Embed Size (px)

Citation preview

Form 1099 Update

Marianne Couch, J.D. COKALA Tax Information Reporting Specialists, LLC

www.cokala.com October, 2016

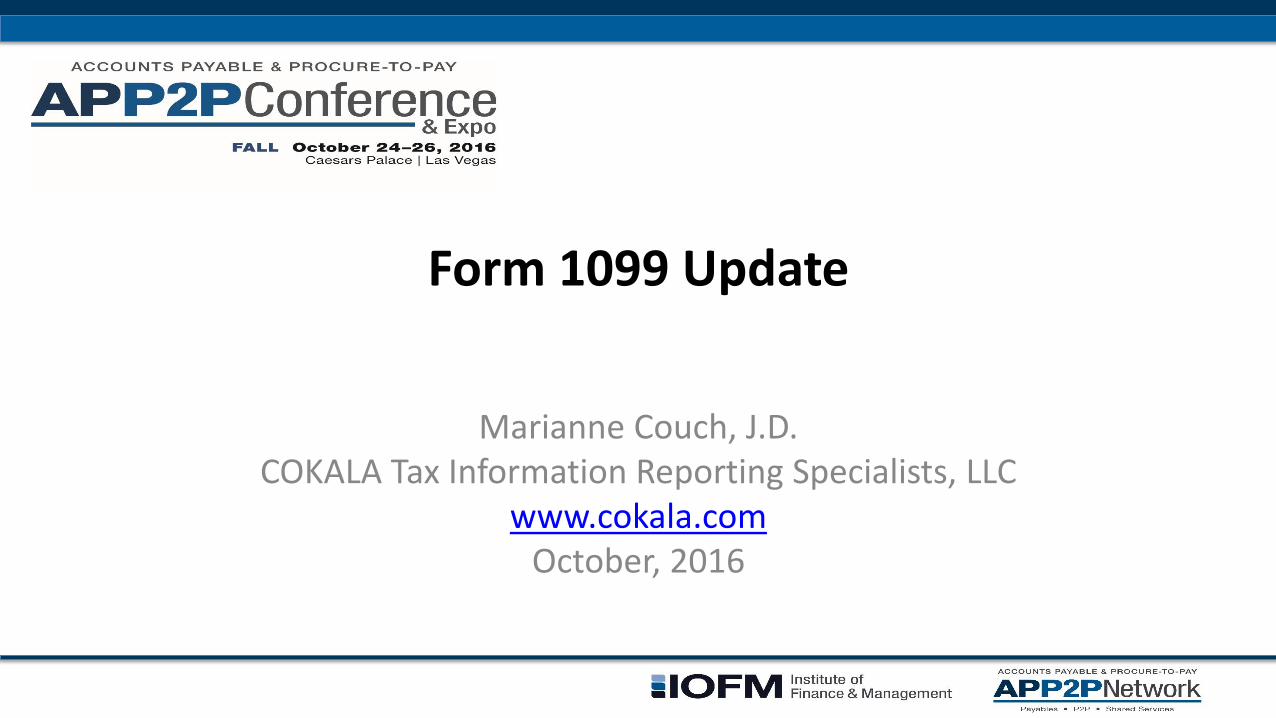

No New Form W-9 Yet

• We are watching for it.

• IRS has modified the Form W-8BEN-E; you should be using the new form within 6 months of its being finalized (so by October 18, 2016).

– New Limitation on Benefits section for treaty claims

• You will need to include an LOB code on Forms 1042-S that report amounts exempted from withholding per an income tax treaty

– New FATCA-entity type

– More space to include a GIIN

– Parts XXIX and XXX have switched places so that now, the names of U.S. owners of passive NFFEs have been moved above signature line

