Embed Size (px)

Citation preview

Citibank Japan Ltd.

Annual Report For the Fiscal Year Ended March 31, 2014

www.citibank.co.jp

Table of Contents

Message from the CEO 1

Company Overview 2

Our History 5

Management Strategy 6

Business Outline 8

Risk Management Framework 17

Compliance Framework 19

Diversity and CSR Activities 20

Citibank Japan Ltd. Financial Information under Japanese GAAP 21 For the Fiscal Year Ended March 31, 2014

1. Matters Related to Principal Business 22

2. Financial Statements 40

3. Market Value Information 56

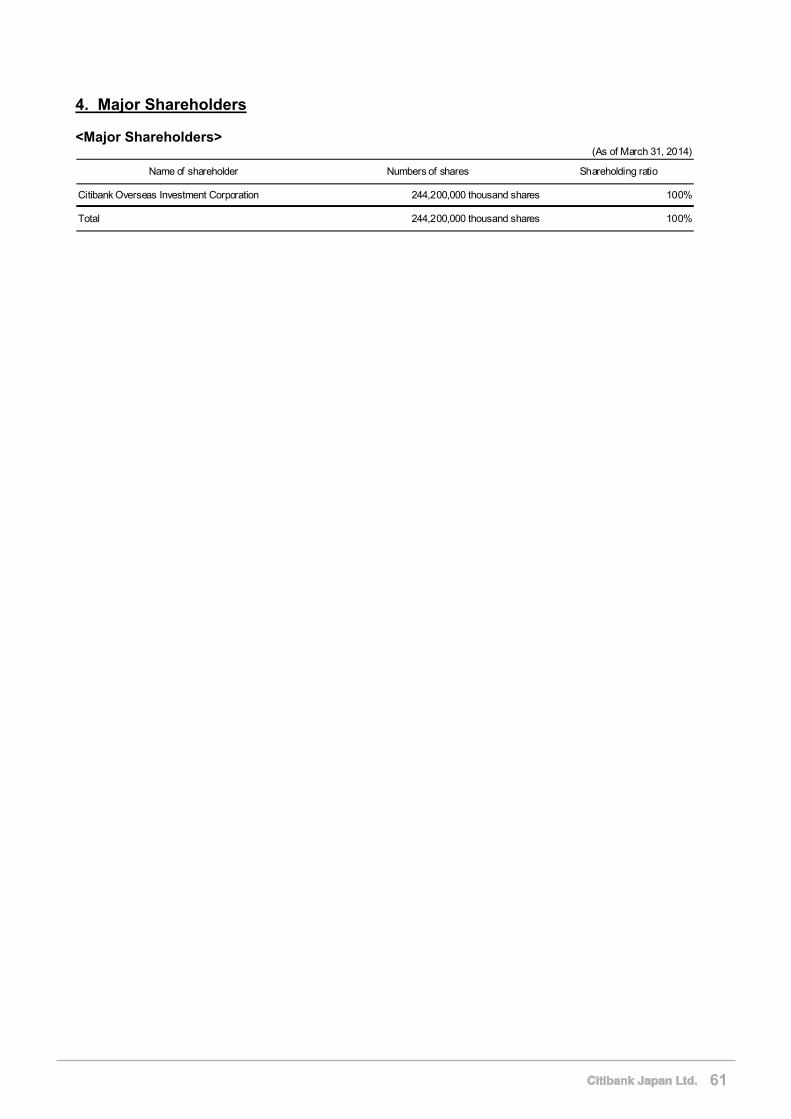

4. Major Shareholders 61

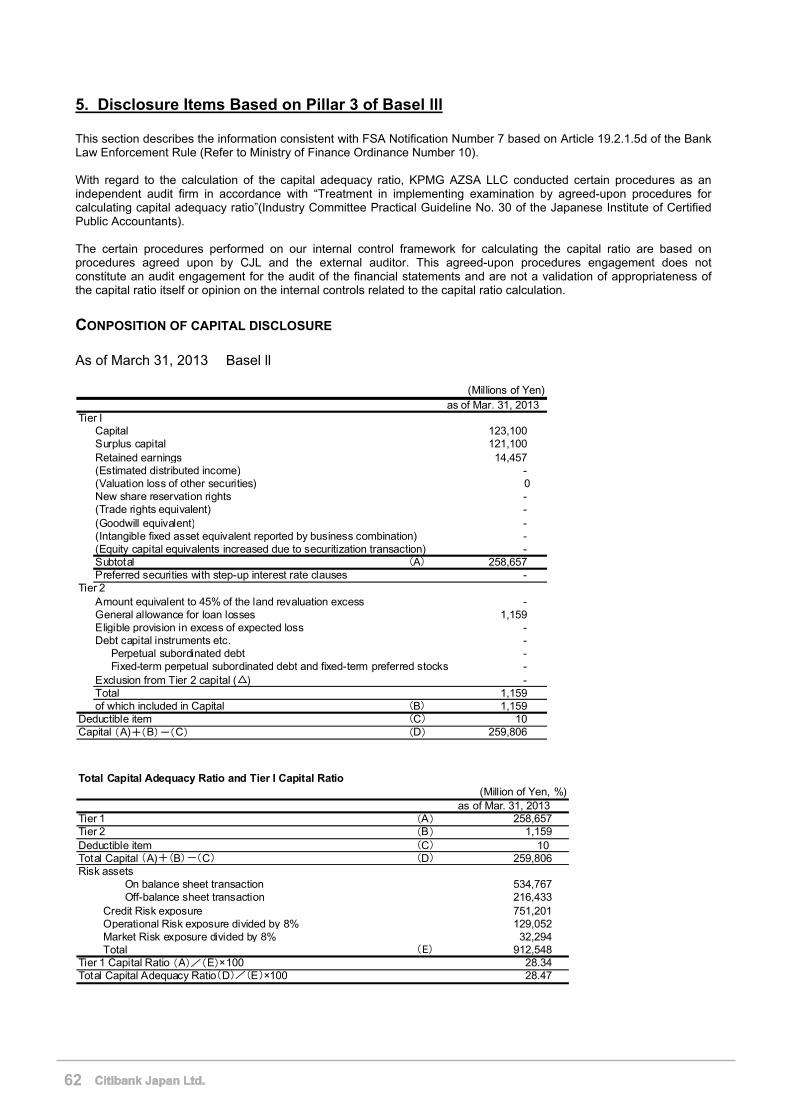

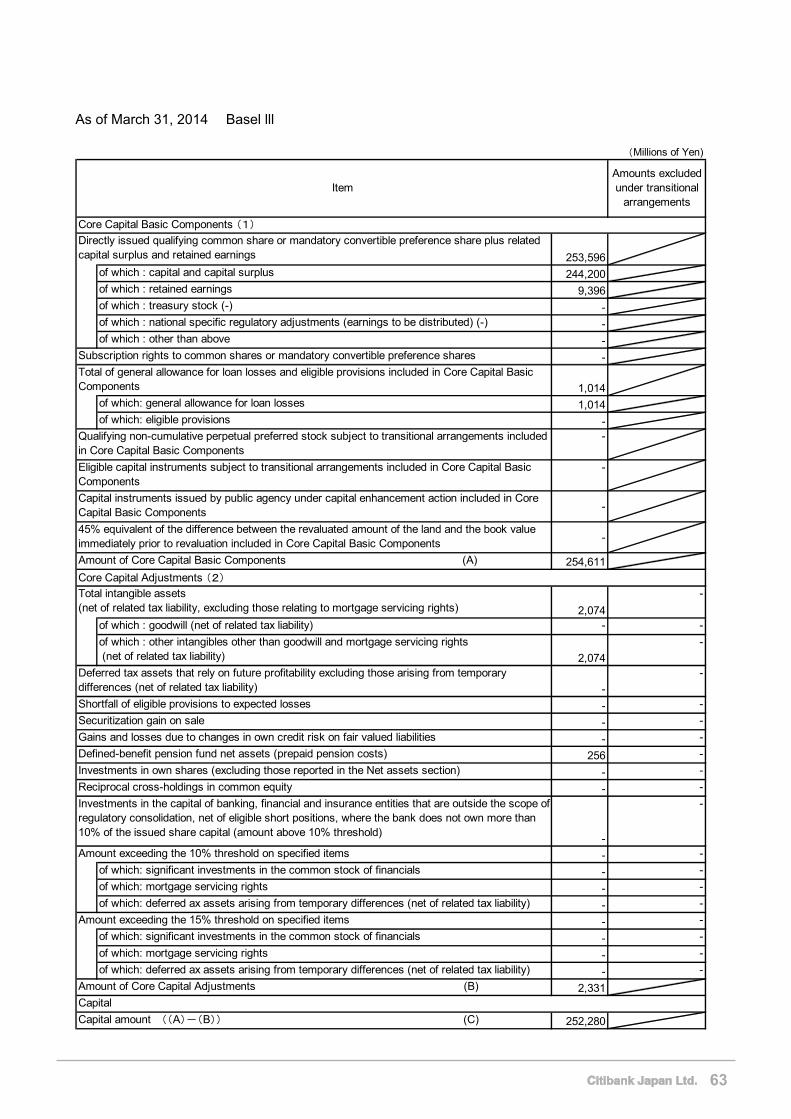

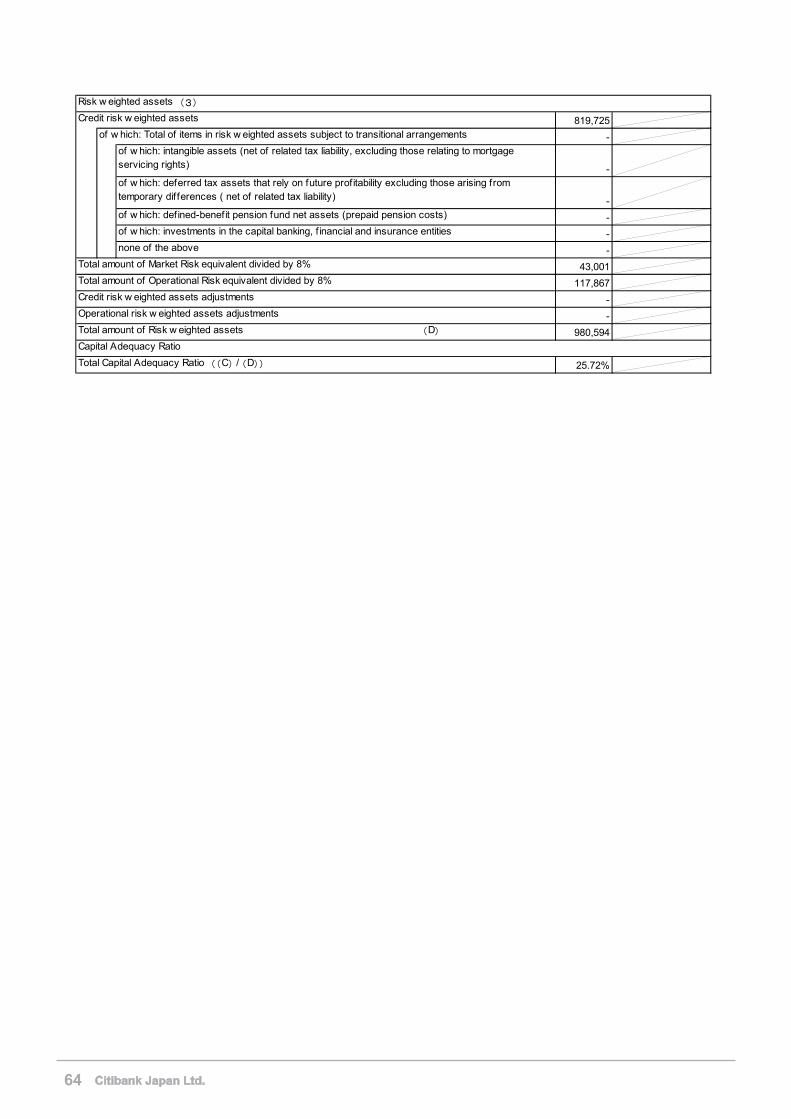

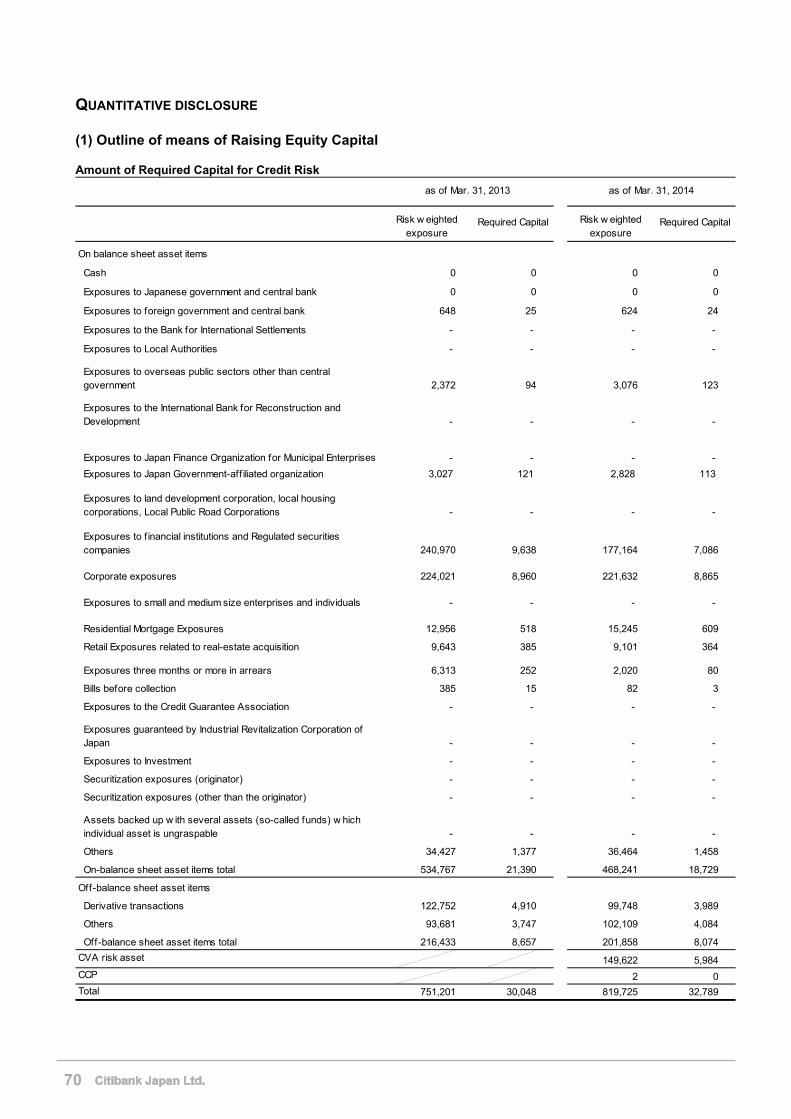

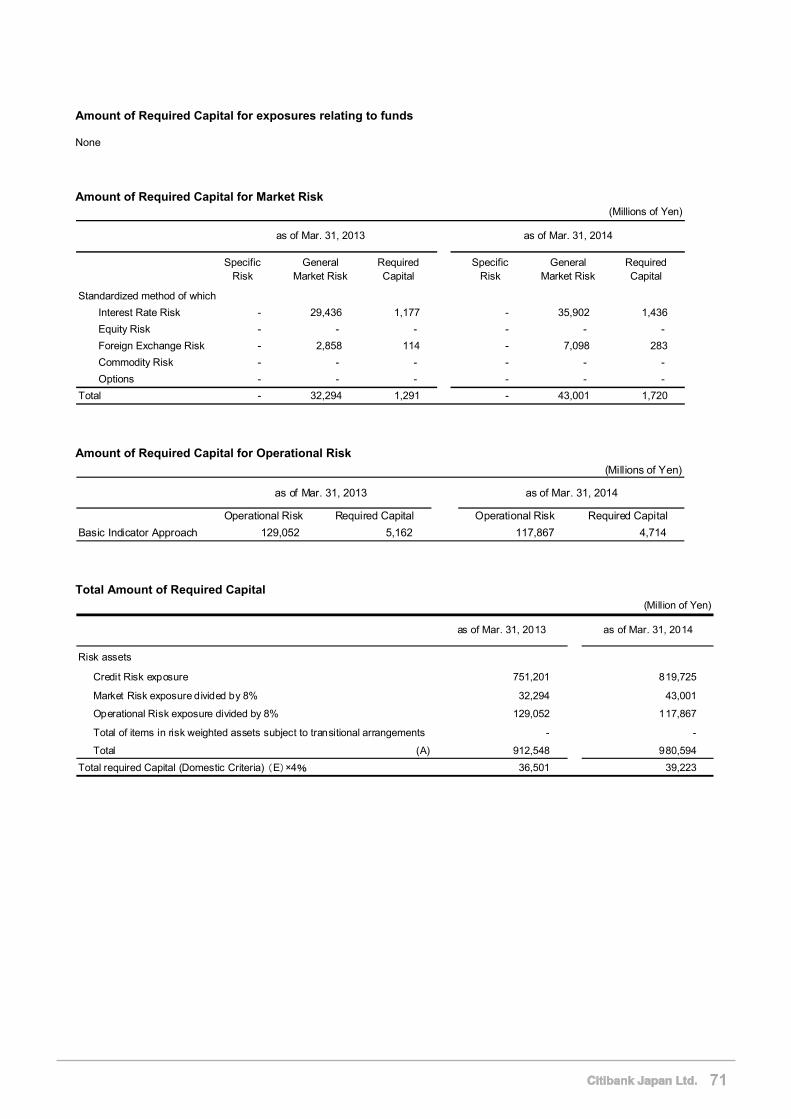

5. Disclosure Items Based on Pillar 3 of Basel III 62

Citibank Japan Ltd. 1

Message from the CEO

To Our Valued Customers,

On June 1, 2014, I assumed the role of President & CEO of Citibank Japan Ltd. It is a great honor to lead this company and proudly serve our clients as we have been doing over our 112 year history. Over that time Citibank Japan has built a reputation for providing innovative and high quality services to our retail, corporate and institutional customers. I am determined to work with our employees to further strengthen our business and continue to improve the quality of our products and services for our customers in Japan and around the world.

Fiscal year 2013 has seen moderate recovery in the Japanese economy, as several measures aimed at boosting the Japanese economy have taken effect. This has brought with it both opportunities and challenges for Japanese individuals and corporations. Citibank Japan is well positioned to help our customers succeed in such an environment.

Citibank Japan is financially strong and well capitalized, and as a part of Citi is a member of a global financial services group that does business in more than 160 countries and jurisdictions. Citibank Japan is committed to being a bank that meets local market expectations, with a strong compliance and governance framework; to serving Japanese consumers, corporations, governments and institutions; and to making our contribution as part of Japan's society and economy.

Thank you very much for your continued patronage and support.

July 2014

Peter B. Eliot Representative Director, President & CEO

Citibank Japan Ltd.

