Embed Size (px)

Citation preview

Forecasting Tax Revenues in Latvia: Analysis and Models

Velga Ozolina, Astra Auzina-Emsina, Remigijs Pocs

Riga Technical University, Latvia

Data Analysis• CSB data• Ministry of Finance data• State Revenue Service (SRS)

data• Eurostat data

Tax Burden in Latvia in 1995-2012, % of GDP

05

101520253035

%

Data Source: CSB database

Tax Burden in the EU Countries in 2012, % of GDP

0

10

20

30

40

50

60

Denm

ark

Belg

ium

Fran

ceAu

stria

Swed

enIta

lyFi

nlan

dEU

-28

Ger

man

yLu

xem

bour

gN

ethe

rland

sH

unga

rySl

oven

iaU

nite

d …G

reec

eCr

oatia

Cypr

usCz

ech

Repu

blic

Port

ugal

Mal

taSp

ain

Esto

nia

Pola

ndIre

land

Rom

ania

Slov

akia

Latv

iaBu

lgar

iaLi

thua

nia

%

Data Source: Eurostat database

Tax Revenues in Latvia (ESA95 methodology), m EUR

0

5000

10000

15000

20000

25000

0

500

1000

1500

2000

2500m EURm EUR

Value Added Tax Customs Duties Excise Taxes

Personal Income Tax Corporate Income Tax Social Contributions

Other Taxes Nominal GDP (right axes)

Data Source: CSB database

Social Contributions in Latvia, m EUR

00.511.522.533.544.55

0

500

1000

1500

2000

2500

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

m EUR

ESA95 methodology National methodology Ratio (right axes)

Data Source: CSB database, Ministry of Finance data

Analysis of Legal AspectsThe main laws in the group of

direct taxes are:• On State Social Insurance,• On Personal Income Tax,• On Corporate (Enterprise)

Income Tax,• Micro-enterprise Tax Law.

Analysis of Legal Aspects• Employed persons by professional status, thsd

Overall statistics (CSB) Taxpayers (SRS)

0

200

400

600

800

1000

01020304050607080

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

thsdthsd

Employers (owners) Self-employed

Family workers Self-employed in the second job

Employees (workers), right axes

0102030405060708090100

0100200300400500600700800900

1000

I III I III I III I III I III I III I III I III I III I III I III

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

thsdthsd

Employed Self-employed, right axes

Data Source: CSB database, State Revenue Service data

Analysis of Legal AspectsThe main laws in the group of

indirect taxes are:• Value Added Tax Law (before

2013 law On Value Added Tax),

• On Excise Duty.

