Embed Size (px)

Citation preview

Forecasts of Price Level Change Adjustors – 2016 Update

Note to Society of Local Government Managers

September 2016

www.berl.co.nz

Author(s): Dr Ganesh Nana and Konrad Hurren

All work is done, and services rendered at the request of, and for the purposes of the client only. Neither

BERL nor any of its employees accepts any responsibility on any grounds whatsoever, including negligence, to

any other person.

While every effort is made by BERL to ensure that the information, opinions and forecasts provided to the

client are accurate and reliable, BERL shall not be liable for any adverse consequences of the client’s

decisions made in reliance of any report provided by BERL, nor shall BERL be held to have given or implied

any warranty as to whether any report provided by BERL will assist in the performance of the client’s

functions.

©BERL Reference No: #5685 September 2016

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Making sense of the numbers i

Making sense of the numbers

This report contains forecasts for price level change adjustors for local authorities (LAs) to use in their budget

processes consistent with their Long Term Plans (LTPs). It incorporates the latest actual data to June 2016 and

forecasts the adjustors to June 2027. It continues the work undertaken over previous years.

Using the adjustors

As previously, differences in classifications of activities between councils lead to a degree of subjectivity in

terms of how to apply the adjustors to council expenditures. Last year’s report outlined suggested council

activities and how they might map across to the five adjustors. Using this information, councils can map their

expenditure items (or categories) to appropriate ‘category’ adjustors, and apply the relevant forecast change.

Alternatively, councils can (should they wish) directly use the forecasts for the eight individual price indices,

applying them to relevant expenditure items.

Forecasts

Similar to last year’s picture, the overall forecasts across the five adjustors remain relatively muted when

compared to those of earlier periods.

This is a reflection of a subdued inflationary picture both globally and domestically. It is broadly agreed that

the global economy is in a significant low inflationary period; with the US and Europe in particular close to

deflation. Faltering growth in China, and slow growth in the Eurozone have made for a subdued year; however,

growth in the United States economy is modestly more promising and may offset this somewhat.

With the Christchurch rebuild continuing to slow, the ongoing low level of dairy payouts and the difficult global

picture, there are few sources of sustained inflationary pressures ahead. In line with this context for the New

Zealand economy, these forecasts for price level adjustors present a subdued inflationary outlook for the local

government sector.

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Contents ii

Contents

1 Introduction .............................................................................................................. 1

1.1 Category adjustors and related price indices .......................................................................................1

1.2 Overall Local Government Cost Index ..................................................................................................2

1.3 LGCI vs CPI ..............................................................................................................................................2

1.4 Individual price indices ..........................................................................................................................3

2 The economic context for the adjustor forecasts .................................................. 4

2.1 General price inflation ...........................................................................................................................4

2.2 NZ macroeconomic picture ...................................................................................................................5

2.3 Global macroeconomic situation ..........................................................................................................6

3 Forecast for adjustors .............................................................................................. 8

3.1 Forecasted category adjustors ..............................................................................................................8

4 Forecast for overall LGCI ........................................................................................ 10

5 Forecasts for eight price indices ............................................................................ 13

Appendix A Equations to explain and forecast eight price indices .......................... 15

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Contents iii

Tables

Table 1: Category adjustors and related price indices ................................................................................................1

Table 2: Forecast of economic driver variables ...........................................................................................................4

Table 3: Adjustors: Index Jun 2016 = 1000 ..................................................................................................................8

Table 4: Adjustors: % per annum change ....................................................................................................................9

Table 5: Adjustors: Cumulative % change from Jun 2016 ...........................................................................................9

Table 6: LGCI, Index value (Jun 2016 = 1000) ........................................................................................................... 10

Table 7: LGCI, annual average % change ................................................................................................................... 11

Table 8: LGCI, cumulative % change from Jun 2016 ................................................................................................. 12

Table 9: Forecasts for eight price indices, annual average % change ..................................................................... 13

Table 10: Forecasts for eight price indices, cumulative % change from Jun 2016 ................................................. 14

Figures

Figure 1: Average price inflation in New Zealand retail sector ...................................................................................5

Figure 2: Annual GDP and employment growth ..........................................................................................................6

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Introduction 1

1 Introduction

These notes have been prepared for the Society of Local Government Managers (SOLGM). This document

contains provisional updates of forecasts for price level change adjustors for local authorities (LAs) to use in

their budget processes consistent with their Long-term Plans (LTP). It incorporates the latest actual data to

June 2016 and forecasts the adjustors to June 2026.

Our earlier reports (2005 to 2014) outlined the approach and methodology and discussed alternative adjustors

and reasons why the particular adjustors were chosen for forecasting. Last year a full review of the LGCI and its

subcomponents (i.e. the cost adjustor categories and their associated price indices) was undertaken. This

resulted in some revisions to the adjustors used and the relevant weighting distributions of the LGCI. This

review was undertaken by analysing the Annual Reports for the year ended June 2014 for a sample selection of

12 councils representing a cross-section of the local government sector. A breakdown of this review is

provided in Section 2 of the BERL report titled Forecasts of Price Level Change Adjustors – 2015 Update #5597.

The forecasts provide a medium-term view of the likely movement of the adjustors, rather than the movement

over the next year or two. There will always be unexpected reasons why individual costs might rise faster or

slower in a particular year. However, this does not necessarily mean that the medium-term forecast will, or

should, be adjusted. There will always be regional differences in the rate of change for a particular adjustor.

These adjustors are therefore forecasts at the national level and councils may need to consider if they have

further information to show why a difference might occur at the regional level.

1.1 Category adjustors and related price indices

BERL has forecast a total of eight unique adjustors against five categories for the period to 2026.

This differs from previous editions of the LGCI to reflect the revision of the cost adjustor categories and their

associated price indices, and the subsequent weight redistributions within the LGCI. Some of these category

adjustors are used applied against multiple categories, e.g. local government administration PPI.

Table 1: Category adjustors and related price indices

Category adjustor Related price indices

1. Planning and Regulation Local government sector salaries and wages

Local government administration PPI

Earthmoving and site work CGI

Pipelines CGI

Reclamation and river control CGI

2. Roading

Private sector salaries and wages

Earthmoving and site work CGI

Local government administration PPI

3. Transport Local government sector salaries and wages

Earthmoving and site work CGI

Local government administration PPI

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Introduction 2

4. Community Activities

Local government sector salaries and wages

Earthmoving and site work CGI

Arts and recreation services PPI

5. Water and Environmental Management Local government sector salaries and wages

Earthmoving and site work CGI

Pipelines CGI

Reclamation and river control CGI

Water, sewer, drainage, and waste services PPI

1.2 Overall Local Government Cost Index

These notes also contain forecasts for an overall cost index for local authorities (LGCI). This index has been

developed by BERL and is reported in ‘A Local Government Cost Index for New Zealand’, BERL reference #4877.

The LGCI is based on the cost structures of local authorities and includes operating expenditure (Opex) and

capital expenditure (Capex) variables.

The operating expenditure of the LGCI includes:

purchases of goods and services, grants and donations, and all other expenditure;

employee costs, which includes wages and salaries; and

interest paid, which includes interest paid on local government debts and is covered by the mortgage

interest component of the CPI.

The capital expenditure of the LGCI includes:

transport, which includes spending on transport projects and in particular roading;

infrastructure spending associated with the three waters; including water supply, wastewater, and

stormwater;

capital expenditure on community facilities such as pools, parks and reserves; and

other, which is capital expenditure not captured elsewhere.

1.3 LGCI vs CPI

An important point to note is the distinction between the LGCI and the Consumers Price Index (CPI). The main

distinction is in the composition of the basket of goods and services that each measures. The basket of goods

and services in the CPI represents the overall expenditure pattern of New Zealand households. These include

items such as food, health, clothing and footwear, and health. Such items are not directly relevant to, and do

not reflect the expenditure of LAs; hence the construction of the LGCI.

The LGCI is intended to reflect the selection and relative importance of the goods and services which represent

broadly the expenditure pattern of LAs in New Zealand. This basket thus includes more directly relevant items

including capital expenditure on pipelines, and earthmoving and site works, and operating expenditure such as

local government sector salary and wage rates.

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Introduction 3

1.4 Individual price indices

We have maintained and updated a separate local government wage indicator as per previous LGCI reports.

These are provided in section 5, along with forecasts for each of the individual price indices that together make

up the set of adjustors.

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

The economic context for the adjustor forecasts 4

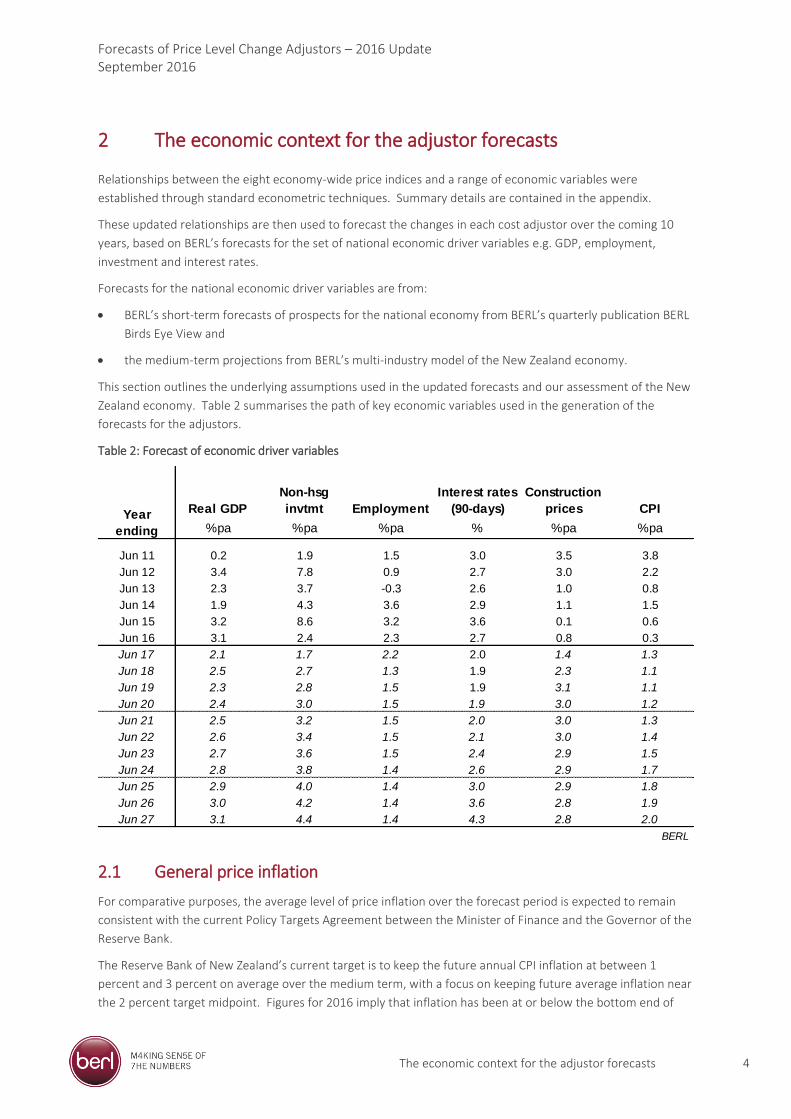

2 The economic context for the adjustor forecasts

Relationships between the eight economy-wide price indices and a range of economic variables were

established through standard econometric techniques. Summary details are contained in the appendix.