1

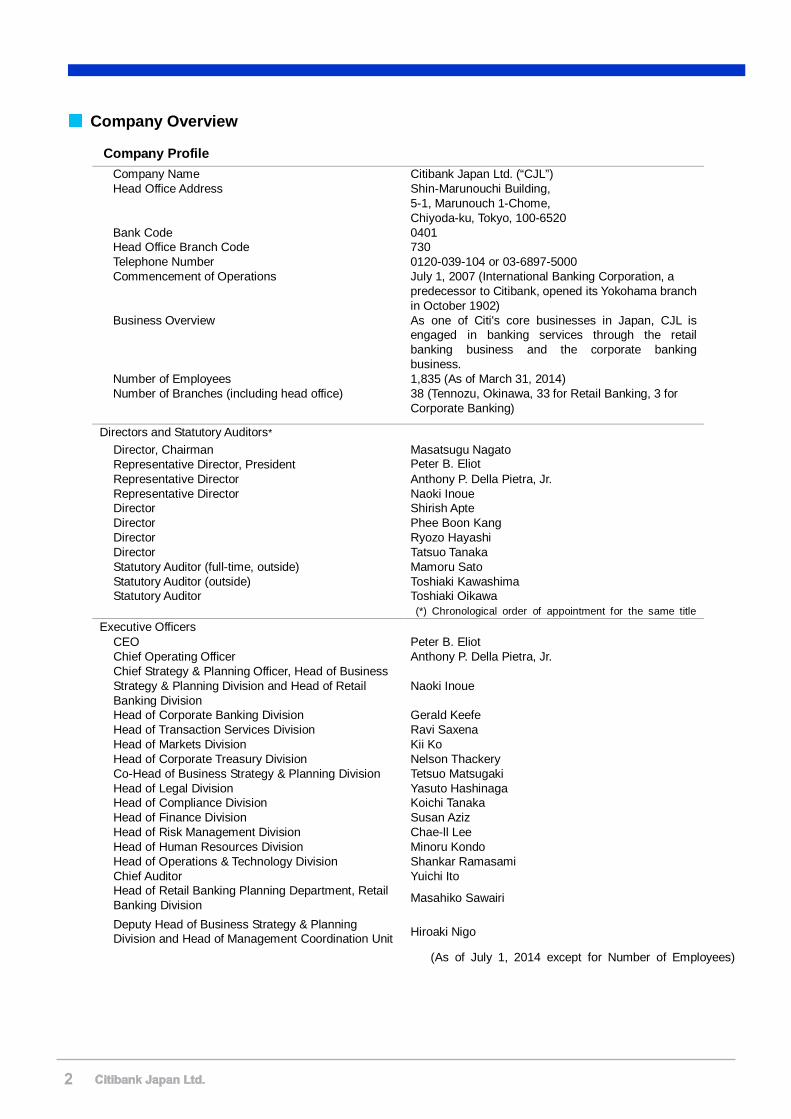

2 Citibank Japan Ltd.

Company Overview

Company Profile Company Name Citibank Japan Ltd. (“CJL”) Head Office Address Shin-Marunouchi Building,

5-1, Marunouch 1-Chome, Chiyoda-ku, Tokyo, 100-6520

Bank Code 0401 Head Office Branch Code 730 Telephone Number 0120-039-104 or 03-6897-5000 Commencement of Operations July 1, 2007 (International Banking Corporation, a

predecessor to Citibank, opened its Yokohama branch in October 1902)

Business Overview As one of Citi's core businesses in Japan, CJL is engaged in banking services through the retail banking business and the corporate banking business.

Number of Employees 1,835 (As of March 31, 2014) Number of Branches (including head office) 38 (Tennozu, Okinawa, 33 for Retail Banking, 3 for

Corporate Banking)

Directors and Statutory Auditors* Director, Chairman Masatsugu Nagato Representative Director, President Peter B. Eliot Representative Director Anthony P. Della Pietra, Jr. Representative Director Naoki Inoue Director Shirish Apte Director Phee Boon Kang Director Ryozo Hayashi Director Tatsuo Tanaka Statutory Auditor (full-time, outside) Mamoru Sato Statutory Auditor (outside) Toshiaki Kawashima Statutory Auditor Toshiaki Oikawa

(*) Chronological order of appointment for the same title Executive Officers

CEO Peter B. Eliot Chief Operating Officer Anthony P. Della Pietra, Jr. Chief Strategy & Planning Officer, Head of Business Strategy & Planning Division and Head of Retail Banking Division

Naoki Inoue

Head of Corporate Banking Division Gerald Keefe Head of Transaction Services Division Ravi Saxena Head of Markets Division Kii Ko Head of Corporate Treasury Division Nelson Thackery Co-Head of Business Strategy & Planning Division Tetsuo Matsugaki Head of Legal Division Yasuto Hashinaga Head of Compliance Division Koichi Tanaka Head of Finance Division Susan Aziz Head of Risk Management Division Chae-ll Lee Head of Human Resources Division Minoru Kondo Head of Operations & Technology Division Shankar Ramasami Chief Auditor Yuichi Ito Head of Retail Banking Planning Department, Retail Banking Division Masahiko Sawairi

Deputy Head of Business Strategy & PlanningDivision and Head of Management Coordination Unit Hiroaki Nigo

(As of July 1, 2014 except for Number of Employees)

2

Citibank Japan Ltd. 3

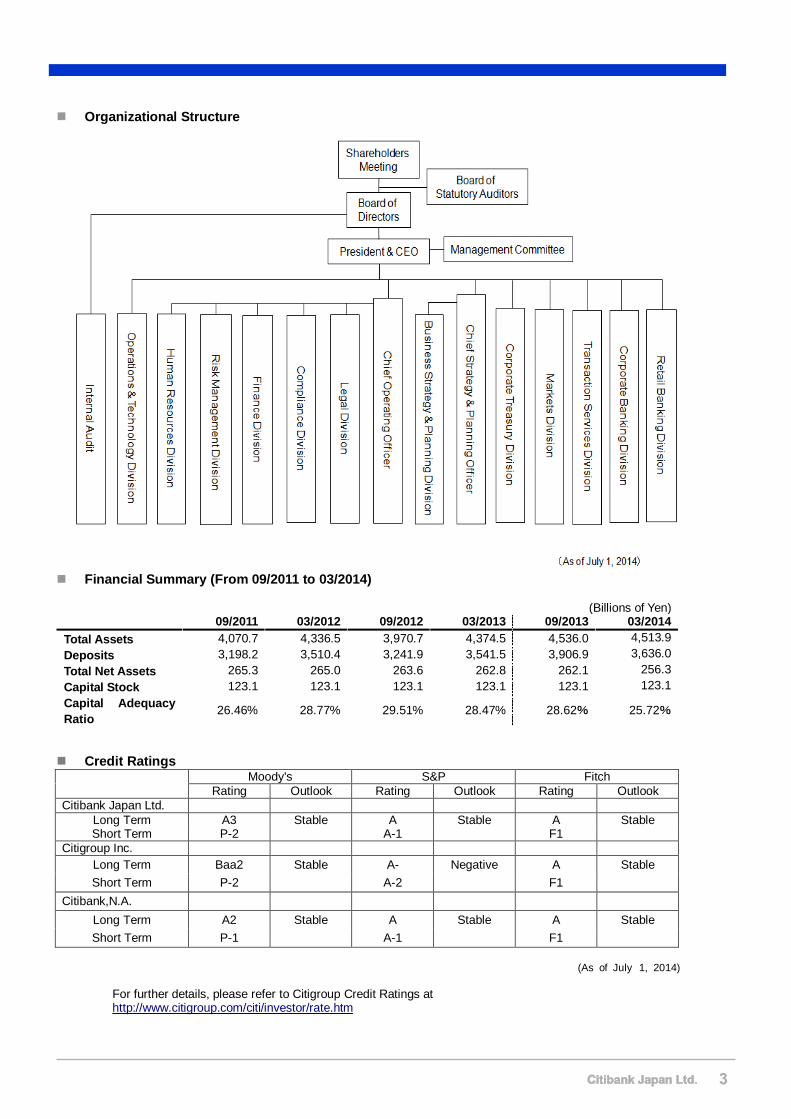

Organizational Structure

Financial Summary (From 09/2011 to 03/2014)

(Billions of Yen) 09/2011 03/2012 09/2012 03/2013 09/2013 03/2014 Total Assets 4,070.7 4,336.5 3,970.7 4,374.5 4,536.0 4,513.9 Deposits 3,198.2 3,510.4 3,241.9 3,541.5 3,906.9 3,636.0 Total Net Assets 265.3 265.0 263.6 262.8 262.1 256.3 Capital Stock 123.1 123.1 123.1 123.1 123.1 123.1 Capital Adequacy Ratio

26.46% 28.77% 29.51% 28.47% 28.62% 25.72%

Credit Ratings

Moody's S&P Fitch Rating Outlook Rating Outlook Rating Outlook

Citibank Japan Ltd. Long Term A3 Stable A Stable A Stable Short Term P-2 A-1 F1

Citigroup Inc. Long Term Baa2 Stable A- Negative A Stable Short Term P-2 A-2 F1

Citibank,N.A. Long Term A2 Stable A Stable A Stable Short Term P-1 A-1 F1

(As of July 1, 2014)

For further details, please refer to Citigroup Credit Ratings at http://www.citigroup.com/citi/investor/rate.htm

3

4 Citibank Japan Ltd.

Deposit Insurance

CJL has its head office located in Japan and is a member of the Deposit Insurance Corporation (DIC). Pursuant to the Deposit Insurance System, non-interest-bearing Yen deposits for payment and settlement purposes accepted by CJL are protected in full per depositor; and interest-bearing Yen deposits accepted by CJL are protected up to a maximum of 10 million yen in principal plus related interest thereon per depositor.

Bank Agency Service

Name of Bank Agent Citigroup Global Markets Japan, Inc. (“CGMJ”) Offices of Bank Agent CGMJ Tokyo Headquarters Service Coverage Intermediary of certain produces offered by CJL’s Corporate

Banking Division (yen/foreign currency deposits and remittance services)

Foreign Bank Agency Service

Designated Dispute Resolution Organization for CJL

Japanese Bankers Association (“JBA”) Contact for consultation and exchange of views: JBA Customer Relations Center 0570-017109 or 03-5252-3772

CJL has concluded a Basic Contract for Implementation of Dispute Resolution Procedure with JBA, the Designated Dispute Resolution Organization under the Banking Act. JBA runs the JBA Customer Relations Center as a contact point to which customers can go for consultation and inquiries or to which they can direct their opinions and complaints about banks. Refer to the JBA website for more information. http://www.zenginkyo.or.jp/adr/ * JBA Customer Relations Center’s services are available only in Japanese.

Name of Affiliated ForeignBank

Citibank, N.A.

Offices of Bank Agent CJL Head Office and Osaka Branch Service Coverage -Intermediation for acceptance of deposits or installment savings

-Intermediation for making of loans or negotiation of bills/notes -Intermediation for exchange transactions -Intermediation for issuance of bank guarantee and acceptance of bills/notes

-Intermediations for other ancillary services(Letter of Credit related)

4

Citibank Japan Ltd. 5

Our History

1812 City Bank of New York established.

1902 International Banking Corporation opened its first branch in Yokohama.

1923 International Banking Corporation opened Tokyo Branch (temporarilyclosed in 1941, reopened in 1946).

1973 First National City Corporation listed on Tokyo Stock Exchange (delisted in1998 with the merger between Citicorp and Travelers Group).

1974 First National City Corporation holding company changed its name to Citicorp.

1977 Citibank N.A. launched Citicard Banking Centers, anchored by ATMs andCitiCard. The 24-hour ATMs are for the first time used for more than emergency cash.

1980 Decades of innovation and expansion lead to Citibank operations in90 countries.

1991 Citibank Japan launches International Cash Card.

1998 Citicorp and Travelers Group merge to form Citigroup Inc.Citibank Japan starts internet banking.

2007 Citibank Japan Ltd. commences operations as a locally incorporated bank.Citigroup Inc.’s shares listed on the first section of the Tokyo Stock Exchange.

2010 Citibank Japan Ltd. opens three smart banking branches in the area ofTokyo and Nagoya.

2011 Citi expands its Japan Desk network around the globe, opening in citiessuch as Manila, Dubai and Sao Paulo.

2012 Citi celebrates its 200th anniversary globally and its 110th in Japan.

5

6 Citibank Japan Ltd.

Management Strategy

Citi’s Mission: Enabling Progress

Citi works tirelessly to serve individuals, communities, institutions and nations. With 200 years of experience meeting the world's toughest challenges and seizing its greatest opportunities, we strive to create the best outcomes for our clients and customers with financial solutions that are simple, creative and responsible. An institution connecting over 1,000 cities, 160 countries and millions of people, we are your global bank; we are Citi.

The four key principles—the values that guide us as we perform our mission—are:

Citibank Japan Management Strategy

Citibank Japan Ltd. (“CJL” or “Citibank Japan”) is a 100%-owned indirect subsidiary of Citigroup Inc. (“Citigroup” or “Citi”). It was established on July 1, 2007 by succeeding the operations of the Japan Branches of Citibank, N.A., thus becoming the first foreign bank in the Japanese market to locally incorporate its banking operations. The bank’s presence in Japan dates back to 1902, when the International Banking Corporation (a predecessor to Citibank) first opened a branch office in Yokohama.

CJL’s goal, in line with global trends and the needs of our client base, is to fully respond to the needs of its retail and corporate clients by leveraging Citi’s global network and local footprint to offer innovative products and services. CJL is uniquely positioned to connect and serve our Japanese corporate and individual clients that are global citizens. We strive to provide seamless global financial solutions in line with our long terms strategy of being Japan’s true global bank aligned with the three global trends of globalization, urbanization and digitization. With strategic coordination across business lines and group companies, CJL aims to continually develop its business and gain increased presence in the Japan market, leveraging its unique position as a locally incorporated foreign bank.

CJL has a long and distinguished history of over 110 years in Japan. We have a proud legacy as a bank of over 200 years of focusing our energy fully on our customers, delivering new innovations and market firsts, bringing the best of the world to our local clients, providing an excellent working environment, and investing in future growth.

CJL continues to focus on a balanced growth strategy through its retail and corporate banking businesses. The retail banking business continually invests in new products, distribution and service innovations to grow its mass affluent customer base and expand its premier Citigold proposition. In addition to broadening the segments we serve and breadth and depth of products we offer, CJL continously strives to better grasp and respond to our customer’s needs as part of our broader startegy of lengthening and deepening our relationships to serve our customers better over time. The corporate

• Common Purpose One team, with one goal: serving our clients and stakeholders.

• Responsible Finance Conduct that is transparent, prudent and dependable.

• Ingenuity Enhancing our clients’ lives through innovation that harnesses the breadth and depth of our information, global network, and world-class products.

• Leadership Talented people with the best training who thrive in a diverse meritocracy that demands excellence, initiative and courage.

6

Citibank Japan Ltd. 7

banking business has a selected core group of relationships which it leverages to deliver Citi's global strengths, providing high quality financial products, services and advice to help our customers succeed. Both the retail and corporate businesses continually look to improve customer experience and operational excellence. CJL is committed to handle earnestly any consultation from Small and Medium-sized Enterprises customers related to business improvement, or those related to the amendments to the existing lending conditions, etc. In addition, CJL will continue its best efforts to fulfill corporate social responsibility to local communities. The Financial Service Agency of Japan (“FSA”) issued an administrative action against CJL on December 16, 2011. In response, CJL submitted a business improvement plan to the FSA on January 31, 2012. CJL takes this administrative action very seriously and implements the business improvement plan including all necessary measures to prevent future occurrence of the problems identified, and endeavors to sustain this improvement actions within the organization. CJL takes seriously its obligations to confront in a resolute manner any undue demands from anti-social forces that threaten social order and safety. CJL is committed to providing a working environment where its employees can thrive and achieve their full potential. The diversity of our workforce is a core value and a source of strength and pride for CJL and our clients. By attracting and training the best people, and providing them broad career development opportunities at every level, we aim to foster an environment where employees are able to provide our clients with outstanding financial products, services and advice that fit their needs over the long term. CJL is proud of its contributions to a broad range of diversity and community initiatives. Our community activities focus broadly on improving access to financial education, assisting those with disabilities, promoting environmental and social sustainability, as well as development of the communities in which we operate. In addition we also continue to enhance the opportunities available to working parents through our childcare center in our head office.

7

8 Citibank Japan Ltd.

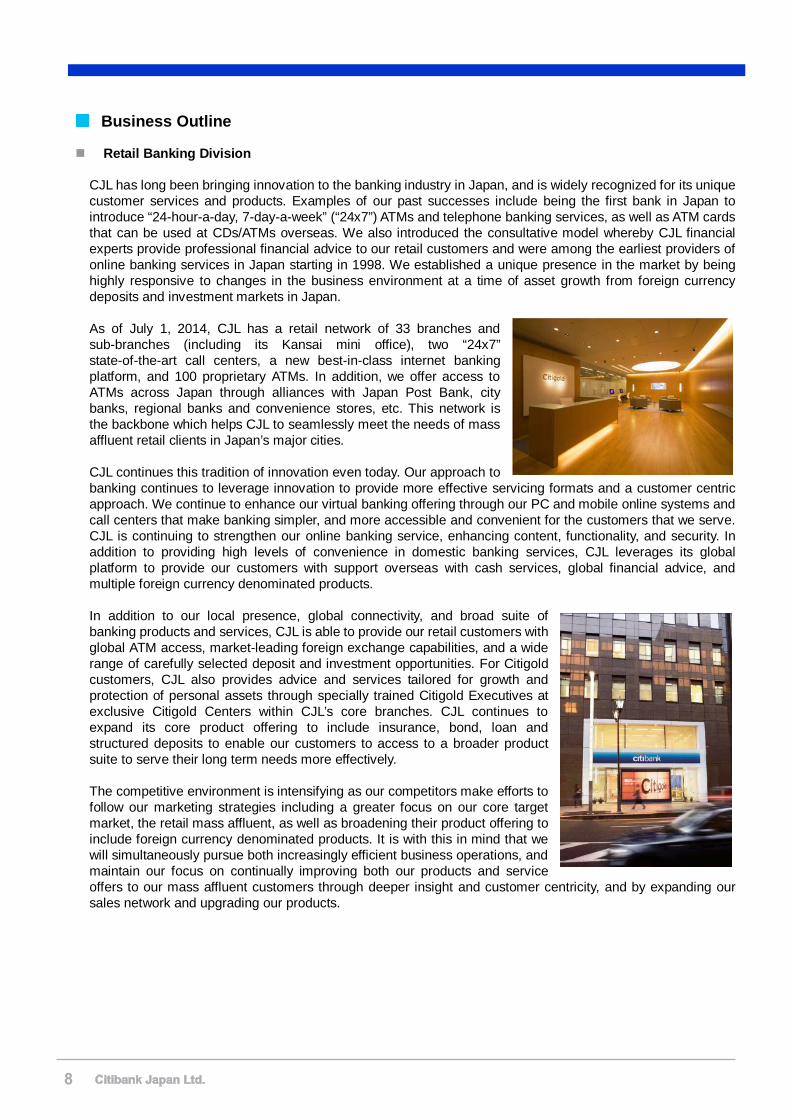

Business Outline

Retail Banking Division

CJL has long been bringing innovation to the banking industry in Japan, and is widely recognized for its unique customer services and products. Examples of our past successes include being the first bank in Japan to introduce “24-hour-a-day, 7-day-a-week” (“24x7”) ATMs and telephone banking services, as well as ATM cards that can be used at CDs/ATMs overseas. We also introduced the consultative model whereby CJL financial experts provide professional financial advice to our retail customers and were among the earliest providers of online banking services in Japan starting in 1998. We established a unique presence in the market by being highly responsive to changes in the business environment at a time of asset growth from foreign currency deposits and investment markets in Japan. As of July 1, 2014, CJL has a retail network of 33 branches and sub-branches (including its Kansai mini office), two “24x7” state-of-the-art call centers, a new best-in-class internet banking platform, and 100 proprietary ATMs. In addition, we offer access to ATMs across Japan through alliances with Japan Post Bank, city banks, regional banks and convenience stores, etc. This network is the backbone which helps CJL to seamlessly meet the needs of mass affluent retail clients in Japan’s major cities. CJL continues this tradition of innovation even today. Our approach to banking continues to leverage innovation to provide more effective servicing formats and a customer centric approach. We continue to enhance our virtual banking offering through our PC and mobile online systems and call centers that make banking simpler, and more accessible and convenient for the customers that we serve. CJL is continuing to strengthen our online banking service, enhancing content, functionality, and security. In addition to providing high levels of convenience in domestic banking services, CJL leverages its global platform to provide our customers with support overseas with cash services, global financial advice, and multiple foreign currency denominated products. In addition to our local presence, global connectivity, and broad suite of banking products and services, CJL is able to provide our retail customers with global ATM access, market-leading foreign exchange capabilities, and a wide range of carefully selected deposit and investment opportunities. For Citigold customers, CJL also provides advice and services tailored for growth and protection of personal assets through specially trained Citigold Executives at exclusive Citigold Centers within CJL’s core branches. CJL continues to expand its core product offering to include insurance, bond, loan and structured deposits to enable our customers to access to a broader product suite to serve their long term needs more effectively. The competitive environment is intensifying as our competitors make efforts to follow our marketing strategies including a greater focus on our core target market, the retail mass affluent, as well as broadening their product offering to include foreign currency denominated products. It is with this in mind that we will simultaneously pursue both increasingly efficient business operations, and maintain our focus on continually improving both our products and service offers to our mass affluent customers through deeper insight and customer centricity, and by expanding our sales network and upgrading our products.

