in the market, investors need to follow goals-based investing as it brings in a fresh perspective in one's investment process. Not only it helps in mitigating irrational behaviour caused by volatile economic climate but also reduces the volatility of most long-term investments. Besides, it helps in ensuring a balance between preservation of capital and pursuit of investment returns.

Warm regards,

Hemant RustagiEditor

Inside Pg No.

Wealthwise

2Money ManagementFor Newlyweds

4Q & A

5Performance of Select Funds

5-6Stay The Course -Portfolio gone awry?

June 2012 | Page No. 2

Money Management For Newlyweds

Marriage marks the start of a partnership in all aspects of life, not least of all,

the couple's financial decisions. Managing finances together could be a

daunting task for those who have just taken the plunge, and taking a few steps

together in this direction could help the partners ease into a comfortable

financial zone.

It can be quite a challenge for newly married couples to manage their limited

resources with their seemingly unlimited needs. Many young couples get

overwhelmed by the thought of saving a large amount of money that they will

require to lead a peaceful and happy life. Hence, it is very important to

develop good saving and spending habits, as well to as learn to budget. Here

are a few tips in this regard:

Have an open conversation

An open conversation is the key for a newly married couple to understand

each other's financial standing, i.e. income, expenses, investments, loans and

any other assets. By discussing these, the couple can hope to find their risk-

taking capacity and ascertain how to achieve the perfect synergies required to

achieve various financial goals.

Discuss bank accounts

The key issue for newly married couples is whether to have separate bank

accounts or to have a joint account. This decision needs to be a practical one,

as an emotionally driven decision can backfire. For example, having separate

accounts is generally a great idea for a working couple.

Identify financial goals

In today's complex financial environment, investing money judiciously to

ensure that one has enough at every stage of one's life is becoming

increasingly challenging. Financial planning can play an important role here.

Having a financial plan in place and a strategy to implement it would mean

that the couple can allocate funds appropriately for all their goals.

Goal-based investing can go a long way in ensuring that the couple invests

with a clear time horizon and avoids making abrupt changes in their

portfolios. The asset allocation process, which is an integral part of financial

planning, would largely determine the level of risk and the likely returns from

their portfolio. Knowing their goals would also ensure that both take

responsibility to achieve them.

Having adequate risk cover in the form of life and health insurance is an

important aspect of financial planning. While the thumb rule for life

insurance is to have a cover equivalent to 10 years of the annual income, the

extent of health insurance cover required will depend upon whether the

couple's employers offer any such facility or not, and if yes, how much that is.

Create an emergency fund

Before starting the investment process, the priority should be to create an

emergency fund. An emergency fund is needed not only to take care of

anything unexpected that may come along, but also to allow the couple to

continue their long-term investment process uninterrupted. Above all, it gives

peace of mind to the newlyweds, which is crucial in the early stage of their

married life.

The size of the emergency fund is something that the couple needs to decide

taking into consideration their monthly expenses, the level of liquidity in the

investment portfolio and the kind of jobs that they are engaged in. Ideally, an

emergency fund should be enough to take care of the couple's monthly

expenses for at least six months.

It is equally important to invest this emergency fund in options that provide

the required levels of liquidity, tax efficiency and decent returns. Some of the

options that can be considered are bank savings accounts with auto-sweep

facility, as well as ultra short-term and short-term debt funds.

Manage debt efficiently

In today's world, it is practically impossible to live debt free. However, the

impact of a loan on a couple's overall financial health would depend on the

purpose for which a loan is taken. For example, a housing loan not only helps

in buying a house at an early stage in the couple's life but also in saving taxes

(greater savings in case of a joint loan).

On the other hand, indiscreet use of credit cards may result in a disaster with

long lasting financial implications. Therefore, it makes sense to keep credit

card usage within reasonable limits. Managing debt efficiently can go a long

way in helping young couples stabilise their future.

(This article written by our CEO, Mr. Hemant Rustagi was published in

Dalal Street Journal-Issue dated May 21, 2012).

Page No. 3 | June 2012

Q & A

Q. I have been investing in mutual funds for quite some time and

come across lot of advisors who do not give proper advice. How can

one ascertain whether justice is being done to one's hard eared

money?

A: Once you start working with an advisor, it is very important to periodically

evaluate what type of advice and service you're getting and whether it is

helping you achieve your financial goals. Here's what you should look for:

• It is important that your advisor determines your risk level before

suggesting the schemes. Remember, it is the level of risk that provides the

guidance about the kind of return you can expect as well as the level of

volatility, while achieving it.

• Ensure that your advisor provides you with a comprehensive, well

thought-out plan for your money. Also ensure that the plan has the

required flexibility to take care of changes that might take place in your

needs.

