Embed Size (px)

Citation preview

Annual Report2008

Level 3 Hyatt Centre123 Adelaide TerraceEast Perth WA 6004

GPO Box 2606Perth WA 6001

Telephone: +61 8 9220 5700Facsimile: +61 8 9220 5757Email: [email protected]: www.metalsx.com.au

For

per

sona

l use

onl

y

1

Corporate Directory

DirectorsPeter J Newton (Chairman)Peter G Cook (Managing Director)Warren S HallamD Mark OkebyMichael L JefferiesWang WeiYimin Zhang (Alternate for Wang Wei)

Company SecretaryFiona Van Maanen

Key ManagementScott J Huffadine (Chief Operating Offi cer)Duncan J Coutts (Chief Development Offi cer)Paul M Cmrlec (GM – Central Musgrave Project)

Share RegistrySecurity Transfer Registrars Pty Ltd770 Canning HighwayAPPLECROSS WA 6153

Phone: 61-8-9315 2333Fax: 61-8-9315 2233E-mail: [email protected]

Registered Offi ceLevel 3, Hyatt Centre123 Adelaide TerraceEAST PERTH WA 6004

Phone: 61-8-9220 5700Fax: 61-8-9220 5757E-mail: [email protected]: www.metalsx.com.au

Postal AddressGPO Box 2606PERTH WA 6001

Securities ExchangeListed on the Australian Securities Exchange

Codes: MLX and MLXO

Domicile and Country of IncorporationAustralia

For

per

sona

l use

onl

y

2

Table of Contents

Corporate Directory 1

Chairman’s Letter 3

Managing Director’s Report 4

Director’s Report 17

Auditor’s Independence Declaration 38

Corporate Governance Statement 39

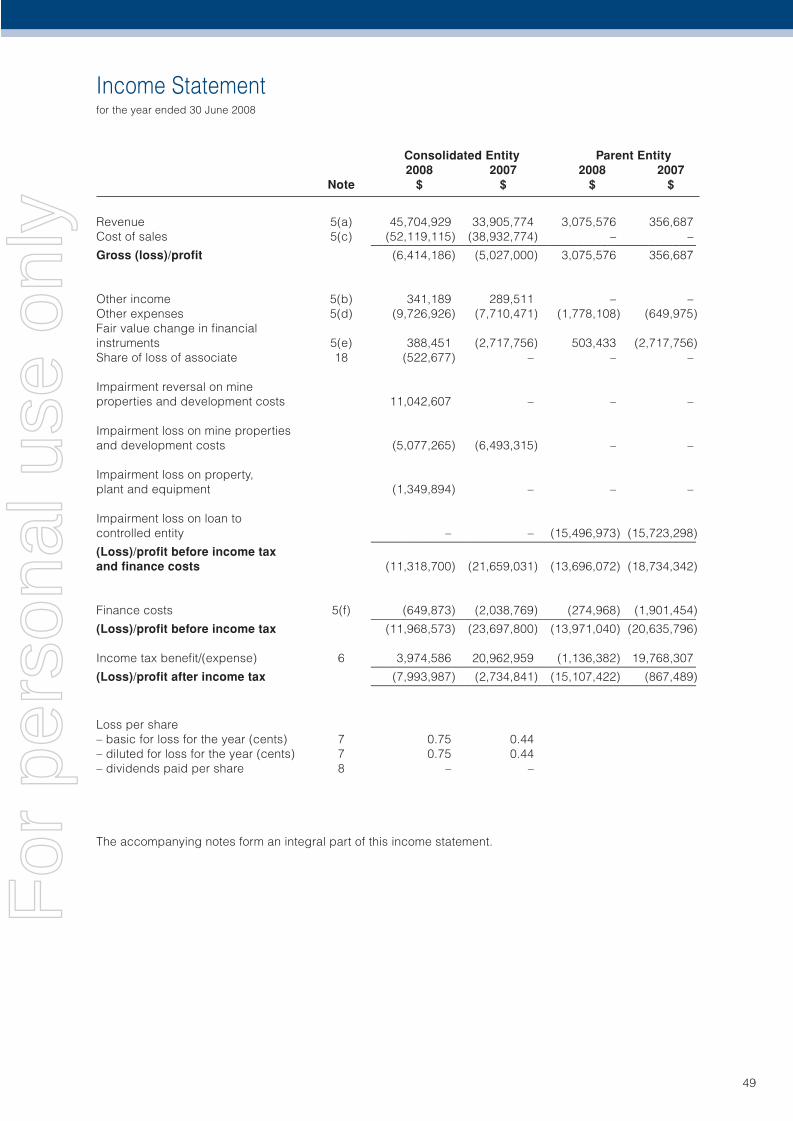

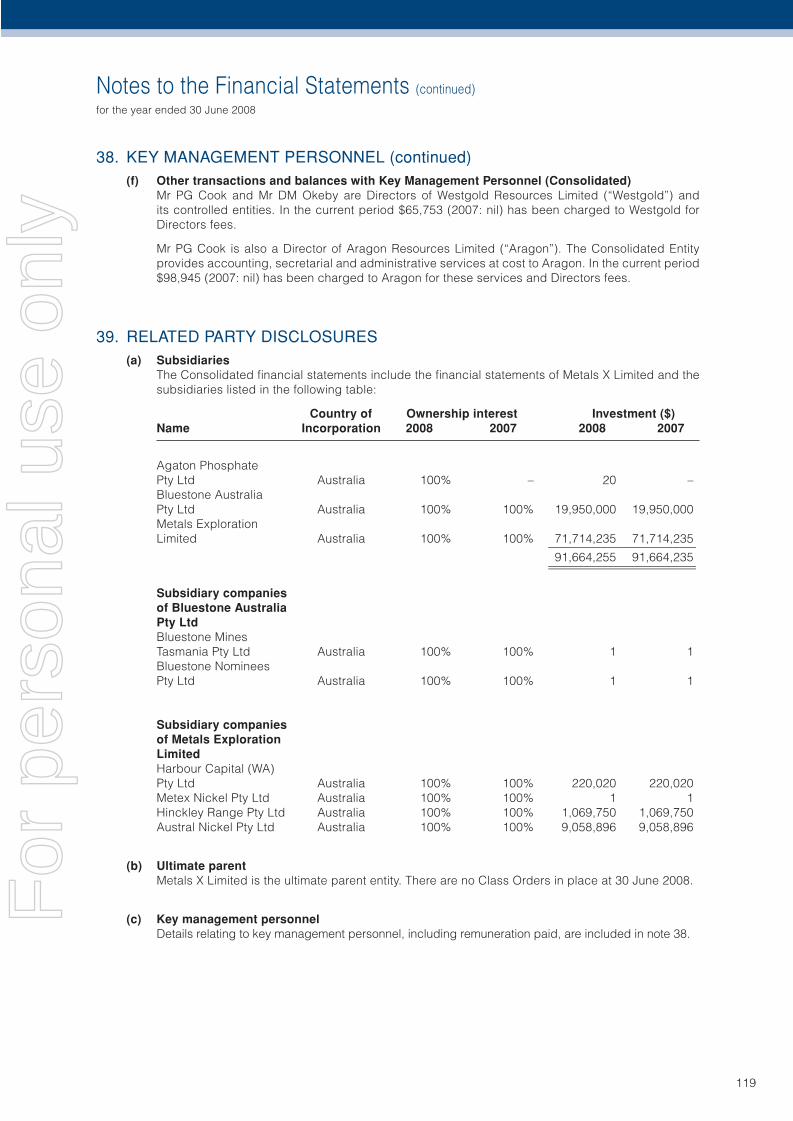

Income Statement for the year Ended 30 June 2008 49

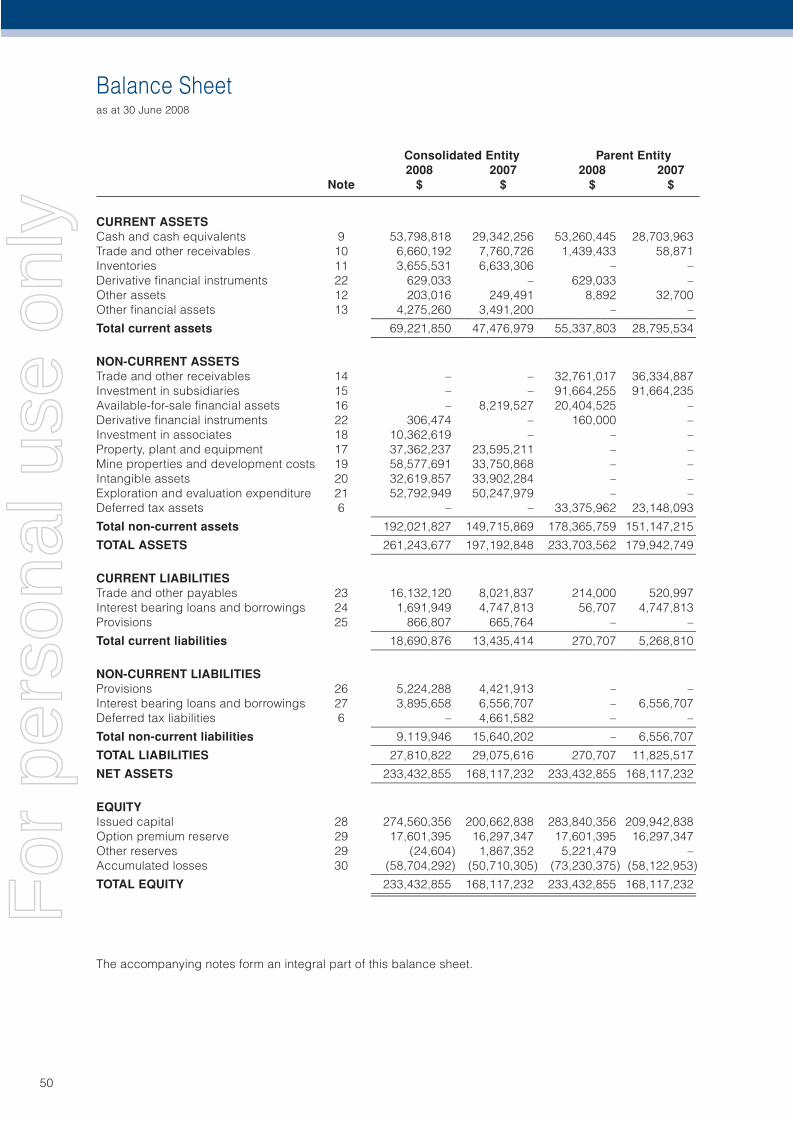

Balance Sheet as at 30 June 2008 50

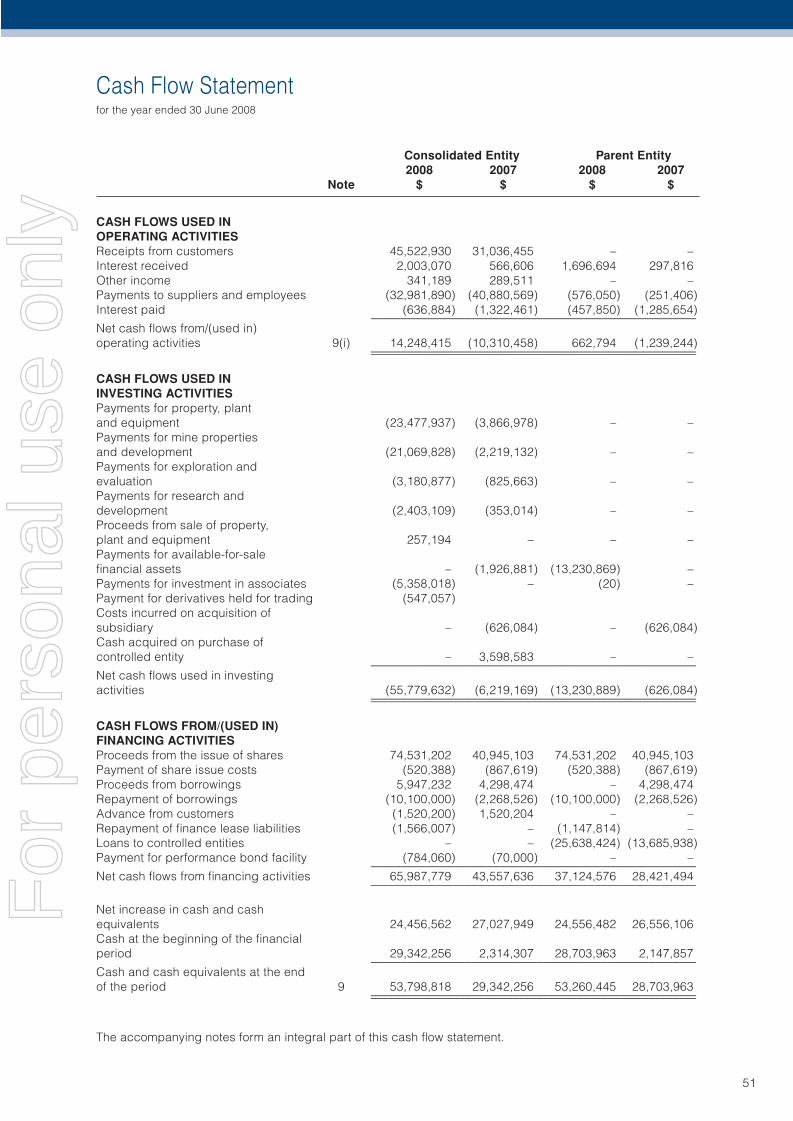

Cash Flow Statement for the Year Ended 30 June 2008 51

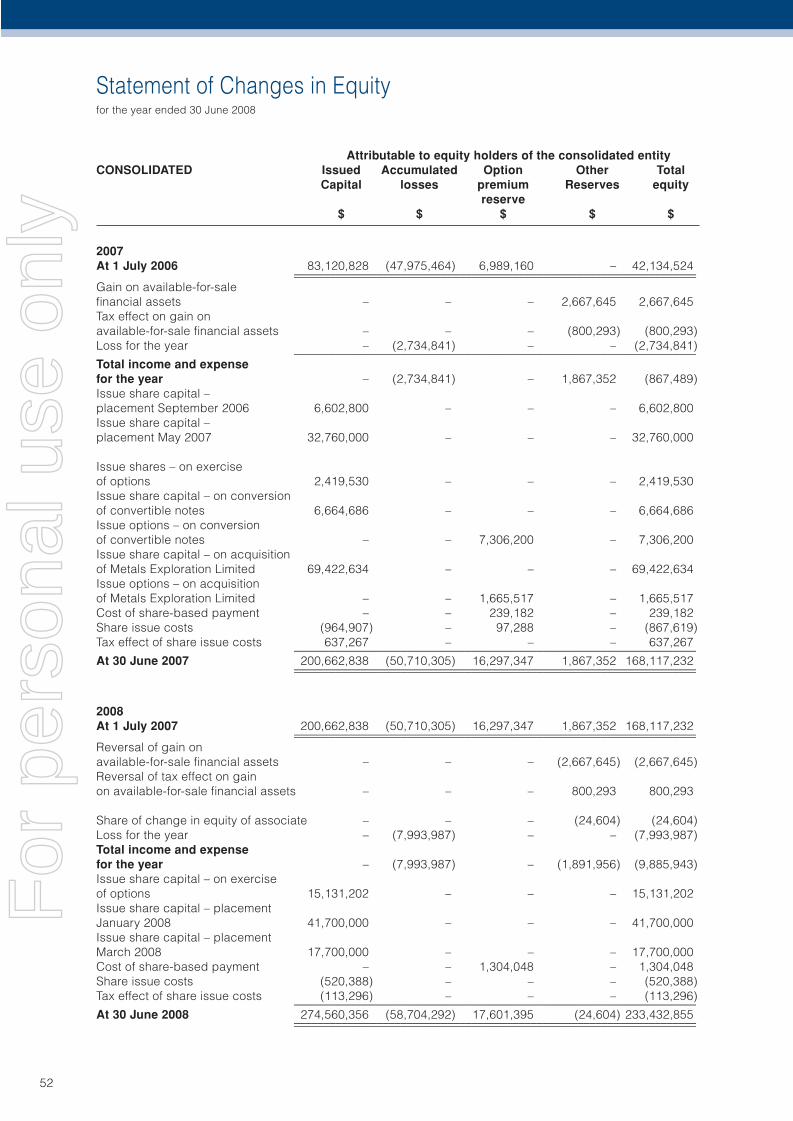

Statement of Changes in Equity for the Year Ended 30 June 2008 52

Notes to the Financial Statements for the Year Ended 30 June 2008 54

Director’s Declaration 121

Independent Audit Report 122

Security Holder Information as at 22 September 2008 124

Summary of Mining Tenements as at 22 September 2008 126

For

per

sona

l use

onl

y

Chairman’s Letter

3

Dear Shareholders

I present to you the Metals X Limited (“Metals X” or “the Company”) Annual Report for the period ending 30 June 2008.

The fi nancial year just past has been one of signifi cant progress for Metals X.

The Board continued with its diversifi cation strategy and the Company has now positioned itself as a truly diversifi ed explorer and developer of Australian resource projects.

Our strategic decisions to maintain our core focus on the tin and nickel industries has been vindicated by these two metals, specifi cally Tin, climbing its way to be amongst the highest priced commodities on the LME.

Capital raisings of $59.4 million dollars mid-way through the fi nancial year resulted in a signifi cant strengthening of our balance sheet and cash reserves which has funded the growth plans of the company.

We closed the smaller and struggling Collingwood Tin Project during the year to focus on the larger and more signifi cant Renison.

We re-started our expanded Renison Tin project in early 2008 and at the time of writing we are building up to full capacity. We commenced mining at Mt Bischoff in March 2008 and underground mining from the Renison Bell mine in May 2008 and a signifi cant stockpile of ore was available for the commencement of operations. Renison will in 2008/2009 emerge as a tin and copper producer and in addition to being the largest tin producer in Australia, the project will build to become a signifi cant player in the world tin market.

The phase 1 feasibility study on Wingellina was completed and confi rmed that the project is capable of materialising to be a major and long term nickel-cobalt producer. The signifi cant value of this project has not been missed by Jinchuan Group Limited, China’s largest nickel producer and for that matter by APAC Resources Ltd (HK1104) who have emerged as our largest single shareholder. Both of these companies are focussed on the potential and long term benefi ts that will come from the development of Wingellina. We are grateful and appreciative of their support and commitment to the Wingellina Project and the Company.

During the year we have diversifi ed our exploration with brownfi elds exploration in and around our existing key projects and additional greenfi elds exposure through signifi cant shareholdings in Westgold Resources Limited (“Westgold”), Aragon Resources Limited (“Aragon”) and Agaton Phosphate Pty Ltd (“Agaton”). These have given the group excellent exploration projects and exposure to gold, copper, lead, zinc, silver, uranium and phosphates. Each of these entities has delivered strong exploration results from their specialised areas and we expect some of these projects to turn into development projects in future years.

We look forward to the ensuing fi nancial year as one that will see the company evolve as a miner with strong earnings and further enhanced growth prospects.

On behalf of my Board, I would like to thank senior management and employees for their contribution to the Company’s activities and the Company’s shareholders for their continued support.

Peter NewtonChairmanF

or p

erso

nal u

se o

nly

Managing Director’s Report

4

Strategic Review