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 2

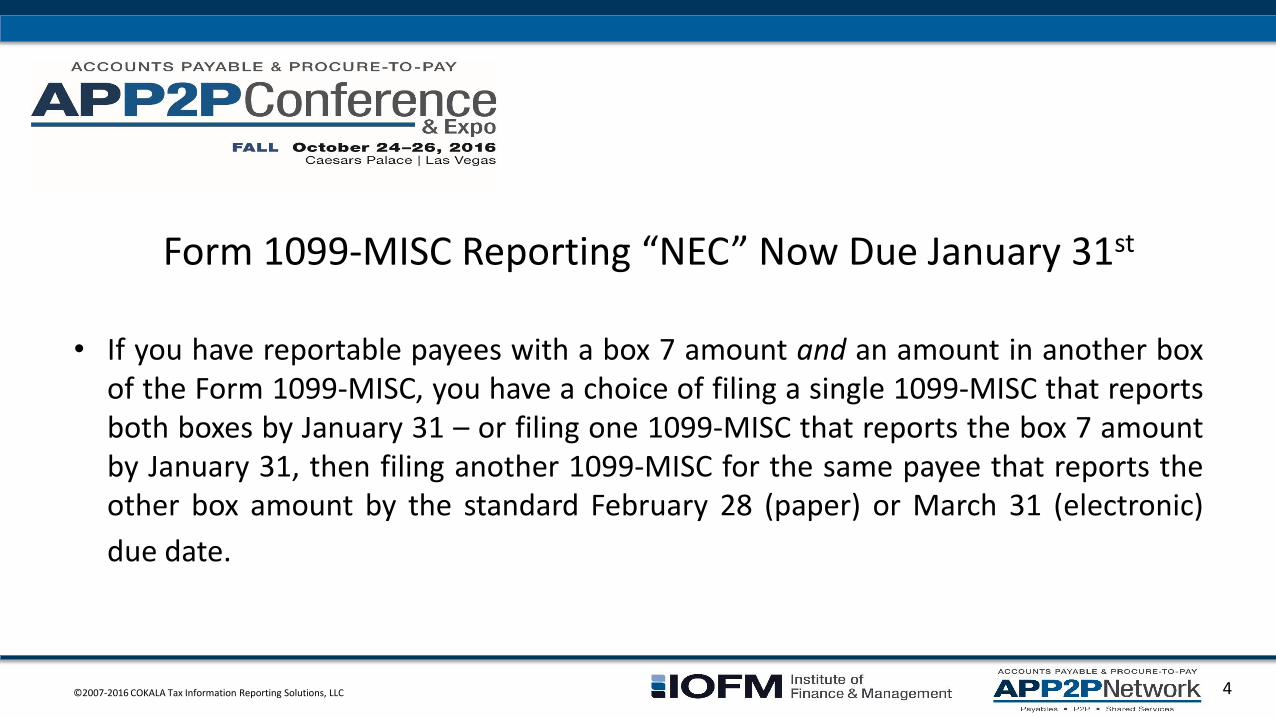

Form 1099-MISC Reporting “NEC” Now Due January 31st

• “NEC” = non-employee compensation (amounts reported in box 7).

• These forms will be due January 31 to both the payee and the IRS beginning in 2017 (reporting TY 2016 payments).

• The January 31 IRS due date applies equally to paper forms and electronically filed forms. – For 1099-MISC box 7 reporting, electronic filing does not give you any later filing date. – Forms W-2 and W-3 are also subject to the new January 31 filing due date.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 3

Form 1099-MISC Reporting “NEC” Now Due January 31st

• If you have reportable payees with a box 7 amount and an amount in another box of the Form 1099-MISC, you have a choice of filing a single 1099-MISC that reports both boxes by January 31 – or filing one 1099-MISC that reports the box 7 amount by January 31, then filing another 1099-MISC for the same payee that reports the other box amount by the standard February 28 (paper) or March 31 (electronic)

due date.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 4

Form 1096 – Transmittal for TY 2016 shows change to cover NEC

1099-MISC • Filers of paper forms should note that the IRS has made changes to Form 1096 for

use with information returns that report 2016 payments (Form 1096 is the

transmittal form that must accompany paper Forms 1099 filed with the IRS.)

• Box 7 of Form 1096 has been changed to provide a checkbox that must be checked if

the form accompanies “Forms 1099-MISC with NEC in box 7.”

• The IRS has eliminated indications of “final return.”

– That was the previous use of box 7 on Form 1096 but it has been removed from the form.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 5

Probable Elimination of Automatic 30-day Extension

• Proposed regulations, REG-132075-14, would eliminate automatic 30-day extensions of the IRS filing due date, but the first filings for which this could apply would be 2017 forms due in 2018.

• The term "automatic" means that the filer does not have to provide a reason as to why it needs an extension, but it must still file Form 8809 to request the extension.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 6

Probable Elimination of Automatic 30-day Extension

• When the automatic 30-day extension is eliminated, the IRS will still accept and consider requests for 30-day extensions but a sufficiently worthy reason must be provided to the IRS and the form will require the signature of an individual authorized to sign for the reporting business. • This is the standard that currently applies if a second 30-day extension is

requested by a payer that already claimed a first 30-day automatic extension.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 7

Extension and Form 1099-MISC Reporting NEC

• The automatic 30-day extension is still available for Forms 1099 filed in 2017 for payments made in 2016, but note the change in due date if requesting an extension for Forms 1099-MISC reporting non-employee compensation ("NEC").

• The IRS filing due date for Forms 1099-MISC reporting "NEC" is January 31 beginning with forms that report payments made in 2016 (due January 31, 2017).

• If you decide to claim the automatic 30-day extension for your 2016 1099-MISC NEC forms, and your other 1099s, and your 1042-S forms, you will be able to claim them all on one Form 8809 but you must send the 8809 no later than January 31 (the earliest due date out of all the due dates you want to extend).

• Or you can send more than one Form 8809, each one sent no later than the earliest due date of the form(s) you specify on the 8809.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 8

Changes on the Form 8809 • Form has been converted to a fill-in form that lets you type information into the form after you download

the PDF from the IRS website.

– IRS won’t start accepting your Forms 8809 for filing extensions until after January 1, 2017. The form is on the IRS website at https://www.irs.gov/pub/irs-pdf/f8809.pdf?_ga=1.249828102.1819310419.1358430541.

• The first 30-day extension of the IRS filing due date, usually referred to as an “automatic” extension because it is simply claimed by the filer on Form 8809 without having to furnish a written explanation of need, is available for 2016 Forms 1094-C, 1095-C, 1095-B, 1097, 1098 series, 1099 series, 1099-MISC NEC, 3921, 3922, W-2G, 5498, 5498-ESA, 5498-QA, 5498-SA, 1042-S, and 8027.

• Form 8809 is also used to request a second 30-day extension for the information returns listed above, but a second extension is not automatic.

– A second extension may be granted at the discretion of the IRS; it requires a showing of extraordinary circumstances or catastrophe explained in writing attached to a Form 8809 signed under penalties of perjury.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 9

