Embed Size (px)

Citation preview

www.apexminerals.com.au

Apex Minerals NL ABN 22 098 612 974

Annual Report 30 June 2008

ApexCover08.indd 1 13/10/08 3:14:50 PM

For

per

sona

l use

onl

y

Directors

Mark Ashley Managing Director

Mark Bennett Exploration Director

Glenn Jardine Operations Director

Stephen Lowe Non Executive Director

Todd Bennett Non Executive Director

Kim Robinson Non Executive Chairman

company secretary

Graham Douglas Anderson

principal office

level 1, 10 ord streetWest perth Wa 6005po Box 682, West perth Wa 6872telephone: (08) 6311 5555facsimile: (08) 6311 5556email: [email protected]

registereD office

level 1, 10 ord streetWest perth Wa 6005po Box 682, West perth Wa 6872

share registry

advanced share registry services pty ltd110 stirling highway, nedlands Wa 6009po Box 1156, nedlands Wa 6909telephone: (08) 9389 8033facsimile: (08) 9389 7871

auDitors

stantons internationallevel 1, 1 havelock street, West perth Wa 6005telephone: (08) 9481 3188facsimile: (08) 9321 1204

solicitors

salter powerlevel 2, 6 Kings park road, West perth Wa 6005telephone: (08) 9216 0900facsimile: (08) 9216 0901

asX coDe: aXmacn: 098 612 974

WeB: www.apexminerals.com.au

Corporate Directory

ApexCover08.indd 2 13/10/08 3:14:50 PM

For

per

sona

l use

onl

y

1Annual Report 08

Table of Contents

Managing Director’s Address 2

Apex Project Location Map 5

Overview 7

Operations Project Development 14

Exploration and Resources 18

Resource Table 30

Reserves Table 32

Directors’ Report 34

Independent Auditor’s Report 44

Independence Declaration 46

Director’s Declaration 47

Income Statements 48

Balance Sheets 49

Statement of Changes in Equity 50

Cash Flow Statements 51

Notes to Financial Statements 52

Corporate Governance Statement 86

Additional Information 91

A Year of Highlights

1Annual Report 08

Positive Completion of Wiluna Implementation study in June forecasts cash costs of A$560/oz;

A$62m equity raising completed in June;

A$60.5m raised in September via issuance of Bonds, Warrants and Gold Upside Participation Notes;

Major resource upgrades announced in February, June and September;

Maiden reserve announced in June;

Refurbishment of plant well advanced;

Mining at Wiluna commenced in October;

First gold pour expected in November;

Second Lawlers Nickel JV with Barrick announced in June.

For

per

sona

l use

onl

y

2Apex Minerals NL

MD & CEO Address

Dear Fellow Shareholder,

It is with pleasure I present to you the Annual Report for 2008. Apex has had an exciting year, and we now stand on the cusp of beginning significant and profitable gold production at Wiluna. First gold production is scheduled to commence in November 2008. Production for the 2009 calendar year is expected to be around 130,000 ounces increasing to 200,000 ounces per annum in subsequent years.

The results of the Project Implementation Study announced in June and the imminent return to production have validated the integrated mine strategy adopted by Apex when it began consolidating the Wiluna, Wilsons and Youanmi projects in early 2007. As Apex moves into production, it will emerge as one of Australia’s largest domestically listed gold producers at competitive cash costs delivering substantial cash margins. We have significant growth opportunities ahead and are now fully funded.

We have had substantial exploration success since acquiring these deposits, particularly at Wiluna, where gold resources now stand at over 1.5 million ounces. When we acquired Wiluna mid 2007, we set our selves a target to increase the Reserve base from approximately 6 to 9 months at that time to 3-5 years by the time we get back into production.

On 29 September we announced a 70% increase in the Indicated Resource base in the Calais area of the Wiluna mine to around 600,000 ounces. We are currently re-calculating the Reserves there, but the new underground resource together with the new open pit resource at Wiluna will, I’m confident, result in our getting close to the 5 year target.

The exploration success that we have experienced at Wiluna in recent months has resulted in the process plant being able to be fed completely with the lower cost Wiluna ore and the requirement to truck supplementary feed from our nearby Wilsons deposit has been deferred such that commencement of the development of this deposit has been put back at least until the March 09 quarter.

Significant progress on the development of the Wiluna project was made throughout the year, with a number of development plans coming to fruition. We successfully finalised the consolidation all the required assets to commence our integrated mine strategy, with the purchase of Wiluna, Wilsons and Youanmi. Detailed metallurgical test work and engineering studies were undertaken for the project implementation study, culminating in the decision to commit to development in June 2008.

At this time the refurbishment of the Wiluna plant is nearing completion, with over 150 workers on site and production on schedule to recommence in November 2008.

Overall cash costs are estimated to be $560 per ounce, which will deliver a healthy cash margin based on the current gold price. Apex’s medium term goal is to reach 500,000 oz per annum of profitable gold production and multiple growth options are open to Apex to achieve this goal.

All necessary capital to develop the Wiluna Project has been raised. It is of great credit to Apex’s management team and the strength of the project that the funds, amounting to over $120 million were raised during the year at a time of extreme global financial conditions which is adversely affecting all businesses in raising development finance. A $62 million placement was achieved in March and a $60.5m Senior Secured Note with detaching warrants and a rather unique Gold Upside Participation Note announced on 29 September.

The funds from this raising now results in your company being fully funded and will enable the highly successful exploration program to be maintained at around $20 million per annum.

World economic conditions remain clouded, with many markets continuing to suffer extreme volatility. For centuries, gold has acted as the traditional store of wealth and safe haven for investors in troubled times. In these uncertain times, the outlook for gold remains extremely positive and this is an opportune time to be entering gold production.

For

per

sona

l use

onl

y

3Annual Report 08

I would like to thank the management team and staff at Apex for their hard work during 2008 and very much look forward to the culmination of all their efforts in our first gold pour in late 2008. I would also like to thank you, our shareholders for your loyalty and support over the past 12 months.

Kind Regards,

Mark Ashley

Managing Director and Chief Executive Officer

All the photographs that appear in this Report reflect the current refurbishment occuring at the Wiluna plant, new mining fleet vehicles purchased and continued drilling. The focus is to present this by showing all the people actively engaged in the process.

500Oct Oct Oct Oct Oct Oct03 04 05 06 07 08

600

700

800

900

1000

11005

Year AUD Gold Price

200Oct Oct Oct Oct Oct Oct03 04 05 06 07 08

300

400

500

600

700

8005

Year USD Gold Price

For

per

sona

l use

onl

y

4Apex Minerals NL

For

per

sona

l use

onl

y

5Annual Report 08

Apex Project Locations Eastern GoldfieldsF

or p

erso

nal u

se o

nly

6Apex Minerals NL

For

per

sona

l use

onl

y

7Annual Report 08

Overview

THE REGIONAL GOLD STRATEGY

Apex has assembled a portfolio of gold assets capable of elevating the company to producer status by early 2009. The projects are located in the Eastern Goldfields of Western Australia as shown on page 5.

Apex’s regional gold development strategy is to consolidate the ownership of various high grade, but currently undeveloped, refractory gold deposits. Following the completion of the Implementation Study in June, Apex is set sequentially develop Wiluna, Wilsons and Youanmi lifting group production to 200,000 ounces per annum.

The Aphrodite project also has the potential to be an additional processing hub producing either a high grade gold concentrate for trucking to Wiluna for treatment through the BIOX® bacterial oxidation plant or, gold metal on site further increasing annual group gold production.

IMPLEMENTATION STUDY

The Implementation Study into the refurbishment of the Wiluna gold treatment plant and the development of the Wiluna, Wilsons and Youanmi high grade underground gold mines was completed in June 2008. The study used reserves estimated in June 2008 based upon resource estimates completed in May 2008.

The study showed that a minimum 3 year production life could be supported at each of the mines feeding the Wiluna plant. Formal Board approval to proceed with the development of the project was given in June 2008, just 12 months after Apex took control of the Wiluna mine.

Following the resource expansion at Wiluna announced in September 2008 additional studies will now be undertaken with a view to expanding the reserve and production base at Wiluna.

For

per

sona

l use

onl

y

8Apex Minerals NL

8Apex Minerals NL

Wiluna Project Location of New ResourcesF

or p

erso

nal u

se o

nly

9Annual Report 08

Overview continued

WILUNA

The Wiluna Gold Mine is located 1,000 kilometres northeast of Perth in the Eastern Goldfields of Western Australia. Apex took possession of the Wiluna operations with effect from 1 August 2007. The assets acquired as part the Wiluna transaction include all equipment necessary to operate a modern gold mining and processing facility, namely:

• 1Mtpa gold processing facility (including BIOX® bacterial oxidation plant);

• Fully equipped administration facilities;• 12MW gas power station;• 300 person accommodation village;• Borefields and associated pumping system;• Workshops and stores;• Fully developed and serviced underground mine;• Established roads.

