Embed Size (px)

Citation preview

Cour File Number:

iL__i

IN THE SUPREME COURT OF CANADA

(ON APPEAL FROM THE COURT OF APPEAL FOR ONTARO)

IN THE MATTER OF THE COMPANIES' CREDITORSARRNGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF THE BANKRUPTCY ANDINSOLVENCY ACT, R.S.C. 1985, c. B-3, AS AMENDED

AND IN THE MATTER OFA PLAN OF COMPROMISE ORARRGEMENT OF SMURFIT -STONE CONTAINER

CANADA INC. AND THE OTHER APPLICANTS LISTED ONSCHEDULE "A"

Respondents

APPLICATION RECORDOF THE APPLICANTS, AURLIUS CAPITAL MAAGEMENT, LP

and COLUMBUS IDLL MANAGEMENT L.P.(together, the "Fund Ma.nagers")

(Filed Pursuant to Section 40 of the Supreme Court Act and Rule 25(1)(a)of the Rules of the Supreme Court of Canada)

VOLUM IPAGES 1 to 195

FRASER MILNER CASGRA LLPBarsters and Solicitors1 First Canadian Place100 King Street WestToronto ON M5X 1B2Facsimile: 416-863-4592

Neil S. RabinovitchTel: 416-863-4656

E-Mail: neil.rabinovitch~fmc-Iaw.com

Jane O. Dietrich

Tel: 416-863-4467

E-Mail: jane.dietrich~fmc-Iaw.com

Lawyers for the Applicants, AurelliusCapital Management, LP and Columbus

. Hil Capital Management, L.P.56610665JDoe

FRASER MILNER CASGRA LLPBarsters and SolicitorsSuite 142099 Ban StreetOttawa, ON KIP IH4Facsimile: 613-783-9690

K. Scott McLeanTel: 613-783-9665Email: scott.mclean~fmc-Iaw.com

Corey A. Vileneuve (Law Clerk)Tel: 613-783-9699Email: corey.vileneuve~fmc-Iaw.com

Ottawa Agents forthe Applicants, AurellusCapital Management, LP and Columbus HilCapital Management, L.P.

2

ORIGINAL TO: THE REGISTRAR

COPIES TO: STIKEMAN ELLIOT LLP5300 Commerce Cour West199 Bay StreetToronto, ON M5L IB9

Sean DunphyTel: 416-869-5662

Fax: 416-947-0866

E-mail:sdunphy(ßstikeman.com

Alexander RoseTel: (416) 869-5261

Fax: 416-947-0866

E-mail: arose(ßstikeman. com

Lawyers for Smurt-Stone Container Canada Inc.and the other Applicants Listed on Schedule A

AN TO: GOODMAS LLP333 Bay StreetSuite 3400Toronto, Ontaro M5H 2S7

Rob ChadwickTel: 416-979-2211

Fax: 416-979-1234

E-mail:rchadwick(ßgoodmans.ca

Chris ArmstrongTel: 416-979-2211

Fax: 416-979-1234

E-mail:carstrong(ßgoodmans.ca

Lawyers for Deloitte & Touche Inc.

56610665JDoe

AND TO:

AND TO:

56610665JDoe

3

BENNTT JONES LLP3400 One First Canadian PlaceP.O. Box 130Toronto ON M5X 1A4

Kevin ZychTel: 4l6-777-5738

Fax: 416-863-1716

E-mail:zychk(ßbennettjones.com

S. Richard OrzTel: 416-777-5737

Fax: 416-863-1716

E-mail:orzvr(ßbennettjones.com

Derek FruehTel: 416-777.6237

Fax: 416-863-1716

E-mail:frehd(ßbennetijones.com

Raj SahniTel: 416-777-4804

Fax: 416-863-1716

E-mail: sahr(ibennettj ones. com

Lawyers for Offcial Committee of Unsecured Creditors of Smurfit-StoneContainer Corporation, et al

THORNTON GROUT FINNGAN LLPSuite 3200, Canadian Pacific Tower100 Wellington St. West, P.O. Box 329Toronto-Dominion CentreToronto ON M5K 1K7

Robert I. ThorntonTel: 416-304-0560

Fax: 416-304-1313

E-mail:rtomton(itgf.ca

Seema AggarwalTel: 416-304-0603

Fax: 416-304-1313

E-mail:saggarwal(itgf.ca

Lawyers for the Indentue Trustee

4

SCHEDULE "A"

Smurfit-Stone Container Canada Inc.

3083527 Nova Scotia Company

MBI LimitedlLimitée

639647 British Columbia Ltd.

B.C. Shipper Supplies Ltd.

Specialty Containers Inc.

605681 N.B. Inc.

Francobec Company

Stone Container Finance Company of Canada II

56610665JDoe

n ex

Cour File Number:

IN THE SUPREME COURT OF CANADA

(ON APPEAL FROM THE COURT OF APPEAL FOR ONTARO)

IN THE MATTER OF THE COMPANIES' CREDITORSARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMNDED

AND IN THE MATTER OF THE BANKRUPTCY ANDINSOLVENCY ACT, R.S.C. 1985, c. B-3, AS AMENDED

AND IN THE MATTER OF A PLAN OF COMPROMISE ORARGEMENT OF SMUIT-STONE CONTAINER

CANADA INC. AND THE OTHER APPLICANTS LISTED ONSCHEDULE "A"

Respondents

APPLICATION FOR LEAVE TO APPEAL - TABLE OF CONTENTS

Tab Document Pages

1 Notice of Application for Leave to Appeal 1-12

2 Affdavit of Allyson Roy sworn April 8, 2010 13-17

A Exhbit "A" - CCAA Records from the website of the Offce of the 18-26Superintendent of Banptcy Canada

B Exhbit "B" - Aricle by Jans Sara, "Corporate Group Insolvencies: 27-52Seeing the Forest and the Trees" (2008) ICC-ART 2008-6 (W.L.).

C Exhbit "C" - Anotated Provisional Agenda for the Thrt-First Session 53-58ofUNCITRA Working Group V (Insolvency Law)

D Exhibit "D" - Anotated Provisional Agenda for the Thirt-Eight Session 59-65ofUNCITRA Working Group V (Insolvency Law)

56609575JDoe

11.

Tab Document Pages

E Exhbit "E" - Draft Recommendations on the Treatment of Enterprise 66-127Groups in Insolvency from the Thirt-Seventh Session ofUNCITRAWorking Group V (Insolvency Law)

3 Certificate of Counsel for the Applicants, Aurelius Capital Management, 128-131LP and Columbus Hil Capital Management, L.P.

4 Order of the Honourable Madam Justice Pepall made on December 11, 132-1362009 with respect to the motion brought by Aurelius CapitalManagement, LP and Columbus Hil Capital Management, L.P. withreasons to follow (the "December 11 th Order")

5 Order of the Honourable Madam Justice Pepall made on Januar 28,2010 137-141with respect to the motion brought by the Applicants in the CCAAProceedings (the "Januar 28th Order")

6 Reasons for Decisions of the Honourable Madam Justice Pepall dated 142-163Januar 28, 2010 with respect to the December 11 th Order and the Januar28th Order

7 Endorsement of the Ontaro Cour of Appeal with respect to the 164-165December 11 th Order application for leave to appeal to the Ontaro Courof Appeal dated March 9, 2010

8 Endorsement of the Ontario Cour of Appeal with respect to the Januar 166-16728th Order application for leave to appeal to the Ontaro Cour of Appealdated March 9,2010

9 Memorandum of Arguent of Aurelius Capital Management, LP and 168-195Columbus Hil Capital Management, L.P.

10 Affdavit of Dan Gropper sworn September 14, 2009 ("Gropper 196-207Affidavit")

A Exhbit "A" to the Gropper Affidavit - Simplified Corporate Char 208-209showig Enterprises, Finance II and Smurt Canada

B Exhbit "C" to the Gropper Affidavit - Schedule of Assets and Liabilties 210-266and Statement of Financial Affairs of Finance II

11 Affdavit of Dean Jones sworn September 21,2009 ("Jones Afdavit") 267-273

A Exhibit "A" to the Jones Affdavit - Afdavit of Dean Jones sworn 274-322Januar 25,2009 without exhbits

56609575_I.DOe

111.

Tab Document Pages

B Exhbit "E" to the Jones Affdavit - Loan Agreement dated July 20, 2004 323-330

12 Endorsement of the Honourable Madam Justice Pepall dated October 20, 331-3392009

13 Affdavit of Melissa paz sworn December 2, 2009 ("paz Affidavit") 340-345

A Excerpt from Exhbit "H" to the paz Affdavit - Offering Memorandum 346-348

14 Affdavit of Douglas R. A. McFadyen sworn December 8, 2009 349-353

15 Afdavit of Malcolm M. Mercer sworn December 9, 2009 354-361

16 Transcript Brief - Cross-Examination of Melissa paz on December 9, 362-3712009

17 Notice of Motion of the Applicants retuable December 11,2009 372-379

56609575_I.DOe

1Cour File Number:

IN THE SUPREME COURT OF CANADA

(ON APPEAL FROM THE COURT OF APPEAL FOR ONTARO)

IN THE MATTER OF THE COMPANIES' CREDITORSARRNGEMENT ACT, RS.C. 1985, c. C-36, AS AMENDED

AN IN THE MATTER OF THE BANKRUPTCY ANDINSOLVENCY ACT, RS.C. 1985, c. B-3, AS AMENDED

AND IN THE MATTER OF A PLAN OF COMPROMISE ORARGEMENT OF SMURFIT-STONE CONTAINER

CANADA INC. AND THE OTHER APPLICANTS LISTED ONSCHEDULE "A"

Respondents

NOTICE OF APPLICATION FOR LEAVE TO APPEALOF THE APPLICANTS, AURELIUS CAPITAL MANAGEMENT, LP

and COLUMUS IDLL MAAGEMENT L.P.(together, the "Fund Managers")

(Filed Pursuant to Subsection 40(1) of the Supreme Court Act and Rule 25(1)(a)of the Rules of the Supreme Court of Canada)

". .