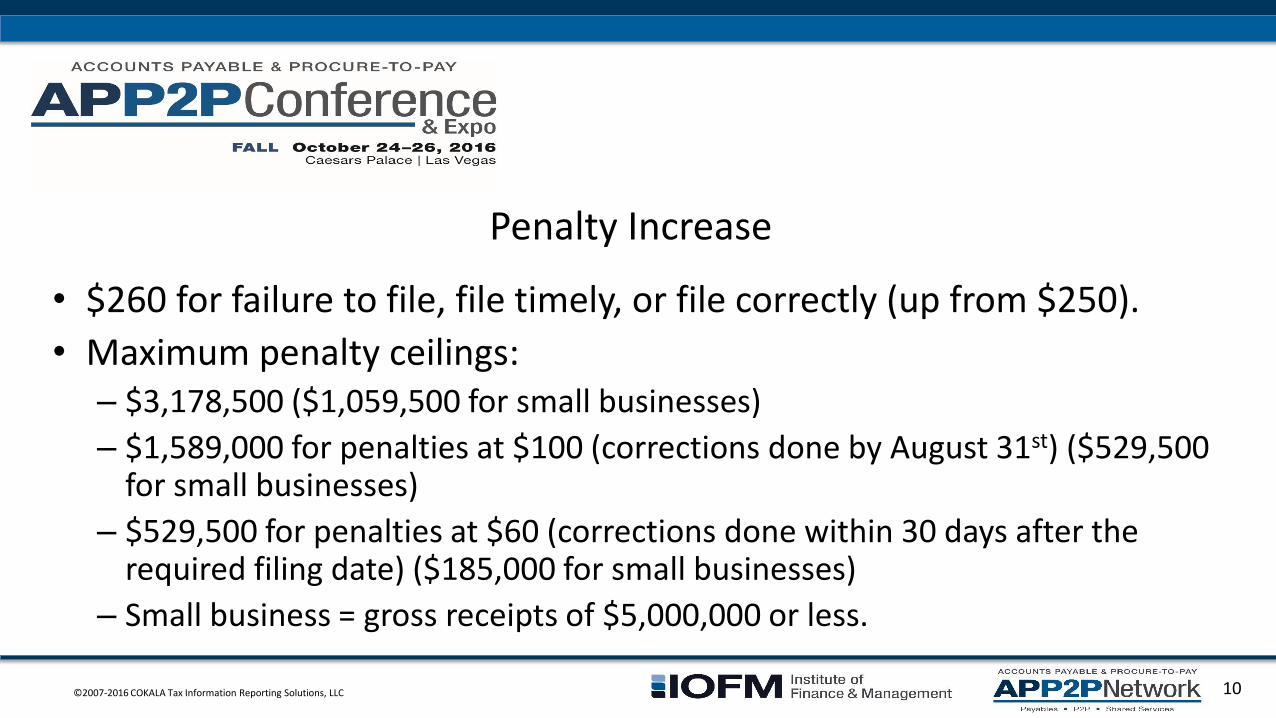

Penalty Increase

• $260 for failure to file, file timely, or file correctly (up from $250).

• Maximum penalty ceilings: – $3,178,500 ($1,059,500 for small businesses)

– $1,589,000 for penalties at $100 (corrections done by August 31st) ($529,500 for small businesses)

– $529,500 for penalties at $60 (corrections done within 30 days after the required filing date) ($185,000 for small businesses)

– Small business = gross receipts of $5,000,000 or less.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 10

Corrections

• For 1099s filed after 12/31/16, no correction will be required if:

– the dollar amount for a single type of payment reported on the Form 1099 was in error but within $100 of the correct amount; or

– the dollar amount reported as withheld tax was in error but within $25 of the correct amount.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 11

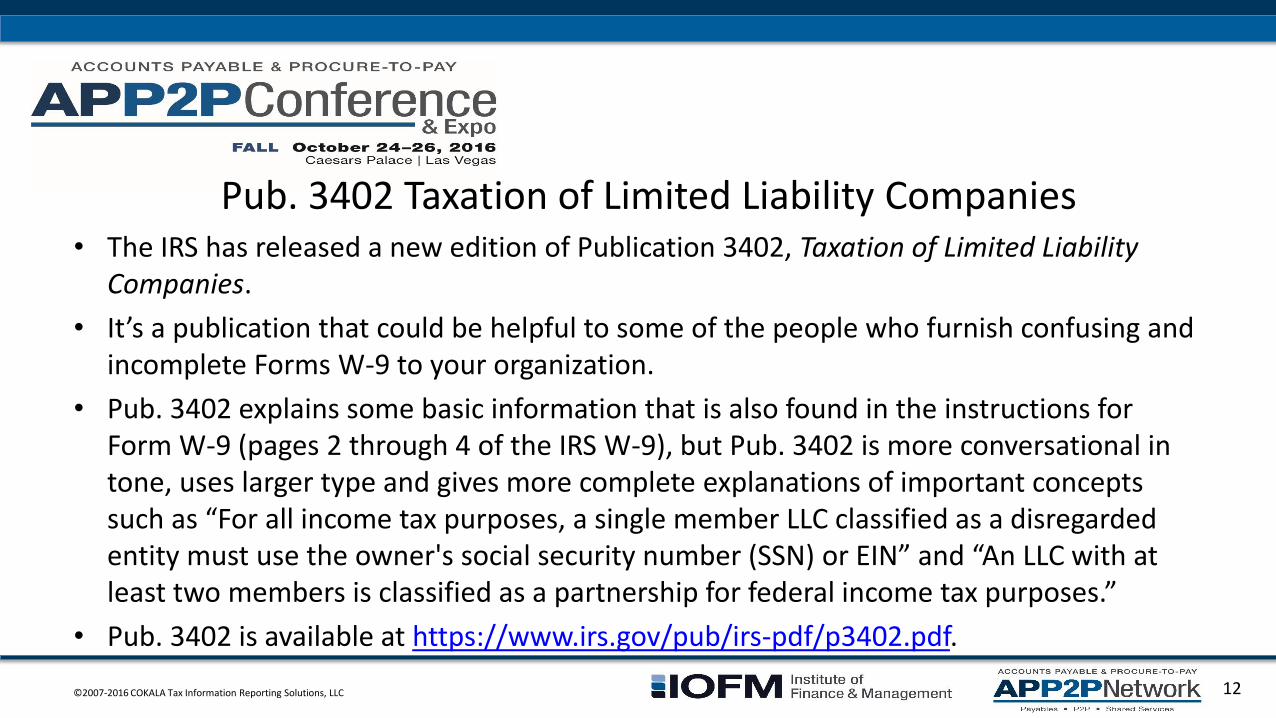

Pub. 3402 Taxation of Limited Liability Companies • The IRS has released a new edition of Publication 3402, Taxation of Limited Liability

Companies.