Metals X has in the past 12 months re-positioned itself from a specialist tin company to a much larger and diversifi ed group with a strong portfolio of assets at all phases of the mining cycle with exposure to many metals.

The Company’s largest exposure is to both tin and nickel, but through our strategic investments in Westgold and Aragon we have added lead, zinc, copper, gold and uranium to our portfolio. As opposed to previous years where the merits of one metal could refl ect heavily on our share price, we now carry a portfolio of metals and remain strongly positioned to benefi t from longevity and the inevitable volatility of the demand for metals.

We view the driver for the demand for metals as a direct result of the world entering a major industrialisation phase. Unlike other industrial revolutions that have set the path and prosperity for life as we know it, this industrial revolution directly involves one-third of the worlds population. The unprecedented economic growth in China and India has resulted in strong demand on the supply and pricing of the world’s resources, goods and services.

There will inevitably be fl uctuations and volatility in consumption and growth rates for metals. We have a world where the dynamics of Chinese and Indian growth will clash with a sophisticated western-world trading platform where many feed from volatility and trade patterns and information fl ows which perpetuate it as a healthy necessity of mature markets. In the backdrop of all this we will have witnessed unprecedented growth in demand and capacity building for the long term supply of metals to feed the hungry Asian dragons.

Not all metals will go up at the same time, at the same rate or stay up for the same periods. Consumption patterns in an industrialisation process are varied. As the process matures and industrialisation moves to urbanisation and thence westernisation, demand for metals will change and consumption patterns and sustainable demand for resources will be determined.

Metals X has attempted to position itself with key exposure to those metals that it believes will have sustainable demand and have the weakest supply side capabilities.

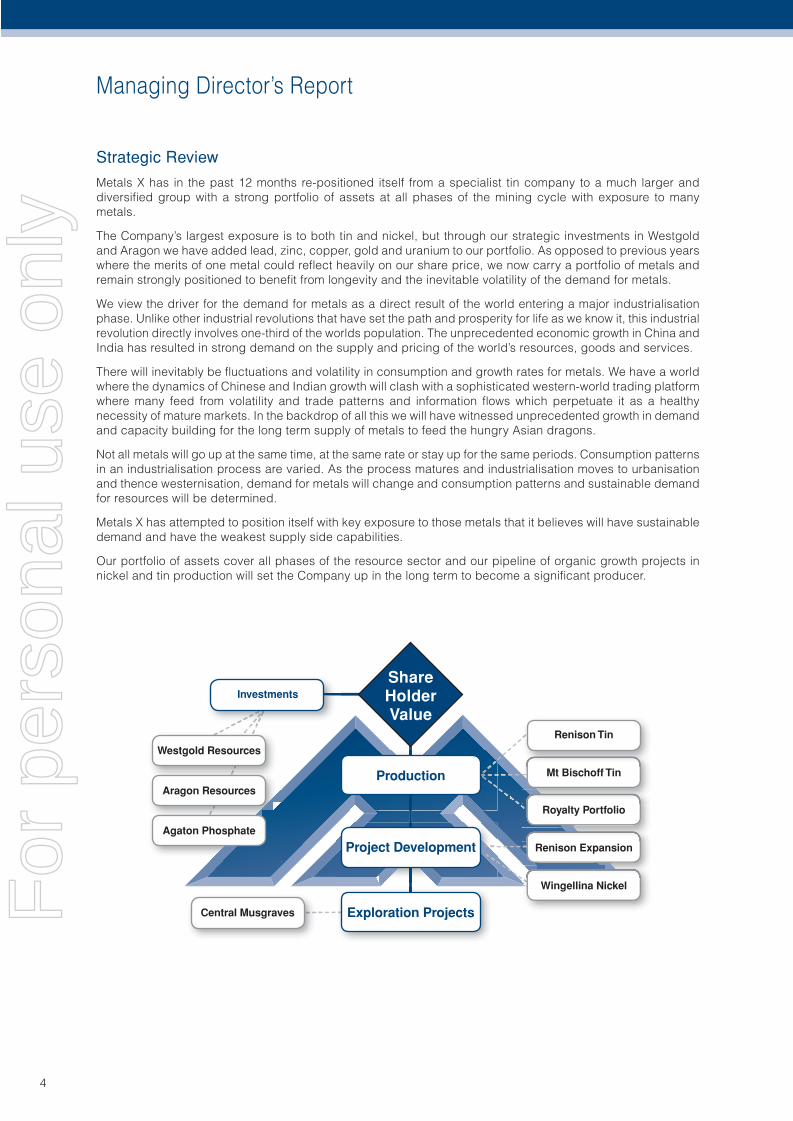

Our portfolio of assets cover all phases of the resource sector and our pipeline of organic growth projects in nickel and tin production will set the Company up in the long term to become a signifi cant producer.

ShareHolderValue

Production

Investments

Westgold Resources

Aragon Resources

Agaton Phosphate

Central Musgraves

Wingellina Nickel

Renison Expansion

Royalty Portfolio

Mt Bischoff Tin

Renison Tin

Project Development

Exploration ProjectsFor

per

sona

l use

onl

y

Managing Director’s Report (continued)

5

NICKEL DIVISION

The group’s nickel division has two key components:

1. The Central Musgrave Project (including Wingellina);2. A Nickel Royalty Portfolio.

Central Musgrave Project

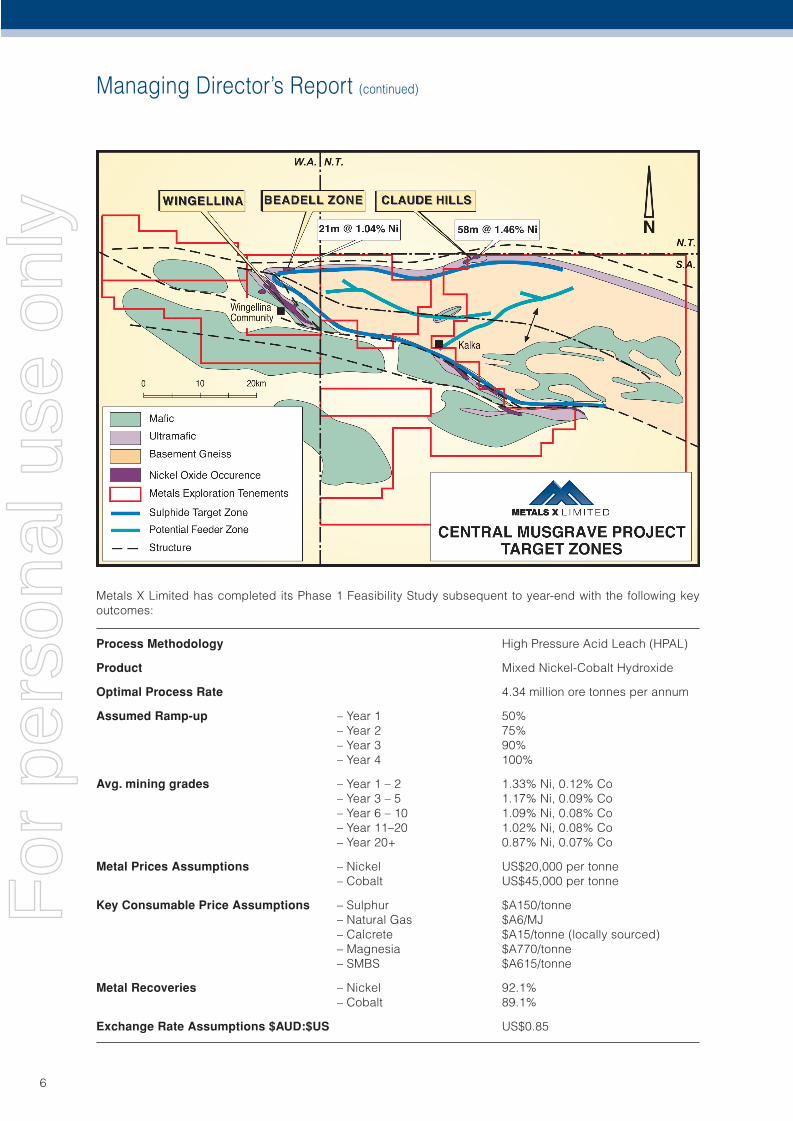

The Central Musgrave Project (“CMP”) consists of 1785km² of exploration titles in Western Australia and South Australia covering the Giles complex intrusives of the Musgrave block in central Australia. The CMP straddles the triple-point of the WA/NT/SA borders. Key geological units are Giles Complex ultramafi c and mafi c layered intrusives, which are known to host nickel and copper sulphides mineralsiation. Of signifi cance, oxidised derivatives of these ultramafi c rocks forms nickel and cobalt rich limonite mineralization, especially at the Wingellina Prospect.

The Wingellina Prospect is located in Western Australia on EL 69/355 within Aboriginal Reserve 17614.

Nickeliferous limonites in weathered ultramafi c rocks of the Giles complex were discovered at Wingellina in 1955. Exploration and mining access to the area was lost between 1971 and 2000 after developers and landowner representatives failed to reach agreement. Land access agreements between Acclaim Exploration NL (“Acclaim”) and the traditional owners were reached in 2001. A small amount of exploration work was completed by Acclaim from 2001 to 2004.

Metals X entered the project in March 2005 by entering an agreement with Acclaim to earn an 80% interest in the project by free carrying Acclaim to the completion of a bankable feasibility study.

In late March 2006, Metals X acquired all remaining interests in the project area from Acclaim.

Metals X has been undertaking detailed investigations at the Wingellina Project since early 2005. The work has included a signifi cant amount of resource defi nition drilling and evaluation. Identifi ed Mineral Resource estimates have been completed. The Identifi ed Mineral Resource estimate defi nes a body containing nearly 1.8 million tonnes of nickel metal, 139,000 tonnes of Cobalt metal and 60.3 million tonnes of Fe.

A summary of the Identifi ed Mineral Resource estimate at a 0.5% Ni lower cut-off grade is tabulated below:

Total Identifi ed Mineral Resource Estimate– 0.5% Ni (cut-off)

Class Million Tonnes Ni Co Fe2O3

Measured 68,847 1.00 0.078 48.71 Indicated 98,623 0.97 0.075 46.39 Inferred 15,727 0.97 0.069 42.73

Grand Total 183,197 0.98 0.076 46.95

In April 2007 Metals X completed a scoping study for the Wingellina project considering both technical and economic factors. Key outcomes of the scoping study concluded that the project should advance to feasibility study.

