Embed Size (px)

Citation preview

This offering memorandum is confidential. By acceptance hereof, prospective investors agree that they will not transmit, reproduce or

make available to anyone this offering memorandum or any information contained herein.

FORM 45-106 F2

Offering Memorandum for Non-Qualifying Issuers

Date: July 17, 2020

The Issuer:

Name: Brazil Potash Corp. (the “Company”, “Brazil Potash”, “we” and “our”)

Head office: 65 Queen Street West, Suite 800

Toronto, Ontario M5H 2M5

Phone: (416) 309-2963 / Fax: 647.438.2701

E-mail: [email protected]

Currently listed or quoted?

No. These securities do not trade on any exchange or market.

Reporting issuer: No.

SEDAR filer? No.

The Offering:

Securities Offered:

Up to 12,500,000 common shares in the capital of the Company (the “Shares”) (the “Offering”).

Price per security: US$4.00 per Share.

Minimum/Maximum offering: Maximum offering of US$50,000,000 (12,500,000) Shares (the “Maximum Offering”). There is

no minimum. You may be the only purchaser. Funds available under the Offering may not

be sufficient to accomplish our proposed objectives.

Minimum subscription amount: US$2,500 (625 Shares). Management of the Company may waive this minimum amount

requirement.

Payment terms: The full subscription price is payable at the time of Closing by wire transfer, electronic funds

transfer, credit card, bank draft or certified cheque or such other manner as may be acceptable to

the Company. There may be one or more additional closings under this Offering

Memorandum. Where required by law, the subscription funds will be held in trust pending

closing for two (2) business days (and in any event until midnight on the 2nd business day)

after the purchaser signs the subscription agreement for the purchase of Shares (the

“Subscription Agreement”). This does not constitute acceptance of a subscription.

Proposed closing date(s): On or about August 12, 2020 (the “Initial Closing Date”). Closings of the sales of Shares offered

hereunder will take place on such dates and at such times as are chosen by the Company (each

such closing, a “Closing”). If on the Initial Closing Date, the Company has sold less than the

Maximum Offering, then the Company may hold one or more additional Closings for additional

sales.

Selling agent? No.

Resale restrictions: You will be restricted from selling your securities for an indefinite hold period. See Item 10.

Purchaser’s rights: You have two (2) business days to cancel your agreement to purchase these securities. If there is a

misrepresentation in this offering memorandum (the “Offering Memorandum”), you have the right to sue either for damages or to

cancel the agreement. See Item 11.

No securities regulatory authority or regulator has assessed the merits of these securities or reviewed this Offering

Memorandum. Any representation to the contrary is an offence. This is a risky investment. See Item 8.

TABLE OF CONTENTS

Item 1. Use of Available Funds .................................................................................................................. 1 1.1. Funds ............................................................................................................................................. 1 1.2. Use of Available Funds ................................................................................................................. 1 1.3. Reallocation .................................................................................................................................. 2

Item 2. Business of the Company ............................................................................................................... 2 2.1. Structure ........................................................................................................................................ 2 2.2. Our Business ................................................................................................................................. 2 2.3. Development of Business.............................................................................................................. 2 2.4. Long Term Objectives .................................................................................................................. 3 2.5. Short Term Objectives and How We Intend to Achieve Them .................................................... 3 2.6. Insufficient Funds ......................................................................................................................... 4 2.7. Material Agreements ..................................................................................................................... 4

Item 3. Interests of Directors, Management, Promoters and Principal Holders................................... 5 3.1. Compensation and Securities Held ............................................................................................... 5 3.2. Management Experience ............................................................................................................... 6 3.3. Penalties, Sanctions and Bankruptcies .......................................................................................... 6 3.4. Loans ............................................................................................................................................. 6

Item 4. Capital Structure ........................................................................................................................... 7 4.1. Share Capital ................................................................................................................................. 7 4.2. Long Term Debt Securities ........................................................................................................... 7 4.3. Prior Sales ..................................................................................................................................... 8

Item 5. Securities Offered ........................................................................................................................... 8 5.1. Terms of Securities ....................................................................................................................... 8 5.2. Subscription Procedure ................................................................................................................. 8

Item 6. Income Tax Consequences and RRSP Eligibility ...................................................................... 10

Item 7. Compensation Paid to Sellers and Finders ................................................................................ 10

Item 8. Risk Factors .................................................................................................................................. 10

Item 9. Reporting Obligations.................................................................................................................. 11

Item 10. Resale Restrictions ..................................................................................................................... 12 10.1. General Statement ....................................................................................................................... 12 10.2. Restricted Period ......................................................................................................................... 12

Item 11. Purchasers’ Rights ..................................................................................................................... 12

Item 12. Financial Statements .................................................................................................................. 15

Item 13. Date and Certificate ................................................................................................................. C-1

Schedule “A” ........................................................................................................................................... A-1

BACKGROUND

Attached hereto as Schedule “A” and forming part of this Offering Memorandum is the offering circular

of the Company dated July 17, 2020 (the “Offering Circular”). The Offering Circular was prepared in

respect of the offer for sale of the Shares being made in the United States of America pursuant to

Regulation A (Regulation A+) under the Securities Act of 1933, as amended (this exemption is

hereinafter referred to as the “SEC Exemption”).

This Offering Memorandum has been prepared and is being provided to prospective purchasers of

Shares that are resident in each of the provinces of Canada, or the purchase of the Shares by a

purchaser that is otherwise subject to the securities legislation of the applicable province and such

purchaser does not qualify for the SEC Exemption.

NOTE TO READER: The body of the Offering Memorandum will include certain information regarding

the Company, the Shares and the Offering; however, the more detailed information regarding the

Company, the Shares and the Offering can be found in the Offering Circular attached hereto as Schedule

“A”. In each applicable section of the body of the Offering Memorandum a reader will find cross-

references to the page number(s) or heading(s) in the Offering Circular where further relevant information

is contained.

Except as otherwise provided herein, capitalized terms used in this Offering Memorandum without

definition have the meanings assigned to them in the Offering Circular.

1

SUMMARY

Investors should refer to the “Summary” section from pages 1 to 4 in the attached Offering Circular for a

summary regarding, among other matters, the Company, the Shares and the Offering.

ITEM 1.

USE OF AVAILABLE FUNDS

1.1. Funds

The Offering Proceeds and the funds which will be available to the Company as a result of the Offering

are estimated as follows:

Assuming

Minimum Offering

(in US$)

Assuming Maximum

Offering

(in US$)

(a) Amount to be raised by this Offering $0 $50,000,000

(b) Selling commissions and fees(1) $0 $1,555,000

(c) Estimated Offering costs (legal, accounting, audit,

etc.) $(170,000) $170,000

(d) Available funds $(170,000) $48,275,000

(e) Additional sources of funding required $0 $0

(f) Working capital deficiency(2) $6,795,655 $6,795,655

(g) Total $(6,965,655) $41,479,345

Notes:

(1) The Company has agreed to pay Dalmore Group, LLC (“Dalmore”), a one-time setup fee of US$5,000 and a one-time

consulting fee of US$50,000, as well as a 3% commission on the aggregate amount raised in the seven states where

Dalmore is engaged to provide broker-dealer services (Washington, Arizona, Texas, Alabama, North Dakota, Florida

and New Jersey).

(2) Working capital deficiency is as at June 30, 2020.

Investors should refer to the “Plan of Distribution and Selling Securityholders” and “Use of Proceeds to

Issuer” sections, at pages 17 to 18, in the attached Offering Circular for further information regarding

the use of the funds raised by the Company.

1.2. Use of Available Funds

The funds available as a result of the Offering are anticipated to be used by the Company as set forth in

the table below.

Description of intended use of Offering Proceeds

listed in order of priority

Assuming

Maximum Offering

(in US$)

Land Acquisition & Maintaining Mineral Rights $6,000,000

Environmental & Social License (LP) compliance $5,000,000

Obtain Installation License (LI)

Executive Compensation

Engineering for Other Applications & Permits

$8,000,000

$1,750,538

$4,000,000

Optimize Feasibility Study $3,000,000

2

Description of intended use of Offering Proceeds

listed in order of priority

Assuming

Maximum Offering

(in US$)

Essential Testwork Prior to Starting EPCM Phase $6,000,000

Conduct Basic Engineering $2,479,345

General and administrative $5,249,462

Total $41,479,345

Investors should refer to the “Use of Proceeds to Issuer” section, at pages 17 to 18, in the attached

Offering Circular for further information regarding the use of the funds raised by the Company.

1.3. Reallocation

The Company intends to use funds available as a result of the Offering as stated in Section 1.2 above.