• It’s a publication that could be helpful to some of the people who furnish confusing and incomplete Forms W-9 to your organization.

• Pub. 3402 explains some basic information that is also found in the instructions for Form W-9 (pages 2 through 4 of the IRS W-9), but Pub. 3402 is more conversational in tone, uses larger type and gives more complete explanations of important concepts such as “For all income tax purposes, a single member LLC classified as a disregarded entity must use the owner's social security number (SSN) or EIN” and “An LLC with at least two members is classified as a partnership for federal income tax purposes.”

• Pub. 3402 is available at https://www.irs.gov/pub/irs-pdf/p3402.pdf.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 12

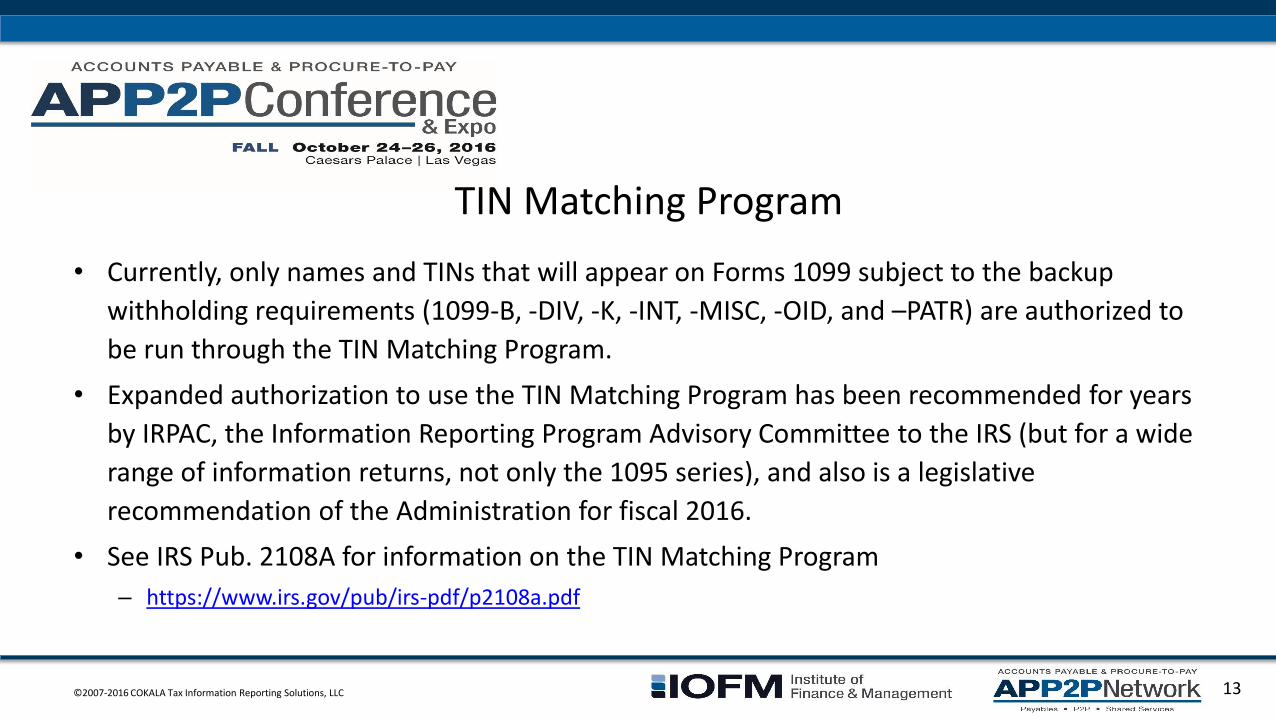

TIN Matching Program

• Currently, only names and TINs that will appear on Forms 1099 subject to the backup

withholding requirements (1099-B, -DIV, -K, -INT, -MISC, -OID, and –PATR) are authorized to

be run through the TIN Matching Program.

• Expanded authorization to use the TIN Matching Program has been recommended for years

by IRPAC, the Information Reporting Program Advisory Committee to the IRS (but for a wide

range of information returns, not only the 1095 series), and also is a legislative

recommendation of the Administration for fiscal 2016.

• See IRS Pub. 2108A for information on the TIN Matching Program

– https://www.irs.gov/pub/irs-pdf/p2108a.pdf

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 13

Disregarded Entities

• The IRS has issued a clarifying regulation applicable to partnerships that own disregarded entities, and has several times clarified that a disregarded business entity (DE) is a separate taxpayer in its own name only for employment and excise taxes, but this is not the case for purposes of filing information returns.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 14