• Ensure that your portfolio is a well diversified one. Diversification means

spreading your investments over a range of different options such as

equity schemes, balanced and debt-oriented schemes.

• While reviewing your investments, if you notice that your investments

are consistently losing money, make sure your advisor has the right

answer for it. If he recommends sticking with an investment that's on the

decline, ask why?

• Make sure you know the reasons for investing or redeeming any MF

investment. Also, you should know how a recommended scheme fits into

your personal financial plan.

Q: An investor can invest about ̀ 15,000 a month. How can he allocate the

money? His goal is to achieve 4 crore in 30 years and he has some current

investments and a couple of mutual funds like HDFC Midcap Fund and the

ICICI Focused Bluechip Fund. He has an insurance of 50 lakh in HDFC term

plan insurance.

A: The time horizon is around 30 years and the objective is to build a corpus

over a period of time. Systematic investment plan in equity funds will be the

right strategy. When you invest for 30 years, you need to focus on an asset

class which has a potential to beat inflation. This is where I think equity

definitely has a role.

My recommendation for him would be that even if he is a little risk averse, he

can take a call on investing in equity given a 30 year time horizon. The fact

that he will be investing systematically every month, the volatility over a

longer period is automatically taken care of.

I think his current investments are in two funds - HDFC Midcap Opportunity

and ICICI Focused Bluechip fund. ICICI Focused Bluechip, a quality large

cap fund, can be continued. ` 10,000 is being invested in HDFC Midcap

Opportunity which is a leader in its own category. It is not always about

investing in the top performing funds, it is also about looking at which funds

are suitable for you and what kind of risk profile you have.

In this case, almost two third of the money is going into midcap fund, which is

not the right strategy for someone who is looking to begin investing. Yes,

midcap fund has a potential to do well over a longer period. But it's also a fact

that they tend to be more volatile compared to well diversified equity funds.

My recommendation is that he should make one change in this. He can

continue to invest in HDFC Midcap Opportunity maybe, around 5000 & the

balance 5000 should be invested in well diversified multi-cap fund. He can

either look at Canara Robeco Equity Diversified Fund or HDFC Equity Fund.

With this, he will have three funds in the portfolio - one multi-cap, one midcap

and one pure large cap fund. That will create the right balance. If he continues

to invest for 30 years assuming a return of around 12%, he should be able to

build a corpus of around 4.57 crore. The key, of course, is that he should

continue the process irrespective of the market condition.

(This personal query was answered by our CEO, Mr. Hemant Rustagi in

the programme Markets & Macros in CNBC TV18 on May 29, 2012).

`

`

`

`

`

Performance of Select Funds

June 2012 | Page No. 4

Data as on May 25, 2012

Mutual funds, like securities investments, are subject to market and other risks. As with any investments in securities, the NAV of units can go up or down depending on the factors and forces affecting capital markets.

EQUITY FUNDS

Diversified Fund Launch 1-Month* 3-Month* 6-Month* 1-Year* 2-Year** 3-Year** 5-Year**

