Embed Size (px)

Citation preview

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 1/50

Session 1Financial Management

Foundation and FinancialBackground

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 2/50

Outline of Chapter

1. Business and Its Forms

2. Finance

3. The role of the financial manager today is so important.

4. Financial management

5. Three major Financial decision.6. The goals of the firm

7. Why shareholders' wealth maximization is preferred over other goals.

8. Agency Theory

9. Corporate governance.

10. Social responsibility of the firm.11. The basic responsibilities of financial managers and the differencesbetween a "treasurer" and a "controller."

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 3/50

Business

Any legal activity which is undertaken to

earn profit is called business

Forms of Business

Sole Proprietorship

Partnership

Corporation

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 4/50

The Business Environment

Oldest form of business organization.Business income is accounted for on the

owner’s personal income tax form.

Sole Proprietorship -- A business

form for which there is one owner.

This single owner has unlimitedliability for all debts of the firm.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 5/50

Summary for

Sole Proprietorship

Advantages

Simplicity

Low setup cost

Quick setup

Single tax filing on

individual form

Disadvantages

Unlimited liability

Hard to raise additionalcapital

Transfer of ownership

difficulties

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 6/50

The Business Environment

Business income is accounted for on

each partner’s personal income taxform.

Partnership -- A business form in

which two or more individuals

act as owners.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 7/50

Types of Partnerships

Limited Partnership -- Limited partners have

liability limited to their capital contribution

(investors only). At least one general partner isrequired and all general partners have unlimited

liability.

General Partnersh ip -- All partners have

un l imi ted l iabi l i ty and are liable for all

obligations of the partnership.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 8/50

Summary for Partnership

Advantages

Can be simple

Low setup cost, higher thansole proprietorship

Relatively quick setup

Limited liability for limited

partners

Disadvantages

Unlimited liability for the

general partner

Difficult to raise additional

capital, but easier than sole

proprietorship

Transfer of ownership

difficulties

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 9/50

The Business Environment

An artificial entity that can own assets

and incur liabilities.

Business income is accounted for on theincome tax form of the corporation.

Corporation -- A business form

legally separate from its owners.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 10/50

