Embed Size (px)

Citation preview

Frank J. ChaloupkaChair, WHO Collaborating Centre on the

Economics of Tobacco & Tobacco ControlDistinguished Professor, UIC

The Economics of Tobacco Control – What Have We Learned and What Do

We Need to Know

Research Conference on Tobacco Control in AfricaCape Town, South Africa, 16 July, 2014

2

3

21

The Economics of Tobacco Control

Overview

What have we learned about the economics of tobacco control

What do we still need to know about the economics of tobacco control• Draws on WHO’s NCD research priorities

How can we apply the lessons learned to other public health problems

Tobacco Taxes, Prices, and Tobacco Use

6

Taxes, Prices and Tobacco Use Increases in tobacco taxes that increase

tobacco product prices:• Induce current users to try to quit

Many will be successful in long term

• Keep former users from restarting

• Prevent potential users from starting Particularly effective in preventing transition from

experimentation to regular use

• Reduce consumption among those who continue to use

• Lead to other changes in tobacco use behavior, including substitution to cheaper products or brands, changes in buying behavior, and compensation

7

Taxes, Prices and Tobacco Use

2002 2003 2004 2005 2006 2007 2008 2009 20102,950.0

3,150.0

3,350.0

3,550.0

3,750.0

3,950.0

13.3

13.8

14.3

14.8

15.3

15.8

16.3

16.8

17.3

Cigarette Prices and Cigarette Consumption, Guatemala, Inflation Adjusted, 2002-2010

Consumption Price

Consum

pti

on (

million s

ticks)

Pri

ce (

infl

ati

on a

dju

ste

d,

2010)

8

Source: IARC Handbook 14, 2011

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Midpoint of period over which study was performed

Shor

t-run

pric

e el

astic

ity o

f dem

and

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

1970 1975 1980 1985 1990 1995 2000 2005

Midpoint of period over which study performed

Shor

t-run

pric

e elas

ticity

of d

eman

d

High-Income, Non-US Low/Middle-Income

Elasticity EstimatesAggregate Demand Studies

9

2006 2007 2008 2009 2010 2011 2012 201311

12

13

14

15

16

3.4

3.9

4.4

4.9

5.4

Adult Smoking Prevalence and Cigarette PriceBrazil, Inflation Adjusted, 2006-2013

Adult

Sm

okin

g P

revale

ence

Pri

ce p

er

Pack,

2013 B

RL

Adult Prevalence & Price, Brazil

Sources: Ministry of Health, Brazil; EIU; World Bank

100

50,000

100,000

150,000

200,000

Monthly Quit Line Calls, United States11/04-11/09

4/1/09 Federal Tax Increase

1/1/08 WI Tax Increase

Source: BRFSS, Tax Burden on Tobacco, 2010, and author’s calculations

350 400 450 500 550 600 650 700 750 800 85045

50

55

60

65

70

f(x) = 0.0283499138817126 x + 43.0832236078183R² = 0.371042346639463

Cigarette Prices and CessationUS States & DC, 2009

Average price (in cents)

% E

ver

Sm

okers

Who H

ave Q

uit

12

Source: MTF, Tax Burden on Tobacco, 2011, and author’s calculations

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007$2.50

$3.25

$4.00

$4.75

$5.50

6

11

16

21

26

31

36

Cigarette Price and Youth Smoking Prevalence, United States, 1991-2010

Cigarette Price 12th grade prevalence 10th grade prevalence 8th grade prevalence

Year

Pric

e pe

r pa

ck (

8/11

dol

lars

)

Sm

okin

g P

reva

lenc

e

Taxes, Prices and Health:France, 1980-2010

Source: Jha, et al., in progress

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

1980 1985 1990 1995 2000 2005 2010

Year

Nu

mb

er/

ad

ult

/da

y a

nd

de

ath

ra

tes

50

100

150

200

250

300

Pri

ce

(%

re

lati

ve

to

19

80

)

Lung cancer death rates per 100,000 (divided by four): men age 35-44

Relative price

# cigarettes/adult/day

15

Source: Chaloupka, et al., in progress

Qatar

Luxe

mbo

urg

Switz

erla

nd

Japa

n

Denm

ark

Israe

l

Swed

en

Nethe

rland

s

Finla

ndIta

ly

Greec

e

Spai

n

Hunga

ry

Czech

Rep

ublic

Portu

gal

UKIra

n

Colom

bia

Brazil

China

Tuni

sia

Thai

land

Para

guay

Indo

nesia

Vietn

am Indi

a

Cote

d'Iv

oire

Papu

a New

Gui

nea

Kenya

0%

5%

10%

15%

20%

25%

Relative Income Price for Cigarettes, Selected Countries, 2011

Rela

tive I

ncom

e P

rice (

Perc

enta

ge o

f A

nnual per

capit

a G

DP

requir

ed

to b

uy 1

00 p

acks o

f cig

are

ttes)

16

Source: Chaloupka, et al., in progress

Saudi A

rabia

Denm

ark

Sw

eden

Luxem

bourg

UA

E

Finla

nd

Belg

ium

Gre

ece

Hungary

Canada

Isra

el

Neth

erl

ands

Sw

itze

rland

Italy US

Spain

Chin

a

Mexic

o

Tunis

ia

Chile

South

Afr

ica

Egypt

Para

guay

Indonesi

a

India

Cote

d'Ivoir

e

Papua N

ew

Guin

ea

Kenya

-90%

-70%

-50%

-30%

-10%

10%

30%

50%

70%

90%

110%

Percentage Change in the Relative Income Price of Cigarettes, Selected

Countries, 1996-2011

Perc

enta

ge C

hange in t

he R

ela

tive I

ncom

e P

rice,

1996-2

011

17

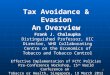

Affordability & Sales, Brazil

Sources: Euromonitor; EIU; World Bank

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 201375,000

77,000

79,000

81,000

83,000

85,000

87,000

89,000

91,000

93,000

95,000

1.8%

1.9%

2.0%

2.1%

2.2%

2.3%

2.4%

2.5%

Cigarette Affordability and Sales, Brazil, 2003-2013

Sales, Million Sticks Affordability

Cig

are

tte S

ale

s,

Million S

ticks

Aff

ord

abilit

y -

% o

f P

er

Capit

a I

ncom

e t

o b

uy 1

00 P

acks

18

Taxes, Prices and Tobacco Use What do we need to know?

• More country-specific evidence from LMICs Lack of overall price, income elasticity of demand

estimates for most low and middle-income countries Even less known about differential impact of price by

age, socioeconomic status, gender, and other factors Limited evidence from LMICs on impact of taxes and

prices on transitions in tobacco use• Non-linearities in effects of taxes/prices

Changes in elasticity over time, as taxes & prices increase, as incomes rise, etc.

Differential impact of incremental vs. large tax and price increases

Interactions between tax/price and tobacco control policies

19

Taxes, Prices and Tobacco Use

What do we need to know?

