Embed Size (px)

Citation preview

Presenting a live 90‐minute webinar with interactive Q&A

Fraudulent Conveyance Exposure Fraudulent Conveyance Exposure for Intercompany Loans and GuaranteesNavigating the Bankruptcy and Insolvency Risks of Intercorporate Obligations

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, FEBRUARY 12, 2013

Today’s faculty features:

Kyung S. Lee, Partner, Diamond McCarthy, Houston

Mark D. Bloom, Shareholder, Greenberg Traurig, Miami

Dr. Kose John, Special Consultant, NERA Economic Consulting, New YorkDr. Kose John, Special Consultant, NERA Economic Consulting, New York

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your locationattendees at your location

• Click the SEND button beside the box

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Fraudulent Conveyance Exposure for Intercompany Loans and Guarantees

Stafford Webinar Presentation Sta o d Web a ese tat o February 12, 2013

Dr. Kose JohnS i l C l NERA E i C l iSpecial Consultant at NERA Economic Consulting(New York, New York)Kyung S. LeeDiamond McCarthy LLPDiamond McCarthy LLP(Houston, Texas)Mark D. Bloom and Ari NewmanGreenberg Traurig, LLPg g,(Miami, Florida)

Intercompany/Inter-Estate Claims

• Generally, priority of intercompany claims is dependent on whether the claim is dependent on whether the claim resembles or was intended to be debt, equity or preferred equity/subordinated debtdebt

• Intercompany claims can be treated pari passu in right of payment with third-party p g p y p yunsecured claims

• In many significant cases, intercompany claims are ignored or disallowed either claims are ignored or disallowed either because of cost and difficulty reconciling such claims

6

Scheduling of Claims

Bankruptcy Code § 521(1) requires the d bt t fil h d l f t d debtor to file schedules of assets and liabilities

If not noted as C U or D such creditor is If not noted as C, U or D, such creditor is not required to file proof of claim and under Bankruptcy Rule 3003(b)(1), such

h d li i f i id scheduling represents prima facie evidence of the validity and amount of the claim. See, Bankruptcy Code §§ 1111(a), 501 and , p y ( ),521(1).

7

Intercompany Claims: Debt or Equity

Characterization of intercompany claims affects the priority of recovery and thereby affects the priority of recovery and thereby the amount available to creditors

Most bankruptcy cases dealing with p y gcharacterization of obligations as debt or equity have done so in the context of inter-creditor disputes involving p grecharacterization of “third” party, non-debtor “loans rather than treatment of inter-debtor obligations” g

8

Is Loan “Debt” or “Equity”?

Courts factors rely upon fall into 3 general t icategories:

□ (i) the formality of the loan agreement

(ii) th fi i l it ti f th i t th ti □ (ii) the financial situation of the issuer at the time the creditor made the purported loan

□ (iii) the relationship between the debtor and creditor

9

Factors Courts Look at to Determine Whether Claim is Debt or EquityWhether Claim is Debt or Equity

• Names given to instrument

• Fixed maturity date and schedule of paymentsFixed maturity date and schedule of payments

• Fixed rate of interest and interest payments

• Source of Repayment

• Adequacy of capitalization • Adequacy of capitalization

• Identity of interests between creditor and stockholder

• Security for the transfer

• Ability to obtain financing from outside lending institutions• Ability to obtain financing from outside lending institutions

• Extent to which advances are subordinated to claims of outside creditors

• Extent to which advances were used to acquire capital assets

Si ki f d t id t • Sinking fund to provide repayment

• Right to enforce payment of principal and interest

• Participation in management flowing as a result of the advance

• Intent of the parties

• Source of interest payments and payment of interest according to the terms of the loan10

Is Intercompany Claim Debt or Equity?

In re Radnor, 353 B. R. 820 (D. Del. 2006)(“ overarching inquiry is Intent of . . . overarching inquiry is . . . Intent of

parties at the time of transaction . . . Through a common sense evaluation of the facts and circumstances surrounding a facts and circumstances surrounding a transaction.”)

