Embed Size (px)

Citation preview

CATALYST RESEARCH REPORT

From Customer Relationship Management to Customer-Managed Relationships:

TARA LITCHFIELD | DIRECTOR OF EXPERIENCE DESIGN

The Key to Successful Retail Bank Onboarding

The Key to Successful Retail Bank Onboarding Page 2

TABLE OF CONTENTS

Executive Summary.......................................................................3

About Catalyst ..............................................................................4

Who Should Read This Report .......................................................4

Study Methodology .....................................................................4

Global Findings .............................................................................5

Account Opening Preferences ....................................................5

Building Trust .............................................................................. 5

Recommendations ..................................................................... 7

Customer Segment Findings .......................................................10

Bank Segmentation and Use-Based Personas ........................10

Carli—Mobile Free Spirit ...................................................... 11

Eric—Tech-Savvy Researcher ..............................................13

Paulette—Trusted Community Member ..............................15

Bank onboarding journeys and opportunities ....................17

Conclusions ................................................................................18

Next Steps ..................................................................................19

About the Author, Tara Litchfield .................................................20

More About Catalyst ...................................................................20

The Key to Successful Retail Bank Onboarding Page 3

EXECUTIVE SUMMARY

In retail banking, it’s a well-established axiom that the best time to expand the account relationship is during onboarding, or the first 90 days. We know from previous research that 75% of all cross-sell opportunities occur within the first 90 days.

What is not so clear-cut is, what is the best approach to maximize opportunities during those first 90 days of onboarding. What are the right products to offer customers? When? How?

First and foremost, it’s critical to earn the customer’s trust before presenting cross-sell offers. To earn the customer’s trust, the bank must be able to gain a deeper understanding of that customer, which is accomplished through persona development and segmentation. Only after it is armed with this knowledge will the bank be able to deliver the right products and services at the right times in the right channels.

At its most basic, to expand the customer relationship, the bank must be able to deliver in three key areas: effective customer segmentation, properly personalized communications and giving the customer more control over financial decisions. Only after implementing these strategies can a bank consistently and successfully cross-sell and upsell, give appropriate financial advice, and deliver a superior customer experience.

But what exactly is involved in effective customer segmentation? Who are these customer segments? What are their needs and wants? How do you get them to trust you? According to what bank

customers told us during the research interviews we conducted, new account holders had three distinct personas, based on the different ways that they banked:

1. Mobile Free Spirits—Customers with a preference for mobile banking

2. Tech-Savvy Researchers—Customers with a preference for online banking

3. Trusted Community Members—Customers with a preference for branch banking

By analyzing their feedback about their recent onboarding experiences, we uncovered a general framework to increase cross-sell opportunities for every customer. We also uncovered segment-specific preferences that pointed to additional opportunities.

Moderate trust

Minimal trust or no trust

Complete trust

44%

49%

7%

Degree of trust in provider

Moderate trust

Minimal trust or no trust

Complete trust

44%

49%

7%

Degree of trust in provider

1 Source: Winning through customer experience, EY Global Consumer Banking Survey 2014, http://www.ey.com/Publication/vwLUAssets/EY_-_Global_Consumer_Banking_Survey_2014/$FILE/EY-Global-Consumer-Banking-Survey-2014.pdf

The Key to Successful Retail Bank Onboarding Page 4

ABOUT CATALYST

Catalyst is a marketing agency that combines complex data analysis, marketing technology and experience design to deliver more profitable retail banking customers. From time to time, we conduct research to help our clients better understand their customers and their customers’ journeys. We then apply analytics and technology to develop solutions that translate these insights into improved customer experiences.