These updated relationships are then used to forecast the changes in each cost adjustor over the coming 10

years, based on BERL’s forecasts for the set of national economic driver variables e.g. GDP, employment,

investment and interest rates.

Forecasts for the national economic driver variables are from:

BERL’s short-term forecasts of prospects for the national economy from BERL’s quarterly publication BERL

Birds Eye View and

the medium-term projections from BERL’s multi-industry model of the New Zealand economy.

This section outlines the underlying assumptions used in the updated forecasts and our assessment of the New

Zealand economy. Table 2 summarises the path of key economic variables used in the generation of the

forecasts for the adjustors.

Table 2: Forecast of economic driver variables

2.1 General price inflation

For comparative purposes, the average level of price inflation over the forecast period is expected to remain

consistent with the current Policy Targets Agreement between the Minister of Finance and the Governor of the

Reserve Bank.

The Reserve Bank of New Zealand’s current target is to keep the future annual CPI inflation at between 1

percent and 3 percent on average over the medium term, with a focus on keeping future average inflation near

the 2 percent target midpoint. Figures for 2016 imply that inflation has been at or below the bottom end of

Real GDP

Non-hsg

invtmt Employment

Interest rates

(90-days)

Construction

prices CPI

%pa %pa %pa % %pa %pa

Jun 11 0.2 1.9 1.5 3.0 3.5 3.8

Jun 12 3.4 7.8 0.9 2.7 3.0 2.2

Jun 13 2.3 3.7 -0.3 2.6 1.0 0.8

Jun 14 1.9 4.3 3.6 2.9 1.1 1.5

Jun 15 3.2 8.6 3.2 3.6 0.1 0.6

Jun 16 3.1 2.4 2.3 2.7 0.8 0.3

Jun 17 2.1 1.7 2.2 2.0 1.4 1.3

Jun 18 2.5 2.7 1.3 1.9 2.3 1.1

Jun 19 2.3 2.8 1.5 1.9 3.1 1.1

Jun 20 2.4 3.0 1.5 1.9 3.0 1.2

Jun 21 2.5 3.2 1.5 2.0 3.0 1.3

Jun 22 2.6 3.4 1.5 2.1 3.0 1.4

Jun 23 2.7 3.6 1.5 2.4 2.9 1.5

Jun 24 2.8 3.8 1.4 2.6 2.9 1.7

Jun 25 2.9 4.0 1.4 3.0 2.9 1.8

Jun 26 3.0 4.2 1.4 3.6 2.8 1.9

Jun 27 3.1 4.4 1.4 4.3 2.8 2.0

BERL

Year

ending

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

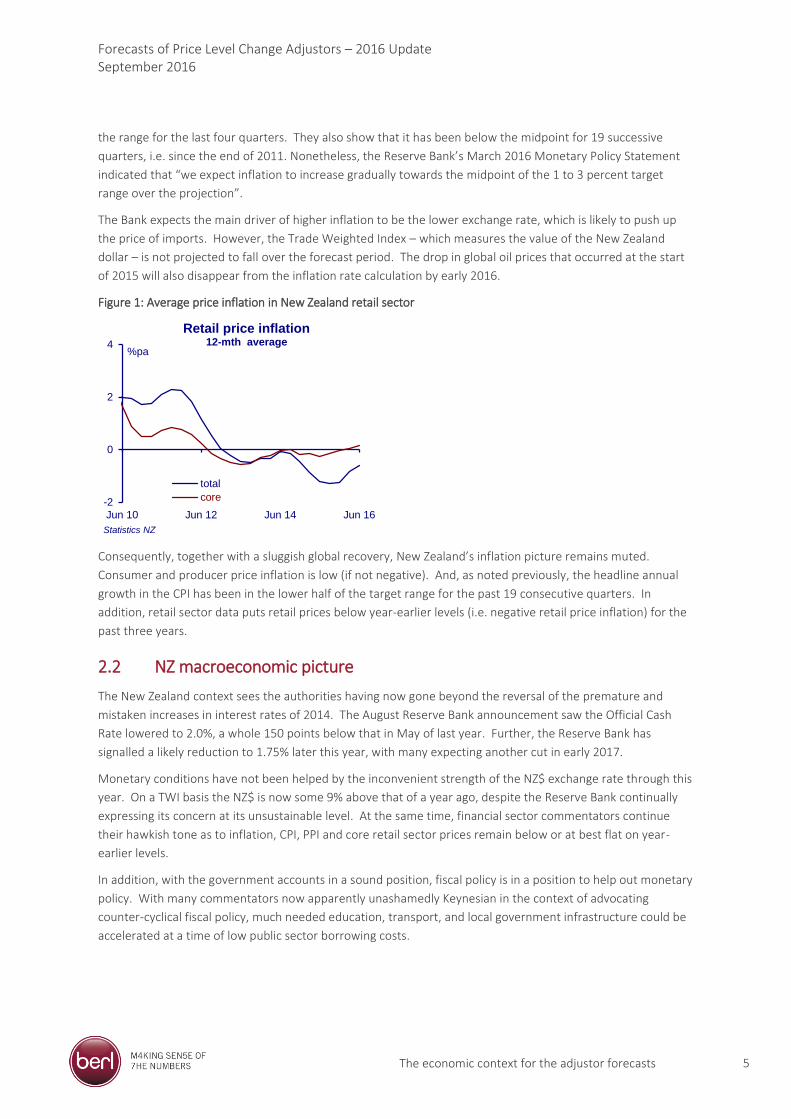

The economic context for the adjustor forecasts 5

the range for the last four quarters. They also show that it has been below the midpoint for 19 successive

quarters, i.e. since the end of 2011. Nonetheless, the Reserve Bank’s March 2016 Monetary Policy Statement

indicated that “we expect inflation to increase gradually towards the midpoint of the 1 to 3 percent target

range over the projection”.

The Bank expects the main driver of higher inflation to be the lower exchange rate, which is likely to push up

the price of imports. However, the Trade Weighted Index – which measures the value of the New Zealand

dollar – is not projected to fall over the forecast period. The drop in global oil prices that occurred at the start

of 2015 will also disappear from the inflation rate calculation by early 2016.

Figure 1: Average price inflation in New Zealand retail sector

Consequently, together with a sluggish global recovery, New Zealand’s inflation picture remains muted.

Consumer and producer price inflation is low (if not negative). And, as noted previously, the headline annual

growth in the CPI has been in the lower half of the target range for the past 19 consecutive quarters. In

addition, retail sector data puts retail prices below year-earlier levels (i.e. negative retail price inflation) for the

past three years.

2.2 NZ macroeconomic picture

The New Zealand context sees the authorities having now gone beyond the reversal of the premature and

mistaken increases in interest rates of 2014. The August Reserve Bank announcement saw the Official Cash

Rate lowered to 2.0%, a whole 150 points below that in May of last year. Further, the Reserve Bank has

signalled a likely reduction to 1.75% later this year, with many expecting another cut in early 2017.

Monetary conditions have not been helped by the inconvenient strength of the NZ$ exchange rate through this

year. On a TWI basis the NZ$ is now some 9% above that of a year ago, despite the Reserve Bank continually

expressing its concern at its unsustainable level. At the same time, financial sector commentators continue

their hawkish tone as to inflation, CPI, PPI and core retail sector prices remain below or at best flat on year-

earlier levels.

In addition, with the government accounts in a sound position, fiscal policy is in a position to help out monetary

policy. With many commentators now apparently unashamedly Keynesian in the context of advocating

counter-cyclical fiscal policy, much needed education, transport, and local government infrastructure could be

accelerated at a time of low public sector borrowing costs.

-2

0

2

4

Jun 10 Jun 12 Jun 14 Jun 16

%pa

Statistics NZ

Retail price inflation12-mth average

total

core

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

The economic context for the adjustor forecasts 6

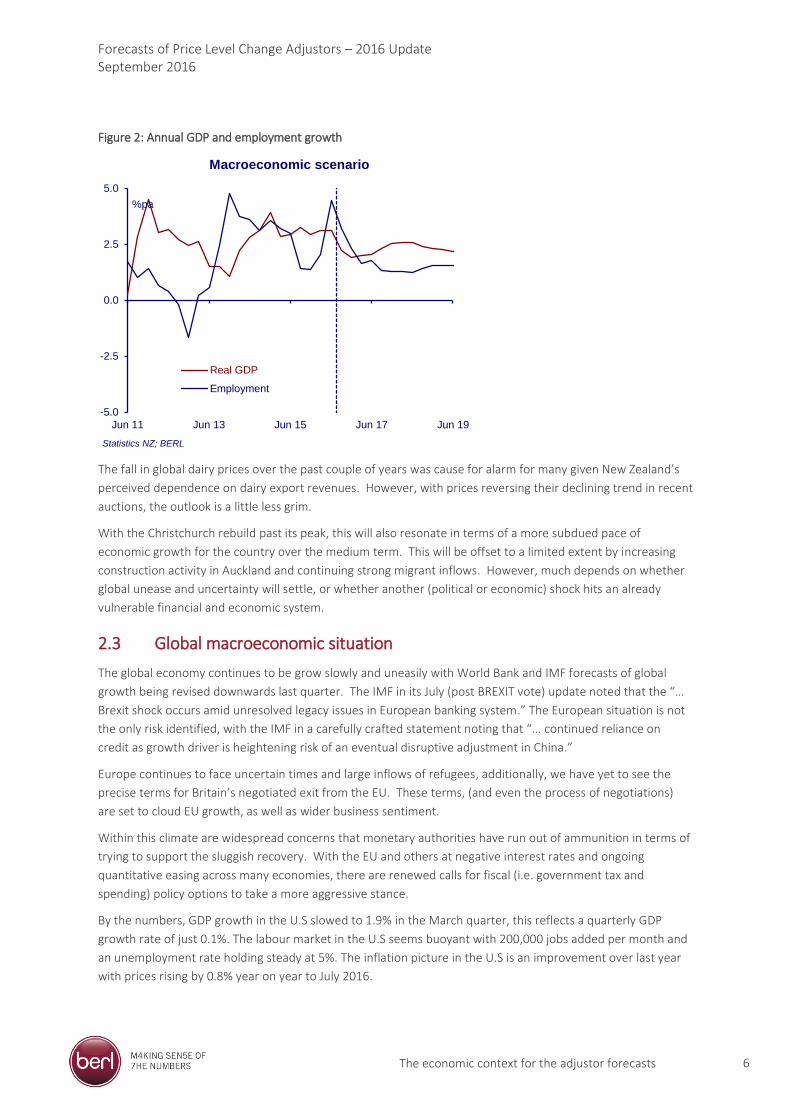

Figure 2: Annual GDP and employment growth

The fall in global dairy prices over the past couple of years was cause for alarm for many given New Zealand’s

perceived dependence on dairy export revenues. However, with prices reversing their declining trend in recent

auctions, the outlook is a little less grim.