8

Citibank Japan Ltd. 9

<Major Business Activities> We continued to serve our customers based on our positioning as Japan’s True Global Bank, offering a unique set of capabilities from basic banking services to more specialized wealth management offerings including local and global ATM access, market-leading foreign exchange capabilities, a wide range of carefully selected deposit and investment opportunities, insurance products, mortgages and other secured loans, and preferential “Citigold” and “Citigold Premium” services. CJL continues to focus on building out our online offering from both the point of view of expanding our business as offering a better customer experience. We continue to strive to serve our clients better online through enhancing the product selection, functionality, usability and security of Citibank Online, our online banking platform for retail customers. In order to better serve our customer’s long term needs we have enhanced our banking products and services line up to offer a broader range of products across the risk spectrum. We have not only enhanced our insurance products but also strengthened our range of lending products based upon an analysis of customers’ needs. In addition we have also put greater emphasis on publically offered and privately placed fixed income bonds and structured notes. One of our primary focus areas continued to be in lending activities. We broadened the range of customers eligible for our Investment Property Loan, Commercial Real Estate Loan (CRE), and Securities Backed Loan (SDBL) to include our Gold as well as Premium customers. Also, we have launched a new fee structured Housing Loan featuring a low interest rate from April 2014 to better serve our customers' needs. In addition, to help meet our clients’ needs for medium and long-term investments we have continued to expand both the breadth of our Whole Life insurance product line-up denominated in both Japanese Yen and foreign currency as well as our alliance with world leading insurance companies to provide expert insurance specialists to better advise our customers regarding their insurance needs.

9

10 Citibank Japan Ltd.

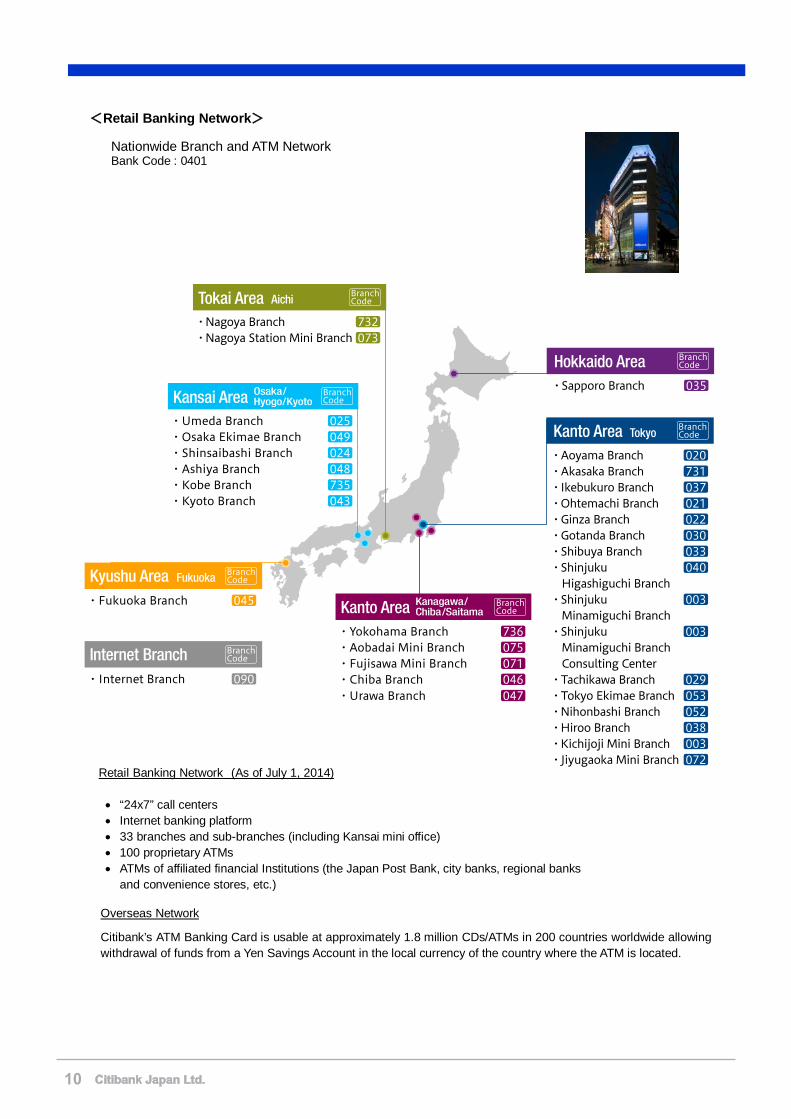

<Retail Banking Network>

Retail Banking Network (As of July 1, 2014)

• “24x7” call centers• Internet banking platform• 33 branches and sub-branches (including Kansai mini office)• 100 proprietary ATMs• ATMs of affiliated financial Institutions (the Japan Post Bank, city banks, regional banks

and convenience stores, etc.)

Overseas Network

Citibank’s ATM Banking Card is usable at approximately 1.8 million CDs/ATMs in 200 countries worldwide allowing withdrawal of funds from a Yen Savings Account in the local currency of the country where the ATM is located.

Nationwide Branch and ATM Network Bank Code : 0401

10

Citibank Japan Ltd. 11

Corporate Banking Division

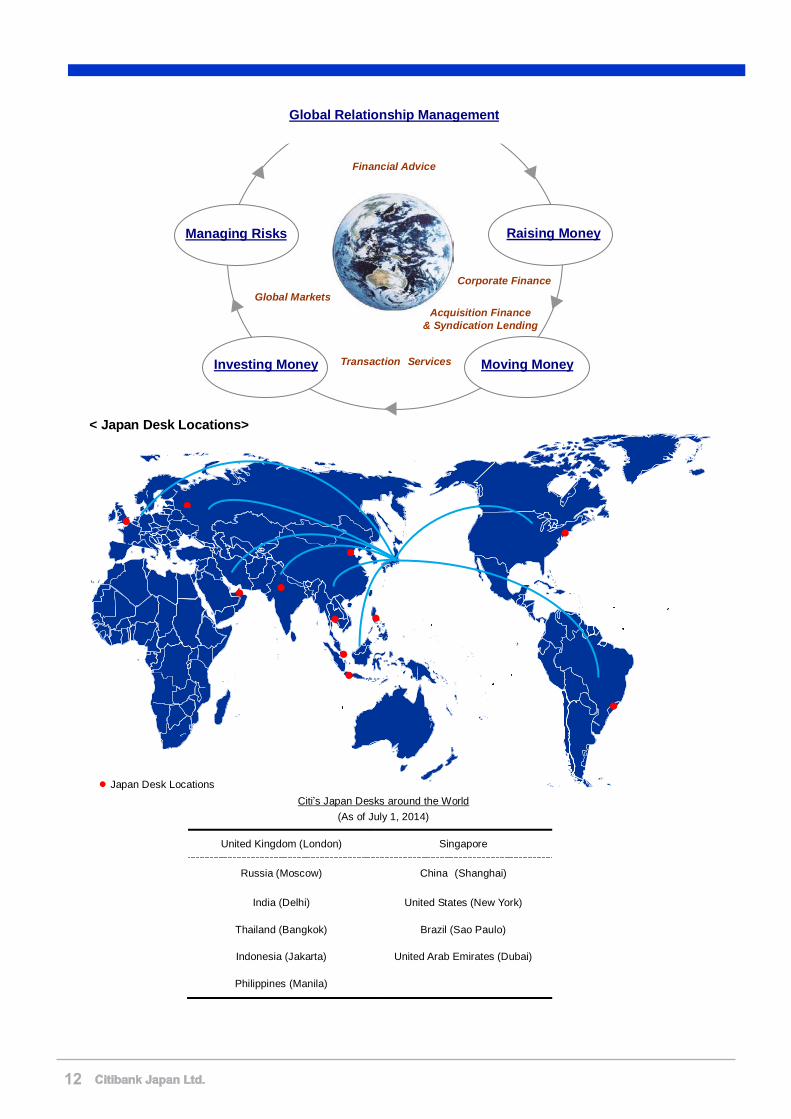

In corporate banking, CJL focuses on providing comprehensive global relationship management services to a targeted set of Japan’s largest multi-national companies and institutions. We coordinate and leverage Citi’s broad range of products and services, together with Citi’s unrivaled global network, in order to support the growth ambitions of our clients both here in Japan and around the globe. CJL’s Corporate Banking Division, located in Tokyo and Osaka, focuses on delivering innovative relationship-driven solutions for our clients’ needs related to both their day-to-day operations and their strategic business objectives. We are one of the leading finance providers in the syndicated loan market in Japan. Furthermore, CJL pioneered the structured finance market in Japan in the mid-1980’s and over the years has played a vitally important role as a market leader in providing innovative solutions to many of our clients. Corporate Banking Division has a client group consisting of relationship managers and a product group responsible for Corporate Finance product development and offering. Citibank Japan Ltd. also has product groups in Transaction Services Division and in Markets Division. The client group and product groups together provide solutions to the diversified client needs. Each client group and product group coordinates across the respective global network within Citi, which enables us to build comprehensive relationships with our clients and their affiliates both in Japan and overseas. This has been the unique and unrivaled strength of Citi. <Major Business Activities> Our client coverage model consists of 3 departments: Corporate Relationship Management Dept., Financial Institutions & Public Sector Relationship Management Dept. and Global Subsidiaries Group Relationship Management Dept. Each client coverage department is committed to serving the unique needs of their client set, by combining information and services with specialized Industry insight. By combining a deep understanding of each client’s unique needs with a view of key industry trends, we are in a position to tailor structured solutions to help our clients meet their growth ambitions. We focus on responding to our clients’ various day-to-day needs, as well as strategic business objectives by offering financing alternatives and bank capital in an effort to build and further deepen long term relationships. Corporate Banking Division works closely with 3 product groups of Citibank Japan Ltd. - Transaction Services Division (Cash Management, Trade Finance, Securities Fund Services and Export Agency Finance), Markets Division (Foreign Exchange and Risk Treasury) and Corporate Finance Department (Structured Finance, Real Estate and Acquisition Finance & Syndicated Lending) - to serve our clients and provide solutions that meet their needs. We have further strengthened our capability to support our Japanese clients around the globe through “Japan Desks” offering exclusive relationship management efforts by experienced bankers. We are located in 11 countries. Many of these Japan Desks provide coverage to neighboring countries and jurisdictions. Our client support structure has become increasingly more available pan-regionally around the globe, covering North and South America, Europe, Middle East, Africa, and Asia. Citi’s Japan Desk Network is an unrivaled and unique service to our clients. Our bankers at Japan Desks leverage their vast experiences in Japan, continue to build and further deepen great relationships with our clients and colleagues around the globe, and support our clients to meet their financial needs.

11

12 Citibank Japan Ltd.

< Japan Desk Locations>

United Kingdom (London) Singapore

Russia (Moscow) China (Shanghai)

India (Delhi) United States (New York)

Thailand (Bangkok) Brazil (Sao Paulo)

Indonesia (Jakarta) United Arab Emirates (Dubai)

Philippines (Manila)

●

●

●

●

●

●

●

●

● Japan Desk Locations

●

●

●

Global Markets

Financial Advice

Acquisition Finance & Syndication Lending

Transaction Services

Managing Risks

Global Relationship Management

Investing Money Moving Money

Raising Money

Corporate Finance

Citi’s Japan Desks around the World (As of July 1, 2014)

12

Citibank Japan Ltd. 13

Transaction Services Division

Transaction Services Division provides various services in the Treasury and Trade Solutions (TTS) and Securities Services (SS) businesses. Our services integrate cash management, trade finance, and securities services to multinational corporations, financial institutions and public sector clients in Japan and around the world.

Transaction Services is closely aligned with three important on-going trends - globalization, urbanization and digitization – and as the business world continues to get smaller and our clients continue to expand globally, we have been stepping up support to assist our Japanese and other global clients expand. Capability Leveraging the industry's largest proprietary network, we serve both the local and cross-border interests of clients. As Japanese companies continue the process of rapid globalization, Citi is positioned to be their partner and Global Bank. CJL Transaction Services is part of Citi’s global network servicing clients in over 100 countries and top cities in the world. Experience Transaction Services is part of Citi’s legacy in Japan which dates back over 110 years to when we opened our first Japanese branch. We strive to be a trusted advisor on industry issues such as local securities markets, emerging markets, settlement risk, receivables and payment processes, securities infrastructure and technology integration to our clients, regulatory organizations and third-party partners. Innovation Our on-line portal, CitiDirect BE and its mobile/Tablet version are examples of Citi’s investments in innovation that add to our offering of solutions in Japan. We introduced a Japanese language version of our mobile smart phone application and launched Tablet version in 2013. We also provide our clients in Japan with Treasury analytics and technology tools to enhance their efforts to effectively manage their businesses.

< Major Business Activities >

Treasury and Trade Solutions Citi serves our clients in as an industry leader in cash management solutions. With 232 connections to Cash clearing systems across the globe, Citi has a global infrastructure providing a wide range of innovative financial solutions. Our extensive network of qualified banking professionals provides a combination of local knowledge and global expertise to help meet clients’ strategic business goals. Citi's portfolio of global cash management products offers tailored solutions to help manage collection and payment processes by establishing interfaces between the client’s treasury system and Citi's payment systems. Trade Finance and Services Unit provides web-based, simple and quick supplier financing for not only domestic purchases but also cross-border international trade transactions. Various risk-hedge solutions are provided to clients’ exports to help them effectively manage their risk and supply chains. In addition to traditional financial support for exports and investments from Japan, our Export and Agency Finance Unit has started to provide new services such as medium-long term loans for overseas Japanese subsidiaries’ exporting and agricultural commodities imported by our clients in Japan. Securities Services In Securities Services, CJL supports foreign investors’ investment in Japanese securities through our stable capabilities in custody services. In addition to such traditional services, the introduction of innovative Third Party Clearing offerings allow our resident intermediary clients to focus on what matters most, to grow core businesses through our clearing and settlement outsourcing solutions. Our proprietary network is the largest in the industry covering 61 markets surpassing our closest competitor by over 20 markets.

13

14 Citibank Japan Ltd.

2013 Japan Awards Best Overall Internet Bank - Global Winner by Global Finance, World’s Best Internet Banks 2013 Best Corporate / Institutional Internet Bank – Global Winner by Global Finance, World’s Best Internet Banks

2013 Best Overall Trade Finance Bank in Asia Pacific – Trade Finance 2013 Trade Finance Deal of the Year for NEXI untied loan to Vinacomin – Trade Finance 2013 Top Rated in Japan for Leading Clients Category and Cross-Border/Non-Affiliate Category in Global

Custodian’s Agent Banks in Major Markets Survey 2013 Best Subcustodian in Japan for The Asset’s Triple A Asset Servicing Awards 2013

14

Citibank Japan Ltd. 15

Markets Division

The Markets Division is a division, established in July 2013, with a mission to provide foreign exchange, money market and derivative products and services to the customers of the Corporate Banking Division and the Transaction Services Division. Prior to its establishment, these services were provided by the Markets Department in the Corporate Banking Division and the Treasury Division. An independent division was established to focus on market trades and aim to build a more robust transaction base for customers by providing more valuable information. The Markets Division consists of two departments, Market Sales and Risk Treasury. The Market Sales Department consists of two units, Corporate FX Sales Unit and Corporate Derivative Sales Unit, and conducts foreign exchange and derivative transactions for the customers of the Corporate Banking Division and the Transaction Services Division. The Corporate FX Sales unit leverages Citigroup’s international network and global resources to deliver real-time information to the customers. The unit also provides various types of risk-management related advice and foreign exchange transaction support, building on its well-established and powerful presence as a “market maker” in the foreign exchange market. The Corporate Derivative Sales unit offers a wide range of derivative solutions to the customers, in order to satisfy their diverse needs. The Risk Treasury Department leverages Citigroup’s extensive international network to provide money market transactions in various currencies, in order to meet the customers’ funding and investment needs. Risk Treasury also acts as a funding department in CJL. Based on the policy decisions of the Asset Liability Committee, a sub-committee of CJL’s Management Committee, Risk Treasury ensures appropriate liquidity management and conducts Banking account management as part of the comprehensive risk management framework, in coordination with the Corporate Treasury Division, which is responsible for liquidity risk management.

15

16 Citibank Japan Ltd.

List of CJL’s Major Activities

CJL provides the following services:

1. Acceptance of Deposits Current deposit, savings deposit, time deposit, negotiable certificate of deposit, foreign currency deposit, etc.

2. Fund Lending etc.

Loan on bills, loan on deeds, overdraft, discount of commercial bills, etc. 3. Fund Transfer, etc.

Outward/inward remittance, fund transfer and collection of payment 4. Foreign Exchange, etc.

Foreign exchange transactions (including foreign currency sales and purchase) 5. Others

(1) Guaranty of liabilities (acceptance of payments), issuance of letter of credit and acceptance of bills

(2) Arrangement for syndicated loan (3) Trade finance (purchase of trade notes, etc.) (4) Investment / Trading in securities (Japanese government bonds, etc.) (5) Acquisition or transfer of monetary claims, and securitization related services (6) Handling of receipt of money and other affairs pertaining to money of Government of Japan, local

public authorities, and companies, etc. (7) Dealing in financial derivatives (interest rate, currency, etc.) (8) Over-the-counter sales of mutual funds and insurance products (9) Safekeeping and transfer of securities, etc. (10) Brokerage for clearing of securities, etc. (11) Handling of private placement of securities (12) Financial instruments intermediary service (13) Money exchange (14) Foreign Bank Agency Service (15) Transaction service for electronically recorded monetary claims

16

Citibank Japan Ltd. 17

Risk Management Framework

Risk Management Structure CJL’s risk management framework balances strong corporate oversight by the Board of Directors with well defined oversight roles and responsibilities amongst the Control functions covering the various risk types. CJL has the following three layers of risk management or control:

1) Risk ownership by the business divisions 2) Oversight by the control functions 3) Independent Assessment by Internal Audit

All three layers of control work together to achieve CJL’s shared goals with the following particular items:

• To maintain a highly effective control environment and to establish efficient, proactive risk management; and

• To foster appropriate solutions for our customers and to facilitate business growth in accordance with agreed strategic goals and with the risk management capacity of CJL

CJL establishes a fundamental principle “Comprehensive Risk Management Policy” which is approved by Board of Directors and it defines its risk management structure. Additionally, CJL establishes “Comprehensive Risk Management Rules” to define its risk management procedures. CJL adopts a comprehensive risk management approach and a Comprehensive Risk Manager who oversees risks will ensure that Management Committee and the Board of Directors are kept advised of the risks of and to CJL in a comprehensive management.

Type of risk to be managed CJL identifies credit risk, market risk, liquidity risk, and operational risk as major risks and those are subjected to manage.

• Credit Risk

1. Structure of Credit Risk Management: Credit risk is the risk of loss arising from decline in asset value attributable to deterioration of obligor’s credit condition. It includes the risk of difficulty to collect principal and interest due to default of obligor and decline in credit value due to increase of reserves arising from deterioration of obligor’s credit condition. CJL establishes “Credit Risk Management Policies” which defines the fundamental principle to comprehensively manage its credit risk in Corporate Banking Division and Retail Banking Division. In terms of credit management in each division, CJL also follows “Institutional Client Group Risk Management Manual”, “Global Consumer Credit and Fraud Risk Policies” and “Global Commercial Credit Policies” in order to set and govern credit risk management structure. Furthermore, Credit Risk Management Committee (“CRMC”) is established and managed by Head of the Risk Management Division to oversee CJL’s credit risk including the management of self-assessment of assets with further involvement of management.

2. Procedure of Credit Risk Management: CJL manages credit risk based on obligor analysis and whole portfolio analysis, monitoring concentration of credit to certain industries, ratings, obligors on relationship basis and delinquency trend of a portfolio. Such portfolio view of our credit exposures is reviewed and reported to the Credit Risk Management Committee in a timely manner.