Description

Wiluna has produced approximately four million ounces of gold to date. Early mining for gold at Wiluna commenced in the late 19th century through a series of shallow underground and open pit workings, and two million ounces of gold were produced from underground workings at East Lode and West Lode during the 1930’s to 1950.

Modern gold mining operations at Wiluna commenced in the 1980s with the treatment of tailings from historic workings and non-refractory open pit reserves through what is now conventional CIP/CIL technology.

Gold at Wiluna is predominantly contained within sulphide minerals, particularly arsenopyrite, and is not amenable to extraction via normal cyanide leaching. It is however readily amenable to extraction using bacterial oxidation and has been successfully extracted in the company’s BIOX plant over the past 15 years. The common term used for this style of gold mineralisation is “refractory”.

Wiluna also hosts gold mineralisation associated with quartz reefs which is “free milling”, that is, amenable to conventional cyanide leaching.

Geology and Title

The Wiluna project comprises granted Mining Leases and is situated at the northern end of the Norseman-Wiluna greenstone belt – the most highly gold endowed greenstone belt in Australia, which contains major gold mines such as those at Norseman, St.Ives, the Golden Mile, Leonora and Thunderbox.

At Wiluna, gold mineralisation is found where a series of northerly striking faults intersects a northwest striking and southwest dipping sequence of basalts and dolerites. This series of faults includes the East Lode, West Lode and Moonlight Lode, which together have produced approximately four million ounces of gold since their discovery (page 8).

Each of these lodes contains several orebodies, which have been previously mined by open pit or underground methods to a depth of up to 900 metres (page 19).

For

per

sona

l use

onl

y

10Apex Minerals NL

Overview continued

WILSONS (GIDGEE)

Description

The Gidgee gold mine is located 640 kilometres northeast of Perth and approximately 130kilometres by road from Wiluna. Early mining for gold commenced in the 1930s through a series of shallow underground and open pit workings. Modern gold mining operations at Gidgee commenced in the late 1980s.

The assets acquired by Apex at Gidgee include:

• 600,000tpa conventional gold processing facility;• Underground pumping and electrical equipment;• 100 person accommodation village;• Airstrip;• Administration offices;• 1MW diesel power station;• Ready access to bore and pit water;• Workshop and Stores buildings; and• Established roads.

Geology and Title

The Gidgee project covers an area of approximately 2,500 square kilometres of the Gum Creek greenstone belt. The central core of the area is held as granted Mining Leases, which cover a 70 kilometre long structural corridor containing numerous occurrences of gold mineralisation (page 11).

Approximately twenty open pits have previously mined near surface gold mineralisation and underground mining was undertaken beneath the Swan Bitter and Kingfisher pits. Most of the gold is free milling, with the exception of the Wilsons deposit, which is refractory.

For

per

sona

l use

onl

y

11Annual Report 08

Gidgee Project Proposed Infrastructure Location Wilsons Mine

11Annual Report 08

For

per

sona

l use

onl

y

12Apex Minerals NL

For

per

sona

l use

onl

y

13Annual Report 08

Overview continued

YOUANMI

Description

The Youanmi gold mine is located 480 kilometres northeast of Perth and approximately 330 kilometres by road from Wiluna. Early mining for gold commenced in the 1930s through a series of shallow underground and open pit workings.

Modern gold mining operations at Youanmi recommenced in the 1980s. Like Wiluna, the gold mineralisation at Youanmi is predominantly contained within the matrix of sulphide particles, particularly arsenopyrite, at a microscopic level.

Similarly to Wiluna, gold extraction of refractory ore at Youanmi was achieved by using bacteria following sulphide flotation. The bacterial oxidation process at Youanmi used BacTech® patented bacteria, which is proprietary technology owned by BacTech®, but essentially similar in nature toBIOX® technology.

The assets acquired by Apex at Gidgee include:

• 600,000tpa conventional gold processing facility (including BacTech®);

• 40 person accommodation village;• Airstrip;• Administration offices;• 1MW diesel power station;• Ready access to bore and pit water;• Ready access to bore and pit water;• Workshop and Stores buildings; and• Established roads.

Geology and Title

The Youanmi project covers 40 strike kilometres of the gold mineralised Youanmi shear zone, with known resources and infrastructure being situated on granted Mining Leases. The Youanmi deposit is a high grade narrow vein style deposit, with gold intimately associated with sulphide minerals.

The main Youanmi deposit plunges steeply to the south and remains open at depth (page 26). Several parallel plunging shoots have been mined historically, with limited exploration beneath them.

APHRODITE

Description

The Aphrodite gold deposit is located 65 kilometres north of Kalgoorlie on a tenement package which covers 51 square kilometres of the Bardoc Tectonic Zone – a highly prospective regional gold bearing shear zone.

The project contains two known refractory gold deposits, the Alpha lode and the Phi lode, which are located within 200 metres of each other and could potentially be accessible from a shared underground development in the event of a decision to mine.

Geology and Title

The Aphrodite project covers 50 square kilometres of prospective geology in the Bardoc Tectonic Zone – a part of the Boulder-Lefroy Fault which also hosts the nearby Paddington Gold Mine and the Golden Mile, some 65 kilometres to the south. Gold mineralisation occurs in two main zones, the Alpha and Phi lodes.

The Alpha lode is a porphyry-hosted shear zone, and the Phi lode is a sediment-hosted shear zone.

For

per

sona

l use

onl

y

14Apex Minerals NL

Operations Project Development

WILUNA

Apex took control of the Wiluna mine in August 2007. Prior to the approval of the project by the Board in June 2008 the surface plant and infrastructure was on care and maintenance. The underground mine was kept fully serviced to allow diamond drilling activities to be undertaken. The company used the period ahead of Board approval to undertake detailed inspections and engineering reviews of the existing plant and infrastructure at Wiluna in order to develop a detailed refurbishment plan.

In addition, long lead time equipment items were ordered including the underground mobile equipment fleets for Wiluna and Wilsons, to eliminate any potential delays to the re-commencement of production.

Processing

Plant and Infrastructure Refurbishment

Infrastructure and plant refurbishment at Wiluna budgeted at $31M has included:

• Repair of the village wet and dry messes and accommodation units and facilities;

• Updating the engine management and control systems of the 13MW gas power station and undertaking repairs to the generators;

• Repair of the generators in the 8MW back-up diesel power station;

• Installation of new motor control centres (MCC’s) around the plant and improvement and replacement where necessary of high voltage (HV) and low voltage (LV) distribution and control systems around the plant, village and other surface installations;

• Semi automation and upgrading of the site water supply system;

• Removal, repair and re-installation of all crushers and screens within the crushing circuit;

• Inspection and replacement as necessary of all mill bearings and re-alignment of mill drives and gearboxes;

• Repair and re-adjustment of the flotation cells and the installation of a second flash flotation unit;

• Repair and replacement of rubber lining as well as internal and external cleaning of cooling coils in the BIOX tanks;

• Removal, repair and re-installation of all pumps (over 400) within the plant;

• Repair and upgrade of the plant monitoring and control system;

• Repair of plant tankage;• Expansion of the gold room; and• Refurbishment and expansion of the mine workshops

and pumping, water supply, power and communication systems.

Re-commissioning of the plant will be staged as the refurbishment of each circuit of the plant is completed. The first circuit to be re-commissioned will be the crushing circuit and this is expected to take place in the second week of October.

Bacteria

As previously advised bacteria from the Wiluna plant were retained at the cessation of operations in July 2007 and kept active at laboratories in Perth by being fed Wiluna concentrate retained from previous operations.

In mid 2008, the bacteria started being propagated in the laboratories in Perth and transported to the Wiluna site in 1 tonne batches. The bacteria is now being transferred into BIOX reactors on site and is being propagated using concentrate retained from previous operations and from a separate milling campaign conducted in April this year.

The company proposes to have 3 primary reactors full of live bacteria ready to receive ore by the start of November.

The bacteria propagation is being conducted on site by Apex employees all of whom have previously worked with the bacteria in the Wiluna plant. Work is proceeding on a 24 hour basis and using equipment that is not susceptible to interruption by power outages as a result of refurbishment of the electrical system.

Mining

Mining will commence at Wiluna at the East Pit open cut and Wiluna underground mine.

East Pit Open Cut

Mining of the East Pit open cut was temporarily suspended following the announcement of the acquisition of the Wiluna mine by Apex in April 2007. The pit was left with all waste pre-stripping having been completed and the next bench drilled out awaiting charging with explosives.F

or p

erso

nal u

se o

nly

15Annual Report 08

For

per

sona

l use

onl

y

16Apex Minerals NL

Operations Project Development continued

The contract for the mining of the East Pit open cut was awarded to Mining and Civil Australia Pty Ltd in September 2008. MACA commenced mobilisation to site in the week of 15 September and has now completed its mobilisation. Blasting of the next bench in East Pit is expected to occur in the second week of October. Accordingly the company expects that this will result in approximately 50,000 tonnes of broken ore stocks being available when the plant recomissions in November.