TAKE NOTICE that the Fund Managers hereby apply for leave to appeal to the Cour pursuantto subsection 40(1) of the Supreme Court Act, RS.C. 1985, c. S-26, as amended and rule25(1)(a) of the Rules of the Supreme Court of Canada, from the Orders of the Cour of Appeal

for Ontario in cour of appeal fie nos. M38445 and M38502 made March 9, 2010, in respect ofOrders made by the Ontario Superior Cour of Justice in cour file no. CV -09-7966 on December11,2009 and January 28, 2010, for its costs of this application and for any furter or other orderthat the Cour may deem appropriate;

AND FURTHER TAK NOTICE that ths application for leave is made on the followinggrounds:

Nature of the CCAA Proceedings and the Procedural History Leading to this Application

1. Stone Container Finance Company of Canada II ("Finance II") and Smurt-Stone

Container Canada Inc. ("Smurft Canada") are applicants in proceedings under the Companies'

Creditors Arrangement Act, RS.C. 1985, c. C-36, bearing Ontaro Cour File no. CV -09-7966

56592730JDoe

22

(the "CCAA Proceedings") and debtors in related proceedings under Chapter 11 of Title 11 of

The United States Banptcy Code (the "US Proceedings").

2. Finance II issued certain 7 3/8% Senior Notes due July 15, 2014 (the "Notes") pursuant

to an indentue dated as of July 20, 2004. The Applicants for leave to appeal, Aurelius Capital

Management, LP and Columbus Hil Capital Management, L.P. (the "Fund Managers"),

manage fuds that hold a majority of the Notes.

3. Finance II loaned the US$200 milion proceeds from issuance of the Notes to Smurfit

Canada (the "Intercompany Loan") under a loan agreement dated July 20, 2004 (the "Loan

Agreement"). The Loan Agreement is governed by Quebec Law.

4. The CCAA Applicants commenced a motion within the CCAA Proceedings for a

determination by the CCAA cour as to whether Finance II's claim (the "Intercompany Claim")

against Smurt Canada under the Loan Agreement should properly be characterized as an equity

clai or a debt claim (the "Characterization Issue").

5. Prior to raising this issue, the CCAA Applicants had always treated the Intercompany

Loan as debt. However, the CCAA Applicants then took the position that the Intercompany

Loan was extinguished or converted into equity upon insolvency of Smurfit Canada.

6. All of Finance II's directors are directors or offcers of Smurfit Canada.

7. The interests of Finance II are directly adverse to those of Smurt Canada and the other

applicants in the CCAA Proceedings (the "CCAA Applicants") with respect to recovery on all

of Finance II's disclosed assets, including the Intercompany Loan.

56592730JDoe

33

8. Finance II and Smurfit Canada are represented by the same counsel in the CCAA

proceedings. Finance II and Smurfit Canada's counsel also acted as counsel on the Finance II

and predecessor Finance I loan transactions.

9. There is no evidence that Finance II's directors have received independent legal advice,

including with respect to the matters in ths proceeding. There is also no evidence that the

directors have considered whether they and their counsel are conflcted or whether the positions

being taken in the CCAA proceedings are in the best interests of Finance II.

10. Immediately prior to the retu of the motion to determine the Characterization Issue (the

"Characterization Motion"), the Fund Managers brought a cross-motion, based on the

developing record with respect to the conficts of the directors of Finance II and the conficts of

Finance II's counsel and the refusal to produce relevant information and witnesses, requesting

among other thngs that:

(a) the motions' judge appoint independent counsel for Finance II, including for the

puroses of the hearng of the Characterization Motion; and

(b) the motions' judge adjourn the Characterization Motion to permit new counsel for

Finance II to prepare for that motion and to consider whether the motion should

proceed by way of a j oint hearing with the US Banptcy Court.

11. On December 11, 2009, the motions' judge dismissed the cross-motion with reasons to

follow (the "Representation Order") and allowed the Characterization Motion to continue.

56592730_2.Doe

4 4

12. As a result, the Characterization Motion proceeded with the same counsel acting for the

legal and economic .interests of Smurt Canada and against the legal and economic interests of

Finance II.

13. On Januar 28, 2010, the motions' judge also released reasons for her decision on the

Characterization Motion where she found that (the "Characterization Order"):

(a) the Intercompany Loan claim was debt (and not equity), but was not a debt

provable in banptcy; and alternatively,

(b) the Intercompany Loan claim did not ran pari passu with the unsecured creditors

of Smurfit Canada and had a value of zero.

14. The Fund Managers brought a motion to the Cour of Appeal for Ontario for leave to

appeal the Representation Order and argued that the motions' judge erred in law by:

(a) failing to appoint independent counsel for Finance II in the CCAA Proceedings

and the Characterization Motion, and in so doing, failed to follow well-

established standards concernng conficts of interest when a lawyer represents

clients whose interests are adverse;

(b) holding that the Fund Managers' counsel could represent the interests of Finance

II at the Characterization Motion without the Fund Managers' counsel having the

benefit of a solicitor-client relationship; and

(c) allowing Stikemans to act as gatekeeper of the information available to the Fund

Managers in the CCAA Proceedings and the Characterization Motion, in the face

56592730_2.Doe

55

of these conficts, which resulted in material evidence relating to the Finance I

loan transaction being witheld.

15. The Fund Managers brought a second motion to the Cour of Appeal for Ontario for leave

to appeal the Characterization Order 1 and argued, inter alia, that the motions' judge erred in law

by:

(a) applying common law principles of contractual interpretation in the face of a loan

agreement that is governed by the laws of Quebec which requires the principles of

contractual interpretation under the Civil Code of Quebec S.Q. 1991, c. 64

("CCQ") to be applied, and finding that:

(i) the Intercompany Loan was not recoverable by legal process and was

therefore not a debt provable in banptcy;

(ii) Finance II's claim should not ran pari passu with the unsecured debt

claims against Smurt Canada; and

(iii) the paries to the Loan Agreement contemplated that in an insolvency

proceeding the value of Finance II's claim would be zero.

16. On March 9, 2010, the Cour of Appeal for Ontaro dismissed the Fund Managers'

motions for leave to appeaL. As is the practice on such leave applications, no reasons were

released.

1 The motions for leave to appeal the Representation and Characterization Orders were brought separately due to the

earlier date that the Representation Order was made and the limitation period for bringing motions for leave undersection 14(2) of the CCAA.56592730_2.Doe

66

The Issues of Public and National Importance Justifying Review by this Court

17. The CCAA is federal legislation that applies thoughout Canada. Proceedings under the

CCAA often involve an international dimension. Many cases, such as this one, have companion

proceedings in the US under Chapter 11 of the US Bankruptcy Act.

18. Outside of the CCAA context, the jurisprudence of this Court and international precedent

have established clear national and international standards for dealing with conflicts of interest

for directors and lawyers.

19. In US cases under the US Banptcy Act, the US court has taken a strict approach to

conficts of interest in cases where the debtors seek the cour's assistance in adjudicating

intercompany disputes.

20. The international reputation of Canada's administration of justice requires that Canada

adhere to certain minum standards for addressing conflcts of interest while resolving

intercompany claims. It is important that there be clear national standards for dealing with

conficts of interest durg CCAA proceedings.

21. Faced with the diffcult position of having to assert claims against other companes of

which they are also directors, it is unealistic to expect those conficted directors to be able to

fulfill their fiduciar obligations to each of the corporations they serve.

22. Having an independent fiduciar (whether a cour-appointed litigation representative,

independent counsel, an independent director, or an independent monitor) is critical to the proper

administration of justice. A company that does not share a common legal and economic interest

with the other entities in CCAA proceedings should have some level of independent

56592730_2.Doe

7 7

representation to ensure that the intercompany claim is appropriately preserved, protected and

pursued.

23. The deleterious effects of failing to have some independent fiduciar In this case

manfested themselves as follows:

(a) The Fund Managers, who were forced into the position of arguing the position of

Finance II, were deprived of access to relevant information, including the file

relating to the "Finance I" transaction on which the Finance II Intercompany Loan

was copied, even though the witnesses proffered on behalf of Smurfit Canada and

Finance II described the Finance II Loan Agreement as a "cookie cutter" copy of

the Finance I transaction, with only the quantu, interest rate and matuity date

being changed.

(b) The Fund Managers were denied access to interviews with Finance II

representatives including offcers, directors and former employees.

(c) The Fund Managers were forced to interview or cross-examine witnesses

(including directors of Finance II) under the watchful eye of counsel for the

Applicants, who refused numerous questions that ought to have been answered

and denied access to relevant information, documents and witnesses (such as

lawyers and accountants) to which Finance II would have been entitled if it had

been permitted to argue this motion itself with the benefit of independent

representation.

56592730JDoe

88

(d) Even though, Finance II had a fudamental right to have its dispute with Smurfit

Canada determined on the basis of Québec law based on the Loan Agreement,

counsel for the CCAA Applicants failed to prove Québec law.

(e) Under the CCQ, the interpretative task is to consider the tre common intentions

of the paries (volonté réelle). An independent fiduciar of Finance II could have

waived the right to Québec law on behalf of Finance II. However, in this case,

Finance II's counsel gave the very advice that would have been in issue as par of

determining the volonté réelle.

24. It was unown whether the information contained in Finance II's counsel's fies would

have been of assistance to Finance II because Finance II's counsel refused to produce or permit

the production of anything (tax, legal, accounting and other fies or reports) relating to the

Finance I transaction and refused to identify or provide access to interview or examine

individuals with knowledge of that transaction, including counsel, employees and accountants.

25. However, as a result of a production order made in the Chapter 11 proceedings additional

documents were subsequently produced which demonstrated that the position being advocated

by the CCAA Applicants ran contrar to the opinion given by Finance II's counsel in the Finance

I transaction.

26. The Fund Managers seek costs of this application for leave to appeaL.

56592730_2.Doe

9 9

tLDated at Toronto, Ontaro this "' day of April, 2010.