The priority of intercompany claims will be p y p ydependent on whether the claim resembles or was intended to be debt, equity or preferred equity/subordinated debtp q y

11

Subordination of Intercompany Claims

In addition to recharacterization, intercompany claims may also be equitably intercompany claims may also be equitably subordinated under Bankruptcy Code §510(c) or applicable law

Factors courts look to:□ Has claimant engaged in some type of inequitable

conduct (fraud, illegality, breach of fiduciary conduct (fraud, illegality, breach of fiduciary duties, undercapitalization, use of debtor as mere instrumentality or alter ego)

□ Has claimant caused injury to creditors or has his □ Has claimant caused injury to creditors or has his conduct conferred an unfair advantage on the claimant

□ Subordinate as long as it is not inconsistent with the □ Subordinate as long as it is not inconsistent with the provisions of the Bankruptcy Code

12

Elimination of Intercompany Claims

Substantive consolidation is another way to deal with intercompany claimsdeal with intercompany claims

The idea is that related companies liabilities are combined, eliminating intercompany claims and creating a larger intercompany claims, and creating a larger pool of creditors to vote on a single plan of reorganization

While different depending on circuit the While different depending on circuit, the general inquiry is whether creditors dealt with the entities as a single economic unit in extending credit or whether the affairs in extending credit or whether the affairs of the debtor are so entangled that consolidation benefits all creditors

13

How are Intercompany Claims Created?

Cash transfers between related entities

Contribution of assets among entities

Allocation of costs of doing business among entities

Allocation of tax benefits among parent and subsidiariessubsidiaries

Guarantee claims of parents and subsidiariessubsidiaries

14

Fraudulent Transfer Issues that Arise Relating to Inter-Company Claims in Bankruptcy

S b idi t th b i f Subsidiary guarantees the borrowing of Parent (Upstream Guaranty)□ What value did Sub obtain by guaranteeing Parent

bli ti ?obligation?

□ Was that value fair consideration or for reasonably equivalent value to the cost of the guaranty

Difficult issuesR i d t i ti f h t th “ t” f th □ Requires a determination of what the “cost” of the guaranty

□ What + value did Sub confer upon Parent by signing the guaranty?the guaranty?

15

Parent guarantees the debts of a Subsidiary (d t t ) hil S b i l t (downstream guaranty) while Sub is solvent should not be a fraudulent conveyance

A downstream guaranty however may A downstream guaranty however may qualify as a fraudulent conveyance if the subsidiary is insolvent

Not likely to find these guarantees qualify as a fraudulent conveyance

16

I TOUSA A C S dIn re TOUSA: A Case Study

Mark D. Blooma ooGreenberg Traurig333 SE 2nd AvenueSuite 4400Suite 4400Miami, FL [email protected]

Background

TOUSA, Inc. and its subsidiaries were one of the largest residential homebuilders in the U Slargest residential homebuilders in the U.S.

In June 2005, TOUSA enters into a joint venture and in connection therewith, borrows $675 million from h T L d ( h “T JV”)the Transeastern Lenders (the “Transeastern JV”).

TOUSA, Inc. (Parent) guaranteed the obligations of the Transeastern JV to the Transeastern Lenders.

None of TOUSA Inc.’s subsidiaries were borrowers, pledgors, or guarantors to the Transeastern Lenders.

18

Background

Towards the end of 2006, the Transeastern JV fails and the Transeastern Lenders sue TOUSA, Inc. on its guarantees (“Transeastern Litigation”).

A significant judgment against TOUSA, Inc. would constitute a default under various other financial obligations, including bond and other debtdebt.

TOUSA, Inc.'s subsidiaries were guarantors of those other financial obligations and had pledged their assets as security for some of those obligations.

To avoid defaults under those other obligations, TOUSA, Inc. settled the Transeastern Litigation on July 31, 2007 for over $421 million.

TOUSA, Inc. and its subsidiaries (“Conveying Subsidiaries”) b d l f $500 illi f N L d ( h “N L ”) borrowed a total of $500 million from New Lenders (the “New Loans”) to finance the Transeastern settlement, and both TOUSA and the Conveying Subsidiaries pledged substantially all of their collective assets to secure the New Loans. The Conveying Subsidiaries were joint obligors on these New Loans despite not being parties to the joint-obligors on these New Loans despite not being parties to the Transeastern Litigation.