Wiluna Underground Mine

Underground mining will take place initially in the immediate vicinity of existing decline development in the Calais area. Activity will focus on the extraction of Calais reserves above the 600mRL and decline access to new zones at Henry V and Henry V North.

Underground Mobile Equipment Fleet

The underground mobile equipment fleet required for Wiluna has been delivered to site. The fleet has been acquired from Atlas Copco and is being financed under a finance lease arrangement also through Atlas Copco.

The fleet comprises:

• Jumbos – 2 x M2D and 1 x H104;• Production Drills – 2 x Simba M7 and 1 x Simba 1257;• LHD’s – 3 x ST1520 and 2 x 1030;• Trucks – 4 x MT6020;• Service Vehicles – 2 x Volvo IT.

Personnel

All operating activities at the mine with the exception of the East Pit open cut will be undertaken under an owner operator regime.

Accordingly, the company has embarked upon an extensive direct recruitment programme. Employees are initially being sought for the Wiluna operation and to date over 1200 applications have been received for approximately 150 positions.

The senior management team at Wiluna is in place.

For

per

sona

l use

onl

y

17Annual Report 08

Operations Project Development continued

WILSONS (GIDGEE)

The Implementation Study showed the commencement of decline development at Wilsons occurring in October 2008 with full production being reached 6 months later in April 2009. However, the recent success of infill and extensional drilling programmes at Wiluna has allowed the timing of development and production from Wilsons to be deferred by up to 5 months.

Ore produced from Wilsons will be trucked to the Wiluna plant for treatment. Production is planned to be sourced from extensions to the Wilsons 1, 2 and 3 deposits immediately below existing open pit workings. Minimal dewatering is required of the existing pits.

Production at Wilsons will commence following:

• Establishment of surface mine infrastructure at Wilsons including offices, workshops and power station;

• Decline development off the Wilsons 3 pit to the first ore horizons and establishment of underground services including power, ventilation, pumping and communication systems; and

• Upgrade of the existing Wilsons to Wiluna road.

Works conducted for the development of Wilsons this year comprised refurbishment of the existing village and associated infrastructure at Gidgee. Studies will continue into opportunities for improving upon the existing robust base case at Wilsons between now and the re-scheduled commencement of decline development in March 2009.

YOUANMI

The Implementation Study showed production from the Youanmi mine being scheduled for mid 2009. However, the recent success of infill and extensional drilling programmes at Wiluna has allowed the timing of production from Youanmi to be deferred to mid 2010.

Ore produced from Youanmi will be trucked to the Wiluna plant for treatment. Production is planned to be sourced from extensions to the deposit immediately below existing workings.

Production at Youanmi will commence following:

• Dewatering of the Main Pit and existing underground workings;

• Refurbishment of the existing decline and services; and• Detailed infill drilling and extensional drilling of the

resource from underground.

Works conducted at Youanmi this year has comprised:

• Minor refurbishment of the existing village and associated infrastructure;

• Refurbishment of existing surface evaporation ponds;• nstallation of dewatering pumps and pipelines in the

Main Pit; and• Dewatering of the Main Pit.

Prior to the commencement of dewatering in January 2008 the Main Pit contained 1.8 million cubic metres of water. By mid year approximately 1.0 million cubic metres had been dewatered and dewatering of the Main Pit is on schedule for completion in December 2008.

For

per

sona

l use

onl

y

18Apex Minerals NL

Exploration and Resources

WILUNA

Resources and Reserves

Since purchasing the Wiluna Mine in mid 2007 Apex has increased gold resources by 120%, from 700,000 ounces to over 1.5 million ounces of gold. This comprises Measured Resources of 550,000t @ 3.4g/t for 60,000 ounces in open pits, Indicated Resources of 3.5 million tonnes @ 6.5g/t for 741,000 ounces and Inferred Resources of 3.9 million tonnes @ 5.9g/t for 738,000 ounces of gold. A detailed breakdown of these resources is shown on pages 30 & 31.

Exploration and Resource Development

As detailed in the Company’s ASX announcements during the year, Apex has had considerable success in its program of resource definition drilling aimed at establishing sufficient mineral resources to underpin an initial ore reserve capable of sustaining production for a minimum of four years, sourced from within or close to existing underground development. The program of extensional drilling has significantly increased resources in the vicinity of the Calais zone, where the discovery of the Baldric zone has supplemented the Calais, Burgundy, Henry5 and Henry5 North zones. Infill drilling has been very successful in all zones and has enabled most of the resource to be classified as Indicated (pages 20 & 21).

Drilling has also commenced at the Crispin, East Lode North and Calvert zones, and an initial resource of over 200,000 ounces has been defined at East Lode North.

Grade control drilling in the East Lode open pit has discovered a significant additional zone of mineralisation, leading to a 70% increase in resources and a 94% conversion of Indicated Resources to the Measured category within the pit.

Drilling will continue with the aim of extending the limits of known mineralised zones, infilling these to Indicated Resource status and testing additional nearby targets. Several zones of mineralisation will be drilled to resource status as new underground drilling positions become available during the development of access to existing resources. These include the Brothers Reef and the newly discovered fault offset extension of the Golden Age Reef. Drilling will also continue to delineate additional mineralisation beneath the East Lode open pit adjacent to the historic East Lode workings. Historic production in this area exceeded 2 million ounces and there is considerable scope to identify additional resources close to, and in the immediate hanging wall of the old workings (page 19).

For

per

sona

l use

onl

y

19Annual Report 08

Wiluna Project Long projection of the East Lode open pit and North Resources

19Annual Report 08

For

per

sona

l use

onl

y

20Apex Minerals NL

Wiluna Project Long projection of the East Lode 50 Lens in the Calais area, showing new resources

20Apex Minerals NL

For

per

sona

l use

onl

y

21Annual Report 08

21Annual Report 08

Wiluna Project Long projection of the East Lode 100 Lens in the Calais area, showing new resources

For

per

sona

l use

onl

y

22Apex Minerals NL

Exploration and Resources continued

WILSONS (GIDGEE)

Resources and Reserves

Since purchasing the Gidgee Gold project in early 2007 Apex has increased gold resources by 33% from 490,000 ounces to 652,000 ounces. This is based on a doubling of the Wilsons resource from 164,000 ounces to 325,000 ounces of gold.

The new Wilsons resource comprises an Indicated Resource of 921,000t @ 7.2g/t for 215,000oz and an Inferred Resource of 535,000t @ 6.4g/t for 110,000 ounces of gold. A detailed breakdown of these resources is shown on pages 30 & 31.

The Indicated Resource at Wilsons underpins a Probable Ore Reserve of 826,000 tonnes @ 6.4g/t for a contained 170,000 ounces of gold, which supports an initial three year mine life.

Exploration and Resource Development

The Wilsons ore reserve is based only on drilling within the uppermost 250m of the deposit (page 24). The deposit continues at depth and drilling is proceeding with the dual aim of identifying extensions and infilling successive 100m panels to a spacing sufficient to classify additional zones of the resource as Indicated as a prerequisite to estimating additional ore reserves and extending mine life.

In addition to this, drilling has commenced scoping the Premium and Cascade prospects, which comprise free milling quartz veins (page 25). These zones are small but high grade and ideal for trucking to the Wiluna plant.

A regional exploration program has commenced to create a pipeline of prospects to continue defining additional resources which could supplement ongoing production from Wilsons.