17

18 Citibank Japan Ltd.

• Market Risk / Liquidity Risk

1. Structure of Market Risk / Liquidity Risk Management: Market risk is the risk of loss resulting from fluctuating value of financial asset and debt position which CJL possesses or executes, reflecting market trend. Liquidity risk is the risk of loss resulting from unavailability to secure sufficient asset liquidity against debt due to rising financing costs or mismatch of use of funds and source of funds. In CJL, market risk and liquidity risk management structures are established and operated in accordance with the “Liquidity Risk Management Policy”, the “Market Risk Management Policy” or related management policies. Furthermore, CJL has established Asset Liability Committee (“ALCO”) which is chaired by President and Head of the Corporate Treasury Division to oversee market risk and liquidity risk, monitoring accrual portfolio and trading portfolio of CJL and managing balance sheet as well as capital adequacy.

2. Procedure of Market / Liquidity Risk Management:

CJL Market Risk Management captures consolidated profiles of interest rates and durations of the financial assets and liabilities, performs risk monitoring process using gap analysis and interest rate factor sensitivity analysis, and reports the result to the ALCO meeting on a monthly basis. CJL’s market risk amount is measured by Value-at-Risk (“VaR”) method quantitatively and its regulated compliance status is monitored. ALCO is managing Liquidity Risk by monitoring various liquidity ratios such as Large Fund Provider concentration ratio, Total Customer Deposits / Total Customer Loans ratio. ALCO is also monitoring whether there is sufficient liquidity to meet all maturing obligations within 12 months under the Highly Stressed Market Disruption stress scenario.

• Operational Risk

1. Structure of Operational Risk Management: Operational risk is the risk of loss resulting from inadequate or failed internal processes, systems, or human factors, or from external events. It includes reputation and franchise risks associated with CJL’s business practices or market conduct. It also includes the risk of failing to comply with laws, regulations, ethical standards, regulatory administrative actions or Citigroup policies. To comprehensively manage operational risk, CJL establishes policies and rules for operational risk which clearly defines risks, the control environment, as well as assessment and reporting procedures. CJL separately manages its Jimu risk and System risk in accordance with the established policies and standards. Moreover, CJL has established Enterprise Risk Management Unit under Risk Management Division as a responsible unit for comprehensive operational risk management. The status update of operational risk management is reported to Business Risk, Compliance & Control Committee (“BRCC”), and Jimu risk and System risk are reported to System and Operations Committee (“SOC”), with further involvement of management.

2. Procedure of Operational Risk Management: CJL adopts a Manager’s Control Assessment (“MCA”) program as a tool to manage ‘significant’ operational risks. The MCA is used to self-assess key operational risks and controls and identify and address weaknesses in the design and/or effectiveness of internal controls that mitigate significant operational risks. Corrective actions are monitored continuously for full implementation. Results of MCA are reported managements through BRCC at quarter end. Critical operational processes of each business department are reviewed periodically in consideration of changes to the operational processes and regulatory environment, and latest information shall be reflected into MCA

18

Citibank Japan Ltd. 19

Compliance Framework

Basic Policy

As a bank, CJL fully recognizes the importance of its social responsibilities and the public nature of its business. We understand that conducting business with fairness and integrity based on the Code of Conduct and in compliance with laws and regulations, etc. is the basic principle of our management.

Compliance Management Framework

CJL’s Compliance Division covers compliance related matters and is independent from businesses. The Division consists of 5 units under the Head of Compliance Division; (i) Retail Banking Compliance Unit, (ii) Corporate Banking Compliance Unit, (iii) Anti-Money Laundering Compliance Unit, (iv) Infrastructure Unit and (v) Compliance Testing Unit. The first two units are responsible for compliance matters relevant to businesses, AML Compliance Unit covers matters relevant to anti-social forces and the prevention of money laundering, and Infrastructure Unit is responsible for matters relevant to overall banking operations. Compliance Testing Unit has responsibility for testing to assure that controls over compliance matters are reasonably designed and functioning effectively. The Compliance Division owns the Code of Conduct and, in accordance with Compliance Policy, promotes compliance and cultivates a compliance mindset, through following activities.

The Compliance Division reports compliance related issues and compliance status to the Business Risk, Compliance and Control Committee and the Management Committee on a regular and ad-hoc basis. Material issues are to be escalated to the Board of Director through the Management Committee.

Preventive Measures against Anti-Social Forces and Money Laundering

CJL considers that preventive measures against anti-social forces and money laundering are one of the most important parts of legal compliance as a financial institution with public nature, and has continued its efforts to establish a proper prevention framework.

Measures against the Breach of Legal Compliance

It is the responsibility of each of the directors and the employees to comply with the Code of Conduct that provides an overview of some of the key policies of which all need to be aware. We strongly encourage employees to raise concerns or questions regarding ethics and applicable laws, regulations and policies, and to report violations and suspected violations in accordance with the relevant internal policies. We believe that it is critical to identify issues at an early stage and proactively resolve those issues in order to maintain the highest standards of conduct required at a financial institution. CJL has established, in addition to the standard reporting procedures, an Ethics Hotline in order to properly take measures for a violation or a suspected violation of legal compliance.

• Advice and support related to Compliance • Creation and execution of internal rules related to Compliance • Oversees the development and maintenance of adequate risk management systems related to

Compliance • Education and training related to Compliance • Monitors legal and regulatory development that affect the Bank • Oversees the development and maintenance of adequate risk management systems related to

Anti-Money Laundering activities, including customer identification and matters related to Anti Social Forces

• Conducts Compliance Testing

19

20 Citibank Japan Ltd.

Environment

CJL believes that working to promote environmental and social sustainability is a good business practice. Under the banner of “Green Citi”, we are committed to protect the environment through the following initiatives: <Major Activities>

- The Equator Principles - The Carbon Principle (Citi was a drafting member and has adopted these principles) - Achieved LEED (Leadership in Energy and Environmental

Design) Certification Received Silver certification: Citibank Tokyo Call Center

(June 2009) Received Gold certification ・Aoyama Branch (May 2010) ・Nihonbashi Branch and Tokyo Ekimae Branch (July 2011) ・Nagoya Branch (October 2011) ・Shinjuku Higashiguchi Branch and Kobe Branch (April 2012) ・Ikebukuro branch (July 2012), Shinjuku Minamiguchi Branch (Sep. 2012)

- Office Initiatives Energy and Resource Savings Paperless processes Recycling in the office

Diversity and CSR Activities

CJL pursues Corporate Social Responsibility (“CSR”) activities in alignment with Citi’s global policies and priorities. We embrace the responsibility, as a socially responsible financial group, to make a difference in the community and to promote environmental and social sustainability by building positive relationships with customers, employees and their families, the community, and stakeholders. Through our CSR activities, we respond to corporate governance and compliance initiatives and also reinforce our commitment to Financial Education, Community Development, the Environment, and Diversity with employees from various backgrounds and nationalities.

Diversity

CJL values and promotes Diversity as a strategic activity. By respecting and accepting various values, ways of thinking and attributes such as nationality, age, gender, sexual orientation, language and religion, we create an environment where differences are respected. Creating an environment where Diversity thrives, actively encourages a wide range of thoughts and ideas in support of our business goals. We encourage our employees to participate and take responsibility for their engagement in Diversity activities, internally and externally which adds to the richness of the society in which we live. <Major Activities>

- Improving career development for women; Celebrating women’s success , International Women’s day 2014

- Work-Life Balance - Encourage the hiring of people with

disabilities

Community Development

CJL strives to make a difference where our employees live and work. We encourage and provide support for philanthropic activities undertaken by our employees and their families, leading many of them to participate actively in the community. <Major Activities>

- Support for the disaster-impacted areas: Volunteer activities by the employees and family, Relief Donations by the employees and the customers, Grants to NPO’s actively engaged in the disaster-impacted areas.

- United Nations World Food Program (WFP) School Feeding Initiatives through Cafeteria Charity Program "Share Your Lunch"

- FIT (Financial Industry in Tokyo) for Charity Run - YMCA Charity Run - Citi Volunteer Program - Global Community Day - Supporting NPOs and NGOs

Financial Education

Taking advantage of our business expertise, we provide various financial education programs ranging from elementary school to mature adults. We provide learning materials and support for financial education programs, so that the next generation of children can learn not just about money and the economy, but also how to think effectively, and ultimately plan their careers and lives in order to realize their dreams. We launched a new financial education program for mature women in 2011. <Major Activities>

- Student City - Travel to the Future - MESE (Management Economic Simulation Exercise) - National Economics Quiz Tournament - University Program - Financial Life Skills and Money Management for Women

In part, funded by the Citi Foundation. The Citi Foundation supports the economic empowerment and financial Inclusion of people in the communities where Citi operates.

20

Citibank Japan Ltd.

Financial Information under Japanese GAAP For the fiscal year ended March 31, 2014

21

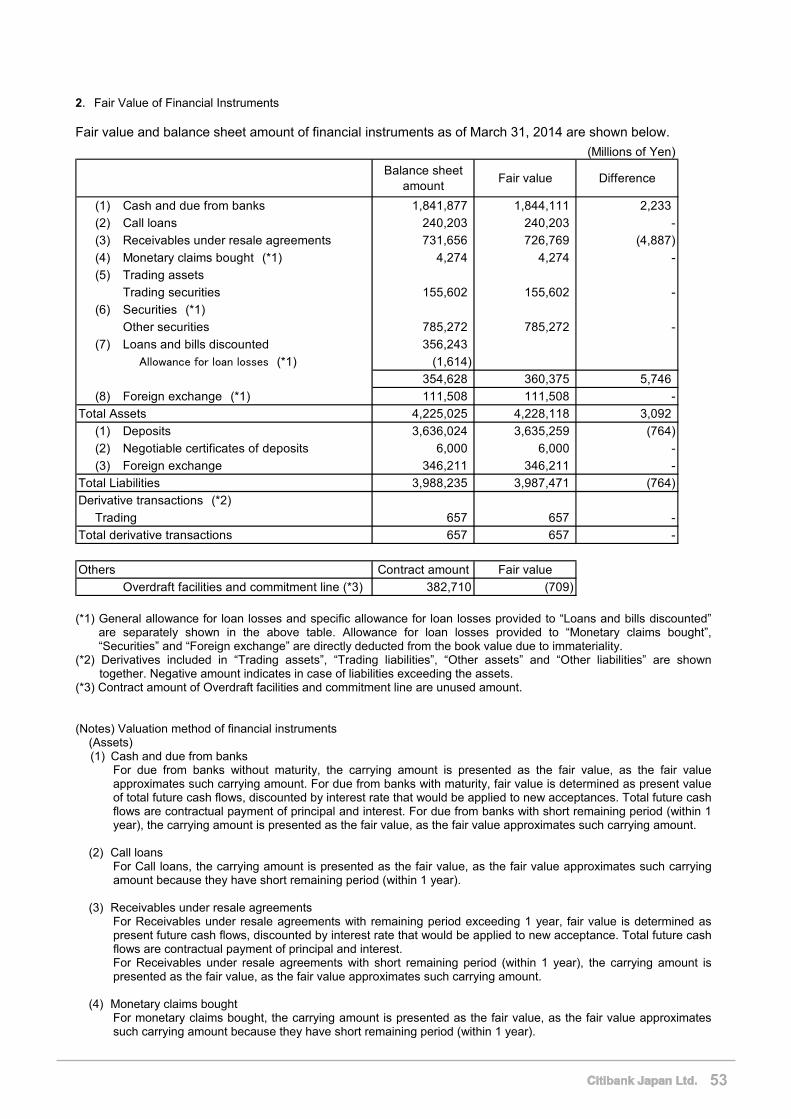

1. Matters Related to Principal Business

< Business Overview>

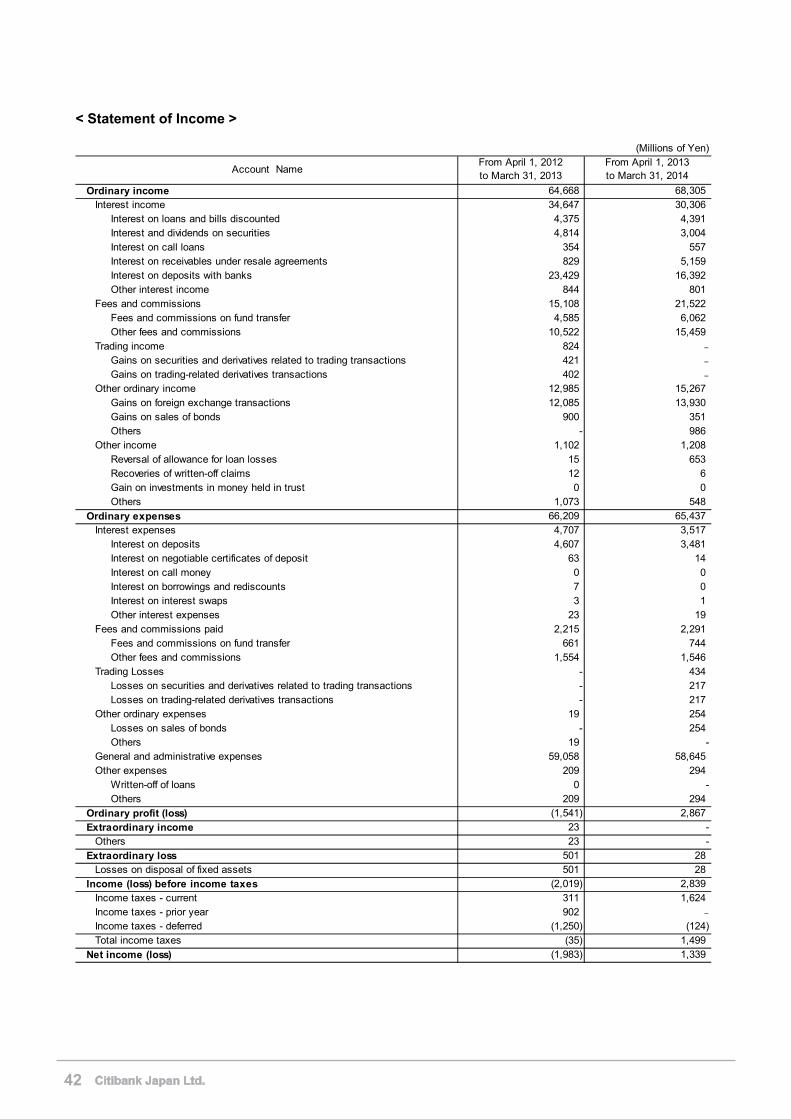

Results of Operations for Fiscal Year ended March 31, 2014

We had a net income of 1.3 billion yen for the year ended March 31, 2014 compared to net loss of 1.9 billion yen for the prior fiscal year.

Ordinary income totaled 68.3 billion yen, up by 3.6 billion yen from the prior fiscal year.

Interest income totaled 30.3 billion yen, down by 4.3 billion yen from the prior fiscal year. Fees and commissions totaled 21.5 billion yen, up by 6.4 billion yen from the prior fiscal year. Other ordinary income totaled 15.2 billion yen, up by 2.2 billion yen from the prior fiscal year.

Ordinary expenses totaled 65.4 billion yen, down by 0.7 billion yen from the prior fiscal year.

Interest expense totaled 3.5 billion yen, down by 1.1 billion yen from the prior fiscal year. Trading losses was 0.4 billion yen compared to trading income of 0.8 billion yen in the prior fiscal

year. General and administrative expenses totaled 58.6 billion yen, down by 0.4 billion yen from the prior

fiscal year. Ordinary profit was 2.8 billion yen compared to ordinary loss of 1.5 billion yen in the prior fiscal year.

Income before income taxes (including extraordinary income and loss) was 2.8 billion yen compared

to loss before income taxes of 2.0 billion yen in the prior fiscal year.

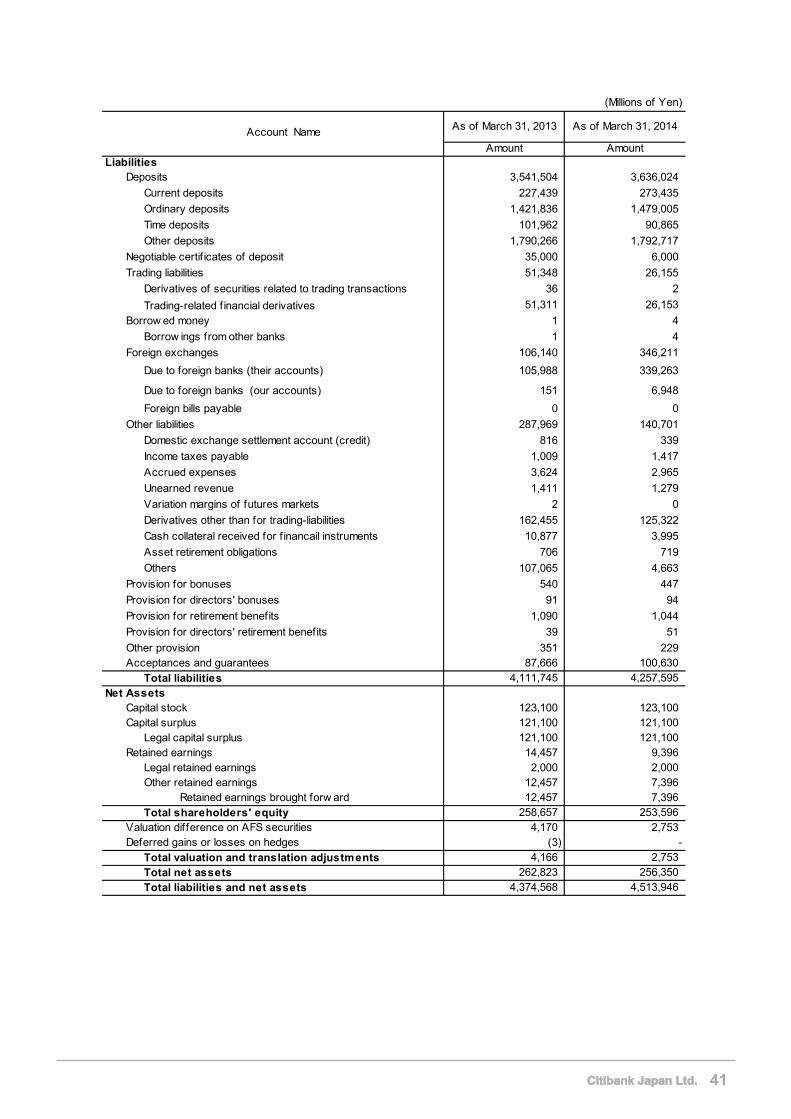

Assets, liabilities, net assets, cash flows, and capital adequacy ratio were as follows;

As of March 31, 2014, total assets were 4,513.9 billion yen, up by 139.3 billion yen compared to March 31, 2013.

Cash and deposits to other banks (due from banks) totaled 1,841.8 billion yen, up by 112.6 billion

yen from the prior fiscal year end. Call loans were 240.2 billion yen, up by 68.1 billion yen from the prior fiscal year end. Receivables under resale agreements were 731.6 billion yen, up by 42.8 billion yen from the prior

fiscal year end. Trading assets were 181.4 billion yen, up by 45.9 billion yen from the prior fiscal year end. Available for sales securities (“AFS securities”) were 785.2 billion yen, down by 73.4 billion yen

from the prior fiscal year end. Loans and bills discounted totaled 356.2 billion yen, up by 25.6 billion yen from the prior fiscal year

end.

As of March 31, 2014, total liabilities were 4,257.5 billion yen, up by 145.8 billion yen compared to March 31, 2013.

Deposits totaled 3,636.0 billion yen, up by 94.5 billion yen from the prior fiscal year end. Negotiable certificates of deposit totaled 6.0 billion yen, down by 29.0 billion yen from the prior

fiscal year end. Foreign exchanges totaled 346.2 billion yen, up by 240.0 billion yen from the prior fiscal year end.