19

TOUSA Files Bankruptcy and the Committee Files Suit Committee Files Suit

TOUSA, Inc. and most of its subsidiaries, i l di th C i S b idi i fil including the Conveying Subsidiaries, file for bankruptcy in January, 2008.

In addition to its secured debt TOUSA owed In addition to its secured debt, TOUSA owed over $1 billion in bond debt.

The Official Committee of Unsecured The Official Committee of Unsecured Creditors files an adversary proceeding on behalf of the Conveying Subsidiaries seeking to avoid the loan obligations and seeking to avoid the loan obligations and liens granted to the New Lenders and to recover over $400 million in payments made to the Transeastern Lenders.

20

The Committee’s Claims

Loan obligations assumed and liens granted by Conveying Subsidiaries in connection with New Loans were avoidable fraudulent transfers in accordance with 11 U.S.C. § 548

□ Obligations under New Loan rendered Conveying g y gSubsidiaries insolvent

□ Conveying Subsidiaries were not obligated on Transeastern Loan (and did not receive any portion of ( y pNew Loans) so did not receive reasonably equivalent value

Loan obligations assumed and liens granted were Loan obligations assumed and liens granted were avoidable fraudulent transfers, and since transfers were made for the benefit of the Transeastern Lenders, they were recoverable pursuant to 11 y pU.S.C. § 550 (the “entity for whose benefit such transfer was made”)

21

The Lenders’ Defenses

Solvency:

□ The Conveying Subsidiaries were not insolvent before the Transeastern Settlement and were not rendered insolvent by the settlement.

Reasonably equivalent value Reasonably equivalent value

□ The Transeastern Settlement staved off a TOUSA bankruptcy filing that would have triggered an event of default under Conveying Subsidiaries’ financial obligations (bonds). Co vey g Subs d a es a c al obl gat o s (bo ds).

□ Settling Transeastern litigation brought value to entire enterprise, including the Conveying Subsidiaries.

Savings Clause: Savings Clause:

□ The New Loans contained “Savings Clauses” that purported to reduce the obligations incurred and liens granted to the extent necessary to prevent the obligor’s insolvency.y p g y

22

Bankruptcy Court Decision

Official Comm. of Unsecured Creditors of TOUSA I Citi N A I (I TOUSA, Inc. v. Citicorp N. Am., Inc. (In re TOUSA, Inc.), 422 B.R. 783 (Bankr. S.D. Fla. 2009).)

The bankruptcy court ruled in favor of the Committee in a 180-page opinion.

Bankruptcy Court’s Findings:□ TOUSA and its subsidiaries were insolvent even

b f i i th N Lbefore incurring the New Loans

□ Conveying Subsidiaries received no direct benefits and, at most, minimal indirect benefits from the Transeastern Settlement

23

Bankruptcy Court Decision

□ Savings clauses unenforceable because they were Conditioned on Insolvency in violation of §541(c)(1)(b) Conditioned on Insolvency in violation of §541(c)(1)(b) and “too cute to be enforced.”

□ The Transeastern Lenders were the entities "for whose benefit the transfers were made“ and had a duty to benefit the transfers were made and had a duty to determine that Conveying Subsidiaries had received fair value or that they were solvent before accepting settlement payment.

24

District Court Decision

3V Capital Master Fund Ltd v Official Comm. Of Unsecured Creditors of TOUSA Inc (In re TOUSA Unsecured Creditors of TOUSA Inc (In re TOUSA, Inc.), 444 B.R. 613 (S.D. Fla. 2011).

Reverses and Quashes Bankruptcy Court Ruling

There was no liability under Section 548 because:

□ The Transeastern Settlement provided indirect benefits to the Conveying Subsidiaries which included avoiding a to the Conveying Subsidiaries, which included avoiding a default on bond and other financial obligations and temporarily avoiding bankruptcy. Additional indirect benefits can be recognized through enterprise theory.