For

per

sona

l use

onl

y

23Annual Report 08

For

per

sona

l use

onl

y

24Apex Minerals NL

24Apex Minerals NL

Gidgee Project Wilsons Deposit Long ProjectionF

or p

erso

nal u

se o

nly

25Annual Report 08

25Annual Report 08

Gidgee Project Premium Long Projection

For

per

sona

l use

onl

y

26Apex Minerals NL

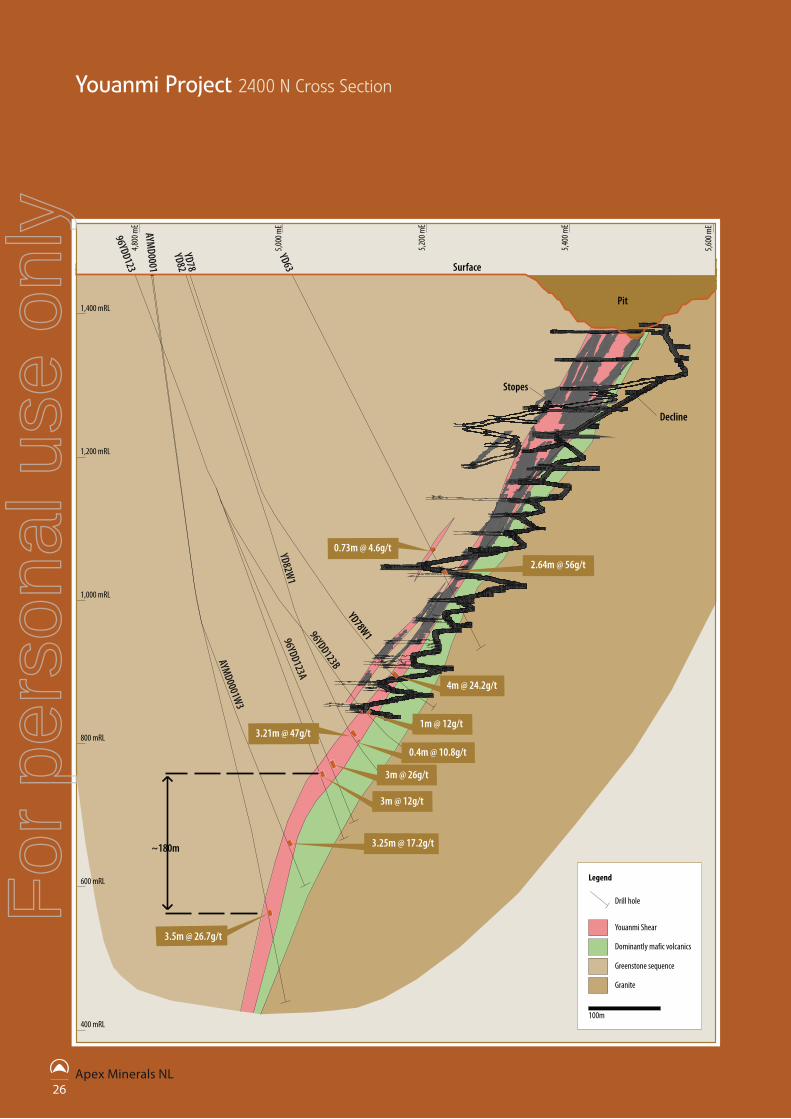

Youanmi Project 2400 N Cross Section

26Apex Minerals NL

For

per

sona

l use

onl

y

27Annual Report 08

Exploration and Resources continued

YOUANMI

Resources and Reserves

The Youanmi Gold Mine was purchased with a total resource inventory of 951,000 ounces of gold, estimated in compliance with JORC and NI 43-101 requirements. This includes an Indicated and Inferred resource of 2.4 million tonnes @ 8.5 g/t for 658,000 ounces of gold in the Youanmi Deeps gold deposit, estimated using a 4g/t lower cutoff.

Once infill drilling has been completed, the company intends to re-estimate the underground resource using a higher cutoff grade, in order to define a higher grade resource capable of sustaining the targeted production head grade of 11g/t, However, this will also reduce the tonnes and contained metal. A detailed breakdown of current resources is shown on pages 30 & 31.

Exploration and Resource Development

An initial surface diamond drilling program, undertaken to provide confidence in the down dip continuity of mineralisation, succeeded in defining high grade mineralisation up to 180 metres down dip of previous drilling and 100 metres beneath the base of the current resource. Detailed resource definition drilling will be undertaken from underground positions once the decline has been dewatered and refurbished. Detailed evaluation of other prospects in the Youanmi tenement package will commence in calendar 2009.

APHRODITE

Resources and Reserves

The Aphrodite deposit was purchased with an Inferred Resource of 1.44 million tonnes @ 6.2 g/t for 287,000 ounces of gold, estimated in compliance with the JORC code. This resource is based solely on the Alpha lode. In addition to this, a substantial amount of gold mineralisation exists within the Phi lode which is, as yet, unclassified. Resources are shown on pages 30 & 31.

Exploration and Resource Development

An initial phase of resource definition drilling has been completed on the Phi lode and an initial resource estimate is scheduled for completion late in 2008. This program has also provided a comprehensive set of samples for metallurgical testwork. Further drilling is planned during 2009.

OTHER EXPLORATION

Apollo Hill

Apex withdrew from the Apollo Hill Joint Venture during the year and has no ongoing rights or obligations.

For

per

sona

l use

onl

y

28Apex Minerals NL

Lawlers Nickel Project Electromagnetic Surveys and targets on Magnetics

28Apex Minerals NL

For

per

sona

l use

onl

y

29Annual Report 08

Exploration and Resources continued

OTHER EXPLORATION continued

Lawlers Nickel Joint Venture

Apex has entered into a second agreement with Barrick Gold to earn an initial 56% interest in the nickel rights on Barrick’s tenements adjacent to ist first JV, extending its coverage to a 234 square kilometres of nickel prospective terrain in the Lawlers district of the North Eastern Goldfields of Western Australia.

The terms of the JV are identical to the first JV, as detailed in the company’s ASX announcement 11 December 2006. The Barrick tenements are part of Barrick’s Lawlers Gold Operations, and the two JV’s contain over 80 strike kilometres of relatively unexplored nickel sulphide prospective ultramafic rocks in the heart of the world class North Eastern Goldfields nickel province. The JV area is surrounded by Xstrata’s Cosmos, Prospero and Sinclair nickel mines, BHP Billiton’s Perseverance and Rockys Reward nickel mines, and Norilsk’s Waterloo nickel mine.

Importantly, no effective nickel sulphide exploration has been undertaken on these tenements since Selection Trust explored the area thirty years ago. Since then, nickel sulphide exploration has been very limited, with most exploration focussing on nickel laterite and gold.

During the year Apex has extended its electromagnetic (EM) geophysical survey, which has identified several EM targets. Future work will comprise further EM surveying and ongoing drill testing of targets (page 28).

Jillawarra

The Jillawarra Joint Venture (“JJV”) covers an area of approximately 1,500 square kilometres adjoining and to the west of Abra Mining’s namesake lead-zinc deposit, which is estimated to contain 50mt @ 5.5% lead. The project is managed by Abra Mining.

During the year, Abra earned a 70% interest in this project, and as per the terms of the farm in agreement, Apex elected to take a 10% free carried interest to the completion of a bankable feasibility study.

Abra Mining have completed induced polarisation (IP) geophysical surveys, geochemical sampling and several drilling programs at the Copper Chert and other prospects during the year. Exploration for Abra-style lead-zinc-copper-gold deposits is ongoing.

BUSINESS DEVELOPMENT

While Apex Minerals is now fully committed to the execution of its regional gold strategy and exploration of its other projects it intends to continue to use its unique in-house expertise to evaluate other assets complimentary to its strategy both regionally and abroad.

HEALTH AND SAFETY

The Company has existing health and safety systems in place for its exploration activities. That system will be expanded to cover operations activities ahead of production re-commencing in November at Wiluna. To date, no lost time injuries have been sustained during the care and maintenance, underground and surface diamond drilling and plant refurbishment activities.

ENVIRONMENT AND COMMUNITY RELATIONS

The Company has obtained all necessary environmental approvals for the commencement of development and production at its operations. Comprehensive environmental management, monitoring, rehabilitation and reporting processes have been implemented by a dedicated team of environmental professionals over the past 12 months.

Good relations with stakeholders including local councils, indigenous groups, community groups and land owners are being maintained through a variety of initiatives. These initiatives include sponsorship of:

• Clontarf Girls Academy;• Two doctors at the Wiluna Community Medical Centre;• Annual Wiluna Rodeo.

INVESTMENTS

Empire Resources

During the year Apex acquired 5 million shares at 17 cents per share in Empire Resources positioning Apex as a 6.95% stakeholder in Empire with the right to nominate a representative to join the Empire Board of Directors.

Empire is currently exploring for volcanogenic massive sulphide (VMS) style copper-gold occurrences within its Yuinmery tenements just 6.5km from Apex Minerals Youanmi Plant. Both companies have signed a Memorandum of Understanding (MoU) to enter into commercial negotiations relating to the Yuinmery Project. Under the MoU, Empire and Apex will investigate the possibility of future development and production for Yuinmery, including the use of the Youanmi plant and its flotation circuit to treat Yuinmery ore.

For

per

sona

l use

onl

y

30Apex Minerals NL

Resource Table as at 7 October 2008M

EASU

RED

IND

ICAT

EDIN

FERR

EDTO

TAL

Not

eTo

nnes

Gol

d, g

/tO

zTo

nnes

Gol

d, g

/tO

zTo

nnes

Gol

d, g

/tO

zTo

nnes

Gol

d, g

/tO

z

WIL

UN

A

Und

ergr

ound

Cala

is un

derg

roun

d0

0.0

02,

380,

000

6.8

520,

000

1,41

0,00

06.

228

0,00

03,

790,

000

6.6

800,

000

1

East

Lod

e N

orth

00.

00

440,

000

5.9

80,0

0067

0,00

05.

712

0,00

01,

110,

000

5.8

210,

000

1

East

& W

est L

ode

othe

r0

0.0

063

0,00

06.

212

0,00

078

0,00

05.

714

0,00

01,

400,

000

5.9

270,

000

2

Hap

py Ja

ck0

0.0

00

0.0

012

0,00

07.

630

,000

120,

000

7.6

30,0

002

Lone

Han

d-Ad

elai

de-M

oonl

ight

00.

00

00.

