Embed Size (px)

Citation preview

CONSOLIDATED FINANCIAL HIGHLIGHTS

STATEMENT OF THE CHAIRMAN

CORPORATE GOVERNANCE• Corporate Governance Framework • Biographies of Board Members • Group Chart • Organization Chart - Fransabank SAL• Executive and Management Committees - Fransabank SAL• Management - Fransabank SAL• Local Banking Subsidiaries - Board of Directors and General Managers• Overseas Banking Subsidiaries and Associate - Board of Directors and General Managers

HISTORICAL MILESTONES

MANAGEMENT REPORT• Lebanon’s Economic Performance in 2016• Consolidated Results of Operations• Main Ratios• Resolutions of Fransabank SAL Ordinary General Assembly• Core Banking Activities

- Investment and Private Banking - Corporate Banking - Retail Banking - China Desk

• Local Subsidiaries and Associate- BLC Bank SAL- Fransa Invest Bank SAL (FIB)- Lebanese Leasing Company SAL (LLC)- Bancassurance SAL- Société Générale Foncière SAL (Sogefon)

• Overseas Subsidiaries and Associate- Fransabank (France) SA- Fransabank El Djazaïr SPA- Fransabank OJSC (Belarus)- Fransabank SAL Iraq branches- United Capital Bank (Sudan)

• Risk Management• Compliance • Human Resources• Information and Communication Technology• Corporate Social Responsibility• Environmental and Social Management System (ESMS)

CONSOLIDATED FINANCIAL STATEMENTS• Independent Auditors’ Report• Consolidated Statement of Financial Position• Consolidated Statement of Profit or Loss• Consolidated Statement of Profit or Loss and Other Comprehensive Income• Consolidated Statement of Changes in Equity• Consolidated Statement of Cash Flows• Notes to the Consolidated Financial Statements

GROUP NETWORK• Lebanon - Parent Company, Subsidiaries and Associates • Overseas Subsidiaries and Branches • Overseas Associate• Representative Offices

CONTENTS

2

6

1013161820212223

26

303243444545454647484848494949505050515151525556585963

66707273747678

130134136136

0

30

60

90

120

150

180

210

(in million of USD)

Net ProfitFor The Financial Year

2015201420132012 2016

+ 5.80% CAGR + 7.27% + 7.79%CAGR CAGR

(in million of USD)

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

TotalAssets

(in million of USD)

Loans & AdvancesTo Customers (Net)

2015201420132012 2016

160.37

160.75

166.98

179.62 20

0.9

5

18,942

.47

19,993

.66

20,8

54.6

1

15,750

.64

16,964

.39

2015201420132012 2016

4,83

9.17

5,29

2.86 6,28

8.59

5,819.06

6,53

3.39

31.12.13

14,121.09

5,292.86

160.75

1,654.76

16,964.39

14.72%

116

3,265

1,507.5

31.12.12

13,065.30

4,839.17

160.37

1,488.57

15,750.64

12.44%

114

3,227

1,507.5

31.12.14

15,346.48

5,819.06

166.98

1,865.74

18,942.47

15.07%

124

3,416

1,507.5

31.12.15

16,306.91

6,288.59

179.62

1,956.34

19,993.66

14.74%

124

3,493

1,507.5

Customers' Creditor Accounts

Loans & Advances to Customers (net)

Net Profit for the Financial Year

Shareholders' Equity

Total Balance Sheet

Capital Adequacy Ratio

Number of Local Branches

Staff Number

Exchange Rate USD/LBP

as per Basel III as per Basel III as per Basel III as per Basel III

+8.08%

+9.38%

+0.24%

+11.16%

+7.71%

31.12.16

17,007.08

6,533.39

200.95

2,127.06

20,854.61

15.37%

125

3,561

1,507.5

as per Basel III

In million of USD

+8.68%

+9.94%

+3.88%

+12.75%

+11.66%

+6.26%

+8.07%

+7.57%

+4.86%

+5.55%

prog.15/14

prog.14/13

prog.13/12

CONSOLIDATED FINANCIAL HIGHLIGHTS

+4.29%

+3.89%

+11.88%

+8.73%

+4.31%

prog.16/15

0

300

700

900

1,200

1,500

1,800

2,100

2,400

2015201420132012 2016

2015201420132012 20162015201420132012 2016

+ 6.81% CAGR

+ 9.33% CAGR

+ 2.10% CAGR + 4.48% CAGR

0

3,000

6,000

9,000

12,000

15,000

18,000

0

5

10

15

20

25

30

35

40

0

1

2

3

4

5

6

7

8

(in million of USD)

Customers’Creditor Accounts

(in million of USD)

Shareholders’Equity

(in USD)(in million of USD)

Earningsper Common Share

Loans & Advances To Customers To Customers’ Creditor Accounts (%)

0

100

200

300

400

Net InterestIncome

13,065

.30

14,121.0

9

15,346

.48

16,306.91

17,0

07.

08

2,12

7.0

6

1,488

.57

1,654

.76

1,865

.74

1,956

.34

392.

20

360.91

373.00

388.30

396.04

38.4

2%

37.04%

37.48%

38.56%

37.92%

2015201420132012 2016

6.63

6.37 6.59

7.26 7.

90

2015201420132012 2016

FRANSABANK | ANNUAL REPORT 2016 | 2-3

FOLLOW YOURSENSES WITHTHE BELIEF IN

RIGHTEOUSNESS

FRANSABANK | ANNUAL REPORT 2016 | 4-5

S TAT E M E N T O F T H E

C H A I R M A N

We are pleased to report that 2016 wasanother year of solid growth forFransabank Group.

The financial sector is experiencingsubstantial changes directed by internaland external players. Geopoliticalinstability, macroeconomic conditions,changing customer expectations,technological advances, along with astronger competitive market andgreater regulatory pressure, are drivinga more challenging banking environment. Yet, we believe that thesesame changes will lead, as well as, tonew opportunities reinforcing our statusand conveying long-term values for allour stakeholders.

Amidst these developments, theLebanese financial market managed todeliver satisfactory financial results. Atyear-end 2016, total assets of banksoperating in Lebanon grew by 9.7%reaching USD 209 billion and customers’deposits and loans to the private sectorincreased by 7% and 5.4% respectively.

In sync, Fransabank Group’s resultsonce again echoed the strength of ourdiversified business model andconfirmed our hard work to grow into amore customer-centric Bank, embracinga transparent and resourceful financialexperience, and continue to generategreat outcomes.

Shrewdly managing risks and resources,Fransabank Group delivered a netprofit of USD 200.9 million in 2016, upby 11.9% from USD 179.6 million in2015. In this context, Return on AverageCommon Equity (ROACE) reached 11.21%

STATEMENT OF THE CHAIRMAN

Adnan Kassar - Chairman & Adel Kassar - Deputy Chairman

"Fransabank Group’s resultsonce again echoed the strength ofour diversified business model andconfirmed our hard work to grow intoa more customer-centric Bank"

FRANSABANK | ANNUAL REPORT 2016 | 6-7

and Return on Average Assets (ROAA)reached 0.98%. Total assets reachedUSD 20.86 billion, an increase of 4.3%from USD 19.99 billion at year-end 2015.Net loans and advances to customersstood at USD 6.53 billion at year-end2016, up by 3.9% from year-end 2015.Customers’ deposits amounted toUSD 17.01 billion at year-end 2016,an increase of 4.3% from year-end 2015.In addition, the solvency ratio as perBasle III attained 15.4% by end-December2016, exceeding the standards requiredby the Central Bank of Lebanon.

Accordingly, the preceding has advancedFransabank Group’s ranking inLebanon in terms of net profits fromthe fourth position at end 2015 to thethird position at end 2016, sustained itsthird position in terms of total assetsand loans and advances to customersand consolidated its fourth rankingin terms of customer’s deposits.

Furthermore, Fransabank Groupfollows a sound expansion strategygrabbing potential opportunitieswhether internationally or locally.

In this vein, we retain a focusedinternational presence to assist ourcustomers across our countries ofoperation, targeting mainly the well-spread Lebanese Diaspora but alsodrawing foreign customers to our corebusiness. Fransabank intensivelyworked on further developing itsbilateral relations with The Republic ofChina. Through our dedicated ChinaDesk, we have been proactivelydeveloping products and services incorrespondent banking, corporate

banking, SME, and retail, as well as,hosting promotional events in bothcountries. Fransabank is workingtowards the development of trade andtourism for the benefit of its clientele,and for the Chinese companies.

Locally, our “Go Green” Strategycontinued to build on our position andreputation as the Sustainable EnergyFinance (SEF) leader Bank in Lebanonwhereby, we received the highestrecognition from Business for Peaceand were selected to representSustainable Development Goal 13:Climate Action. Fransabank SEF loanwas also recognized as a “replicable”success story, at the Conference ofParties (COP22) in Marrakech, whichthe International Finance Corporation(IFC) will recommend as best practiceto its clients in the Middle East & NorthAfrica region. Further, integratingsustainability in our product portfolio,Fransabank has been helping clientsbetter understand green investments;their long-term benefits for thebusinesses, as well as, combattingclimate change.

In view of that, we have worked in 2016on updating our corporate socialresponsibility strategy for the years2016 to 2018 focusing on integratingcorporate responsibility further in ourcore business. We aim to do this byestablishing common grounds andclear directives on integrating a holisticsustainability approach. As such,Fransabank was much involved inimplementing updated compliancerequirements, whether arising fromlocal or international regulatory bodies;

covering risk management, corporategovernance, anti-money laundering,combatting terrorism financing, FATCA,etc…

Likewise, our approach to improvingquality is proactive. We aim to identifythe needs and expectations of ourcustomers and strive to provide solutions.We sustain our quality throughcontinuously investing in our valuablehuman resources and technology inorder to achieve continued progress.

While we are satisfied with theprogress made by the Group in 2016,we will go on with the fulfilment of ourvision and mission, carrying out ourresponsible strategy while keeping ourcustomers’ at the heart of what we do.In 2017, we will consolidate our effortsto improve the customer experience,sustain a solid financial performance;while reinforcing our compliance andrisk management know-hows over andabove a sound market growth.