With the Christchurch rebuild past its peak, this will also resonate in terms of a more subdued pace of

economic growth for the country over the medium term. This will be offset to a limited extent by increasing

construction activity in Auckland and continuing strong migrant inflows. However, much depends on whether

global unease and uncertainty will settle, or whether another (political or economic) shock hits an already

vulnerable financial and economic system.

2.3 Global macroeconomic situation

The global economy continues to be grow slowly and uneasily with World Bank and IMF forecasts of global

growth being revised downwards last quarter. The IMF in its July (post BREXIT vote) update noted that the “…

Brexit shock occurs amid unresolved legacy issues in European banking system.” The European situation is not

the only risk identified, with the IMF in a carefully crafted statement noting that “… continued reliance on

credit as growth driver is heightening risk of an eventual disruptive adjustment in China.”

Europe continues to face uncertain times and large inflows of refugees, additionally, we have yet to see the

precise terms for Britain’s negotiated exit from the EU. These terms, (and even the process of negotiations)

are set to cloud EU growth, as well as wider business sentiment.

Within this climate are widespread concerns that monetary authorities have run out of ammunition in terms of

trying to support the sluggish recovery. With the EU and others at negative interest rates and ongoing

quantitative easing across many economies, there are renewed calls for fiscal (i.e. government tax and

spending) policy options to take a more aggressive stance.

By the numbers, GDP growth in the U.S slowed to 1.9% in the March quarter, this reflects a quarterly GDP

growth rate of just 0.1%. The labour market in the U.S seems buoyant with 200,000 jobs added per month and

an unemployment rate holding steady at 5%. The inflation picture in the U.S is an improvement over last year

with prices rising by 0.8% year on year to July 2016.

-5.0

-2.5

0.0

2.5

5.0

Jun 11 Jun 13 Jun 15 Jun 17 Jun 19

%pa

Statistics NZ; BERL

Macroeconomic scenario

Real GDP

Employment

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

The economic context for the adjustor forecasts 7

Forecasts suggest that the US economy will strengthen its current growth pattern over the next two years, with

annual GDP growth between 1.5 to 2.0%, which combined with unemployment predicted to fall below 5

percent, will see the US buying more goods and services from the rest of the world.

China’s faltering economic growth has been concerning, with the Chinese government surprising global

markets by devaluing the Yuan by 1.9 percent last year. Also, weaker than expected factory activity has been

reported due to declining domestic and export demand for manufactured goods. The Chinese economy grew

by 6.7% in the year to June 2016. China still holds its official target of 7.0% GDP growth annually however the

IMF forecasts Chinese growth to slow to 6.3% by year’s end.

The EU, particularly the main members, has continued their slow but sure growth out of the last recession,

with an increase of 1.7 percent for the year. The UK has continued their run of strong positive growth with a

2.1 percent increase for the year, lower than the annual increase of 2.6 percent for the year to June 2015.

Germany has seen its annual GDP growth remain at 1.6 percent for the year to June 2016, after dropping down

to just 1.0 percent in the year to March 2015. The unemployment rate in EU remains high, though there are

signs of improvement. The official EU unemployment rate is 8.7% with Greece the highest at 24% and Germany

lowest at 4.2%.

Forecasts for the Euro zone are expecting that GDP growth for Europe will almost reach 2 percent in 2016, with

GDP growth in Germany climbing back to 1.9 percent in 2016.

Australian GDP growth has picked up, now at 3.1% to March 2016, Australia has managed to stop its rising

unemployment. Despite this recent uptick, signs are pointing to the Australian economy to continue its slow

down, with iron ore prices still below $50 a tonne, well down on the $100+ a tonne last seen at the start of

2014, low investment in the mining industry, and Chinese GDP growth and imports declining.

Forecasts have Australia bouncing back in 2016 with GDP growth once again growing by almost 3 percent per

annum, and unemployment remaining below 6 percent.

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecast for adjustors 8

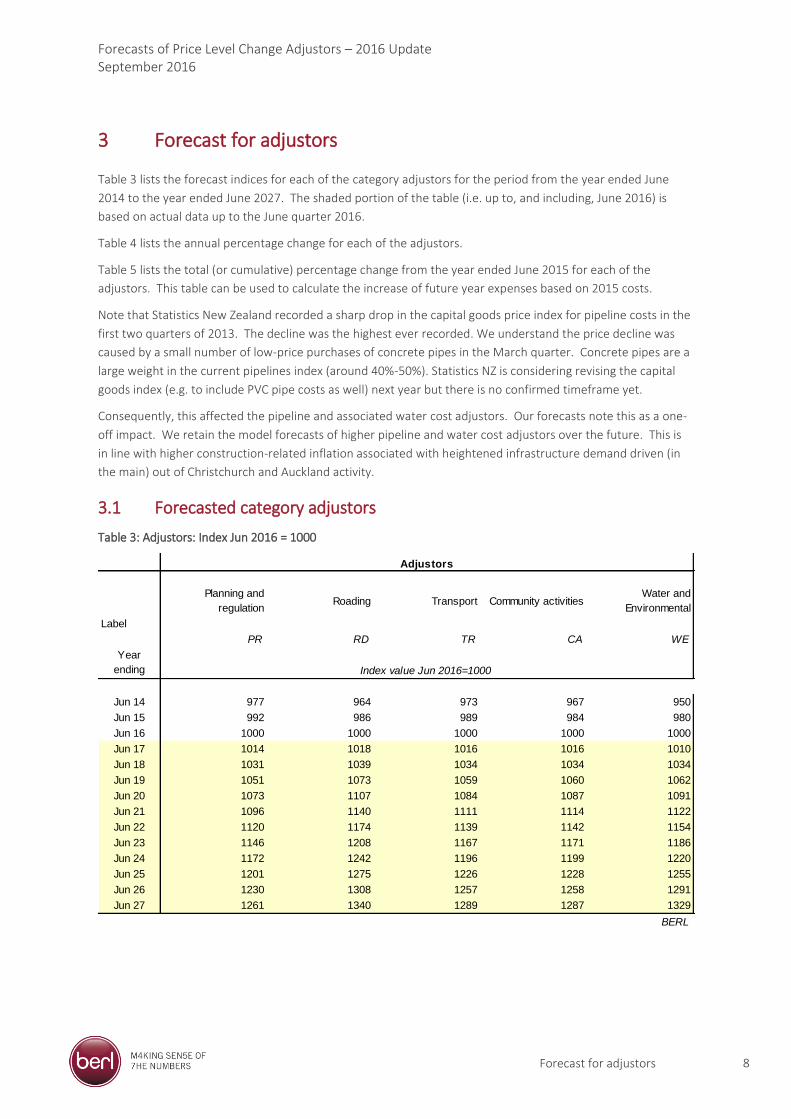

3 Forecast for adjustors

Table 3 lists the forecast indices for each of the category adjustors for the period from the year ended June

2014 to the year ended June 2027. The shaded portion of the table (i.e. up to, and including, June 2016) is

based on actual data up to the June quarter 2016.

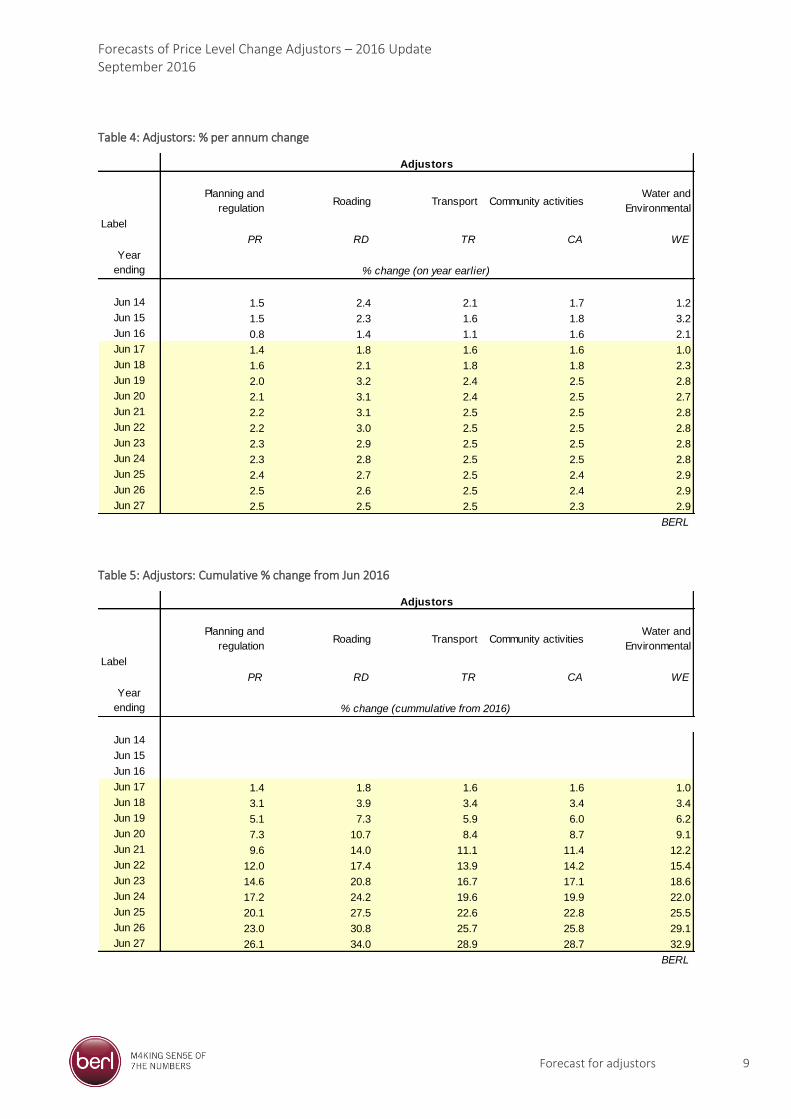

Table 4 lists the annual percentage change for each of the adjustors.

Table 5 lists the total (or cumulative) percentage change from the year ended June 2015 for each of the

adjustors. This table can be used to calculate the increase of future year expenses based on 2015 costs.

Note that Statistics New Zealand recorded a sharp drop in the capital goods price index for pipeline costs in the

first two quarters of 2013. The decline was the highest ever recorded. We understand the price decline was

caused by a small number of low-price purchases of concrete pipes in the March quarter. Concrete pipes are a

large weight in the current pipelines index (around 40%-50%). Statistics NZ is considering revising the capital

goods index (e.g. to include PVC pipe costs as well) next year but there is no confirmed timeframe yet.