00

710,

000

6.3

140,

000

710,

000

6.3

140,

000

2

Tota

l Wilu

na u

nder

grou

nd0

0.0

03,

440,

000

6.6

730,

000

3,68

0,00

06.

172

0,00

07,

120,

000

6.3

1,44

0,00

0

Ope

n pi

t & st

ockp

iles

East

Pit

370,

000

4.1

50,0

000

0.0

030

,000

4.2

4,00

040

0,00

04.

153

,000

3

Nor

th P

it0

0.0

00

0.0

040

,000

3.0

4,00

040

,000

3.0

4,00

04

Lone

Han

d-Ad

elai

de-M

oonl

ight

00.

00

50,0

005.

79,

000

140,

000

2.5

11,0

0019

0,00

03.

321

,000

4

Mag

azin

e0

0.0

050

,000

3.6

6,00

010

,000

4.7

1,00

060

,000

3.8

7,00

04

Stoc

kpile

s18

0,00

01.

810

,000

00.

00

00.

00

180,

000

1.8

10,0

005

Tota

l Wilu

na o

pen

pit &

stoc

kpile

s55

0,00

03.

460

,000

100,

000

4.7

15,0

0022

0,00

02.

921

,000

870,

000

3.4

96,0

00

TOTA

L W

ILU

NA

550,

000

3.4

60,0

003,

540,

000

6.5

741,

000

3,90

0,00

05.

973

8,00

08,

000,

000

6.0

1,53

9,00

0

GID

GEE

Und

ergr

ound

Wils

ons

00.

00

920,

000

7.3

215,

000

540,

000

6.4

110,

000

1,46

0,00

06.

932

5,00

06

Oth

er30

,000

10.4

9,00

021

0,00

012

.080

,000

560,

000

7.4

134,

000

800,

000

8.7

223,

000

7

Tota

l Gid

gee

unde

rgro

und

30,0

0010

.49,

000

1,13

0,00

08.

129

4,00

01,

100,

000

6.9

245,

000

2,25

0,00

07.

654

8,00

0

Ope

n pi

t & st

ockp

iles

Oth

er0

0.0

01,

050,

000

3.1

103,

000

00.

00

1,05

0,00

03.

110

3,00

08

Tota

l Gid

gee

open

pit

& st

ockp

iles

00.

00

1,05

0,00

03.

110

3,00

00

0.0

01,

050,

000

3.1

103,

000

TOTA

L G

IDG

EE30

,000

10.4

9,00

02,

180,

000

5.7

398,

000

1,10

0,00

06.

924

5,00

03,

300,

000

6.1

652,

000

YOUA

NM

I

Und

ergr

ound

Youa

nmi u

nder

grou

nd0

0.0

081

0,00

08.

121

0,00

01,

610,

000

8.7

449,

000

2,41

0,00

08.

565

9,00

09

Tota

l You

anm

i und

ergr

ound

00.

00

810,

000

8.1

210,

000

1,61

0,00

08.

744

9,00

02,

410,

000

8.5

659,

000

Ope

n pi

t & st

ockp

iles

Vario

us o

pen

pits

20,0

005.

53,

000

4,62

0,00

01.

521

9,00

01,

180,

000

1.9

72,0

005,

820,

000

1.6

294,

000

10

Tota

l You

anm

i ope

n pi

t & st

ockp

iles

20,0

005.

53,

000

4,62

0,00

01.

521

9,00

01,

180,

000

1.9

72,0

005,

820,

000

1.6

294,

000

TOTA

L YO

UAN

MI

20,0

005.

53,

000

5,43

0,00

02.

542

9,00

02,

790,

000

5.8

521,

000

8,23

0,00

03.

695

3,00

0

APH

ROD

ITE

Und

ergr

ound

Alph

a Lo

de0

0.0

00

0.0

01,

440,

000

6.2

287,

000

1,44

0,00

06.

228

7,00

011

Tota

l Aph

rodi

te u

nder

grou

nd0

0.0

00

0.0

01,

440,

000

6.2

287,

000

1,44

0,00

06.

228

7,00

0

TOTA

L AP

HRO

DIT

E0

0.0

00

0.0

01,

440,

000

6.2

287,

000

1,44

0,00

06.

228

7,00

0

GLO

BAL

Und

ergr

ound

30,0

0010

.49,

000

5,38

0,00

07.

11,

231,

000

7,83

0,00

06.

71,

698,

000

13,2

30,0

006.

92,

938,

000

Ope

n Pi

t & S

tock

pile

s57

0,00

03.

463

,000

5,77

0,00

01.

833

7,00

01,

400,

000

2.1

93,0

007,

740,

000

2.0

493,

000

TOTA

L60

0,00

03.

872

,000

11,2

00,0

004.

41,

570,

000

9,20

0,00

06.

01,

790,

000

21,0

00,0

005.

13,

430,

000

For

per

sona

l use

onl

y

31Annual Report 08

Competent Person’s statement for exploration results and Mineral Resources Estimates

Note

1. Resource estimated September 2008 by Andy Thompson at a 3.5g/t Au lower cut off.

2. Resource estimated June 2007 by Paul Tan at a 4.5g/t Au lower cut off.

3. Resource estimated September 2008 by Andy Thompson at a 1.0g/t Au lower cut off.

4. Resource estimated June 2007 by Paul Tan at a 0.75g/t Au lower cut off.

5. Resource estimated June 2007 by Paul Tan at a 1.5g/t Au lower cut off.

6. Resource estimated May 2008 by Andy Thompson at a 4.5g/t Au lower cut off.

7. Resource estimated June 2006 by Spero Carras at a 1.3g/t Au lower cut off.

8. Resource estimated June 2006 by Spero Carras at a 3.0g/t Au lower cut off.

9. Resource estimated July 2006 by Steve Hyland at a 4.0g/t Au lower cut off.

10. Resource estimated July 2006 by Steve Hyland at a 1.0g/t Au lower cut off.

11. Resource estimated December 2005 by Richard Allan at a 2.5g/t Au lower cut off.

The information in this report that relates to Exploration Results is based on information compiled by Mr. Andrew Thompson who is an employee of the company. The information in this report that relates to Mineral Resources at the Calais, East Lode North and East Pit zones at Wiiluna, and the Wilsons deposit at Gidgee is based on information compiled by Mr. Andrew Thompson who is an employee of the company. The information in this report that relates to other Mineral Resources at Wiluna is based on information compiled by Mr. Paul Tan who is a former employee of Agincourt and Oxiana at Wiluna. The information in this report that relates to Mineral Resources other than the Wilsons deposit at Gidgee is based on information compiled by Mr. Spero Carras who is a consultant. The information in this report that relates to Mineral Resources at the Youanmi project is based on information compiled by Mr. Steve Hyland who is a consultant. The information in this report that relates to Mineral Resources at the Aphrodite deposit is based on information compiled by Mr. Richard Allan who is an employee of Barrick Gold. Mr. Thompson, Mr. Tan, Mr. Carras, Mr. Hyland and Mr. Allan are Members of the Australasian Institute of Mining and Metallurgy and have sufficient experience of relevance to the styles of mineralisation and the types of deposits under consideration, and to the activities undertaken, to qualify as Competent Persons as defined in the 2004 Edition of the Joint Ore Reserves Committee (JORC) Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves. Mr. Thompson, Mr. Tan, Mr. Carras, Mr. Hyland and Mr. Allan consent to the inclusion in this report of the matters based on information in the form and context in which it appears.

Reverse circulation (RC) drill samples are obtained by collecting meter samples via a three stage riffle or cone splitter, and diamond drill hole results are obtained from half NQ core or quarter HQ core sampled to geological boundaries where appropriate.

Assay results are obtained from Intertek (formerly known as Genalysis) and ALS Chemex Laboratories in Perth. Samples are prepared using single stage pulverization of the entire sample. Gold assays are obtained using a 30g or 50g lead collection fire assay digest and atomic absorption spectrometry (AAS) analysis techniques. Multi-element analyses (arsenic, sulphur, iron, lead, zinc, bismuth, antimony and tellurium) are obtained using a four acid total digest and inductively coupled plasma optical emission spectrometry (ICP OES) analysis techniques. Full analytical quality assurance – quality control(QAQC) is achieved using a suite of certified standards, laboratory standards, field duplicates, laboratory duplicates, repeats, blanks and grind size analysis. Assays quoted in announcements may be of a preliminary nature. Assays used in resource estimates have undergone full QAQC.

The spatial location of samples from surface holes is derived using a combination of surveyed grid co-ordinates and 3D differential GPS collar survey pickups, and Reflex single shot and gyroscopic downhole surveys. The spatial location of samples from underground holes is derived using surveyed rig setups and Reflex multi-shot downhole surveys. True widths are calculated using the mean dip and strike of the mineralization from 3D wireframe models and downhole surveys.

Quoted drill intersections are based on situation specific criteria, which include using a lower cutoff of 1g/t or 2g/t gold and acceptable levels of internal dilution.