• More evidence on the demand for other tobacco products Own price and income elasticities Cross-price elasticities Changes in elasticities in response to new nicotine

products• More evidence on interactions between tobacco

use and other health-related behaviors Alcohol, illicit drug use Diet, activity and obesity

Disposable Electronic CigarettesSales Volume and Price: Total US 2010 -

2012

2010 Q1

2010 Q2

2010 Q3

2010 Q4

2011 Q1

2011 Q2

2011 Q3

2011 Q4

2012 Q1

2012 Q2

2012 Q3

2012 Q4

8

10

12

14

16

18

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

Real Sales Price Sales Volume

Sale

s P

rice (

in r

eal 2011 Q

4 d

ollars

)

Sale

s V

olu

me (

thou

san

ds o

f p

ieces)

Reusable Electronic Cigarettes Sale Volume and Price: Total US 2010 - 2012

2010 Q1

2010 Q2

2010 Q3

2010 Q4

2011 Q1

2011 Q2

2011 Q3

2011 Q4

2012 Q1

2012 Q2

2012 Q3

2012 Q4

10

15

20

25

30

35

40

-

100,000

200,000

300,000

400,000

500,000

600,000

Real Sales Price Sales Volume

Sale

s P

rice (

in r

eal 2011 Q

4 d

ollars

)

Sale

s V

olu

me (

thou

san

ds o

f p

ieces)

Importance of Tobacco Tax Structure

23

Types of Taxes Variety of tobacco taxes

• Taxes on value of production• Customs duties on tobacco leaf, tobacco products

imports and/or exports• Sales taxes/Value added taxes• Implicit taxes when government monopolizes

production and/or distribution• Excise taxes (or similar taxes)

Many of these are applied to variety of agricultural and/or consumer goods and services

Excise taxes are of most interest given specificity to tobacco products

24

Types of Taxes Excise Taxes

• Two types of excises Specific Taxes: excises based on quantity or weight

(e.g. tax per pack of 20 cigarettes) Ad Valorem taxes: excises based on value of

products (e.g. a specific percentage of manufacturer’s prices for tobacco products)

• Variety of tax systems/structures Uniform systems Mixed systems Tiered systems

Excise systems on cigarettes

Source: WHO 2013

Number of countries,

2012

186 Total covered

56 Specific excise only

50 Ad valorem excise only

60 Mixture of both excises

20 No Excise

Excise systems on cigarettes

Source: WHO 2013

# of countries Country Base of tiers

6 Bangladesh, Mozambique, Philippines, Belarus,

Indonesia, Pakistan Retail price

2 Burkina Faso, Senegal High, standard and low end

cigarettes

1 China Producer price

1 Indonesia Production volume

11 Armenia, Belarus, India, Nepal, Georgia,

Kazakhstan, Kyrgyzstan, Moldova, Papua New Guinea, Tajikistan, Ukraine

filter/non filter

Type

3 Indonesia, India, Philippines hand/machine made

2 Indonesia, Myanmar kretek/white

cigarette, cheerot/cigarette

2 Andorra, Algeria Tobacco content (dark/blonde or

dark/light)

3 Brazil, Mozambique, Uganda soft/hard Packaging

4 India, Nepal, Hong Kong, Sri Lanka Cigarette length

2 Andorra, Uzbekistan Trade (domestic/imported)

2 Belize, New Zealand Weight (tobacco content in

cigarette)

1 Fiji Leaf content (domestic/imported)

Average price and excise tax by tax structure, 2012

Source: WHO 2013

Average excise PPP Average price PPP Excise tax structure

1.57 3.73 Specific only

1.28 2.50 Ad valorem only

1.32 2.86 Mixed system

1.67 3.84 Relying more on specific

1.11 2.29 Relying more on ad

valorem

- 1.70 No excise

28

Cigarette Tax Structure & PricesSelected Countries, 2009-10

Source: Chaloupka, et al., 2014

Roman

ia

Pola

nd

Unite

d St

ates

Thai

land

Indi

a

Ukrai

ne

Mex

ico

Urugu

ay

Egyp

t

China

Bangl

ades

h

Russia

n Fe

dera

tion

Philip

pine

s

Vietn

am

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Sta

ndard

Devia

tion,

Pri

ces o

f Top 5

Bra

nds

29

WHO’s Best Practices in Tobacco Taxation

Simpler is better

• Complex tax structures more difficult to administer

• Greater opportunities for tax evasion and tax avoidance under complex tax structures

• Where existing structure is more complex, simplify over time with goal of achieving single uniform tax

Simplifying the Excise Tax System: Egypt

2009: Tiered specific

Net of tax price per pack (P.T.)

GST/pack (P.T.)

Less than 65 108

More than 65 to 73 112

More than 73 to 84 125

More than 84 to 95 140

More than 95 to 106

153

More than 106 to 300

175

More than 300 to 425

315

More than 425 325

Mixed system 2010 cigarette excise

system: mixture of ad valorem (40% of retail price) and specific (EP 1.25/pack)

2011 cigarette excise system: mixture of ad valorem (50% of retail price) and specific (EP 1.35/pack)

Source: WHO and Ministry of Finance, Egypt.

Simplifying the Excise Tax System: Indonesia

Production tier Production capacity2009 2010 2011

Machine-made kreteks SKM HJE (Rp/stick) HJE (Rp/stick) HJE (Rp/stick)660- 290 310 325 660- 355 669- 375630-660 280 300 315 630-660 345 631-669 355600-630 260 280 295 600-630 325430- 210 230 245 430- 270 549- 285380-430 175 195 210 374-430 235 440-549 245374-380 135 155 170

Hand-made kreteks SKT590- 200 215 590- 255 749- 275550-590 150 165 520-590 195 550-749 205520-550 130 145379- 90 105 125 130349-379 80 95 115 120336-349 75 90 105 110

III > 6 million to 500 million 234- 40 65 75 250- 80White cigarettes SPM

550- 290 310 325 365 680- 380430-550 230 275 295 365375-430 185 225 245 365300- 170 200 215 235 444- 245254-300 135 165 175 190 345-444 195217-254 80 105 110 125

Specific excise / stick (Rp)2012 2013

II> 500 million to 2 billion

I > 2 billion

II > 500 million to 2 billion

I > 2 billion

II > 500 million to 2 billion

I > 2 billion

Source: WHO and Ministry of Finance, Indonesia.

32

WHO’s Best Practices in Tobacco Taxation

Rely more on specific tobacco excises as the share of total excises in prices increases• Greater public health impact of specific excises

given reduced opportunities for switching down in response to tax/price increases

• Sends clear message that all brands are equally harmful

• Produces more stable, higher revenues stream less susceptible to industry price manipulation

Increasing Emphasis on Specific Excise Tax: Mexico

2009:• Ad valorem tax of 150% of pre-tax price to retailer

November 2009:• Added specific tax of 0.80 pesos/pack in 2010• Increased specific tax by 0.40 pesos each year

through 2013 (2.00 pesos/pack)

2010 legislation, effective 2011:• Increased ad valorem tax to 160% of pre-tax price• Raised specific tax immediately to 7 pesos/pack

Source: Cherukapalli, 2013; Waters, et al., 2010

Mexico

Source: Tobacco-Free Kids, 2012

Adoption of Uniform Specific Excise Tax: Philippines

Source: WHO and Ministry of Finance, Philippines.