With the valuable commitment andcontributions of our shareholders, theunfaltering trust of our customers andcontinued unwavering commitment ofour employees, we will continue topursue our mission to create value forshareholders, customers, employeesand the society at large.

Sincerely,

Adnan Kassar

LISTEN TO THENEED OF

ENSURINGMORAL

PRACTICES

LISTEN TO THENEED OF

ENSURINGMORAL

PRACTICES

FRANSABANK | ANNUAL REPORT 2016 | 8-9

C O R P O R A T E

G O V E R N A N C E

Fransabank Corporate Governance framework revolves essentiallyaround the Corporate Governance Code as adopted by theBoard of Directors in line with the regulatory requirements andinternational best practices. It also includes a set of governancerelated policies and charters, as well as, a Code of Conduct & Ethics.

This framework promotes the commitment of the Bank to thehighest level of transparency, integrity, fairness and accountabilityand helps in disseminating a strong governance culture withinthe Bank by setting the ‘tone at the top’.

The Group’s strategy remains to standardize the implementationof Good Corporate Governance practices across its entities and

to strengthen its governance and control culture, taking intoconsideration the Corporate Governance requirements of hostjurisdictions.

Governance Structure

Fransabank governance structure, which aims to provide anefficient framework for the assignment of responsibility andaccountability, includes the General Assembly of Shareholders;the Board of Directors; the Chairman; the Deputy Chairman;the various Committees; control functions; the external auditors;senior management and the business and support functions.

Fransabank is committed to implement sound Corporate Governance practices,which focus on the main guiding principles of transparency, accountability, integrityand fairness in the treatment of all stakeholders.

CORPORATE GOVERNANCE FRAMEWORK

Corporate Governance

ManagementCommittees

ExecutiveCommittee

RemunerationCommittee

CorporateGovernanceCommittee

BoardRisk

Committee

BOARD COMMITTEES

Board of Directors

GENERAL ASSEMBLY (SHAREHOLDERS)

AuditCommittee

Chairman &Deputy Chairman

General Managers

AML/CFTBoard

Committee

Corporate Governance &Group Risk Management

GroupInternal Audit

External Audit

GroupCompliance

Inspection

Senior Management

Business &Support Functions

Rights of Shareholders

Shareholders enjoy all rights conferred upon them by theLebanese Code of Commerce, including the right to vote at theGeneral Assembly, the right to receive dividends, the right totransfer their shares and the preferential right to subscribe tocapital increases. All common shareholders, including minority

shareholders, enjoy the same rights and benefits and have onevoting right for each common share (the principle of one share,one vote) without limitation. Shareholders who own registeredshares for at least two years are entitled to a double voting rightaccording to Article 117 of the Lebanese Code of Commerce.

Adnan KassarAdel KassarDeutsche Investitions - und Entwicklungsgesellschaft mbH (DEG) (2)Al-Fadl Holdings LimitedThe Public Institution for Social Security – KuwaitOthers (3)

Total Shareholding

(1) Percent of total share capital consisting of 21,500,000 Common Shares as at 31.12.2016(2) Deutsche Investitions - und Entwicklungsgesellschaft mbH DEG is one of Germany’s top development and investment banks. DEG is owned by

Kreditanstalt für Wiederaufbau KfW, which, in turn, is owned by the German Government. (3) Each with less than 2%.

39.5739.605.002.702.00

11.13

100

PERCENT (1)Main Holders of Common Shares as at December 31, 2016

Fransabank Governance Structure

Board of Directors

Fransabank is governed by a Board of Directors, which consistsof twelve members elected by the General Assembly ofshareholders for three years.

The management of the Bank is vested in the Board of Directors,which, at Fransabank, consists of a sufficient mixture of non-executive and independent members. The majority of Boardmembers qualify as non-executive. This composition aims tosafeguard the governance and effectiveness of the Board andto ensure the objective of adding value to all shareholders,investors, clients and community in the short, medium andlong terms.

The Board has overall responsibility of the Bank, includingadopting and overseeing the implementation of the Bank’sstrategic objectives, risk strategy, risk policies, corporategovernance and corporate values, as well as ensuring thatadequate, effective and independent controls are in place.

A charter of the Board of Directors was developed in line withthe prevailing Lebanese laws & regulations and internationalgood practices. The charter aims to define the composition,roles and responsibilities and the authority of the Board ofDirectors, including the adoption of a framework to collectivelyevaluate the Board performance in relation to its compliancewith the Corporate Governance Principles.

During 2016, the Board of Directors has met four times.

In carrying out its oversight responsibilities, the Board issupported by the Corporate Governance Committee, BoardRisk Committee, Audit Committee and the RemunerationCommittee. These committees are chaired by independentnon-executive members.

H.E. Mr. Adnan KassarExecutive Director

Mr. Adel KassarExecutive DirectorMember of the AML/CFT Board Committee

Mr. Antoine Jeancourt GalignaniNon-Executive DirectorChair of the Audit Committee and the Corporate Governance Committee

Mr. Bernd TümmersNon-Executive DirectorMember of the Board Risk Committee

The Public Institution for Social Security - KuwaitNon-Executive Director

Mrs. Magda RizkNon-Executive DirectorChair of the AML/CFT Board Committee

H.E. Mr. Nehmé TohméNon-Executive Director

H.E. Mr. Walid Daouk, Esq.Non-Executive DirectorMember of the Audit Committee, the Corporate Governance Committee, the AML/CFT Board Committee and the Remuneration Committee

Mr. Rafic CharafeddineNon-Executive DirectorChair of the Remuneration Committee

Mr. Nadim KassarExecutive Director

Mr. Henri GuilleminNon-Executive DirectorChair of the Board Risk Committee

Dr. Walid NajaNon-Executive DirectorMember of the Board Risk Committee, the Audit Committee, the Corporate Governance Committee, the Remuneration Committee and the AML/CFT Board Committee

Board Members

FRANSABANK | ANNUAL REPORT 2016 | 10-11

The Corporate Governance Committee, Risk ManagementCommittee and Audit Committee meet at least quarterly andwhen necessary. The Remuneration Committee shall meet atleast semi-annually. A charter was established to eachCommittee, which indicates the Committee’s scope of work,membership structure and composition, meetings, as well as,its roles and responsibilities. The Charters are regularlyupdated to ensure compliance with local and internationalstandards.

During 2016, each of the Corporate Governance Committee,the Board Risk Committee and the Audit Committee held fourmeetings and the Remuneration Committee held two meetings.

Corporate Governance Committee

The responsibility of the Corporate Governance Committee isto provide oversight of all material Corporate Governanceissues affecting the Bank and its subsidiaries and to ensurethat Fransabank Corporate Governance practices are in linewith the regulatory requirements and international bestpractices.

Board Risk Committee

The Board Risk Committee’s responsibilities are to assist theBoard of Directors in fulfilling its risk-related duties and tooversee the proper implementation of the risk managementprinciples. In discharging its responsibilities, the Committeemonitors the Bank’s risk profile through the reports submittedby the Chief Risk Officer to the Board Risk Committee prior topresenting them to the Board of Directors. The Committee isalso responsible for recommending to the Board of Directorsthe Bank’s risk policy including the risk appetite and risktolerance.

Audit Committee

The Audit Committee is established to assist the Board ofDirectors in its oversight responsibilities regarding the:

• Evaluation of the internal control regulations and procedures• Assessment of the qualifications and independence of theexternal auditors

• Supervision of the internal audit’s activities• Integrity of the financial statements• Review of the Bank’s disclosure standards.

Remuneration Committee

The Remuneration Committee ensures that the Bank hascomprehensive remuneration policies and procedures andoversees their implementation.

In December 2016, the Board has established an Anti-MoneyLaundering/Combating the Financing of Terrorism - AML /CFTBoard Committee. The Committee’s charter is underpreparation to be further submitted to the Board of Directorsfor approval.

Management

The Chairman of the Board may suggest to the Board theappointment of one or more General Managers and DeputyGeneral Managers, who shall act for account and under thefull responsibility of the Chairman. In addition, seniormanagement would include heads of key departments tosupport the general management in running the day-to-daymanagement of the Bank.

Specialized Management Committees are established, whosemembers include senior staff, having the responsibility to setstrategies and take decisions as necessary for the developmentof the Bank’s activities.

Control Functions

Fransabank implements sound internal control systemsto ensure appropriate segregation of duties and avoidance ofconflicts of interest within the organization structure.

The Bank recognizes the importance of implementing soundcontrol functions at the Bank including risk management,compliance, internal audit and inspection functions. Thesefunctions ensure that the Bank’s activities are performed inaccordance with the prevailing laws and regulations, as wellas, with the Bank’s policies and procedures.

Charter of Board Committees

Corporate Governance

BIOGRAPHIES OF BOARD MEMBERS

FRANSABANK | ANNUAL REPORT 2016 | 12-13

H.E. MR. ADNAN KASSARChairman of the Board of Directors

H.E. Mr. Adnan Kassar is the Chairman & CEO of Fransabank Group and member of theBoard of Directors of BLC Bank SAL and Fransabank (France) SA. He is also the Chairmanof the Supervisory Board of Fransabank OJSC in Belarus. He and his brother Adel acquiredFransabank in 1980. H.E. Mr. Kassar served as Minister of Economy and Trade in Lebanonfrom 2004 to 2005 and Minister of State in Lebanon from 2009 to 2011. He was the first Arabbusinessman elected Chairman of the International Chamber of Commerce (ICC) andheaded the World Business Organization from 1999 to 2000. He is also former President ofthe Lebanese Federation of Chambers of Commerce, Industry and Agriculture in Lebanonand headed this Federation for over thirty years (from 1972 to 2002). He is the President ofthe Lebanese Economic Organizations and is the Honorary Chairman of the General Unionof Chambers of Commerce, Industry and Agriculture of the Arab Countries which groupsmillions of companies and associations from the 22 member Arab countries. He is theHonorary Chairman of the Silk Road Chamber of International Commerce (SRCIC) electedin 2016. Mr. Kassar has received global awards and high distinguished decorations frommany Heads of States and International Organizations including the Oslo Business for PeaceAward in 2014 and the “China Arab Outstanding Contribution” Award from China’s PresidentXi in 2016. He holds a law degree from Saint Joseph University, Beirut and an HonoraryDoctorate from the Lebanese American University. www.adnankassar.com

Born in 1930 - Lebanon

MR. ADEL KASSARDeputy Chairman of the Board of Directors

Mr. Adel Kassar is the Deputy Chairman and Chief Executive Officer of Fransabank Group.He is the Chairman of the Board of Directors of Fransabank France SA. He is also theChairman of the Board of Directors and General Manager of Bancassurance SAL andLebanese Leasing Company SAL. He is member of the Board of Directors of BLC Bank SALand member of the Supervisory Board of Fransabank OJSC in Belarus. He and his brotherAdnan acquired Fransabank in 1980. He is a former Chairman of the Association of Banksin Lebanon and is the Honorary Consul General of the Republic of Hungary in Lebanon. Heholds a degree in Lebanese and French law from Saint Joseph University, Beirut, affiliatedto the Faculty of Law of Lyon, France.