Mineral Resources have been estimated using standard accepted industry practices. All Resources have been estimated via Block Ordinary Kriging using 1m composite samples. Top cuts have been applied to the composites and are considered appropriate for the nature and style of mineralization in all cases. Directional grade variography was modeled for all zones based on 1m composites. Geological and mineralization modeling has been achieved by 3D modeling of footwall and hangingwall structures (a lower 2g/t Au cutoff was applied in the case of Wilsons Deposit). Block models have been developed for both deposits incorporating a suitable parent and sub block dimension to allow adequate volume resolution of modeled geology and mineralization. Grade interpolation (via Block Ordinary Kriging) was then undertaken using a multiple estimation pass strategy.

Where quoted, Mineral Resource and Ore Reserve tonnes and ounces are rounded to appropriate levels of precision, causing minor computational errors.

Mineral Resources are classified on the basis of drillhole spacing, geological continuity and predictability, geostatistical analysis of grade variability, sampling, analytical, spatial and density QAQC criteria and demonstrated amenability of mineralization style to proposed processing methods.

For

per

sona

l use

onl

y

32Apex Minerals NL

Reserves Table as at 23 June 2008

Competent Person’s statement for Ore Reserves Estimates

Ore Reserves have been estimated in accordance with the guidelines defined in the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (The JORC Code, 2004 Edition).

The information in this report which relates to the Wiluna and Wilsons Underground Ore Reserves is based on and accurately reflects the information compiled by Mr Blair Duncan a consultant to Apex Minerals NL and Principal of Arbitrage Consulting Australia Pty Ltd. The information in this report which relates to the Wiluna Open Pit Ore Reserve is based on and accurately reflects the information compiled by Mr Linton Putland a consultant to Apex Minerals NL and Principal of Linton Putland and Associates Pty Ltd. Mr. Duncan and Mr. Putland are members of The Australasian Institute of Mining and Metallurgy (“AusIMM”) and have sufficient experience of relevance to the styles of mineralisation and the types of deposits under consideration, and to the activities undertaken, to qualify as a ‘Competent Person’ as defined in the 2004 Edition of the Joint Ore Reserves Committee (JORC) Australasian Code fro reporting of Exploration Results, Mineral Resources and Ore Reserves. Mr. Duncan and Mr. Putland consent to the inclusion in this report of the matters based on information in the form and context in which it appears.

Proved Probable Total

Ore Reserves000’s

tonnesGrade g/t Au

000’s oz Au

000’s tonnes

Grade g/t Au

000’s oz Au

000’s tonnes

Grade g/t Au

000’s oz Au

Wiluna u/g – Calais area 955 6.4 197 955 6.4 197

Wiluna East Lode pit 264 3.3 30 264 3.3 30

Wiluna total 1,219 5.8 227 1,219 5.8 227

Wilsons u/g 826 6.4 170 826 6.4 170

Total 2,045 6.0 397 2,045 6.0 397

For

per

sona

l use

onl

y

33Annual Report 08

For

per

sona

l use

onl

y

34Apex Minerals NL

Directors’ Report

The Directors present their report on the Company and its consolidated entity (referred to hereafter as the Group) for the year ended 30 June 2008.

DireCTorsThe names and details of the Company’s directors in office during the financial year and until the date of this report are as follows. Directors were in office for this entire period unless otherwise stated.

Mark Ashley – Managing DirectorFCMAHe is a Fellow of the Chartered institute of Management Accountants and has over 20 years experience in the resources industry.

in 1992, Mr Mark Ashley joined Forrestania Gold – which was subsequently acquired by Lionore in 1994 and was with the company through its emergence as a growing international nickel producer up until 31 March 2006. Mark who was a main board Director and Ceo of its Australian operations, left Lionore at that time to run Apex Minerals.

Within the prior three years, Mark is a Non-executive Director of Kagara Zinc and Metallica Minerals Limited, both AsX listed companies. He was also a Non-executive director for AsX listed company Tianshan Goldfields Limited appointed on 11 April 2006 and resigned on 7 september 2007. Mark is a Member of Council at the Curtin University of Technology and is a member of the university’s Finance Committee. He has also served as Chairman of the Major Gifts Committee for the royal Flying Doctor service and as a Director of the Australian Gold Council.

Glenn Jardine – Operations DirectorBEng FAusIMMMr Glenn Jardine has over 20 years experience in the mining industry and was most recently succeeded Mark Ashley as Managing Director of Lionore Mining international’s Australian operations, where he also held roles including Chief operating officer and prior to that, General Manager, New Business and Project Manager. During his time with Lionore Australia, Mr Jardine oversaw the successful development of the emily Ann, Maggie Hays and Waterloo nickel mines, leading teams whose work was subsequently recognised by the achievement of two separate major environmental awards.

Glenn graduated with a Be Mining from the University of Queensland in 1984 and is a member of the institute of Company Directors and a Fellow of the Aus iMM.

Within the prior three years, Mr Jardine has not been a director for any other public listed company.

Mark Bennett – Exploration DirectorBSc PhD MAusIMM FGSDr Bennett is a geologist with over 21 years experience, predominantly in gold, nickel and base metal exploration and mining. He holds a Bsc in Mining Geology from the University of Leicester, and a PhD from the University of Leeds, is a member of the Australasian institute of Mining and Metallurgy and an elected Fellow of the Geological society of London.

Mark has worked in europe, West Africa, and Australia, and has spent much of his career working for WMC resources and Lionore in Australia. Previous positions held include exploration Manager and Chief Geologist, including periods at WMC’s Kambalda Nickel operations, Gold Fields’ st.ives Gold Mines, Forrestania Gold’s Bounty Gold Mine, and WMC’s Melbourne head office.

in 2002, Mark received the Association of Mining and exploration Companies (AMeC) Prospector of the Year award in recognition of his contribution to the discovery of the Thunderbox gold and the Waterloo nickel deposits.

Within the prior three years, Mr Bennett has not been a director for any other public listed company.

Stephen Lowe – Non Executive DirectorBBus (ECU) GradDipAdvTax (UNSW) MTax (UNSW) FTIA MAICDMr stephen Lowe is a taxation specialist with over 15 years experience consulting to a wide range of corporate and private clients on a broad range of taxation issues including mining and international matters, GsT and CGT. He is a director of AsX listed Croesus Mining NL. He is also a director of the Perth based specialist taxation firm MKT – Taxation Advisors and has been a director of several other public unlisted companies. His qualifications include a Bachelor of Business, Post-Graduate Diploma in Advanced Taxation and a Master of Taxation from the University of New south Wales. steve is a Fellow of the Taxation institute of Australia and a Member of the Australian institute of Company Directors.

Within the prior three years Mr Lowe has not been a director of any other publicly listed company.

Kim Robinson – Non Executive ChairmanBSc (Geology)Mr Kim robinson is a founding Director of Kagara Zinc Limited and its current executive Chairman. Mr robinson graduated from the University of Western Australia in 1973 with a degree in Geology and has 29 years experience in the minerals exploration and mining industries, including 10 years as executive Chairman of Forrestania Gold NL. Mr robinson is also the Non-executive Chairman of Metex resources Ltd.

For

per

sona

l use

onl

y

35Annual report 08

Directors’ Report continued

Todd Bennett – Non Executive Director (appointed 18 July 2008)Mr Todd Bennett is the Managing Director of AMB Holdings, a private investment company associated with the Bennett family. Mr Bennett oversees the management of a broad portfolio of assets, which includes a significant share in the rhodes ridge iron ore project in the Pilbara, and AMB’s strategic relationships with the rio Tinto Group. Mr Bennett holds an MBA from The University of Western Australia (UWA) and is also an executive Director of unlisted Finance and energy exchange (FeX) a premium provider of energy and financial derivatives with a focus on Asia.

CoMPANY seCreTArY

Graham AndersonBBus CAMr Graham Anderson is a graduate of Curtin University and has over 20 years’ commercial experience as a Chartered Accountant. He operates his own specialist accounting and management consultancy practise, providing a range of corporate advisory services to both public and private companies. From 1990 to 1997 he was an audit partner at Duesburys and from 1997 to 1999 he was an audit partner at Horwath Perth. He is currently Director and Company secretary of APA Financial services Limited, echo resources Limited, Pegasus Metals Limited, Dynasty Metals Limited and Company secretary of Catalpa resources Ltd, iron road Limited, Westonia Mines Limited and Mamba Minerals Limited.

PriNCiPAL ACTiviTiesThe principal activity of the Group during the financial year was exploration for mineral resources.