However, these amounts are current estimates of development activities and there is no certainty that

actual costs will not vary from these estimates. Management of the Company retains broad discretion over

the use of net proceeds from the Offering and reserves the right to change the estimated allocation of net

proceeds set forth above. The Company does not currently intend to reallocate available funds, but if it

does so, it will be only for sound business reasons.

ITEM 2.

BUSINESS OF THE COMPANY

2.1. Structure

Brazil Potash Corp. was incorporated on October 10, 2006 pursuant to the provisions of the Business

Corporations Act (Ontario).

Investors should refer to the “Notes to the Consolidated Financial Statements” section, at page F-8 and

the “Summary” section, at page 1, in the attached Offering Circular for further information regarding

the structure and organization of the Company.

2.2. Our Business

Brazil Potash is a private mineral exploration and development company headquartered in Toronto,

Canada. The Company is focused on the extraction and processing of potash ore from underground

mines, as well as the distribution of the processed potash in Brazil.

Investors should refer to the “Our Business” and the “Description of Property” sections, at pages 18 to

29, in the attached Offering Circular for further information regarding the business objectives and

strategies of the Company.

2.3. Development of Business

In 2017, the Company raised total gross proceeds of US$13.25 million from private placement financings,

as well as US$540,000 from stock options exercises. The Company, upon completion of the bankable

feasible study report and securing its previous license for the Autazes Project, commenced work on

satisfying the necessary conditions to secure its construction license, such as environmental conditions

and social studies.

3

In 2018, the Company raised a total of US$4.75 million from stock option exercises. The Company

commenced consultations with indigenous communities close to the Autazes Project and continued

environmental and social studies in order to request the Installation License. The Company engaged in

discussions with various groups to secure project debt financing for the Autazes Project. As of April

2020, the Company has completed 76 of 78 items required to obtain the Installation License and 69 have

been approved by various agencies of Brazil’s government. The main item outstanding is additional

consultations with indigenous communities, which are ongoing and anticipated to be completed mid to

end of 2020.

In 2019, the Company raised aggregate gross proceeds of US$2.25 million from private placement

financings and US$1.5 million from option exercises. The Company continued work to complete the

construction license conditions for the Autazes Project and began formal negotiations of documentation

for debt project financing. The Company completed work on a Chinese feasibility study to help secure

debt financing in China and completed the basic engineering for a transmission line.

Investors should refer to the “Our Business” and the “Description of Property” sections, at pages 18 to

29, in the attached Offering Circular for further information regarding the general development of the

business of the Company.

Investors should also refer to the Company’s technical report titled “Autazes Potash Project – Bankable

Feasibility Study Report, 207040-00156-00-PM-REP-0008, for Brazil Potash Corporation” dated April

22, 2016, prepared in accordance with National Instrument 43-101 – Standards of Disclosure for

Mineral Projects, a copy of which is available from the Company upon request.

2.4. Long Term Objectives

The Company believes that if the Maximum Offering is raised, it will have sufficient capital to finance its

operations for at least the next 24 months..

The objectives of the Company for the next few years include: conducting basic engineering; and

construction of Brazil Potash’s Autazes potash Project.

What we must do and how we

will do it

Target completion date or, if not known,

number of months to complete

Our cost to complete

Conduct Basic Engineering Start in August of 2021

$9,275,000

Project Construction

Initiate in the second half of 2021 $2,170,800,000

Investors should refer to the “Use of Proceeds” and the “Plan of Operations” sections, at pages 17 & 18

and page 32, respectively, in the attached Offering Circular for further information regarding the

business objectives of the Company.

2.5. Short Term Objectives and How We Intend to Achieve Them

During the next 12 months, the Company intends to invest the proceeds of the Offering in the manner

more fully described in the Offering Circular. The objectives of the Company over the next 12 include:

securing the Installation License (LI) for construction of the Autazes potash project; environmental and

social license compliance; engineering for other applications and permits; optimizing the feasibility study;

4

land acquisition and maintaining mineral rights; and conducting essential testwork prior to starting the

EPCM phase.

What we must do and how we will do it Target completion date or,

if not known, number of

months to complete

Our cost to

complete

Land Acquisition & Maintaining Mineral Rights Land Q1 2021; mineral rights

payments for 24 months

$6,000,000

Environmental & Social License (LP)

compliance 24 months $5,000,000

Obtain Installation License (LI)

Engineering for Other Applications & Permits

Q1 2021 $8,000,000

Optimize Feasibility Study Q2 2021

$4,000,000

Essential Testwork Prior to Starting EPCM Phase June 2021 $3,000,000

Land Acquisition & Maintaining Mineral Rights June 2021 $6,000,000

Investors should refer to the “Use of Proceeds” and “Plan of Operations” sections, at pages 17 & 18

and page 32 respectively, in the attached Offering Circular for further information regarding the short

term business objectives of the Company.

2.6. Insufficient Funds

It is possible that the Company will only raise a minimal amount of capital; as a result, the raised capital

may not be sufficient to accomplish all of the Company’s proposed objectives and there is no assurance

that alternative financing will be available on terms acceptable to the Company, or at all.

Investors should refer to the heading “No Minimum Capitalization” under the “Risk Factors” section at

page 13 in the attached Offering Circular for further information regarding the possibility of insufficient

funds.

2.7. Material Agreements

The following is a list of agreements which are material to this Offering and to the Company, all of which

are in effect:

(a) the consulting agreement with Forbes & Manhattan Inc. dated October 1, 2009. For

details regarding the consulting agreement see the “Compensation of Directors and

Executive Officers” section, at page 35 to 37, in the attached Offering Circular;

(b) the consulting agreement with Iron Strike Inc. dated February 1, 2015. For details

regarding the consulting agreement see the “Compensation of Directors and Executive

Officers” section at page 35 to 37, in the attached Offering Circular;

(c) the consulting agreement with Jacome Gestao De Projetos LTDA dated June 1, 2017. For

details regarding the consulting agreement see the “Compensation of Directors and

Executive Officers” section at page 35 to 37, in the attached Offering Circular;

5

(d) the loan agreement with Sentient Global Resources Fund IV LP dated October 29, 2019.

For details regarding the loan agreement see the “Interest of Management and Others in

Certain Transactions” section, at page 38, in the attached Offering Circular;

(e) the consulting agreement with Helio Diniz dated July 1, 2009. For details regarding the

consulting agreement see the “Compensation of Directors and Executive Officers”

section at page 35 to 37, in the attached Offering Circular; and

(f) the broker-dealer agreement with Dalmore Group, LLC dated January 17, 2020, as

amended. For details regarding the broker-dealer agreement see pages i to ii and “Plan

of Distribution and Selling Securityholders” section at page 17, in the attached Offering

Circular.

ITEM 3.

INTERESTS OF DIRECTORS, MANAGEMENT, PROMOTERS AND PRINCIPAL HOLDERS

3.1. Compensation and Securities Held

The following table sets out certain information regarding each director and officer and holders of greater

than 10 percent of the Shares of the Company as at June 30, 2020, after giving effect to the Offering:

Name and

Municipality of

Principal Residence

Position with

Company

Compensation paid

and anticipated to be

paid by the Company

(in US$)

Percentage and Type

of Securities of the

Company/Funds Held

After Completion of

the Offering(1)

Matthew Simpson

Toronto, Ontario

Director and Chief

Executive Officer

$650,000 Nil

David Gower

Toronto, Ontario

Director and President $Nil 1,344,956 Shares /

0.94%

Ryan Ptolemy

Toronto, Ontario

Chief Financial Officer $45,271 Nil

Neil Said

Toronto, Ontario

Corporate Secretary $45,271 Nil

Helio Diniz

Toronto, Ontario

Managing Director

Brazil

$180,000(2) 442,566 Shares / 0.31%

Guilherme Jacome

Belo Horizonte, Brazil

Project Director $250,000 Nil

Stan Bharti

Toronto, Ontario

Chairman $579,996 16,482,937 Shares(3) /

11.56%

Andrew Pullar

Sydney, Australia

Director $Nil 29,510,912 Shares(4) /

20.69%

Pierre Pettigrew

Toronto, Ontario

Director $Nil 44,831 Shares / 0.03%

Carmel Daniele

London, England

Director $Nil 42,338,833 Shares(3)(5) /

29.68% Notes:

(1) 142,644,334 common shares outstanding assuming completion of the Maximum Offering.

(2) As of January 1, 2020, Helio Diniz’s annual compensation has been revised to $180,000.

(3) Ms. Carmel Daniele is the founder and Chief Investment Officer of the CD Capital Natural Resources group of funds.