□ The Conveying Subsidiaries had no property interest in the New Loans such that the Transeastern Lenders did not receive any transfer from the debtor (Conveying

b d d b l lSubsidiaries) as required by Section 548 (only applies to a transfer of “an interest of the debtor” in property).

25

District Court Decision

□ Transeastern Lenders were not the entities “for whose benefit” the Conveying Subsidiaries whose benefit the Conveying Subsidiaries transferred liens to the New Lenders.

□ Even if Transeastern Lenders were “immediate f ” h k f l f lid transferees,” they took for value—payment of valid

antecedent debt—and there was no evidence of bad faith. The Bankruptcy Court’s standard for lender diligence in connection with accepting payment diligence in connection with accepting payment deemed "patently unreasonable and unworkable.“

□ The District Court did not reach the savings clause issue.

26

Eleventh Circuit Decision

Senior Transeastern Lenders v. Official C f U d C dit (I Comm. of Unsecured Creditors (In re TOUSA, Inc.), 2012 W.L. 1673910 (11th Cir. May 15, 2012).y , )

Two Issues on Appeal:□ Whether Bankruptcy Court clearly erred in finding p y y g

that Conveying Subsidiaries did not receive reasonably equivalent value.

□ Whether Transeastern Lenders were entities “for □ Whether Transeastern Lenders were entities for whose benefit” the Conveying Subsidiaries transferred the liens.

27

Eleventh Circuit Decision

District Court Reversed□ Bankruptcy Court did not commit “clearly error” in

finding subsidiaries did not receive reasonably equivalent value; and

□ Transeastern Lenders were entities “for whose benefit” the liens were granted

28

Eleventh Circuit Decision

Reasonably Equivalent Value

□ The bankruptcy record supported that the value to the Conveying Subsidiaries considered as a whole, “fell well short of reasonably equivalent value”

Minimal value to Conveying Subsidiaries “far out-weighed any perceived benefits.”

Transeastern Settlement and New Loans did more harm than good and “at most delayed the inevitable”good and “at most delayed the inevitable”

□ Avoidance of bankruptcy has very limited value -- “The opportunity to avoid bankruptcy does not free a company to pay any price or bear any burden After all ‘there is to pay any price or bear any burden. After all, there is no reason to treat bankruptcy as a bogeyman, as a fate worse than death.’” Olympia Equip. Leasing Co. v. W. Union Tel. Co., 786 F.2d 794, 802 (7th Cir. 1986) (Easterbrook, J., concurring)

29

Eleventh Circuit Decision

The New Loans were “for the benefit of” th T t L dthe Transeastern Lenders□ Transeastern Lenders were “initial transferees”

A t t d i ti ith N L □ Agreements executed in connection with New Loans expressly provided that the loan proceeds were to be used to fund the Transeastern Settlement

□ TOUSA subsidiaries not initial transferees because of a lack of any control over the funds

30

Eleventh Circuit Decision

Reasonable to expect “some” diligence f dit b i id h d d f from creditors being repaid hundreds of millions of dollars

In response to Transeastern Lenders’ In response to Transeastern Lenders argument that the Bankruptcy Court exercised hindsight bias, the Eleventh Ci i dCircuit noted:□ “In contrast with the surprise attack at Pearl

Harbor, the warnings about the collapse of TOUSA Harbor, the warnings about the collapse of TOUSA made that event as foreseeable as the bombing of Nagasaki after President Truman’s ultimatum”

31

Eleventh Circuit Decision

Remanded to the District Court to consider th f ll i ithe following issues:□ Remedies –- In light of the District Court’s reversal

and quashing of the Bankruptcy Court’s decision, q g p y ,the District Court did not address the remedies imposed by the Bankruptcy Court.

□ Issues of judicial assignment and consolidation □ Issues of judicial assignment and consolidation.

32

Follow Up

Eleventh Circuit denied en banc rehearing f TOUSA lof TOUSA appeal.

On remand, case was re-assigned to, and consolidated nine separate appeals before consolidated nine separate appeals before, Judge Michael Moore (no, not that Michael Moore).