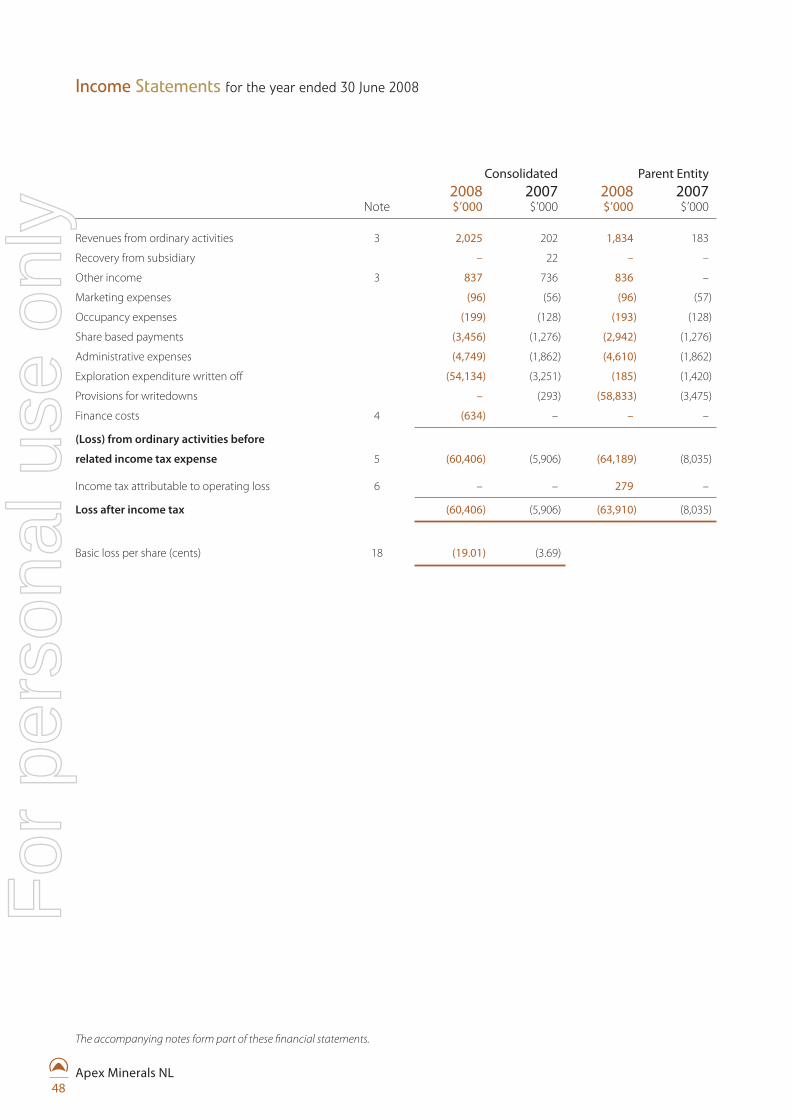

resULTsThe consolidated loss for the year after income tax was $60,406,355 (2007 $5,906,489).

oPerATiNG revieWDuring the year ended 30 June 2008, the Company completed the following acquisitions:

• The Gidgee Gold Project, located 640 kilometres northeast of Perth and covering 90 kilometres of strike of the Gum Creek greenstone belt, comprising a total JorC compliant resource inventory of 490,000 ounces gold, including the Wilsons refractory gold deposit (Current resource: 734,000t @ 6.9g/t for 164,000oz), a 600,000 tpa gold treatment plant (currently not in operation), a 150 man camp, additional high-grade non-refractory resources close to the existing developments, and significant exploration upside;

• The Youanmi Gold Project, located 480 kilometres northeast of Perth and covering 40 kilometres of strike of the Youanmi shear zone, with a total JorC and Ni 43-101 compliant resource inventory of 951,000 ounces of gold, including the Youanmi Deeps refractory gold deposit (indicated and inferred resource of 2.4 million tonnes @ 8.5 g/t for 658,000 ounces of gold) plus a 600,000 tpa gold treatment plant, a 270,000tpa sulphide flotation plant and a Bactech bacterial oxidation treatment plant capable of treating the gold concentrate (currently not in operation) from TsXv-listed Goldcrest resources Ltd; and

• The Aphrodite Gold Project, located 65 kilometres north of Kalgoorlie and covering 51 square kilometres of the Bardoc Tectonic Zone, comprising a refractory gold deposit with a JorC compliant inferred resource of 1.44 million tonnes @ 6.2 g/t for 287,000 ounces of gold as well as a significant inventory of unclassified gold mineralisation, from Barrick (PD) Australia Limited; and

• The Wiluna Gold Project is situated 1,000 kilometres northeast of Perth and comprises granted mining leases covering approximately 50 square kilometres, as well as miscellaneous licences. The operation has access to the Goldfields Gas Pipeline and includes gold resources totalling over 700,000 ounces (see Table 1), a ~1Mtpa processing facility and a BioX® bacterial oxidation plant, along with other established infrastructure.

Further details in relation to the projects above are contained in announcements lodged with the AsX.

The Project implementation study was completed in June 2008 at which point project development commenced at the Wiluna Gold Project. The site has been kept under active care and maintenance immediately following its acquisition. Mining is scheduled to begin at Wiluna (underground) and east Pit (open pit) in october 2008 with ore being immediately accessible from these two sources. At the same time, decline development is scheduled to begin towards new zones at Wiluna and at Wilsons (Gidgee), where first ore is expected to be mined in February 2009. Commercial production is scheduled to begin in the first quarter of 2009 following a ramp-up phase.

siGNiFiCANT CHANGes iN THe sTATe oF AFFAirsDuring the financial year the Company raised $117,569,879 less capital raising costs of $6,683,602 on the issue of 147,755,445 shares.

other than the above there were no significant changes in the state of affairs of the Company during the financial year, not otherwise disclosed in the attached financial report.

For

per

sona

l use

onl

y

36Apex Minerals NL

Directors’ Report continued

LiKeLY DeveLoPMeNTsThe Group will continue to develop, explore and assess its mineral projects and will also consider new projects that could provide growth for shareholders.

Further information on the likely developments and expected results of operations of the Group have not been included in this report because the directors believe it would be likely to result in unreasonable prejudice to the Group.

DiviDeNDsNo dividends have been paid during the year and the Directors have not recommended that any dividend be paid.

eveNTs sUBseQUeNT To rePorTiNG DATeon 7 July 2008, an announcement was made on the AsX that the Company was to be a substantial holder in empire resources Ltd. A total of 5,000,000 shares was purchased at 17 cents each and also entered into a signed Memorandum of Understanding thus giving the right to the Company to nominate a representative to join the empire Board of Directors.

on 18 July 2008, it was released to the AsX that the Company had appointed Todd Bennett to the Board as a Non-executive Director, further strengthening the Company’s access to international resource industry investors and project developers. Mr Bennett is the Managing Director of AMB Holdings, a private investment company associated with the Bennett family. Mr Bennett oversees the management of a broad portfolio of assets, which includes a significant share in the rhodes ridge iron ore project in the Pilbara, and the AMB’s strategic relationships with the rio Tinto Group.

on 3 August 2008, two partly paid shareholders had fully paid the remainder of their shares totalling $120,940 (605,000 shares at $0.1999). The total number of partly paid shares remaining is 19,125,000.

on 29 september 2008, the Group raised $58,500,000 gross of costs through the issue of Notes, Gold Upside Participation (“GUP”) Notes and Unsecured Warrants to investors.

The Notes have a coupon of 11.25% and a 3 year term. The GUP Notes are based on a floor price as at the date of and are for 500,000 units. The Warrants are exercisable at 33.5 cents and expire after 5 years. More details are contained in the offering Circular lodged with the AsX.

Options Issuedon 18 July 2007, the Company issued to:

(a) an entity associated with Director of the Company, Mark Ashley, 500,000 unlisted options in the Company, and

(b) an entity associated with Director of the Company, Mark Bennett, 500,000 unlisted options in the Company; and

(c) Director of the Company, Glenn Jardine, 1,000,000 unlisted options in the Company; and

(d) Non-executive Director of the Company, stephen Lowe, 300,000 unlisted options in the Company; and

(e) Non-executive Director of the Company, Kim robinson, 300,000 unlisted options in the Company, pursuant to a resolution of shareholders at general meeting. each option is exercisable at $0.65 and expires on 1 June 2012.

on 31 July 2007, the Company issued 2,050,000 options exercisable at $1.00 expiring 30 July 2012 pursuant to the Company’s employee share option Plan.

on 16 october 2007, the Company issued 350,000 options exercisable at $1.30 expiring 15 october 2012 pursuant to the Company’s employee share option Plan.

on 31 october 2007, the Company issued 200,000 options exercisable at $1.30 expiring 30 october 2012 pursuant to the Company’s employee share option Plan.

on 12 November 2007, the Company issued 350,000 options exercisable at $1.30 expiring 11 November 2012 pursuant to the Company’s employee share option Plan.

on 11 January 2008, 75,000 unlisted options that were issued pursuant to the Company’s employee share option Plan lapsed due to the relevant employees ceasing employment with the Company.

on 11 January 2008, the Company issued 50,000 options exercisable at $1.60 expiring 10 January 2013 pursuant to the Company’s employee share option Plan.

on 28 April 2008, the Company issued to:

(a) an entity associated with Director of the Company, Mark Bennett, 350,000 unlisted options in the Company; and

(b) a Director of the Company, Glenn Jardine, 350,000 unlisted options in the Company,

pursuant to a resolution of shareholders at general meeting. each option is exercisable at $1.30 and expires on 27 April 2013.

on 12 May 2008, the Company issued 1,911,000 options exercisable at $1.30 expiring on 11 May 2013 pursuant to the Company’s employee share option Plan.

on 20 June 2008, the Company issued 600,000 options exercisable at $1.30 expiring on 19 June 2013 pursuant to the Company’s employee share option Plan.

on 30 June 2008, the Company cancelled 50,000 unlisted options in the Company. The options had been exercisable at $1.30 expiring 19 June 2013.

on 18 July 2008, the Company issued 1,000,000 options exercisable at $0.70 expiring on 18 July 2013.

since 30 June 2008, the Directors are not aware of any other matter or circumstance that has significantly or may significantly affect the operations of the Company or the results of those operations, or the state of affairs of the Company in subsequent financial years.