SIGNED BY

J) ei¡! Q~'r \.,, \,'f LJ (¿tl-"Lawyers for the Applicants

FRASER MILNER CAS GRAN LLPBaristers and Solicitors1 First Canadian Place100 King Street WestToronto ON M5X IB2Facsimile: 416-863-4592

Neil S. RabinovitchTel: 416-863-4656

E-Mail: neiLrabinovitch(ifmc-law.com

Jane O. Dietrich

Tel: 416-863-4467E-Mail: jane.dietrch(ifmc-Iaw.com

Lawyers for the Applicants, AurellusCapital Management, LP and ColumbusHil Capital Management, L.P.

J)~'~~\-or " Agent

FRASER MILNER CAS GRAIN LLPBaristers and SolicitorsSuite 142099 Ban StreetOttawa, ON KIP IH4Facsimile: 613-783-9690

K. Scott McLeanTel: 613-783-9665Email: scott.mclean~fmc-Iaw.com

Corey A. Vileneuve (Law Clerk)Tel: 613-783-9699Email: corey.vileneuve~fmc-Iaw.com

Ottawa Agents for the Applicants, AurellusCapital Management, LP and Columbus HilCapital Management, L.P.

ORIGINAL TO: THE REGISTRA

STIKEMA ELLIOT LLP5300 Commerce Cour West

COPIES TO: 199 Bay StreetToronto, ON M5L IB9

Sean DunphyTel: 416-869-5662

Fax: 416-947-0866

E-mail:sdunphy(istikeman.com

Alexander RoseTel: (416) 869-5261

Fax: 416-947-0866

E-mail:arose(istikeman.com

Lawyers for Smurt-Stone Container Canada Inc.and the other Applicants Listed on Schedule A

56592730_2.Doe

10

56592730JDoe

AND TO:

AND TO:

10

GOODMAS LLP333 Bay StreetSuite 3400Toronto, Ontaro M5H 2S7

Rob ChadwickTel: 416-979-2211

Fax: 416-979-1234

E-mail:rchadwick(igoodmans.ca

Chris ArmstrongTel: 416-979-2211

Fax: 416-979-1234

E-mail:carstrong(igoodmans.ca

Lawyers for Deloitte & Touche Inc.

BENNETT JONES LLP3400 One First Canadian PlaceP.O. Box 130Toronto ON M5X lA4

Kevin ZychTel: 416-777-5738

Fax: 416-863-1716

E-mail:zychk(ibennettjones.com

S. Richard OrzTel: 416-777-5737

Fax: 416-863-1716

E-mail:orzyrCIbennettjones.com

Derek FruehTel: 416-777.6237

Fax: 416-863-1716

E-mail:fruehd(ibennetijones.com

Raj Sahni

Tel: 416-777-4804

Fax: 416-863-1716

E-mail: sahr(ibennettj ones.com

Lawyers for Official Committee of UnsecuredCreditors of Smurfit-Stone ContainerCorporation, et al

1111

AND TO: THORNTON GROUT FINNIGAN LLPSuite 3200, Canadian Pacific Tower100 Wellngton St. West, P.O. Box 329Toronto-Dominion CentreToronto ON M5K lK7

Robert I. ThorntonTel: 416-304-0560

Fax: 416-304-1313

E-mail:rthomton(ßtgfca

Seema AggarwalTel: 416-304-0603

Fax: 416-304-1313

E-mail: saggaral!ßtgfca

Lawyers for the Indentue Trustee

SCHEDULE "A"

Smurfit-Stone Container Canada Inc.

3083527 Nova Scotia Company

MBI Limited.imitée

639647 British Columbia Ltd.

B.C. Shipper Supplies Ltd.

Specialty Contaiers Inc.

605681 N.B. Inc.

Francobec Company

Stone Container Finance Company of Canada II

NOTICE TO THE RESPONDENT: A respondent may serve and fie a memorandum in responseto ths application for leave to appeal within 30 days after service of the application. If noresponse is filed withn that time, the Registrar will submit ths application for leave to appeal to

the Cour for consideration pursuant to section 43 of the Supreme Court Act.

"', .

56592730_2.Doe

Cou

rt F

ile N

o.l-

.fv

IN T

HE

MA

TT

ER

OF

TH

E C

OM

PA

NIE

S' C

RE

DIT

OR

S A

RR

NG

EJi

NT

AC

T, R

.S.C

. 198

5, c

. C-3

6A

N I

N T

HE

MA

TT

R O

F T

HE

BA

NK

RU

PTC

Y A

ND

IN

SOL

VE

NC

Y A

CT

, R.S

.C. 1

985,

c. B

-3 A

ND

IN T

HE

MA

TT

ER

OF

A P

LA

N O

F C

OM

PRO

MIS

E O

R A

RN

GE

ME

NT

OF

SMU

IT-S

TO

NE

CO

NT

AIR

CA

NA

DA

IN

C. A

N T

HE

OT

HE

R A

PPL

ICA

NT

S L

IST

ED

ON

SC

HE

DU

LE

"A

"I

IN T

HE

SU

PR

EM

E C

OU

RT

OF

CA

NA

DA

(ON

APP

EA

L F

RO

M T

H C

OU

RT

OF

APP

EA

L T

OO

NT

AR

O)

NO

TIC

E O

F A

PPL

ICA

TIO

N F

OR

LE

AV

E T

OA

PPE

AL

, AU

RL

IUS

CA

PIT

AL

MA

AG

EM

EN

T, L

Pan

d C

OLU

MU

S Il

L M

AA

GE

ME

NT

L.P

.(t

oget

her,

the

"Fun

d M

anag

ers"

)(F

iled

Pur

suan

t to

Sec

tion

40 o

f the

Sup

rem

e C

ourt

Act

and

Rul

e 25

(1)(

a)of the Rules of

the

Supr

eme

Cou

rt o

f C

anad

a)

Fraser Milner Cas

grai

n L

LP

Suite

390

0, 1

Fir

st C

anad

ian

Plac

e10

0 K

ing

Stre

et W

est

Tor

onto

ON

M5X

IB

2

Nei

l S. R

abin

ovitc

h L

SUC

# 33

442F

Tel: (416) 863-4656

Jane

Die

tric

h LS

UC

# 49

302U

Tel: (416) 863-4467

Law

yers

for

the

App

lican

ts,

Aur

eliu

s C

apita

l Man

agem

ent,

LP

and.

Col

umbu

s H

il C

apita

l Man

agem

ent,

L.P

.

5661

0665

_1.D

OC

13

File No.

IN THE SUPREME COURT OF CANADA

(ON APPEAL FROM THE COURT OF APPEAL FOR ONTARO)

IN THE MATTER OF THE COMPANIES' CREDITORSARRANGEMENT ACT, RS.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF THE BANKRUPTCY ANDINSOLVENCY ACT, RS.C. 1985, c. B-3, AS AMENDED

AND IN THE MATTER OF A PLAN OF COMPROMISE ORARGEMENT OF SMUIT-STONE CONTAINR

CANADA INC. AND THE OTHER APPLICANTS LISTED ONSCHEDULE "A"

Respondents

AFFIDAVIT OF ALLYSON ROYFILED BY THE APPLICANTS, AURLIUS CAPITAL MANAGEMENT, LP

and COLUMBUS IDLL MAAGEMENT L.P.(Sworn April 8, 2010)

I, ALLYS ON ROY, of the City of Toronto, MAKE OATH AND SAY:

1. I am a student-at-Iaw at Fraser Milner Casgrain LLP, lawyers for the Applicants,

and as such, have knowledge of the matters to which I hereinafter depose.