Summary for Corporation

Advantages

Limited liability

Easy transfer ofownership

Unlimited life

Easier to raise largequantities of capital

Disadvantages

Double taxation

More difficult toestablish

More expensive to set

up and maintain

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 11/50

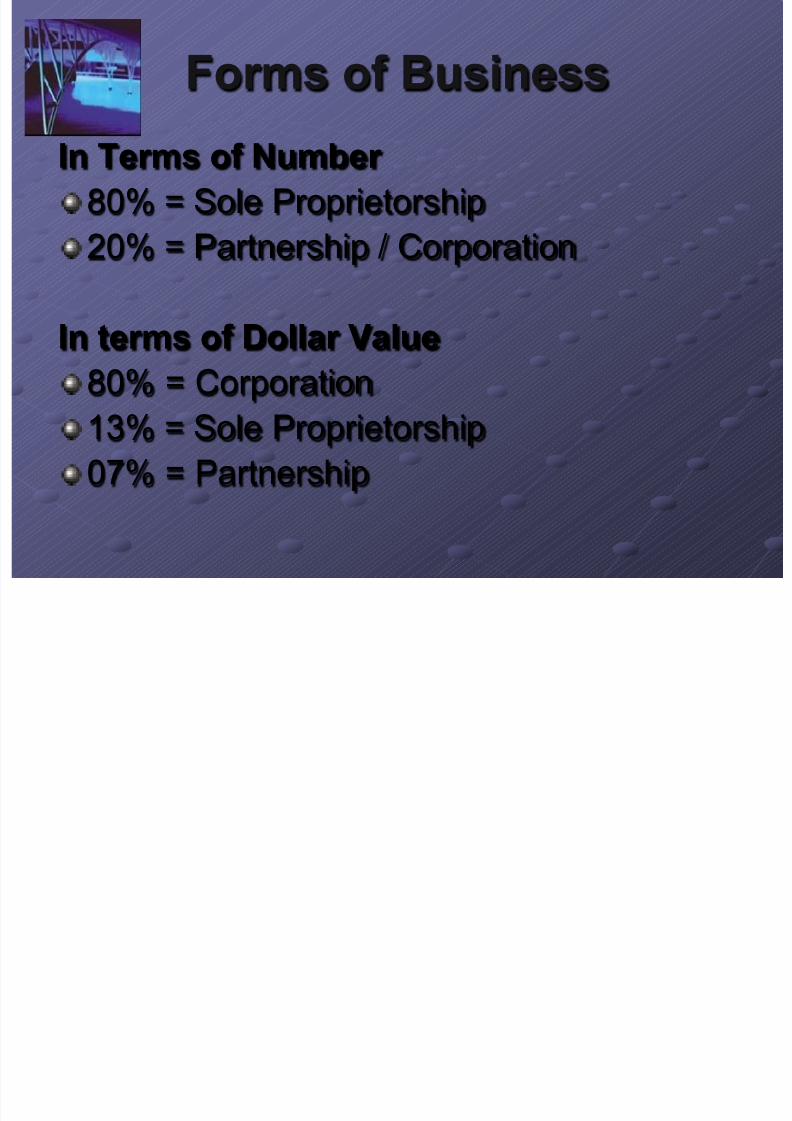

Forms of Business

In Terms of Number

80% = Sole Proprietorship

20% = Partnership / Corporation

In terms of Dollar Value

80% = Corporation

13% = Sole Proprietorship

07% = Partnership

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 12/50

Depreciation

Generally, profitable firms prefer to use an

accelerated method for tax reporting purposes.

Depreciation represents the

systematic allocation of the cost of

a capital asset over a period of timefor financial reporting purposes, tax

purposes, or both.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 13/50

Common Types of

Depreciation

Straight-line (SL)

Accelerated Types Double-Declining-Balance (DDB)

Modified Accelerated Cost Recovery System

(MACRS)

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 14/50

MACRS Schedule

Recovery Property Class

Year 3-Year 5-Year 7-Year

1 33.33% 20.00% 14.29%2 44.45 32.00 24.49

3 14.81 19.20 17.49

4 7.41 11.52 12.49

5 11.52 8.936 5.76 8.92

7 8.93

8 4.46

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 15/50

Financial Decision Making

Three major Decisions that a Financial

Manager has to take

The Investment Decision

The Financing DecisionThe Assets Management Decision

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 16/50

Investment Decisions

What is the optimal firm size?

What specific assets should be

acquired?

What assets (if any) should be reduced

or eliminated?