Net retail price per pack (excluding VAT and excise) 2007 2008 2009 2010 2011 2012

More than Ps. 10 26.1 26.1 27.2 27.2 28.3 28.3

Ps. 6.50 - Ps. 10 10.9 10.9 11.4 11.4 12 12

Ps. 5 - Ps. 6.50 6.7 6.7 7.1 7.1 7.6 7.6

Below Ps. 5 2.2 2.2 2.5 2.5 2.7 2.7

Net retail price per pack (excluding VAT and excise)

2013 2014 2015 2016 2017 2018

More than Ps. 11.5025 27 28 29

Ps. 11.50 and below12 17 21 25

30Annual

4% increase

Cigarette (machine packed) excise tax rate

SIN TAX REFORM ACT, 2012

36

WHO “Best Practices” for Tobacco Excise Taxes

Adopt comparable taxes and tax increases on all tobacco products

• Maximizes public health impact of tobacco tax increases by minimizing opportunities for substitution

37

WHO’s Best Practices in Tobacco Taxation

Set tobacco excise tax levels so that they account for at least 70 percent of the retail prices for tobacco products

• Update of World Bank ‘yardstick’ of any taxes accounting for 2/3 to 4/5 of retail prices

• Well above where most countries are currently

• Further increases in countries that do reach this target

Average Price of the Most Sold Brand & Excise Tax per pack, and Total Tax Share

By Income Group 2012

Source: WHO 2013

High income Upper middle Lower middle Low income China All

5.82

3.29

2.67

1.65

1.18

3.00 3.12

1.57

0.97 0.61

0.31

1.35

65.90%

63.34%

48.72% 50.31%

40.76%

58.40%

Retail price, PPP Excise tax PPP Total tax share (%)

PP

P

39

Tobacco Tax Structure

What do we need to know?

• More evidence on the impact of tobacco tax structure on prices, tobacco use Relative prices within/across product categories Substitution between brands/products

• Evidence on industry responses to alternative tax structures and changes in tax structures Pricing strategies Product characteristics, product mix

• Optimal tax structure for harm minimization Differential taxes based on relative risk?

Globalization of the Tobacco Industry

41

Globalization of Tobacco Industry

• Opening of markets through bilateral, regional, and global trade agreements

• Loosening of restrictions on foreign direct investment

• Privatization of government run tobacco companies

A few significant exceptions

• Consolidation among multinational tobacco companies

42

Trade in Tobacco Products

Impact of freer trade on tobacco use

• Growing evidence that reduction in barriers to trade increase tobacco use

• Impact greater on lower income countries

• Results from increased competition, lower prices, and increased use of sophisticated marketing strategies by multinational tobacco companies

Source: Chaloupka & Laixuthai, 1996; Taylor, Chaloupka, Guindon & Corbett, 2000; Perucic, et al., in progress

43

Direct Investment & Privatization Opening of markets has also resulted in increased

openness to direct investment

• Investment in new production facilities/capacity owned and operated by multinational tobacco companies

By far the most widespread Facilitated by Bilateral Investment Treaties

• Privatization of government owned tobacco companies for example, Turkish TEKEL acquired by BAT in 2008 after being

on the market for many years) Partial privatization of Egypt Tobacco Company (government

still retains controlling interest)

• Joint ventures between local monopoly and multinational tobacco companies

For example, PMI and China National Tobacco company

44

Direct Investment & Privatization Can be good or bad for public health – depends

on how it’s done; “best practices” for public health

• Agreements with multinational tobacco companies can inhibit government’s ability to adopt strong tobacco control policies

E.g. experiences in former Soviet republics where agreements with MTCs prevented significant tax increases and strong tobacco control measures

• Can eliminate conflict of interest between government tobacco production/distribution and tobacco control

E.g. Turkey where sale of TEKEL followed by aggressive implementation of FCTC, including significant regular tax increases, comprehensive smoke-free policy, comprehensive TAPS ban, and more

Source, Yurekli, Shin &Chaloupka, in press

45

Mergers & Acquisitions Considerable consolidation among tobacco

companies

• Acquisition of local cigarette companies by MTCs Acquisition of popular local brands For example, BAT acquisition of Protabaco - 2nd largest

Colombian company - in 2011

• Mergers between local tobacco companies and MTCs For example, Philip Morris International and Fortune Tobacco

Company merge in 2010, creating Philip Morris Fortune Tobacco Company that nearly monopolizes Philippine cigarette market

• Acquisition of one MTC by another MTC For example, Imperial Tobacco Group’s acquisition of Altadis in

2008

46

Mergers & Acquisitions Has led to consolidation/centralization of production

in regional production hubs

• Capitalize on significant economies of scale in production of tobacco products

• Take advantage of regional trade agreements that greatly reduce or eliminate barriers to trade in tobacco products

• Generally located in: Large consuming country within region Country where labor, tobacco leaf, other costs are low

• Case study - Central America BAT Caribbean and Central America hub in Honduras supplies

others in region Philip Morris International subsidiary Tabacalera

Centroamericana in Guatemala does the same Together, 2 companies control nearly all of the market

Cigarette Company Market Shares

Source: Maxwell Tobacco Fact Book, various years; Euromonitor, 2013; note: PMI includes Philip Morris International and Altria Group Inc.

1985-2011, Selected Years

1985 1990 1995 2000 2006 20110%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CNTC PMI BAT JTI ITG Others

48

Mergers & Acquisitions

Increasingly, consolidation across products

• Altria, US’ largest cigarette company, acquisition of US Smokeless Tobacco Company in 2008, largest smokeless company in the US

• Lorillard Inc. acquisition of Blu, a leading e-cigarette company

• JTI’s acquisition of Gryson, a leading RYO/MYO manufacturer in Western Europe

• PMI’s purchase of Jed Rose’s patent for a nicotine inhaler

49

Mergers & Acquisitions Combined with development and marketing

of new products

• Altria, RJR and others develop and market variety of dissolvable products, extending brands across products

• 2011 - BAT creates Nicoventures to develop reduced risk tobacco products, other nicotine delivery products

• 2012 - Altria markets Verve – a non-tobacco, nicotine lozenge

• 2012 – Swisher launches e-cigarettes, e-cigars

50

Marlboro

51

Camel

52

53

Globalization and Tobacco Control

Increasing challenges to national tobacco control policies under trade and investment agreements• Investor-state disputes being brought under Bilateral

Investment Treaties E.g Philip Morris Asia v. Australia under bilateral investment

treaty between Hong Kong & Australia; PMI v. Uruguay under bilateral investment treaty between Switzerland & Uruguay

• State-state disputes being brought in World Trade Organization

E.g. Indonesia v. United States; multiple countries v. Australia

• Challenges in national courts E.g. Australia, United States

54

Trade Disputes US-Thailand and GATT/WTO

• After relatively easy success in Japan, Taiwan, and South Korea, US tried to open Thai cigarette markets

• Thai government fought back

• Key issues: Near total ban on cigarette imports Differential taxes on foreign and domestically produced

cigarettes Comprehensive ban on advertising and promotion

• Dispute brought before GATT in 1990 Ban, differential taxes are violations of agreement Ad/promo ban is allowable Decision depends on whether or not measures are applied

equally to domestic and foreign products

Source: Chaloupka & Laixuthai, 1996

55

Trade Disputes US-Thailand and GATT/WTO

• Article XX of GATT allows for protection of public health over interests in trade:

• “Subject to the requirement that such measures are not applied in a manner which would constitute a means of arbitrary and unjustifiable discrimination between countries where the same conditions prevail, or a disguised restriction on international trade, nothing in this Agreement shall be construed to prevent the adoption or enforcement by any contracting party of measures…necessary to protect human ….health (or) necessary to secure compliance with the laws or regulations which are not inconsistent with the provisions of this Agreement”

Source: Chaloupka & Laixuthai, 1996

56

Trade Disputes Trade dispute between Indonesia and US over

clove cigarettes

• US FDA banned flavored cigarettes (except menthol) under the US Family Smoking Prevention and Control Act

• Indonesia leading exporter of clove cigarettes (kreteks) brought challenge saying ban is discriminatory and unnecessary

• Sept. 2011 – WTO rules that the ban is discriminatory, but not unnecessary given evidence that availability of flavored cigarettes contributes to youth smoking uptake

Calls on US to bring policy into compliance with trade agreements

US appealed, lost; unclear how it will comply

57

Trade Disputes Norway’s ban on retail tobacco product displays

• Challenged by Philip Morris Norway arguing that display ban violated Article 11 of European Economic Area by ‘hindering the free movement of goods’

• European Free Trade Agreement court ruled that the ban effectively restricted imports, but left it to Norway’s court to determine whether or not the public health objective was likely to be met and could not be achieved by less trade restrictive measure

• September 14, 2012, Oslo district court upheld ban:“there exist no other measures that will have an effect

equivalent to that of the Display Ban.” “Absence of visible tobacco products in shops will be vital

both in terms of the absence of advertising effect, and as a part of de-normalisation.”

59

Trade and Investment Disputes Australia’s Plain Packaging Policy

Announced April 29, 2010 Legislation introduced April 7, 2011 Passed House August 24, 2011, Senate November 2,

2011 Phased in by December 1, 2012 Prohibits use of trade marks, symbols, graphics or

images on pack Allows brand, business/company name, variant

name in standard font/position

Coupled with other provisions Graphic warnings expanded (75% front, 90% back) Pack/cigarette specifications Similar details for other tobacco products

60

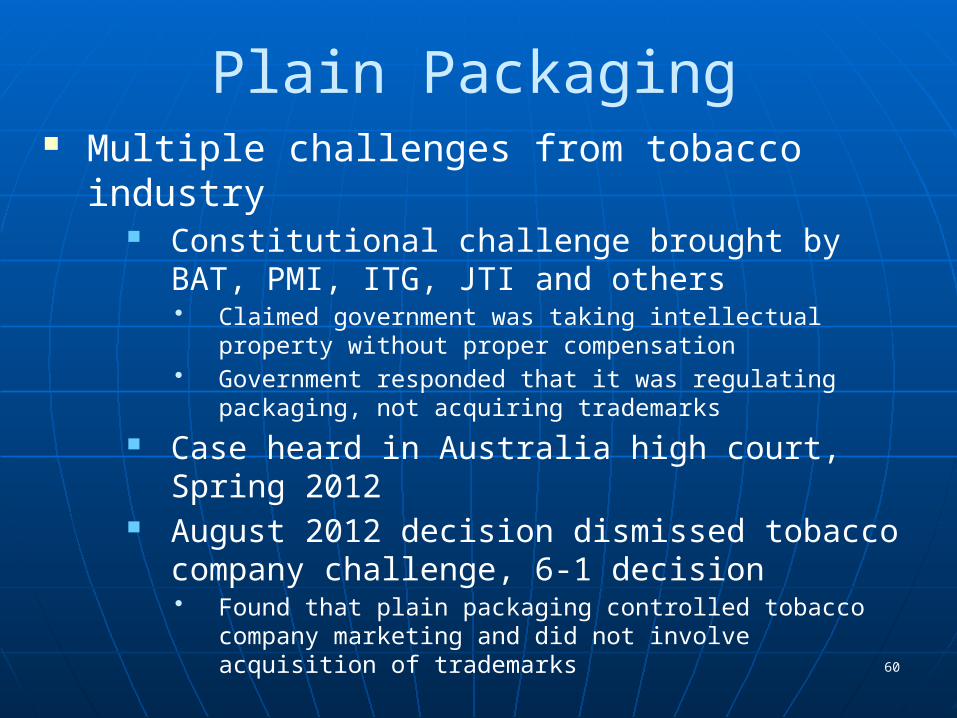

Plain Packaging Multiple challenges from tobacco industry

Constitutional challenge brought by BAT, PMI, ITG, JTI and others• Claimed government was taking intellectual property

without proper compensation• Government responded that it was regulating

packaging, not acquiring trademarks

Case heard in Australia high court, Spring 2012

August 2012 decision dismissed tobacco company challenge, 6-1 decision• Found that plain packaging controlled tobacco company

marketing and did not involve acquisition of trademarks

61

Plain Packaging Multiple challenges from tobacco industry

Pending WTO challenges brought by Ukraine, Indonesia, Dominican Republic, Honduras and Cuba• Trade-Related aspects of Intellectual Property

Rights (TRIPS) Agreement• Technical Barriers to Trade (TBT) Agreement• Harm to domestic industry due to

commoditization of product, falling prices, and increased illicit trade

1993 Hong Kong – Australia Bilateral Investment Treaty challenge• PM-Asia acquisition of PM-Australia in Feb. 2011

62

Investment Disputes PMI 2012 challenge to Uruguay tobacco control

law under bilateral investment treaty between Uruguay and Switzerland

• Three regulations originally at issue: Health warnings covering 80% of cigarette pack “Repulsive and shocking” images used in graphic

warnings (subsequently dropped) “Single presentation” - permission to sell only one

variation per brand (current focus)• PMI argues that these “deprive the company of its

ability to use its legally-protected trademarks and brands”