The Board of Metals X established a project team and commissioned the Feasibility Study assessment to be completed in two phases:

The purpose of the Phase 1 feasibility study was to:

• Identify all project requirements, and to investigate development options with the mixed nickel-cobalt hydroxide processing route selected following the scoping study;

• Select the optimal development option in each of the major project disciplines (mining, processing, infrastructure, etc);

• Complete engineering design for the selected option in each of the project disciplines to the level of detail required to produce a reliable capital development cost estimate with a maximum variance of ±25%;

• Complete an operating cost estimate with a maximum variance of ±25% in any of the individual project disciplines; and

• Defi ne work programs for subsequent development stages of the project.

Outcropping nickeliferous ochre at Wingellina

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

6

Metals X Limited has completed its Phase 1 Feasibility Study subsequent to year-end with the following key outcomes:

Process Methodology High Pressure Acid Leach (HPAL)

Product Mixed Nickel-Cobalt Hydroxide

Optimal Process Rate 4.34 million ore tonnes per annum

Assumed Ramp-up – Year 1 50% – Year 2 75% – Year 3 90% – Year 4 100%

Avg. mining grades – Year 1 – 2 1.33% Ni, 0.12% Co – Year 3 – 5 1.17% Ni, 0.09% Co – Year 6 – 10 1.09% Ni, 0.08% Co – Year 11–20 1.02% Ni, 0.08% Co – Year 20+ 0.87% Ni, 0.07% Co

Metal Prices Assumptions – Nickel US$20,000 per tonne – Cobalt US$45,000 per tonne

Key Consumable Price Assumptions – Sulphur $A150/tonne – Natural Gas $A6/MJ – Calcrete $A15/tonne (locally sourced) – Magnesia $A770/tonne – SMBS $A615/tonne

Metal Recoveries – Nickel 92.1% – Cobalt 89.1%

Exchange Rate Assumptions $AUD:$US US$0.85

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

7

The feasibility study has determined a project development strategy that builds a High Pressure Acid Leach (“HPAL”) plant on site to produce a mixed nickel-cobalt hydroxide concentrate for shipping to third party refi neries. The project has a nameplate annual production of 40,000 tonnes of nickel and 3,000 tonnes of cobalt metal and a mine life of 39 years.

The feasibility study has signifi cantly eliminated the perceived disadvantage of location and isolation by identifying local supplies of gas for power supply, calcrete for neutralisation, sources of process water, and the delineation of road, rail and transport logistics to service the project.

The feasibility study has distinguished the project from other operating nickel laterite deposits in Australia on the basis of the ore style being a limonite or tropical laterite. The chemical make-up and physical characteristics of the ore vary markedly from typical Australian laterite deposits, having an iron oxide content averaging 47%, magnesium content of less than 2%, a low strip ratio and the ability to excavate the ore without blasting. In addition acid and consumable consumptions are low.

Key fi nancial outcomes for the feasibility study are tabulated: 39 yr Mine Life 20 yr Mine Life

Average Annualised Prod’n – Ni (t) 38,200 41,600 – Co (t) 2,900 3,250

Capital Cost $US 1.882 Billion $US 1.882 Billion (A$2.214 Billion) (A$2.214 Billion)

Avg. Capital Cost US$/pound Ni–equiv. $US 0.57/lb $US 1.02/lb

Operating Cost – average $A p. annum $US 411m $US 414M

Avg. OpCost $US/t Ni. $US 10,300/t $US 9,950/tAvg. OpCost $US/t Ni (after Co Credits) $US 7,370/t $US 7,180/t ($US 3.34/lb) ($US 2.92/lb)

Total Prod’n Cost $US/t Ni. $US 12,040/t US$ 12,210/t

Total Prod’n Cost $US/Ni (after Co Cr) $US 8,680/t $US 8,880/t ($US 3.91/lb) ($US 3.94/lb)

Est. Avg. EBITDA – A$ per annum $US 483 Million $US 565 Million (A$ 568 M) (A$ 665 M)

Est Avg. EBIT – A$ per annum $US 434 Million $US 470 Million (A$ 511 M) (A$ 553M)

Based on the assumptions used in the feasibility study the estimated NPV (8%) of the projet is A$3.4 billion.

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

8

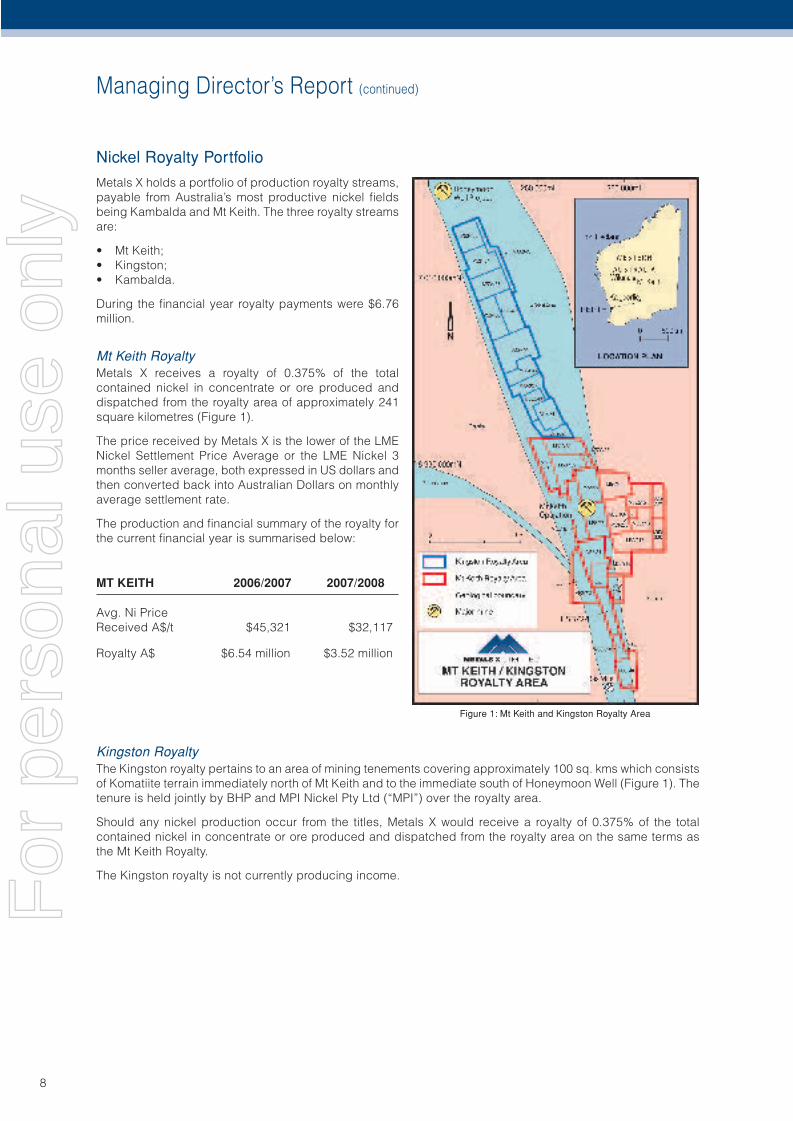

Nickel Royalty Portfolio

Metals X holds a portfolio of production royalty streams, payable from Australia’s most productive nickel fi elds being Kambalda and Mt Keith. The three royalty streams are:

• Mt Keith;• Kingston;• Kambalda.

During the fi nancial year royalty payments were $6.76 million.

Mt Keith RoyaltyMetals X receives a royalty of 0.375% of the total contained nickel in concentrate or ore produced and dispatched from the royalty area of approximately 241 square kilometres (Figure 1).

The price received by Metals X is the lower of the LME Nickel Settlement Price Average or the LME Nickel 3 months seller average, both expressed in US dollars and then converted back into Australian Dollars on monthly average settlement rate.

The production and fi nancial summary of the royalty for the current fi nancial year is summarised below:

MT KEITH 2006/2007 2007/2008

Avg. Ni Price Received A$/t $45,321 $32,117

Royalty A$ $6.54 million $3.52 million

Kingston RoyaltyThe Kingston royalty pertains to an area of mining tenements covering approximately 100 sq. kms which consists of Komatiite terrain immediately north of Mt Keith and to the immediate south of Honeymoon Well (Figure 1). The tenure is held jointly by BHP and MPI Nickel Pty Ltd (“MPI”) over the royalty area.

Should any nickel production occur from the titles, Metals X would receive a royalty of 0.375% of the total contained nickel in concentrate or ore produced and dispatched from the royalty area on the same terms as the Mt Keith Royalty.

The Kingston royalty is not currently producing income.

Figure 1: Mt Keith and Kingston Royalty Area

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

9

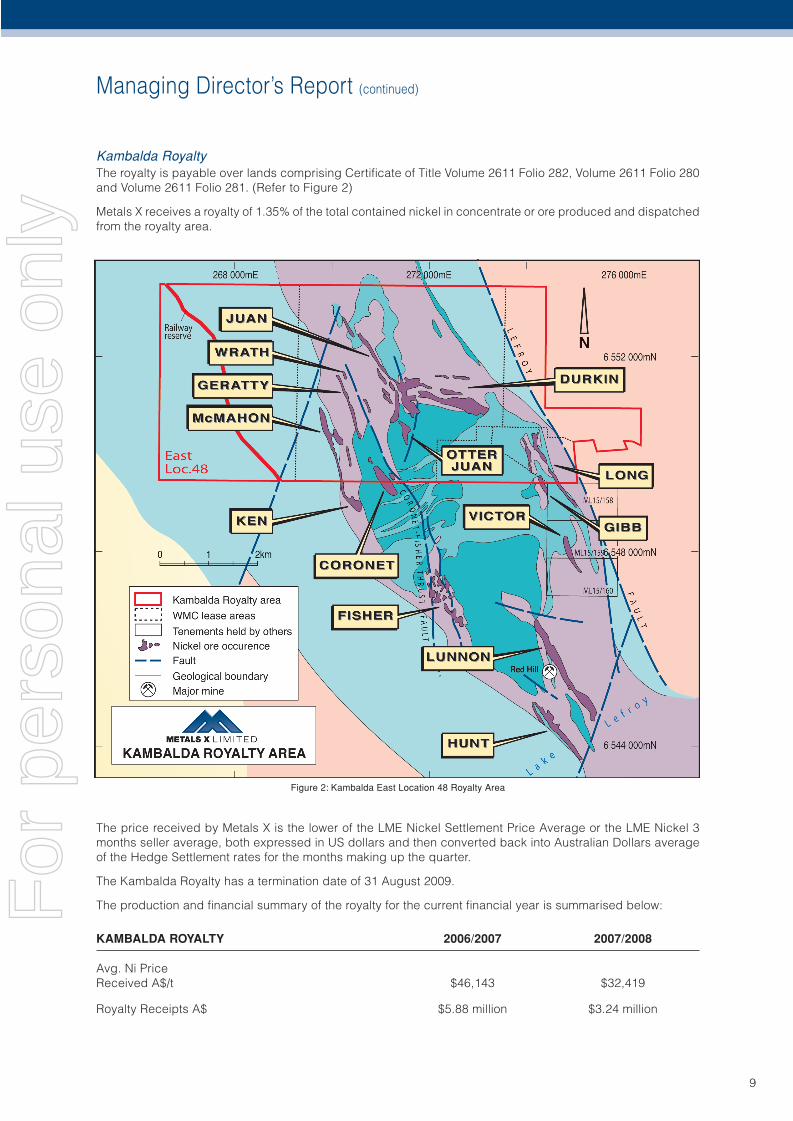

Kambalda RoyaltyThe royalty is payable over lands comprising Certifi cate of Title Volume 2611 Folio 282, Volume 2611 Folio 280 and Volume 2611 Folio 281. (Refer to Figure 2)

Metals X receives a royalty of 1.35% of the total contained nickel in concentrate or ore produced and dispatched from the royalty area.

The price received by Metals X is the lower of the LME Nickel Settlement Price Average or the LME Nickel 3 months seller average, both expressed in US dollars and then converted back into Australian Dollars average of the Hedge Settlement rates for the months making up the quarter.

The Kambalda Royalty has a termination date of 31 August 2009.

The production and fi nancial summary of the royalty for the current fi nancial year is summarised below:

KAMBALDA ROYALTY 2006/2007 2007/2008

Avg. Ni PriceReceived A$/t $46,143 $32,419

Royalty Receipts A$ $5.88 million $3.24 million

Figure 2: Kambalda East Location 48 Royalty Area

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

10

TIN DIVISION

The backbone of Metals X’s tin division is its Tasmanian Tin Strategy which looks to generate maximum effi ciency and shareholder value from Metals X’s tin assets and infrastructure in Tasmania. These assets are held within a wholly owned subsidiary company, Bluestone Mines Tasmania Pty Ltd (“BMT”).

The key assets of BMT are the cornerstone of Tasmania’s and Australia’s hard-rock tin history. They include:

1. The Renison Bell Mine;

2. The Renison Tin Concentrator;

3. The Mt Bischoff Tin Project;

4. The Renison Expansion Project (“Rentails”).

Collectively they are referred to as the Renison Project with the Rentails Project forming the Renison Expansion Project. The key development steps in chronological order of the strategy are:

1. Re-start the Renison Project with ores sourced from the Renison Bell underground mine and the Mt Bischoff open pit, with the re-commissioning of the Renison Tin Concentrator.

2. The completion of a defi nitive feasibility study on the Rentails Project.

3. The construction of the Rentails tailings re-treatment “Tin Fumer” project.

4. The integration of tin fuming within the Renison Tin process route.

5. The extension of project life for the tin fumer plan by integration of other tin ores and known stannite rich ores into the process.

Mt Bischoff open pit August 2008

For

per

sona

l use

onl

y

Renison ProjectThe Renison Bell Mine was re-started during the year following a sustained increase in world tin prices.

Ore from the Renison Bell underground is blended with ore from Mt Bischoff open pit mine to provide feedstock for the Renison Tin Concentrator.

A substantial appraisal of the tin concentrator was completed and minor modifi cations and additions to the plant have been implemented to improve process effi ciencies.

Mining commenced at the Mt Bischoff open pit in March 2008 followed by Renison Bell in May 2008. A strategic component of the re-start strategy will see a progressive build up of stockpiles from open pit and underground mining prior to plant re-commissioning.

Subsequent to fi nancial year end the re-commissioning of the Tin Concentrator commenced in late July 2008 with commissioning nearing completion by the end of September 2008 preparing the operation for its fi rst full production quarter in the December quarter of 2008.