Seasonality Analysis• Revenues of Direct Taxes, m EUR

-50

0

50

100

150

200

250

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

m EUR

Social Contributions Personal Income Tax Enterprise Income Tax

Data Source: Ministry of Finance data

Quarterly Seasonal Indexes for Social Contributions

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1

Q2

Q3

Q4

Data Source: Ministry of Finance data

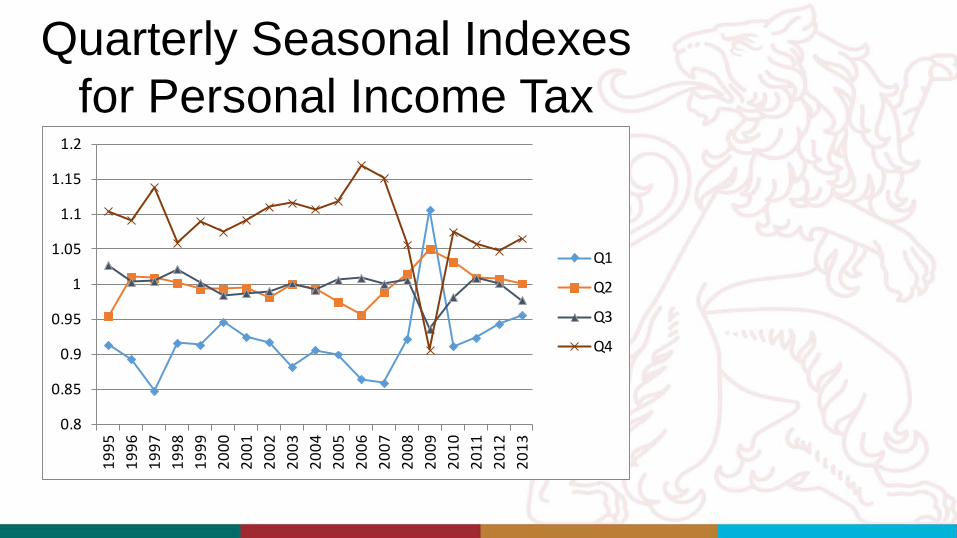

Quarterly Seasonal Indexes for Personal Income Tax

0.8

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1

Q2

Q3

Q4

Quarterly Seasonal Indexes for Corporate Income Tax

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1

Q2

Q3

Q4

Seasonality Analysis• Revenues of Indirect Taxes, m EUR

020406080

100120140160180200

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

m EUR

Value Added Tax Excise Duty

Data Source: Ministry of Finance data

Quarterly Seasonal Indexes for Value Added Tax

0.75

0.8

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1

Q2

Q3

Q4

Data Source: Ministry of Finance data

Quarterly Seasonal Indexes for Excise Duty

0.6

0.8

1

1.2

1.4

1.6

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1

Q2

Q3

Q4

Data Source: Ministry of Finance data

Productivity and Economic Activity Analysis

• Labor productivity and real GDP growth rate(2004-2007) (2008-2010) (2011-2012)

• .

Methodology• Modelling Approaches • Models and Equations

– Monthly– Quarterly– Annual

Monthly Data• Seasonality Indexes• Corporate Income Tax

Revenues

Corporate Income Tax Revenues

• CIT revenues = coefmonthly * CIT revenueslag *(1 + + PCIinfl/100)/12 + coefmay *PROFlag/100

where CIT revenues – corporate income tax revenues,CIT revenueslag – annual corporate income tax revenues with 17-month lag,coefmonthly – corporate income tax advance payments coefficient,PCIinfl – annual growth rate of private consumption price index in the previous year,coefmay – corporate income tax revenues coefficient applied only in May,PROFlag – annual profit in the previous year.

-0.5

0

0.5

1

1.5

2

2.5

-1000

-500

0

500

1000

1500

2000

2500

3000

3500

-1

0

1

2

3

4

5m EUR%

Corporate income tax revenues coefficient, %

Annual profit in the previous year, m EUR

Corporate Income Tax Revenues

SEE = 0.32 RSQ = 0.7593 RHO = 0.45 Obser = 196 from 1997.009

SEE+1 = 0.28 RBSQ = 0.7530 DW = 1.11 DoFree = 190 to 2013.012

MAPE = 9.70

Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 LTAX_UIN - - - - - - - - - - - - - - - - - 2.89 - - -

1 intercept 5.45808 5.9 1.89 4.15 1.00

2 @log(PCI[12]) -2.37844 18.5 -3.97 2.90 4.82 -0.904

3 @log(IM[12]) 0.48841 2.1 1.03 1.47 6.09 0.467

4 @log(IM[6]) 0.80975 7.9 1.72 1.26 6.15 0.761

5 D_5*@log(IM[6]) 0.09099 11.2 0.02 1.04 0.51 0.241

6 @log(W_NOM[8]/PCI[8]) 0.86536 1.8 0.31 1.00 1.05 0.375

Quarterly Data• Identities• Econometric Equations

Identitiestax_rev = taxr_coef*taxr*tax_base,

where tax_rev – tax revenues,taxr_coef – tax rate coefficient,taxr – tax rate,tax_base – tax base.

00.010.020.030.040.050.060.070.080.090.1

0

0.1

0.2

0.3

0.4

0.5

0.6

I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III

19951996199719981999200020012002200320042005200620072008200920102011201220132014

Tax rate coefficient of the value added tax Tax rate coefficient of excise duty, right axes

0.7

0.75

0.8

0.85

0.9

0.95

I III I III I III I III I III I III I III I III I III I III I III I III I III

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Tax rate coefficient of social contributions