Birla Sun Life Frontline Equity Aug-02 -4.99 -6.97 4.10 -7.15 1.84 8.99 7.41

Canara Robeco Equity Diversified Sep-03 -4.42 -4.63 5.97 -1.32 4.19 13.22 10.11

DSPBR Top 100 Equity Reg Mar-03 -6.16 -8.64 6.44 -3.97 3.98 10.17 8.11

DSPBR Equity Apr-97 -6.03 -6.68 5.14 -5.96 2.28 11.32 8.46

Fidelity Equity May-05 -5.51 -8.07 2.16 -7.00 2.92 12.42 6.61

Fidelity India Growth Oct-07 -5.23 -8.33 1.81 -7.09 3.13 12.30 —

Franklin India Flexi Cap Mar-05 -5.83 -9.27 2.06 -9.46 2.77 9.74 5.49

HDFC Equity Jan-95 -6.04 -7.48 5.89 -9.66 2.53 13.34 9.14

HDFC Top 200 Oct-96 -6.06 -8.52 5.42 -7.65 2.83 11.29 9.80

ICICI Prudential Dynamic Oct-02 -3.08 -5.98 7.80 -4.15 4.34 14.35 7.52

ICICI Prudential Focused Bluechip May-08 -5.25 -8.56 2.85 -3.62 6.83 13.73 —

Kotak 50 Dec-98 -4.58 -8.02 1.74 -7.18 1.15 6.98 4.70

Kotak Opportunities Fund Sep-04 -5.52 -7.60 3.24 -6.65 0.38 7.67 5.58

Reliance Regular Savings Equity Jun-05 -5.46 -5.99 5.06 -10.01 -1.41 8.40 9.73

Reliance Equity Opportunities Mar-05 -2.98 -0.55 12.86 2.80 9.03 21.88 9.72

Tata Equity PE Jun-04 -6.66 -10.46 3.52 -8.26 -0.39 11.37 7.32

Sector, Specialty & Tax Saving

ICICI Prudential FMCG Mar-99 -4.22 10.58 16.84 28.61 31.12 35.13 15.90

Reliance Banking Retail May-03 -5.07 -9.51 8.43 -8.62 4.70 14.10 15.55

Reliance Pharma Jun-04 -3.17 4.76 9.28 3.65 8.28 30.32 20.13

Canara Robeco Equity Tax Saver Mar-93 -3.98 -4.33 6.01 -1.73 3.88 13.73 11.84

Fidelity Tax Advantage Feb-06 -4.71 -6.68 3.53 -6.30 3.42 13.55 7.71

HDFC Taxsaver Mar-96 -6.06 -8.07 3.39 -7.88 1.68 13.12 6.50

Gold: Fund of Funds

Kotak Gold Mar-11 1.4923 2.1399 6.6681 29.0904 — — —

Reliance Gold Savings Mar-11 0.9769 2.2726 6.3114 29.0093 — — —

Midcap & Smallcap

Birla Sun Life Dividend Yield Plus Feb-03 -6.38 -6.71 3.25 -3.23 4.51 16.20 11.71

DSPBR Small and Mid Cap Reg Nov-06 -5.06 -2.83 5.43 -3.67 2.91 17.67 7.88

HDFC Mid-Cap Opportunities Jun-07 -5.45 -3.35 8.18 1.12 9.95 21.80 —

ICICI Prudential Discovery Aug-04 -3.74 -0.99 12.84 -1.81 5.75 21.66 11.15

IDFC Premier Equity Sep-05 -3.34 -0.92 7.34 2.06 9.64 19.69 15.86

IDFC Sterling Equity Mar-08 -5.85 1.42 10.01 -0.06 5.68 19.87 —

Sundaram Select Midcap Reg Jul-02 -4.08 -5.40 1.86 -5.91 2.92 12.43 7.64

UTI Dividend Yield May-05 -5.21 -9.09 0.73 -6.52 3.49 13.75 10.76

UTI Master Value Jul-98 -5.73 -6.24 1.83 -8.01 2.60 17.09 8.71

Hybrid: Equity Oriented Fund Launch 1-Month* 3-Month* 6-Month* 1-Year* 2-Year** 3-Year** 5-Year**

Canara Robeco Balanced Feb-93 -2.89 -1.66 7.16 2.40 5.82 11.59 9.39

HDFC Balanced Sep-00 -3.70 -3.24 6.70 1.35 9.56 17.09 12.14

HDFC Prudence Feb-94 -4.03 -3.30 7.54 -0.78 6.23 16.38 11.69

Reliance Regular Savings Balanced Jun-05 -1.93 -2.03 7.64 0.16 3.70 12.46 12.25

Hybrid: Debt Oriented

Canara Robeco MIP Apr-01 -0.5371 1.1315 4.9063 7.0153 6.8342 7.5641 9.7362

HDFC MIP LTP Dec-03 -0.9433 -0.0357 5.4151 5.1356 6.3952 9.4765 9.6743

L&T MIP Jul-03 -0.3783 0.5213 4.1135 5.6525 5.2298 6.3474 9.1297

Reliance MIP Dec-03 -0.3282 1.0670 8.2522 7.5638 7.1733 9.8414 11.3425

FT India Dynamic PE Ratio FoF Oct-03 -2.5741 -4.8994 3.3866 0.5331 4.7351 8.5992 9.2370

*Absolute ** Annualised. Past performance may or may not be sustained in future.

Debt Oriented & Ultra Short Term Debt Fund Funds Launch 1 Week* 1 Month* 3 Months*6 Months* 1 Year* 2 year** 3 Year**

Birla Sun Life Dynamic Bond Ret Sep-04 0.1070 0.6626 2.1801 5.3172 10.4533 7.9356 7.6401

BNP Paribas Flexi Debt Reg Sep-04 0.1444 0.5144 2.4307 6.1816 8.1282 5.7506 5.7061

L&T Select Income-Flexi Debt Ret Oct-09 0.1834 0.7781 2.3928 4.701 9.5149 8.2515 ----

L&T Ultra Short Term Mar-02 0.1765 0.7722 2.4717 4.842 9.5884 8.2182 6.9828

Templeton India Short-term Income Ret Jan-02 0.1505 0.5993 2.2671 4.4736 9.4956 7.6388 8.3001