Born in 1932 - Lebanon

MR. ANTOINE JEANCOURT GALIGNANIChair of the Audit Committee & the Corporate Governance Committee

Mr. Antoine Jeancourt Galignani started his career at the French Ministry of Finance andlater joined Chase Manhattan Bank in New York and Crédit Agricole. He was appointed asManaging Director, then Chairman of Bank Indosuez. He was also member of the Board ofDirectors of Banque Saudi Fransi, in Saudi Arabia and the Chairman and CEO of AGF, whichwas later acquired by Allianz Group and the Chairman of the holding company of SNA. Healso served in numerous Boards such as TOTAL, Bouygues and Société Générale and hechaired the Board of the Institute of International Finance in Washington from 1991 to 1994.Mr. Galignani was until the 1st of December 2012 the Chairman of the Board of EurodisneyFrance. He holds a master degree in economics and political sciences from ENA, France.

Born in 1937 - France

Corporate Governance

MRS. MAGDA RIZKChair of the AML/CFT Board Committee

Mrs. Magda Rizk is the owner and manager of Rizk Real Estate and Agricultural Properties. She chairedthe Remuneration Committee and was member of the Risk Management Committee at FransabankSAL until December 2016. She was also a member of the Audit Committee at Fransabank SAL from2008 to 2012. She is a specialized lawyer in property law and a member of the Beirut Bar Association.She holds a degree in Lebanese and French law from Saint Joseph University, Beirut.

THE PUBLIC INSTITUTION FOR SOCIAL SECURITY – KUWAIT

The Public Institution for Social Security is a public institution which has an independent budgetand is under the supervision of the Minister of Finance. The Institution has a Board of Directors,chaired by the Minister of Finance and a General Manager who is responsible for executing thepolicy as drawn-up by the Board of Directors. The Public Institution for Social Security isrepresented by Mr. Mohammad Al-Qassar in the Board of Directors.

Mr. Bernd Tümmers began his career as business administration trainer in a German manufacturingcompany, followed by being the assistant to the CFO of a large engineering and construction companyin the USA. He joined Deutsche Investitions - und Entwicklungsgesellschaft mbH (DEG), Cologne -member of the KFW Banking Group, as Investment Manager for South East and East Asia in 1980 andthen Head of Department in charge of DEG’s activities in Asia. In 1996, he became Senior VicePresident and served in various management positions; among others, he was responsible for DEG’sinvestments for approximately five hundred companies worldwide with an investment volumeof USD 6 billion. After his retirement in 2012, he founded his own consulting firm and became partnerof AdminiStraight GmbH, a company advising German companies in different fields. He still serves asa member of the Board of Directors in DEG’s few companies. He holds an MBA degree from Universityof Cologne, Germany.

MR. BERND TÜMMERSMember of the Board Risk Committee

Born in 1947 - Germany

Born in 1957 - Lebanon

H.E. Mr. Nehmé Tohmé is the Chief Executive Officer for many contracting companies operating inSaudi Arabia, Qatar and Bahrain. He also established several corporations and was a shareholder,partner or member of the Board of Directors in many companies. He was elected as member ofthe Lebanese Parliament in 2000 and served as Minister of Displaced from 2005 to 2008. He holdsa BS in civil engineering from the American University of Beirut.

H. E. MR. NEHMÉ TOHMÉ

Born in 1939 - Lebanon

H.E. Mr. Walid Daouk, Esq is a specialized lawyer in commercial law, civil and property law. He startedhis career in 1981, as an associate in Takla & Trad law firm becoming thereafter a partner. In 2005, heoccupied the position of Vice Chairman at the International Affairs Commission at the Beirut BarAssociation, and in 2008, he became a member of the Arbitration Commission. In 2011, hewas appointed Minister of Information and Minister of Justice per interim. After the termination ofhis appointment in 2014, he resumed his practice as lawyer and legal consultant in above mentionedfirm. He is a lawyer and legal advisor for multinational and Lebanese companies performing businessin various fields. Also, he is a Board member of many corporations in Lebanon and abroad includingFransabank SAL, Fransabank (France) SA, Fransabank El Djazaïr SPA, BLC Bank SAL, Semiramis SAL,Beirut Waterfront Development SAL, Tourism and Hotel Development Company SAL. He was a memberof the Board of Directors of the Council for Development and Reconstruction of Lebanon (CDR)2001-2004. He is the Commissioner of the Lebanese Government at the Beirut Stock Exchange since1994. He holds a degree in Lebanese and French law from Saint Joseph University, Beirut and hadprepared a degree in Business Management at the Beirut University College.

H.E. MR. WALID DAOUK , ESQ.Member of the Audit Committee, the Corporate Governance Committee, the AML/CFT Board Committee and the Remuneration Committee

Born in 1958 - Lebanon

FRANSABANK | ANNUAL REPORT 2016 | 14-15

MR. NADIM KASSAR

Mr. Nadim Kassar is a General Manager of Fransabank SAL. He is also the Vice Chairman andGeneral Manager of BLC Bank SAL, Founder and Board Member of Fransa Invest Bank SAL (FIB),Founder and Chairman of Fransabank El Djazaïr SPA, Board Member of the Association of Banksin Lebanon since 2001, Vice Chairman and Board Member of USB Bank PLC, Board Member ofLebanese International Finance Executives (LIFE), Co-Manager of A.A. Kassar (France) SARLand General Manager of A.A. Kassar SAL. Mr. Kassar is also a Board Member of the followinginstitutions: MasterCard Incorporated Asia, Pacific, Middle East & Africa, SAMEA Regional Boardof Directors since 2005, NetCommerce, International Payment Network (IPN) SAL, Credit CardManagement, Founder and Board Member of the American Lebanese Chamber of Commerce. Heholds as well the position of Deputy Chairman of Société Financière du Liban SAL. He holdsa bachelor’s degree in Business Administration from the American University of Beirut.

Mr. Rafic Charafeddine is a businessman, and has participations in various companies. He deals inconstruction projects and real estate investments.

MR. RAFIC CHARAFEDDINEChair of the Remuneration Committee

Born in 1939 - Lebanon

Born in 1964 - Lebanon

Dr. Walid Naja is former Chairman of the Banking Control Commission - Central Bank of Lebanon.He previously served as Economic Counselor at the Lebanese Embassy in Washington D.C., andGeneral Manager of the Federation of Chambers of Commerce, Industry and Agriculture inLebanon. He holds graduate degrees in economics and international relations from the AmericanUniversity of Beirut and Yale University, USA.

DR. WALID NAJAMember of the Board Risk Committee, the Audit Committee, the Corporate Governance Committee, the Remuneration Committee and the AML/CFT Board Committee

Born in 1941 - Lebanon

Mr. Henri Guillemin started his career at Crédit Lyonnais. He then joined Indosuez Bank in 1978and was appointed at different management positions in Singapore, Saudi Arabia (Jeddah andRiyadh), Bahrain and Paris. He became Managing Director of Banque Saudi Fransi in Riyadh in1993 for four years and then was promoted Director for the Middle East and Africa region for CréditAgricole Indosuez, based in Paris. Mr. Guillemin was the Managing Director of Crédit AgricoleEgypt SAE, Cairo between 2007 and 2011. He holds a degree in economic sciences from SorbonneUniversity, Paris, as well as a degree in political studies, and an MBA degree from INSEADFontainebleau.

MR. HENRI GUILLEMIN Chair of the Board Risk Committee

Born in 1947 - France

L

G

1

1

BANKS ABROAD

REPRESENTATIVE OFFICES

68%

• Group CMA-CGM (Franco-Lebanese) 25%

• Maghreb Truck Cie SPA Algeria 7%

79.21%**

• BPCE International et Outre Mer (IOM) 20.79%**

20%

• Aref Investment Group Kuwait 25%

• Athman Moushtaraks for Trading Co. - Kuwait 15.02%

• Boubyan Bank KSC Kuwait 21.67%

• Financial Company for Investment & Development Egypt 6.25%

• Al Imtiyaz Investment Co. Kuwait 5.83%

• Others 0.04%

• Riyada Capital - Kuwait 2.92%

• Others 3.31%

91.55%

• Fransa Holding SAL Lebanon 8.41%

Nota: Fransabank Group Chart updated for events occurring up to May 2017.

BLC Bank has two subsidiaries in Lebanon: BLC Finance & BLC Services.