Disregarded Entities

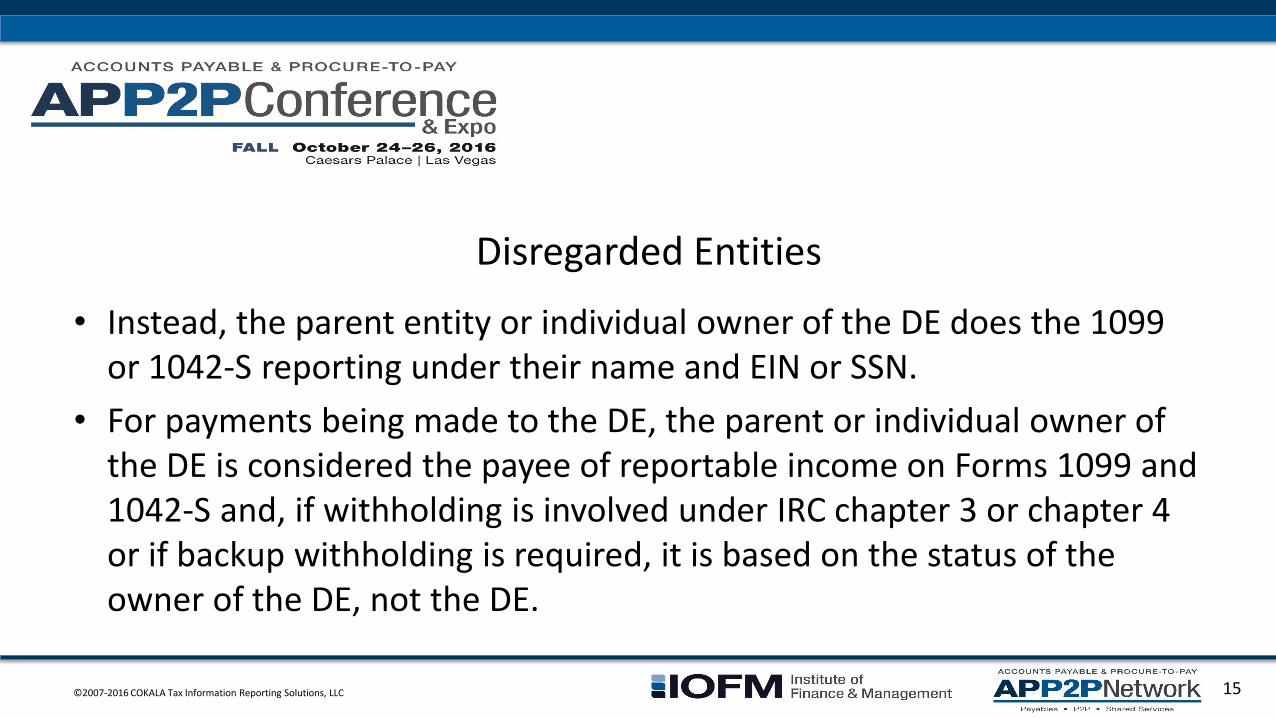

• Instead, the parent entity or individual owner of the DE does the 1099 or 1042-S reporting under their name and EIN or SSN.

• For payments being made to the DE, the parent or individual owner of the DE is considered the payee of reportable income on Forms 1099 and 1042-S and, if withholding is involved under IRC chapter 3 or chapter 4 or if backup withholding is required, it is based on the status of the owner of the DE, not the DE.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 15

Disregarded Entities and the Form W-9

• Line 1 (name) should be the name of the parent of the DE • Line 2 (business name/DE name, if different) should be the name of the DE • Line 3 (tax status) should indicate the tax status (C corp; S Corp; Partnership, etc.) of the

parent • Line 4 (codes): if exempt recipient code is included, it should be the code applicable to

the parent (line 4 is optional) • Part I (TIN) should include the TIN of the parent • Report reportable payments using the name and TIN of the parent, even if you made

the payments to or in the name of the DE.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 16

Sole Proprietors/Single-Member LLCs/DEs on the Form W-9

• Sole proprietorships and single-member LLCs should complete the Form W-9 the same way as do DEs; filers should report reportable payments to sole proprietors and single-member LLCs under the name and TIN of the owner, even if payments are made to or in the business name of the sole proprietorship or single-member LLC.

• For sole proprietorships, and single-member LLCs owned by an individual, you may use either the SSN or the EIN of the owner; IRS prefers the SSN, if you have it.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 17

Audit/Examination – Employment Tax Examinations Include Exam Of Information Return Filing Compliance

• If a company undergoes an employment tax examination by the IRS, the examiner is required to also determine whether the company filed information returns as required.

• The internal IRS directive calls the examiners’ attention specifically to look at Forms 1099-MISC, 1099-K, 1099-INT and W-2, plus “etc.”

• If the appropriate forms were not correctly filed, the examiner must consider expanding the audit to include a penalty case file and/or review Form 945 in connection with establishing whether backup withholding requirements have been met.

• See https://www.irs.gov/pub/foia/ig/spder/SBSE-04-0915-0058.pdf.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 18

TIN Truncation on Correspondence from IRS

• You may see the IRS truncate your organization’s TIN on correspondence it sends to you.

• If done, IRS probably presumes you could identify the entity to which the correspondence applies if only the final four digits of the TIN are visible.

• Example: truncated EIN would appear as **-***6789 or xx-xxx6789.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 19