CCAA Cases Involving More Than One Applicant

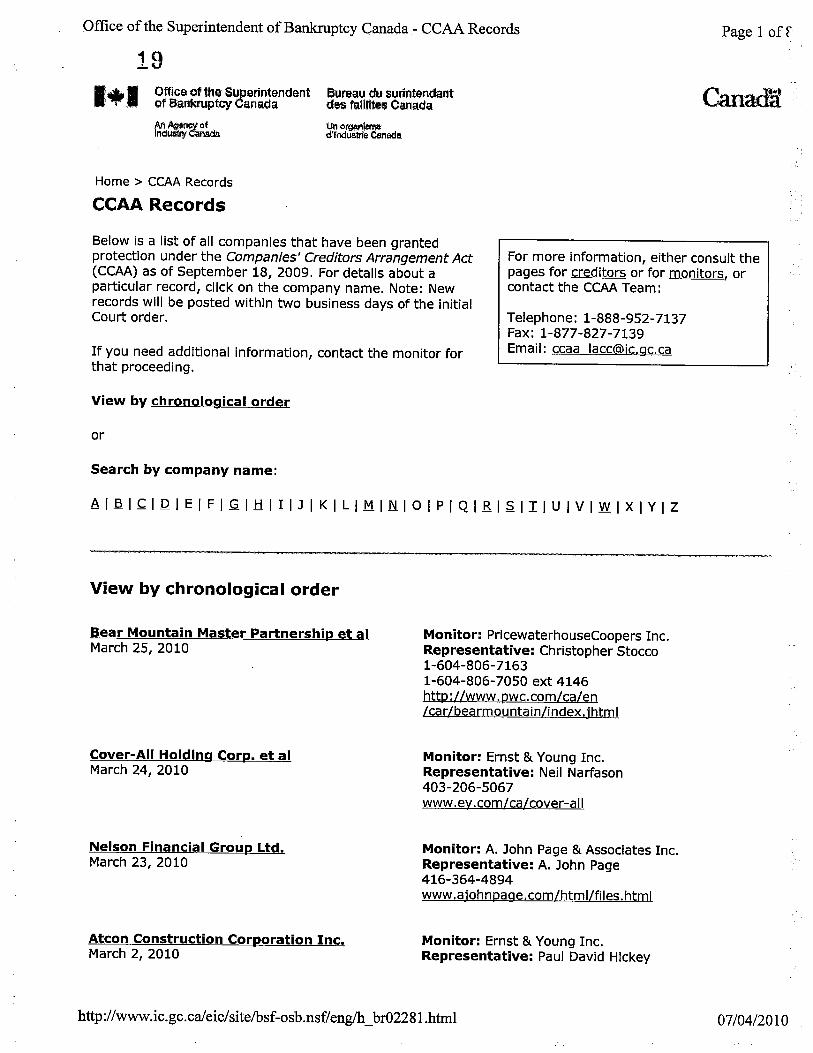

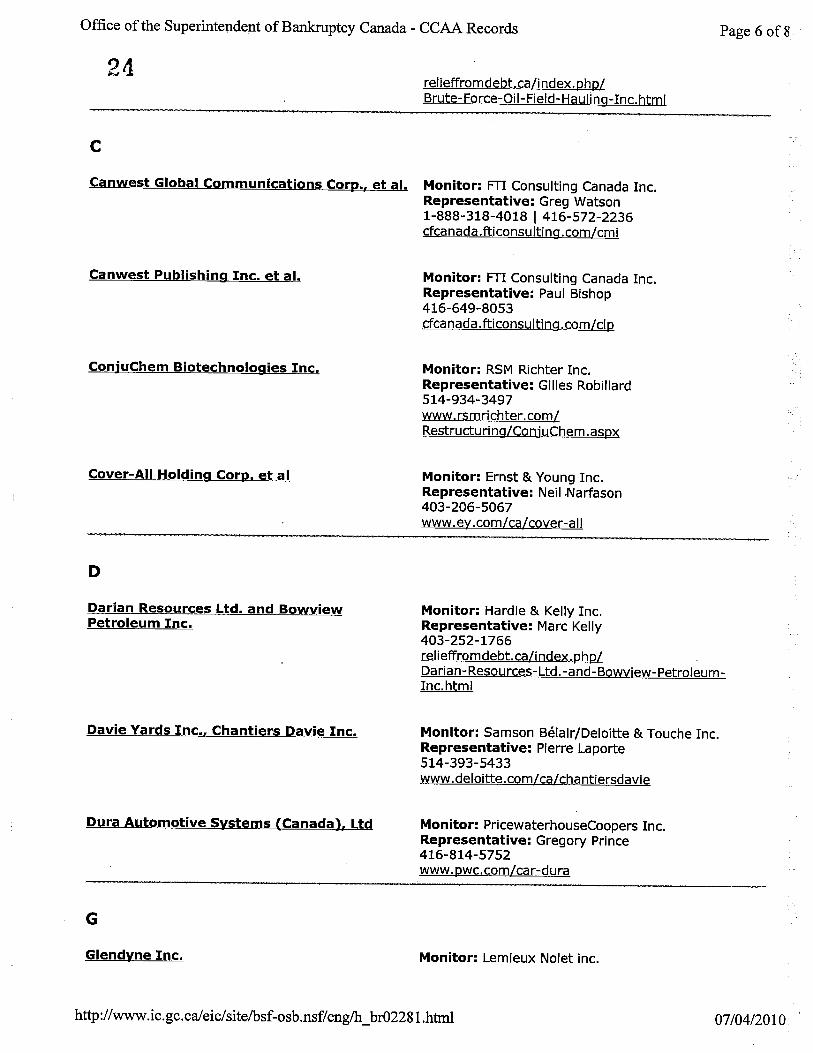

2. Since September 18, 2009, the Office of the Superintendent of Banptcy

Canada ("OSB") has kept a public record of certain information relating to proceedings

under the CCAA (the "CCAA Records") in accordance with section 26 of the !

Companies' Creditors Arrangement Act ("CCAA").

14 2.3. On April 7, 2010, I reviewed the CCAARecords which are

posted on the website

of the OSB (htt://ww.ic.gc.ca/eic/sitelbsf-osb.nsf/eng/home). A print out of this

website is attached as Exhbit "A" to this my Affidavit.

4. A review of the CCAA Records show that since September 18, 2009, there were

27 initial applications for protection made under the CCAA by debtor companies where

protection was granted. Of these 27 applications, 13 (or approximately 48%) involved

more than one applicant (i.e. a corporate group of some sense). As well, two applications

for recognition of foreign insolvency proceedings were made (both of which involved

more than one entity).

ImportancelPrevalence of Enterprise Groups in Insolvency Proceedings

5. The Insolvency Institute of Canada ("IIC") has recognized the prevalence of

insolvencies which involve multiple related entities and the corresponding unque and

important issues raised thereby. In her paper entitled "Corporate Group Insolvencies:

Seeing the Forest and the Trees" prepared for the IIC, Dr. Janis Sara1 has commentated

that "( c )orporate group financial distress poses unque challenges under insolvency and

banptcy law." A copy of ths publication has been attached hereto as Exhbit "B".

6. Internationally, the United Nations Commission on International Trade Law

("UNCITRA") has recognized that the insolvency of enterprise groups is a matter of

international importance that requires consideration.

1 Professor of Law at the University of British Columbia, Faculty of Law and Director of the National

Centre for Business Law

153.

7. In September 2006, the treatment of enterprise groups in insolvency was referred

to UNCITRA Working Group V (Insolvency Law) ("Working Group V") for

consideration, as is outlined in paragraph 9 of the Anotated Provisional Agenda for the

Thirt-First Session of Working Group V, a copy of which has been attached hereto as

Exhbit "C".

8. Publications by Working Group V indicate that Working Group V meets bi-

anually and is composed of the following States: Algeria, Arenia, Australia, Austria,

Bahain, Belars, Benin, Bolivia (plurinational State of), Bulgaria, Cameroon, Canada,

Chile, China, Colombia, Czech Republic, Ecuador, Egypt, EI Salvador, Fiji, France,

Gabon, Germany, Greece, Guatemala, Honduras, India, Iran (Islamic Republic of), Israel,

Italy, Japan, Kenya, Latvia, Lebanon, Madagascar, Malaysia, Malta, Mexico, Mongolia,

Morocco, Namibia, Nigeria, Norway, Pakstan, Paraguay, Poland, Republic of Korea,

Russian Federation, Senegal, Serbia, Singapore, South Africa, Spain, Sri Lana,

Switzerland, Thailand, Uganda, United Kingdom of Great Britain and Northern Ireland,

United States of America, Venezuela (Bolivarian Republic of) and Zimbabwe. A copy of

the Anotated Provisional Agenda for the Thrty-Eighth Session of Working Group V,

which sets out the composition of Working Group V at paragraph 1, is attached hereto as

Exhbit "D".

9. In consideration of the treatment of enterprise groups in insolvency, Working

Group V has recognized that, while it is important to have coordinated insolvency

proceedings, conficts of interest may arse and need to be addressed. Specifically,

paragraph 177 of the draft commentar and recommendations of par three of the

UNCITRAL Legislative Guide on Insolvency Law dated August 31, 2009, which is

164.

based on the Report of Working Group V from its thirt-sixth session in May 2009 and is

attached hereto as Exhbit "E", states the following:

Where a single or the same insolvency representative isappointed to administer several members of a group withcomplex financial and business relationships and differentgroups of creditors, there is the potential for loss ofneutrality and independence. Conficts of interest mayarise, for example, with respect to cross guarantees, intra-group claims and debts, post-commencement finance,lodging and verification of claims; or the wrongdoing byone group member with respect to another group member.The obligation to disclose potential or existing conficts ofinterest contained in recommendations 116 and 117 wouldbe relevant to the group context. As a safeguard against

possible conflcts, the insolvency representative could be

required to provide an undertakng or be subject to apractice rule or statutory obligation to seek direction fromthe cour. Additionally, the insolvency law could provide

for the appointment of one or more fuher insolvency

representatives to administer the entities in confict. That

appointment might relate to the specific area of confict,with the appointment being limited to its resolution, or bemore general and for the duration of the proceedings.

10. I make this Affdavit in support of the within application for leave to appeal the

judgment of the Ontario Cour of Appeal made March 9, 2010 refusing leave to appeal

from the Orders of Justice Pepall, dated December 11, 2009 and January 28, 2010, and

for no other or improper purose.

SWORN BEFORE ME at theCity of Toronto, ths 8th day of

April, 2010

~Commissioner for Takng Affdavits

))))

~

Q~&"'Á.nysoy

Douglas B. B. Stewart

Court File No. I.. ~

IN T

HE

MA

TT

ER

OF

TH

E C

OM

PAN

IES'

CR

ED

ITO

RS

AR

RN

GE

ME

NT

AC

T, R

.S.c

. 198

5, c

. C-3

6A

ND

IN

TH

E M

AT

TE

R O

F T

HE

BA

NK

RU

PTC

Y A

ND

IN

SOL

VE

NC

Y A

CT

, R.S

.C. 1

985,

c. B

-3 A

ND

IN T

HE

MA

TT

R O

F A

PLA

N O

F C

OM

PR

OM

ISE

OR

AR

GE

ME

NT

OF

SM

UIT

-ST

ON

EC

ON

TA

INR

CA

NA

DA

IN

C. A

N T

HE

OT

HE

R A

PPL

ICA

NT

S L

IST

ED

ON

SC

HE

DU

LE

"A

"I

IN T

HE

SU

PR

EM

E C

OU

RT

OF

CA

NA

DA

(ON

APP

EA

L F

RO

M T

H C

OU

RT

OF

APP

EA

L T

OO

NT

AR

O)

AFFIDAVIT OF ALLYS

ON

RO

Y

(Sw

orn

Apr

il 8,

200

9)

Fra

ser

Miln

er C

asgr

ain

LLP

Suite

390

0, 1

Fir

st C

anad

ian

Plac

e10

0 K

ing

Stre

et W

est

Tor

onto

ON

M5X

IB

2

Nei

l S. R

abin

ovitc

h L

SUC

# 33

442F

Tel: (416) 863-4656

Jane

Die

tric

h LS

UC

# 49

302U

Tel: (416) 863-4467

Law

yers

for

the

App

lican

ts,

Aur

eliu

s C

apita

l Man

agem

ent,

LP

and.