Ms. Daniele’s beneficial ownership above includes shares owned by CD Capital. Mr. Bharti and Ms. Daniele have

agreed Ms. Daniele has a proxy to vote in her sole discretion the 16,482,937 shares included above in Mr. Bharti’s

6

beneficial ownership respective to pre-emptive rights, tag-along rights, and resolutions related to an initial public

offering of the Company, if any. As representative of CD Capital, Ms. Daniele is entitled to appoint an additional

director of the Company.

(4) Mr. Bharti and Mr. Pullar have agreed Mr. Pullar, as representative of Sentient Global Resources Fund IV LP, is

entitled to appoint an additional director of the Company.

(5) Ms. Daniele’s ownership in the table excludes 16,482,937 shares for which she has certain voting rights as stated above

in footnote (3).

Investors should refer to the “Directors, Executive Officers and Significant Employees”, “Compensation

of Directors and Executive Officers” and “Security Ownership of Management and Certain

Securityholders” sections, at pages 32, 35 to 38, respectively, in the attached Offering Circular for

further information regarding compensation and securities held by the directors, management, promoters

and principal holders.

3.2. Management Experience

Investors should refer to the “Business Experience” section at pages 33 to 34 in the attached Offering

Circular for further information regarding experience of the directors and officers of the Company.

3.3. Penalties, Sanctions and Bankruptcies

Except as disclosed below, there are no penalties, sanctions, declarations of bankruptcy, voluntary

assignments in bankruptcy, proposals under any bankruptcy or insolvency legislation or proceedings,

arrangements or compromises with creditors, appointments of a receiver, receiver manager or trustee to

hold assets, that have been in effect during the last ten years against or in connection with any of the

directors, executive officers, control persons or promoters of the Company or any issuer of which any

director, executive officer, control person or promoters of the Company was a director, executive officer

or control person.

On December 16, 2013, the Federal Prosecutor (the “MPF”) in Brazil filed civil and criminal lawsuits

against the Company’s Subsidiary and one of its officers alleging one drill hole was executed without the

proper licenses. The Company defended the matter vigorously as it believes the claims are without merit.

On June 28, 2018, the MPF requested an acquittal on the criminal lawsuit and the Company and its

officer agreed to pay fines of R$45,000 (US$13,131). During the year ended December 31, 2018, the

Company received insurance proceeds of R$650,000 (US$238,353) to partially offset legal defense fees

incurred of US$289,655 included in professional fees in the statement of loss.

Investors should refer to the “Involvement in Certain Legal Proceedings” section at pages 34 & 35 and

“Commitments and contingencies” on page F-31 in the attached Offering Circular for further

information.

3.4. Loans

On July 2, 2020, the Company entered into a loan agreement with Aberdeen International Inc. Stan

Bharti, director and chairman of the Company, and Ryan Ptolemy, Chief Financial Officer of the

Company, are each a director and officer of Aberdeen International Inc. Under the terms of the loan

agreement, the Company can borrow up to $100,000 in principal. The principal outstanding at any time

bears interest at 12% per annum. This loan is unsecured and has a six month term.

On October 29, 2019, the Company entered into a loan agreement with Sentient Global Resources Fund

IV LP, of which Andrew Pullar, a director of the Company, is a principal. Under the terms of the loan

agreement the Company borrowed $1,000,000 in principal amount in consideration for a one-time set-up

7

fee of $200,000. The principal outstanding at any time bears interest at 30% per annum; provided, no

interest accrues on the principal for the period from first drawdown until the earlier to occur of six

months, and the occurrence of an event of default. As of the date hereof the full principal is outstanding.

The Company, as at December 31, 2019, had trade payables and accrued liabilities reflected on its

balance sheet in the amount of $2,809,249 owing to directors and officers of the Company for consulting

fees.

The Company, as at December 31, 2019, paid or accrued $579,996 for business and operational

consulting services with Forbes & Manhattan Inc, a company for which Stan Bharti, a director and the

Chairman of the Company, is the Executive Chairman and Matthew Simpson, the Chief Executive Officer

of the Company, is the Chief Executive Officer.

Investors should refer to the “Certain Relationships” section and notes 14 & 21 of the “Notes to the

Consolidated Financial Statements” section at pages 33, F-21, & F-30 to F-31, respectively, in the

attached Offering Circular for further information regarding the amounts owing by the Company.

ITEM 4.

CAPITAL STRUCTURE

4.1. Share Capital

The Company is authorized to issue an unlimited number of Shares.

Description

of Security

Number authorized to be

issued

Weighted

Average Price

per Security(1)

Number

outstanding

as at the date

hereof

Number

outstanding after

max. offering

Shares unlimited US$1.73 130,144,344 142,644,334

Warrants N/A US$2.43 23,343,500 23,343,500

Options 10% of the Company’s

issued and outstanding

share capital

US$2.05 8,690,500 8,690,500

Note: (1) Assumes Maximum Offering is completed.

Investors should refer to the “Dilution”, “Securities Being Offered”, and notes 15, 16 & 17 of “Notes to

the Consolidated Financial Statements” sections, at page 16, page 39, and pages F-22 to F-27,

respectively, in the attached Offering Circular for further information regarding the share capital of the

Company.

4.2. Long Term Debt Securities

Description of long-term

debt

Interest Rate Repayment terms Amount outstanding

at June 30, 2020

Loan agreement with

Sentient Global Resource

Fund IV LP

30% annually Due July 31, 2020 US$1,000,000

Andrew Pullar (a director of the Company) is a principal at Sentient.

8

Investors should refer to “Interest of Management and Others in Certain Transactions” and note 14 of

the “Notes to the Consolidated Financial Statements ” sections, at page 38 and page F-21, respectively,

in the attached Offering Circular for further information regarding the leverage and borrowings of the

Company.

4.3. Prior Sales

Date of Issuance Type of Security

Issued

Number of

Securities Issued

Price per

Security

Total Funds

Received

November 29, 2019 Common Shares

from Option Exercise 1,000,000 $1.00 $1,000,000

November 29, 2019 Common Shares

from Option Exercise 298,809 $1.00 $298,809

November 29, 2019 Common Shares

from Option Exercise 233,363 $1.00 $233,363

November 29, 2019 Common Shares 200,000 3.75 $750,000

April 7, 2020 Common Share from

DSU settlement 850,000 - -

ITEM 5.

SECURITIES OFFERED

5.1. Terms of Securities

The Company is authorized to issue an unlimited number of Shares, without any special rights or

restrictions.

The Shares have the following rights, privileges and conditions attached to them as set out in the Business

Corporations Act (Ontario) and the Company’s articles of incorporation;

• to vote at meetings of shareholders;

• to share equally in the remaining property of the Company on liquidation, dissolution or winding

up of the Company; and

• to receive dividends if, as, and when declared by the Board of Directors.

Investors should refer to the “Securities Being Offered” section, at pages 39 to 41, in the attached

Offering Circular for further information regarding the rights of the shareholders.

5.2. Subscription Procedure

A purchaser may subscribe for Shares by delivering the following to the Company:

(a) a completed Subscription Agreement, including all schedules and exhibits attached

thereto, in a form acceptable to the Company; and

(b) (a wire transfer, bank draft or certified cheque deposited to the bank account set out in the

Subscription Agreement in the amount of the subscription price.

Purchasers will be required to enter into a Subscription Agreement with the Company which will contain,

among other things, representations, warranties, acknowledgements and covenants by the purchaser that it

is duly authorized to purchase the Shares, that it is purchasing the Shares as principal and for investment

9

and not with a view to resale and as to its corporate or other status to purchase the Shares and that the

Company is relying on an exemption from the requirements to provide the purchaser with a prospectus

and, as a consequence of acquiring the securities pursuant to such exemption, certain protections, rights

and remedies provided by applicable securities laws will not be available to the purchaser.

After the Company receives a completed Subscription Agreement and the funds required under the

Subscription Agreement have been transferred to the designated account, the Company reserves the right

to review and accept or reject subscriptions in whole or in part for any reason or for no reason. The

Company will return all monies from rejected subscriptions immediately to the purchaser, without interest

or deduction.

It is expected that the Initial Closing Date will occur on or about August 3, 2020. If the Maximum

Offering has not been reached, additional closings may be held until the Maximum Offering is achieved.

Shares are being sold in all of the Provinces of Canada under available exemptions from the prospectus

requirements under National Instrument 45-106 – Prospectus Exemptions (“NI 45-106”). Purchasers will

be required to make certain representations in the Subscription Agreement and the Company will rely on

such representations to establish the availability of the exemptions from the prospectus requirements. The

Company will also be offering Shares in reliance on the offering memorandum exemption (as provided in

NI 45-106).