WHO SHOULD READ THIS REPORT

• CMOs

• VPs of Marketing

• VPs of Analytics

• Customer Experience Professionals

• Acquisition and Retention Professionals

• Digital Marketing Professionals

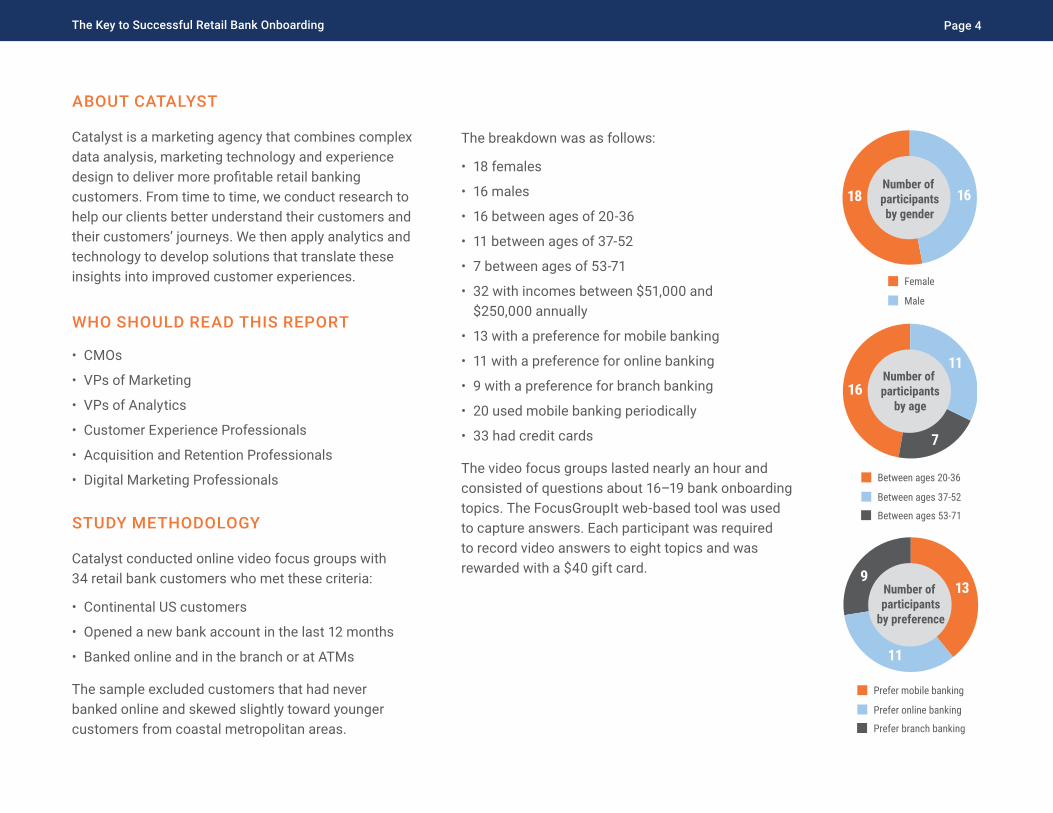

STUDY METHODOLOGY

Catalyst conducted online video focus groups with 34 retail bank customers who met these criteria:

• Continental US customers

• Opened a new bank account in the last 12 months

• Banked online and in the branch or at ATMs

The sample excluded customers that had never banked online and skewed slightly toward younger customers from coastal metropolitan areas.

The breakdown was as follows:

• 18 females

• 16 males

• 16 between ages of 20-36

• 11 between ages of 37-52

• 7 between ages of 53-71

• 32 with incomes between $51,000 and $250,000 annually

• 13 with a preference for mobile banking

• 11 with a preference for online banking

• 9 with a preference for branch banking

• 20 used mobile banking periodically

• 33 had credit cards

The video focus groups lasted nearly an hour and consisted of questions about 16–19 bank onboarding topics. The FocusGroupIt web-based tool was used to capture answers. Each participant was required to record video answers to eight topics and was rewarded with a $40 gift card.

Between ages 53-71

Between ages 37-52

Between ages 20-36

16

7

11Number of participants

by age

Prefer branch banking

Prefer online banking

Prefer mobile banking

9

11

13Number of participants

by preference

Male

Female

18 16Number of participantsby gender

The Key to Successful Retail Bank Onboarding Page 5

GLOBAL FINDINGS

ACCOUNT OPENING PREFERENCES

Most customers prefer to open an account online

Customers from all three segments preferred to open an account online because it was more convenient, and they were able to ask bankers questions via online chat and phone. Many participants had opened an account online before and were pleasantly surprised by the quick and easy process. Most customers would have liked being able to add additional products and services online without making a trip to the branch.

One group of customers preferred to open an account at the branch because they felt that it was more important to develop a personal relationship with their banker. These customers wanted to interact face to face to validate the credibility of the banker’s advice. However, they were frustrated by wait times in the branch and preferred to make a specific appointment.

“ Ideally I would love to do everything online using an online banking platform because it would be convenient and I can do it at home or at work and I don’t have to miss work or set aside time to do it.” Daney

“ I would prefer to sign up online because it is usually quick and easy to do so, with instant approval in some cases.” Brandon

BUILDING TRUST

Banks need to show that they are trustworthy to capitalize on opportunities

Customers initiated their bank relationship with a great deal of trust already established. They believed that the bank would keep their money and personal data safe. Most customers were willing to provide their bank with a great deal of personal information in exchange for tailored financial options … but only at the time they opened their new account. Stated “fair game” information included:

• Family members’ ages• Household income• Information about other accounts or investments• Information about occupation or business• Loan and mortgage information• Asset information• Insurance information• Retirement information• Financial goals• Information about upcoming financial needs

We recommend taking advantage of the customer’s willingness to provide information during account opening because customers are much less inclined to provide it later.

“ Sharing personal information—it’s part of the process when signing up. I have no problem sharing any of this information. I guess I would rather share it in the beginning.” David

The Key to Successful Retail Bank Onboarding Page 6

It takes time to develop trust. Great customer service with great self-service tools are key

Typically, it took customers one to three months—and sometimes even longer—to trust the bank’s ability to provide financial advice about new products and services. The bank first had to prove to the customer that it could be trusted. Customers immediately lost trust in their bank when they felt like bank associates were trying to upsell them with other products or offers too soon.