Col

umbu

s H

il C

apita

l Man

agem

ent,

L.P

.

5661

0665

JDoe

18

This is Exhibit "A" referred to inthe Affdavit of Allyson Roy swornbefore me ths 8th day of April,2010.~=s=

CONER, ETC.

Douglas B. B. Stewari

Office of the Superintendent of Banptcy Canada - CCAA Records Page 1 off

19

1+1 Offlce of 1he Superintendentof'Bankruptc Canada

Ni~'$niYQfIndua Ca

Bureu du surintendantdes faUites Canada Ca,. .' ...d....l...,;a aI,nQ~n"d'lndua1re Canada

Home ;: CCAA Records

CCAA Records

Below is a list of all companies that have been grantedprotection under the Companies' Creditors Arrangement Act(CCM) as of September 18, 2009. For details about aparticular record, click on the company name. Note: Newrecords will be posted within two business days of the initialCourt order.

For more information, either consult thepages for creditors or for monitors, orcontact the CCAA Team:

If you need additional information, contact the monitor forthat proceeding.

Telephone: 1-888-952-7137Fax: 1-877-827-7139Email: ccaalacc(âic.gc.ca

View by chronological order

or

Search by company name:

A I ß I ç I Q I ElF I G I til l I J I K I L I MIN 10 I P I Q I R I S III u I V I w I X I Y I z

View by chronological order

Bear Mountain Master Partnership et alMarch 25, 2010

Monitor: PricewaterhouseCoopers Inc.Representative: Christopher Stocco

1 -604-806- 7 1 631-604-806-7050 ext 4146http://www.pwc.com/ca/enIca r Ibea rm ou nta i nIl ndex.jhtm i

Cover-All Holding Corp. et alMarch 24, 2010

Monitor: Ernst & Young Inc.

Representative: Neil Narfason

403-206-5067www.ey.com/ca/cover-all

Nelson Financial Group Ltd.March 23, 2010

Monitor: A. John Page & Associates Inc.Representative: A. John Page416-364-4894www.ajohnpage.com/html/files.htm i

Atcon Construction Corporation Inc.March 2, 2010

Monitor: Ernst & Young Inc.

Representative: Paul David Hickey

htt://ww.ic.gc.ca/eic/site/bsf-osb.nsf/eng/ _ br02281.htm 07/0412010

Offce of the Superintendent of Banptcy Canada - CCAA Records Page 2 ofS.'

201-877-806-3597www.ey.com/ca/atcon

ConjuChem Biotechnologies Inc.February 26, 2010

Monitor: RSM Richter Inc.Representative: Gilles Robillard514-393-5433www.rsmrichter.com/Restructuri ngl

ConjuChem .aspx

Davie Yards Inc., Chantiers Davie Inc.February 25, 2010

Monitor: Samson Bélair/Deloitte & Touche Inc.Representative: Pierre Laporte514-393-5433www.deloitte.com/ca/chantiersdavie

White Birch Paper CompanyFebruary 24, 2010

Monitor: Ernst & Young Inc.

Representative: Martin P. Rosenthal

514-879-6549www.ey.com/ca/WhiteBirch

Darian Resources Ltd. and BowviewPetroleum Inc.February 12, 2010

Monitor: Hardie & Kelly Inc.Representative: Marc Kelly

403-252-1766http://rel ieffromdebt. cali ndex. phplDaria n- Resou rces- Ltd. -a nd - Bowview- Petroleu m-Inc.html

Archangel Diamond CorporationFebruary 3, 2010

Monitor: Monitor Not Appointed by the Court

Signature Aluminum Canada Inc.January 29, 2010

Monitor: m Consulting Canada Inc.Representative: Nigel Meakin

416-649-8065http://cfcanada.fticonsulti ng .comlsignature

North Star Manufacturing (London) Limited.January 20, 2010

Monitor: Ernst & Young Inc.

Representative: Michael Philip Dean

1-877 -855-0085www.ey.com/ca/northstar

Mariner Seafoods Inc.January 14, 2010

Monitor: Grant Thornton Limited.Representative: Daniel Rozon

902-420-7195www.grantthornton.ca/services/reorgl bankruptcy and insolvencylMarinerSeafoods

Canwest Publishing Inc. et al.January 8, 2010

Monitor: m Consulting Canada Inc.Representative: Paul Bishop

http://ww.ic.gc.ca/eic/site/bsf-osb.nsf/eng/ _ br02281.html 07/0412010

Offce of the Superintendent of Banptcy Canada - CCAA Records

21

MMFX Steel of Canada, Inc., et al.January 6, 2010

TLC Vision CorporationDecember 23, 2009

Résidences du Collège CRP Inc.December 17, 2009

Les Industries Show Canada Inc., LesIndustries Show Canada (US) inc.,3665658 Canada inc.December 16, 2009

Impax Energy Services Income Trust, et alDecember 14, 2009

Hollnger Canadian Publishing Holdings Co.December 10, 2009

Allen-Vanguard CorporationDecember 9, 2009

Brainhunter Inc., Treklogic Inc., BrainhunterCanada Inc., Brainhunter (Ottawa) Inc. andProtec Employment Services LimitedDecember 2, 2009

Page 3 of8

.416-649-8053http://cfcanada.fticonsulting .com/c1p

Monitor: RSM Richter Inc.Representative: Mitch Vininsky

416-932-6013416-932-6228www.rsmrichter.com/Restructu ri ng/M M FX. aspx

Monitor: Alvarez & Marsal Canada Inc

Representative: Richard Anthony Morawetz416-847-5172www.alvarezandmarsal.com/tlcca nada

Monitor: PricewaterhouseCoopers Inc.Representative: Christian Bourque

514-205-5434www.pwc.com/car-crp

Monitor: Raymond Chabot inc.Representative: Nicolas Boily514-393-4777www.raymondchabot.com/showcanada

Monitor: KPMG Inc.

Representative: Pardeep (Pam) Boparai604-691-3422403-691-7996www.kpmg.ca/impax

Monitor: Ernst & Young Inc.

Representative: Alex Morrison

416-943-7743http://www . ey. comft/hcp-h

Monitor: Deloitte & Touche Inc.Representative: David James Boddy613-751-5227www.deloitte.com/ca/allen-vanguard

Monitor: Deloitte & Touche Inc.Representative: Paul M.Casey

416-775-7172www.deloitte.com/ca/brainhunter

Aero Inventory (UK) Limited, Aero Inventory Monitor: KPMG Inc.Pic Representative: Nicholas BreartonNovember 11, 2009 416-777-3768

htt://ww.ic.gc.ca/eic/site/bsf-osb.nsfieng/h_br02281.html 07/04/2010

Office of the Superintendent of Banptcy Canada - CCAA Records Page 4 of8

22www.kpmg.ca/en/ms/cl/aeroinventory

Big Sky Farms Inc., Drycast Systems Inc. andBig Sky Management Consulting Corp. .November 10, 2009

Monitor: Ernst & Young Inc.

Representative: Kevin Brennan604-891-8300www.ey.com/ca/bigskyfarms

A.C. Ltd.October 30, 2009

Monitor: RSM Richter Inc.Representative: Robert J. Taylor403-233-7112www.rsmrichter.com/Restructuring/AC. aspx

Dura Automotive Systems (Canada), LtdOctober 30, 2009

Monitor: PricewaterhouseCoopers Inc.Representative: Gregory Prince

416-814-5752www.pwc.com/car-dura

Brute Force Oil Field Hauling Inc.October 15, 2009

Monitor: Hardie & Kelly Inc.Representative: Marc Kelly

403-252-1766http://relieffromdebt.ca/i ndex. phplBrute-Force-Oil- Field-Hauling- Inc. html

Glendyne Inc.October 9, 2009

Monitor: Lemieux Nolet inc.Representative: Claude Moisan418-659-7374www.lemieuxnolet.ca/bibliotheque.asp

Bruce R. Smith Limited and John Henry SmithLand Inc.October 8, 2009

Monitor: The Fuller Landau Group Inc.Representative: David Filce416-645-6506www.fullerlandau.com/site/brucersmith.htm

Canwest Global Communications Corp., et al.October 6, 2009

Monitor: ITI Consulting Canada Inc.Representative: Greg Watson1-888-318-4018 I 416-572-2236http://cfcanada.fticonsulting .com/cmi

..Top of Page

Search by company name

A

A.C. Ltd. Monitor: RSM Richter Inc.

htt://ww.ic.gc.ca/eic/sitelbsf-osb.nsfieng/_br02281.htm 07/04/2010

23

Offce of the Superintendent of Banptcy Canada - CCAA Records Page 5 off

Aero Inventory (UK) Limited, Aero InventoryPic

Allen-Vanguard Corporation

Archangel Diamond Corporation

Atcon Construction Corporation Inc.

Representative: Robert J. Taylor403-233-7112www.rsmrichter.com/Restructuri ngLACasgx

Monitor: KPMG Inc.Representative: Nicholas Brearton

416-777-3768www.kpmg.ca/en/ms/cllaeroinventQ

Monitor: Deloitte & Touche Inc.Representative: David James Boddy613-751-5227www.deloitte.com/ca/a II en-va ngua rd.

Monitor: Monitor Not Appointed by the Court

Monitor: Ernst & Young Inc.

Representative: Paul David Hickey1-877-806-3597www.ey.com/ca/atcon

B

Bear Mountain Master Partnership et al

Big Sky Farms Inc., Drycast Systems Inc. andBig Sky Management Consulting Corp.

Brainhunter Inc., Treklogic Inc., BrainhunterCanada Inc.. Brainhunter (Ottawa) Inc. andProtec Emplment Services Limited

Bruce R. Smith Limited and John Henry SmithLand Inc.

Brute Force Oil Field Hauling Inc.

Monitor: PricewaterhouseCoopers Inc.Representative: Christopher Stocco

1-604-806-71631-604-806-7050 ext 4146http:llwww.pwc.comlca/enI car Ibea rmou nta i n/i ndex.j htm i

Monitor: Ernst & Young Inc.