Conditions Precedent to Completion of Offering

The conditions precedent to the completion of the Offering, amongst other things, are that:

(a) Subscription Agreements received will have been accepted by the Company;

(b) the Subscription Agreements for each purchaser that have been accepted by the Company

shall be in full force and effect, completed and duly executed;

(c) duly completed and executed copies of the applicable prospectus exemption certificate

and risk acknowledgment in the form(s) attached to the Subscription Agreement shall

have been received from each subscriber;

(d) a wire transfer, bank draft or certified cheque made payable on or before the Closing Date

in same day freely transferable Canadian funds at par in Toronto, Ontario to “Brazil

Potash Corp.” representing the purchase price payable by each prospective investor shall

have been received by the Company;

(e) the representations and warranties of each of the subscribers contained in the respective

Subscription Agreement, including in the applicable prospectus exemption certificate and

risk acknowledgment, shall be true and correct as at the Closing Date;

(f) the issue, sale and delivery of the Shares under this Offering shall be exempt from the

requirements to file a prospectus or any similar document under applicable securities

laws relating to the purchase and sale of the Shares, and all orders, consents or approvals

as may be required to permit such sale without the requirement of filing a prospectus or

any similar document shall have been received; and

(g) the Company will have received such other documents as it may reasonably request.

10

Where required by law, the subscription funds will be held in trust pending closing for two (2) business

days (and in any event until midnight on the 2nd business day) after the purchaser signs the Subscription

Agreement.

ITEM 6.

INCOME TAX CONSEQUENCES AND RRSP ELIGIBILITY

You should consult your own professional advisers to obtain advice on the income tax consequences that

apply to you.

The Shares are not eligible for investment in a registered retirement savings plan. You should consult

your own professional advisers to obtain advice on the registered retirement savings plan eligibility of

these securities.

ITEM 7.

COMPENSATION PAID TO SELLERS AND FINDERS

There is no commission payable by purchasers or by the Company.

ITEM 8.

RISK FACTORS

Investors should refer to the “Risk Factors” section, at pages 4 to 16, in the attached Offering Circular

for further information regarding the risk factors material to the Company and its shareholders.

Public Health Crises such as the COVID-19 Pandemic and other Uninsurable Risks

Events in the financial markets have demonstrated that businesses and industries throughout the world are

very tightly connected to each other. General global economic conditions seemingly unrelated to the

Company or to the mining industry, including, without limitation, interest rates, general levels of

economic activity, fluctuations in the market prices of securities, participation by other investors in the

financial markets, economic uncertainty, national and international political circumstances, natural

disasters, or other events outside of the Company’s control may affect the activities of the Company

directly or indirectly. In the course of development and advancement of mineral properties, certain risks,

and in particular, unexpected or unusual geological operating conditions including rock bursts, cave-ins,

fires, flooding and earthquakes may occur. The Company’s business, operations and financial condition

could also be materially adversely affected by the outbreak of epidemics or pandemics or other health

crises. For example, in late December 2019, a novel coronavirus (“COVID-19”) originated, subsequently

spread worldwide and on March 11, 2020, the World Health Organization declared it was a pandemic.

The risks of public health crises such as the COVID-19 pandemic to the Company’s business include

without limitation, the ability to gain access to government officials, ability to conduct the necessary

indigenous studies required to advance the Autazes project, the ability to conduct site visits with

investors, consultants, agents, contractors and/or government officials, employee health, workforce

productivity, increased insurance premiums, limitations on travel, the availability of industry experts and

personnel, disruption of the Company’s supply chains and other factors that will depend on future

developments beyond the Company’s control. In particular, the continued spread of the coronavirus

globally, prolonged restrictive measures put in place in order to control an outbreak of COVID-19 by

Canadian and Brazilian governments or other adverse public health developments could materially and

adversely impact the Company’s business and the advancement and development of the Autazes project

and could materially slow down or the Company could be required to suspend the advancement of the

project for an indeterminate period. There can be no assurance that the Company’s personnel will not

11

ultimately see its workforce productivity reduced or that the Company will not incur increased medical

costs or insurance premiums as a result of these health risks. In addition, the coronavirus pandemic or the

fear thereof could adversely affect global economies and financial markets resulting in volatility or an

economic downturn that could have an adverse effect on the demand for potash and the Company’s future

prospects.

The Company’s Autazes project is not located on Indigenous land, the closest reserve is 8km away and

based on Brazilian law any indigenous people located within 10km from a future mine site have the right

to be consulted. There are two major steps that need to be followed in these consultations. The first is

indigenous people need to determine who within their tribes will be involved in consultations. This first

step has been completed. The second is the actual consultation process which was scheduled to start in

March 2020 but is currently on hold due to the outbreak of Covid19. There can be no assurances as to

when the consultation process will start and this is an important step to obtain the Installation License for

project construction to commence.

Epidemics such as COVID-19 could have a material adverse impact on capital markets and the

Company’s ability to raise sufficient funds to finance the ongoing development of its material business.

All of these factors could have a material and adverse effect on the Company’s business, financial

condition and results of operations. The extent to which COVID-19 impacts the Company’s business,

including its operations and the market for its securities, will depend on future developments, which are

highly uncertain and cannot be predicted at this time, and include the duration, severity and scope of the

outbreak and the actions taken to contain or treat the coronavirus outbreak. It is not always possible to

fully insure against such risks, and the Company may decide not to insure such risks as a result of high

premiums or other reasons. Should such liabilities arise, they could reduce or eliminate any future

profitability and result in increasing costs and a decline in the value of the common shares of the

Company. Even after the COVID-19 pandemic is over, the Company may continue to experience material

adverse effects to its business, financial condition and prospects as a result of the continued disruption in

the global economy and any resulting recession, the effects of which may persist beyond that time. The

COVID-19 pandemic may also have the effect of heightening other risks and uncertainties disclosed and

described in this Offering Memorandum and the Offering Circular.

ITEM 9.

REPORTING OBLIGATIONS

The Company is not a reporting issuer in any of the Provinces or Territories of Canada. It is therefore not

required to disclose material changes which occur in its business and affairs, nor is it required to file with

any securities regulatory authorities or provide security holders with interim financial statements. The

Company is required to place before the shareholders of the Company before every annual meeting of the

Company the audited financial statements of the Company. The Company shall, not less than 10 days

before each annual meeting of the shareholders of the Company or before the signing a resolution in lieu

of an annual general meeting, provide a copy of the annual financial statements of the Company to each

shareholder.

12

ITEM 10.

RESALE RESTRICTIONS

10.1. General Statement

The Shares offered by this Offering Memorandum are being distributed pursuant to exemptions from the

prospectus requirements of applicable securities laws; consequently, the resale of these securities by

investors is subject to restrictions.

The Shares will be subject to resale restrictions, including a restriction on trading. Until the restriction on

trading expires, if ever, you will not be able to trade the Shares unless you comply with an exemption

from the prospectus and registration requirements under securities legislation. As the Company may not

become a reporting issuer in any Province or Territory of Canada, these restrictions on trading in the

Shares may not expire. Consequently, holders of Shares may not be able to sell their Shares in a timely

manner, if at all.

Purchasers are advised to consult with their advisors concerning restrictions on resale and are further

advised against reselling their Shares until they have determined that any such resale is in compliance

with the requirements of applicable legislation and the articles of incorporation of the Company, as may

be amended from time to time.

10.2. Restricted Period

Unless permitted under securities legislation, you cannot trade the Shares before the date that is 4 months

and a day after the date the Company becomes a reporting issuer in any Province or Territory of Canada.

ITEM 11.

PURCHASERS’ RIGHTS

If you purchase these securities you will have certain rights, some of which are described below. For

information about your rights you should consult a lawyer.

In certain circumstances, subscribers resident in certain provinces and territories of Canada are provided

with a remedy for rescission or damages, or both, in addition to any other right they may have at law,

where an offering memorandum and any amendment to it contains a misrepresentation. A

“misrepresentation” is generally defined in the applicable securities legislation as an untrue statement of a

material fact or an omission to state a material fact that is required to be stated or that is necessary to

make any statement not misleading in light of the circumstances in which it was made. These remedies, or

notice with respect thereto, must be exercised or delivered, as the case may be, by the subscriber within

the time limits prescribed by the applicable securities legislation.

The following is a summary of rights of rescission or damages, or both, available to subscribers. The

following summary is subject to the express provisions of the applicable securities laws, regulations and

rules, and reference is made thereto for the complete text of such provisions. Such provisions may contain

limitations and statutory defenses not described herein which the Company and other applicable parties

may rely. Purchasers should refer to the applicable securities legislation for particulars of these

provisions or consult their legal advisers.

The rights of action described below are in addition to and without derogation from any other right or

remedy available at law to the purchaser and are intended to correspond to the provisions of the relevant

securities legislation and are subject to the defenses contained therein. The enforceability of these rights

13

may be limited. The rights of action discussed below will be granted to the subscribers to whom such

rights are conferred upon acceptance by the Company of the subscription price for the Shares.