99.25%

Fransabank(France) SAFrance

UnitedCapital BankSudan

FransabankOJSCBelarus

USBBank PLCCyprus

FransabankEl DjazaïrSPA - Algeria

Cuba(Havana)

Ivory Coast(Abidjan)

UAE(Abu Dhabi)

FRANSABANK

** as of 31 March 2016

GROUP CHART

Corporate Governance

50%

• Banque Libano-Française SAL 40%

• BLC Bank SAL 10%

87.49%

• DEG Germany 12.50%

• Others 0.01%

99.88% 99.70% 99.70% 96.70%

68.58% 100%

• Holding M. Sehnaoui 18.44%

• Others 1.87%

• Silver Capital Holding 4.86%

37.067%

BANKS IN LEBANON

COMPANIES IN LEBANON

74 branches in Lebanon and 2 branches in Iraq

49 branches in Lebanon

(F 2

A

6.25%

Lebanese LeasingCompany SAL

Fransabank Insurance Services Co SAL

SogefonSAL

ExpressSARL

Switch & ElectronicServices SAL

BLC BankSAL

BancassuranceSAL

SAL

FransaInvest BankSAL

Bank of Beirut andthe Arab CountriesSAL

FRANSABANK | ANNUAL REPORT 2016 | 16-17

ORGANIZATION CHART - FRANSABANK SAL

Corporate Governance

Boardof Directors

Chairman &Deputy Chairman

Inspection

Compliance

Strategy &Development

CorporateBanking

LegalAffairs

Judicial

GeneralManager

GeneralManager

BranchNetwork

RetailBanking

LoanRecovery

RealEstate

CentralOperations

CreditReporting

& DocumentationCredit

InformationFinancialControl

& AccountingCredit

Appraisal

FRANSABANK | ANNUAL REPORT 2016 | 18-19

RiskManagement

InternalAudit

G GeneralManager

B

Policies& Procedures

InternationalBanking

Treasury &Capital Markets ICT & Projects Engineering

& Logistics Administration HumanResources

Marketing &Corporate

CommunicationOrganization

EXECUTIVE AND MANAGEMENT COMMITTEES – FRANSABANK SAL

Corporate Governance

H.E. Mr. Adnan Kassar Chairman General Manager

& or

Mr. Adel Kassar Deputy Chairman General Manager

Mr. Nadim Kassar General Manager

Mr. Mansour Bteish General Manager

Mr. Nabil Kassar General Manager

H.E. Mr. Walid Daouk, Esq.

Mr. Nabih Saddy Group Chief Financial Officer

Miss Mona Khoury Group Chief Risk Officer (Non-voting Member)

Credit Committees

Asset / Liability Committee

Overseas Expansion Committee

Banking Technology Committee

Information Security Committee

Compliance Committee

Human Resources Committee

Marketing & Corporate Communication Committee

Purchasing Committee

Management Committees

Executive Committee

FRANSABANK | ANNUAL REPORT 2016 | 20-21

MANAGEMENT – FRANSABANK SAL

Mr. Nadim Kassar General ManagerMr. Mansour Bteish General ManagerMr. Nabil Kassar General ManagerDr. Mohamad Daher Deputy General Manager, Head of Corporate Banking Mr. Philippe El Hajj Deputy General Manager, Head of Retail BankingMiss Mona Khoury Deputy General Manager, Group Chief Risk OfficerMr. Nadim Moujaes Deputy General Manager, Head of Strategy & DevelopmentMr. Nabih Saddy Deputy General Manager, Group Chief Financial Officer Mr. Nabil Tannous Deputy General Manager, Head of Treasury & Capital Markets Mr. Wajdi Abi Chacra Secretary General

Mr. Georges Andraos Head of International Banking Mr. Zouheir Chouraiki Group Chief Internal AuditorMr. Fouad Khalifeh Group Chief Compliance Officer Mr. Pierre Posbic Head of OrganizationMr. Antoine Asmar Business Development Consultant, Corporate BankingMr. Roland Tabib Chief Information OfficerMr. Zakaria El Khatib Head of Inspection Mr. Fouad Helou Head of Central Operations Mrs. Dania Kassar Head of Marketing & Corporate Communication Dr. Walid Yazigi Head of Human Resources Mr. Antoine Younes Head of Credit Appraisal Mr. Antoine Zarifeh Head of Small & Medium Enterprises Mr. Khalil Assaf Head of Special CreditsMrs. Gretta Boustany Head of Trade Finance Mrs. Lama Dick Head of Local & Overseas Credit CardsMrs. Lama Ghoutaymi Head of Loan RecoveryMiss Hoda Kadi Head of Policies & Procedures Mrs. Magida Kasbani Head of AdministrationMr. Adel Moubarak Head of Security & Business ContinuityMr. Roger Abboud Head of Credit InformationMrs. Dalal Halabi Head of Credit Reporting & DocumentationMr. Nagi Makhlouf Head of Engineering & Logistics Me. Joumana Oueidat Head of Judicial Mrs. Sawsan Rawda Head of Consumer Protection

Mr. Joseph Akiki Head of Branch Management, Regional Manager, Hamra Main Branch

Mrs. Najwa Sandid Regional Manager, Beirut IMr. Antoine Nehmeh Regional Manager, Beirut IIMr. Francis Abi Nakhoul Regional Manager, Mount Lebanon, Group AMr. Georges Saliba Regional Manager, Mount Lebanon, Group BMr. Amine Abou Mhaya Regional Manager, BekaaMr. Assaad Fadel Regional Manager, SouthMr. Nazih Chaarani Regional Manager, NorthMr. Farouk Chreif Area Manager, BekaaMr. Raed Hajj Area Manager, Beirut I

H.E. Mr. Adnan Kassar Chairman General Manager

Mr. Adel Kassar Deputy Chairman General Manager

General Management

Management

Local Network Management

LOCAL BANKING SUBSIDIARIESBoard of Directors and General Managers

Corporate Governance

LEBANON

BLC BANK SAL

Board of DirectorsH.E. Mr. Maurice Sehnaoui Chairman General Manager

Mr. Nadim Kassar Vice Chairman General Manager

H.E. Mr. Adnan Kassar Member

Mr. Adel Kassar Member

Mr. Nabil Kassar Member

H.E. Mr. Walid Daouk, Esq. Member

Mr. Mansour Bteish Member

H.E. Mr. Nazem El Khoury Member

Mr. Walid Ziade, Esq. Member

Ms. Youmna Ziade Member

H.E. Mr. Ziad Baroud, Esq. Member

Mr. Henri De Courtivron Member

General Manager Mr. Nadim Kassar

FRANSA INVEST BANK SAL

Board of DirectorsMr. Nabil Kassar Chairman General Manager

Fransabank SAL Member

Mr. Nadim Kassar Member

H.E. Mr. Walid Daouk, Esq. Member

Mr. Mansour Bteish Member

Mr. Michel Saroufim Member

Mr. Mohammed Mou'minah Member

Mr. Henri Guillemin Member

Mr. Ghantous Gemayel Member

General Manager Mr. Michel Saroufim

BLC FINANCE SAL

Board of DirectorsMr. Mansour Bteish Chairman

Fransabank SAL Member

Holding M. Sehnaoui SAL Member

General Manager Mr. Mansour Bteish

BLC SERVICES SAL

Board of DirectorsH.E. Mr. Nazem El Khoury Chairman General Manager

BLC Bank SAL Member represented by H.E. Mr. Maurice Sehnaoui

Holding M. Sehnaoui SAL Member represented by H.E. Mr. Maurice Sehnaoui

H.E. Mr. Walid Daouk, Esq. Member

Mr. Walid Ziade, Esq. Member

Mr. Khaled Salman Member

General Manager H.E. Mr. Nazem El Khoury

FRANSABANK | ANNUAL REPORT 2016 | 22-23

OVERSEAS BANKING SUBSIDIARIES & ASSOCIATEBoard of Directors and General Managers

BELARUS

FRANSABANK OJSC

Supervisory BoardH.E. Mr. Adnan Kassar Chairman,

representing Fransabank SAL

Mr. Adel Kassar Deputy Chairman, representing Fransa Holding SAL

Mr. Georges Andraos Member, Independent Director

Mr. Ghantous Gemayel Member, Independent Director

General Manager Mr. Alexandr Ignatov

FRANCE ALGERIA

FRANSABANK (FRANCE) SA

Board of DirectorsMr. Adel Kassar Chairman

BPCE IOM, Deputy Chairman represented by Mr. Philippe Garsuault

Fransabank SAL, Memberrepresented by Mr. Nabil Kassar

H.E. Mr. Adnan Kassar Member

Mr. Mansour Bteish Member

H.E. Mr. Walid Daouk, Esq. Member

Mr. Yvan de La Porte du Theil Member

Mrs. Patricia Lantz Member

Mr. Henri de Courtivron Member

General Manager Mr. Andre Tyan

CYPRUS

USB BANK PLC (Subsidiary of BLC Bank)

Board of DirectorsH.E. Mr. Maurice Sehnaoui Chairman Non Independent, Non-Executive (BLC Bank)

Mr. Nadim Kassar Vice Chairman Non Independent, Non-Executive (BLC Bank)

Fransa Invest Bank SAL, Non Independent, Non-Executiverepresented by Mr. Mansour Bteish (Fransa Invest Bank SAL being a shareholder in BLC Bank)H.E. Mr. Ziad Baroud, Esq. Independent, Non-ExecutiveMr. Henri Guillemin Independent, Non-ExecutiveMr. Agis Taramides Independent, Non-ExecutiveMr. George Galatariotis Independent, Non-ExecutiveMr. George Stylianou Independent, Non-ExecutiveMr. Philippos Philis Independent, Non-ExecutiveMr. Andreas Theodorides Non Independent-Executive Mrs. Despo Polycarpou Non Independent-Executive

General Management Mr. Andreas Theodorides, CEO

SUDAN

UNITED CAPITAL BANK

Board of DirectorsMr. Mohamad Al Adasani Chairman representing Aref Investment Group

Mr. Mansour Bteish Vice Chairman Mr. Abdul Salam Alsaleh Member representing Boubyan BankMr. Ghanem Al Ghanem Member representing Aref Investment Group

Mr. Yousuf El-Thuwaihk Member representing Aref Investment Group

Mrs. Amira Al Alami Member representing Financial Company for Investment and Development - Egypt

Mr. Al Sherif Badur Member Independent DirectorProf. Ahmed Majzoub Ahmed Member Independent DirectorMr. Yousif Ahmed El-Tinay Member General Manager Mr. Yousif Ahmed El-Tinay

FRANSABANK EL DJAZAÏR SPA

Board of DirectorsMr. Nadim Kassar Chairman

Fransabank SAL, Memberrepresented by Mr. Nabil Kassar

CMA CGM SA, Memberrepresented by Mr. Raja Sarkis

Merit Corporation SAL, Memberrepresented by Mr. Raja Sarkis

H.E. Mr. Walid Daouk, Esq. Member

Mr. Mansour Bteish Member

General Manager Mr. Mohammed Tifour

INHALE THEFUTUREOF AN

UNCEASINGLEGACY

INHALE THEFUTUREOF AN

UNCEASINGLEGACY

FRANSABANK | ANNUAL REPORT 2016 | 24-25

H I S T O R I C A L

M I L E S T O N E S

Fransabank issued itsSeries "A" preferredshares for USD 100 millionas additional Tier 1 capital.