Representative: Kevin Brennan

604-891-8300www.ey.com/ca/bigskyfarms

Monitor: Deloitte & Touche Inc.Representative: Paul M.Casey

416-775-7172www.deloitte.com/ca/brainhunter

Monitor: The Fuller Landau Group Inc.Representative: David Filice416-645-6506www.fullerlandau.com/site/brucersmith.htm

Monitor: Hardie & Kelly Inc.Representative: Marc Kelly403-252-1766

http://ww.ic.gc.caJeic/site/bsf-osb.nsf/eng/ _ br02281.htm 07/04/2010

Offce of the Superintendent of Banptcy Canada - CCAA Records Page 6 of!?

24relieffromdebt. cali ndex. ph pIBrute-Force-Oi 1- Field-Hauli ng- Inc. html

c

Canwest Global Communications Corp., et al. Monitor: FTI Consulting Canada Inc.Representative: Greg Watson1-888-318-4018 I 416-572-2236cfcanada. fticonsulting .com/cmi

Canwest Publishing Inc. et al. Monitor: m Consulting Canada Inc.Representative: Paul Bishop

416-649-8053cfcanada. fticonsulting .com/clp

ConjuChem Biotechnologies Inc. Monitor: RSM Richter Inc.Representative: Gilles Robillard514-934-3497www.rsmrichter.com/Restructuring/ConjuChem .aspx

Cover-All Holding Corp. et al Monitor: Ernst & Young Inc.Representative: Neil -Narfason

403-206-5067www.ey.com/ca/cover-all

D

Darian Resources Ltd. and BowviewPetroleum Inc.

Monitor: Hardie & Kelly Inc.Representative: Marc Kelly403-252-1766rei i effrom debt. cali ndex. ph pIDa rian- Resources- Ltd. -a nd- Bowview- Petroleu m-Inc.html

Davie Yards Inc., Chantiers Davie Inc. Monitor: Samson BélairfDeloitte & Touche Inc.Representative: Pierre Laporte514-393-5433www.deloitte.com/ca/cha ntiersdavie

Dura Automotive Systems (Canada), Ltd Monitor: PricewaterhouseCoopers Inc.Representative: Gregory Prince416-814-5752www.pwc.com/car-dura

G

Glendyne Inc. Monitor: Lemieux Nolet inc.

htt://ww.ic.gc.ca/eic/sitelbsf-osb.nsf/eng/ _ br02281.htm 07/04/2010

Offce of the Superintendent of Banptcy Canada - CCAA Records Page 70f8

25Representative: Claude Moisan418-659-7374www.¡emieuxnolet.ca/bi bl i otheg ue. aSQ

'~"""""""-'-"""'~-"~---~~'-"-~""'¥--""''.''-''-~''-''-'''-'''-'''-.............._----...,........_------....-..._-....._............_......"..-......-_....__."......."--......--......-..-"....,,....---.......----.............-..__....."........¥.._-..........~...

H

Hollnger Canadian Publishing Holdings Co. Monitor: Ernst & Young Inc.

Representative: Alex Morrison

418-659-7374www.ey.com/ca/hcph

,..._.........,......_......."._...._.._.OW...."".."..._......._......................"..........._"'....._.........__--....__.._......_.."_._.._____..._.."__~..,,..._........""_.,,""...._,,...._..._....,....__........"'...._,,_"'_...._..._......_...-_........_...._..__"'......,._.............."".......,.

I

Impax Energy Services Income Trust, et al. Monitor: KPMG Inc.Representative: Pardeep (Pam) Boparai604-691-3422403-691 -7996www.kpmg.ca/impax

M

Mariner Seafoods Inc. Monitor: Grant Thornton Limited.Representative: Daniel Rozon

902-420-7195www.grantthornton.ca/servicesIreorg/bankruptcy andi nsolvency/M a ri nerSeafoods

MMFX Steel of Canada. Inc.. et al. Monitor: RSM Richter Inc.Representative: Mitch Vininsky

416-932-6013416-932-6228www.rsmrichter.com/Restructuring/M M FX.aspx

N

Nelson Financial Group Ltd. Monitor: A. John Page & Associates Inc.Representative: A. John Page416-364-4894www.ajohnpage.com/htmllfiles.html

North Star Manufacturing (London) Limited. Monitor: Ernst & Young Inc.Representative: Michael Philip Dean

1-877-855-0085www.ey.com/ca/northstar

R

http://ww.ic.gc.ca/eic/site/bsf-osb.nsf/eng/ _ br02281.html 07/04/2010

Offce of the Superintendent of Banptcy Canada - CCAA Records

26Page 80f8

Résidences du Collège CRP Inc. Monitor: PricewaterhouseCoopers Inc.Representative: Christian Bourque514-205-5434www.pwc.com/car-crp

sLes Industries Show Canada Inc. LesIndustries Show Canada (US) inc. 3665658Canada inc.

Monitor: Raymond Chabot inc.Representative: Nicolas Boily514-393-4777www.raymondchabot.com/showcanada

Signature Aluminum Canada Inc. Monitor: ITI Consulting Canada Inc.Representative: Nigel Meakin

416-649-8065cfcanada. fticonsulting .com/signature

T

TLC Vision Corporation Monitor: Alvarez & Marsal Canada Inc

Representative: Richard Anthony Morawetz416-847-5172www.alvarezandmarsal.com/tlccanada

w

White Birch Paper Company Monitor: Ernst & Young Inc.

Representative: Martin P. Rosenthal

514-879-6549www.ey.com/ca/WhiteBirch

Date Modified: 2010-03-30

htt://ww.ic.gc.caJeic/sitelbsf-osb.nsf/eng/ _ br02281.htm 07/0412010

27

This is Exhibit "B" referred to inthe Affdavit of Allyson Roy swornbefore me this 8th day of April,2010.

l¡2:;::~ ETC

Douglas B. B. Stewart

28IIC-ART 2008-6nc. Ar. 2008-6

Page 1

IIC-ART 2008-6

Insolvency Institute of Canada (Aricles)

- Corporate Group Insolvencies: Seeing the Forest and the Trees - Janis SaraIE

~ Thomson Reuters Canada Limited or its Licensors. All rights reserved.

Canadian courts have occasionally allowed substantive consolidation of commercial insolvency proceedings wherethere are multiple entities in a corporate group and the assets and debts are highly intertwined. Often, time is of theessence in making such judgments and there is little opportunity to reflect on the jurisdiction being exercised andthe broader principles being applied. A view of the globally integrated corporate group may ignore important as-pects of the individual business enterprise and its local creditors; at the same time, one can lose sight of the impor-tance of the global business entity if one is too caught up in viewing subsidiaries and related entities as separate.Treatment of corporate groups can challenge accepted notions of the separate legal personality, and requires care-

ful consideration when applied to cross-border proceedings.

Les tribunaux canadiens ont à /'occasion permis la réunion d'instances en insolvabilté commerciale lorsqu'un

groupe de sociétés compte diverses entités et que les actif et les passif sont fortement entremêlés. Souvent, les dé-lais sont de rigueur au moment où il faut prendre des décisions à cet égard ou réfléchir à la compétence judiciaireappropriée et aux principes plus généraux applicables. Une vision du groupe de sociétés globalement intégrées peut

faire en sorte que soient ignorés d'importants aspects propres à chaque société qui compose Ie groupe et aux créan-ciers respectif de ces sociétés. De la même façon, il est possible de perdre de vue /'importance de l'entité commer-ciale globale si les ¡Wales et les entités connexes sont perçues d'une maniére trop distincte. La façon dont sont con-sidérés les groupes de sociétés peut mette à l'épreuve la notion acceptée de personnalité juridique distincte et doitêtre mûrement réfléchie dans Ie cas d'instances internationales.

1. - Introduction

Corporate group fmancial distress poses unique challenges under insolvency and banptcy law.rFN21 When cor-porations have assets or operations in multiple jursdictions, separate legal entities are often formed to operate ineach jurisdiction, thus faciltating compliance with local regulatory requirements and managing liabilty risk for theentities. These business enterprises may be highly integrated and operate as a global unt, or they may operate rela-tively independently of one another.fFN31 A corporate group may also have separate legal entities for fmancingpuroses; for example, placing paricular assets in special purose entities with the asset lender as sole creditor, eventhough those entities are highy integrated on an operational basis.

When corporate groups are fmancially healthy, the "centre of control" is often the entity governing strategic andoperational oversight, with the separate subsidiaries or entities ensurg they meet expected regulatory and commer-cial standards of conduct in those multiple jursdictions. Each state in which the business enterprise is operatingsteps in to regulate the entities' conduct. The corporate group is a risk reduction strategy in the sense that claimsagainst one entity for parcular kids of conduct in a jurisdiction wil attach only to that legal entity, except in verylimited circumstances where the cours consider piercing the corporate veil.FN41

On insolvency, creditors in each of the domestic jursdictions wil seek to use domestic law to realize on their

Copr. ~ West 2010 No Claim to Orig. Govt. Works

2 SIC-ART 2008-6nc. Ar. 2008-6

Page 2

claims. Where companies in a corporate group operate independently and have few operational or financial linsother than a parent-subsidiar relationship, it may not pose a problem to deal with their insolvency as separate enti-ties. However, even in ths situation, there can be an issue where the practice has been to transfer the profits gener-ated by the subsidiar's economic activities to the parent corporation on a regular basis. In such a case, assets arelocated in one entity, the parent, whereas the credit, trade supplies and labour that were used to generate those assetswere advanced to the subsidiar. Given that they are separate legal entities in different jursdictions, fewer assets are

then available to meet creditors' claims.