Customers’ trust grew exponentially after successfully using online platforms, mobile applications and customer service call centers to get help and manage their accounts. The more trust customers had in their bank, the more willing they were to consider that bank for additional products and services. The better the customer service and the better the time-saving digital self-service tools, the more likely customers were to trust the bank.

Customers liked having access to relevant product information in the least intrusive ways.

“ I like to do both an in-person and online process. In person, I can ask questions, I can go over things. It’s more personable. Online, I can do my own search and explore every bit of a service. So at the end you are full of information, which makes it easier to make a decision.” David

“ I think that there would be a certain amount of time that would need to pass for me to feel comfortable enough to give them all this personal information therefore having access to an online tool where I can provide this information at a later time would be best.” Daney

Exceptional customer service required more than just being helpful and fixing customers’ problems promptly. In addition to a customer service telephone number, customers wanted live chat, video conferencing, email, and online messaging. If there was a problem, most customers expected immediate personal assistance.

Customers also expected their mobile application and online banking platform to be personalized as well as easy to use. They wanted tailored financial advice and offers specific to their individual situations. Customers also wanted to be able to schedule and engage in real-time personal discussions, and they expected the person on the other end to be familiar with their personal situation.

The Key to Successful Retail Bank Onboarding Page 7

RECOMMENDATIONS

Give customers more control: Pull vs. push

Customers want to be in the driver’s seat and reach out when they are ready. Banks should train their employees to provide service, not sell. Following are three ways that banks should behave to drive customers to them, rather than the other way around:

1. Digital interaction with self-service tools

Banks need to provide customers with personalized interactive tools that let customers interact how they want, when they want. This is the key to evolving from customer relationship management to customer-managed relationships.

“�I�would�love�an�interactive�financial�tool.”�Eric

“ If I feel like my bank is educating me to be smarter about my finances,�I’d�be�less�likely�to�feel�like�they’re�trying�to�take�advantage of me later when they suggest a service.” Dayle

2. Branch behavior

In the branch, banks need to focus on solving customers’ problems and giving helpful advice vs. pushing products. Banks have not gained the customer’s permission to market to them at this point in the relationship, and doing so erodes trust and satisfaction.

“ I prefer to get info that I specifically ask for, or info about something new and innovative (not just a run of the mill product or promotion).” Cynthia

“ Banking customer service is very impersonal and I find that the representatives are too scripted.” Lawrence

3. Phone behavior

When customers call the customer service line for help solving a problem, the last thing they want or need is an automated message or a live human attempting to upsell them on a product or service—often one that is entirely inappropriate for their personal situation. Again, banks need to focus on solving the problem at hand and offering tailored advice rather than upselling, which is perceived as an intrusion.

“ The customer service was excellent—just lots of annoying, super-nice upselling.” Kristian

“ I want information on products. I would want to be gently told where�to�find�the�information�when�I�was�ready,�not�barraged�with it.” Eric

The Key to Successful Retail Bank Onboarding Page 8

Add live chat and video conferencing

The preferred customer service channels were live chat and phone. Overwhelmingly, customers wanted live online chat via mobile app or online banking platform to resolve problems quickly and answer questions. Online chat was preferred mostly because it was available anywhere and more often.

Customers preferred service by phone or by video conference when a problem or request was complex. Customers liked video conferencing because they could see the bank associate face to face and could use their computer to make the call. Tech-savvy customers preferred this option most.

Phone calls with a live person and video conferencing also helped build trust: Customers could develop more of a personal connection to a person they could see and hear. Ideally, customers wanted to chat, conference and call their personal banker whenever possible, rather than make the trip to the branch.

“ It could be improved by having a live chat feature because questions could be answered quickly, rather than waiting for email communications.” Audrey

“ One way that my bank could improve their customer service is they could be available 24/7 online in case I have questions.” Daney

“ Chat with a knowledgeable person is the best customer service option.” Eric

Don’t automatically send a printed welcome kit

Most new customers didn’t use their welcome kits. Many customers said the welcome kit was redundant or that they lost them shortly thereafter.

Customers who did use welcome kits preferred to receive them digitally. Online-only bank customers liked welcome kits most.

“ I think the welcome kit just had some information about direct deposit and bank services. It wasn’t that helpful because most of it was available online. I would prefer a welcome kit via email because the paper kit seems wasteful.” Audrey

“ The welcome kit was a few brochures “upselling” different services that the bank offered, which I promptly threw away.” Dayle

The Key to Successful Retail Bank Onboarding Page 9

Give qualified customers a personal banker

Certain customers wanted a personal banker to add value to the bank-customer relationship. They expected to have access to this relationship not only in the branch but also online. Many customers liked the idea of monthly meetings with their personal banker to get help managing their finances and plan for the future.