Fransabank acquiredFransabank OJSC - Belarus, formerly knownas Golden Taler Bank.

Fransabank was first established in Beirut as afull branch of one of themajor French banks then,Crédit Foncier d’Algérie etde Tunisie (C.F.A.T.).

Fransabank is registeredn° 1 on the list of banksoperating in Lebanon indicating that it is theoldest Bank in the country.

Société Centrale deBanque in Beirut was acquired by BanqueFrançaise pour le Moyen-Orient SAL (B.F.M.O.), aLebanese company whoseshares were predomi-nantly owned by BanqueIndosuez Group.

C.F.A.T. changed itsname to Société Centrale de Banque.

Banque Indosuez (nowCrédit Agricole Corporateand Investment Bank –CACIB which is the investment arm of CréditAgricole SA) was also themajor shareholder ofBanque Sabbag SAL.Banque Indosuez mergedthese two banks underthe name of BanqueSabbag et Française pourle Moyen-Orient SAL.

The Bank’s denominationwas changed to FransabankSAL.

Fransabank concluded a cooperation agreementwith Crédit Agricole SA –France. It led at first to thejoint creation in Paris of Fransabank (France) SA,and to the participation ofCrédit Agricole SA - Francein the shareholding ofFransabank SAL. In linewith its global strategy,Crédit Agricole SA exited from Fransabank(France) SA in 2007 andfrom Fransabank SALshareholding in 2012.

Fransabank acquired37.067% in BBAC SAL.

Fransabank acquired allthe shares of Banque dela Békaa SAL. Subsequently, in 2007,the Bank sold Banque dela Békaa as an emptyshell.

Fransabank was the firstLebanese Bank to enterthe Algerian market withthe opening of its subsidiary Fransabank El Djazaïr SPA.

Fransabank launched itsoperations in Sudanthrough an associatebank, United CapitalBank.

Fransabank acquired BLCBank SAL along with itstwo subsidiaries, BLC Services SAL and BLC Finance SAL.

Fransabank concurrentlypurchased 34% of theshare capital of Fransabank (France) SAheld by Crédit Agricole SA(bringing its participationin the share capital to100%), and sold 40% of theshare capital of Fransabank (France) SA to Financière Océor, a subsidiary of GroupeCaisse d’Epargne (France) -currently BPCE, following which the Bank’sparticipation in the share capital of Fransabank (France) SA became 79.21% as fromMarch 2016.

Fransabank acquired United Bank ofSaudi & Lebanon SAL.

Banque Indosuez soldits shares in BanqueSabbag et Françaisepour le Moyen-OrientSAL to a financial groupheaded by Messrs.Adnan & Adel Kassar.

1921

HISTORICAL MILESTONES

2002 2003 2005 2006 2007 2008

1963 1971 1978 1980 1984

FRANSABANK | ANNUAL REPORT 2016 | 26-27

Fransabank acquired BanqueTohmé sal.

A private placementof shares took place,pursuant to which5% of the Bank’sshares were sold toLebanese, Arab andforeign investors.

The Public Institutionfor Social Security –Kuwait, acquired 2%of the Bank’s sharecapital.

Fransabank concluded an agreement withDeutsche Investitions- und Entwicklungs-gesellschaft mbH(DEG), which led tothe acquisition byDEG of 5% of theBank’s share capital.

Fransabank established theLebanese LeasingCompany SAL.

Fransabank acquired Universal Bank sal.

Fransabank issued its Series "B" preferredshares for USD 85million as additionalTier 1 capital.

BLC Bank SAL acquired 9.9% of USB Bank PLC – Cyprusand increased thisshare gradually toreach 99.25% in July2016.

Fransabank celebrated its 90years anniversary oflegacy and expertise.

Fransabank issuedits Series "C" preferred shares forUSD 75 million asadditional Tier 1capital.

BLC Bank opened itsrepresentative office in Abu Dhabi.

Fransabank acquired the assets & liabilities ofChase ManhattanBank’s branches inBeirut.

Fransa Invest Bank(FIB), the investment banking subsidiary ofFransabank started itsoperations.

Fransabank has setup a China Deskwith the objectiveto promote and facilitate exchangesbetween Lebanon andChinese businessmenby using Fransabankplatform.

Fransabank and Predica SA – the insurance arm ofCrédit Agricole SA –France established Bancassurance SAL.

Fransabank inaugurated its twonew branches in Baghdad and in Erbil-Kurdistan, Iraq.

Fransabank acquired and mergedAhli International Bank SAL.

Fransabank issued itsSeries "D" preferredshares for USD 85 million as additionalTier 1 capital.

Fransabank redeemedits Series "A" preferredshares for USD 100 million and issued Series "E" preferredshares for USD 105 million as additionalTier 1 capital.

Fransabank establisheda representative officein Abidjan - Ivory Coast.

2010 2011 2012 2013 2014 2015

1985 1993 1995 1997 1998 1999 2001

SAVORTHE GREATMOMENTS

OFACCOMPLISHMENT

SAVORTHE GREATMOMENTS

OFACCOMPLISHMENT

SAVORTHE GREATMOMENTS

OFACCOMPLISHMENT

SAVORTHE GREATMOMENTS

OFACCOMPLISHMENT

FRANSABANK | ANNUAL REPORT 2016 | 28-29

M A N A G E M E N T

R E P O R T

LEBANON’S ECONOMIC PERFORMANCE IN 2016

Management Report

Lebanon’s macro economy recorded a relative improvementand better performance in 2016 relative to 2015 due mainly tomore favorable domestic political environment and a decelerationof regional turmoil. This was accompanied by an improvingperformance in the main pillars of the Lebanese economy: thereal-estate sector, the monetary and financial situations, thestrong capital inflows and the balance of payments.

The real sector experienced an improved performance in 2016relative to 2015. The number of real-estate transactionsincreased by 1.4% to reach 64,248 transactions in 2016. Also,the value of real-estate transactions grew by 4.9% to reachUSD 8.4 billion during the same period. The constructionpermits, an indicator of future construction activity and futuresupply in the real-estate sector, slightly decreased by 0.9% toreach 12.2 million square meters in 2016.

Concerning the activity of Beirut International Airport, anindicator of the tourism activity, the total number of passengersincreased by 5.5% to reach 7.6 million passengers in 2016;while hotel occupancy rate, an indicator of hotel activity andtourism as well, increased slightly by 1% to reach 59% in 2016.In general, the tourism activity was healthier in 2016 ascompared to 2015, with the number of tourists increasing

by 11.2% on annual basis to reach nearly 1.7 million touristsin 2016.

In parallel, the banking sector maintained its steady growth in2016, along with relatively better performance for the BeirutStock Exchange (BSE). The banking activity, as provided by theconsolidated balance sheet of commercial and MLT banks inLebanon, has improved in 2016, with consolidated assetsrecording USD 209 billion at end of December 2016, anincrease of 9.7% from the end of December 2015. The sector’sassets constituted nearly 410% of GDP in 2016 relative to 385%in 2015, one of the highest ratios worldwide. Deposits of theprivate sector increased by 7% during this period, reachingUSD 164.5 billion at the end of December 2016 as comparedto USD 153.7 billion at the end of December 2015. Total loansto the private sector increased by 5.4% to USD 58.6 billion atthe end of December 2016, compared to USD 55.6 billion at theend of December 2015, while total loans to the public sectorreached USD 35.4 billion at the end of December 2016, comparedto USD 38.3 billion at the end of December 2015, registering adecrease of 7.6%.

The commercial and MLT banks’ capital base rose by 9.5% toreach USD 19.6 billion at the end of 2016, reflecting a growingcapitalization of the sector.

BANKING SECTOR INDICATORS (COMMERCIAL AND MLT BANKS)

Total assets Total deposits of private sector Total loans to the private sector Total loans to the public sector Banks’ capital base

190.5153.755.638.317.9

+ 9.7%+ 7%

+ 5.4%- 7.6%+ 9.5%

209164.558.635.419.6

2016In billion of USD 2015 Variation

BSE’s activity in 2016 mirrored the activity of the capital market,which was superior to the year 2015. The total trading volumeof BSE increased by 46.8% on an annual basis reaching109.5 million shares at end-2016. The aggregate turnoverincreased by 50% to reach USD 943.2 million during the sameperiod; and the average daily value of trading surged by 49.4%to reach USD 3.90 million at end-2016.

In addition, market capitalization increased by 6.1%, fromUSD 11.22 billion at end-2015 to USD 11.90 billion at end-2016.Its ratio to GDP reached 23.3% at end-2016, reflecting a narrowcapital market in Lebanon. Market capitalization continues tobe dominated by banking stocks, followed by real-estatestocks, and industrial stocks.

BEIRUT STOCK EXCHANGE INDICATORS

Market capitalization (USD, billion)Total trading volume (Shares, million)Aggregate turnover (USD, million)Average daily trading value (USD, million)

11.2274.66292.61

+ 6.1%+ 46.8%+ 50%

+ 49.4%

11.90109.5943.23.90

2016 2015 Variation

Sources: Central Bank of Lebanon and Association of Banks in Lebanon

Sources: BSE and Central Bank of Lebanon

The fiscal conditions remain unfavorable in light of continuedfiscal deficits and growing public indebtedness and the crowding-out effect of private investment initiated and fueled by publicborrowing.

In view of that, public deficit registered USD 5 billion in the year2016, increasing by 28.2% from the year 2015. When deflatedby GDP, the fiscal deficit constituted nearly 9.8% in 2016,relative to 7.9% in 2015. Public revenues increased by 3.1% in2016, but was counterbalanced with a growth in public spendingby 10.4% during the period mentioned above. As a result ofthese developments on the fiscal front, public indebtedness,

increased by 6.5% in gross debt figures over 2015 reachingUSD 74.9 billion at the end of 2016.

Excluding the public sector’s deposits at the Lebanese BankingSystem from the gross debt figures, the net public debtincreased by 6.2% on annual basis to reach USD 65.4 billion atend-December 2016.

On the other hand, the gross debt-to-GDP ratio increased overthe past two years, from 142% in 2015 to 146.9% in 2016. Theseratios are very high by international standards and clearly reflectthe deep fiscal imbalances in Lebanon’s national accounts.