Briefing was completed a few weeks ago.

33

Intercompany Loans and G V l i IGuarantees: Valuation Issues

Kose Johnose JoNERA Economic Consulting

kj h t [email protected]

Overview

Economic Perspective on the pvaluation of risky debt, and that of intercompany guaranteesp y g

Effect of Fraudulent Conveyance on creditor outcomeon creditor outcome

Not to be construed as legal d iadvise

35

Basics

Default risk and valuation of risky debt

Two approaches in the finance Two approaches in the finance literature

St t l M d l Structural Models

Reduced-Form Models

36

Structural Models APPROACH: Likelihood of borrower default

over the horizon is modeled using the borrower’s capital structure the covenants borrower s capital structure, the covenants, intercompany guarantees, the guarantor’s capital structure, the asset value process of h b h l f hthe borrower, the asset value process of the

guarantor, and the degree of recourse implied by the guarantee.p y g

Starting point: Merton (Journal of Finance,1974).

Implemented using equity market information

37

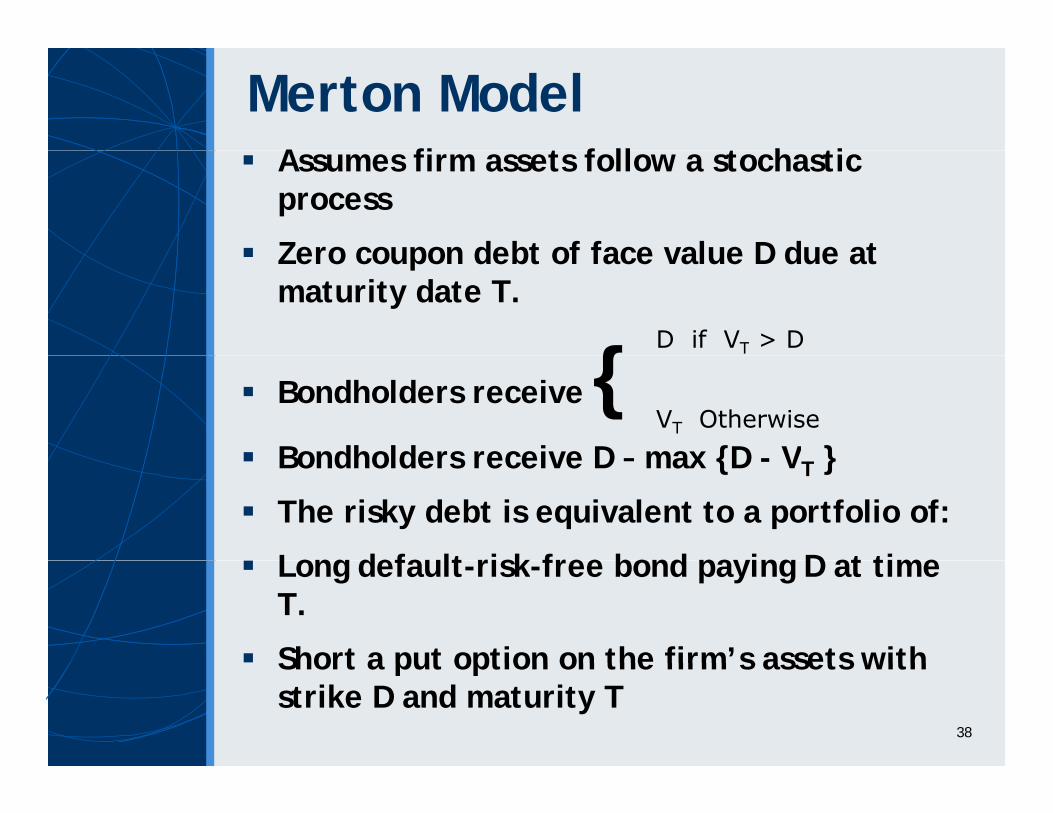

Merton ModelA fi t f ll t h ti Assumes firm assets follow a stochastic process

Zero coupon debt of face value D due at Zero coupon debt of face value D due at maturity date T.