Most important of the three

decisions.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 17/50

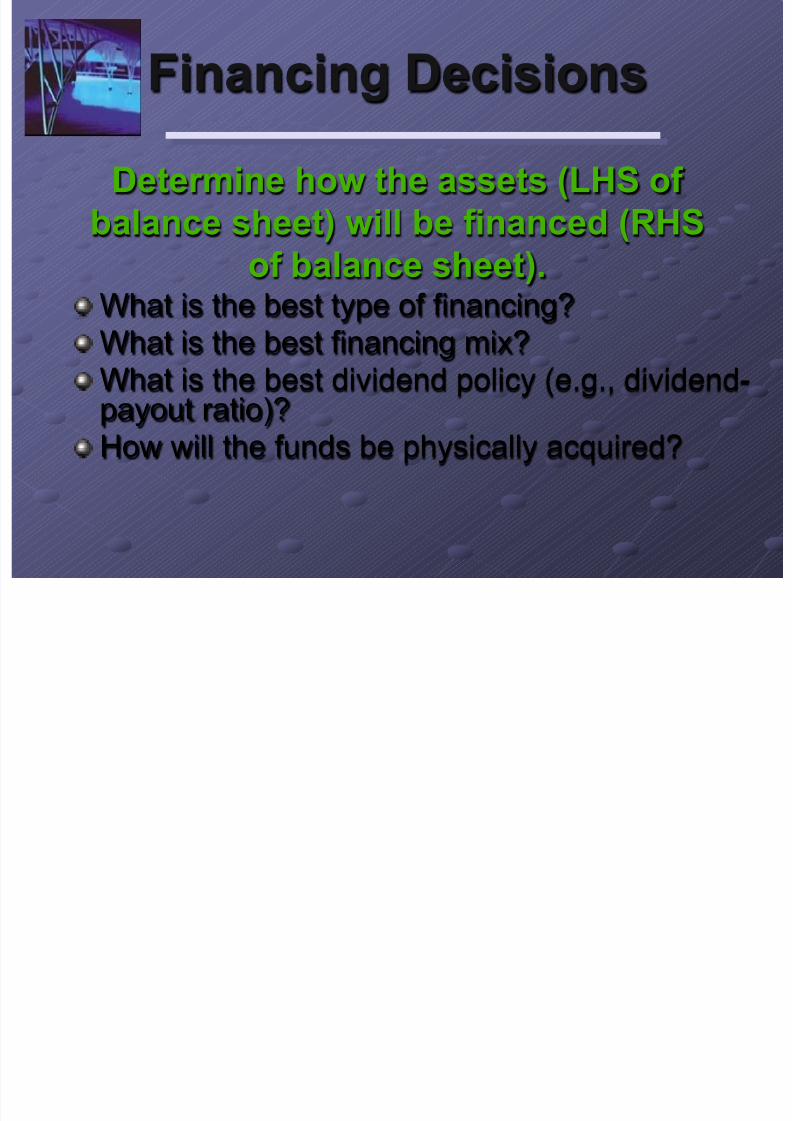

Financing Decisions

What is the best type of financing?

What is the best financing mix?

What is the best dividend policy (e.g., dividend-

payout ratio)?How will the funds be physically acquired?

Determine how the assets (LHS of

balance sheet) will be financed (RHS

of balance sheet).

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 18/50

Asset Management

Decisions

How do we manage existing assets efficiently ?

Financial Manager has varying degrees of

operating responsibility over assets.Greater emphasis on current asset management

than fixed asset management.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 19/50

What is Financial

Management?

Concerns the acquisition,

financing, and management of

assets with some overall goal in

mind.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 20/50

Finance Function Involves

Preparation of Cash Budget

Monitoring Performance

Evaluating Prospective InvestmentsRaising Funds

Forecasting and Planning

Coordination and ControlInteraction with Capital Market

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 21/50

Goals of Firm

Profit Maximization

Wealth Maximization

Preserve the Stakeholders Wealth

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 22/50

Profit Maximization

Issue common stock for profit maximization Example).

Ignores changes in the risk level of the firm.

Calls for a zero payout dividend policy.

A financial Manager should take those decision

which increase profits for the firms

Maximizing a firm’s earnings after taxes or Maximize

Earning Per Share (EPS).

Problems

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 23/50

Maximization of

Shareholder Wealth

Value creation occurs when we maximizethe share price for current shareholders.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 24/50

Stock Prices are Dependant on

following factors

Projected Earning Per Share

Timing of Earning Stream

Risk Involved

Use of Debt

Dividend Policy

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 25/50

Strengths of Shareholder

Wealth Maximization

Takes account of: current and future profits

and EPS; the timing, duration, and risk of

profits and EPS; dividend policy; and allother relevant factors.

Thus, share price serves as a barometer for

business performance.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 26/50

What companies say about

their corporate goal*

Cadbury: “governing objective is growth in shareownervalue”

Credit Suisse Group: “achieve high customer satisfaction,

maximize shareholder value and be an employer of choice” Dow Chemical Company: “maximize long-term shareholdervalue”

ExxonMobil: “long-term, sustainable shareholder value”

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 27/50

The Modern Corporation

There exists a SEPARATION between

owners and managers.

Modern Corporation

Shareholders Management

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 28/50

Role of Management

An agent is an individual authorized by

another person, called the principal, to

act in the latter’s behalf.

Management acts as an agent

for the owners (shareholders)

of the firm.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 29/50

Agency Theory

Agency Theory is a branch of

economics relating to the behavior ofprincipals and their agents.

Jensen and Meckling developed

a theory of the firm based onagency theory .

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 30/50

Agency Theory

Incentives include, stock options, perquisites, and bonuses.