Tax rate coefficient of personal income tax

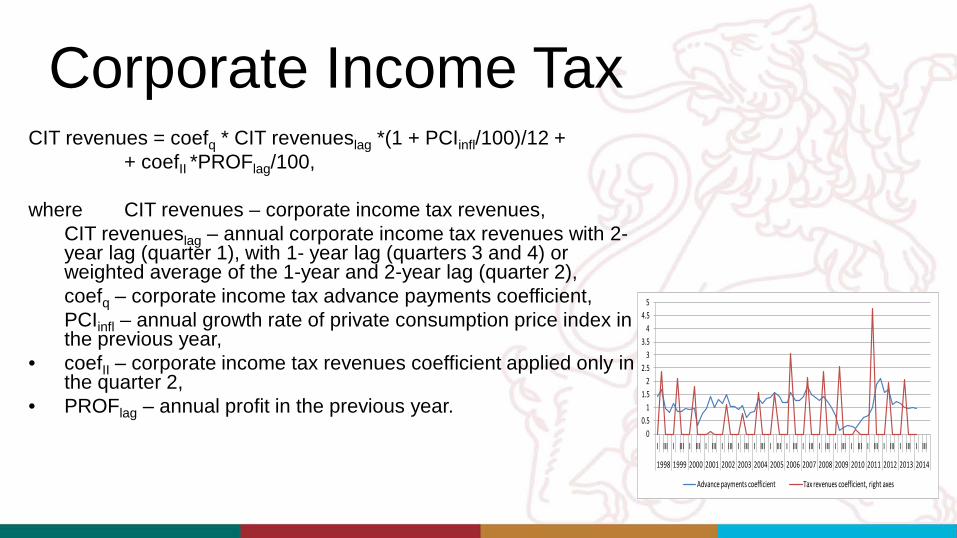

Corporate Income TaxCIT revenues = coefq * CIT revenueslag *(1 + PCIinfl/100)/12 +

+ coefII *PROFlag/100,

where CIT revenues – corporate income tax revenues,CIT revenueslag – annual corporate income tax revenues with 2-year lag (quarter 1), with 1- year lag (quarters 3 and 4) or weighted average of the 1-year and 2-year lag (quarter 2),coefq – corporate income tax advance payments coefficient,PCIinfl – annual growth rate of private consumption price index in the previous year,

• coefII – corporate income tax revenues coefficient applied only in the quarter 2,

• PROFlag – annual profit in the previous year.0

0.51

1.52

2.53

3.54

4.55

I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III I III

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Advance payments coefficient Tax revenues coefficient, right axes

Social Contributions Revenues

SEE = 12.80 RSQ = 0.9911 RHO = 0.43 Obser = 48 from 2002.100

SEE+1 = 11.82 RBSQ = 0.9907 DW = 1.14 DoFree = 45 to 2013.400

MAPE = 2.39

Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 TAX_SOC - - - - - - - - - - - - - - - - - 394.63 - - -

1 intercept -15.67795 5.9 -0.04 112.06 1.00

2 TAXR_SOC*((EMPL*W_NOM*3)/100000)

0.82441 929.9 1.03 1.22 492.62 1.007

3 D_EU 13.39648 10.3 0.01 1.00 0.31 0.046

Personal Income Tax Revenues

SEE = 10.34 RSQ = 0.9841 RHO = 0.14 Obser = 48 from 2002.100

SEE+1 = 10.34 RBSQ = 0.9834 DW = 1.72 DoFree = 45 to 2013.400

MAPE = 3.24

Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 TAX_INC_PERS - - - - - - - - - - - - - - - - - 246.31 - - -