Consequently, this affected the pipeline and associated water cost adjustors. Our forecasts note this as a one-

off impact. We retain the model forecasts of higher pipeline and water cost adjustors over the future. This is

in line with higher construction-related inflation associated with heightened infrastructure demand driven (in

the main) out of Christchurch and Auckland activity.

3.1 Forecasted category adjustors

Table 3: Adjustors: Index Jun 2016 = 1000

Label

Planning and

regulationRoading Transport Community activities

Water and

Environmental

PR RD TR CA WE

Jun 14 977 964 973 967 950

Jun 15 992 986 989 984 980

Jun 16 1000 1000 1000 1000 1000

Jun 17 1014 1018 1016 1016 1010

Jun 18 1031 1039 1034 1034 1034

Jun 19 1051 1073 1059 1060 1062

Jun 20 1073 1107 1084 1087 1091

Jun 21 1096 1140 1111 1114 1122

Jun 22 1120 1174 1139 1142 1154

Jun 23 1146 1208 1167 1171 1186

Jun 24 1172 1242 1196 1199 1220

Jun 25 1201 1275 1226 1228 1255

Jun 26 1230 1308 1257 1258 1291

Jun 27 1261 1340 1289 1287 1329

BERL

Year

ending Index value Jun 2016=1000

Adjustors

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecast for adjustors 9

Table 4: Adjustors: % per annum change

Table 5: Adjustors: Cumulative % change from Jun 2016

Label

Planning and

regulationRoading Transport Community activities

Water and

Environmental

PR RD TR CA WE

Jun 14 1.5 2.4 2.1 1.7 1.2

Jun 15 1.5 2.3 1.6 1.8 3.2

Jun 16 0.8 1.4 1.1 1.6 2.1

Jun 17 1.4 1.8 1.6 1.6 1.0

Jun 18 1.6 2.1 1.8 1.8 2.3

Jun 19 2.0 3.2 2.4 2.5 2.8

Jun 20 2.1 3.1 2.4 2.5 2.7

Jun 21 2.2 3.1 2.5 2.5 2.8

Jun 22 2.2 3.0 2.5 2.5 2.8

Jun 23 2.3 2.9 2.5 2.5 2.8

Jun 24 2.3 2.8 2.5 2.5 2.8

Jun 25 2.4 2.7 2.5 2.4 2.9

Jun 26 2.5 2.6 2.5 2.4 2.9

Jun 27 2.5 2.5 2.5 2.3 2.9

BERL

Year

ending % change (on year earlier)

Adjustors

Label

Planning and

regulationRoading Transport Community activities

Water and

Environmental

PR RD TR CA WE

Jun 14

Jun 15

Jun 16

Jun 17 1.4 1.8 1.6 1.6 1.0

Jun 18 3.1 3.9 3.4 3.4 3.4

Jun 19 5.1 7.3 5.9 6.0 6.2

Jun 20 7.3 10.7 8.4 8.7 9.1

Jun 21 9.6 14.0 11.1 11.4 12.2

Jun 22 12.0 17.4 13.9 14.2 15.4

Jun 23 14.6 20.8 16.7 17.1 18.6

Jun 24 17.2 24.2 19.6 19.9 22.0

Jun 25 20.1 27.5 22.6 22.8 25.5

Jun 26 23.0 30.8 25.7 25.8 29.1

Jun 27 26.1 34.0 28.9 28.7 32.9

BERL

Year

ending % change (cummulative from 2016)

Adjustors

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecast for overall LGCI 10

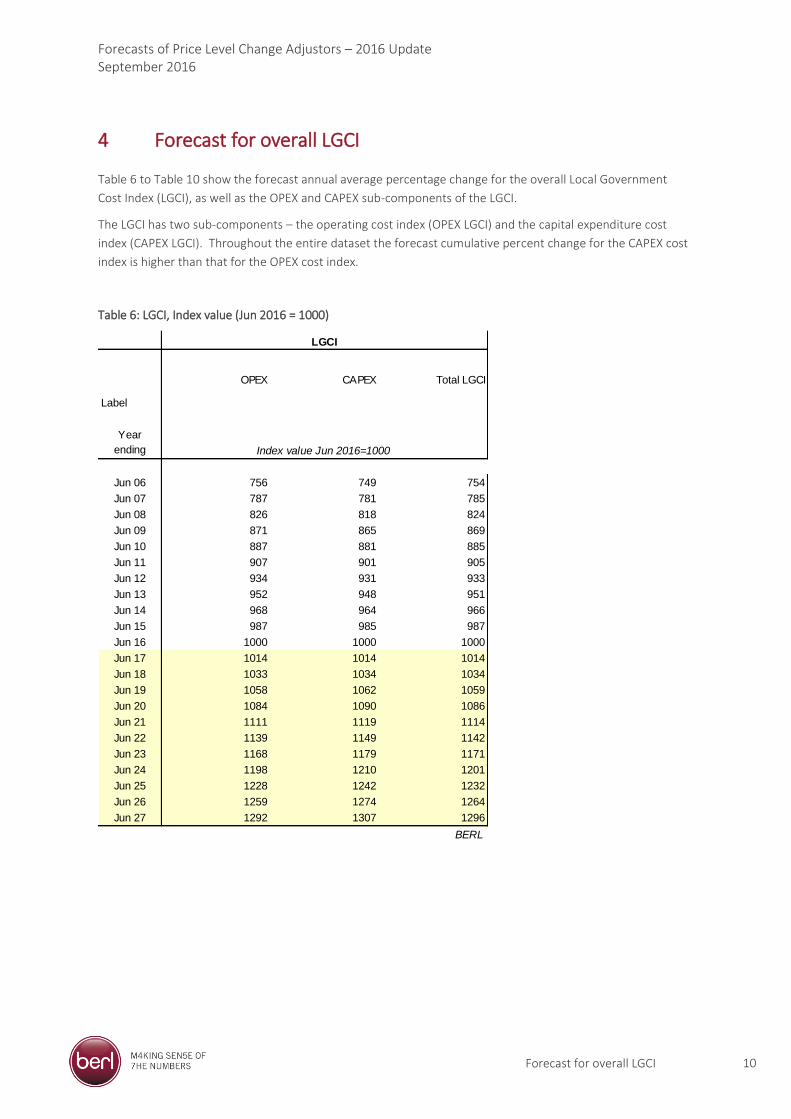

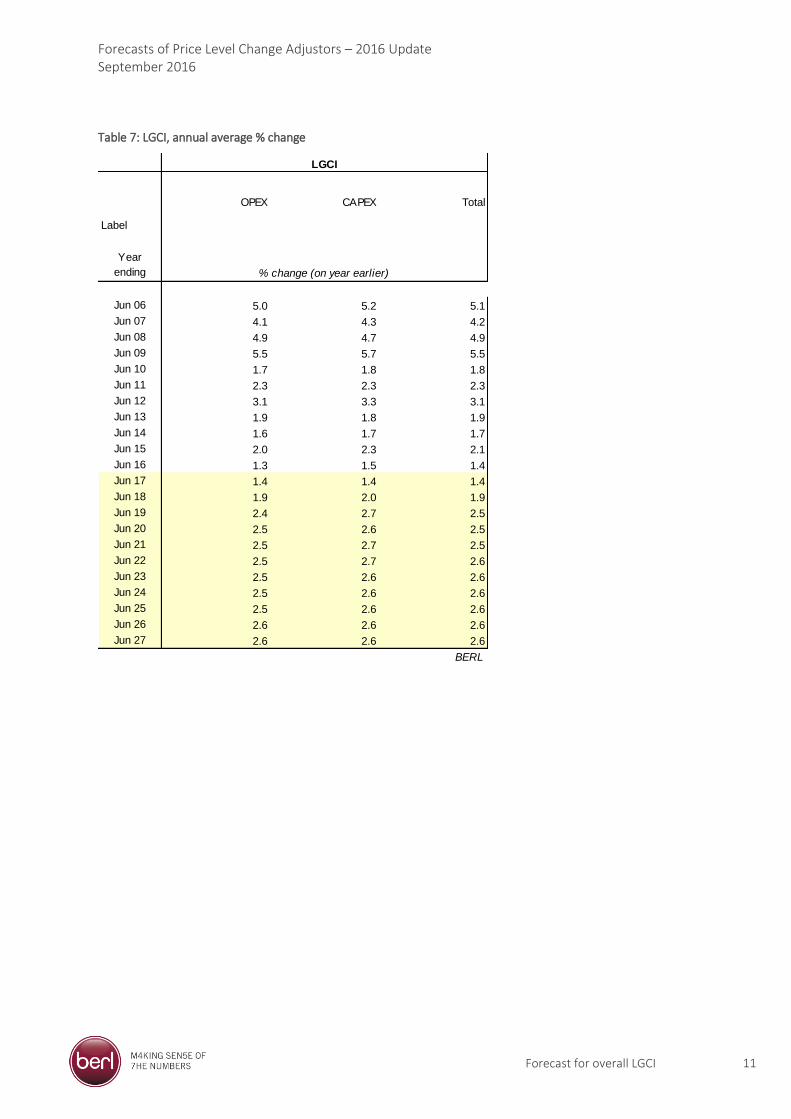

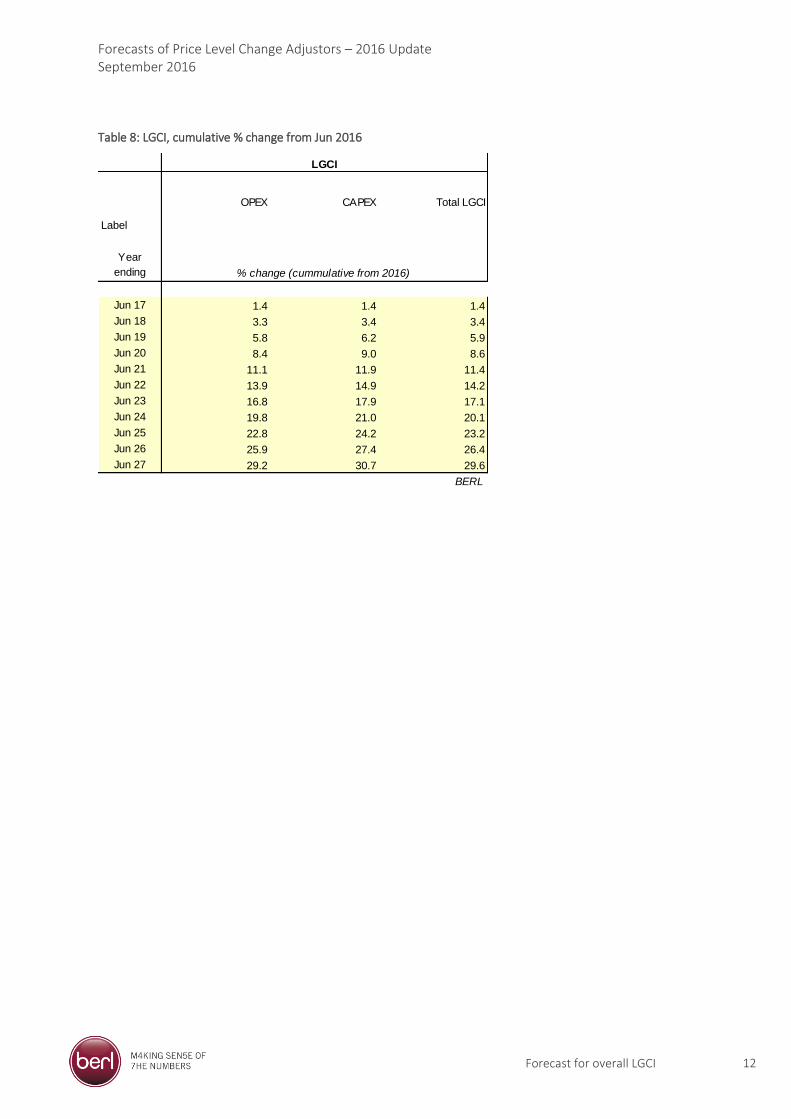

4 Forecast for overall LGCI

Table 6 to Table 10 show the forecast annual average percentage change for the overall Local Government

Cost Index (LGCI), as well as the OPEX and CAPEX sub-components of the LGCI.