Templeton India Income Opportunities Dec-09 0.1251 0.5471 2.1899 4.4885 9.5290 7.7426 —

BNP Paribas Money Plus Reg Oct-05 0.1781 0.7412 2.4730 4.7644 9.3277 8.2284 7.1036

Kotak Floater LT Aug-04 0.1876 0.7880 2.3673 4.7099 9.5543 8.3970 7.2555

Please check whether you have received dividend for the fund/s that you may have in your portfolio out of this list. In case, you do not maintain any portfolio statement, Wiseinvest Advisors can do that for you free of charge. Once we have the details, we would send your updated statement every month. You can contact our corporate office or any of the branches to avail of this free service.

Dividends declared by equity and equity-oriented funds during

the month of May 2012 Scheme name Date Dividend declared in ̀ Per unit

ICICI Pru Blended Plan - B (MD) 09/05/2012 0.07

ICICI Pru Blended -B Inst. (MD) 09/05/2012 0.08

Tata Balanced Fund (MD) 11/05/2012 0.30

FT India Balanced Fund (D) 18/05/2012 2.00

IDFC Arbitrage Plus-A (D) 21/05/2012 0.03

IDFC Arbitrage Plus-B (D) 21/05/2012 0.03

IDFC Arbitrage Fund (D) 21/05/2012 0.03

Birla SL Advantage Fund (D) 25/05/2012 4.00

Kotak Equity Arbitrage (D) 28/05/2012 0.10

ICICI Pru Blended Plan - B (DD) 28/05/2012 0.01

ICICI Pru Blended -B Inst. (DD) 28/05/2012 0.01

Edelweiss E.D.G.E. Top 100 -C (D) 30/05/2012 0.75

Page No. 5 | June 2012

Mutual fund investors in India have had a roller-coaster ride. Little wonder

then that despite having the potential to fit every investor's portfolio, mutual

funds have failed to become the first investment choice. While it cannot be

denied that investors' participation in mutual funds has been increasing over

the years, issues like mismatch between expectations and reality, mis-

selling, lack of understanding and wrong positioning of products have

hampered the growth of the industry time and again. Besides, wrong

investment strategies have added to investors' woes.

Here is how investor portfolios get affected when they follow wrong

strategies, and how they can be rectified:

The first instinct of investors who invest in equity funds without a defined

time horizon is to abandon them during a market downturn. A similar

reaction is seen in investors who invest through a systematic investment

plan (SIP) without any time commitment. While they happily invest in a

rising market, they develop cold feet when the markets are actually

presenting great long-term investment opportunities. Clearly, their fetish for

catching the market bottom often makes them wary of taking the plunge. On

the other hand, someone who invests with a long-term commitment has time

on his side and hence is better prepared to handle these situations.

Remember, short-term adverse movements in the market do not take away

the ability of equity to outperform other asset classes in the long run. By

continuing to invest during turbulent times, one can benefit a great deal

when the market rebounds.

Investors often rely on short-term performance while investing in equity

funds. This strategy takes them beyond their risk-taking capacity because

investing in top-performing funds, when mid-cap stocks are doing well,

would result in a significant amount getting allocated to mid-cap funds.

Although mid-cap funds have the potential to do well, it is important to have

a restricted exposure to them to maintain the risk-reward balance in the

portfolio. No doubt, past performance is an important aspect in the decision-

making process, but relying too much on it can be disastrous.

Abandoning equity funds during downturn

Relying too much on past performance

Stay The Course - Portfolio gone awry?

Too many schemes in portfolio

Investing just before dividend payout

Compromising long-term growth

Many investors believe that the best way to diversify a mutual fund portfolio

is to have a large number of funds. As a result, their portfolios suffer from

over-diversification. Moreover, having too many overlapping funds makes

portfolio-tracking quite complicated. In fact, a few carefully selected funds

can not only provide a higher level of diversification but also improve

portfolio returns.

While there is nothing like an optimal number of funds that one needs to own

to have a sufficiently diverse portfolio, factors like size of the portfolio and

asset allocation can play a key role in deciding that number.

It is a common belief among a set of investors that investing in an equity fund

just before dividend payment is a good strategy. The truth is that they receive

a part of their own capital as dividend. Besides, the attraction of dividend

often blinds their investment decisions and they end up investing in funds

that do not actually merit an investment.

Here is an example of why it does not make sense to follow this strategy.