1 intercept -15.42434 9.4 -0.06 62.85 1.00

2 TAXR_IIN*((EMPL*(W_NOM-TAX_NMIN))/1000-TAX_SOC*TAX_SOC_E)

3.39666 687.7 1.08 2.44 78.20 1.022

3 D_10 -46.54480 56.2 -0.02 1.00 0.08 -0.157

Corporate Income Tax Revenues

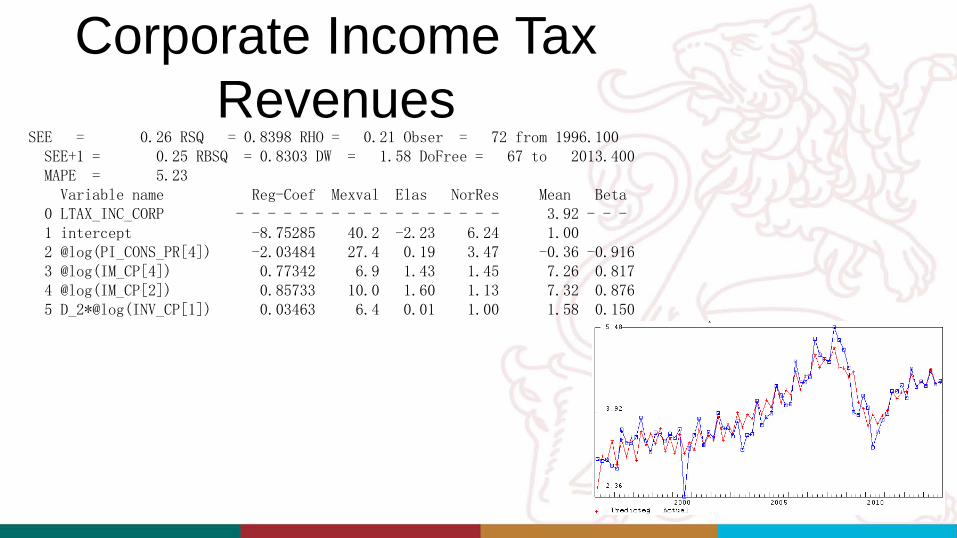

SEE = 0.26 RSQ = 0.8398 RHO = 0.21 Obser = 72 from 1996.100SEE+1 = 0.25 RBSQ = 0.8303 DW = 1.58 DoFree = 67 to 2013.400MAPE = 5.23Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 LTAX_INC_CORP - - - - - - - - - - - - - - - - - 3.92 - - -1 intercept -8.75285 40.2 -2.23 6.24 1.002 @log(PI_CONS_PR[4]) -2.03484 27.4 0.19 3.47 -0.36 -0.9163 @log(IM_CP[4]) 0.77342 6.9 1.43 1.45 7.26 0.8174 @log(IM_CP[2]) 0.85733 10.0 1.60 1.13 7.32 0.8765 D_2*@log(INV_CP[1]) 0.03463 6.4 0.01 1.00 1.58 0.150

Value Added Tax Revenues

SEE = 0.10 RSQ = 0.9723 RHO = 0.13 Obser = 76 from 1995.100

SEE+1 = 0.09 RBSQ = 0.9712 DW = 1.74 DoFree = 72 to 2013.400

MAPE = 1.37

Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 LTAX_VAT - - - - - - - - - - - - - - - - - 5.27 - - -

1 intercept -2.56866 55.4 -0.49 36.14 1.00

2 @log(GDP_CP) 1.03000 201.5 1.54 1.28 7.89 1.094

3 @log(TIME) -0.09040 6.8 -0.06 1.13 3.37 -0.143

4 D_EU 0.09103 6.5 0.00 1.00 0.20 0.063

Excise Duty RevenuesSEE = 0.08 RSQ = 0.9767 RHO = 0.06 Obser = 60 from 1999.100

SEE+1 = 0.08 RBSQ = 0.9759 DW = 1.87 DoFree = 57 to 2013.400

MAPE = 1.25

Variable name Reg-Coef Mexval Elas NorRes Mean Beta

0 LTAX_EXC - - - - - - - - - - - - - - - - - 4.70 - - -

1 intercept -3.29918 170.7 -0.70 42.90 1.00

2 @log(GDP_CP) 0.98389 514.3 1.70 1.39 8.11 0.958

3 D_0910 0.14311 17.7 0.00 1.00 0.13 0.098

Annual Data• Calculations in ESA95• Identities• Transformation Coefficients to

forecast national data

Dynamics of Estimated II Pillar Rates in 2003-2013

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Estimated II pillar rate (based on assets)

Estimated II pillar rate (based on differences in national and ESA95 methodologies)

Estimated II pillar rate (combined)

Max II pillar rate

Tax Rate Coefficients

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Tax rate coefficient of personal income tax

Tax rate coefficient of corporate income tax

Tax rate coefficient of social contributions

0.00

0.02

0.04

0.06

0.08

0.10

0.0

0.1

0.2

0.3

0.4

0.5

0.6

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Tax rate coefficient of the value added tax

Tax rate coefficient of excise duty, right axes

Forecasts• Evaluation of precision• Numbers

Corporate Income Tax (Monthly Data)