• Uruguay argues that these are necessary to protect public health

63

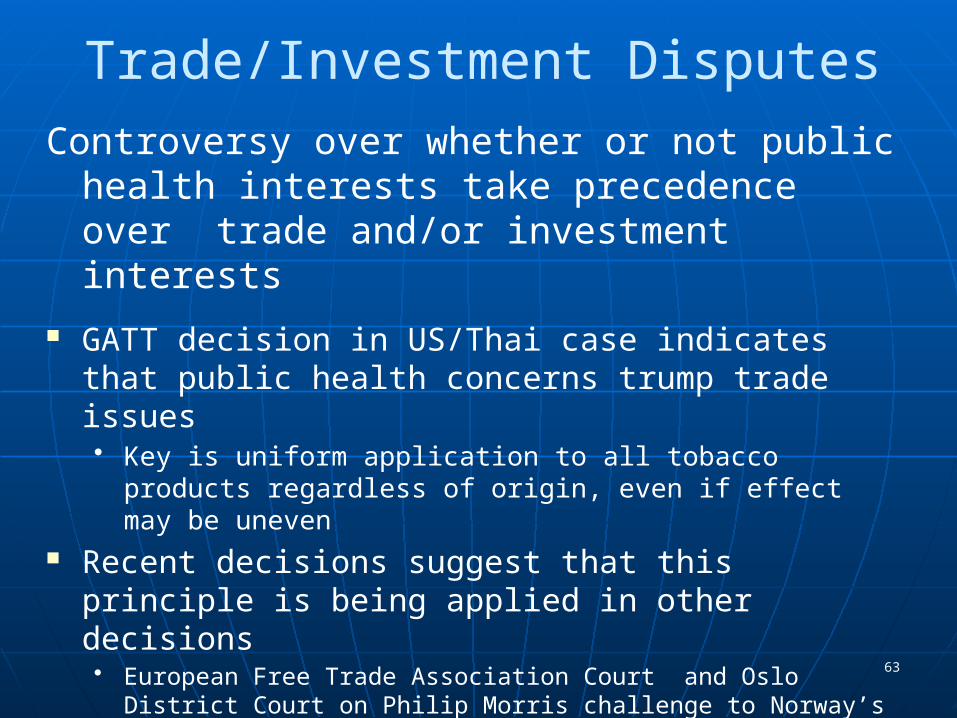

Trade/Investment Disputes

Controversy over whether or not public health interests take precedence over trade and/or investment interests

GATT decision in US/Thai case indicates that public health concerns trump trade issues• Key is uniform application to all tobacco products

regardless of origin, even if effect may be uneven Recent decisions suggest that this principle is

being applied in other decisions• European Free Trade Association Court and Oslo District Court

on Philip Morris challenge to Norway’s tobacco products display ban

• WTO panel decision in Indonesia case• Australia High Court decision on industry challenges to plain

packaging legislation

64

Globalization

What do we need to know?

• Impact of globalization on tobacco use and its consequences Pricing and marketing strategies Product innovation/diffusion

• Research to counter industry challenges to national tobacco control policies under bilateral, regional, and global agreements

• Research on the effects of globalization on tobacco control policies Political economy of tobacco control policies Consequences of delayed, weakened policies

Oppositional Arguments

66

Tobacco Taxes & Tax Revenues

Myth: increases in tobacco taxes will lead to lower tobacco tax revenues given reductions in tobacco use

67

Tobacco Taxes & Tax Revenues

Fact: tobacco tax increases lead to increased tax revenues

• Tobacco taxes account for a fraction of tobacco prices

Increase in tax leads to smaller increase in price

• Reductions in tobacco use less than proportionate to price increase

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

0

5

10

15

20

25

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Industry Price Excise Tax VAT Excise Tax Revenues

Rand p

er

Pack

Tax R

evenues,

Million R

and

South AfricaTaxes, Prices, and Tax Revenues, 1970-2012

Inflation Adjusted

69

Tobacco Taxes & the Poor

Myth: tobacco tax increases harm the poor

70

Tobacco Taxes & the Poor

Fact: tobacco use harms the poor

Cycle of tobacco and

poverty

Poor men

smoke

Forgone income 1: More money spent Less money spent on tobacco: on education, nutrition, etc High opportunity cost

Breadwinner gets

sick due to tobacco use

Forgone income 2:

Treatment cost &Lost working days &

income

Forgone income 3:

Breadwinner dies prematurely

Family falls into poverty

Tobacco and Poverty

Source: Yurekli, 2007

72

Poverty and Tobacco Use

Burdens of poverty are compounded by tobacco use• Responsible for impoverishment of over 50

million in China and over 15 million in India

• Crowding out of other spending:• Bangladesh: tobacco money spent

equivalent to:• Males = 1402 calories of rice per day• Females = 770 calories of rice per day

Sources: Hu, et al., 2008; John, et al., 2011; Efroymson, et al., 2001

73

Tobacco Taxes & the Poor

Fact: tobacco tax increases can be progressive• Tobacco use among low-income

populations more responsive to price

Pay smaller share of tax increase Receive greater share of health

benefits from higher tax

Who Pays& Who BenefitsTurkey, 25% Tax Increase

Source: Adapted from Önder & Yürekli, 2014

-36%

-31%

-26%

-21%

-16%

-11%

-6%

-1%

4%

9%

-35.3%

-20.4%-18.5%

-2.2%

8.5%9.7%

Change in Consumption Change in Taxes Paid

Source: Chaloupka et al., in progress; assumes higher income smokers smoke more expensive brands

Who Pays& Who Benefits Impact of Federal Tax Increase, U.S., 2009

<poverty line 1-2* poverty line >2* poverty line0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

11.9%

20.7%

67.4%

46.3%

29.5%

24.2%

Share of Tax Increase Share of Reduced Deaths

Impact on the Poor• Also need to consider overall fiscal system

Key issue is what’s done with the revenues generated by the tax

Greater public support for tobacco tax increases when revenues are used for tobacco control and/or other health programs

Net financial impact on low income households can be positive when taxes are used to support programs targeting the poor

Concerns about regressivity offset by use of revenues for programs directed to poor

77

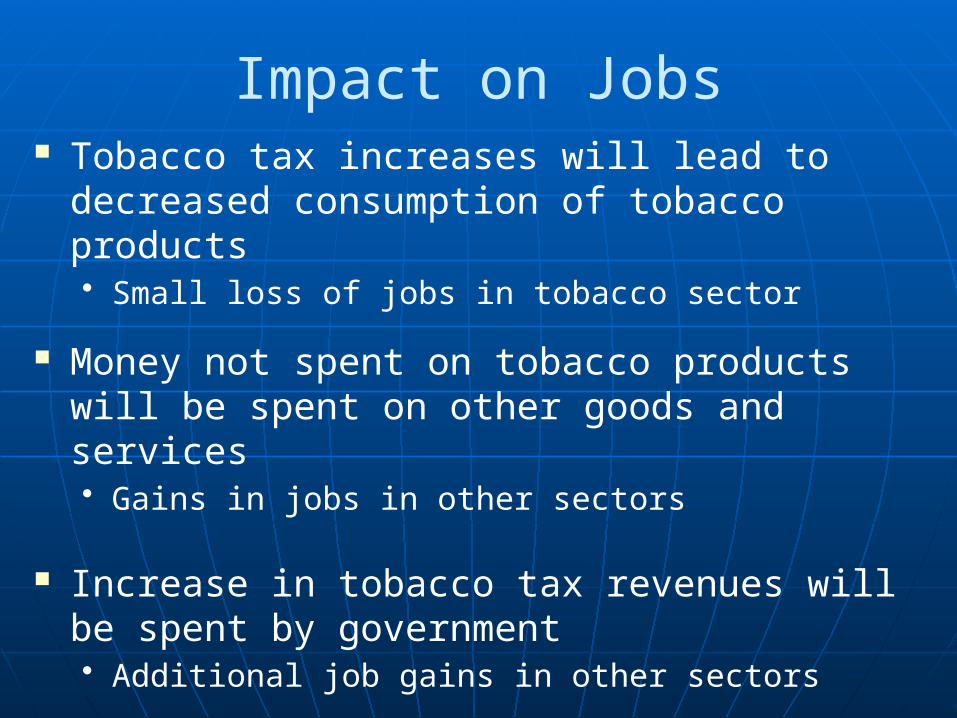

Tobacco Control & Employment

Myth: tobacco control will result in significant job losses as tobacco use falls

78

Tobacco Taxes & Employment

Fact: tobacco control results in net increase in jobs in most countries

Impact on Jobs Tobacco tax increases will lead to decreased

consumption of tobacco products• Small loss of jobs in tobacco sector

Money not spent on tobacco products will be spent on other goods and services• Gains in jobs in other sectors