First, if a fund declares 100 per cent dividend, it is paid on the face value,

which is ̀ 10 in most cases, and not on the NAV. Second, once the dividend is

paid, the fund's NAV gets reduced by the dividend amount. For example, if

the NAV of a fund paying 100 per cent dividend is ̀ 40 on the record date, it

will come down to ` 30 post-dividend. Therefore, while an investment of `

10,000 will get an investor a dividend of ̀ 2,500, its current value will also

come down to ̀ 7,500.

It is important to know that dividend payment by mutual funds is a process of

distributing gains to its unit holders, and only those who remain in the fund

for a considerable period benefit from it in the real sense.

Investors often lose sight of their long-term goals when they spot an

opportunity to make some short-term gains. For example, in a market

situation such as now, it can be tempting to either pull money out of equity

funds or stop investing in them and instead redirect funds to attractive debt

options such as fixed maturity plans (FMP). Cont. on page 6...

A few, simple-to-follow steps can put it back on track

June 2012 | Page No. 6

R.N.I. No.: MAHENG/2007/19802 • Postal Regd. No.: MH/MR/N/MBI/72/10-12 • Posted at Mumbai Patrika Channel Sorting Office, GPO, Mumbai on 9th & 10th of every month.

DISCLAIMER: All reasonable care has been taken to ensure that the information contained herein is neither misleading nor untrue at the time of publication, but we make no representation as to its accuracy or completeness. All information is provided without any liability whatsoever on the part of Wiseinvest Advisors Private Limited.

RISK FACTORS: Mutual funds, like securities investments, are subject to market and other risks and there can be no assurance that the scheme's objectives will be achieved. As with any investments in securities, the NAV of units can go up or down depending on the factors and forces affecting capital markets. Please read the offer document before investing.

Edited, Published and Printed by Mr. Hemant Rustagi, on behalf of Wiseinvest Advisors Pvt. Ltd. from 202, Shalimar Morya Park, New Link Road, Andheri West, Mumbai 400053 at AdvantEdge Offset Printers, K-7 Rizvi Park, S V Road , Santacruz (W), Mumbai 400 054. Design by Mosaic Design. Copyright reserved © 2007. All rights reserved in favour of Wiseinvest Advisors Pvt. Ltd.

• Corporate Office:

202, Shalimar Morya Park, New Link Road, Andheri West, Mumbai 400053. Tel : 65281507 / 09

Fax : 2673 2671. E-mail : [email protected]

• Branches:

Fort : 107, Vikas Building, Above Jimmy Boy Restaurant, 11, N.G.N. Vaidya Marg, Fort, Mumbai - 400 001. Tel: 6524 5333 / 34, 2263 2329

Fax: 2263 2330. E-mail : [email protected]

Thane : Aishwarya Laxmi, Shop No. 4, Opp. Namdeo Wadi Hall, Maharshi Karve Road, Thane (W) - 400 602. Tel : 6592 7051 / 52

Fax : 2539 1306. E-mail : [email protected]

www.wiseinvestadvisors.com

WISEINVEST ADVISORS PVT. LTD.

Date of Publication: 5th of every month.

A Note to our esteemed readersWealthwise is being sent to some of you on a Complimentary basis as a part

of our humble effort to ensure that more and more investors benefit from the

potential of mutual funds. We sincerely hope that you would like the

contents of Wealthwise and in some way benefit from it. However, if you do

not wish to receive “Wealthwise” on a regular basis, please let us know

either by sending us a mail on or by

calling us on (022) 65281507/09. You can also write to us at our Corporate

Office address mentioned below.

Stay The Course...

While this might look like a great investment decision now, investors will

still have reinvestment risk to tackle when the FMPs mature.

A likely scenario of lower interest rates and improved indices levels might

compel the same investors to re-enter the stock market at a higher level. Such

strategies can affect the end result for a long-term investor.

It is quite common to see investors ignore their debt portfolio as they are

considered to be safe. It is important for debt fund investors to know that

bond prices move inversely to interest rates. When interest rates go up, bond

prices go down and when interest rates go down, bond prices go up.

Since movements in interest rates can have a significant impact on a debt

portfolio, there is a need to monitor it not only to realign it in line with the

changing interest rate scenario but also to protect gains.

Simply put, the key is to manage credit and duration risk efficiently. Among

the debt funds, a major differentiator is the maturity duration of the portfolio.

Each category of debt funds has a different risk profile and commensurate

return potential. The longer the maturity duration of the portfolio, the greater

is the impact of an interest rate change. As is evident, debt fund investors

need to tread carefully and keep an eye on the emerging rate scenario.

(This article written by our CEO, Mr. Hemant Rustagi was published in

Business world Issue dated April 30, 2012).

Ignoring debt portfolio

...Cont. from page 5