22

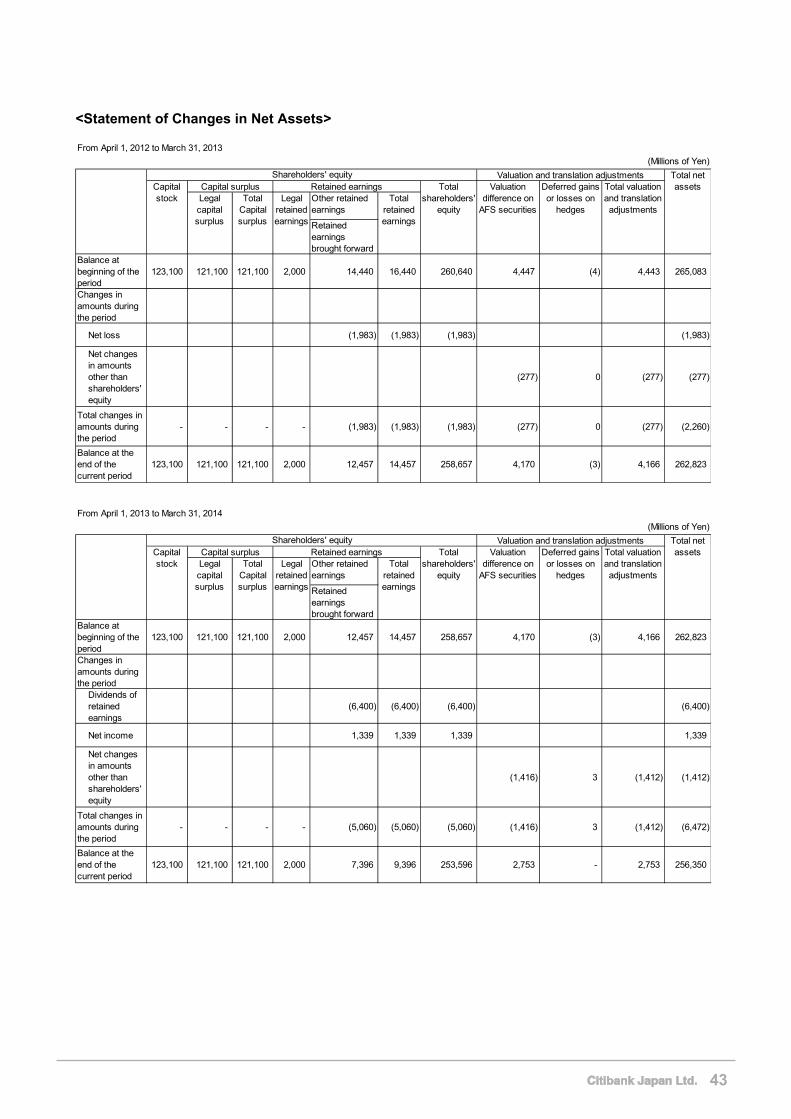

As of March 31, 2014, total net assets were 256.3 billion yen, down by 6.4 billion yen from the prior fiscal year end. Among net assets, retained earnings decreased 5.0 billion yen to 7.3 billion yen, due to 6.4 billion yen payment as interim dividend.

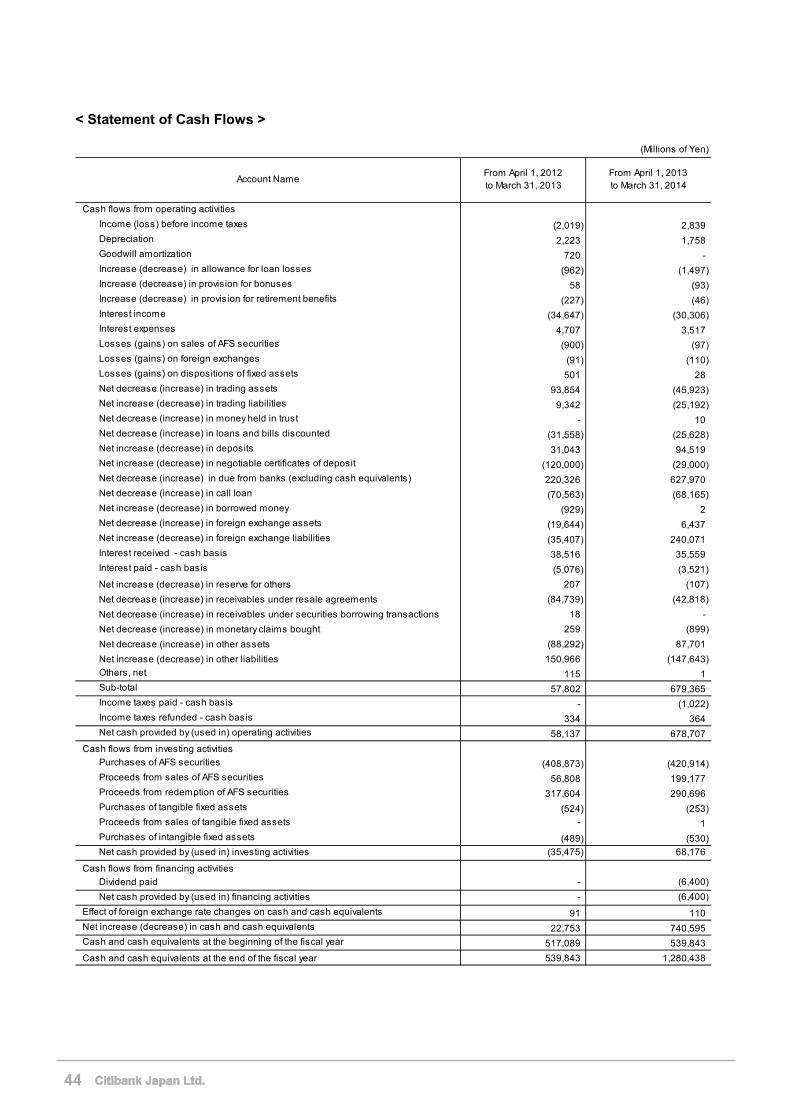

Cash flows from operating activities in the year totaled 678.7 billion yen (Inflow). Cash from investing

activities was 68.1 billion yen (Inflow). Cash from financing activities was 6.4 billion yen (Outflow). As a result, cash and cash equivalents as of the end of the period totaled 1,280.4 billion yen.

The capital adequacy ratio (Basel3 National standards) at the end of the period was 25.72%. (Basel2

National standards as of March 31, 2013 28.47%).

23

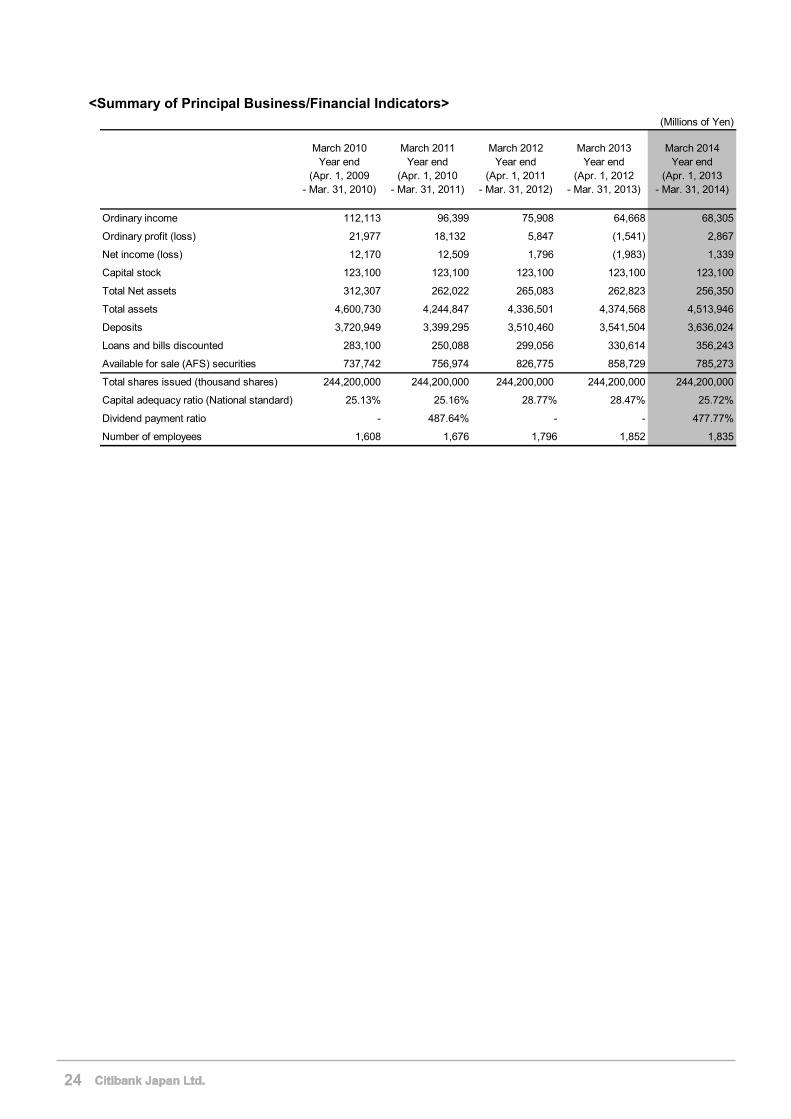

<Summary of Principal Business/Financial Indicators> (Millions of Yen)

Ordinary income 112,113 96,399 75,908 64,668 68,305

Ordinary profit (loss) 21,977 18,132 5,847 (1,541) 2,867

Net income (loss) 12,170 12,509 1,796 (1,983) 1,339

Capital stock 123,100 123,100 123,100 123,100 123,100

Total Net assets 312,307 262,022 265,083 262,823 256,350

Total assets 4,600,730 4,244,847 4,336,501 4,374,568 4,513,946

Deposits 3,720,949 3,399,295 3,510,460 3,541,504 3,636,024

Loans and bills discounted 283,100 250,088 299,056 330,614 356,243

Available for sale (AFS) securities 737,742 756,974 826,775 858,729 785,273

Total shares issued (thousand shares) 244,200,000 244,200,000 244,200,000 244,200,000 244,200,000

Capital adequacy ratio (National standard) 25.13% 25.16% 28.77% 28.47% 25.72%

Dividend payment ratio - 487.64% - - 477.77%

Number of employees 1,608 1,676 1,796 1,852 1,835

March 2014Year end

(Apr. 1, 2013- Mar. 31, 2014)

March 2010Year end

(Apr. 1, 2009- Mar. 31, 2010)

March 2011Year end

(Apr. 1, 2010- Mar. 31, 2011)

March 2012Year end

(Apr. 1, 2011- Mar. 31, 2012)

March 2013Year end

(Apr. 1, 2012- Mar. 31, 2013)

24

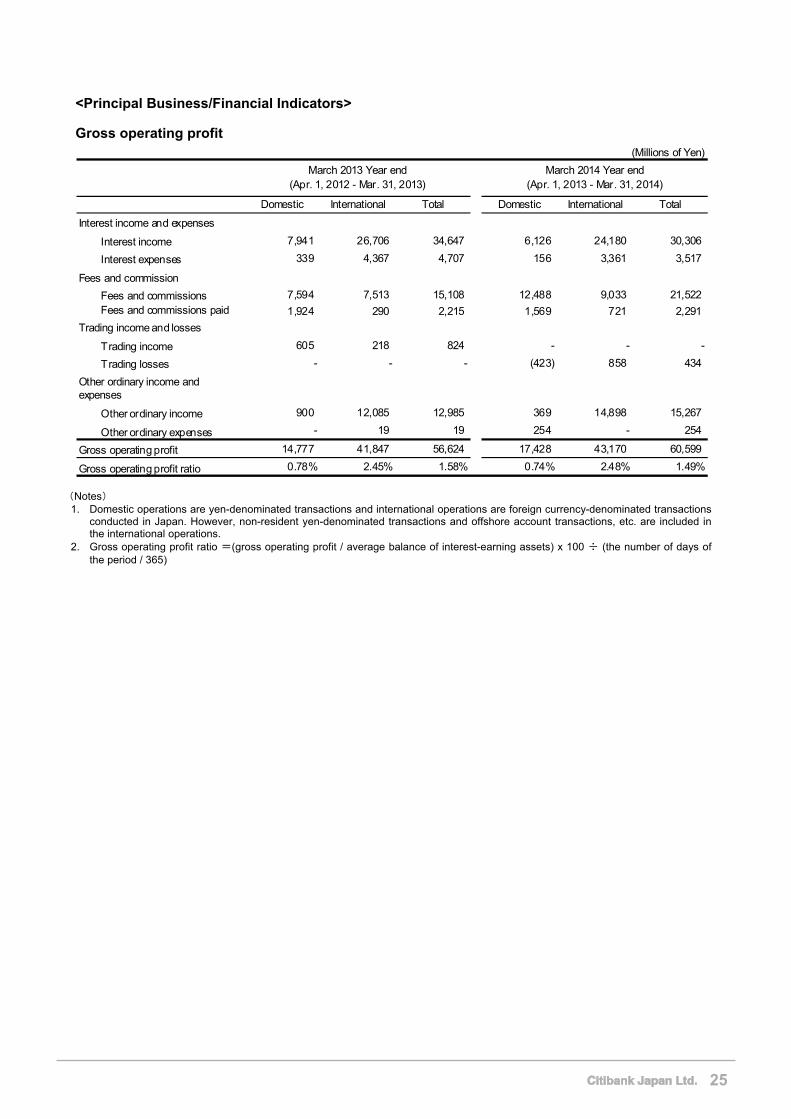

<Principal Business/Financial Indicators> Gross operating profit

(Millions of Yen)

Domestic International Total Domestic International Total

Interest income 7,941 26,706 34,647 6,126 24,180 30,306

Interest expenses 339 4,367 4,707 156 3,361 3,517

Fees and commissions 7,594 7,513 15,108 12,488 9,033 21,522

Fees and commissions paid 1,924 290 2,215 1,569 721 2,291

Trading income 605 218 824 - - -

Trading losses - - - (423) 858 434

Other ordinary income 900 12,085 12,985 369 14,898 15,267

Other ordinary expenses - 19 19 254 - 254

14,777 41,847 56,624 17,428 43,170 60,599

0.78% 2.45% 1.58% 0.74% 2.48% 1.49%

Gross operating profit

Gross operating profit ratio

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Interest income and expenses

Fees and commission

Trading income and losses

Other ordinary income andexpenses

(Notes) 1. Domestic operations are yen-denominated transactions and international operations are foreign currency-denominated transactions

conducted in Japan. However, non-resident yen-denominated transactions and offshore account transactions, etc. are included in the international operations.

2. Gross operating profit ratio =(gross operating profit / average balance of interest-earning assets) x 100 ÷ (the number of days of the period / 365)

25

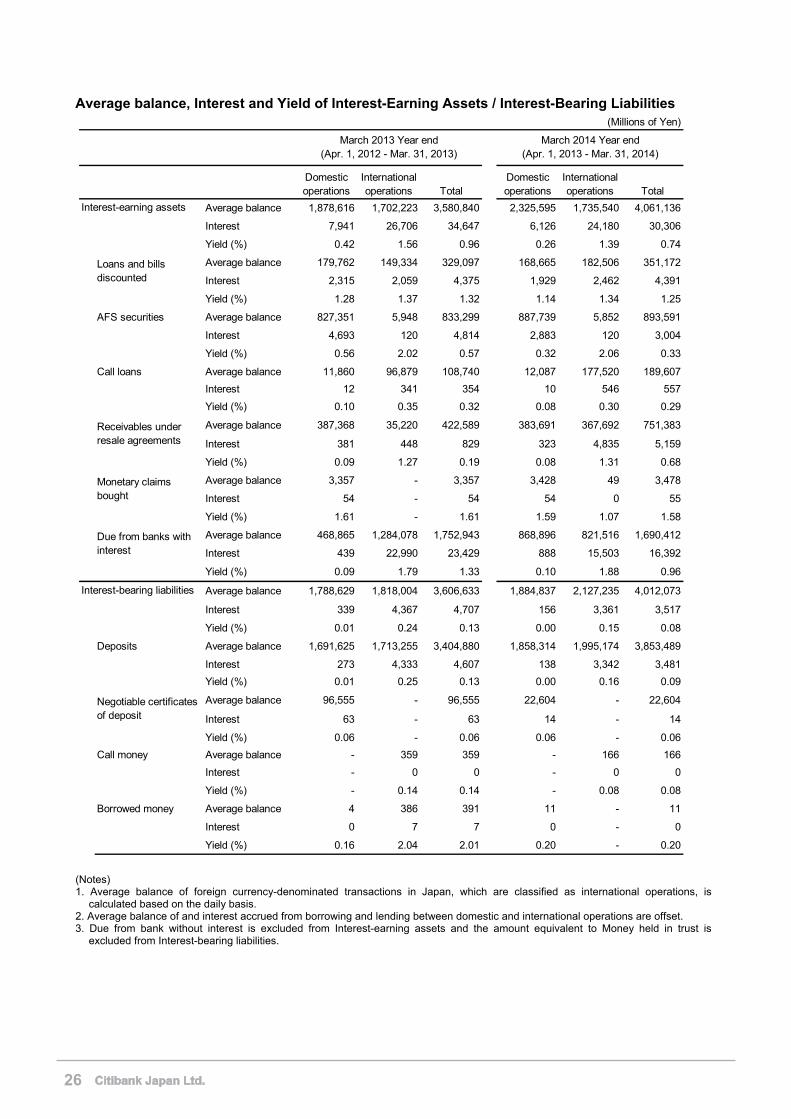

Average balance, Interest and Yield of Interest-Earning Assets / Interest-Bearing Liabilities (Millions of Yen)

Domesticoperations

Internationaloperations Total

Domesticoperations

Internationaloperations Total

Average balance 1,878,616 1,702,223 3,580,840 2,325,595 1,735,540 4,061,136

Interest 7,941 26,706 34,647 6,126 24,180 30,306

Yield (%) 0.42 1.56 0.96 0.26 1.39 0.74

Average balance 179,762 149,334 329,097 168,665 182,506 351,172

Interest 2,315 2,059 4,375 1,929 2,462 4,391

Yield (%) 1.28 1.37 1.32 1.14 1.34 1.25

AFS securities Average balance 827,351 5,948 833,299 887,739 5,852 893,591

Interest 4,693 120 4,814 2,883 120 3,004

Yield (%) 0.56 2.02 0.57 0.32 2.06 0.33

Call loans Average balance 11,860 96,879 108,740 12,087 177,520 189,607

Interest 12 341 354 10 546 557

Yield (%) 0.10 0.35 0.32 0.08 0.30 0.29

Average balance 387,368 35,220 422,589 383,691 367,692 751,383

Interest 381 448 829 323 4,835 5,159

Yield (%) 0.09 1.27 0.19 0.08 1.31 0.68

Average balance 3,357 - 3,357 3,428 49 3,478

Interest 54 - 54 54 0 55

Yield (%) 1.61 - 1.61 1.59 1.07 1.58

Average balance 468,865 1,284,078 1,752,943 868,896 821,516 1,690,412

Interest 439 22,990 23,429 888 15,503 16,392

Yield (%) 0.09 1.79 1.33 0.10 1.88 0.96

Average balance 1,788,629 1,818,004 3,606,633 1,884,837 2,127,235 4,012,073

Interest 339 4,367 4,707 156 3,361 3,517

Yield (%) 0.01 0.24 0.13 0.00 0.15 0.08

Deposits Average balance 1,691,625 1,713,255 3,404,880 1,858,314 1,995,174 3,853,489

Interest 273 4,333 4,607 138 3,342 3,481

Yield (%) 0.01 0.25 0.13 0.00 0.16 0.09

Average balance 96,555 - 96,555 22,604 - 22,604

Interest 63 - 63 14 - 14

Yield (%) 0.06 - 0.06 0.06 - 0.06

Call money Average balance - 359 359 - 166 166

Interest - 0 0 - 0 0

Yield (%) - 0.14 0.14 - 0.08 0.08

Borrowed money Average balance 4 386 391 11 - 11

Interest 0 7 7 0 - 0

Yield (%) 0.16 2.04 2.01 0.20 - 0.20

Negotiable certificatesof deposit

Loans and billsdiscounted

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Interest-earning assets

Interest-bearing liabilities

Due from banks withinterest

Monetary claimsbought

Receivables underresale agreements

(Notes) 1. Average balance of foreign currency-denominated transactions in Japan, which are classified as international operations, is

calculated based on the daily basis. 2. Average balance of and interest accrued from borrowing and lending between domestic and international operations are offset. 3. Due from bank without interest is excluded from Interest-earning assets and the amount equivalent to Money held in trust is

excluded from Interest-bearing liabilities.