Increase in tobacco tax revenues will be spent by government• Additional job gains in other sectors

Net increase in jobs in most countries

80

Tobacco Control & Illicit Trade

Myth: tobacco tax increases and other tobacco control policies will lead to increases in illicit trade, eliminating the public health and revenue benefits of higher taxes

81

Tobacco Taxes & Illicit Trade

Fact: tobacco use falls and tax revenues increase following tax increases even in the presence of illicit tobacco trade

Fact: no evidence that other tobacco control policies lead to increase in illicit trade

82

Tax Avoidance & Evasion Do NOT Eliminate Health Impact of Higher Taxes

Source: Schroth, 2014

83

Cook County Cigarette Tax and Tax Revenues - FY01-FY06

$0.15

$0.35

$0.55

$0.75

$0.95

$1.15

$1.35

$1.55

$1.75

2001 2002 2003 2004 2005 2006

Fiscal Year

Tax

per P

ack

$25,000,000

$45,000,000

$65,000,000

$85,000,000

$105,000,000

$125,000,000

$145,000,000

$165,000,000

$185,000,000

$205,000,000

$225,000,000

Tax

Reve

nues

Tax Revenues

Chicago tax risesfrom 16 to 48 cents

Chicago tax upto 68 cents, 1/1/06Chicago smoking ban, 1/16/06

Tax Avoidance & Evasion Do NOT Eliminate Revenue Impact of Higher Taxes

84

Tobacco Taxes & Illicit Trade

Fact: other factors more important than tobacco taxes and tobacco control policies in explaining illicit trade

85

Determinants of Tax Avoidance & Evasion

• Tax and price differentials More important for individual tax

avoidance and bootlegging Larger scale efforts avoid all taxes

Illicit Cigarette Market Share& Cigarette Prices, 2012

0 2 4 6 8 10 12 140.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Algeria

ArgentinaAustralia

Austria

Azerbaijan

Belarus

Begium

Bolivia

Bosnia

Brazil

Bulgaria

CameroonCanada

Chile

China

Colombia

Costa RicaCroatia

Denmark

Dominican Republic

Ecuador

Egypt

Estonia

Finland

France

Georgia

Germany

GreeceGuatemala

Hungary

India

Indonesia

IranIreland

IsraelItaly

JapanKazakhstan

Kenya

Latvia

Lithuania

Malaysia

Mexico

MoroccoNetherlands

New Zealand

Nigeria

Norway

Pakistan

Peru

Philippines

Poland

Portugal

South Korea

Turkey

Russia

Saudi Arabia

Serbia

Singapore

Slovakia

Slovenia

South Africa

Spain

Sweden

Switzerland

ThailandMacedonia

Tunisia

Romania

Ukraine

UAE

United Kingdom

USA

Uruguay

Uzbekistan

Venezuela

Vietnam

f(x) = − 0.0075588620251965 x + 0.175221285967319R² = 0.0495903303891168

Price USD

Illici

t tra

de sh

are

as %

of l

egal

ciga

rette

cons

umpti

on

Sources: Euromonitor, WHO

87

• Corruption

• Weak tax administration Absence of tax stamps; weak or non-existent

physical controls; unlicensed manufacturers, distributors, retailers; weak customs authorities

• Poor enforcement Limited resources for border patrols, customs

authorities, etc; low penalties

Determinants of Avoidance & Evasion

88

Smuggling and Corruption, 2011

1 2 3 4 5 6 7 8 9 100

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Algeria

Argentina

Australia

Austria

Azerbaijan

Belarus

Belgium

Bolivia

Bosnia

BrazilBulgaria

0.16

Canada

Chile

China

Colombia

Costa Rica

Croatia

Denmark

Dominican Republic

Ecuador

Egypt

Estonia

Finland

France

GeorgiaGermanyGreece

Guatemala

HungaryIndia

Indonesia

Iran

Ireland

IsraelItaly

JapanKazkhstan

Kenya

Latvia

LithuaniaMalaysia

Mexico

Morocco Netherlands

New Zealand

Nigeria

Norway

Pakistan

Peru

Philippines

Poland

Portugal

South Korea

Romania

Russia

Saudi Arabia

SerbiaSingapore

Slovakia

Slovenia

South Africa

Spain

Sweden

Switzerland

Thailand

MacedoniaTunisia

Turkey

Ukraine

United Arab Emirates

United Kingdom

United States

Uruguay

Uzbekistan

Venezuela

Vietnamf(x) = − 0.0130735750576566 x + 0.202775985117035R² = 0.081456105531796

Transparency Index

illici

t cig

arett

e tr

ade

volu

me

Sources: Euromonitor, Transparency International

89

• Presence of informal distribution channels

e.g. Street vendors, unlicensed distributors

• Presence of criminal networks e.g. Organized crime, terrorist organizations

• Access to cheaper sources e.g. reservations, duty free, cross border

Determinants of Avoidance & Evasion

90

Tobacco Taxes & Illicit Trade

Fact: there exist effective interventions to reduce illicit trade in tobacco products

Cigarette tax and illegal cigarette market, Spain 1991-2008

Spain: Size of contraband cigarette market & total tax level on cigarette price

59.0%

71.7%

71.2% 71.4%

77.6%17.7%

13.6%

2.7%

1.1% 1.0%

21.2%

-3.0%

2.0%

7.0%

12.0%

17.0%

22.0%

% o

f co

ntr

ab

an

d c

igare

ttes i

n d

uty

paid

sale

s

45%

50%

55%

60%

65%

70%

75%

80%

To

tal

tax a

s %

of

Mo

st

Po

pu

lar

Bra

nd

Pri

ce

total tax incidence

% of contraband

92

Combating Tax Avoidance & Evasion

Illicit trade protocol to the WHO FCTC• Adopted November 2012; currently in process