The LGCI has two sub-components – the operating cost index (OPEX LGCI) and the capital expenditure cost

index (CAPEX LGCI). Throughout the entire dataset the forecast cumulative percent change for the CAPEX cost

index is higher than that for the OPEX cost index.

Table 6: LGCI, Index value (Jun 2016 = 1000)

Label

OPEX CAPEX Total LGCI

Jun 06 756 749 754

Jun 07 787 781 785

Jun 08 826 818 824

Jun 09 871 865 869

Jun 10 887 881 885

Jun 11 907 901 905

Jun 12 934 931 933

Jun 13 952 948 951

Jun 14 968 964 966

Jun 15 987 985 987

Jun 16 1000 1000 1000

Jun 17 1014 1014 1014

Jun 18 1033 1034 1034

Jun 19 1058 1062 1059

Jun 20 1084 1090 1086

Jun 21 1111 1119 1114

Jun 22 1139 1149 1142

Jun 23 1168 1179 1171

Jun 24 1198 1210 1201

Jun 25 1228 1242 1232

Jun 26 1259 1274 1264

Jun 27 1292 1307 1296

BERL

Year

ending Index value Jun 2016=1000

LGCI

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecast for overall LGCI 11

Table 7: LGCI, annual average % change

Label

OPEX CAPEX Total

Jun 06 5.0 5.2 5.1

Jun 07 4.1 4.3 4.2

Jun 08 4.9 4.7 4.9

Jun 09 5.5 5.7 5.5

Jun 10 1.7 1.8 1.8

Jun 11 2.3 2.3 2.3

Jun 12 3.1 3.3 3.1

Jun 13 1.9 1.8 1.9

Jun 14 1.6 1.7 1.7

Jun 15 2.0 2.3 2.1

Jun 16 1.3 1.5 1.4

Jun 17 1.4 1.4 1.4

Jun 18 1.9 2.0 1.9

Jun 19 2.4 2.7 2.5

Jun 20 2.5 2.6 2.5

Jun 21 2.5 2.7 2.5

Jun 22 2.5 2.7 2.6

Jun 23 2.5 2.6 2.6

Jun 24 2.5 2.6 2.6

Jun 25 2.5 2.6 2.6

Jun 26 2.6 2.6 2.6

Jun 27 2.6 2.6 2.6

BERL

Year

ending % change (on year earlier)

LGCI

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecast for overall LGCI 12

Table 8: LGCI, cumulative % change from Jun 2016

Label

OPEX CAPEX Total LGCI

Jun 17 1.4 1.4 1.4

Jun 18 3.3 3.4 3.4

Jun 19 5.8 6.2 5.9

Jun 20 8.4 9.0 8.6

Jun 21 11.1 11.9 11.4

Jun 22 13.9 14.9 14.2

Jun 23 16.8 17.9 17.1

Jun 24 19.8 21.0 20.1

Jun 25 22.8 24.2 23.2

Jun 26 25.9 27.4 26.4

Jun 27 29.2 30.7 29.6

BERL

% change (cummulative from 2016)

LGCI

Year

ending

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecasts for eight price indices 13

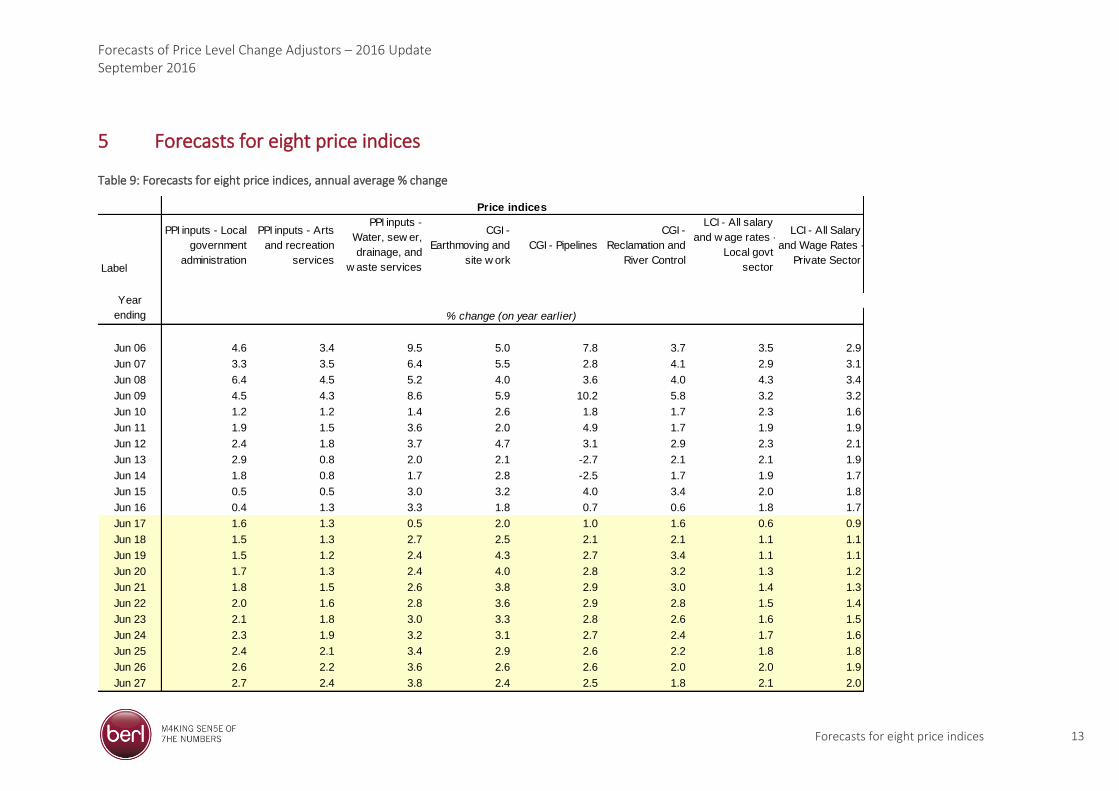

5 Forecasts for eight price indices

Table 9: Forecasts for eight price indices, annual average % change

Label

PPI inputs - Local

government

administration

PPI inputs - Arts

and recreation

services

PPI inputs -

Water, sew er,

drainage, and

w aste services

CGI -

Earthmoving and

site w ork

CGI - Pipelines

CGI -

Reclamation and

River Control

LCI - All salary

and w age rates -

Local govt

sector

LCI - All Salary

and Wage Rates -

Private Sector

Jun 06 4.6 3.4 9.5 5.0 7.8 3.7 3.5 2.9

Jun 07 3.3 3.5 6.4 5.5 2.8 4.1 2.9 3.1

Jun 08 6.4 4.5 5.2 4.0 3.6 4.0 4.3 3.4

Jun 09 4.5 4.3 8.6 5.9 10.2 5.8 3.2 3.2

Jun 10 1.2 1.2 1.4 2.6 1.8 1.7 2.3 1.6

Jun 11 1.9 1.5 3.6 2.0 4.9 1.7 1.9 1.9

Jun 12 2.4 1.8 3.7 4.7 3.1 2.9 2.3 2.1

Jun 13 2.9 0.8 2.0 2.1 -2.7 2.1 2.1 1.9

Jun 14 1.8 0.8 1.7 2.8 -2.5 1.7 1.9 1.7

Jun 15 0.5 0.5 3.0 3.2 4.0 3.4 2.0 1.8

Jun 16 0.4 1.3 3.3 1.8 0.7 0.6 1.8 1.7

Jun 17 1.6 1.3 0.5 2.0 1.0 1.6 0.6 0.9

Jun 18 1.5 1.3 2.7 2.5 2.1 2.1 1.1 1.1

Jun 19 1.5 1.2 2.4 4.3 2.7 3.4 1.1 1.1

Jun 20 1.7 1.3 2.4 4.0 2.8 3.2 1.3 1.2

Jun 21 1.8 1.5 2.6 3.8 2.9 3.0 1.4 1.3

Jun 22 2.0 1.6 2.8 3.6 2.9 2.8 1.5 1.4

Jun 23 2.1 1.8 3.0 3.3 2.8 2.6 1.6 1.5

Jun 24 2.3 1.9 3.2 3.1 2.7 2.4 1.7 1.6

Jun 25 2.4 2.1 3.4 2.9 2.6 2.2 1.8 1.8

Jun 26 2.6 2.2 3.6 2.6 2.6 2.0 2.0 1.9

Jun 27 2.7 2.4 3.8 2.4 2.5 1.8 2.1 2.0

Year

ending

Price indices

% change (on year earlier)

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Forecasts for eight price indices 14