In addition to the recovery of tin, a copper circuit has been established to recover copper as a co-product. This circuit will be commissioned in the December 2008 quarter.

Annualised production is planned at a rate of 8,000 – 10,000t of tin and 1,000 – 1,500t of copper in concentrate.

Both tin and copper concentrates are sold to third party smelters in Asia.

Managing Director’s Report (continued)

11

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

12

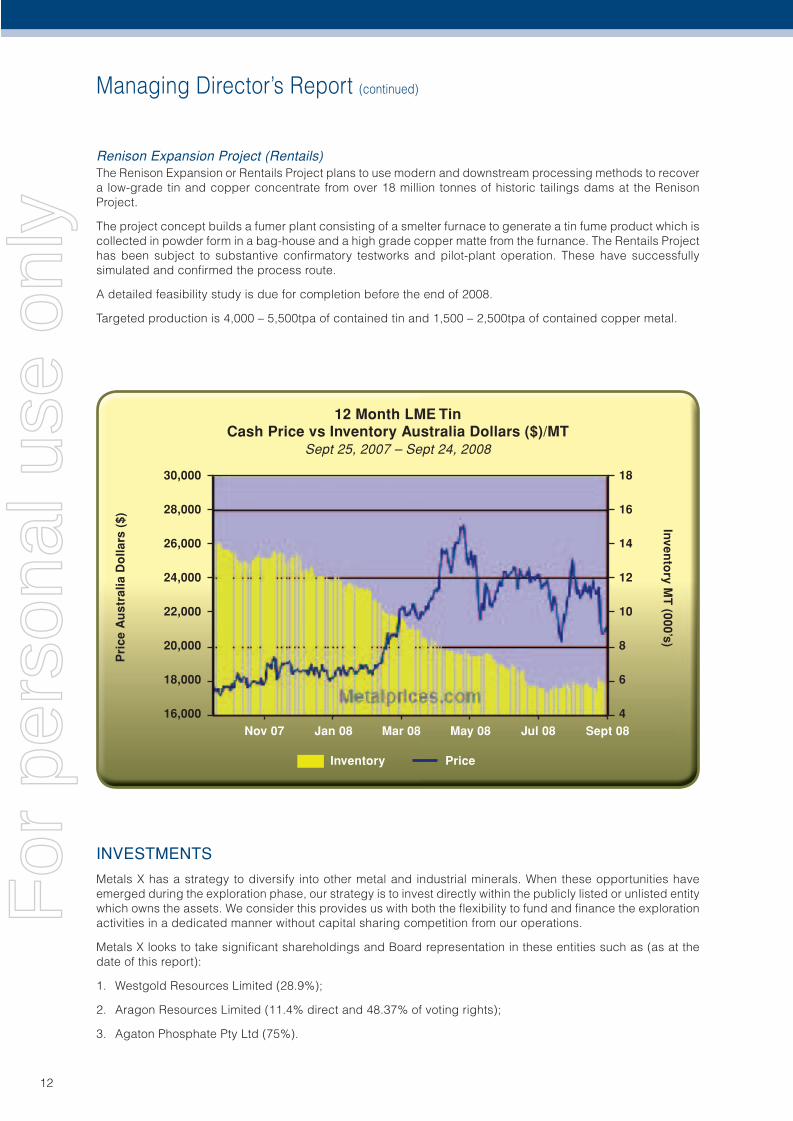

Renison Expansion Project (Rentails)The Renison Expansion or Rentails Project plans to use modern and downstream processing methods to recover a low-grade tin and copper concentrate from over 18 million tonnes of historic tailings dams at the Renison Project.

The project concept builds a fumer plant consisting of a smelter furnace to generate a tin fume product which is collected in powder form in a bag-house and a high grade copper matte from the furnance. The Rentails Project has been subject to substantive confi rmatory testworks and pilot-plant operation. These have successfully simulated and confi rmed the process route.

A detailed feasibility study is due for completion before the end of 2008.

Targeted production is 4,000 – 5,500tpa of contained tin and 1,500 – 2,500tpa of contained copper metal.

INVESTMENTS

Metals X has a strategy to diversify into other metal and industrial minerals. When these opportunities have emerged during the exploration phase, our strategy is to invest directly within the publicly listed or unlisted entity which owns the assets. We consider this provides us with both the fl exibility to fund and fi nance the exploration activities in a dedicated manner without capital sharing competition from our operations.

Metals X looks to take signifi cant shareholdings and Board representation in these entities such as (as at the date of this report):

1. Westgold Resources Limited (28.9%);

2. Aragon Resources Limited (11.4% direct and 48.37% of voting rights);

3. Agaton Phosphate Pty Ltd (75%).

12 Month LME TinCash Price vs Inventory Australia Dollars ($)/MT

Sept 25, 2007 – Sept 24, 2008

30,000

28,000

26,000

24,000

22,000

20,000

18,000

16,000

18

16

14

12

10

8

6

4

Pri

ce A

ust

ralia

Do

llars

($) Inven

tory M

T (000’s)

Nov 07 Jan 08 Mar 08 May 08 Jul 08 Sept 08

Inventory Price

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

13

Westgold Resources Limited

Westgold holds a large portfolio of highly prospective tenure in the Tennant Creek region of Australia’s Northern Territory.

Two of Westgold’s advanced prospects, Rover 1 and Explorer 108 are taking shape as potential mines.

Rover 1 – IOCG (“Iron Oxide Copper-Gold”)Rover 1 is a major gold and copper rich ironstone system with signifi cant associated cobalt and bismuth mineralisation. The Rover 1 system has many of the characteristics of the large Warrego mine near Tennant Creek where over 0.5Moz of high-grade gold averaging 20g/t was discovered in two distinct pods during mining of the much larger copper rich ironstone system. The land tenure of Westgold is targeting what is conceptually a repetition of the Tennant Creek Goldfi eld under transported cover south of Tennant Creek.

Exploration at Rover 1 commenced in February 2008 with the fi rst drilling in over 25 years intersecting and confi rming a strongly mineralised and polymetallic IOCG system.

Westgold reported excellent results from initial diamond drilling into Rover 1, including the following outstanding intercepts:

WGR1D002 65.7m @ 17.7g/t Au Eq (11.0g/t Au, 0.75%Cu, 0.15%Co, 0.09%Bi)

WGR1D002-w1 66.0m @ 10.7g/t Au Eq ( 4.3g/t Au, 0.56% Cu, 0.08%Co, 0.20%Bi)

WGR1D002-w2 49.0m @ 16.6g/t Au Eq ( 5.8g/t Au, 1.05% Cu, 0.10%Co, 0.42%Bi)

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

14

Explorer 108Explorer 108 is a large alteration system, mineralised throughout with broad (100m+) intervals grading 2 to 5% Zn + Pb, but importantly contains a number of high grade lenses up to 60 metres thick containing grades over 7% Zn + Pb. The most signifi cant of these discovered to date occurs in the base of dolomite sequence directly above the contact with the underlying acid volcanic sequence.

Westgold continued exploration of this target in the fi rst half of the year, before pausing to estimate a resource.

Westgold announced a maiden identifi ed mineral resource estimate for Explorer 108 as follows:

8.7 million tonnes @ 5.7% (Zn + Pb) using a 2.5% Zn+Pb lower cut-off or4.0 million tonnes @ 8.2% (Zn + Pb) using a 5.0% Zn + Pb lower cut-off

Aragon Resources Limited

Metals X invested in the spin-off of Westgold’s Western Australian gold, nickel and uranium assets early in the fi nancial year. Aragon holds a large portfolio of gold nickel and uranium assets in Western Australia. The key of these is a +2000 sq. km land position covering highly prospective gold and uranium tenure in the Yandal Gold Belt.

Aragon completed its IPO raising $8.75 million and listing on the ASX on 10 August 2007.

Aragon achieved early exploration success in gold exploration at its Mission and Cables prospects, approximately 7km north of the Darlot Mine. Aragon reported excellent drill intercepts suggest two primary gold discoveries during the year, with best results of:

Mission ProspectADRC004 1m @ 75.6g/t Au from 48mADRC007 2m @ 18.6g/t Au from 74mADRC008 2m @ 28.3g/t Au from 52m

Cables ProspectADRC019 4m @ 18.8g/t Au from 182mADRC022 7m @ 27.5g/t Au from 133mADRC027 4m @ 42.0g/t Au from 78m

Subsequent to year end Aragon acquired all of the assets of Territory Phosphate Pty Ltd and has moved into phosphate exploration in the Southern Georgina and West Wiso basins near Tennant Creek in the Northern Territory.

Agaton Phosphate Pty Ltd

During the year Metals X entered into a Heads of Agreement with All Classic Enterprises Pty Ltd and Bishop Exploration Pty Ltd (the Vendors) to establish a 75% Metals X owned subsidiary company to acquire a 90% interest in the Agaton Phosphate Project. The remaining 10% owned by the Vendors is free carried to the completion of a feasibility study.

The Project is located between the town of Moora and the Cooljaroo Mineral Sands areas approximately 120km north of Perth. Agaton is a phosphate sands project, with phosphate occurring as nodules and precipitates within sedimentation phases of the Dandaragan Trough. The phosphate mineralization is considered to have formed by precipitation during the mixing of cold phosphate rich waters with warm continental shelf waters, as has occurred in the giant phosphate deposits of Florida.

Exploration titles were granted and land access agreements over key areas were established during the period. Preliminary shallow seismic geophysics was completed to outline the basement of the trough and phosphate nodule trap structures. Reconnaissance drilling is planned to commence in the September 2008 quarter with results to follow later in the year.

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

15

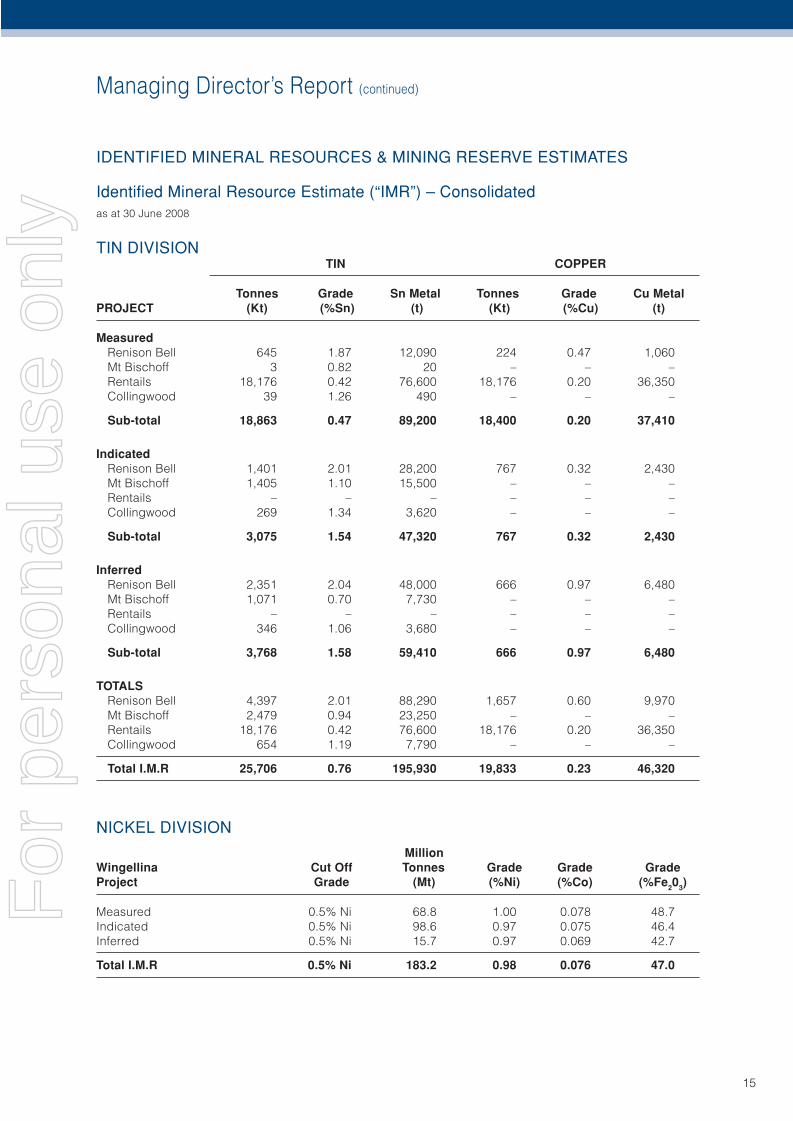

IDENTIFIED MINERAL RESOURCES & MINING RESERVE ESTIMATES

Identifi ed Mineral Resource Estimate (“IMR”) – Consolidatedas at 30 June 2008

TIN DIVISION TIN COPPER

Tonnes Grade Sn Metal Tonnes Grade Cu MetalPROJECT (Kt) (%Sn) (t) (Kt) (%Cu) (t)

Measured Renison Bell 645 1.87 12,090 224 0.47 1,060Mt Bischoff 3 0.82 20 – – –Rentails 18,176 0.42 76,600 18,176 0.20 36,350Collingwood 39 1.26 490 – – –

Sub-total 18,863 0.47 89,200 18,400 0.20 37,410

Indicated Renison Bell 1,401 2.01 28,200 767 0.32 2,430Mt Bischoff 1,405 1.10 15,500 – – –Rentails – – – – – –Collingwood 269 1.34 3,620 – – –

Sub-total 3,075 1.54 47,320 767 0.32 2,430

Inferred Renison Bell 2,351 2.04 48,000 666 0.97 6,480Mt Bischoff 1,071 0.70 7,730 – – –Rentails – – – – – –Collingwood 346 1.06 3,680 – – –

Sub-total 3,768 1.58 59,410 666 0.97 6,480

TOTALS Renison Bell 4,397 2.01 88,290 1,657 0.60 9,970Mt Bischoff 2,479 0.94 23,250 – – –Rentails 18,176 0.42 76,600 18,176 0.20 36,350Collingwood 654 1.19 7,790 – – –

Total I.M.R 25,706 0.76 195,930 19,833 0.23 46,320

NICKEL DIVISION

MillionWingellina Cut Off Tonnes Grade Grade GradeProject Grade (Mt) (%Ni) (%Co) (%Fe203)

Measured 0.5% Ni 68.8 1.00 0.078 48.7Indicated 0.5% Ni 98.6 0.97 0.075 46.4Inferred 0.5% Ni 15.7 0.97 0.069 42.7

Total I.M.R 0.5% Ni 183.2 0.98 0.076 47.0

For

per

sona

l use

onl

y

Managing Director’s Report (continued)