of being signed/ratified; provisions calling for:• Strong tax administration

Prominent, high-tech tax stamps and other pack markings

Licensing of manufacturers, exporters, distributors, retailers

Export bonds Unique identification codes on packages

• Better enforcement Increased resources Focus on large scale smuggling

• Swift, severe penalties• Multilateral/intersectoral cooperation

93

Oppositional Arguments

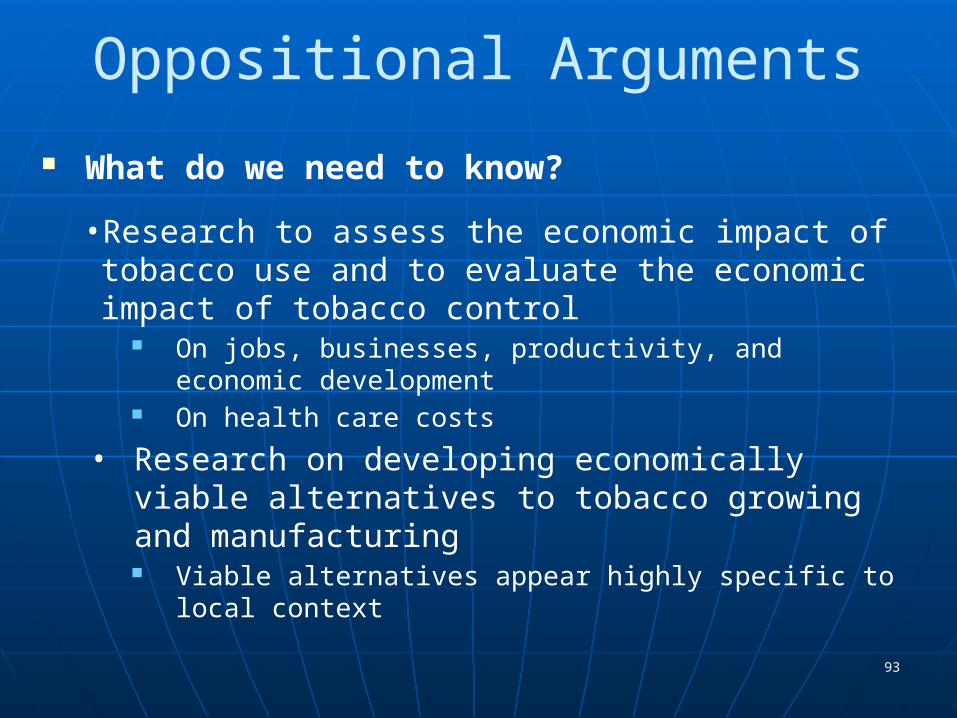

What do we need to know?

• Research to assess the economic impact of tobacco use and to evaluate the economic impact of tobacco control

On jobs, businesses, productivity, and economic development

On health care costs

• Research on developing economically viable alternatives to tobacco growing and manufacturing Viable alternatives appear highly specific to local

context

94

Oppositional Arguments

What do we need to know?

• Research on the interrelationships between tobacco use and poverty

• the role of tobacco use in causing poverty and compromising other spending

• the differential effect of tobacco control policies & programmes on the poor

• Research on tobacco tax avoidance/evasion Measurement, determinants, and consequences Effectiveness of alternative approaches to

strengthening tax administration

95

Oppositional Arguments

What do we need to know?

• Research on the cost-effectiveness of tobacco control policies, programs and other interventions To identify the ‘optimal policy mix’ called for in

1998 conference

96

Key Tobacco Control PoliciesCost-Effectiveness

Source: WHO, unpublished data

Incr

ease

d ta

xatio

n

Compr

ehen

sive

adve

rtisin

g ba

n

Clean

indo

or a

ir laws

Info

rmat

ion

and

labe

lling

Nicotin

e Rep

lace

men

t the

rapy

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

High Income Upper Middle Income Lower Middle Income Low Income

Cost

per

DA

LY

Avert

ed

Applying Lessons from the Economics of Tobacco Control

to Other Health-Related Behaviors

98

"Sugar, rum, and tobacco, are commodities which are no where

necessaries of life, which are become objects of almost universal

consumption, and which are therefore extremely proper subjects of

taxation.

Adam Smith, An Inquiry into the Nature and Causes of The Wealth of Nations, 1776

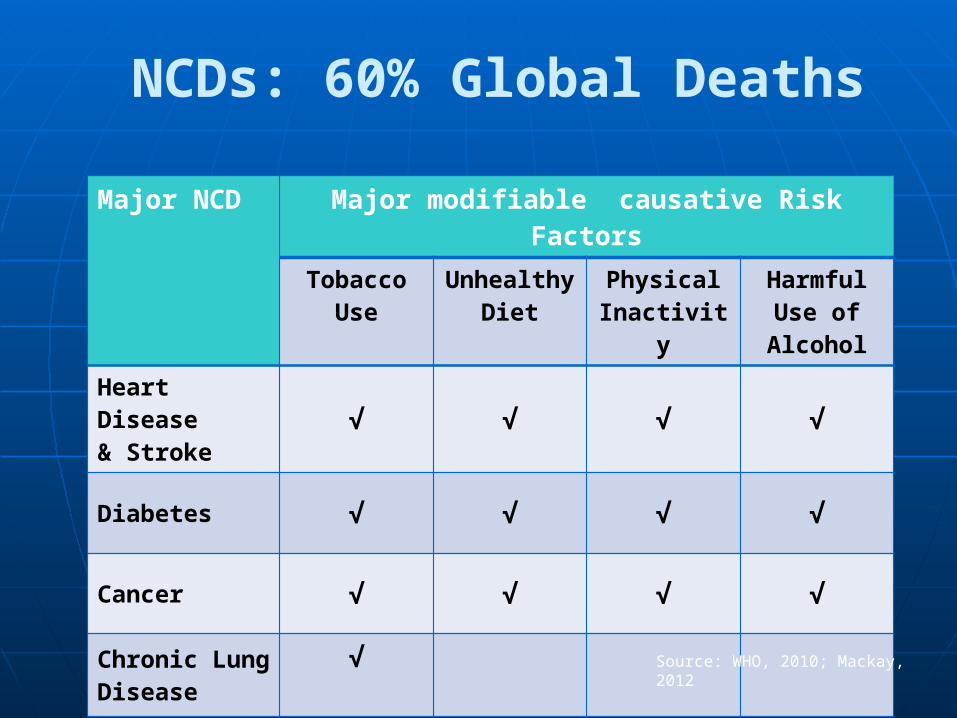

NCDs: 60% Global Deaths

Major NCD Major modifiable causative Risk FactorsTobacco Use Unhealthy

DietPhysical

InactivityHarmful Use

of Alcohol

Heart Disease& Stroke √ √ √ √

Diabetes √ √ √ √

Cancer √ √ √ √

Chronic Lung Disease

√

Source: WHO, 2010; Mackay, 2012

Extensive econometric and other research shows that higher prices for alcoholic beverages significantly reduce drinking:

• 10 percent price increase would reduce:

• Beer consumption by 1.7 to 4.6 percent

• Wine consumption by 3.0 to 6.9 percent

• Spirits consumption by 2.9 to 8.0 percent

• Overall consumption by 4.4 percent

• Heavy drinking by 2.8 percent

• Generally larger effects on youth and young adults

Alcohol Prices and Drinking

Source: Wagenaar et al., 2009; Xu & Chaloupka, 2013

Beer Tax and Binge Drinking Prevalence US States, 2010

Source: Xuan et al., 2013

Extensive econometric and other research shows that higher prices for alcoholic beverages significantly reduce:

• Drinking and driving, traffic crashes, and motor-vehicle accident fatalities

• Deaths from liver cirrhosis, acute alcohol poisoning, alcohol-related cancers, cardiovascular diseases, and other health consequences of excessive drinking

• Violence, including spouse abuse, child abuse, and suicides

• Other consequences of drinking, including work-place accidents, teenage pregnancy, and incidence of sexually transmitted diseases