Principals must provide incent ives

so that management acts in the

principals’ best interests and then

moni tor results.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 31/50

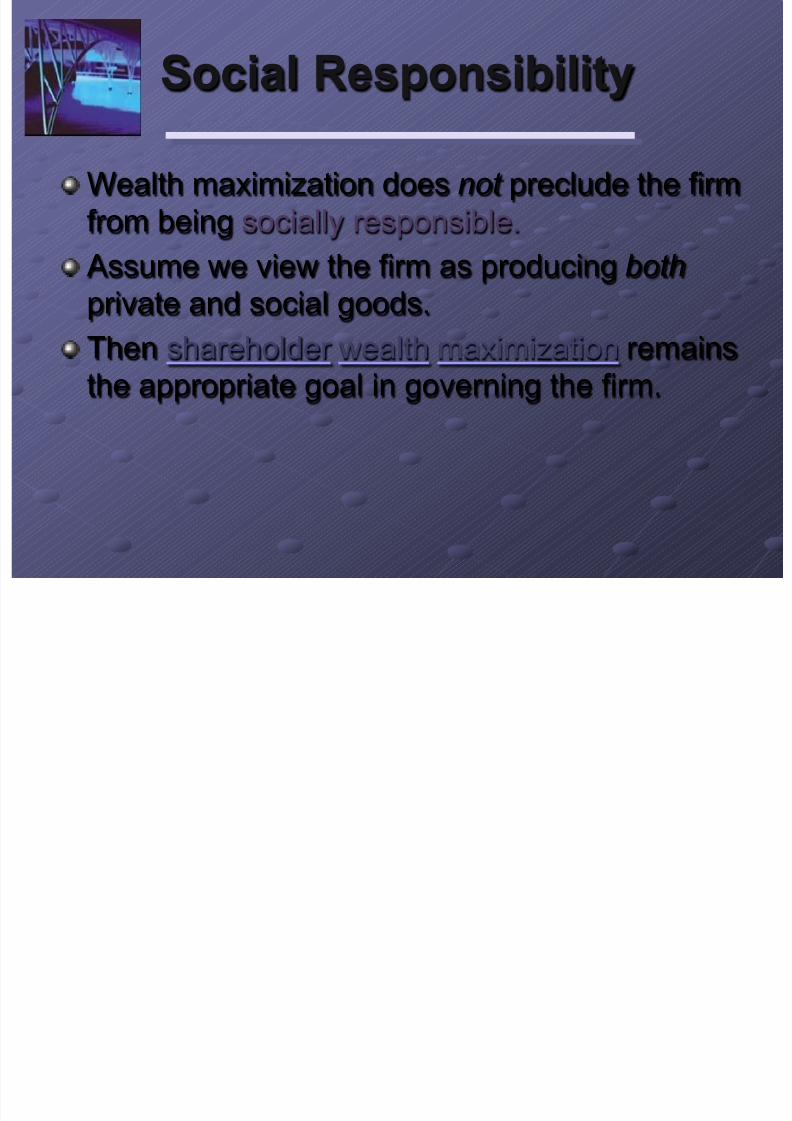

Social Responsibility

Wealth maximization does not preclude the firm

from being socially responsible.

Assume we view the firm as producing both private and social goods.

Then shareholder wealth maximization remains

the appropriate goal in governing the firm.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 32/50