Notwithstanding that applicable securities laws of certain provinces do not provide, or require the

Company to provide, to subscribers resident in such provinces, any rights of action in circumstances

where the Offering Memorandum or an amendment thereto contains a misrepresentation, the Company

hereby grants to such subscribers contractual rights of action that are equivalent to the statutory rights of

action set forth above with respect to subscribers resident in Ontario.

You can cancel your agreement to purchase these Shares. To do so, you must send a notice to the

Company by midnight on the 2nd Business Day after you sign the agreement to purchase the Shares.

Ontario

In accordance with Section 130.1 of the Securities Act (Ontario) (the “Ontario Act”), in the event that

this Offering Memorandum or any amendment hereto contains a misrepresentation (as defined in the

Ontario Act) the subscriber who purchases Shares offered by this Offering Memorandum during the

period of distribution has, without regard to whether the subscriber relied upon the misrepresentation, a

right of action against the Company, and a selling security holder on whose behalf the distribution is

made, for damages, or, while the subscriber is still the owner of the Shares purchased by that subscriber,

for rescission, in which case, if the subscriber elects to exercise the right of rescission, the subscriber will

have no right of action for damages against the Company, provided that:

(a) no person or company will be liable if it proves that the subscriber purchased the Shares

with knowledge of the misrepresentation;

(b) in the case of an action for damages, the defendant will not be liable for all or any portion

of the damages that it proves do not represent the depreciation in value of the Shares as a

result of the misrepresentation relied upon; and

(c) in no case will the amount recoverable in any action exceed the price at which the Shares

were sold to the subscriber.

The foregoing rights provided in accordance with Section 130.1 of the Ontario Act do not apply to the

following subscribers relying upon the accredited investor exemption in Ontario:

(a) a Canadian financial institution, meaning either:

(i) an association governed by the Cooperative Credit Associations Act (Canada) or

a central cooperative credit society for which an order has been made under

section 473(1) of that Act; or

(ii) a bank, loan corporation, trust company, trust corporation, insurance company,

treasury branch, credit union, caisse populaire, financial services corporation, or

league that, in each case, is authorized by an enactment of Canada or a

jurisdiction of Canada to carry on business in Canada or a jurisdiction in Canada;

(b) a Schedule III bank, meaning an authorized foreign bank named in Schedule III of the

Bank Act (Canada),

14

(c) The Business Development Bank of Canada incorporated under the Business

Development Bank of Canada Act (Canada), or

(d) a subsidiary of any person referred to in paragraphs (a), (b) or (c) if the person owns all

of the voting securities of the subsidiary, except the voting securities required by law to

be owned by the directors of the subsidiary.

In accordance with Section 138 of the Ontario Act, no action shall be commenced to enforce these

statutory rights more than:

(a) in an action for rescission, 180 days from the date of the transaction that gave rise to the

cause of action; or

(b) in an action for damages, the earlier of:

(i) 180 days after the plaintiff first had knowledge of the facts giving rise to the

cause of action; or

(ii) three years after the date of the transaction that gave rise to the cause of action.

Investors from Other Provinces

Securities legislation in certain other provinces and territories of Canada provides purchasers of securities

with, in addition to any other right they may have at law, rights of rescission or damages, or both, where

any document, purporting to describe the business and affairs of an issuer that has been prepared

primarily for delivery to and review by a prospective purchaser so as to assist the prospective purchaser to

make an investment decision in respect of securities and, in some cases, advertising and sales literature

used in connection with the offering of the offered securities, contains a misrepresentation. For the

purposes of this section, “misrepresentation” means:

(a) an untrue statement of a fact that significantly affects, or would reasonably be expected to

have a significant effect, on the market price of the securities of the Company (a

“material fact”); or

(b) an omission to state a material fact that is required to be stated or that is necessary to

make a statement not misleading in the light of the circumstances in which it was made.

These rights must be exercised by purchasers of the offered securities within the prescribed time limits

under applicable securities legislation. Purchasers should refer to the applicable provisions of the

securities legislation of their province or territory for the full particulars of these rights or consult with

their legal advisor.

15

ITEM 12.

FINANCIAL STATEMENTS

Investors should refer to pages F-1 to F-7, in the attached Offering Circular for Audited Consolidated

Financial Statements of Brazil Potash Corp. for the Years Ended December 31, 2019 and December 31,

2018 (Expressed in US Dollars).

Investors should refer to pages F-8 to F-32, in the attached Offering Circular for the accompanying

Notes to the Consolidated Financial Statements of Brazil Potash Corp. for the Years Ended December 31,

2019 and December 31, 2018.

Please find attached the following financial statements:

- Unaudited Condensed Consolidated Interim Financial Statements of Brazil Potash Corp. for the

three months ended March 31, 2020 and March 31, 2019.

Brazil Potash Corp.

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

For the three months ended March 31, 2020 and 2019

-- Stated in US dollars –

(unaudited)

Brazil Potash Corp.

See accompanying notes to the condensed consolidated interim financial statements Page 2

Condensed Consolidated Interim Statements of Financial Position (Expressed in U.S. dollars)

Reporting entity and going concern (Note 1) Subsequent event (Note 11) Approved by the Board of Directors on June 2, 2020

“STAN BHARTI”, Director

“ANDREW PULLAR”, Director

As at:March 31,

2020

December 31,

2019

(unaudited)

ASSETS

Current

Cash and cash equivalents $ 448,400 $ 1,360,010

Restricted cash 14,802 16,169

Amounts receivable 331,029 340,815

Prepaid expenses 29,138 47,147

Total current assets 823,369 1,764,141

Non-current

Property and equipment (Note 4) 930,679 1,202,988

Exploration and evaluation assets (Note 5) 112,621,532 128,996,822

Total assets $ 114,375,580 $ 131,963,951

LIABILITIES

Current

Trade payables and accrued liabilities (Note 6) $ 5,540,051 $ 5,356,293

Loans payable (Note 7) 1,000,000 1,000,000

Total current liabilities 6,540,051 6,356,293

Non-current

Long term portion of land fee installment payable (Note 6) 119,617 200,537

Deferred income tax liability 1,538,273 1,945,723

Total liabilities 8,197,941 8,502,553

Equity

Share capital 194,116,957 194,116,957

Share-based payments reserve (Note 8) 39,270,846 38,342,655

Warrants reserve 23,715,254 23,715,254

Accumulated other comprehensive loss (70,161,582) (53,201,693)

Deficit (80,763,836) (79,511,775)

Total equity 106,177,639 123,461,398

Total liabilities and equity $ 114,375,580 $ 131,963,951

Brazil Potash Corp.

See accompanying notes to the condensed consolidated interim financial statements Page 3

Condensed Consolidated Interim Statements of Loss and Other Comprehensive Loss (Expressed in U.S. dollars) (unaudited)

Three months

ended

Three months

ended

March 31, March 31,

2020 2019

Expenses

Consulting and management fees 511,780$ 649,032$

Professional fees 117,247 18,366

General office expenses 34,633 44,172

Share-based compensation (Note 8) 664,754 (77,016)

Travel expenses 42,414 189,607

Communications and promotions 70,697 6,677

Foreign exchange (gain) loss (222,585) 6,637

Operating Loss 1,218,940 837,475

Other income - (10,084)

Finance income (Note 3) (1,504) (609)

Loss for the period before income taxes 1,217,436 826,782

Income taxes 34,625 44,217

Loss for the period 1,252,061$ 870,999$

Other comprehensive loss:

Items that subsequently may be reclassified into net income:

Foreign currency translation 16,959,889 506,440

Total comprehensive loss for the period 18,211,950$ 1,377,439$

Basic and diluted loss per share 0.01$ 0.01$

Weighted average number of common

shares outstanding - basic and diluted 129,294,334 127,162,162

Brazil Potash Corp.

See accompanying notes to the condensed consolidated interim financial statements Page 4

Condensed Consolidated Interim Statement of Changes in Equity (Expressed in U.S. dollars) (unaudited)

Share-based

payments

Accumulated

Other

Comprehensive Accumulated Shareholders'

Warrants reserve Income (Loss) Deficit Equity

# $ $ $ $ $ $

Balance, December 31, 2018 127,162,162 186,120,585 24,540,488 38,164,138 (50,137,421) (72,037,312) 126,650,478

Deferred share units - - - (30,024) - - (30,024)

Option expiry - - - (1,306,864) - 1,306,864 -

DSUs forfeited - - - (833,332) - 833,332 -

Net (loss) and comprehensive (loss) for the

period - - - - (506,440) (870,999) (1,377,439)

Balance, March 31, 2019 127,162,162 186,120,585 24,540,488 35,993,918 (50,643,861) (70,768,115) 125,243,015

Balance, December 31, 2019 129,294,334 194,116,957 23,715,254 38,342,655 (53,201,693) (79,511,775) 123,461,398

Deferred share units - - - 928,191 - - 928,191

Net (loss) and comprehensive (loss) for the

period - - - - (16,959,889) (1,252,061) (18,211,950)

Balance, March 31, 2020 129,294,334 194,116,957 23,715,254 39,270,846 (70,161,582) (80,763,836) 106,177,639

Common Shares

Brazil Potash Corp.