16

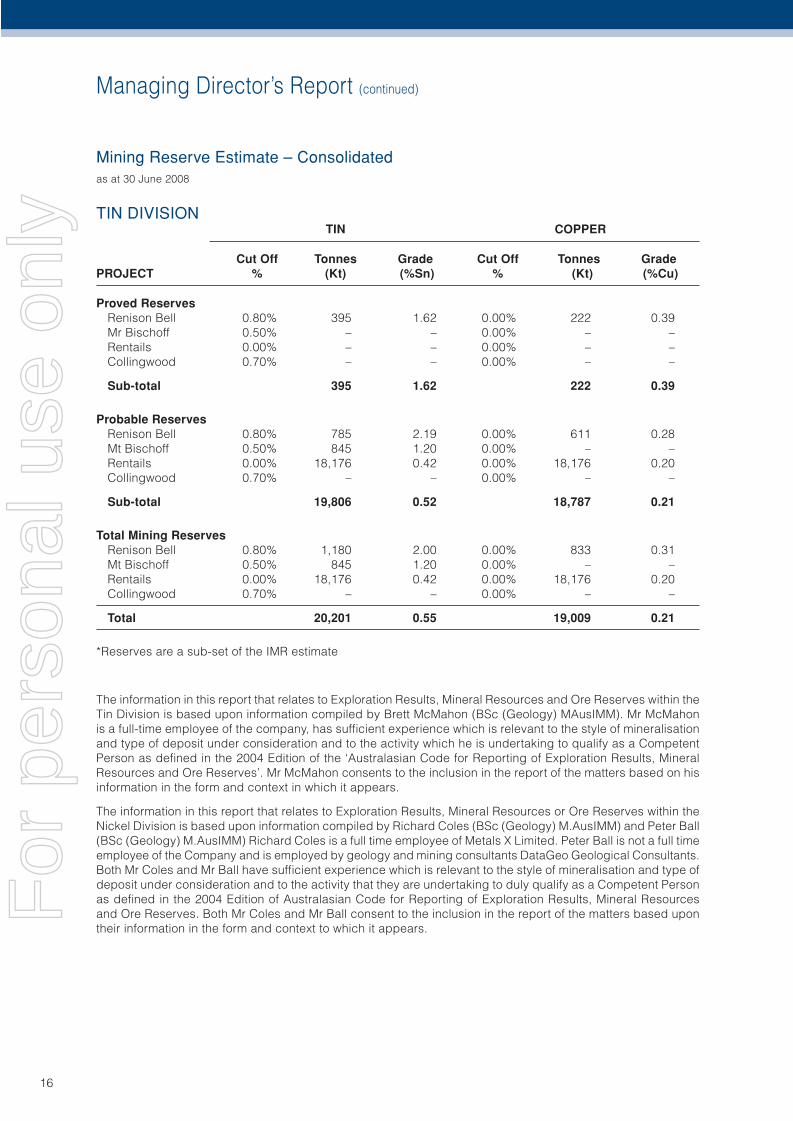

Mining Reserve Estimate – Consolidatedas at 30 June 2008

TIN DIVISION TIN COPPER

Cut Off Tonnes Grade Cut Off Tonnes GradePROJECT % (Kt) (%Sn) % (Kt) (%Cu)

Proved Reserves Renison Bell 0.80% 395 1.62 0.00% 222 0.39Mr Bischoff 0.50% – – 0.00% – –Rentails 0.00% – – 0.00% – –Collingwood 0.70% – – 0.00% – –

Sub-total 395 1.62 222 0.39

Probable Reserves Renison Bell 0.80% 785 2.19 0.00% 611 0.28Mt Bischoff 0.50% 845 1.20 0.00% – –Rentails 0.00% 18,176 0.42 0.00% 18,176 0.20Collingwood 0.70% – – 0.00% – –

Sub-total 19,806 0.52 18,787 0.21

Total Mining Reserves Renison Bell 0.80% 1,180 2.00 0.00% 833 0.31Mt Bischoff 0.50% 845 1.20 0.00% – –Rentails 0.00% 18,176 0.42 0.00% 18,176 0.20Collingwood 0.70% – – 0.00% – –

Total 20,201 0.55 19,009 0.21

*Reserves are a sub-set of the IMR estimate

The information in this report that relates to Exploration Results, Mineral Resources and Ore Reserves within the Tin Division is based upon information compiled by Brett McMahon (BSc (Geology) MAusIMM). Mr McMahon is a full-time employee of the company, has suffi cient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defi ned in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr McMahon consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

The information in this report that relates to Exploration Results, Mineral Resources or Ore Reserves within the Nickel Division is based upon information compiled by Richard Coles (BSc (Geology) M.AusIMM) and Peter Ball (BSc (Geology) M.AusIMM) Richard Coles is a full time employee of Metals X Limited. Peter Ball is not a full time employee of the Company and is employed by geology and mining consultants DataGeo Geological Consultants. Both Mr Coles and Mr Ball have suffi cient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity that they are undertaking to duly qualify as a Competent Person as defi ned in the 2004 Edition of Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves. Both Mr Coles and Mr Ball consent to the inclusion in the report of the matters based upon their information in the form and context to which it appears.

AF

or p

erso

nal u

se o

nly

Director’s Report

17

The Directors submit their report together with the fi nancial report of Metals X Limited (“Metals X” or “the Company”) and of the Consolidated Entity, being the Company and its controlled entities, for the year ended 30 June 2008.

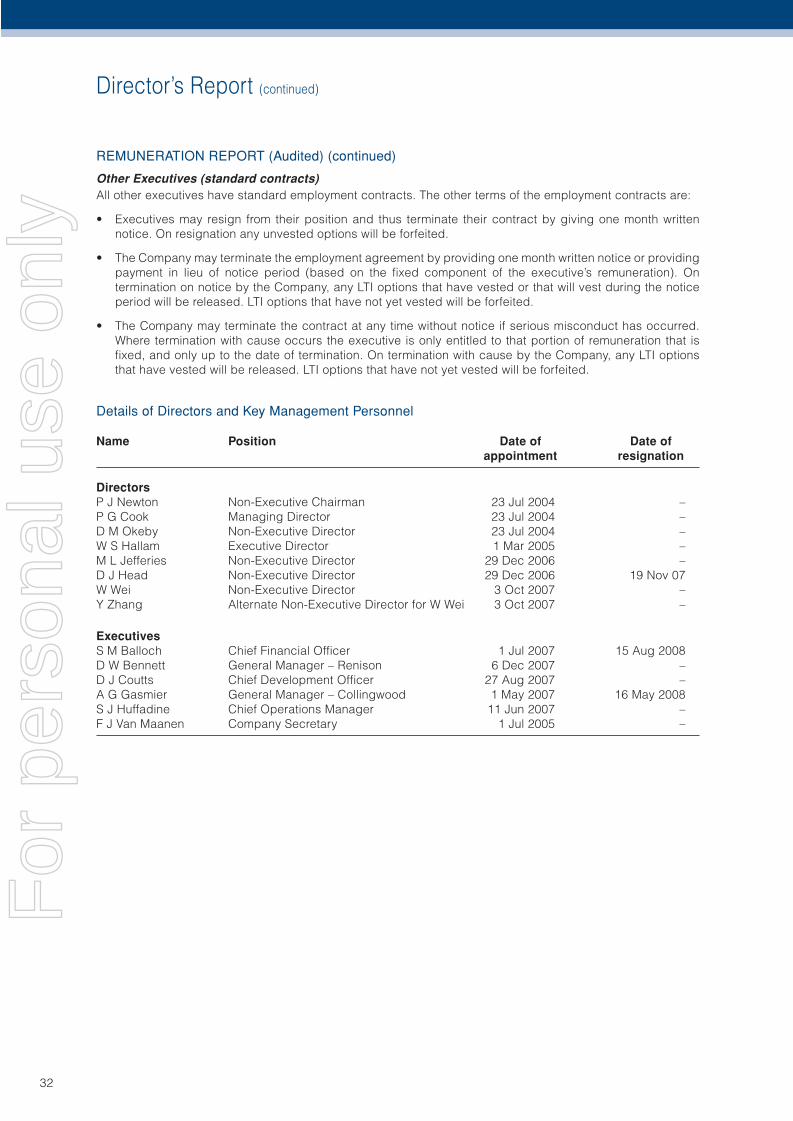

DIRECTORS

The names and details of the Company’s Directors in offi ce during the fi nancial period and until the date of this report are as follows. Directors were in offi ce for this entire period unless otherwise stated.

Names, qualifi cations, experience and special responsibilitiesPeter John Newton – ChairmanMr Newton was a stockbroker for 25 years until 1994. Since then he has been a signifi cant participant in the Australian resource industry as an investor and a director of a number of listed companies. In recent years he has been the Chairman of both Hill 50 Limited and Abelle Limited. Mr Newton is also the Chairman of the Company’s Remuneration Committee.

During the past three years he has served as a director of the following public listed companies:

• Lynas Corporation Ltd (Appointed 24 November 2004 – Resigned 8 December 2005); and• Metals Exploration Limited** (Appointed 14 June 2004).

Peter Gerard Cook – Managing DirectorMr Cook is a Geologist (BSc (Applied Geology)) and a Mineral Economist (MSc (Min. Econ), MAusIMM). In recent years he has been the Managing Director of Hill 50 Limited, the Chief Executive Offi cer of Harmony Gold Australia Pty Ltd and the Managing Director of Abelle Limited. He has considerable experience in the fi elds of exploration and project and corporate management of mining companies. He is also a director of Westgold Resources Limited and the Chairman of Aragon Resources Limited.

During the past three years he has served as a director of the following public listed companies:

• Metals Exploration Limited** (Appointed 14 June 2004);• Westgold Resources Limited* (Appointed 19 March 2007); and• Aragon Resources Limited* (Appointed 18 May 2007).

Warren Shaye Hallam – Executive DirectorMr Hallam is a Metallurgist (B. App Sci (Metallurgy)) and a Mineral Economist (MSc (Min. Econ)) and holds a Graduate Diploma in fi nance. He has considerable technical and commercial experience within the resources industry. In recent times he was the Managing Director of Metals Exploration and previously worked for WMC Resources Ltd (“WMC”). In his last position with WMC, he was Group Manager – Corporate Planning and Strategy.

During the past three years he has served as a director of the following public listed company:

• Metals Exploration Limited** (Appointed 14 June 2004).

Donald Mark Okeby – Non-Executive DirectorMr Okeby has considerable experience in the resources industry both as a Solicitor and as a director of listed companies. He holds a Master of Laws (LLM). In recent years he has been an Executive Director of Hill 50 Limited, Abelle Limited and a non-executive director of Lynas Corporation Ltd. He is presently a director of Westgold Resources Limited. Mr Okeby also serves on the Company’s Audit and Remuneration Committees.

During the past three years he has served as a director of the following public listed companies:

• Lynas Corporation Ltd (Appointed 24 November 2004 – Resigned 8 December 2005);• Metals Exploration Limited** (Appointed 14 June 2004); and• Westgold Resources Limited* (Appointed 19 March 2007).

Michael Leslie Jefferies – Non-Executive DirectorMr Jefferies is an executive of Guinness Peat Group plc (“GPG”). He is a director of Tower Limited and Chairman of TAFMO Limited. He has extensive experience in fi nance and investment, including 16 years as an executive of GPG. He is a chartered accountant and holds a B. Comm. Mr Jefferies also serves on the Company’s Audit Committee.

For

per

sona

l use

onl

y

Director’s Report (continued)

18

During the past three years he has served as a director of the following public listed companies:

• Metals Exploration Limited** (Appointed 14 June 2004);• Australian Wealth Management Limited (Appointed 29 October 2004 – Resigned 24 April 2007);• Ozgrove Limited* (Appointed 31 October 2007)• Tower Australia Group Limited (Appointed 8 August 2006 – Resigned 8 August 2008 ); and• Tower Limited* (Appointed 14 December 2006).

Wang Wei – Non-Executive Director (Appointed 3 October 2007)Mr Wei is currently the Vice President of Jinchuan Group Limited (“Jinchuan”) in charge of engineering construction of overseas projects in which Jinchuan participates. Mr Wang is a professor classed engineer specialising in non-ferrous metallurgy and he brings to the Company substantial experience and knowledge of metallurgical nickel processing techniques, in particular high pressure acid leach technology and operation.

Yimin Zhang – Alternate Non-Executive Director (Appointed 3 October 2007)Mr Zhang joined the Board to act as an alternate director for Wang Wei. Mr Zhang is the Chief Representative for Jinchuan Australia and is also an Executive Director of Sino Nickel Pty Limited. Mr Zhang has worked for Jinchuan since 1981 and has been posted to several overseas positions to which he has been involved in numerous Jinchuan overseas co-operative ventures. Mr Zhang holds a Diploma from the Metallurgical and Architectural Institute of Chung Chan.

During the past three years he has served as a director of the following public listed company:

• Allegiance Mining NL (Appointed 7 November 2007 – Resigned 2 June 2008)

Donald James Head – Non-Executive Director (Deceased 19 November 2007)Mr Head was a metallurgist with more than 30 years experience in the mining industry. He held several senior management positions with WMC Resources Limited, including a number of years as the manager of the Kwinana Refi nery. He was a member of the Australian Institute of Mining and Metallurgy and ran his own metallurgical consulting business providing services to several mining and construction groups. In recent years he was a Non-Executive Director of Tectonic Resources NL, Abelle Limited and Acclaim Exploration NL. Mr Head also served on the Company’s Remuneration Committee.

During the past three years he has served as a director of the following public listed company:

• Acclaim Exploration NL (Appointed 1 December 2003 – Resigned 27 March 2006).

* Denotes current directorship.** Metals Exploration Limited was delisted by the ASX on 17 January 2007 subsequent to the merger with the

Company.