26

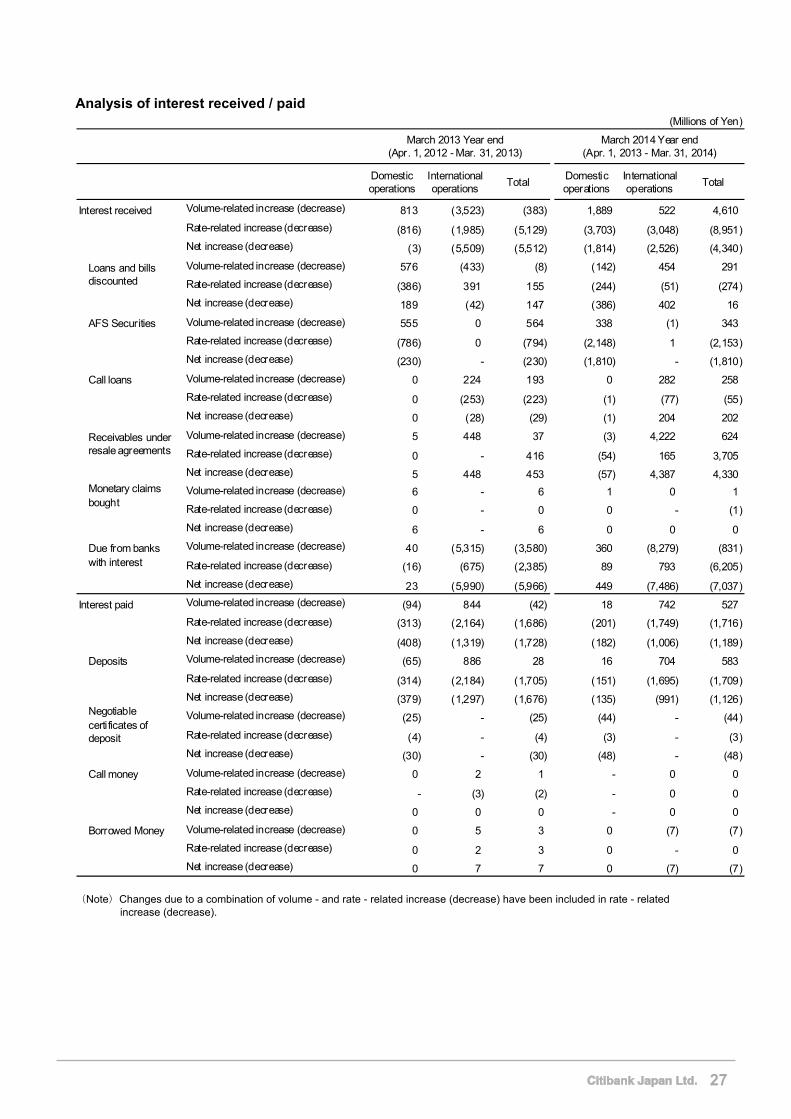

Analysis of interest received / paid (Millions of Yen)

Domesticoperations

Internationaloperations

TotalDomesticoperations

Internationaloperations

Total

Volume-related increase (decrease) 813 (3,523) (383) 1,889 522 4,610

Rate-related increase (decrease) (816) (1,985) (5,129) (3,703) (3,048) (8,951)

Net increase (decrease) (3) (5,509) (5,512) (1,814) (2,526) (4,340)

Volume-related increase (decrease) 576 (433) (8) (142) 454 291

Rate-related increase (decrease) (386) 391 155 (244) (51) (274)

Net increase (decrease) 189 (42) 147 (386) 402 16

AFS Securities Volume-related increase (decrease) 555 0 564 338 (1) 343

Rate-related increase (decrease) (786) 0 (794) (2,148) 1 (2,153)

Net increase (decrease) (230) - (230) (1,810) - (1,810)

Call loans Volume-related increase (decrease) 0 224 193 0 282 258

Rate-related increase (decrease) 0 (253) (223) (1) (77) (55)

Net increase (decrease) 0 (28) (29) (1) 204 202

Volume-related increase (decrease) 5 448 37 (3) 4,222 624

Rate-related increase (decrease) 0 - 416 (54) 165 3,705

Net increase (decrease) 5 448 453 (57) 4,387 4,330

Volume-related increase (decrease) 6 - 6 1 0 1

Rate-related increase (decrease) 0 - 0 0 - (1)

Net increase (decrease) 6 - 6 0 0 0

Volume-related increase (decrease) 40 (5,315) (3,580) 360 (8,279) (831)

Rate-related increase (decrease) (16) (675) (2,385) 89 793 (6,205)

Net increase (decrease) 23 (5,990) (5,966) 449 (7,486) (7,037)

Volume-related increase (decrease) (94) 844 (42) 18 742 527

Rate-related increase (decrease) (313) (2,164) (1,686) (201) (1,749) (1,716)

Net increase (decrease) (408) (1,319) (1,728) (182) (1,006) (1,189)

Deposits Volume-related increase (decrease) (65) 886 28 16 704 583

Rate-related increase (decrease) (314) (2,184) (1,705) (151) (1,695) (1,709)

Net increase (decrease) (379) (1,297) (1,676) (135) (991) (1,126)

Volume-related increase (decrease) (25) - (25) (44) - (44)

Rate-related increase (decrease) (4) - (4) (3) - (3)

Net increase (decrease) (30) - (30) (48) - (48)

Call money Volume-related increase (decrease) 0 2 1 - 0 0

Rate-related increase (decrease) - (3) (2) - 0 0

Net increase (decrease) 0 0 0 - 0 0

Borrowed Money Volume-related increase (decrease) 0 5 3 0 (7) (7)

Rate-related increase (decrease) 0 2 3 0 - 0

Net increase (decrease) 0 7 7 0 (7) (7)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Negotiablecertificates ofdeposit

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

Interest received

Interest paid

Loans and billsdiscounted

Receivables underresale agreements

Due from bankswith interest

Monetary claimsbought

(Note)Changes due to a combination of volume - and rate - related increase (decrease) have been included in rate - related

increase (decrease).

27

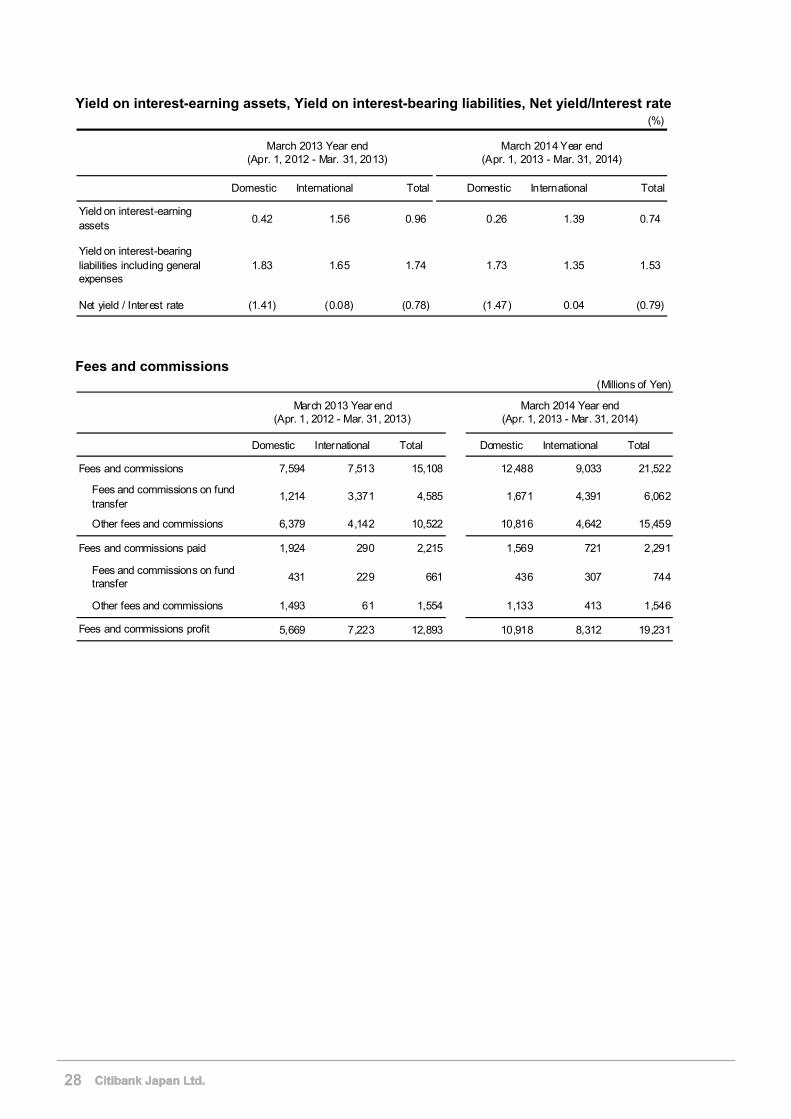

Yield on interest-earning assets, Yield on interest-bearing liabilities, Net yield/Interest rate (%)

Domestic International Total Domestic International Total

Yield on interest-earningassets

0.42 1.56 0.96 0.26 1.39 0.74

Yield on interest-bearingliabilities including generalexpenses

1.83 1.65 1.74 1.73 1.35 1.53

Net yield / Interest rate (1.41) (0.08) (0.78) (1.47) 0.04 (0.79)

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Fees and commissions

(Millions of Yen)

Domestic International Total Domestic International Total

7,594 7,513 15,108 12,488 9,033 21,522

Fees and commissions on fundtransfer

1,214 3,371 4,585 1,671 4,391 6,062

Other fees and commissions 6,379 4,142 10,522 10,816 4,642 15,459

1,924 290 2,215 1,569 721 2,291

Fees and commissions on fundtransfer

431 229 661 436 307 744

Other fees and commissions 1,493 61 1,554 1,133 413 1,546

5,669 7,223 12,893 10,918 8,312 19,231Fees and commissions profit

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Fees and commissions

Fees and commissions paid

28

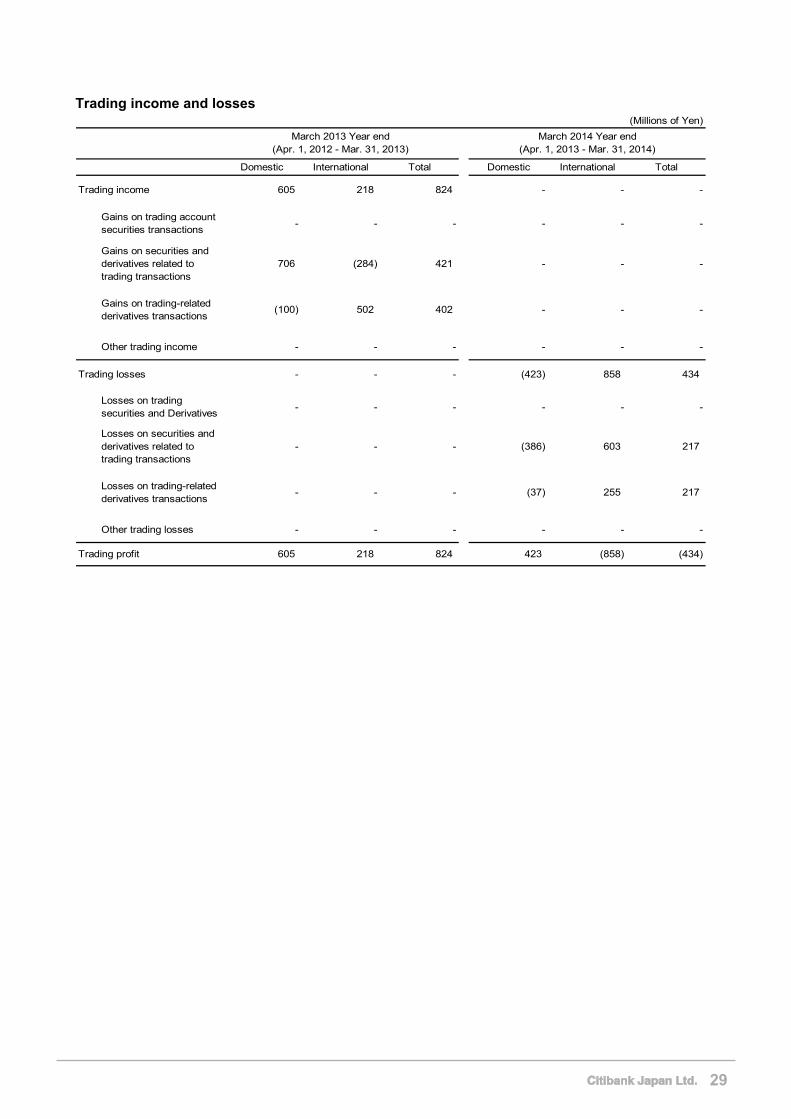

Trading income and losses (Millions of Yen)

Domestic International Total Domestic International Total

Trading income 605 218 824 - - -

Gains on trading accountsecurities transactions

- - - - - -

Gains on securities andderivatives related totrading transactions

706 (284) 421 - - -

Gains on trading-relatedderivatives transactions

(100) 502 402 - - -

Other trading income - - - - - -

Trading losses - - - (423) 858 434

Losses on tradingsecurities and Derivatives

- - - - - -

Losses on securities andderivatives related totrading transactions

- - - (386) 603 217

Losses on trading-relatedderivatives transactions

- - - (37) 255 217

Other trading losses - - - - - -

Trading profit 605 218 824 423 (858) (434)

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

29

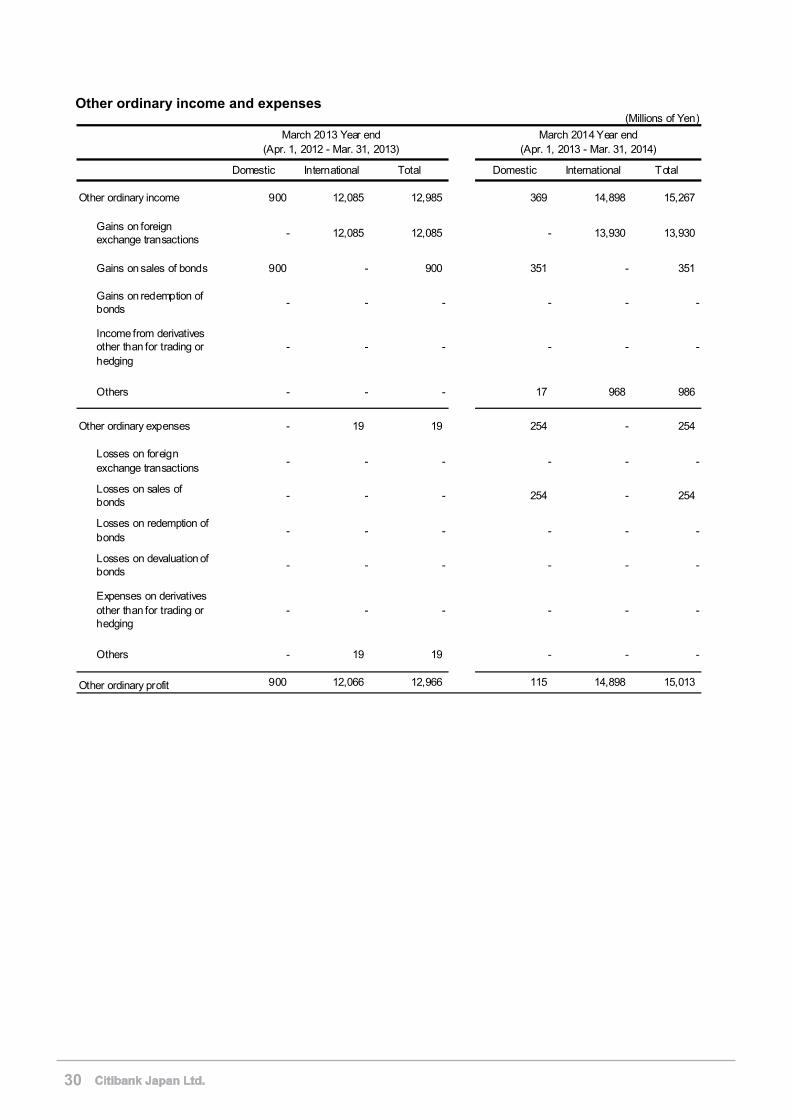

Other ordinary income and expenses (Millions of Yen)

Domestic International Total Domestic International Total

Other ordinary income 900 12,085 12,985 369 14,898 15,267

Gains on foreignexchange transactions

- 12,085 12,085 - 13,930 13,930

Gains on sales of bonds 900 - 900 351 - 351

Gains on redemption ofbonds

- - - - - -

Income from derivativesother than for trading orhedging

- - - - - -

Others - - - 17 968 986

Other ordinary expenses - 19 19 254 - 254

Losses on foreignexchange transactions

- - - - - -

Losses on sales ofbonds

- - - 254 - 254

Losses on redemption ofbonds

- - - - - -

Losses on devaluation ofbonds

- - - - - -

Expenses on derivativesother than for trading orhedging

- - - - - -

Others - 19 19 - - -

Other ordinary profit 900 12,066 12,966 115 14,898 15,013

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

30

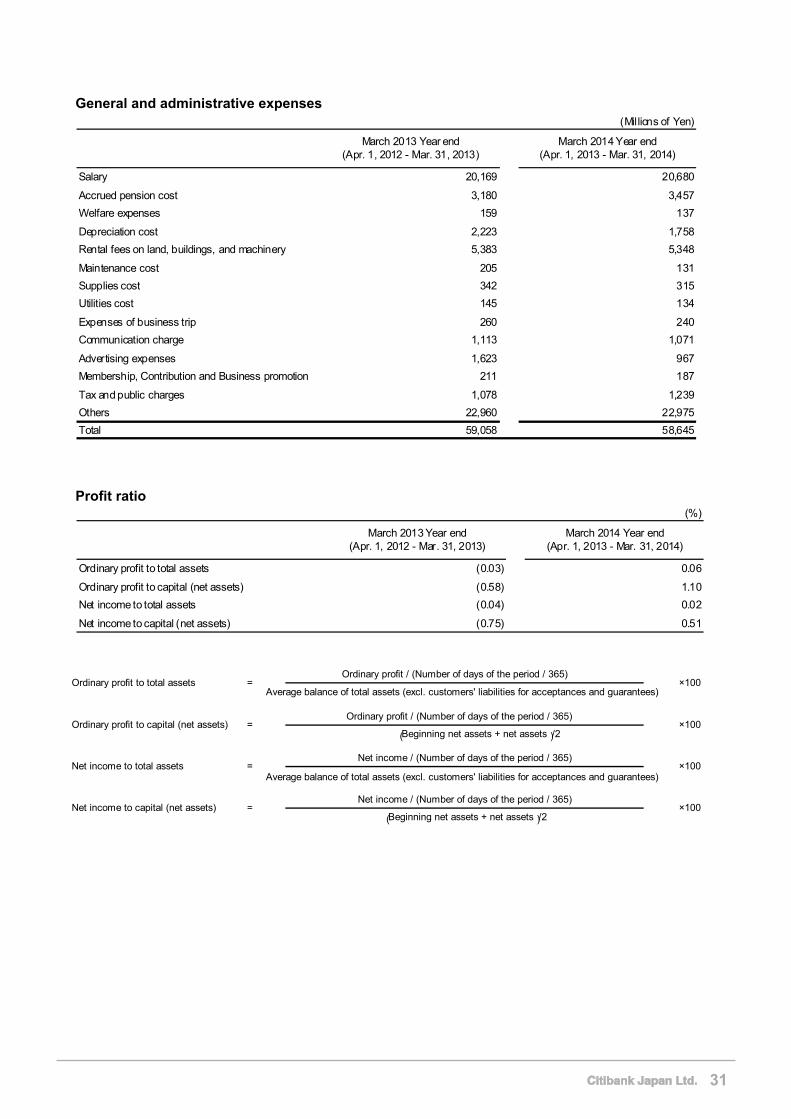

General and administrative expenses (Millions of Yen)