FRANSABANK | ANNUAL REPORT 2016 | 30-31

PUBLIC FINANCE INDICATORS

Public revenues Public expenditures Fiscal deficit Deficit / Expenditures (%) Gross public debt Net public debt Gross public debt / Nominal GDP (%)

9.613.53.9

28.970.361.6142

+ 3.1%+ 10.4%+ 28.2%

-+ 6.5%+ 6.2%

-

9.914.9

533.674.965.4146.9

2016In billion of USD 2015 Variation

Sources: Ministry of Finance and Central Bank of Lebanon

MONETARY SITUATION INDICATORS

Central Bank of Lebanon’s assets in foreign currency Central Bank of Lebanon’s gold reserves Financial sector depositsConsumer Price Index (CPI variation) (%)

35.99.8

72.9- 3.75

+ 10.3%+ 9.2 %+ 14.4%

-

39.610.783.4

- 0.82

2016In billion of USD 2015 Variation

Sources: Central Bank of Lebanon, Association of Banks in Lebanon, and Central Administration of Statistics

FOREIGN TRADE SECTOR INDICATORS

Exports Imports Trade deficit Capital inflows Balance of payments

2.9518.0715.1211.7- 3.4

+ 1%+ 3.5%+ 4%

+ 44.4%-

2.9818.7115.7316.9+ 1.2

2016In billion of USD 2015 Variation

Sources: Higher Customs Council and Central Bank of Lebanon

The monetary authorities have maintained their monetarystabilization and economic stimulus policies during 2016. Also,financial engineering policies were a major focus of the monetaryauthorities in 2016 which reflected positively on the bankingsystem and economy.

Actually, the second half of 2016 witnessed substantial financialinflows driven by the financial engineering operations of theCentral Bank directed to strengthen Lebanon’s foreign assetsand to support the balance sheets of operating banks. Swapoperations between the Central Bank of Lebanon and theMinistry of Finance and between banks and the Central Bankreached around USD 13 billion, raising the Central Bank foreigncurrency denominated assets by 10.3% at the end of 2016 to arecord high of USD 39.6 billion, as compared to USD 35.9 billionat the end of 2015. These operations enhanced the Central

Bank’s foreign-currency reserves, the growth of non-residentdeposits of banks, the banks’ liquidity in Lebanese pounds, and thebanks’ capitalization base and ratios. In addition, gold reserveswere valued at USD 10.7 billion in 2016, as compared toUSD 9.8 billion in 2015. In contrast, the financial sector depositsat the Central Bank reached USD 83.4 billion at end-2016,as compared to USD 72.9 billion at end-2015, with an increaseof 14.4%.

Due to the moderate growth rate recorded and falling oil prices,Lebanon has continued to experience deflation in 2016. Conse-quently, the Consumer Price Index decreased by 0.82% on averagein 2016 as compared to 3.75% in 2015; while the Beirut TradersAssociation-Fransabank Retail Index stood at 54.78 for the fourthquarter of the year 2016 with a minor decrease as compared to55.56 for the fourth quarter of the year 2015.

The balance of payments, mirroring the aggregate foreign sectoractivity, recorded better activity in 2016 relative to 2015, due tothe substantial increase in capital inflows which resulted in anoffsetting of the trade deficit and produced a substantial surplusin the balance of payments.

The trade deficit widened by a moderate growth rate of 4% onannual basis and reached USD 15.73 billion in 2016, as comparedto USD 15.12 billion in 2015, thus reflecting a radical and continuedforeign deficit which represented nearly 31% of GDP in 2016. Thisminor increase in trade deficit was the result of a weak growthin exports of 1% on annual basis reaching USD 2.98 billion in2016, as compared to USD 2.95 billion in 2015, and a growth in

imports of 3.5% reaching USD 18.71 billion in 2016, as comparedto USD 18.07 billion in 2015.

The year 2016 experienced a substantial level of capital inflowsrecording nearly USD 16.9 billion relative to a level of USD 11.7 billionin 2015, an annual increase of 44.4%. These capital inflows wereinduced by a lowering regional turmoil and political tension inLebanon.

The balance of payments achieved a considerable surplus in2016, recording USD 1.2 billion relative to a substantial deficit ofUSD 3.4 billion a year earlier. The surplus recorded in 2016 wasthe first annual surplus since 2010, as the period 2011-2015 experienced continuous deficits.

Economic growth recorded in 2016: 1% according to theInternational Monetary Fund (IMF) and 1.4% according to theInstitute of International Finance (IIF). Economic growth isexpected to continue in 2017 and 2018, with enhanced real

growth rates and controlled inflation rates. Real economicgrowth is estimated at 2% for 2017 and 2.5% for 2018 accordingto the IMF, and 3.3% and 3.5% respectively for 2017 and2018 according to the IIF.

AVERAGE VOLUME OF INTEREST-EARNING ASSETS

Investment securitiesBanks and financial institutionsLoans and advances to customers TOTAL

10,580,883,5317,146,421,7558,400,772,677

26,128,077,963

11,170,362,7057,298,327,3909,049,450,822

27,518,140,917

2016In thousands of LBP 2015

1. NET INCOME

In 2016, Fransabank SAL net income, amounted toLBP 189.40 billion (USD 125.64 million) compared toLBP 184.34 billion (USD 122.28 million) in 2015, an increase of2.75%. This has translated into a Return on Average Assets of0.90% and a Return on Average Common Equity of 9.46%.

In 2016, the Group’s net income amounted to LBP 302.94 billion(USD 200.95 million) compared to LBP 270.78 billion(USD 179.62 million) in 2015, an increase of 11.88%. This hastranslated into a Return on Average Assets of 0.98% anda Return on Average Common Equity of 11.21%.

BREAKDOWN OF INTEREST RECEIVED

In 2016, the Group’s monthly average interest-earning assetsreached LBP 27,518.14 billion (USD 18,254.16 million)compared to LBP 26,128.08 billion (USD 17,332.06 million) in2015 (+ 5.32%). This growth is due to the increase in:- investment securities (+ LBP 589.48 bill ion or c/vUSD 391.03 million),

- loans and advances to customers (+ LBP 648.68 billion or c/vUSD 430.30 million),

- loans to banks and financial institutions plus placementswith banks and financial institutions (+ LBP 151.90 billion orc/v USD 100.77 million).

OverviewIn 2016, the Lebanese economy grew at a marginally higher pace than last year, despite the challenging regional and local marketconditions. Nevertheless, the Lebanese banking sector sustained its growth proving once again its resilience. Similar to the previousyear, Fransabank Group has managed to achieve another satisfactory performance in 2016 backed by a dynamic, well-perceivedand efficiently implemented business strategy.

From loans and advances to customersFrom investment securitiesFrom loans to banks and placements with banksFrom investments at FVTPL TOTAL

636,741,639682,003,635242,587,37748,888,397

1,610,221,048

662,948,953726,164,749243,578,63441,351,223

1,674,043,559

2016In thousands of LBP 2015

1.1 Net Interest Income

In 2016, the Group’s net interest income amounted toLBP 591.24 billion (USD 392.20 million) compared toLBP 597.04 billion (USD 396.04 million) in 2015, a slightdecrease of 0.97%. This decrease is due to the fact thatthe increase during 2016 in interest expense was greater thanthat in interest received.

In 2016, the Group’s interest received amounted to

LBP 1,674.04 billion (USD 1,110.48 million) compared toLBP 1,610.22 billion (USD 1,068.14 million) in 2015, an increase of3.96%. Interest received from loans and advances to customers,investment securities, loans to banks & placements withbanks and investments at Fair Value Through Profit or Loss(FVTPL), represents 39.60%, 43.38%, 14.55% and 2.47%respectively of total 2016 interest income, compared to 39.54%,42.35%, 15.07% and 3.04% respectively in 2015.

CONSOLIDATED RESULTS OF OPERATIONS

Management Report

In 2016, the Group’s interest paid amounted to LBP 1,082.80 billion(USD 718.28 million) compared to LBP 1,013.18 billion(USD 672.10 million) in 2015 (+ 6.87%). In 2016, the largest

single component of interest paid belongs to customers’deposits, which represents 96.98% of the total comparedto 95.86% in 2015.

In 2016, the Group’s monthly average interest-bearing liabilitiesreached LBP 26,516.83 billion (USD 17,589.94 million) comparedto LBP 25,316.21 billion (USD 16,793.51 million) in 2015 (+ 4.74%).

This growth is largely attributed to an increase in the customers’creditor accounts at amortized cost of 6.28%, i.e. LBP 1,467.50 billion(USD 973.47 million).

BREAKDOWN OF INTEREST PAID

FRANSABANK | ANNUAL REPORT 2016 | 32-33

On deposits and borrowings from banks On deposits from customers and related parties at amortized costOn deposits from customers designated at FVTPLOn obligation under finance leaseOn subordinated loansOn bonds issued and Certificates of depositsOn cash contribution to Share Capital

TOTAL

(37,169,074)(969,306,289)

(1,931,890)(325,744)

(3,168,868)(255,015)

(1,026,833)

(1,013,183,713)

(28,999,146)(1,046,538,245)

(3,525,103)(469,809)

(2,236,993)(7,535)

(1,026,833)

(1,082,803,664)

2016In thousands of LBP 2015

AVERAGE VOLUME OF INTEREST-BEARING LIABILITIES

BDL, Banks and financial institutionsLiabilities designated at FVTPLCustomers’ creditor accounts at amortized costBonds issued and Certificates of depositsSubordinated loansCash contribution to Share Capital