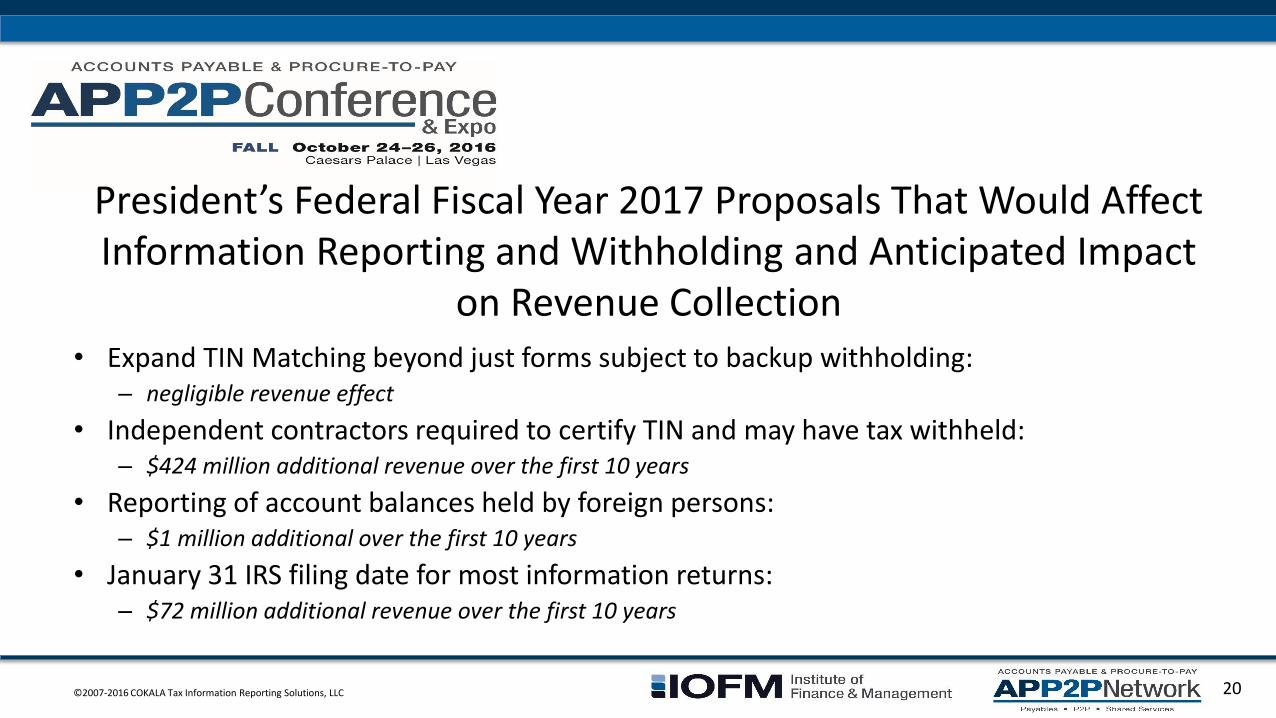

President’s Federal Fiscal Year 2017 Proposals That Would Affect Information Reporting and Withholding and Anticipated Impact

on Revenue Collection • Expand TIN Matching beyond just forms subject to backup withholding:

– negligible revenue effect

• Independent contractors required to certify TIN and may have tax withheld: – $424 million additional revenue over the first 10 years

• Reporting of account balances held by foreign persons: – $1 million additional over the first 10 years

• January 31 IRS filing date for most information returns: – $72 million additional revenue over the first 10 years

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 20

President’s Federal Fiscal Year 2017 Proposals That Would Affect Information Reporting and Withholding and Anticipated Impact

on Revenue Collection • Require the use of average cost basis method for stock that is a covered security:

– $1.2 billion additional revenue over the first 10 years

• Require non-spouse beneficiaries to take inherited IRA distributions over no more than five years: – $6.1 billion additional revenue over the first 10 years

• Limit Roth conversions to pre-tax dollars: – $231 million additional revenue over the first 10 years.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 21

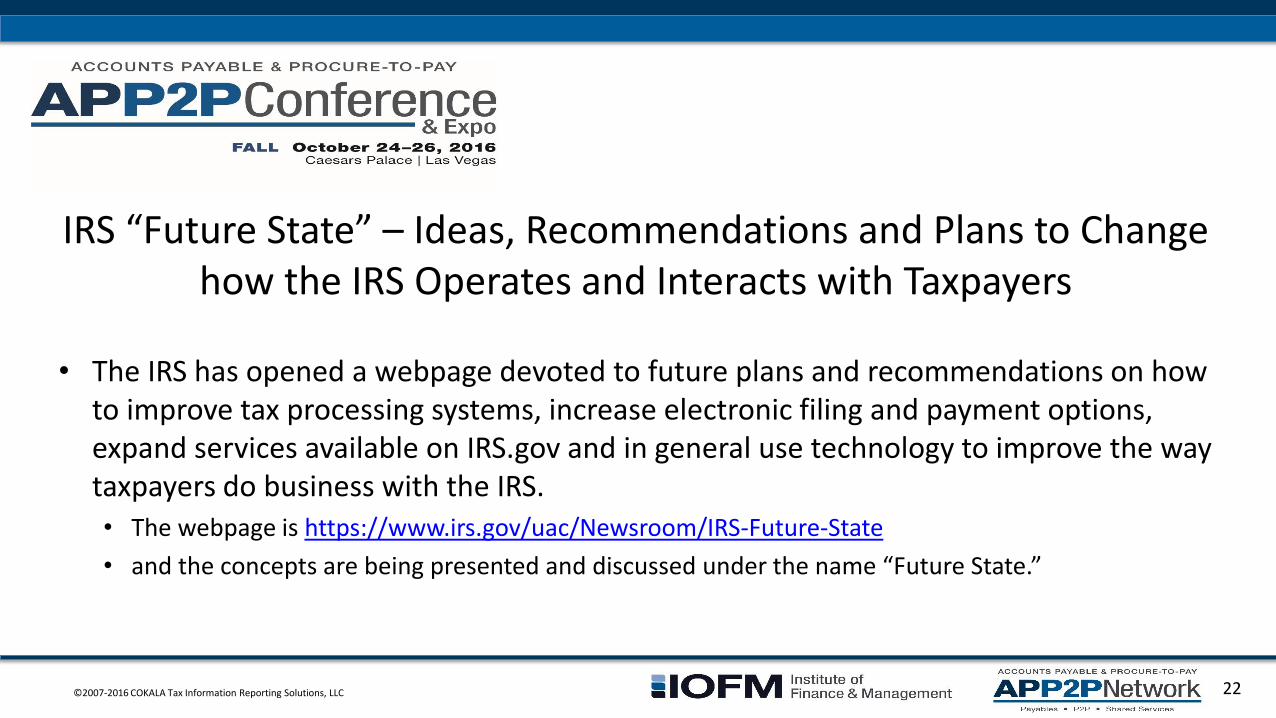

IRS “Future State” – Ideas, Recommendations and Plans to Change how the IRS Operates and Interacts with Taxpayers

• The IRS has opened a webpage devoted to future plans and recommendations on how to improve tax processing systems, increase electronic filing and payment options, expand services available on IRS.gov and in general use technology to improve the way taxpayers do business with the IRS. • The webpage is https://www.irs.gov/uac/Newsroom/IRS-Future-State

• and the concepts are being presented and discussed under the name “Future State.”