“ My needs are better served with dedicated customer service reps who I do not have to wait in a queue for. The option to have the rep call me back at a time that will work for me is an extremely nice feature.” Cynthia

“ [I want] someone I can work with directly and consistently who could get to know my situation and advise me to the best of their ability.” Jeanine

Communicate digitally

Our focus group participants overwhelmingly preferred to receive personalized, helpful advice that they could read digitally. They liked the online banking platform, email, or mobile application for product and offer information. Many customers preferred secure online tools for financial advice. Most were interested in trying an interactive online tool that offered personalized advice.

Most customers we interviewed preferred to receive bank communications, including product offers, digitally. They welcomed an online platform and a mobile application with personalized offers in a dashboard, which they could view at their leisure.

A monthly email with financial advice from their personal banker was acceptable, in terms of both content and frequency. The more personalized the email communications were, the more helpful they were, and the more they helped encourage trust.

Different segments responded differently to various types of offers, communication styles and communication channels. But even people who preferred to bank in-branch wanted to hear from their bank via email.

Note: Since our sample excluded customers who had no digital interaction with their bank, we would expect to see a preference for digital communications.

The Key to Successful Retail Bank Onboarding Page 10

CUSTOMER SEGMENT FINDINGS

BANK SEGMENTATION AND USE-BASED PERSONAS

We separated participants into three segments based on their preference for mobile, online, or branch banking. We leveraged recruitment marketing data and the study’s qualitative data to develop personas for three distinct groups of customers:

1. Mobile Free Spirits (mobile preference)

2. Tech-Savvy Researchers (online preference)

3. Trusted Community Members (branch preference)

Customer Journeys

Account Opening Follow-Up Self-Service Long-Term Advice

Tech-Savvy Researchers

MobileFree Spirits

Trusted CommunityMembers

+feeling

_feeling

LiveChat

ByPhone

InBranch

OnlinePlatform

ByEmail

Preferred Customer Service Option

Tech-SavvyResearchers

Mobile FreeSpirits

TrustedCommunityMembers

Bank Persona Populations

Prefer keepingmultiple banks for different products

Prefer 1 bank

Open toconsolidatinginto 1 bank

Preferred Banking Relationship

During the recruitment process, we found larger groups of mobile and online users, plus a smaller group that preferred to bank in-branch. The mobile preference group was slightly larger than the online preference group. Mobile Free Spirits were the most diverse group in terms of demographics: They owned more products and were looking for financial advice from their bank more often than Tech-Savvy Researchers. Thus, Mobile Free Spirits represented the largest opportunity group.

Although Trusted Community Members were fewer in number, they represented significant opportunities because they were loyal to one bank and held the second-highest number of products. These customers, often approaching retirement, were also seeking financial advice from their bank.

The Key to Successful Retail Bank Onboarding Page 11

Carli’s Story

Carli is a full-time mom who enjoys being out and about often during the day with her two young children. Her husband owns a landscaping company, so sometimes she runs errands for him. Since she is very busy, she doesn’t spend much time in front of a computer screen at home. She is a former corporate accountant, so she likes to take an active role in the family’s finances. She loves her new Bank of America mobile app and prefers to use it for most of her banking needs. If she does have a question or a problem on her account, she will call customer service or stop by her local branch to get assistance.

Banking Preference

Payment Preference

NUMBER OF FINANCIAL PRODUCTS

Context of Use

LOW HIGH

ATM USE

LOW HIGH

CASH USE

LOW HIGH

TECHNICAL SKILL

LOW HIGH

CarliMobile Free Spirit

AGE

OCCUPATION

MARITAL STATUS

LOCATION

30

STAY-AT-HOME MOM

MARRIED

RICHMOND, CA

NEW BANK

OTHER BANKS

BANK OF AMERICA

WELLS FARGO, FIDELITY

“I opened a new bank account because I was tired of the lack of locations by my current bank, so I wanted to have more convenience when it came to banking and a better user experience with the mobile app.”

Yoga, Exercising, Gardening, Swimming, Travel, Blogging

Interests

Friendly Active Easygoing

Customer Service Channel Preference

LIVE CHAT ON MY MOBILE APP

CALLING BY PHONE

TEXT OR EMAIL REPLY

ONLINE PLATFORM & VIDEO CONFERENCE

IN PERSON IN THE BRANCH

Mobile Banking

Digital Wallet orCredit Card

Biggest Opportunity

Mobile Live Chat

CONVENIENCEConvenient banking when and how I need it, including mobile, ATM, and branch banking

SELF-SERVICEEasy-to-use mobile app for basic tasks like viewing balances, depositing checks, paying bills, and transferring money

TRANSPARENCY OF COSTClear communications on fees, rates, discounts, and bank product options

Banking Goals

The Key to Successful Retail Bank Onboarding Page 12

Carli’s Bank Onboarding Journey

ACCOUNT OPENING

FEEL

ING

OP

PO

RTU

NIT

IES

–

DO

ING

+TH

INKI

NG

Quick & Convenient Account Opening

MOBILE FREE SPIRIT – WANTS CONVENIENCE

Easy Access to InformationUsing My Phone

Easy-to-Use Mobile App &Quick 24/7 Customer Service

Mobile App AdviceI Can Follow Up On When Ready

FOLLOW-UP SELF-SERVICE & PROBLEM RESOLUTION LONG-TERM ADVICE

STARTDAY 1

DAY 90

DAY 7

DAY 14 DAY 30

Took longer than expected to open account at the branch

Logs in to mobile app Throws out welcome kit–

prefers digital documents

Bank sales associate calls and leaves product offer message on voicemail

Deposits checks and transfers money using the mobile app

“Online account sign-up just makes everything a lot quicker and more efficient. I don’t have to hear a sales pitch, I don’t have to spell anything out.”