TOTAL

1,843,667,36039,185,175

23,367,774,2446,374,884

42,095,01617,113,885

25,316,210,564

1,564,237,58069,938,336

24,835,278,5564,225

30,256,57417,113,885

26,516,829,156

2016In thousands of LBP 2015

1.2 Net Fee and Commission Income

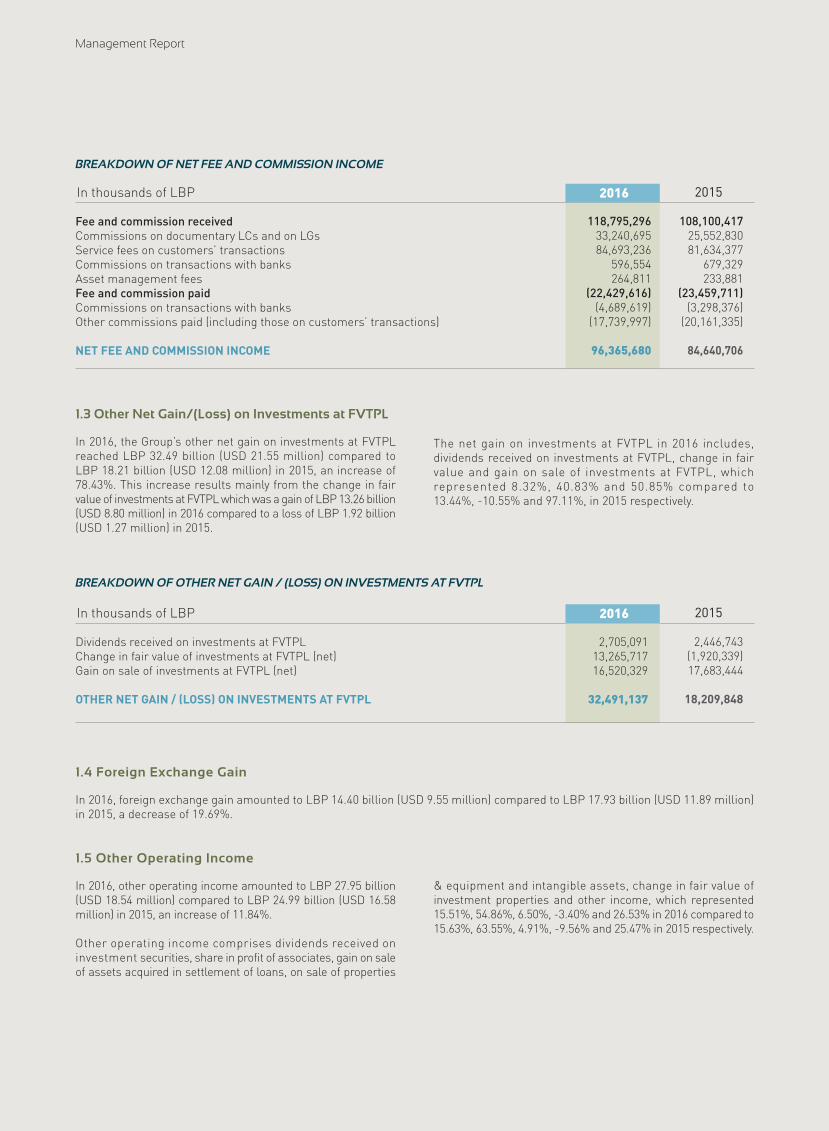

In 2016, the Group’s net fee and commission income reachedLBP 96.37 bill ion (USD 63.92 million) compared toLBP 84.64 billion (USD 56.15 million) in 2015, an increaseof 13.85%.

Fees and commissions received in 2016 reached LBP 118.80 billion(USD 78.80 million) compared to LBP 108.10 bill ion(USD 71.71 million) in 2015, an increase of 9.89%.

Fees and commissions received in 2016 comprise mainly feeson customers’ transactions and commissions on documentary

LCs and on LGs, which represented 71.29% and 27.98%respectively compared to 75.52% and 23.64% in 2015.

Fees and commissions paid in 2016 reached LBP 22.43 billion(USD 14.88 million) compared to LBP 23.46 bill ion(USD 15.56 million) in 2015, a decrease of 4.39%.

Fees and commissions paid in 2016 comprise fees on customers’transactions and commissions on transactions with banks,which represents 79.09% and 20.91% respectively comparedto 85.94% and 14.06% in 2015.

Management Report

1.3 Other Net Gain/(Loss) on Investments at FVTPL

In 2016, the Group’s other net gain on investments at FVTPLreached LBP 32.49 billion (USD 21.55 million) compared toLBP 18.21 billion (USD 12.08 million) in 2015, an increase of78.43%. This increase results mainly from the change in fairvalue of investments at FVTPL which was a gain of LBP 13.26 billion(USD 8.80 million) in 2016 compared to a loss of LBP 1.92 billion(USD 1.27 million) in 2015.

The net gain on investments at FVTPL in 2016 includes,dividends received on investments at FVTPL, change in fairvalue and gain on sale of investments at FVTPL, whichrepresented 8.32%, 40.83% and 50.85% compared to13.44%, -10.55% and 97.11%, in 2015 respectively.

1.4 Foreign Exchange Gain

In 2016, foreign exchange gain amounted to LBP 14.40 billion (USD 9.55 million) compared to LBP 17.93 billion (USD 11.89 million)in 2015, a decrease of 19.69%.

1.5 Other Operating Income

In 2016, other operating income amounted to LBP 27.95 billion(USD 18.54 million) compared to LBP 24.99 billion (USD 16.58million) in 2015, an increase of 11.84%.

Other operating income comprises dividends received oninvestment securities, share in profit of associates, gain on saleof assets acquired in settlement of loans, on sale of properties

& equipment and intangible assets, change in fair value ofinvestment properties and other income, which represented15.51%, 54.86%, 6.50%, -3.40% and 26.53% in 2016 compared to15.63%, 63.55%, 4.91%, -9.56% and 25.47% in 2015 respectively.

BREAKDOWN OF NET FEE AND COMMISSION INCOME

Fee and commission receivedCommissions on documentary LCs and on LGsService fees on customers’ transactionsCommissions on transactions with banksAsset management feesFee and commission paidCommissions on transactions with banksOther commissions paid (including those on customers’ transactions)

NET FEE AND COMMISSION INCOME

108,100,41725,552,83081,634,377

679,329233,881

(23,459,711)(3,298,376)

(20,161,335)

84,640,706

118,795,29633,240,69584,693,236

596,554264,811

(22,429,616)(4,689,619)

(17,739,997)

96,365,680

2016In thousands of LBP 2015

BREAKDOWN OF OTHER NET GAIN / (LOSS) ON INVESTMENTS AT FVTPL

Dividends received on investments at FVTPLChange in fair value of investments at FVTPL (net)Gain on sale of investments at FVTPL (net) OTHER NET GAIN / (LOSS) ON INVESTMENTS AT FVTPL

2,446,743(1,920,339)17,683,444

18,209,848

2,705,09113,265,71716,520,329

32,491,137

2016In thousands of LBP 2015

FRANSABANK | ANNUAL REPORT 2016 | 34-35

BREAKDOWN OF OTHER OPERATING INCOME

Dividends income on investment securitiesShare in profit of associatesGain resulting from the sale of assets acquired in settlement of loans, properties & equipmentand intangible assetsChange in fair value of investment propertiesOther OTHER OPERATING INCOME

3,904,45915,879,755

1,227,694(2,388,213)6,363,237

24,986,932

4,333,68915,330,578

1,818,344(950,806)7,414,504

27,946,309

2016In thousands of LBP 2015

NET ALLOCATION TO PROVISIONS FOR LOANS & ADVANCES TO CUSTOMERS

Allowance for impairment of loans and advances and off Balance Sheet itemsWrite-back of impairment loss on loans and advances and off Balance Sheet itemsBad debts expenseWrite-back of discount on purchased loan portfolio TOTAL

(99,054,299)37,479,478(737,415)352,865

(61,959,371)

(89,729,933)82,313,088(716,318)610,503

(7,522,660)

2016In thousands of LBP 2015

BREAKDOWN OF GENERAL EXPENSES

Staff costsAdministrative expensesDepreciation and amortization of assets TOTAL

(254,007,016)(118,977,713)(30,148,911)

(403,133,640)

(258,267,012)(118,144,447)(30,760,107)

(407,171,566)

2016In thousands of LBP 2015

In 2016, the Group’s net allocation to provisions for loans andadvances to customers amounted to LBP 7.52 billion(USD 4.99 million) compared to LBP 61.96 billion (USD 41.10 million)in 2015, a decrease of 87.86%, which may be described asfollows:

- allowance for impairment of customers’ loans and advancesand off Balance Sheet Items for LBP 89.73 bill ion(USD 59.52 million) compared to LBP 99.05 billion(USD 65.71 million) in 2015, a decrease of 9.41%,

- bad debts expense for LBP 0.71 billion (USD 0.48 million),compared to LBP 0.74 billion (USD 0.49 million) in 2015,

- write-back of impairment loss on loans and advances and offBalance Sheet Items for LBP 82.31 billion (USD 54.60 million),against LBP 37.48 billion (USD 24.86 million) in 2015, anincrease of 119.62%,

- write-back of discount on purchased loan portfolio forLBP 0.61 billion (USD 0.41 million) against LBP 0.35 billion(USD 0.24 million) in 2015, an increase of 73.01%.

1.7 General Expenses

In 2016, the Group’s general expenses comprising staff costs,administrative expenses, depreciation and amortization ofassets, reached LBP 407.17 billion (USD 270.10 million)compared to LBP 403.13 billion (USD 267.42 million) in 2015,an increase of 1% . This increase is due to the following :

- salaries and related charges amounted to LBP 258.27 billion(USD 171.32 million) in 2016 compared to LBP 254 billion(USD 168.50 million) in 2015, an increase of 1.68%,

- administrative expenses amounted to LBP 118.14 billion(USD 78.37 million) in 2016 compared to LBP 118.98 billion(USD 78.92 million) in 2015, a decrease of 0.70%,

- depreciation and amortization of assets amounted toLBP 30.76 billion (USD 20.41 million) in 2016 comparedto LBP 30.15 billion (USD 20 million) in 2015, an increase of2.03%.

1.6 Net Allocation to Provisions for Loans & Advances to Customers

Management Report

1.8 Income Tax and Deferred Tax

The Group’s income tax for the financial year 2016 amountedto LBP 53.98 billion (USD 35.81 million), compared toLBP 58.58 billion (USD 38.86 million) for the financial year2015, a decrease of 7.86%. Deferred tax on associates and

subsidiaries’ profits for the financial year 2016 amounted toLBP 9.15 billion (USD 6.07 million), compared to LBP 8.02 billion(USD 5.32 million) for the financial year 2015, an increase of13.99%.