See accompanying notes to the condensed consolidated interim financial statements Page 5

Consolidated Statement of Cash Flows (Expressed in U.S. dollars) (unaudited)

Three months ended Three months ended

March 31, 2020 March 31, 2019

$ $

CASH FLOWS FROM

OPERATING ACTIVITIES

Loss for the period before taxes (1,217,436) (826,782)

Adjustment for:

Finance Income (Note 3) (1,504) (609)

Share-based compensation (Note 8) 664,754 (77,016)

(554,186) (904,407)

Change in amounts receivable 9,144 (17,349)

Change in prepaid expenses 14,171 9,456

Change in trade payables and accrued liabilities 372,619 693,846

Net cash used in operating activities (158,252) (218,454)

CASH FLOWS FROM

INVESTING ACTIVITIES

Exploration and evaluation assets (645,185) (1,420,575)

Finance income 1,504 609

Net cash used in investing activities (643,681) (1,419,966)

Effect of exchange rate changes on cash and cash equivalents (109,677) (42,652)

NET (DECREASE) IN CASH AND CASH EQUIVALENTS (911,610) (1,681,072)

CASH AND CASH EQUIVALENTS, beginning of period 1,360,010 2,278,641

CASH AND CASH EQUIVALENTS, end of period 448,400 597,569

SUPPLEMENTAL INFORMATION:

2,522 5,603

Share-based compensation included in exploration and evaluation assets 263,437 46,992

Amortization of assets capitalized to exploration and evaluation assets

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 6

1. Reporting entity and going concern

Brazil Potash Corp. (the “Company”) was incorporated under the laws of the Province of Ontario, Canada by Articles of Incorporation on October 10, 2006. The Company remained inactive until June 16, 2009. On June 18, 2009, the Company’s subsidiary Potassio do Brasil Ltda. (the “Subsidiary”) was incorporated. The principal activity of Brazil Potash Corp. is the exploration and development of potash properties in Brazil. The Company’s head office is located at 65 Queen Street West, 8th floor, Toronto, Ontario, M5H 2M5, Canada.

The condensed consolidated interim financial statements include the financial statements of the Company and its subsidiary that is listed in the following table:

The Company received its Preliminary Social and Environmental License (LP) for the Autazes potash project in Brazil from the Amazonas Environmental Protection Institute (IPAAM) in July 2015 based on submission of a full Environmental and Social Impact Assessment completed by the Company in January 2015. Prior to receiving the LP, the Company and its consultant Golder Associates Ltd. (“Golder”) conducted several rounds of indigenous consultations and despite this work, the Brazil Federal Public Ministry (MPF) opened a civil investigation on the Company’s LP based on a motion from a non-governmental organization. The MPF commenced legal proceedings questioning the validity of the Company’s LP. The result of the legal proceedings brought by the MPF is that the Company voluntarily agreed to temporarily suspend its LP and to conduct additional indigenous consultations with local communities in accordance with International Labour Organization (ILO 169) given Brazil is a signatory to this international convention. There are two major steps that need to be followed in these consultations. The first is indigenous people need to determine the means and who within their tribes will be involved in consultations. This first step has been completed. The second is the actual consultation process which was scheduled to start in March 2020 but is currently on hold due to the outbreak of Covid19. Following the first round of indigenous consultations a judge may authorize the Company’s indigenous impact study to be submitted for review and reinstate the L.P. Going Concern The preparation of the condensed consolidated interim financial statements requires an assessment on the validity of the going concern assumption. The validity of the going concern concept is dependent on financing being available for the continuing working capital requirements of the Company and for the development of the Company's projects. The Company incurred a loss of $1,252,061 for the three months ended March 31, 2020 ($870,999 for the three months ended March 31, 2019) and as at March 31, 2020 had an accumulated deficit of $80,763,836 (December 31, 2019 - $79,511,775) and a working capital deficiency of $5,716,682 as at March 31, 2020 (including cash of $448,400) (December 31, 2019 - $4,592,152 (including cash of $1,360,010)).

Country of

incorporation

March 31,

2020

December 31,

2019

Potassio do Brasil Ltda. Brazil 100% 100%

% Ownership

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 7

1. Reporting entity and going concern (continued)

The Company requires equity capital and/or financing for working capital and exploration and development of its properties. As a result of continuing operating losses, the Company's continuance as a going concern is dependent upon its ability to obtain adequate financing and to reach profitable levels of operation. It is not possible to predict whether financing efforts will be successful or if the Company will attain profitable levels of operations. Management has previously been successful in raising the necessary funding to continue operations in the normal course of operations and was able to close private placement financings on July 2, 2019 and on November 29, 2019. Further, on October 29, 2019, the Company entered into a loan agreement to fund operating expenses (see Note 7). The Company is also currently in the process of offering up to 12,500,000 (the “Maximum Offering”) shares of the Company at a price of $4.00 per share to be sold in an offering. See note 11. However, there is no assurance, that the Company will be successful in closing the offering of shares, be successful in raising sufficient financing, or achieve profitable operations, to fund its working capital deficiency, or the future exploration and development of its properties. These circumstances raise substantial doubt as to the Company’s ability to continue to operate as a going concern. These condensed consolidated interim financial statements do not include any adjustments to the carrying amount, or classification of assets and liabilities, if the Company was unable to continue as a going concern. These adjustments may be material. On the basis that additional funding as outlined above will be received when required, the directors are satisfied that it is appropriate to continue to prepare the consolidated financial statements of the Company on the going concern basis.

2. Basis of preparation

a) Statement of compliance:

The condensed consolidated interim financial statements are in compliance with IAS 34, Interim Financial Reporting. Accordingly, certain information and disclosures normally included in annual financial statements prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”), have been omitted or condensed. These condensed consolidated interim financial statements should be read in conjunction with the Company’s consolidated financial statements for the year ended December 31, 2019.

The condensed consolidated interim financial statements were authorized for issue by the Board of Directors on June 2, 2020.

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 8

2. Basis of preparation (continued)

b) Significant accounting policies:

The unaudited condensed consolidated interim financial statements (“interim financial statements”) were prepared using the same accounting policies and methods as those used in the Company’s consolidated financial statements for the year ended December 31, 2019, except for the adoption of the following new standards and amendments issued by the IASB that were effective as of January 1, 2020. IAS 1, Presentation of Financial Statements (“IAS 1”) and IAS 8 – Accounting Policies, Changes in Accounting Estimates and Errors (“IAS 8”) were amended in October 2018 to refine the definition of materiality and clarify its characteristics. The revised definition focuses on the idea that information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements. The adoption of IAS 1 on January 1, 2020 did not have a material impact on the Company’s condensed consolidated interim financial statements. 3. Finance income and expenses

Three months ended March 31, 2020 2019

Finance income:

Interest on bank deposits (16)$ -$

Interest on short-term deposits (1,488) (609)