{D if VT > D

Bondholders receive { Bondholders receive D – max {D - V }

VT Otherwise

Bondholders receive D – max {D - VT }

The risky debt is equivalent to a portfolio of:

Long default risk free bond paying D at time Long default-risk-free bond paying D at time T.

Short a put option on the firm’s assets with Short a put option on the firm s assets with strike D and maturity T

38

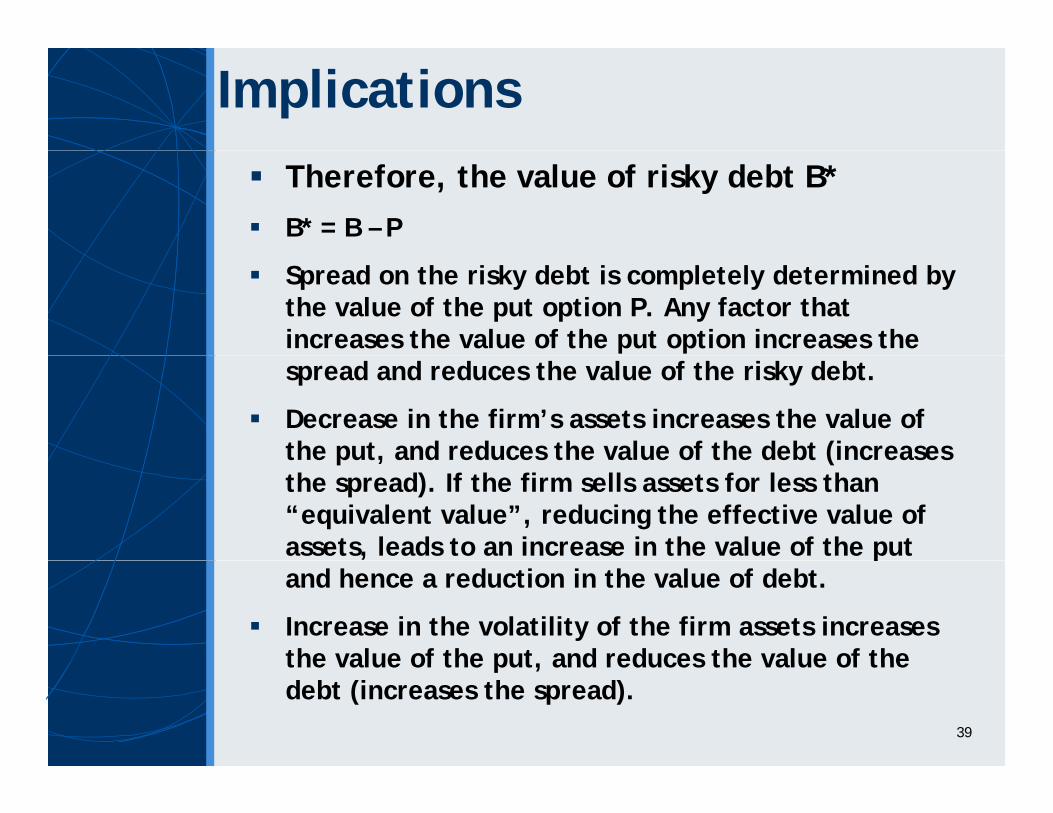

Implications Therefore, the value of risky debt B* B* = B – P

Spread on the risky debt is completely determined by the value of the put option P. Any factor that increases the value of the put option increases the spread and reduces the value of the risky debt.

Decrease in the firm’s assets increases the value of the put, and reduces the value of the debt (increases the put, and reduces the value of the debt (increases the spread). If the firm sells assets for less than “equivalent value”, reducing the effective value of assets, leads to an increase in the value of the put pand hence a reduction in the value of debt.

Increase in the volatility of the firm assets increases the value of the put and reduces the value of the the value of the put, and reduces the value of the debt (increases the spread).

39

Value of an absolute guarantee

Value of risky debt B* B* = B – P

Assume that our loan now is guaranteed by another company with sufficient unencumbered assets. The level of assets of the guarantor are such that with the guarantee the originally risky debt is effectively “riskless”. (We call this a “Absolute” guarantee. Since the guarantee increases the value of the risky d bt f B* t B th l f th t i debt from B* to B, the value of the guarantee is

B – B* = P.