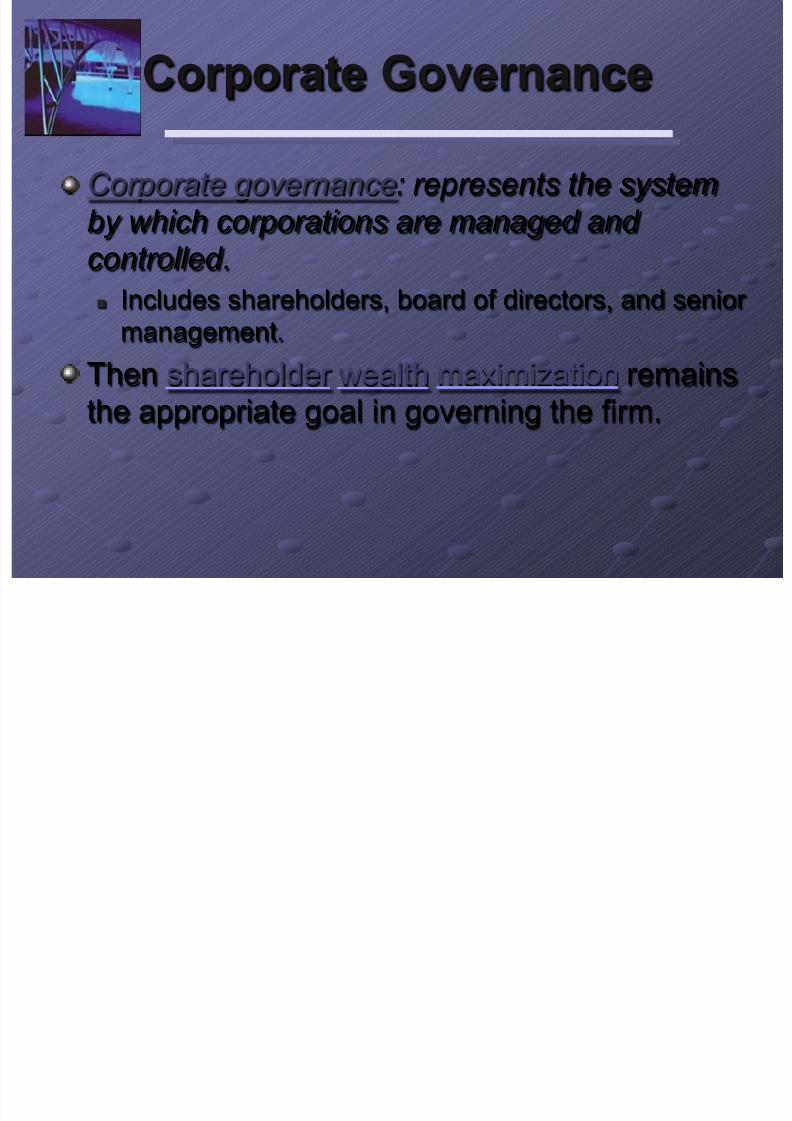

Corporate Governance

Corporate governance: represents the system

by which corporations are managed and

controlled .

Includes shareholders, board of directors, and senior

management.

Then shareholder wealth maximization remains

the appropriate goal in governing the firm.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 33/50

Board of Directors

Typical responsibilities: Set company-wide policy;

Advise the CEO and other senior executives; Hire, fire, and set the compensation of the CEO;

Review and approve strategy, significant

investments, and acquisitions; and

Oversee operating plans, capital budgets, andfinancial reports to common shareholders.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 34/50

Organization of the Financial

Management Function

Board of Directors

President

(Chief Executive Officer)

Vice President

Operations

Vice President

Marketing

VP of

Finance

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 35/50

TreasurerCapital Budgeting

Cash Management

Credit Management

Dividend DisbursementFin Analysis/Planning

Pension Management

Insurance/Risk Mngmt

Tax Analysis/Planning

Organization of the Financial

Management Function

VP of Finance

ControllerCost Accounting

Cost Management

Data Processing

General LedgerGovernment Reporting

Internal Control

Preparing Fin Stmts

Preparing Budgets

Preparing Forecasts

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 36/50

Financial Environment

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 37/50

Interest

No one lends money for free as manyfactors involved to get back the money

So, lenders want some compensation

called interest.Interest rate is expressed in percentage

Prevailing rate of Interest in any situation

is called nominal Interest rate.Real Rate of Interest

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 38/50

Interest Deductibility

Interest Expense is the interest paid onoutstanding debt and is tax deductible.

Cash Dividend is the cash distribution of

earnings to shareholders and is not a taxdeductible expense.

The after-tax cost of debt is:

(Interest Expense) X ( 1 - Tax Rate)Thus, debt financing has a tax advantage!

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 39/50

Financial Environment

Businesses interact continually with the financial

markets.

Financial Markets are composed of allinstitutions and procedures for bringing buyers

and sellers of financial instruments together.

The purpose of financial markets is to efficiently

allocate savings to ultimate users.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 40/50

Financial Markets

Moving of funds from saving sector toinvestment sector.

A forum where financial securities aresold.

May or may not have fixed location.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 41/50

Types of Financial Markets

Money Market: ST Securities, maturity up to one year.Player: State Bank, Commercial banks, Investmentbanks. (e.g. TB, Commercial papers). Issued by private& govt.

Funds used to meet temporary cash requirements.

Capital Market: LT Securities, maturity more than one year.(e.g. Bonds & Stocks). Funds used for LT investment.

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 42/50

Primary Market: When new security is sold first timeto general public & institutions. Deficit economic unitsdirectly sell new security to surplus economic units.

e.g. SB sold TB to banks (money market).e.g. first time selling of CS, PS, TFC, Bonds (capital

market)

Secondary Market: When issued securities are

traded. Thousands transaction occur.e.g. When TBs are traded among institution (money

market).

e.g. Trading of CS,TFC, Bonds in stock exchanges.

(capital market)

Types of Financial Markets

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 43/50

Stock Exchange: Just like KSE, ISE. The organizationthat facilitate trading of stocks & bonds amongst investors.Supervised, monitored and regulated by SECP.

OTC Market: have no fixed locations. Network of dealerswho maintain inventory of securities for resale purpose.

e.g. if you required some securities, you ask your broker whowill shop from those dealers having best price for you.

NASDAQ (National association of security dealersautomated quote system).

Dealers in OTC market are connected through computernetworks.