Where control, finances and operations are highly integrated within the corporate group, then insolvency proceed-ings in the separate jurisdictions where the business entities are registered can pose enormous problems, creating therisk of premature liquidation of the companies to satisfy multiple domestic claims in multiple jursdictions'(FN51

The separate natue of these entities may make it diffcult to reorganize the corporate group as a whole, even wherevalue might be better maximized for creditors though a global resolution of the fi's financial distress. Even where

liquidation is the expected outcome, there may be merit in corporate group proceedings in order to preserve or en-hance value pending a going concern sale of one or more of the entities.(FN61

On a pure liquidation basis, arguably, entities in a corporate group should be liquidated as separate entities such thatcreditors that made explicit contracts with the specific corporation and evaluated their risk based on the stabilty ofthat corporation should be able to rely on that separate personality. Even this distinction can be blured, however,when the liquidation takes the form of a going concern sale, in which pars of the corporate group may be suff-ciently integrated that they are necessar to maximize sale value or perhaps necessar to the sale itself rFN71 Thereneeds to be operating priciples in respect of how to make a determination or how to proceed. However, to date,

consolidation cases have been approved on a pragmatic commercial basis with few judgments providing a detailedanalysis of the authority being involved or the operating principles being applied.

With the first experience internationally with the UNCITRA Model Law on Cross-Border Insolvency and Can-ada's recent adoption of large pars of the Model Law, the most significant outstading question for cross-border

insolvency is how to address the issue of corporate groups.rFN81 The Model Law, Chapter 15 of the United StatesBankruptcy Code, which adopts the Model Law almost in its entirety, and the new cross-border insolvency provi-sions in Par IV of the Companies' Creditors Arrangement Act (CCAA) are all silent on the issue of corporategroups.rFN91

There is the fuctional reality, especially with globalization, whereby the corporate parent can have a subsidiar inanother countr that is absolutely vital to the worldwide organation, but if the parent canot get coordinationacross jurisdictions, there is no maxiization of value. In such cases, commercial reality suggests that there must be,at minimum, coordination of multiple proceedings. This challenge is complicated by the use of centre of main inter-est (COM!) in jurisdictions adopting the Model Law or governed by EU insolvency directives. A paricularly diff-cult issue is where some of the corporate entities with the group are insolvent and others are not, an acute issue for

the civil law jurisdictions.

This aricle begins to examine the challenges posed and potential avenues for addressing both the legal and govern-ance issues of corporate groups in insolvency. As the expression "canot see the forest for the trees" suggests, onecan lose sight of the importance of the global business entity if one is too caught up in viewing subsidiaries and re-lated entities in different countries as separate legal personalities; equally, however, a view of the globally integrated

corporate group may ignore important aspects of the individual business enterprise and its local creditors. Hence,one must look at the "forest and the trees" in analysing the issue of corporate groups. Ths aricle seeks to ariculateprinciples that can be utilized by the cours in determing how to deal with corporate groups in insolvency proceed-ings. Par 2 of the aricle begins to defme what is meant by corporate group. Par 3 explores the legal treatment of

corporate groups. Par 4 discusses cross-border protocols as an important tool for coordination of proceedings. Par 5looks at the use of procedural and substantive consolidation in Canada and the U.S. as a mechanism for dealing withthe insolvency of corporate groups. Par 6 examines the concept of centre of main interests (COMI) in the EC Regu-

Copr. (Ç West 2010 No Claim to Orig. Govt. Works

3 OIlC-ART 2008-6nc. Ar. 2008-6Page 3

¡alion and elsewhere and how it may influence the treatment of corporate groups. Finally, Part 7 discusses whetherCOMI should be adopted as a mechanism for dealing with cross-border insolvencies of corporate groups operatingas a global enterprise.

2. - Defining Corporate Group

There is not a universal defintion of the term corporate group. In many jurisdictions, corporate entities are separatelegal entities but their governance and capital strctues may be highly integrated, as in the U.K. and Germany. Inseveral jurisdictions, there is not really a concept of separate legal entities, but rather, the entities are subdivisions ofthe parent and thus seen as one corporate strctue, as in the Russian Federation.Wl In other jurisdictions, thecontrol is held through a family strctue, such that while legally the entities are separate, there is considerable con-trol exercised between the entities, as in some corporations in India or Canada.

Hence, it is helpful to commence with a working definition of corporate group. UNCITRAL's working definition ofcross-border enterprise groups is "two or more enterprises that are bound together by means of ownership or con-trol".rFN 1 11 Enterprise is defined as any entity, regardless of its legal form, engaged in economic activities, includ-ing entities engaged on an individual or parership basis as a parership or association, and can include business

trsts.rFNl21 The UNCITRAL Workig Group has defined control as "the power normally associated with theholding of a strategic position within the enterprise group that enables its possessor to dominate directly or indirectlythose organs entrsted with decision-makg authority."(FN131

Although there is not a universal defiition of corporate group, cours in different jurisdictions have recognized theterm as applying to the situation where two or more separate legal corporate entities are associated either though aparent-subsidiar relationship or lined by common, mutual, and/or interlocking shareholdings with capacity to con-

tro1.FN141 The challenge of a defiition is complicated by the natue of capital strctues in different jurisdictions.In Canada, Latin America, East Asia, and pars of Europe, the capital strctue of corporate groups is generally py_

ramidal in natue, with a controlling shareholder or group of shareholders holding voting control blocks in tiers ofthe corporation though both direct and indirect control, often with equity interest that is considerably less than thecontrol wielded though the corporate strctue.FNIS1 At the point offinancial distress, the controlling sharehold-ers, whose residual claims may be worthless, can utilize existing control to delay fiing or retain a governance strc-tue for a period even though it is not maxiizing value. While creditors wil ultimately determe the fate of thebusiness enterprises, the centralized control contrasted with the often fragmented natue of creditors' claims withseparate legal entities, can skew the process and work against maxizing value for creditors. In contrast, in the U.S.and U.K., corporate groups generally refer to one listed corporation with fully owned subsidiaries.(FN161

Corporate groups can create effciencies through lateral integration with suppliers or with retail outlets, often acquir-ing such entities during financially healthy periods.rFNl71 In some cases, such as a parent company's decision tomerge two wholly owned subsidiaries, a merger might not have significant economic effect, but when the combina-tion represents the union of two distinct businesses, new value may be created.rFNl81 Canadian companies oftengrow their business through mergers or acquisitions rather than relying solely on the longer term process of invest-ing in organic growth. In a highly competitive industr sector, a company may not have the time or resources to de-velop a new line of business that it feels is important to its success and may acquire a business that has the desirablecharacteristics that it is after.rFNl91 However that acquisition is strctued, either though a merger or maintenanceof separate legal entities with common control, the company may operate as a single integrated whole.rFN201

Where there is a single entity, there is transparency in that creditors understand the entity they are dealing with andcan make appropriate credit decisions. (FN211 Where the corporation is comprised of separate legal entities, the inte-gration of financial systems, co-miglig of supplies and common control can lead less sophisticated creditors intobelieving that they are dealing with one entity with a reputation that leads them to believe it is a good credit risk,while in reality their legal relationship is with a separate legal personality.rFN221 When fis are fiancially healthyand creditors receive timely payment, the corporate strctue is not paricularly important; however, when some

Copr. ~ West 2010 No Claim to Orig. Govt. Works

31 IIC-ART 2008-6I.C. Ar. 2008-6

Page 4

par, or all, of the corporate group becomes fiancially distressed, the corporate form chosen at the outset wil affectthe treatment of creditors' interests in insolvency proceedings'(FN231 Where there is one legal entity, the corpora-tion wil be liquidated or restrctued as such, often involving the sale of pars of the business that have stand-alonevalue. Where, however, the corporate group consists of multiple legal entities, there is a greater challenge in respectof how to address the insolvency, given the natue of claims and the expectations of creditors that have dealt withthe separate entities.~

Once one moves beyond the corporate groups held in a pyramidal strctue, many companies in Canada are subsidi-aries of large multinational business enterprises, most often with the parent corporation in the U.S., but increasinglywith parent companes in Europe and Asia. Hence the Canadian capital strctue is a mix of parent corporations andsubsidiaries, many of which are par of a corporate group that spans borders. Consideration of corporate groups ininsolvency needs to account for the central and controlling featues of its pyramidal corporate groups, as well as thechallenge of multiple subsidiaries and the implications for domestic creditors if the corporate group's insolvency isdealt with on a centralized basis elsewhere, paricularly in jurisdictions where creditors and employees are not af-forded the same level of protection.

3. - Treatment of Corporate Groups

Canada's cross-border provisions in the Bankruptcy and Insolvency Act (BfA) and the Companies' Creditors Ar-rangement Act (CCAA) since 1997 have faciltated cross-border proceedings for financially distressed companies,the cours granting recognition under the priciples of comity and co-operation'(FN251 Treatment of corporate

groups has vared, and the cours have used cross-border protocols, as well as procedural and/or substantial consoli-dation, as tools to restrctue corporate groups or coordinate processes for liquidation and realization of

claims. (FN261

UNCITRAL defines procedural consolidation as "coordination of the administration of (separate) insolvency pro-ceedings in respect of two or more members of an enterprise group. Each member remains separate and distinct,thus preserving the integrity of the individual enterprises". The Workig Group has yet to agree on a defition ofsubstantive consolidation, but has proposed that it be defied as: "the pooling ofthe assets and liabilties of two ormore members of an enterprise group to create a single insolvency estate for the benefit of creditors of the substan-tively consolidated members".Il

Procedural consolidation can promote cost effcient and timely proceedings by faciltating dissemination of informa-tion regarding the economic activities of the enterprise group members subject to the insolvency proceedings; canfaciltate valuation of assets; can assist in identification and processing of creditors' claims; and can avoid duplica-tion of proceedings.~ Procedural consolidation can include the appointment of a single receiver or other insol-vency professional to assist with the proceedings or provide for coordination of such professionals. Such consolida-tion may include joint hearings and/or joint meetings of creditors; can allow for a consolidated service list for provi-sion of notice; can coordinate processing of creditors' claims; can coordinate the sale of assets; and can include, inthose jurisdictions that require creditors' committees, a single creditors' committee or coordination between credi-tors' committees.~