For

per

sona

l use

onl

y

37Annual report 08

Directors’ Report continued

DireCTors’ iNTeresTsThe relevant interest of each director in the shares, debentures, interests in registered schemes and rights or options over such instruments issued by the companies within the Group and other related bodies corporate, as notified by the directors to the Australian securities exchange in accordance with s205G(1) of the Corporations Act 2001, at the date of this report is as follows:

Apex Minerals NL

Fully Paid shares options

M Ashley Direct – –

indirect 16,800,000 2,500,000

M Bennett Direct – –

indirect 1,472,471 2,850,000

G Jardine Direct 2,315,000 2,850,000

indirect – –

K robinson Direct 5,800,000 1,300,000

indirect – –

s Lowe Direct 186,201 800,000

indirect – –

T Bennett Direct 255,000 –

indirect – –

MeeTiNGs oF DireCTorsThe following table sets out the number of meetings of the Company’s Directors held during the year ended 30 June 2008.

There were a total of 6 Director’s Meetings held during the year.

Number eligible to Attend

Number Attended

Director

M Ashley 6 6

M Bennett 6 6

G Jardine 6 6

K robinson 6 6

s Lowe 6 6

reMUNerATioN rePorT (AUDiTeD)This remuneration report outlines the director and executive remuneration arrangements of the Company and the Group in accordance with the requirements of the Corporations Act 2001 and its regulations.

Details of key management personnel (including the five highest executives of the Company and the Group):

• Mark Ashley – Managing Director

• Mark Bennett – exploration Director

• Glenn Jardine – operations Director

• Grant Brock – Chief operating officer

• Anna Neuling – Chief Financial Controller

• William Dix – exploration Manager

Directors’ and Executives Emolumentsremuneration and other terms of employment of executives, including executive directors, are reviewed periodically by the Board having regard to performance, relevant comparative information and, where necessary, independent expert advice. remuneration packages which can include bonuses are set at levels that are intended to attract and retain executives capable of managing the Company’s operations.

Bonuses are paid at the discretion of the Board and currently are not directly linked to any key performance indicators.

The terms of engagement and remuneration of executive directors is reviewed periodically by the Board, with recommendations being made by the non-executive director. Where the remuneration of a particular executive director is to be considered, the director concerned does not participate in the discussion or decision-making.

The policy of the Company is to pay remuneration of directors and senior executives in cash and in amounts in line with employment market conditions relevant in the mining industry. Minor amounts of employee fringe benefits in the form of employee meals and entertainment are provided as a part of the executives’ way of conducting business.

The Company’s performance, and hence that of its directors and executives, is measured in terms of:

(i) Company share price growth;

(ii) Cash raised;

(iii) exploration carried out; and

(iv) Farm-in expenditure attracted.

For

per

sona

l use

onl

y

38Apex Minerals NL

reMUNerATioN rePorT (AUDiTeD) continued

Directors’ and Executives Emoluments continuedThe emoluments of each Director and Key executive were as follows:

short term employee benefits Post employment benefitsshare based

payments

Percentage of remuneration by options %

Performance related %

salary and Directors’

Fees $ Bonuses $other

services $

Non-Monetary Benefits $

super-annuation $

retirement Benefit $ options $ Total $

Director

M Ashley

2008 300,000 100,000 – 31,720 36,000 – 400,357 868,077 46% 12%

2007 298,495 – – – 24,750 – 249,032 572,277 44% 0%

M Bennett

2008 304,167 100,000 – 34,525 36,375 – 415,178 890,245 47% 11%

2007 257,336 – – – 21,591 – 249,032 527,959 47% 0%

G Jardine

2008 304,167 100,000 – – 36,375 – 517,059 957,601 54% 10%

2007 29,375 – – – 2,250 – – 31,625 0% 0%

K robinson

2008 45,628 – – – 6,665 – 225,019 277,312 81% 0%

2007 28,424 – – – – – 118,891 147,315 81% 0%

s Lowe

2008 36,002 – – – 1,620 – 171,032 208,654 82% 0%

2007 33,511 – 9,293 – – – 59,445 102,249 58% 0%

s stone

2008 – – – – – – – – 0% 0%

2007 8,308 – – – – – 116,383 124,691 93% 0%

Total

2008 989,964 300,000 – 66,245 117,035 – 1,728,645 3,201,889

2007 655,449 – 9,293 – 48,591 – 792,783 1,506,116

Key Executives

G Anderson

2008 – – 66,000 – – – 32,823 98,823 33% 0%

2007 – – 66,000 – – – 2,798 68,798 4% 0%

G Brock

2008 137,820 – – – 2,250 – 3,086 143,156 2% 0%

2007 – – – – – – – – 0% 0%

A Neuling

2008 146,154 20,000 – 6,725 14,602 – 66,855 254,336 26% 8%

2007 – – – – – – – – 0% 0%

W Dix

2008 157,500 30,000 – 25,326 16,875 – 173,576 403,277 43% 7%

2007 – – – – – – – 0% 0%

Total

2008 441,474 50,000 66,000 32,051 33,727 – 276,340 899,592

2007 – – 66,000 – – – 2,798 68,798

Directors’ Report continued

For

per

sona

l use

onl

y

39Annual report 08

reMUNerATioN rePorT (AUDiTeD) continued

Directors’ and Executives Emoluments continued

Employment BenefitsThe details of the executive employment contracts are as follows:

The Managing Director, Mark Ashley, current employment contract is a 3 year contract that commenced on 18 April 2006 and terminates on 17 April 2009, unless earlier terminated in accordance with this agreement. Upon the expiration of the term of this agreement, the executive’s appointment will continue on the same terms as this agreement unless the agreement is terminated in accordance with its terms. Under the terms of the present contract:

• Mr Ashley will be paid a minimum remuneration package of $300,000p.a. base salary plus superannuation. The Company will also provide a motor vehicle to the value of $65,000 and will be responsible for costs associated with the maintenance, licensing, running of and repairs to the vehicle together with any fringe benefits tax payable in relation to the vehicle.

• The Company may terminate this agreement by not less than three months’ notice in writing if the executive becomes incapacitated by illness or accident for an accumulated period of three months or the Company is advised by an independent medical officer that the executive’s health has deteriorated to a degree that it is advisable for the executive to leave the Company. on termination on notice by the Company, the Company is obliged to pay the executive a six month service fee.

• The Company may terminate the contract at any time without notice if serious misconduct has occurred. on termination with cause, the executive is not entitled to any payment.

The exploration Director, Mark Bennett, current employment contract is a 3 year contract that commenced on 9 May 2006 and terminates on 8 May 2009, unless earlier terminated in accordance with this agreement. Upon the expiration of the term of this agreement, the executive’s appointment will continue on the same terms as this agreement unless the agreement is terminated in accordance with its terms. Under the terms of the present contract:

• Mr Bennett will be paid a minimum remuneration package of $350,000p.a. base salary plus superannuation. The Company will also provide a motor vehicle to the value of $65,000 and will be responsible for costs associated with the maintenance, licensing, running of and repairs to the vehicle together with any fringe benefits tax payable in relation to the vehicle.

• The Company may terminate this agreement by not less than three months’ notice in writing if the executive

becomes incapacitated by illness or accident for an accumulated period of three months or the Company is advised by an independent medical officer that the executive’s health has deteriorated to a degree that it is advisable for the executive to leave the Company. on termination on notice by the Company, the Company is obliged to pay the executive a six month service fee.

• The Company may terminate the contract at any time without notice if serious misconduct has occurred. on termination with cause, the executive is not entitled to any payment.

The operations Director, Glenn Jardine, current employment contract is a contract that commenced on 31 May 2007. Upon the expiration of the term of this agreement, the executive’s appointment will continue on the same terms as this agreement unless the agreement is terminated in accordance with its terms. Under the terms of the present contract:

• Mr Jardine will be paid a minimum remuneration package of $350,000p.a. base salary plus superannuation.