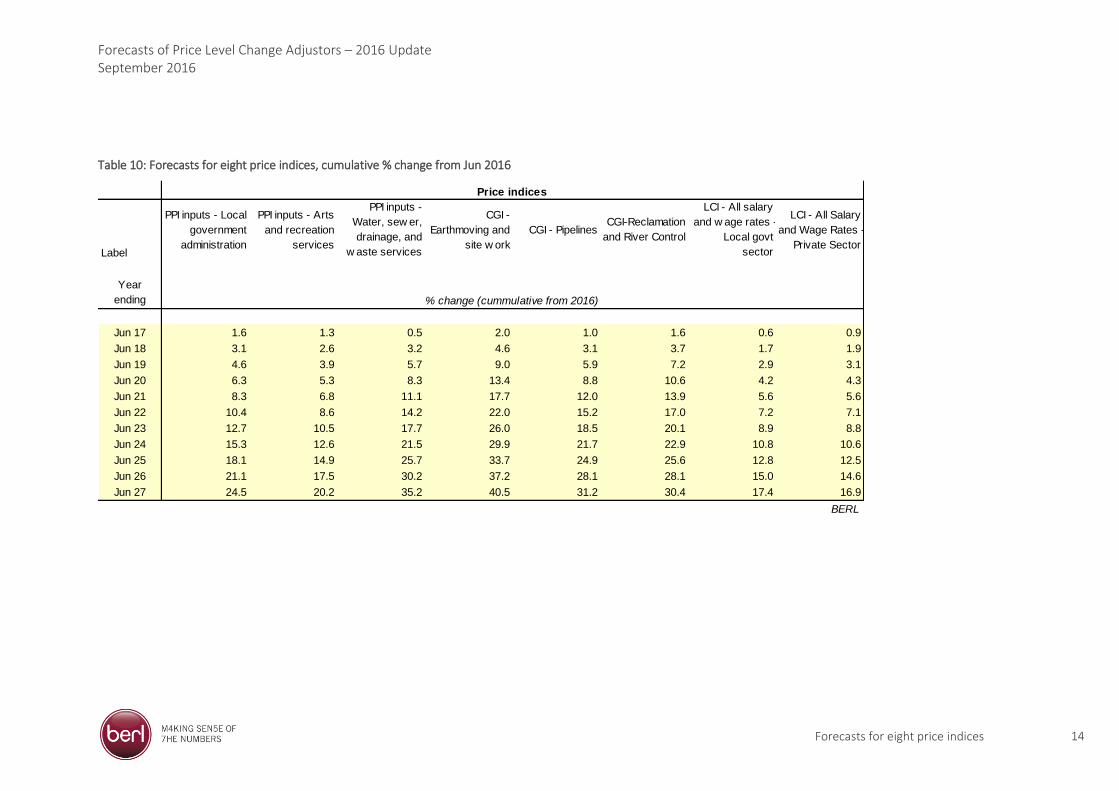

Table 10: Forecasts for eight price indices, cumulative % change from Jun 2016

Label

PPI inputs - Local

government

administration

PPI inputs - Arts

and recreation

services

PPI inputs -

Water, sew er,

drainage, and

w aste services

CGI -

Earthmoving and

site w ork

CGI - PipelinesCGI-Reclamation

and River Control

LCI - All salary

and w age rates -

Local govt

sector

LCI - All Salary

and Wage Rates -

Private Sector

Jun 16 0.4 1.3 3.3 1.8 0.7 0.6 1.8 1.7

Jun 17 1.6 1.3 0.5 2.0 1.0 1.6 0.6 0.9

Jun 18 3.1 2.6 3.2 4.6 3.1 3.7 1.7 1.9

Jun 19 4.6 3.9 5.7 9.0 5.9 7.2 2.9 3.1

Jun 20 6.3 5.3 8.3 13.4 8.8 10.6 4.2 4.3

Jun 21 8.3 6.8 11.1 17.7 12.0 13.9 5.6 5.6

Jun 22 10.4 8.6 14.2 22.0 15.2 17.0 7.2 7.1

Jun 23 12.7 10.5 17.7 26.0 18.5 20.1 8.9 8.8

Jun 24 15.3 12.6 21.5 29.9 21.7 22.9 10.8 10.6

Jun 25 18.1 14.9 25.7 33.7 24.9 25.6 12.8 12.5

Jun 26 21.1 17.5 30.2 37.2 28.1 28.1 15.0 14.6

Jun 27 24.5 20.2 35.2 40.5 31.2 30.4 17.4 16.9

BERL

Year

ending

Price indices

% change (cummulative from 2016)

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 15

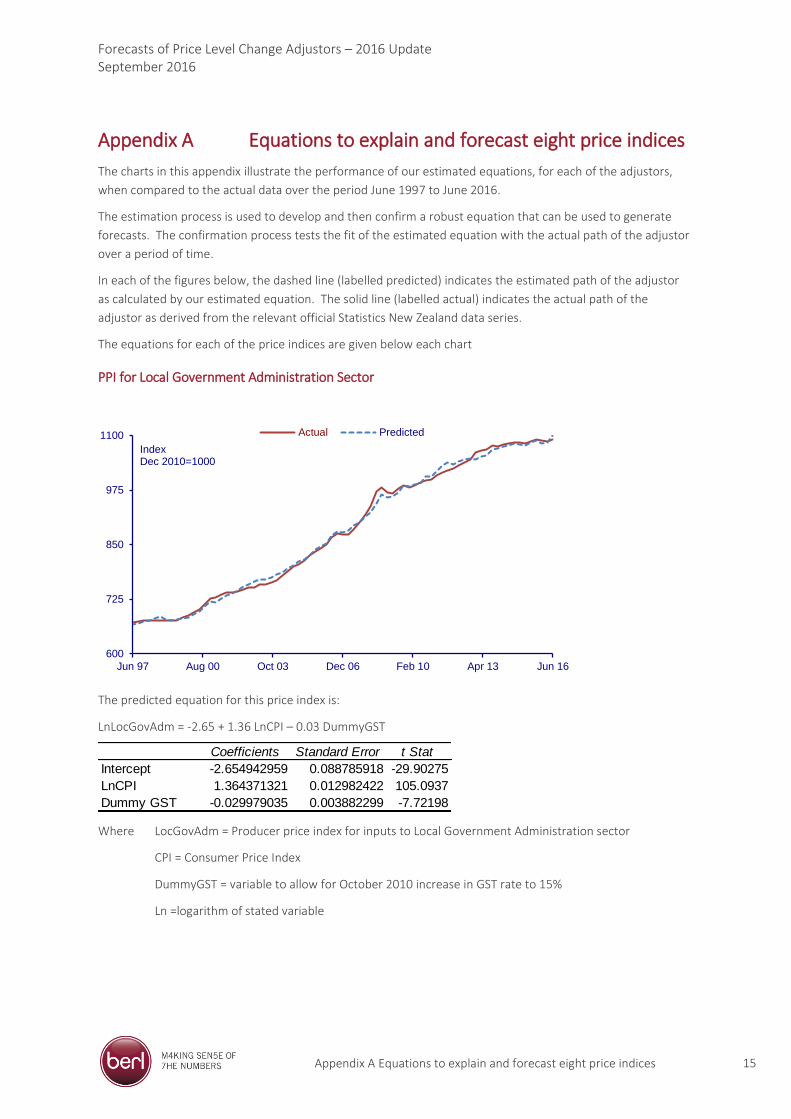

Appendix A Equations to explain and forecast eight price indices

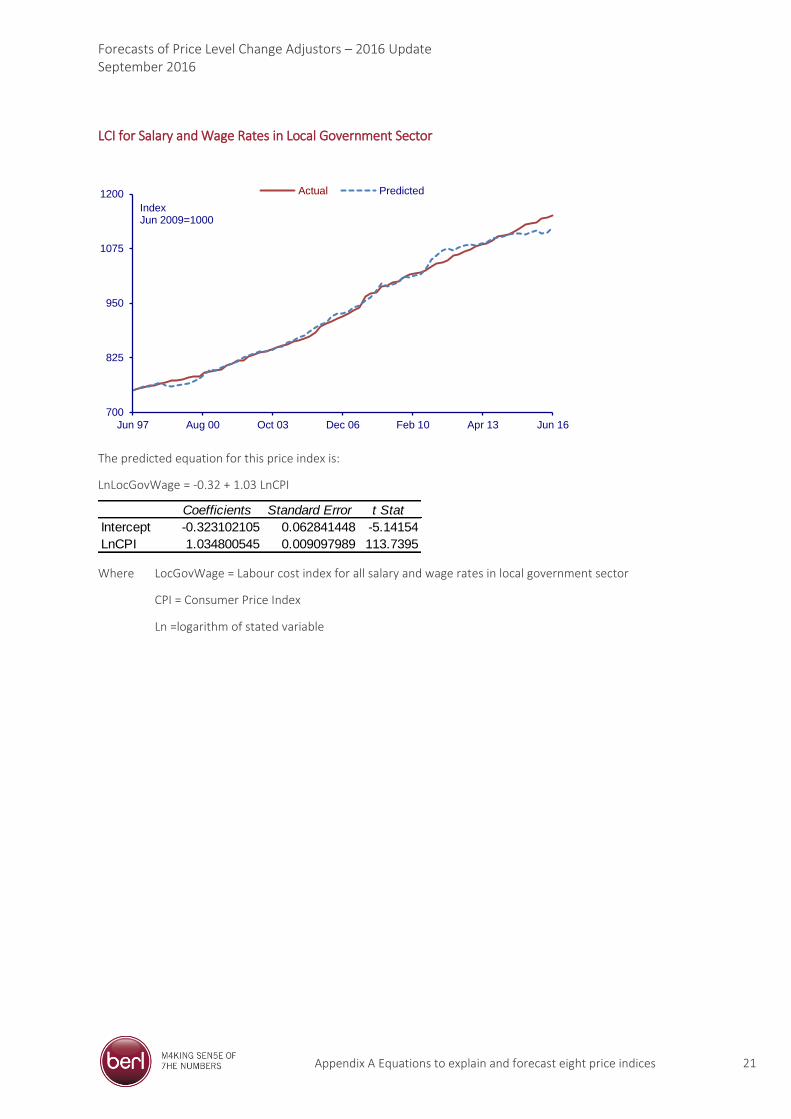

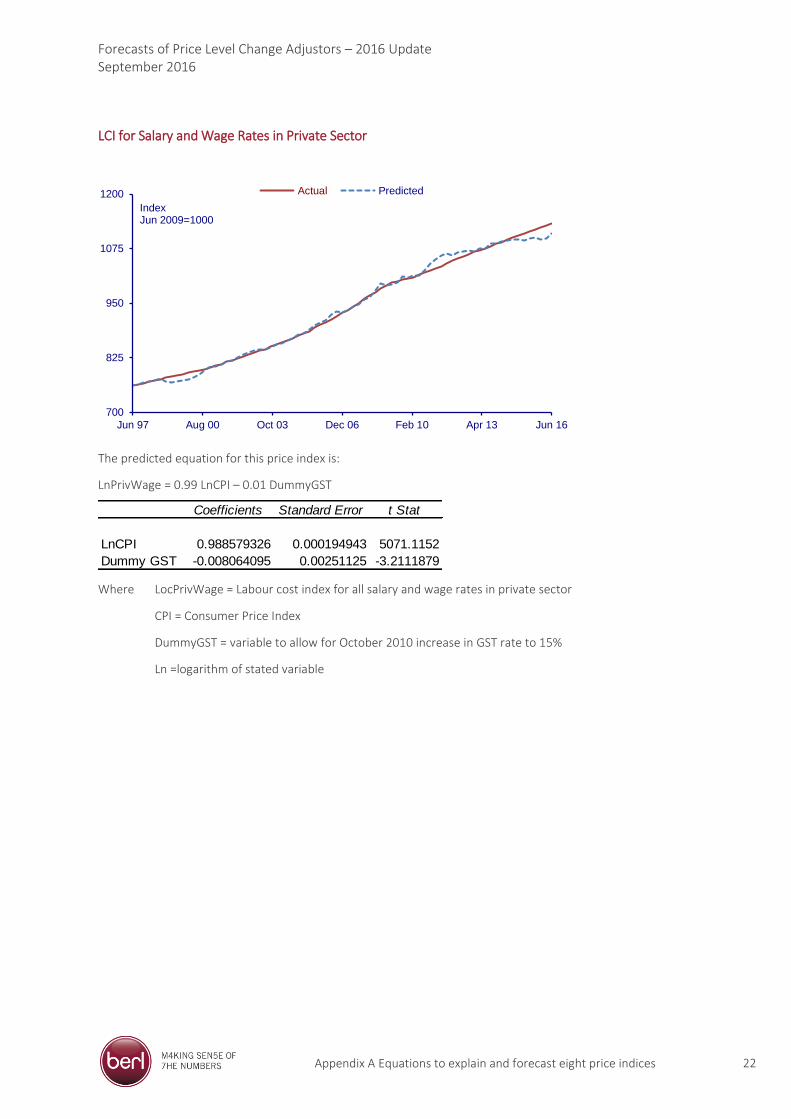

The charts in this appendix illustrate the performance of our estimated equations, for each of the adjustors,

when compared to the actual data over the period June 1997 to June 2016.