“Sharing personal information - it's part of the process when signing up. I have no problem sharing any of this information. I guess I would rather share it in the beginning.”

“Actually, the kit was unhelpful I tossed it in the garbage. With the whole world online, I felt it was unnecessary.”

“If I need a service I don't need the bank to send me info. I would research it on my own then if I want the service I would call the bank.”

“I believe the bank's platform should have video demos.”

“I like chat and instant messaging to get answers to any questions.”

“I am generally looking for deals or cashback promotions that I can go ahead and add it to my account online as well as detailed graphs on my spending and a quick screenshot of all my account information.”

“I like to do both an in person and online process. In person I can ask questions, I can go over things. It's more personable. Online I can do my own search and explore every bit of a service.”

“I would prefer to do a credit card online. It’s hassle free and I feel confident in the bank's security.”

Uses live chat on the mobile app to understand a charge

Long wait time on customer service line to stop a check

Receives mobile app alert to transfer funds to avoid an overdraft

Receives email promotion about cash back credit card

Responds to email to ask about the credit card offer

Frustrated - online account openingwould be more convenient

Annoyed - communications shouldbe digital

Satisfied - I can use the mobile appfor most of my banking needs

Hopeful - looks like my bank has other great products and offers

• Account opening by phone or online

• Ask for information that can help personalize financial advice during the account opening process

• Account managers shouldn’t press new customers to add products, just offer options and explain the benefits

• Digital welcome kit

• An assigned account manager with direct contact details

• Follow-up communications by email, text, or mobile app

• Video demos of product features

• Mobile app that allows you to make wire transfers to different banks

• 24/7 live chat accessible via mobile app

• Mobile alerts that help you avoid unnecessary charges

• ATM locator on mobile app

• Ability to schedule appointments with bank associates

• Money management tools built into the mobile app

• Product recommendations and advice built into the mobile app experience

• Online product sign-up

Bank associate tries to push other product sign-up

No ATM locator on mobile app

GO

ALS

The Key to Successful Retail Bank Onboarding Page 13

Eric’s Story

Eric is a lawyer who specializes in corporate law. He represents many large companies and must travel often on assignment. He has been at his firm for a few years and has almost paid off his student loans. His daughter Jayla was born this past year, and he made it a priority to start saving for her future. He did a lot of online research before he found his new high-interest savings account. He is confident that he made the right decision now but will reevaluate his decision over time. He owns his own home and is paying a mortgage but likes to keep that and his student loans separate from his savings and checking accounts. He trusts the bank with his money and information, but he likes to make his own decisions when it comes to investing his money and opening accounts.

Banking Preference

Payment Preference

SELF-SERVICEEasy-to-use online platform that allows me to take care of all my banking online without going to a branch

EASY PRODUCT & RATE COMPARISONFinding the best financial products and rates for my needs

QUICK CUSTOMER SERVICEQuick and convenient remote customer service options

Banking Goals

NUMBER OF FINANCIAL PRODUCTS

Context of Use

LOW HIGH

ATM USE

LOW HIGH

CASH USE

LOW HIGH

TECHNICAL SKILL

LOW HIGH

EricTech-Savvy Researcher

AGE

OCCUPATION

MARITAL STATUS

LOCATION

37

LAWYER

MARRIED

CINCINNATI, OH

NEW BANK

OTHER BANKS

CAPITAL ONE 360

NRL MORTGAGE, CHASE

“I determined I needed an interest-bearing account for all the savings I was accumulating and my new account gives me a high 1.1% interest rate.”

Classic Cars, Working Out, Politics, and Current Affairs

Interests

Highly Educated Analytical Proactive

Customer Service Channel Preference

LIVE CHAT

CALLING BY PHONE

EMAIL REPLY

ONLINE PLATFORM & VIDEO CONFERENCE

IN PERSON IN THE BRANCH

Online Banking

Credit Card to maximize points

Biggest Opportunity

Interactive Online Self-Service Tools

The Key to Successful Retail Bank Onboarding Page 14

Eric’s Bank Onboarding Journey

ACCOUNT OPENING

FEEL

ING

OP

PO

RTU

NIT

IES

–

DO

ING

+TH

INKI

NG

Quick & Convenient Account Opening

TECH-SAVVY RESEARCHER – WANTS DIGITAL EASE OF USE

Unobtrusive Communications Easy-to-Use Online Platform &Remote Customer Service Options

Interactive Tools ThatProvide Information I Need

FOLLOW-UP SELF-SERVICE & PROBLEM RESOLUTION LONG-TERM ADVICE

STARTDAY 1

DAY 90Easy online account opening process

“I did fill out everything online. I had to submit identification and proof of address online. I would have preferred verification questions instead of sending documentation.”