Alcohol Prices and Consequences

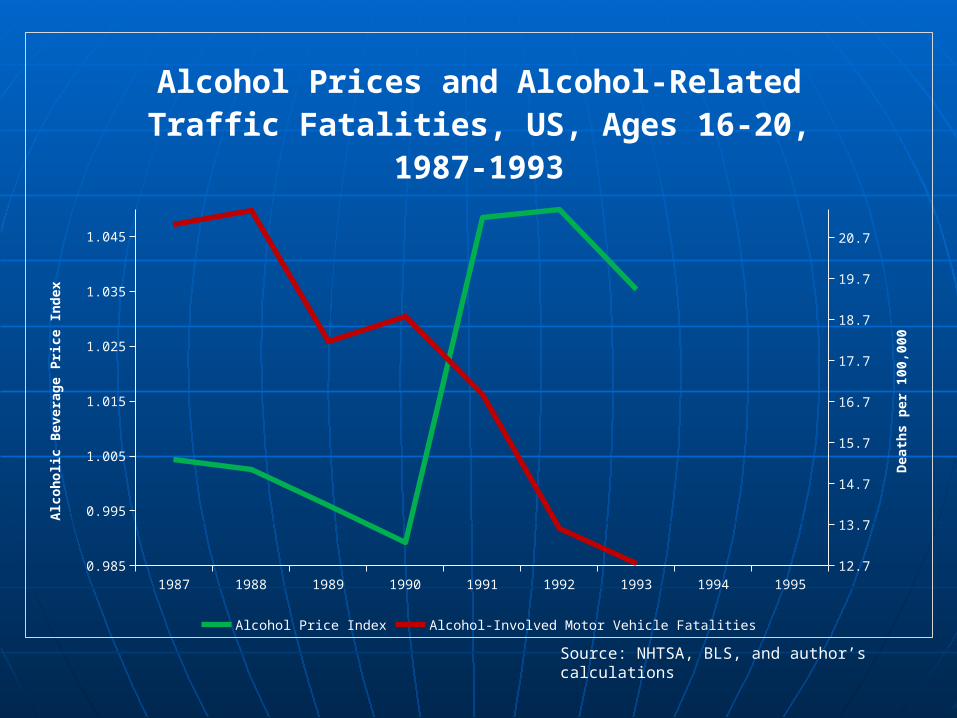

Source: NHTSA, BLS, and author’s calculations

1987 1988 1989 1990 1991 1992 1993 1994 19950.985

0.995

1.005

1.015

1.025

1.035

1.045

12.7

13.7

14.7

15.7

16.7

17.7

18.7

19.7

20.7

Alcohol Prices and Alcohol-Related Traffic Fatalities, US, Ages 16-20, 1987-

1993

Alcohol Price Index Alcohol-Involved Motor Vehicle Fatalities

Alc

oholic B

evera

ge P

rice I

ndex

Death

s p

er

100,0

00

State Cigarette & Beer Tax Increases, 2000-2013

Sources: Campaign for Tobacco Free Kids; NIAAA Alcohol Policy Information System; Brewers Almanac;

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

5

10

15

20

Cigarettes Alcohol

105

AZ

WY

OR

ID

MT

UTNV

WA

CA

TX

AROK

ND

LA

KS

IANE

SD

CO

NM

MO

MN

TN

AL

KY

OH

MS

MI

IN

GA

FL

PA

ME

NY

WV VA

NC

SC

VT

D.C.

NJ

MD

DE

NHMA

IL

WI

AK

2000s

CT

RI

Decade of Last Permanent Beer Tax Increase

HI

1990s

1980s 1970s

1960s

1950s

1940s or earlier

Average Beer & Cigarette TaxesUnited States, Inflation Adjusted 1973-2012

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

$0.00

$0.50

$1.00

$1.50

$2.00

Beer Tax Cigarette Tax

Tax P

er

Pack o

f 20 C

igare

ttes &

6 P

ack o

f B

eer,

2012

dollars

Sources: Campaign for Tobacco Free Kids; NIAAA Alcohol Policy Information System; Brewers Almanac; Bureau of Labor Statistics; and authors calculations. Note: 2012 beer tax is through June 2012

Source: Tax Burden on Tobacco, 2011, and author’s calculations

0.850000000000001

1.35

1.85

2.35

2.85

3.35

Alcoholic Beverage & Tobacco Product Prices, Relative to CPI,

1953-2010

Alcoholic Beverages Tobacco Products

Public Health Rationale for SSB Taxes

• Link to obesity• Several meta-analyses conclude that increased

SSB consumption causes increased weight, obesity

• Increased calories from SSBs not offset by reductions in calories from other sources

• Other health consequences• type 2 diabetes, lower bone density, dental

problems, headaches, anxiety and sleep disorders

Soda Consumption & ObesityCalifornia Counties, 2005

Source: Babey, et al., 2009 and authors' calculations.

10 15 20 25 30 35 4040

45

50

55

60

65

70

f(x) = 16.4401260028826 ln(x) + 6.11419822765063R² = 0.665636557713179

% Adults Drinking One or More Sodas per Day

% of Adults

Who Are Overweight or Obese

Evidence on SSB Taxes/Prices & Obesity

• Growing literature demonstrating the higher prices for SSBs lead to reductions in SSB consumption

• Powell et al. (2013) review finds greater impact of SSB only prices; elasticity of -1.2

• Limited, mixed evidence on impact of taxes/prices on weight outcomes

• Small, less than comprehensive sales taxes• Substitution to untaxed products, larger volumes• Some effects among most at-risk populations

Carbonated Beverage Prices & Youth Obesity1995-2009, Inflation Adjusted

Source: BLS; YRBS

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009143

145

147

149

151

153

155

10

10.5

11

11.5

12

12.5

13

Carb. Bev. Obese

States with Sales Taxes on Regular Soda (as of January 1, 2014)

States with Sales Taxes on Bottled Water (Jan. 1, 2014)

Source: Bridging the Gap Research Program, University of Illinois at Chicago, 2014

Importance of Tax Structure From a public health and revenue perspective, specific

excise tax (tax based on quantity/volume) preferable to sales tax or ad valorem excise tax (taxes based on price) for several reasons:

• Included in shelf price, so more apparent to consumer

• Easier administratively

• Reduce incentives for switching to cheaper brands, larger quantities

• Revenues more stable, less subject to industry price manipulation

• Disadvantage of specific tax: need for inflation adjustment

115

Counterarguments

Same as have been raised against tobacco taxes• Employment impact

Recently published research assessing impact of reduced SSB consumption on employment

Forthcoming research assessing impact of reduced alcohol consumption on employment

• Impact on the poor• Tax avoidance/evasion

Summary

117

Counterarguments Much has been learned about the economics of

tobacco and tobacco control over the past decade• Particularly rapid growth in research from LMICs• Key factor in significant tax increases, stronger

tobacco control policies, and implementation of programs and other interventions to reduce tobacco use and its consequences

However, much remains to be learned• Particularly in some regions, including Africa

Many lessons learned can be applied to other health behaviors that contribute to NCDs

For more information:

Bridging the Gaphttp://www.bridgingthegapresearch.org

Tobacconomicshttp://www.tobacconomics.org

@BTGResearch

@tobacconomics