(1,504)$ (609)$

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 9

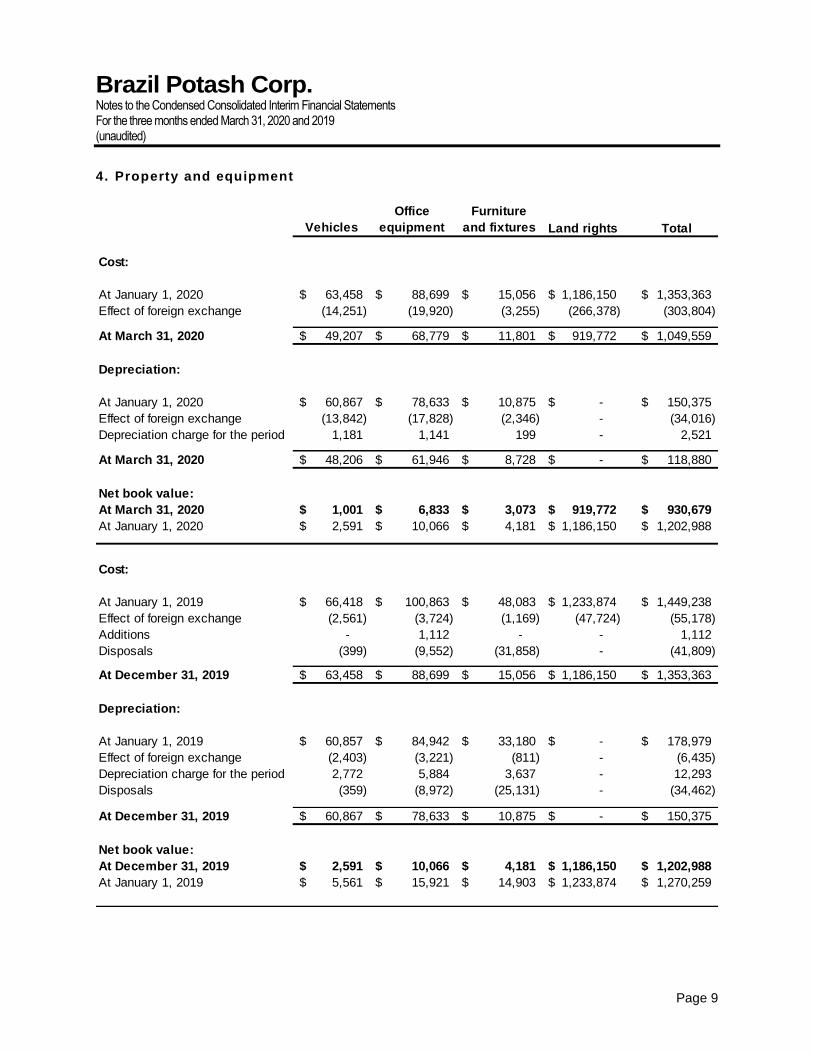

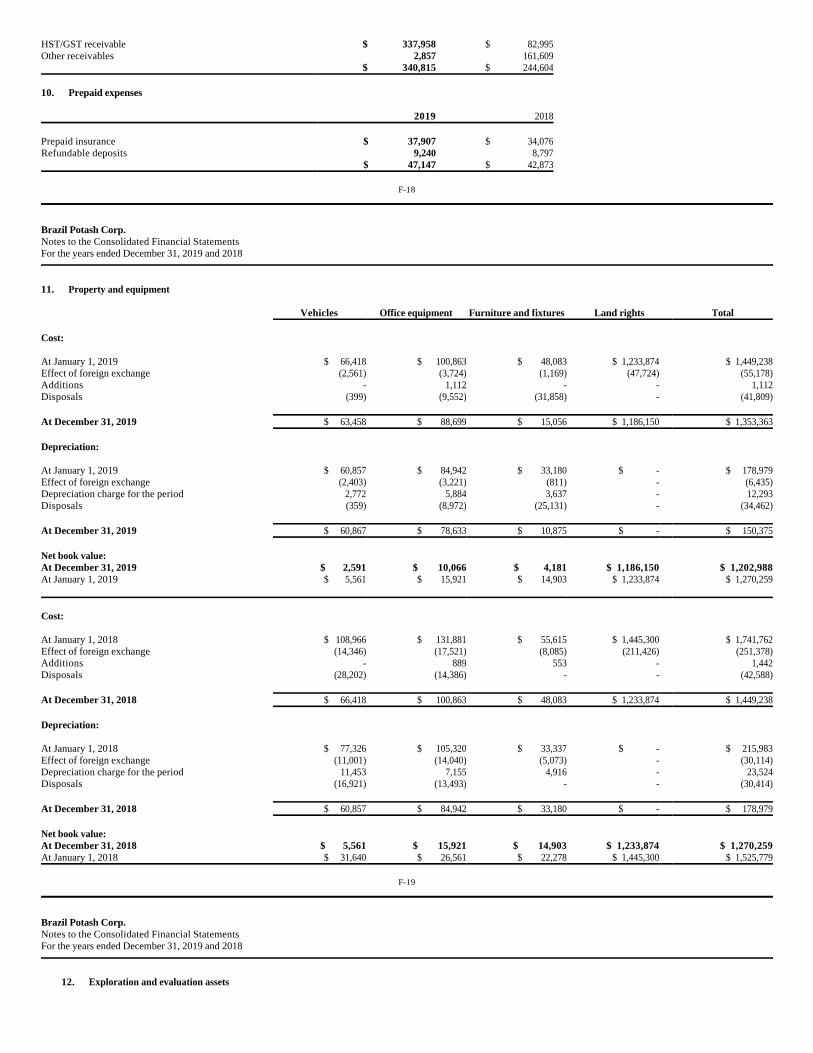

4. Property and equipment

Vehicles

Office

equipment

Furniture

and fixtures Land rights Total

Cost:

At January 1, 2020 63,458$ 88,699$ 15,056$ 1,186,150$ 1,353,363$

Effect of foreign exchange (14,251) (19,920) (3,255) (266,378) (303,804)

At March 31, 2020 49,207$ 68,779$ 11,801$ 919,772$ 1,049,559$

Depreciation:

At January 1, 2020 60,867$ 78,633$ 10,875$ -$ 150,375$

Effect of foreign exchange (13,842) (17,828) (2,346) - (34,016)

Depreciation charge for the period 1,181 1,141 199 - 2,521

At March 31, 2020 48,206$ 61,946$ 8,728$ -$ 118,880$

Net book value:

At March 31, 2020 1,001$ 6,833$ 3,073$ 919,772$ 930,679$

At January 1, 2020 2,591$ 10,066$ 4,181$ 1,186,150$ 1,202,988$

Cost:

At January 1, 2019 66,418$ 100,863$ 48,083$ 1,233,874$ 1,449,238$

Effect of foreign exchange (2,561) (3,724) (1,169) (47,724) (55,178)

Additions - 1,112 - - 1,112

Disposals (399) (9,552) (31,858) - (41,809)

At December 31, 2019 63,458$ 88,699$ 15,056$ 1,186,150$ 1,353,363$

Depreciation:

At January 1, 2019 60,857$ 84,942$ 33,180$ -$ 178,979$

Effect of foreign exchange (2,403) (3,221) (811) - (6,435)

Depreciation charge for the period 2,772 5,884 3,637 - 12,293

Disposals (359) (8,972) (25,131) - (34,462)

At December 31, 2019 60,867$ 78,633$ 10,875$ -$ 150,375$

Net book value:

At December 31, 2019 2,591$ 10,066$ 4,181$ 1,186,150$ 1,202,988$

At January 1, 2019 5,561$ 15,921$ 14,903$ 1,233,874$ 1,270,259$

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 10

5. Exploration and evaluation assets

6. Trade payables and accrued liabilities

During the year ended December 31, 2017, the Company entered into an installment program with the National Mining Agency (“ANM”) for the payment of its mineral rights and land fees. The installment program allows for the payment of outstanding land fees on a monthly basis over a period of five years. The Company accrued interest charges and penalties of $103,805 (R$432,286) on the date the installment program was entered into in connection with the consolidation of its outstanding fees under the program. In addition, each installment is charged interest at the rate posted by the Special Settlement and Custody System (“SELIC”) until the month prior to payment plus 1% in the month of payment. Any monthly installments not paid by the due date will incur additional fines of 0.33% per day up to a maximum of 20%. Failure to pay two consecutive monthly installments will result in the cancellation of the instalment plan. As at March 31, 2020, the balance owing on the installment plan was $263,157 (R$1,367,890), included in current and long-term portion of land fee installments in the table above, which approximates the present value of the expected payments.

Expenditures:

Three months

ended March 31,

2020

Year ended

December 31,

2019

Balance, beginning of period $ 128,996,822 $ 128,257,742

Additions:

Mineral rights and land fees - 10,957

Additions to exploration and evaluation assets 500,040 2,563,842

Share-based compensation 263,437 1,178,596

Effect of foreign exchange (17,138,767) (3,014,315)

Balance, end of period $ 112,621,532 $ 128,996,822

March 31,

2020

December 31,

2019

Trade payables 3,730,460$ 3,542,682$

Current portion of land fee installments 143,540 185,111

Accruals 1,666,051 1,628,500

Current 5,540,051$ 5,356,293$

Long-term portion of land fee installments 119,617$ 200,537$

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 11

7. Loans payable

On October 29, 2019, Brazil Potash entered into a loan agreement with Sentient Global Resource Fund IV LP, (“Sentient”). Pursuant to the terms of the loan agreement (the “Loan”), Sentient agreed to lend the Company $1,000,000 at an interest rate of 30% per annum and a repayment date of July 31, 2020. The Company also accrued a setup fee of $200,000, included in accounts payable and accrued liabilities, in connection with the loan. An additional extension fee becomes payable if the Company extends the loan due date beyond April 29, 2020. No interest accrues or is payable on the loan until the earlier of a) a date that is six months from October 29, 2019 or b) default on the loan. Andrew Pullar (a director of the Company) is a principal at Sentient.