“I thought it was simpler to do the entire process online even though I could have done it in the branch. I was unprepared during this process for them to start soliciting the opening of other accounts like a money market and CD.”

“A small welcome kit came by mail. I did not find it useful because I already knew the terms of my account.”

“I had to call customer service to activate my account even though I signed up online under the promotional deal. Bank's customer service would have been improved if they did what they said they would do, which was sending out my debit card within the next 5-7 business days.”

“I received answers to my questions by phone. Email is my preferred channel for getting answers.”

“I got all my answers thru the FAQ section also live chat feature... One improvement would be intuitive navigation with explicit tabs. I can navigate it yet it took months to understand.”

“If I feel like my bank is educating me to be smarter about my finances, I'd be less likely to feel like they're trying to take advantage of me later when they suggest a service.”

“I would want to be gently told where to find the information online when I was ready, not barraged with it. I would love a interactive financial tool.”

Relieved - online account openingprocess was easy

Mostly Satisfied - digitalcommunications suit my needs

Restless - I want to know if I amgetting the best experience

Pensive - I want to compareproducts across banks

• Account opening by phone or online

• Require as little personal info as possible during process

• Direct me to information on other possible products, but don’t include steps in the account sign-up process that ask for other account sign-up

• Digital welcome kit

• Postsign-up communication should be via email or online platform only

• Promptly send debit cards in 5-7 business days or less

• Fully responsive online platform and fully functional mobile app

• Searchable robust FAQs section on online platform

• Live chat

• Fast turnaround on email responses

• Video conferences with account manager

• Product offers via online platform and email only

• Interactive tool that makes personal recommendations without asking for additional personal information

• Offer online sign-up for products

Unnecessary personal data collection and solicitation of other products

Quick approval & account activation

Digital welcome kit and email

Promotional offers received through online platform

Debit card arrived late after an inquiry call

Navigation is not intuitive across all devices – information should be consistent

Easy login to online platform

Used FAQs and set up online bill pay

Resolved suspicious charge via video conference

Used mobile appto view balance& transfer money

Account manager called to explain product offers

Used money management & rate comparison tools on mobile app

Scheduled videoconference withaccount manager

DAY 30

GO

ALS

The Key to Successful Retail Bank Onboarding Page 15

Paulette’s Story

Paulette is a special education teacher in an elementary school and is happiest when she feels connected to people and things. She started looking for a new bank because she felt like a number at her old bank, and they didn’t have a location close to her house. She saw an appealing offer at a new bank and had to take advantage of it. Paulette is nearing retirement and has been saving for a while. She is looking forward to retirement but worries that she may need to increase her savings to be financially comfortable. Her biggest issue with her last bank: when she went into a branch to ask a question related to an account, she had to wait a long time and the person that she spoke to never followed up with her.

Banking Preference

Payment Preference

CONVENIENCEQuick transactions and advice in the branch

PERSONAL FINANCIAL ADVICETo develop a relationship with my banker so they can offer me advice based on knowledge about me and my accounts

EXCEPTIONAL CUSTOMER SERVICEMore ways to stay in touch with my banker when I want to, by phone, email, and in person

Banking Goals

NUMBER OF FINANCIAL PRODUCTS

Context of Use

LOW HIGH

ATM USE

LOW HIGH

CASH USE

LOW HIGH

TECHNICAL SKILL

LOW HIGH

PauletteTrusted Community Member

AGE

OCCUPATION

MARITAL STATUS

LOCATION

56

TEACHER

DIVORCED

RALEIGH, NC

NEW BANK

OLD BANK

BB&T

WELLS FARGO

“I need a bank that will take the time to get to know me. An institution that offers a variety of products and services. An institution that rewards customers who carry large balances in their accounts and values me as a customer.”

Visiting Family and Friends, Community Service, Church Group Outings, Hiking

Interests

Personable Social Loyal

Customer Service Channel Preference

LIVE CHAT

CALLING BY PHONE

TEXT OR EMAIL REPLY

ONLINE PLATFORM & VIDEO CONFERENCE

IN PERSON IN THE BRANCH

Branch Banking

Debit Card

Biggest Opportunity

Personalized Communications From Trusted Financial Adviser

The Key to Successful Retail Bank Onboarding Page 16

Paulette’s Bank Onboarding Journey

ACCOUNT OPENING

FEEL

ING

OP

PO

RTU

NIT

IES

–

DO

ING

+TH

INKI

NG

Easy & Convenient Account Opening

TRUSTED COMMUNITY MEMBER – WANTS HELPFUL, PERSONAL ADVICE

Personal Communications Quick & ConvenientCustomer Service Personalized Face-to-Face Advice

FOLLOW-UP SELF-SERVICE & PROBLEM RESOLUTION LONG-TERM ADVICE

STARTDAY 1

DAY 90

Waited 20 minutes before starting the account opening process in branch

“I think it can be simplified in many ways, including options to complete various forms and steps at home at your convenience.”