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 22

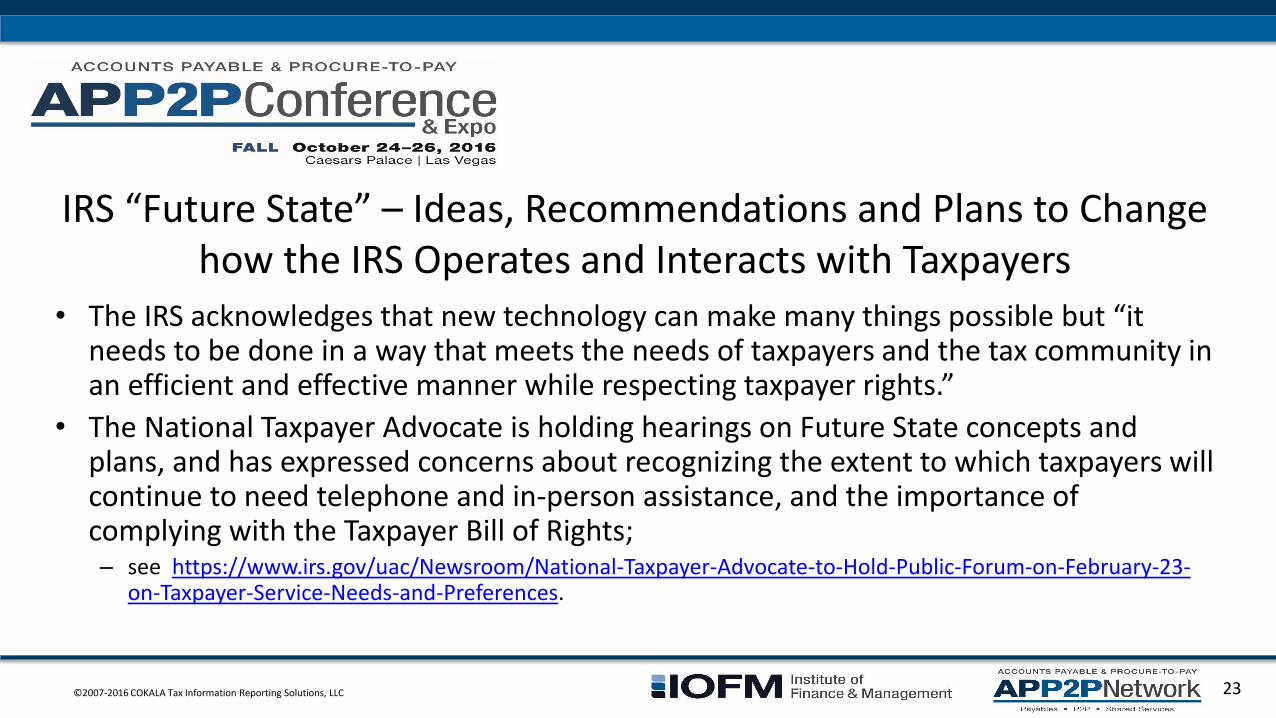

IRS “Future State” – Ideas, Recommendations and Plans to Change how the IRS Operates and Interacts with Taxpayers

• The IRS acknowledges that new technology can make many things possible but “it needs to be done in a way that meets the needs of taxpayers and the tax community in an efficient and effective manner while respecting taxpayer rights.”

• The National Taxpayer Advocate is holding hearings on Future State concepts and plans, and has expressed concerns about recognizing the extent to which taxpayers will continue to need telephone and in-person assistance, and the importance of complying with the Taxpayer Bill of Rights; – see https://www.irs.gov/uac/Newsroom/National-Taxpayer-Advocate-to-Hold-Public-Forum-on-February-23-

on-Taxpayer-Service-Needs-and-Preferences.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 23

National Taxpayer Advocate Report • National Taxpayer Advocate Nina Olson publicly released her Annual Report to

Congress. – It’s available at http://www.taxpayeradvocate.irs.gov/reports/2015-annual-report-to-congress.

– The report discusses the 24 most serious problems encountered by taxpayers, many of which have to do with IRS customer service.

– 2016 Report will be delivered to Congress at the end of December.

• The Advocate recommends that Congress amend IRC sections 6055 and 6056 to allow entities required to file information returns under these sections (Forms 1095-B and 1095-C) to verify TINs with the IRS prior to filing the returns(i.e., expand the TIN Matching Program to cover more than just the Forms 1099 subject to backup withholding).

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 24

Legislation • The Stolen Identity Refund Fraud Prevention Act (S. 3157) was introduced in Congress in August with

bipartisan approval of the Senate Finance Committee.

– It contains some provisions of a bill sponsored last year by Senators Hatch and Wyden (Chairman and Ranking Member, respectively, of the Senate Finance Committee).

• Direct impact on information reporting would result from the following provisions of S. 3157:

– Electronic filing threshold reduced to 20 returns.

• The threshold for mandatory e-filing of information returns would go from 250 to 20 over a five-year phase-in period.

– On-line Form 1099 filing and statement production.

• The IRS would be required to provide an on-line service to prepare and file Forms 1099, prepare Forms 1099 for distribution to recipients, and create and maintain necessary taxpayer records.

• If passed, this would begin with Form 1099-MISC for 2018 (due to the IRS and recipients in 2019), and be available for other Forms 1099 for 2020 (due to the IRS and recipients in 2021).

– Scannable code required on paper returns that were prepared with an electronic program.

• Any return of tax which is prepared electronically, but is printed and filed on paper, would have to display a code which can, when scanned, convert the return to electronic format.

• This would begin with information returns for 2017 due to the IRS in 2018.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 25

S. 3157 Cont.

• The bill also contains two provisions that would affect IRS use of budgeted funds.

– Streamlined critical pay authority would be restored to fund important IRS information technology jobs through September 30, 2021.

– The loss of critical pay authority, and the resulting loss of highly valued technology experts, were recently publicized by the Commissioner.

– In addition, the Commissioner would be given authority to transfer up to $10 million from any IRS account appropriation, to any other IRS account if the transferred amounts are used solely for preventing, detecting, and resolving potential cases of tax fraud.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 26

Legislation

• Identity theft for purposes of filing federal tax returns or any other documents filed to the IRS or Treasury would be a felony under a Code amendment included in S. 3157, punishable by up to five years’ imprisonment and/or a fine of up to one-quarter million dollars.