2014.001 – 2014.007• MAPE = 14.3%• Modified dummy MAPE = 3.6%

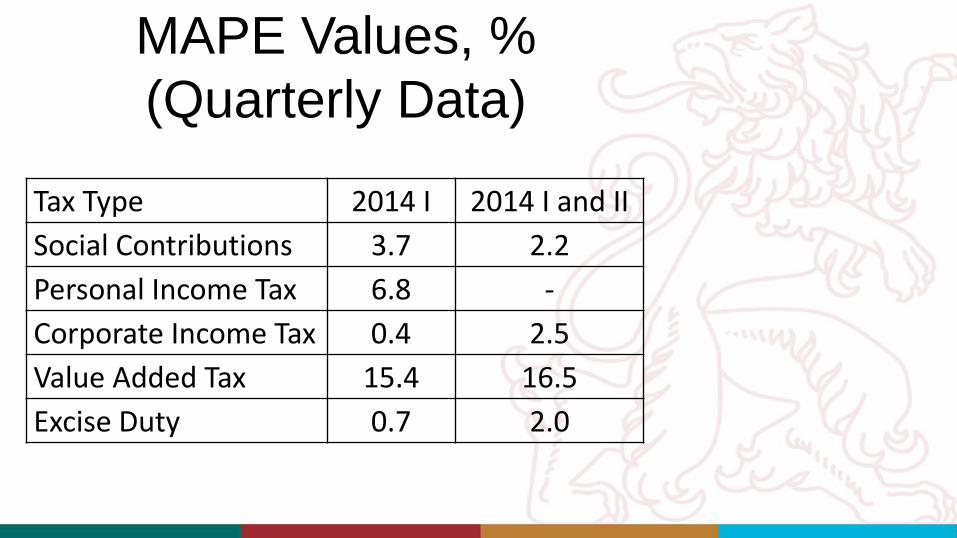

MAPE Values, % (Quarterly Data)

Tax Type 2014 I 2014 I and IISocial Contributions 3.7 2.2Personal Income Tax 6.8 -Corporate Income Tax 0.4 2.5Value Added Tax 15.4 16.5Excise Duty 0.7 2.0

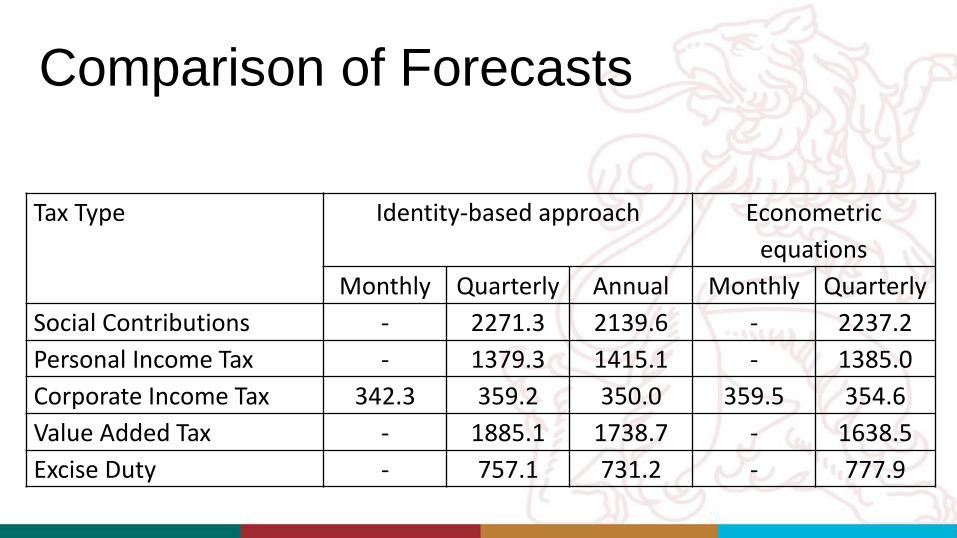

Comparison of Forecasts

Tax Type Identity-based approach Econometric equations

Monthly Quarterly Annual Monthly QuarterlySocial Contributions - 2271.3 2139.6 - 2237.2Personal Income Tax - 1379.3 1415.1 - 1385.0Corporate Income Tax 342.3 359.2 350.0 359.5 354.6Value Added Tax - 1885.1 1738.7 - 1638.5Excise Duty - 757.1 731.2 - 777.9

Conclusions• Using annual data, identity-based approach

should be prefered, however quarterly and monthly data can give similar results and thus the choice is in hands of the model-user

• Identity-based approach allows for a greater flexibility in scenario-building process. Econometric approach involves less assumptions and thus may seem to be more objective

• Forecasts depend very much on the values of exogenous indicators, therefore modelling approaches should be tested regulary to find the most reliable ones

LAIMA• Latvian Interindustry Model

(Aggregated/Annual)• Goddess of destiny

Thank You for Attention

Questions?