“Telephonic onboarding is attractive and fits well in to my schedule.”

“I opened my account in the branch. The person was knowledgeable and friendly. It was a positive experience for me.”

“I received a follow up call from a representative who went over several items with me and who also fielded my questions. She gave me her name and number to act as my contact. I did call her back on a couple occasions to pose questions, which she answered.”

“Nothing about the kit was something that I reviewed in detail. It should all be done online.”

“I want an Associate to ask if I need assistance (only once). And I do NOT want to have to wait A LONG TIME before getting assistance when I am in the branch.”

“I do like getting to know my contact at the bank, a familiar face as it were. I would like to be able to see that person when I go to transact financial business.”

“My needs are better served with dedicated customer service reps who one does not have to wait in a queue for. The option to have the rep call me back at a time that will work for me is an extremely nice feature.”

“Someone I can work with directly and consistently who could get to know my situation and advise me to the best of their ability.”

Eager to Get Started -account opening was easy

Underwhelmed - would havepreferred more help and less sales

Satisfied - weekly branchinteractions have been pleasant

Engaged & Connected -established relationship with bank

• Allow customers to schedule account opening appointments

• Allow customers to open account by phone

• Provide information about additional products that could be of benefit but don’t pressure the customer

• Offer to show the customers their online account

• Digital welcome kit

• Promptly send debit cards in 5-7 business days or less

• Call and email customers to make sure they’re comfortable with their new accounts and answer questions

• Provide kiosks to reduce wait times in the branch

• Email and text alerts

• Follow up promptly by phone if the customer communicates a problem

• Make sure customers’ problems have been resolved

• Account manager should schedule a recurring monthly check-in meeting at the branch

• Take time to get to know the customers and be able to speak knowledgeably about their account when they visit the branch

• Special offers based on preferred customer status

Bank associate was friendly and helpful

30-minute approval process was quick

Bank associate showed me how to log in to my account and gave me his card

Debit card didn’t arrive for weeks Received 3 calls in 1

week from the bank about product offers

No wait in branch- cashed check and asked questions

On hold 10 minutes with customer service to ask questions about bill pay

Account manager called to make sure my problem was resolved

Received text fee alert to avoid fee

Account manager answered questions and set up recurring advice meetings

Viewed product offers email

Financial advice meeting

DAY 30 Viewed product information online

Financial advice meeting

DAY 60

Financial advice meeting

Misplaced welcome kit

GO

ALS

The Key to Successful Retail Bank Onboarding Page 17

Bank onboarding journeys and opportunities

We looked at the bank onboarding journey for new customers, beginning with account opening and ending 90 days into the new bank relationship. Most opportunities for all customers were related to customer service and self-service tasks and occurred between weeks one and eight in the Follow-Up and Self-Service stages of onboarding.

After opening an account in the Follow-Up stage, all customers had some negative feelings associated with the customer service they received. In most cases, customers felt that the bank was trying to sell them additional products and wasn’t trying to help them better manage their money. In the Self-Service stage, there was a great

Account Opening Follow-Up Self-Service Long-Term Advice

Tech-Savvy Researchers

MobileFree Spirits

Trusted CommunityMembers

+feeling

_feeling

deal of emotional fluctuation among both Mobile Free Spirits and Tech-Savvy Researchers. These two personas had high expectations for the online platform and mobile app that often were not met.

There is a significant opportunity to improve the account opening experience with a faster online account opening process for Mobile Free Spirits and Tech-Savvy Researchers.

All customers are open to receiving financial advice from their bank during the Follow-Up stage. However, Trusted Community Members required more personal advice sooner and more often than others. Banks should have personal bankers take the time to get to know

The Key to Successful Retail Bank Onboarding Page 18

these customers and follow up with them personally using tailored email templates and scheduling recurring face-to-face financial planning meetings at the branch. After the Trusted Community Member is won over, he or she will likely trust the bank for all his or her banking needs.

For Mobile Free Spirits, during the Follow-Up and Self-Service stages, banks should personalize communications through the mobile application, online banking platform and email. These customers would welcome an interactive tool that could offer personalized financial advice. Mobile Free Spirits consider adding new products and services all the time but prefer to research online before engaging the bank. They are willing to give quite a bit of personal information during account opening to get good financial advice from a dedicated personal banker.

Across the whole 90-day journey, Tech-Savvy Researchers prefer to receive advice from the online banking platform and other digital channels. They trust their bank the least in terms of providing personal information. The more the online banking tools educate, compare products and provide convenient self-service features, the more likely Tech-Savvy Researchers are to consider their bank for additional products and services after 90 days. Banks should create an interactive tool that uses account information and answers to a few basic questions to give financial advice to these customers. The interactive tool should provide detailed product information and a link to online product sign-up.