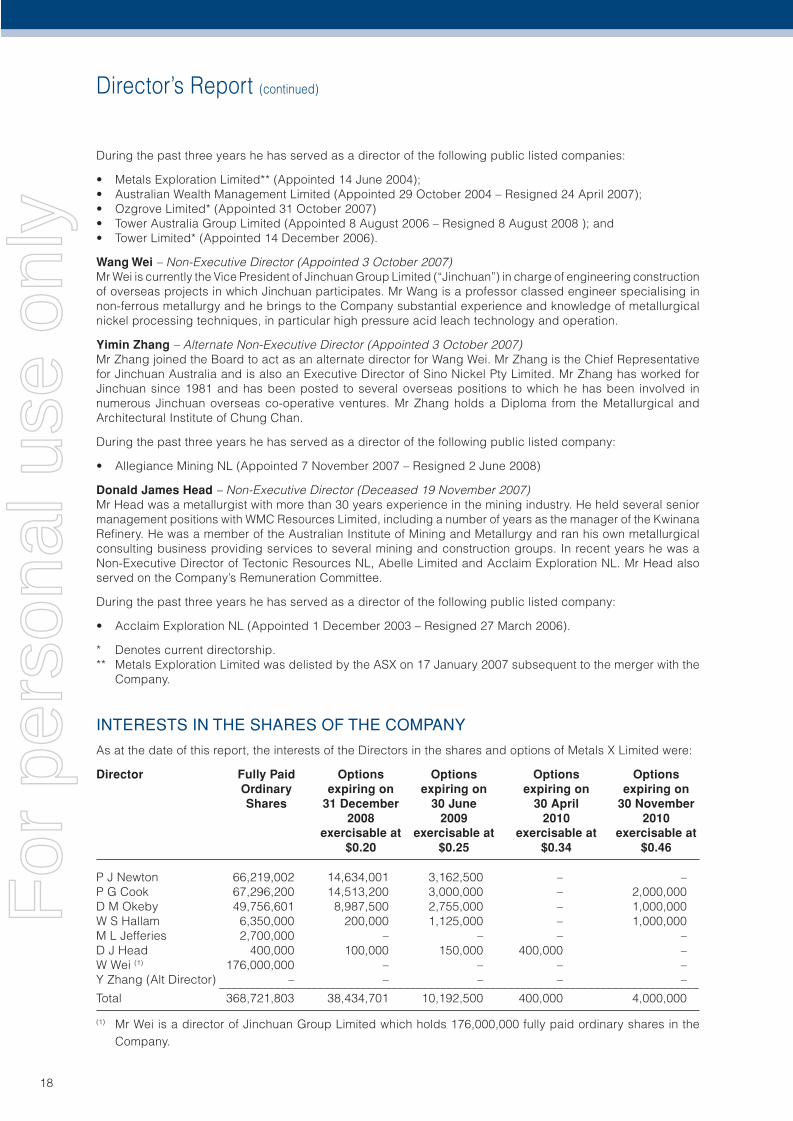

INTERESTS IN THE SHARES OF THE COMPANY

As at the date of this report, the interests of the Directors in the shares and options of Metals X Limited were:

Director Fully Paid Options Options Options Options Ordinary expiring on expiring on expiring on expiring on Shares 31 December 30 June 30 April 30 November 2008 2009 2010 2010 exercisable at exercisable at exercisable at exercisable at $0.20 $0.25 $0.34 $0.46

P J Newton 66,219,002 14,634,001 3,162,500 – –P G Cook 67,296,200 14,513,200 3,000,000 – 2,000,000D M Okeby 49,756,601 8,987,500 2,755,000 – 1,000,000W S Hallam 6,350,000 200,000 1,125,000 – 1,000,000M L Jefferies 2,700,000 – – – –D J Head 400,000 100,000 150,000 400,000 –W Wei (1) 176,000,000 – – – –Y Zhang (Alt Director) – – – – – ______________________________________________________________________________Total 368,721,803 38,434,701 10,192,500 400,000 4,000,000

(1) Mr Wei is a director of Jinchuan Group Limited which holds 176,000,000 fully paid ordinary shares in the Company.

For

per

sona

l use

onl

y

Director’s Report (continued)

19

COMPANY SECRETARY

Fiona Van Maanen – Company SecretaryMrs Van Maanen is a CPA, holds a Bachelor of Business (Accounting) degree and a Graduate Diploma in Company Secretarial Practice. She has 16 years of accounting and fi nancial management experience in the mining and resources industry and has been with the Company since incorporation.

DIVIDENDS

No dividends have been paid or declared by the Company during the fi nancial period or up to the date of this report.

Refer to note 8 for available franking credits.

PRINCIPAL ACTIVITIES

The principal activities during the year of entities within the Consolidated Entity were:

• exploration for and the mining, treatment and marketing of tin concentrate in Australia;• exploration for nickel in Australia;• exploration for phosphate in Australia;• development of nickel projects;• development and construction of tin mine projects; and• the ownership of nickel mining royalty rights; and• exploration for precious and base metals through signifi cant shareholdings in Westgold Resources Limited

and Aragon Resources Limited.

Other than the addition of the exploration for phosphate minerals, there have been no other signifi cant changes in the nature of these activites during the year.

EMPLOYEES

The Consolidated Entity employed 188 employees at 30 June 2008 (2007: 132).

For

per

sona

l use

onl

y

Director’s Report (continued)

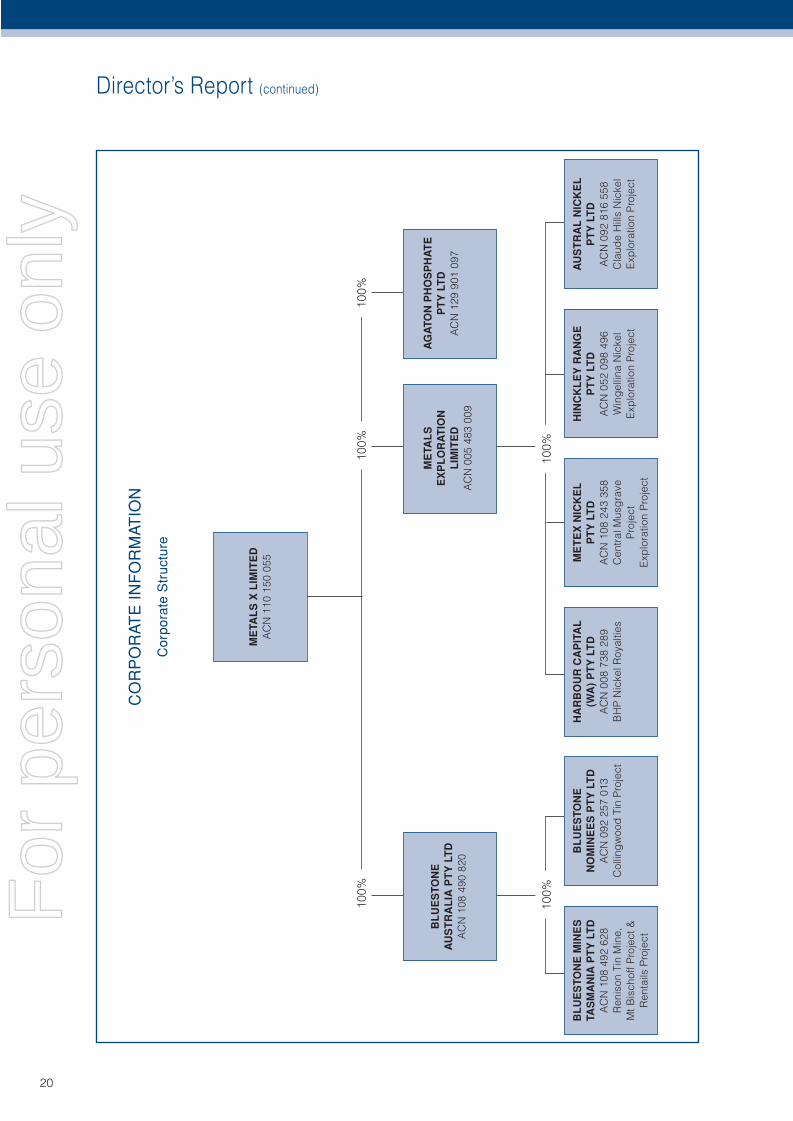

20

BL

UE

STO

NE

MIN

ES

TA

SM

AN

IA P

TY

LT

DA

CN

108

492

628

Ren

ison

Tin

Min

e,

Mt B

isch

off P

roje

ct &

R

enta

ils P

roje

ct

BL

UE

STO

NE

A

US

TR

AL

IA P

TY

LT

DA

CN

108

490

820

ME

TAL

S X

LIM

ITE

DA

CN

110

150

055

ME

TAL

S

EX

PL

OR

AT

ION

L

IMIT

ED

AC

N 0

05 4

83 0

09

AG

ATO

N P

HO

SP

HA

TE

P

TY

LT

D

AC

N 1

29 9

01 0

97

BL

UE

STO

NE

N

OM

INE

ES

PT

Y L

TD

A

CN

092

257

013

Col

ling

woo

d T

in P

roje

ct

HA

RB

OU

R C

AP

ITA

L

(WA

) P

TY

LT

DA

CN

008

738

289

BH

P N

icke

l Roy

altie

s

ME

TE

X N

ICK

EL

P

TY

LT

DA

CN

108

243

358

Cen

tral

Mus

gra

veP

roje

ct

Exp

lora

tion

Pro

ject

HIN

CK

LE

Y R

AN

GE

P

TY

LT

DA

CN

052

098

496

Win

gel

lina

Nic

kel

Exp

lora

tion

Pro

ject

AU

ST

RA

L N

ICK

EL

P

TY

LT

DA

CN

092

816

558

Cla

ude

Hill

s N

icke

l E

xplo

ratio

n P

roje

ct

100%

100%

100%

100%

100%

CO

RP

OR

ATE

IN

FO

RM

ATIO

N

Cor

pora

te S

truc

ture

20

For

per

sona

l use

onl

y

Director’s Report (continued)

21

OPERATING AND FINANCIAL REVIEW

Group OverviewMetals X Limited was incorporated as Bluestone Tin Limited on 23 July 2004 in Western Australia.

On 19 December 2006 the Company completed the merger with Metals Exploration Limited by way of a Scheme of Arrangement.

On 2 January 2007 the Company changed its name from Bluestone Tin Limited to Metals X Limited to refl ect the diversifi ed nature of the new business. On 9 January 2007 the Company commenced trading on the Australian Securities Exchange (“ASX”) under its new trading code MLX.

Metals X is a diversifi ed explorer and developer of minerals and metals. It owns a royalty portfolio generating revenue from sales of nickel at third party operations. It’s activities span brownfi eld exploration and production from its development and mining projects. Metals X performs greenfi elds exploration in its own right and through signifi cant investment in other publicly listed exploration companies.

The Company holds a 28.9% (2007: 19.1%) interest in Westgold Resources Limited (“Westgold”), which is involved in the exploration for base metals in the Northern Territory. Westgold is listed on the ASX. On 30 August 2007 the Company increased its interest from 19.1% to 22.4% and gained signifi cant infl uence over Westgold. During the year the Company charged Westgold for Directors fees for Mr Cook and Mr Okeby.

On 30 July 2007 the Company acquired a 12.8% interest in Aragon Resources Limited (“Aragon”), which is involved in the exploration for base and precious metals in Western Australia. Aragon is listed on the ASX. Westgold has a 41.7% interest in Aragon. As a result of the Company increasing its interest in Westgold in August 2007, it has gained signifi cant infl uence over Aragon. During the year the Company charged Aragon for accounting, secretarial and administrative services at cost, and for Directors fees for Mr Cook.

On 26 February 2008 Agaton Phosphate Pty Ltd was incorporated in which the Company will hold a 75% interest. Agaton phosphate Pty Ltd was established to acquire phosphate exploration prospects in the Dandaragan area of Western Australia.

The Company has signifi cantly expanded and diversifi ed its resource assets. It has resulted in a larger single company with revenue from royalties and mining operations and a pipeline of growth assets ranging from greenfi elds exploration to large scale resource developments.

Review of Financial Position

Share issues during the year

Share PlacementsThe Company allotted and issued 139,000,000 shares at 30 cents each on 22 January 2008 pursuant to a placement to raise an amount of $41,700,000 and contributed equity increased by $41,231,789 after costs of capital raising of $468,211.

The Company allotted and issued 59,000,000 shares at 30 cents each on 14 March 2008 pursuant to a placement to raise an amount of $17,700,000 and contributed equity increased by $17,680,706 after costs of capital raising of $19,294.

Option ConversionsDuring the year option holders converted 74,326,004 options into ordinary shares increasing equity by $15,131,200 (refer to note 28(f) for details).

Liquidity and Capital ResourcesThe consolidated cash fl ow statement illustrates that there was an increase in cash and cash equivalents in the year ended 30 June 2008 of $24,456,559 (2007: $27,027,949). The increase in cash infl ow in comparison with the prior year is caused by a number of factors. Financing activities generated $65,987,779 (2007: $43,557,636) of net cash in-fl ows. This increase in comparison to 30 June 2007 is largely due to the placement of 139,000,000 shares to Apac Resources Limited and 59,000,000 shares to Jinchuan Group Limited and to option conversions for a total of $74,010,814 after capital raising costs. This net increase in cash fl ows from fi nancing activities has been offset by an increase in the amount of cash used for investing activities $55,779,632 (2007: $6,219,169), which was mainly attributable to the re-start of the Renison Tin Project.

For

per

sona

l use

onl

y

Director’s Report (continued)

22

There has also been a net increase in the amount of cash from operating activities of $14,248,416 (2007: decrease $10,310,458), which is largely due to an increase in revenue from tin concentrate sales from the Collingwood Tin Project.

The Consolidated Entity’s debt has decreased by $5,716,913 over the last year mainly due to the repayment of unsecured loans of $10,100,000, which was offset by fi nance agreements secured by mobile plant and equipment of $5,947,232 entered into during the year. Of the Consolidated Entity’s debt, 30% is repayable within one year of 30 June 2008, compared to 42% in the previous year.

Capital ExpenditureThere has been an increase in cash used on capital expenditure for 30 June 2008 to $55,779,632 from $6,219,169 in the year ended 30 June 2007 due primarily to the re-start of the Renison Tin Project (including the Mt Bischoff open pit mine). Further capital commitments of $3,120,220 existed at the balance sheet date, principally relating to the construction of residential accommodation and plant refurbishment for the Renison Tin Project.

Operating ResultsThe consolidated operating loss before income tax of the Consolidated Entity attributable to members for the period was $11,968,573 (2007: $23,697,800), down by 49% as compared to the previous year. This result refl ects an increase in income from tin concentrate sales. The consolidated operating loss after tax for the period was $7,993,987 (2007: $2,734,841). This refl ects the recognition in the previous year of an income tax credit of $20,962,959 relating to carried forward losses recognised.

REVIEW OF OPERATIONS

The key activities of the Consolidated Entity are listed below:

TIN PROJECTSDuring the year the Company’s tin projects were:

1. Tasmanian Tin Strategy• Renison Tin Project• Rentails Tin Project• Tasmanian Tin Exploration

2. Far North Queensland Tin Strategy• Collingwood Tin Project• Gillian and Windemere Tin Projects (Gillian sold on 21 February 2008)

TASMANIAN TIN STRATEGY

Renison Tin ProjectThe Renison Tin Project is located approximately 15km NE of Zeehan on Tasmania’s West Coast. The Renison Project is built around the Renison Bell underground mine and the Renison Tin Concentrator. These were both extensively refurbished during the 2005 fi nancial year and operated until October 2005 before being placed on care & maintenance due to low tin prices.