Salary 20,169 20,680

Accrued pension cost 3,180 3,457

Welfare expenses 159 137

Depreciation cost 2,223 1,758

Rental fees on land, buildings, and machinery 5,383 5,348

Maintenance cost 205 131

Supplies cost 342 315

Utilities cost 145 134

Expenses of business trip 260 240

Communication charge 1,113 1,071

Advertising expenses 1,623 967

Membership, Contribution and Business promotion 211 187

Tax and public charges 1,078 1,239

Others 22,960 22,975

Total 59,058 58,645

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Profit ratio (%)

Ordinary profit to total assets (0.03) 0.06

Ordinary profit to capital (net assets) (0.58) 1.10

Net income to total assets (0.04) 0.02

Net income to capital (net assets) (0.75) 0.51

March 2013 Year end(Apr. 1, 2012 - Mar. 31, 2013)

March 2014 Year end(Apr. 1, 2013 - Mar. 31, 2014)

Ordinary profit / (Number of days of the period / 365)

Average balance of total assets (excl. customers' liabilities for acceptances and guarantees)

Ordinary profit / (Number of days of the period / 365)

(Beginning net assets + net assets)/2

Net income / (Number of days of the period / 365)

Average balance of total assets (excl. customers' liabilities for acceptances and guarantees)

Net income / (Number of days of the period / 365)

(Beginning net assets + net assets)/2

×100

= ×100

×100

×100

=

=

=

Ordinary profit to total assets

Ordinary profit to capital (net assets)

Net income to total assets

Net income to capital (net assets)

31

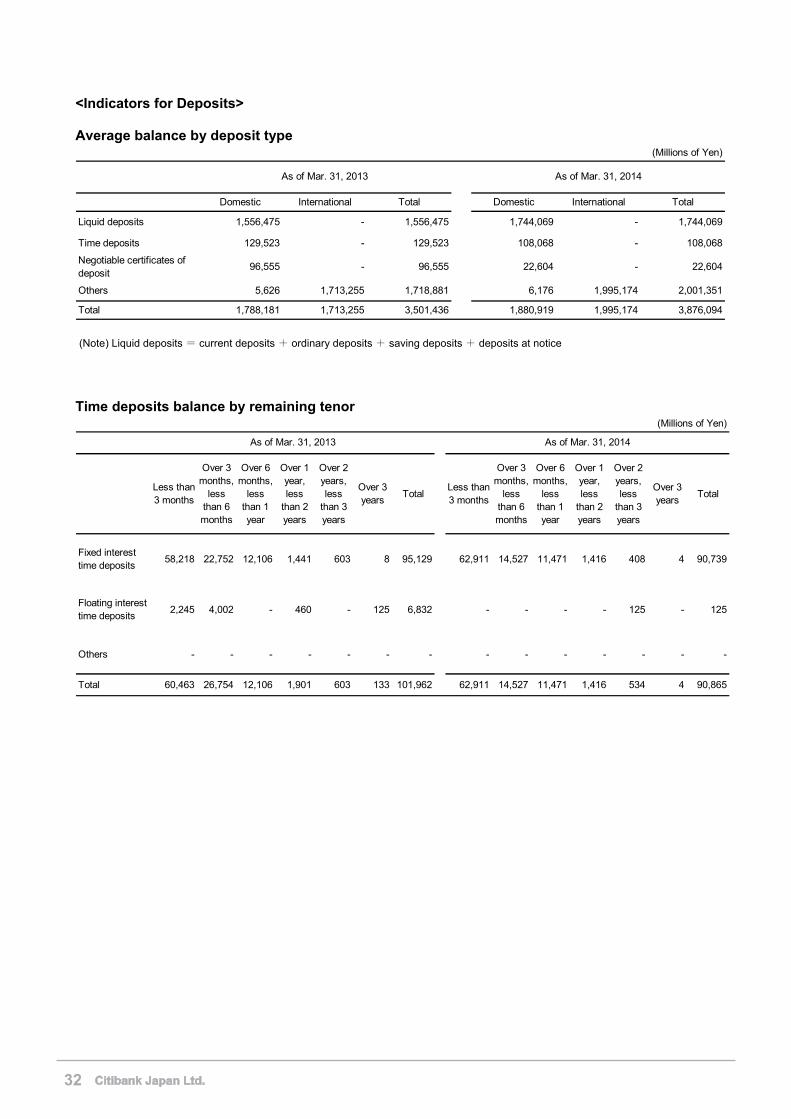

<Indicators for Deposits>

Average balance by deposit type (Millions of Yen)

Domestic International Total Domestic International Total

Liquid deposits 1,556,475 - 1,556,475 1,744,069 - 1,744,069

Time deposits 129,523 - 129,523 108,068 - 108,068

Negotiable certificates ofdeposit

96,555 - 96,555 22,604 - 22,604

Others 5,626 1,713,255 1,718,881 6,176 1,995,174 2,001,351

Total 1,788,181 1,713,255 3,501,436 1,880,919 1,995,174 3,876,094

As of Mar. 31, 2013 As of Mar. 31, 2014

(Note) Liquid deposits = current deposits + ordinary deposits + saving deposits + deposits at notice

Time deposits balance by remaining tenor

(Millions of Yen)

Less than3 months

Over 3months,

lessthan 6months

Over 6months,

lessthan 1year

Over 1year,less

than 2years

Over 2years,less

than 3years

Over 3years

TotalLess than3 months

Over 3months,

lessthan 6months

Over 6months,

lessthan 1year

Over 1year,less

than 2years

Over 2years,less

than 3years

Over 3years

Total

Fixed interesttime deposits

58,218 22,752 12,106 1,441 603 8 95,129 62,911 14,527 11,471 1,416 408 4 90,739

Floating interesttime deposits

2,245 4,002 - 460 - 125 6,832 - - - - 125 - 125

Others - - - - - - - - - - - - - -

Total 60,463 26,754 12,106 1,901 603 133 101,962 62,911 14,527 11,471 1,416 534 4 90,865

As of Mar. 31, 2013 As of Mar. 31, 2014

32

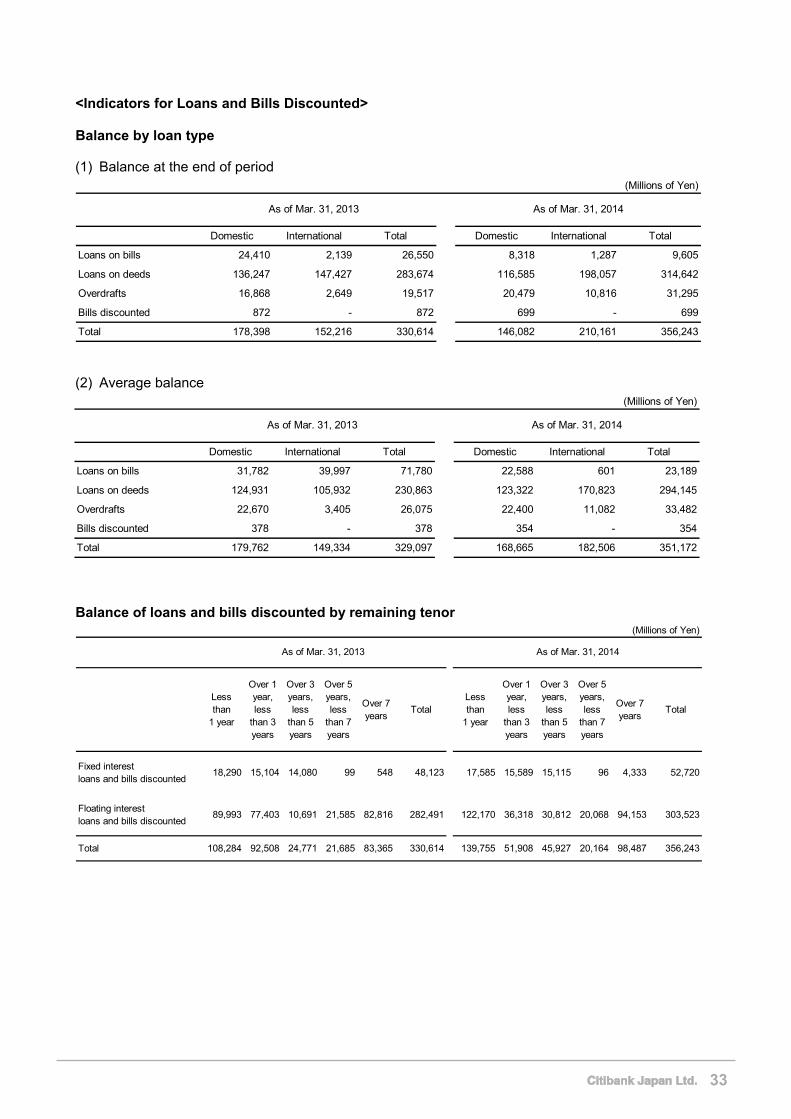

<Indicators for Loans and Bills Discounted>

Balance by loan type (1) Balance at the end of period

Domestic International Total Domestic International Total

Loans on bills 24,410 2,139 26,550 8,318 1,287 9,605

Loans on deeds 136,247 147,427 283,674 116,585 198,057 314,642

Overdrafts 16,868 2,649 19,517 20,479 10,816 31,295

Bills discounted 872 - 872 699 - 699

Total 178,398 152,216 330,614 146,082 210,161 356,243

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

(2) Average balance

Domestic International Total Domestic International Total

Loans on bills 31,782 39,997 71,780 22,588 601 23,189

Loans on deeds 124,931 105,932 230,863 123,322 170,823 294,145

Overdrafts 22,670 3,405 26,075 22,400 11,082 33,482

Bills discounted 378 - 378 354 - 354

Total 179,762 149,334 329,097 168,665 182,506 351,172

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Balance of loans and bills discounted by remaining tenor

(Millions of Yen)

Lessthan

1 year

Over 1year,less

than 3years

Over 3years,less

than 5years

Over 5years,less

than 7years

Over 7years

TotalLessthan

1 year

Over 1year,less

than 3years

Over 3years,less

than 5years

Over 5years,less

than 7years

Over 7years

Total

Fixed interestloans and bills discounted

18,290 15,104 14,080 99 548 48,123 17,585 15,589 15,115 96 4,333 52,720

Floating interestloans and bills discounted

89,993 77,403 10,691 21,585 82,816 282,491 122,170 36,318 30,812 20,068 94,153 303,523

Total 108,284 92,508 24,771 21,685 83,365 330,614 139,755 51,908 45,927 20,164 98,487 356,243

As of Mar. 31, 2013 As of Mar. 31, 2014

33

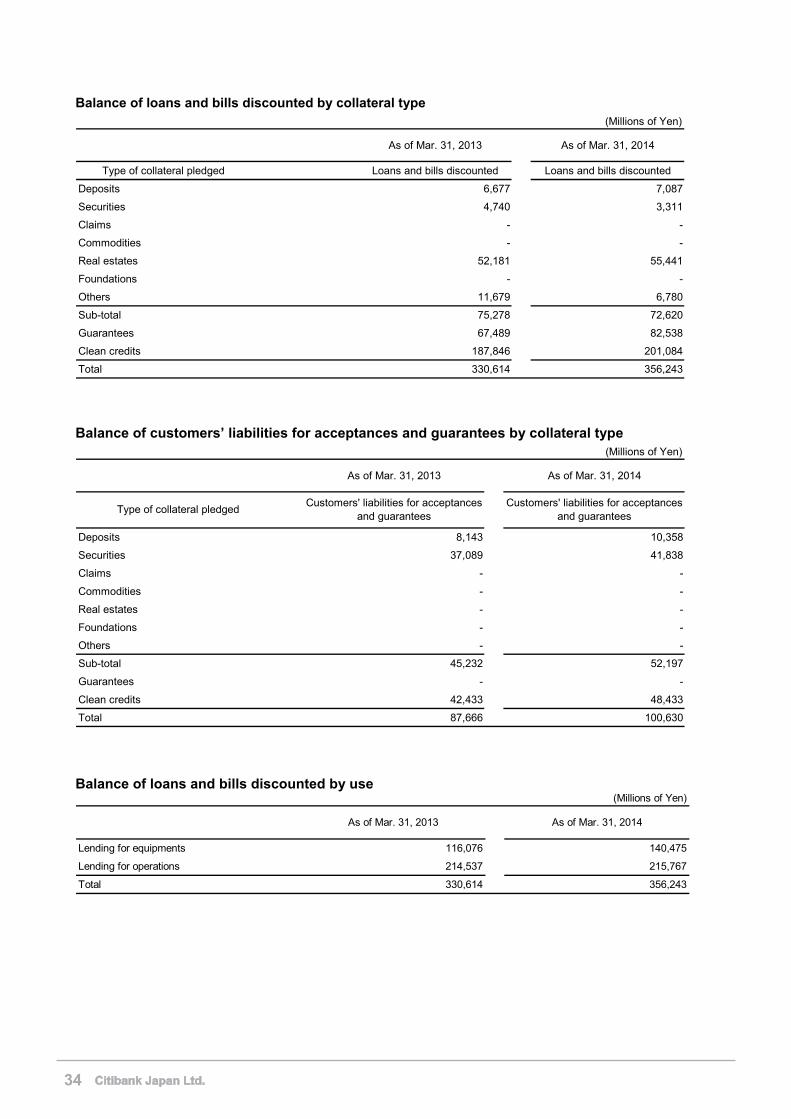

Balance of loans and bills discounted by collateral type (Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Type of collateral pledged Loans and bills discounted Loans and bills discounted

Deposits 6,677 7,087

Securities 4,740 3,311

Claims - -

Commodities - -

Real estates 52,181 55,441

Foundations - -

Others 11,679 6,780

Sub-total 75,278 72,620

Guarantees 67,489 82,538

Clean credits 187,846 201,084

Total 330,614 356,243 Balance of customers’ liabilities for acceptances and guarantees by collateral type

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Deposits 8,143 10,358

Securities 37,089 41,838

Claims - -

Commodities - -

Real estates - -

Foundations - -

Others - -

Sub-total 45,232 52,197

Guarantees - -

Clean credits 42,433 48,433

Total 87,666 100,630

Type of collateral pledgedCustomers' liabilities for acceptances

and guaranteesCustomers' liabilities for acceptances

and guarantees

Balance of loans and bills discounted by use

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Lending for equipments 116,076 140,475

Lending for operations 214,537 215,767

Total 330,614 356,243

34

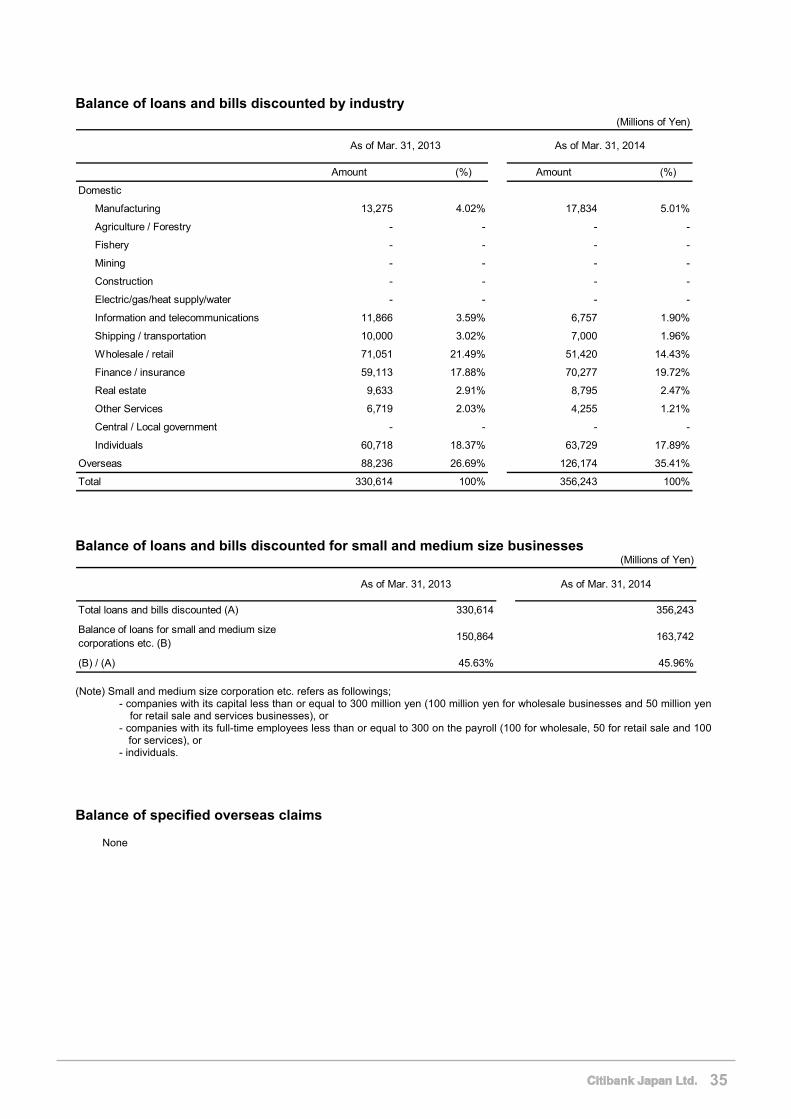

Balance of loans and bills discounted by industry (Millions of Yen)

Amount (%) Amount (%)

Domestic

Manufacturing 13,275 4.02% 17,834 5.01%

Agriculture / Forestry - - - -

Fishery - - - -

Mining - - - -

Construction - - - -

Electric/gas/heat supply/water - - - -

Information and telecommunications 11,866 3.59% 6,757 1.90%

Shipping / transportation 10,000 3.02% 7,000 1.96%

Wholesale / retail 71,051 21.49% 51,420 14.43%

Finance / insurance 59,113 17.88% 70,277 19.72%

Real estate 9,633 2.91% 8,795 2.47%

Other Services 6,719 2.03% 4,255 1.21%

Central / Local government - - - -

Individuals 60,718 18.37% 63,729 17.89%

Overseas 88,236 26.69% 126,174 35.41%

Total 330,614 100% 356,243 100%

As of Mar. 31, 2013 As of Mar. 31, 2014

Balance of loans and bills discounted for small and medium size businesses

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Total loans and bills discounted (A) 330,614 356,243

Balance of loans for small and medium sizecorporations etc. (B)

150,864 163,742

(B) / (A) 45.63% 45.96% (Note) Small and medium size corporation etc. refers as followings;

- companies with its capital less than or equal to 300 million yen (100 million yen for wholesale businesses and 50 million yen for retail sale and services businesses), or

- companies with its full-time employees less than or equal to 300 on the payroll (100 for wholesale, 50 for retail sale and 100 for services), or

- individuals.