The estimation process is used to develop and then confirm a robust equation that can be used to generate

forecasts. The confirmation process tests the fit of the estimated equation with the actual path of the adjustor

over a period of time.

In each of the figures below, the dashed line (labelled predicted) indicates the estimated path of the adjustor

as calculated by our estimated equation. The solid line (labelled actual) indicates the actual path of the

adjustor as derived from the relevant official Statistics New Zealand data series.

The equations for each of the price indices are given below each chart

PPI for Local Government Administration Sector

The predicted equation for this price index is:

LnLocGovAdm = -2.65 + 1.36 LnCPI – 0.03 DummyGST

Where LocGovAdm = Producer price index for inputs to Local Government Administration sector

CPI = Consumer Price Index

DummyGST = variable to allow for October 2010 increase in GST rate to 15%

Ln =logarithm of stated variable

600

725

850

975

1100

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Dec 2010=1000

Actual Predicted

Coefficients Standard Error t Stat

Intercept -2.654942959 0.088785918 -29.90275

LnCPI 1.364371321 0.012982422 105.0937

Dummy GST -0.029979035 0.003882299 -7.72198

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 16

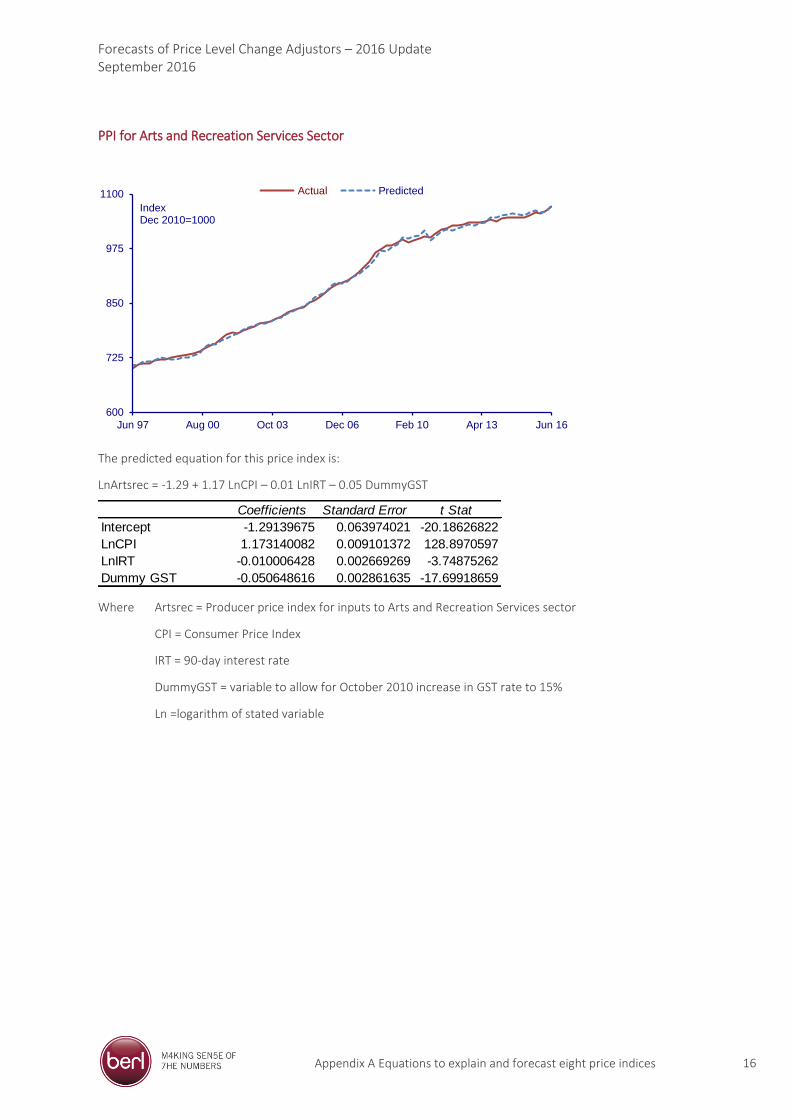

PPI for Arts and Recreation Services Sector

The predicted equation for this price index is:

LnArtsrec = -1.29 + 1.17 LnCPI – 0.01 LnIRT – 0.05 DummyGST

Where Artsrec = Producer price index for inputs to Arts and Recreation Services sector

CPI = Consumer Price Index

IRT = 90-day interest rate

DummyGST = variable to allow for October 2010 increase in GST rate to 15%

Ln =logarithm of stated variable

600

725

850

975

1100

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Dec 2010=1000

Actual Predicted

Coefficients Standard Error t Stat

Intercept -1.29139675 0.063974021 -20.18626822

LnCPI 1.173140082 0.009101372 128.8970597

LnIRT -0.010006428 0.002669269 -3.74875262

Dummy GST -0.050648616 0.002861635 -17.69918659

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 17

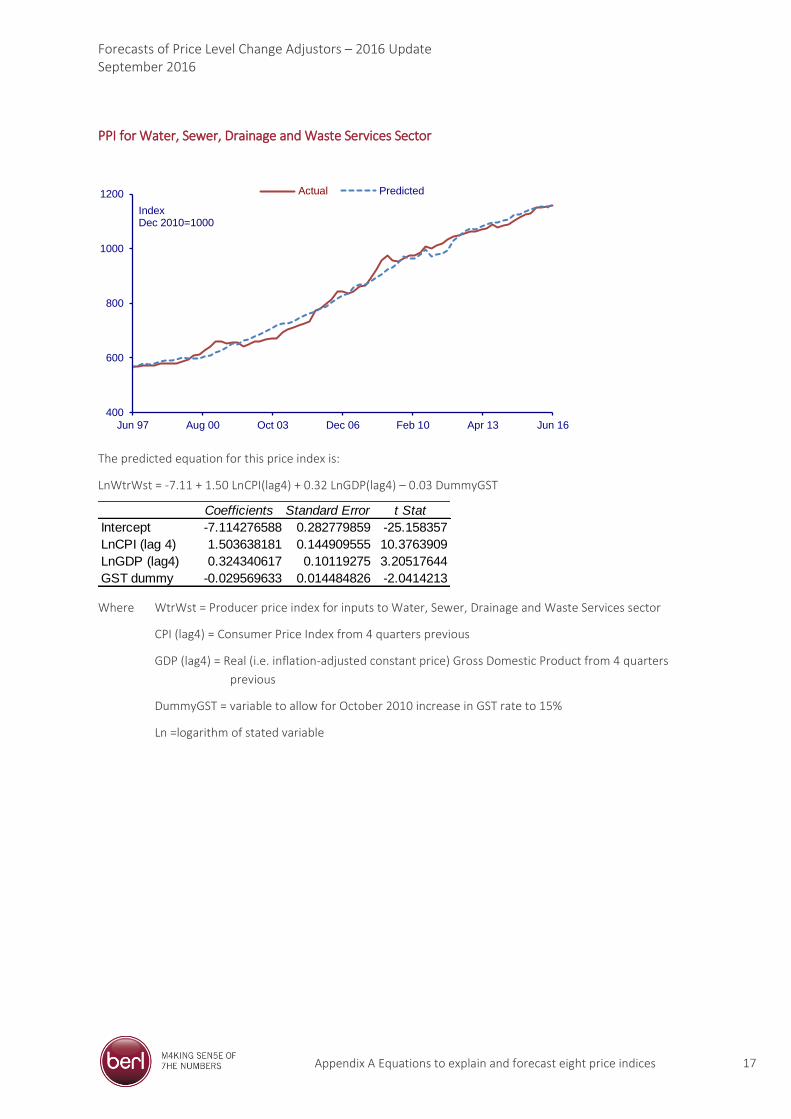

PPI for Water, Sewer, Drainage and Waste Services Sector

The predicted equation for this price index is:

LnWtrWst = -7.11 + 1.50 LnCPI(lag4) + 0.32 LnGDP(lag4) – 0.03 DummyGST

Where WtrWst = Producer price index for inputs to Water, Sewer, Drainage and Waste Services sector

CPI (lag4) = Consumer Price Index from 4 quarters previous

GDP (lag4) = Real (i.e. inflation-adjusted constant price) Gross Domestic Product from 4 quarters