The Mt Bischoff Tin Project is located approximately 80km north of the Renison Project. Mt Bischoff contains a moderately sized open pit resource and an advanced exploration project with considerable potential for additional tin discovery and mining.

During the fi nancial period the Company progressed with the re-start of the Renison Tin Project. Open pit and underground mining had commenced with commissioning of the Concentrator and a ramp up to full capacity underway by the end of the fi nancial period. First tin concentrates from the re-started project were dispatched in July 2008.

The new operating plan for the Renison Tin Project is based predominantly on owner-operated underground mining at the Renison Bell Mine with open pit mining at the Mt Bischoff mine using mining contractors. Ore from both sources are blended at the Tin Concentrator (approx 1/3rd from Mt Bischoff) to create a ROM feedstock averaging 1.5-2.0% Sn. Ore is processed at approximately 85 tonne per hour through the tin concentrator to generate a high grade tin concentrate. The tin concentrate is trucked to port and then shipped to Malaysia or Thailand for smelting into LME grade tin ingots.

For

per

sona

l use

onl

y

Director’s Report (continued)

23

Additional new technology has been incorporated into the Concentrator which is expected to have a positive impact on overall tin recoveries. The revised Renison Project will be upgraded to include a copper circuit that will enable the generation of a copper co-product. The copper circuit is expected to be commissioned in late September 2008.

At full capacity and in steady-state the Renison Project is forecast to produce 8,500 – 10,000 tonnes of tin metal and 1,000 tonnes of copper per annum.

The net operating profi t after income tax for the Renison Project for the fi nancial year was $3,419,908 compared to an operating loss of $3,786,991 for the previous year. The operating profi t for the current fi nancial period is due to the reversal of impairment losses on mine properties and developments costs of $11,042,607 associated with the increase in tin prices during the period, the approval to mine at Mt Bischoff and the re-start of the Renison Project.

There was no revenue from tin concentrate sales from the Renison Project for the fi nancial year or in the previous year due to the project being on care and maintenance during these periods.

Rentails Tin ProjectThe Rentails project is aimed at the re-processing and recovery of tin and copper from an estimated 18.2 million tonnes of tailings at an average grade of 0.42% Tin and 0.20% Copper (containing over 76,000 tonnes of tin and over 36,000 tonnes of copper metal) that remain at the site from the historic processing of tin ores from the Renison Bell mine.

The project has been through a conceptual pre-feasibility study in 2005, which identifi ed that a combination of sulphide fl otation and tin fl otation separation techniques could produce a low-grade concentrate, which could be fumed to produce a saleable tin product. During the fi nancial period a complete phase of pilot testing, including concentration, pilot fuming and gas emissions studies have been completed that confi rm the technical merits of the project.

GR Engineering was commissioned to complete the detailed feasibility on the project. In consultation with and following a review of the available data, there has been a conscious decision by the Company to shift itself along the concentrate grade-tonnage curve to a position of more optimal operating performance and higher overall metal recovery.

This shift change has been from a target of 55% recovery of tin to concentrate and a 15% concentrate grade to that of a 62% recovery of tin to concentrate and a 10% concentrate grade. Coincident with this shift is an associated reduction in operating risk and the optimisation of coincident copper recovery from the process. The consequence of such a shift is an increase in the overall scale of the tin fumer project. This will result in higher capital costs which is expected to be compensated for by improved operating performance and lower operating risk.

The stages of the fl ow sheet remain relatively unchanged and the process fl ow sheet consists of fi ve key stages:

1. Grinding;2. Sulphide Flotation;3. High-G Gravity separation;4. Tin (cassiterite) Flotation; and5. Fuming.

During the fi nancial year, a review of the tailings resource estimate and a complete reconciliation against mill production via the establishment of an historic dam construction plan based upon actual plant outputs was completed. In addition a dam de-construction strategy and ore recovery has been developed which will enable a mining reserve estimate to be fi nalised in August. The fi nal bankable standard feasibility is due for completion in late 2008.

Tasmanian Tin ExplorationPlans for underground tin exploration programs coincident with the ensuing re-start of the Renison project were completed during the period. Renison underground exploration delivered excellent early success, encountering high grade tin and copper mineralisation over considerable widths outside the existing Resource and Reserve.

Underground exploration to extend and in particular upgrade the inferred resources into measured and indicated category commenced during May 2008. A drill rig equipped to drill holes beyond 1,000m vertical to test depth extensions and conceptual targets beneath the existing mine will commence work on the Renison underground

For

per

sona

l use

onl

y

Director’s Report (continued)

24

operation by September 2008. In particular, the key target area is for greisen style mineralisation coinciding with the intersection of the major Federal Basset Fault system and the Pine Hill Granite carapace. This represents an integral part of the Tasmanian Tin Strategy aimed at proving new resources to enhance the development pipeline and complement the conversion of the existing resource base to reserves.

A program of Reverse Circulation drilling at Mt Bischoff aimed at extending the existing resource, providing resource infi ll and waste characterisation at Mt Bischoff and exploring for additional tin mineralisation was completed during the period and a further program has commenced in August 2008.

FAR NORTH QUEENSLAND TIN

Collingwood Tin ProjectThe Company’s Collingwood Tin Project is located in Far North Queensland approximately 30km south of Cooktown.

The Collingwood mine operated for most of the reporting period before being placed on care & maintenance in May 2008. The mine has experienced production shortfalls and these have been associated with three key areas; mine grade estimates, equipment reliability and skilled manpower.

Mine reconciliations for the Collingwood mine continued to under-call in tonnes and grade compared to pre-mining and reserve estimates. During the period forward production estimates were factored based upon historic performance and revised mines plans were developed based upon these parameters. Underground exploration was undertaken during the period to target extensions to the known mineralisation. Drilling returned a number of signifi cant intercepts of narrow zones of tin in greisen showing that the orebody continues to both the north and south and at depth, although depth potential appeared limited due to the narrowing of the lodes.

Metals X made the decision to undertake an orderly closure of the Collingwood Tin Mine and the sale of its other North Queensland tin exploration assets in order to focus its attention on the Renison and Rentails Projects of its Tasmanian Tin Strategy. The operation was successfully put on care and maintenance in May 2008. The project will remain on care and maintenance whilst a review of all options is undertaken.

The net operating loss after income tax for the Collingwood Project for the fi nancial year was $13,202,061 compared to $15,963,251 for the previous year. The operating loss for the current year is higher due to the mine production constraints, termination costs and the impairment of property, plant and equipment and mine properties and development assets of $7,328,432 (2007: $6,493,315). Revenue from tin concentrate sales was $35,562,632 for the period compared to $25,588,717 sales in the previous year.

Collingwood Project performance is summarised below:

Mining 2008 2007Ore Hoisted 232,003 tonnes 251,530 tonnesGrade 0.87 % Sn 1.03 % Sn

Tin ConcentrationTonnes Processed 232,297 tonnes 251,130 tonnesGrade 0.87 % Sn 1.01 % SnRecovery to Conc. 80% 76%Concentrate Grade 57% Sn 59% SnSn Metal Produced 1,632 tonnes Sn metal 1,917 tonnes Sn metalSn Metal Sales 1,773 tonnes Sn metal 1,686 tonnes Sn metal

Gillian & Windemere Tin ProspectsThe Company signed option agreements on 17 October 2007 to sell the Gillian prospect for $250,000 in cash and a royalty of 1.5% of total tin sales and subject to renewal of the title, the Windemere prospect for $1 in cash and a royalty of 1.5% of total tin sales to Consolidated Tin Mines Ltd. The transactions were contingent upon Consolidated Tin Mines Ltd listing on the ASX.

Consolidated Tin Mines Ltd exercised the option to acquire the Gillian tenement on 21 February and subsequently listed on the ASX on 26 February 2008.

For

per

sona

l use

onl

y

Director’s Report (continued)

25

NICKELThe Company has two key nickel assets:

1. Nickel Royalty Portfolio• Mt Keith Royalty• Kambalda Royalty• Kingston Royalty

2. The Central Musgrave Project• Wingellina Nickel Prospect• Regional Nickel Sulphide Exploration• Regional Nickel Limonite Exploration

NICKEL ROYALTY PORTFOLIO

Mt Keith RoyaltyThe Mt Keith Royalty is a 0.375% production royalty over all production from BHP Billiton Limited’s Mt Keith nickel project – the largest nickel producer in Australia. There is no expiry date on this royalty.

Kambalda RoyaltyThe Kambalda or East Location 48 Royalty is a 1.35% nickel production royalty payable by Independence Group NL and Goldfi elds Mine Management Pty Ltd over several mining operations, which includes part of the Long and all of the Otter/Juan mines. This royalty expires on 31 August 2009.

Kingston RoyaltyThe Kingston Royalty is a 0.375% production royalty covering approximately 100 square kilometres of mining tenure and 40 lineal kilometres of the komatiite sequence rocks between Mount Keith and Honeymoon Well. These tenements are not currently in production.

Royalty project performance is summarised below:

Royalty 2008 2007

Mt Keith 3,516,115 3,801,072Kambalda 3,244,230 3,890,508Kingston – – ______________________________Total 6,760,345 7,691,580

The net operating profi t after tax for the Royalty Portfolio for the fi nancial year was $2,136,589 compared to $3,865,095 for the previous year. The operating profi t for the current year is lower due to a decline in the nickel price and a reduction in production from both Mt Keith and Kambalda. The royalties were acquired on 19 December 2006 and only profi ts attributable to the period 19 December 2006 to 30 June 2007 is included in the previous period. A dispute has arisen with BHP Billiton over the correct calculation of the Kambalda royalty payments, with BHP claiming the royalty has been overpaid to the Company. The Company has requested an independent audit to be undertaken and does not consider that it is in a position to determine whether any liability exists at this point in time.

For

per

sona

l use

onl

y

Director’s Report (continued)

26

THE CENTRAL MUSGRAVE PROJECT

Wingellina Nickel ProspectThe Central Musgrave Project (“CMP”) is located in the Musgrave ranges trangressing the S.A./N.T./W.A. borders in central Australia and comprises four exploration licences covering an area of approximately 1,800 square kilometres. The Consolidated Entity has commenced feasibility and development studies for the project.

The key geological feature of the CMP is the Wingellina layered intrusive complex. This feature exposes layered ultramafi c stratigraphy of the Giles Complex which is prospective for nickel, cobalt and platinum group metals. The complex consists of a series of stacked sills and dykes of mafi c, ultramafi c and anorthositic composition that were intruded at successively shallower crustal levels.

Metals X is undertaking a detailed feasibility study for the development of a major nickel-cobalt mine at Wingellina. The study is being completed in two phases with the option elimination and fi nancial update feasibility stage compled in mid 2008 and the detailed feasibility stage planned for completion in mid 2009.

Wingellina is a world-class accumulation of nickel-cobalt limonite mineralisation. The feasibility study is focusing on the development of a mine and associated infrastructure to produce approximately 40,000 tonnes of nickel and 3,000 tonnes of cobalt metal per annum with a mine life of over 40 years.

The Wingellina ore is planned to be mined by free-dig conventional open pit methods with estimated overall waste:ore ratio of 0.5:1 for the fi rst 20 years. Limonite ores are planned to be processed by High Pressure Acid Leach (“HPAL”) methodology to produce approximately 110,000 dry tonnes of a mixed nickel and cobalt hydroxide product per annum. The mixed hydroxide product is intended to be sold as concentrate to external refi neries.

To expedite the process, the Wingellina feasibility study has been split into a number of work packages. Individual studies by specialist consultants have been completed. Metals X project personnel are in the process of completing report reviews, and undertaking fi nancial modelling for the project. Finalisation of the fi rst phase of feasibility study is expected in the September 2008 quarter. The study will address all aspects of capital and operating for the project.

Land access agreements to enable the Water licence to be granted have been signed. The water licence applications cover both prospective sedimentary basins including the Cobb Depression and the Northern part of the Offi cer Basin. Desktop studies have indicated high confi dence in obtaining sustainable quantities of good quality water from one or both of these areas.

Metals X has commenced the negotiation process for a Mining Agreement for the Wingellina Project with the Ngaanyatjarra Land Council and the Yarnangu Ngaanyatjarraku Parna Corporation, representing the Traditional Owners. To facilitate the process of obtaining a Mining Agreement as provided for in the existing Access Agreement signed in July 2001, in October 2007 the Company signed a Memorandum of Understanding to address procedural issues and the establish of a coordination committee to represent traditional owners, native title holders and community members in this process.

Regional Nickel Sulphide ExplorationDuring the period the Consolidated Entity continued its search for Nickel Sulphides within the layered intrusive complex. Ground electromagnetic surveys of the postulated gabbro feeder zones within basement rocks that had revealed fi ne and weakly disseminated sulphides, including nickel sulphides (violarite after pentlandite, chalcopyrite, pyrite and pyrrhotite) were completed with no conductors deemed worthy of drill testing outlined.

In the Giles Layered complex, primary mineralisation occurs in three known styles:

1. Primary (magmatic sulphide) Nickel-Copper-PGE’s, as occurs at the Nebo and Babel discoveries of BHP Billiton (ex WMC), near Jamieson;

2. Secondary (oxide) Nickel-Cobalt mineralisation associated with the weathering of ultramafi c rocks of the Giles Complex as at Wingellina; and

3. Vanadium and Titanium magnetite bands associated with the most fractionated and highly evolved portions of the gabbro-troctolite intrusions, as occur in the Jamieson Ranges.

Peterological, geophysical, geochemical and drilling has occurred on key target areas and to date no signifi cant discovery of nickel or copper sulphide mineralisation has been made.

For

per

sona

l use

onl

y

Director’s Report (continued)

27

Regional Nickel Limonite ExplorationWithin the tenure of the Central Musgrave Project, deep oxidation of the ultramafi c units (predominantly dunites) that comprise the layered complex has resulted in the formation of substantial resources of iron-rich nickel-cobalt oxide mineralisation. Exposures of extensive ochreous clays in soils characterise the presence of outcropping nickel limonite mineralisation have been made and in the ensuing years these areas will be drill tested with an expectation of additional limonite nickel discoveries being made.

PHOSPHATE PROJECT

Agaton Phosphate ProjectDuring the period the Consolidated Entity entered into a Heads of Agreement with All Claassic Enterprises Pty Ltd and Bishop Exploration Pty Ltd (the vendors) to establish a 75% Metals X owned subsidiary company (Agaton Phosphate Pty Ltd) to acquire a 90% interest in the Agaton Phosphate Project.

The Agaton Phosphate Project (“Agaton”) is a phosphate sands project located between the town of Moora and the Cooljaroo Mineral Sands areas approximately 120km north of Perth. Agaton is a phosphate sands project, with phosphate occurring as nodules and precipitates within sedimentation phases within the Dandaragan Trough. The phosphate mineralisation is considered to have formed by precipitation during the mixing of cold phosphate rich waters with warm continental shelf waters, as has occurred in the giant phosphate deposits of Florida.