Balance of specified overseas claims None

35

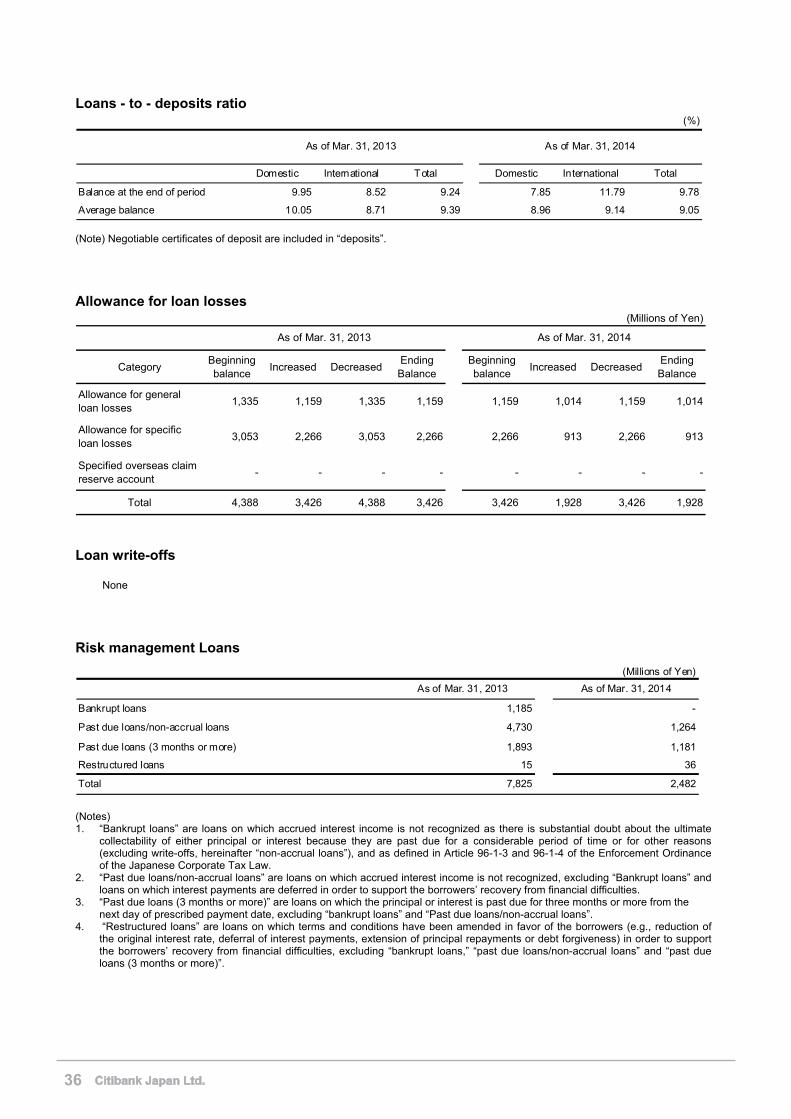

Loans - to - deposits ratio (%)

Domestic International Total Domestic International Total

Balance at the end of period 9.95 8.52 9.24 7.85 11.79 9.78

Average balance 10.05 8.71 9.39 8.96 9.14 9.05

As of Mar. 31, 2013 As of Mar. 31, 2014

(Note) Negotiable certificates of deposit are included in “deposits”.

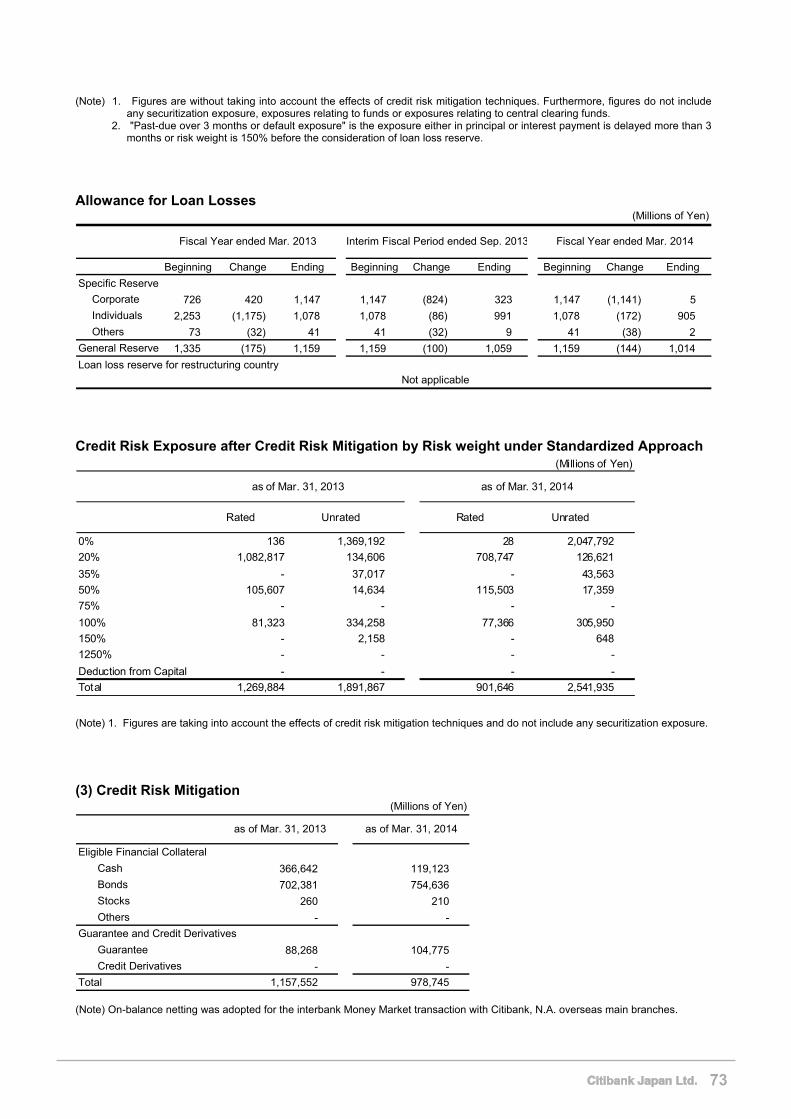

Allowance for loan losses (Millions of Yen)

CategoryBeginningbalance

Increased DecreasedEndingBalance

Beginningbalance

Increased DecreasedEndingBalance

Allowance for generalloan losses

1,335 1,159 1,335 1,159 1,159 1,014 1,159 1,014

Allowance for specificloan losses

3,053 2,266 3,053 2,266 2,266 913 2,266 913

Specified overseas claimreserve account

- - - - - - - -

Total 4,388 3,426 4,388 3,426 3,426 1,928 3,426 1,928

As of Mar. 31, 2013 As of Mar. 31, 2014

Loan write-offs

None

Risk management Loans

(Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Bankrupt loans 1,185 -

Past due loans/non-accrual loans 4,730 1,264

Past due loans (3 months or more) 1,893 1,181

Restructured loans 15 36

Total 7,825 2,482

(Notes) 1. “Bankrupt loans” are loans on which accrued interest income is not recognized as there is substantial doubt about the ultimate

collectability of either principal or interest because they are past due for a considerable period of time or for other reasons (excluding write-offs, hereinafter “non-accrual loans”), and as defined in Article 96-1-3 and 96-1-4 of the Enforcement Ordinance of the Japanese Corporate Tax Law.

2. “Past due loans/non-accrual loans” are loans on which accrued interest income is not recognized, excluding “Bankrupt loans” and loans on which interest payments are deferred in order to support the borrowers’ recovery from financial difficulties.

3. “Past due loans (3 months or more)” are loans on which the principal or interest is past due for three months or more from the next day of prescribed payment date, excluding “bankrupt loans” and “Past due loans/non-accrual loans”.

4. “Restructured loans” are loans on which terms and conditions have been amended in favor of the borrowers (e.g., reduction of the original interest rate, deferral of interest payments, extension of principal repayments or debt forgiveness) in order to support the borrowers’ recovery from financial difficulties, excluding “bankrupt loans,” “past due loans/non-accrual loans” and “past due loans (3 months or more)”.

36

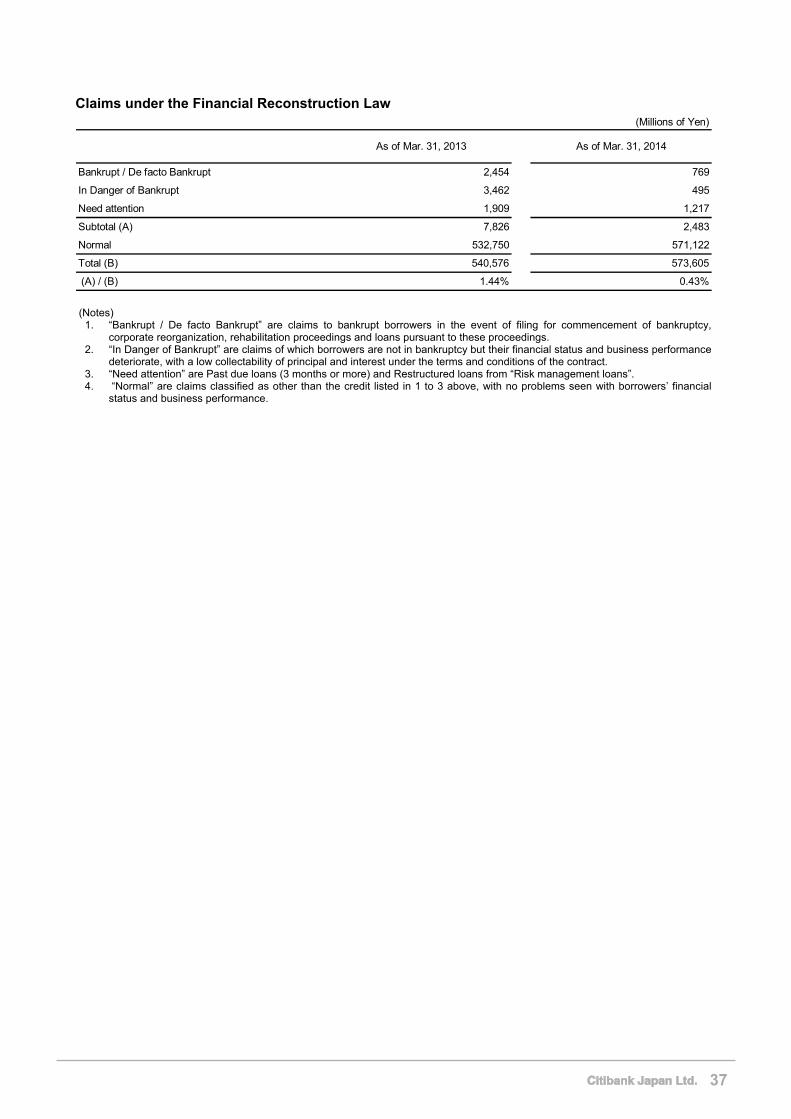

Claims under the Financial Reconstruction Law (Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Bankrupt / De facto Bankrupt 2,454 769

In Danger of Bankrupt 3,462 495

Need attention 1,909 1,217

Subtotal (A) 7,826 2,483

Normal 532,750 571,122

Total (B) 540,576 573,605

(A) / (B) 1.44% 0.43%

(Notes)

1. “Bankrupt / De facto Bankrupt” are claims to bankrupt borrowers in the event of filing for commencement of bankruptcy, corporate reorganization, rehabilitation proceedings and loans pursuant to these proceedings.

2. “In Danger of Bankrupt” are claims of which borrowers are not in bankruptcy but their financial status and business performance deteriorate, with a low collectability of principal and interest under the terms and conditions of the contract.

3. “Need attention” are Past due loans (3 months or more) and Restructured loans from “Risk management loans”. 4. “Normal” are claims classified as other than the credit listed in 1 to 3 above, with no problems seen with borrowers’ financial

status and business performance.

37

<Indicators for Securities >

Average balance of securities related to trading transactions (Millions of Yen)

As of Mar. 31, 2013 As of Mar. 31, 2014

Trading Japanese government bonds 226,616 176,956

Trading municipal bonds - -

Trading government guaranteed bonds - -

Other trading securities 1,096 17,555

Total 227,713 194,512

Balance of AFS securities by remaining tenor

(Millions of Yen)

CategoryUp to 1

year1 - 5years

5 - 10years

Over 10years

Indefiniteterm

TotalUp to 1

year1 - 5years

5 - 10years

Over 10years

Indefiniteterm

Total

Japanesegovernment bonds

189,719 635,510 11,464 - - 836,694 85,167 641,130 38,147 - - 764,446

Municipal bonds - - - - - - - - - - - -

Corporate bonds - - - 16,121 - 16,121 - - - 15,022 - 15,022

Stocks - - - - - - - - - - - -

Foreign bonds - 5,913 - - - 5,913 - 5,804 - - - 5,804

Foreign stocks - - - - - - - - - - - -

Others - - - - - - - - - - - -

Total 189,719 641,423 11,464 16,121 - 858,729 85,167 646,935 38,147 15,022 - 785,273

As of Mar. 31, 2013 As of Mar. 31, 2014

Average balance of AFS securities (Millions of Yen)

Domestic International Total Domestic International Total

Japanese government bonds 805,746 - 805,746 872,297 - 872,297

Municipal bonds - - - - - -

Corporate bonds 21,604 - 21,604 15,441 - 15,441

Stocks - - - - - -

Foreign bonds - 5,948 5,948 - 5,852 5,852

Foreign stocks - - - - - -

Others - - - - - -

Total 827,351 5,948 833,299 887,739 5,852 893,591

As of Mar. 31, 2013 As of Mar. 31, 2014

38

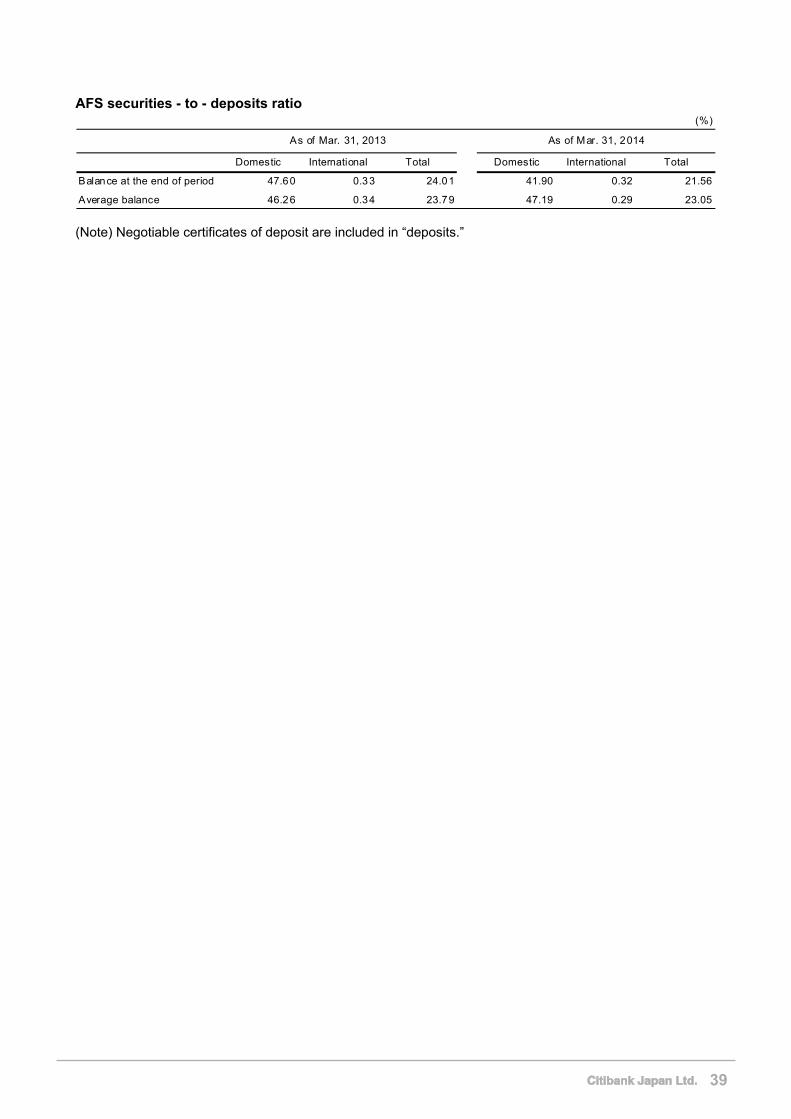

AFS securities - to - deposits ratio (%)

Domestic International Total Domestic International Total

Balance at the end of period 47.60 0.33 24.01 41.90 0.32 21.56

Average balance 46.26 0.34 23.79 47.19 0.29 23.05

As of Mar. 31, 2013 As of Mar. 31, 2014

(Note) Negotiable certificates of deposit are included in “deposits.”

39

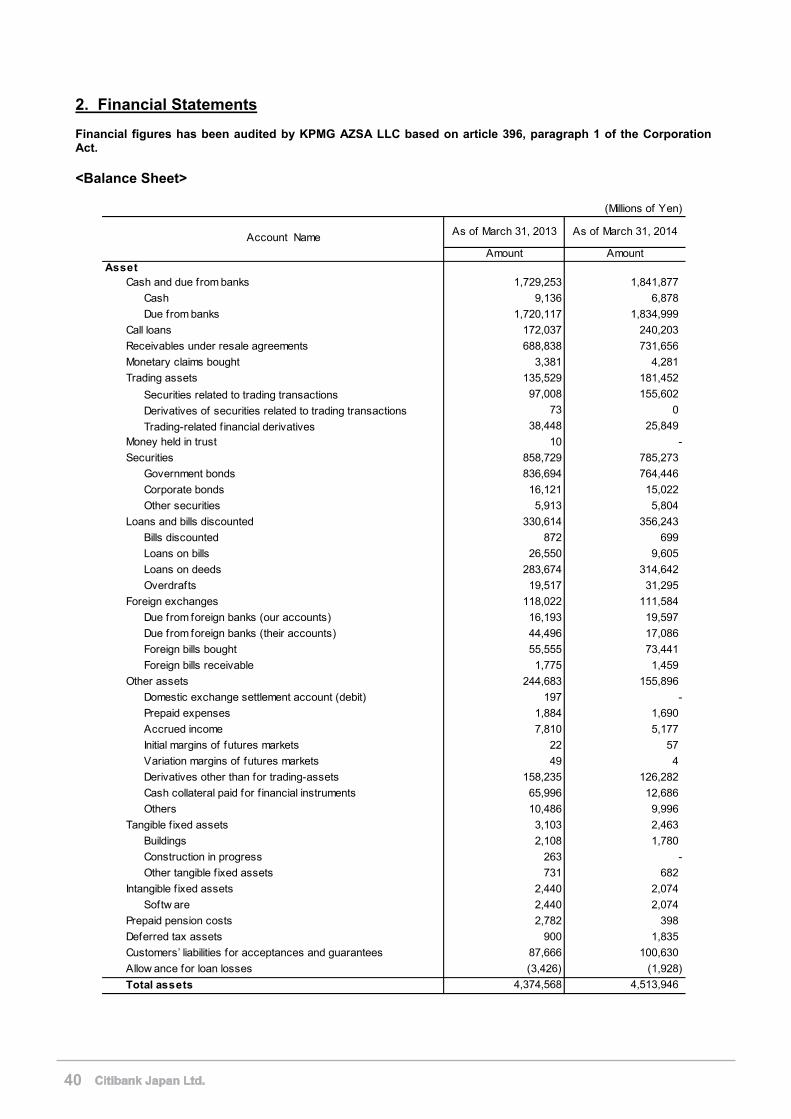

2. Financial Statements Financial figures has been audited by KPMG AZSA LLC based on article 396, paragraph 1 of the Corporation Act. <Balance Sheet>

(Millions of Yen)

As of March 31, 2013 As of March 31, 2014

Amount AmountAsset

Cash and due from banks 1,729,253 1,841,877

Cash 9,136 6,878

Due from banks 1,720,117 1,834,999

Call loans 172,037 240,203

Receivables under resale agreements 688,838 731,656

Monetary claims bought 3,381 4,281

Trading assets 135,529 181,452

Securities related to trading transactions 97,008 155,602

Derivatives of securities related to trading transactions 73 0

Trading-related f inancial derivatives 38,448 25,849

Money held in trust 10 -

Securities 858,729 785,273

Government bonds 836,694 764,446

Corporate bonds 16,121 15,022

Other securities 5,913 5,804

Loans and bills discounted 330,614 356,243

Bills discounted 872 699

Loans on bills 26,550 9,605

Loans on deeds 283,674 314,642

Overdrafts 19,517 31,295

Foreign exchanges 118,022 111,584

Due from foreign banks (our accounts) 16,193 19,597

Due from foreign banks (their accounts) 44,496 17,086

Foreign bills bought 55,555 73,441

Foreign bills receivable 1,775 1,459

Other assets 244,683 155,896

Domestic exchange settlement account (debit) 197 -

Prepaid expenses 1,884 1,690

Accrued income 7,810 5,177

Initial margins of futures markets 22 57

Variation margins of futures markets 49 4

Derivatives other than for trading-assets 158,235 126,282

Cash collateral paid for f inancial instruments 65,996 12,686

Others 10,486 9,996

Tangible f ixed assets 3,103 2,463

Buildings 2,108 1,780

Construction in progress 263 -

Other tangible f ixed assets 731 682

Intangible f ixed assets 2,440 2,074

Softw are 2,440 2,074

Prepaid pension costs 2,782 398

Deferred tax assets 900 1,835

Customers’ liabilities for acceptances and guarantees 87,666 100,630