The bottom line is: The more negative experiences customers have with self-service and customer service during the first 90 days, the less likely they are to trust their bank, and the less likely they are to sign up for additional products and services. Banks need to start

thinking about how they can give their customers more control over their finances, thus moving from customer relationship management to customer-managed relationships.

CONCLUSIONS

A customer-managed relationship is based on proper customer segmentation, tailored customer communications and interactive digital tools that provide tailored, relevant information with more control over finances. Proper customer segmentation represents one of the most powerful opportunities to improve the customer’s onboarding journey. By segmenting effectively, it is possible to improve onboarding procedures, target customers through the right channels, determine the ideal communication cadence, and personalize communications so that customers feel that the bank is serving their interests and values their business. A customer who feels valued is not only more likely to remain with the bank but also more likely to buy multiple products and open multiple accounts.

Technology’s ability to improve the onboarding experience is profound. The preferred channels for retail banking continue to shift toward mobile and online for most retail banking customers. More and more customers choose to open accounts online, add products online, provide and receive information through the secure online banking platform, and access self-service features and live chat using their mobile phones. Instead of trying to meet the needs of all bank customers through the branch, banks should focus on improving the branch experience for the specific group of customers who prefer branch banking … and improve digital tools and communications for everybody else.

The Key to Successful Retail Bank Onboarding Page 19

NEXT STEPS

Catalyst can help you successfully onboard more retail banking customers with these solutions:

Insight development—Qualitative and quantitative research with accompanying data analysis to identify and prioritize customer experience opportunities.

Advanced analytics—Customer segmentation, persona development, attribution analysis, marketing mix modeling, and more to help you transform customer data into business intelligence.

CX design—Customer journey maps and other customer-centric solutions that help solve marketing issues and find the gaps in your current communications programs. Our solutions are tested with your customers to measure effectiveness prior to launch.

Customer acquisition and retention programs—Catalyst’s SEM, digital and direct marketing solutions combine powerful data analysis with marketing technology to help deliver more customers. Our targeted marketing services will help you measurably find and keep more profitable customers.

Behaviors and preferred communications channels differ across segments of the banking population. Banks need to study their personas and the specific customer journeys of each customer segment to uncover new opportunities to provide tailored, stellar onboarding experiences.

Basic trust in banks is strong, but complete trust in a bank is garnered over time through positive self-service and customer service interactions. For one segment of the population, branches help establish trust at critical junctures like account opening, adding products and during customer service problem resolution. Most customers do not expect to be pushed to add products during the sign-up process and prefer not to receive offer-related phone calls. Most customers prefer to learn about financial opportunities, view bank product details, compare bank product options, and get answers about products online. When customers are ready, they will contact their bank to learn more or they will use the bank’s platform to sign up for the product online.

Banks that take the approach of educating and helping their customers make beneficial financial decisions, instead of trying to sell additional products and services, will be rewarded with a great reputation and a customer base with larger portfolios.

The Key to Successful Retail Bank Onboarding Page 20

ABOUT THE AUTHOR

TARA LITCHFIELD Director of Experience Design

MORE ABOUT CATALYST

Catalyst (www.catalystinc.com) is a marketing agency that helps retail bankers develop more profitable customer relationships. By combining our intellectual curiosity and inquisitiveness with hard-core analytics and measurement, we create acquisition, retention, CRM, and CX programs that improve the customer experience at every stage of the life cycle, from account opening through onboarding through relationship expansion.

We call it Science + Soul.

It’s a powerful combination that results in a measurable increase in new accounts, deposits, upsell and cross-sell opportunities, and increased customer lifetime value.

TO LEARN HOW CATALYST CAN HELP YOUR RETAIL BANKING BUSINESS, CONTACT:

Christian Banach at 585.453.8313 or email: [email protected]

or

Mike Osborn at 585.453.8331 or email: [email protected]

As Catalyst’s director of experience design, Tara develops engaging and effective experiences for our clients’ customers. She leads research initiatives to uncover new insights, then translates those insights into optimized customer experiences.

Her tool kit includes personas, journey maps and touch point analyses to help clients understand their customers in new ways, which leads to new business opportunities. She is an experienced UX designer who creates information architecture, workflow diagrams, detailed wireframes, interactive prototypes, user experience requirement documentation, content strategy, and heuristic evaluations to develop detailed customer-focused creative solutions. She conducts in-depth usability studies to validate and measure a solution’s effectiveness.

Tara holds an MA in visual arts and a BS in psychology. She has worked with a variety of Fortune 500 clients, including American Express, Honeywell, Kaspersky Lab, Paychex, Sears, Anthropologie, Carpet One, Reebok, Verizon, and Campbell’s Soup, among others.

800.836.7720 | www.catalystinc.com | [email protected] Facebook Twitter LinkedIn © 2017 Catalyst