Exploration titles were granted and land access agreements over key areas were entered into during the period. Preliminary shallow seismic geophysics was completed to outline the basement of the trough and phosphate nodule trap structures.

SIGNIFICANT CHANGES IN THE STATE OF AFFAIRSTotal equity increased to $233,432,855 from $168,117,232, an increase of $65,315,623. The movement was largely as a result of increased contributed equity. A further $59,400,000 of capital before capital raising costs was raised through the placement of shares to fi nance project development and fund working capital.

The Consolidated Entity successfully completed the re-start of its Renison Tin Project with shipment of its fi rst concentrates in July 2008. The revised Renison Project has been upgraded to include a copper circuit that will enable the generation of a copper co-product. Production will be approximately 8,500 tonnes of tin metal per annum.

The Consolidated Entity commenced the closure of its Collingwood Tin Project. The Consolidated Entity mined out the majority of its fully developed lodes and ceased operations at the end of the current economic mine life. The Consolidated Entity is in the process of assessing whether it will hold the project on care & maintenance for a future restart, permanently close the operation or sell the project.

SIGNIFICANT EVENTS AFTER THE BALANCE DATEOn 17 July 2008 the Company issued 1,250,000 employee options pursuant to the Employee Option Scheme at an exercise price of $0.45 expiring 31 July 2012.

On 23 July 2008 the Company issued 1,000,000 options as an incentive to a contractor at an exercise price of $0.46 expiring 30 November 2010.

LIKELY DEVELOPMENTS AND EXPECTED RESULTSIt is expected that the Consolidated Entity will continue to receive income from its royalty assets, will continue its exploration, mining, treatment and marketing of tin concentrate in Australia, and will continue its exploration and development of its nickel and phosphate projects. These are described in more detail in the Review of Operations above.

Further information regarding likely developments in the operations of the Consolidated Entity and the expected results from those operations in future fi nancial years has not been included in this report because, in the opinion of your directors, its disclosure would prejudice the interests of the Consolidated Entity.

For

per

sona

l use

onl

y

Director’s Report (continued)

28

ENVIRONMENTAL REGULATION AND PERFORMANCEThe Consolidated Entity’s activities are subject to the relevant environmental protection legislation (Commonwealth and State legislation) at its projects. The Consolidated Entity believes that sound environmental practice is not only a management obligation but the responsibility of every employee and contractor.

During the period our achievements in the environmental area included:

• Continued focus on environmental management; and• Continuous review and improvement of our environmental management systems across all projects.

Bluestone Nominees Pty Ltd the Operator of the Collingwood Tin Mine received a $600 infringement notice during the period as a result of a hydrocarbons discharge from the waste oil sump and a hydraulic leak on an out of service drilling rig.

SHARE OPTIONS

Unissued sharesAs at the date of this report, there were 139,399,196 unissued ordinary shares under option (137,149,596 at reporting date), refer to note 28(e) for further details.

There are no participating rights or entitlements inherent in the options and option holders are not entitled to participate in new issues of capital or bonus issues offered or made to shareholders during the currency of the options.

Shares issued as a result of exercising optionsDuring the fi nancial year 74,326,004 options were exercised to acquire fully paid ordinary shares in the Company at a weighted average exercise price of $0.20, refer to note 28(f) for further details.

INDEMNIFICATION AND INSURANCE OF DIRECTORS AND OFFICERSDuring the fi nancial year, the Company paid a premium in respect to a contract of insurance to insure Directors and offi cers of the Company and related bodies corporate against those liabilities for which insurance is permitted under section 199B of the Corporations Act 2001. Disclosure of the nature of the liabilities and the amount of the premium is prohibited under the conditions of the contract of insurance.

DIRECTORS’ MEETINGSThe number of meetings of Directors’ (including meetings of committees of Directors) held during the year and the number of meetings attended by each Director were as follows:

Directors Meetings Audit Remuneration

No of meetings held: 8 3 1

No of meetings attended:P J Newton 8 – 1P G Cook 8 – –D M Okeby 8 3 1W S Hallam 8 – –M L Jefferies 8 3 –D J Head 3 – –W Wei – – –Y Zhang (Alt Director) 4 – –

All Directors were eligible to attend all meetings held, except for D Head who was eligible to attend 4 meetings before he passed away on 19 November 2007 and W Wei and Y Zhang, his alternate, who were eligible to attend 4 Directors’ meetings following their appointment on 3 October 2007.

For

per

sona

l use

onl

y

Director’s Report (continued)

29

Committee MembershipAs at the date of this report, the Company had an Audit Committee and a Remuneration Committee of the Board of Directors.

Members acting on the committees of the Board during the year were:

Audit RemunerationM L Jefferies * P J Newton *D M Okeby D M OkebyF J Van Maanen ** M L Jefferies

Notes:

* Designates the Chairman of the Committee.** Mrs Van Maanen is the Company Secretary and is not a Director.

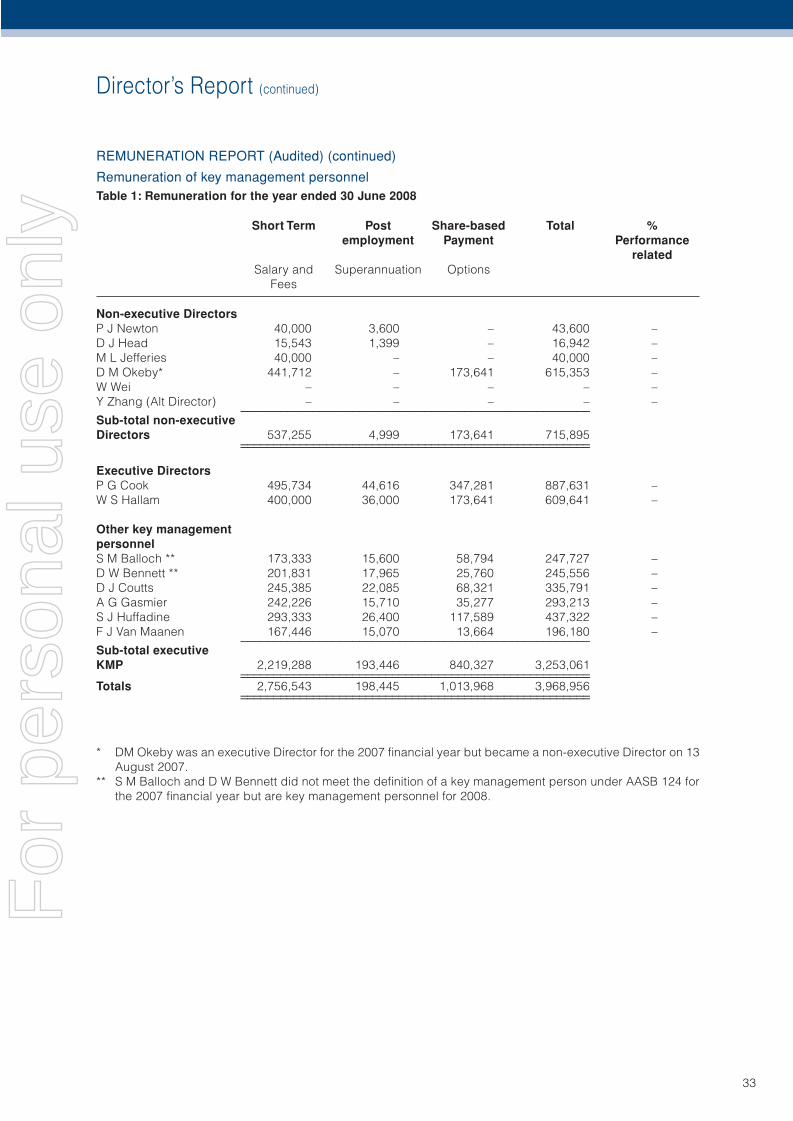

REMUNERATION REPORT (Audited)This remuneration report outlines the director and executive remuneration arrangements of the Consolidated Entity in accordance with the Corporations Act 2001 and its Regulations. For the purposes of this report Key Management Personnel (“KMP”) of the Consolidated Entity are defi ned as those persons having authority and responsibility for planning, directing and controlling the major activities of the Company and the Consolidated Entity, directly or indirectly, including any Director (whether executive or otherwise) of the parent company, and includes the fi ve executives in the parent and the Consolidated Entity receiving the highest remuneration.

For the purposes of this remuneration report, the term ‘executive’ encompasses the Managing Director, senior executives, general managers and secretary of the parent and the Consolidated Entity.

Remuneration CommitteeThe Remuneration Committee of the Board of Directors of the Company is responsible for determining and reviewing remuneration arrangements for the Board and executives.

The Remuneration Committee assesses the appropriateness of the nature and amount of remuneration of executives on a periodic basis by reference to relevant employment market conditions with the overall objective of ensuring maximum stakeholder benefi t from the retention of a high quality, high performing Board and executive team.

Remuneration PhilosophyThe performance of the Company depends upon the quality of its Directors and executives. To prosper, the company must attract, motivate and retain highly skilled Directors and executives.

To this end, the company embodies the following principles in its remuneration framework:

• retention and motivation of key executives;• attraction of quality management to the Company; and• performance incentives which allow executives to share the rewards of the success of the Company.

Remuneration StructureIn accordance with best practice corporate governance, the structure of non-executive director and senior executive remuneration is separate and distinct.F

or p

erso

nal u

se o

nly

Director’s Report (continued)

30

REMUNERATION REPORT (Audited) (continued)

Non-executive Director Remuneration

ObjectiveThe Board seeks to set aggregate remuneration at a level which provides the Company with the ability to attract and retain Directors of the highest calibre, whilst incurring a cost which is acceptable to shareholders.

StructureThe Constitution and the ASX Listing Rules specify that the aggregate remuneration of non-executive directors shall be determined from time to time by a general meeting. The latest determination was on the incorporation of the Company (23 July 2004) and the remuneration was set at $40,000 (excluding superannuation) per year for each non-executive Director, except for Mr Okeby who receives $1,853 (including superannuation) per day for each day worked on behalf of the Company.

The amount of aggregate remuneration and the fee structure is reviewed annually. The Board considers advice from external consultants as well as the fees paid to non-executive Directors of comparable companies when undertaking the annual review process.

Non-executive Directors have long been encouraged by the Board to hold shares in the Company. The shares are purchased at the prevailing market share price. The non-executive Directors are entitled to receive retirement benefi ts and to participate in any incentive programs. There are currently no specifi c incentive programs.

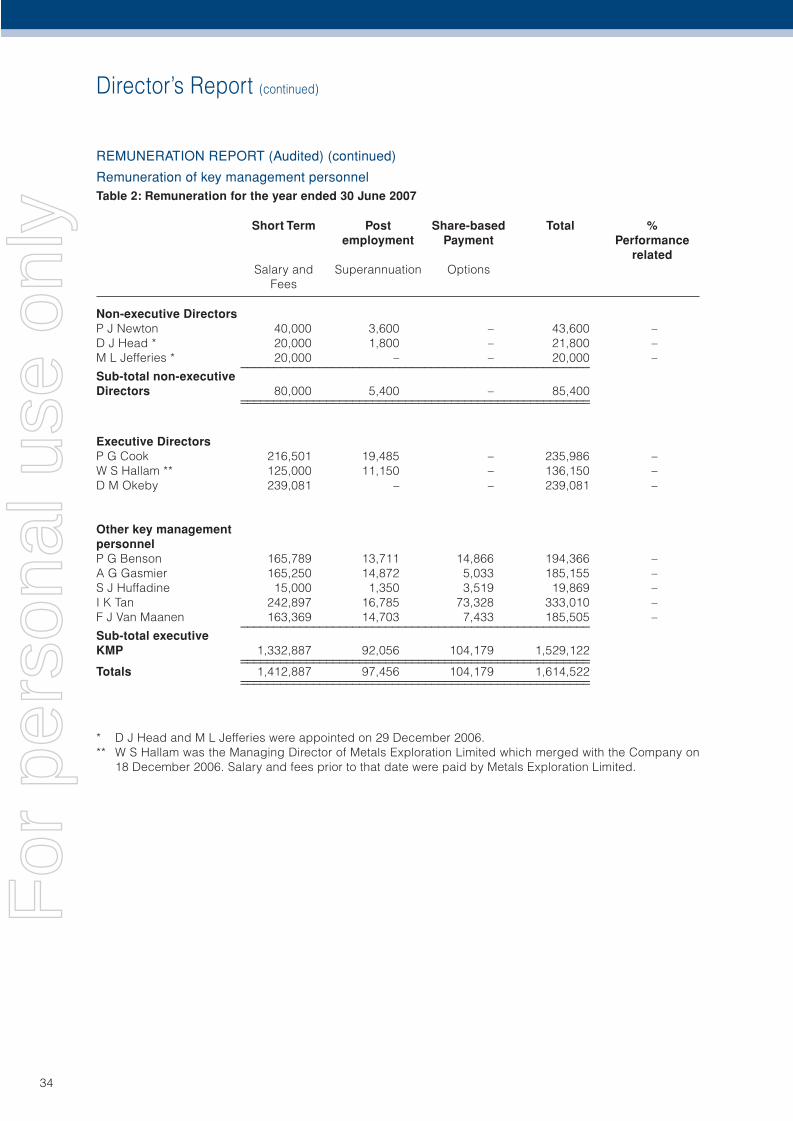

The remuneration report for the non-executive Directors for the year ending 30 June 2008 and 30 June 2007 is detailed in Table 1 and Table 2 respectively of this report.

Executive RemunerationObjectiveThe Company aims to reward executives with a level and mix of remuneration commensurate with their position and responsibilities within the Company. The current remuneration policy adopted is that no element of any executive package be directly related to the Company’s fi nancial performance. Indeed there are no elements of any executive remuneration that are dependent upon the satisfaction of any specifi c condition. Remuneration is not linked to the performance of the Company but rather on the ability to attract and retain executives of the highest calibre. The overall remuneration policy framework however is structured in an endeavour to advance/create shareholder wealth.

StructureIn determining the level and make-up of executive remuneration, the Remuneration Committee engages external consultants as needed to provide independent advice.

Remuneration consists of the following key elements:

• Fixed remuneration (base salary and superannuation); and• Variable remuneration (share options).

The proportion of fi xed remuneration and variable remuneration for each executive for the period ending 30 June 2008 and 30 June 2007 are set out in Table 1 and Table 2.

Fixed RemunerationObjectiveFixed remuneration is reviewed annually by the Remuneration Committee. The process consists of a review of the Company, business unit and individual performance, relevant comparative remuneration in the market and internally and, where appropriate, external advice on policies and practices. As noted above, the Committee has access to external advice independent of management.