8. Share-based payments

The continuity of shares-based payments reserve activity during the period was as follows:

(a) Option plan: The Company has an incentive share option plan (“the Plan”) whereby the Company may grant to directors, officers, employees and consultants options to purchase shares of the Company. The Plan provides for the issuance of share options to acquire up to 10% of the Company's issued and outstanding capital at the date of grant. The Plan is a rolling plan, as the number of shares reserved for issuance pursuant to the grant of stock options will increase as the Company's issued and outstanding share capital increases. Options granted under the Plan will be for a term not to exceed five years. The plan provides that it is solely within the discretion of the Board to determine who would receive share options and in what amounts. In no case (calculated at the time of grant) shall the plan result in:

- the number of options granted in a twelve-month period to any one consultant exceeding 2% of the issued shares of the Company;

- the aggregate number of options granted in a twelve-month period to any one optionee exceeding 5% of the outstanding shares of the Company; and

- the number of options granted in a twelve-month period to employees and management company employees undertaking investor relations activities exceeding in aggregate 2% of the issued shares of the Company.

Three months

ended

March 31, 2020

Year ended

December 31,

2019

Balance, beginning of the period 38,342,655$ 38,164,138$

Stock options granted and/or vested during the period - 5,227,600

Option extension - 134,500

Options exercised - (4,214,200)

Forfeited options - (3,179,501)

Vesting of DSUs 928,191 3,043,450

Forfeited DSUs - (833,332)

Balance, end of the period 39,270,846$ 38,342,655$

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 12

8. Share-based payments (continued)

(a) Option plan (continued): Share option transactions continuity during the period were as follows (in number of options):

There were no options granted during the three months ended March 31, 2020 or the three months ended March 31, 2019. At March 31, 2020, outstanding options to acquire common shares of the Company were as follows:

Number of

options

Weighted

average

exercise

price

Number of

options

Weighted

average

exercise

price

Balance, beginning of period 8,690,500 $ 2.05 9,890,500 $ 1.99

Granted - - 1,982,172 1.62

Exercised - - (1,532,172) 1.00

Forfeited - - (1,650,000) 2.12

Balance, end of period 8,690,500 $ 2.05 8,690,500 $ 2.05

Three months ended

March 31, 2020

Year ended

December 31, 2019

Date Options Options Exercise Grant date

of expiry outstanding exercisable price fair value vested

September 23, 2020 2,975,000 2,975,000 $1.00 4,316,322

September 23, 2020 3,717,500 3,717,500 $2.50 8,769,710

July 22, 2020 1,348,000 1,348,000 $2.50 2,272,197

November 19, 2021 200,000 200,000 $3.75 349,400

November 25, 2021 200,000 200,000 $2.50 537,800

June 1, 2024 250,000 250,000 $3.75 664,000

8,690,500 8,690,500 16,909,429$

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 13

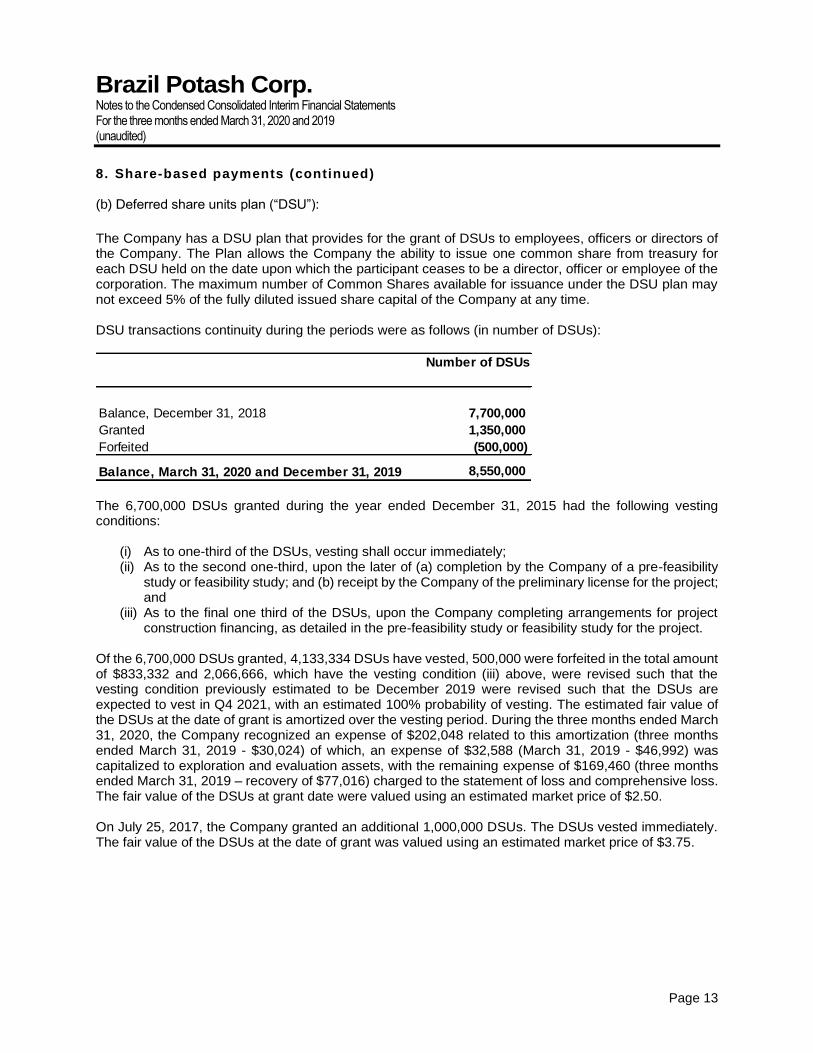

8. Share-based payments (continued) (b) Deferred share units plan (“DSU”):

The Company has a DSU plan that provides for the grant of DSUs to employees, officers or directors of the Company. The Plan allows the Company the ability to issue one common share from treasury for each DSU held on the date upon which the participant ceases to be a director, officer or employee of the corporation. The maximum number of Common Shares available for issuance under the DSU plan may not exceed 5% of the fully diluted issued share capital of the Company at any time. DSU transactions continuity during the periods were as follows (in number of DSUs):

The 6,700,000 DSUs granted during the year ended December 31, 2015 had the following vesting conditions:

(i) As to one-third of the DSUs, vesting shall occur immediately; (ii) As to the second one-third, upon the later of (a) completion by the Company of a pre-feasibility

study or feasibility study; and (b) receipt by the Company of the preliminary license for the project; and

(iii) As to the final one third of the DSUs, upon the Company completing arrangements for project construction financing, as detailed in the pre-feasibility study or feasibility study for the project.

Of the 6,700,000 DSUs granted, 4,133,334 DSUs have vested, 500,000 were forfeited in the total amount of $833,332 and 2,066,666, which have the vesting condition (iii) above, were revised such that the vesting condition previously estimated to be December 2019 were revised such that the DSUs are expected to vest in Q4 2021, with an estimated 100% probability of vesting. The estimated fair value of the DSUs at the date of grant is amortized over the vesting period. During the three months ended March 31, 2020, the Company recognized an expense of $202,048 related to this amortization (three months ended March 31, 2019 - $30,024) of which, an expense of $32,588 (March 31, 2019 - $46,992) was capitalized to exploration and evaluation assets, with the remaining expense of $169,460 (three months ended March 31, 2019 – recovery of $77,016) charged to the statement of loss and comprehensive loss. The fair value of the DSUs at grant date were valued using an estimated market price of $2.50. On July 25, 2017, the Company granted an additional 1,000,000 DSUs. The DSUs vested immediately. The fair value of the DSUs at the date of grant was valued using an estimated market price of $3.75.

Number of DSUs

Balance, December 31, 2018 7,700,000

Granted 1,350,000

Forfeited (500,000)

Balance, March 31, 2020 and December 31, 2019 8,550,000

Brazil Potash Corp.

Notes to the Condensed Consolidated Interim Financial Statements For the three months ended March 31, 2020 and 2019 (unaudited)

Page 14

8. Share-based payments (continued) (b) Deferred share units plan (“DSU”): On June 1, 2019, the Company granted 400,000 DSU’s. 100,000 DSUs vested on July 1, 2019, 100,000 DSUs will vest on October 1, 2019, 100,000 will vest on January 1, 2020 and another 100,000 DSU’s will vest on April 1, 2020. During the three months ended March 31, 2020, the Company recognized an expense of $113,638 related to this amortization charged to the statement of loss. The fair value of the DSUs at the date of grant was valued using an estimated market price of $3.75.