Hence Value of an Absolute guarantee = P the Hence, Value of an Absolute guarantee = P, the value of the put.

40

Value of a loan guaranteeI th l f i t In the more general case of an intercompany guarantee, it is not absolute. The guarantor has assets of value VG and debt of face value G DG. Also assume that the guarantor’s debt has priority over the guaranteed debt. Under these assumptions the debt with the these assumptions, the debt with the guarantee will have a value, BG* = B – PG

Where the value of a put option PG with p p G underlying assets, (VT + VG – DG ) and strike price D. The value of the guarantee is the increase in value of the debt with the guarantee: increase in value of the debt with the guarantee: BG* - B* = (B – PG ) - (B – P) = P – PG

Hence, the value of the guarantee is the e ce, t e value o t e gua a tee s t e reduction in the value of the put (= P – PG ) due to the guarantee. 41

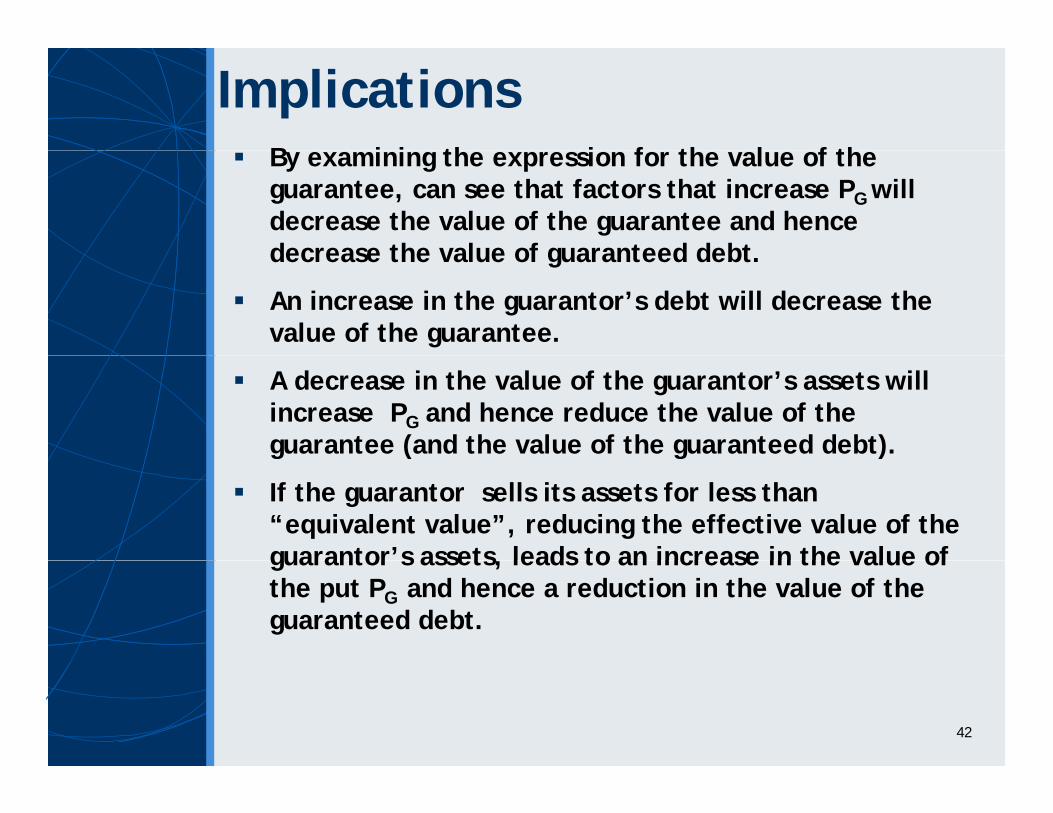

ImplicationsB i i th i f th l f th By examining the expression for the value of the guarantee, can see that factors that increase PG will decrease the value of the guarantee and hence decrease the value of guaranteed debt decrease the value of guaranteed debt.