previous

DummyGST = variable to allow for October 2010 increase in GST rate to 15%

Ln =logarithm of stated variable

400

600

800

1000

1200

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Dec 2010=1000

Actual Predicted

Coefficients Standard Error t Stat

Intercept -7.114276588 0.282779859 -25.158357

LnCPI (lag 4) 1.503638181 0.144909555 10.3763909

LnGDP (lag4) 0.324340617 0.10119275 3.20517644

GST dummy -0.029569633 0.014484826 -2.0414213

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 18

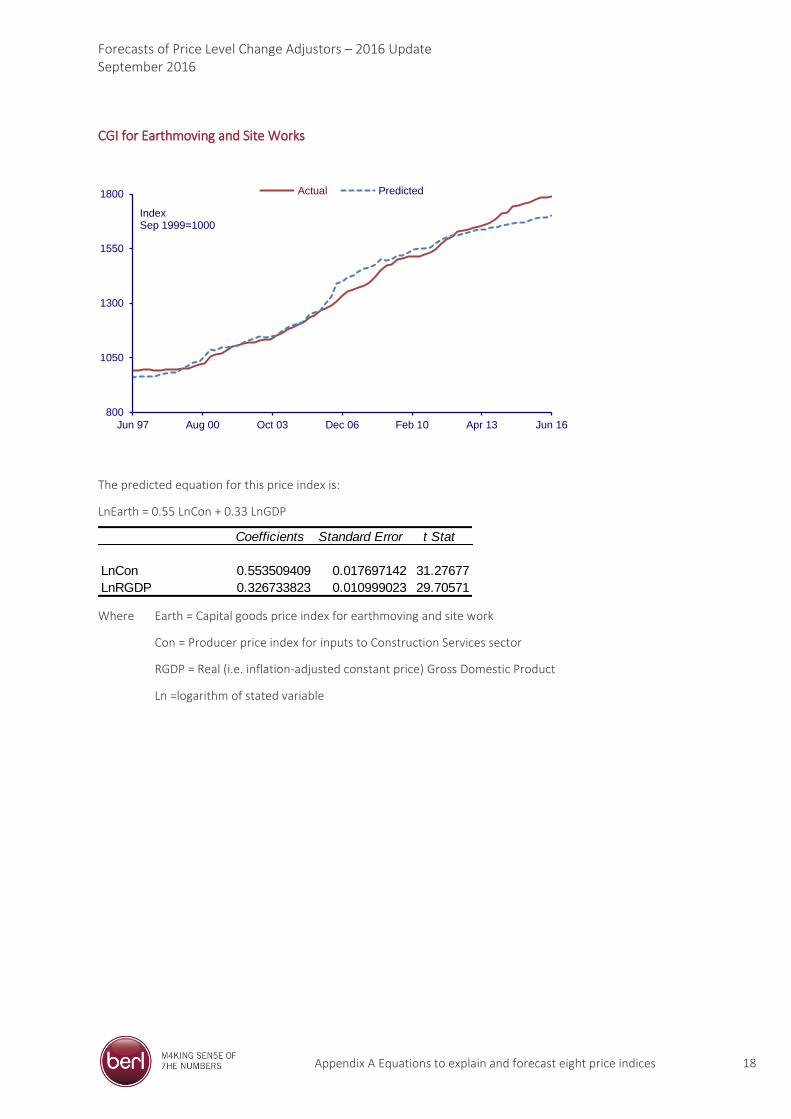

CGI for Earthmoving and Site Works

The predicted equation for this price index is:

LnEarth = 0.55 LnCon + 0.33 LnGDP

Where Earth = Capital goods price index for earthmoving and site work

Con = Producer price index for inputs to Construction Services sector

RGDP = Real (i.e. inflation-adjusted constant price) Gross Domestic Product

Ln =logarithm of stated variable

800

1050

1300

1550

1800

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

IndexSep 1999=1000

Actual Predicted

Coefficients Standard Error t Stat

LnCon 0.553509409 0.017697142 31.27677

LnRGDP 0.326733823 0.010999023 29.70571

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 19

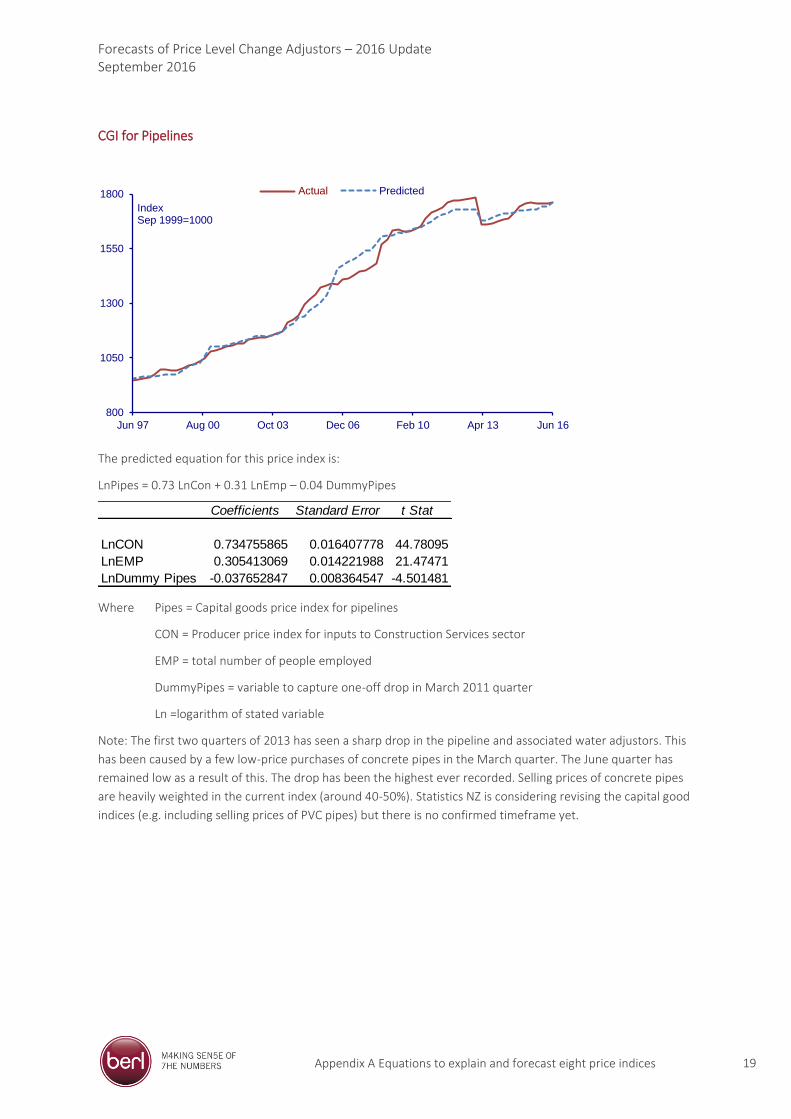

CGI for Pipelines

The predicted equation for this price index is:

LnPipes = 0.73 LnCon + 0.31 LnEmp – 0.04 DummyPipes

Where Pipes = Capital goods price index for pipelines

CON = Producer price index for inputs to Construction Services sector

EMP = total number of people employed

DummyPipes = variable to capture one-off drop in March 2011 quarter

Ln =logarithm of stated variable

Note: The first two quarters of 2013 has seen a sharp drop in the pipeline and associated water adjustors. This

has been caused by a few low-price purchases of concrete pipes in the March quarter. The June quarter has

remained low as a result of this. The drop has been the highest ever recorded. Selling prices of concrete pipes

are heavily weighted in the current index (around 40-50%). Statistics NZ is considering revising the capital good

indices (e.g. including selling prices of PVC pipes) but there is no confirmed timeframe yet.

800

1050

1300

1550

1800

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Sep 1999=1000

Actual Predicted

Coefficients Standard Error t Stat

LnCON 0.734755865 0.016407778 44.78095

LnEMP 0.305413069 0.014221988 21.47471

LnDummy Pipes -0.037652847 0.008364547 -4.501481

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 20

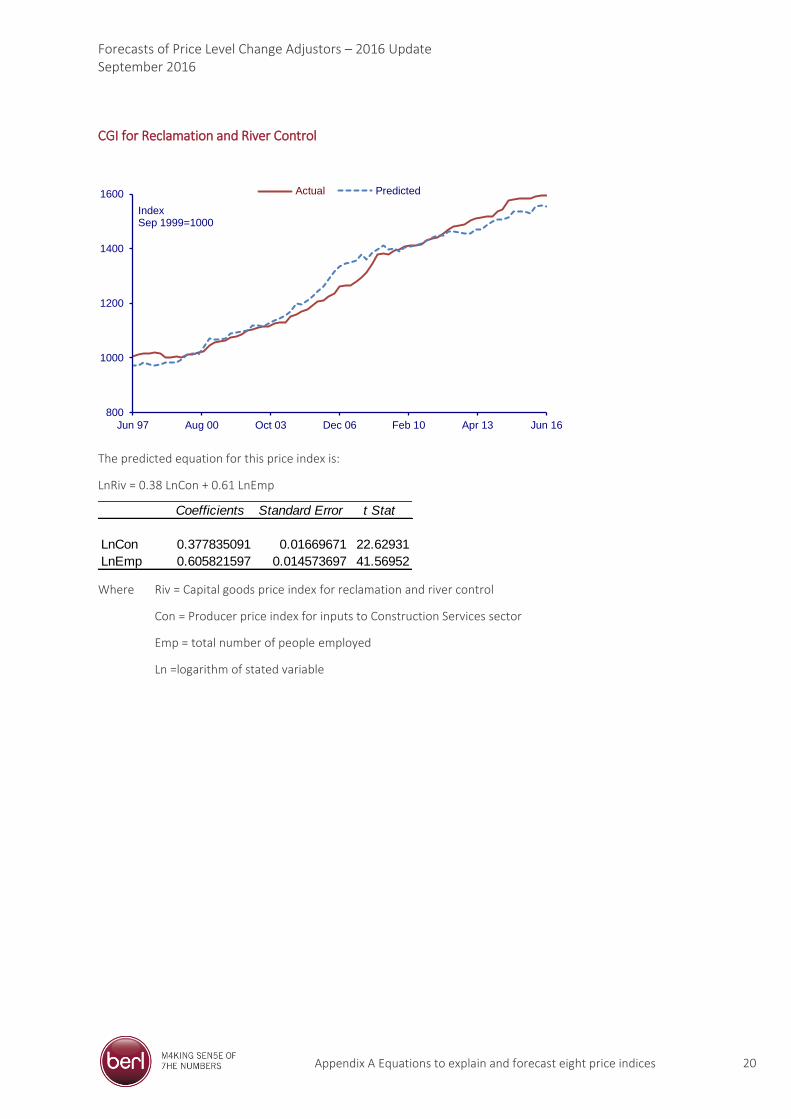

CGI for Reclamation and River Control

The predicted equation for this price index is:

LnRiv = 0.38 LnCon + 0.61 LnEmp

Where Riv = Capital goods price index for reclamation and river control

Con = Producer price index for inputs to Construction Services sector

Emp = total number of people employed

Ln =logarithm of stated variable

800

1000

1200

1400

1600

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Sep 1999=1000

Actual Predicted

Coefficients Standard Error t Stat

LnCon 0.377835091 0.01669671 22.62931

LnEmp 0.605821597 0.014573697 41.56952

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 21

LCI for Salary and Wage Rates in Local Government Sector

The predicted equation for this price index is:

LnLocGovWage = -0.32 + 1.03 LnCPI

Where LocGovWage = Labour cost index for all salary and wage rates in local government sector

CPI = Consumer Price Index

Ln =logarithm of stated variable

700

825

950

1075

1200

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Jun 2009=1000

Actual Predicted

Coefficients Standard Error t Stat

Intercept -0.323102105 0.062841448 -5.14154

LnCPI 1.034800545 0.009097989 113.7395

Forecasts of Price Level Change Adjustors – 2016 Update September 2016

Appendix A Equations to explain and forecast eight price indices 22

LCI for Salary and Wage Rates in Private Sector

The predicted equation for this price index is:

LnPrivWage = 0.99 LnCPI – 0.01 DummyGST

Where LocPrivWage = Labour cost index for all salary and wage rates in private sector

CPI = Consumer Price Index

DummyGST = variable to allow for October 2010 increase in GST rate to 15%

Ln =logarithm of stated variable

700

825

950

1075

1200

Jun 97 Aug 00 Oct 03 Dec 06 Feb 10 Apr 13 Jun 16

Index Jun 2009=1000

Actual Predicted

Coefficients Standard Error t Stat

LnCPI 0.988579326 0.000194943 5071.1152

Dummy GST -0.008064095 0.00251125 -3.2111879