Soft loans from Banque du LibanLong-term borrowingsBanks and financial institutionsCustomers’ creditor accounts at FVTPLCustomers’ creditor accounts at amortized costSubordinated loanShareholders’ equity

TOTAL

BREAKDOWN OF FUNDING SOURCES AS AT 31 DECEMBER

1.10%4.46%1.00%0.16%

83.17%0.11%

10.00%

100%

323,290,6681,315,013,895295,311,93648,867,277

24,533,805,85631,874,580

2,949,177,947

29,497,342,159

%Amount

273,537,647997,881,769285,611,112136,487,357

25,501,689,77225,499,664

3,206,549,007

30,427,256,328

0.90%3.28%0.94%0.45%

83.81%0.08%

10.54%

100%

Amount %

2016In thousands of LBP 2015

Lebanese PoundsU.S. DollarsEurosOther foreign currencies

TOTAL

FUNDING SOURCES BY CURRENCY AS AT 31 DECEMBER

43.90%47.16%7.26%1.68%

100%

12,949,529,79613,911,098,0772,140,486,375496,227,911

29,497,342,159

%Amount

13,480,881,26714,119,528,8062,197,014,257629,831,998

30,427,256,328

44.31%46.40%7.22%2.07%

100%

Amount %

2016In thousands of LBP 2015

2.1 Funding Sources

As at 31 December 2016, the Group’s funding sourcesamounted to LBP 30,427.79 billion (USD 20,183.92 million)compared to LBP 29,497.34 billion (USD 19,567.06 million) asat 31 December 2015, an increase of 3.15%.

Similar to all other banks in Lebanon, the principal source offunding is customers’ creditor accounts which representedas at 31 December 2016, 84.26% of total funding sources

as compared to 83.33% as at 31 December 2015. Other fundingsources include in addition to the shareholders’ equity whichincludes preference shares, long-term credit lines provided byinternational banks and financial Institutions, deposits ofbanks and financial institutions, subordinated loans and softloans granted by Banque du Liban for the Bank mergers andacquisitions according to the pertinent Lebanese Law ofmergers and acquisitions.

2. TOTAL BALANCE SHEET

As at 31 December 2016, the Group’s Total Balance Sheet amounted to LBP 31,438.32 billion (USD 20,854.61 million) compared toLBP 30,140.45 billion (USD 19,993.66 million) as at year-end 2015, an increase of 4.31%. As at 31 December 2016, theGroup maintained its 3rd rank within the Lebanese banking sector in terms of Total Balance Sheet same as at 31 December 2015.Market share reached 9.36% as at 31 December 2016 compared to 9.85% as at 31 December 2015.

FRANSABANK | ANNUAL REPORT 2016 | 36-37

As at 31 December 2016, 55.69% of the Bank’s major funding sources were denominated in foreign currencies, as compared to56.10% as at 31 December 2015.

Short-term funding (less than 1 year)Medium-term funding (between 1 & 5 years)Long-term funding (more than 5 years)

TOTAL

FUNDING SOURCES BY MATURITY AS AT 31 DECEMBER

86.72%1.72%

11.56%

100%

25,581,376,443505,985,969

3,409,979,747

29,497,342,159

%Amount

25,963,293,028615,534,784

3,848,428,516

30,427,256,328

85.33%2.02%

12.65%

100%

Amount %

2016In thousands of LBP 2015

Customers’ Creditor Accounts

As at 31 December 2016, the Group’s customers’ creditoraccounts at FVTPL and at amortized cost amounted toLBP 25,638.18 billion (USD 17,007.08 million) compared toLBP 24,582.67 billion (USD 16,306.91 million) as at 31December 2015, an increase of 4.29%.

The 4.29% increase was mainly due to the growth in (i) timesaving accounts of LBP 463.15 billion (USD 307.23 million),in ( i i ) term deposits accounts of LBP 446.58 bill ion(USD 296.24 million), in (iii) demand and sight saving accountsof LBP 169.93 billion (USD 112.72 million), in (iv) Customers’

liabilities at Fair Value Through Profit or Loss of LBP 87.62 billion(USD 58.12 million), and in (v) margins and collateral accountsof LBP 85.91 billion (USD 56.99 million). As at 31 December2016, customers’ creditor accounts represent 81.55% of theGroup’s Total Balance Sheet as compared to 81.56% as at31 December 2015.

As at 31 December 2016, the Group maintained its 4th rankwithin the Lebanese banking sector in terms of customers’creditor accounts, with a market share of 9.41% comparedto 9.69% as at 31 December 2015.

BREAKDOWN OF CUSTOMERS' CREDITOR ACCOUNTS BY TYPE AS AT 31 DECEMBER

Customers’ Liabilities at Fair Value Through Profit or Loss (FVTPL)Customers’ liabilities at Fair Value Through Profit or LossRelated parties’ liabilities at Fair Value Through Profit or LossAccrued interestCustomers’ Creditor Accounts at Amortized CostDemand and sight saving accountsTime saving accountsTerm depositsBlocked accountsMargins and collateral accountsRelated parties accountsAccrued interest

TOTAL CUSTOMERS’ CREDITOR ACCOUNTS AT FVTPL & AT AMORTIZED COST

Lebanese PoundsForeign currencies

48,867,27748,485,734

-381,543

24,533,805,8562,392,904,616

13,369,995,9104,890,948,051

72,109,0481,616,394,1462,044,596,684146,857,401

24,582,673,133

39.80%60.20%

136,487,357132,613,147

2,944,192930,018

25,501,689,7722,562,832,319

13,833,140,9585,337,525,209

59,069,4391,702,308,6411,857,623,063149,190,143

25,638,177,129

39.96%60.04%

2016In thousands of LBP 2015

Management Report

BREAKDOWN OF CUSTOMERS’ CREDITOR ACCOUNTS BY AMOUNT AS AT 31 DECEMBER 2016

Amount % % Cum.

1,239,913,710874,271,380

1,176,750,7571,830,316,2712,150,193,1892,491,455,6205,629,292,124

15,392,193,051

8.06%5.68%7.64%

11.89%13.97%16.19%36.57%

8.06%13.74%21.38%33.27%47.24%63.43%

100%

Amount % % Cum.

1,484,887,7121,041,450,2221,385,468,5531,948,939,2071,733,519,9561,183,063,0131,468,655,415

10,245,984,078

14.49%10.17%13.52%19.02%16.92%11.55%14.33%

14.49%24.66%38.18%57.20%74.12%85.67%

100%

A < 50 million50 million ≤ A < 100 million

100 million ≤ A < 200 million200 million ≤ A < 500 million500 million ≤ A < 1.5 billion

1.5 billion ≤ A < 5 billionA ≥ 5 billion

TOTAL 100% 100%

BREAKDOWN OF CUSTOMERS’ CREDITOR ACCOUNTS BY INITIAL MATURITY AS AT 31 DECEMBER 2016

FCsLBP

2,724,801,4221,915,721,6022,562,219,3103,779,255,4783,883,713,1453,674,518,6337,097,947,539

25,638,177,129

10.63%7.47%9.99%

14.74%15.15%14.33%27.69%

10.63%18.10%28.09%42.83%57.98%72.31%

100%

Amount % % Cum.TOTALIn thousands of LBP

100%

Amount % % Cum.

4,501,050,7824,940,475,0593,679,915,4062,063,826,684

45,573,85077,208,60984,142,661

15,392,193,051

29.24%32.10%23.91%13.41%

0.29%0.50%0.55%

29.24%61.34%85.25%98.66%98.95%99.45%

100%

Amount % % Cum.

2,268,473,8614,817,211,0472,843,529,988

199,649,80717,538,55133,603,32465,977,500

10,245,984,078

22.14%47.02%27.75%

1.95%0.17%0.33%0.64%

22.14%69.16%96.91%98.86%99.03%99.36%

100%

P ≤ 1 month1 month < P ≤ 3 months3 months < P ≤ 12 months1 year < P ≤ 3 years3 years < P ≤ 5 years

P > 5 yearsAccrued interest

TOTAL

Number of accountsAverage per account

100% 100%

FCsLBP

6,769,524,6439,757,686,1066,523,445,3942,263,476,491

63,112,401110,811,933150,120,161

25,638,177,129

26.40%38.06%25.44%

8.83%0.25%0.43%0.59%

26.40%64.46%89.90%98.73%98.98%99.41%

100%

Amount % % Cum.TOTALIn thousands of LBP

100%

290,27335,298

325,11247,344

615,38541,662

Shareholders’ Equity

Shareholders’ equity as at 31 December 2016 amounted to LBP 3,206.55 billion (USD 2,127.06 million), compared to LBP 2,949.18 billion(USD 1,956.34 million) as at 31 December 2015, an increase of 8.73%. This increase is mainly due to the incorporation of 2016 net profitsand to the issue of a new series of preference shares by one of the Bank’s subsidiaries.

2.2 Uses of Funds

The Bank uses its funds to comply with Central Banks regulatoryreserve requirements, cash, short term placements and liquidfinancial instruments with international banks and financial

institutions, loans and advances to customers and investmentsecurities.

Cash on handCompulsory / regulatory deposits and Central BanksBanks and financial institutionsInvestment securitiesLoans and advances to customers

TOTAL

BREAKDOWN OF USES OF FUNDS AS AT 31 DECEMBER

0.80%21.70%

4.89%39.70%32.91%

100%

230,236,6856,250,477,1381,409,364,496

11,438,709,6489,480,043,915

28,808,831,882

%Amount

222,382,9417,428,205,7701,407,146,445

11,197,730,7949,849,089,736

30,104,555,686

0.74%24.67%

4.67%37.20%32.72%

100%

Amount %

2016In thousands of LBP 2015

FRANSABANK | ANNUAL REPORT 2016 | 38-39

Lebanese PoundsU.S. DollarsEurosOther foreign currencies

TOTAL

USES OF FUNDS BY CURRENCY AS AT 31 DECEMBER

45.44%45.02%

7.04%2.50%

100%

13,090,621,11512,969,557,592

2,028,544,087720,109,088

28,808,831,882

%Amount

13,693,983,56513,444,842,272

2,201,949,041763,780,808

30,104,555,686

45.49%44.66%

7.31%2.54%

100%

Amount %

2016In thousands of LBP 2015

2016In thousands of LBP 2015