• Another provision requires the IRS to establish a new system for notifying taxpayers of suspected identity theft.

• Other amendments would provide that the unauthorized use of the identity of an individual includes the unauthorized use of the identity of the individual to obtain employment, and require additional coordination between the Social Security Administration and IRS.

• The text of S. 3157, covering these and other items, is available at https://www.congress.gov/bill/114th-congress/senate-bill/3157/text.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 27

Legislation, Cont.

• The Taxpayer Protection Act of 2016, S. 3156, was also introduced in August after bipartisan approval by the Senate Finance Committee.

– This bill includes numerous provisions governing IRS administration and operations, plus a provision for mandatory electronic filing by tax-exempt organizations and for the IRS to publicly release tax-exempt organization returns “as soon as practicable in a machine readable format that does not permit alteration or manipulation of such return.”

• See S. 3156 at https://www.congress.gov/bill/114th-congress/senate-bill/3156/text.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 28

SENATE DEMOCRATS SPONSOR A BILL TO ADDRESS EMPLOYEE VERSUS INDEPENDENT CONTRACTOR ISSUES

• S 2252 would permit the IRS to issue “prospective guidance” clarifying whether individual workers are employees or contractors for purposes of employment taxes, and would prohibit retroactive assessments with respect to employees who are reclassified as employees through this process.

• Section 530 of the Revenue Act of 1978 would be repealed.

– Currently under section 530, a service recipient may treat a worker as an independent contractor for federal employment tax purposes, even though the worker actually may be an employee under common law rules, if the service recipient has a reasonable basis for treating the worker as an independent contractor and certain other requirements are met—

• if the worker (or any in a substantially similar position) has not been treated as an employee for any period beginning after 1977 and

• the service recipient filed all federal tax returns (including 1099s) on a basis consistent with treating the worker as an independent contractor.

– If a service recipient meets the requirements of section 530 under current rules the IRS is prohibited from reclassifying the workers as employees, even prospectively and even as to newly hired workers in the same class.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 29

How Can You Tell if Someone Is An Employee or An Independent Contractor?

• Behavioral Control

• Financial Control

• Type of Relationship

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 30

Behavioral Control

• Instructions the business gives to the worker – When and where to do the work – What tools or equipment to use – What workers to hire or to assist with the work – Where to purchase supplies and services – What work must be performed by a specified individual – What order and sequence to follow

• Training the business gives to the worker

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 31

Financial Control

• The extent to which the worker has unreimbursed business expenses. • The extent of the worker’s investment. • The extent to which the worker makes his or her services available to the

relevant market. • How the business pays the worker.

– Salary, hourly or flat fee?

• The extent to which the worker can realize a profit or a loss. – An independent contractor can make a profit or take a loss.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 32

Type of Relationship

• Written contracts describing the relationship the parties intended to create. – A contract is insufficient, by itself, to confer independent contractor status.

• Whether the business provides the worker with employee-type benefits, such as insurance, a pension plan, vacation or sick pay.

• The permanency of the relationship. – Indefinite or for fixed period of time?

• The extent to which the services performed by the worker are a key aspect of the regular business of the company.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 33

Resources for Determining Worker Status

• IRS Pub. 15-A – https://www.irs.gov/pub/irs-pdf/p15a.pdf

• Form SS-8 – https://www.irs.gov/pub/irs-pdf/fss8.pdf

• IRS Page – https://www.irs.gov/businesses/small-businesses-self-employed/independent-

contractor-self-employed-or-employee

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 34

NEW IRS AUDIT TECHNIQUE GUIDE COVERS ENTERTAINMENT INDUSTRY

• IRS Audit Technique Guides (ATGs) are written to instruct examiners about issues and terminology pertinent to a particular industry and what to look for when conducting income tax audits.

• A new ATG was issued for the entertainment industry and is well worth reviewing if your organization makes payments to artists, entertainers, technicians, producers and managers or other payees in the businesses of music, film, video and live performance.

• It provides useful background for how the IRS views payments that are income or affect net income including royalties, advances, expense reimbursement or allowances, fringe benefits, travel.

• See https://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Entertainment-Audit-Technique-Guide.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 35

Entertainers and Agents

• Remember that the entertainer is the beneficial owner of the income for tax reporting purposes even if you make payments to the entertainer’s agent.

• Report reportable payments in the name and TIN of the entertainer; not the name of the agent.

• The agent is a “middleman” without the reporting obligation to the entertainer.

• You remain the payer for tax purposes even if the contract says the agent will attend to the reporting and withholding requirements. – You, as the payer, will be on the hook for any reporting and withholding penalties if the

agent fails to report or withhold when required

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 36

Change in Internet Security Technical Standards for FIRE System

• The IRS FIRE Text System server no longer supports SSL 3.0 (Secure Socket Layer 3.0) as one of the FIRE System’s Internet Security Technical Standards, and the IRS intends to soon remove SSL 3.0 from the FIRE Production System (the active filing system for Forms 1099, 1098, and similar information returns and Forms 1042-S).

• The removal date for the FIRE Production System will be posted on the FIRE website, https://fire.irs.gov/.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 37

Change in Internet Security Technical Standards for FIRE System

• Transmitters using IE 6.0 or lower as their browser may have problems logging in and connecting to the FIRE System.

• The IRS says that in most situations the following steps will allow a transmitter to connect and upload a file: – In IE, Go to Tools>Internet Options>Advance

– Scroll down and find Security

– Uncheck both SSL 2.0 and SSL 3.0 Check TLS 1.0, TLS 1.1, TLS 1.2 and select “Apply”.

©2007-2016 COKALA Tax Information Reporting Solutions, LLC 38

Questions? Q uestions

?

Questions?

Questions?