Substantive consolidation, according to the UNCITRAL proposed definition, "generally results in the extinguish-ment of intra-group liabilties. "Ir Often a single insolvency professional is appointed, although, as

UNCITRAL notes, that may depend on the stage in the proceeding at which consolidation occurs.Il The cur-

rent UNCITRAL draft suggests that substantive consolidation may be appropriate where the cour is satisfied thatthere has been such an intermingling of assets of the enterprise group members that it is impossible to identify own-ership of the assets or they canot be identified without undue expense and delay; where members of an enterprisegroup are engaged in fraudulent schemes with no legitimate purose and the cour is satisfied that substantive con-solidation is essential to rectify that activity; or where the cour is satisfied that the enterprise group presented itselfas a single enterprise or otherwise acted in a maner that encouraged third paries to believe that they were dealing

Copr. ~ West 2010 No Claim to Orig. Govt. Works

32 IIC-ART 2008-6LLC. Ar. 2008-6Page 5

with a single enterpriseJFN321 The draft acknowledges that there could be a parial substantive consolidation; spe-cifically, the cour may exclude specified assets or claims from an order for substantive consolidation, such as ex-cluding secured creditors to the extent they relied on the encumbered assets, or the cour may determine with respectto a solvent member of the enterprise group that consolidation includes only the net equity of the solvent members,leaving their creditors unaffected,(FN331

While the definition of corporate group or business enterprise group includes the notion of an integrated economicand operational unit, as noted above, corporate groups can be strctued in many ways. It is the corporate group thatoperates as an integrated global unit that requires public policy consideration of its treatment during insolvency; andspecifically, consideration of whether procedural or substantive consolidation of the insolvencies of the businessenterprise group is the appropriate mechanism to maximize value of the group'(FN34J.

Where there is a corporate group, the debtors' fiing choices are influenced by the specific objectives of the insol-vency proceeding. This is best ilustrated by the difference between Canadian and U.S. insolvency law, given thatmore than 90% of cross-border insolvency proceedings in Canada are with the U.S. For example, if a sale of all orsubstantially all of the businesses is anticipated, Canadian CCAA proceedings may be more expeditious and lessrigid than fiing in the U.S. and conducting the sale processes there. Similarly, treatment of executory contracts can

differ considerably and this differig treatment may affect choice of laws. DIP fiancing is more rule driven in theU.S. than Canada and may influence choice ofregimeJFN35J Directors and offcers tend to have broader indemnifi-cation in Canada than in U.S. restrctuing proceedings, and depending on the natue of claims against the debtorand its offcers, this may also influence where the debtors fie. The two countries differ in the natue and extent ofpriorities and provisions on avoidable transactions, fraudulent conveyances and preferences. Proposed changes toCanadian insolvency and banptcy law wil strengthen the priority given to employee claims and provide a differ-ent approach than the U.S. for treatment of collective agreements'(FN36J Many of these fiing considerations are not

attached to the notion of centre of main interests or control, but rather, the debtor's decision to initiate the fiing of aninsolvency proceeding, paricularly a restrctuing attempt, by using one or more entities to gain access to the juris-diction that offers the best statutory regime for the debtors' goals in the insolvency proceeding'(FN37J This practicemay not align with what creditors in each jurisdiction perceive as the jurisdiction that wil best serve their interests.

Where management or fiancing control is centralized, the corporate group may need to fie concurently in multiplejursdictions in order to continue operating, because a stay in one jurisdiction is not suffcient to allow such a cen-tralized strctue to continue durg the workout negotiation process,(FN38J Various companies in the corporate

group may be critical suppliers for other entities in the group. In such a case, there may be inter-company flow ofassets, which could give rise to claims on a solvent member of the corporate group or reviewable transaction claimswhere payments have been made in the period leading up to filing'(FN39J The debt strctue may be highly inte-grated, with inter-company loans that cross borders. There may be guarantees by one entity for another or by theoffcers of the company for debts of a member of the corporate group. Hence the corporate group may need to be

treated as an integrated whole, rather than numerous separate entities. Yet domestic creditors may have dealt onlywith a separate legal entity and not the corporate or enterprise group.

Concurent proceedings in respect of related companies frequently are commenced in multiple jurisdictions, al-though such proceedings mayor may not advance a global resolution of the debtor companes' insolvency, paricu-larly where regimes differ as to their liquidation or rehabiltation goals or where procedures var considera-bly'(FN40J Most of Canada's cross-border experience is with the U.S., where there is a degree of compatibilty inprocedural protections. However, where systems do not converge, the issue of centre of main interests and how thatmight align with corporate groups that cross borders is yet to be determed.

In a cross-border corporate group proceeding, the facilty with which the debtor wil be able to restrctue wil de-

pend to a large measure on the cour's wilingness to grant relief that faciltates the restrctuing but is not inconsis-

tent with domestic legislation.fFN411 Given that different regimes internationally have different normative concep-tions of insolvency, with paricular focus on rehabiltation or liquidation or a mix of both, the abilty to restrctue

Copr. ~ West 2010 No Claim to Orig. Govt. Works

33IIC-ART 2008-6nc. Ar. 2008-6

Page 6

as a corporate group may be hampered if the cours narowly interpret an entity-based test for recognition or areunwiling to grant specific orders because they are not consistent with domestic law.(FN421

Cross-border proceedings also raise serious potential bariers for smaller trade suppliers or employee groups, whoface collective action problems in terms of being able to participate in hearings in a foreign jursdiction or even tomake the appearance in that other jurisdiction to voice concern about the potential prejudice to their interests,fFN431While some jurisdictions such as Canada may provide for representative counsel for paricularly vulnerable groupsor in the U.S. provide unsecured creditors' committees to address such bariers, where such mechanisms are notavailable, an issue is how the cour can be assured of the fairess and reasonableness of orders being sought in re-spect of the corporate group when all stakeholders are not before it. In Canada, the cour have addressed this in parby their careful admonition to monitors and proposal trstees that they are to be imparial offcers of the court thatare to have regard to the interests of all staeholders.

4. - Cross-Border Protocols

Cross-border insolvency protocols have been approved by Canadian, U.S. and other foreign cours as a mechanismto faciltate cross-border proceedings involving multiple related corporate entities. The protocols create a legalframework for the conduct of insolvency proceedings and coordination of administration of an insolvent estate inone jursdiction with administration in another.~ The cour orders endorsing cross-border protocols have dealt

with communcation and co-operation in the administration of proceedings, coordiation in ongoing operations, as-set sales and distrbution, claims fiing procedures and choice of law issues, and coordiation of development ofplans in two or more countries.

Protocols have been used effectively to reduce the cost of litigation and place the focus on restrctuing issues in-stead of conflct of laws disputes. These cases have involved Canadian debtor corporations with significant opera-tions and asset holdings in the U.S., or vice versa, and thus the debtor corporation's required recourse to protection

of insolvency laws in both jursdictions. A protocol sets out the ground rules by which concurent insolvency pro-ceedings can be coordinated; honours the sovereignty of the respective cours; haronizes activities in multi-jurisdictional insolvency proceedings; promotes the orderly and effcient administration of proceedings; promotesinternational co-operation and respect for comity among the cours; faciltates fair and open processes for insol-vency proceedings for the benefit of all paries; and implements a framework of general principles to address basicadministration issues arising out of cross-border insolvencies.~

Canadian cours, though their orders, directly request information and assistance, and in a nwnber of cases, proto-cols have allowed direct communication. For example, in Muscletech Research and Development Inc., the CCAAjudge and the Chapter 15 U.S. judge were in direct communication in respect of coordination and co-operation,fFN461 There have also been joint heargs conducted by Canadian and U.S. cours in restrctuing appli-

cations, allowing paries on both sides of the border to have the benefit of makg submissions and hearing the con-cerns of the cour without the fiter of reading their views in foreign judgments,fFN471 Joint heargs allow thejudges to directly communicate instead of only though wrtten judgments,fFN481 Given the time sensitive natue ofrestrctug proceedings, the use of joint hearings can expedite decisions, cut costs in terms of nwnbers of cour

appearances, and faciltate decisions that have pragmatic effect in bothjurisdictions,fFN491

With the amendments in 1997 to the CCAA to add section 18.6 and parallel cross-border provisions in the BIA, Ca-nadian practitioners in a number of cases have relied more directly on the provisions of the statutes and less on pro-tocols than previously. Section 18.6 allows the judges in different cross-border proceedings to directly communicatewith one another under the discretion that allows the CCAA judge to seek the aid and assistance of anothercour.(FN501

In Menegon v. Philip Services Corp., the Cour held that the objective of a protocol is to protect claimants on either

Copr. ~ West 2010 No Claim to Orig. Govt. Works

3 4IIC-ART 2008-6nc. Ar. 2008-6

Page 7

side of the border from being swept into the rigours of the other countr's regime, where to do so might preventthem from asserting their substantive rights under the applicable laws of their own jursdictions; and while faciltat-ing cross-border proceedings, the protocols canot undermine domestic statutory standards.rFN51l

The Alberta Cour of Queen's Bench in Calpine made some observations in respect of protocols in terms of whenthey may be inappropriate or prematue.rFN521 With US$18 biIionin debt, Calpine and almost 300 subsidiariesfied under Chapter 11 of the U.S. Bankruptcy Code and twelve Canadian Calpine entities applied for protectionunder the CCAA. Calpine had operated as a global company with a large amount of highly complex inter-companydebt; however, the Chapter 11 and CCAA proceedings were conducted relatively independently of one another at theoutset. Yet this separation of the global operations into two proceedings was challenging, as there was an ongoingneed to supply gas from the Canadian entities to the U.S. power plants, and the Canadian Calpine affliates weresome of the U.S. Calpine companes' largest creditors.rFN53J Neither the CCAA debtors nor the Chapter 11 debtorshad sought to have their proceedings recognized in the other jursdiction; and when an application was made for across-border protocol, Romaine J. held that a cross-border protocol was prematue.FN541 The Cour held that aprotocol should not be a method to delay or obfuscate proceedings or to provide re-hearg of the cour of one juris-