An increase in the guarantor’s debt will decrease the value of the guarantee.

A decrease in the value of the guarantor’s assets will increase PG and hence reduce the value of the guarantee (and the value of the guaranteed debt).g ( g )

If the guarantor sells its assets for less than “equivalent value”, reducing the effective value of the guarantor’s assets leads to an increase in the value of guarantor s assets, leads to an increase in the value of the put PG and hence a reduction in the value of the guaranteed debt.

42

Extensions Default only at maturity

No covenants, No coupons

No deviations from Absolute Priority Rule

No renegotiation of debtg

No guarantees

Liquidation and transfer is costlessLiquidation and transfer is costless

Several Extensions

Delianedis-Geske (1998) UCLA-WPDelianedis Geske (1998) UCLA WP

The Moody’s KMV model: Based on Merton (1974) model ( )http://www.moodyskmv.com

43

Reduced Form Models APPROACH: A process is posited for the

default likelihood that is then calibrated to the prices of debt securities and credit the prices of debt securities and credit derivatives.

Implemented using debt market and credit Implemented using debt market and credit derivative data.

Litterman-Iben (1991, Journal of Portfolio Management).

Duffie-Singleton (1999, Review of Financial St di )Studies)

My opinion, given all necessary data is available structural models are superior available, structural models are superior for valuing complex debt and intercompany guarantees. 44

Who gets what value?W d b fi d t fi We assumed borrower firm and guarantor firm are independent.

The value of the guarantee is (P P ) The value of the guarantee is (P – PG)

Debt with guarantee is higher in value by

(P P )(P – PG)

If debt is correctly priced, the debt holders pay the borrowing firm the higher pricethe borrowing firm the higher price.

After the guarantee, the equity of the guarantor firm would be of lower value by (P – PG).y ( G)

The borrowing firm should pay (P – PG) to the equity holders of the guarantor firm equity holders of the guarantor firm (P – PG), the value of the guarantee.

45

Parent-Subsidy Guarantees Thus far, we assumed borrower firm and guarantor Thus far, we assumed borrower firm and guarantor

firm are independent.

Consider the case where the guarantor is the parent firm and the borrower is a subsidiary.

Ownership structure would matter for the allocation of the value of the guarantee (P P )allocation of the value of the guarantee (P – PG)

Debt holders pay the subsidiary firm the higher price.price.

After the guarantee, the equity of the parent firm would be of lower value by (P – PG).

If the subsidiary is fully owned, the increase in the value of the sub equity will offset the reduction in the value of the parent equity.p q y

No explicit payment for the guarantee is necessary. 46

Parent-Subsidy Guarantees (Cont’d)

O th th h d if b idi i t f ll On the other hand, if subsidiary is not fully owned, the parent equity holders will only be partially compensated by the increase in value of p y p ysub equity from the guarantee. An explicit payment is necessary to compensate the equity holders of the parent firm holders of the parent firm.

A parallel analysis will do for the case of the parent debt being guaranteed by the subsidiary p g g y yassets.

Again, ownership structure would matter for the allocation of the value of the guarantee (P – PG)

47

Parent-Subsidy Guarantees (Cont’d)

In the case of a fully owned subsidiary, the loss in value of the sub equity due to the guarantee is offset by the gain in value guarantee is offset by the gain in value resulting from the guarantee enjoyed by the parent equity (given the debt holders pay h h h h l f d bthe parent the higher value of debt

reflecting the subsidiary guarantee). No explicit payment for guarantee is necessary.p p y g y

On the other hand, if subsidiary is not fully owned, the subsidiary equity holders will only be partially compensated for the loss in value and an explicit payment is necessary.

48

![UNDOING FRAUDULENT CONVEYANCE...other person’s death.] The couple believed it to be the case and it was in fact the case that the transferor had no beneficial interest in the property](https://img.pdfslide.net/doc/110x75/5fa058a9e885ad067b1bd105/undoing-fraudulent-other-personas-death-the-couple-believed-it-to-be-the.jpg)