Types of Financial Markets

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 44/50

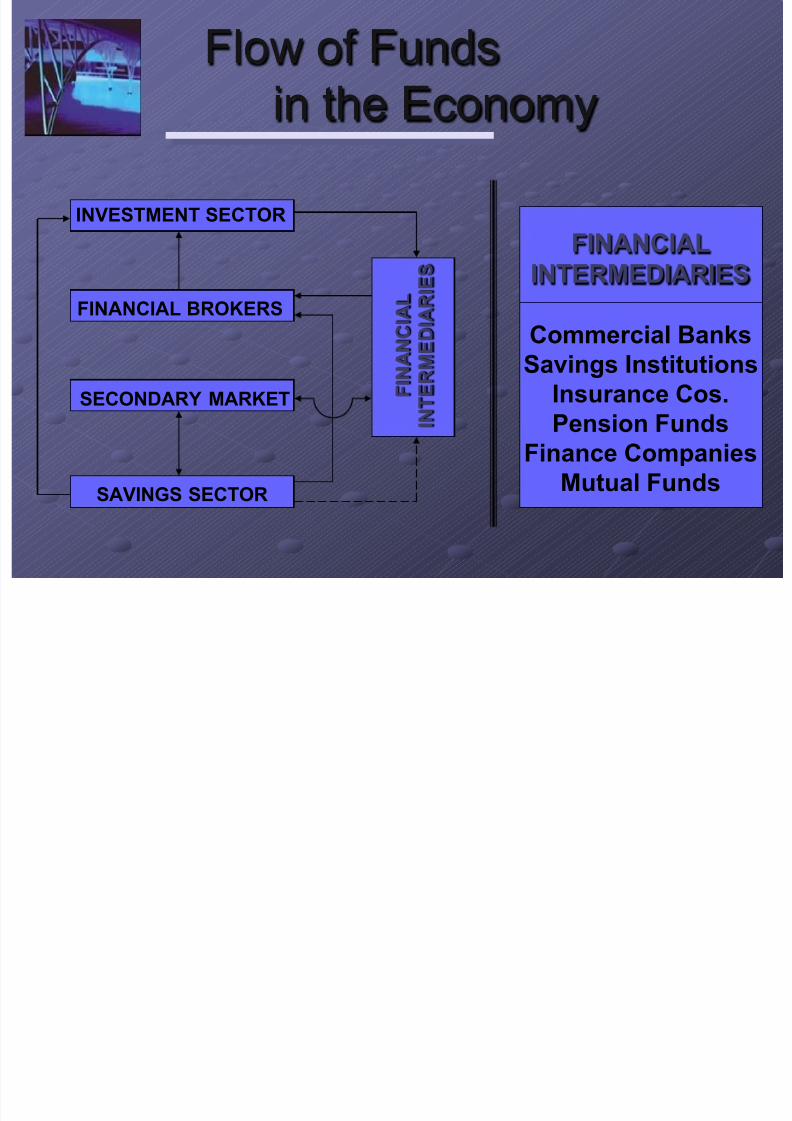

Flow of Funds

in the Economy

INVESTMENT SECTOR

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 45/50

Flow of Funds

in the Economy

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

INVESTMENT

SECTOR

Businesses

Government

Households

INVESTMENT SECTOR

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 46/50

Flow of Funds

in the Economy

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

SAVINGS

SECTOR

Households

Businesses

Government

INVESTMENT SECTOR

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 47/50

Flow of Funds

in the Economy

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

FINANCIAL

BROKERS

Investment

Bankers

Mortgage

Bankers

INVESTMENT SECTOR

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 48/50

Flow of Funds

in the Economy

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

FINANCIAL

INTERMEDIARIES

Commercial Banks

Savings Institutions

Insurance Cos.

Pension Funds

Finance Companies

Mutual Funds

INVESTMENT SECTOR

Fl f F d

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 49/50

Flow of Funds

in the Economy

F I N A N C I A L

I N

T E R M E D I A R I E S

SAVINGS SECTOR

FINANCIAL BROKERS

SECONDARY MARKET

SECONDARY

MARKET

Security

Exchanges

OTC

Market

INVESTMENT SECTOR

7/25/2019 Foundation and Financial Background

http://slidepdf.com/reader/full/foundation-and-financial-background 50/50

Allocation of Funds

In a rational world, the highest expected returns will

be offered only by those economic units with the

most promising investment opportunities.

Result: Savings tend to be allocated to the mostefficient uses.

Funds will flow to economic units that are

willing to provide the greatest expected

return (holding risk constant).

![Financial Administration [Rai Foundation Final]](https://img.pdfslide.net/doc/110x75/61b34c672d0d46602c1eb3ee/financial-administration-rai-foundation-final.jpg)